Embed Size (px)

Citation preview

08/13/2013

1

©2013 Foley & Lardner LLP • Attorney Advertising • Prior results do not guarantee a similar outcome • Models used are not clients but may be representative of clients • 321 N. Clark Street, Suite 2800, Chicago, IL 60654 • 312.832.4500

1

For audio participation, dial 800.311.0799 and enter conference ID 234306.

©2013 Foley & Lardner LLP

2

Anti-Corruption Enforcement Trends and

Compliance in Latin America

July 30, 2013

12:00 p.m. – 1:00 p.m. CST

08/13/2013

2

©2013 Foley & Lardner LLP

3

Housekeeping Items

Call 888.569.3848 for technology assistance Dial *0 (star/zero) for audio assistance If you have any questions following the Web conference, please contact

your Foley attorney directly. Click on the Full Screen button located above the presentation slides to

maximize the presentation for full screen viewing. Click on the Download Files button located to the right of the presentation

slides to get a copy of the slides. Foley will apply for CLE credit after the Web conference. If you did not

supply your CLE information upon registration, please e-mail it to [email protected].

NOTE: Those seeking Kansas, New York and New Jersey CLE credit are required to complete the Attorney Affirmation Form. A 4-digit code will be announced during the presentation. Email the code to [email protected] get a copy of the form. Immediately fill it out and return it after the program.

