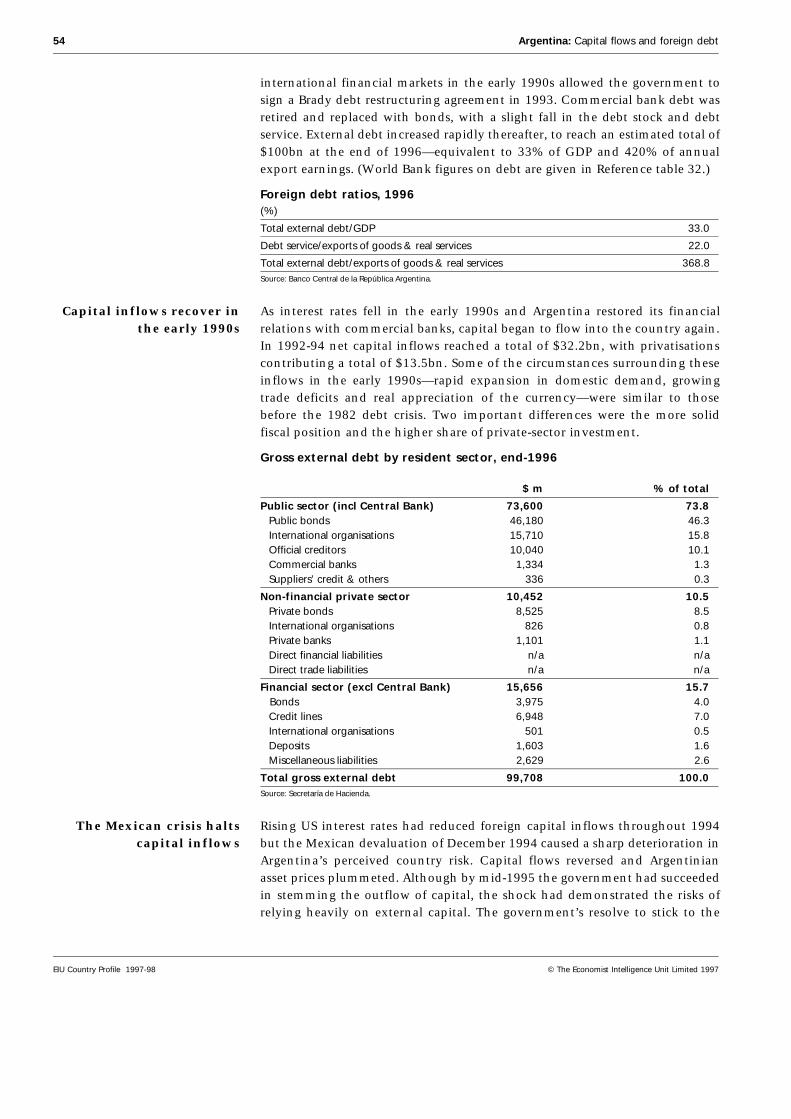

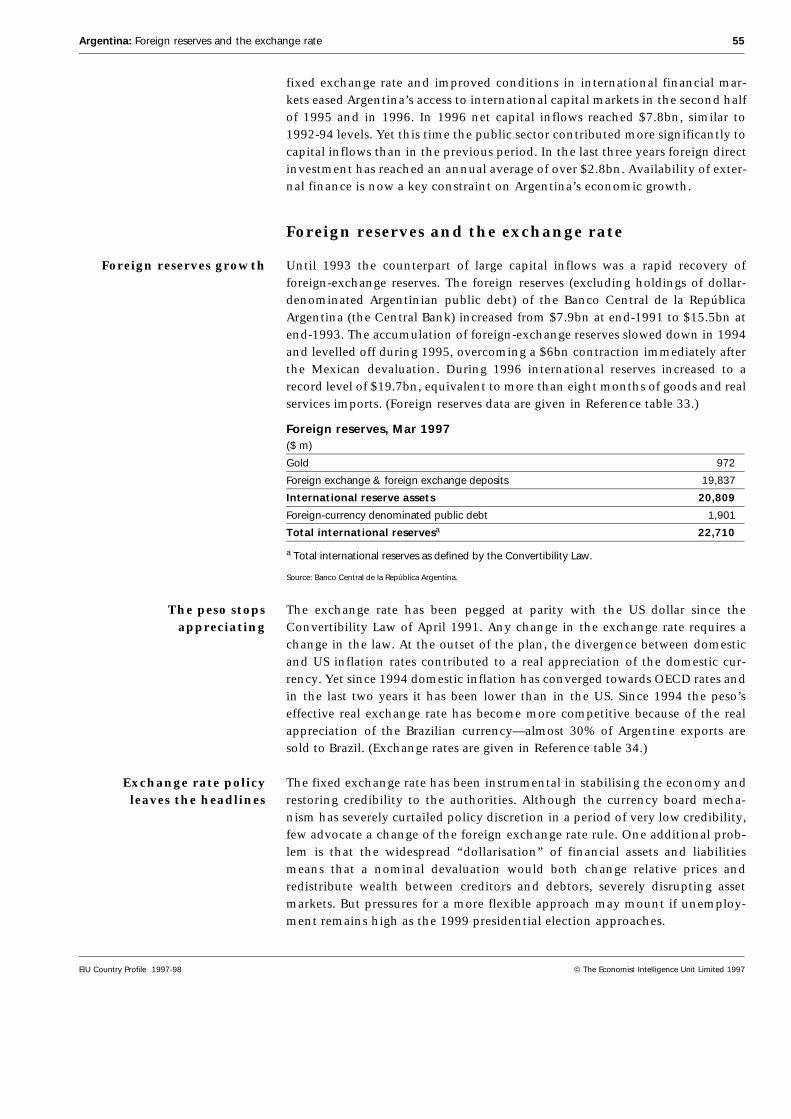

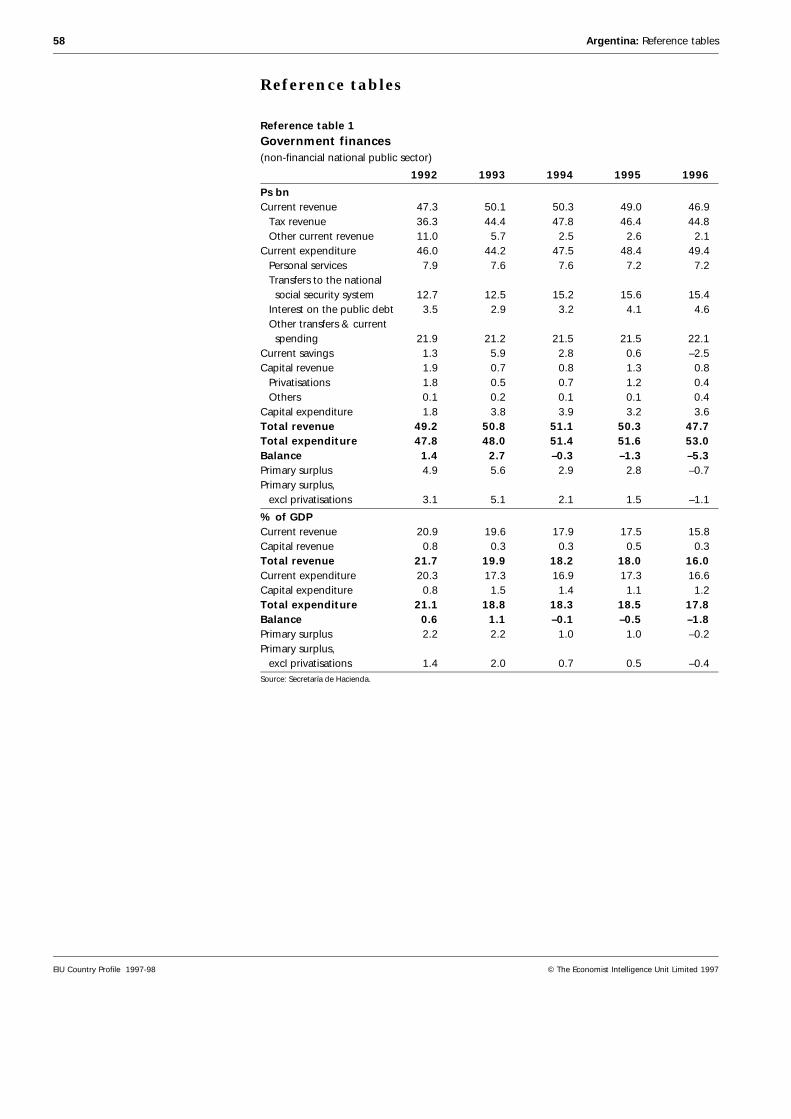

Embed Size (px)

Citation preview

COUNTRY PROFILE

ArgentinaOur quarterly Country Report on Argentina analyses currenttrends. This annual Country Profile provides backgroundpolitical and economic information.

1997-98The Economist Intelligence Unit15 Regent Street, London SW1Y 4LRUnited Kingdom

The Economist Intelligence Unit

The Economist Intelligence Unit is a specialist publisher serving companies establishing and managingoperations across national borders. For over 50 years it has been a source of information on businessdevelopments, economic and political trends, government regulations and corporate practice worldwide.

The EIU delivers its information in four ways: through subscription products ranging from newslettersto annual reference works; through specific research reports, whether for general release or for particularclients; through electronic publishing; and by organising conferences and roundtables. The firm is amember of The Economist Group.

London New York Hong KongThe Economist Intelligence Unit The Economist Intelligence Unit The Economist Intelligence Unit15 Regent Street The Economist Building 25/F, Dah Sing Financial CentreLondon 111 West 57th Street 108 Gloucester RoadSW1Y 4LR New York Wanchai United Kingdom NY 10019, US Hong KongTel: (44.171) 830 1000 Tel: (1.212) 554 0600 Tel: (852) 2802 7288Fax: (44.171) 499 9767 Fax: (1.212) 586 1181/2 Fax: (852) 2802 7638e-mail: [email protected] e-mail: [email protected] e-mail: [email protected]

Website: http://www.eiu.com

Electronic deliveryEIU ElectronicNew York: Lou Celi or Lisa Hennessey Tel: (1.212) 554 0600 Fax: (1.212) 586 0248London: Moya Veitch Tel: (44.171) 830 1007 Fax: (44.171) 830 1023

This publication is available on the following electronic and other media:

Online databases CD-ROM Microfilm

FT Profile (UK) Knight-Ridder Information World Microfilms Publications (UK)Tel: (44.171) 825 8000 Inc (US) Tel: (44.171) 266 2202

DIALOG (US) SilverPlatter (US) University Microfilms Inc (US)Tel: (1.415) 254 7000 Tel: (1.800) 521 0600

LEXIS-NEXIS (US)Tel: (1.800) 227 4908

M.A.I.D/Profound (UK)Tel: (44.171) 930 6900

Copyright© 1997 The Economist Intelligence Unit Limited. All rights reserved. Neither this publication nor any part of it may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the prior permission of The Economist Intelligence Unit Limited.

All information in this report is verified to the best of the author’s and the publisher’s ability. However,the EIU does not accept responsibility for any loss arising from reliance on it.

Symbols for tables“n/a” means not available; “–” means not applicable

Printed and distributed by Redhouse Press Ltd, Unit 151, Dartford Trade Park, Dartford, Kent DA1 1QB, UK

ISSN 0269-4468

December 1st 1997 Contents

2 Basic data

3 Political background3 Historical background8 Constitution and institutions9 Political forces

11 International relations and defence

13 The economy13 Economic structure14 Economic policy17 Economic performance19 Regional trends

21 Resources21 Population23 Education25 Health26 Natural resources and the environment

28 Economic infrastructure28 Transport and communications32 Energy provision34 Financial services40 Other services

41 Production41 Manufacturing45 Mining and semi-processing46 Agriculture, forestry and fishing 49 Construction

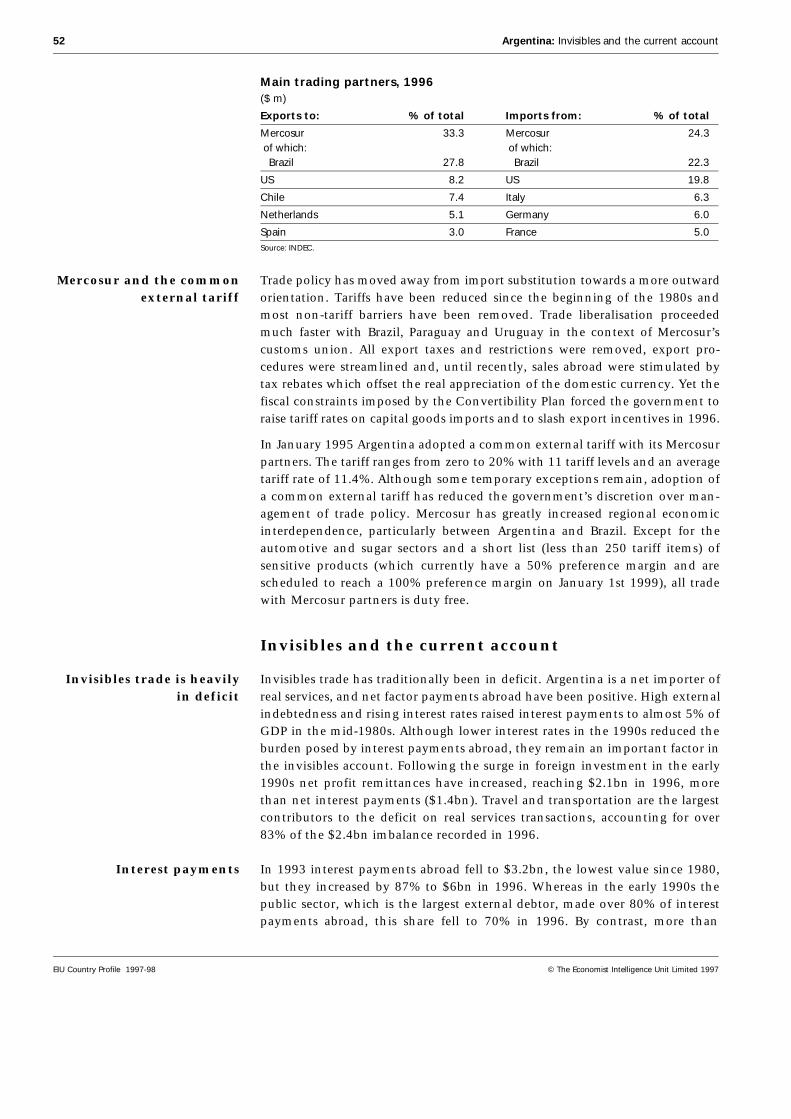

50 The external sector50 Merchandise trade52 Invisibles and the current account53 Capital flows and foreign debt55 Foreign reserves and the exchange rate

