Embed Size (px)

Citation preview

Annual Report57T H Year of Activity

PKB Privatbank sa

2014

Governing bodies of PKB SA 4Board of Directors’ Report 8 Highlights 9

Consolidated Financial

Comments on the consolidated balance sheet 12 Comments on the income statement 13 Consolidated financial statements 14 Consolidated income statement 16 Consolidated cash flow statement 17 Annex to the consolidated annual financial statements 18 Auditors’ report 35

Parent Company Financial Statements

Comments on the balance sheet 39 Comments on the income statement 41 Financial Statements 42 Income Statement 44 Annex to the annual financial statements 46 Auditors' report 55

C o n t e n t s

Board of Directors Henry Peter 1) 3) Lugano (TI) Chairman

Maurizio Jesi Ferrari1) 2)4) Lugano (TI) Vice-Chairman Fernando Zari Malacrida1) 3) Gentilino (TI) Vice-Chairman

Edio Delcò Taverne - Torricella (TI)

Claudio Ferrari1) 3) Zug (ZG) Dieter Hauser2) 3) Zumikon (ZH) Jean-Philippe Rochat2) 3) Épalinges (VD)

Massimo Trabaldo Togna2) 5) Milan (I)

Secretary Elena Trabaldo Togna Conches (GE)

Internal Audit Mirko Angelini First Internal Auditor Diego Pecorone Internal Auditor

External Auditor Ernst & Young SA

Executive Board Umberto Trabaldo Togna Chief Executive OfficerFerdinando Coda Nunziante Managing DirectorLuca Soncini Managing DirectorLorenzo Tavola Executive Vice PresidentEnrico Tonella Executive Vice President

4

1) Member of the Executive Committee2) Member of the Audit Committee3) Independent directors pursuant to FINMA circular 08/244) Up to the General Meeting on 17/4/20145) From the General Meeting on 17/4/2014

G o v e r n i n g b o d i e s o f p k b s a

Senior Vice Roberto AlgisiPaolo AnastasiFiorenzo AndreolettiRoberto BertiPaolo BonacinaLuca BravinBernardo BrunschwilerGino Cardone Emanuele Carrassi del VillarGiovanni CastellinoPierluigi CroceOberto della Torre di LavagnaFrancesco DolfiFlavio FacchinMassimo FallettaAnthony Graves Raffaella JaquetNicolas MartinStefano NocchiLuca Parmeggiani Luciano PasqualiniCarlo PenatiAntonino Pisciotta Francesco PromuticoMatteo SaladinoSandro TreichlerLibero Valsangiacomo

Vice Francesco Alberio Presidents Sabine Amann

Felix ArnoldChristoph BenzGianluca BollaPaolo CalastriEros CalligherLucio CeribelliNicolò Dosi Delfini Heitor Duarte Villela René GrassiSascha Kever Catherine Kuhn Gabriele Larghi Andrea Luchetti

Alessandro LussoStefano MalteseRoberto PedrottiPierluigi PetrucciNicholas PorterRenzo RicciGiovanni Rickenbach Thorsten SackmannMario SalaAntonio SanchezMichele ScarmignanOlivier Selig Rolf Spannagel Marco Talleri

First Marco Bertagna Vice Presidents Paola Bolliger

Alessandro CavadiniCristina Chendi Giorgio CompagnoniFabio Conti Salvatore Dell'AiraFiorenzo IndiHans KundertAlessandro Lanzara Matteo LuratiDaniele MallozziMauro MarchesiStefano MarcotullioMassimo MattioliFilippo Moor Edy Muscionico Antonella PelizzariLuca Radaelli Emilio Re Carlo ReichlinPatrizia Rivera MariottiCarmine SalernoMarco Torino Tiziana Torri Marcello TronconiSergio VincentelliAndrea Zuccheri

PKB Geneva Director Gennaro Caracciolo di VietriPKB ZurichDirector René KaufmannPKB Bellinzona Director Dario SimoniPKB Lausanne Director a.i. Francesco DolfiPKB Privatbank Ltd AntiguaVice President Michele DelcòPKB Banca Privada (Panamá) SADirector Francesco Catanzaro

Management (Situation as at 1 April 2014)

Apprenticed in Casale with his father Pietro da Campanigo, Giovanni Martino Spanzotti is documented to have painted in Vercelli in 1481 and in 1490, and in Casale Monferrato after 1498. In 1501, he opened his workshop in Chivasso. In 1507, for Duke Carlo II of Savoia, he painted a copy (now lost) of the The Virgin of the House of Orleans masterpiece by Raphael painted the previous year. His production has been reconstructed beginning with the signed Madonna on Throne with St. Ubaldo and St. Sebastian (Galleria Sabauda in Turin), and compared against the cycle of frescoes of the Life of Christ in the church of San Bernardino in Ivrea 1480-1490. Characterized by a knowledge of Lombard (Vincenzo Foppa) and Provençal models (Enguerrand Quarton), the artist's works include the Tucher Madonna (Turin Civic Museum, 1475-1480 circa), whose composition was derived from a drawing by Francesco del Cossa for the stained glass in the San Martino al Monte Church in Bologna, and the Baptism of Christ (Turin Cathedral), painted in 1508 in cooperation with his student Defendente Ferrari.

Cut along their four sides, the panels came from one board (poplar?), with variable thicknesses (between about 1.5 and 2.5 cm). The upper and lower edges, where originally these were framed, are not painted. The gold background was decorated with large punched floral motifs (each with a diameter of about 5 cm), which were placed before insertion of the figures, whose outlines were applied to the gesso ground. The layer of paint film, relatively well preserved regardless of some faults coming through, reveals technical execution of great quality.

These panels make up the fragments of a predella, which was to depict Christ and his twelve apostles in different poses. Saint James the Lesser, whose tunic was originally decorated with a collar with gold motifs, holds a staff. Saint Peter is holding the keys and the book. The other two apostles are not as easy to identify. One, who seems to be reading a page, might be Saint Paul (generally represented along with the apostles). The other, whose cloak maintains some undecipherable inscriptions along its edge, rests his head on his left hand in a melancholic attitude. I propose to link these fragments with four others, which, defined by the same technical and stylistic features, originated from the same predella. These were published in 1975 by Michel Laclotte, who placed them between the Provence of Nicolas Dipre and the Piedmont of Giovanni Martino Spanzotti. The first three are preserved in the Esztergom Christian Museum, whilst the last was at one time in the collection of Alex Shaw.1

This predella, from which five figures are still missing, (Christ and four apostles), links back to a Piedmont tradition represented by Antoine de Lonhy, a Burgundy painter also active in Piedmont, who in the 1470s painted the Apostles found in the Turin Civic Museum and conceives the designs for the sculpted predella from an altar originating in the Sant'Orso Collegiate Church in Aosta (whose fragments are also preserved in the Turin Civic Museum). From a stylistic perspective, the panels purchased by PKB may be likened to the Giovanni Martino Spanzotti's juvenile works, specifically the two panels with four saints and a donor and four saints, which perhaps originated from the Val Vigezzo (Galleria Sabauda in Turin inv. numbers 1038 and 1039). Judging by their dimensions, I do not believe it can be excluded that the two paintings in Turin and the eight predella fragments reunited here, originally belonged to the same polyptych, which we can date around 1475-1480.

In addition, the punched motifs are similar to those in the Madonna on Throne with St. Ubaldo and St. Sebastian (Galleria Sabauda in Turin).

Frédéric Elsig (Università di Ginevra)

Giovanni Martino Spanzotti(Casale Monferrato, 1455 ca. –

Chivasso, 1526/1528)

Four Apostles 1475-1480 circa

Tempera and gold on panel (poplar?), 22.9 x 16.8 cm (San Pietro)

et 22.9 x 20.3 cm (the other three)Origin: Christie’s, New York, NY,

29 January, 2014, LOT 146

p k b c o l l e c t i o n

1 M. Laclotte, «A propos de quelques primitifs méditerranéens», in Etudes d’art français offertes à Charles Sterling, edited by A. Châtelet and N. Reynaud, Parigi, 1975, pp. 145-150.

2 G. Romano, file in the Superintendency of the Galleries and Works of Art of Piedmont. Recoveries and new acquisitions, exhibition catalogue, Turin, 1975, pp. 12-15.

B o a r d o f d i r e c t o r s ’ r e p o r t

Dear Shareholders,The year 2014 was distinguished by an acceleration of the economic recovery in the United States of America and by a timid return to growth in most of the Eurozone countries.In terms of the financial markets, 2014 was a year of contrasts with the American markets showing gains of better than 10%, European markets on average making moderate gains with the world's emerging markets generally down. The bond markets were marked by a decrease in the yields of the ten-year maturities.As concerns currency trends, exchange rate ratios between chf and eur were marked by the appreciation of the usd and in a smaller measure by that of related currencies (nzd, gbp, aud and can) and by a drop in the Scandinavian currencies (nok and sek).In July, the price of oil started its strong downward trend bringing it to nearly half its previous value and putting the major oil producing countries and industry companies under significant pressure. The crude oil price trends, together with the sanctions imposed on Russia by western nations due to the situation in the Ukraine, triggered in turn a period of tension concerning the movements of the rouble, the Russian market and Russian borrower's government bonds (private and state held). At the end of the year, the rouble showed a 46.04% decrease against the USD compared to 1 January.On 15 January 2015, the SNB decided to abandon the defence of the eur/chf exchange rate at 1.20, which began in the summer of 2011. This sudden decision triggered a strong appreciation of the chf against all other currencies. Therefore, the eur/chf trends quickly hit 85.17, to then stabilize in the following days, slightly above parity. The strength of the chf has been the subject of deep concern for everyone involved in the Swiss economy. Should this continue, it will not fail to create a negative impact on a large part of the sectors in the Swiss economy.For our bank, 2014 was distinguished by a showing of new progress for the domestic market development strategy in Ticino and Romandie with the resumption of the Ticino activity of the LLB Liechstensteinische Landesbank AG (Switzerland) in early January, the acquisition, in March, of Alasia Investissements SA, a Lausanne asset management company and the opening of a branch in Lausanne in early summer.In October, there was the creation of the PKB Servizi Fiduciari Spa Trust Company, with offices in Milan, with 70% held by PKB and 30% by Cassa Lombarda, which completed the range of services now available to our Italian customers.In 2014, the consolidated gross profit of the PKB Group rose considerably, compared to the results for 2013, to chf 48.7 M (+chf 12.3 M, equal to +33.8%). After allowing for depreciation, provisions and value adjustments totalling chf 24.5 M, consolidated net profits came to chf 26.0 M, an increase of 33.76% over the previous year, while that of PKB Privatbank SA, Lugano was chf 22.2 M (+chf 5.7 M, which is an increase of 34.71%).The Board of Directors has expressed its satisfaction with the results obtained during the 2014 financial year and its thanks to its clientele for the trust placed in the Bank, its general management and its entire staff for their devoted service and strong cooperative spirit.

