Embed Size (px)

Citation preview

Annual accounts of the

SESAR

Joint Undertaking

Financial year 2016

Ref. Ares(2017)3166182 - 23/06/2017

Annual accounts of the SESAR Joint Undertaking 2016

2

CONTENTS

CERTIFICATION OF THE ACCOUNTS .................................................................... 3

BACKGROUND INFORMATION ON THE SJU ........................................................... 4

FINANCIAL STATEMENTS AND EXPLANATORY NOTES ............................................ 5

BALANCE SHEET ....................................................................................................... 7

STATEMENT OF FINANCIAL PERFORMANCE ................................................................... 8

CASHFLOW STATEMENT ............................................................................................. 9

STATEMENT OF CHANGES IN NET ASSETS ................................................................. 10

NOTES TO THE FINANCIAL STATEMENTS .................................................................... 11

REPORTS ON THE IMPLEMENTATION OF THE BUDGET ......................................... 26

Annual accounts of the SESAR Joint Undertaking 2016

3

CERTIFICATION OF THE ACCOUNTS

The final annual accounts of the SESAR Joint Undertaking for the year 2016 have been prepared in accordance with the Financial Rules of the JU and the accounting rules adopted by the Commission's Accounting Officer, as are to be applied by all the institutions, agencies and joint undertakings.

I acknowledge my responsibility for the preparation and presentation of the annual accounts of the Joint

Undertaking in accordance with Article 43 of the Financial Rules of the JU.

I have obtained from the Authorising Officer, who guaranteed its reliability, all the information necessary for the production of the accounts that show the JU's assets and liabilities and the budgetary implementation.

I hereby certify that based on this information, and on such checks as I deemed necessary to sign off the accounts, I have a reasonable assurance that the accounts present a true and fair view of the financial

position of the JU in all material aspects.

[signed]

Rosa ALDEA BUSQUETS

Accounting Officer

23 June 2017

Annual accounts of the SESAR Joint Undertaking 2016

4

BACKGROUND INFORMATION ON THE SJU

SESAR Joint Undertaking (SJU) is the European public-private partnership based in Brussels that is responsible for the modernisation of the European air traffic management (ATM) system by coordinating and concentrating all ATM relevant research and innovation efforts in the EU. In particular, the SJU is responsible for the implementation of the European ATM Master Plan and for carrying out specific activities aiming at

developing the new generation of air traffic management system capable of ensuring the safety and fluidity

of air transport worldwide over the next thirty years. A substantial part of the benefit of the SESAR Programme lays in the involvement of most of the European ATM stakeholders for the development of the

operational and technical solutions which best meet the objectives set out in the European ATM Master Plan. SESAR is funded by the members contributing either in cash or in-kind to the administrative and operational costs of the joint undertaking.

The SJU was established by Council Regulation (EC) No 219/20071, and last amended by the Council Regulation (EC) 721/20142 (hereinafter the 'Regulation'). The Regulation extended the mandate of SJU up to 31 December 2024 to continue research and innovation on air traffic management and in particular the coordinated approach in the context of the Single European Sky to achieve the performance targets there

defined. This decision was taken in recognition of the need to foster Research and Innovation on Air Traffic Management beyond the organisation’s original mandate until 2016, as well as in appreciation of the SESAR partnership’s ability to respond to evolving business needs and fast track technological and operational

improvements in Europe’s ATM system.

Following the Article 49 of the SJU Financial Rules3, the Administrative Board of SJU appoints the Accounting Officer who is, among other tasks, responsible for preparation of the annual accounts of the joint

undertaking. Following Article 93 of the SJU Financial Rules the annual accounts shall be prepared in accordance with the accounting rules adopted by the Commission's Accounting Officer (EU Accounting Rules, EAR) that are based on the International Public Sector Accounting Standards (IPSAS). By the decision ADB(D)18-2016 of the SJU Administrative Board, the Accounting Officer of the Commission shall also act as

the Accounting Officer of SJU as of 01 November 2017.

