Embed Size (px)

Citation preview

ANZ Commodity Strategy

AIBC Coal Update

Mark PervanHead of Commodities Research

June 2010

2

MACRO

3

Source: Bloomberg

Purchasing Managers Indices

China rebounded much quicker from the GFC

26

30

34

38

42

46

50

54

58

62

Jan-06 Jul-06 Jan-07 Jul-07 Jan-08 Jul-08 Jan-09 Jul-09 Jan-10

USEUChinaJapan

points

expanding

contracting

4

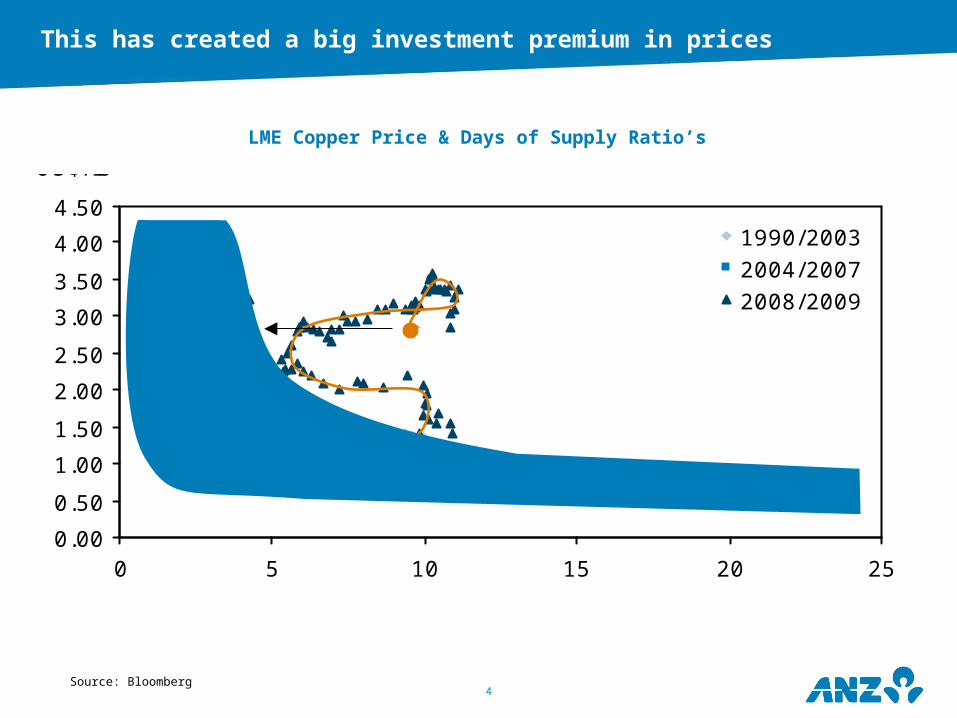

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

0 5 10 15 20 25

1990/2003

2004/20072008/2009

Copper

days of supply

US$/ lb

Source: Bloomberg

LME Copper Price & Days of Supply Ratio’s

This has created a big investment premium in prices

5

0

5

10

15

20

25

90 92 94 96 98 00 02 04 06 08 100

200

400

600

800

1,000

1,200

days of supply Total LME Supply (RHS)

'000t

9 9

days

Source: Bloomberg

LME Copper Stockpiles & Days of Supply

However, funds may be calling it right

6

(600)

(400)

(200)

0

200

400

600

800

J an-03 J an-04 J an-05 J an-06 J an-07 J an-08 J an-09 J an-10

Long Short Net (Long-Short)

Kt

Source: Bloomberg

Non-Commercial Copper Positions

Funds have taken profits

7

(300)

(200)

(100)

0

100

200

300

J an-03 J an-04 J an-05 J an-06 J an-07 J an-08 J an-09 J an-10

Long Short Net (Long-Short)

Mbbls

Source: Bloomberg

Non-Commercial Oil Positions

Oil positioned heavily in both directions

8Source: Bloomberg

Discount to Historical High Price Level

(3.1)

(15.2)

(26.0)

(26.4)

(28.9)

(31.6)

(32.8)

(40.1)

(47.8)

(48.6)

(53.2)

(57.0)

(59.9)

(60.9)

(80) (70) (60) (50) (40) (30) (20) (10) 0 10 20 30 40 50

Gold

Silver

Copper

Iron ore

Dow Jones

Tin

Platinum

Aluminium

US Dollar

Coal

Oil

Lead

Zinc

Nickel $24.52/lb - May 2007

120.9 - Jul 2001

$2.09/lb - Nov 2006

$195/t - Jul 2008

$145.30/bbl - Jul 2008

$1.81/lb - Oct 2007

$148.38/lb - Jul 2008

$11.49/lb - May 2008

$2,250/oz - Mar 2008

14,164 - Oct 2007

$4.04/lb - Jul 2008

$210/t - Mar 2008

$20.81/oz - Mar 2008

$1,220/oz - Mar 2008

Coal prices look cheap from a historical high basis

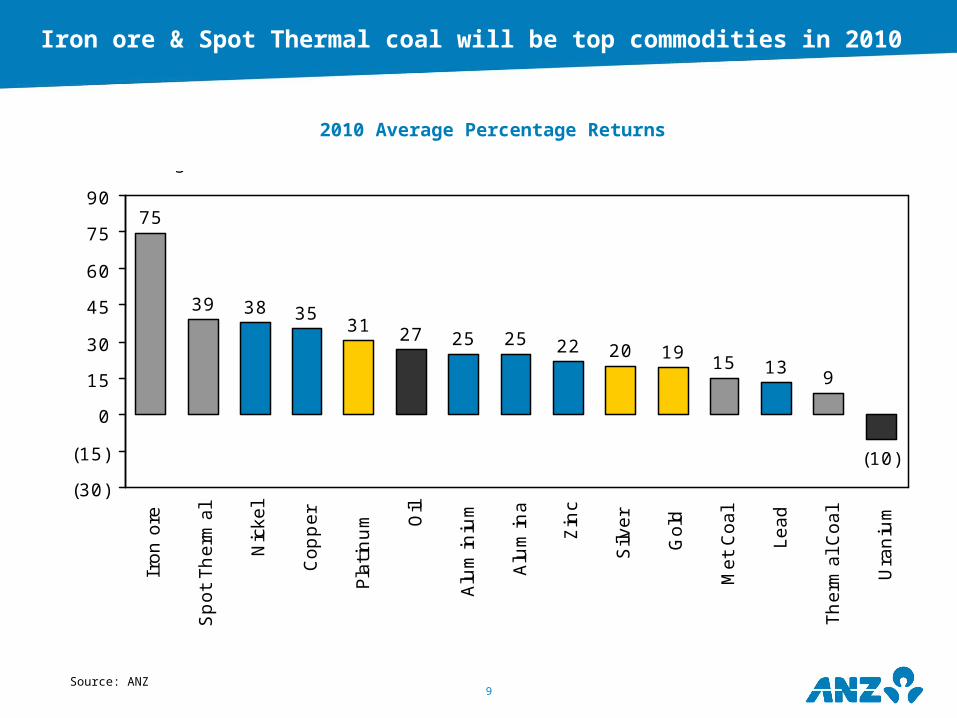

9Source: ANZ

2010 Average Percentage Returns

Iron ore & Spot Thermal coal will be top commodities in 2010

75

39 38 3531 27 25 25 22 20 19

15 139

(10)