For the Board of Directors, the Chairman

Henry Peter

PKB Group a mo u n ts i n c f / 0 0 0

PKB Group a mo u n ts i n c f / 0 0 0

2013

2013

1998

1998

2014

2014

H I G H L I G H T S

Income statement

Operating income 128,148 100,313

Operating expenses –79,448 –63,915

Gross profit 48,700 36,398

Group profits 26,027 19,458

Balance sheet

Balance sheet total 3,531,803 2,605,727

Gross shareholders' equity 331,763 325,286

Customers' credits

Total net of credits recorded in double-entry 11,700,397 9,058,021

Capital indicators

Tier 1 ratio 21.39% 26.65%

Solvency ratio 22.25% 27.12%

Headcount (expressed as full-time employees)

Headcount 275 236,7 of whom in Switzerland 241,7 212,4

of whom abroad 33,3 24,3

Income statement

Operating income 118,356 93,939

Operating expenses –73,746 –60,385

Gross profit 44,610 33,554

Net profit for the year 22,243 16,512

Balance sheet

Balance sheet total 3,103,469 2,205,008

Gross shareholders' equity 323,111 315,867

Capital indicators

Tier 1 ratio 20.80% 26.48%

Solvency ratio 20.90% 26.86%

Consolidation principles

PKB Privatbank SA, Lugano Parent company

PKB Privatbank Limited, St. John’s, Antigua (W.I.) Subsidiary (100%)

PKB Banca Privada (Panamá) SA, Panama Subsidiary (100%)

PKB Alasia SA, Lausanne Subsidiary (100%)

PKB Servizi Fiduciari SpA, Milan Subsidiary (70%)

c o n s o l i d at e d f i n a n c i a l s tat e m e n t s

Contents Comments on the consolidated balance sheet 12

Comments on the income statement 13 Consolidated balance sheet 14 Consolidated income statement 16 Consolidated cash flow statement 17 Annex to the consolidated annual financial statements 18 Auditors' report 35

As at 31.12.2014 the total assets amounted to chf 3,531.8 million against liabilities of chf 3,234.8 million, shareholders' equity, including net profit for the year, therefore totalled chf 297 million. The increase in the balance sheet total with respect to the previous year was chf 926.1 million, or 35.5%. This strong rise was due mainly to the acquisition of the LLB Lugano branch.

Assets Liquid assets This item includes cash plus clearing and postal account balances. The total of chf 1,002.5 million is well above the legal requirement for primary liquidity

Receivables from banks Down by chf 514,9 million (–39.8%), amounts held with banks went from chf 1,295.1 million to chf 780.2 million.

Due from customers Amounts due from customers rose by 37.8%, from chf 530.6 million to chf 731.3 million.

Mortgage loans Mortgage loans increased by 358.5%, going from chf 139.1 million a chf 637.8 million, as a result of the acquisition of the LLB Lugano branch portfolio.

Securities and precious metals The book value rose from chf 0.4 million to chf 16.7 million. held for trading

Financial investments As at 31.12.2014 financial investments totalled chf 154.1 million against chf 101.3 million the previous year (+52.2%). Fund investments came to chf 20.8 million (chf 16.9 million as at 31.12.2013), while fixed-yield securities increased to chf 133.3 million (chf 84.4 million as at 31.12.2013).

Principal non-consolidated holdings The bank holds the entire share capital of Valuevalor AG, Lugano. This item also includes minority shareholdings in Cassa Lombarda Spa, Milan (33.9%), Anthilia Capital Partner Spa, Milan (36.6%), Aduno SA, Zurich (0.28%), Queluz Gestao de Ativos, San Paolo (10%) and EIH Endurance Investments Holding SA, Lugano (25%).

Fixed assets This item rose from chf 62.1 million to chf 64.8 million. This represents tangible fixed assets, which include the bank’s properties, fixtures, furnishings, any capitalised renovation works and computer hardware.

Intangible assets Intangible assets concern the goodwill paid for the acquisition of Banca Gesfid SA, of Liech-tensteinische Landesbank (Switzerland) SA («LLB») of Lugano and PKB Alasia SA. The Goodwill for «LLB» shall be determined finally on 30.06.15 whilst the Goodwill for PKB Alasia SA on 31.12.16.

Other asset Other assets increased to chf 52.9 million as at 31.12.2014, against chf 22.6 million at the end of the preceding year. This item consists mainly in positive replacement values that amount to chf 51.6 million. Positive replacement values concern derivative financial in-struments, taken out on behalf of the bank or on behalf of clients and represent claims on counterparties.

Liabilities Payables to banks Payables to banks went from chf 140.1 million to chf 33.7 million (–75.9%).

Payables to clients Are up by chf 978.9 million, being 48.6% (chf 2,991.9 million as at 31.12.2014, chf 2,013.0 million as at 31.12.2013). The very low level of interest rates of the main currencies and the uncertainty in financial markets generated a build-up of cash in customers’ bank accounts, pending better investment opportunities.

Other liabilities This item amounted to chf 54.1 million as at 31.12.2014 (+chf 27.2 million, or 101.2% compared to the previous year). These predominantly comprise the Bank’s liabilities for indirect taxes (chf 0.3 million) as well as negative replacement values on derivative instru-ment transactions (chf 51.1 million), representing its liability exposure to counterparties.

c o m m e n t s o n t e c o n s o l i d at e d b a l a n c e s e e tBalance sheet total

The result from interest operations came to chf 20.4 million, sharply up from the previous year (+53.4%) as a result of merger for the most part, as at 01.01.2014 and the LLB, Lugano receivables portfolio.

Commissions and provision of services increased to chf 89.5 million (+23.3%) which may be broken down into credit operations (+14.4%), securities trading and investment operations (+25.5%), provision of other services (+12.1%) and expenses for commissions (+17.3%): apart from the aforementioned acquisition, also an encouraging organic development of the business carried out by all of the Bank's Swiss and foreign units also contributed to all of these items.

Overall, the result from trading operations totalled chf 15.3 million against 13.1 million as at 31.12.2013 (+16.2%).

Other ordinary income came in at chf 2.9 million, compared to chf 1.3 million the previous year (+128.6%).

Operating expenses Personnel costs went from chf 48.9 million as at 31.12.2013 to chf 60.2 million as at

31.12.2014 (+chf 11.2 million coming to 23.0%). A good part of the increase may be put down to staff acquired with the LLB Lugano branch merger, as well as to a strengthening of the entire organization, specifically in front-office business and in what are considered the Bank's «core» markets. These include good business development in Latin America, in particular at the PKB Banca Privada subsidiary (Panama). Other operating expenses increased over the previous year, which as at 31.12.2014 came to chf 19.2 million (+28.5%). This was in any event an exceptional and non-recurrent rise, mostly brought about by special development projects, legal and regulatory risk management and data migration.

Gross profit Gross profit for the year came to chf 48.7 million, up by chf 12.3 million (+33.8%) over 2013.

Amortisation of fixed assets Total depreciation came to chf 16.3 million, up compared to the previous year (+51.0%). Of the total, chf 8.7 million were used to amortise the Goodwill of Banca Gesfid, of the

Lugano Liechtensteinische Landesbank (Switzerland) SA (LLB) and PKB Alasia SA, to which were added infrastructure Amortisation of investments incurred by the parent com-pany and the subsidiaries.

Valuation adjustments, These increased from chf 6.7 million to chf 8.2 million mainly due to the growth in provisions and losses legal risks. In 2014, losses totalling chf 0.5 million were posted to the accounts, while

provisions for operational risks of chf 7.7 million were made.

Extraordinary income Out of the total of chf 7.8 million, chf 5.1 million arose from the use of the elimination of reserves for general banking risks and chf 2.2 [sic million] arose essentially from the elimination of tax credits.

Extraordinary expenses The entire amount of chf 0.2 million may be accounted for by miscellaneous losses.

Financial year profit Net profit for the year came to chf 26.0 million, showing a rise of chf 6.5 million (+33.8%).

c o m m e n t s o n t e c o n s o l i d at e d i n c o m e s tat e m e n tRevenues

C O N S O L I D AT E D B A L A N C E S H E E TAssets a mo u n ts i n c f 20132014

Liquid assets 1,002,551,262.66 386,125,993.66

Receivables arising from money market securities 4,657,523.33 291.62

Due from banks 780,164,778.18 1,295,056,479.71

Due from customers 731,265,636.37 530,610,810.84

Mortgage loans 637,836,268.94 139,119,506.24

Securities and precious metals held for trading 16,653,550.14 384,946.62

Financial investments 154,140,847.72 101,281,150.81

Non fully-consolidated participations 39,675,914.70 38,195,914.70

Fixed assets 64,780,323.40 62,149,365.25

Intangible assets 12,188,904.24 8,424,400.00

Prepayments and accrued income 34,950,233.10 21,751,261.48

Other assets 52,939,609.96 22,626,741.87

Total assets 3,531,804,852.74 2,605,726,862.80

Total deferred credits 0.00 0.00

Total receivables from non-consolidated companies and holders of qualifying holdings 0.00 0.00

Liabilities a mo u n ts i n c f

Due to banks 33,763,849.45 140,143,648.88

Commitments to customers in savings and investments 2,996,667.88 2,369,033.56

Other payables to customers 2,988,963,615.34 2,010,607,361.01

Medium-term notes 0.00 0.00

Prepayments and accrued income 39,215,366.12 31,071,536.32

Other liabilities 54,078,556.06 26,879,896.93

Value adjustments and provisions 66,024,146.40 55,369,575.18

Reserves for general banking risks 49,719,200.00 54,794,013.00

Share capital 16,000,000.00 16,000,000.00

Reserves generated from profits 254,928,333.66 249,033,607.70

Minority stakes in equity capital 87,310.14 0.00

Group profit 26,027,807.69 19,458,190.22

of which minority stakes –61,009.72 0.00 Total liabilities 3,531,804,852.74 2,605,726,862.80

Total deferred commitments 0.00 0.00

Total commitments to non-consolidated companies and holders of qualifying holdings 33,286,364.70 26,436,134.00

201319982014

c o n s o l i d at e d o f f - b a l a n c e s e e t o p e r at i o n s a mo u n ts i n c f 20132014

Contingent liabilities 77,485,960.67 45,590,520.03

Irrevocable commitments 10,009,928.67 6,976,916.18

Payment and additional funding commitments 2,427,376.54 2,806,702.15 Credit commitments Derivative financial instruments: Positive replacement value 44,665,118.16 20,558,652.85