©2013 Foley & Lardner LLP

4

Today’s Speakers

Francisco J. Cerezo Jaime B. Guerrero

08/13/2013

3

©2013 Foley & Lardner LLP

5

Outline

1. FCPA Enforcement Activity

2. FCPA Basics Prohibitions and Essential Elements

Jurisdiction

Common Issues and Traps

3. Other Anti-Corruption Regimes

4. Anti-Corruption Compliance Assess FCPA Risk

Key Compliance Touchstones

Best Practices

©2013 Foley & Lardner LLP

6

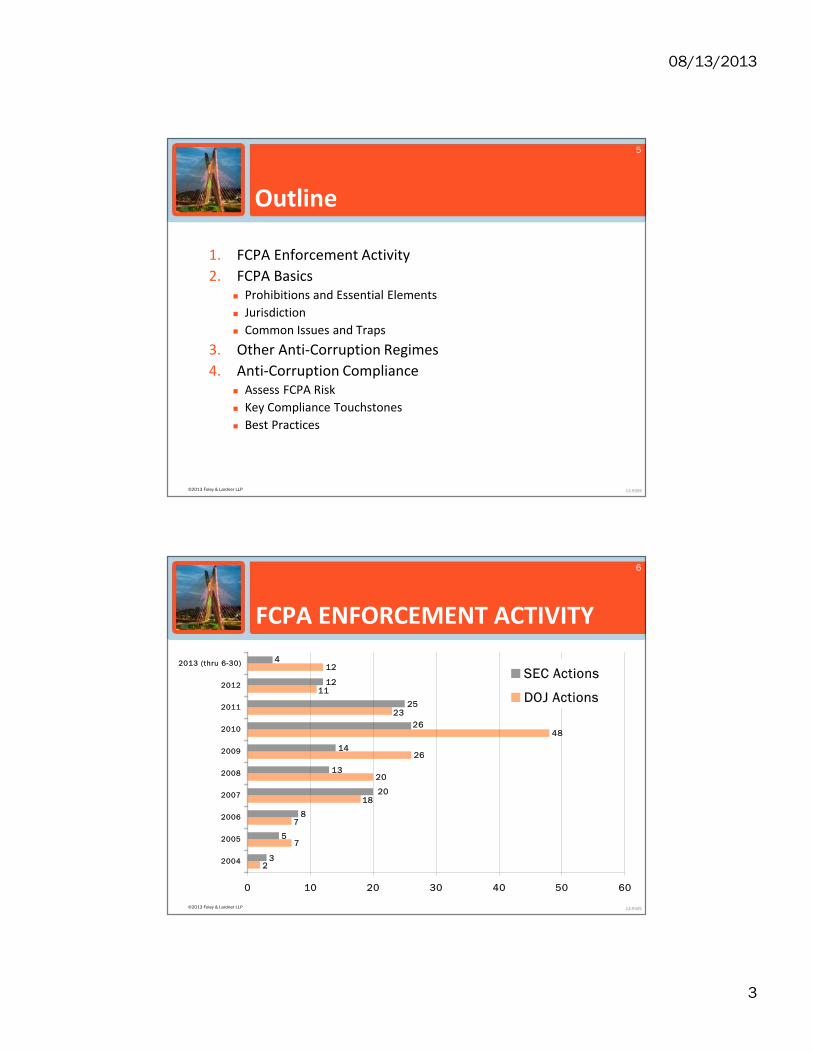

FCPA ENFORCEMENT ACTIVITY

7

20

26

48

12

3

5

8

13

14

25

12

2

7

23

11

18

4

20

26

0 10 20 30 40 50 60

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013 (thru 6-30)

SEC Actions

DOJ Actions

08/13/2013

4

©2013 Foley & Lardner LLP

7

TOP 10 FCPA-RELATED MONETARY SETTLEMENTS

$95.1

$218.8$149

$400$365$338

$185$137

$579

$800

$0

$100

$200

$300

$400

$500

$600

$700

$800

$900

Siemens

( 2008)

H al l iburton /

KBR (2009)

Alcatel -

Lucent

(2010)

Daimler

( 2010)

Techn ip

( 2010)

Snamprogetti

/ ENI (2010)

BAE ( FCPA-

related)

( 2010)

Deutsche

Telekom

( 2011)

Jeff rey Tesler

(2011)

JGC (2011)

in Mill ions

Largest FCPA Settlements (Combined Penalties/Disgorgement)

2008

2009

2010

2011

©2013 Foley & Lardner LLP

8

Where the FCPA Enforcement Action Is:

Country 2010-2011 Totals 2012 TOTALArgentina 2 3 5Brazil 2 3 5China 13 11 24Costa Rica 7 - 7Croatia 3 4 7Greece 7 3 10Honduras 9 - 9India 3 3 6Indonesia 9 3 12Iraq 18 - 18Kazakhstan 6 2 8Kyrgyzstan 8 - 8Mexico 10 4 14Nigeria 25 2 27Poland 3 3 6Russia 5 3 8Saudi Arabia 2 4 6Serbia 1 3 4Thailand 9 2 11U.A.E. 2 3 5Vietnam 9 - 9

Countries Implicated Most Frequently in Enforcement Actions2010 – 2011 vs. 2012*

*Approximate numbers

08/13/2013

5

©2013 Foley & Lardner LLP

9

9

CORRUPTION PERCEPTION INDEX (CPI) (2012)

©2013 Foley & Lardner LLP

10

2012 CPI Scores and Rankings of Sample Latin American Countries

Venezuela – score 19, rank 165/174 Honduras – score 28, rank 133/174 Ecuador – score 32, rank 118/174 Dominican Republic – score 32, rank 118/174 Mexico – score 34, rank 105/174 Argentina – score 35, rank 102/175 Colombia – score 36, rank 94/174 Peru – score 38, rank 83/174 Brazil – score 43, rank 69/174 Costa Rica – score 54, rank 48/174 Chile – score 72, rank 20/174

08/13/2013

6

©2013 Foley & Lardner LLP

11

Enforcement in Latin America

Number of FCPA prosecutions with a Latin America component is increasing.

– Indications that government regulators are taking a hard look at alleged violations of the FCPA in Latin America.

In 2010 and 2011, the DOJ disclosed approximately 44 FCPA and related enforcement actions.

– Of the 44 actions, 14 (32%) had a Latin America component, with affected countries including but not limited to Argentina, Brazil, Costa Rica, Honduras, Mexico, and Nicaragua.

FCPA ENFORCEMENT ACTIVITY

©2013 Foley & Lardner LLP

12

RECENT FCPA ENFORCEMENTIN LATIN AMERICA

BizJet International– Charged in 2012 with bribing Mexican, Panamanian, and

Brazilian government officials from 2004-2010 to obtain aircraft maintenance contracts.

– The officials demanded the bribes (including cash payments of $30,000-40,000) as “commissions” for awarding of the contracts.

– Many bribes paid through a shell company.