(30)

(15)

0

15

30

45

60

75

90

Iron

ore

Sp

ot

Th

erm

al

Nic

kel

Cop

per

Pla

tin

um

Oil

Alu

min

ium

Alu

min

a

Zin

c

Silv

er

Gold

Met

Coal

Lead

Th

erm

al C

oal

Ura

niu

m

YoY % change

10Source: ANZ

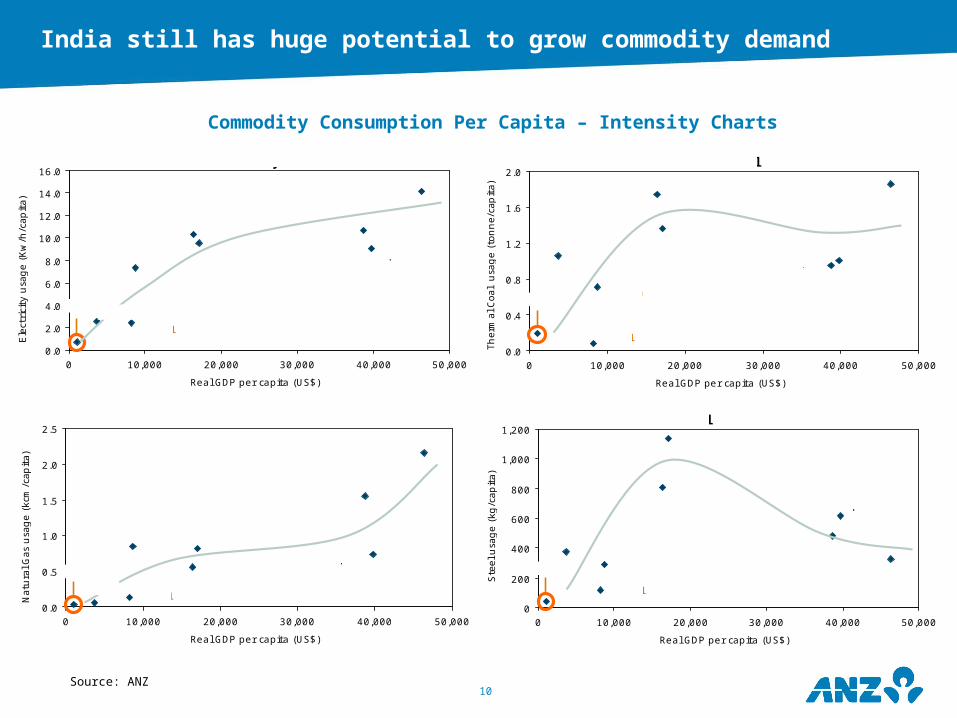

Commodity Consumption Per Capita – Intensity Charts

India still has huge potential to grow commodity demand

0

200

400

600

800

1,000

1,200

0 10,000 20,000 30,000 40,000 50,000

Real GDP per capita (US$)

Ste

el u

sag

e (

kg

/cap

ita)

Steel

India

Brazil

Russia

China

Taiwan

Sth Korea

Japan

EU

US

0.0

0.5

1.0

1.5

2.0

2.5

0 10,000 20,000 30,000 40,000 50,000

Real GDP per capita (US$)

Natu

ral G

as

usa

ge (

kcm

/cap

ita)

Natural Gas

India

Brazil

Russia

Taiwan

Sth KoreaJapan

EU

US

China

0.0

0.4

0.8

1.2

1.6

2.0

0 10,000 20,000 30,000 40,000 50,000

Real GDP per capita (US$)

Th

erm

al C

oal u

sag

e (

ton

ne/c

ap

ita)

Thermal Coal

India

Brazil

Russia

China Taiwan

Sth Korea

JapanEU

US

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

0 10,000 20,000 30,000 40,000 50,000

Real GDP per capita (US$)

Ele

ctri

city

usa

ge (

Kw

/h/c

ap

ita)

Electricity

India

Brazil

Russia

Taiwan

Sth Korea Japan

EU

US

China

11

THERMAL COAL

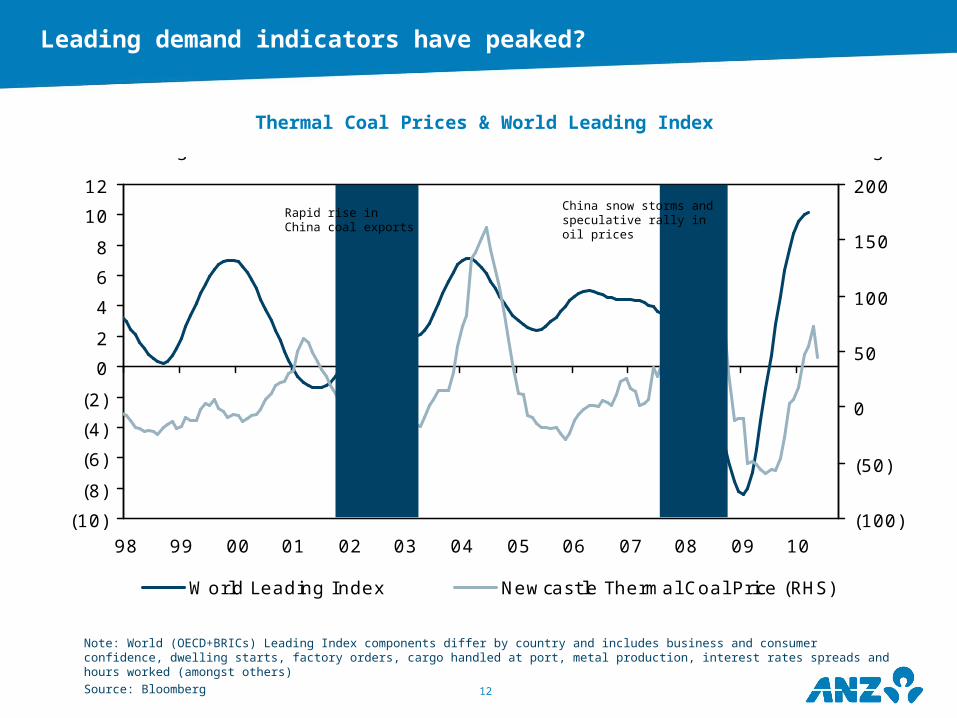

12

(10)

(8)

(6)

(4)

(2)

0

2

4

6

8

10

12

98 99 00 01 02 03 04 05 06 07 08 09 10(100)

(50)

0

50

100

150

200

World Leading Index Newcastle Thermal Coal Price (RHS)

YoY % changeYoY % change

Note: World (OECD+BRICs) Leading Index components differ by country and includes business and consumer confidence, dwelling starts, factory orders, cargo handled at port, metal production, interest rates spreads and hours worked (amongst others)Source: Bloomberg

Thermal Coal Prices & World Leading Index

Leading demand indicators have peaked?