56 Appendices56 Sources of information58 Reference tables

1

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Argentina

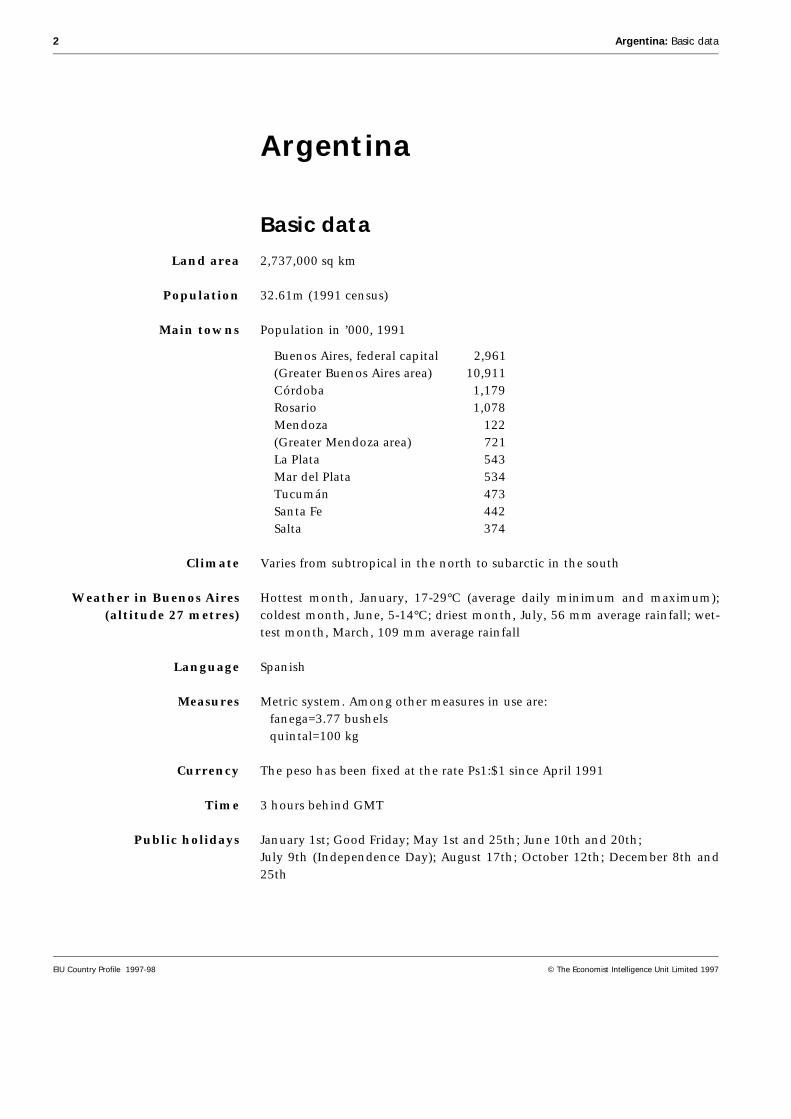

Basic data

Land area 2,737,000 sq km

Population 32.61m (1991 census)

Main towns Population in ’000, 1991

Buenos Aires, federal capital 2,961(Greater Buenos Aires area) 10,911Córdoba 1,179Rosario 1,078Mendoza 122(Greater Mendoza area) 721La Plata 543Mar del Plata 534Tucumán 473Santa Fe 442Salta 374

Climate Varies from subtropical in the north to subarctic in the south

Weather in Buenos Aires(altitude 27 metres)

Hottest month, January, 17-29°C (average daily minimum and maximum);coldest month, June, 5-14°C; driest month, July, 56 mm average rainfall; wet-test month, March, 109 mm average rainfall

Language Spanish

Measures Metric system. Among other measures in use are: fanega=3.77 bushels quintal=100 kg

Currency The peso has been fixed at the rate Ps1:$1 since April 1991

Time 3 hours behind GMT

Public holidays January 1st; Good Friday; May 1st and 25th; June 10th and 20th;July 9th (Independence Day); August 17th; October 12th; December 8th and25th

2 Argentina: Basic data

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Political background

The president is head of state and government. The present incumbent isCarlos Menem. There is a two-chamber parliament. Mr Menem’s party, thePartido Justicialista, lost in the lower house at the October 1997 election.

Historical background

A poor Spanish colony— Argentina was one of the poorest and most sparsely populated Spanish coloniesin America. Having neither gold nor silver, nor a climate suitable for raisingtropical crops, the role of the Argentinian economy was to provide inputs tothe Potosí silver mines in Upper Peru (now Bolivia). In 1777 the Spanish crowncreated the Río de la Plata viceroyalty to stop the westward expansion of thePortuguese rather than to establish a new economic centre.

Independence from Spain in 1816 was followed by decades of instability andcivil strife. The 1853 constitution, based on the US model, created modernArgentina. But there were ten more years of civil war before the rich provinceof Buenos Aires (which controlled the port) joined the union.

—became one of therichest countries in the

world

In the late 19th century innovations in transport and the conservation of foodsmade possible the exploitation of the fertile pampas, turning the country intoa supplier of grains and meat to Europe (particularly the UK). Liberal-mindedgovernments encouraged foreign investment and immigration. By the turn ofthe century Argentina was the tenth largest trading country in the world andthe sixth in terms of income per head. Almost 40% of its 6m inhabitants wereforeigners. UK investments were larger in Argentina than in Australia, Canadaor the US.

Throughout this time of growth the economy and society diversified. Theestablishment of secret and mandatory voting in 1912 paved the way for thevictory of the Unión Cívica Radical (UCR) in the 1916 election. The UCR,founded in 1890 to advance the interests of the rapidly growing middle classes,did not change the economic profile of the country in substance; foreign traderemained the engine of growth and the UK the closest partner.

The Great Depression The rapid economic growth and political pluralism was brought to an end bythe Great Depression of the 1930s. Falling agricultural prices and export vol-umes depressed the Argentinian economy. In 1930 the alleged ineffectivenessof the Radical government was the excuse for the first of what would turn outto be a long list of military interventions. By means of fraudulent electoralpractices, Conservatives returned to office in 1932 and stayed in power formore than a decade. Conservative governments attempted to overcome theeconomic crisis by means of a combination of preferential arrangements withthe UK, foreign-exchange controls and protection of domestic markets.

The emergence ofPeronism

The second world war reawakened demand for Argentinian exports. At thesame time, the influence in the army of a group of nationalist officers, amongthem Colonel Juan Domingo Perón, began to grow. In 1943 another military

Argentina: Historical background 3

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

coup brought to power a government which was sympathetic to the Axispowers, but maintained neutrality until the end of the war. Having been theminister for labour in the military government, Perón won the 1946 pres-idential election as a Labour Party candidate. The constitution was reformed in1949 to allow his re-election as president for an additional six-year term in1952. During his years in office Perón nationalised most foreign-owned publicservices, such as the railways, and presided over a period of active governmentinvolvement in the economy. He had the support of the trade unions, whichhe had strengthened as minister for labour in the mid-1940s, and the businesssectors which produced for the domestic market, as well as part of the army.

Military intervention inthe 1950s and 1960s

Perón remained in power until 1955, when he was ousted by a new militarycoup. The next three decades saw recurrent military intervention. (The armedforces displaced elected governments in 1962, 1966 and 1976.) In the 1950sand 1960s Perón was exiled and barred from taking part in elections, whichweakened the legitimacy of civilian governments. Amid such political instabil-ity, the economy proved unable to recover its pre-1929 dynamism. Yet withhindsight the 1960s appear a period of strong, fairly smooth growth, led byindustry.

Perón’s comeback and thereturn of military rule

In 1973 Perón was finally allowed to stand for election, winning the presidencyfor the third time. But by now he was old and in poor health. He died less thana year after taking office, and was succeeded by his wife, María Estela Martínezde Perón.

The new Peronist government returned to populist economic policies. YetMrs Perón’s administration was quickly discredited, not least because of risinginflation as union bosses pressed successfully for higher wages. Violent con-frontation between guerrillas, right-wing paramilitary groups tolerated by thegovernment, and the military made matters worse. In 1976 the armed forcestook power again to implement a programme of economic liberalisation and aruthless anti-terrorist policy. In this “dirty war” the death toll was estimated atmore than 7,000 desaparecidos (disappeared people), who had been abductedand killed, their bodies buried in secret graves or disposed of at sea.

By the late 1970s the economy was showing acute signs of strain and a rapidaccumulation of external debt fuelled by an appreciating real exchange rate. Afinancial crisis broke out in March 1980 and several local banks went bankrupt.The liberalisation programme of the military government collapsed and a seriesof large devaluations and mounting inflation followed.

Democracy is restored in1983—

On April 2nd 1982 the armed forces invaded the Falkland Islands (IslasMalvinas), which had been occupied by the British since the 1830s, in anattempt to recapture public support. General Leopoldo Galtieri, the leader ofthe junta and the Argentinian military command, assumed that the UK wouldnot go to war to defend the islands. The assumption was wrong and defeatrapidly followed. The regime became isolated, both domestically and inter-nationally. General Reynaldo Bignone took over from General Galtieri and themilitary called a general election for October 1983. Unexpectedly, the winnerwas the UCR candidate, Raúl Alfonsín.

4 Argentina: Historical background

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Mr Alfonsín’s administration was successful in consolidating political demo-cracy, and facing up to the human rights abuses committed under the militaryregime. Mr Alfonsín had to deal with military uprisings led by junior officers,known as carapintadas, dissatisfied with the army’s treatment in the investig-ations. He also succeeded in bringing into public debate previously intractableissues such as trade liberalisation, market deregulation and privatisation. But hiseconomic policies proved ineffectual. The Plan Austral to stabilise the economy,launched in mid-1985 with the support of the IMF, was initially successful andinflation was contained. But fiscal equilibrium was never achieved. The govern-ment failed to enforce the strong measures necessary to bring about a change inthe country’s macroeconomic environment and economic structure. By 1987—when Argentina reached an understanding with its creditor banks on a debtrestructuring plan—inflation was rising again. Mr Alfonsín’s Radicals were badlybeaten by a rejuvenated Partido Justicialista (PJ, Peronist party) in the September1987 parliamentary election. The economy went from bad to worse, and in April1988 interest payments to creditor banks were suspended. In February 1989capital flight forced the Banco Central de la República Argentina (the CentralBank) to devalue and Argentina sank into hyperinflation.

—and Mr Menem launchesan ambitious structural

reform programme

For the May 1989 presidential election the leader of the PJ, Carlos Menem,campaigned on the promise of higher wages and a “productive revolution”,whereby closed factories would be reopened. This traditional Peronist platform,together with his ability to communicate and widespread dissatisfaction withthe previous government’s record, led to a sweeping victory. Mr Alfonsínhanded over power five months early, in July 1989, as hyperinflation ravagedthe economy. But in a dramatic U-turn Mr Menem did not implement thepolicies promised in the campaign, opting instead for austerity and a majorstructural reform programme involving privatisation, trade liberalisation andmarket deregulation. This constituted a dismantling of many of the legacies ofPeronism.

