Embed Size (px)

Citation preview

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 1/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 1

1.INTRODUCTION

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 2/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 2

RISK ANALYSIS

Risk is inherent in almost every business decision. More so in capital budgeting decisions as

they involve costs and benefits extending over a long period of time during which many

things can change in unanticipated ways.

For the sake of expository convenience, we assume that all investments considered for inclusion in the capital budget have the same risk as those of the existing investments of the

firm. Hence, average cost of Capital is used for evaluating the project. But, investment

proposals differ in risk. A research and development project may be more risky than an

expansion project and the latter tends to be more risky than a replacement project. In view of

such differences, variations in risk need to be considered explicitly in capital investment

appraisal.

Risk analysis is one of the mist complex and slippery aspects of capital budgeting. Many

different techniques have been suggested and no single technique can be deemed as best in all

situations. The variety of techniques suggested for handling risk in capital budgeting fall into

two broad categories:

i. Approaches that consider the standalone risk of a project.

ii. Approaches that consider the risk of a project in the context of the firm or in the

context of the market.

Risk analysis is a technique to identify and assess for mitigation of risks, at project initiation

and during task execution. It therefore attempts to identify any factors that can place a project

in jeopardy before and during the execution of the work, assigning ownership of each risk.

The advantage of this approach is that it is clear to all sides, vendor, contractors and

purchaser, what the risks are and who has ownership of each one. Also, it identifies risks

introduced into the project by all parties, whether they have a sustainable relationship with

the organization performing the work.

This approach to mitigating the risk factors also helps to define preventive measures to

reduce the probability of occurrence and identify methods to avert possible negative effects

on the effectiveness of the company to compete in this particular market.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 3/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 3

SOURCES OF RISK

There are several sources of risk in a project. Some of the risks are:

Project-specific risk

The earnings and cash flows of the project may be lower than expected because of estimationerror or some factors specific to the project like the quality of management.

Competitive risk

The earnings and cash flows of the project may be affected by unanticipated actions of

competitors.

Industry-specific risk

Unexpected technological developments and regulatory changes, that are specific to the

industry to which the project belongs will have an impact on the earnings and cash flows of

the project as well.

Market risk

Unanticipated changes in macroeconomic factors like the GDP growth rate, interst rate, and

inflation have an impact on all projects, albeit in varying degrees.

International risk

In the case of a foreign project, the earnings and cash flows may be different than expected

due to exchange rate risk or political risk.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 4/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 4

PERSPECTIVES ON RISK

Regardless of the risk measure employed, there are different perspectives on risk. The project

can be viewed from at least three different perspectives. These are:

Stand-alone risk

This represents the risk of a project when it is viewed in isolation.

Firm Risk

It is also called corporate risk. This represents the contribution of the project to risk of the

firm.

Market Risk

This represents the risk of a project from the point of view of a diversified investor. It is also

called systematic risk.

Since the primary goal of the firm is to maximise shareholder value, what matters finally is

the risk that a project imposes on shareholders. If shareholders are well diversified, market

risk is the most appropriate measure of risk.

In practice, however, the project¶s standalone risks as well as its corporate risks are

considered important.

The project¶s standalone risk is considered important for the following reasons.

y Measuring a project¶s stand-alone risk is easier than measuring its corporate risk and

far easier than measuring its market risk.

y In most of the cases, standalone risk, corporate risk, and market risk are highly

correlated. If the overall economy does well, the firm too would do well. Further, if

the firm does well, most of its projects would do well. Thanks to this high correlation,

standalone risk may be used as a proxy for corporate risk and market risk.

y The proponent of a capital investment is likely to be judged on the performance of

that investment. Hence he will naturally be concerned baout its stand-alone risk and

not about its contribution to the risk of the firm or the risk of a diversified investor.

y In most firms, the capital budgeting committee considers investment proposals one at

a time. The committee often does not have the time or information or expertise to

fully consider the interactions of the investments with the other investments of the

firm or its shareholders.

Corporate risk is considered important for the following reasons:

y Undiversified shareholders are more concerned about corporate risk than market risk.

Promoters who generally have a substantial equity stake tend to be undiversified or

poorly diversified shareholders.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 5/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 5

y Empirical studies suggest that both market risk and corporate risk have a bearing on

required returns. Perhaps even diversified investors consider corporate risk in addition

to market risk when they specify required returns.

y The stability of overall corporate cash flows and earnings is valued by managers,

workers, suppliers, creditors, customers and the community in which the firm

operates. If the cash flow and earnings of the firm are perceived to be highly volatileand risky, the firm will have difficulty in attracting talented employees, loyal

customers, reliable suppliers, and dependable lenders. This will impair its

performance and destroy shareholder wealth.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 6/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 6

2.FINANCIAL ANALYSIS

TECHNIQUES

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 7/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 7

FINANCIAL ANALYSIS TECHNIQUES

1. Simple Pay Back Period:

Simple Payback Period (SPP) represents, as a first approximation; the time (number of years)

required to recover the initial investment (First Cost), considering only the Net Annual

Saving:

The simple payback period is usually calculated as follows:

Simple payback Period = {First Cost / (Yearly Benefits ± Yearly Costs)}

Examples

Simple payback period for a continuous Deodorizer that costs Rs.60 lakhs to purchase and

install, Rs.1.5 lakhs per year on an average to operate and maintain and is expected to save

Rs. 20 lakhs by reducing steam consumption (as compared to batch deodorizers), may be

calculated as follows:

Simple Payback Period = {60 / (20 - 1.5)}

= 3 years 3 months

According to the payback criterion, the shorter the payback period, the more desirable is the

project.

Advantages

A widely used investment criterion, the payback period seems to offer the following

advantages:

y It is simple, both in concept and application. Obviously a shorter payback generallyindicates a more attractive investment. It does not use tedious calculations.

y It favours projects, which generate substantial cash inflows in earlier years, and

discriminates against projects, which bring substantial cash inflows in later years but

not in earlier years.

Limitations

y It fails to consider the time value of money. Cash inflows, in the payback

calculation, are simply added without suitable discounting. This violates the most

basic principle of financial analysis, which stipulates that cash flows occurring atdifferent points of time can be added or subtracted only after suitable

compounding/discounting.

y It ignores cash flows beyond the payback period. This leads to discrimination

against projects that generate substantial cash inflows in later years.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 8/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 8

To illustrate, consider the cash flows of two projects, A and B:

Investment Rs. (100,000) Rs.(100,000)

Savings in Year Cash Flow of A Cash flow of B

1 50,000 20,000

2 30,000 20,0003 20,000 20,000

4 10,000 40,000

5 10,000 50,000

6 - 60,000

The payback criterion prefers A, which has a payback period of 3 years, in comparison to B,

which has a payback period of 4 years, even though B has very substantial cash inflows in

years 5 and 6.

y It is a measure of a project¶s capital recovery, not profitability.

y Despite its limitations, the simple payback period has advantages in that it may be

useful for evaluating an investment.

Time Value of Money

A project usually entails an investment for the initial cost of installation, called the capital

cost, and a series of annual costs and/or cost savings (i.e. operating, energy, maintenance,

etc.) throughout the life of the project. To assess project feasibility, all these present and

future cash flows must be equated to a common basis. The problem with equating cash flows

which occur at different times is that the value of money changes with time. The method by

which these various cash flows are related is called discounting, or the present value

concept.

