Embed Size (px)

Citation preview

1

Incorporating Financial Results for the twelve months ended 31 December 2014

ANNUALREPORT

2

3

4

5

01 STRATEGIC REPORTFinancial Highlights 8

Galasys At a Glance 10

Products and Services 11

Chairman’s Statement 16

Chief Executive Officer’s Statement 18

Principal Risks and Uncertainties 21

02 CORPORATE GOvERnAnCEBoard of Directors 26

Directors’ Report 28

Remuneration Committee Report 32

Corporate Governance Report 34

03 FInAnCIAl STATEmEnTSIndependent Auditor’s Report to the Members of Galasys Plc 38

Consolidated Statement of Comprehensive Income 40

Consolidated Statement of Financial Position 41

Consolidated Statement of Changes in Equity 43

Consolidated Statement of Cash Flows 45

Notes to the Financial Statements 47

TABLE OFCONTENTS

6

7

8Financial Highlights

10Galasys At a Glance

11Products and Services

16Chairman’s Statement

18Chief Executive Officer’s Statement

21Principal Risks and Uncertainties

STRATEGIC REPORT

8

01 STRATEGIC REPORT

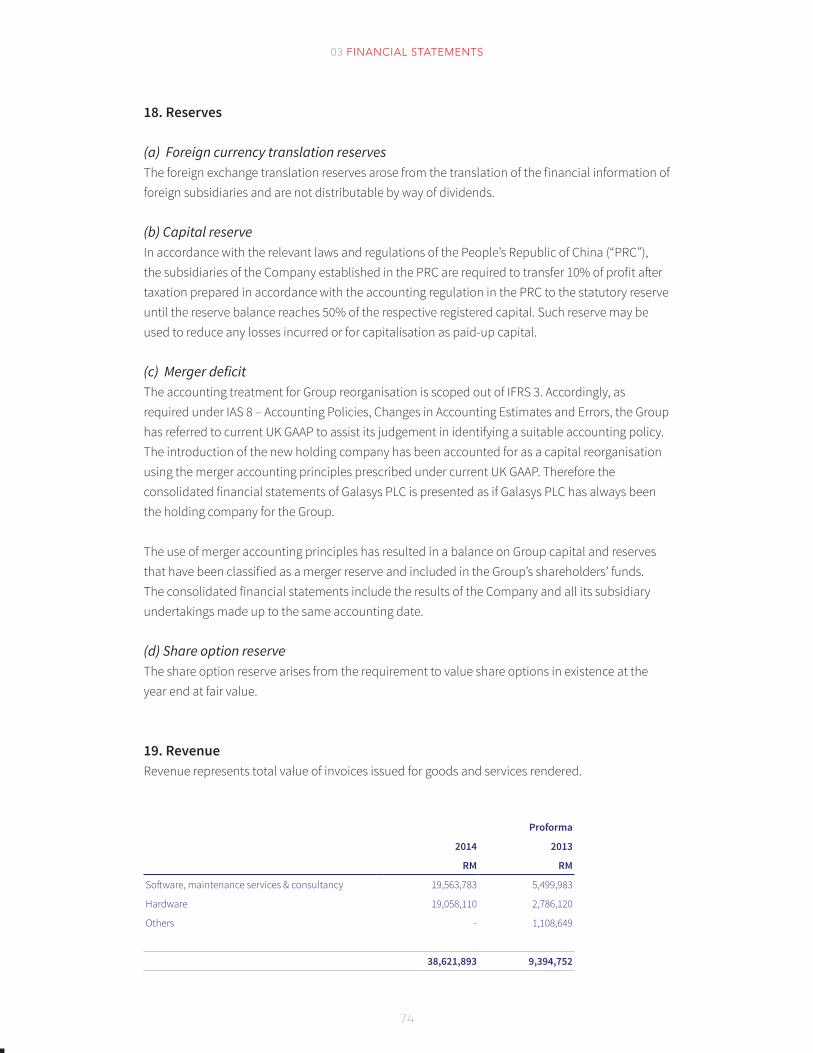

RM (GBP) ‘in millions 2014 2013 Variance %

Revenue 38.62 (7.13) 26.67 (4.92) 45%

Gross Profit 19.52 (3.60) 10.64 (1.96) 83%

PBT 11.34 (2.09) 8.38 (1.55) 35%

PAT 9.40 (1.73) 7.21 (1.33) 30%

EBITDA 12.58 (2.34) 8.50 (1.57) 48%

Cash and cash equivalents (includes net proceedsfrom IPO of c. RM10.5m) 12.22 (2.25) 2.16 (0.39) 466%

Repeat & recurring revenue 66% of Sales Revenue 60% of Sales Revenue 10%

Additional Highlights

^Earnings per share (EPS) RM 15.79 sen or GBP 2.91 pence

* The comparative figures for the 12 months to 31 December 2013 (refer to note 24) included above were on the basis that Galasys GLT (formally known as Green Laser Technology) was part of Galasys Group from 1 January 2013

^Earnings per share has been calculated by dividing the consolidated profit after taxation attributable to ordinary shareholders by the weighted average number of ordinary shares in issue during the period

Financial highlights

FINANCIALHIGHLIGHTS

2013 2014

Revenue

Gross Profit

Profit Before Tax

Profit After Tax

EBITDA

9

01 STRATEGIC REPORT

Cash and cash equivalents

2014

2013

0 2 4 6 8 10 12 14

RM in Millions

Recurring, Repeat & New Business 2013

Repeating & Recurring Revenue60%

New Business40%

Recurring, Repeat & New Business 2014

Repeating & Recurring Revenue66%

New Business34%

Software, Maintenance Services& Consultancy

51%

Hardware49%

Revenue Breakdown 2014

Revenue Breakdown 2013

Software, Maintenance Services& Consultancy

58%

Hardware30%

Others12%

10

01 STRATEGIC REPORT

GALASySAT A GLANCE

Our Story• Galasys Global (Suzhou) Co., Ltd founded in 2005• Merger with Galasys Solutions (MSC) Sdn Bhd in 2010• Acquisition of Galasys GLT Sdn Bhd in 2013• Listed on AIM, May 2014 (Galasys PLC)• Acquisition of I Logic Sdn Bhd in 2014

A leading integrated and modular amusement-park solutions and services provider to premier amusement parks in China and South East Asia

Operational Highlights• Successful AIM IPO in May 2014, raising gross proceeds of £3.10 million at a placing price of

22.5p (net proceeds of RM10.50m / £2.20m)• 46 new installed sites since IPO roadshow in April 2014• Secured various new clients including Dalian Wanda Group in China and Enchanted Kingdom

in the Philippines which are significant new wins• Extended our sales network and channels into the Philippines, Indonesia, Vietnam and the UK• Completed R&D for a number of new modules including eWallet on RFID, Mobile Ticketing,

Park Map & Navigation and Smart-Q Apps and Ticketing Redemption & Vending Kiosk• Successfully launched our Cloud Online Travel Agency (“CLOTA”) platform for theme park

ticketing• Galasys GLT (formerly Green Laser Technology) successfully integrated into the Group and

performing ahead of management expectations• Successful acquisition of ILogic Solutions Sdn Bhd (“ILogic”), a leisure and entertainment

solutions provider in Malaysia • Total staff strength increased by 40% to more than 140 as of 31 December 2014

Key strengths• Reputable clients with long-term relationships• Chimelong Group and OCT Group: >7 years• To date, 108 installed sites in Asia• Products are developed in-house• 37 software IPs registered to-date• Over 50 man-years of development time & over US$1 mil R&D• > 60% annual repeat and recurring revenue

11

01 STRATEGIC REPORT

ProPrietary SoftwareThe Group provides information technologies solutions and management services through its "Galasys Ticketing System" ("GSET"), a system developed by and continually updated within the Group to manage and analyse tickets, visitors, merchandise sales and amusement park operations. GSET is a system to manage and analyze visitors, merchandise sales and amusement-park business operations within the complex information flow. GSET can be divided into two parts: the front-end interface and back-end system. The front-end is designed for, amongst other things, ticketing-counters, merchandise points of sale and kiosks, in which all transactions and ticket printings take place. The back-end contains the GSET servers that process and store the incoming data from the front-end. As the front-end and back-end communicate, data is compiled allowing for historical and real-time management reports to be generated. Modular BaSiSThe Group's services and solutions have been designed on a modular basis, enabling the up sale of "add-on" modules, without the need of further implementation expenditure once Galasys is undertaking the ticketing operations. These modules can be split into two categories:

1. Ticketing – The Group's key product package modules which cover Ticketing Management Systems, including Admission Control, Online Ticketing Systems and Intelligent Cloud Systems; and

2. Add-on Modules – Modules that are still serviced through GSET, and are upsold to customers during or after implementation of the Ticketing services, covering, Point of Sales Management System, Customer Relationship Management System, E-Wallet System, Memberships System, Shop Management System, Theatre Ticket Management System, Linking System and Reporting System.