China snow storms and speculative rally in oil prices

Rapid rise in China coal exports

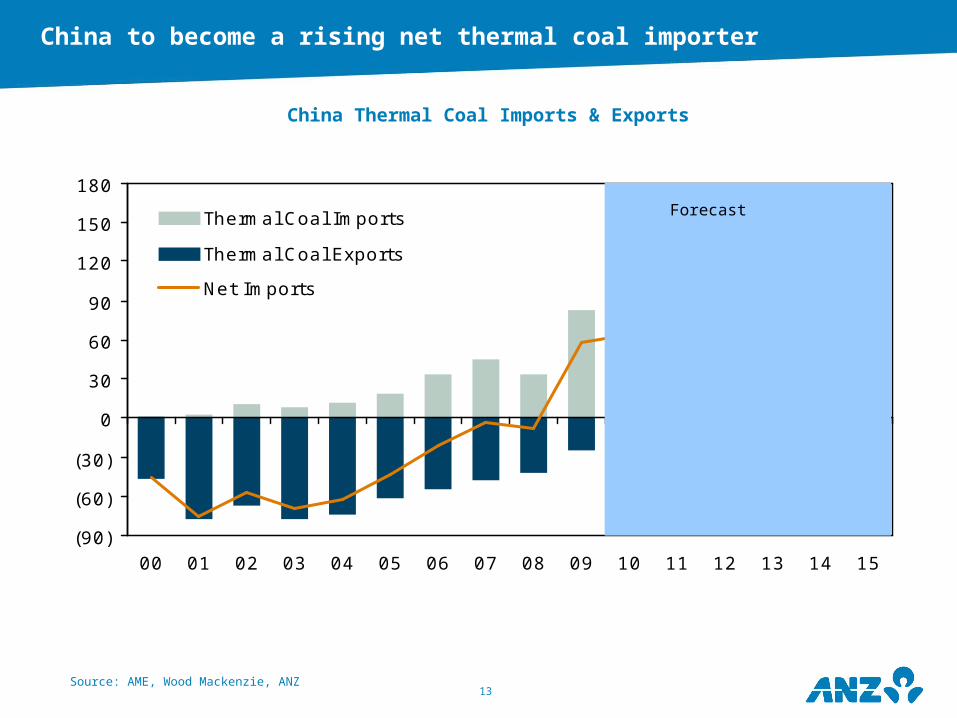

13

(90)

(60)

(30)

0

30

60

90

120

150

180

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Thermal Coal Imports

Thermal Coal Exports

Net Imports

m tonnes

57

140

China Thermal Coal Imports & Exports

Source: AME, Wood Mackenzie, ANZ

China to become a rising net thermal coal importer

Forecast

14

0

25

50

75

100

125

150

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 150%

5%

10%

15%

20%

25%

30%

35%

40%

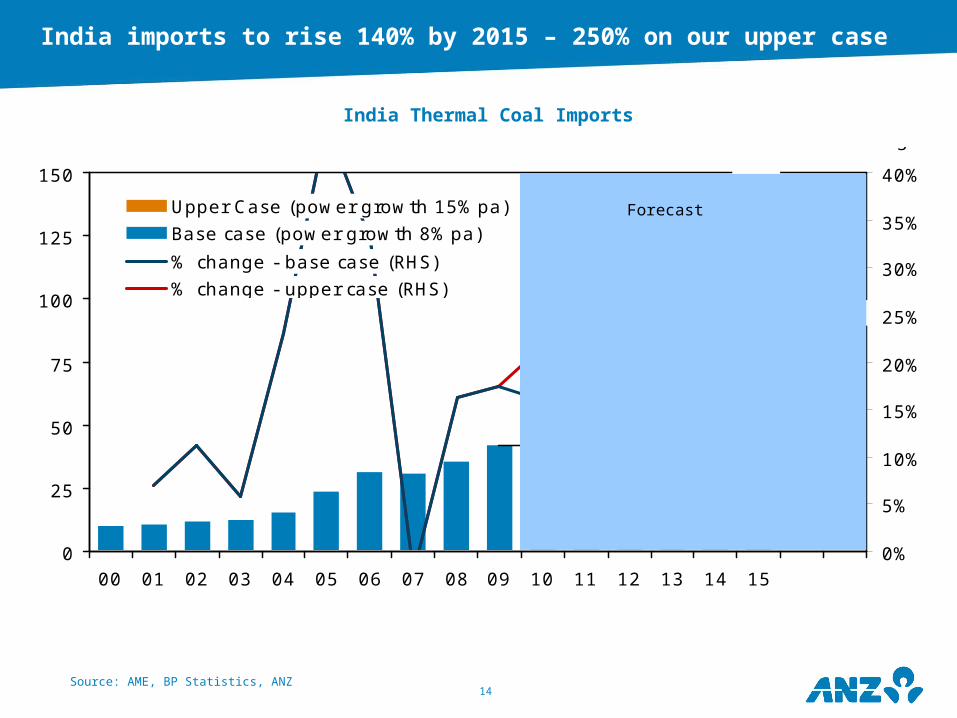

Upper Case (power growth 15%pa)

Base case (power growth 8%pa)

% change - base case (RHS)

% change - upper case (RHS)

m tonnes YoY change

42

146

100

58

104

India Thermal Coal Imports

Source: AME, BP Statistics, ANZ

India imports to rise 140% by 2015 – 250% on our upper case

Forecast

15Source: AME, ANZ, Wood Mackenzie

Thermal Coal Import Demand (million tonnes)

