Embed Size (px)

Citation preview

ANZ – RETIREMENT COMMISSION FINANCIAL KNOWLEDGE SURVEY

�

ANZ RETIREMENT COMMISSION FINANCIAL KNOWLEDGE SURVEY MARCH 2006

Funded by ANZ, the Retirement Commission, with the support of the Ministry of Economic

Development, commissioned market research company Colmar Brunton to measure the

level of financial knowledge within the adult population. In the past, research has been

conducted among New Zealand school children, but this project considered knowledge

among the adult population for the first time.

The handling of money is no longer a physical matter. Long gone are the days when people were paid

in cash and probably managed their money by putting it into jam jars; one for groceries, one for bills and

another for a rainy day. Now, we have sophisticated banking systems and financial products and there

are many competing offers to be evaluated. Social, economic and political developments are also

having an influence on our finances. Borrowing is part of modern life, to pay for homes, education and

much more. We are living longer which means that more money will be needed to support us than for

previous generations. This means that individuals are under pressure to save much larger sums than their

parents and grandparents.

WHAT NEW ZEALANDERSKNOW ABOUT MONEY In the past few decades the financial lives of people in developed countries

have been transformed. The experience of New Zealanders is no exception.

THE SURVEY AT A GLANCE

~ Overviewoffinancialknowledgelevelsof

NewZealandersaged18andover.

~ Interviewsconductedbetween1Octoberand

20November2005with856peoplenationwide.

~ Amongthoseinvitedtotakepart,60%responded.

~ Interviewsof55minutesduration,onaverage.

~ Boostersamplesof104Maoriand96Pacific

peopletoensurestatisticallysignificantresults

forthesegroupsasiscommonpracticein

socialresearch.

~ Dataweightedtopopulationproportionsbyage,

genderandethnicity.

~ Peopledividedintothreemaingroups,depending

onscoresforanswersgiven;low,mediumand

highknowledge.

RESULTS AT A GLANCE

~ OverallNewZealandershaveareasonablelevel

ofpersonalfinancialknowledge.

~ Strongcorrelationbetweenfinancialknowledge

andsocio-economicstatus,butsomesignificant

exceptions.Somepeopleonhighincomesachieved

lowscoresandviceversa.

~ SomeconfusionoverNewZealandSuperannuation;

significantnumberthinkitisincomeand/or

assettested.

~ Understandingofcompoundinterestanddebt

consolidationrelativelyweak.

~ Mortgageholders’knowledgeofmortgagesshows

somelowlevelsinkeyareas.

~ Somebasicfinancialtermsarenotwellunderstood.

~ Mixedunderstandingofinvestmentstrategies,

particularlylongtermreturnsfromstockmarket

andrelevanceofcompoundinterest.

~ Somepeoplethinkitisalrighttodivulgetheir

internetbankingpasswordtobankstaff.

Why financial knowledge

is particularly important

in New Zealand

The more financial understanding

people have, the more effectively

they can manage their day-to-

day and long term financial

planning. In New Zealand this

is particularly relevant.

~ Youngpeopleneedtobeequippedtomake

financialdecisionsearlyasmanyuseloans

tofinancefurthereducation.

~ Thefinancialmarketisrelativelyderegulated

andencouragescompetitionsoconsumersneed

tobeabletocompareandcontrastproductsto

makethebestdecisions.

~ NewZealandhasavoluntaryapproachtosaving

forretirement.Manypeoplewillwantandneed

tosavefromtheirownresourcestotopuptheir

statepensionsandthisrequiresanunderstanding

ofdebt,savings,investmentsandbasic

moneymanagement.

� �

ANZ RETIREMENT COMMISSION FINANCIAL KNOWLEDGE SURVEY MARCH 2006

FINANCIAL KNOWLEDGE DEFINED

Financial knowledge, for the purposes of the study,

was defined as:

“Theabilitytomakeinformedjudgementsandtotakeeffectivedecisionsregardingtheuseandmanagementofmoney.”Source: Schagen, S. “The Evaluation of NatWest Face 2 Face With Finance”: NFER, 1997.