PRODUCTSAND SERVICES

12

01 STRATEGIC REPORT

A full list of modules offered are set out below:

Online/Mobile Ticketing System (B2C)

Online/Mobile Individual Ticket Booking Online/Mobile Point Redeem Management

Online Group Ticket Booking Online/Mobile User Management

Online E-mail System Online/Mobile Booking Management

Mobile APPS Smart Q

Intelligent Cloud System (B2B2C)

Cloud Products Management Cloud Credit or Debit Managament Online Distributors System Online Travel Agencies Management

Cloud Agreement Management Third Party Payment Gateway Online Distributors Management Online Travel Agencies Interface

SMS or MMS Gateway Online 2 Offline Interface Wholesales or Retail Management Reseller APP System

Ticketing Management System

Ticket Setup Potential Customer Management Admission Management Turnstile Control

Individual Ticket Sales Order Management Wireless Admission Control Park Capacity Control

Group Ticket Sales Event Management 2D Handphone Barcode Admisson Crowd Control

Agent Management Voucher Management Sub Parks Control Exits Control

Reseller Sales Management Void Management Refund Management Staff Entry Control

GPOS (Point of Sales System)

Purchase Management Merchandise Entries Merchandise Sales Terminal

POS Sales Management Package Sales Setting Fast Food Sales Terminal

Inventory Management Stock Setting Supplier Entries

Costing Management Account Setting Sales Finance Control

Group Purchase Group Distribution Group Analysis

Membership System

Membership Policies Setting Membership Detail Entries Membership e-Credit Policies

Membership Point Collection Annual Pass Policy Setting Membership Top-Up Sales

Membership Activities Various Type Annual Pass Setting Membership Top-Up Management

Shopping Mall Management System

Property Shop Policies Potential Customer Management

Property Shop Rental Policies Customer Contract Management

Property Activities Management Shop Collection Management

Theatre Tickets & Seats Management System

Organizers, Performer Management Ticket Sales (Individual/Group)

Shows or Event Management Wireless Admission Control

Seat Pricing Management Joint Marketing Management

Area Pricing Management Ticket Setup (with Combo)

CRM Management System

Customer Relationship Policies Setting

Customer Relationship Entries

Customer Relationship Management

Customer Relationship Analysis

e-Wallet System

e-Credit Policies Setting

Cash Card Top-Up Management

Cash Card Refund Management

Linking System

Finance System Property Sales System

Human Resource System Property System

QA System GPS System

Hotel System Others System

Reporting & Analysis System

Ticketing Analysis POS Management Analysis Membership Analysis CRM Analysis Business Intelligent (BI)

13

01 STRATEGIC REPORT

ticketing ManageMentThe Group's Ticketing Management System allows the processing of all types of tickets (e.g. agent ticket sales, membership entry tickets, pre-sold tickets, discount cardholders, special passes and wrist bands using 2D-barcode and Radio Frequency Identification ("RFID"). In addition, the system also allows for all types of payment to be made by the visitors (e.g. credit cards, debit cards, cash and gift vouchers). adMiSSion control ManageMentOnce a ticket has been acquired, GSET then manages the process by which the holder of such ticket enters the park. This can take the form of physical possession of a paper ticket which requires being fed into an automated clearance system (full height turnstile, tripod turnstile, flat barrier or manual ticket reader), affording quicker entry than the more dated ticket check point. If the park user is part of a membership program, or is in possession of an RFID wristband, the purchased ticket will be recorded on their card or wristband, without the need for actual printing, which the turnstile reader will recognise. The GSET is then able to track the entry and exit requirements of each Theme Park User ensuring that expired or used wristbands are not accepted.

e-walletFollowing entry into a Theme Park, the GSET oversees all transactions that take place in the Theme Park. These transactions, just like the acquisition of tickets, can take place via all types of payment (e.g. cash or e-wallet) are recorded on the GSET server for real-time analysis.

E-Wallet (using either 2D-Barcode or RFID technology) acts as electronic wallet can be reloaded with cash credits. Theme Park visitors use their e-Wallet to pay for food & beverages, merchandizes and also as an electronic key for their lockers and hotel rooms. This reduces the problem of making cash payment frequently, which directly discourages visitors to spend more. GSET payment functions are highly secured. All payments go through the process of validation and recognition.

Point of SaleS (PoS)Galasys Point-of-Sales (GPOS) system is a solution that automates daily sales transactions, track customer spending behaviours, provide an integrated web storefront as well as provide a real-time balance sheet and profit & loss statement at days end. GPOS keeps track of this information in a back-end database. GPOS on the front-end allows users to sell, void and skim transaction.

GPOS system runs on a network which would allow an on-line real time information on the operations from the number of visitors to the point of sales at any one point in time.

An added benefit from the Theme Park Operator's perspective is that the cash float is monitored on a real-time basis so that treasury departments can be alerted. Any excess cash held above the daily float will trigger an alert so that the cashier is instructed to transfer any excess cash to the supervisor for safekeeping.

14

01 STRATEGIC REPORT

linking SySteMS and ManageMent and analySiS rePortSAll of the above modules described in 5.3 to 5.6 feed into the central GSET server. Combined with the Linking Systems module, in which all transactions are recorded and compiled, management and analysis reports can be generated on a real-time basis. Currently, the GSET can offer 200 types of standard built in reports, allowing amusement park operators quick access to the number of visitors (daily, monthly and annually), point of sales reports, reports detailing the movement and spend per member (if the Membership Systems add-on module has been deployed) or simply footfall reports on a particular attraction. Real time data is crucial for Theme Park Operators to tailor their marketing and promotional efforts, although as will be discussed later, Galasys have identified further scope for their software to be used in conjunction with Theme Park Operator's marketing and sales departments.

clota CLOTA is a middleware platform that allows theme park operators and owners to open up new sales channels, in addition to the traditional offline channels, by connecting their ticketing systems with the OTAs enabling the sale of tickets online, via the OTAs in real time, direct to the end customer.

CLOTA(CLOUD OTA PLATFORM)

Dry Parks/Theme Parks

Water Parks

Qunar

MAJOR OTAONLINE TRAVEL AGENCIES TRAVEL AGENCIES

Ctrip Lvmama Tuniu OTA..n Online Travel Agencies

Hot Spring Parks

Zoos/MuseumsHotels/Resorts

15

01 STRATEGIC REPORT

galotaSAn Internet platform that targets end customers directly and provides flexibility in making bookings within their theme park visit e.g. enabling the consumers to organize theme park entrance packages and accommodation as the ticketing system links into the hotel reservation system.

MoBile aPPS (MaPPS) Galasys is working with clients to introduce mobile applications (apps) that will allow increased interaction between amusement park visitors and operators during their visit. The apps will provide visitors with useful information like a map of the site and additionally will help operators advertise promotions, discounts and offers, with the aim of increasing visitor’s in park spending. Galasys believes it can receive a share of this additional in park spend.

M-Commerce Park Map & Navigation Attraction details,real-time waiting time

and reserve rides

16

01 STRATEGIC REPORT

Strategy & BuSineSS reviewThe Group’s key event for 2014 was undoubtedly our successful IPO debut on AIM on 12 May 2014. This is a momentous event for the Group, all our staff, shareholders, customers and partners alike after an almost 10-year build-up of the business from 2005. The IPO injected much needed new energy and direction for the Group. It also brought in enhanced corporate governance and strengthened management and enabled the Group to nearly double its staff headcount from a year ago. All these have resulted in the Group’s much stronger position in Asia, our home turf, and are shown in the new markets and customers we have added, new products and services we have developed and launched and the completion of our first acquisition following our IPO.

Through our newly launched CLOTA platform and Ticketing IT Outsourcing (“TiTo”) engagement model, we have ventured beyond our traditional project sales revenue model and into the transformational strategy we have spoken about since our IPO. We expect to pivot more on the available mobile and internet infrastructures to refine and accelerate both our Business to Business to Consumer (“B2B2C”) and Business to Consumer (“B2C”) business models and strategies. In time to come, we seek to correlate our growth more directly with the numbers of visitors to the parks whilst continuing to build our market share in the number of parks using our technology and solutions.

