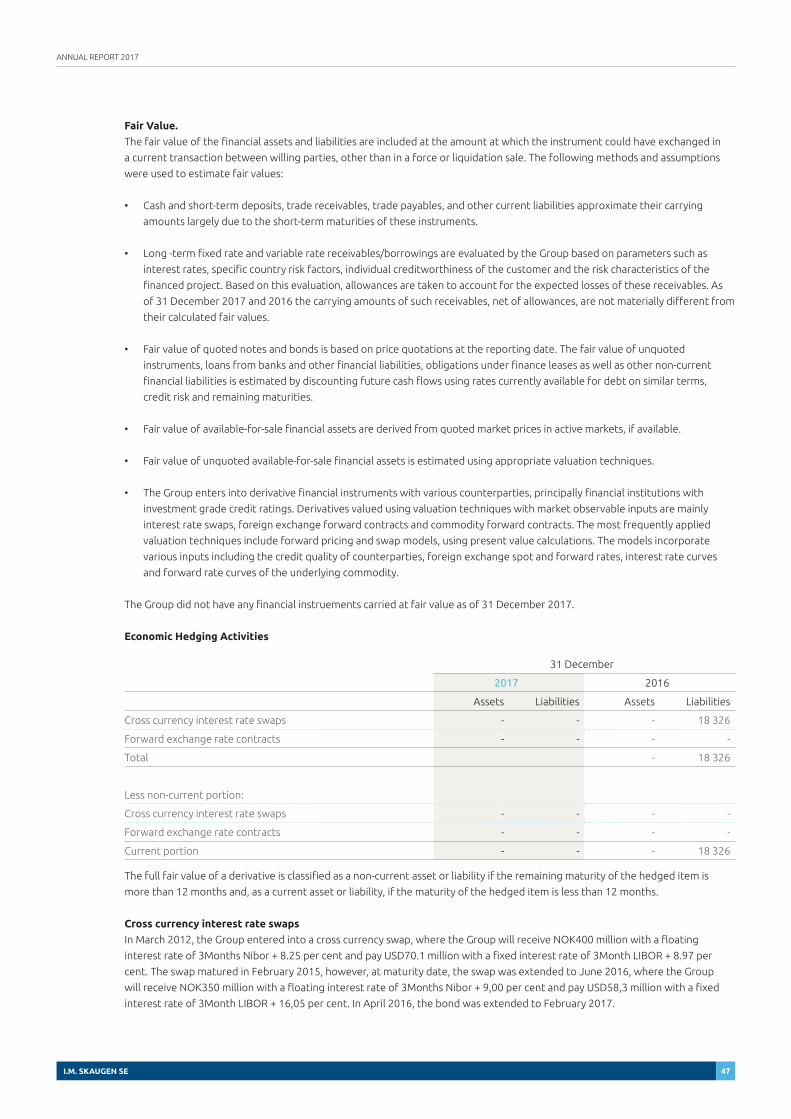

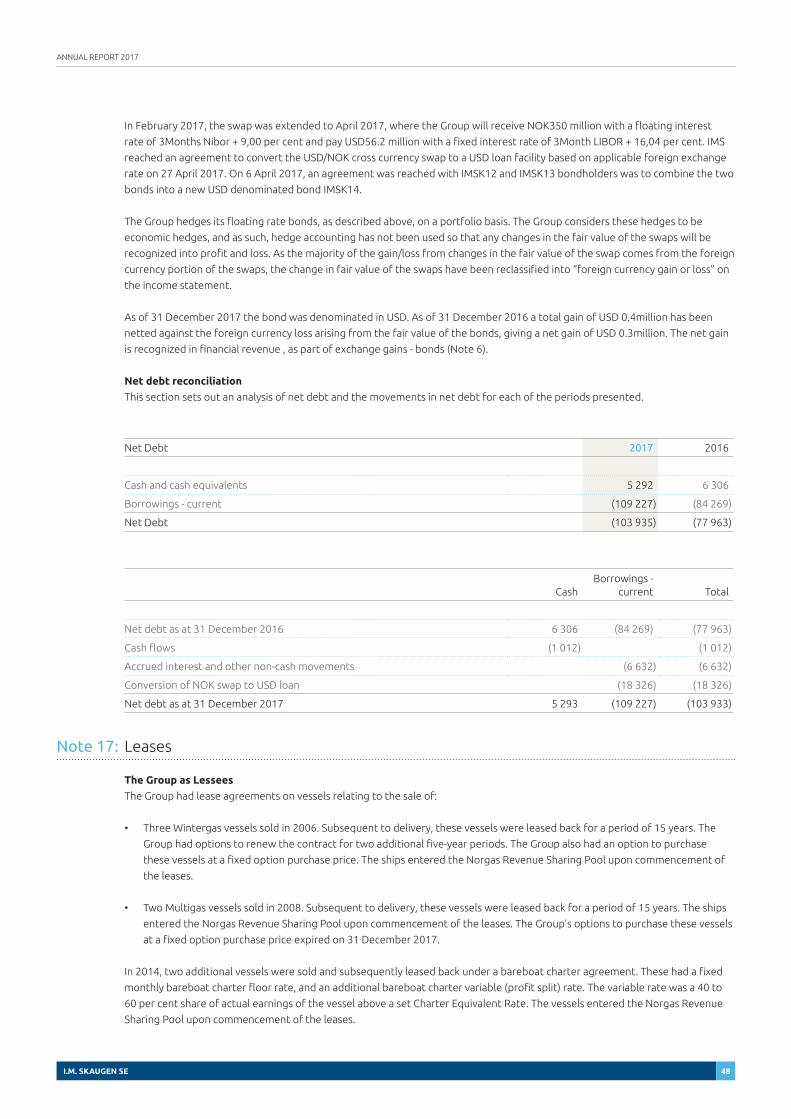

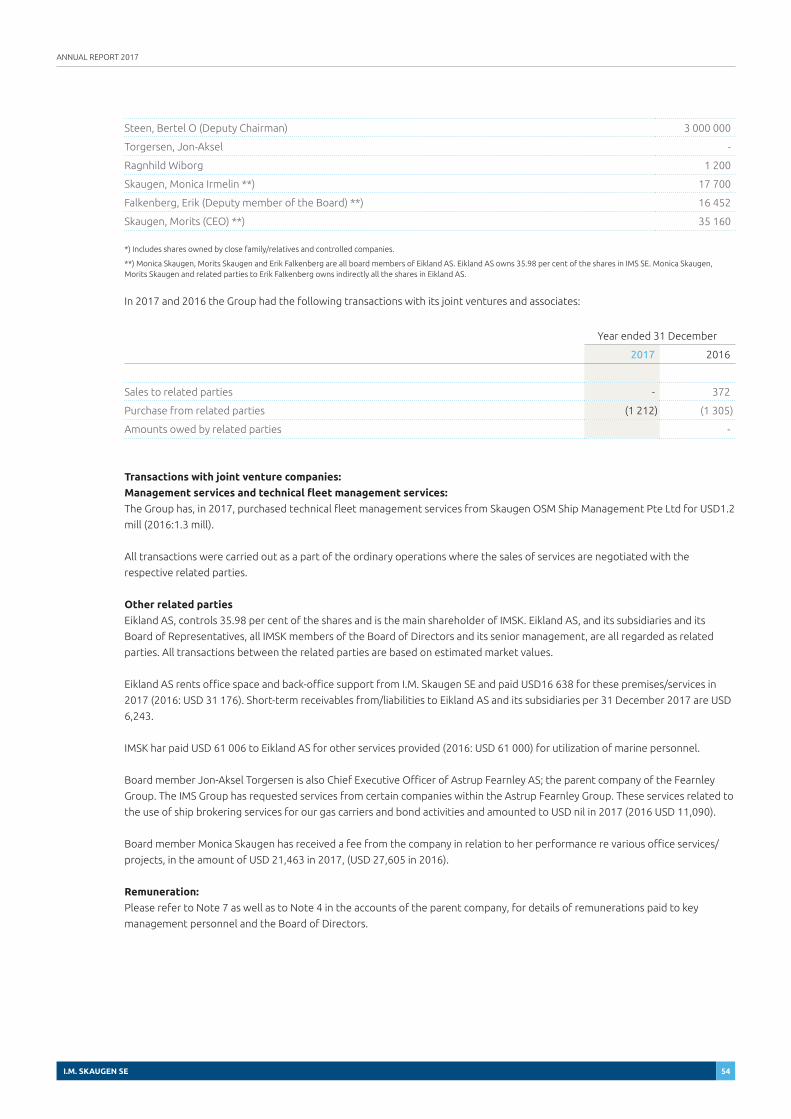

Embed Size (px)

Citation preview

Annual report 2017I.M. Skaugen SE – Innovative Maritime Solutions

ANNUAL REPORT 2017

I.M. SKAUGEN SE 2

Board of Directors’ Report 2017

The I.M. Skaugen Group’s (IMSK) is operating in a most challenging

LPG/Petchem gas transportation market that negatively affected the

trading of the vessels and thus the Groups earnings in 2017.

There was a sudden drop in demand in 2Q17, and we did see the

average “Norgas Time charter earnings” in 2017 at an “all-time”

low. The trading conditions were thus exceptionally difficult with

considerable waiting time for the cargo opportunities. This is

an industry wide situation and it reflects the performance of all

operators within our market segment.

The markets are still challenging with too many vessels available in

the market resulting in a low utilization of the global competitive

fleet. Voyage related costs have increased vs 2016 due to an increase

in bunker cost.

However, despite all this, we have also in 2017 managed to have

a better utilization of our fleet in terms of laden days (days with

paid cargo onboard) as compared with our competitors with spot

vessels. We are further satisfied with our safety record, operational

performance and relevant KPIs during the year.

The result for the year was further affected negatively by

impairments made in 4Q related to the unilateral termination of 6

bareboat chartered vessels by Teekay LNG Partners L.P (Teekay),

which were implemented in November 2017. On 16 November

Teekay announced to the public its intention to start a competing

pool with Norgas Carriers in the LPG/Petchem field but more

importantly within the Small Scale LNG field of business targeted by

IMSK in cooperation with Teekay and our other Norgas pool partners.

IMSK is in the process of completing a business transformation,

shifting its focus from seaborne transportation of LPG/

Petrochemicals (mostly spot business) to regional distribution of LNG

(feedstock for power plants or energy related/long term contract

business) through our unique fast-track, low capex Small Scale LNG

(SSLNG) concepts.

With the SSLNG contracts being lined up in the early parts of

2017, IMSK has been working very hard to execute on a previously

communicated refinancing plan, a plan which was prepared for IMSK to

be able to pursue these SSLNG business opportunities for the benefit

of all its stakeholders. The intention of this refinancing plan was to

make all the financial lenders and operational leaseholders (7 vessels)

whole over time, by securing a financing structure with maturity to

match the expected future cash flow of the group. This, we believed,

was achievable when the SSLNG projects would be operational.

Acceptable agreements with the secured creditors and the

bondholders were successfully secured with all conditions completed

by 8 June 2017. The refinancing extended the debt maturity until

6 April 2018 (certain conditions related to the agreements with

the secured lenders have been waived on a shorter-term basis due

to delayed start-up of the SSLNG project) and enabled the group

to engage in the next steps of the refinancing plan – namely a

rearrangement of the group’s operational leaseholders (7 vessels).

IMSK subsequently engaged in extensive discussions with the vessel

owners or the lease counterparties, with the aim of securing a

long-term rearrangement of these relationships for our Singapore

based subsidiary SMIPL Pte. Ltd (“SMIPL”). The counterparties of

these leases were in this period paid on an agreed “pay as you earn”

scheme with a deferment of the applicable bareboat hire. The

arrangement was contemplated to endure until the SSLNG contract

was operational. In the third quarter of 2017, IMSK managed to

agree on a consensual termination and redelivery with GasMar AS for

an 8,556 cbm LPG/Ethylene carrier that was on in-charter or lease.

