Embed Size (px)

Citation preview

Applications of Parametric Quadratic Optimization

Oleksandr Romanko

Joint work with Alireza Ghaffari Hadigheh and Tamás Terlaky

November 1, 2004

2

Outline

Introduction Parametric QO Numerical illustration Simultaneous perturbation Financial portfolio example DSL example Multiparametric QO Conclusions and future work

3

Parametric optimization Parameter is introduced into objective

function and/or constraints The goal is to find

• – optimal solution

• – optimal value function

Allows to do

sensitivity analysis Applications

Introduction: Parametric Optimization

4

Convex Quadratic Optimization (QO) problem:

Quadratic Optimization and Its Parametric Counterpart

Parametric Convex Quadratic Optimization (PQO) problem:

5

Optimal Partition and Invariancy Intervals

The optimal partition of the index set {1, 2,…, n} is

The optimal partition is unique!!! Invariancy intervals:

Covering all invariancy intervals:

6

PQO:NumericalIllustration

type l u B N T () -----------------------------------------------------------------------------------------------------------------

invariancy interval +3.33333 Inf 3 4 5 1 2 0.002 - 0.00 + 0.00

transition point -8.00000 -8.00000 3 5 1 4 2 -0.00 invariancy interval -8.00000 -5.00000 2 3 5 1 4 8.502 + 68.00 + 0.00 transition point -5.00000 -5.00000 2 1 3 4 5 -127.50 invariancy interval -5.00000 +0.00000 1 2 3 4 5 4.002 + 35.50 - 50.00 transition point +0.00000 +0.00000 1 2 3 4 5 -50.00 invariancy interval +0.00000 +1.73913 1 2 3 4 5 -6.912 + 35.50 - 50.00 transition point +1.73913 +1.73913 2 3 4 5 1 -9.15 invariancy interval +1.73913 +3.33333 2 3 4 5 1 -3.602 + 24.00 - 40.00 transition point +3.33333 +3.33333 3 4 5 1 2 0.00

Solution output

7

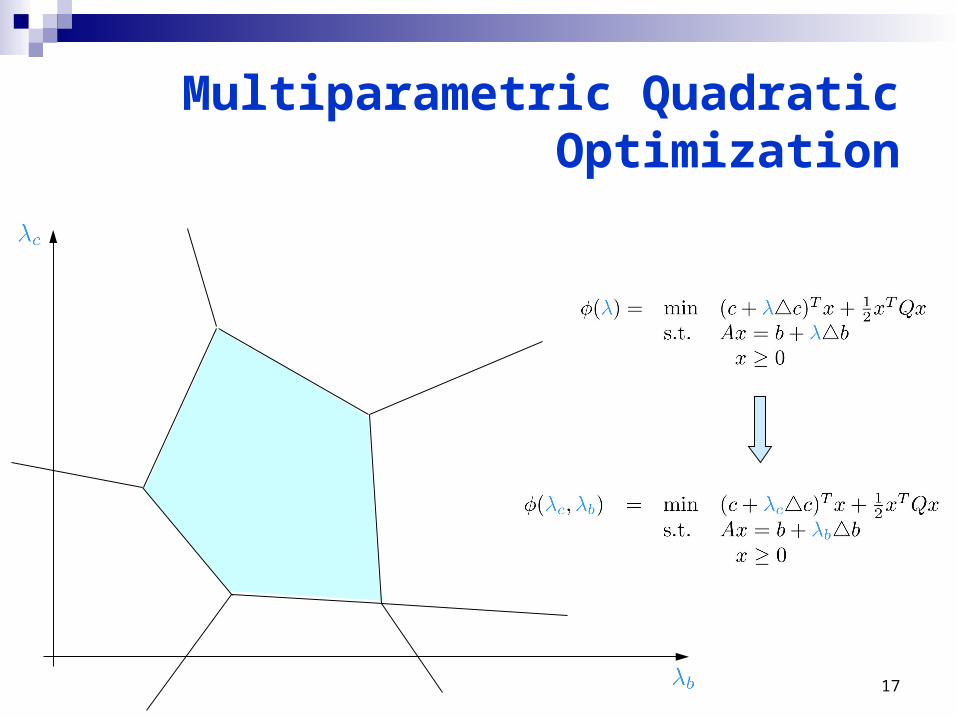

Simultaneous perturbation parametric QO can be extended to multiparametric QO:

Simultaneous Perturbation

Simultaneous perturbation parametric QO generalizes two models:

8

Financial Portfolio ExampleDate CocaCola Kodak HP IBM JP Morgan Walmart

Jul 1991 10.32% 5.73% 5.91% 4.25% -0.48% 11.40% Aug 1991 9.36% 5.23% -1.63% -4.32% 7.47% 6.30% Sep 1991 -1.90% -1.18% -6.38% 6.97% 6.50% -5.68% Oct 1991 3.29% 5.86% 1.77% -5.19% 9.05% -3.14% Nov 1991 4.13% 3.37% -4.47% -5.85% -7.34% 5.68% Dec 1991 15.68% 3.43% 18.44% -3.78% 14.38% 20.46% Jan 1992 -3.43% 4.69% 3.95% 1.12% -11.84% -8.49%