Following on from the acquisition of Galasys GLT in 2013, we made a small acquisition in 2014. Galasys GLT’s integration has been successful and we look forward to seeing more synergies being realised in the coming years. Since inception, Galasys has undertaken and successfully integrated three acquisitions and M&A continues to be an

CHAIRMAN’SSTATEMENT

integral part of the Group’s strategy to accelerate growth and stay abreast of trends and innovations. We continue to be on the lookout for other potential businesses that could complement us and accelerate our growth plan.

The Galasys team has been busy since IPO implementing this strategy and I am pleased that the efforts are reflected in the Group’s full year results for 2014, which have shown significant improvements compared to 2013 and which have exceeded expectations.

ProSPectSThe Group is in an important phase of our technology and product development and 2015 will see the continuing efforts to enhance the existing core ticketing platform and its associated modules including mobile apps and solutions. We expect more exciting product development and launches during the course of the year and to see more financial contribution arising from the commercialization of products and services launched in 2014. In particular, as part of the transformational growth plan, we will develop and launch more products and services that will be mobile and internet based so that our revenue base is broadened and to enable us to reach out more directly to the park visitors.

As a testament to the reliability and quality of our products and services, we have not lost any clients in the last 3 years and continue to secure new and highly reputable ones, such as the Dalian Wanda Group from China and the Enchanted Kingdom from the Philippines.

Our strategy of introducing different engagement and therefore, revenue models has borne fruit as we have, through the TiTo model, successfully secured more clients of different sizes, some of whom we would not have been

17

01 STRATEGIC REPORT

in a position to engage before our IPO. A number of the engagements under the TiTo model have given us significantly higher gross margins. We will continue to pursue this strategy of customer engagement to penetrate further into different segments of the ticketing industry including the broader sub-segment of leisure and entertainment.

In terms of marketing and business development, the Group has invested and increased the size and capability of the sales and marketing team and the additional resources available are being successfully deployed in reaching out to new business prospects in the whole of Asia.

We expect to maintain the positive trends in the business in the coming financial year as we deliver on our long term strategic objective of transforming our current project based business and revenue model into one which correlates our revenue and profits more directly to the number of visitors to our theme-park customers.

dividendAs a result of the positive growth achieved both organically and through acquisition, the Board intends to bring forward its plans to implement a progressive dividend policy by proposing a maiden dividend for 2014, whilst recognising the need for Galasys to continue investing in its expansion and product development plans throughout 2015 and beyond. Consequently, the Board is recommending a final dividend of 1.084sen, c. 0.2 pence per share subject to shareholder approval at the Company’s Annual General Meeting. The final dividend will be payable on 3 July 2015 to shareholders on the register on 5 June 2015.

aPPreciationOn behalf of the Board I would like to express my deep appreciation to the management and staff for their dedication and hard work for the past year and congratulate them on the successful completion of our IPO. Last but not least, I would also like to thank our investors, shareholders, customers and partners for their strong support and patience throughout the year and we look forward to working cohesively with each and every one of you in the months to come.

Kim Seng TehNon-Executive Chairman15 April 2015

18

01 STRATEGIC REPORT

I am very pleased to provide my first full year review since the Group joined AIM on 12 May 2014.

reSultSGalasys has delivered a strong financial performance with revenues up 45% at RM38.62m (FY2013: RM26.7m^). We have seen continued growth in demand for our products and services from existing customers as well as successfully adding new large customers such as Dalian Wanda in China and Enchanted Kingdom in the Philippines. Our earnings before interest, tax, depreciation and amortization (EBITDA) also saw significant improvement being up 48% at RM12.58m (FY2013: RM8.5m^) and this was reflected in both pre-tax profit being up 35% at RM11.34m (FY2013: RM8.38m^) and cash up to RM12.22m* (FY2013: RM2.16m^). The net proceeds from our successful IPO were RM10.50m.

^The comparative figures for the 12 months to 31 December 2013 (refer to note 24) included above were on the basis that Galasys GLT (formally known as Green Laser Technology) was part of Galasys Group from 1 January 2013

*includes net proceeds from IPO of RM10.50m (£2.20m)

Market overviewAccording to Global Attractions Attendance Report published by Themed Attraction Association and AECOM, the outlook for the theme park industry in Asia is very strong with annual growth in attendance numbers of 7.5% is almost double that in the Americas whilst zero growth is expected in Europe. The report also stated that attendance total for the top 15 Asian water-parks has, for the first time, surpassed attendance for the top 15 water-parks in North America. AECOM further predicts the total attendance for the top 20 Asia Pacific theme parks will also surpass those of North America in the not-too-distant future. Against this backdrop of high growth, we intend to continue building on our market leading position across Asia and have made good progress entering into new and emerging South East Asian markets such as the Philippines, Thailand, Vietnam and Indonesia.

new winS, ParkS and titoWe are pleased with the number of new project wins throughout 2014. In particular, we are especially proud to have secured the first ever theme park related contract awarded by the Dalian Wanda Group in the face of keen international competition for this landmark deal. As reported in our interim results announcement, the Group has to-date signed up two key projects with the Dalian Wanda Group, namely Wuhan Movie Park and Wanda Indoor Kids’ Park. We believe there are many more contracts to come in the following years and will work closely with the Wanda team.

Outside China, the Group has made significant progress by entering into new and emerging South East Asia markets. The Group secured contracts with the Enchanted Kingdom, which is the largest

CHIEF ExECUTIVE OFFICER’S STATEMENT

19

01 STRATEGIC REPORT

theme park in the Philippines. This contract was a direct replacement of the client’s existing solution provided by a European ticketing solutions provider and further validates the Group’s standing amidst its international competitors.

Whilst theme parks remain the core segment, the Group is making strides in diversifying into other segments within the leisure and entertainment industry. This is reflected in the contracts secured with museums, tourism and cultural centres. The Group has also added exciting sites such as Zoo Negara and the Sepang International Circuit in Malaysia as part of the portfolio of sites incorporated into the Group following the acquisition of iLogic.

The four TiTo projects signed by the Group in 2014 are also significant as they mark the Group’s move toward the new revenue model, whereby the Group’s clients are engaged with a revenue model that brings both higher profit margins and a recurring revenue stream that is correlated more to ticket sales than the total number of installed sites.

clotaWe are delighted to have completed this significant product development and taken an important step towards positioning Galasys in the heart of the online market segment. After nearly a year of intensive development by the R&D team, we are proud to add a key component to our product platform that offers a fully integrated B2B online sales and distribution network connecting online travel agencies with theme park operators and owners in Asia.

To-date, Galasys has signed up ten online travel agents (OTAs), including Beijing Qunar Software Technology (“Qunar”), Ctrip.com International Ltd (“Ctrip”), Shanghai Lvmama International Travel Agency Co. Ltd (“Lvmama”), Sichuan Brigade Butler Network Technology (“Lvxiaobao”), Tuniu Corporation (“Tuniu”) and Chengdu Chenyu Culture Communication Co., Ltd. These OTAs account for most of the online travel traffic in China with Ctrip alone commanding 54.2% of the market.

There are nine theme parks which have signed up so far and are now fully integrated into CLOTA including Wugang Xianglong Valley Water Park, Gui Lin Yugui Park Universal theme park, Seven Colour Sand River Water Park, Wuhan Mulan Park and Shanxi Water Park.

We will continue to grow the revenues from our CLOTA platform by signing up more parks and OTA partners in the coming months. The tie up with Qunar, Ctrip, Tuniu and Lvmama, the four OTA giants in China, is a testament to the Group’s track record in China and a powerful endorsement of our CLOTA platform.

reSearch and develoPMentResearch and development (“R&D”) remains a key business driver for the Group in order to maintain its competitive advantage in delivering innovative solutions ahead of the market and creating new business trends. The Group has strong and proven R&D capability, which we will continue to deploy to bring new products and services to the market.

The R&D team has successfully played their part and amongst the highlights is CLOTA that was officially launched last year as well as the eWallet on RFID. Furthermore, the R&D for Mobile Ticketing, Park Map & Navigation Apps and Smart-Q MAPPs has been completed and is now ready for deployment.

Through the acquisition of iLogic, the development of GALOTAS has been fast-tracked and further refinements are ongoing with a scheduled launch in later in 2015.

The Group also intends to sell and ship Galasys GLT’s kiosk products (Ticketing Redemption / Vending Kiosk) for amusement park customers in China and South East Asia. Galasys’ kiosk software program is localised to support multi-language and multi currencies payment.

reSourceSTo strengthen our team further, we have recruited more than 40 new staff since the IPO. These new hires will focus on customer generation, developing new technologies

20

01 STRATEGIC REPORT

including GALOTAS and deployment of new installations on new client wins. The Group will continue to hire new sales and technical talents as our business expands.