– Bizjet paid $11.8 million criminal penalty in exchange for deferred prosecution agreement (“DPA”). Voluntary disclosure and cooperation noted in reducing penalty.

– Bizjet executives were also charged – sentenced to eight months home detention in exchange for cooperation.

08/13/2013

7

©2013 Foley & Lardner LLP

13

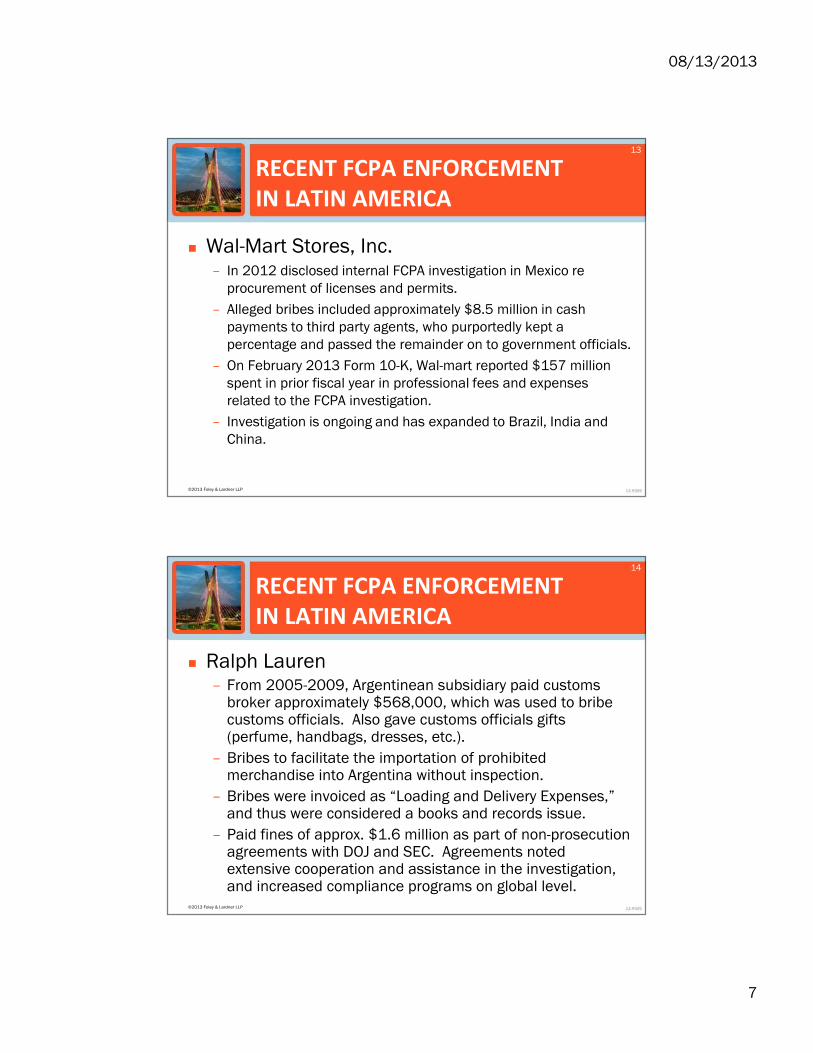

RECENT FCPA ENFORCEMENTIN LATIN AMERICA

Wal-Mart Stores, Inc.– In 2012 disclosed internal FCPA investigation in Mexico re

procurement of licenses and permits.

– Alleged bribes included approximately $8.5 million in cash payments to third party agents, who purportedly kept a percentage and passed the remainder on to government officials.

– On February 2013 Form 10-K, Wal-mart reported $157 million spent in prior fiscal year in professional fees and expenses related to the FCPA investigation.

– Investigation is ongoing and has expanded to Brazil, India and China.

©2013 Foley & Lardner LLP

14

RECENT FCPA ENFORCEMENTIN LATIN AMERICA

Ralph Lauren– From 2005-2009, Argentinean subsidiary paid customs

broker approximately $568,000, which was used to bribe customs officials. Also gave customs officials gifts (perfume, handbags, dresses, etc.).

– Bribes to facilitate the importation of prohibited merchandise into Argentina without inspection.