Negative replacement value 40,204,795.44 20,079,032.15

Contract volumes 3,129,329,691.40 1,662,830,698.37

Fiduciary operations 34,204,158.51 73,819,727.42

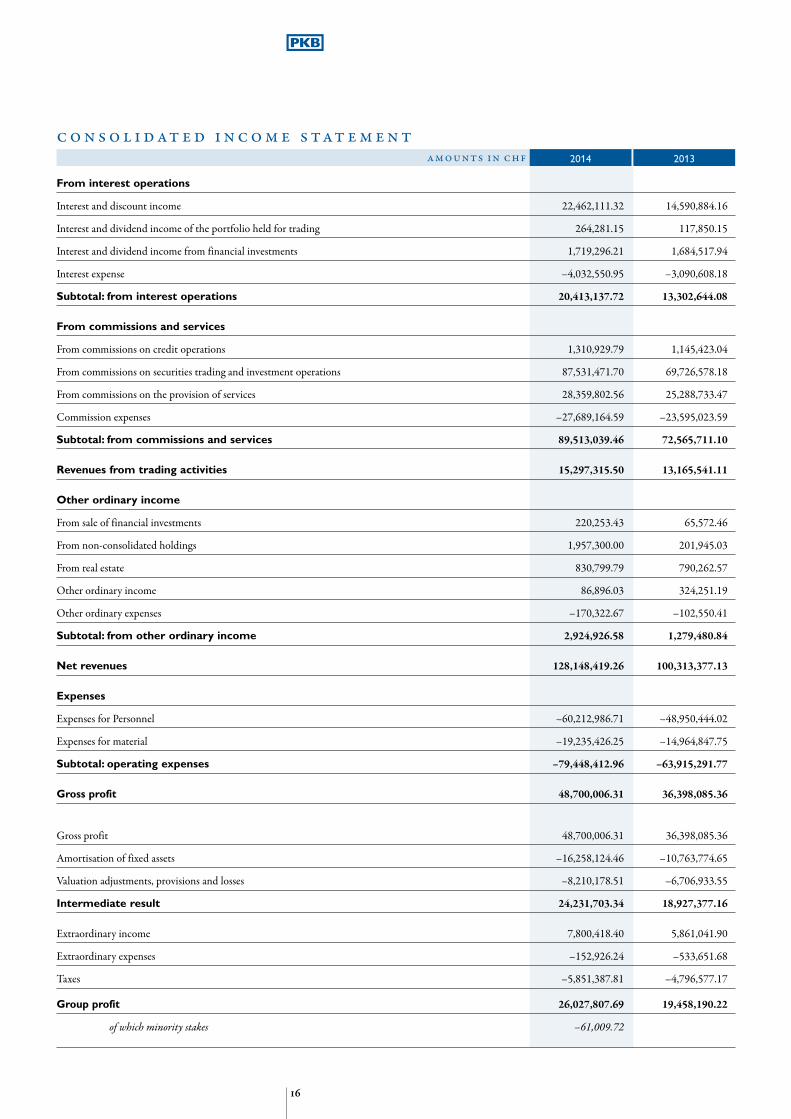

c o n s o l i d at e d i n c o m e s tat e m e n t a mo u n ts i n c f 20132014

From interest operations

Interest and discount income 22,462,111.32 14,590,884.16

Interest and dividend income of the portfolio held for trading 264,281.15 117,850.15

Interest and dividend income from financial investments 1,719,296.21 1,684,517.94

Interest expense –4,032,550.95 –3,090,608.18

Subtotal: from interest operations 20,413,137.72 13,302,644.08

From commissions and services

From commissions on credit operations 1,310,929.79 1,145,423.04

From commissions on securities trading and investment operations 87,531,471.70 69,726,578.18

From commissions on the provision of services 28,359,802.56 25,288,733.47

Commission expenses –27,689,164.59 –23,595,023.59

Subtotal: from commissions and services 89,513,039.46 72,565,711.10

Revenues from trading activities 15,297,315.50 13,165,541.11

Other ordinary income

From sale of financial investments 220,253.43 65,572.46

From non-consolidated holdings 1,957,300.00 201,945.03

From real estate 830,799.79 790,262.57

Other ordinary income 86,896.03 324,251.19

Other ordinary expenses –170,322.67 –102,550.41

Subtotal: from other ordinary income 2,924,926.58 1,279,480.84

Net revenues 128,148,419.26 100,313,377.13

Expenses

Expenses for Personnel –60,212,986.71 –48,950,444.02

Expenses for material –19,235,426.25 –14,964,847.75

Subtotal: operating expenses –79,448,412.96 –63,915,291.77

Gross profit 48,700,006.31 36,398,085.36

Gross profit 48,700,006.31 36,398,085.36

Amortisation of fixed assets –16,258,124.46 –10,763,774.65

Valuation adjustments, provisions and losses –8,210,178.51 –6,706,933.55

Intermediate result 24,231,703.34 18,927,377.16

Extraordinary income 7,800,418.40 5,861,041.90

Extraordinary expenses –152,926.24 –533,651.68

Taxes –5,851,387.81 –4,796,577.17

Group profit 26,027,807.69 19,458,190.22

of which minority stakes –61,009.72

c o n s o l i d at e d c a s f l o w s tat e m e n t a mo u n ts i n c f ⁄ 0 0 0

Origin Use

2014

Origin Use

2013

Flow of funds based on the operating result (internal financing)

Group profit 26,028 19,458

Amortisation of fixed assets 16,258 10,764

Value adjustments and provisions 7,816 6,550

Prepayments and accrued income 13,199 7,762

Accrued expenses and deferred income 8,144 11,489

Other items 4,835 4,031

Dividend previous year 14,000 14,500

Balance 26,212 21,968

Flow of funds from equity capital transactions

Changes in minority stakes in equity capital 87

Balance 87

Flow of funds from changes in fixed assets and holdings

Non fully-consolidated participations 2,227 130

Real Estate 1,311 1,405

Other fixed assets 8,102 6,677

Intangible assets 12,494

Balance 24,134 8,212

Cash flow from banking

Medium- and long-term (> 1 year)

Due from banks

Due from customers 36,897 177

Mortgage loans 90,645 1,244

Financial investments 22,455 5,736

Short-term assets

Due to banks 106,380 74,910

Due to customers 978,984 231,508

Receivables arising from money market securities 4,657 2,926

Due from banks 514,892 525,951

Due from customers 237,551 86,100

Mortgage loans 408,072 5,318

Financial investments 30,405

Securities and precious metals held for trading 16,269 263

Other assets 30,313 11,706

Other liabilities 27,199 9,005

Other items 3,035 1,468

Liquid assets

Cash and cash equivalents 616,425 300,434

Balance 2,165 13,756

1. Operations and staff The PKB Group is present in Switzerland in Lugano, Bellinzona, Geneva, Zurich and

Lausanne and in Antigua, W.I. and Panama through its subsidiaries PKB Privatbank Limited (West Indies) and PKB Banca Privada (Panama) SA. The principal activities of the Group are private banking and commercial and financial operations. The head-count, expressed as full-time employees, was 275 at 31.12. 2014 (2013: 236.70 units).

All of the essential bank's activities are undertaken internally, without recourse to out-sourcing.

a n n e x t o t e c o n s o l i d at e d a n n u a l f i n a n c i a l s tat e m e n t s

2. Accounting and valuation principles used

Consolidation principles The Group's accounting standards comply with the provisions of the Swiss Federal Law on Banks and Savings Banks, and the accounting regulations of the Swiss Financial Markets Su-pervisory Authority (FINMA). The consolidation is prepared using the purchase method.

Fully-consolidated holdings The consolidated financial statements contain the annual accounts of PKB Privatbank SA, Lugano, PKB Privatbank Ltd, St. John's, PKB Banca Privada (Panama) SA, Panama, PKB Alasia SA Lausanne and PKB Servizi Fiduciari SpA, Milan.

Accounting and valuation standards Accounts are established by submitting operations on their posting date. The accounting standards set out below were adopted.

Foreign funds and currencies Valuation at year-end rates. Exchange differences were booked in the income statement under «Results from trading operations».

Exchange rates used for the main currencies were as follows: eur 1.2027 (2013: 1.2272) usd 0.9894 (2013: 0.8915).

Receivables and general liabilities Valuation at nominal value.

Securities and precious metals Valuation at market value. held for trading

Financial investments Shares: at market value at the end of the financial year, however not exceeding the acqui-sition price. Fixed-yield securities: the difference between the acquisition price and the re-demption value is distributed over the number of years between the acquisition date and the maturity date.

Not fully consolidated holdings Holding: Valuation at purchase price, after deduction not greater than 20%: of the economically necessary depreciation.

Holding: Valuation at net worth. Investment at between 20% and 50%:

Regardless of the size of investment, companies not significant for proper valuation of the group's equity and income are valued at the purchase price, after deducting the economically necessary depreciation.

Fixed assets Stated at acquisition cost after necessary deductions for ordinary depreciation. Works of art are not depreciated. All other fixed assets are shown on the balance sheet at purchase cost or the market value, whichever is lower. Depreciation is charged using the straight-line method.

The depreciation periods are as follows:

Properties used by the bank maximum 50 years Renovations maximum 20 years Plants maximum 10 years Furniture maximum 10 years Equipment and vehicles maximum 5 years Hardware/Software maximum 3 years Intangible assets maximum 5 years

Reserves for general banking risks Reserves for general banking risks include a taxed amount of chf 3,369,200.00

Intangible assets Intangible assets booked concern the goodwill paid for the acquisition of Banca Gesfid SA, of Liechtensteinische Landesbank (Switzerland) SA («LLB») of Lugano and PKB Alasia SA.

The Goodwill for «LLB» shall be determined finally on 30.06.15 whilst the Goodwill for PKB Alasia SA on 31.12.16.

Solvency risks Where necessary, the bank shall allocate appropriate provisions, which are booked under «Value adjustments and provisions».

Doubtful interest Interest and commissions outstanding for over 90 days are not recognized as revenues but are booked under provisions. The concerned loans are considered as non-performing.

Revenues from trading transactions These figures are recorded in the income statement before deduction of refinancing expenses.

Contingent liabilities, irrevocable commitments These are booked as off-balance sheet items at nominal value. Provisions for known risks payment commitments and credit commitments are reported under «Value adjustments and provisions».

Derivative financial instruments Valuation is effected at market value using the marked-to-market standard. The use of de-rivative financial instruments on the bank’s own behalf is mainly for hedging purposes and only marginally for trading operations within limits established by internal regulations.

Standards applied for identification of Loan applications are regularly assessed, at least once per year. risk of loss and calculation of When the risk warrants it, assessment is more frequent and prompt, in particular for value adjustments non-performing loans. Where a need is identified to raise provisions for the unsecured portion, these are booked

immediately.

Collateral assets for loans The realizable value is calculated on the basis of the market price or sale value, from which the costs of disposal and refinancing are deducted.