The agreement was reached with standard and customary subjects

and the vessel was redelivered to GasMar AS in the early part of

December 2017. IMSK agreed to cover cost of a part of an upcoming

drydocking of the vessel to redeliver the vessel as per our contract.

This consensual solution did fit our ambitions as per the announced

refinancing plan as it allowed for a consensual solution where the

vessel owner can redeploy the vessel as desired and with the risk/

reward profile that fits the vessel owner.

IMSK further tried to reach consensual agreements with Teekay,

being the owners of the 6 vessels on charter to SMIPL. Five of these

vessels were on long term in-charter and one vessel was on a shorter

term in-charter. The one vessel on shorter term in-charter was subject

to performance guarantee by the parent company IM Skaugen SE.

Our plan was to arrange for a refinancing plan to ensure Teekay

was paid in full and in exchange for assisting us with the short-term

difficulties we had. Given the strategic partnership with Teekay,

and a long history of finding solutions and managing difficulties

we engaged with the aim to find solutions to the problems as they

transpired, and we believed that this was possible. Until 3Q2017

the discussions with Teekay (since 2003) were constructive in terms

of trying to find a consensual solution, in line with our refinancing

plan and thus also to benefit all our stakeholders, including Teekay

(since 2003). A key feature was the agreement to have a “pay as

you earn” scheme with Teekay re its 6 ships given the operational

challenges in the industry. We believe that, given time to successfully

implement the SSLNG projects, this was a feasible plan and to the

clear advantage of Teekay. We exchanged significant and detailed

information re the IMSK business plans and IMSK refinancing

plan. Teekay further asked for and got supplemental detailed and

confidential information not shared with any others. After the

exchange of detailed financial forecasts in late August 2017 we

noticed immediately a more complicated situation in our relationships

with Teekay. In the early parts of 4Q2017 we continued to pursue and

negotiated to get to the revised commercial terms and continued

the transparent cooperation in good faith with the assumption that

the strategic partnership remained. It was therefore a major surprise

to IMSK that our subsidiary SMIPL received unilateral termination

notices concerning these 6 Teekay vessels on 16 November 2017.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 3

IMSK was further informed by media releases the same day that

Teekay had already established its own competing LPG/Petchem and

SSLNG pool intended to operate these vessels and other Norgas pool

vessels on their own, instead of through the Norgas Carriers pool.

In the aftermath of this a “surprise attack”, a massive legal process has

followed between the parties. Although Teekay has publicly announced

that terminating the charters was for it a beneficial and profitable

move, Teekay has taken legal steps against IMSK group of companies

concerning alleged losses. It is evident that these activities cannot be

measured against the commercial realities of a financial creditor and

when looking at the tactical activities before November 16th, 2017

and the many legal activities afterwards there is a plan to scuttle the

Norgas Carriers` activities and enable the competing Teekay pool to

take over the business and the relationships. The IMSK group on its

end has large counterclaims because of the events that have unfolded

and leading up to unilateral terminations. The cases are currently being

dealt with through the courts and in arbitrations, and we do believe

that it will take some time for these to be resolved.

IMSK – Refinancing Plan 2018

The Board has continuously assessed continued operations based on

the main factors of upcoming debt payment, future cash flows and

the refinancing plans, with book equity as a secondary factor. On this

basis we have pursued a comprehensible refinancing plan that would

enable the company to continue to operate as envisioned and as per

our strategy. As announced by IMSK in December 2017, the overall

refinancing plan needed to be reworked as its subsidiary SMIPL had

reduced ability to make any of its counterparties whole because of the

huge loss of revenue caused by the unilateral lease terminations by

Teekay. As such, SMIPL made the steps to right size its business and

particularly to reduce liabilities and debt and by this improve its cash

flow. As IMSK has had no legal obligation to, or guarantees for SMIPL

liabilities, save for a guarantee re one vessel, IMSK decided that it will

discontinue recognizing further losses of SMIPL on a consolidated level.

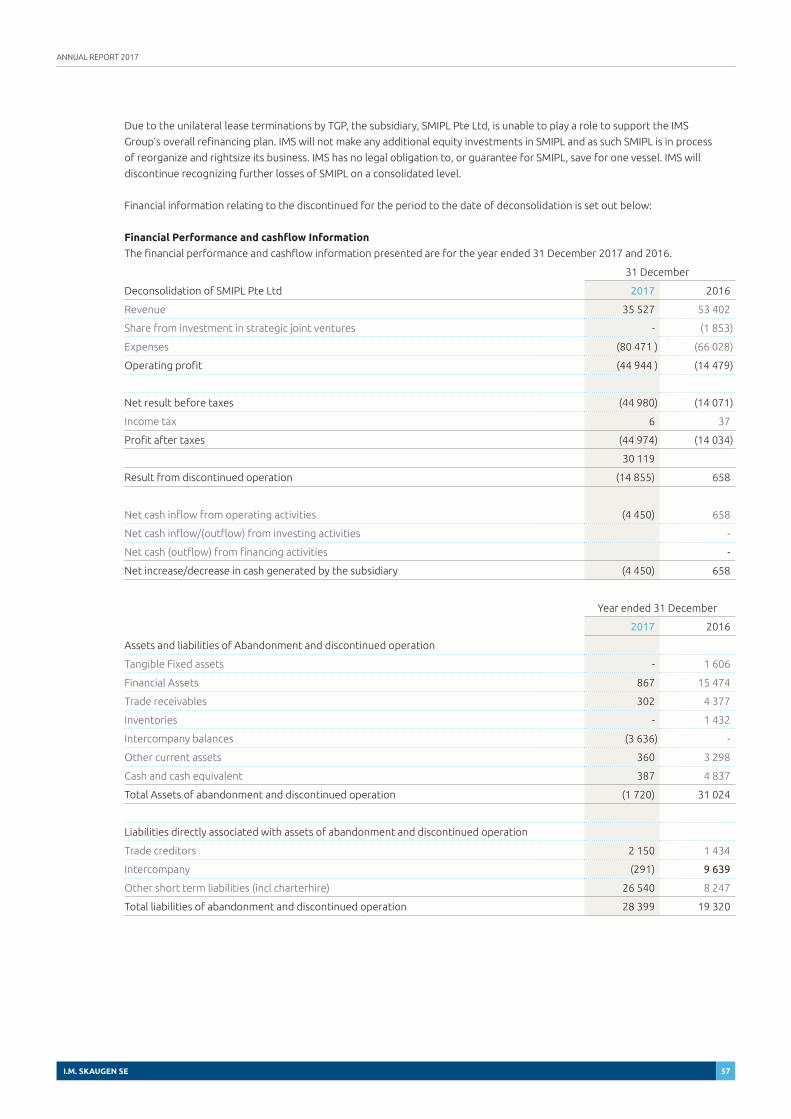

Consequently, SMIPL is deconsolidated per year end 2017.

The Board has actively worked to refine and execute the required

or revised refinancing plan of IMSK and on 4 April 2018 the Board

announced its plan to carry out refinancing by a “Newco structure”

and the “Newco plan” was discussed with shareholders on 25

April 2018 and with IMSK 14 bondholders on 19 April 2018. Both

stakeholders approved the “Newco plan” in principle and urged

for the Board to execute on the plan. Teekay made it immediately

known that it had objections to the “Newco plan”. There was and

is a need for consensual solutions to be reached with all creditors

and subsequently the Board decided on 31 May 2018 to file for a

moratorium under the Singapore Scheme of Arrangement, to achieve

the best outcome possible for all stakeholders. The 31 May 2018 filing

for the Scheme of Arrangement in Singapore was preliminary. On 27

June 2018, the Singapore Court granted a moratorium of 3 months

beginning from 28 June 2018, and worldwide against certain entities

of Teekay which commenced arbitrations and/or court proceeding

against IMSK and certain subsidiaries. On this basis the Board has

decided that it can continue its operations based on a going concern

assessment that the plan submitted on 4 April 2018 and later

amended and submitted to the Singapore courts has a significant

chance of being implemented.

There are two large debt payments that are currently due:

1. The Bond of debt of abt. US$57m which fell due on 6 April 2018.

2. The Bank payments totalling abt. US$55m due on 6 April 2018.

There are also various trade creditors from ongoing expenses

including the costs being expended on protecting the Group against

the legal processes bought about by Teekay as well as making the

IMSK claims against MAN.

The group’s cash position and cash flow are not in a state to fully

meet all the above on an ongoing basis.

In addition, it has been important to prepare the way for additional

risk capital acquisition in the future, in order to, enable a further

development of the SSLNG business to take place failing which this

project will not proceed as envisioned. As such fresh capital infusion

or debt is much wanted.

The markets for arranging debt finance are challenging and debt

financing is hard to attract for a company of our size and structure.

This is a particular challenge for our company going forward and one

the Company is putting considerable effort into overcoming. The

refinancing in the next several months is also dependent upon the

SSLNG project to reach its operational phase, which will contribute to

cash surplus from operations from the SSLNG project. The sad state

of the LPG/Petchem gas markets cannot yield any cash flow that can

sustain much debt on such a vessel.

The process had shown that it was not realistic to acquire any

debt funding or any new risk capital into IMSK at the present time

given the uncertainties created by the Teekay legal actions and

unwillingness to agree to any consensual solution. Investors were not

willing to commit fresh funds into the existing group due to these

legal efforts by Teekay. Their preference was, to invest in a new

investment vehicle and accordingly, we have in the above mentioned

“Newco Plan” set up Norgas Carriers AS which, at present, is a

subsidiary of IMSK, to be the proposed investment vehicle and if the

shareholders so desire, eventually become the new parent company

in a restructured group.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 4

During the refinancing process, the Board considered it expedient

for IMSK to remain listed on the Oslo Stock Exchange. However, with

the “Newco plan” being implemented IMSK will be delisted from Oslo

Stock Exchange 17 September 2018. Last day of listing will be 14

September 2018.

As per the plan it is for the time being not intended that Norgas

Carriers AS should be listed on the Oslo Stock Exchange. Rather, it will

be attempted to list it on an OTC exchange.

Filing Scheme Moratorium in Singapore

As it was announced on 31 May 2018, IMSK is seeking the assistance

of the Singapore Court to complete its refinancing plan. The

restructuring plan, if implemented, is in line with IMSK’ wishes to be

in a position to be able to remain a going concern and by this pay its

liabilities in full with its upcoming cash flow matching an amended

amortisation schedule of its liabilities. To achieve this goal, IMSK will

need the assistance of the Singapore Court through the scheme of

arrangement process.

IMSK, together with its wholly owned subsidiaries, SMIPL Pte Ltd and

IMSPL Pte Ltd (the “IMSK Scheme Companies”), filed applications

to the High Court of Singapore for a moratorium to commence

the reorganisation of liabilities and businesses of the IMS Scheme

Companies.

With the filing of the Scheme Moratorium, the IMSK Scheme

Companies now qualify for protection from the Singapore Court

under a 3-month moratorium that will apply against creditors’ claims.

The moratorium will provide much needed space and time for the

IMSK Scheme Companies to complete their business transformation

of LPG/Petrochemicals to regional distribution of LNG through its

unique fast-track, low capex Small Scale LNG concepts; target areas

for growth and pursue new business opportunities; and focus on the

ongoing discussions with strategic investors.

The Board is confident that this process may lead to an acceptable

refinancing plan being adopted and a reinvigoration of the IMSK

Group and it will assist us to be able to generate cash flow for the

benefit of the stakeholders.

In the meantime, the IMSK Group continues to pursue the announced

SSLNG opportunities, via Norgas Carriers AS, Norgas Carriers Pte Ltd,

and Somargas II Pte Ltd, which the IMSK Group has kept outside of

the Singapore scheme process.