Also used in “ANZ Survey of Adult Financial Literacy in Australia” report by Roy Morgan Research, May 2003 (this definition was adopted from UK and Australian research with a view to international consistency).

The main objectives of the survey were to:

~ Identifyareasoflowfinancialknowledge,bytopic

andpopulation,andtoassisteducatorstoimprove

literacyinthoseareas.

~ Developbenchmarkmeasuresoffinancial

knowledgeacrosstheentireadultpopulationand

keysegmentssothattrendscanbemeasuredand

programmestargetedatareasofneed.

~ Assistthefinancialservicesindustrytoidentifywhich

aspectsoffinancialskills,productsorservicesare

causingthegreatestproblemsforNewZealanders

andthusimprovedesignorcommunication.

The survey also provided the Ministry of Economic

Development with information to:

~ Developlawreformprogrammesthatprovide

effectiveconsumerprotectionandaddressreal

issuesfacingindividuals.

~ Identifyparticipationrates,investmentbehaviours,

habitsandlevelofsophisticationofretailconsumers

inNewZealand’ssecuritiesmarket.Resultsspecific

totheseobjectivesarereportedonpage11.

SO HOW ARE WE DOING?

While the knowledge levels are reasonable overall, there are gaps that could be pivotal in deciding how

the population adapts in future to the modern financial environment and how well we do in retirement.

There is a strong correlation between financial knowledge and socio-economic status. Across all topics,

knowledge generally increases with age, income, education and also net wealth. This finding matches that

of other international surveys.

~ Levelsofknowledgearespecifictocircumstancesorrelatedtoexperiencesandthedifferentlivesthat

peoplelead.Forexample,thoseonlowincomesmayhavelessknowledgeofinvestmentastheydonot

havethemoneytoinvest.

~ Peoplewithlowerlevelsofpersonalfinancialknowledgearemorelikelytobeyoung(18-24);orolder

(75yearsandover);havelowerlevelsofeducation,incomeandnetwealth;orbeofMaoriorPacific

ethnicity(possiblybecauseoftheiryoungerageprofile,lowerlevelsofeducation,income

andnetworth);andbetenantsratherthanhomeowners.

� �

ANZ RETIREMENT COMMISSION FINANCIAL KNOWLEDGE SURVEY MARCH 2006

Investing

~ Thereisalackofunderstandingaboutsharemarket

returnsrelativetootherformsofinvestment.

~ Whilethemajority,93%,dounderstandthat

thesharemarkethasitsupsanddownsinthe

shortterm,54%incorrectlythoughtthata

rangeoffixedinterestinvestmentswould

makemoremoneyover18yearsthanshares.

Nearlyathird,30%,answeredthatshareswould

makemoremoney.

~ Nearly20%thoughtthatinvestingonlyin

propertywasawaytoreduceinvestmentrisk.

Scams

~ Mostpeoplecanpickseveralaspectsofscams,

suchasthepromiseofveryhighreturnswithlittle

risk,89%,andtheofferbeingmadetoaselect

fewpeople,91%.Fewer,69%,understoodthat

onesignofascamisthattheminimumamountto

investkeepsreducing.

Understanding financial terms

~ Significantminoritieswereunabletogivethe

correctdefinitionoftheterm‘asset’,with25%

unabletomatchthedefinition.Athirdcouldnot

matchthedefinitionsfor‘liability’and‘capital

gains’,40%wereunabletodefine‘realrateof

return’andmorethanhalfhadtroublewith

‘networth’.

~ Aquarterhaddifficultywiththeterm‘securedloan’

andathirddidnotknowthemeaningof‘equity’.

~ Most,90%,understandthatinflationmeansyou

wouldneedmoreeachyeartomaintainthesame

livingstandardsand79%knowthatinflation

affectsthevalueofsavingsovertime.

Banking

~ NewZealandhasahighlevelofbankinginclusion,

with97%ofconsumershavingatransactionor

savingsaccount(Source:ACNielsenConsumer

FinanceMonitor).

~ Thevastmajorityofpeople,92%,couldreadand

understandabankstatementpresentedtothem.

However,whenaskedfourquestionswhich

requiredadditionalcalculations58%could

answerallfourcorrectly.