Risk assessment and management Risk assessment and management form an integral part of the internal control system as provided for by FINMA circular 08/24. Responsibility for the Group's internal control sys-tem is entrusted to the Board of Directors, who establishes the guidelines and periodically checks their suitability and effectiveness.

The Board of Directors is supported in its duties by an Audit Board, which advises and makes proposals, while the operational management of the Consolidated Supervision is pro-vided by the Executive Board, in its turn supported by the Risk Committee (RICO) and the Compliance Committee (COCO) whose duties are to define the processes for measuring, managing and controlling risks for the PKB Group and COFI Group (Banking&Finance). The RICO and COCO meet at least every quarter and benefit from an integrated Group risk reporting system. Internal Audit checks and evaluates the internal control system, and helps in constantly fine-tuning it.

In compliance with current regulations, the Group has Regulations for Consolidated Su-pervision of the COFI Group (Banking&Finance) and a Risk Policy, which define, in an integrated manner, the guidelines for risk assessment and management with which all the companies of the Group must comply. Risk management policy, examined every year by the Board of Directors, constitutes the basis of the PKB Group’s risk management process. This is combined with a limits structure, defined for each identified risk category, which is checked constantly with particular regard to the risks indicated below.

Credit risk Credit risk is managed by the Board of Directors through the COFI Group Credit Policy

(Banking&Finance) and the PKB Group Credit Regulations. General Management conducts credit risk management through the Credit Committee (COCR), which supervises the ap-plication of company strategies and analyses, in terms of quality and quantity, the solvency of the counterparties and their guarantees.

Credit risk control is conducted using a system of risk and exposure limits in the PKB Group and COFI Group (Banking&Finance), and by concentration according to groups of counter-parties (large risks and 10 major debtors) and by country. There are special provisions for del credere and country risk.

Capital requirements for credit risk are calculated using the international method with a com-plete approach to handling guarantees.

Market risk (balance sheet) Management of the market risk resulting from balance sheet activity is governed by Reg-

ulations approved by the Board of Directors. General Management supervises market risk through the Asset & Liability Committee (ALCO).

Rate risk is controlled by indicators of income effect and value effect calculated on the basis of stress scenarios, while the counterparty and exchange risks are controlled by a system of exposure limits. Interest rate swaps are mainly used to cover the rate risk, while the exchange risk is mainly covered by forward exchange and currency options.

Rate risk is calculated using the modified duration method in accordance with the su-pervisory authorities.

Market risk (trading portfolio) Management of the trading portfolio is governed by Regulations approved by the Board

of Directors and Guidelines approved by the General Management. PKB Switzerland is active on the primary market for bond issues in Swiss francs as Market Maker and on the currency, bond and share market as well. Market risk associated with the trading portfolio is controlled using a system of exposure limits, the results of which are reported to the General Management.

Capital requirements for market risk are calculated using the standard method with the delta-plus approach for options.

Liquidity risk Liquidity management is governed by the Board of Directors via the Liquidity Policy of

the COFI (Banking & Finance) Group. General Management supervises and manages liquidity risk through ALCO.

Liquidity risk is supervised in accordance with legal provisions and the results of checks are reported by ALCO.

Operational risk Management and control of operational risk, which includes legal and compliance risks,

are governed by the Board of Directors through a set of Regulations and by the General Management through Directives. Operational risk is managed as follows:

• processes: the Group governs its own activities, in particular those that are likely to affect external activities, in accordance with current legal and ethical standards on banking and insurance matters, ensuring understanding and transparency of operational and contractual provisions with clients, with particular reference to contracts on derivative financial instru-ments for which the Bank has signed specific ISDA and CSA contracts. The principle of separation of functions is ensured, allowing mitigation of operational risks;

• human resources: the Bank's aim is to recruit qualified personnel capable of implementing its strategy and identifying with the Bank’s culture. The latter is reflected by Management and staff as well as by the approach of the COFI (Banking & Finance) Group to risk management. As regards compliance risk and its impact on the bank’s reputation, risk mitigation is achieved through the constant training and awareness raising of staff at all levels, a clear definition of work processes and responsibilities, as well as the dissemination of a corporate culture founded on the pillars of total integrity and uncompromising ethical and professional standards. For the PKB Group, a PKB Charter of Values was also introduced. This was presented and dis-cussed at all levels throughout the Bank. The PKB Group has a Legal and Compliance depart-ment that covers all aspects of compliance;

• internal systems: the Group has the internal and external expertise to ensure in-house devel-opment and maintenance of its IT system;

• exogenous events: the Bank has implemented security measures specifically designed to prevent unauthorised persons from accessing areas where «sensitive» documents are stored. General Management in its preparation of the General Continuity Plan to ensure the continuity of its activities and cope with the different scenarios outlined therein through detailed analysis has iden-tified the minimum resources necessary for the continuity plan.

Operational risk is monitored by a system of measuring losses whose results are reported in the RICO. Vigilance capital requirements for operating risks are calculated according to the base method.

Legal risk To prevent risks, the bank ensures that its activity particularly that involving any external

impact, is governed by legal and ethical standards applicable in the banking sector, and by en-suring knowledge and transparency in its operational and contractual relations with clients.

To adequately cover the various legal risks (including those relating to the outcome of the checks being carried out as part of the US Program), the bank has allocated the necessary provisions.

Reputational and compliance risks While Compliance risks are related to the violation of laws and regulations, reputational

damage may be the result of such violation but may also be the consequence of inappropri-ate behavior, or behavior viewed as inacceptable by a general public, although fully in line with laws and regulations. In order to capture the wide range of reputational risks PKB has established a Code of Values. The Code of Values is designed to support a corporate culture that is based on impeccable conduct as well as on best in class professional standards.

Compliance risks are addressed by a comprehensive set of Policies and procedures reaching out to all facets of our business. With our business being international, the internal rules go beyond the Swiss legal and regulatory landscape, and address all cross-border activities and issues relevant in the context of serving our clients, in particular in the area of investment advisory and when dealing in foreign financial markets.

Compliance with the Code of Values, our Policies and our internal procedures is assured through a three level control program. The primary responsibility for compliance with all these rules is with the line management. Controls built into the processes and workflows to assure an institutionalized «4-eyes principle» and additional management controls, includ-ing escalation processes, are the backbone of this first control level. Ongoing training and education for staff on all levels form an additional and integral part of our efforts to miti-gate reputational and Compliance risks. The second control level consists of independent controls executed by the operational control function Legal & Compliance, which reports to the Executive Board. The relevant risks are assessed annually and a Compliance Action Plan is established to make sure Compliance risks are addressed timely and accurately. The third level of the control framework consists of controls performed by the non-operational control function Internal Audit reporting to the Board of Directors. In addition, External Audit performs its own independent controls.

Group policy on the use of Positions taken in derivative instruments are, in general, held on behalf of clients. derivative financial instruments For the structural management of the balance sheet, the PKB Group hedges interest rate

risk using Interest Rate Swaps and Forward Rate Agreements.

Other information On 31.12.2013, an agreement was signed for the acquisition of the Lugano branch of LLB Liechstensteinische Landesbank AG (Switzerland). The migration to PKB occurred on 01.01.2014. With this transaction, the PKB Group increased business by about chf 1.8 bil-lion in client assets (deposits and securities) and receivables.

PKB acquired customer receivables for approximately chf 0.6 billion, customer cash depos-its of approximately chf 0.4 billion with customer securities of chf 0.8 billion also being transferred.

3. Information on the consolidated balance sheet

3.1 Coverage of loans and off-balance sheet operations a mo u n ts i n c f ⁄ 0 0 0 TOTALTYPE OF COVERAGE

Mortgage Other Without coverage coverage

Loans

Due from customers 128,644 552,007 50,615 731,266

Mortgage loans 637,836 637,836 residential properties 522,139 commercial properties 113,547 craft and industry 2,150

Total Loans 766,480 552,007 50,615 1,369,102

Previous year 193,979 433,231 42,521 669,731

Off-balance sheet operations

Contingent liabilities 1,563 66,922 9,001 77,486

Irrevocable commitments 402 9,608 10,010

Payment and additional funding commitments 2,427 2,427

Total off-balance sheet transactions 1,563 69,751 18,609 89,923

Previous year 1,849 40,093 13,432 55,374

Doubtful loans

Amount Value Amount Provisions Gross Estimated Net realizable of collateral

Current year 8,673 1,668 7,005 7,065

Previous year 10,806 3,931 6,875 6,905

3.2 Breakdown of the precious metals held for trading a mo u n ts i n c f ⁄ 0 0 0 financial investments and holdings

20132014

Securities and precious metals held for trading

Negotiable instruments

listed on the stock exchange 14,819 374

not listed on the stock exchange

Equity securities 1,820

Precious metals 15 11

Total securities and precious metals held for trading 16,654 385

of which securities eligible for pensions under the provisions on liquidity 1,614

a mo u n ts i n c f ⁄ 0 0 0 2014 2013 2014 2013

Book Book Value ValueFinancial investments value value market market

Negotiable instruments

of which are intended to be held to maturity 133,293 84,384 135,449 86,057

of which valued according to the principle of the lowest value

Equity securities 20,848 16,897 23,624 18,799

of which qualifying holdings

Precious metals

Real Estate

Total financial investments 154,141 101,281 159,073 104,856

of which securities eligible for pensions under the provisions on liquidity 14,129 16,066

3.3 Information on holdings

Main non fully-consolidated holdings Valuation Head- Business Currency Share Share of investment method quarters capital 2014 2013

Cassa Lombarda SpA Equity Milan Credit EUR 18,000 33.94% 33.94% institutions

Anthilia Capital Partners SpA Equity Milan Financial EUR 5,371 36.60% 36.60% company

EIH Endurance Investments Holding SA Equity Lugano Financial CHF 100 25.00% 25.00% holding company