India jumps to number 4 – and number 2 on the upper case

2009 2015

83101

2009 2015

4866

China

Russia

Europe

INDIA

J apan

Korea

2009 2015

108

138

Taiwan

2009 2015

83

2009 2015

23 25

2009 2015

42

2009 2015

107122

161

100

146

16

0

100

200

300

400

500

600

700

800

900

1,000

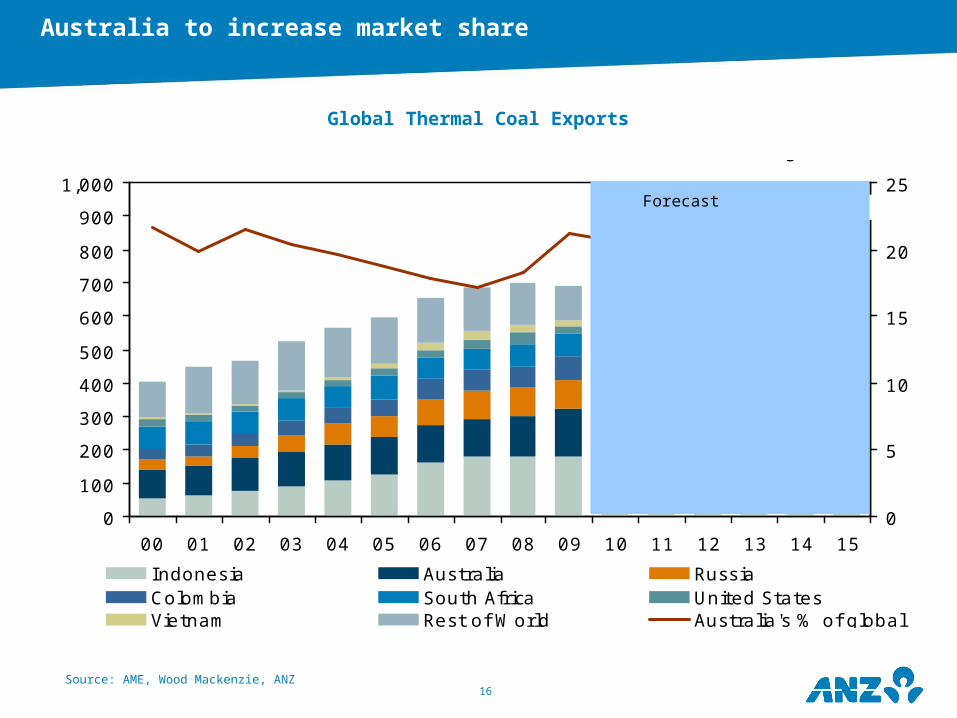

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 150

5

10

15

20

25

Indonesia Australia RussiaColombia South Africa United StatesVietnam Rest of World Australia's % of global

% global sharem tonnes

21% 24%

Source: AME, Wood Mackenzie, ANZ

Global Thermal Coal Exports

Australia to increase market share

Forecast

17

Source: Wood Mackenzie

New South Wales Coal Infrastructure Capacity

Port capacity constraints in NSW addressed by 2015?

0

50

100

150

200

250

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Port Capacity Rail Capacity

m tonnes

18

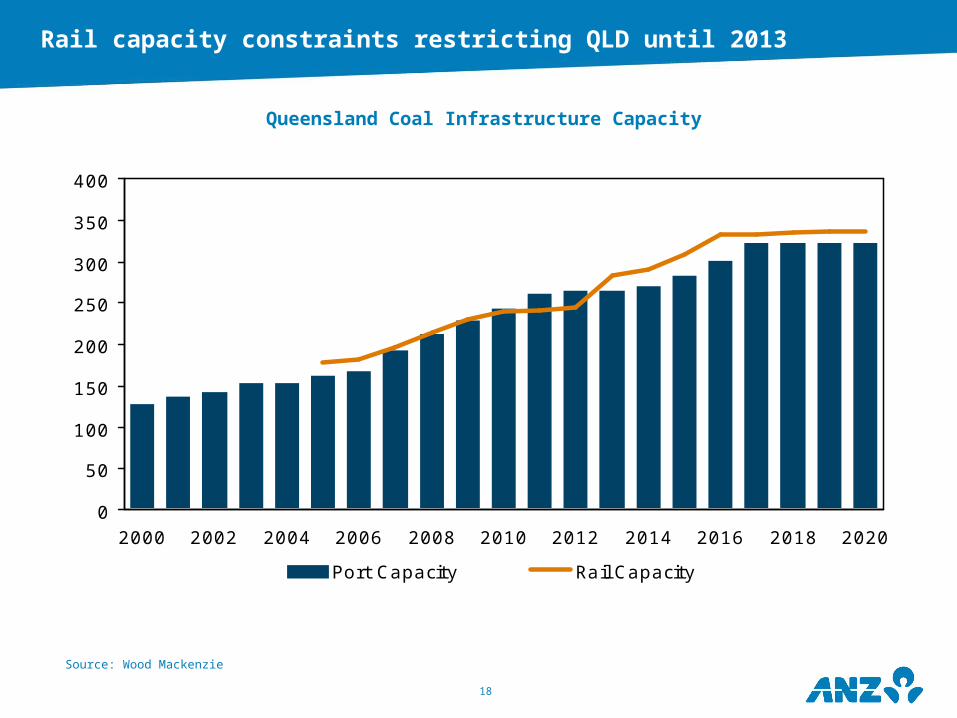

Source: Wood Mackenzie

Queensland Coal Infrastructure Capacity

Rail capacity constraints restricting QLD until 2013

0

50

100

150

200

250

300

350

400

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

Port Capacity Rail Capacity

m tonnes

19Source: Indonesian Coal Mining Association, BP Statisctics

Global Thermal Proven Coal Reserves (million tonnes)

Australia has the reserves to provide longer term

246 bt50 bt

Africa

Europe

15 bt 32 bt

147 bt

59 bt

115 bt

76 bt

4 btLatin

America

North America

India

Russia

China

Australia

Indonesia

Total World826 bt

20

METALLURGICAL COAL

21

China Coking Coal Imports & Exports

Source: AME, ANZ

China to become a substantial coking coal importer

(30)

(20)

(10)

0

10

20

30

40

50

60

70

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Coking Coal Imports

Coking Coal Exports

Net Imports

m tonnes

33

62

22

0

10

20

30

40

50

60

70

80

90

100

110

00 01 02 03 04 05 06 07 08 09 10F 11F 12F 13F 14F 15F0%

5%

10%

15%

20%

25%

30%

35%Upper Case (Steel growth 15%pa)

Base case (Steel growth 9%pa)

% change - base case (RHS)

% change - upper case (RHS)

m tonnes YoY change

4638

76

30

76

106

India Coking Coal Imports

Source: AME, Wood Mackenzie, ANZ

India imports to rise 160% by 2015 – 260% on our upper case

Forecast

23Source: AME, Wood Mackenzie, ANZ

Coking Coal Import Demand (million tonnes)

