Embed Size (px)

Citation preview

Meridian Petroleum plc

Meridian Petroleum plcAnnual Report & Accounts 2005

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 1

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 2

M E R I D I A N P E T R O L E U M P L C

Contents Page

Corporate Information 2

Chief Executive’s Officer’s Statement and Review of Operations 3

Directors’ Report 6

Report of the Independent Auditors 9

Consolidated Profit & Loss Account 11

Consolidated Statement of Total Recognised Gains & Losses 12

Consolidated Balance Sheet 13

Company Balance Sheet 14

Consolidated Cash Flow Statement 15

Accounting Policies 16

Notes to the Accounts 19

{ 1 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 1

M E R I D I A N P E T R O L E U M P L C

CorporateInformation

Directors Donald Blanks Caldwell – Non-Executive Chairman

Anthony John Mason – Chief Executive Officer

Peter Richard Clutterbuck – Non-Executive Director

Company Secretary Niel Redpath FCA

Registered Office 42 Berkeley Square

London W1J 5AW

Nominated Advisor and Broker Westhouse Securities LLP

Clements House

14-18 Gresham Street

London EC2V 7NN

Auditors Grant Thornton UK LLP

Manor Court

Barnes Wallis Road

Segensworth

Fareham

Hampshire PO15 5GT

Solicitors Field Fisher Waterhouse LLP

35 Vine Street

London EC3N 6AE

Bankers Barclays Bank

54 Lombard Street

London EC3P 3AH

Registrars Lloyds TSB Registrars

Princess House

1 Suffolk Lane

London EC4R 0AN

Registered number 05104249

{ 2 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 2

M E R I D I A N P E T R O L E U M P L C

Chief Executive’sOfficer’s Statement& Reviewof Operations

Although 2005 was a year of varied fortunes for Meridian Petroleum PLC (“Meridian” or the “Company”), our progress since

the year end has been much more promising.

We experienced some mixed results in the development of our US prospect portfolio with even the successes frustrated by

the difficulty of obtaining the right equipment and personnel for various tasks. However, we believe we have achieved much

more significant results in the development of our larger projects, both in the USA and Australia.

Current US Prospects

Meridian’s first and primary producing asset, Emery Hudson, began production in July of 2004. However, the well, after very

promising initial production rates, experienced a gradual decline in pressure and as a result production levels dropped from

a peak of 900 mcfpd in the early part of 2005 to 278 mcfpd in mid 2005. What became evident on analysis was that the reef

in question was highly compartmentalized and in order to counter this issue, two step out legs were drilled in October of 2005,

the C & D Wells. These step out legs encountered gas, but not in commercial quantities. After further analysis of the 3D

Seismic data, it was determined that a direct approach to the reef was required. It is likely that operations will re-commence

on Emery Hudson at some stage in the third quarter of 2006 in order to enhance the production potential of this large gas

prone reef.

Meridian drilled the Calvin 36 #1 test well in September and October of 2004. The gas shows from the Sligo Petit formation

looked highly promising. However, the Rodessa Zone, whilst apparently prolific in other areas, was found to be wet. Based

upon recent experience this is likely to be a local phenomenon and is unlikely to be the case across the entire acreage

position. The initial issue with the 36 # 1 well was water ingress in the lower portion of Sligo Petit due primarily to the vertical

fracturing in this zone. Throughout the year the well was monitored and both bottom hole pressure and surface pressure

continued to rise on a gradual basis, indicating the presence of good reservoir. The well bore was re entered in early 2006

and significant gas flow resulted. The well is currently being completed and will be on line in the summer of 2006.

Overall we view the potential of the Calvin field to be significant from both the Sligo Petit and Rodessa formations in the

shallow zones. Meridian is developing a detailed plan to fully exploit at minimal cost the potential of these zones. The

Company is also in negotiation to acquire the deeper and highly prolific Lower Cotton Valley Troy Lime and Calvin Gas Sand

areas. These formations are being produced to the North of the Calvin Field by Anadarko, on geologic trend with the

Company’s acreage position at Calvin. The full reserve potential will be released post the acquisition and after a detailed

review by ECL Scott Pickford the Company’s reserve consultants. The Calvin Field meets the Company’s criteria of being

both technically sound and having an existing infrastructure in the field which enables gas to be processed and transported

to market at an economic cost. Thus, maximizing profitability and return to shareholders.

The Milford 36 well (25% WI) was drilled in March of 2005 and encountered approximately 103 feet of net pay in the reef.

Initial production tests were indicative of a potentially “tight” zone in the reef and exhibited limited porosity. The acid wash

injected in the well bore did not counter this issue and the Company, along side our joint venture partners, proposes to drill

a series of lateral legs using a coiled tubing unit, a method which was successfully utilized at the Calvin 36 # 1 well. This

work is planned for late second quarter 2006 with the prognosis being very good and we look forward to completion and

subsequent hook up.

{ 3 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 3

M E R I D I A N P E T R O L E U M P L C

Chief Executive’sOfficer’s Statement& Reviewof Operations

The Brighton 36 well, drilled in April of 2005, was plugged and abandoned which was disappointing given the initial potential

exhibited for the reef in question. There are no plans to re enter this well bore. The exploration costs of approximately

$200,000 were expensed during the year.

In late 2005 Meridian commenced the process for the acquisition of the Orion lease in Oakland County Michigan. This

acquisition was completed in early 2006 on the initial lease position for a cost of $40,000. The Orion prospect consists of a

2.7 to 3 BCF shut in reserve. The reef was previously drilled with 2 wells in 1989 and 1990 but both were shut in due to H2S

emissions. Our proposed technical solution was to utilize alternate sulphur treat towers and this proposal was accepted by

the Michigan Department of Environmental Quality (DEQ). Additionally, the planned well site is located on an asphalt mining

area, and also adjacent to a Michigan Gas Storage Company Pipeline. Hence, a direct tap into the line can be made saving

time and money. It is proposed to drill this well upon completion of the permitting process in late second quarter 2006.

Meridian purchased a 10% interest in the producing Victory 1-21 well in April 2005. The well has been in production

throughout and was recently deepened.

As part of Meridian’s initiative to develop a greater inventory of prospects, several seismic lines were shot over areas in

Mississippi that have been purchased by the Company. These lines in turn were reprocessed in November 2005, and

several oil producing sand channels identified. In order to fully define these channels it was decided that the 3D seismic

would be a substantial aid plus it would further minimize dry hole risk. The Company has subsequently entered into an

agreement whereby a third party will shoot 3D seismic over the acreage in return for a 50% working interest. This is

anticipated in 3rd or 4th quarter 2006.