The first 18 months in office were not easy, with a second burst of hyperinfla-tion in 1990 and a series of corruption scandals. But the government stuck toits economic reform programme, partly enforced by special decrees. Mr Menemdivided the labour movement and forged an alliance with business and thetraditionally anti-Peronist establishment. The Convertibility Plan launchedin April 1991 brought inflation under control and initiated an unprecedentedperiod of price stability and economic growth under a currency board system.Aided by a favourable external financial environment, the 1991-94 economicexpansion combined with price stability turned into one of the main politicalassets of the government. Mr Menem was able to push successfully for anagreement with the Radicals to reform the constitution in order to allow re-election of the president. A constitutional assembly was convened in May 1994and a new constitution was adopted three months later.

Menem is re-elected for asecond term in 1995—

The electorate’s fear of a return to the chaotic past, the government’s resolve tostick to the Convertibility Plan to face the fall-out of the Mexican foreign-exchange crisis, and the external support package which the authorities wereable to put together contributed to a new Peronist victory on May 14th 1995.Remarkably, Mr Menem was re-elected in the first round with 49.9% of the

Argentina: Historical background 5

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

vote, followed by the centre-left coalition, Frente del País Solidario (Frepaso),with 30%. The UCR’s performance, with only 17% of the vote, was the worst inthe party’s history. Mr Menem’s sweeping victory also provided him with amajority in both houses of Congress.

Main political figures

Carlos Saúl Menem: The president of Argentina and head of the Peronist party.Re-elected for an additional four-year period in 1995. His second term wasinaugurated under the influence of the Mexican peso crisis and has been marred byhigh unemployment. Mr Menem’s authority is being challenged by contenders forthe 1999 Peronist presidential nomination. Eduardo Duhalde: Governor of Buenos Aires province, the largest electoral districtand a Peronist stronghold. He has considerable electoral support in his district andwas the most likely Peronist candidate for the 1999 election, but lost ground whenhis wife lost to the Alianza por el Trabajo, la Justicia y la Producción in the October1997 congressional election. Influential within the party structures and with stronglinks with traditional Peronist interest groups, he will have to cultivate theestablishment to win the presidency.Roque Fernández: A professional economist and former Central Bank presidenteducated in the University of Chicago tradition. He became economy minister whenDomingo Cavallo was ousted in mid-1996, amid great concern over the future of theeconomy. Yet he successfully managed to steer the economy on to a positive growthpath.Domingo Cavallo: Former economy minister and architect of the ConvertibilityPlan. He was ousted by Mr Menem in 1996 and has since increased his allegations ofcorruption within the administration. He won a congressional seat in the October1997 election, from where he plans to rebuild his political career.Raúl Alfonsín: Former president and leader of a Unión Cívica Radical (UCR) faction.His authority within the party has been challenged and his popularity with theelectorate has declined, but his political ambitions remain strong. He is credited withworking behind the scenes to enable the creation of the Alianza.Fernando de la Rúa: Mayor of the city of Buenos Aires, former senator andlong-standing member of the UCR. He was opposed to the Pacto de Olivos, theagreement in which the UCR supported the constitutional amendment allowingMr Menem to stand for re-election in 1995. He is a strong candidate for the 1999Alianza presidential candidacy.Carlos Alvarez: A deputy, he is one of the prominent figures of the centre-leftcoalition, Frente del País Solidario (Frepaso), and the new Alianza. Formerly aPeronist, he will remain one of the most visible opposition leaders and may competewith Graciela Fernández Meijide as the (Frepaso) choice for the Alianza nominationin the 1999 election.Graciela Fernández Meijide: former Frepaso senator for Buenos Aires. Shesuccessfully ran for a congressional seat for Buenos Aires province in the October1997 election to enhance the Alianza’s electoral chances in the district. She is astrong contender for the Alianza nomination in 1999.

—which is plagued bysocial and political

problems

Despite Mr Menem’s strong mandate in the national ballots, his government’ssecond term has faced several problems. The most significant have been highunemployment rates and an early struggle for his own succession in 1999.Unprecedentedly high unemployment rates led to the first successful general

6 Argentina: Historical background

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

strike of Mr Menem’s presidency in 1996, as well as episodes of social unrestthroughout 1997.

The early struggle for Mr Menem’s succession, in turn, has upset the Peronistparty and the government itself. In particular, the investigation into the mur-der of a journalist in January 1997 deepened the clash between the presidentand the powerful governor of the province of Buenos Aires (who is also aPeronist frontrunner), Eduardo Duhalde. But if the Peronists are to have afighting chance in the 1999 elections Mr Menem and Mr Duhalde will event-ually have to come to a truce. After eight years in power Mr Menem’s star maybe fading as his administration begins to look a little tired, making the need forparty unity all the more pressing.

The 1997 congressionalelection will be a

barometer

The October 1997 congressional election was expected to determine the polit-ical climate for the remaining two years of the government’s mandate. Analliance between the UCR and Frepaso, dubbed the Alianza por el Trabajo, laJusticia y la Producción, won a clear-cut victory over the Peronists, deprivingMr Menem of his majority in the lower house. Ironically his position in the PJmay be bolstered since the party’s heaviest upset was suffered in Mr Duhalde’sBuenos Aires province. The 1999 elections could be a significant test of thecountry’s political maturity. For many decades the transition from one admin-istration to the next in Argentina has been far from smooth, the last one in1989 taking place amid a hyperinflationary bout. After a profound economictransformation, it remains to be seen whether the Argentinian polity hasevolved towards a more stable and predictable pattern.

Important recent events

November 1993: Mr Menem and Mr Alfonsín announce an agreement to reformthe 1853-60 constitution (the so-called Pacto de Olivos).July 1994: A new constitution is adopted, enabling Mr Menem to run forre-election in 1995.May 1995: Mr Menem is re-elected for a second term with the support of 50% ofthe vote. He also obtains a majority in both houses of Congress. His second term isinaugurated in July 1995.July 1996: Mr Menem fires Domingo Cavallo, architect of the Convertibility Plan.Mr Cavallo is succeeded by the president of the Banco Central de la RepúblicaArgentina (the Central Bank), Roque Fernández. Mr Cavallo’s departure goesunnoticed by the markets and the new economy minister emphasises fiscalconsistency and labour-market reform. January 1997: Since police and private security forces appear to be involved, themurder of a journalist turns into a major issue for both the government and theopposition.October 1997: The Peronists suffer a severe defeat in the congressional election.

Argentina: Historical background 7

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Constitution and institutions

A strong presidentialtradition

Argentina is a federal republic with a strong presidential tradition. The pres-ident appoints a cabinet chief, a secretary-general of the presidency and eightministers. The 1994 constitutional reform established the upgrading of foursecretaries (of culture, social development, sports and tourism, and naturalresources and the environment) to ministerial level, but the decision has so farfailed to be implemented.

The cabinet chief, a post created with the intention of moderating presidentialpower, is in charge of the general administration of the country and can beremoved by a majority vote of both houses of Congress. In practice, the cabinetchief’s effectiveness as an administrator and moderator has proved modest andheavily dependent upon both personalities and the president’s willingness todelegate powers.

The new constitution also established a four-year presidential term with only asingle re-election allowed, two-round direct elections for the presidency (nosecond round is needed if the winner receives more than 45% of the vote, or atleast 40% with a 10-percentage-point lead over the second-placed candidate)and prohibited presidential emergency decrees on tax, criminal law or electoralissues. As established by the 1994 constitutional reform, in 1996 the federaldistrict was made autonomous and its mayor directly electable by the city’sresidents. The federal district is currently run by the UCR.

Traditionally, the Ministry of the Economy has wielded vast powers within thecabinet. This is unlikely to change with the creation of the post of cabinetchief, but much will depend on personalities. Pressure has been mounting tosplit the Ministry of the Economy into two ministries (treasury and economy).To what extent the post of cabinet chief will change the balance of powerbetween the executive and Congress also remains to be seen. So far, the officialmajority in both houses has prevented the opposition from succeeding inremoving the cabinet chief.

The head of the National Audit Bureau is designated by the opposition andreports to Congress.

Congress Congress is bicameral, with a 257-member Chamber of Deputies and a72-member Senate. Deputies are directly elected for four-year periods and half ofthem stand for re-election every two years. Senators, who represent the 23 pro-vincial states and the autonomous federal district, are elected for six-year terms.

In the lower house the Peronists lost their majority in the October 1997 con-gressional election. They hold 118 seats while the Alianza holds 110 and otherminority groups (mainly provincial parties) hold 29. In the Senate thePeronists hold 39 seats, the Radicals 21 and other minority parties 12. Relationsbetween Congress and the executive will be tested by the Peronists’ minorityposition in the lower house.

A weak judiciary After the trial and condemnation of the military juntas, the judiciary’s prestigereached a peak. But in recent years its image has deteriorated. There are long-standing infrastructural and organisational problems but, more importantly,

8 Argentina: Constitution and institutions

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

the government has intervened too often in judicial issues. In 1989 Mr Menemraised the number of Supreme Court members to alter the court’s politicalbalance. Congress has appointed judges with dubious experience or compe-tence and several have been removed as a result of allegations of corruption.Although there is a judicial reform under way (including the use of oral pro-ceedings to speed up trials), progress has been slow.

The new constitution established the appointment of judges by a council ofjurists and created a judges’ jury which is responsible for removing judges. Butso far the government and the opposition have failed to agree on the council’scomposition. The required legislation needs a special congressional majoritywhich the government has been unable to reach.

The need for an effective and independent judiciary has been highlighted byseveral highly publicised corruption scandals involving government officialsand foreign and domestic corporations. Public opinion is in favour of astronger fight against corruption and a more decisive promotion of the rule oflaw and calls for this have also been made by influential international organis-ations, such as the IMF. Although Congress has reached agreement on a bill topromote ethics in the public service, there is a shared consensus that Argentinaneeds more decisive action to fight corruption and poor enforcement of law.The murder of a journalist in January 1997 brought the issue to the forefront ofthe national debate and contributed to the opposition’s victory in October’scongressional election.

Political forces

A two-party politicalsystem—

Traditionally, the Argentinian political system has been bipartisan, the twomain political organisations being the Partido Justicialista (PJ, Peronist Party)and the Unión Cívica Radical (UCR). Yet the emergence of the centre-leftcoalition Frente del País Solidario (Frepaso) as a significant actor in nationalelections has altered this balance.

The stronghold of the Peronists has been the low- and middle-income sectors.Linked to the formerly powerful trade unions, the Peronists were regarded asunbeatable in free elections. But Mr Menem transformed the PJ into a party ofprivatisation, trade liberalisation and deregulation—the opposite of the poli-cies espoused by Perón himself. Mr Menem justified this on the grounds thattimes had changed and that the doctrine of the party should be updated. Buthis U-turn, warmly supported by business and financial elites, has not beenaccepted happily by either the party or the trade unions.

The internal competition for Mr Menem’s succession in the context of un-precedented unemployment rates and a worsening distribution of income hasfuelled this debate. While sharing a conviction that a return to the past is outof the question, the frontrunner for the 1999 Peronist nomination,Mr Duhalde, would like to see a stronger emphasis on social and industrialpolicies. Yet Mr Duhalde still has to win the support and the trust of theeconomic “establishment”. Peronism seems to be at a crossroads, with thechoice and performance of Mr Menem’s successor indicative of its futurecourse.

Argentina: Political forces 9

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

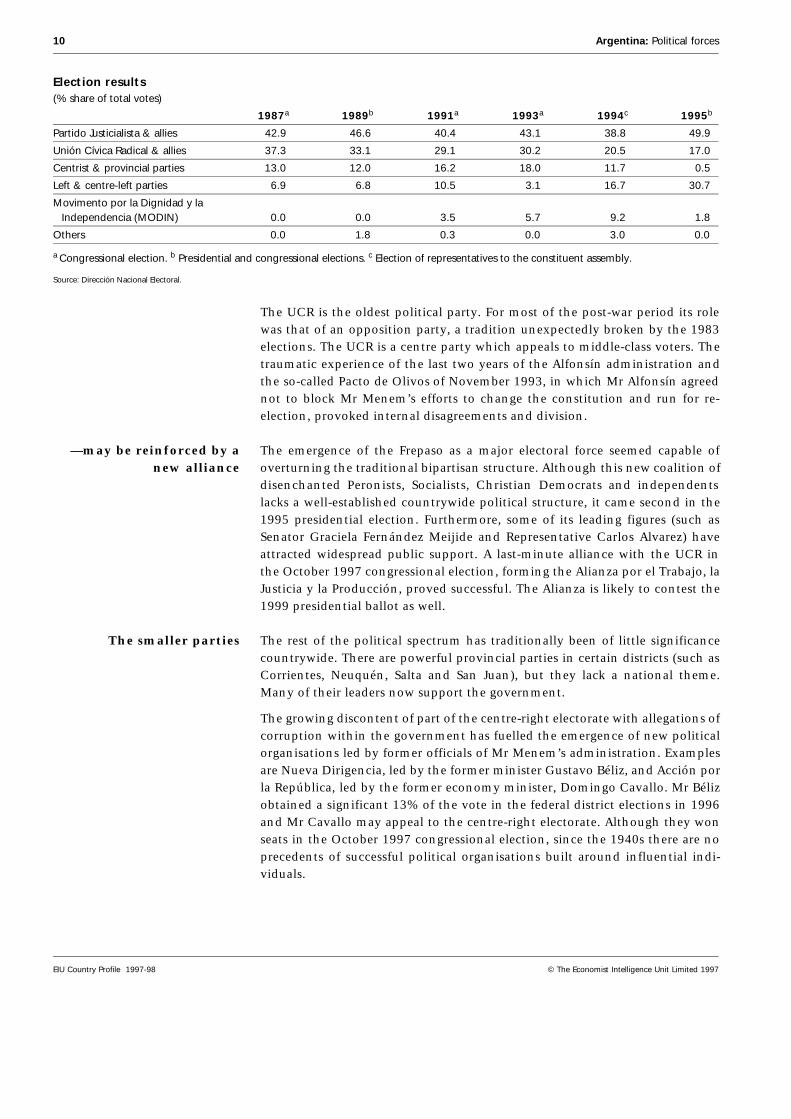

Election results(% share of total votes)

1987a 1989b 1991a 1993a 1994c 1995b

Partido Justicialista & allies 42.9 46.6 40.4 43.1 38.8 49.9

Unión Cívica Radical & allies 37.3 33.1 29.1 30.2 20.5 17.0

Centrist & provincial parties 13.0 12.0 16.2 18.0 11.7 0.5

Left & centre-left parties 6.9 6.8 10.5 3.1 16.7 30.7

Movimento por la Dignidad y la Independencia (MODIN) 0.0 0.0 3.5 5.7 9.2 1.8

Others 0.0 1.8 0.3 0.0 3.0 0.0

a Congressional election. b Presidential and congressional elections. c Election of representatives to the constituent assembly.