India jumps to number 1 on both growth scenario’s

2009 20152009 2015

2009 2015

2009 2015

2009 2015

2009 2015

2009 20152009 2015

USA

China

Brazil

J apanEurope

Taiwan

Korea

32

53

30

68

5 10

49

66

1727

1225

6 834

62

146

76

INDIA

24

0

50

100

150

200

250

300

350

400

00 01 02 03 04 05 06 07 08 09 10F 11F 12F 13F 14F 15F0

10

20

30

40

50

60

70

Australia Canada United States

Russia Rest of the World Australia % of global

million tonnnes % global share

61%

54%

Source: AME, Wood Mackenzie, ANZ

Global coking coal supply to remain leveraged to Australia

Forecast

Global Coking Coal Exports

25

APPENDIX

26

Appendix: ANZ quarterly commodity price forecasts

Source: Bloomberg, ANZ

End of Period Mar-10 J un-10 Sep-10 Dec-10 Mar-11 J un-11 Sep-11 Dec-11 Mar-12 J un-12 Sep-12 Dec-12 Mar-13 J un-13unit

Copper US$/ lb 3.52 2.90 3.10 3.20 3.30 3.40 3.50 3.50 3.55 3.60 3.55 3.40 3.20 3.00Aluminium US$/ lb 1.04 0.89 0.92 0.94 0.95 0.96 0.98 1.00 0.99 0.95 0.93 0.92 0.93 0.93Lead US$/ lb 0.96 0.77 0.84 0.88 0.92 0.96 0.98 1.00 1.01 1.02 1.00 0.98 0.96 0.94Nickel US$/ lb 11.32 8.50 8.80 9.10 9.30 9.50 9.80 10.00 10.00 9.70 9.40 9.10 8.80 8.50Zinc US$/ lb 1.06 0.80 0.85 0.90 0.94 0.98 1.00 1.02 1.05 1.05 1.02 1.00 0.98 0.96Gold US$/oz 1,113 1,210 1,190 1,160 1,130 1,100 1,070 1,050 1,050 1,060 1,080 1,100 1,100 1,070Silver US$/oz 17.5 17.9 18.0 17.8 17.5 17.2 17.0 16.7 16.9 17.1 17.7 17.5 17.5 17.0Platinum US$/oz 1,644 1,550 1,566 1,611 1,614 1,594 1,574 1,544 1,522 1,514 1,521 1,528 1,528 1,466WTI Crude US$/bbl 84 75 80 85 85 88 90 95 98 100 102 105 105 102Iron Ore Fines US$/t 60 120 150 145 155 160 160 155 150 145 140 135 130 120Iron Ore Lump US$/t 72 135 160 155 165 170 170 165 160 155 150 145 140 130Premium Coking Coal US$/t 128 200 225 240 260 260 270 270 260 255 250 245 240 240Steaming Coal US$/t 70 98 98 98 98 120 120 120 120 130 130 130 130 125Alumina US$/t 335 284 289 296 304 300 302 304 301 283 277 274 277 277Uranium US$/ lb 42 40 42 45 48 52 55 58 60 63 65 65 62 60A$/US$ US$ 0.92 0.84 0.88 0.90 0.92 0.94 0.94 0.92 0.90 0.88 0.86 0.84 0.75 0.74

Average Mar-10 J un-10 Sep-10 Dec-10 Mar-11 J un-11 Sep-11 Dec-11 Mar-12 J un-12 Sep-12 Dec-12 Mar-13 J un-13unit

Copper US$/ lb 3.29 3.21 3.00 3.15 3.25 3.35 3.45 3.50 3.53 3.58 3.58 3.48 3.30 3.10Aluminium US$/ lb 0.98 0.97 0.91 0.93 0.95 0.96 0.97 0.99 1.00 0.97 0.94 0.93 0.93 0.93Lead US$/ lb 1.00 0.87 0.81 0.86 0.90 0.94 0.97 0.99 1.01 1.02 1.01 0.99 0.97 0.95Nickel US$/ lb 9.10 9.91 8.65 8.95 9.20 9.40 9.65 9.90 10.00 9.85 9.55 9.25 8.95 8.65Zinc US$/ lb 1.04 0.93 0.83 0.88 0.92 0.96 0.99 1.01 1.04 1.05 1.04 1.01 0.99 0.97Gold US$/oz 1,110 1,162 1,200 1,175 1,145 1,115 1,085 1,060 1,050 1,055 1,070 1,090 1,100 1,085Silver US$/oz 16.9 17.7 18.0 17.9 17.7 17.4 17.1 16.8 16.8 17.0 17.4 17.6 17.5 17.2Platinum US$/oz 1,565 1,597 1,558 1,588 1,613 1,604 1,584 1,559 1,533 1,518 1,518 1,524 1,528 1,497WTI Crude US$/bbl 79 79 78 83 85 87 89 93 97 99 101 104 105 104Iron Ore Fines US$/t 60 120 150 145 155 160 160 155 150 145 140 135 130 120Iron Ore Lump US$/t 72 135 160 155 165 170 170 165 160 155 150 145 140 130Premium Coking Coal US$/t 128 200 225 240 260 260 270 270 260 255 250 245 240 240Steaming Coal US$/t 70 98 98 98 98 120 120 120 120 130 130 130 130 125Alumina US$/t 325 308 285 293 302 299 299 301 303 289 280 275 275 277Uranium US$/ lb 42 41 41 44 47 50 54 57 59 62 64 65 64 61A$/US$ US$ 0.90 0.88 0.86 0.89 0.91 0.93 0.94 0.93 0.91 0.89 0.87 0.85 0.80 0.75

27

Appendix: ANZ annual commodity price forecasts

Source: Bloomberg, ANZ

End of Period 2003 2004 2005 2006 2007 2008 2009 2010F 2011F 2012F 2013F 2014F 2015F LTunit

Copper US$/ lb 1.05 1.48 2.06 2.86 3.01 1.38 3.33 3.20 3.50 3.40 2.80 2.20 2.30 2.30Aluminium US$/ lb 0.72 0.89 1.03 1.28 1.07 0.68 1.00 0.94 1.00 0.92 0.94 0.98 1.00 1.00Lead US$/ lb 0.33 0.47 0.49 0.77 1.15 0.46 1.09 0.88 1.00 0.98 0.90 0.79 0.80 0.80Nickel US$/ lb 7.52 6.75 6.07 15.43 11.80 5.27 8.37 9.10 10.00 9.10 8.00 7.30 7.50 7.50Zinc US$/ lb 0.46 0.57 0.86 1.95 1.07 0.54 1.15 0.90 1.02 1.00 0.93 0.84 0.85 0.85Gold US$/oz 417 438 513 635 834 882 1,097 1,160 1,050 1,100 1,030 880 750 750Silver US$/oz 6.0 6.8 8.8 12.9 14.8 11.4 16.9 17.8 16.7 17.5 16.5 14.4 12.5 12.5Platinum US$/oz 814 860 965 1,118 1,526 935 1,466 1,611 1,544 1,528 1,411 1,173 1,000 1,000WTI Crude US$/bbl 33 43 61 61 96 45 79 85 95 105 95 84 85 85Iron Ore Fines US$/t 20 23 39 47 51 92 60 145 155 135 115 100 80 80Iron Ore Lump US$/t 25 29 50 59 65 128 72 155 165 145 125 105 90 90Premium Coking Coal US$/t 46 58 127 114 98 305 128 240 270 245 230 180 150 150Steaming Coal US$/t 27 45 53 53 56 125 70 98 120 130 125 115 90 90Alumina US$/t 340 405 585 205 360 225 305 296 304 274 280 292 300 300Uranium US$/ lb 14 21 36 72 90 54 45 45 58 65 58 52 50 50A$/US$ US$ 0.75 0.78 0.73 0.79 0.80 0.69 0.90 0.90 0.92 0.84 0.74 0.72 0.72 0.72