At the end of 2014, we also announced the appointment of WH Ireland Limited as our new Nominated Adviser (NOMAD) and Broker.

outlook for 2015The Group currently operates in Asia, the strongest growth market for amusement parks and visitor numbers. The Group’s growth strategy is built on new key customer acquisitions, new products through continuous R&D and technology partnership, the rollout of the TiTo engagement model to increase recurring revenue, the execution of the CLOTA sales and distribution platform to correlate our revenue and growth more closely to the number of visitors to our installed sites, and geographical expansion into new territories.

The Group is also exploring collaborations with various technology partners to realise mutual synergies and will keep the market and our shareholders informed in due course.

The Group continues to expand into new territories by signing up partners in countries such as the Philippines, Vietnam, Indonesia, Hong Kong, Japan and the UK. Additionally, the Group is acquiring new clients while continuing to serve and deepen ties to its existing client base.

Asia remains the fastest growing market for the global amusement park industry and Galasys is well positioned to continue its growth in this region. The Group is working on a strong sales pipeline of projects for financial year 2015 and the Board is confident of delivering another year of good progress and financial performance.

Sean SeahChief Executive Officer15 April 2015

21

01 STRATEGIC REPORT

The risk management framework of the Group is designed to identify, manage and mitigate material risks to the achievement of the Group’s strategic and business objectives.

Operational riskDependence on key executives and personnel and the ability to attract, motivate and retain employeesThe Group’s development and prospects are dependent upon the continued services and performance of its senior management and other key personnel. The Group is very dependent on CEO, COO, CFO, MD for China, Sales Director for China, MD of I Logic Solutions and MD of GLT. The loss of the services of any of these executive, the senior management or key personnel may have an adverse impact on the Group.

Attracting, retaining and motivating employees, including individuals with significant relevant technical expertise and associated managed services, is a critical component of the future success of the Group’s business. Competition for qualified technical personnel is intense and is likely to remain so for the foreseeable future and could cause the Group to offer higher compensation and other benefits in order to attract and retain them, which could materially and adversely affect the Group’s financial condition and results of operations. If the Group is unsuccessful in attracting qualified employees or retaining or motivating existing employees, it may be unable to grow its business effectively.

MitigationRetaining qualifying employees especially the technical team has always been a challenge to any software companies. However, the Group has adopted employee share option plan and periodic review of key management team total remuneration to ensure it remains competitive in order to retain them.

Business and market risksTechnology riskAs software technology is evolving daily, the company’s products are subject to technology going obsolete therefore, shortening the product life cycle.

PRINCIPAL RISkSAND UNCERTAINTIES

22

01 STRATEGIC REPORT

MitigationThe Company places a high focus on R&D initiatives and continuously strives to develop better and innovative software solutions The Group continues to invests in R&D and market research to realise the potential of new and existing products, and maintain its market-leading position. With continuous investment in R&D, technical staffs make up to 70% of the total staff strength.

Project-based customersThe Group is an integrated services and solutions provider that provides information technologies solutions and management services for the amusement industry globally. The Group tends to be project-based and as a result long-term customer contracts amount for a relatively small part of the Group’s revenue; however, a substantial part of revenue is recurring or repeated in nature. There may also be lag periods (usually 6-9 months) before the repeat customer purchases additional modules once a project is completed. The Directors believe that Recurring Revenues and Repeat Revenues give some revenue certainty for the Group. However, given the largely project- based nature of certain sales, there is no assurance that the Company will be able to leverage on these existing customers for on-going revenue. In addition, a significant increase in turnover rates from the current levels or any failure to recruit new customers or to retain existing customers could have a material adverse effect on the Group’s business, financial condition and results of operations.

MitigationDue to the need of retaining customers for a longer period of time and also strengthening financials, the Group had already role out a new engagement model call Ticket IT Outsourcing (“TiTo”). Essentially TiTo is an engagement model where the customer will pay Galasys for the infrastructure installed via tickets. The customer, i.e. theme park, will provide Galasys steep discounted tickets, for example at 50% discounted price per ticket. Galasys will then sell these tickets to online travel agencies, travel agencies as well as through Cloud Online Travel Agency (“CLOTA”) to end customers.

Market risk The Group may be affected by general market trends that are unrelated to the performance of the Group. The success of the Group is dependent on the market acceptance of its products, of which there can be no guarantee.

MitigationThe Group conducts ongoing studies of general market trends and developments, in order to enable it to make responsive changes to its business plan when necessary.

Fluctuation in the exchange rates of the Chinese Renminbi or Ringgit may have a material adverse effect on an investor’s investment.Currency fluctuations may affect the cashflow which the Group will realise from its operations, as it is likely to receive payment for the services it provides in the currencies of the countries in which it operates, whilst certain of the Group’s costs are likely to be incurred in other currencies.

23

01 STRATEGIC REPORT

MitigationNotwithstanding that this is an inherent risk for any multi-national organization, the Group endeavors to match as far as possible its revenue and cost with the same currency within the respective jurisdictions as well as closely monitor FOREX fluctuations.

Compliance riskMandatory reporting and announcementPossible delays in reporting could arise due to untimely or unavailable information or a failure in internal procedures for mandatory reporting.

MitigationInternal procedures monitor mandatory reporting and other regulatory requirements closely and consistently. The company has compliance policy in place by have appointing a compliance officer responsible to ensure comply with all the necessary regulations including reporting and announcements.

24

25

CORPORATEGOVERNANCE

26Board of Directors

28Directors’ Report

32Remuneration Committee Report

34Corporate Governance Report

26

02 CORPORATE GOVERNANCE

Kim Seng Teh (Age 49)Non-Executive Chairman

• Executive Chairman of Netrove Ventures Group, a boutique regional venture capital and corporate finance firm that is focused primarily on Asian technology companies

• Sits on various advisory panels and boards including boards of publicly listed companies, and their remuneration and audit committees

• LL.B. (Hons) from Leeds University, England and an LL.M. (Hons) from Queens' College, University of Cambridge, England

BOARD OFDIRECTORS

Sean Seah (Age 48)CEO and Founder, Executive Director

• Co-founder of the Group in 2010 and a shareholder

• Master in Computer Science, California State University, USA

• Started career in Silicon Valley as a software applications developer for Software Publishing Corporation listed on NASDAQ

• Worked at Sun Microsystems Inc. between 1997-2003 and held position of Sun Professional Services Business Operation & Channels Management of Greater China

• He co-founded several companies including Afor Pte Ltd Singapore which went IPO in 2008 and subsequently rebranded as “EpiCentre Holdings Ltd”

Chee Keong Hee (Age 44)CFO, Executive Director

• Chartered Accountant of the Malaysian Institute of Accountants (MIA) and a fellow member of Association of Chartered Certified Accountants (FCCA)

• Experience in both private and public companies. Hee was the Finance Director of a listed company Global Soft in Malaysia

• Actively involved in various industries including IT, property development, leisure and entertainment

• Hands-on experience in corporate compliance and financial reporting.

27

02 CORPORATE GOVERNANCE

Chee Seong Chin (Age 55)Non-Executive Director

• Currently the elected Deputy Chairman of PIKOM, the National ICT Association of Malaysia.

• Served as an independent non-executive director of M-Mode Bhd (2009-2012) (KLSE: MMB) listed on the Ace Market. Over the years, Mr Chin has provided, and continues to provide, significant business network opportunities to the Group.

Garry Peagam (Age 59)Independent Non-Executive Director

• His previous appointments include Group Finance Director of Good Energy Group plc and Blick Group plc (which was sold to The Stanley Works Inc.)

• Was also a Managing Director of M-Netics Ltd, a private company. His experience encompasses large multinational companies in the IT and energy sectors.

Teong Ming Chuah (Age 37)Head of China, Executive Director

• Has over 8 years of working experience in the IT industry and provides significant business knowhow and advice to the management team of the company.

• A Malaysian national, he has headed the Group’s expansion in China since the group was reorganized in 2010.

• Graduated as a Bachelor of Engineering Technology in University of Southern Queensland.