For example, if money can be deposited in the bank at 10% interest, then a Rs.100 deposit

will be worth Rs.110 in one year's time. Thus the Rs.110 in one year is a future value

equivalent to the Rs.100 present value.

In the same manner, Rs.100 received one year from now is only worth Rs.90.91 in today's

money (i.e. Rs.90.91 plus 10% interest equals Rs.100). Thus Rs.90.91 represents the present

value of Rs.100 cash flow occurring one year in the future. If the interest rate were something

different than 10%, then the equivalent present value would also change. The relationship between present and future value is determined as follows:

Future Value (FV) = NPV (1 + i)n

or NPV = FV / (1+i)n

Where

FV = Future value of the cash flow

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 9/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 9

NP V= N et P resent Value of the cash flow

i = Interest or discount rate

n = N umber of years in the future

2. Return on Investment (ROI)ROI expresses the "annual return" from the project as a percentage of capital cost. The annual

return takes into account the cash flows over the project life and the discount rate by

converting the total present value of ongoing cash flows to an equivalent annual amount over

the life of the project, which can then be compared to the capital cost. ROI does not require

similar project life or capital cost for comparison.

This is a broad indicator of the annual return expected from initial capital investment,

expressed as a percentage:

ROI = { (Annual Net Cash Flow / Capital Cost) x 100 }

ROI must always be higher than cost of money (interest rate); the greater the return on

investment better is the investment.

Limitations

y It does not take into account the time value of money.

y It does not account for the variable nature of annual net cash inflows.

3. Net Present Value

The net present value (NPV) of a project is equal to the sum of the present values of all the

cash flows associated with it. Symbolically,

Where NPV = Net Present Value

CFt= Cash flow occurring at the end of year µt¶ (t=0,1,«.n)

n = life of the project

= Discount rate

The discount rate () employed for evaluating the present value of the expected future cash

flows should reflect the risk of the project.

NPV = {(CF0

/ (1 + )0

) + ( CF1

/ (1 + )1

) + - - - + ( CFn

/ (1 + )n

)

Example

To illustrate the calculation of net present value, consider a project, which has the following

cash flow stream:

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 10/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 10

Investment Rs. (1,000,000)

Saving in Year Cash flow

1 200,000

2 200,000

3 300,000

4 300,000

5 350,000

The cost of capital, , for the firm is 10 per cent. The net present value of the proposal is:

NPV = {(1,000,000/(1.10)0

) + (200,000/(1.10)1

) + (200,000/(1.10)2

) + (300,000/(1.10)3

) +

(300,000/(1.10)4

) + (350,000/(1.10)5

)}

= (5,273)

The net present value represents the net benefit over and above the compensation for time and

risk.

Hence the decision rule associated with the net present value criterion is: ³Accept the project if

the net present value is positive and reject the project if the net present value is negative´.

Advantages

The net present value criterion has considerable merits.

y It takes into account the time value of money.

y It considers the cash flow stream in its project life.

4. Internal Rate of Return

This method calculates the rate of return that the investment is expected to yield. The internal rate

of return (IRR) method expresses each investment alternative in terms of a rate of return (a

compound interest rate). The expected rate of return is the interest rate for which total discounted

benefits become just equal to total discounted costs (i.e net present benefits or net annual benefits

are equal to zero, or for which the benefit / cost ratio equals one). The criterion for selection

among alternatives is to choose the investment with the highest rate of return.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 11/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 11

The rate of return is usually calculated by a process of trial and error, whereby the net cash

flow is computed for various discount rates until its value is reduced to zero.

The internal rate of return (IRR) of a project is the discount rate, which makes its net present

value (NPV) equal to zero. It is the discount rate in the equation:

NPV = {(CF0

/ (1 + )0

) + ( CF1

/ (1 + )1

) + - - - + ( CFn

/ (1 + )n

) = 0

Where, CFn= Cash flow at the end of year ³n´

= discount rate

n = life of the project.

CFtvalue will be negative if it is expenditure and positive if it is savings.

In the net present value calculation we assume that the discount rate (cost of capital) is known

and determine the net present value of the project. In the internal rate of return calculation,

we set the net present value equal to zero and determine the discount rate (internal rate of return), which satisfies this condition.

To illustrate the calculation of internal rate of return, consider the cash flows of a project:

Year 0 1 2 3 4

Cash Flow (100,000) 30,000 30,000 40,000 45,000

The internal rate of return is the value of ³ k ´ which satisfies the following equation:

The calculation of ³´ involves a process of trial and error. We try different values of ³´ till

we find that the right-hand side of the above equation is equal to 100,000. Let us, to begin

with, try = 15 per cent. This makes the right-hand side equal to:

{(30000/1.15) + (30000/(1.15)2

) + (40000/(1.15)3

) + (45000/(1.15)4

) + ----- + -----}

= 100, 802

This value is slightly higher than our target value, 100,000. So we increase the value of

from 15 per cent to 16 per cent. (In general, a higher lowers and a smaller r increases the

right-hand side value). The right-hand side becomes:

{(30000/1.16) + (30000/(1.16)

2

) + (40000/(1.16)

3

) + (45000/(1.16)

4

) + ----- + -----

= 98,641

Since this value is now less than 100,000, we conclude that the value of k lies between 15 per

cent and 16 per cent. For most of the purposes this indication suffices.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 12/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 12

Advantages

A popular discounted cash flow method, the internal rate of return criterion has several

advantages:

y It takes into account the time value of money.

y It considers the cash flow stream in its entirety.

y It makes sense to businessmen who prefer to think in terms of rate of return and find

an absolute quantity, like net present value, somewhat difficult to work with.

Limitations

y The internal rate of return figure cannot distinguish between lending and borrowing

and hence a high internal rate of return need not necessarily be a desirable feature.

Example

Calculate the internal rate of return for an economizer that will cost Rs. 500,000 will last 10

years, and will result in fuel savings of Rs. 150,000 each year.

Find the i that will equate the following:

Rs. 500,000 = 150,000 x PV (A = 10 years, i = ?)

To do this, calculate the net present value (NPV) for various i values, selected by visual

inspection;

NPV 25% = Rs. 150,000 x 3.571 ± Rs. 500,000

Rs. 35,650

NPV 30% = Rs. 150,000 x 3.092 ± Rs. 500,000

= -Rs. 36,200

For,

i = 25 per cent, net present value is positive;

i = 30 per cent, net present value is negative.

Thus, for some discount rate between 25 and 30 per cent, present value benefits are equated

to present value costs. To find the rate more exactly, one can interpolate between the tworates as follows:

i = 0.25 + (0.30-0.25) x 35650 / (35650 + 36200)

= 0.275 or 27.5 percent

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 13/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 13

Cash Flows

Generally there are two kinds of cash flow; the initial investment as one or more instalments,

and the savings arising from the investment. This over simplifies the reality of energy

management investment.