Average 2003 2004 2005 2006 2007 2008 2009F 2010F 2011F 2012F 2013F 2014F 2015F LTunit

Copper US$/ lb 0.81 1.30 1.67 3.06 3.24 3.16 2.34 3.16 3.39 3.54 3.05 2.45 2.29 2.30Aluminium US$/ lb 0.65 0.78 0.86 1.17 1.20 1.17 0.76 0.95 0.97 0.96 0.93 0.96 1.00 1.00Lead US$/ lb 0.23 0.40 0.44 0.58 1.17 0.95 0.78 0.88 0.95 1.01 0.94 0.84 0.80 0.80Nickel US$/ lb 4.37 6.28 6.71 10.96 16.87 9.58 6.65 9.15 9.54 9.66 8.51 7.66 7.48 7.50Zinc US$/ lb 0.38 0.48 0.63 1.48 1.48 0.85 0.75 0.92 0.97 1.03 0.96 0.89 0.85 0.85Gold US$/oz 364 410 445 604 697 873 973 1,162 1,101 1,066 1,071 956 821 750Silver US$/oz 4.9 6.7 7.3 11.6 13.4 15.0 14.7 17.6 17.2 17.2 17.1 15.5 13.5 12.5Platinum US$/oz 693 847 899 1,142 1,305 1,577 1,208 1,577 1,590 1,523 1,475 1,288 1,092 1,000WTI Crude US$/bbl 31 41 56 66 72 100 63 80 88 100 102 88 85 85Iron Ore Fines US$/t 19 22 35 45 50 81 68 119 158 143 120 105 88 80Iron Ore Lump US$/t 24 28 45 57 64 112 86 130 168 153 130 108 101 90Premium Coking Coal US$/t 47 55 110 117 102 253 172 198 265 253 235 196 165 150Steaming Coal US$/t 28 40 51 53 55 108 84 91 115 128 126 118 101 90Alumina US$/t 272 404 452 444 342 370 243 303 300 287 277 286 299 300Uranium US$/ lb 11 18 28 48 99 64 47 42 52 62 61 60 71 50A$/US$ US$ 0.65 0.74 0.76 0.75 0.84 0.85 0.79 0.88 0.93 0.88 0.76 0.72 0.72 0.72

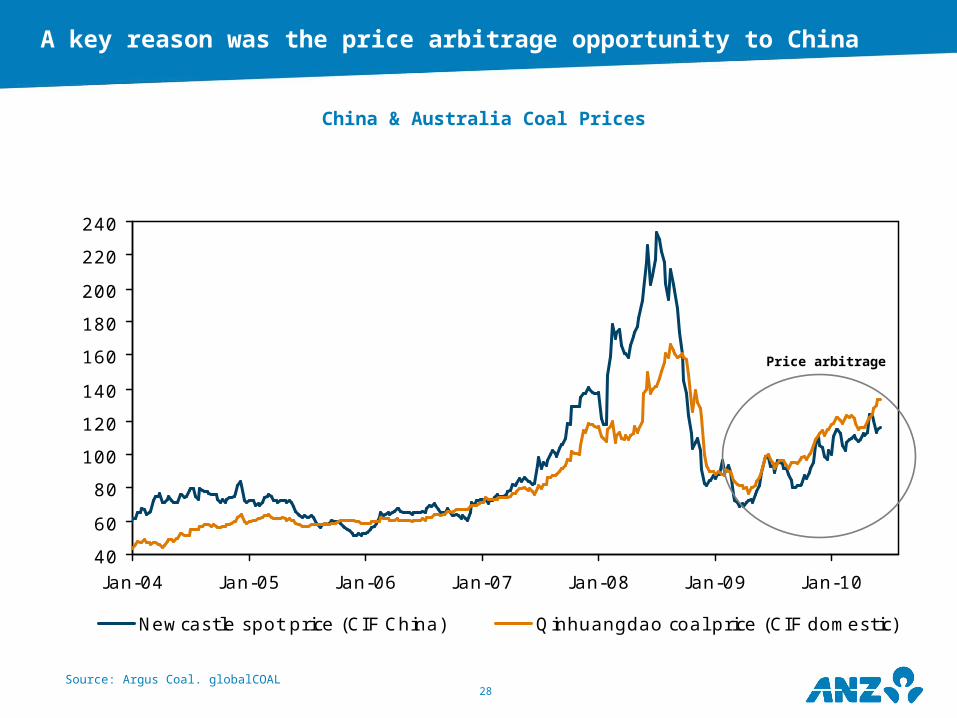

28

40

60

80

100

120

140

160

180

200

220

240

Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Newcastle spot price (CIF China) Qinhuangdao coal price (CIF domestic)