1 Council Regulation (EC) No 219/2007 of 27 February 2007 on the establishment of a Joint Undertaking to develop the new generation

European air traffic management system (SESAR). 2 Council Regulation (EC) No 721/2014 of 16 June 2014 amending Regulation (EC) No 219/2007 on the establishment of a Joint Undertaking to develop the new generation European air traffic management system (SESAR) as regards the extension of the Joint Undertaking until 2024. 3 Adopted by the decision SJU-AB-033-15-DOC-01 of the SJU Administrative Board.

Annual accounts of the SESAR Joint Undertaking 2016

5

SESAR JOINT UNDERTAKING

FINANCIAL YEAR 2016

FINANCIAL STATEMENTS AND

EXPLANATORY NOTES

It should be noted that due to the rounding of figures into thousands of euros, some financial data in the

tables below may appear not to add-up.

Annual accounts of the SESAR Joint Undertaking 2016

6

CONTENTS

BALANCE SHEET ............................................................................................... 7

STATEMENT OF FINANCIAL PERFORMANCE .......................................................... 8

CASHFLOW STATEMENT .................................................................................... 9

STATEMENT OF CHANGES IN NET ASSETS ......................................................... 10

NOTES TO THE FINANCIAL STATEMENTS ........................................................... 11

1. SIGNIFICANT ACCOUNTING POLICIES .................................................................. 12

2. NOTES TO THE BALANCE SHEET .......................................................................... 19

3. NOTES TO THE STATEMENT OF FINANCIAL PERFORMANCE ..................................... 23

4. OTHER SIGNIFICANT DISCLOSURES .................................................................... 24

5. FINANCIAL INSTRUMENTS DISCLOSURES ............................................................. 25

Annual accounts of the SESAR Joint Undertaking 2016

7

BALANCE SHEET

EUR '000

Note 31.12.2016 31.12.2015

NON-CURRENT ASSETS

Intangible assets 2.1 36 131

Property, plant and equipment 2.2 63 208

Pre-financing 2.3 40 840 –

40 939 338

CURRENT ASSETS

Pre-financing 2.3 35 971 61 884

Exchange receivables and non-exchange recoverables 2.4 54 250 423

Cash and cash equivalents 2.5 17 10 129

90 237 72 436

TOTAL ASSETS 131 176 72 774

CURRENT LIABILITIES

Payables and other liabilities 2.6 (224 339) (314 503)

Accrued charges and deferred income 2.7 (18 375) (11 583)

(242 714) (326 085)

TOTAL LIABILITIES (242 714) (326 085)

NET ASSETS (111 538) (253 311)

Contribution from Members 2.8 1 563 940 1 264 744

Accumulated deficit (1 518 085) (1 233 329)

Economic result of the year (157 393) (284 756)

NET ASSETS (111 538) (253 311)