– Bribes were invoiced as “Loading and Delivery Expenses,” and thus were considered a books and records issue.

– Paid fines of approx. $1.6 million as part of non-prosecution agreements with DOJ and SEC. Agreements noted extensive cooperation and assistance in the investigation, and increased compliance programs on global level.

08/13/2013

8

©2013 Foley & Lardner LLP

15

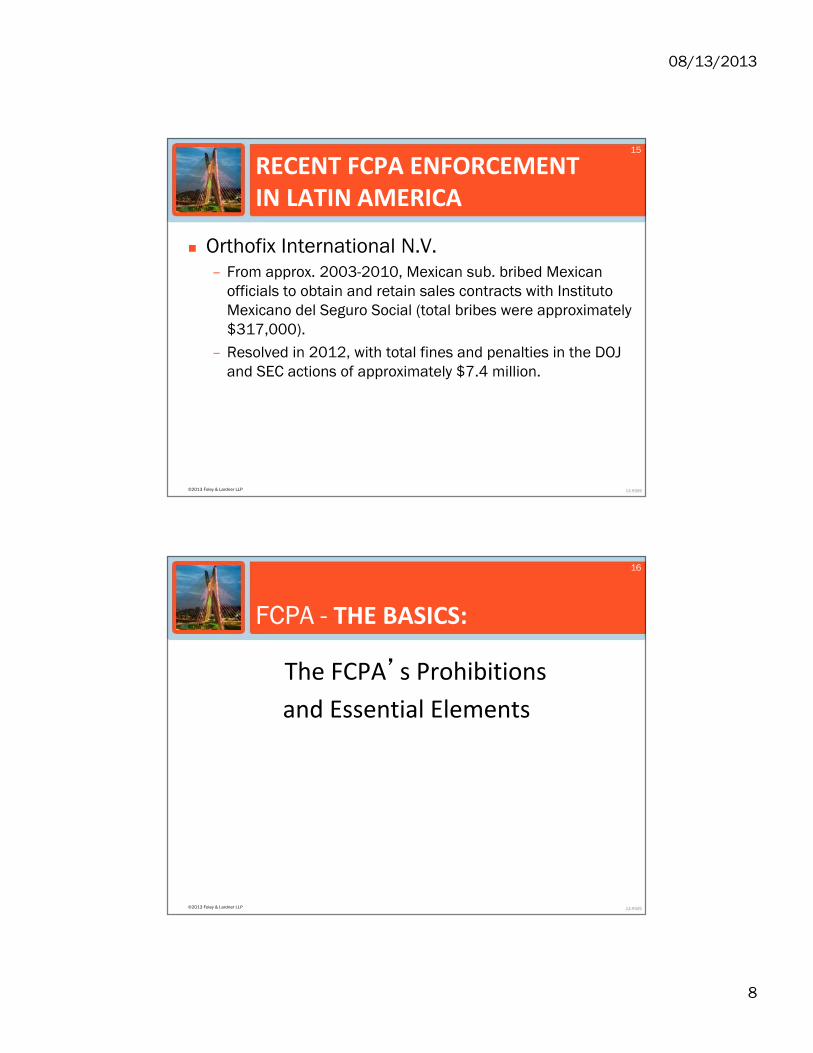

Orthofix International N.V.– From approx. 2003-2010, Mexican sub. bribed Mexican

officials to obtain and retain sales contracts with Instituto Mexicano del Seguro Social (total bribes were approximately $317,000).

– Resolved in 2012, with total fines and penalties in the DOJ and SEC actions of approximately $7.4 million.

RECENT FCPA ENFORCEMENTIN LATIN AMERICA

©2013 Foley & Lardner LLP

16

FCPA - THE BASICS:

The FCPA’s Prohibitions

and Essential Elements

08/13/2013

9

©2013 Foley & Lardner LLP

17

TWO MAIN COMPONENTS:

Anti-Bribery Provisions

Books and Records and Internal Control Provisions

©2013 Foley & Lardner LLP

18

ANTI-BRIBERY PROVISIONS

Apply to:– Domestic concerns (“private” companies, LLC’s, etc., and U.S.

citizens);

– Issuers (basically, “public” companies); and

– Any person who, while in the U.S., commits an improper act

Including non-U.S. citizens

Covers payments made by third parties with “knowledge” that the payment would be used to fund FCPA-illegal activity

Extra-territorial jurisdiction

08/13/2013

10

©2013 Foley & Lardner LLP

19

WHAT IS PROHIBITED?