For the execution of the “Newco plan” IMSK is in advanced discussion

with a “white knight” investor who will be able to provide USD3

million to Norgas Carriers AS for the refinancing and/or working

capital and restructuring purposes. However, as a condition

precedent to the investment, the investor had requested that the

IMS Group undertake a restructuring on the following broad terms,

which again are subject to further negotiations with the relevant

counterparts:

a. Norgas Carriers AS will purchase the two vessels necessary to

support the SSLNG Contract from Somargas (the “Somargas

Vessels”), or shares of Somargas; and

b. I.M. Skaugen SE will assign its economic benefit under the MAN

Claim to Norgas Carriers AS

The details of the proposed restructuring plan as submitted to the

Singapore court on 31 May 2018 are set out below where IMSK

intends to implement a scheme of arrangement and compromise

with the creditors on the following terms:

a. Norgas Carriers AS will either purchase:

1. Two vessels owned by Somargas II Pte Ltd (“Somargas”), or

2. The shares of Somargas from I.M. Skaugen SE

b. IMSSE will enter into an agreement with Norgas Carriers AS where

the economic benefits due to IMS under the certain claims against

MAN Diesel & Turbo S.E. and MAN Diesel & Turbo AS (the “MAN

Claims”) will be assigned to Norgas Carriers AS.

c. Norgas Carriers AS will, by way of novation, undertake to repay

in full the two facilities provided by the secured lenders to

Somargas and IM Skaugen SE respectively, and which are secured

by mortgage over the Somargas vessels, on terms to be agreed.

The outstanding debt due under these facilities stands at about

USD57 mill as of mid-May 2018.

d. Norgas Carriers AS will undertake to repay the unsecured creditors

of IM Skaugen SE in full via a one-to-one conversation of their

claims to two notes. The tentative terms of these two notes are:

1. A five-year note of approximately USD32 million with a

payment-in-kind interest of 3% per annum for the first three

years, and cash interest of 7.5% thereafter; and

2. An interest-free loan of approximately USD25 million, which

can be converted to 25% of the shares in NCAS on a fully

diluted basis.

The current unsecured creditors of IMSSE are: (i) the holders of

the IMSK14 Bonds, which currently stands at approximately USD57

million, (ii) GasMar AS, which currently stands at approximately

USD950,000; and (iii) other unsecured creditors. There is a contingent

claim by Teekay Group under the corporate guarantee provided by

IMS for SMIPL which is disputed.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 5

e. The shareholders of IMSE will be offered a 1 to 1 exchange of their

shares in IMSSE with shares in Norgas Carriers AS, and these shares

will constitute 50% of the share capital in Norgas Carriers AS.

Risks

IMSK is, through its normal business activities, exposed to political,

financial, operation and market related risks. These risks are closely

monitored to mitigate and manage our exposure.

Refinancing Risk. The markets for arranging debt finance are

challenging and debt financing is hard to attract for a company of our

size and structure for the time being. This is a particular challenge

for our company going forward and one the Company is putting

considerable effort into overcoming. The group’s current process

of refinancing in the next few months is also dependent upon the

Singapore Scheme of Arrangement being carried out and that the

SSLNG project will reach its operational phase, which again will

contribute to cash surplus from operations from the SSLNG project.

Failing to arrive at a acceptable refinancing plan, approved by the

Singapore Courts, through the Scheme of Arrangement will not

enable us to continue operations.

Market related risks. “Asset utilization” or keeping our ships gainfully

employed with the most efficient scheduling is the key driver to

profitability for the company. The demand for our services is exposed to

the changes in price levels of the commodities we transport and volumes

changes. The most relevant commodities are the core petrochemical

gases (ethylene, butadiene, propylene, vcm), as well as LNG. The

prices and trade of these four key petrochemical gases as well as LPG

and naphtha are monitored on a regular basis to uncover arbitrage

possibilities for our clients and where transportation will be needed.

IMSK monitors the LNG and the heavy fuel oil/diesel price differences,

which provides for the returns of potential investment and cost of

shipping, conversion, storage and re-gas for the SSLNG projects.

We are also subject to the changing costs for the services and raw

material we use. A significant part is related to fuel costs (bunker

prices) which directly affect our operating costs. In TC contracts, fuel

costs are paid for by the charterer and in spot contracts the freight

rate takes into account current fuels cost and by this we mitigate the

risks. Our COA contracts normally contain a “bunker escalation clause”

which protects both us and the charterer from changes above or

below certain agreed thresholds. Our risk exposure to fluctuations in

bunker prices is thus on the spot contracts.

Our main exposures to the financial market risks are currently due

to the USD, SGD and NOK exchange rates and in interest rates. Most

of our revenues are in USD. Most of our liabilities and assets are in

USD. Our bond and mortgage debt are currently exposed to variable

interest rates.

The group is also exposed to counterparty risks regarding our

counterparties` ability to meet their obligations. However, we aim

to trade only with recognized and creditworthy third parties, and

have historically had very few disputes relative to recovery of our

receivables.

Piracy at sea is a threat to the wellbeing of our crew and their

families, as well as to the business of our clients. We are focused

on the prevention of piracy incidents through early detection and

evasive tactics. The Norgas vessels are, as a matter of policy, sailing

with armed guards or in convoys if armed guards are not available,

when piracy hot spots cannot be avoided.

We have insurances for our ships, that also cover third party vessels

in case of accident, as well as damages to the environment and

accidents causing personnel harm. We also carry insurance to cover

potential losses related to pirate activities. In all cases, we carry a

higher deductible to ensure lower costs. We do not carry external

loss of hire insurance, but manage this through an internal loss of

hire pool. This has paid off historically, due to the well-functioning

management of the company.

We have a few times been subject to fraud and embezzlement that

cause a significant loss to the company and/or its reputation. We take

every precaution to avoid such risks and always aim to recovering our

funds. Legal steps have been taken to recover funds from fraud in

the MAN cases and funds embezzled from us in China, of which some

of these have been traced to the US. We have successfully identified

these funds in China and in the US and are in the process of recover

some of the funds. See separate cover below of the MAN litigation

for its fraud.

Major legal disputes - A summary of the MAN fraud claim

In 2017, IMS managed to extract payment from MAN of around

EUR6.25 mill., which represented our principal claims and legal cost

as awarded in an ICC arbitration award dated May 12th 2017. In the

arbitral award, the arbitrators gave a unanimous decision that IMS

had been defrauded by MAN in connection with the sale of 8 MAN

medium speed marine diesel engines (sold by MAN in the period

2000 - 2006), including the 2 engines in this dispute (not yet installed

in any ships). The arbitrators held that IMS had proven that all 8

MAN engines consumed considerably more fuel oil than shown in

the official Factory Acceptance Tests (FAT) for these engines and

ANNUAL REPORT 2017

I.M. SKAUGEN SE 6

considerably more than the level warranted by MAN. The arbitrators

also considered it proven by IMS that MAN had committed fraud by

manipulating these FATs in order to conceal their fraud and by this

show a lower-than actual fuel consumption. The secret software

installed at the MAN factory test bed was installed with the sole

purpose of concealing their fraud and the true performance of

their engines. Due to years of neglect of their R&D the MAN marine

diesel engines consumed much more fuel than all their competitors.

In order to be able to sell underperforming marine diesel engines

they had to manipulate the FAT tests and make the statements that

were misleading to the clients. MAN has admitted the fraud when it

comes to 3 of the 8 engines sold to IMS, but not the two resolved by

this dispute. Previously MAN has admitted that the “parent engine”

in question has a fuel consumption that is considerably higher than

the solution they offered in 2000 and which was ordered by IMS. In a

court award dated 28 March 2013 from the Augsburg District Court a

judge awarded MAN a fine for their fraudulent processes committed.

From the admitted fraud of our “parent Engine” ordered in 2000

and the fraud as per Augsburg court documents these fraudulent

processes must have lasted for more than a decade at this one

factory.

Despite the arbitral award, MAN refused to acknowledge their

fraud and pay the amount awarded to IMS. Therefore, IMS had to

initiate enforcement proceedings before the Danish court in order

to force MAN to pay the monies owed under the arbitral award. The

Danish courts agreed with IMS, denied all of MAN’s objections to

enforcement, and granted enforcement, and granted enforcement

of IMS’ principal claim. Resulting in MAN paying around EUR6.25

million. MAN also objected to pay IMS’ claims for interest under the

arbitral award. MAN did, however in enforcement court, pay around

EUR384,000 in interest to IMS.

Based on the successful outcome of the above award and

determining fraud related to 8 engines we need to pursue MAN for

the remaining 6 engines The Supreme Court of Norway has in 2017

decided that IMS can proceed to bring claims against MAN with

respect to the remaining 6 of the 8 medium speed diesel engines

mentioned above, which are installed in vessels currently in operation.

The case will proceed before the Oslo courts in 4Q18. The claim for

excess fuel consumption is due to the MAN fraud in this respect are

expected to amount to about USD 50-60mill for the six engines in

question. About 2/3 of this amount is actual cost for covering excess

fuel costs (for the lifetime of these engines) caused by MAN’s fraud

in relation to these engines and the rest it is compounded interest

on these amounts since year 2003. These six affected vessels are

by now a little more than half way in their expected lifetime, and

the requested damages for the excess fuel costs will likely depend

on a number of factors. It is too soon to indicate a timing for a final

decision in this respect in the Norwegian court system.

IMS also has 4 x two-stroke or low speed MAN engines (2 of which

are installed in vessels currently in operation) that we have evidence

of having been subject to a similar fraud. A claim for this fraud will

be discussed, pending arbitration proceedings with MAN in Denmark

under Danish laws. It is too soon to indicate a timing for a decision

in this case, but it will only be in 2019. The USD cost of the excess

fuel consumption due to the fraud is at similar levels to the six

vessels mentioned above, but since we only claim for losses for two

ships until December 2017 the total claim is for about USD 8 mill. In

addition we claim for refund of prepayment, resulting in a total claim

of around USD 10 mill. in the arbitration. Finally, IMSPL Pte. Ltd.

(“IMSPL”) has brought setting aside proceedings before the Danish

courts applying for the setting aside of an arbitral award rendered in

a prior arbitration concerning the mentioned two-stroke engines. This

award was rendered in April 2017 with a strong dissenting opinion

in IMSPL’s favor. In the case, IMSPL was not allowed to introduce

significant evidence in relation to MAN’s fraud, including the technical

evidence mentioned above showing an overconsumption of fuel on

the engines in question. The above-mentioned pending arbitration

therefore arises out of this prior arbitration. We have also had a

positive judgement by Singapore courts to allow the case of tort

against MAN to proceed in Singapore. MAN has however appealed

this decision in an effort to fight off Singapore as a jurisdiction and

venue for dispute.