Development projects

In September of 2005 the Company commenced detailed work on the Dolores prospect located in South Australia. This

entailed the re processing of all of the original field data and seismic lines over the prospect area. This significant exercise

was carried out in our Houston office. On its completion we conducted an AVO analysis on the area which confirmed the

evidence of hydrocarbons in two distinct areas via bright spots and AVO reflection. The results of this highly detailed work

were made public in the recent Scott Pickford report which gave a P2 reserve of 543 BCF Gas in Place. This is clearly a

substantial asset and the Company has commenced active discussions with potential farm in or joint venture partners. The

asset is located some 40 KM West of the Moomba to Adelaide pipeline and is therefore not stranded gas, but rather a

commercially exploitable reserve that can taken to the growing market of South East Australia. Additionally, gas prices are

rising in Australia and the market is moving towards less price regulation over time. The Company is in the final stages of

Native Title deliberation and is highly confident of a successful outcome in the next several months.

As part of its growth strategy, Meridian has been keen to seek out development projects within the USA with significant

upside, preferably onshore. Within this context the Company examined various opportunities and eventually confirmed a

substantial opportunity located in the Warrior Basin, Alabama. In order to take this opportunity to the next level the Company

commissioned a detailed feasibility study from an internationally renowned consultant in the area. This study revealed a Coal

Bed Methane (“CBM”) project with a potential gas reserve likely to be in excess of 1 TCF. This study was in turn reviewed

by Scott Pickford and the results of which were made available to the public market in May 2006. At this time the Company

{ 4 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 4

M E R I D I A N P E T R O L E U M P L C

Chief Executive’sOfficer’s Statement& Reviewof Operations

is commencing leasing of an initial footprint that will in turn be utilized for the proposed pilot project. The pilot project is likely

to take the form of a ten well pilot scheme designed to test various areas of the project and not least of all the production of

gas on a commercial basis. The project is located in an area of mature production and also an area with abundant

infrastructure enabling the gas to get to market on advantageous commercial terms. We have great confidence in the

potential of this project and look forward to developing the Pilot Scheme as the first phase later in 2006.

The Company's Working Interests in Proven, Probable and Prospective Reserves

The Companies working interest in proven and probable reserves as at 31 December 2005 were:

Total BOE Oil bbl Gas mmcf

Reserves at 31 December 2004 443,399 30,733 2,476

Revisions -208,430 13,741 -1,333

Acquisitions 379,422 46,249 1,999

Production -9,741 0 -58

Reserves at 31 December 2005 604,650 90,723 3,084

The reserves at 31 December have been derived by Scott Pickford and include the Calvin (Sligo-Pettet),

Victory 21 and Orion 36 licenses. In addition to the probable reserves above, Scott Pickford identified

the following prospective resources:

Prospective Resources (P50) Total BOE Oil bbl Gas mmcf

Calvin (Rodessa) 280,975 55,470 1,353

Milford 36 78,082 54,898 139

Emery Hudson 40,738 12,987 167

Delores (Australia) 72,000,000 432,000

Total 72,399,795 123,355 433,659

The above Reserves and Resources are based on certain assumptions which are described in the Scott Pickford Valuation

Update Report dated April 2006.

Summary

In conclusion, Meridian has made significant progress towards the securing of larger commercial assets as evidenced by

Australia, CBM in the Warrior Basin and potentially deep gas at Calvin. Over the course of the year the smaller US assets

will be brought on line as cash producers, but more importantly the development of Dolores in Australia will commence as

will work in the Warrior Basin. Despite the frustrations of 2005, Meridian has been able to position itself for a sustained effort

in 2006 with the identification and securing of larger assets. The focus in future will not be on the development of smaller

assets but rather on these larger assets that will provide more significant long term value to shareholders.

Anthony Mason

Date: 28 June 2006

{ 5 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 5

M E R I D I A N P E T R O L E U M P L C

Directors’Report

The Directors present their report together with the audited financial statements for the year ended 31 December 2005.

Principal Activities

The Group’s activities are the exploration and production of oil and gas.

Business Review

A review of the Group’s trading during the period is contained in the Chief Executive Officer’s Statement and Review of

Operations on page 3 to 5.

There was a Group loss after taxation for the period of £872,307 (2004: £1,081,100). The Directors do not recommend

a dividend.

Directors

The interests of the directors in office at 6 June 2006 and their families in the shares of the company throughout the

year ended 31 December 2005 were as follows:

Number of Shares Number of Warrants

31 December 2005 31 December 2004

Donald Caldwell 400,000 450,000

Anthony Mason 24,700,000 24,700,000 2,240,124

Peter Clutterbuck - -

Post Balance Sheet Events

(1) On 20 February 2006 the Company completed the placing of 7,171,426 ordinary shares at 14p per share

raising £1,004,000.

(2) On 24 April 2006 the Company issued 1,140,000 ordinary shares at 30p per share pursuant to an exercise

of warrants raising £342,000.

(3) On 19 May 2006 the Company issued 300,000 ordinary shares at 10p per share pursuant to an exercise of

options raising £30,000.

Directors’ Responsibilities for the Financial Statements

The directors are responsible for ensuring that the directors' report and other information included in the annual report

is prepared in accordance with company law in the United Kingdom.

United Kingdom company law requires the directors to prepare financial statements for each financial year which give

a true and fair view of the state of affairs of the company and the group and of the profit or loss of the group for that

period. In preparing those financial statements, the directors are required to:

{ 6 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 6

M E R I D I A N P E T R O L E U M P L C

Directors’Report

- select suitable accounting policies and then apply them consistently

- make judgements and estimates that are reasonable and prudent

- state whether applicable accounting standards have been followed, subject to any material departures

disclosed and explained in the financial statements

- prepare the financial statements on the going concern basis unless it is inappropriate to presume that the

company will continue in business.

The directors are responsible for maintaining proper accounting records, for safeguarding the assets of the group and

for taking reasonable steps for the prevention and detection of fraud and other irregularities.

Legislation in the United Kingdom governing the preparation and dissemination of the financial statements and other

information included in annual reports may differ from legislation in other jurisdictions.

The Annual Report will be available on the company’s website.

The maintenance and integrity of the web site is the responsibility of the directors; the work carried out by the auditors

does not involve consideration of these matters and, accordingly, the auditors accept no responsibility for any changes

that may have occurred to the information contained in the financial statements since they were initially presented on

the web site.

Substantial Shareholders

At 20 June 2006 the following had an interest in 3% or more of the nominal value of the company's shares:

Name Shareholding %

Mellon Nominees UK Limited 15,127,334 20.81%

HSBC Global Custody Nominee UK Limited 7,639,900 10.51%

HSDL Nominees Limited 7,329,437 10.08%

Barclayshare Nominees Ltd 6,333,389 8.71%

TD Waterhouse Nominees Europe Limited 6.068.699 8.35%

L R Nominees Limited 3,431,183 4.72%

Raven Nominees Limited 2,350,000 3.23%

Tony Mason holds a total of 24,700,000 (34%) shares which are held in the name of Mellon Nominees and HSBC Global

Custody Nominees and in other nominee companies.