~ Twothirds,67%,understoodhowtominimise

theirtransactioncostsbypayingbyEFTPOSand

gettingcashoutatthesametime.

~ Overhalf,56%,understoodthatinternetbanking

ischeaperorattractslessfeesthanoverthe

counterbankingattheirlocalbranch.

~ Asmightbeexpected,olderpeoplewereless

likelythanyoungerpeopletouseelectronic

ornewerformsofbanking.

Numeracy

~ Threequarterswereabletocorrectlyanswera

scenariorequiringbasicaddition,subtractionand

multiplicationrelatingtohouseholdexpenditure

andtakehomepay.Malesweresignificantlymore

likelythanfemalestogettherightanswerwhere

calculationswereneeded.

Saving

~ Themajority,80%,understoodthatinflation

affectssavingsandthespendingpowerofsavings.

~ Justover80%canidentifyhowsimpleinterest

accruestoasavingsaccount.

DETAILED KNOWLEDGE FINDINGS

Financial planning for retirement

Asked what a person needs to think about to

work out how much to save for retirement,

80% mentioned lifestyle and the amount of

spending required in retirement; almost half

mentioned their current situation and their ability

to save right now; 40% mentioned the income they

will have when they retire; 10% mentioned life

expectancy as a key factor.

~ Thiswasanareaofknowledgeparticularly

challengingforpeoplewithhouseholdincomes

of$20,000orless.Forpeopleinthisgroup

NewZealandSuperannuation(NZSuper)

replacescurrentincomeinretirement.

~ Most,83%,knewthatNZSuperispaidat65

butathirdthoughtthatitisincome-testedand

aquarterdidnotknow.Nearly30%thoughtit

isassettestedand25%didnotknow.

~ KnowledgeofNZSuperincreasedwithage;those

over50weremorelikelytoknowtheactuallevel

ofNZSuper($13,302aftertaxforasingleperson

livingalone)andthefactthatNZSuperisnot

affectedbypersonalincomeorassets.

Debt and interest

~ Consolidationofdebtwasarelativelyweakarea

offinancialknowledge;fewerthanhalfidentified

groupingofdebtstogetherinonelowinterest

loanasagoodwaytopayoffdebt.

~ Compoundinterestwaslesswellunderstood.

Whenpresentedwithtwoscenarios,justover

athirdwereabletoidentifythatonesaver

(whosavedasmalleramountthantheother

butoveralongerperiod)hadmoremoney.

Mortgages

~ Aquarterofpeoplewithmortgagesdidnot

appreciatethatmakingfortnightlyratherthan

monthlypaymentswouldbethebetterpayment

optionforreducinginterestpaid.

~ 24%ofmortgageholdersdidnotknowthe

meaningoftheterm‘equity’.

~ Afifth,20%,ofmortgageholderscouldnotgive

thecorrectanswerastowhenitisbesttohave

afixedratehomeloan.

~ Askedtochoosefromarangeofoptionsasto

thebestwaytofinanceaninvestmentproperty,

halfofpeoplewithmortgagesdidnotchoose

thecheapestoptionofborrowingagainstan

existingproperty.

Credit cards

~ Themajorityofcreditcardholders,94%,

understoodthatpayingtheminimumonacredit

cardmeantthatmoneywasstillowed.

~ 20%ofcreditcardholdersdidnotknowthat

payingoffthefullamountonthecreditcardeach

monthwouldgiveinterest-freedaysonpurchases.

Internet banking – password security

~ Mostpeople,96%,thoughtitwasnotappropriate

totellafriendtheirinternetbankingpassword

but51%thoughtitwouldbealrighttotelltheir

partner.17%thoughtitwasalrighttotella

memberofthebank’sstaff.

Protection

~ Mostpeople,91%,gavetherightanswerabout

lifeinsurancewhenaskedtosaywhoneededthe

most–asinglemotherwithchildren–outofa

groupofscenarios.

~ 80%understoodthepropertysharingimplications

ofthePropertyRelationshipAct,whenpresented

withascenariorelatingtoentitlementtothe

shareofahousewhenacoupleseparatesafter

fouryears.