28

02 CORPORATE GOVERNANCE

The Directors submit their report together with the audited consolidated financial statements of the Galasys Plc group of companies for the year ended 31 December 2014. This Directors’ Report includes the Chairman’s Statement, the Chief Executive’s Overview, the Strategic Report, the Corporate Governance section and the Directors’ responsibility statement. The Company is required to set out a fair review of the business of the Group and a description of the principal risks and uncertainties facing the business, which can be found in the Strategic Report. This requirement includes an analysis of the development and performance of the Company’s business during the reporting period, and the position of the Group at the end of the reporting period consistent with our size and complexity. The Directors’ Report has been prepared, and is published, in accordance with, and in reliance upon, applicable Jersey company law and the liabilities of the Directors in relation to that report are subject to the limitations and restrictions provided by such law.

Principal activityThe Company is a holding company and its principal activity is the holding of investment in its subsidiaries. The Group is an Amusement Park solutions and services provider that provides information technology solutions and management services to Amusement Park operators in Asia.

The Company’s registered office address is Queensway House, Hilgrove Street, St. Helier, Jersey JE1 1ES.

Capital StructureThe Group is financed through equity share capital. There is about RM700,000 in debt for working capital purposes. The Company do not need to leverage on debt financing as many of the operating subsidiaries are enjoying tax holidays and this is expected to continue in near future (see note 22 to the financial statements).

Business review and future developmentsGalasys Plc has continued to perform strongly across all its business areas throughout 2014. Full details of the Group’s performance and future developments can be found in the Chairman’s Overview.

Financial results• Revenue for 2014 up 45% at RM38.62m (2013: RM26.67m^)• Gross Profit up 83% at RM19.52m (2013: RM10.64m^)• EBITDA up 48% at RM12.58m (2013: RM8.5m^)

DIRECTORS’REPORT

29

02 CORPORATE GOVERNANCE

• Profit Before Tax up 35% at RM11.34m (2013: RM8.38m^)• Profit After Tax up 30% at RM9.40m (2013: RM7.21m^)• Cash RM12.22m* (2013: RM2.16m^)• EPS RM0.16, or c. 2.91 pence • Repeat and recurring revenue increased to 66% of sales (2013: 60%)

^The comparative figures for the 12 months to 31 December 2013 (refer to note 24) included above were on the basis that Galasys GLT (formally known as Green Laser Technology) was part of Galasys Group from 1 January 2013

* includes net proceeds from IPO of RM10.50m (£2.20m)

DividendsThe Board is recommending a final dividend of 1.084sen, c. 0.2 pence per share subject to shareholder approval at the Company’s Annual General Meeting. The final dividend will be payable on 3 July 2015 to shareholders on the register on 5 June 2015.

Significant shareholdersSignificant shareholders holding over 3% of the issued share capital as at 31 December 2014, other than any Directors and their family as defined in the AIM rules, whose holdings are detailed below:

Ordinary shares As at 31 December 2014 %

Well Oriental Investments Limited (“WOI”)* 26,783,984 40.23

Netrove Ventures Corporation^ 11,417,566 17.15

Soo Choon Meng 7,842,989 11.78

WGLS Foundation 2,151,201 3.23

*WOI is an investment vehicle incorporated in the British Virgin Islands, the shareholders of which are Mr Sean Seah (Company’s Chief Executive Officer), holding 20,709 ordinary shares in WOI (representing a 41.42 per cent. Shareholding interest), Mr Teong Ming Chuah (an executive director of the Company), holding 15,198 ordinary shares in WOI (representing a 30.40 per cent. shareholding interest), Mr Low Kok Thai, holding 10,843 ordinary shares in WOI (representing a 21.69 per cent. shareholding interest) and Mr Chee Keong Hee (the Company’s Chief Finance Officer), holding 3,250 ordinary shares in WOI (representing a 6.50 per cent. shareholding interest).

^Netrove Ventures Corporation, incorporated in the British Virgin Islands, is wholly owned by Kim Seng Teh, the Company’s Non-Executive Chairman

Directors and Directors’ shareholdingsThe Directors during the period under review were:

Kim Seng Teh, Non-Executive ChairmanSean Seah, Executive Director, CEOChee Keong Hee, Executive Director, CFOTeong Ming Chuah, Executive DirectorChee Seong Chin, Non-Executive DirectorGarry Peagam, Independent Non-Executive Director

The Directors’ beneficial interests in the share capital of the Company and remuneration are set out in the Remuneration Committee Report.

30

02 CORPORATE GOVERNANCE

The company paid for sufficient directors and officer’s indemnity insurance during the period, and to the date of approval of these financial statements, to enable the directors to carry out their duties.

Directors’ responsibilitiesThe Directors are responsible for preparing the financial statements in accordance with applicable laws and International Financial Reporting Standards (IFRS) as adopted by the European Union. Company law requires the Directors to prepare financial statements for each financial year which give a true and fair view of the state of affairs of the Company and of the profit or loss of the Company for that year.

In preparing those financial statements, the Directors are required to: • select suitable accounting policies and then apply them consistently; • make judgements and estimates that are reasonable and prudent; • state whether applicable accounting standards have been followed, subject to any material departures disclosed and explained in the financial statements; and • prepare the financial statements on the going concern basis (unless it is inappropriate to presume that the Group will continue in business).

The Directors are responsible for keeping adequate accounting records that disclose with reasonable accuracy of any time the financial position of the Company and to enable them to ensure that the financial statements comply with the Companies (Jersey) Law 1991. They are also responsible for safeguarding the assets of the Company and hence for taking reasonable steps for them prevention and detection of fraud and other irregularities. The Directors are responsible for the maintenance and integrity of the corporate and financial information included on the Group’s website. Legislation in Jersey governing the preparation and dissemination of financial statements may differ from legislation in other jurisdictions.

Research and developmentAs previously mentioned the Directors estimate that the Group has invested over 50 man years and over USD1 million in developing and updating the Group’s proprietary systems and software. The Directors believe that by continuingly investing in R&D, the Group will be able to improve service offerings to its customers and therefore look to distinguish itself from its competitors. It is the Directors’ intention that the Group will continue to invest progressively in R&D.

EmployeesThe Group’s policy is to have a competitive remuneration and benefits provision to attract and retain the best and brightest talent. The Group is committed to ensuring that equal opportunities are accorded to all of its employees irrespective of age, gender and nationality in training, career development and advancement in an effort towards ensuring that the Group employs the most skilled workforce.

The Company recognises that on-going share ownership is an important part of the Group’s incentivisation and retention policy. The Company has therefore adopted the Share Option Plan. Options may be granted to employees of the Company and any Participating Company.

31

02 CORPORATE GOVERNANCE

Risks relating to the Group and its businessA review of the risks associated with the Group and the nature of its business is set out in the Principal Risks and Uncertainties section.

Going concernThe Company’s activities and developments of its products, services and markets are set out in the CEO’s statement. The performance of the Company in terms of revenue, profitability and cash flows is explained in the Financial Statements.

After the assessment of the available financial information, and taking into account the nature of the business, which has recurring revenue with high cash conversion, as reflected in the current financial position of the Group with cash position of RM12.2 million as at 31 December 2014, the Directors believe that the Group has adequate resources to continue to operate for the foreseeable future. Therefore, it is appropriate to continue to adopt the going concern basis of accounting in the preparation of the Company consolidated financial statements.

Auditor and disclosure of information to auditor The Directors who held office on the date of approval of this Directors’ Report confirm that, so far as they are aware, there is no relevant audit information of which the Company’s auditor is unaware. The Directors have confirmed that they have taken all steps that they ought to have taken as Directors in order to make themselves aware of any relevant audit information and to establish that the Company’s auditor is aware of that information. Crowe Clark Whitehill LLP has been appointed as the auditor of the Company during the year.

This report was approved by the Board and signed on its behalf.

Sean SeahChief Executive Officer15 April 2015

32

02 CORPORATE GOVERNANCE

Galasys Plc, being an AIM quoted company, has adopted the general principles of the Remuneration Committee Guide for Smaller Quoted Companies of The Quoted Companies Alliance.

Remuneration CommitteeThe remuneration Committee comprises the Chairman of Committee, Kim Seng Teh (Non-Executive Chairman), Garry Peagam (Non-Executive Director), and Chee Seong Chin (Non-Executive Director). The terms of reference of the Committee are available on the Company’s website and are reviewed annually by the Board. The Remuneration Committee is responsible for determining the Group’s policy on the remuneration of senior executives and specific remuneration packages for Executive Directors, including pension rights and compensation payments.

Remuneration PolicyThe objective of the remuneration policy is to attract, retain and motivate high caliber Executives as well as to achieve the overall objective of promoting teamwork in delivering outstanding shareholder returns while maintaining an appropriate compensation balance for all the employees of the Group.

Directors’ remunerationThe normal remuneration arrangements for Executive Directors consist of base salary, annual performance-related bonuses and other benefits as determined by the Board. Each of the Executive Directors has a service agreement that can be terminated at any time by either party giving to the other 6 months’ written notice.