Source: Dirección Nacional Electoral.

The UCR is the oldest political party. For most of the post-war period its rolewas that of an opposition party, a tradition unexpectedly broken by the 1983elections. The UCR is a centre party which appeals to middle-class voters. Thetraumatic experience of the last two years of the Alfonsín administration andthe so-called Pacto de Olivos of November 1993, in which Mr Alfonsín agreednot to block Mr Menem’s efforts to change the constitution and run for re-election, provoked internal disagreements and division.

—may be reinforced by anew alliance

The emergence of the Frepaso as a major electoral force seemed capable ofoverturning the traditional bipartisan structure. Although this new coalition ofdisenchanted Peronists, Socialists, Christian Democrats and independentslacks a well-established countrywide political structure, it came second in the1995 presidential election. Furthermore, some of its leading figures (such asSenator Graciela Fernández Meijide and Representative Carlos Alvarez) haveattracted widespread public support. A last-minute alliance with the UCR inthe October 1997 congressional election, forming the Alianza por el Trabajo, laJusticia y la Producción, proved successful. The Alianza is likely to contest the1999 presidential ballot as well.

The smaller parties The rest of the political spectrum has traditionally been of little significancecountrywide. There are powerful provincial parties in certain districts (such asCorrientes, Neuquén, Salta and San Juan), but they lack a national theme.Many of their leaders now support the government.

The growing discontent of part of the centre-right electorate with allegations ofcorruption within the government has fuelled the emergence of new politicalorganisations led by former officials of Mr Menem’s administration. Examplesare Nueva Dirigencia, led by the former minister Gustavo Béliz, and Acción porla República, led by the former economy minister, Domingo Cavallo. Mr Bélizobtained a significant 13% of the vote in the federal district elections in 1996and Mr Cavallo may appeal to the centre-right electorate. Although they wonseats in the October 1997 congressional election, since the 1940s there are noprecedents of successful political organisations built around influential indi-viduals.

10 Argentina: Political forces

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

International relations and defence

The South Atlantic war:mending the damage done

The Alfonsín and Menem governments had a hard job trying to repair thedamage done to Argentina’s international reputation by the invasion of theFalkland Islands (Islas Malvinas). Although relations with developed countriesimproved markedly during the Alfonsín government, a number of difficultissues remained unresolved, such as the ratification of the Tlatelolco Treaty—which bars nuclear weapons from Latin America and the Caribbean—and there-establishment of diplomatic relations with the UK.

To reinforce his economic reform programme, Mr Menem decided to settle allpolitical disputes with industrial countries, particularly the US and the UK. TheMenem administration abandoned the Non-Aligned Movement and movedcloser to the US. Mr Menem supported UN intervention in Iraq, Bosnia andHaiti, even sending troops to participate in the operations. The governmentalso dismantled the Cóndor missile programme—which had been heavily criti-cised by the US administration—ratified the Tlatelolco document and pro-posed that the administration of the US president, Bill Clinton, upgradeArgentina to the category of an “extra-NATO” ally of the US. Mr Menem alsobecame one of the most vociferous critics of the Cuban president, Fidel Castro.

Similarly, relations with the UK were normalised and the Falklands sovereigntyissue set aside. The government has not renounced Argentinian claims to theislands, but has renounced the use of force to retrieve them. Following a policyof “charm diplomacy”, it has considered giving financial compensation to theislanders to settle the issue. In 1995 after months of negotiations theArgentinian and UK governments signed an agreement to share the potentialeconomic benefits from oil exploration in a specially designated area in theSouth Atlantic.

Improving relations withneighbouring countries

One area in which the Alfonsín and Menem administrations have been consis-tent is in their approach to neighbouring countries. Relations with Argentina’stwo largest neighbours—Brazil and Chile—had traditionally been poor. Brazilwas generally regarded as a threat to Argentinian supremacy in the region,while long-standing border disputes with Chile frequently inflamedArgentinian nationalism. Mr Alfonsín radically changed the approach. In 1985he and the then Brazilian president, José Sarney, launched a bilateral economicco-operation programme, to be followed in 1991 by the Treaty of Asunciónlaunching Mercado Común del Sur (Mercosur), the common market of thesouth. Yet co-operation with Brazil went far beyond economic issues. TheArgentinian and Brazilian governments have developed a foreign policy con-sultation mechanism, agreed on the mutual inspection of nuclear facilities andlaunched a military co-operation programme.

Argentina and Chile almost went to war in 1978 over three islands in theBeagle Channel. In 1984 the UCR government put a solution reached byarbitration (which did not favour Argentinian claims) to a plebiscite whichreceived majority support. Likewise, Mr Menem closed all pending territorialdisputes with Chile when he signed a Tratado de Paz y Amistad (Treaty of Peaceand Friendship). As a result, the Laguna del Desierto border dispute was re-solved by arbitration in 1994. Yet the agreement reached by the two

Argentina: International relations and defence 11

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

governments over the division of the continental glaciers area has so far failedto obtain legislative approval in either of the countries. If the agreement fails tobe passed by their respective legislatures the issue will have to be put before anarbitration panel. Mr Menem is keen to solve the issue before 1999 in order toconclude his term as the president who brought to an end all pending territo-rial disputes with Chile.

The establishment of Mercosur is a key part of this policy of regional economicand political co-operation. Mercosur is a customs union comprising Argentina,Brazil, Paraguay and Uruguay, and it has so far signed free-trade agreements(FTAs) with Chile (June 1996) and Bolivia (December 1996). Negotiations ofother FTAs with the Andean community (Colombia, Ecuador and Venezuela)and Peru are currently under way, following the pattern set by the Mercosur-Chile FTA. Mercosur (and unilateral trade liberalisation) has presided over aperiod of rapid growth of intra-regional trade and, to a lesser extent, invest-ment flows.

Finding a new role for thearmed forces

Improved relations with Brazil and Chile have had a major impact on the role ofArgentinian armed forces, as two traditional perceived threats to national secu-rity have almost disappeared. This development added to the military’s identitycrisis, originally brought about by the Falklands fiasco and the “dirty war”revelations. Once one of the largest and proudest armed forces in Latin America,the Argentinian military lost both influence and prestige in the 1980s. Morerecently, military spending has been trimmed because of fiscal constraints. Asthe carapintadas’ (junior officers’) uprisings were brought to an end in 1990 andthe armed forces were purged of anti-democratic elements, the challenge was tofind a new role for the military. Participation in UN peacekeeping operationswas instrumental in reincorporating a heavily criticised and demoralised mili-tary into social life. Yet professionalisation has advanced slowly, the last stepbeing the replacement of conscription with voluntary service.

The government and Congress are working on new legislation to restructurethe national defence system. The aim is to downsize the military and upgradeits abilities. In the process it may lose some of its traditional privileges, such asspecial social security and retirement regimes. Yet so far few details of thereform have been agreed or made public. The more expeditious privatisation ofthe remaining arms industries announced after the scandals of illegal armssales to Ecuador and Bosnia has also failed to materialise.

The Southern Cone countries’ armed forces compared

Argentina Brazil Chile

Land area (’000 sq km) 2,950 8,511 757

Population (m) 33.5 158.0 14.0

Total armed forces personnel (no.) 72,300 294,000 95,000 Army 40,000 195,000 56,000 Navy 19,000 50,000 25,000 Air force 13,300 49,000 14,000Source: EIU.

12 Argentina: International relations and defence

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

The economy

Economic structure

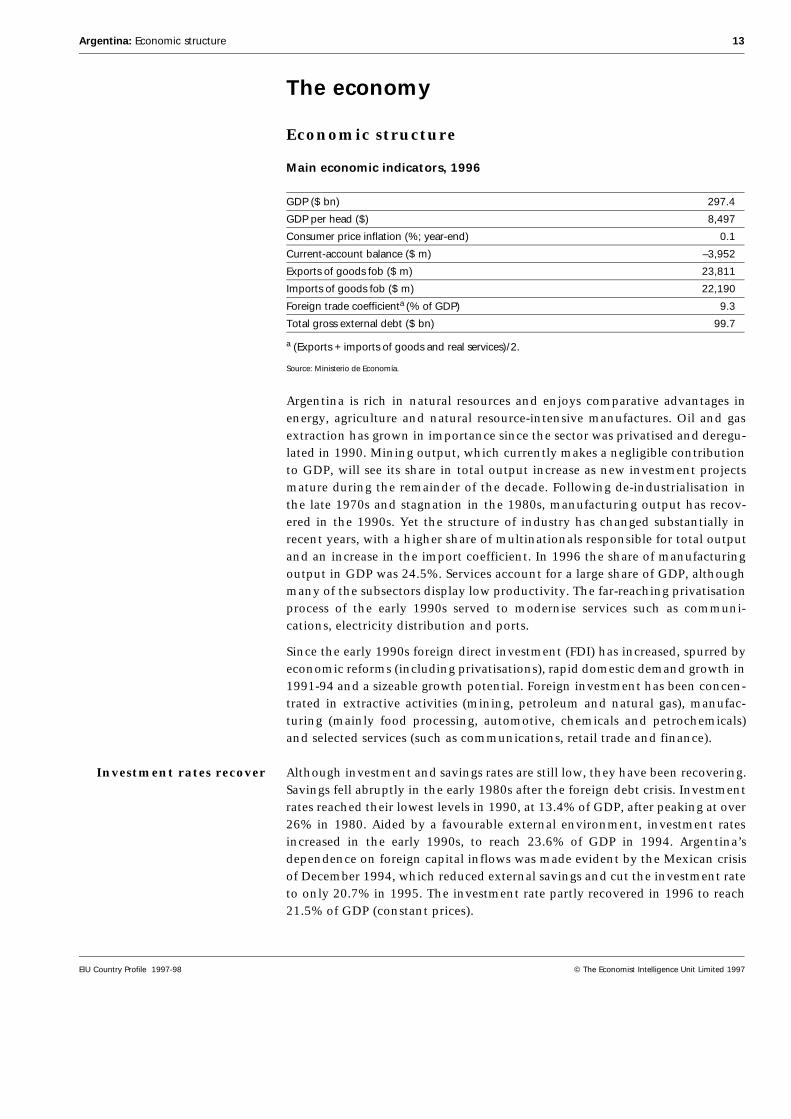

Main economic indicators, 1996

GDP ($ bn) 297.4

GDP per head ($) 8,497

Consumer price inflation (%; year-end) 0.1

Current-account balance ($ m) –3,952

Exports of goods fob ($ m) 23,811

Imports of goods fob ($ m) 22,190

Foreign trade coefficienta (% of GDP) 9.3

Total gross external debt ($ bn) 99.7

a (Exports + imports of goods and real services)/2.

Source: Ministerio de Economía.

Argentina is rich in natural resources and enjoys comparative advantages inenergy, agriculture and natural resource-intensive manufactures. Oil and gasextraction has grown in importance since the sector was privatised and deregu-lated in 1990. Mining output, which currently makes a negligible contributionto GDP, will see its share in total output increase as new investment projectsmature during the remainder of the decade. Following de-industrialisation inthe late 1970s and stagnation in the 1980s, manufacturing output has recov-ered in the 1990s. Yet the structure of industry has changed substantially inrecent years, with a higher share of multinationals responsible for total outputand an increase in the import coefficient. In 1996 the share of manufacturingoutput in GDP was 24.5%. Services account for a large share of GDP, althoughmany of the subsectors display low productivity. The far-reaching privatisationprocess of the early 1990s served to modernise services such as communi-cations, electricity distribution and ports.