Annual accounts of the SESAR Joint Undertaking 2016

8

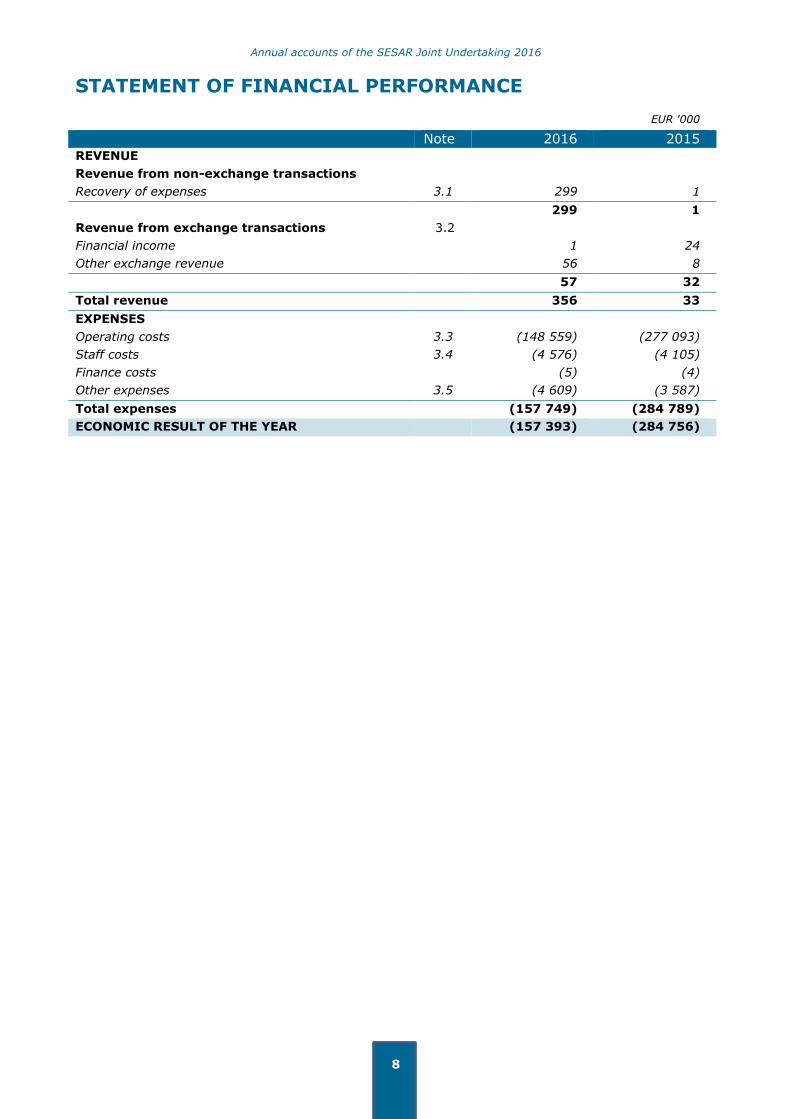

STATEMENT OF FINANCIAL PERFORMANCE

EUR '000

Note 2016 2015

REVENUE

Revenue from non-exchange transactions

Recovery of expenses 3.1 299 1

299 1

Revenue from exchange transactions 3.2

Financial income 1 24

Other exchange revenue 56 8

57 32

Total revenue 356 33

EXPENSES

Operating costs 3.3 (148 559) (277 093)

Staff costs 3.4 (4 576) (4 105)

Finance costs (5) (4)

Other expenses 3.5 (4 609) (3 587)

Total expenses (157 749) (284 789)

ECONOMIC RESULT OF THE YEAR (157 393) (284 756)