� �

ANZ RETIREMENT COMMISSION FINANCIAL KNOWLEDGE SURVEY MARCH 2006

EDUCATIONAL OppORTUNITIES

There are opportunities to improve the understanding that New Zealanders have of a wide range of financial

concepts. Improving knowledge will help people to manage their money day-to-day and for the future.

This is particularly important in relation to the introduction of legislation to establish a workplace savings

scheme. Education will also enable people to make sound, well informed decisions in the context of their

entire financial situation.

~ Keyareasforimprovingknowledgeincludethemanagementofdebtthroughconsolidatingloans,theeffect

ofcompoundinterestonsavingsoveralongperiod,choiceofmortgageandmanagingmortgagedebt,

NewZealandSuperannuation–particularlywhetheritisaffectedbyprivatewealth,investmentandstock

marketinvestment,andeffectiveuseofcreditcards.

WHO KNOWS THE MOST ABOUT MONEY?

One of the major objectives of the research project was to develop benchmark measures of knowledge across

groups within the population. These can be used in future to monitor changes in financial knowledge among the

groups concerned. Respondents were given scores for their levels of basic financial knowledge and divided into

three knowledge groups, low, medium and high. Those who scored highly on the advanced knowledge questions

were classified as Advanced Investors.

Even though levels of knowledge generally increased with socio-economic status and other factors, there were

exceptions, for example:

~ Whileyoungpeoplegenerallyknowlessacrosstheboard,11%of18-24yearoldsscorehighly.

~ Nearlyafifth,19%,ofpeoplenotinpaidemploymentalsoscorehighly.

~ Whilethosewithlowereducationalachievementgenerallyhavelowfinancialknowledge,

14%scorehighlyand32%areinthemediumknowledgegroup.

~ Amongthoseearning$20,000orless,8%scorehighly.

~ Amongthosewithnetwealthof$300,000ormore15%areinthelowknowledgegroup.

~ While67%ofMaoriwereinthelowknowledgegroup,11%areinthehighknowledgegroup.

(See table of Financial Knowledge Groups on page 10.)

ATTITUDES AND BEHAVIOUR

~ Themajorityofpeople,83%,saytheyfeelconfidentaboutmanagingtheirfinancialaffairsand84%feelin

controloftheirborrowinganddebtgenerally.

~ While31%saytheyhavenodifficultiesmanagingmoney,26%saythatnothavingenoughmoneyistheir

greatestdifficulty.Peopleinlowincomegroupsweremorelikelythanotherstosaythatnothavingenough

moneyistheirgreatestdifficulty.Allknowledgegroupshavethesameproportionwhoreporttheyhave

nodifficulties.

~ Nearlyafifth,19%,saytheirgreatestdifficultyisincontrollingtheirimpulsebehaviour.

~ Themajority,80%,havefinancialgoalsand21%awrittenfinancialplan.Peopleaged45-54yearsaremore

likelytohaveawrittenplanthanothers.

~ Morethan60%saytheycouldcopeforthreemonthsiftheyhadamajorlossofincome,but30%saythey

couldnot.

SIGNpOSTS FOR THE FUTURE

~ Thegenerallypoorlevelofknowledgeamongsomeyoungpeoplecouldhinderthemfrommanagingtheir

financeswellinfuture.Whileyoungpeoplecouldbeexpectedtogainknowledgewithage,theincreased

pressuresonyoungadults,suchasthenecessitytoborrowforfurthereducationandeasyaccesstocredit,could

meanthattheyarenotequippedtomakethebestchoicesatavulnerabletimeintheirlives.

~ Somepeoplehaveanunsteadygraspoffinancialtermsandconcepts.Inanenvironmentwheremanywillbenefit

fromsavingforretirementtheymaybeatadisadvantageiftheydonotunderstand,forexample,thebenefitsof

savingsmallamountsfromayoungage.

~ AlthoughunderstandingofNZSuperincreasedwithage,youngerpeoplewhodonotknowthatthestate

pensionisnotasset-testedmightbedeterredfromsavingprivately.

~ Gapsinknowledgeaboutmortgagesmightdeterborrowersfrompayingoffdebtquicklyandenhancingtheir

financialpositionoverthelongterm.