{ 7 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 7

M E R I D I A N P E T R O L E U M P L C

Directors’Report

Payment Policy and Practice

It is the company's normal practice to settle the terms of payment when agreeing the terms of the transaction, to ensure

that suppliers are aware of those terms, and to abide by them. Trade creditors at the period end amount to 36 days

(2004: 47) of average supplies for the period.

Financial risk management objectives and policies

The Company has to date financed its operations from internally generated cash flows and equity issues. It raises

additional equity funds in pounds sterling and pays for exploration and development costs in US$. To date, the company

has chosen not to hedge this exchange rate risk. The company reviews its financing requirements and its hedging policy

when required. For further details refer to note 19.

Third Party Indemnities

The Company has taken out Directors and Officers Insurances.

Related parties

The Company has entered into related party transactions, the details of which are outlined in note 23.

Auditors

Grant Thornton UK LLP offer themselves for reappointment as auditors in accordance with section 385 of the

Companies Act 1985.

Annual General Meeting

The Annual General Meeting will be held on 27 July 2006 at 42 Berkeley Square, London W1.

ON BEHALF OF THE BOARD

A. Mason

Director

28 June 2006

{ 8 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 8

M E R I D I A N P E T R O L E U M P L C

Report of theIndependentAuditorsto the Members ofMeridian Petroleumplc

We have audited the group and parent company financial statements (the "financial statements") of Meridian Petroleum plc

for the year ended 31 December 2005 which comprise the principal accounting policies, the group profit and loss account,

the group and company balance sheets, the group statement of total recognised gains and losses and notes 1 to 21. These

financial statements have been prepared under the accounting policies set out therein.

This report is made solely to the company’s members, as a body, in accordance with Section 235 of the Companies Act

1985. Our audit work has been undertaken so that we might state to the company’s members those matters we are required

to state to them in an auditors' report and for no other purpose. To the fullest extent permitted by law, we do not accept or

assume responsibility to anyone other than the company and the company’s members as a body, for our audit work, for this

report, or for the opinions we have formed.

Respective responsibilities of directors and auditors

The directors' responsibilities for preparing the Annual Report and the financial statements in accordance with United

Kingdom law and Accounting Standards (United Kingdom Generally Accepted Accounting Practice) are set out in the

Statement of Directors' Responsibilities.

Our responsibility is to audit the financial statements in accordance with relevant legal and regulatory requirements and

International Standards on Auditing (UK and Ireland).

We report to you our opinion as to whether the financial statements give a true and fair view, whether they are properly

prepared in accordance with the Companies Act 1985 and whether the information given in the Directors' Report is not

consistent with the financial statements. We also report to you if, in our opinion, the company has not kept proper accounting

records, if we have not received all the information and explanations we require for our audit, or if information specified by

law regarding directors' remuneration and other transactions is not disclosed.

We read other information contained in the Annual Report, and consider whether it is consistent with the audited financial

statements. This other information comprises only the Directors' Report and the Chief Executive's Statement and Review of

Operations. We consider the implications for our report if we become aware of any apparent misstatements or material

inconsistencies with the financial statements. Our responsibilities do not extend to any other information.

Basis of audit opinion

We conducted our audit in accordance with International Standards on Auditing (UK and Ireland) issued by the Auditing

Practices Board. An audit includes examination, on a test basis, of evidence relevant to the amounts and disclosures in the

financial statements. It also includes an assessment of the significant estimates and judgments made by the directors in the

{ 9 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 9

M E R I D I A N P E T R O L E U M P L C

Report of theIndependentAuditorsto the Members ofMeridian Petroleumplc

preparation of the financial statements, and of whether the accounting policies are appropriate to the company's

circumstances, consistently applied and adequately disclosed.

We planned and performed our audit so as to obtain all the information and explanations which we considered necessary in

order to provide us with sufficient evidence to give reasonable assurance that the financial statements are free from material

misstatement, whether caused by fraud or other irregularity or error. In forming our opinion we also evaluated the overall

adequacy of the presentation of information in the financial statements.

Opinion

In our opinion:

• the financial statements give a true and fair view, in accordance with United Kingdom Generally Accepted

Accounting Practice, of the state of the group's and the parent company's affairs as at 31 December 2005 and

of the group's loss for the year then ended;

• the financial statements have been properly prepared in accordance with the Companies Act 1985; and

Emphasis of matter - carrying value of tangible fixed assets

In forming our opinion, which is not qualified, we have considered the adequacy of the disclosures made in note 9 to the

financial statements concerning the carrying value of tangible fixed assets. The assets concerned relate to the capitalised

exploration and development costs of the Emery Hudson field, where production commenced during 2004 but was

suspended during 2005 pending a step out well which proved unsuccessful. Further analysis has been performed by the

company to identify a re-entry point, and exploration activities are expected to resume in the third quarter of 2006. The

outcome of these activities is uncertain, however the directors are of the opinion that the carrying value of these assets is

currently supported.

GRANT THORNTON UK LLP

REGISTERED AUDITORS

CHARTERED ACCOUNTANTS

Segensworth

28 June 2006

{ 1 0 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 10

M E R I D I A N P E T R O L E U M P L C

ConsolidatedProfit andLoss AccountFor the year ended31 December 2005

2005 2004

Restated

Note £ £

Turnover 1

Continuing operations 87,703 -

Acquisitions - 355,982

87,703 355,982

Cost of sales

Continuing operations (114,824)

Acquisitions - (119,172)

Gross profit (27,121) 236,810

Other operating charges (net)

Continuing operations (857,672) (397,512)

Acquisitions - (939,195)

Operating Loss

Continuing operations (884,793) (397,512)

Acquisitions - (702,385)

(884,793) (1,099,897)

Interest receivable 2 12,486 18,797

Loss on Ordinary Activities Before Taxation 3 (872,307) (1,081,100)

Tax on ordinary activities 5 - -

Loss for the financial year (872,307) (1,081,100)

Loss per share (pence) 7 (1.4) (2.4)

The 2004 comparative figures have been restated to represent the foreign currency differences arising from the re-

translation of the net investment in foreign subsidiaries (previously reported by inclusion in “Other operating charges”)

as a movement in reserves (profit and loss account).

{ 1 1 }

The accompanying accounting policies and notes form an integral part of these financial statements.

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 11

M E R I D I A N P E T R O L E U M P L C

ConsolidatedStatement of TotalRecognised Gainsand LossesFor the year ended31 December 2005

2005 2004

Restated

£ £

Loss for the financial year (872,307) (1,081,100)

Currency differences on foreign currency net investments 107,167 (92,444)

Total gains and losses recognised since last financial statements (765,140) (1,173,544)

2005 2004

Restated

£ £

Loss for the financial year (872,307) (1,081,100)

Foreign currency translation difference on investment in foreign subsidiary 107,167 (92,444)

Share options granted - 206,000

Profit and loss account (765,140) (967,544)

Issue of shares (net of costs) 654,856 4,346,942

Net (decrease) / increase in shareholders’ funds (110,284) 3,379,398

Shareholders’ funds at beginning of period 3,379,398 -

Shareholders’ funds at 31 December 2005 3,269,114 3,379,398

The 2004 comparative figures have been restated to represent the foreign currency differences arising from the re-

translation of the net investment in foreign subsidiaries (previously reported by inclusion in “Other operating charges”)

as a movement in reserves (profit and loss account).