There are usually other cash flows related to a project. These include the following:

y Capital costs are the costs associated with the design, planning, installation and

commissioning of the project; these are usually one-time costs unaffected by inflation

or discount rate factors, although, as in the example, instalments paid over a period of

time will have time costs associated with them.

y Annual cash flows, such as annual savings accruing from a project, occur each year

over the life of the project; these include taxes, insurance, equipment leases, energy

costs, servicing, maintenance, operating labour, and so on. Increases in any of these

costs represent negative cash flows, whereas decreases in the cost represent positive

cash flows.

Factors that need to be considered in calculating annual cash flows are:

y Taxes, using the marginal tax rate applied to positive (i.e. increasing taxes) or

negative (i.e. decreasing taxes) cash flows.

y Asset depreciation, the depreciation of plant assets over their life; depreciation is a

³paper expense allocation´ rather than a real cash flow, and therefore is not included

directly in the life cycle cost. However, depreciation is ³real expense´ in terms of tax

calculations, and therefore does have an impact on the tax calculation noted above.

For example, if a Rs.10,00,000 asset is depreciated at 20% and the marginal tax rate

is 40%, the depreciation would be Rs.200,000 and the tax cash flow would be

Rs.80,000 and it is this later amount that would show up in the costing calculation.

y Intermittent cash flows occur sporadically rather than annually during the life of the

project, relining a boiler once every five years would be an example.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 14/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 14

3.TECHNIQUES

FOR RISK ANALYSIS

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 15/42

APPL AT E T T ANAL N CAPITAL B ETING

A.I.M.S. 15

TECHNIQUES FOR RISK ANAL SIS

Techni esof Risk

Anal sis

Anal sis of Standalone

R sik

Sensiti ityAnalysis

Scenar ioAnalysis

Analysis of Contexual

r isk

Corporate

Risk Analysis

Market Risk

Analysis

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 16/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 16

SENSITIVITY AND RISK ANALYSIS

Many of the cash flows in the project are based on assumptions that have an element of

uncertainty. The present day cash flows, such as capital cost, energy cost savings,

maintenance costs, etc. can usually be estimated fairly accurately. Even though these costs

can be predicted with some certainty, it should always be remembered that they are onlyestimates. Cash flows in future years normally contain inflation components which are often

"guess-timates" at best. The project life itself is an estimate that can vary significantly.

Sensitivity analysis is an assessment of risk. Because of the uncertainty in assigning values to

the analysis, it is recommended that a sensitivity analysis be carried out - particularly on

projects where the feasibility is marginal. How sensitive is the project's feasibility to changes

in the input parameters? What if one or more of the factors in the analysis is not as favourable

as predicted? How much would it have to vary before the project becomes unviable? What is

the probability of this happening?

Suppose, for example, that a feasible project is based on an energy cost saving that escalates

at 10% per year, but a sensitivity analysis shows the break-even is at 9% (i.e. the project

becomes unviable if the inflation of energy cost falls below 9%). There is a high degree of

risk associated with this project - much greater than if the break-even value was at 2%.

Many of the computer spreadsheet programs have built-in "what if" functions that make

sensitivity analysis easy. If carried out manually, the sensitivity analysis can become

laborious - reworking the analysis many times with various changes in the parameters.

Sensitivity analysis is undertaken to identify those parameters that are both uncertain and for

which the project decision, taken through the NPV or IRR, is sensitive. Switching values

showing the change in a variable required for the project decision to change from acceptance

to rejection are presented for key variables and can be compared with post evaluation results

for similar projects. For large projects and those close to the cut-off rate, a quantitative risk analysis incorporating different ranges for key variables and the likelihood of their occurring

simultaneously is recommended. Sensitivity and risk analysis should lead to improved project

design, with actions mitigating against major sources of uncertainty being outlined

The various micro and macro factors that are considered for the sensitivity analysis are listed

below.

Micro factors

y Operating expenses (various expenses items)

y Capital structurey Costs of debt, equity

y Changing of the forms of finance e.g. leasing

y Changing the project duration

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 17/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 17

Macro factors

Macro economic variables are the variable that affects the operation of the industry of which

the firm operates. They cannot be changed by the firm¶s management.

Macro economic variables, which affect projects, include among others:y Changes in interest rates

y Changes in the tax rates

y Changes in the accounting standards e.g. methods of calculating depreciation

y Changes in depreciation rates

y Extension of various government subsidized projects e.g. rural electrification

y General employment trends e.g. if the government changes the salary scales

y Imposition of regulations on environmental and safety issues in the industry

y Energy Price change

y Technology changes

The sensitivity analysis will bring changes in various items in the analysis of financial

statements or the projects, which in turn might lead to different conclusions regarding the

implementation of projects.

Evaluation

A very popular method for assessing risk, sensitivity analysis has certain merits:

y It shows how robust or vulnerable a project is to changes in values of the underlying

variables.

y It indicates where further work may be done. If the net present value is highly

sensitive to changes in some factor, it may be worthwhile to explore how the

variability of that critical factor may be contained.

y It is intuitively very appealing as it articulates the concerns that project evaluators

normally have.

Notwithstanding its appeal and popularity, sensitivity analysis suffers from several

shortcomings:

y It merely shows what happens to NPV when there is a change in some variable,

without providing any idea of how likely that change will be.

y Typically, in sensitivity analysis only one variable is changed at a time. In the real

world, however, variables tend to move together.

y It is inherently a very subjective analysis. The same sensitivity analysis may lead one

decision maker to accept the project while another may reject it.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 18/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 18

SCENARIO ANALYSIS

Scenario analysis is a process of analysing possible future events by considering alternative

possible outcomes (scenarios). The analysis is designed to allow improved decision-making

by allowing more complete consideration of outcomes and their implications.

For example, in economics and finance, a financial institution might attempt to forecast

several possible scenarios for the economy (e.g. rapid growth, moderate growth, slow

growth) and it might also attempt to forecast financial market returns (for bonds, stocks and

cash) in each of those scenarios. It might consider sub-sets of each of the possibilities. It

might further seek to assign probabilities to the scenarios (and sub-sets if any). Then it will be

in a position to consider how to distribute assets between asset types (i.e. asset allocation );

the institution can also calculate the scenario-weighted expected return (which figure will

indicate the overall attractiveness of the financial environment).

Depending on the complexity of the financial environment, in economics and finance

scenario analysis can be a demanding exercise. It can be difficult to foresee what the futureholds (e.g. the actual future outcome may be entirely unexpected), i.e. to foresee what the

scenarios are, and to assign probabilities to them; and this is true of the general forecasts

never mind the implied financial market returns. The outcomes can be modelled

mathematically/statistically e.g. taking account of possible variability within single scenarios

as well as possible relationships between scenarios.

Financial institutions can take the analysis further by relating the asset allocation that the

above calculations suggest to the industry or peer group disposition of assets. In so doing the

financial institution seeks to control its business risk rather than the client's portfolio risk.

Procedure

The steps involved in scenario analysis are as follows:

a. Select the factors around which the scenarios will be built. The factor chosen must be

the largest source of uncertainty for the success of the project. It may be the state of

the economy or interest rate or technological development or response of the market.

b. Estimate the values of each of the variables in investment analysis (investment outlay,

revenues, costs, project life, and so on) for each scenario.

c. Calculate the next present value and / or internal rate of return under each scenario.