In Singapore IMSK and IMSPL have claimed MAN and MAN Diesel &

Turbo Norge AS with similar claims and reasons as described above,

and MAN has initiated enforcement proceeding in Singapore against

IMSPL concerning the arbitral award mentioned above. Both cases

will need to be settled following the decisions on the matters dealt

with above.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 7

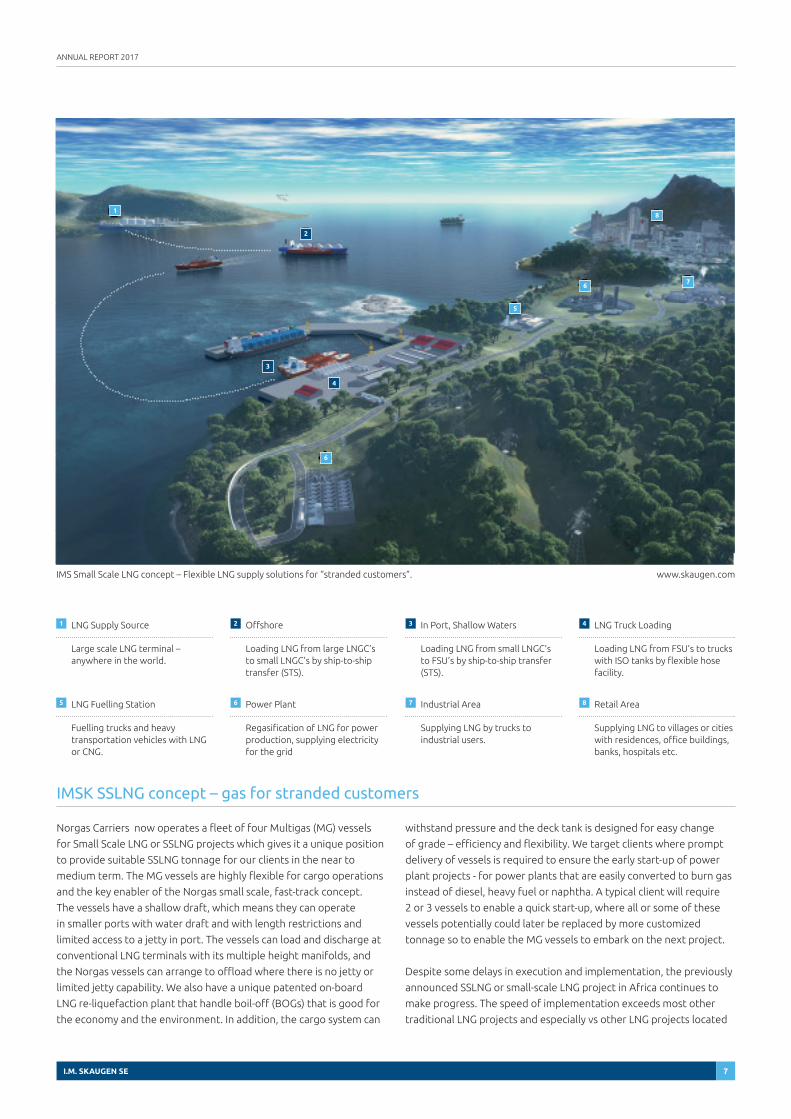

IMSK SSLNG concept – gas for stranded customers

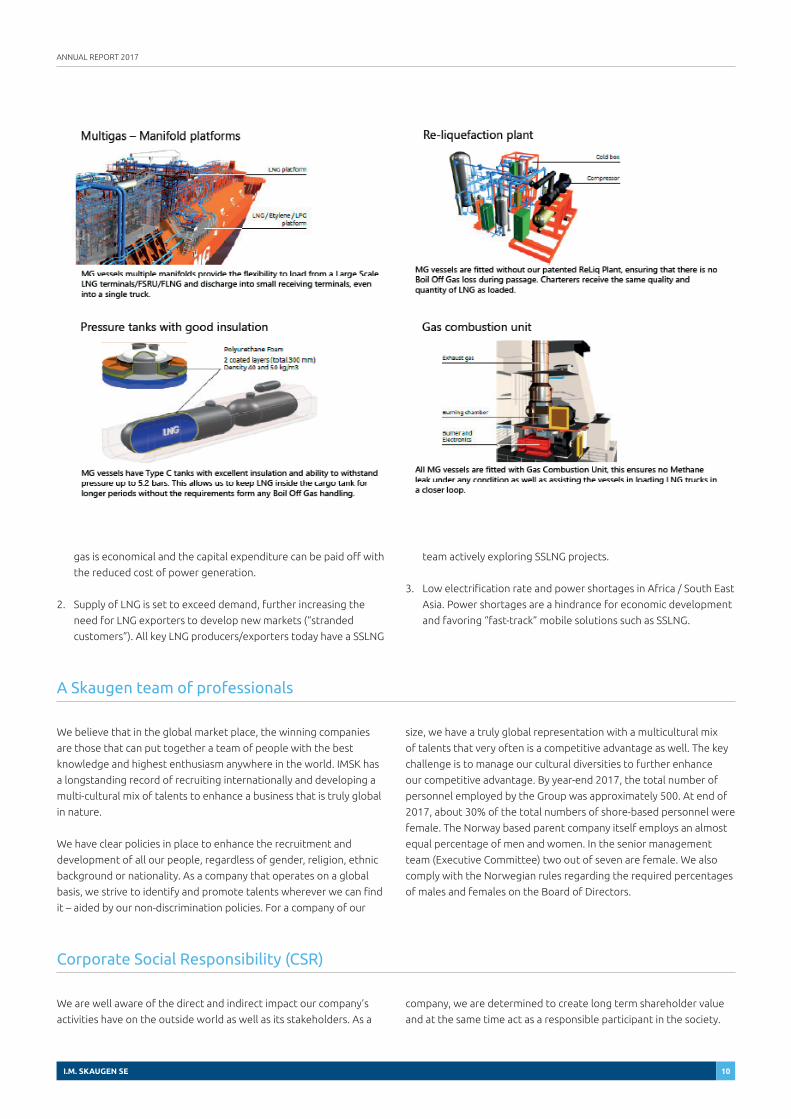

Norgas Carriers now operates a fleet of four Multigas (MG) vessels

for Small Scale LNG or SSLNG projects which gives it a unique position

to provide suitable SSLNG tonnage for our clients in the near to

medium term. The MG vessels are highly flexible for cargo operations

and the key enabler of the Norgas small scale, fast-track concept.

The vessels have a shallow draft, which means they can operate

in smaller ports with water draft and with length restrictions and

limited access to a jetty in port. The vessels can load and discharge at

conventional LNG terminals with its multiple height manifolds, and

the Norgas vessels can arrange to offload where there is no jetty or

limited jetty capability. We also have a unique patented on-board

LNG re-liquefaction plant that handle boil-off (BOGs) that is good for

the economy and the environment. In addition, the cargo system can

withstand pressure and the deck tank is designed for easy change

of grade – efficiency and flexibility. We target clients where prompt

delivery of vessels is required to ensure the early start-up of power

plant projects - for power plants that are easily converted to burn gas

instead of diesel, heavy fuel or naphtha. A typical client will require

2 or 3 vessels to enable a quick start-up, where all or some of these

vessels potentially could later be replaced by more customized

tonnage so to enable the MG vessels to embark on the next project.

Despite some delays in execution and implementation, the previously

announced SSLNG or small-scale LNG project in Africa continues to

make progress. The speed of implementation exceeds most other

traditional LNG projects and especially vs other LNG projects located

1

2

3

4

5

67

IMS Small Scale LNG concept – Flexible LNG supply solutions for “stranded customers”. www.skaugen.com

LNG Supply Source

Large scale LNG terminal – anywhere in the world.

Offshore

Loading LNG from large LNGC’s to small LNGC’s by ship-to-ship transfer (STS).

In Port, Shallow Waters

Loading LNG from small LNGC’s to FSU’s by ship-to-ship transfer (STS).

LNG Truck Loading

Loading LNG from FSU’s to trucks with ISO tanks by flexible hose facility.

LNG Fuelling Station

Fuelling trucks and heavy transportation vehicles with LNG or CNG.

Power Plant

Regasification of LNG for power production, supplying electricity for the grid

Industrial Area

Supplying LNG by trucks to industrial users.

Retail Area

Supplying LNG to villages or cities with residences, office buildings, banks, hospitals etc.

1 2 3 4

5 6

6

7 8

8

ANNUAL REPORT 2017

I.M. SKAUGEN SE 8

Power plant #1 site’s LNG storage and newly built regas facility on site.

Simulation of operations at the port facility in December 2017.

Professional IMS team and Norgas team.

Power plant #2 site’s LNG storage and newly built regas facility on site.

Port facility installation completed.

Port facility installation completed.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 9

in other locations . This will be the first LNG receiving facilities put

into use in sub-Sahara Africa and is a good proof of concept in West

Africa where ports are congested and often with shallow water

Our clients spent at first less time on approvals, both preparations

and applications, than in many other places. But the clients are now

spending this time after completion of the SSLNG facilities to enable

them to get all approvals for import and to receive the LNG, and

arrange the regasification of the LNG at site.

The power plant clients, with support of the Norgas team of

professionals, are ready to receive and consume gas in the form

of LNG. All equipment is site-specific equipment and whatever is

required has been installed at site. By being site specific and tailor

made, it is also a nice fit with the Norgas SSLNG solutions and its

ships. All capex expended on these facilities to date has been paid for

by our clients. Complete gassing up and cooldown of the receiving

LNG and on site regas - facilities with liquid nitrogen has been

performed and no major deficiencies were observed. Construction of

the port facility to receive LNG and load trucks has been completed.

The power plant clients initiated the SSLNG project with Norgas

on a “private” basis and without any formal support from the

local Government. We all managed to construct an LNG receiving

infrastructure in less than 12 months – this has never been done

before in the world. Since 3Q2017 the government has taken interest

in the concept and want it to be an integral part of their energy plans.

An alignment with their national energy policy has been ongoing and

this has caused some delays. A state owned entity has been selected

as the government owned entity that will import the LNG and then

supply the power plants and to be the aggregator. This is very positive

for power plant clients who by this will buy gas from the government,

sell electricity to the government, and better balance their cash flow /

risk.

Startup of the project is in reality only pending finalization of the final

relevant government approvals related to LNG import to the country.

Our clients have made good progress and managed so far to obtain

all the necessary endorsements, permits and approvals. We believe

that our clients will be able to obtain the remaining Government

approvals shortly, which will enable them to start the importation of

LNG with our MG vessels. The SSLNG project will start with 2 x MG

vessels shuttling and going soon to 3 ships (and then perhaps 4 ships

as volume in the region increases).

There is a limited availability of alternative tonnage for fast track

SSLNG projects, except for the 4 Norgas vessels. With the first SSLNG

proof of concept being operational shortly, we envision that it will

be relatively easier to initiate contractual talks regarding the balance

of the fleet within SSLNG projects in the pipeline. In this connection,

Norgas has several projects that we are pursuing which will be easier

to move to a close after this SSLNG proof of concept has now been

demonstrated.

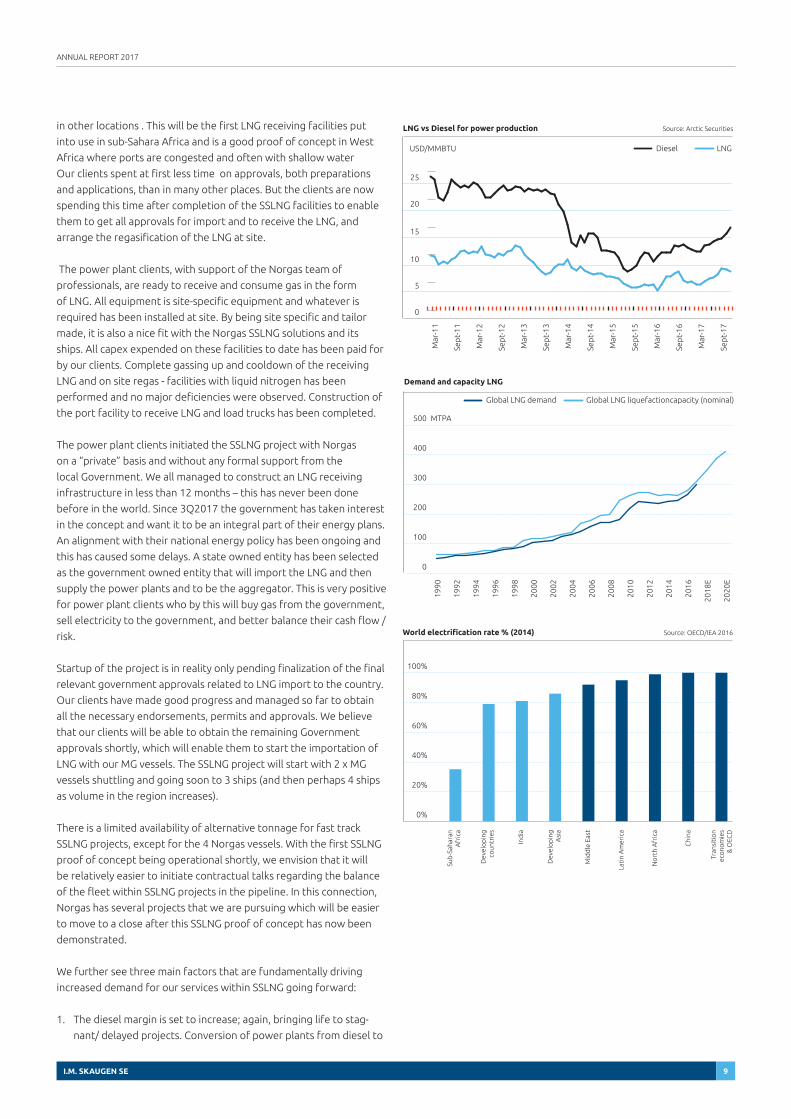

We further see three main factors that are fundamentally driving

increased demand for our services within SSLNG going forward:

1. The diesel margin is set to increase; again, bringing life to stag-

nant/ delayed projects. Conversion of power plants from diesel to

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

2018

E

2020

E

Global LNG liquefactioncapacity (nominal)Global LNG demand

0

100

200

300

400

500 MTPA

Demand and capacity LNG

0

5

10

15

20

25

Mar

-11

Sep

t-11

Mar

-12

Sep

t-12

Mar

-13

Sep

t-13

Mar

-14

Sep

t-14

Mar

-15

Sep

t-15

Mar

-16

Sep

t-16

Mar

-17

Sep

t-17

USD/MMBTU LNGDiesel

LNG vs Diesel for power production Source: Arctic Securities

Sub

-Sah

aran

Afr

ica

Dev

elo

pin

gA

sia

Tran

siti

on

eco

nom

ies

& O

ECD

Mid

dle

Eas

t

Lati

n A

mer

ica

No

rth

Afr

ica

Chi

na

Dev

elo

pin

gco

untr

ies

Ind

ia

0%

20%

40%

60%

80%

100%

World electrification rate % (2014) Source: OECD/IEA 2016

ANNUAL REPORT 2017

I.M. SKAUGEN SE 10

gas is economical and the capital expenditure can be paid off with

the reduced cost of power generation.

2. Supply of LNG is set to exceed demand, further increasing the

need for LNG exporters to develop new markets (“stranded

customers”). All key LNG producers/exporters today have a SSLNG

team actively exploring SSLNG projects.

3. Low electrification rate and power shortages in Africa / South East

Asia. Power shortages are a hindrance for economic development

and favoring “fast-track” mobile solutions such as SSLNG.

A Skaugen team of professionals

We believe that in the global market place, the winning companies

are those that can put together a team of people with the best

knowledge and highest enthusiasm anywhere in the world. IMSK has

a longstanding record of recruiting internationally and developing a

multi-cultural mix of talents to enhance a business that is truly global

in nature.

We have clear policies in place to enhance the recruitment and

development of all our people, regardless of gender, religion, ethnic

background or nationality. As a company that operates on a global

basis, we strive to identify and promote talents wherever we can find

it – aided by our non-discrimination policies. For a company of our

size, we have a truly global representation with a multicultural mix

of talents that very often is a competitive advantage as well. The key

challenge is to manage our cultural diversities to further enhance

our competitive advantage. By year-end 2017, the total number of

personnel employed by the Group was approximately 500. At end of

2017, about 30% of the total numbers of shore-based personnel were

female. The Norway based parent company itself employs an almost

equal percentage of men and women. In the senior management

team (Executive Committee) two out of seven are female. We also

comply with the Norwegian rules regarding the required percentages

of males and females on the Board of Directors.

Corporate Social Responsibility (CSR)

We are well aware of the direct and indirect impact our company’s

activities have on the outside world as well as its stakeholders. As a

company, we are determined to create long term shareholder value

and at the same time act as a responsible participant in the society.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 11

We are a marine transportation service company with a global reach

and a hundred years of history. It has always been the principle for us

to follow not only the strict industry standards, laws and regulations

set by the international maritime industry as a minimum, but the

moral and ethical boundaries as set by our culture. IMS follows the

Norwegian code of practice for corporate governance. Our Corporate

Governance Statement is published on our web site (www.skaugen.

com). We report annually on safety, health, environment and quality

in our annual reports. Internally, we report and follow up a number of

key indicators on a monthly basis. Improvement plans, and targets are

agreed with management on an annual basis.

As a company we need to disclose information for our policies on

how we integrate the respect for human rights, social and employee

related aspects, environmental matters and anti-corruption and

bribery issues in our strategies as well as in the day to day operations,

and in our relationship with our stakeholders. IMSK have had a zero

tolerance policy for being involved in any corrupt practices with our

clients or government entities affecting our business and we demand

the same for our suppliers and partners. We pay attention to the

working conditions and safety within our own operations and those

of our suppliers and we try to ensure they reflect our standards for

how to organize and operate. IMSK does not yet have all the required

policy statements embedded into one single report nor have its

CSR guidelines been embodied into one single document. We have

in place guidelines and policy statements that collectively, in our

views, are adequately and reflect our mode of operations, policies

and history, as well as culture. In our work to incorporate these into

a more comprehensive documentation, we have continued our work

to finalize the IMSK code of conduct. We provide formal training to

implement proper formal procedures into these fields. These codes

will give formal, in addition to informal, guidelines on our ethics and

principles, and should facilitate the way we work and interact both

internally and with the outside world.

SHEE&Q – Safety, Health, Environmental, Energy & Quality

IMSK recognizes that, as a business, everything we do has an impact

on people – both within and outside the company. We have strategic

objectives for our corporate responsibility taking into account social,

environmental and ethical considerations.

Our aim is to make all our employees proud to work for IMSK and

demonstrate the highest levels of integrity and responsible business

management. We always strive to achieve continuous improvements

in our operations in all areas that affect our customers, the physical

environment and society as a whole through measuring, monitoring

and reviewing our performance regularly and by committing

ourselves to become “best in class”.

We have a proactive approach to the safety, health and

environmental requirements laid down by regulations and our own

company policies.

Safety

Due to the nature of the business, the transportation of gas and

petrochemical products involves risks and we pride ourselves

in carrying out this business in the safest manner possible. Our

guiding principle is that all accidents and environmental harm can

be prevented and that zero accidents is an achievable target. That

is why continuous improvement and prevention of personnel injury,

material damage, spill or pollution is an inherent part of all areas of

our activities. In 2017 we had no fatalities and we lowered our LTIF

(Lost Time Injuries Frequency per one million worked hours) to 0.9

compared to 1.22 in 2016.

Occupational health

The working environment throughout the Group’s companies is

considered satisfactory. The Group is measuring absence due to

illness and had an overall sick leave statistic during 2017 of 0.9%,

2016 (1.1%).

Quality control

The world gas transportation activity continuous to be ISO9000:2008

certified. Several ISM/ISO 9001:2000 audits were conducted year

including our shore based activities. All the recorded observations

were analyzed and presented to senior management.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 12

Environmental

IMS recognizes the responsibility we have to treat the environment

in which we operate with the outmost respect. To this end, reducing

environmental impact is an imperative in our operations.

Our guiding principle is that all accidents resulting in environmental

harm can be prevented. That is why continuous improvement and

prevention of pollution is an inherent part of all areas of our activities.

We will continuously evaluate the environmental risk factor of our

operations. As a major participant in the transportation sector we

are actively working to minimize the environmental impact of our

activities and reduce the use of energy and natural resources. We are

aiming to reduce waste through efficient recycling and continuous

improvement of the management of our resources.

The gas carrier activity did not experience any overboard oil spill

in 2017 and our ISO 14001:2004 certificate was renewed after a

successful audit without any observations.

Training

Maintaining a knowledgeable and highly skilled workforce is vital for

any company in order to exceed the expectations of its customers.

We believe this can only be achieved through carefully managed

training. To develop meaningful on the job training is a constant

challenge. We also make extensive use of our training center in

Wuhan, China (50% owned).

Corporate governance

Good corporate governance is characterized by responsible

interaction between the owners, the Board of Directors and its

management to develop long-term value. All stakeholders should be

able to trust that a business is run properly, and the governing bodies

are sufficiently independent to perform their functions.

Confidence in IMSK and in its business activities is the most important

factor to ensure its competitiveness. The directors, officers and

employees must demonstrate that they aim to continually preserve

the confidence of the Group. To support this work, the company has

formalized a process to develop a “code of conduct” that applies for

all the employees in the group. The code of conduct will allow us

to formalize the corporate values and ethical guidelines we have in

place. The code covers areas that are important to secure acceptable,

Group-wide business ethics. They contain specific and practical rules

- and set the standards - for how anyone working for, or on behalf

of the company, should proceed to meet our business objectives in

today’s competitive environment.

The Board of Directors acknowledges the considerable responsibility

the company has in relation to safety, security, environment and society

in general, together with our responsibility towards our stakeholders.

The Corporate Governance statement, posted on our website

at www.skaugen.com, outlines key principles and guidelines for

the governance of IMS. The statement, approved by the Board of

Directors, is reviewed annually or more often if deemed necessary.

Shareholder statement

IMS aims to keep shareholders, analysts and investors updated to

the company’s operations in a timely fashion, both by releasing

information regularly and holding presentations. The financial

calendar showing publication dates for the company’s quarterly

interim reporting and Annual Report is available on our website at

www.skaugen.com.

IMS focuses on achieving and maintaining a transparent and accountable

financial reporting system. Accurate and thorough information is vital for

securing reasonable pricing for the company, based on underlying values

and earnings. The Group maintains a regular dialogue with and conducts

presentations to analysts and investors.

All documents concerning matters to be dealt with at the general

meeting are made available to shareholders at the company’s

website. This also applies to documents which shall be included in or

attached to the notice of the general meeting. A shareholder may still

request to receive documents concerning matters to be dealt with

at the meeting. Material can and will be produced in English and/or

Norwegian as most of our stakeholders (in numbers) read Norwegian.

The company has a Shareholder Policy as well as an Investor Relations

Policy, which are reviewed on a regular basis. Both these policies are

available at the company’s web site.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 13

Financial result IM Skaugen SE – parent company

The parent company, I.M. Skaugen SE, showed a negative result of

NOK 1,070 million.

Total assets for the parent company at year-end were NOK210 million

and the total equity after allocations is negative NOK 415 million.

The negative impact from the discontinued operations following the

Teekay actions as implemented in November 2017 and the following

legal actions have had significant financial impact on the Financial

Accounts of the Parent company. This has led to a situation where all

the debt is overdue and no agreement with any creditors resulting in

impairment of all our SSLNG values. Assets are measured to a greater

extent against realization values. This again has led to the need for

the Scheme of Arrangements in Singapore and on the basis of the

Court decision on June 28th we can start to implement the “Newco

plan” as described herein to achieve the approporiate refinancing

plan. If the plan is implemented as envisioned, with acceptance from

the creditors and approval by the court, the IMSK company will be

able to return to a positive book equity.

The Board of Directors received authorization to increase the share

capital with up to NOK 40,632,789. The authorization remains in force

until the next annual general meeting. The authorization has so far

not been utilized.

IM Skaugen SE Group result for 2017

IMSK net result for 2017 from continuing operations was a negative

USD 48.8 mill, of which USD 31.5 mill is related to impairments

charges on vessels and expired purchase options for vessels.This

compared with negative USD 8.9 mill for 2017 on a re-presented

basis.

Result from discontinued activities was negative USD 14.8 million

compared to a negative USD 14.2 mill for 2017 on a re-presented

basis.

Outlook for 2018 and 2019

The SSLNG projects, when operational, should enable the company

to carry out the business transformation of IMSK and its refinancing

plan by the assistance of the Singapore Scheme of Arrangement and

revert to a possible positive equity base and continue to operate to

develop its business again

The Board of Directors truly appreciates the extraordinary

challenging work made and dedication shown by everyone involved

with the Company to further improve the company’s standing in a

very challenging business environment.