US$/tonne

Source: Argus Coal. globalCOAL

China & Australia Coal Prices

A key reason was the price arbitrage opportunity to China

Price arbitrage

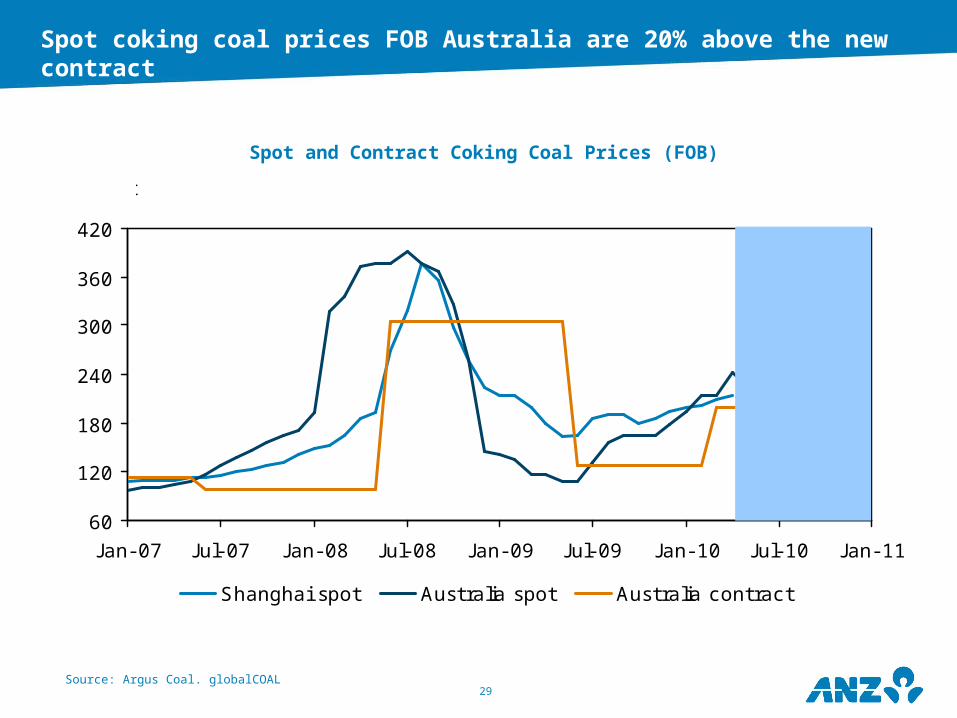

29

60

120

180

240

300

360

420

J an- 07 J ul- 07 J an- 08 J ul- 08 J an- 09 J ul- 09 J an- 10 J ul- 10 J an- 11

Shanghai spot Australia spot Australia contract

US$/t

Source: Argus Coal. globalCOAL

Spot and Contract Coking Coal Prices (FOB)

Spot coking coal prices FOB Australia are 20% above the new contract

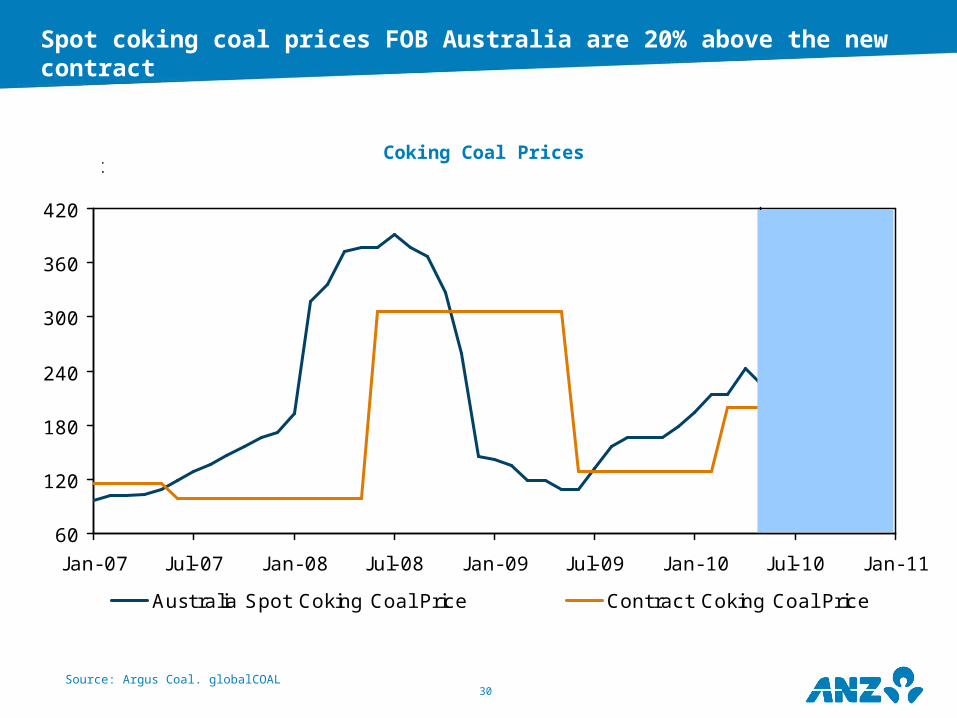

30

60

120

180

240

300

360

420

J an- 07 J ul- 07 J an- 08 J ul- 08 J an- 09 J ul- 09 J an- 10 J ul- 10 J an- 11

Australia Spot Coking Coal Price Contract Coking Coal Price

US$/t

ANZ forecast - 240

J SM annoucement225

forecast

Source: Argus Coal. globalCOAL

Coking Coal Prices

Spot coking coal prices FOB Australia are 20% above the new contract

31Source: AME, Clarksons, ANZ

New Bulk Fleet Shipping Capacity

Low freight rates should spur stronger seaborne coal demand in 2010

0

20

40

60

80

100

120

98 99 00 01 02 03 04 05 06 07 08 09F 10F 11F 12F

Capesize Panamax Handymax Handysize

million dwt

32Source: globalCOAL, Bloomberg

Coal, Oil Prices & Freight Rates

Coal and oil price correlation improving

0

20

40

60

80

100

120

140

160

180

200

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-100

2,000

4,000

6,000

8,000

10,000

12,000

14,000

Newcastle Thermal Coal FOB Baltic Freight Rate (RHS)

US$/tonne pointsCoal Price & Freight Rates

0

20

40

60

80

100

120

140

160

180

200

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-100

20

40

60

80

100

120

140

160

Newcastle Thermal Coal FOB WTI Oil Price (RHS)

US$/tonne Coal Price & Oil Price US$/bbl

(1.0)

(0.8)

(0.6)

(0.4)

(0.2)

0.0

0.2

0.4

0.6

0.8

1.0

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Newcastle FOB/WTI 12mth rolling correlation

Correlation coefficient Oil Price Correlation

(1.0)

(0.8)

(0.6)

(0.4)

(0.2)