Non-Executive DirectorsNon-Executive Directors are remunerated solely in the form of director fees determined by the Board and are not entitled to pensions, annual bonuses or employee benefits. They are entitled to participate in share option arrangements relating to the Company’s shares but as there are no such share option arrangements in place at this time, there is no participation from the Non-Executive Directors from this form of remuneration. Each of the Non-Executive Directors has a letter of appointment stating his annual fee and that the appointments are to continue unless terminated by the Company by giving 1 month’ written notice or at any time by a resolution of the Shareholders and subject to reappointment at the first annual general meeting following his appointment.

Directors are not involved in specific discussions on their own remuneration.

REMUNERATION COMMITTEE REPORT

33

02 CORPORATE GOVERNANCE

Directors' interests

Ordinary shares As at 31 December 2014 %

Sean Seah* 26,783,984 40.23

Chee Keong Hee* 26,783,984 40.23

Teong Ming Chuah* 26,783,984 40.23

Kim Seng Teh^ 11,862,010 17.82

Chee Seong Chin 660,462 0.99

*Sean Seah, Chee Keong Hee and Teong Ming Chuah’s shareholding is held indirectly through Well Oriental Investments Ltd. They are therefore deemed or taken to be interested in 100 per cent. of the Ordinary Shares held by Well Oriental Investments Ltd.

^Kim Seng Teh’s shareholding is held indirectly through Netrove Ventures Corporation and Netrove Strategic Corporation. He is therefore deemed or taken to be interested in 100 per cent. of the Ordinary Shares held by Netrove Ventures Corporation and Netrove Strategic Corporation.

Directors’ remuneration

FY2014 Salary Fees (RM’000)

Bonus(RM’000)

Benefits(RM’000)

Total(RM’000)

Executive Directors

Sean Seah 202 - 117 319

Chee Keong Hee 92 - 43 135

Teong Ming Chuah 125 - 3 128

Non-Executive Directors

Kim Seng Teh 103 - - 103

Garry Peagam 82 - - 82

Chee Seong Chin 21 - - 21

34

02 CORPORATE GOVERNANCE

The Directors recognise the importance of sound corporate governance and intend for the Company to comply with the provisions of the UK Corporate Governance Code insofar as they are appropriate given the Company’s size and stage of development. In any event, the Directors intend to comply with the provisions of the Quoted Companies Alliance (QCA) Guidelines.

The Board is responsible for formulating, reviewing and approving the Company’s strategy, budgets and corporate actions. Following Admission, the Directors intend to hold Board meetings at least quarterly and at such other times as they deem necessary. The Board has established a remuneration committee, an audit committee and a nomination committee.

Board of Directors and Board CommitteesThe Board of Directors consists of 3 Executive and 3 Non-Executive members that include a Non-Executive Chairman. The respective appointments of the Board members provide an appropriate balance of skills and experience for the Board to lead the Group in the interests of all shareholders.

The roles of Chairman and Chief Executive are separate and clear. The Chairman’s role is to lead the Board in Board meetings and ensure the effectiveness of the Board. The role to ensure that the Group’s long term strategic and financial objectives are achieved with the Group’s resources and in accordance to the risk level of the Group is the responsibility of the Chief Executive.

The Board is responsible to shareholders by providing leadership and direction to the Group. The role of the Board is to set the strategic direction and goals of the Group within its expertise and risk framework. The Board has a schedule of matters reserved for its decision which include, but are not limited to, decisions on strategy and risk management, approval of financial budgets, major capital expenditure, material acquisitions and disposals, the interim and annual results and the interim and final dividend recommendations. The Board Committees that have been established to assume some of the responsibilities of the Board with clearly defined terms of reference are the Audit, Nomination, Remuneration Committees.

The Board has had regular Board meetings for the financial year ended 31 December 2014. For the period, 5 board meetings have been conducted by the Company. Formal agendas and reports are provided to the Board for the Board meetings and all Directors are properly briefed on the matters to be discussed and deliberated. All Directors in carrying out their duties as members of the Board

CORPORATEGOVERNANCEREPORT

35

02 CORPORATE GOVERNANCE

are able to obtain further advice and information from within the Company or from independent professional advisers. The Company maintains an appropriate directors’ and officers’ insurance policy cover in respect of any legal actions against the Directors.

The performance of the Board is currently assessed by the Chairman with respect to the various operations of the Board that include, among others, the appropriate skill level of the members, the conduct of Board meetings and the decisions achieved, the guidance with regard to the Group’s strategy and objectives, and the effectiveness of the 3 standing Board Committees in carrying out their responsibilities in accordance to the set terms of reference.

The table below sets out the Board meetings as well as the Audit, Remuneration and Nomination Committee meetings respectively held by the Company for the financial year ended 31 December 2014 and attendance of each Director:

Board meetingsAudit Committee

meetings

RemunerationCommittee

meetings

NominationCommittee

meetings

Executive Directors

Sean Seah 5/5 - - -

Chee Keong Hee 5/5 - - -

Teong Ming Chuah 5/5 - - -

Non-Executive Directors

Kim Seng Teh 5/5 1/1 - -

Garry Peagam 5/5 1/1 - -

Chee Seong Chin 5/5 1/1 - -

Board CommitteesThe Board has established 3 Committees with clearly defined terms of reference and detailed below are the members of the Committees and their duties and responsibilities.

Audit CommitteeThe audit committee will initially consist of Garry Peagam as chairman and Kim Seng Teh and Chee Seong Chin. It will meet at least twice each year and will be responsible for ensuring that the financial performance of the Group is properly monitored and reported on and for meeting with the auditors and reviewing findings of the audit with the external auditor. It is authorised to seek any information it properly requires from any employee and may ask questions of any employee. It will meet with the auditors once a year without any members of management being present and is also responsible for considering and making recommendations regarding the identity and remuneration of such auditors.

Remuneration CommitteeThe remuneration committee will initially consist of Kim Seng Teh as chairman and Garry Peagam

36

02 CORPORATE GOVERNANCE

and Chee Seong Chin. It will meet at least once each year and will consider and recommend to the Board the framework for the remuneration of the executive Directors and any other senior management. It will further consider and recommend to the Board the total individual remuneration package of each executive Director including bonuses, incentive payments and share options or other share awards. In addition, subject to existing contractual obligations, it will review the design of all share incentive plans for approval by the Board and the Company’s shareholders and, for each such plan, will recommend whether awards are made and, if so, the overall amount of such awards, the individual awards to executive Directors and the performance targets to be used. No Director will be involved in decisions concerning his own remuneration.

Nomination CommitteeThe nomination committee will initially consist of Kim Seng Teh as chairman and Sean Seah and Garry Peagam. The nomination committee will meet at least once each year and will consider the selection and re-appointment of Directors. It will identify and nominate candidates to all Board vacancies and will regularly review the structure, size and composition of the Board (including the skills, knowledge and experience) and will make recommendations to the Board with regard to any changes.

Investor relationsCompany following the interim and annual results announcements and on an as-needed basis are attended by the Non-Executive Chairman, Chief Executive Officer and Chief Financial Officer to update the shareholders on the progress of the Group in terms of its business, financial performance and strategic direction. The annual report and accounts is published on the Company’s website and can be accessed by shareholders.

Internal control and risk managementThe Board is responsible for the Group’s systems of internal controls and for reviewing the effectiveness of the systems. The systems can only provide reasonable but not absolute assurance against material misstatements

or losses as the systems are put in place to manage and minimise the risks but not to eliminate them.

With the active involvement of the Executive Directors of the Company in the daily operations and management of the Group, and with regular meetings with staff, business risks are identified and appropriate control systems implemented to manage the risks. The effectiveness of the control systems are reviewed and updated periodically by the Principal Management Office.

The Group’s internal financial control procedures and monitoring systems include: • financial policies and approval procedures with proper authorization level and segregation of duties for financial management; • maintenance of proper records for the production of accurate and timely financial management information; • an annual budgetary process to set the appropriate target for monitoring of the progress of the Group; • a detailed monthly financial reporting system that reports on operating results, cash flow, assets and liabilities with comparisons against budgets; • reporting on any non-compliance with internal financial controls and procedures; and • a review of the Audit Committee report issued by external auditor.

The Audit Committee on behalf of the Board reviews reports from the external auditor together with management’s response regarding proposed actions. Through such review, they have reviewed the effectiveness of the internal control systems for the period covered by the accounts.