Best and Worst Case Analysis

Firms often do a kind of scenario analysis called the best case and worst case analysis. In this

kind of analysis the following scenarios are considered:

Best Scenario: High Demand, high selling price, low variable cost, and so on.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 19/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 19

Normal Scenario: Average demand, average selling price, high variable cost, and so on.

Worst Scenario: Low demand, low selling price, high variable cost, and so on.

The objective of such a scenario analysis is to get a feel of what happens under the most

favourable or the most adverse configuration of key variables, without bothering much about

the internal consistency of such configurations.

Evaluation

Scenario Analysis may be considered as an improvement over Sensitivity Analysis because it

considers variations in several variables together.

However, Scenario analysis has its own limitations:

y It is based on the assumption that there are few well- delineated scenarios. This may

not be true in many cases. For example, the economy does not necessarily lie in threediscrete states, viz. recession, stability, and boom. It can in fact be anywhere on the

continuum between the extremes. When a continuum is converted into three discrete

states some information is lost.

y Scenario analysis expands the concept of estimating the expected values. Thus in a

case where there are 10 inputs, the analyst has to estimate 30 expected values (3 x 10)

to do the scenario analysis.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 20/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 20

RISK ANALYSIS IN PRACTICE

Several methods to incorporate the risk factor into capital expenditure analysis are used in

practice. The most common ones are:

Conservative Estimation of Revenues

In many cases the revenues expected from a project are conservatively estimated to ensure

that the viability of the projects is not easily threatened by unfavourable circumstances. The

capital budgeting systems often have built-in devices for conservative estimation. This is

indicated by the following remarks made by two executives:

³We ask the project sponsor to estimate revenues conservatively. This checks the optimism

common among project sponsors.´

³The Capital budgeting committee requires justification for revenue figures given by those

who propose capital expenditures. This has a sobering effect on them.´

Safety Margin in Cost Figures

A margin of safety is generally included in estimating cost figures. This varies between 10

percent and 30 percent of what is deemed as normal cost. The size of the margin depends on

what management feels about the likely variation in cost. The following observation suggests

this:

³In estimating the cost of raw material we add about 20 to 25 percent to the current prices as

the raw material price is not stable and often we pay a high price to get it. For labour cost we

add about 10 to 12 percent as this is the annual increase.´

Flexible Investment Yardsticks

The cut-off point on an investment varies according to the judgement of management about

the riskiness of the project. In one company replacement investments are okayed if the

expected post-tax return exceeds 15 percent but new investments are undertaken only if the

expected post-tax return is greater than 20 percent. Another company employs a short

payback period of three year for new investments. Its decision rule was stated by its financial

controller as follows:

³Our policy is to accept a new project only if it has a payback period of three years. We have

never, as far as I know, deviated from this. The use of short payback period automatically

weeds out risky projects.´

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 21/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 21

Sensitivity Analysis

It is a common practice to judge how robust or vulnerable a project is to adverse variations in

the values of the underlying variables like selling price, raw material cost, and quantity sold.

As a manager puts it as:

³We examine the impact of 5 percent and 10 percent adverse variation in selling price, raw

material cost, and quantity sold on NPV and IRR.´

Scenario Analysis

Companies often look at a few scenarios and the top management or the board of directors

decides on the basis of such information. Two examples are given below:

In a pharmaceutical company sponsors are required to give three estimates of rate of return:

most pessimistic, most likely and most optimistic.

In a shipping company three estimates, labelled high, medium, and low are developed for

proposed investments.

Relative Importance of Various Methods of Assessing Project Risk:

% of companies rating it as very

important or important

y Sensitivity Analysis 90.10

y Scenario Analysis 61.60

y Risk-adjusted Discount rate 31.70

y Decision Tree Analysis 12.20

y Monte Carlo Simulation 8.20

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 22/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 22

4. APPLICATION OF

SENSITIVITY ANALYSIS

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 23/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 23

APPLICATION OF SENSITIVITY ANALYSIS

Consider a company X Ltd. manufacturing dry batteries. A manufacturing unit is set up by X

Ltd. for this purpose. Income to the unit is majorly by the means of the Sales done by the unit

and some minor other income such as interest on Advance tax and other miscellaneous

income. The Expenses include Raw Materials Cost, Power and Fuel Cost, Employee Cost,Other Manufacturing Expenses, Selling and Admin Expenses and Other Miscellaneous

Expenses.

A Sensitivity analysis is done so as to study the major expenses related to the production of

the batteries. Also the Net Present Value of the unit at different discount rates is to be

calculated and its relation to the major expenses and its effects on the cash flow are to be

determined. A Tornado Diagram is to be developed so as to facilitate decision making related

to the major expenses of the production unit.

The Income and Expenses of Year 0 i.e. the present year is as follows:

Year 0

(Rs. Lakhs)

Income

Net Sales 857.33

Other Income 2.05

Total Income 859.38

ExpensesRaw Materials 517.34

Power & Fuel Cost 12.36

Employee Cost 79.11

Other ManufacturingExpenses

9.24

Selling and Admin Expenses 110.62

Miscellaneous Expenses 14.92

Total Expenses 743.59

The Cash Flow of the unit needs to be calculated. We consider only the income from theSales as the Income from the Unit. Therefore, the Cash Flow is calculated as:

Cash Flow of the Unit = Income ± Expenses

= Net Sales ± Total Expenses

= 857.33 ± 743.59

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 24/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 24

= Rs. 113.74 lakhs

Thus, the Cash flow from the Operations of the Unit, which is considered as the only cash

flow to the unit, is Rs. 113.74 lakhs.

Now, we will forecast the Income and Expenses of the Unit for next 3 years on a year-on-

year basis. That is, for each of the 3 years separately.

For Forecasting purpose, we have assumed all the other income and the expenses are

considered to be as a percentage of the Sales achieved each year.

Year 0(Rs. Lakhs)

% of Sales

Income Net Sales 857.33

Other Income 2.05 0.24%

Total Income 859.38

Expenses

Raw Materials 517.34 60.34%

Power & Fuel Cost 12.36 1.44%

Employee Cost 79.11 9.23%

Other Manufacturing

Expenses 9.24 1.08%

Selling and Admin Expenses 110.62 12.90%

Miscellaneous Expenses 14.92 1.74%

Total Expenses 743.59

Thus, we observe that the major portion of the Sales value is from the Raw Materials Cost,

Employee Cost and Selling and Admin Expenses.

We expect the Sales to increase 20% each year. Therefore, Net Sales for Year 1 would becalculated as:

Net Sales (Year 1) = Net Sales (Year 0) + 0.20 x Net Sales (Year 0)

= 857.33 + 0.20 x 857.33

= 1028.796

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 25/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 25

Thus, Net Sales for Year 1 is Rs. 1028.796 lakhs.

We now forecast the Income and the Expenses of the unit.

The Cash flow from the Year 0 is added as an income in Year 1. But, the Cash flow from

Year 0 does not play any part in the calculation of the Cash flow in Year1. All the other

values are calculated as percentage of Sales as derived in the earlier table.