Paying or offering to pay “anything of value”

Directly or indirectly

To a “foreign official,” or to any other person

“while knowing” that all or part of the thing of

value will be paid or offered to a foreign official

Corruptly

For the purpose of influencing the official in some

official act or to secure any improper advantage

In order to “obtain or retain business”

©2013 Foley & Lardner LLP

20

“ANYTHING OF VALUE”

Examples: Cash or a cash equivalent Gifts Travel expenses and/or

payment of personal expenses

Services Golf outings or other

entertainment Charitable donations Medical treatment Loans Jobs for relatives

08/13/2013

11

©2013 Foley & Lardner LLP

21

FOREIGN OFFICIAL?

©2013 Foley & Lardner LLP

22

“FOREIGN OFFICIAL”

Any officer or employee of a foreign government or any department, agency, or instrumentality thereof

– DOJ interprets instrumentality to include employees of state owned or controlled enterprises (“SOEs”)

– No distinction made as to rank or title

U.S. v. Esquinazi – “foreign official” challenge pending before 11th Circuit Court of Appeals

– Conviction premised on bribes paid to employees of Haiti Teleco, a state-owned telephone utility

08/13/2013

12

©2013 Foley & Lardner LLP

23

“OBTAIN OR RETAIN BUSINESS”

“Business Purpose” Test– Includes payments related to the renewal of

contracts, the execution or performance of contracts, or the retention of existing business

Examples from DOJ/SEC:– Winning a contact– Influencing procurement process– Circumventing import rules– Gaining access to non-public bid tender– Evading taxes or penalties– Influencing enforcement actions or litigation– Obtaining exceptions to regulations– Avoiding contract termination

©2013 Foley & Lardner LLP

24

Jurisdiction

DOJ and SEC have taken an expansive view of jurisdiction under the FCPA

Parties subject to the FCPA include:

– Domestic concerns and U.S. persons

Including U.S. subsidiaries of foreign corporations

– Issuers

– Officers, directors, employees, or agents of an Issuer or domestic concern

– Any person that violates the FCPA within the territory of the United States

08/13/2013

13

©2013 Foley & Lardner LLP

25

Jurisdiction Based on Acts Committed on U.S. Soil

Based on illegal acts that take place on U.S. soil

– Relevant parts of conspiracy take place on U.S. soil

– SHOT Show

Based on making payments to foreign officials that make use of U.S. financial institutions or mails

– Make use of U.S. banks or wire transfers

– Panalpina

– Halliburton/KBR

©2013 Foley & Lardner LLP

26

EXCEPTIONS & AFFIRMATIVE DEFENSES

Affirmative Defenses– Written local law

Custom is not the same as written laws and regulations

– Facilitating payments Emerging “best practice”– prohibition of

facilitating payments except where the health and safety of an employee is involved

08/13/2013

14

©2013 Foley & Lardner LLP

27

EXCEPTIONS & AFFIRMATIVE DEFENSES

Reasonable and bona fide expenditures

Directly related to – The promotion or demonstration of product or

services or

– The negotiation, execution or performance of a contract

Examples:– Travel and expenses to visit company facilities

– Travel and expenses for training

– Travel and expenses for meetings

©2013 Foley & Lardner LLP

28

PENALTIES FOR VIOLATING ANTI-BRIBERY PROVISIONS

Criminal Penalties (Knowing/Willful Blindness)– Business Entities: Up to $2 million per violation.– Individuals: Up to $100‚000 and/or receive prison sentences of up to 5 years. – Alternative Fines: U.S. law authorizes alternative maximum fines equal to the greater

of twice the gross gain or twice the gross loss to the extent a criminal offense causes a pecuniary gain or loss.

Civil Penalties– Business Entities & Individuals: Up to $10‚000.– Additional Fines: In an SEC enforcement action‚ the court may impose an additional

fine not to exceed the greater of (i) the gross amount of the pecuniary gain to the defendant as a result of the violation‚ or (ii) a specified dollar limit ranging from $5‚000 to $100‚000 for a natural person and $50‚000 to $500‚000 for business entities.