Reconciliation ofMovements inShareholders’ FundsFor the year ended31 December 2005

{ 1 2 }

The accompanying accounting policies and notes form an integral part of these financial statements.

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 12

M E R I D I A N P E T R O L E U M P L C

ConsolidatedBalance SheetAt 31 December 2005

2005 2004

Note £ £

Fixed assets

Intangible assets

- Exploration costs and leases 8 246,978 577,194

Tangible Assets 9 2,939,924 2,026,896

Total Fixed Assets 3,186,902 2,604,090

Current assets

Debtors 11 80,190 259,093

Cash at bank and in hand 217,779 742,036

Total current assets 297,969 1,001,129

Creditors: amounts falling due within one year 12 (215,757) (225,821)

Net current assets 82,212 775,308

Total assets less current liabilities 3,269,114 3,379,398

Capital and reserves

Called up share capital 14 3,204,660 2,829,660

Share premium account 15 1,797,138 1,517,282

Profit and loss account 15 (1,732,684) (967,544)

Total equity shareholders’ funds 3,269,114 3,379,398

The financial statements were approved by the Board of Directors on 28 June 2006

Director

Date: 28 June 2006

{ 1 3 }

The accompanying accounting policies and notes form an integral part of these financial statements.

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 13

M E R I D I A N P E T R O L E U M P L C

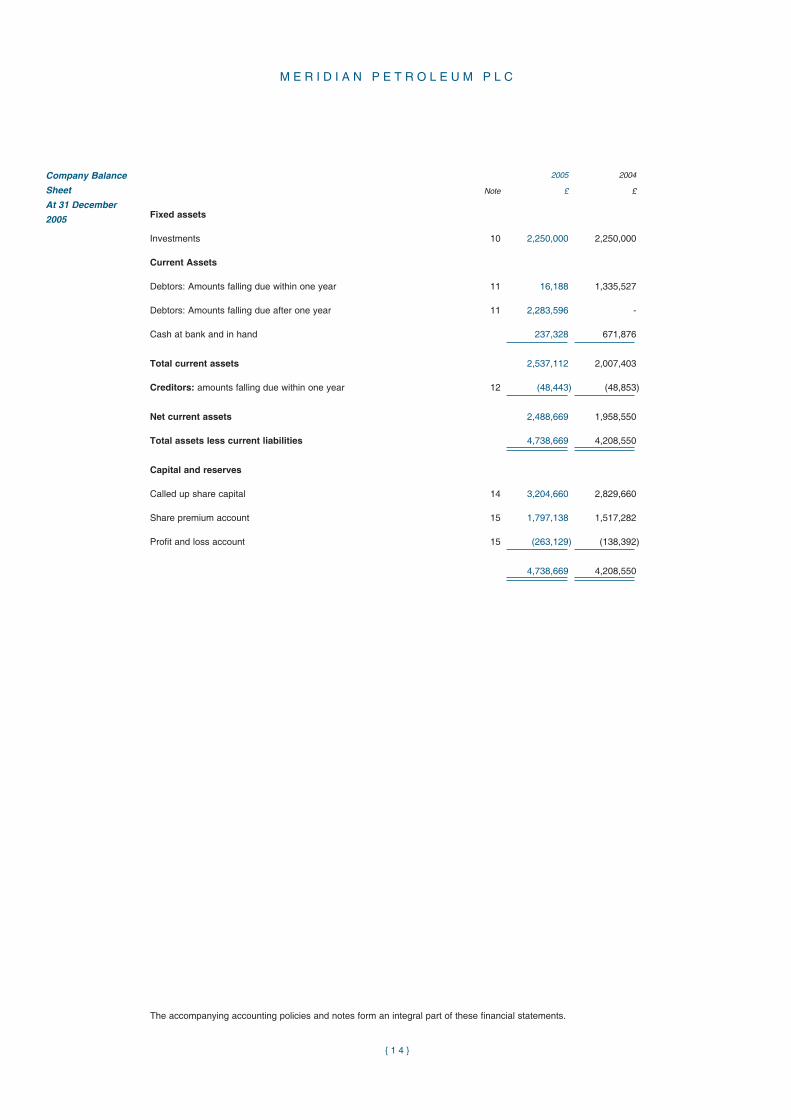

Company BalanceSheetAt 31 December2005

2005 2004

Note £ £

Fixed assets

Investments 10 2,250,000 2,250,000

Current Assets

Debtors: Amounts falling due within one year 11 16,188 1,335,527

Debtors: Amounts falling due after one year 11 2,283,596 -

Cash at bank and in hand 237,328 671,876

Total current assets 2,537,112 2,007,403

Creditors: amounts falling due within one year 12 (48,443) (48,853)

Net current assets 2,488,669 1,958,550

Total assets less current liabilities 4,738,669 4,208,550

Capital and reserves

Called up share capital 14 3,204,660 2,829,660

Share premium account 15 1,797,138 1,517,282

Profit and loss account 15 (263,129) (138,392)

4,738,669 4,208,550

{ 1 4 }

The accompanying accounting policies and notes form an integral part of these financial statements.

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 14

M E R I D I A N P E T R O L E U M P L C

ConsolidatedCash FlowStatementFor year ended31 December 2005

2005 2004

Note £ £

Net cash outflow from operating activities’ 16 (599,020) (698,079)

Returns on investments and servicing of finance

Interest received 12,486 18,797

Net cash inflow from returns on investments and servicing of finance 12,486 18,797

Capital expenditure and financial investment

Exploration and development expenditures (653,555) (763,047)

Sales proceeds from re-determination of interest 60,976 -

Net cash outflow from capital expenditure and financial investment (592,579) (763,047)

Acquisitions and disposals

Net cash acquired with subsidiary undertakings - 87,424

Net cash outflow before financing (1,179,113) (1,354,905)

Financing

Issue of shares 750,000 2,478,208

Expenses paid in connection with share issues (95,144) (381,267)

Net cash inflow from financing 654,856 2,096,941

(Decrease) / Increase in cash (524,257) 742,036

{ 1 5 }

The accompanying accounting policies and notes form an integral part of these financial statements.

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 15

M E R I D I A N P E T R O L E U M P L C

Accounting Policies Basis of Preparation

The financial statements have been prepared under the historical cost convention and in accordance with applicable UK

Accounting Standards and the Statement of Recommended Practice “Accounting for Oil and Gas Exploration,

Development, Production and Decommissioning Activities” revised in June 2001 (the SORP).

In preparing the financial statements for the current year, the group has adopted the following Financial Reporting

Standards:

- the presentation requirements of FRS 25 Financial Instruments: Disclosure and Presentation

This Standard requires financial instruments to be presented in accordance with their substance. Therefore

shares, which previously were always presented as part of shareholders' funds regardless of the substance of

the instrument, may now be presented as a liability when in substance that share is equivalent to a liability.