Annual accounts of the SESAR Joint Undertaking 2016

9

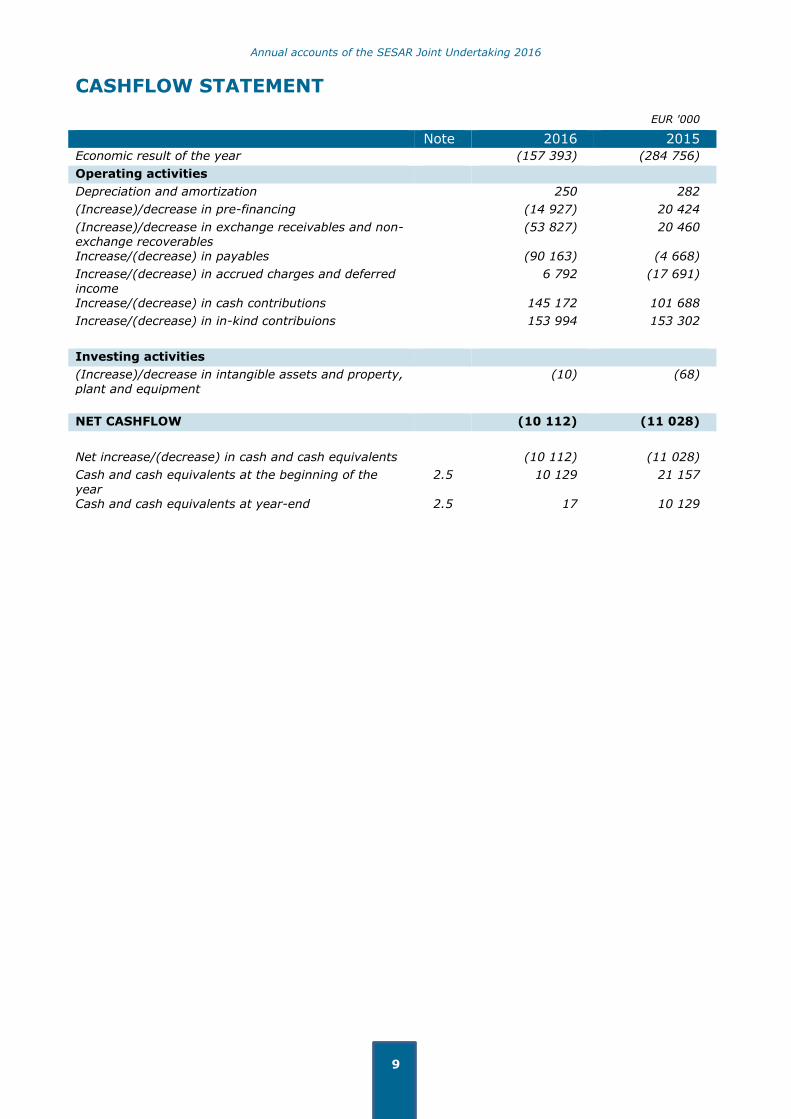

CASHFLOW STATEMENT

EUR '000

Note 2016 2015

Economic result of the year (157 393) (284 756)

Operating activities

Depreciation and amortization 250 282

(Increase)/decrease in pre-financing (14 927) 20 424

(Increase)/decrease in exchange receivables and non-exchange recoverables

(53 827) 20 460

Increase/(decrease) in payables (90 163) (4 668)

Increase/(decrease) in accrued charges and deferred

income

6 792 (17 691)

Increase/(decrease) in cash contributions 145 172 101 688

Increase/(decrease) in in-kind contribuions 153 994 153 302

Investing activities

(Increase)/decrease in intangible assets and property,

plant and equipment

(10) (68)

NET CASHFLOW (10 112) (11 028)

Net increase/(decrease) in cash and cash equivalents (10 112) (11 028)