Aduno Holding SA Cost Zurich Credit CHF 25,000 0.28% 0.28% institutions

Valuevalor SA Cost Lugano Trust CHF 1,000 100.00% 100.00% company

Queluz Gestao de Ativos Ltda Cost San Paolo Financial BRL 1,248 10.00% 10.00% company

a mo u n ts i n ⁄ 0 0 0

a mo u n ts i n c f ⁄ 0 0 0 20132014

Non fully-consolidated participations Participations

with stock market value

without stock market value 39,676 38,196

Total holdings 39,676 38,196

3.4 Presentation of fixed assets

a mo u n ts i n c f ⁄ 0 0 0 2014

Purchase value

Deprecia-tion and

valueadjustments made so far

Book value as at

31.12.2013Reclassifica-

tion Investments Divest-ments

Deprecia-tion

Value adjustments

for equity valuation/revaluation

Year end book value

Participations

Valued with equity method 42,972 –7,657 35,315 160 1,890 37,045

Other 17,285 –14,404 2,881 250 2,631

Total holdings 60,257 –22,061 38,196 410 1,890 39,676

Fixed assets

Property bank use Lugano 50,469 –22,784 27,685 1,290 1,474 27,501

Property bank use Zurich 9,478 –7,314 2,164 135 2,029

Property bank use Geneva 13,154 –8,379 4,775 11 416 4,370

Property bank use Panama 3,375 –25 3,350 9 115 3,244

Other properties 9,954 –3,492 6,462 6,462

Other fixed assets 56,613 –38,900 17,713 8,125 4,664 21,174

Total tangible assets 143,043 –80,894 62,149 9,435 6,804 64,780

Leased assets

Others

Intangible assets

Goodwill 67,797 –59,372 8,425 12,493 8,729 12,189

Total intangible assets 67,797 –59,372 8,425 8,729 12,189

3.6 Assets not freely available and assets with retention of title a mo u n ts i n c f ⁄ 0 0 0 2014 2013

Securities as collateral 21,552 16,682

Due from banks 252,000

Value of fire insurance

Real Estate 63,111

Other fixed assets 36,672

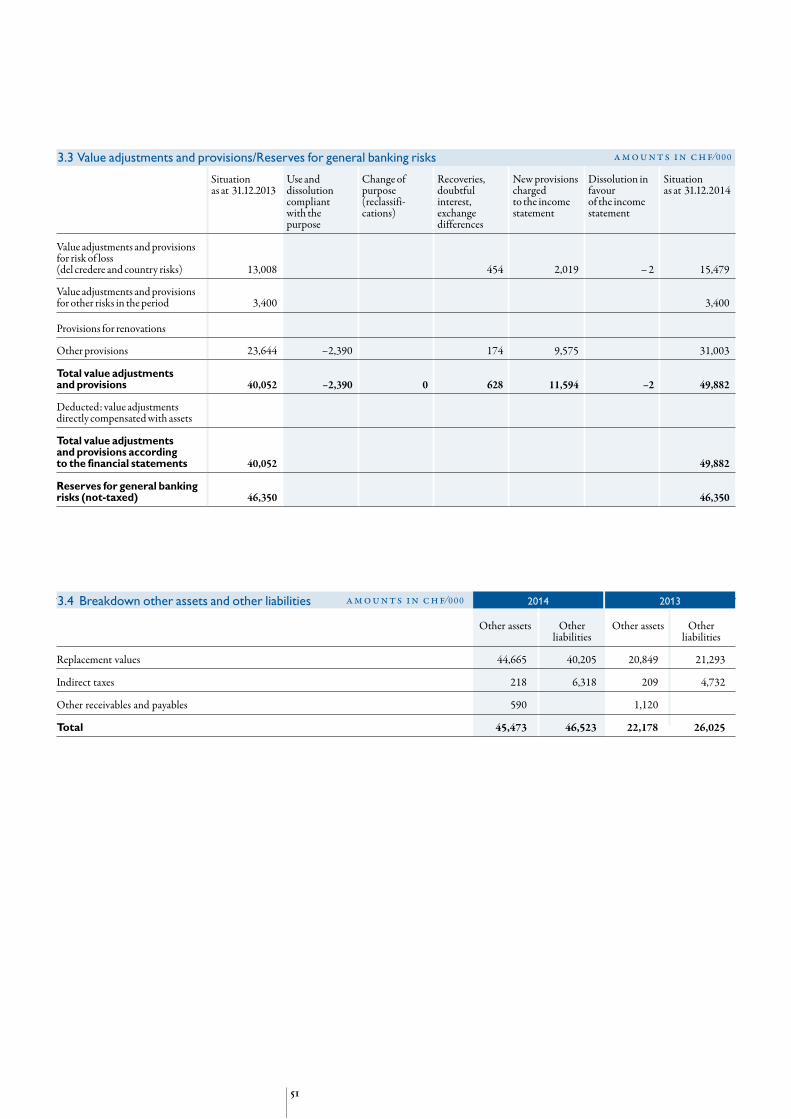

3.5 Breakdown other assets and other liabilities a mo u n ts i n c f ⁄ 0 0 0 2013

Other assets Other liabilities Other assets Other liabilities Replacement values 51,098 47,545 20,559 20,079 Indirect taxes 336 6,421 209 4,887

Other receivables and payables 1,506 113 1,859 1,914

Total 52,940 54,079 22,627 26,880

2014

a mo u n ts i n c f ⁄ 0 0 0

Book value Book Value Reserves for Financial as at at employer Statements 31.12.2014 31.12.2014 contributions as atReserves for employer contributions 31.12.2014 31.12.2014

Employer's pension institution 1,300 1,300 Pension institution

Total 1,300 1,300

a mo u n ts i n c f ⁄ 0 0 0

Excess Economic Contributions Contributions paid during coverage/ advantage/ paid during the period, recorded as insuff . commitment 2014 personnel expenses coverage as at of the entity 31.12.2014 as at Economic advantages/commitments and pension costs 31.12.2014 2014 2013

Employer's pension institution with excess coverage 132

Pension institution with excess coverage 6,090 4,853 3,435

Total 4,853 3,435

The Bank must determine for each pension plan whether the degree of coverage and the pension institution’s particular situation will give rise to a financial advan-tage or commitment. The assessment is based on the financial position as at 31 December 2013 and the development of the 2014 financial position.Based on the estimates received from the employer's pension institution and the pension institution, the level of cover pursuant to Article 44 OPP2 (Ordinanza sulla previdenza professionale [Occupational welfare order]) is 573.70% (2013: 528.50%) respectively 105.8% (2013: 100.80%).

The Bank’s employees are affiliated with an autonomous and independent pension institution pursuant to legal provisions on occupational pension requirements in Switzerland (LPP). The rules of the fund are based on those of a defined contributions scheme. Pension liabilities are calculated each year by an actuary. The bank accounts for its contributions to the employees’ occupational pension scheme as expenses for the financial year concerned.To complete the occupational pension arrangements under the terms of federal law, an autonomous and independent social security foundation was established – i.e., employer contribution – based pension funds. This foundation may provide assistance to employees.

3.7 Commitments towards own social welfare institutions a mo u n ts i n c f ⁄ 0 0 0 2014 2013

Total 32,223 9,315

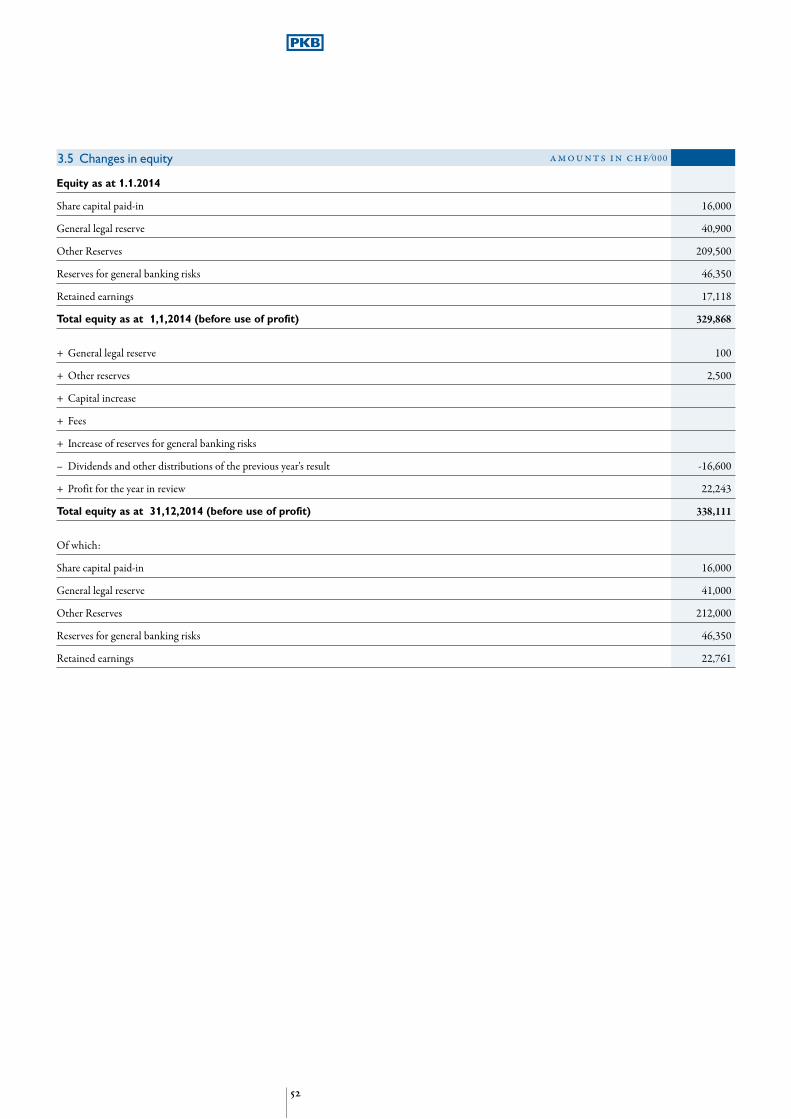

3.9 Changes in equity a mo u n ts i n c f ⁄ 0 0 0

Equity as at 1.1.2014

Share capital 16,000

deducting share capital not paid-in

Share capital paid-in 16,000

Reserves generated from profits 249,034

Reserves for general banking risks 54,794

Group profit 19,458

Total equity as at 1.1.2014 (before use of profit) 339,286

+ Reserves generated from profit 2,600

+ Capital increase

+ Fee

– Conversion differences 435

– Decrease of reserves for general banking risks –5,074

– Dividends and other distributions of the previous year's result –16,600

+ Profit for the year in review 26,028

Total equity as at 31.12.2014 (before use of profit) 346,675

of which:

Share capital paid-in 16,000

Reserves generated from profits 254,928

Reserves for general banking risks 49,719

Group profit 26,028

3.8 Value adjustments and provisions/Reserves for general banking risks a mo u n ts i n c f ⁄ 0 0 0

Situationas at 31.12.2013

Changes in consolidation area

Use and dissolution compliant with the purpose

Change of the purpose (reclassifica-tions)

Recoveries, doubtful interest, exchange differences

New provisions charged to the income statement

Dissolution in favour of the income statement

Situation as at31.12.2014

Provisions for deferred taxes 14,784 262 829 15,875

Value adjustments and provisions for risks of loss(del credere and country risks) 13,352 454 2,019 –346 15,479

Value adjustments and provisions for other operating risks 3,400 3,400

Provisions for renovations

Other provisions 23,834 84 –2,443 176 9,619 31,270

Total value adjustments and provisions 55,370 346 –2,443 0 630 12,467 –346 66,024

deducted: value adjustments directly compensated with assets

Total value adjustments and provisions according to the financial statements 55,370 66,024

Reserves for general banking risks 54,794 –5,075 49,719

3.11 Receivables and commitments against associated a mo u n ts i n c f ⁄ 0 0 0 companies and loans to bodies

20132014

Receivables from associated companies 16,887 23,379

Commitments to associated companies 1,581 789

Loans to bodies of the bank 7,607 5,302

Loans granted to the management are awarded under the same conditions applied to Bank staff.Transactions with associated companies were carried out at arm’s length and concern securities transactions, payments and treasury activities.