� �

ANZ RETIREMENT COMMISSION FINANCIAL KNOWLEDGE SURVEY MARCH 2006

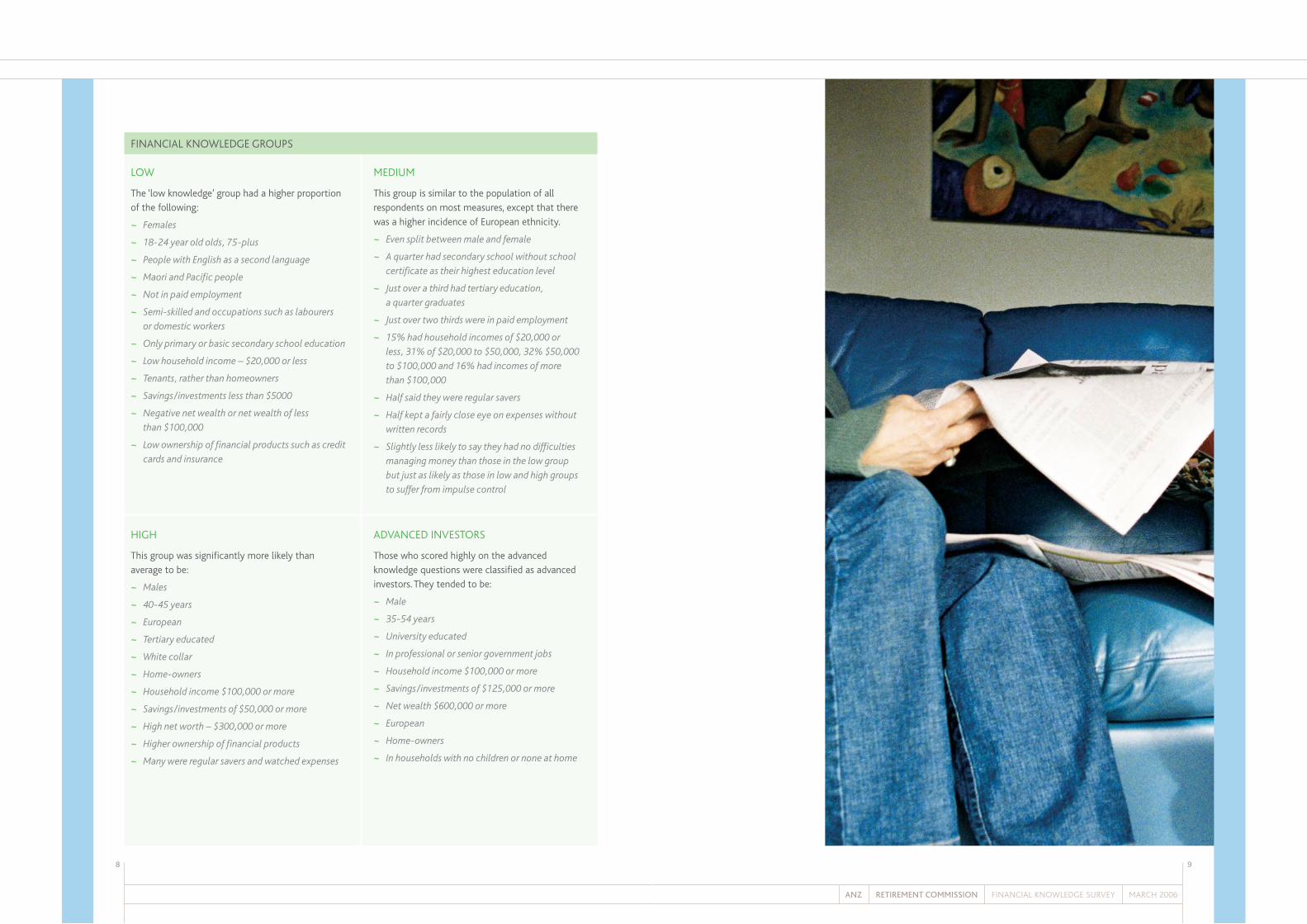

LOW

The ‘low knowledge’ group had a higher proportion

of the following:

~ Females

~ 18-24yearoldolds,75-plus

~ PeoplewithEnglishasasecondlanguage

~ MaoriandPacificpeople

~ Notinpaidemployment

~ Semi-skilledandoccupationssuchaslabourers

ordomesticworkers

~ Onlyprimaryorbasicsecondaryschooleducation

~ Lowhouseholdincome–$20,000orless

~ Tenants,ratherthanhomeowners

~ Savings/investmentslessthan$5000

~ Negativenetwealthornetwealthofless

than$100,000

~ Lowownershipoffinancialproductssuchascredit

cardsandinsurance

MEDIUM

This group is similar to the population of all

respondents on most measures, except that there

was a higher incidence of European ethnicity.