Since the early 1990s foreign direct investment (FDI) has increased, spurred byeconomic reforms (including privatisations), rapid domestic demand growth in1991-94 and a sizeable growth potential. Foreign investment has been concen-trated in extractive activities (mining, petroleum and natural gas), manufac-turing (mainly food processing, automotive, chemicals and petrochemicals)and selected services (such as communications, retail trade and finance).

Investment rates recover Although investment and savings rates are still low, they have been recovering.Savings fell abruptly in the early 1980s after the foreign debt crisis. Investmentrates reached their lowest levels in 1990, at 13.4% of GDP, after peaking at over26% in 1980. Aided by a favourable external environment, investment ratesincreased in the early 1990s, to reach 23.6% of GDP in 1994. Argentina’sdependence on foreign capital inflows was made evident by the Mexican crisisof December 1994, which reduced external savings and cut the investment rateto only 20.7% in 1995. The investment rate partly recovered in 1996 to reach21.5% of GDP (constant prices).

Argentina: Economic structure 13

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

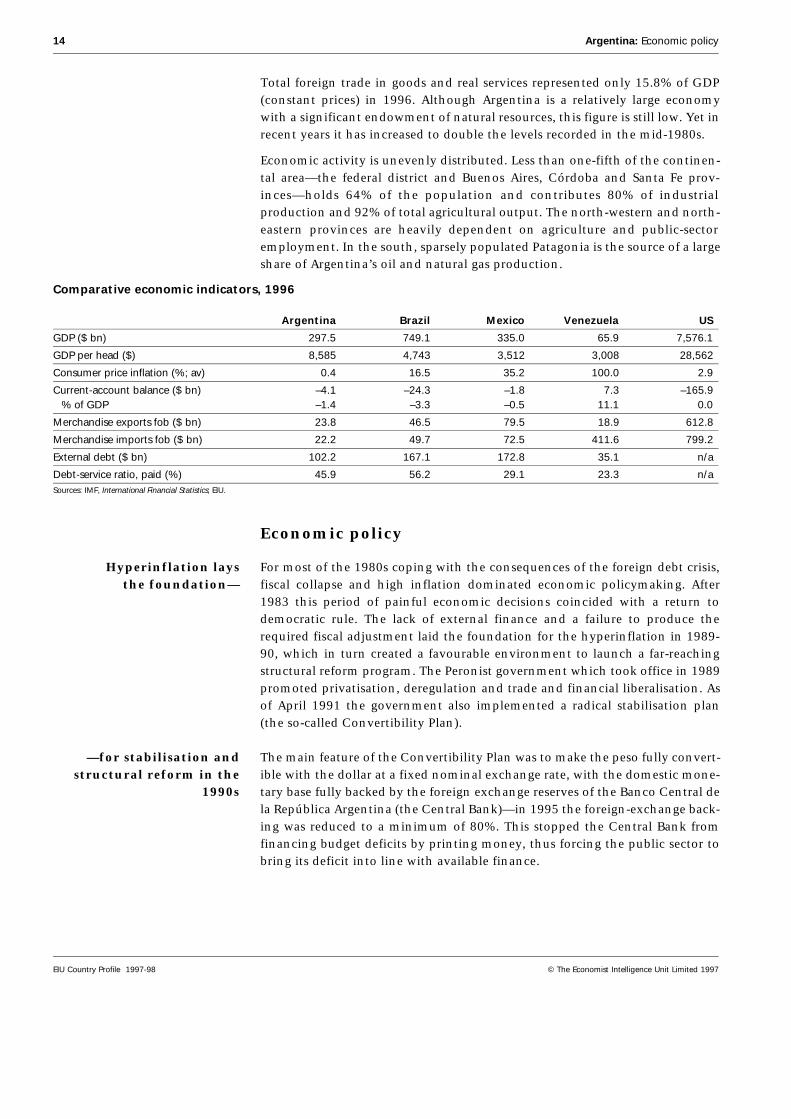

Total foreign trade in goods and real services represented only 15.8% of GDP(constant prices) in 1996. Although Argentina is a relatively large economywith a significant endowment of natural resources, this figure is still low. Yet inrecent years it has increased to double the levels recorded in the mid-1980s.

Economic activity is unevenly distributed. Less than one-fifth of the continen-tal area—the federal district and Buenos Aires, Córdoba and Santa Fe prov-inces—holds 64% of the population and contributes 80% of industrialproduction and 92% of total agricultural output. The north-western and north-eastern provinces are heavily dependent on agriculture and public-sectoremployment. In the south, sparsely populated Patagonia is the source of a largeshare of Argentina’s oil and natural gas production.

Comparative economic indicators, 1996

Argentina Brazil Mexico Venezuela US

GDP ($ bn) 297.5 749.1 335.0 65.9 7,576.1

GDP per head ($) 8,585 4,743 3,512 3,008 28,562

Consumer price inflation (%; av) 0.4 16.5 35.2 100.0 2.9

Current-account balance ($ bn) –4.1 –24.3 –1.8 7.3 –165.9 % of GDP –1.4 –3.3 –0.5 11.1 0.0

Merchandise exports fob ($ bn) 23.8 46.5 79.5 18.9 612.8

Merchandise imports fob ($ bn) 22.2 49.7 72.5 411.6 799.2

External debt ($ bn) 102.2 167.1 172.8 35.1 n/a

Debt-service ratio, paid (%) 45.9 56.2 29.1 23.3 n/aSources: IMF, International Financial Statistics; EIU.

Economic policy

Hyperinflation laysthe foundation—

For most of the 1980s coping with the consequences of the foreign debt crisis,fiscal collapse and high inflation dominated economic policymaking. After1983 this period of painful economic decisions coincided with a return todemocratic rule. The lack of external finance and a failure to produce therequired fiscal adjustment laid the foundation for the hyperinflation in 1989-90, which in turn created a favourable environment to launch a far-reachingstructural reform program. The Peronist government which took office in 1989promoted privatisation, deregulation and trade and financial liberalisation. Asof April 1991 the government also implemented a radical stabilisation plan(the so-called Convertibility Plan).

—for stabilisation andstructural reform in the

1990s

The main feature of the Convertibility Plan was to make the peso fully convert-ible with the dollar at a fixed nominal exchange rate, with the domestic mone-tary base fully backed by the foreign exchange reserves of the Banco Central dela República Argentina (the Central Bank)—in 1995 the foreign-exchange back-ing was reduced to a minimum of 80%. This stopped the Central Bank fromfinancing budget deficits by printing money, thus forcing the public sector tobring its deficit into line with available finance.

14 Argentina: Economic policy

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Important recent economic policy events

1991: The Convertibility Law fixes the Ps:$ exchange rate and declares fullconvertibility of the domestic currency. The monetary base is to be fully backed byinternational reserves.1992: Congress approves a new Central Bank charter establishing the independenceof monetary authorities.1993: The government agrees a debt-reduction package with commercial banks.Liabilities with commercial banks are exchanged for collateralised bonds.1994: The pension system is reformed to allow for the participation of privatepension funds.1995: The Central Bank charter is reformed to allow more flexibility in managingliquidity crises.1996: The government launches a “second reform of the state” which aims toreduce public-sector expenditure and enhance efficiency, but implementation ishalf-hearted.1997: The government agrees a labour-reform proposal with the labour unions, butis unable to mobilise business support.

The aggressive privatisation programme launched in the early 1990s aimed toease the stance of the public sector in the short term (providing fresh cash anddebt reduction or permitting lower spending) and to raise efficiency in themedium term. Although the first privatisations were poorly managed, the recordimproved as urgency receded and experience was gained. By 1996 the govern-ment had privatised most public utilities—telecommunications, airlines, powergeneration and distribution, gas transportation and distribution, water and sew-erage systems, and passenger and cargo railways—and sold the vast majority ofproductive facilities (including oil and gas extraction, coal mining, petrochemi-cals plants and steel mills). The Banco Hipotecario Nacional (national mortgagebank), the post office, the airports network and the nuclear power stations willbe transferred to the private sector in 1998. Divestiture operations have raised atotal of $17.6bn ($11.3bn in cash and $6.3bn in debt reduction at marketprices). The privatisation of public banks, electricity generation and distrib-ution, and water and sewerage systems by provincial governments has speededup since 1995 but progress has been uneven.

Structural reform also eliminated price and interest rate controls, deregulatedthe majority of economic activities, further liberalised the foreign investmentregime and removed most export taxes and quantitative restrictions on im-ports. Import levies were cut (in 1995 Argentina adopted Mercosur’s commonexternal tariff) and the tax system simplified around a value-added tax (VAT),which is easy to collect and in 1996 contributed 55% of the total tax revenue(excluding contributions to the social security system). The authorities arecurrently studying a major reform of the tax system to simplify it and improvecompliance. The so-called second reform of the state aims to reorganise thepublic sector (through employment cuts and the elimination or reorganisationof public-sector agencies) to improve efficiency and reduce government spend-ing. So far progress has been modest.

Argentina: Economic policy 15

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Fiscal consistency turnsinto a key issue over the

medium term

The fiscal stance improved considerably during the Convertibility Plan’s earlyyears because rapid economic growth produced a significant increase in public-sector revenue. The simplified tax structure and measures to fight tax evasionalso made a contribution. After 1994 the fiscal performance gradually worsened:public spending continued to grow (particularly interest payments and transfersto provinces) as revenue contracted under the impact of structural reform meas-ures (such as the implementation of a private retirement system) and the dropin consumption spending brought about by the Mexican crisis.

The ensuing capital flight ($8bn in deposits—15% of the total—left the banksin only five months) brought financial fragility to the forefront. In the shortterm the run on bank deposits was successfully contained by a reactivation ofthe extended fund facility (EFF) agreement with the IMF which had beensuspended in 1994, a restrictive fiscal package and a reduction of exchange rateuncertainty brought about by Mr Menem’s re-election in May 1995. Thesemeasures prevented a major financial crisis and presided over a recovery indeposits and a sharp fall in interest rates after mid-1995. But easier creditconditions did not pull the economy out of the recession.

A new standby agreement signed with the IMF in early 1996 committed thegovernment to strict fiscal targets (a balanced budget for the year), but failureto comply led to a renegotiation of targets and a new fiscal restraint package inOctober. Notwithstanding these measures, the 1996 fiscal deficit reached thehighest level since the launching of the Convertibility Plan ($5.3bn, equivalentto 1.8% of GDP). The imbalance was cut in 1997 to around $3bn, as agreedwith the IMF.

Strengthening thefinancial system

A continued recovery in deposits and credits throughout 1996 made thegovernment’s efforts to strengthen the financial system easier. The CentralBank authorities arranged $6bn in contingency credit lines with foreign banksto be disbursed in case of emergency. Minimum liquidity requirements weregradually raised to enhance banks’ reserves and strengthen the banks’ ability torespond to deposit flight. Similarly, oversight activities were upgraded andbanking concentration stimulated (see Financial services).

With monetary policy severely constrained by the Convertibility Plan, theauthorities must rely on fiscal policy and microeconomic reforms to spureconomic growth. Against this background, the increase in public-sector defi-cits during 1995 and 1996 was not unwelcome because it served as a counter-cyclical influence. But with growth restored, fiscal consolidation has againbecome a priority. A reform of the tax revenue-sharing system will be needed ifthe increase in tax revenue is to be prevented from being automatically trans-ferred into higher spending on the part of local governments.

With a strong economic recovery under way and unemployment still at veryhigh rates, the debate over whether more active (targeted) policies are neces-sary has reignited.

16 Argentina: Economic policy

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Public-sector accounts(Ps bn)

1996 1997a

Current revenue 47.7 53.7

Current expenditure 53.0 55.2

Primary surplus (excl privatisations) –1.1 1.4

Privatisation receipts 0.4 0.3

Primary surplus –0.7 1.7

Interest payments 4.6 4.7

Balance –5.3 –3.0

a Estimates.

Sources: Secretaría de Hacienda; Carta Económica.