3.10 Maturity structure of current assets and borrowed capital a mo u n ts i n c f ⁄ 0 0 0

Sight Rescindable Within 3 and 12 between More fixed assets Total 3 months months 1 to 5 years than 5 years

Current assets

Liquid assets 1,002,551 1,002,551

Receivables arising from money market securities 41 4,616 4,657

Due from banks 182,746 210,131 216,034 171,254 780,165

Due from customers 1,144 154,616 447,096 82,690 44,720 1,000 731,266

Mortgage loans 169,700 306,790 25,084 94,764 41,498 637,836

Securities and precious metals held for trading 16,654 16,654

Financial investments 22,063 37,132 76,884 18,062 154,141

Total current assets 1,203,136 534,447 991,983 320,776 216,368 60,560 3,327,270

Previous year 883,489 478,523 571,041 343,715 143,763 32,049 2,452,580

Borrowed capital

Commitments arising from money market securities

Due to banks 23,841 9,923 33,764

Due to customersas savings and investment 2,997 2,997

Other payables to customers 2,856,913 111,463 361 20,227 2,988,964

Medium-term notes

Total borrowed capital 2,883,751 111,463 10,284 20,227 3,025,725

Previous year 2,003,983 117,559 7,316 24,262 2,153,120

Maturity between

3.13 Assets broken down by countries a mo u n ts i n c f ⁄ 0 0 0 or groups of countries

20132014

Assets % %

Italy 179,704 5,09 152,870 5,87

Remaining OECD countries 912,386 25,83 987,824 37,91

Remaining American countries (non-OECD) 214,818 6,08 137,416 5,27

Other countries 130,141 3,68 355,153 13,63

Total foreign loans 1,437,049 40,69 1,633,263 62,68

Switzerland 2,094,756 59,31 972,464 37,32

Total assets 3,531,805 100,00 2,605,727 100,00

3.12 Financial statements broken down according a mo u n ts i n c f ⁄ 0 0 0 to Swiss of foreign domicile amounts

20132014

Switzerland Abroad Switzerland Abroad

Assets

Liquid assets 1,002,547 4 386,126

Receivables arising from money market securities 4,657

Due from banks 92,280 687,885 236,053 1,059,004

Due from customers 177,187 554,079 98,238 432,373 Mortgage loans 637,836 139,120

Securities and precious metals held for trading 10,595 6,059 235 150

Financial investments 53,878 100,263 34,544 66,737

Non fully-consolidated participations 2,096 37,580 2,256 35,940

Fixed assets 60,358 4,422 57,817 4,332

Intangible assets 12,189 8,424

Prepayments and accrued income 34,950 21,751

Other assets 45,789 7,151 9,650 12,977

Total assets 2,094,755 1,437,050 972,463 1,633,264

Liabilities

Due to banks 19,046 14,718 132,987 7,157

Commitments to customers in savings and investments 2,979 18 2,348 21

Other payables to customers 651,406 2,337,558 365,754 1,644,853

Medium-term notes

Prepayments and accrued income 3,530 35,685 1,962 29,109

Other liabilities 51,951 2,128 10,435 16,445

Value adjustments and provisions 66,024 55,370

Reserves for general banking risks 49,719 54,794

Share capital 16,000 16,000

Minority stakes in equity capital 87

Reserves generated from profits 254,928 249,034

Group profit 26,028 19,458

Total liabilities 1,141,698 2,390,107 908,142 1,697,585

3.14 Financial statements broken down by currencies

CHF USD EUR Other Total

Assets

Liquid assets 999,944 162 2,325 120 1,002,551

Receivables arising from money market securities 10 4,647 4,657

Due from banks 36,229 450,588 229,494 63,854 780,165

Due from customers 139,367 184,485 374,727 32,687 731,266 Mortgage loans 637,836 637,836

Securities and precious metals held for trading 14,625 344 1,356 329 16,654

Financial investments 89,546 19,872 44,697 26 154,141

Non fully-consolidated participations 2,096 750 36,830 39,676

Fixed assets 60,797 3,960 23 64,780

Intangible assets 12,189 12,189

Prepayments and accrued income 21,830 3,771 9,259 90 34,950

Other assets 41,431 5,676 5,566 267 52,940

Total assets 2,055,890 669,608 704,287 102,020 3,531,805 Forward exchange 107,497 1,147,562 1,356,495 166,332 2,777,886 Long position 2,163,387 1,817,170 2,060,782 268,352 6,309,691

Long position previous year 1,083,474 1,226,744 1,303,878 236,669 3,850,765

Liabilities

Due to banks 16,393 1,570 8,370 7,431 33,764

Commitments to customers in savings and investments 2,997 2,997

Other payables to customers 427,011 1,122,580 1,349,828 89,545 2,988,964

Medium-term notes

Prepayments and accrued income 30,062 3,425 5,720 8 39,215

Other liabilities 40,575 4,880 8,582 42 54,079

Value adjustments and provisions 47,725 10,098 8,201 66,024

Reserves for general banking risks 49,719 49,719

Share capital 16,000 16,000

Minority stakes in equity capital 87 87

Reserves generated from profits 254,928 254,928

Group profit 26,028 26,028

Total liabilities 911,525 1,142,553 1,380,701 97,026 3,531,805 Forward exchange 1,239,228 673,231 696,712 170,198 2,779,369 Short position 2,150,753 1,815,784 2,077,413 267,224 6,311,174

Short position previous year 1,063,759 1,226,118 1,325,609 234,074 3,849,560 Net position long (short) 12,634 1,386 -16,631 1,128 Net position long (short) previous year 19,715 626 -21,731 2,595

CURRENCIES (equivalent in CHF/000)

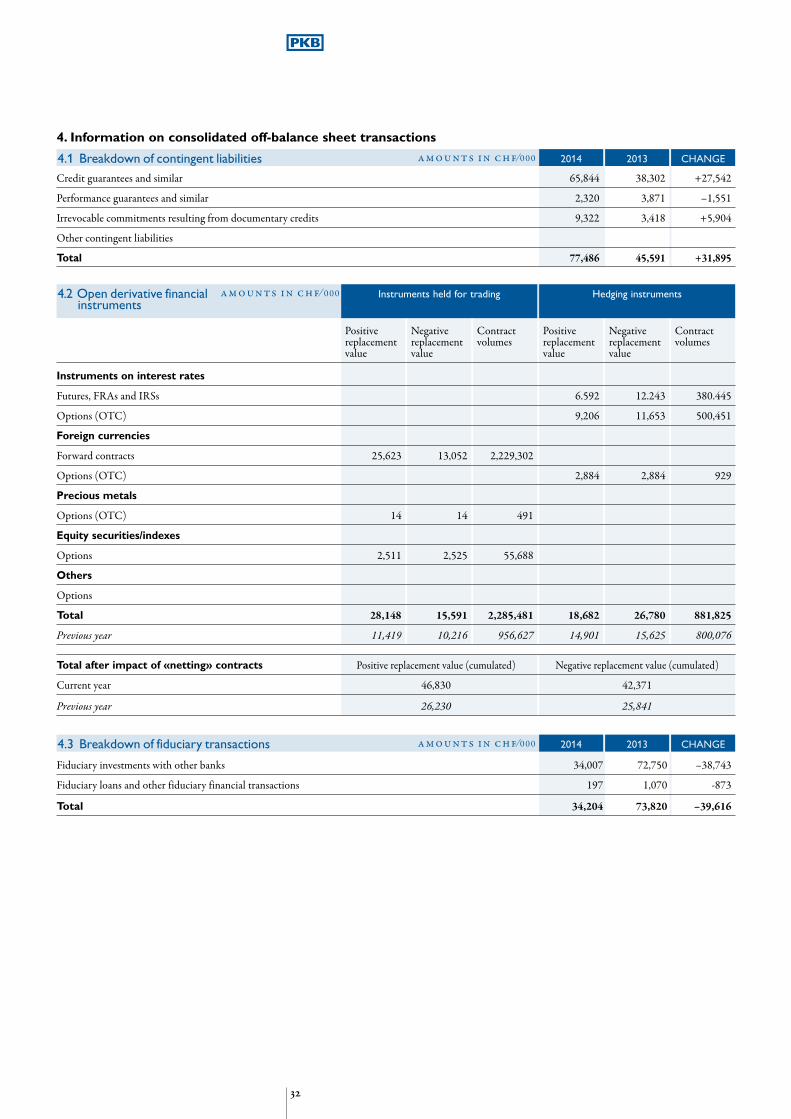

4. Information on consolidated off-balance sheet transactions

Credit guarantees and similar 65,844 38,302 +27,542

Performance guarantees and similar 2,320 3,871 –1,551

Irrevocable commitments resulting from documentary credits 9,322 3,418 +5,904

Other contingent liabilities

Total 77,486 45,591 +31,895

4.1 Breakdown of contingent liabilities a mo u n ts i n c f ⁄ 0 0 0 2013 CHANGE2014

4.3 Breakdown of fiduciary transactions a mo u n ts i n c f ⁄ 0 0 0 2013 CHANGE2014

Fiduciary investments with other banks 34,007 72,750 –38,743

Fiduciary loans and other fiduciary financial transactions 197 1,070 -873

Total 34,204 73,820 –39,616

4.2 Open derivative financial a mo u n ts i n c f ⁄ 0 0 0 instruments

Hedging instruments

Instruments held for trading

Positive Negative Contract Positive Negative Contract replacement replacement volumes replacement replacement volumes value value value value

Instruments on interest rates

Futures, FRAs and IRSs 6.592 12.243 380.445

Options (OTC) 9,206 11,653 500,451 Foreign currencies

Forward contracts 25,623 13,052 2,229,302

Options (OTC) 2,884 2,884 929 Precious metals

Options (OTC) 14 14 491 Equity securities/indexes

Options 2,511 2,525 55,688 Others

Options

Total 28,148 15,591 2,285,481 18,682 26,780 881,825

Previous year 11,419 10,216 956,627 14,901 15,625 800,076

Total after impact of «netting» contracts Positive replacement value (cumulated) Negative replacement value (cumulated) Current year 46,830 42,371 Previous year 26,230 25,841

5. Information on the consolidated income statement

Operations in foreign exchange and foreign currency 13,492 9,228 +4,264

Operations with precious metals 180 170 +10

Trading in securities 2,008 3,931 –1,923

Other trading operations –418 –163 –255

Total from trading operations 15,262 13,166 +2,096

5.1 Breakdown of results from trading operations a mo u n ts i n c f ⁄ 0 0 0 2013 CHANGE2014

Salaries 47,967 39,575 +8,392

Social benefits 9,660 7,385 +2,275

Other personnel expenses 2,586 1,990 +596

Total personnel expenses 60,213 48,950 +11,263

5.2 Breakdown of personnel expenses a mo u n ts i n c f ⁄ 0 0 0 2013 CHANGE2014

Expenses for premises 2,327 1,872 +455

Expenses for EDP, machines, furniture, vehicles and other equipment 2,142 1,381 +761

Other operating expenses 14,766 11,712 +3,054

Total materials expenses 19,235 14,965 +4,270

5.3 Breakdown of materials expenses a mo u n ts i n c f ⁄ 0 0 0 2013 CHANGE2014

5.4 Extraordinary revenues and expenses Of the total extraordinary revenues at chf 7.8 million, chf 5.1 million are from the elimination of taxed reserves, chf 1.8 million are from the dissolution of tax credit, and chf 0.9 million are represented by sundry revenues.Extraordinary costs are mainly due to sundry losses.