… … … … … … … Jan 1999 -2.52% -9.20% 14.73% -0.61% 0.42% 5.60% Feb 1999 -2.20% 1.24% -15.23% -7.37% 5.63% 0.15% Mar 1999 -3.91% -3.49% 2.07% 4.42% 10.71% 7.04% Apr 1999 10.90% 17.03% 16.31% 18.02% 9.22% -0.20%

May 1999 0.64% -9.53% 19.57% 10.91% 3.39% -7.34% Jun 1999 -9.49% 0.18% 6.56% 11.42% 0.85% 13.20% Jul 1999 -2.32% 2.03% 4.17% -2.76% -8.99% -12.44%

Aug 1999 -1.24% 6.24% 0.66% -0.90% 1.03% 4.88% Sep 1999 -19.33% 2.98% -13.88% -2.86% -11.56% 7.33% Expected Return

1.51% 1.11% 2.45% 2.01% 1.03% 1.79%

Standard Dev.

6.62% 6.50% 9.52% 8.71% 6.74% 7.47%

Problem of choosing an efficient portfolio of assets

50-year Annualized Returns

Return

Standard Deviation

Risk Stocks 11.0% 17.5% Bonds 6.0% 7.7% 40%/60% mix 8.4% 9.2% 50%/50% mix 9.0% 10.3% 60%/40% mix 9.3% 11.6%

9

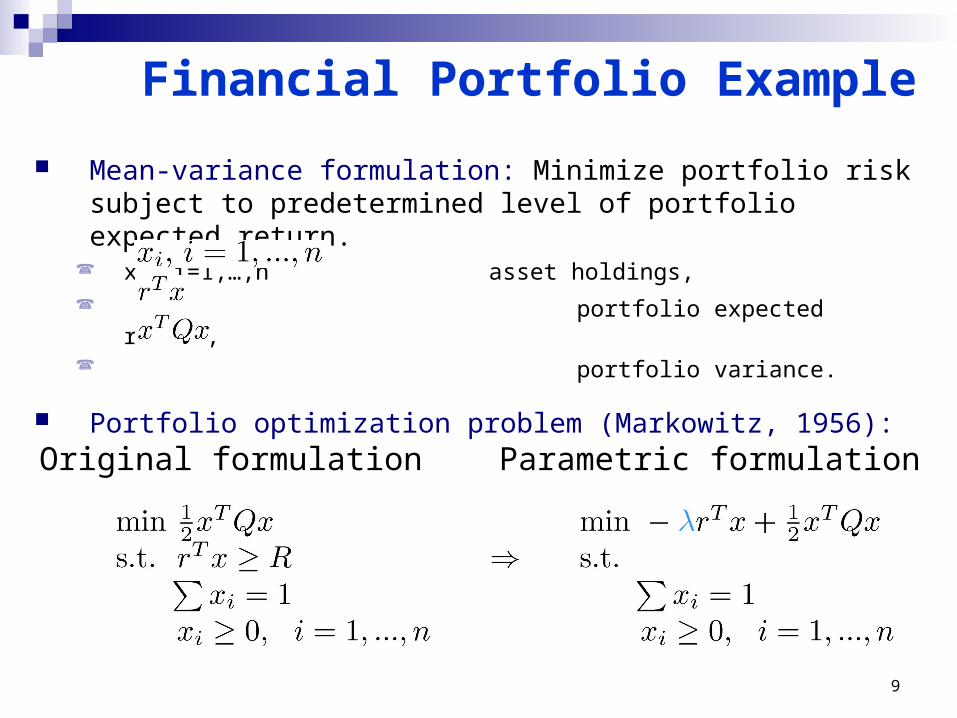

Mean-variance formulation: Minimize portfolio risk subject to predetermined level of portfolio expected return.

xi, i=1,…,n asset holdings,

portfolio expected return, portfolio variance.

Portfolio optimization problem (Markowitz, 1956):

Original formulation Parametric formulation

Financial Portfolio Example

10

Financial Portfolio Example

11

Mean-variance formulation: extensions

Financial Portfolio Example

the investor's risk aversion parameter influences not only risk-return preferences (in the objective function), but also

budget constraints transaction volumes upper bounds on asset holdings etc.