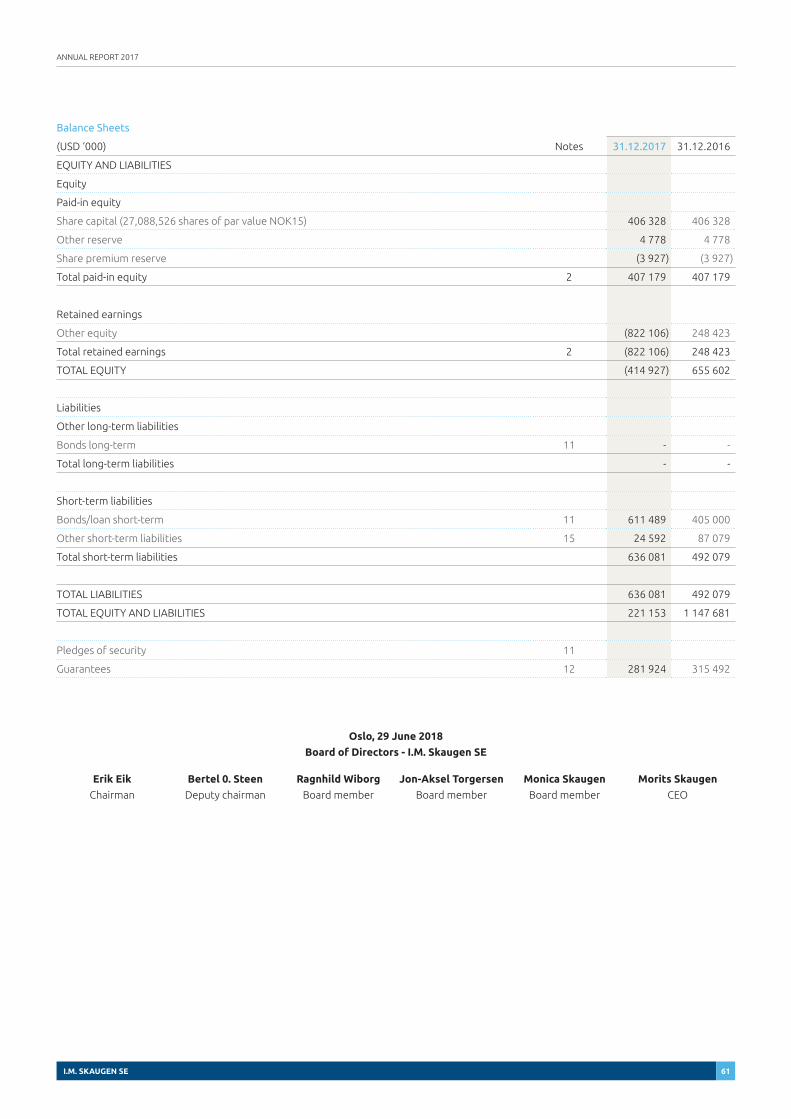

Oslo, 29 June 2018

Board of Directors – I.M. Skaugen SE

Erik Eik

Chairman

Bertel 0. Steen

Deputy chairman

Ragnhild Wiborg

Board member

Jon-Aksel Torgersen

Board member

Monica Skaugen

Board member

Morits Skaugen

CEO

ANNUAL REPORT 2017

I.M. SKAUGEN SE 14

Consolidated Financial Statements

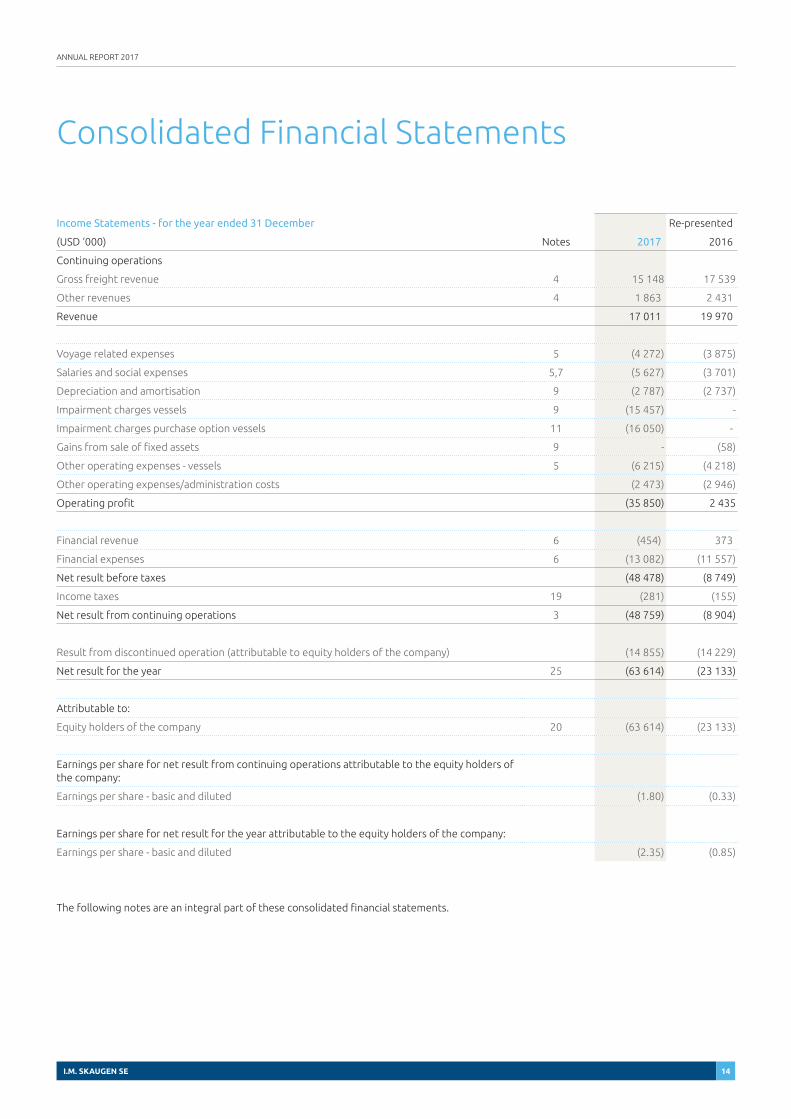

Income Statements - for the year ended 31 December Re-presented

(USD ‘000) Notes 2017 2016

Continuing operations

Gross freight revenue 4 15 148 17 539

Other revenues 4 1 863 2 431

Revenue 17 011 19 970

Voyage related expenses 5 (4 272) (3 875)

Salaries and social expenses 5,7 (5 627) (3 701)

Depreciation and amortisation 9 (2 787) (2 737)

Impairment charges vessels 9 (15 457) -

Impairment charges purchase option vessels 11 (16 050) -

Gains from sale of fixed assets 9 - (58)

Other operating expenses - vessels 5 (6 215) (4 218)

Other operating expenses/administration costs (2 473) (2 946)

Operating profit (35 850) 2 435

Financial revenue 6 (454) 373

Financial expenses 6 (13 082) (11 557)

Net result before taxes (48 478) (8 749)

Income taxes 19 (281) (155)

Net result from continuing operations 3 (48 759) (8 904)

Result from discontinued operation (attributable to equity holders of the company) (14 855) (14 229)

Net result for the year 25 (63 614) (23 133)

Attributable to:

Equity holders of the company 20 (63 614) (23 133)

Earnings per share for net result from continuing operations attributable to the equity holders of the company:

Earnings per share - basic and diluted (1.80) (0.33)

Earnings per share for net result for the year attributable to the equity holders of the company:

Earnings per share - basic and diluted (2.35) (0.85)

The following notes are an integral part of these consolidated financial statements.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 15

Statement of Comprehensive Income Re-presented

(USD ‘000) 2017 2016

Net result for the year (63 614) (23 133)

Other comprehensive income:

Items that may be subsequently reclassified to profit or loss

Currency translation differences - -

Other comprehensive income, net of tax - -

Total comprehensive income for the period (63 614) (23 133)

Attributable to:

Equity holders of the company (63 614) (23 133)

The following notes are an integral part of these consolidated financial statements.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 16