0.0

0.2

0.4

0.6

0.8

1.0

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

Newcastle FOB/Baltic 12mth rolling correlation

Correlation coefficient Freight Rate Correlation

33

0

20

40

60

80

100

120

140

160

00 01 02 03 04 05 06 07 08 09 10F 11F 12F 13F 14F 15F-10%

0%

10%

20%

30%

40%

50%

60%

Thermal Imports Coking Imports % Thermal % Coking

m tonnes

India Thermal Coal & Coking Coal Imports

Source: AME, Wood Mackenzie, ANZ

XXX

Forecast

34

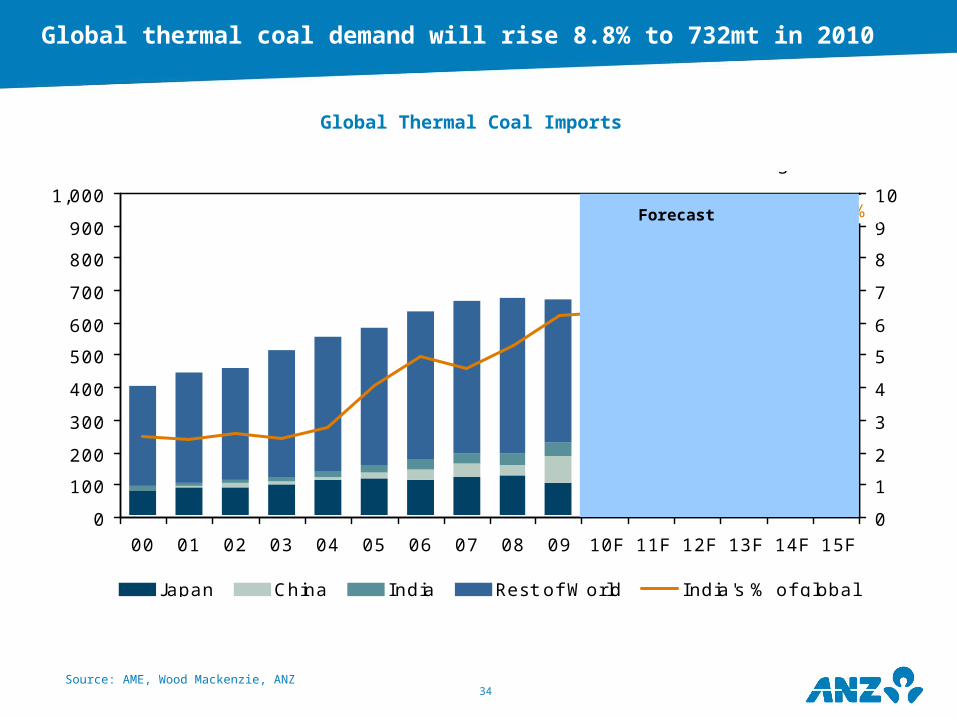

0

100

200

300

400

500

600

700

800

900

1,000

00 01 02 03 04 05 06 07 08 09 10F 11F 12F 13F 14F 15F0

1

2

3

4

5

6

7

8

9

10

Japan China India Rest of World India's % of global

% global sharem tonnes

6%

9%

Source: AME, Wood Mackenzie, ANZ

Global Thermal Coal Imports

Forecast

Global thermal coal demand will rise 8.8% to 732mt in 2010

35

0

50

100

150

200

250

300

350

400

00 01 02 03 04 05 06 07 08 09 10F 11F 12F 13F 14F 15F0

2

4

6

8

10

12

14

16

18

20

Japan China India Rest of the World China's % of global

m tonnes % global share

14%

19%

Source: AME, ANZ

Global Coking Coal Imports

Forecast

Global metallurgical coal demand will jump 14.2% in 2010

36Source: Bloomberg

Newcastle Port Shipment Destinations

Newcastle selling more to China

2006

J apan55%

S Korea13%

Malaysia2%

Taiwan14%

Other2%

China (PR)3%

India3%

EU2%

Mexico6% 2007

J apan56%

S Korea10%

Malaysia2%

Taiwan14%

Mexico6%EU

3%India3%

China (PR)3%

Other3%

2008

J apan61%

S Korea14%

Malaysia1%

Taiwan14%

Mexico1%

EU2%

India3%

China (PR)1%

Other3%

2009

J apan55%

S Korea17%

Malaysia1%

Taiwan10%

Other2%

China (PR)9%

India1%

EU2%

Mexico3%

37

•This document (“document”) is distributed to you in Australia and the United Kingdom by Australia and New Zealand Banking Group Limited ABN 11 005 357 522 (“ANZ”) and in New Zealand by ANZ National Bank Limited (“ANZ NZ”). ANZ holds an Australian Financial Services licence no. 234527 and is authorised in the UK by the Financial Services Authority (“FSA”). •This document is being distributed in the United States by ANZ Securities, Inc. (“ANZ S”) (an affiliated company of ANZ), which accepts responsibility for its content. Further information on any securities referred to herein may be obtained from ANZ S upon request. Any US person(s) receiving this document and wishing to effect transactions in any securities referred to herein should contact ANZ S, not its affiliates.•This document is being distributed in the United Kingdom by ANZ for the information of its market counterparties and intermediate customers only. It is not intended for and must not be distributed to private customers. In the UK, ANZ is regulated by the FSA. Nothing here excludes or restricts any duty or liability to a customer which ANZ may have under the UK Financial Services and Markets Act 2000 or under the regulatory system as defined in the Rules of the FSA.•This document is issued on the basis that it is only for the information of the particular person to whom it is provided. This document may not be reproduced, distributed or published by any recipient for any purpose. This document does not take into account your personal needs and financial circumstances. Under no circumstances is this document to be used or considered as an offer to sell, or a solicitation of an offer to buy.•In addition, from time to time ANZ, ANZ NZ, ANZ S, their affiliated companies, or their respective associates and employees may have an interest in any financial products (as defined by the Australian Corporations Act 2001), securities or other investments, directly or indirectly the subject of this document (and may receive commissions or other remuneration in relation to the sale of such financial products, securities or other investments), or may perform services for, or solicit business from, any company the subject of this document. If you have been referred to ANZ, ANZ NZ, ANZ S or their affiliated companies by any person, that person may receive a benefit in respect of any transactions effected on your behalf, details of which will be available upon request.•The information herein has been obtained from, and any opinions herein are based upon, sources believed reliable. The views expressed in this document accurately reflect the author’s personal views, including those about any and all of the securities and issuers referred to herein. The author however makes no representation as to its accuracy or completeness and the information should not be relied upon as such. All opinions and estimates herein reflect the author’s judgement on the date of this document and are subject to change without notice. No part of the author's compensation was, is or will directly or indirectly relate to specific recommendations or views expressed about any securities or issuers in this document. ANZ, ANZ NZ, ANZ S, their affiliated companies, their respective directors, officers, and employees disclaim any responsibility, and shall not be liable, for any loss, damage, claim, liability, proceedings, cost or expense (“Liability”) arising directly or indirectly (and whether in tort (including negligence), contract, equity or otherwise) out of or in connection with the contents of and/or any omissions from this communication except where a Liability is made non-excludable by legislation.•Where the recipient of this publication conducts a business, the provisions of the Consumer Guarantees Act 1993 (NZ) shall not apply..

Important NoticeAustralia and New Zealand Banking Group Limited is represented in:AUSTRALIA by:Australia and New Zealand Banking Group Limited ABN 11 005 357 52210th Floor 100 Queen Street, Melbourne 3000, AustraliaTelephone +61 3 9273 6224 Fax +61 3 9273 5711UNITED KINGDOM by:Australia and New Zealand Banking Group LimitedABN 11 005 357 52240 Bank Street, Canary Wharf, London, E14 5EJ, United KingdomTelephone +44 20 3229 2121 Fax +44 20 7378 2378

UNITED STATES OF AMERICA by:ANZ Securities, Inc. (Member of NASD and SIPC)6th Floor 1177 Avenue of the AmericasNew York, NY 10036, United States of AmericaTel: +1 212 801 9160 Fax: +1 212 801 9163NEW ZEALAND by:ANZ National Bank LimitedLevel 7, 1-9 Victoria Street, Wellington, New ZealandTelephone +64 4 802 2000

Disclaimer