Cash and cash equivalents at the beginning of the

year

2.5 10 129 21 157

Cash and cash equivalents at year-end 2.5 17 10 129

Annual accounts of the SESAR Joint Undertaking 2016

10

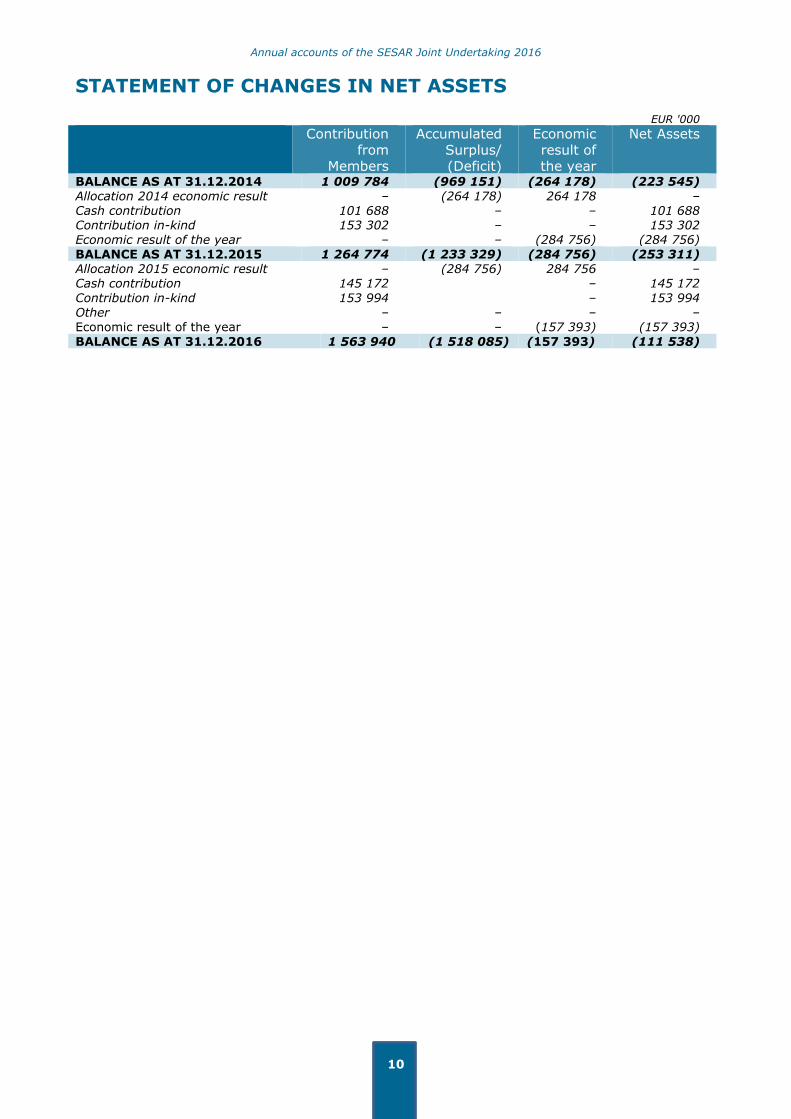

STATEMENT OF CHANGES IN NET ASSETS

EUR '000

Contribution from

Members

Accumulated Surplus/

(Deficit)

Economic result of

the year

Net Assets

BALANCE AS AT 31.12.2014 1 009 784 (969 151) (264 178) (223 545)

Allocation 2014 economic result – (264 178) 264 178 – Cash contribution 101 688 – – 101 688 Contribution in-kind 153 302 – – 153 302 Economic result of the year – – (284 756) (284 756)

BALANCE AS AT 31.12.2015 1 264 774 (1 233 329) (284 756) (253 311) Allocation 2015 economic result – (284 756) 284 756 – Cash contribution 145 172 – 145 172

Contribution in-kind 153 994 – 153 994 Other – – – – Economic result of the year – – (157 393) (157 393)

BALANCE AS AT 31.12.2016 1 563 940 (1 518 085) (157 393) (111 538)

Annual accounts of the SESAR Joint Undertaking 2016

11

NOTES TO THE FINANCIAL STATEMENTS

Annual accounts of the SESAR Joint Undertaking 2016

12

1. SIGNIFICANT ACCOUNTING POLICIES

1.1. ACCOUNTING PRINCIPLES

The objective of financial statements is to provide information about financial position, performance and

cashflows of an entity that is useful to a wide range of users.

The overall considerations (or accounting principles) to be followed when preparing the financial

statements are laid down in EU Accounting Rule 1 'Financial Statements' and are the same as those described in IPSAS 1: fair presentation, accrual basis, going concern, consistency of presentation, materiality, aggregation, offsetting and comparative information. The qualitative characteristics of financial reporting are relevance, reliability, understandability and comparability.

1.2. BASIS OF PREPARATION

1.2.1. Reporting period

Financial statements are presented annually. The accounting year begins on 1 January and ends on 31 December.

1.2.2. Currency and basis for conversion

The annual accounts are presented in thousands of euros, the euro being the EU's functional and reporting currency. Foreign currency transactions are translated into euros using the exchange rates

prevailing at the dates of the transactions. Foreign exchange gains and losses resulting from the settlement of foreign currency transactions and from the re-translation at year-end exchange rates of

monetary assets and liabilities denominated in foreign currencies are recognised in the statement of

financial performance. Different conversion methods apply to property, plant and equipment and intangible assets, which retain their value in euros at the date when they were purchased.

Year-end balances of monetary assets and liabilities denominated in foreign currencies are translated into euros on the basis of the European Central Bank (ECB) exchange rates applying on 31 December.