Disgorgement

08/13/2013

15

©2013 Foley & Lardner LLP

29

OVERVIEW OF ACCOUNTING AND INTERNAL CONTROLS PROVISIONS

Only apply to “issuers” (publicly traded companies or companies which have reporting requirements with the SEC).

Must maintain accurate books and records that reflect in reasonable detail‚ accurately and completely‚ transactions and asset dispositions.

Must establish effective systems of internal accounting controls.

GAAP standard.

Accounting controls apply to foreign affiliates and JV partners depending on the issuer's voting power (discussed below).

You don’t need any evidence of a bribe in order for a books and records violation to occur.

Unrecorded facilitating payment will violate the books and records provisions of the FCPA even though they qualify under an exemption in the anti-bribery section of the FCPA.

©2013 Foley & Lardner LLP

30

PENALTIES FOR ACCOUNTING AND INTERNAL CONTROLS VIOLATIONS

Criminal Penalties (Knowing/Willful)– Business Entities: Fines up to $25 million per willful violation.– Individuals: Fines up to $5 million and/or prison sentences of up to

20 years for willful violations.– Additional Fines: In an SEC enforcement action‚ the court may

impose an additional fine not to exceed the greater of (i) the gross amount of the pecuniary gain to the defendant as a result of the violation‚ or (ii) a specified dollar limitation ranging from $5‚000 to $100‚000 for a natural person and $50‚000 to $500‚000 for business entities.

Civil Penalties– Business Entities: Penalties of up to $500‚000.– Individuals: Penalties of up to $50‚000.

08/13/2013

16

©2013 Foley & Lardner LLP

31

COMMON ISSUES: THE PERILS OF HOSTING CUSTOMER VISITS

©2013 Foley & Lardner LLP

32

COMMON ISSUES: GIFTS, MEALS & ENTERTAINMENT

Companies may provide meals and entertainment, if in good faith, without corrupt intent, and with no expectation of a favor

Must be directly related to legitimate business purpose

Must be reasonable in value

Best practices:– Should be in accordance with generally accepted

business standards

– No cash or equivalents– Company personnel should be in attendance– Should be properly documented

08/13/2013

17

©2013 Foley & Lardner LLP

33

COMMON ISSUES: GIFTS, MEALS & ENTERTAINMENT

“A small gift or token of esteem or gratitude is often an appropriate way for business people to display respect for each other. Some hallmarks of appropriate gift giving are when the gift is given openly and transparently, properly recorded in the giver’s books and records, provided only to reflect esteem or gratitude, and permitted under local law.”

-- U.S. SEC and U.S. DOJ FCPA Resource Guide

©2013 Foley & Lardner LLP

34

CUSTOMER VISITS

Questions to Ask:

Are any of the visitors “foreign officials” under the FCPA’s broad definition of that term?

Is the entire trip for the purpose of promoting the company’s products or services or in connection with the execution or performance of a contract?

Are the proposed expenses proportionate and reasonable in relation to the company’s business purpose for inviting the foreign officials?

How are the foreign official’s expenses being paid?

Who within the company is approving the trip? Is that person sensitive to FCPA issues?

Are the expenses accurately described and recorded on the company’s books and records?

08/13/2013

18

©2013 Foley & Lardner LLP

35

THIRD-PARTY INTERMEDIARIES

Willful Blindness = Knowledge

©2013 Foley & Lardner LLP

36

COMMON ISSUES: THIRD-PARTY INTERMEDIARIES

FCPA expressly prohibits improper payments made through third parties

The majority of recent enforcement actions have involved improper payments made through third-parties

Regulators do not need to prove that the third-party acted on the company’s direct orders or even that a company actually knew the intermediary engaged in prohibited conduct– Most enforcement actions have involved allegations of

actual knowledge, however

– Willful blindness constitutes knowledge

08/13/2013

19

©2013 Foley & Lardner LLP

37

THIRD-PARTY INTERMEDIARIES

Eli Lilly (2012)– $29 million SEC settlement

– Various payments made by agents and distributors in China, Russia, Brazil, Poland

– According to SEC:

“Eli Lilly and its subsidiaries possessed a ‘check the box’mentality when it came to third-party due diligence. Companies can’t simply rely on paper-thin assurances by employees, distributors, or customers. They need to look at the surrounding circumstances of any payment to adequately assess whether it could wind up in a government official’s pocket.”