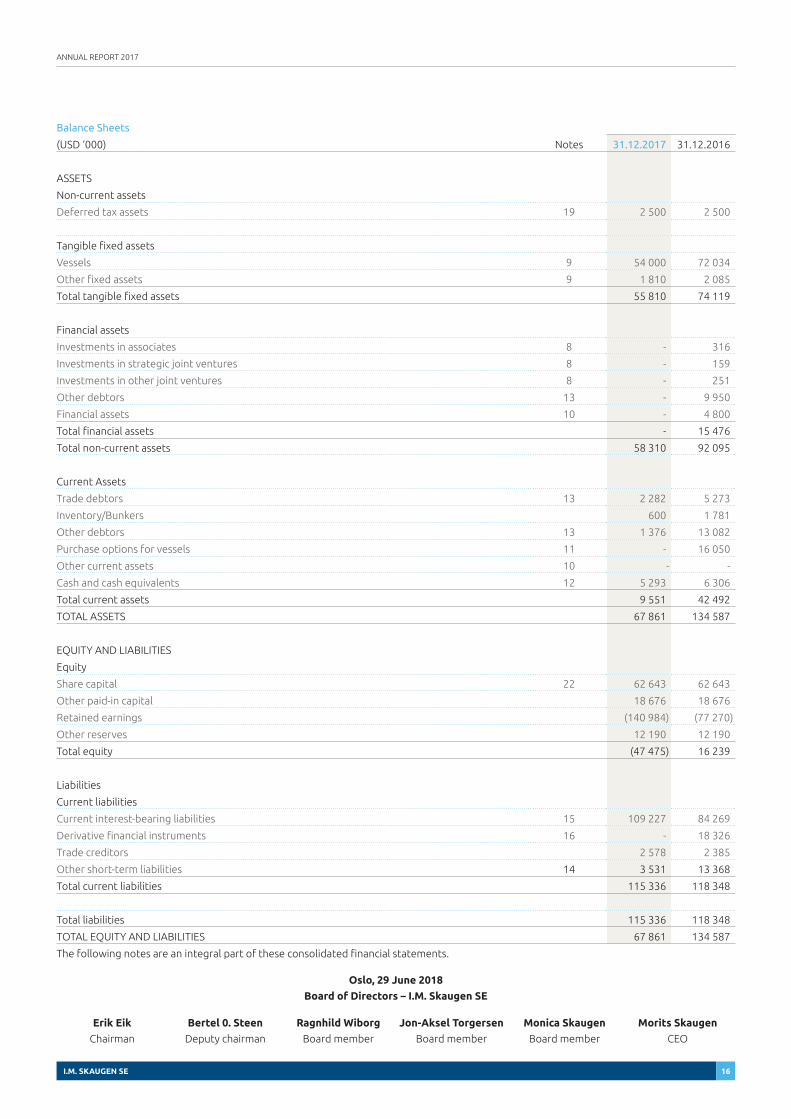

Balance Sheets

(USD ‘000) Notes 31.12.2017 31.12.2016

ASSETS

Non-current assets

Deferred tax assets 19 2 500 2 500

Tangible fixed assets

Vessels 9 54 000 72 034

Other fixed assets 9 1 810 2 085

Total tangible fixed assets 55 810 74 119

Financial assets

Investments in associates 8 - 316

Investments in strategic joint ventures 8 - 159

Investments in other joint ventures 8 - 251

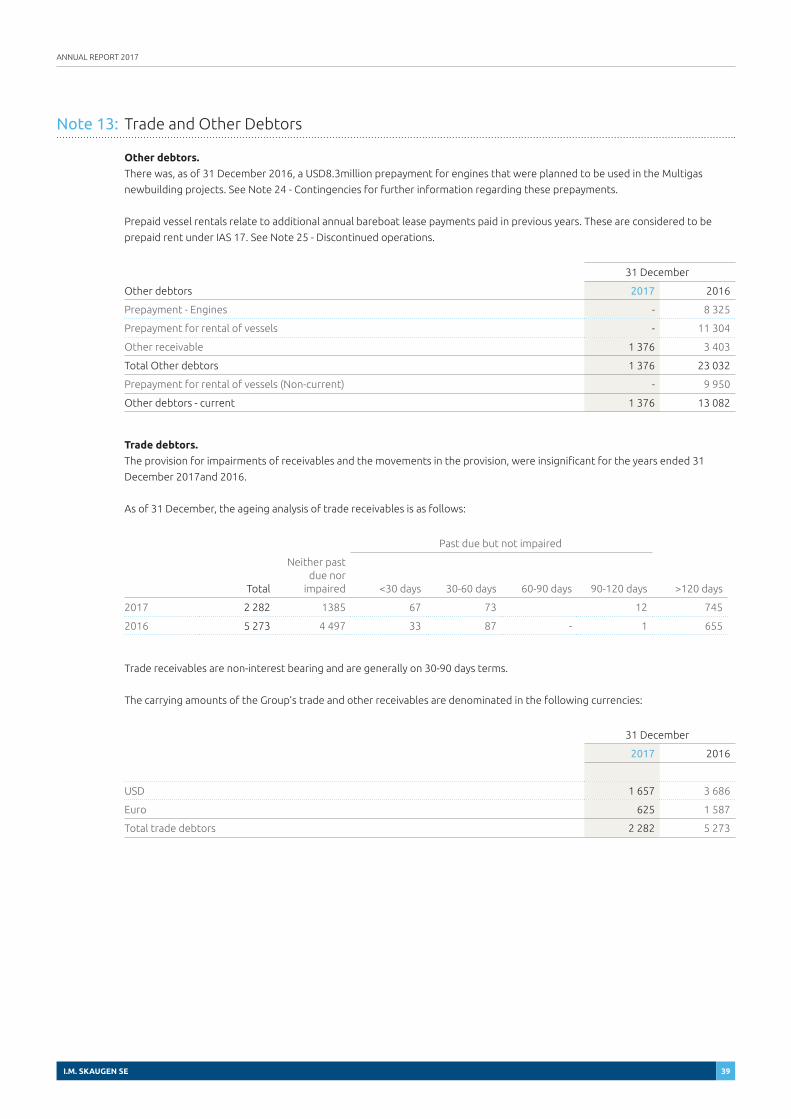

Other debtors 13 - 9 950

Financial assets 10 - 4 800

Total financial assets - 15 476

Total non-current assets 58 310 92 095

Current Assets

Trade debtors 13 2 282 5 273

Inventory/Bunkers 600 1 781

Other debtors 13 1 376 13 082

Purchase options for vessels 11 - 16 050

Other current assets 10 - -

Cash and cash equivalents 12 5 293 6 306

Total current assets 9 551 42 492

TOTAL ASSETS 67 861 134 587

EQUITY AND LIABILITIES

Equity

Share capital 22 62 643 62 643

Other paid-in capital 18 676 18 676

Retained earnings (140 984) (77 270)

Other reserves 12 190 12 190

Total equity (47 475) 16 239

Liabilities

Current liabilities

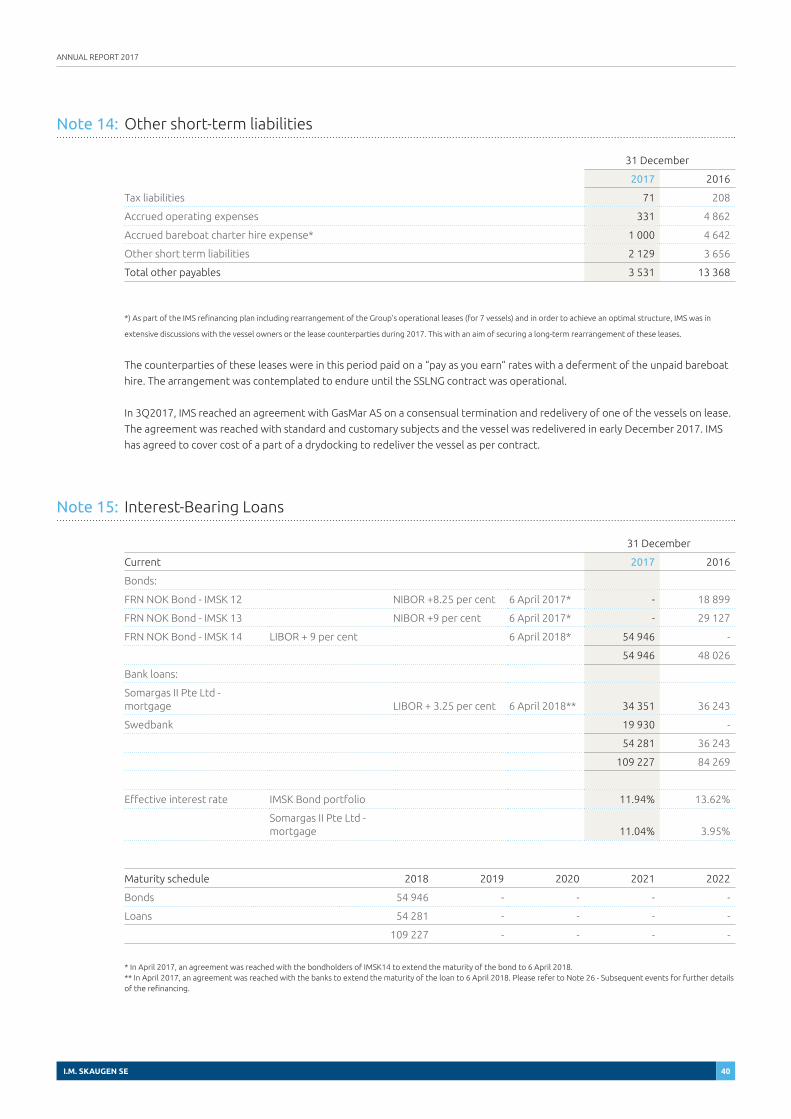

Current interest-bearing liabilities 15 109 227 84 269

Derivative financial instruments 16 - 18 326

Trade creditors 2 578 2 385

Other short-term liabilities 14 3 531 13 368

Total current liabilities 115 336 118 348

Total liabilities 115 336 118 348

TOTAL EQUITY AND LIABILITIES 67 861 134 587

The following notes are an integral part of these consolidated financial statements.

Oslo, 29 June 2018

Board of Directors – I.M. Skaugen SE

Erik Eik

Chairman

Bertel 0. Steen

Deputy chairman

Ragnhild Wiborg

Board member

Jon-Aksel Torgersen

Board member

Monica Skaugen

Board member

Morits Skaugen

CEO

ANNUAL REPORT 2017

I.M. SKAUGEN SE 17

Consolidated Statement of Cash Flows - for the year ended 31 December

(USD ‘000) Notes 2017 2016

Cash Flow from Operations:

Received payments of gross revenues 32 998 74 502

Payments of operating expenses (21 375) (61 203)

Payment of taxes 19 (281) (118)

Net Cash Flow from Operations 1) 11 342 13 180

Cash Flow from Investments:

Payments of purchase of fixed assets 9 (1 521) (78)

Receipts from sale of fixed assets 9 - 191

Proceeds from sale of shares and parts in other companies 8 - 256

Received payment of interest 6 454 272

Dividend distribution from joint ventures and associates 8 - 329

Net Cash Flow from Investments (1 067) 970

Cash Flow from Financing:

Receipts from raising new long-term debt 15 6 632 -

Repayment of other long term debt 15 - (4 351)

Discontinued operation 25 (4 837) -

Payment of interest 6 (13 082) (11 655)

Net Cash Flow from Financing (11 287) (16 006)

Net change in cash and cash equivalents (1 012) (1 855)

Cash and cash equivalents 1. January 12 6 306 8 162

Cash and cash equivalents 31. December 12 5 293 6 306

) Reconciliation: 2017Re-presented

2016

Net result before taxes (48 478) (22 820)

Gains from sale of fixed assets - 58

Ordinary depreciation and amortisation 2 767 2 957

Impairment charges vessels 15 457 -

Impairment charges purchase option vessels 16 050 -

Change in short term receivables 15 987 3 561

Change in short term liabilities (3 069) 16 792

Received payments of interest (454) (1 004)

Payment of interest 13 082 11 655

Share of results from joint ventures and associates - 1 982

Net Cash Flow from Operations 11 342 13 180

The following notes are an integral part of these consolidated financial statements.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 18

Attributable to owners of the parent

Statement of Changes in Equity Share capital

Other paid-in capital

Retained earnings

Other reserves

Total Equity(USD ‘000)

Shareholders' equity at 31.12.2015 62 643 18 676 (54 332) 12 190 39 177

Comprehensive income:

Profit or loss (22 938) (22 938)

Other comprehensive income:

Currency translation differences

Currency translation differences - Joint ventures

Other comprehensive income - - - - -

Total comprehensive income - - (22 938) - (22 938)

Shareholders' equity at 31.12.2016 62 643 18 676 (77 270) 12 190 16 239

Comprehensive income:

Net result from continuing operations (48 759) (48 759)

Net result from discontinued operations (14 855) (14 855)

Other comprehensive income:

Currency translation differences

Currency translation differences - Joint ventures

Other comprehensive income - - - - -

Total comprehensive income - - (63 614) - (63 614)

Shareholders' equity at 31.12.2017 62 643 18 676 (140 884) 12 190 (47 375)

The following notes are an integral part of these consolidated financial statements.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 19

Notes to the consolidatedFinancial Statements

Note 1: General information

I.M. Skaugen SE (“IMSK”) is a Norway based Marine Transportation Service Company, with a focus on Innovative Maritime

Solutions. IMSK is in process of completing a business transformation, shifting its focus from seaborne transportation of LPG/

Petrochemicals (mostly spot business) to regional distribution of LNG (Feedstock for power plants or energy related/long term

contract business) through its unique fast-track, low capex Small Scale LNG (SSLNG) concept.

The I.M. Skaugen SE Group (“Group”) of companies currently operates a fleet of 7 advanced gas carriers. In this fleet we have 4

innovative and unique vessels with the capacity to transport LNG in addition to petrochemical gases and LPG. We recruit, train

and employ our own team of seafarers.

The Group employs approximately 500 team members globally and with nearly 30 nationalities represented. We manage and

operate our activities and service our clients from our offices in Singapore and Oslo.

The company is incorporated and domiciled in Norway. The address of its registered office is Karenslyst Allè 8B, 0278 Oslo,

Norway.

IMSK is listed on the Oslo Stock Exchange under the ticker code, IMSK. During the refinancing process, the Board considered

it expedient for IMSK to remain listed on the Oslo Stock Exchange. IMSK will be delisted from the Oslo Stock Exchange 17

September 2018. Last day of listing will be 14 September 2018.

These consolidated financial statements have been approved by the Board of Directors on 29 June 2018 and will be presented

for approval at the Annual General Meeting on 31 July 2018.

Going concern, liquidity risk and loan covenants

These consolidated financial statements for the year ended 31 December 2017 have been prepared under the going concern

assumption. This assumption is further based upon the successful outcome of the financial challenges facing the company, as

described in this report.

The markets for arranging debt finance are challenging and debt financing is hard to attract for a company of our size and

structure for the time being. The group’s current process of refinancing in the next few months is also dependent upon the

Singapore Scheme of Arrangement being carried out and that the SSLNG project will reach its operational phase, which again will

contribute to cash surplus from operations from the SSLNG project. Failing to arrive at an acceptable refinancing plan, approved

by the Singapore Courts, through the Scheme of Arrangement will not enable us to continue operations.