Euro exchange rates

Currency 31.12.2016 31.12.2015 Currency 31.12.2016 31.12.2015 BGN 1.9558 1.9558 PLN 4.4103 4.2639

CZK 27.0210 27.0230 RON 4.5390 4.5240

DKK 7.4344 7.4626 SEK 9.5525 9.1895

GBP 0.8562 0.7340 CHF 1.0739 1.0835

HRK 7.5597 7.6380 JPY 123.4000 131.0700

HUF 309.8300 315.9800 USD 1.0541 1.0887

1.2.3. Use of estimates

In accordance with IPSAS and generally accepted accounting principles, the financial statements necessarily include amounts based on estimates and assumptions by management based on the most

reliable information available. Significant estimates include, but are not limited to; accrued and deferred income and charges, provisions, financial risk on accounts receivables, contingent assets and liabilities, and degree of impairment of assets. Actual results could differ from those estimates.

Reasonable estimates are essential part of the preparation of financial statements and do not undermine

their reliability. An estimate may need revision if changes occur in the circumstances on which the estimate was based or as a result of new information or more experience. By its nature, the revision of an estimate does not relate to prior periods and is not the correction of an error. The effect of a change in

accounting estimate shall be recognised in the surplus or deficit in the periods in which it becomes known.

Annual accounts of the SESAR Joint Undertaking 2016

13

1.3. BALANCE SHEET

1.3.1. Intangible assets

Acquired computer software licences are stated at historical cost less accumulated amortisation and

impairment losses. The assets are amortised on a straight-line basis over their estimated useful lives.

The estimated useful lives of intangible assets depend on their specific economic lifetime or legal lifetime determined by an agreement. Internally developed intangible assets are capitalised when the relevant criteria of the EU accounting rules are met. The costs capitalisable include all directly attributable costs

necessary to create, produce, and prepare the asset to be capable of operating in the manner intended by management. Costs associated with research activities, non-capitalisable development costs and maintenance costs are recognised as expenses as incurred.