©2013 Foley & Lardner LLP

38

THIRD-PARTY INTERMEDIARIES

Oracle (2012)

– $2 million SEC settlement

– India subsidiary and distributors

– NO ALLEGATION OF BRIBES ACTUALLY PAID

Just a claim that “slush fund” could have been used to pay bribes

08/13/2013

20

©2013 Foley & Lardner LLP

39

COMMON ISSUES: ENGAGING THIRD PARTIES

Appropriate due diligence inquiry to expose any potential red flags

Suggested due diligence– Risk-based

Relationship should be memorialized in writing and contract should include:– Anticorruption reps and warranties– Audit rights

Payment mechanism should be transparent and traceable – no cash

Commission/payment should be reasonable and customary

©2013 Foley & Lardner LLP

40

COMMON ISSUES: DUE DILIGENCE FOR ENGAGING THIRD PARTIES

The following due diligence is advised:– A background check.– That third parties take FCPA training, and that they certify that they have

taken the training.– That third parties sign a certificate that they will comply with anti-

corruption and FCPA laws.– That there be an FCPA provision in the third parties’ contracts.– That they fill out questionnaires attached to the FCPA policy, including

providing references and detailed information about their business.– Representations and warranties that foreign agent is not owned or

controlled by a foreign government and that no foreign official holds an ownership interest in it.

– Annual certification of compliance with FCPA by foreign agent.

The Compliance Representatives will decide what paperwork should or needs to be filled out and whether or not that vendor is a risk.

08/13/2013

21

©2013 Foley & Lardner LLP

41

THIRD-PARTY RED FLAGS

Excessive commissions

Unreasonably large discounts

Consulting agreements that include only vaguely described services

Third-party in different line of business than that for which it was engaged

Third-party related to or closely tied to government official

©2013 Foley & Lardner LLP

42

THIRD-PARTY RED FLAGS

Third-party became involved at the express request of the foreign official

Third-party is a shell corporation incorporated in an offshore jurisdiction

Third-party requests payment to offshore bank accounts

08/13/2013

22

©2013 Foley & Lardner LLP

43

COMMON ISSUES: M&A

Many recent FCPA enforcement actions arose in context of M&A due diligence

Pfizer (2012)– Importance of pre-acquisition due diligence

Pharmacia vs. Wyeth: no attribution to Pfizer for Wyeth’s conduct versus full attribution for Pharmacia’s (entirely pre-acquisition) conduct

The difference: Pfizer’s extensive review and its efforts to integrate Wyeth into Pfizer’s internal controls

– Use of a risk-based approach to due diligence (from the Wyeth transaction)

DOJ’s apparent recognition that companies have limited resources and that extensive due diligence might not always be appropriate

Reemphasizes the importance of a basic FCPA risk assessment

©2013 Foley & Lardner LLP

44

COMMON ISSUES: M&A

Due diligence should include:

– Evaluation of target’s compliance program

– Evaluation of contractual arrangements with third parties

– Evaluation of contracts

– Evaluation of distributor and joint venture arrangements

– Red flag follow up

Plans to integrate compliance programs

08/13/2013

23

©2013 Foley & Lardner LLP

45

COMMON ISSUES: M&A

Look beyond the target’s financial statements

The existence of an improper payment – even prior to the effective date of the agreement –can expose the acquiring or partnering company to an enforcement action based upon knowledge and benefit from past payments

DOJ FCPA Opinion Procedure Release No. 08-01 (Jan. 15, 2008) establishes “best practice” due diligence steps

©2013 Foley & Lardner LLP

46

COMMON ISSUES: JOINT VENTURE

If an issuer owns more than 50% of the voting power of an affiliate or JV entity‚ it must cause such affiliate/JV entity to maintain internal accounting controls.

If an issuer owns 50% or less of the voting power of an affiliate or JV entity‚ it must make a good-faith effort to cause such affiliate/JV entity to maintain internal accounting controls.