% of Sales

Year 1

(Expected)

(Rs. Lakhs)

Income

Net Sales 1028.796

Other Income 0.24% 2.46Cash Flow from Previous

Year 113.74

Total Income 1031.256

Expenses

Raw Materials 60.34% 620.808

Power & Fuel Cost 1.44% 14.832

Employee Cost 9.23% 94.932

Other ManufacturingExpenses

1.08% 11.088

Selling and Admin Expenses 12.90% 132.744Miscellaneous Expenses 1.74% 17.904

Total Expenses 892.308

A Sensitivity Analysis of the projected income and expenses is to be done. So we consider a

Pessimist and an Optimist opinion to the Expected values of the Income and Expenses for

Year 1.

For doing this, we consider the Pessimist view to be 95% and Optimist view to be 105% of

the Expected Values of the Income and 105% for the Pessimist and 95% for the Optimist of

the Expected Values of the Expenses. Thus a 5% change in the Expected values will give us

the Pessimistic and Optimistic Values.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 26/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 26

Year 1

Pessimistic Expected Optimistic

Income

Net Sales 977.3562 1028.796 1080.236Other Income 2.337 2.46 2.583

Cash Flow from Previous

Year 108.053 113.74 119.427

Total Income 979.6932 1031.256 1082.819

Expenses

Raw Materials 651.8484 620.808 589.7676

Power & Fuel Cost 15.5736 14.832 14.0904

Employee Cost 99.6786 94.932 90.1854

Other Manufacturing

Expenses11.6424 11.088 10.5336

Selling and Admin Expenses 139.3812 132.744 126.1068

Miscellaneous Expenses 18.7992 17.904 17.0088

Total Expenses 936.9234 892.308 847.6926

The Cash Flow from the Unit for Year 1 is calculated as:

Cash Flow of the Unit = Income ± Expenses

= Net Sales ± Total Expenses

= 1028.796 ± 892.308

= Rs. 136.488 lakhs

Thus, the Cash flow of the Unit for Year 1 would be Rs. 136.488 lakhs.

Now, the Present Value of the Cash Flow of Year 1 at the discount rate 10 % would be:

PV of Cash flow of Year 1 = 136.488 / (1+0.10)

= Rs. 124.08 lakhs

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 27/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 27

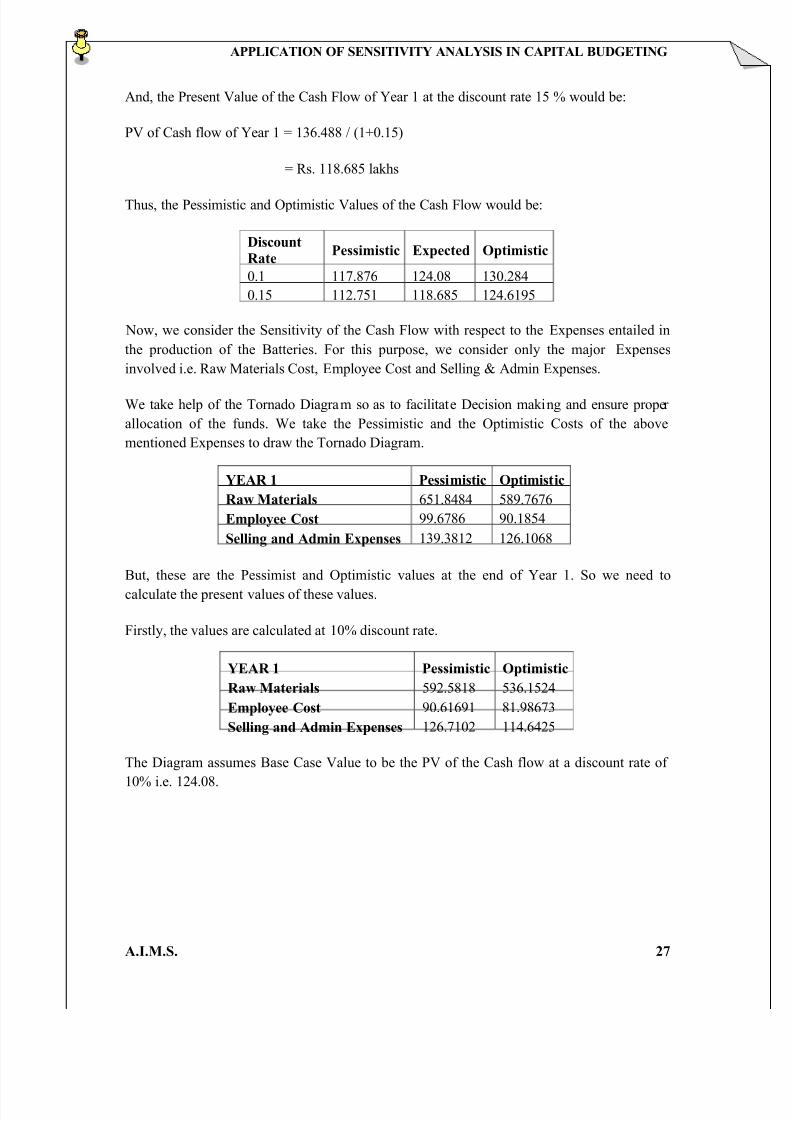

And, the Present Value of the Cash Flow of Year 1 at the discount rate 15 % would be:

PV of Cash flow of Year 1 = 136.488 / (1+0.15)

= Rs. 118.685 lakhs

Thus, the Pessimistic and Optimistic Values of the Cash Flow would be:

Discount

RatePessimistic Expected Optimistic

0.1 117.876 124.08 130.284

0.15 112.751 118.685 124.6195

Now, we consider the Sensitivity of the Cash Flow with respect to the Expenses entailed in

the production of the Batteries. For this purpose, we consider only the major Expenses

involved i.e. Raw Materials Cost, Employee Cost and Selling & Admin Expenses.

We take help of the Tornado Diagram so as to facilitate Decision making and ensure proper

allocation of the funds. We take the Pessimistic and the Optimistic Costs of the above

mentioned Expenses to draw the Tornado Diagram.

YEAR 1 Pessimistic Optimistic

Raw Materials 651.8484 589.7676

Employee Cost 99.6786 90.1854

Selling and Admin Expenses 139.3812 126.1068

But, these are the Pessimist and Optimistic values at the end of Year 1. So we need to

calculate the present values of these values.

Firstly, the values are calculated at 10% discount rate.

YEAR 1 Pessimistic Optimistic

Raw Materials 592.5818 536.1524

Employee Cost 90.61691 81.98673

Selling and Admin Expenses 126.7102 114.6425

The Diagram assumes Base Case Value to be the PV of the Cash flow at a discount rate of

10% i.e. 124.08.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 28/42

APPLICATION OF SENSITIVIT ANAL SIS IN CAPITAL BUDGETING

A.I.M.S. 28

Here, the Pessi istic View suggests more expenses whereas the Optimistic view suggests

fewer expenses.

And now, we calculate the values at 15% discount rate.

YEAR 1 Pessi isti Opti isti

Raw Materials 566.81739 512.84139

E pl ee Cost 86.677043 78.422087

Selli and Admin

E penses

121.20104 109.65809

And, we assume Base Case Value to be the PV of the Cash f low at a discount rate of 15% i.e.

118.685.