There have been no adjustments to the financial statements of the company on adoption of this standard.

- FRS 21: Events after the balance sheet date

The adoption of FRS 21 has resulted in a change in accounting policy in respect of proposed equity dividends.

If the company declares dividends to the holders of equity instruments after the balance sheet date, the

company does not recognise those dividends as a liability at the balance sheet date. Previously where these

equity dividends were proposed after the balance sheet date but before authorisation of the financial statements

they were recorded as liabilities at the balance sheet date. As no dividend is proposed nor been paid no

adjustment has been required to the financial statements for this year nor for the year ended 31 December

2004.

The principal accounting policies of the group, which are considered to be most appropriate to the group’s circumstances,

are set out below.

Basis of Consolidation

The consolidated financial statements incorporate the financial statements of Meridian Petroleum plc and its subsidiaries.

The results of subsidiaries are included from the date of acquisition, on an acquisition accounting basis.

Turnover

The Company’s development and production activities are operated by Wellmaster Production Company LLC. Turnover

represents the Company’s share of sales of oil and gas during the year, excluding sales tax and royalties, and is recognised

on the basis of the group’s working interest when title passes to the customer. All turnover arises in the USA.

{ 1 6 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 16

M E R I D I A N P E T R O L E U M P L C

Accounting Policies Exploration and Development Costs

In accordance with the successful efforts method as set out in the SORP, expenditure including related overheads on the

acquisition, exploration and evaluation of interests in licences not yet transferred to a cost pool is capitalised under

intangible assets and not amortised. Cost pools are established on the basis of specific fields. When it is determined that

such costs will be recouped through successful development and exploitation or alternatively by sale of the interest,

expenditure will be transferred to tangible assets.

Amortisation and Depletion

Exploration and development costs transferred to tangible assets are depreciated over the expected productive life of the

asset using a unit of production basis.

An impairment test will be performed whenever there is an indication that the net book value amount in respect of a project

may no longer be recoverable, and any necessary provision charged through the profit and loss account. The directors

have considered the carrying values of capitalised exploration and development costs as at 31 December 2005 and their

conclusions are documented under Note 9.

Investments

Investments are included at cost less amounts written off.

Deferred Taxation

Deferred tax is recognised on all timing differences where the transactions or events that give the group an obligation to

pay more tax in the future, or a right to pay less tax in the future, have occurred by the balance sheet date. Deferred tax

assets are recognised when it is more likely than not that they will be recovered. Deferred tax is measured using rates of

tax that have been enacted or substantively enacted by the balance sheet date.

Foreign Currencies

Transactions in foreign currencies are translated at the exchange rate ruling at the date of the transaction. Monetary

assets and liabilities in foreign currencies are translated at the rates of exchange ruling at the balance sheet date. The

financial statements of foreign subsidiaries are translated at the rate of exchange ruling at the balance sheet date.

Change in accounting policy

The directors consider that, in line with their conclusion that amounts due from group companies will not be repaid within

one year, the accounting policy should be modified such that the exchange differences arising from the retranslation of the

net investment in subsidiaries, as at December 31, funded by loans from the Company, are taken directly to reserves.

The impact of this change is to credit foreign exchange differences of £107,167 (2004 restated: charge £92,444) to reserves

rather than to the profit and loss account. All other exchange differences are dealt with through the profit and loss account.

{ 1 7 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 17

M E R I D I A N P E T R O L E U M P L C

Accounting policies Financial Instruments

Financial assets are recognised in the balance sheet at the lower of cost and net realisable value. Provision is made for

diminution in value where appropriate.

Interest receivable and payable is accrued and credited or charged to the profit and loss account in the period to which it

relates.

Liquid Resources

Liquid resources comprise funds on deposit at not less than 7 days’ notice.

Operating leases

Rentals payable under operating leases are taken to the profit and loss statement on a straight line basis over the period

of the lease.

{ 1 8 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 18

M E R I D I A N P E T R O L E U M P L C

Notes to theAccounts

1 Turnover and Loss on Ordinary Activities Before Taxation

The turnover of £87,703 is attributable to one segment, namely oil and gas production and all arises in USA.

Net assets and profit before tax all apply to the one business segment.

The geographical breakdown of net assets and net operating loss is:

Net Assets Loss before tax

2005 2004 2005 2004

Restated

£ £ £ £

UK 177,049 597,164 (465,451) (645,583)

USA 3,092,065 2,771,815 (388,800) (365,989)

Australia - 10,419 (18,056) (69,528)

Total 3,269,114 3,379,398 (872,307) (1,081,100)

2 Interest receivable and similar income

2005 2004

£ £

Bank and short term interest 12,486 18,797

3 Operating Loss

Loss on ordinary activities before taxation is stated after charging:

2005 2004

£ £

Amortisation and depreciation 45,701 83,020

Profit on disposal of assets 48,329 -

Auditors’ remuneration

Audit 46,769 17,000

Non-audit - 3,000

Taxation 20,481 3,459

Rentals payable in respect of land and buildings 33,000 22,297

In addition, in 2004, £71,289 was charged against the share premium account in respect of Reporting

Accountant fees paid to Grant Thornton UK LLP on the AIM flotation of the Company

{ 1 9 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 19

M E R I D I A N P E T R O L E U M P L C

Notes to theAccounts

4 Directors and Employees

Staff costs (excluding non executive directors) during the year were as follows:

2005 2004

£ £

Wages and salaries 186,666 176,406

Social security costs 8,116 7,172

194,782 183,578

The average number of employees during the year was: 2.

Remuneration in respect of directors was as follows:

2005 2004

£ £

Emoluments (including amounts paid to third parties) 222,984 295,571

In addition to the above, a UITF 17 charge of £Nil (2004: £206,000) has been made to the profit and loss

account in respect of share options granted to the directors

There are no Company pension schemes.

The amounts set out above include remuneration of £120,000 (2004: £122,206) in respect of the highest paid

director.

5 Tax on Loss on Ordinary Activities

No liability in respect of corporation tax arises as a result of trading losses.

US tax losses to be carried forward as at 31 December 2005 at the standard rate of US corporation tax of

34% (2004: 35%) amount to £1,392,777 (2004: £501,384)

UK tax losses to be carried forward as at 31 December 2005 at the standard rate of UK corporation tax of

30% (2004: 30%) amount to £875,611 (2004: 352,850)

No deferred tax asset has been recognised in respect of losses carried forward since the recognition criteria

of FRS19 are not met.