Note: If an issuer has effective control via management structure of a joint venture it is treated as if it owns more than 50% of the voting power.

08/13/2013

24

©2013 Foley & Lardner LLP

47

UK BRIBERY ACT OF 2010

Prohibits: – Active bribery (paying bribes)

– Passive bribery (accepting bribes)

– Failure of commercial organizations to prevent bribery by “associated persons”

“Relevant commercial organisation”– Incorporated in the UK or under UK law

– Corporate entities that carries on a business or part of a business in the UK

– Affirmative defense: “Adequate procedures”

©2013 Foley & Lardner LLP

48

UK BRIBERY ACT OF 2010

Key Differences with FCPA– Bribery Act explicitly prohibits commercial bribery

– No facilitating payments exception

– No reasonable promotions exception

– “Adequate procedures” as affirmative defense, as opposed to mitigating factor

– No whistleblower incentives

– Scope of indirect knowledge: “associated persons”versus knowledge standard

– No books and records provision

08/13/2013

25

©2013 Foley & Lardner LLP

49

Global Anti-Corruption Enforcement: Parallel Actions

Global law enforcement agencies working together to investigate and prosecute bribery and corruption charges.

U.S. DOJ recently announced 56 new extradition and mutual legal assistance treaties to bolster international cooperation.

Recent U.S FCPA investigations have included parallel investigations in numerous foreign jurisdictions, including:

– Brazil (Gtech);

– China (Siemens);

– Costa Rica (Alcatel Lucent);

– France (Halliburton, Total SA);

– Germany (Bristol Myers, DaimlerChrysler, Siemens);

– Indonesia (Freeport, Monsanto, Siemens);

– Italy (Immucor, UDI, Siemens);

– Korea (IBM); and

– Nigeria (Halliburton, Siemens).

©2013 Foley & Lardner LLP

50

ASSESS FCPA RISK

Major point of emphasis by DOJ/SEC:

“DOJ and SEC will give meaningful credit to a company that implements in good faith a comprehensive, risk-based compliance program, even if that program does not prevent an infraction in a low risk area because greater attention and resources have been devoted to a higher risk area”

FCPA compliance risk is a combination of– Who (public vs. private customers)– What (large public projects vs. producing widgets)– Where (the country’s corruption reputation)– How (use of third parties)

Focus on all variables– Recent FCPA enforcement actions instruct that while

compliance efforts should focus on high-risk situations, business leaders must be alert to the risks present in all countries in all situations

08/13/2013

26

©2013 Foley & Lardner LLP

51

FCPA COMPLIANCEKEY COMPLIANCE TOUCHSTONES

Know your customers (any government agencies, any “private” entities owned or controlled by the state).

Marketing initiatives (what sort of entertainment or marketing expenses are being incurred).

“Go to market” strategies (any use of third-party agents, distributors).

Logistical issues (import/export issues, permits, licenses, certifications).

©2013 Foley & Lardner LLP

52

FCPA COMPLIANCEBEST PRACTICES

In light of ever increasing government enforcement, companies need to implement and monitor anti-corruption compliance programs.

Anti-corruption compliance programs can mitigate exposure.

Effective compliance programs can also act as a defense under the UK Bribery Act and as a mitigating factor for purposes of sentencing under the U.S. sentencing guidelines.

08/13/2013

27

©2013 Foley & Lardner LLP

53

Takeaway – Our Offer

1. Review existing Compliance Program

2. If no program in place, assist company to prepare and implement Compliance Program

3. Provide training to employees

©2013 Foley & Lardner LLP

54

Contact Information

Jaime B. Guerrero

(213) 972-4634

Francisco J. Cerezo

(305) 482-8423

08/13/2013

28

©2013 Foley & Lardner LLP

55

Thank You!

A copy of the PowerPoint presentation and a multimedia recording will be available on Foley’s website within 24 to 48 hours:

http://www.foley.com/anti-corruption-enforcement-trends-and-compliance-in-latin-america/

We welcome your feedback. Please take a few moments before you leave the web conference today to provide us with your feedback.

https://www.surveymonkey.com/s/3F9T2MT