0 100 200 300 400 500 600 700

R aw Mater ials

mployee Cost

Selling and Admin¡

xpenses

Pessimistic

Optimistic

0 100 200 300 400 500 600

R aw Mater ials

¡

mployee Cost

Selling and Admin¡

xpenses

Pessimistic

Optimistic

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 29/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 29

Now, we need to analyse the 2 Tornado Diagrams so as to make decisions regarding the

expenses and find the better option amongst the 2 present values of the cash flow available.

We thus observe that the Raw materials Cost is almost similar in both the cases. But the

Pessimistic Cost i.e. more Expenses is more significant in both the cases. This is in line with

the market conditions generally where the raw materials costs grow. The Employee Cost in both the diagrams shows significance of the Optimistic view i.e. less expenses. So we can say

that the Employee Cost is manageable and may be according to our predictions for the 1st

year. The Selling and Admin Expenses show dominance of the optimistic view i.e. less

expenses. But, in the 2nd

diagram where we take the discount rate as 15%, the pessimistic cost

just comes into picture above the base value i.e. the cash flow value.

So, overall we can predict that if we look for the Raw Materials Cost, Employee Cost as well

as Selling and Admin Expenses then the 10% discounting factor is more suitable as it

provides more cash flow which is beneficial for the organisation.

Now, we move on to forecast for the Cash Flow of Year 2.

Again, we expect the Sales to increase 20% for Year 2. Therefore, Net Sales for Year 2

would be calculated as:

Net Sales (Year 2) = Net Sales (Year 1) + 0.20 x Net Sales (Year 1)

= 1028.796 + 0.20 x 1028.796

= 1234.55

Thus, Net Sales for Year 2 is Rs. 1234.55 lakhs.

We now forecast the Income and the Expenses of the unit for year 2 by using % of Sales

method as done earlier. Again the Cash Flow from the previous year is added to the Income

but, it does not play any part in the calculation of the Cash flow for Year 2.

% of SalesYear 2(Expected)

(Rs. Lakhs)

Income

Net Sales 1234.555

Other Income 0.24% 2.952

Cash Flow from Previous

Year 136.488

Total Income 1373.995

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 30/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 30

Expenses

Raw Materials 60.34% 744.9696

Power & Fuel Cost 1.44% 17.7984

Employee Cost 9.23% 113.9184

Other ManufacturingExpenses 1.08% 13.3056

Selling and Admin Expenses 12.90% 159.2928

Miscellaneous Expenses 1.74% 21.4848

Total Expenses 1070.77

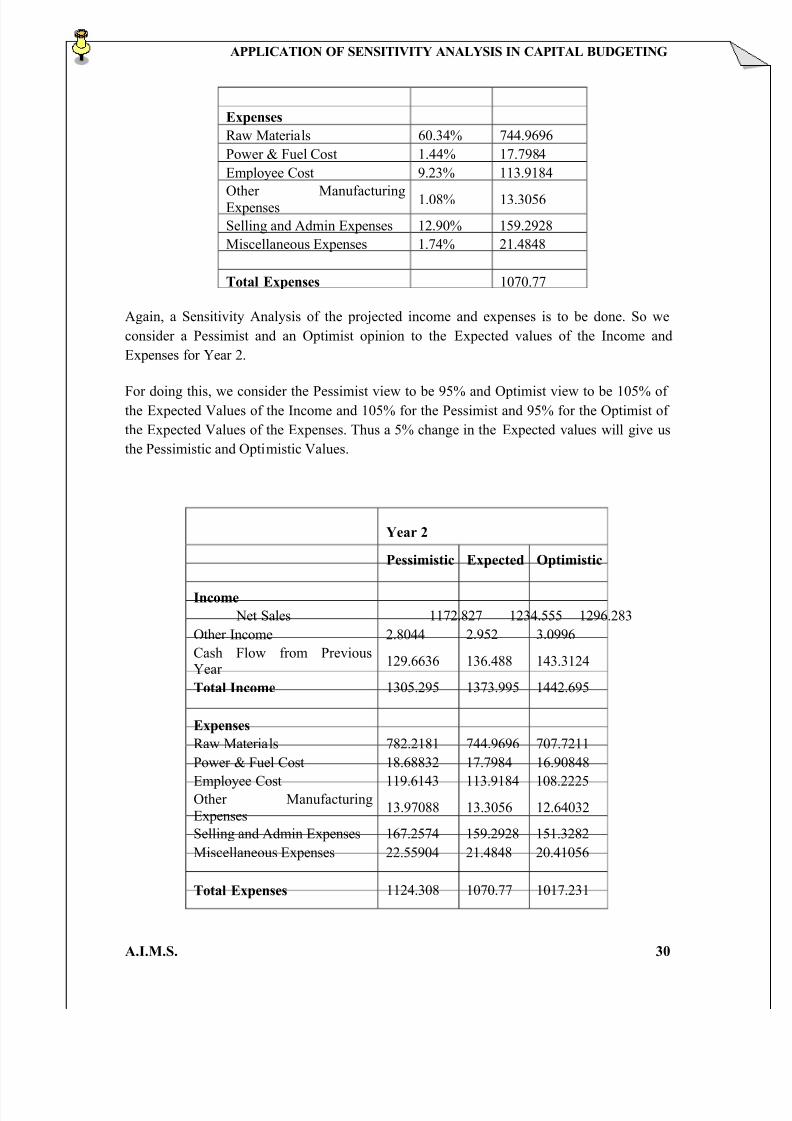

Again, a Sensitivity Analysis of the projected income and expenses is to be done. So we

consider a Pessimist and an Optimist opinion to the Expected values of the Income and

Expenses for Year 2.

For doing this, we consider the Pessimist view to be 95% and Optimist view to be 105% of the Expected Values of the Income and 105% for the Pessimist and 95% for the Optimist of

the Expected Values of the Expenses. Thus a 5% change in the Expected values will give us

the Pessimistic and Optimistic Values.

Year 2

Pessimistic Expected Optimistic

Income

Net Sales 1172.827 1234.555 1296.283

Other Income 2.8044 2.952 3.0996

Cash Flow from PreviousYear

129.6636 136.488 143.3124

Total Income 1305.295 1373.995 1442.695

Expenses

Raw Materials 782.2181 744.9696 707.7211

Power & Fuel Cost 18.68832 17.7984 16.90848

Employee Cost 119.6143 113.9184 108.2225Other Manufacturing

Expenses13.97088 13.3056 12.64032

Selling and Admin Expenses 167.2574 159.2928 151.3282

Miscellaneous Expenses 22.55904 21.4848 20.41056

Total Expenses 1124.308 1070.77 1017.231

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 31/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 31

The Cash Flow from the Unit for Year 2 is calculated as:

Cash Flow of the Unit = Income ± Expenses

= Net Sales ± Total Expenses

= 1234.55 ± 1070.77

= Rs. 163.78 lakhs

Thus, the Cash flow of the Unit for Year 2 would be Rs. 163.78 lakhs.