~ Evensplitbetweenmaleandfemale

~ Aquarterhadsecondaryschoolwithoutschool

certificateastheirhighesteducationlevel

~ Justoverathirdhadtertiaryeducation,

aquartergraduates

~ Justovertwothirdswereinpaidemployment

~ 15%hadhouseholdincomesof$20,000or

less,31%of$20,000to$50,000,32%$50,000

to$100,000and16%hadincomesofmore

than$100,000

~ Halfsaidtheywereregularsavers

~ Halfkeptafairlycloseeyeonexpenseswithout

writtenrecords

~ Slightlylesslikelytosaytheyhadnodifficulties

managingmoneythanthoseinthelowgroup

butjustaslikelyasthoseinlowandhighgroups

tosufferfromimpulsecontrol

HIGH

This group was significantly more likely than

average to be:

~ Males

~ 40-45years

~ European

~ Tertiaryeducated

~ Whitecollar

~ Home-owners

~ Householdincome$100,000ormore

~ Savings/investmentsof$50,000ormore

~ Highnetworth–$300,000ormore

~ Higherownershipoffinancialproducts

~ Manywereregularsaversandwatchedexpenses

ADVANCED INVESTORS

Those who scored highly on the advanced

knowledge questions were classified as advanced

investors. They tended to be:

~ Male

~ 35-54years

~ Universityeducated

~ Inprofessionalorseniorgovernmentjobs

~ Householdincome$100,000ormore

~ Savings/investmentsof$125,000ormore

~ Netwealth$600,000ormore

~ European

~ Home-owners

~ Inhouseholdswithnochildrenornoneathome

FINANCIAL KNOWLEDGE GROUpS

�0 ��

ANZ RETIREMENT COMMISSION FINANCIAL KNOWLEDGE SURVEY MARCH 2006

FINANCIAL MARKET pARTICIpATION FINDINGS

The Ministry of Economic Development was particularly interested in better understanding behaviour in relation

to superannuation, life insurance, shares and other securities products. Questions not specifically related to

financial knowledge were asked to find out the demographics of participation in these markets, and the advice

that investors sought and valued before making their investment decisions.

Superannuation and insurance

The results here tended to confirm what might

be expected.

~ Moremales(71%)thanfemales(62%)haveor

havehadsuperannuationorlifeinsurance.

~ Greaterlevelswerealsoobservedamonghigher

incomehouseholds,amongindividualsaged

30-54years,andthosewhoowntheirownhomes.

Advice

~ 58%ofthosewhohave,orhavehadsuperannuation

orinsurancegotadviceinadvanceofsigning

thecontract.

~ Themainsourcesofadviceweretheinsurance

companyagentoradvisor(38%),anindependent

financialplanner(36%)andarelativeor

friend(36%).

~ Therewasagoodlevelofsatisfactionwiththe

advicereceived.85%foundtheadviceobtained

fromtheinsurancecompanyveryusefulorquite

useful.Thepercentageforadviceobtainedfrom

anindependentfinancialplannerwasconsiderably

higherat94%.

Collective investment schemes and debt securities

~ 28%hadinvestedorseriouslyconsidered

investinginmanagedfunds,contributory

mortgageschemes,bonds,debenturesorother

debtsecurities.Themaindemographictrends

weremuchthesameasnotedforsharesbelow.

~ 63%ofthe28%hadgotadvice.

~ Peopleunder35yearsofagewerelesslikely

tohavegotadvice.

~ Thepredominantsourceofadvicewasaspecialist

investmentadvisor(56%).