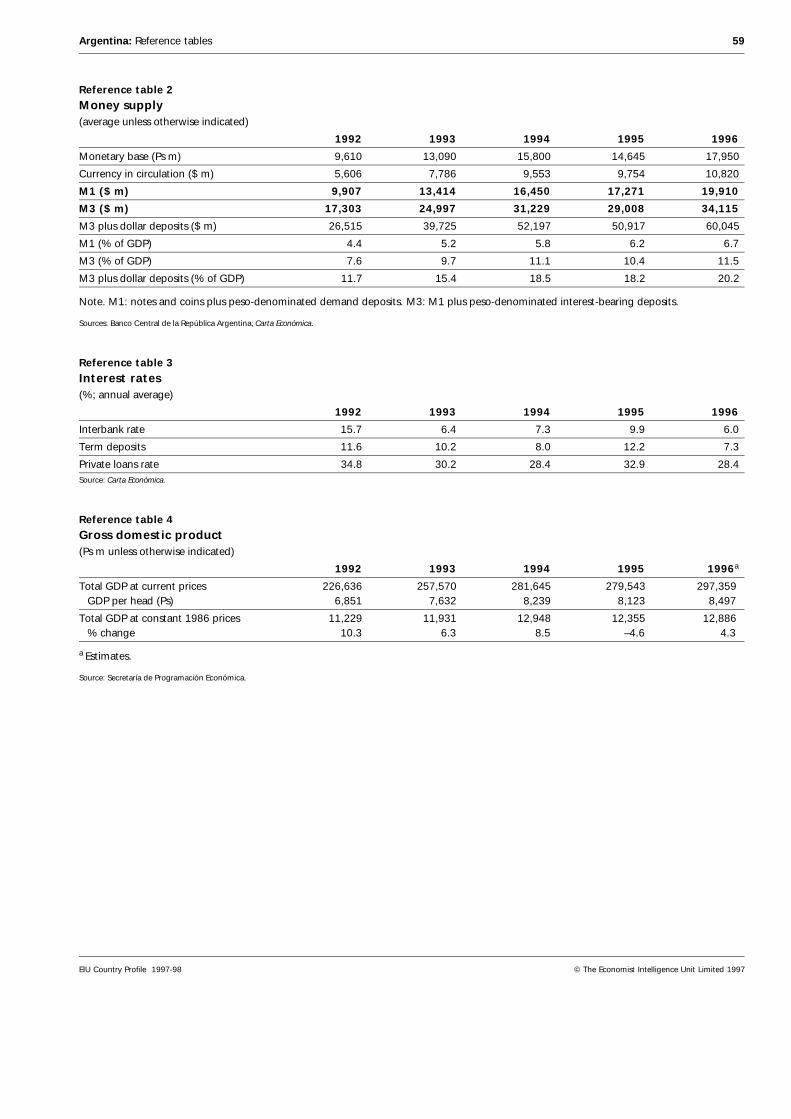

(Historical data on public finances are given in Reference table 1; data onmonetary indicators are in Reference table 2; data on interest rates are inReference table 3.)

Economic performance

For many decades Argentinians have had to tolerate high inflation. But theproblem became much worse as a result of the 1982 debt crisis, which provokedmajor devaluations and a severe contraction of the peso-denominated finan-cial system. Economic growth suffered as financial intermediation declinedand capital flight turned into an endemic feature of the economy. Productiveinvestment was discouraged and resource allocation became inefficient as aresult of high and volatile inflation rates, turning economic stabilisation into aprerequisite of improved economic performance. Against this background thepost-1990 economic stabilisation record has been encouraging. Inflation fellrapidly and growth was fast, aided by a favourable international financialenvironment. The initial shift in relative prices in favour of non-tradeablegoods brought about by the fixed nominal exchange rate was partially reversedafter 1994.

A rapid economic recoveryfollows the Mexican crisis

Owing to the disappointing economic performance of the preceeding decade,in 1990 real output was still slightly below the 1982 level. Yet successful eco-nomic stabilisation and a favourable international financial environment al-lowed real GDP to expand by more than 40% between 1990 and 1994.Domestic demand was the major force behind economic growth, with grossfixed investment being the most dynamic component of aggregate demand.During 1990-94 fixed capital formation rose by nearly 150%, taking the invest-ment rate to the highest level since the 1982 debt crisis—23.6% of GDP (seeReference table 7). Consumption expenditure also expanded rapidly, rising by46% between 1990 and 1994. Domestic demand was fuelled by sizeable inflowsof foreign capital, partly reflected in a rapid accumulation of foreign reservesand an increase in the monetary base. Until 1994 net external demand made anegative contribution to GDP growth as slow export expansion combined withrapidly growing imports.

Argentina: Economic performance 17

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Growth in gross domestic product(% real change)

Average1990-94 1995 1996

GDP 8.9 –4.6 4.3

Goods-producing sectors 8.0 –4.6 4.2 Agriculture, forestry & fishing 2.5 2.3 1.6 Mining & quarrying 8.2 6.7 8.1 Manufacturing 7.8 –7.0 5.2 Electricity, gas & water 8.0 5.6 4.8 Construction 17.1 –10.9 1.1

Services-producing sectors 9.0 –3.0 4.5 Finance, insurance & real estate 11.7 –0.2 5.5 Commerce 10.5 –7.9 4.5 Transport & communications 9.5 0.2 5.8 Community, social & personal services 5.7 –1.9 3.1Source: Secretaría de Programación Económica.

The external shock of the Mexican crisis reversed foreign capital flows, causinga deep contraction of domestic demand. Production declined and the economydipped into a sharp recession. Fixed investment suffered badly, contracting by16%. Then exports increased in what turned out to be a remarkable externaladjustment, in turn explaining why the economic downturn was not deeper.The recovery which followed the 1995 recession was particularly strong, withinvestment and exports being the leading sectors.

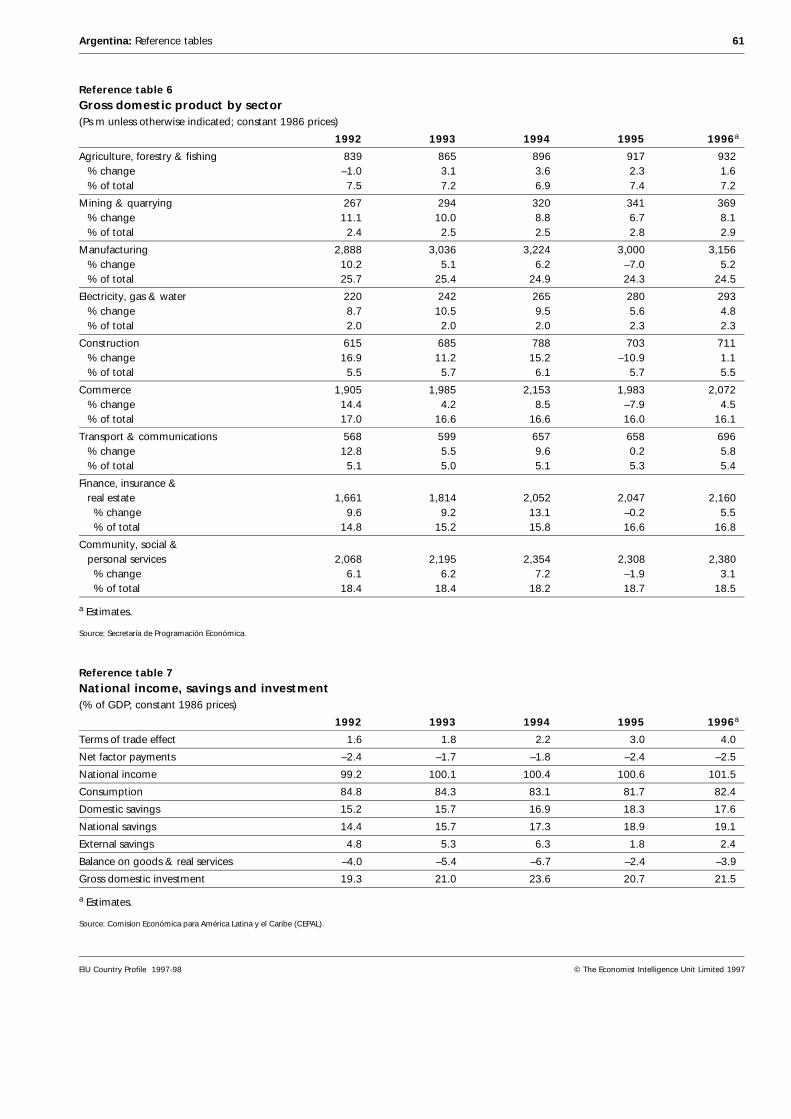

During the expansionary phase of the early 1990s manufacturing growthlagged behind total output growth, a feature which was reversed in the post-1995 recession period. Until 1994 a large share of manufacturing outputgrowth was accounted for by a fourfold increase in car production. Construc-tion and some service activities (for example, financial services and commerce)also expanded rapidly. The sharp 1995 recession hit construction, trade andmanufacturing hard. (Historical data on GDP are given in Reference tables 4-6).But by mid-1997 a new industrial production record was achieved.

Price stability improvesthe real exchange rate—

The Convertibility Plan is to be credited for restoring price stability in aneconomy characterised by decades of high inflation rates. It is most remarkablethat in the 1990-94 period this was achieved in the context of an expandingeconomy. During the 1995 recession a slight deflation in consumer prices wasrecorded, to be followed by price stability thereafter. In 1996 the consumerprice index (CPI) rose by just 0.2%, one of the lowest inflation rates worldwide,compared with a record of 4,900% in 1989.

Falling consumer prices and rising wholesale prices (particularly of agriculturaland industrial commodities) have improved the relative price of tradeablegoods and hence the real exchange rate. The wholesale/consumer price indexratio (a measure of the real exchange rate), which fell by 31% in the March1991-March 1994 period, rose by 6.3% between March 1994 and March 1997.(Data on various prices measures are given in Reference table 9.)

18 Argentina: Economic performance

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Inflation(% change)

Annual average1996 1991-95

Consumer prices 0.2 10.4

Wholesale prices 3.2 3.9Source: Instituto Nacional de Estadística y Censos.

—but unemploymentpeaks and incomeinequality widens

The percentage of families living below the poverty line fell from 38% in 1989(in the middle of hyperinflation) to 14% in 1994, but rose again to 20.1% in1996 as a result of higher unemployment. Real wages have fallen in every yearexcept 1994 (when they rose by a modest 0.6%) and remain well below theaverage for the 1980s.

The most disappointing development of recent years has been the steady rise inthe unemployment rate, which rose from 6.9% in May 1991 to 16.1% in May1997, after peaking at 18.4% in May 1995. In certain urban areas the unemploy-ment rate is near 20%. If the 13.2% underemployment rate is taken intoaccount, almost 30% of the active population (about 3.7m people) currently faceemployment problems. Since the beginning of the Convertibility Plan in 1991 anet total of almost 730,000 jobs have been created. Yet the unemployment ratestill increased owing to an even faster increase in the supply of labour.

The government has responded with a battery of measures aimed at reducinglabour costs (cutting employers’ social security contributions) and further liber-alising the labour market (creating a flexible employment regime for small andmedium-sized firms, authorising more flexible labour contracts and imple-menting new works accident legislation). But the impact of these measures onunemployment is hard to assess: the sharp 1995 recession and widespreadrestructuring in the public and private sectors seem to have been far moresignificant determinants of the trends prevailing in the labour market. Further-more, new forms of contract have contributed to more precarious jobs: tempo-rary employment has increased at the expense of permanent positions. A moreprofound reform of labour regulations is under negotiation, particularly inreference to redundancy payments and collective bargaining mechanisms.

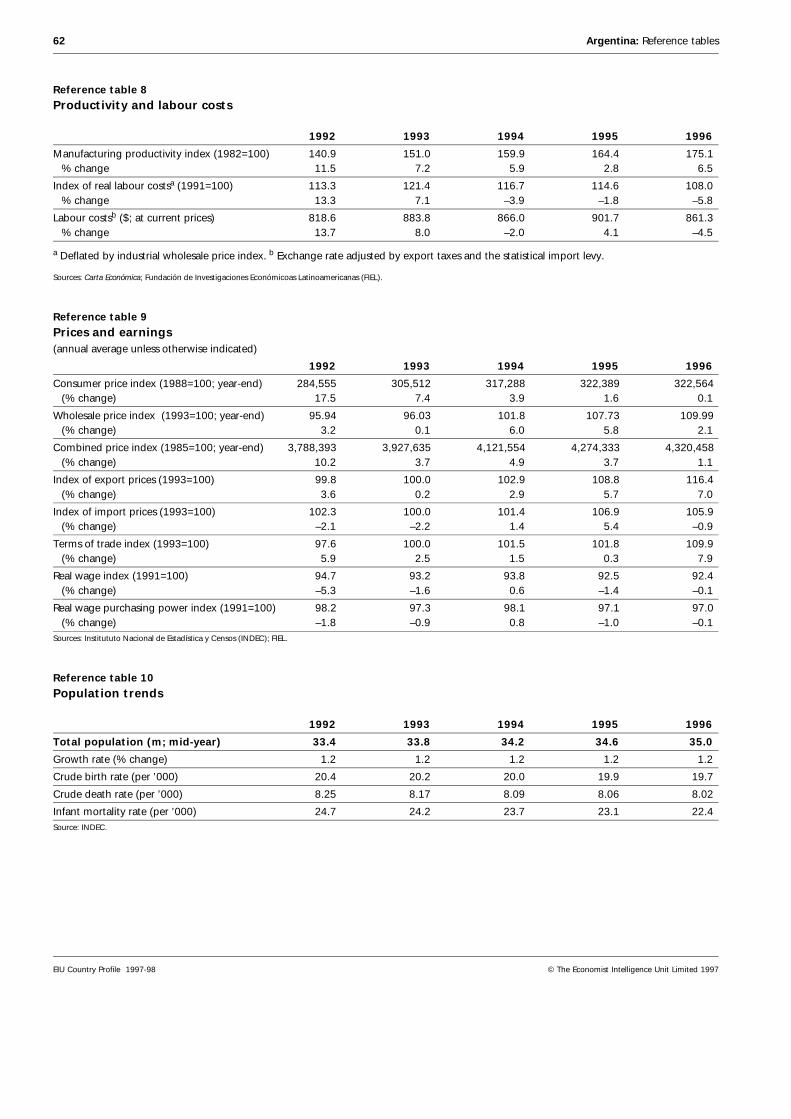

The reach of the social safety net is extremely narrow: less than 10% of thejobless receive unemployment compensation (compared with over one-thirdin Spain and the US) or are beneficiaries of government-sponsored employ-ment programmes. (Historical data are given in Reference table 8.)