Now, the Present Value of the Cash Flow of Year 2 at the discount rate 10 % would be:

PV of Cash flow of Year 2 = 163.78 / (1+0.10)

= Rs. 135.36 lakhs

And, the Present Value of the Cash Flow of Year 2 at the discount rate 15 % would be:

PV of Cash flow of Year 2 = 163.78 / (1+0.15)

= Rs. 123.845 lakhs

Thus, the Pessimistic and Optimistic Values of the Cash Flow would be:

Discount

Rate

Pessimistic Expected Optimistic

0.1 128.592 135.36 142.128

0.15 117.653 123.845 130.037

Again, we consider the Sensitivity of the Cash Flow with respect to the Expenses entailed in

the production of the Batteries. For this purpose, we consider only the major Expenses

involved i.e. Raw Materials Cost, Employee Cost and Selling & Admin Expenses.

We take help of the Tornado Diagram so as to facilitate Decision making and ensure proper

allocation of the funds. We take the Pessimistic and the Optimistic Costs of the above

mentioned Expenses to draw the Tornado Diagram.

YEAR 2 Pessimistic Optimistic

Raw Materials 782.218 707.721

Employee Cost 119.614 108.222

Selling and Admin Expenses 167.257 151.328

But, these are the Pessimist and Optimistic values at the end of Year 2. So we need to

calculate the present values of these values.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 32/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 32

Firstly, the values are calculated at 10% discount rate.

YEAR 2 Pessimisti Optimisti

Raw Materials 646.461 584.893

Employee Cost 98.854 89.439

Selling and Admin E penses 138.228 125.064

The Diagram assumes Base Case Value to be the PV of the Cash f low at a discount rate of

10% i.e. 135.36.

And now, we calculate the values at 15% discount rate.

YEAR 2 Pessimisti Optimisti

Raw Materials 591.469 535.138

Employee Cost 90.445 81.831

Selling and Admin

E penses126.47 114.425

And now, we assume Base Case Value to be the PV of the Cash f low at a discount rate of

15% i.e. 123.845.

0 100 200 300 400 500 600 700

R aw Mater ials

¢

mployee Cost

Selling and Admin£

xpenses

Pessimistic

Optimistic

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 33/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 33

Now, we analyse the 2 Tornado Diagrams so as to make decisions regarding the expenses and

f ind the better option amongst the 2 present values of the cash f low available for Year 2.

We observe that the raw mater ials Cost, the mployee Cost as well as Selling and Admin

xpenses show similar trends at the 10% and 15% discount rates.The R aw mater ials cost

shows dominance of the pessimistic view i.e. more expenses whereas the mployee cost and

Selling and Admin xpenses shows dominance of Optimistic view i.e. less expenses.

So we can conclude that we can take any of the discount rates but the 10% discount rate isa

better option as it provides more cash f low in Year 2.

Now, we move on to forecast for the Cash Flow of Year 3.

Again, we expect the Sales to increase 20% for Year 3. Therefore, Net Sales for Year 3

would be calculated as:

Net Sales (Year 3) = Net Sales (Year 2) + 0.20 x Net Sales (Year 2)

= 1234.55 + 0.20 x 1234.55

= 1481.466

Thus, Net Sales for Year 3 is R s. 1481.466 lakhs.

0 100 200 300 400 500 600 700

R aw Mater ials

¤

mployee Cost

Selling and Admin¥

xpenses

Pessimistic

Optimistic

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 34/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 34

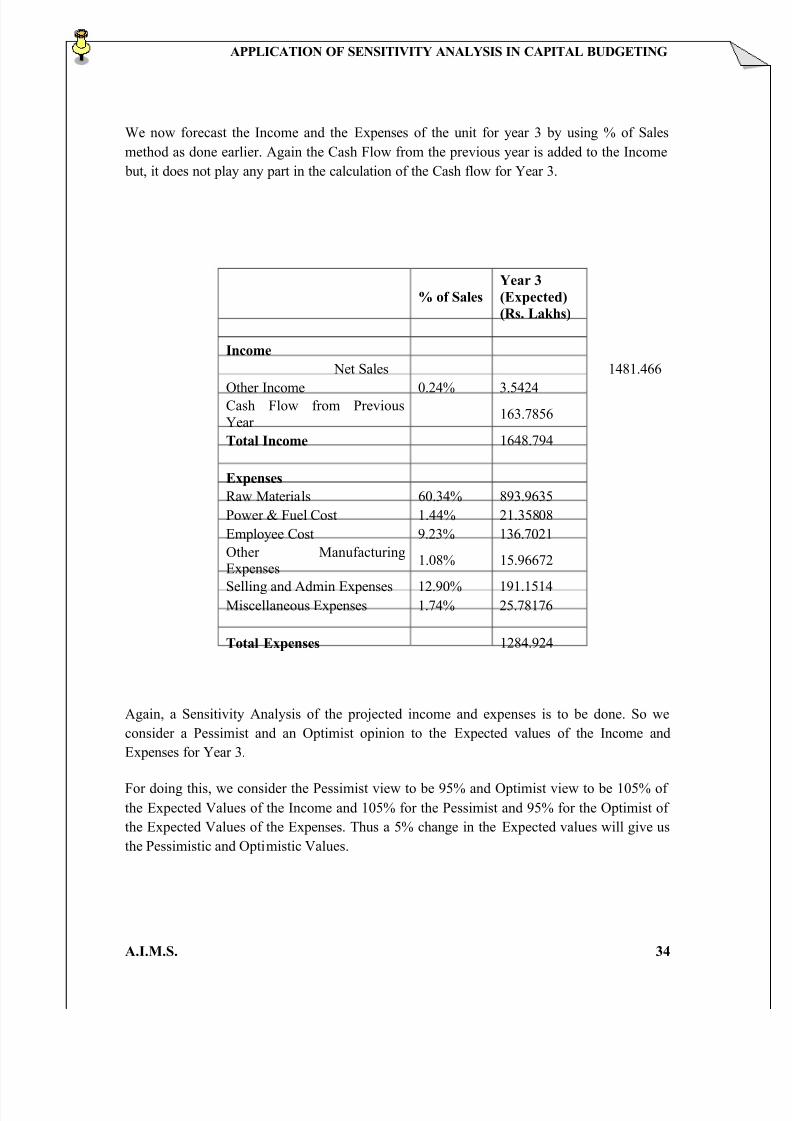

We now forecast the Income and the Expenses of the unit for year 3 by using % of Sales

method as done earlier. Again the Cash Flow from the previous year is added to the Income

but, it does not play any part in the calculation of the Cash flow for Year 3.

% of Sales

Year 3

(Expected)

(Rs. Lakhs)

Income

Net Sales 1481.466

Other Income 0.24% 3.5424Cash Flow from Previous

Year 163.7856

Total Income 1648.794

Expenses

Raw Materials 60.34% 893.9635

Power & Fuel Cost 1.44% 21.35808

Employee Cost 9.23% 136.7021

Other ManufacturingExpenses

1.08% 15.96672

Selling and Admin Expenses 12.90% 191.1514Miscellaneous Expenses 1.74% 25.78176

Total Expenses 1284.924

Again, a Sensitivity Analysis of the projected income and expenses is to be done. So we

consider a Pessimist and an Optimist opinion to the Expected values of the Income and

Expenses for Year 3.