37

FINANCIALSTATEMENTS

38Independent Auditor’s Report to the Members of Galasys Plc

40Consolidated Statement of Comprehensive Income

41Consolidated Statement of Financial Position

43Consolidated Statement of Changes in Equity

45Consolidated Statement of Cash Flows

47Notes to the Financial Statements

38

03 FINANCIAL STATEMENTS

INDEPENDENTAUDITOR’S REPORTTO THE MEMBERS OF GALASyS PLC

We have audited the Financial Statements of Galasys plc for the year ended 31 December 2014 which comprise the Group Statement of Comprehensive Income, Group Statements of Financial Position, Group Statement of Cash flows, Group Statement of Changes in Equity and their related notes.

The financial reporting framework that has been applied in their preparation is applicable law and International Financial Reporting Standards (“IFRS”) as adopted by the European Union.

This report is made solely to the company’s members, as a body, in accordance with Article 113A of the Companies (Jersey) Law, 1991. Our audit work has been undertaken so that we might state to the Company’s members those matters we are required to state to them in an auditor’s report and for no other purpose. To the fullest extent permitted by law, we do not accept or assume responsibility to anyone other than the Company and the Company’s members as a body, for our audit work, for this report, or for the opinions we have formed.

Respective responsibilities of directors and auditorAs explained more fully in the Statement of Directors’ Responsibilities, the Directors are responsible for the preparation of the financial statements and for being satisfied that they give a true and fair view. Our responsibility is to audit and express an opinion on the financial statements in accordance with applicable law and International Standards on Auditing (UK and Ireland). Those standards require us to comply with the Auditing Practices Board’s Ethical Standards for Auditors.

Scope of the audit of the financial statementsAn audit involves obtaining evidence about the amounts and disclosures in the financial statements sufficient to give reasonable assurance that the financial statements are free from material misstatement, whether caused by fraud or error. This includes an assessment of: whether the accounting policies are appropriate to the company's circumstances and have been consistently applied and adequately disclosed; the reasonableness of significant accounting estimates made by the directors; and the overall presentation of the financial statements.

39

03 FINANCIAL STATEMENTS

In addition, we read all the information in the Annual Report to identify material inconsistencies with the audited financial statements and to identify any information that is apparently materially incorrect based on, or materially inconsistent with, the knowledge acquired by us in the course of performing the audit. If we become aware of any apparent material misstatements or inconsistencies we consider the implications for our report.

OpinionIn our opinion: • the financial statements give a true and fair view of the state of the group and parent company’s affairs as at 31 December 2014 and of the group’s profit for the year then ended;• the financial statements have been properly prepared in accordance with IFRSs as adopted by the European Union; and • the financial statements have been prepared in accordance with the requirements of the Companies (Jersey) Law 1991.

Matters on which we are required to report by exception We have nothing to report to you in respect of the following matters where the Companies (Jersey) Law 1991 requires us to report to you if, in our opinion:• proper accounting records have not been kept by the parent company, or • proper returns adequate for our audit have not been received from branches not visited by us; or• the parent company financial statements are not in agreement with the accounting records and returns; or• we have not received all the information and explanations we require for our audit.

Stephen Bullock St Brides HouseSenior Statutory Auditor 10 Salisbury SquareFor and on behalf of LondonCrowe Clark Whitehill LLP EC4Y 8EHStatutory Auditor15 April 2015

40

03 FINANCIAL STATEMENTS

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

Proforma2014 2013

Note RM RM

Revenue 19 38,621,893 9,394,752Cost of sales (19,099,021) (2,913,438)

Gross profit 19,522,872 6,481,314

Other operating income 20 611,722 2,907,885Selling and distribution expenses (725,596) (524,750)Administrative expenses (6,907,528) (1,479,765)Other operating expenses (1,082,203) (235,663)

Operating profit 11,419,267 7,149,021

Finance costs (80,705) (42,001)

Profit before taxation 21 11,338,562 7,107,020

Income tax expense 22 (1,942,803) (350,155)

Profit after taxation 9,395,759 6,756,865

Other comprehensive income:- Items that will or may be reclassified to profit or loss- Foreign currency translation 657,793 581,900

Total comprehensive income for the financial year 10,053,552 7,338,765

Profit after taxation attributable to:-Owners of the Company 9,395,759 6,756,865

Total comprehensive income attributable to:-Owners of the Company 10,053,552 7,338,765

Earnings per share:- Basic (sen) 23 15.79 12.82

- Diluted (sen) 23 15.79 12.82

41

03 FINANCIAL STATEMENTS

CONSOLIDATED STATEMENT OFFINANCIAL POSITION

Proforma2014 2013

Note RM RMNon-current assets Plant and equipment 4 493,095 211,972Intangible assets 5 6,085,901 2,769,538Goodwill on consolidation 6 550,356 515,913Investment in quoted shares - 112,674Deferred tax assets 14,570 -

7,143,922 3,610,097Current assets Inventories 7 1,037,779 2,169,289Trade and other receivables 8 17,233,262 12,672,204Amount owing by contract customers 9 8,564,195 1,368,794Amount owing by related parties 10 - 346,258Fixed deposits with licensed banks 11 477,289 463,362Cash and bank balances 11,739,417 1,700,823

39,051,942 18,720,730

Total Assets 46,195,864 22,330,827

Current liabilities Trade and other payables 12 5,225,181 1,728,352Amount owing to related parties - 560,485Amount owing to directors 13 - 1,667Short-term borrowings 14 467,871 615,618Finance lease payables 15 29,660 29,660Redeemable convertible preference shares 16 - 1,173,564Provision for taxation 1,738,971 1,490,878

7,461,683 5,600,224EquityStated capital account 17 25,406,103 -Foreign currency translation reserves 18 1,294,500 636,707Capital reserve 18 671,556 543,224Share option reserve 172,792 -Retained profits 21,853,473 12,586,046Merger reserve 18 (10,851,562) 2,707,972

38,546,862 16,473,949

42

03 FINANCIAL STATEMENTS

CONSOLIDATED STATEMENT OF FINANCIAL POSITION - CONTINUED

Proforma2014 2013

Note RM RMNon-current liabilities Deferred tax liabilities - 3,038Long term borrowings 14B 81,984 118,621Finance lease payables 15 105,335 134,995

187,319 256,654

Total Equity and Liabilities 46,195,864 22,330,827

The financial statements were approved by the Board of Directors and authorised for issue on 15 April 2015 and are signed on its behalf by:

Sean SeahChief Executive Officer

43

03 FINANCIAL STATEMENTS

CONSOLIDATED STATEMENT OFCHANGES IN EqUITy

NON-DISTRIBUTABLE DISTRIBUTABLE

Stated capitalaccount

Foreigncurrency

translationreserve Capital reserve

Merger Reserve/(deficit) Retained profits

Attributableto owners

of the Group Total

RM ('000) RM ('000) RM ('000) RM ('000) RM ('000) RM ('000) RM ('000)

Balance at 1 January 2013 (Proforma) - 55 304 - 6,068 6,427 6,427

Profit after tax for the year - - - - 6,757 6,757 6,757

Other comprehensive income, net of tax- Foreign currency transalation differences for foreign operations - 582 - - - 582 582

Total comprehensive income for the year - 582 - - 6,757 7,339 7,339

Transfer to capital reserve - - 239 - (239) - -

Issuance of shares on group reorganisation - - - 2,708 - 2,708 2,708

Balance at 31 December 2013 (Proforma) - 637 543 2,708 12,586 16,474 16,474

44

03 FINANCIAL STATEMENTS

NON-DISTRIBUTABLE DISTRIBUTABLE

Stated capitalaccount

Foreigncurrency

translationreserve

Share optionreserve

Capitalreserve

MergerReserve/

(deficit)Retained

profits

Attributableto owners

of the Group Total

RM ('000) RM ('000) RM ('000) RM ('000) RM ('000) RM ('000) RM ('000) RM ('000)

Balance at 1 January 2014 - 637 - 543 2,708 12,586 16,474 16,474

Profit after tax for the year - - - - - 9,396 9,396 9,396

Other comprehensive income, net of tax- Foreign currencytransalation differences for foreign operations - 658 - - - - 658 658

Total comprehensive income for the year - 658 - - - 9,396 10,054 10,054

Transfer to capital reserve - - - 128 - (128) - -

Issuance of shares - - - - 3,939 - 3,939 3,939

Share based payment - - 173 - - - 173 173

Issuance of shares ongroup reconstruction 17,478 - - - (17,478) - - -

Issuance of placing shares 17,076 - - - - - 17,076 17,076

Share issuance expenses (9,148) - - - - - (9,148) (9,148)