Regional trends

Many provinces sufferfrom reform—

Most of Argentina’s 23 provinces did not benefit from rapid economic growthin the 1990-94 period and were severely hit by the 1995 recession. The north-western and north-eastern provinces have been hit by the crisis affecting trad-itional agricultural crops such as sugar cane and tobacco. The southernprovinces suffered as a result of the privatised and deregulated oil industryshedding jobs and the termination of industrial promotion schemes. Oldindustrial centres, such as Rosario in Santa Fe province, have also experienceda severe decline.

Argentina: Regional trends 19

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

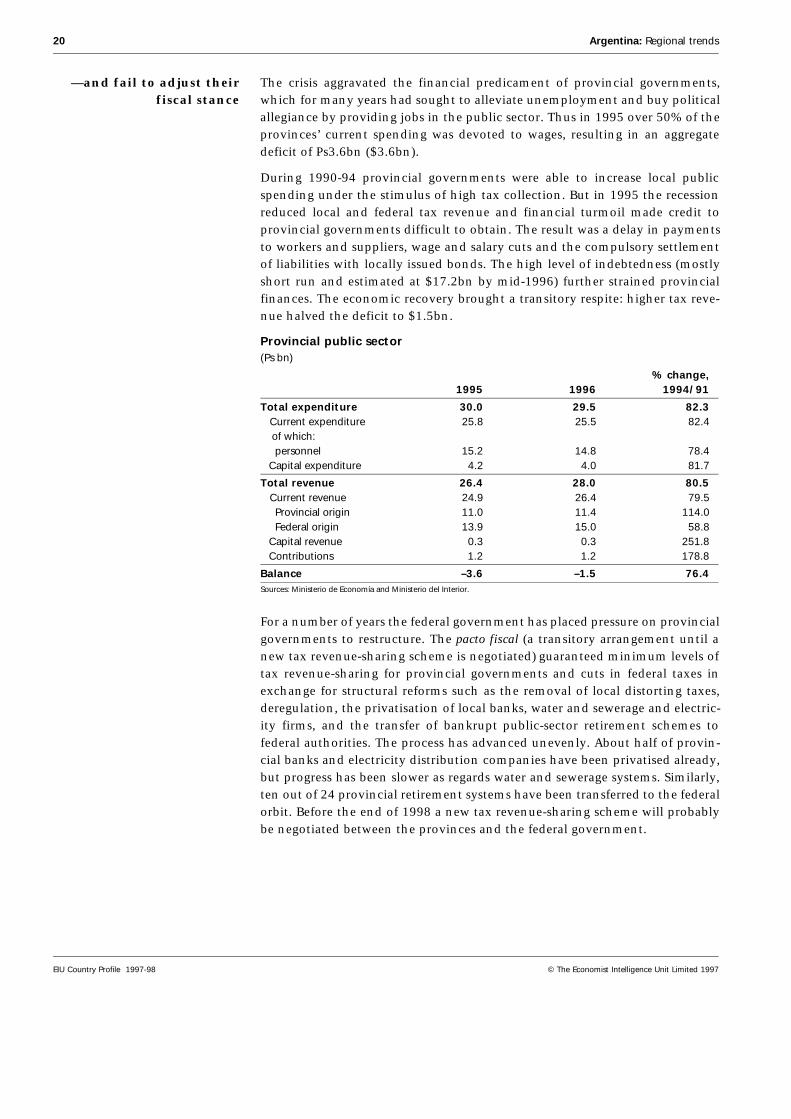

—and fail to adjust theirfiscal stance

The crisis aggravated the financial predicament of provincial governments,which for many years had sought to alleviate unemployment and buy politicalallegiance by providing jobs in the public sector. Thus in 1995 over 50% of theprovinces’ current spending was devoted to wages, resulting in an aggregatedeficit of Ps3.6bn ($3.6bn).

During 1990-94 provincial governments were able to increase local publicspending under the stimulus of high tax collection. But in 1995 the recessionreduced local and federal tax revenue and financial turmoil made credit toprovincial governments difficult to obtain. The result was a delay in paymentsto workers and suppliers, wage and salary cuts and the compulsory settlementof liabilities with locally issued bonds. The high level of indebtedness (mostlyshort run and estimated at $17.2bn by mid-1996) further strained provincialfinances. The economic recovery brought a transitory respite: higher tax reve-nue halved the deficit to $1.5bn.

Provincial public sector(Ps bn)

% change,1995 1996 1994/91

Total expenditure 30.0 29.5 82.3 Current expenditure 25.8 25.5 82.4 of which: personnel 15.2 14.8 78.4 Capital expenditure 4.2 4.0 81.7

Total revenue 26.4 28.0 80.5 Current revenue 24.9 26.4 79.5 Provincial origin 11.0 11.4 114.0 Federal origin 13.9 15.0 58.8 Capital revenue 0.3 0.3 251.8 Contributions 1.2 1.2 178.8

Balance –3.6 –1.5 76.4Sources: Ministerio de Economía and Ministerio del Interior.

For a number of years the federal government has placed pressure on provincialgovernments to restructure. The pacto fiscal (a transitory arrangement until anew tax revenue-sharing scheme is negotiated) guaranteed minimum levels oftax revenue-sharing for provincial governments and cuts in federal taxes inexchange for structural reforms such as the removal of local distorting taxes,deregulation, the privatisation of local banks, water and sewerage and electric-ity firms, and the transfer of bankrupt public-sector retirement schemes tofederal authorities. The process has advanced unevenly. About half of provin-cial banks and electricity distribution companies have been privatised already,but progress has been slower as regards water and sewerage systems. Similarly,ten out of 24 provincial retirement systems have been transferred to the federalorbit. Before the end of 1998 a new tax revenue-sharing scheme will probablybe negotiated between the provinces and the federal government.

20 Argentina: Regional trends

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Resources

Population

According to official projections made on the basis of the 1991 census, in 1996Argentina’s population was 35m, the fourth largest in Latin America behindBrazil, Mexico and Colombia. Projections for 1995-2000 give a 1.2% averageannual rate of population growth, slightly below the Latin American average of1.5%. Argentina’s fertility rates are comparable to the Latin American average.Projections for the remainder of the decade would take the total population to36.6m by 2000 and 46.1m by 2025.

Relatively high life expectancy puts Argentina among the three Latin Americancountries with the lowest share of population below 15 years and the highestshare of population over 65 years. Infant mortality rates in 1996 were 22.4 per1,000 live births, approximately half the Latin American average, and lifeexpectancy was 69 and 76 for men and women respectively, four and threeyears higher than the Latin American average. (Population totals are given inReference table 10; labour force totals in Reference table 11.)

Comparative population indicators(%)

Argentina Brazil Chile Latin America

Annual average growth rate (1995-2000) 1.2 1.2 1.4 1.5

Fertility rate (children per woman, 1995-2000) 2.6 2.2 2.4 2.7

Population below 15 years of age (1995) 28.7 32.3 29.5 33.8

Population over 65 years of age (1995) 9.5 5.2 6.6 5.2

Urban population (1995) 88 78 84 74Sources: UN Fund for Population Activities, The State of the World Population 1997; Instituto Nacional de Estadística y Censos (INDEC).

Regional distribution Population density is low at 12.7 inhabitants per sq km in 1996 and 88% of thetotal is concentrated in urban centres. The Buenos Aires metropolitan area hasa population of approximately 10m, about one-third of the country’s totalpopulation. Córdoba and Rosario are the second and third largest urban cen-tres, with over 1m inhabitants each. The Buenos Aires metropolitan area and itshinterland (the pampas) are home to two-thirds of the population. This reflectsthe large numbers of European immigrants in the early 20th century and rapidindustrialisation in the post-war period which led to a redistribution of thepopulation.

Around 85% of thepopulation is of European

descent

An estimated 85% of the Argentinian population is of European descent,mostly from Italy and Spain. There have been sizeable inflows from central andeastern Europe. The rest consists of a small number of indigenous people, alarger number of mestizos (of mixed Indian and white ancestry) and the descen-dants of immigrants from the Middle East, mainly Syrians and Lebanese. In thelast two decades there has been a small inflow of Asians, mainly Koreans andChinese.

There has been a constant flow of immigration from neighbouring countriessince the 1950s (mainly Bolivia, Chile, Paraguay and Uruguay and, more

Argentina: Population 21

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

recently, Brazil and Peru). These flows gathered pace after 1991 when theeconomy recovered and the exchange rate appreciated. A number of these newimmigrants are undocumented and are employed in the informal sector of theeconomy. In the context of high unemployment rates, these new flows havebrought the debate on more stringent immigration laws and enforcement tothe fore. Yet Argentina has traditionally been a country open to immigrants,and it is likely to remain so in the future.

Housing The standard of housing varies across regions, but overall is better than in mostdeveloping countries. According to 1991 data, 93% of total dwellings hadelectricity and 92% were either connected to the natural gas network or usedbottled gas, 73% of the population had safe drinking water within their owndwellings and 69% had sanitary services (only 34% had sewerage services). Butovercrowding has worsened since the early 1980s: one-quarter of total dwell-ings were overcrowded in 1991 compared with 18.5% in 1980. The regionaldistribution of these figures is uneven. While almost 100% of the population ofthe federal district has sewerage systems, the share is only 31% for those livingin Buenos Aires province and shrinks to 13% in provinces such as Santiago delEstero or Chaco, and to 7% in Misiones.

Poverty indicators Poverty indicators, which improved in the early 1990s after peaking during thehyperinflation at the turn of the decade, worsened again during the 1995recession and thereafter. Available data for the Buenos Aires metropolitan area(which makes up one-third of the population) show that the percentage ofhouseholds below the poverty line, which fell significantly at the beginning ofthe decade, increased by more than 50% between 1994 and 1996. Part of thesehouseholds were formerly middle-class families displaced by economic restruc-turing. The share of households with unsatisfied basic needs and those belowthe indigency line also increased, the latter doubling from a minimum of 2.4%in 1992 to 5.5% in 1996. The recent rise in poverty indicators can be attributedto lower incomes as a result of high unemployment rates and the rise in theprice of basic staples and transportation, which make up a large share of lowincome groups’ spending.

Inequality has also increased in recent years, as income distribution has be-come more concentrated in the top of the pyramid. Between 1991 and 1996the share of total income held by the richest 10% of the population increasedby almost two percentage points (from 34.6% to 36.3%), whereas the incomeshare of the poorest 30% fell from 9.5% to 8.2%. These trends are reversing along-standing feature of Argentinian society, which is generally regarded asone of the most egalitarian in Latin America.

Poverty in the Buenos Aires metropolitan area(%)

1992 1993 1994 1995 1996

Households below the indigency line 2.4 3.1 2.8 4.5 5.5

Households with unsatisfied basic needs 14.2 13.4 14.7 11.8 12.3

Households below the poverty line 14.4 13.3 13.0 17.2 19.8Source: INDEC.

22 Argentina: Population

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Education

The early development of a system of state schools has encouraged high liter-acy rates (96% in 1993) and high enrolment in primary and secondary educ-ation. In the early 1990s around 86% of children of school age were enrolled inthe last year of primary school, while almost two-thirds of children in the13-17 age group were enrolled in secondary school. The system of highereducation is also broadly based, with a total of 82 universities, of which 36 arepublic, although the public education system has deteriorated in the last twodecades owing to the fiscal crisis of the federal and provincial governments.The private education system has been growing rapidly, but quality is ex-tremely uneven and coverage selective.

Primary and secondaryeducation has been

decentralised—

In the late 1970s primary education became less homogeneous as it was decen-tralised from the federal to the local level. The process was repeated in the early1990s with the decentralisation of secondary education. Reasons for shortfallsin local educational services include administrative and technical deficiencies,and the fact that in many districts the educational system became a source ofpolitically motivated public employment. A far-reaching reform process isunder way to improve educational services in the public and private sectors.

—and a reform process isunder way—

The educational system is being reformed on the basis of the 1993 FederalEducation Law. Until 1995 the structure of the education system consisted ofone initial non-mandatory pre-school year, seven mandatory years of primaryeducation, and five non-mandatory years of secondary education and highereducation; the new structure includes one initial mandatory pre-school year,nine years of mandatory basic education, a non-mandatory three-year modularcycle and higher education. These reforms are being implemented throughspecific agreements between the federal and provincial governments. Thegovernment originally expected the new structure to be fully operational by2001, but this is unlikely.