For doing this, we consider the Pessimist view to be 95% and Optimist view to be 105% of

the Expected Values of the Income and 105% for the Pessimist and 95% for the Optimist of

the Expected Values of the Expenses. Thus a 5% change in the Expected values will give us

the Pessimistic and Optimistic Values.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 35/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 35

Year 3

Pessimistic Expected Optimistic

Income

Net Sales 1407.393 1481.466 1555.54Other Income 3.36528 3.5424 3.71952

Cash Flow from Previous

Year 155.5963 163.7856 171.9749

Total Income 1566.355 1648.794 1731.234

Expenses

Raw Materials 938.6617 893.9635 849.2653

Power & Fuel Cost 22.42598 21.35808 20.29018

Employee Cost 143.5372 136.7021 129.867

Other Manufacturing

Expenses16.76506 15.96672 15.16838

Selling and Admin Expenses 200.7089 191.1514 181.5938

Miscellaneous Expenses 27.07085 25.78176 24.49267

Total Expenses 1349.17 1284.924 1220.677

The Cash Flow from the Unit for Year 3 is calculated as:

Cash Flow of the Unit = Income ± Expenses

= Net Sales ± Total Expenses

= 1481.466 ± 1284.924

= Rs. 196.542 lakhs

Thus, the Cash flow of the Unit for Year 3 would be Rs. 196.542 lakhs.

Now, the Present Value of the Cash Flow of Year 3 at the discount rate 10 % would be:

PV of Cash flow of Year 3 = 196.542 / (1+0.10)

= Rs. 147.655 lakhs

And, the Present Value of the Cash Flow of Year 3 at the discount rate 15 % would be:

PV of Cash flow of Year 3 = 196.542 / (1+0.15)

= Rs. 129.23 lakhs

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 36/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 36

Thus, the Pessimistic and Optimistic Values of the Cash Flow would be:

Discount

RatePessimistic Expected Optimistic

0.1 140.282 147.665 155.048

0.15 122.768 129.23 135.691

Again, we consider the Sensitivity of the Cash Flow with respect to the Expenses entailed in

the production of the Batteries. For this purpose, we consider only the major Expenses

involved i.e. Raw Materials Cost, Employee Cost and Selling & Admin Expenses.

We take help of the Tornado Diagram so as to facilitate Decision making and ensure proper

allocation of the funds. We take the Pessimistic and the Optimistic Costs of the above

mentioned Expenses to draw the Tornado Diagram.

YEAR 3 Pessimistic Optimistic

Raw Materials 938.661 849.265Employee Cost 143.537 129.866

Selling and Admin Expenses 200.708 181.593

But, these are the Pessimist and Optimistic values at the end of Year 3. So we need to

calculate the present values of these values.

Firstly, the values are calculated at 10% discount rate.

YEAR 3 Pessimistic Optimistic

Raw Materials 705.2299 638.0654

Employee Cost 107.8415 97.57025

Selling and Admin Expenses 150.7949 136.4335

The Diagram assumes Base Case Value to be the PV of the Cash flow at a discount rate of

10% i.e. 147.665.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 37/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 37

And now, we calculate the values at 15% discount rate.

YEAR 3 Pessimisti Optimisti

Raw Materials 617.18484 558.40552

Employee Cost 94.377907 85.389003

Selling and Admin

E penses 131.96877 119.40035

And now, we assume Base Case Value to be the PV of the Cash f low at a discount rate of

15% i.e. 129.23.

Now, we analyse the 2 Tornado Diagrams so as to make decisions regarding the expenses and

f ind the better option amongst the 2 present values of the cash f low available for Year 3.

0 100 200 300 400 500 600 700 800

R aw Mater ials

¦

mployee Cost

Selling and Admin§

xpenses

Pessimistic

Optimistic

0 100 200 300 400 500 600 700

R aw Mater ials

mployee Cost

Selling and Admin xpenses

Pessimistic

Optimistic

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 38/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 38

We observe that all the Expenses i.e. Raw materials cost, Employee cost and Selling and

Admin Expenses show similar trends for both the discount rates. Thus, we can conclude that

Year 3 follows the same trend as in Year 2 by increase of raw materials cost and decrease of

Employee Cost and Selling % Admin Expenses with the only exception that the Selling and

Admin Expenses have values on either side of the base case value. This states that the Selling

and Admin Expenses will depend upon the value which would hold true in year 3 i.e. the pessimistic or the Optimistic value. Thus, again a discount rate of 10% can be taken as it

provides more cash flows to the unit.

Thus, to conclude overall for the unit for the 3 years we can say that the cash flows generated

would be in direct relation to the raw material cost, employee cost and the selling and admin

expenses which form the major part of any business. Also, the difference in the discounting

factor for the present value does not have much effect on the present values of the cash flows

and hence, we can say that the trends in cash flows and expenses are independent of the

discounting factor. Thus, we can take the discounting rate as 10% for more cash flows.

Speaking about the trend in expenses, the Raw material costs shows an increasing trend over

the next 3 years for the unit. But, the gap between the pessimistic view and the optimistic

view seems to be reducing over the years. The Employee cost may increase over the years

and may bring down the value of cash flows down but if they remain optimistic as shown in

all the diagrams may help in bringing in more cash flows. The Selling and Admin Expenses

show a stable trend in these 3 forecasted years but the pessimist cost just seems to come into

picture in the last year of forecasting and if a similar trend continues, may bring down the

cash flows in future.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 39/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 39

5.CONCLUSION

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 40/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 40

CONCLUSION

The project briefly describes the risks involved and the techniques for analysis of these risks that play a major role in Capital Budgeting of a company.

A detailed study of some of these techniques such as Sensitivity Analysis and

Scenario Analysis is done and the practical approach mostly followed by the corporate is

looked into in detail.

A hypothetical company is selected and a Sensitivity Analysis is done of its

production unit for a period of three years so as to find the major expenses and income that

affect the cash flows of the production unit of the company. The present value of these cash

flows is generated and checked against the optimistic and pessimistic values found by the

Sensitivity Analysis.

A Tornado Diagram is drawn in support of the data obtained and analysis regarding

the effects of the major expenses is done. The analysis suggests that out of the major

expenses raw materials cost is the most dominant factor affecting the cash flows and this has

the capability of making or breaking a cash flow for a particular year. The Selling and Admin

expenses tend to increase but at a very slow and steady pace and are manageable. The

Employee Cost is the most stable cost of the unit for the selected period. But, the diagram

suggests that if it is controlled may result into higher cash flows for the unit.

All this leads to a conclusion that risk analysis is a major part of Capital budgeting as

risk is an integral part of a business. Estimating this risk efficiently and effectively plays asignificant role in the process of Capital Budgeting.

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 41/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

A.I.M.S. 41

6. BIBLIOGRAPHY

8/9/2019 Application of Sensitivity Analysis

http://slidepdf.com/reader/full/application-of-sensitivity-analysis 42/42

APPLICATION OF SENSITIVITY ANALYSIS IN CAPITAL BUDGETING

BIBLIOGRAPHY

BOOKS:

Financial Management ± Prasanna Chandra

Projects ±Prasanna Chandra

Project Finance

WEBSITES:

www.google.com

www.wikipedia.com

www.investopedia.com

www.howstuffworks.com

www.questia.com

www.cambridge.org