5.5 Depreciation of fixed assets

The total amount of depreciation stands at chf 16.3 million, compared with chf 10.8 million in the previous period. This amount comprises depreciation of buildings for chf 6.8 million, goodwill amortisation of chf 8.7 million and devaluations on holdings for chf 0.8 million.

5.6 Rettifiche di valore, accantonamenti e perdite

The figure of chf 8.2 million mainly relates to the establishment of provisions.

Assets held purely for custody purposes are not included in this table.Managed assets include all equity for which the Bank receives commission and/or fees in addition to custody fees and other expenses for holding accounts.Assets under management mandate are clients' assets managed in accordance with a management profile chosen by the client.The net contributions/withdrawals comprise actual input/output movements of clients' funds and assets excluding the performance of securities and currencies, interest, charges, commission and dividends. Credits to clients are not deducted from the total assets managed.Figures from the previous year were changed for proper comparison with 2014.

4.4 Managed assets a mo u n ts i n c f ⁄ 0 0 0 2013 CHANGE2014

Held by self-managed collective investment schemes 1,023,844 937,119 86,725

With management mandate 4,143,750 3,104,826 1,038,924

Other assets 7,193,254 5,618,396 1,574,858

Total managed assets (including assets recorded in double-entry) 12,360,848 9,660,341 2,700,507 Of which considered in double-entry 660,451 575,922 84,529 Net contributions (withdrawals) 2,246,895 907,664 1,339,231

5.7 Gross profit broken down by domicile a mo u n ts i n c f ⁄ 0 0 0 20132014

Switzerland Abroad Switzerland Abroad

From interest operations 18,634 1,780 11,792 1,511

From commissions and services 78,729 10,784 64,649 7,917

Revenues from trading activities 13,390 1,908 11,967 1,197

Other ordinary income 2,925 1,279

Net profit for the year 113,678 14,472 89,687 10,625

Expenses for Personnel –57,532 –2,682 –47,126 –1,824

Expenses for material –17,488 –1,748 –13,259 –1,705

Expenses –75,020 –4,430 –60,385 –3,529 Gross profit 38,658 10,042 29,302 7,096

6.2 Capital requirements a mo u n ts i n c f ⁄ 0 0 0 31.12.201331.12.2014

Credit risk (complete BIS method) 74,839 61,820 of which valuation risk related to equity securities in the portfolio of the bank 3,780 3,146

No counterparty risk (complete BIS method) 5,182 4,972

Market risk (standard) 7,216 2,539

of which interest rate instruments 6,281 416

of which on equity securities 418 203

of which on foreign exchange and precious metals 295 1,661

of which on raw materials 221 259

Operational risks (basic indicator) 16,141 14,195

Capital requirements 103,378 83,526

Ratio of eligible capital and capital requirements required under Swiss law 281% 344%

CET 1 ratio 21.39% 26.65%

Tier 1 ratio 21.39% 26.65%

6.1 Eligible capital a mo u n ts i n c f ⁄ 0 0 0 31.12.201331.12.2014

Gross shareholders' equity 331,763 325,286 of minority interests 87

of «innovative» instruments of paid-in share capital 16,000 16,000

of reserves generated from profits 254,928 249,034 of reserves for general banking risks 49,719 54,794

– regulatory deductions –51,865 –46,620

of intangible values –12,189 –8,424

– other items to decrease basic capital

Gross shareholders' equity 279,898 278,666

+ complementary and supplementary capital 10,998 8,969

– Other deductions attributable to capital

Eligible capital 290,896 287,635

6. Eligible capital and capital requirements

As statutory auditor, we have audited the accompanying consolidated financial statements of PKB Privatbank SA, which comprise the balance sheet, income statement, cash flow state-ment, statement of changes in shareholders' equity and the annex (pages 14 to 34) for the financial year ending on 31 December 2014.

Board of Directors’ responsibilityThe Board of Directors is responsible for the preparation of the consolidated financial state-ments in compliance with the law and the consolidation and valuation standards set out in the annex. This responsibility includes designing, implementing and maintaining an inter-nal control system relevant to the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error. The Board of Directors is also responsible for selecting and applying appropriate accounting standards and estimates.

Auditor’s responsibilityOur responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in compliance with Swiss law and Swiss Auditing Standards. Those standards require that the audit be planned and performed to obtain rea-sonable assurance that the financial statements are free of any significant errors.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. It is up to the auditor's professional judgement to choose the verification procedures. These include the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, the auditor shall consider the internal control system, to the extent that it is significant for preparation of the consolidated financial statements, to design audit procedures suitable to the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the internal control system. An audit also includes evaluat-ing the appropriateness of the accounting policies used and the reasonableness of accounting estimates made, as well as evaluating the overall presentation of the consolidated financial statements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the consolidated financial statements for the year ended 31 December 2014 give a true and fair view of the equity, financial and income position in compliance with Swiss banking and Swiss civil law.

Report on other legal requirementsWe confirm that we meet the legal requirements on licensing pursuant to the Auditor Over-sight Act (AOA) and for independence (article 728 Code of Obligations (CO) and article 11 AOA) and that there are no circumstances incompatible with our independence.

Pursuant to Article 728a, paragraph 1 item 3 CO and Swiss Auditing Standard 890, we con-firm that there is an internal control system designed for the preparation of consolidated financial statements according to the Board of Directors' directives.

We recommend that the consolidated financial statements submitted to you be approved.

Lugano, 24 March 2015Ernst & Young SA

Erico Bertoli Bruno PatusiAccredited Audit Expert Accredited Audit Expert(Auditor in charge)

auditors' report on te consolidated annual financial statements

To the general shareholders' meeting of PKB Privatbank SA, Lugano

Comments on the balance sheet 39 Comments on the income statement 41 Financial Statements 42 Income Statement 44 Annex to the annual financial statements 46 Auditors' report 55

Contents

p a r e n t c o m p a n y f i n a n c i a l s tat e m e n t s

As at 31.12.2014 the total assets amounted to chf 3,103.5 million against liabilities of chf 2,205.0 million; the shareholders' equity, including net profit for the year, therefore totalled chf 291.8 million. The increase in the balance sheet total with respect to the previous year was chf 898.5 million, or 40.8%. This strong rise was due mainly to the acquisition of the LLB Lugano branch.

Assets Liquid assets This item includes cash plus clearing and postal account balances. The total of chf 1,002.5

million is well above the legal requirement for primary liquidity.

Receivables from banks Down by chf 539,2 million (–59.0%), amounts held with banks went from chf 914.4 mil-lion to chf 375.2 million.

These were chf 375.2 million, of funds deposited with major banks in OECD member states. Time deposits accounted for chf 191.4 million, with chf 152.5 million maturing in 90 days, while sight deposits came to chf 183.8 million.

Due from customers Amounts due from customers rose by 40.6%, from chf 504.9 million to chf 710.1 million.

Mortgage loans Mortgage loans increased by 358.5%, going from chf 139.1 million a chf 637.8 million, as a result of the acquisition of the LLB Lugano branch portfolio.

Securities and precious metals The book value rose from chf 0.4 million to chf 13.7 million. held for trading

Financial investments As at 31.12.2014 financial investments totalled chf 143.2 million against chf 95.6 million the previous year (+49.8%). Investments in funds totalled chf 20.8 million (chf 16.9 million as at 31.12.2013), whereas fixed income securities increased, reaching chf 122.4 million (chf 78.7 million as at 31.12.2013), of which chf 21.5 million pledged in favour of correspondent banks (chf 16.7 million as at 31.12.2013).

Principal shareholdings The bank holds the entire share capital of PKB Privatbank Ltd, St. John’s, Antigua, PKB Banca Privada (Panama) SA, Valuevalor AG, Lugano and Planetarium PKB Consultoria SA, Montevideo. Also in this item there are minority shareholdings in Cassa Lombarda Spa, Milan (33.9%), Anthilia Capital Partner Spa, Milan (36.6%), Aduno SA, Zurich (0.28%), Queluz Gestao de Ativos, San Paolo (10%) and EIH Endurance Investments Holding SA, Lugano (25%).

Fixed Assets These rose from chf 31.6 million to chf 42.6 million (+chf 11.1 million, or 35.2%). This represents tangible and intangible fixed assets that include the bank’s buildings along with fixtures and furnishings, any capitalised renovation works, computer hardware and Go-odwill paid for the acquisitions.

Other assets Other assets increased to chf 45.5 million as at 31.12.2014, against chf 22.2 million at the end of the preceding year. This item consists mainly in positive replacement values that amount to chf 44.6 million. Positive replacement values concern derivative financial in-struments, taken out on behalf of the bank or on behalf of clients and represent claims on counterparties.

c o m m e n t s o n t e b a l a n c e s e e t Balance sheet total

Payables to banks Payables to banks went from chf 356.9 million to chf 286.1 million (–19.9%).

Payables to clients These are up by chf 923.3 million, being 65% (chf 2,345.1 million as at 31.12.2014, chf 1,421.8 million as at 31.12.2013). The very low level of interest rates of the main currencies and the uncertainty in financial markets generated a build-up of cash in customers’ bank accounts, pending better investment opportunities.

Other liabilities This item amounted to chf 46.5 million as at 31.12.2014 (+chf 20.5 million, or 78.8% com-pared to the previous year). These predominantly comprise the Bank’s liabilities for indirect taxes (chf 6.3 million) as well as negative replacement values on derivative instrument tran-sactions (chf 40.2 million), representing its liability exposure to counterparties.