Transfer to merger deficit - - - - (20) - (20) (20)

Balance at31 December 2014 (Proforma) 25,406 1,295 173 671 (10,851) 21,854 38,548 38,548

CONSOLIDATED STATEMENT OF CHANGES IN EqUITy- CONTINUED

45

03 FINANCIAL STATEMENTS

CONSOLIDATED STATEMENT OFCASH FLOwS

Proforma2014 2013

Note RM RMCash flow from operating activitiesProfit before taxation 11,338,562 7,107,020 Adjustments for:Depreciation of plant and equipment 4 128,952 29,476 Amortisation charge 5 1,027,328 677,481 Interest income (13,927) (287)Interest expense 80,705 42,001 Fair value loss on receivables - 16,382Write back on impairment loss of receivables (109,679) -Written off of tenancy deposits - 5,169 Written off of trade and other receivables 247,048 184,636 Impairment allowance on trade receivables 299,011 -Share based payments 172,792 -Loss on sales of unquoted shares 48,632 -Unrealised loss on foreign exchange 319,036 -Gain on disposal of plant and equipment - (2,360)Negative goodwill - (2,055,505)

Operating profit before working capital changes 13,538,460 6,004,013 Decrease in inventories 1,188,210 74,417 Increase in trade and other receivables (4,359,113) (2,944,420)Increase/(decrease) in trade and other payables 2,548,887 (1,151,418)Increase in amount owing by contract customers (6,665,732) (319,486)

Cash flow from operations 6,250,712 1,663,106 Interest received 13,927 287 Interest paid (80,705) (9,078)Income tax paid (1,749,913) (350,155)

Net cash flow from operating activities 4,434,021 1,304,160

Cash flow used in investing activitiesAcquisition of plant and equipment (404,974) (34,942)Proceed from disposal of plant and equipment - 22,051 Proceed from sales of unquoted shares 64,042 -Acquisition of a subsidiary, net of cash acquired - 290,719 Addition of intangible assets (4,143,961) (1,763,139)Repayment from holding company - 386,393 Repayment to related parties - (29,030)Repayment of advances from a director - 34,976

46

03 FINANCIAL STATEMENTS

Proforma

2014 2013

Note RM RM

Net cash flow used in investing activities (4,484,893) (1,092,972)

Balance carried forward (50,872) 211,188

Cash flow from financing activities

Repayment of borrowings (36,637) (244,590)

Repayment of finance lease payables (29,660) -

Cash restricted in use (13,927) (463,362)

Net proceeds from issuance of shares 10,673,005 -

Issuance of preference shares - 1,173,564

Repayment to a director - (24,878)

(Repayment to)/ Advances from related parties - 273,332

Net cash from financing activities 10,592,781 714,066

Net Increase in cash and cash equivalents 10,541,909 925,254

Effects of foreign exchange translation (355,568) 17,825

Opening balance 1,134,271 191,192

Closing balance 11B 11,320,612 1,134,271

CONSOLIDATED STATEMENT OF CASH FLOwS - CONTINUED

47

03 FINANCIAL STATEMENTS

1. General InformationGalasys PLC was incorporated in Jersey on 23 January 2014 as a public limited company with registration number 114827. It is listed on the AIM Market of the London Stock Exchange. The registered office of the Company is Queensway House, Hilgrove Street, St Helier, Jersey, JE1 1ES. The principal activity of the Company is to act as the holding company of a group involved in the provision of IT solutions and management services to customers operating in the amusement park industry.

The subsidiaries are principally engaged in providing integrated services and theme-park solutions, information technologies solutions and management services to third parties operating in the amusement park industry in Asia.

2. Summary of significant accounting policies

2.1. Basis of preparation Statement of Compliance The consolidated financial information has been prepared in accordance with International Financial Reporting Standards as adopted by the EU (“IFRS”) issued by the International Accounting Standards Board (“IASB”), including related Interpretations issued by the International Financial Reporting Interpretations Committee (“IFRIC”). The consolidated financial information has been prepared using the accounting policies which are consistent with those adopted in Part IV of the AIM Admission Document of Galasys plc dated 7 May 2014 as well as applying the below accounting policy in respect of the basis of consolidation as extracted from the draft financial statements.

The individual financial information of each entity is measured and presented in the currency of the primary economic environment in which the entity operates (its functional currency). The consolidated financial statements of the Group are presented in Ringgit Malaysia (RM), which is the presentation currency for the consolidated financial statements. The functional currency of each individual entity is the local currency of each individual entity. The primary economic environment for the Group is Malaysia.

The financial information set out in this preliminary announcement does not constitute audited financial statements for the year ended 31 December 2014. The financial information for the year

NOTES TO THEFINANCIALSTATEMENTS

48

03 FINANCIAL STATEMENTS

ended 31 December 2014 is derived from draft financial statements. The audit of the statutory accounts for the year ended 31 December 2014 is not yet complete. These accounts are expected to be finalised on the basis of the financial information presented by the directors in this preliminary announcement and will be delivered to the Jersey Companies Registry following the company's Annual General Meeting. Although the auditors have not yet reported on the financial statements for the year ended 31 December 2014, they currently anticipate issuing an unqualified report.

The financial information set out in this announcement was approved and authorised for issue by the board of directors on 13 April 2015.

2.2. Basis of consolidationBusiness Combinations The consolidated financial statements include the financial statements of the Company and its subsidiaries made up to 31 December each year. On 7 March 2014 the Company acquired the entire share capital of Galasys Holdings Limited (“Galasys Holdings”) via a share swap agreement. As a result of this transaction, the ultimate shareholders in Galasys Holdings received shares in the Company in direct proportion to their original shareholdings in Galasys Holdings.

IFRS does not provide specific guidance on accounting for common control transactions. Therefore, the Directors have selected an accounting policy using the “hierarchy” described in paragraphs 10-12 of IAS 8 Accounting Policies, Changes in Accounting Estimates and Errors. The hierarchy permits the consideration of pronouncement of other standard-setting bodies. The Directors have adopted a policy of accounting for business combinations between entities under common control in accordance with guidance under UK GAAP for guidance (FRS-Acquisitions and Mergers) which does not conflict with IFRS and reflects the economic substance of the transaction. This guidance produces a result that is similar to pooling.

Under UK GAAP, the assets and liabilities of both entities are recorded at book value, not fair value. Intangible assets and contingent liabilities are recognized only to the extent that they were recognized by the legal acquirer in accordance within applicable IFRS, no goodwill is recognised, any expenses of the combination are written off immediately to the income statement and comparative amounts, if applicable, are restated as if the combination had taken place at the beginning of the earliest accounting period presented. Therefore, the consolidated accounts have therefore been prepared as if the Group structure has always been in place, including activity from incorporation of the Group’s subsidiaries, although the Group reconstruction did not become unconditional until [7 March 2014].

Subsidiaries A subsidiary is an entity (including special purposes entities) over which the Company has the power to govern the financial operating policies, generally accompanied by a shareholding giving rise to the majority of the voting rights, as to obtain benefits from their activities. The consolidated financial statements present the results of the Group as if they formed a single entity.

49

03 FINANCIAL STATEMENTS

Intra-group balances and transactions and any income and expenses arising from intra-Group transactions are eliminated on consolidation. Unrealised gains and losses arising from transactions with associates and joint ventures are eliminated against the investment to the extent of the Group’s interest in the investee.

The principal activities of the subsidiaries are as follows:

NamePlace of incorporation/ establishment Principal activities

Issued and paid-up/registered capital

Effectiveinterests %

Galasys Holdings Limited British Virgin Island Investment holding. USD4,133,628 100

Galasys Solutions (MSC) Sdn Bhd * Malaysia Software development and maintenance with a specific focus on software relating to theme park visitor admittance.

RM500,000 100

Galasys Technologies (HK) Limited * Hong Kong Investment holding. HKD190 100

Galasys GLT Sdn Bhd(formerly known as Green Laser Technology Sdn Bhd) *

Malaysia Engaged in production, supplying, distribution of self-service kiosk and other computer related accessories and provide a wide range of business communication solutions.

RM400,000 100

Galasys Global (Suzhou) Co. Limited ^ People’s Republic of China

Software design and development, sale of software products of the company and provision of consulting and after-sale services and software services.

RMB5,379,725 100

Note: * Held through Galasys Holdings Limited ^ Held through Galasys Technologies (HK) Limited. Under Galasys Global (Suzhou) Co. Limited, there is a branch company in Beijing and four representative branch offices in Guangzhou, Chengdu, Shandong and Wuhan.