12

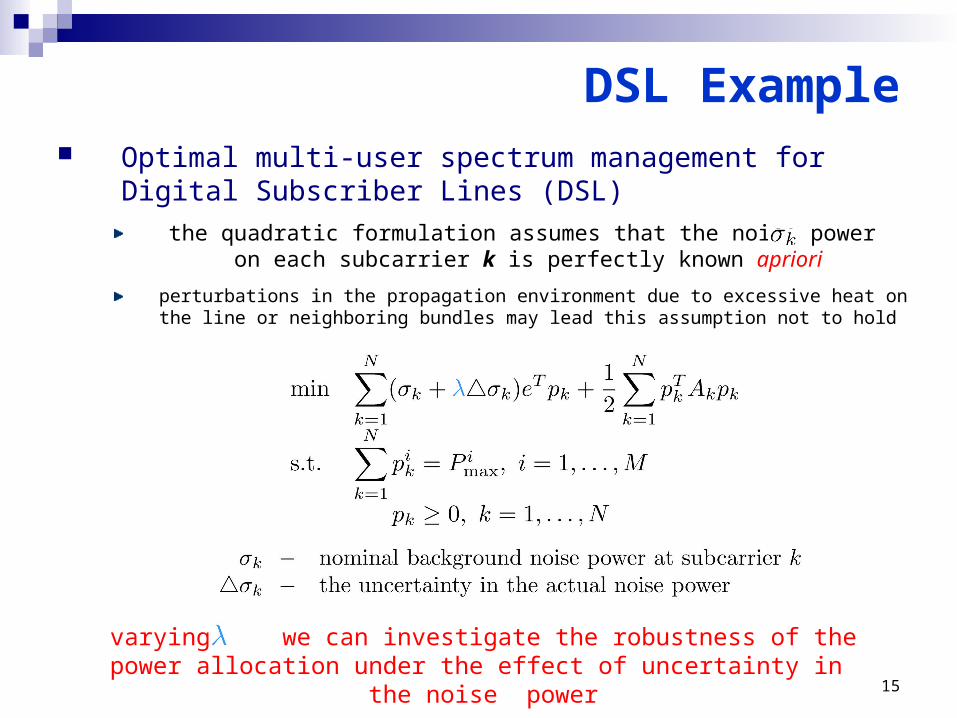

DSL Example Optimal multi-user spectrum management for Digital Subscriber

Lines (DSL)

M users are connected to one service provider via telephone line (DSL)

the total bandwidth of the channel is divided into N subcarriers (frequency tones) that are shared by all users

13

DSL Example

Optimal multi-user spectrum management for Digital Subscriber Lines (DSL)

Each user i tries to allocate his total transmission power to subcarriers to maximize his data transfer rate

14

Allocating each users' total transmission power among the subcarriers "intelligently" may result in higher overall data rates

DSL Example Optimal multi-user spectrum management for Digital Subscriber

Lines (DSL)

Current DSL systems use fixed power levels

Noncooperative game – each user behaves selfishly

Nash equilibrium points of the noncooperative rate maximization game correspond to optimal solutions of quadratic optim. problem

15

DSL Example Optimal multi-user spectrum management for Digital Subscriber

Lines (DSL)

the quadratic formulation assumes that the noise power on each subcarrier k is perfectly known apriori

varying we can investigate the robustness of the power allocation under the effect of uncertainty in the noise power

perturbations in the propagation environment due to excessive heat on the line or neighboring bundles may lead this assumption not to hold

16

DSL Example Optimal multi-user spectrum management for Digital Subscriber

Lines (DSL)

to mitigate the adverse effect of excess noise, the i-th user may decide to increase the transmitted power in steps of size

the parameter is now used to express the uncertainty in noise power as well as power increment to reduce the effect of noise

if the actual noise is lower than the nominal, the user may decide to decrease the transmitted power

17

Multiparametric Quadratic Optimization

18

Conclusions and Future Work

Background and applications of solving parametric convex QO problems

Simultaneous parameterization

Extending methodology to

• Multiparametric QO

• Parametric Second Order Conic Optimization (robust optimization, financial and engineering applications)

19

References A. Ghaffari Hadigheh, O. Romanko, and T. Terlaky. Sensitivity

Analysis in Convex Quadratic Optimization: Simultaneous Perturbation of the Objective and Right-Hand-Side Vectors. Submitted to Optimization, 2003.

A. B. Berkelaar, C. Roos, and T. Terlaky. The optimal set and optimal partition approach to linear and quadratic programming. In Advances in Sensitivity Analysis and Parametric Programming, T. Gal and H. J. Greenberg, eds., Kluwer, Boston, USA, 1997.

T. Luo. Optimal Multi-user Spectrum Management for Digital Subscriber Lines. Presentation at the ICCOPT conference, Troy, USA, 2004.

![A Bilevel Quadratic–Quadratic Fractional Programming ...quadratic fractional programming problem and later on Terlaky [33] also gives an algorithm to solve QFPP. Also Tantawy [32]](https://img.dokumen.tips/doc/110x75/605409ca9cf65110ff31261c/a-bilevel-quadraticaquadratic-fractional-programming-quadratic-fractional.jpg)

![Hazrat Abu Zar Ghaffari [R.a] by Maulana Manazir Ahsan Gillani](https://img.dokumen.tips/doc/110x75/55cf9a3c550346d033a0f208/hazrat-abu-zar-ghaffari-ra-by-maulana-manazir-ahsan-gillani.jpg)