Shareholders' equity Shareholders' equity as per balance sheet totals chf 269.5 million, (excluding reserves for general banking risks and the year’s net profit). After approval of the Board of Directors’ proposal for the allocation of profits by the Shareholders’ Meeting, shareholders’ equity on the balance sheet will amount to chf 276.8 million.

c o m m e n t s o n t e b a l a n c e s e e t Liabilities

An examination of the various totals in the Income Statement shows net interest income at chf 18.6 million, sharply up from the previous year (+57.7%) mostly as a result of the merger, as at 01.01.2014 and the LLB, Lugano receivables portfolio..

Commissions and provision of services increased (+20.8%) which may be broken down into credit operations (+14.5%), securities trading and investment operations (+22.0%), provision of other services (+12.0%) and expenses for commissions (+11.0%): apart from the aforementioned acquisition, there was also an encouraging organic development of the business carried out by all of the Bank's offices.

Overall, the result from trading operations totalled chf 13.3 million against 11.9 million as at 31.12.2013 (+11.6%).

Other ordinary income came in at chf 6.0 million, compared to chf 3.6 million the pre-vious year (+65.3%).

Total revenues can be broken down as follows: 15,7% from interest operations 67,9% from commissions and services 11,3% from trading operations 5,1% from other ordinary income.

Expenses Personnel costs went from chf 47.1 million as at 31.12.2013 to chf 56.7 million as at 31.12.2014

(+chf 9.6 million coming to 20.4%). A good part of the increase may be put down to staff acquired with the LLB Lugano branch merger, as well as to a strengthening of the entire organization, specifically in front-office business and in what are considered the Bank's «core» markets. Overhead increased by 28.4%, which as at 31.12.2014 came to chf 17.0 million compared to chf 13.2 million as at 31.12.2013. This was in any event an exceptional and non-recurrent rise, mostly brought about by special development projects, legal and regulatory risk management and data migration.

Gross profit Gross profit for the year came to chf 44.6 million, up by chf 11.0 million (+32.9%) over 2013.

Depreciation of fixed assets Total depreciation came to chf 11.4 million, up by chf 4.9 million compared to the previous period, mainly due to significant infrastructure investments and ordinary amortisation of the goodwill from the last acquisition made.

Valuation adjustments, These increased from chf 6.3 million to chf 8.1 million mainly due to the rise in legal provisions and losses risks. In 2014, losses totalling chf 0.4 million were posted to the accounts, while provisions

for operational risks of chf 7.7 million were made.

Extraordinary revenues The total of chf 2.3 million, were essentially from the dissolution of tax credit.

Extraordinary expenses The entire amount of chf 0.2 million may be accounted for by miscellaneous losses.

Net profit for the year Net profit came to chf 22.2 million. Comparison with the previous year's profit of chf 16.5 million shows a rise of chf 5.7 million or 34.7%.

Revenues

c o m m e n t s o n t e i n c o m e s tat e m e n t

b a l a n c e s e e t Assets a mo u n ts i n c f 20132014

Liquid assets 1,002,470,629.65 386,125,698.70

Receivables arising from money market securities 4,657,523.33 291.62

Due from banks 375,241,494.45 914,436,584.81

Due from customers 710,061,500.17 504,934,338.44

Mortgage loans 637,836,268.94 139,119,506.24

Securities and precious metals held for trading 13,697,724.14 384,946.62

Financial investments 143,228,872.01 95,624,671.20

Participations 94,241,222.92 89,259,804.70

Fixed assets 42,659,431.65 31,556,928.89

Prepayments and accrued income 33,900,849.97 21,387,575.34

Other assets 45,473,445.94 22,177,866.69

Total assets 3,103,468,963.17 2,205,008,213.25

Total deferred credits 0.00 0.00

Total receivables from companies of the Group and holders of qualifying shareholdings 3,142,926.29 1,544,389.72

Liabilities a mo u n ts i n c f

Due to banks 286,064,585.63 356,894,466.08

Commitments to customers in savings and investments 2,996,667.88 2,369,033.56

Other payables to customers 2,342,126,417.81 1,419,475,338.73

Medium-term notes 0.00 0.00

Prepayments and accrued income 37,764,865.46 30,324,302.38

Other liabilities 46,523,383.37 26,025,067.85

Value adjustments and provisions 49,882,325.11 40,052,350.80

Reserves for general banking risks 46,350,000.00 46,350,000.00

Share capital 16,000,000.00 16,000,000.00

General legal reserve 41,000,000.00 40,900,000.00

Other Reserves 212,000,000.00 209,500,000.00

Retained earnings 517,653.85 605,653.85

Net profit for the year 22,243,064.06 16,512,000.00 Total liabilities 3,103,468,963.17 2,205,008,213.25

Total deferred commitments 0.00 0.00

Total receivables from companies of the Group and holders of qualifying shareholdings 285,007,016.66 241,940,839.86

201319982014

o f f - b a l a n c e s e e t o p e r at i o n sa mo u n ts i n c f 20132014

Contingent liabilities 76,880,157.98 45,590,520.03

Irrevocable commitments 10,009,928.67 6,976,916.18

Payment and additional funding commitments 2,427,376.54 2,806,702.15 Derivative financial instruments:

Positive replacement value 44,665,118.16 20,848,683.03

Negative replacement value 40,204,795.44 21,292,754.65

Contract volumes 3,129,329,691.40 1,662,830,698.37

Fiduciary operations 131,963,401.51 176,485,313.92

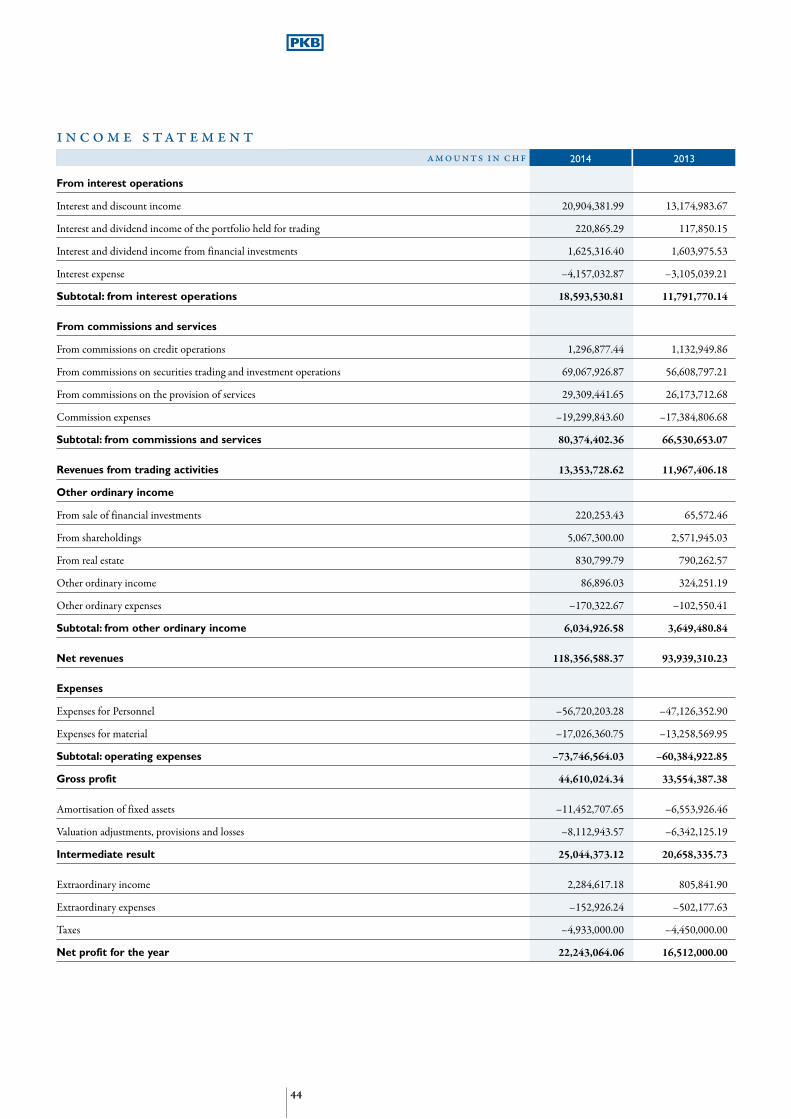

i n c o m e s tat e m e n t a mo u n ts i n c f 20132014

From interest operations

Interest and discount income 20,904,381.99 13,174,983.67

Interest and dividend income of the portfolio held for trading 220,865.29 117,850.15

Interest and dividend income from financial investments 1,625,316.40 1,603,975.53

Interest expense –4,157,032.87 –3,105,039.21

Subtotal: from interest operations 18,593,530.81 11,791,770.14

From commissions and services

From commissions on credit operations 1,296,877.44 1,132,949.86

From commissions on securities trading and investment operations 69,067,926.87 56,608,797.21

From commissions on the provision of services 29,309,441.65 26,173,712.68

Commission expenses –19,299,843.60 –17,384,806.68

Subtotal: from commissions and services 80,374,402.36 66,530,653.07

Revenues from trading activities 13,353,728.62 11,967,406.18

Other ordinary income

From sale of financial investments 220,253.43 65,572.46

From shareholdings 5,067,300.00 2,571,945.03

From real estate 830,799.79 790,262.57

Other ordinary income 86,896.03 324,251.19

Other ordinary expenses –170,322.67 –102,550.41

Subtotal: from other ordinary income 6,034,926.58 3,649,480.84

Net revenues 118,356,588.37 93,939,310.23

Expenses

Expenses for Personnel –56,720,203.28 –47,126,352.90

Expenses for material –17,026,360.75 –13,258,569.95

Subtotal: operating expenses –73,746,564.03 –60,384,922.85

Gross profit 44,610,024.34 33,554,387.38

Amortisation of fixed assets –11,452,707.65 –6,553,926.46

Valuation adjustments, provisions and losses –8,112,943.57 –6,342,125.19

Intermediate result 25,044,373.12 20,658,335.73

Extraordinary income 2,284,617.18 805,841.90

Extraordinary expenses –152,926.24 –502,177.63

Taxes –4,933,000.00 –4,450,000.00

Net profit for the year 22,243,064.06 16,512,000.00

Proposed by the Board of directors a mo u n ts i n c f 20132014

a p p r o p r i at i o n o f r e ta i n e d e a r n i n g s

Net profit for the year 22,243,064.06 16,512,000.00

Retained earnings 517,653.85 605,653.85

Retained earnings 22,760,717.91 17,117,653.85

Distribution of profits

– General legal reserve 100,000.00

– Other reserves 2,000,000.00 2,500,000.00

– Distribution of a dividend of 15,000,000.00 14,000,000.00 Retained earnings 5,760,717.91 517,653.85

1. Operations and staff

PKB Privatbank AG is present in Lugano (registered office), where it operates as a

full-service bank and in Bellinzona, Geneva and Zurich where it provides private banking services.