{ 2 0 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 20

M E R I D I A N P E T R O L E U M P L C

Notes to theAccounts

Tax reconciliation

2005 2004

£ £

Loss on ordinary activities before taxation (872,307) (1,081,100)

Loss on ordinary activities before taxation multiplied by the average of the standard rate of UK corporation tax (30%) and the standard rate of USA federal income tax (34%) 278,092 385,830

Tax effects of

Temporary timing differences - (61,800)

Losses not utilised 278,092 324,030

6 Loss for the year

The Company has taken advantage of Section 320 of the Companies Act 1985 and has not included its own

profit and loss account in these financial statements. The Company loss for the year was (£124,737) (2004

£344,392).

7 Loss per Share

The calculation of the basic loss per share is based on the loss attributable to ordinary shareholders of

£872,307 (2004 £1,081,100) divided by the weighted average number of shares in issue during the year of

59,718,193 (2004 45,178,443).

The outstanding warrants and options (Note 15) are anti-dilutive and hence no diluted loss per share is

presented.

8 Intangible fixed assets

The Group

Cost

2005 2004

£ £

North America Australia Total North America Australia Total

At beginning of period 577,194 15,250 592,444 - - -

Currency translation adjustment 77,574 - 77,574 - - -

Additions in the period 461,730 - 461,730 458,321 15,250 473,571

Acquisition of subsidiary - - - 118,873 - 118,873

Disposals (12,647) - (12,647) - - -

Amounts written off (124,642) - (124,642)

Transfers to tangible assets (Note 9)(732,231) - (732,231) - - -

At 31 December 2005 246,978 15,250 262,228 577,194 15,250 592,444

{ 2 1 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 21

M E R I D I A N P E T R O L E U M P L C

Notes to theAccounts

Amortisation

2005 2004

£ £

North America Australia Total North America Australia Total

At beginning of period - 15,250 15,250 - - -

Charge for the year - - - - 15,250 15,250

At 31 December 2005 - 15,250 15,250 15,250 15,250

Net book value

2005 2004

£ £

North America Australia Total North America Australia Total

At 31 December 246,978 - 246,978 577,194 - 577,194

9 Tangible fixed assets

The Group

Cost

Oil and Gas Assets

2005 2004

£ £

At beginning of period 2,094,666 -

Currency translation adjustment 34,673 -

Additions in the period 191,825 289,476

Acquisitions - 1,805,190

Transfers from intangible assets (Note 8) 732,231 -

At 31 December 3,053,395 2,094,666

Depletion

Oil and Gas Assets

2005 2004

£ £

At beginning of period 67,770 -

Currency translation adjustment 1,174 -

Charge for the year 44,527 67,770

At 31 December 113,471 67,770

{ 2 2 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 22

M E R I D I A N P E T R O L E U M P L C

Notes to theAccounts

Net book value

Oil and Gas Assets

2005 2004

£ £

At 31 December 2,939,924 2,026,896

All of the oil and gas assets are located in North America.

During 2004, the Group acquired interests in six oil and gas exploration and production properties.

Under the acquisition accounting method adopted in the 2004 financial statements, the assets acquired

were recorded at their fair values, with a substantial part of the consideration being allocated to tangible

fixed assets, specifically, to those assets relating to the Emery Hudson field, where production had

commenced. This asset equates to the value of tangible fixed assets on the balance sheet as at 1 January

2005 and was identified by the Competent Person's report, produced on admission to AIM, as being the

only asset with proven reserves. No fair value adjustment was assigned to intangible assets in respect of

the probable reserves.

In October 2005, the Company announced that the step out well on Emery Hudson had not been

successfully completed as a producer and that more work would be undertaken to find a suitable re-entry

point with the intent of bringing the field back into production. It transpires that the geological structure of

the Emery Hudson reserve appears likely to have a degree of compartmentalisation. This work has been

completed with positive indicators, and exploration operations, which are anticipated to lead to renewed

production on this field, are expected to commence in the third quarter of 2006 to confirm these initial

results.

The Directors have commissioned a detailed review of the Group's reserves by their consultants ECL Scott

Pickford. On the basis of consultation with Scott Pickford in conjunction with a review of other data

analyses available, they have taken the view that the carrying value of Emery Hudson and the other assets

is still supported. This will be reviewed regularly and could change as a result of further exploration and

development activity over the coming months given the inherent uncertainties involved in oil and gas

activities.

During 2005 a transfer has been made from intangible to tangible fixed assets in respect of the capitalised

oil and gas development costs relating to the Calvin field where significant probable reserves were

identified in the 2004 Competent Persons report. The directors consider that commerciality of the field was

established in 2005, and that these assets should therefore be reclassified as tangible under the provisions

of the SORP.

{ 2 3 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 23

M E R I D I A N P E T R O L E U M P L C

Notes to theAccounts

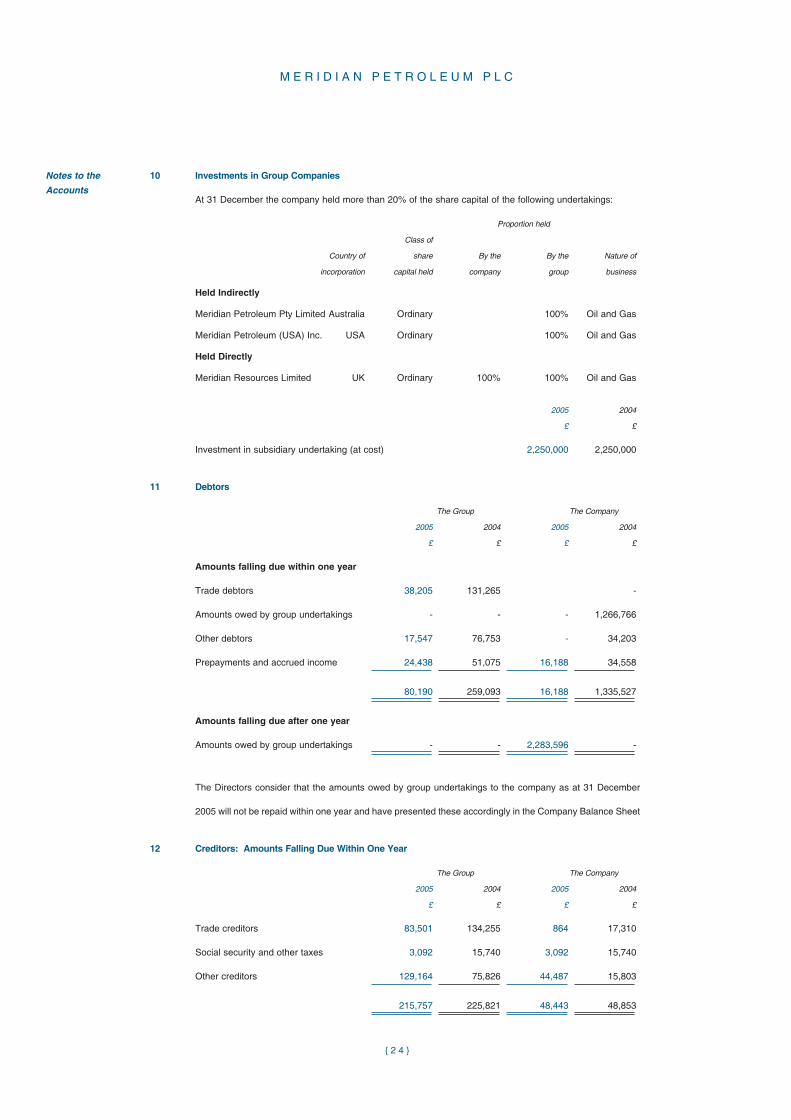

10 Investments in Group Companies

At 31 December the company held more than 20% of the share capital of the following undertakings:

Proportion held

Class of

Country of share By the By the Nature of

incorporation capital held company group business

Held Indirectly

Meridian Petroleum Pty Limited Australia Ordinary 100% Oil and Gas

Meridian Petroleum (USA) Inc. USA Ordinary 100% Oil and Gas

Held Directly

Meridian Resources Limited UK Ordinary 100% 100% Oil and Gas

2005 2004

£ £

Investment in subsidiary undertaking (at cost) 2,250,000 2,250,000

11 Debtors

The Group The Company

2005 2004 2005 2004

£ £ £ £

Amounts falling due within one year

Trade debtors 38,205 131,265 -

Amounts owed by group undertakings - - - 1,266,766

Other debtors 17,547 76,753 - 34,203

Prepayments and accrued income 24,438 51,075 16,188 34,558

80,190 259,093 16,188 1,335,527

Amounts falling due after one year

Amounts owed by group undertakings - - 2,283,596 -

The Directors consider that the amounts owed by group undertakings to the company as at 31 December

2005 will not be repaid within one year and have presented these accordingly in the Company Balance Sheet

12 Creditors: Amounts Falling Due Within One Year

The Group The Company

2005 2004 2005 2004

£ £ £ £

Trade creditors 83,501 134,255 864 17,310

Social security and other taxes 3,092 15,740 3,092 15,740

Other creditors 129,164 75,826 44,487 15,803

215,757 225,821 48,443 48,853

{ 2 4 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 24

M E R I D I A N P E T R O L E U M P L C

Notes to theAccounts

13 Deferred Taxation

No deferred tax asset has been recognised on losses carried forward (see note 6). There is no provided or

unprovided deferred tax liability.

14 Share Capital

2005 2004

£ £

Authorised

150,000,000 ordinary shares of 5p each 7,500,000 7,500,000

Allotted, called up and fully paid

64,093,193 (2004: 56,593,193) ordinary shares of 5p each 3,204,660 2,829,660

During the year the company allotted shares with an aggregate nominal value of £375,000 as follows:

Nature of consideration

Share Capital Share Premium

Price per Share Number £ £

Cash (share placing)

10p 7,500,000 375,000 375,000

The Company has granted warrants to subscribe for shares as follows:

Exercised

Granted in or lapsed in At 31

Exercise price the period the period December 2005

Warrants expiring 20 July 2007 30p 3,940,154

The Company has granted options to subscribe for 1,030,000 shares at 10p exercisable up to 20 July 2007.

{ 2 5 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 25

M E R I D I A N P E T R O L E U M P L C

Notes to theAccounts

15 Share Premium Account and Reserves

The Group

Share premium account Profit and loss account

2005 2004 2005 2004

£ £ £ £

At beginning of period 1,517,282 - (967,544) -

Retained loss for the year - - (872,307) (1,081,100)

Premium on allotment during the year 375,000 1,898,548 - -

Share issue costs (95,144) (381,266) - -

Share options granted - - - 206,000

Foreign currency investment translation - - 107,167 (92,444)

At 31 December 1,797,138 1,517,282 (1,732,684) (967,544)

The Company

Share premium account Profit and loss account

2005 2004 2005 2004

£ £ £ £

At beginning of period 1,517,282 - (138,392) -

Retained loss for the period - - (124,737) (344,392)

Premium on allotment during the year 375,000 1,898,548 - -

Share issue costs (95,144) (381,266) - -

Share options granted - - - 206,000

At 31 December 1,797,138 1,517,282 (263,129) (138,392)

{ 2 6 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 26

M E R I D I A N P E T R O L E U M P L C

Notes to theAccounts

16 Net Cash Outflow from Operating Activities

2005 2004

£ £

Operating loss (884,793) (1,099,897)

Amortisation - 15,250

Depletion 45,701 67,770

Write off exploration and development costs initially capitalised 124,642 -

Gain on disposal of fixed assets (48,329) -

Foreign currency translation difference (5,080) (92,444)

Decrease / (Increase) in debtors 178,903 (19,696)

(Decrease) / Increase in creditors (10,064) 224,938

UITF 17 Stock options charge - 206,000

Net cash outflow from operating activities (599,020) (698,079)

17 Financial instruments

The Group has financed its operations from equity issues.

The Group uses financial instruments, other than derivatives, comprising cash, liquid resources and various

items, such as trade debtors, trade creditors, etc, that arise directly from its operations. The main purpose of

these financial instruments is to raise finance for the Group’s operations.

The Group has not entered into any derivative transactions such as interest rate swaps, forward rate

agreements or forward currency contracts. Funds in excess of immediate requirements are placed in sterling

deposits.

Short-term debtors and creditors have been excluded from all the following disclosures, other than the

currency risk disclosures.

In the normal course of its operations the Group is exposed to foreign currency, commodity price and interest

rate risks. The financial statements are produced in pounds sterling but much of its business is conducted in

US dollars. As a result it is subject to foreign currency exchange risk due to exchange rate movements, which

will affect the Group’s transaction costs and the translation of the results and underlying net assets of its

foreign subsidiaries.

The Group does not hedge its exposure of foreign investments held in foreign currencies.

The net monetary liabilities (2004: assets) held in the US at the year end amounted to $(154,000) (2004:

$290,000)

{ 2 7 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 27

M E R I D I A N P E T R O L E U M P L C

Notes to theAccounts

18 Contingent Liabilities

There were no contingent liabilities at 31 December 2005 (2004: Nil)

19 Operating Leases

There were commitments in respect of the lease of premises amounting to £2,750 (2004 £33,000) due within one

year and £Nil (2004 £2,750) due after one year.

20 Post Balance Sheet Events

(1) On 20 February 2006 the Company completed the placing of 7,171,426 ordinary shares at 14p per

share raising £1,004,000.

(2) On 24 April 2006 the Company issued 1,140,000 ordinary shares at 30p per share pursuant to an

exercise of warrants raising £342,000.

(3) On 19 May 2006 the Company issued 300,000 ordinary shares at 10p per share pursuant to an

exercise of options raising £30,000.

21 Transactions with Directors and Other Related Parties

Donald Caldwell has an interest in each of the Company’s US assets by virtue of his interests in Longwood

Exploration Company and Lodestar Energy, LLC. Donald Caldwell and his wife own the entire issued share capital

of Lodestar Energy, LLC and they are also the sole directors of the company. Donald Caldwell owns 40% of the

issued share capital of Longwood Exploration Company and is also a director and president of the company.