Filing Scheme Moratorium in Singapore

IMSK presented a restructuring plan on 4 April 2018 which has the support from most of its stakeholders. IMSK is now seeking the

assistance of the Singapore Court to complete this plan. The restructuring plan, if implemented, is in line with IMSK’ wishes to be

in a position to be able to pay its liabilities in full with its upcoming cash flow matching an amended amortisation schedule of its

liabilities. To achieve this, IMSK will need the assistance of the Singapore Court through the scheme of arrangement process.

IMSK announced on 31 May 2018 that IMSK, together with its wholly owned subsidiaries, SMIPL Pte Ltd and IMSPL Pte Ltd (“the

IMS Scheme Companies”), filed applications to the High Court of Singapore for a moratorium to commence the reorganisation of

liabilities and businesses of the IMS Scheme Companies.

With the filing of the Scheme Moratorium, the IMSK Scheme Companies qualify for protection from the Singapore Court under

a 3 month moratorium commencing from 28 June 2018, that will apply against creditors’ claims. On this basis the Board has

decided that it can continue its operations based on a going concern assessment that the plan submitted on 4 April 2018 and

later amended and submitted to the Singapore courts has a good chance of being implemented.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 20

The principal elements in the restructuring plan are presented in note 26 Subsequent Events

Deconsolidation of SMIPL Pte Ltd:

As part of the IMSK refinancing plan including rearrangement of the Group’s operational leases (for 7 vessels) and in order to

achieve an optimal structure, IMSK was in extensive discussions with the vessel owners or the lease counterparties during 2017.

This with an aim of securing a long-term rearrangement of these leases. The counterparties of these leases were in this period

paid on a “pay as you earn” rates with a deferment of the unpaid bareboat hire. The arrangement was contemplated to endure

until the SSLNG contract was operational.

During the 2Q and 3Q, the discussions with Teekay were constructive in terms of trying to find a consensual solution, in line with

the IMS Refinancing Plan and thus also to benefit of all stakeholders, including Teekay. The aim was to pay Teekay in full as part of

the overall intention of making all creditors whole with the implementation of the SSLNG projects.

However, surprisingly, on 16 November 2017, our subsidiary SMIPL Pte Ltd., received unilateral termination notices concerning

these six Teekay vessels. IMS was further informed by media releases the same day that TGP had already established its own

competing LPG/Petchem and SSLNG pool intended to operate these vessels and other Norgas pool vessel on their own.

Due to the unilateral lease terminations by Teekay, the subsidiary, SMIPL Pte Ltd, is unable to play a role to support the IMS

Group’s overall refinancing plan. IMSK will not make any additional equity investments in SMIPL and as such SMIPL is in process

to reorganize and rightsize its business. IMSK has no legal obligation to, or guarantee for SMIPL, save for one vessel. IMS will

discontinue recognizing further losses of SMIPL on a consolidated level. SMIPL is deconsolidated per year end 2017.

Please refer to note 25 Discontinued Operations for further information.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 21

Note 2. Summary of significant accounting policies

Basis of Preparation

The consolidated financial statements of I.M. Skaugen SE (the “Parent Company”), and all its subsidiaries (the “Group”), have been

prepared in accordance with International Financial Reporting Standards (IFRS) as adopted by the EU.

The consolidated financial statements have been prepared on a historical cost basis, except for financial instruments at fair value

through profit and loss, and available-for-sale investments. The consolidated financial statements are presented in USD and all

tabular and note amounts are rounded to the nearest thousands, except when otherwise indicated.

The Income Statements are presented on a mixed basis (a blend of expenses by nature and function), as this is the most relevant

and reliable presentation for the Group. Disclosures by nature are provided in the notes to the financial statements.

Changes in Accounting Policies

The accounting policies described below are consistent with those of the previous financial year except as follows:

New and amended standards and interpretations adopted by the Group

The Group has adopted for the first time certain standards and amendments, which are effective for annual periods beginning

on or after 1 January 2017, however none of these have had any significant impact on the Group. The new note disclosure

requirement for the cash flow statement related to changes in financing liabilites is shown in Note 16.

Standards issued but not yet effective

A number of new standards and amendments to standards and interpretations are effective for annual periods beginning after 1

January 2016, and have not been applied in preparing these consolidated financial statements. None of these is expected to have

significant effect on the consolidated financial statements of the Group, except for the following set out below:

IFRS 9 – Financial instruments. This standard addresses the classification, measurement and recognition of financial assets

and financial liabilities and is effective for annual periods beginning on or after 1 January 2018. IFRS 9 retains but simplifies the

mixed measurement model and establishes three primary measurement categories for financial assets: amortized cost, fair value

through OCI and fair value through P&L. The basis of classification depends on the entity’s business model and the contractual

cash flow characteristics of the financial asset.

For financial liabilities, there are no changes to classification and measurement except for the recognition of changes in own

credit risk in OCI, for liabilities designated at fair value through P&L. This category is currently not used by the group.

IFRS 15 – Revenue from Contracts with Customers. IFRS 15 will replace IAS 18 which covers contracts for goods and services

and IAS 11 which covers construction contracts. The new standard is based on the principles that revenue is recognized when

control of a good or service transfers to a customer – so the notion of control replaces the existing notion of risks and rewards.

The Group has undertaken a comprehensive approach to assess the impact of the new standard on its business by reviewing

the current accounting policies and practices to identify any potential differences that may result from applying the new

requirements to the consolidated financial statements.

Part of the Group’s revenue is generated from time charters, where revenue is recognized on an accrual basis and is recorded

over the term of the charter as the service is provided. Management does not believe the new guidance will have any impact on

this aspect of the Group’s revenue.

For spot/voyage charters, Management expects the new guidance will result in a change in the method of recognizing reveue,

whereby the Group’s method of determining proportional performance will change from discharge-to-discharge to load-to-

discharge. This change will result in revenue being recognized later in the voyage which may cause additional volatitlty in revenue

and earnings between periods for vessels in transit at period ends. Costs directly attributable to the voyage from discharge port

to load port will be capitalized under the new approach. For contracts with a slim margin, the earning effect of this issue will not

be material.

The group will apply a modified retrospective application. At this stage, the Group does not expect it to have a material impact

on its financial statements.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 22

IFRS 16 – Leases. IFRS 16 was issued in January 2016 and is effective for annual periods beginning on or after 1 January 2019.

It will result in almost all leases being recognized on the balance sheet, as the distinction between operating and finance

leases is removed. Under the new standard, an asset (the right to use the leased item) and a financial liability to pay rentals are

recognized. The only exceptions are short-term and low-value leases. The accounting for lessors will not significantly change.

Currently the group has few operating leases that are affected. This may change going forward, but it is not possible to assess

the effect.

Critical accounting judgments, estimates and assumptions

The preparation of financial statements in conformity with IFRS requires management to make estimates, judgments and

assumptions that affect the amounts reported in the financial statements and accompanying notes. Management bases its

estimates and judgments on historical experience and on various other factors that are believed to be reasonable under the

circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that

are not readily apparent from other sources. Actual results may differ from these estimates. The key sources of estimation of

uncertainty at the balance sheet date, that have a significant risk for causing a material adjustment to the carrying amounts of

assets and liabilities within the next financial year are discussed below.

Judgments

Due to the lease terminations of seven vessels, the subsidiary, SMIPL Pte Ltd, is unable to play a role to support the IMS

Group’s overall refinancing plan. IMS will not make any additional equity investments in SMIPL and as such SMIPL is in process

to reorganize and rightsize its business. IMS has no legal obligation to, or guarantee for SMIPL, save for one vessel. IMS will

discontinue recognizing further losses of SMIPL on a consolidated level. As such, Management has determined that SMIPL

Pte Ltd meets the definition of a discontinued operation and will be accounted as such. See Note 26 – Subsequent events for

addional details.

Estimates and assumptions

Purchase options – vessels. As an integral part of the SPT transaction, IMS acquired two options to purchase two of its leased

Multigas vessels. The options have been valued using the following methods: (1)Value in use - based on the vessels operating in a

SSLNG market; (2) Newbuilding costs; and (3) Valuation reports for these vessels operating in a SSLNG market. The valuations are

based on estimates that may change. See Note 11 for further details. As of 31 December 2017 and 2016, the purchase options

had a carrying value of USD nil and USD 16.5 million. As at the end of 2017, the options are not recognized as they belong to the

discontinued operation that is no longer consolidated.

Impairment of non-financial assets. Management assesses whether there are any indicators of impairment for all non-financial

assets at each reporting date. Other non-financial assets are tested for impairment when there are indicators that the carrying

amounts may not be recoverable.

An impairment loss shall be recognized if the recoverable amount of non-financial assets is less than the carrying amount. The

recoverable amount of non-financial assets are assessed by reference to the higher of value in use, being the net present value

of future cash flows expected to be generated by the asset, and fair value less costs to dispose. Changes in circumstances and

in management’s evaluations and assumptions may give rise to impairment losses in the relevant periods. The carrying value of

tangible assets was USD 74.1 million, USD 77,2million and USD 78,6 million as of 31 December 2016, 2015 and 2014, respectively.

See Note 9 for additional details.

Deferred Tax Assets. Deferred tax assets are recognized for unused tax losses and deductible temporary differences to the

extent that it is probable that taxable profit will be available against which the losses and the temporary differences can be

utilized. Significant management judgment is required to determine the amount of deferred tax assets that can be recognized,

based upon the likely timing and level of future taxable profits together with future tax planning strategies. The carrying value of

recognized tax losses was USD2.5 million and USD 2.5 million and gross deferred tax assets were USD 18,6 million and USD 15,7

million as of 31 December 2017 and 2016, respectively. Further details are contained in Note 19. Where the final taxable profits

are different from the amounts that were initially recorded, such differences will impact current and deferred tax amounts in the

period in which such determination is made.

ANNUAL REPORT 2017

I.M. SKAUGEN SE 23

Accounting Policies

Consolidation Principles

Subsidiaries

Subsidiaries are all entities over which the Group has the power to govern the financial and operating policies generally

accompanying a shareholding of more than one-half of the voting rights. The existence and effect of potential voting rights

that are currently exercisable or convertible are considered when assessing whether the Group controls another entity. The

Group also assesses existence of control where it does not have more than 50% of the voting power but is able to govern the

financial and operating policies by virtue of de-facto control. Subsidiaries are fully consolidated from the date on which control is

transferred to the Group. They are de-consolidated from the date on which control ceases.

The Group uses the acquisition method of accounting to account for business combinations. The consideration transferred for

the acquisition of a subsidiary is the fair values of the assets transferred, the liabilities incurred and the equity interests issued by

the group. The consideration transferred includes the fair value of any asset or liability resulting from a contingent consideration

arrangement. Acquisition-related costs are expensed as incurred. Identifiable assets acquired and liabilities and contingent

liabilities assumed in a business combination are measured initially at their fair values at the acquisition date. On an acquisition-

by-acquisition basis, the group recognizes any non-controlling interest in the acquiree either at fair value or at the non-controlling

interest’s proportionate share of the acquirer’s net assets.

If the business combination is achieved in stages, the acquisition date carrying value of the acquirer’s previously held equity

interest in the acquiree is remeasured to fair value at the acquisition date; any gains or losses arising from such re-measurement

are recognized in profit and loss.

Any contingent consideration to be transferred by the Group is recognized at fair value at the acquisition date. Subsequent

changes to the fair value of the contingent consideration that is deemed to be an asset or liability is recognized in accordance

with IAS 39 either in profit or loss or as a change to other comprehensive income. Contingent consideration that is classified as

equity in not remeasured, and its subsequent settlement is accounted for within equity.

Inter-company transactions, balances and unrealized gains on transactions between Group companies are eliminated. Unrealized

losses are also eliminated. Accounting policies of subsidiaries have been changed where necessary to ensure consistency with the

policies adopted by the group.

Associates and Joint Ventures