~ 26%obtainedadvicefromarelativeorfriend,

16%fromanaccountant,14%fromashare

broker,9%fromabankand4%fromalawyer.

~ 83%foundtheadvicefromaspecialistinvestment

advisortobeveryusefulorquiteuseful.

FINANCIAL KNOWLEDGE GROUpS

The survey has shown a strong correlation between financial knowledge and socio-economic status.

This table shows how a selection of key demographic groups are spread across the financial knowledge groups.

For example, 40% of females are in the low knowledge group, 32% in the medium and 29% in the high.

Demographic category Low Medium High

Knowledge Knowledge Knowledge

% % %

Total Sample (�00%) �� �� ��

Female 40 32 29

Male 25 36 39

18-24 years 57 32 11

35-54 years 23 29 48

65 years and over 45 33 22

paid employment 24 35 41

Not in paid employment 51 30 19

primary or basic secondary school education (no certificate) 54 32 14

Tertiary or post graduate education 18 36 46

Household income $20,000 or less 62 30 8

Household income $50,000 or more 17 35 48

Negative net wealth 51 37 12

Net wealth $300,000 or more 15 34 51

European 24 37 39

Maori 67 22 11

pacific people 85 11 4

Home owned by self/partner 23 33 44

Home rented 45 36 19

Home duties 45 36 19

Retired 45 33 22

English as first language 29 35 36

English not first language 69 19 12

�� ��

ANZ RETIREMENT COMMISSION FINANCIAL KNOWLEDGE SURVEY MARCH 2006

Shares

~ 20%ofrespondentscurrentlyownshares.

Theownershipratesweresignificantlyhigher

forthoseaged45-74,thosewhoownedtheir

ownhome,havingnomortgage,havingno

childrenornochildrenathome,household

incomeof$100,000ormoreandwitha

postgraduatequalification.

~ 27%ofthe80%whocurrentlydidnotownshares

haddonesointhepast.Themainreasonsfor

sellingwere:aneedforthemoney(38%),concern

thatthesharemarketwastoorisky(27%),better

returnsavailablethroughotherinvestments(11%),

becausetheylostmoney(9%)andcomplexityof

thesharemarket(5%).

~ 30%hadboughtorseriouslyconsideredbuying

sharesthroughapublicoffering.Males,those

aged40-54,ahouseholdincomeof$100,000or

moreandthosewithuniversityqualificationswere

morelikelytohaveownedthem.

~ 37%ofthe30%gotadvicebeforemakingtheir

decision.Thispercentageissubstantiallylower

thanforsuperannuation/lifeinsurance,collective

investmentschemesanddebtsecurities.

~ Themainsourcesofadvicewererelativeor

friend(36%),sharebroker(22%),specialist

investmentadvisor(21%),accountant(21%)

andlawyer(12%).

Obtaining written information about investments

Three quarters of all respondents answered yes

to at least one of the categories of questions in

this section of the questionnaire.

~ 65%ofthisgroupofinvestorsandpotential

investorssaidtheyhadobtainedwritten

informationinadvance.64%hadobtaineda

prospectus,56%obtainedabrochureand46%

aninvestmentstatement.

~ Thosewhohadobtainedaninvestmentstatement

wereaskedhowusefulwerethe10categoriesof

informationthatarerequiredtobeincludedin

aninvestmentstatement.Allcategorieswere

regardedasveryusefulorquiteusefulbyatleast

87%ofthissubsetofrespondents.

~ Thepercentageratingacategory‘veryuseful‘

variedfrom46%to76%.Thehighestratings

weregiventoinformationaboutwhattherisks

are(76%),whatthereturnsare(75%),whoto

contactwithenquiries(74%)andwhatthe

chargesare(76%).

RETIREMENT COMMISSION

LEVEL 3, 69-71 THE TERRACE

pO BOx 12-148

WELLINGTON, NEW ZEALAND

www.retirement.org.nz

www.sorted.org.nz

ANZ

pRIVATE BAG 92210

AUCKLAND, NEW ZEALAND

www.anz.co.nz

A copy of this Summary Report and the full Colmar Brunton Research Report can be found

on www.retirement.org.nz and www.anz.co.nz