Longwood Exploration Company owns a 20% working interest (WI) and a 15.2% net revenue interest (NRI) in the

Emery Hudson field. Lodestar Energy LLC owns a 3.5% WI and a 2.66% NRI in the Emery Hudson field. In

addition, Donald Caldwell personally owns an overriding royalty interest in the lease of around 1.5%.

Longwood Exploration Company owns a 10% WI and a 7.5% NRI in the Brighton 36 prospect.

Longwood Exploration Company owns a 3.33% WI and a 2.5% NRI in the Calvin prospect. Donald Caldwell also

owns a small personal interest in the prospect.

Lodestar Energy, LLC and Longwood Exploration Company also held interests in the West Levees Creek and

Middleton Creek prospects.

The company has a consulting agreement with Lodestar Energy, LLC and during the year £63,984 (2004: £36,092)

was paid by the company under this agreement.

The company has a consulting agreement with Global Energy Consultants Limited which was paid £39,000 (2004:

£18,450) during the year. Peter Clutterbuck is a shareholder and director of Global Energy Consultants.

{ 2 8 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 28

M E R I D I A N P E T R O L E U M P L C

Notice ofAnnual GeneralMeeting

Notice is hereby given that the Annual General Meeting of the Meridian Petroleum Plc will be held on 27th July 2006 at

42 Berkeley Square, London W1J 5AW at 10.00 a.m. for the following purposes, namely:

Ordinary Business

As Ordinary Business, to consider and, if thought fit, pass the following resolutions which will be proposed as Ordinary

Resolutions:

1. To receive and adopt the Directors’ Report and the Financial Statements for the year ended 31 December

2005, together with the report of the auditors thereon.

2. To reappoint Grant Thornton UK LLP as auditors of the Company until the conclusion of the next Annual

General Meeting at which accounts for the Company are presented and to authorise the directors to

determine the Auditors’ remuneration.

3. To re-elect Donald Caldwell as a director of the Company, who retires in accordance with the Company’s

Articles of Association and offers himself for re-appointment.

4. To transact any other ordinary business.

Special Business

As Special Business 1 to consider and if thought fit to pass the following resolutions of which the resolution numbered

5 will be proposed as an ordinary resolution and the resolution numbered 6 will be proposed as a special resolution:

5. That the Directors be and they are hereby generally and unconditionally authorised in accordance with

section 80 of the Companies Act 1985 (the “Act”) to allot relevant securities (as defined in that section) up to

a maximum aggregate nominal amount of £1,250,000 and this authority will (unless renewed) expire at the

conclusion of the next Annual General Meeting of the Company but the Company may, before this authority

expires, make an offer or agreement which would or might require relevant securities to be allotted after the

authority expires and the Directors may allot relevant securities pursuant to such offer or agreement as if the

authority conferred hereby had not expired.

6. That the Directors be and they are hereby empowered pursuant to section 95 of the Act to allot equity

securities (within the meaning of section 94 of the Act) for cash pursuant to the authority conferred by

Resolution 5 above as if section 89(1) of the Act did not apply to any such allotment provided that this power

shall be limited to:

{ 2 9 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 29

M E R I D I A N P E T R O L E U M P L C

Notice ofAnnual GeneralMeeting

(a) the allotment of equity securities in connection with an issue in favour of the holders of ordinary shares

of the Company in proportion (as nearly as may be) to their respective holdings of ordinary shares,

subject only to exclusions or other arrangements which the Directors may deem necessary or

expedient to deal with fractional entitlements, legal or practical problems arising in any overseas

territory or the requirements of any regulatory body or stock exchange in any territory; and

(b) the allotment (otherwise than pursuant to sub-paragraph (a) above) of equity securities up to an

aggregate nominal amount of £1,250,000

and the power hereby granted shall expire at the conclusion of the next Annual General Meeting of the

Company save that the Company may before such expiry make an offer or agreement which would or might

require equity securities to be allotted after such expiry but otherwise in accordance with the foregoing

provisions of this power in which case the Directors may allot equity securities in pursuance of such offer or

agreement as if the power conferred hereby had not expired.

BY ORDER OF THE BOARD

Niel Redpath Registered Office:

Company Secretary 42 Berkeley Square

3 July 2006 London W1J 5AW

Notes:

1. Copies or particulars of contracts of service between directors and the company or any of its subsidiary undertakings will be available for

inspection by members at the registered office of the company during normal business hours from the date of this notice until 26 July

2006 and at the place of the Annual General Meeting for fifteen minutes prior to and until the conclusion of that meeting.

2. A Member entitled to attend and vote at the Meeting convened by this Notice is entitled to appoint one or more proxies to attend and, on

a poll, to vote in his or her stead. A proxy need not be a member of the Company. A form of proxy is enclosed. The appointment of a

proxy will not preclude a member from being present at the Meeting and voting in person if he or she should subsequently decide to do

so.

3. To be valid, forms of proxy must be lodged at the office of the Company’s registrars, The Causeway, Worthing, West Sussex BN99 6ZL,

not less than 48 hours before the meeting or any adjournment.

4. Pursuant to regulation 41 of the Uncertificated Securities Regulations 2001, members will be entitled to attend and vote at the meeting if

they are registered on the Company’s register of members 48 hours before the time appointed for the meeting or any adjournment

thereof.

{ 3 0 }

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 30

{ 3 1 }

M E R I D I A N P E T R O L E U M P L C

Form of ProxyFor AnnualGeneral Meeting

I ....................................................................................................................................... (Name(s) in full in block capitals)

of (address) .........................................................................................................................................................................

.............................................................................................................................................................................................

being a member of the above named Company hereby appoint ...............................................................................

of ............................................................. or, failing him/her the Chairman of the Meeting, as my proxy to vote for me on

my behalf in accordance with the instructions set out below at the Annual General Meeting of the Company to be held

on 27th July 2006 and at any adjournment thereof.

Please delete "Either" or "Or" below and mark "For" or "Against" as appropriate and return this form to the Company

Secretary. To be valid this form must be lodged with the Company’s registrars not less than 48 hours before the Meeting.

Either To vote as my Proxy or failing him/her as the Chairman thinks fit.

Or For Against

Resolution 1

Resolution 2

Resolution 3

Resolution 4

Resolution 5

Resolution 6

Signed .............................................................................................................................................................................

Name ..............................................................................................................................................................................

Date ...............................................................................................................................................................................

✂

PLEASE COMPLETE IF YOU DO NOT INTEND TO ATTEND IN PERSON

(Company No: 05104249)

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 31

SECOND FOLD

BUSINESS REPLY SERVICELicence No. SEA10846 1

Lloyds TSB RegistrarsThe CausewayWorthingWest SussexBN99 6ZL

THIRD FOLD & TUCK IN

DLO

FT

SRI

F

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 32

Printed by CGI (Europe)Ltd

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 33

Annual Report 2005 V3 PRINT.qxp 30/06/2006 14:44 Page 34