Provincial governments are in charge of implementing the reform. Althoughall of them have launched the process, progress is uneven owing to disparatetechnical abilities and, more importantly, poor financial resources. In effect,financing is the main constraint on the reform process. Lack of resourcesinhibit infrastructural investment required to extend the primary cycle to nineyears, while teachers’ participation has been unenthusiastic as a result of lowwages. Although the national government has put forward a federal trainingprogramme, it is unlikely that it will be enough to compensate for a long-termdeterioration in the quality of teachers. The progress and the results of thereform also differ between rich and poor local communities, which make itunlikely that the reform process will turn into a vehicle for reducing inequalityin the quality of the educational services provided.

—but lack of financialresources is hindering

implementation

The Federal Education Agreement, which was signed in September 1994 by thefederal government and most provincial governments, established that federaland provincial educational budgets would be increased by 20% per year during1995-99, and committed the federal government to investing a total of Ps3bnto improve buildings, provide new equipment and train teachers. Total

Argentina: Education 23

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

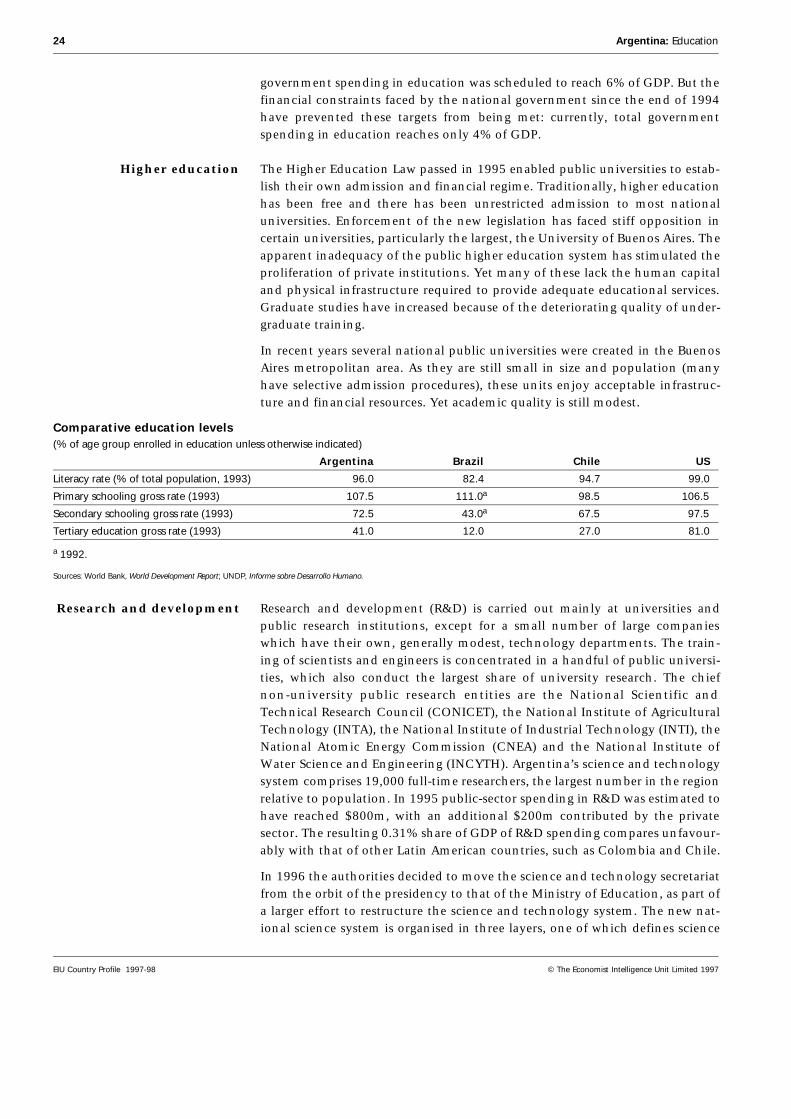

government spending in education was scheduled to reach 6% of GDP. But thefinancial constraints faced by the national government since the end of 1994have prevented these targets from being met: currently, total governmentspending in education reaches only 4% of GDP.

Higher education The Higher Education Law passed in 1995 enabled public universities to estab-lish their own admission and financial regime. Traditionally, higher educationhas been free and there has been unrestricted admission to most nationaluniversities. Enforcement of the new legislation has faced stiff opposition incertain universities, particularly the largest, the University of Buenos Aires. Theapparent inadequacy of the public higher education system has stimulated theproliferation of private institutions. Yet many of these lack the human capitaland physical infrastructure required to provide adequate educational services.Graduate studies have increased because of the deteriorating quality of under-graduate training.

In recent years several national public universities were created in the BuenosAires metropolitan area. As they are still small in size and population (manyhave selective admission procedures), these units enjoy acceptable infrastruc-ture and financial resources. Yet academic quality is still modest.

Comparative education levels(% of age group enrolled in education unless otherwise indicated)

Argentina Brazil Chile US

Literacy rate (% of total population, 1993) 96.0 82.4 94.7 99.0

Primary schooling gross rate (1993) 107.5 111.0a 98.5 106.5

Secondary schooling gross rate (1993) 72.5 43.0a 67.5 97.5

Tertiary education gross rate (1993) 41.0 12.0 27.0 81.0

a 1992.

Sources: World Bank, World Development Report; UNDP, Informe sobre Desarrollo Humano.

Research and development Research and development (R&D) is carried out mainly at universities andpublic research institutions, except for a small number of large companieswhich have their own, generally modest, technology departments. The train-ing of scientists and engineers is concentrated in a handful of public universi-ties, which also conduct the largest share of university research. The chiefnon-university public research entities are the National Scientific andTechnical Research Council (CONICET), the National Institute of AgriculturalTechnology (INTA), the National Institute of Industrial Technology (INTI), theNational Atomic Energy Commission (CNEA) and the National Institute ofWater Science and Engineering (INCYTH). Argentina’s science and technologysystem comprises 19,000 full-time researchers, the largest number in the regionrelative to population. In 1995 public-sector spending in R&D was estimated tohave reached $800m, with an additional $200m contributed by the privatesector. The resulting 0.31% share of GDP of R&D spending compares unfavour-ably with that of other Latin American countries, such as Colombia and Chile.

In 1996 the authorities decided to move the science and technology secretariatfrom the orbit of the presidency to that of the Ministry of Education, as part ofa larger effort to restructure the science and technology system. The new nat-ional science system is organised in three layers, one of which defines science

24 Argentina: Education

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

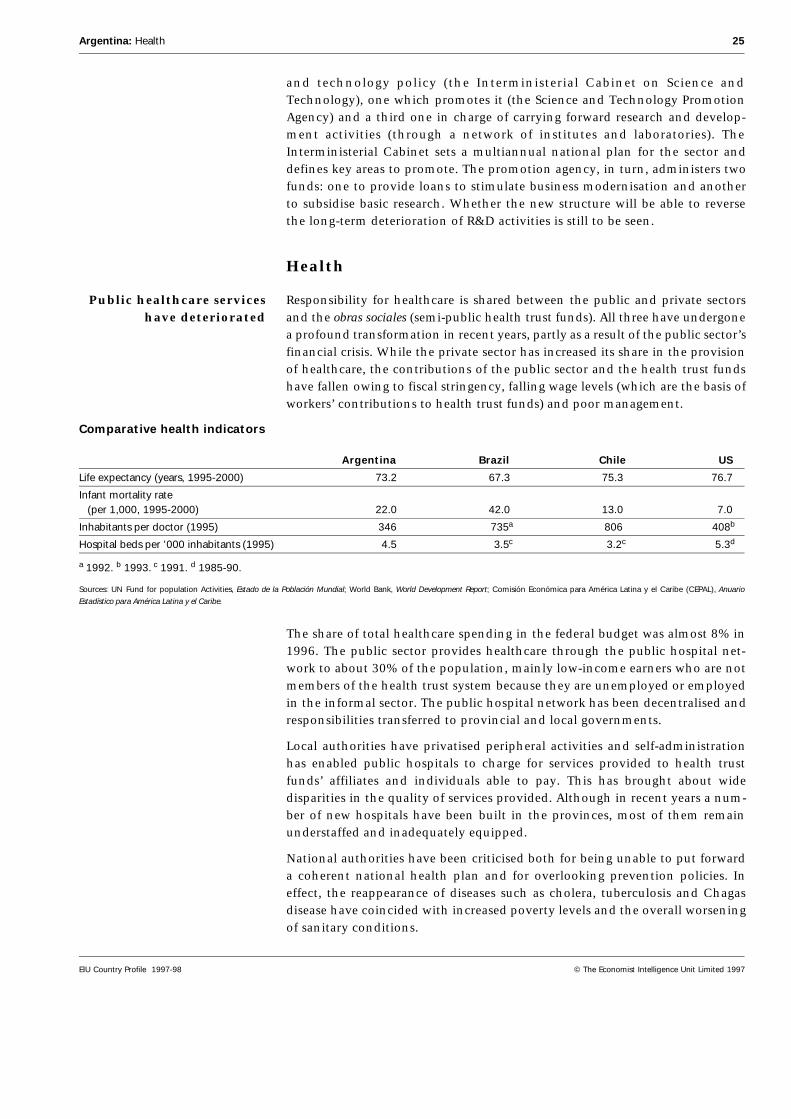

and technology policy (the Interministerial Cabinet on Science andTechnology), one which promotes it (the Science and Technology PromotionAgency) and a third one in charge of carrying forward research and develop-ment activities (through a network of institutes and laboratories). TheInterministerial Cabinet sets a multiannual national plan for the sector anddefines key areas to promote. The promotion agency, in turn, administers twofunds: one to provide loans to stimulate business modernisation and anotherto subsidise basic research. Whether the new structure will be able to reversethe long-term deterioration of R&D activities is still to be seen.

Health

Public healthcare serviceshave deteriorated

Responsibility for healthcare is shared between the public and private sectorsand the obras sociales (semi-public health trust funds). All three have undergonea profound transformation in recent years, partly as a result of the public sector’sfinancial crisis. While the private sector has increased its share in the provisionof healthcare, the contributions of the public sector and the health trust fundshave fallen owing to fiscal stringency, falling wage levels (which are the basis ofworkers’ contributions to health trust funds) and poor management.

Comparative health indicators

Argentina Brazil Chile US

Life expectancy (years, 1995-2000) 73.2 67.3 75.3 76.7

Infant mortality rate (per 1,000, 1995-2000) 22.0 42.0 13.0 7.0

Inhabitants per doctor (1995) 346 735a 806 408b

Hospital beds per ’000 inhabitants (1995) 4.5 3.5c 3.2c 5.3d

a 1992. b 1993. c 1991. d 1985-90.

Sources: UN Fund for population Activities, Estado de la Población Mundial; World Bank, World Development Report; Comisión Económica para América Latina y el Caribe (CEPAL), Anuario

Estadístico para América Latina y el Caribe.

The share of total healthcare spending in the federal budget was almost 8% in1996. The public sector provides healthcare through the public hospital net-work to about 30% of the population, mainly low-income earners who are notmembers of the health trust system because they are unemployed or employedin the informal sector. The public hospital network has been decentralised andresponsibilities transferred to provincial and local governments.

Local authorities have privatised peripheral activities and self-administrationhas enabled public hospitals to charge for services provided to health trustfunds’ affiliates and individuals able to pay. This has brought about widedisparities in the quality of services provided. Although in recent years a num-ber of new hospitals have been built in the provinces, most of them remainunderstaffed and inadequately equipped.

National authorities have been criticised both for being unable to put forwarda coherent national health plan and for overlooking prevention policies. Ineffect, the reappearance of diseases such as cholera, tuberculosis and Chagasdisease have coincided with increased poverty levels and the overall worseningof sanitary conditions.

Argentina: Health 25

EIU Country Profile 1997-98 © The Economist Intelligence Unit Limited 1997

Health trust funds Obras sociales provide healthcare services to about 65% of the population. Theyare pay-as-you-go systems based on compulsory payroll contributions madeboth by the employer and the employee and are co-ordinated by theAdministración Nacional del Seguro de Salud. Most of the 280 health trustfunds do not provide services directly, but subcontract to the private sector. Inthe context of a programme financed by the World Bank, this sector is experi-encing a major restructuring. The aim of the programme is to increase effi-ciency through enhanced competition and consolidation. The first step,implemented in early 1997, consisted of enabling the membership to changetheir health coverage from one obra social to another, an option taken by anestimated 150,000 individuals. The chance will be available once every year. Theprivate sector wants competition within the obras sociales segment to includeprivate healthcare providers, but so far this has been blocked by opposition fromthe trade unions, which administer many health trusts and significant financialresources.

Private-sector healthcare The crisis of public healthcare and health trust funds has stimulated growth ofprivately owned hospitals, diagnostic centres and prepaid healthcare systems,mostly concentrated in large urban centres. Prepaid healthcare insurance takescare of only 3% of the population, often subcontracting the provision of serv-ices. The World Bank-sponsored reform programme demands more stringentregulations of private healthcare systems, if the latter are to be allowed tocompete with the obras sociales. Currently, prepaid healthcare systems operateas commercial firms, with no public oversight either of the kind of services andcoverage provided or the responsibilities assumed.