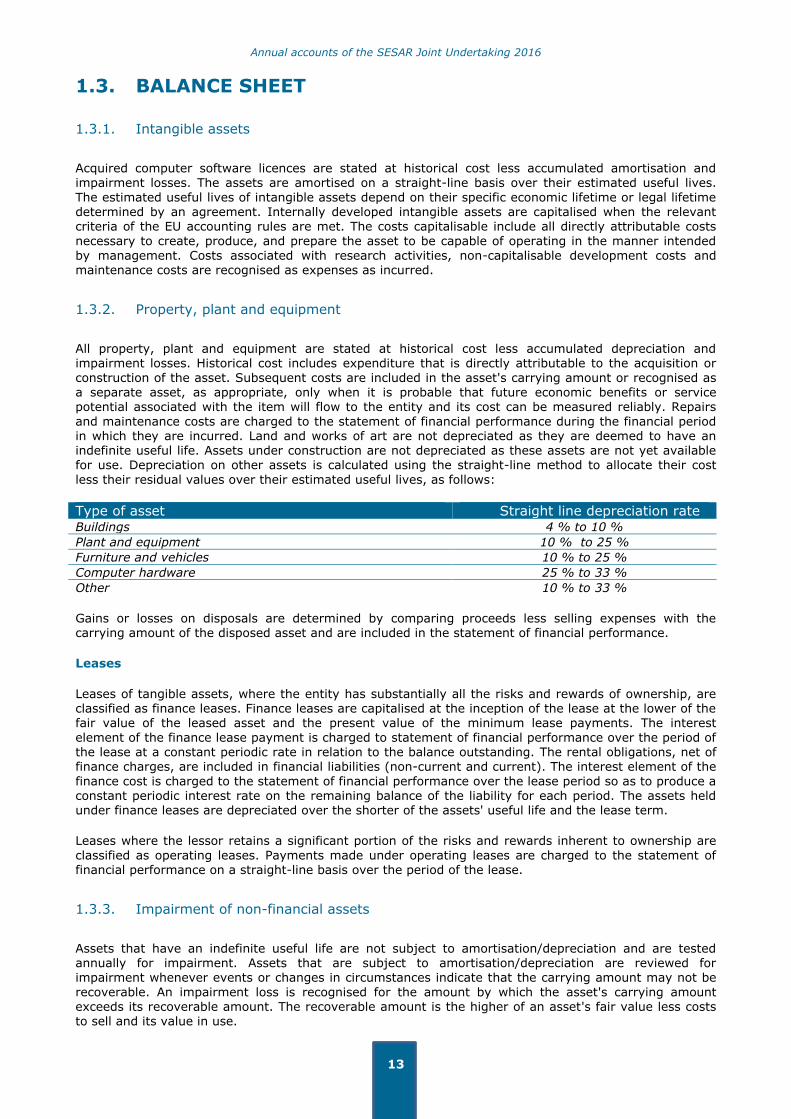

1.3.2. Property, plant and equipment

All property, plant and equipment are stated at historical cost less accumulated depreciation and impairment losses. Historical cost includes expenditure that is directly attributable to the acquisition or

construction of the asset. Subsequent costs are included in the asset's carrying amount or recognised as a separate asset, as appropriate, only when it is probable that future economic benefits or service potential associated with the item will flow to the entity and its cost can be measured reliably. Repairs

and maintenance costs are charged to the statement of financial performance during the financial period in which they are incurred. Land and works of art are not depreciated as they are deemed to have an indefinite useful life. Assets under construction are not depreciated as these assets are not yet available for use. Depreciation on other assets is calculated using the straight-line method to allocate their cost

less their residual values over their estimated useful lives, as follows:

Type of asset Straight line depreciation rate Buildings 4 % to 10 %

Plant and equipment 10 % to 25 %

Furniture and vehicles 10 % to 25 %

Computer hardware 25 % to 33 %

Other 10 % to 33 %

Gains or losses on disposals are determined by comparing proceeds less selling expenses with the carrying amount of the disposed asset and are included in the statement of financial performance.

Leases

Leases of tangible assets, where the entity has substantially all the risks and rewards of ownership, are classified as finance leases. Finance leases are capitalised at the inception of the lease at the lower of the fair value of the leased asset and the present value of the minimum lease payments. The interest

element of the finance lease payment is charged to statement of financial performance over the period of the lease at a constant periodic rate in relation to the balance outstanding. The rental obligations, net of finance charges, are included in financial liabilities (non-current and current). The interest element of the

finance cost is charged to the statement of financial performance over the lease period so as to produce a constant periodic interest rate on the remaining balance of the liability for each period. The assets held under finance leases are depreciated over the shorter of the assets' useful life and the lease term.

Leases where the lessor retains a significant portion of the risks and rewards inherent to ownership are

classified as operating leases. Payments made under operating leases are charged to the statement of financial performance on a straight-line basis over the period of the lease.

1.3.3. Impairment of non-financial assets

Assets that have an indefinite useful life are not subject to amortisation/depreciation and are tested annually for impairment. Assets that are subject to amortisation/depreciation are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be

recoverable. An impairment loss is recognised for the amount by which the asset's carrying amount exceeds its recoverable amount. The recoverable amount is the higher of an asset's fair value less costs to sell and its value in use.

Annual accounts of the SESAR Joint Undertaking 2016

14

Intangible assets and property, plant and equipment residual values and useful lives are reviewed, and adjusted if appropriate, at least once per year. An asset's carrying amount is written down immediately

to its recoverable amount if the asset's carrying amount is greater than its estimated recoverable amount. If the reasons for impairments recognised in previous years no longer apply, the impairment losses are reversed accordingly.

1.3.4. Financial assets

The financial assets are classified in the following categories: financial assets at fair value through profit or loss; loans and receivables; held-to-maturity investments; and available for sale financial assets. The

classification of the financial instruments is determined at initial recognition and re-evaluated at each balance sheet date.

(1) Financial assets at fair value through profit or loss

A financial asset is classified in this category if acquired principally for the purpose of selling in the short term or if so designated by the entity. Derivatives are also categorised in this category. Assets in this category are classified as current assets if they are expected to be realised within 12 months of the balance sheet date. During this financial year, the entity did not hold any investments in this category.

(2) Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market. They arise when the entity provides money, goods or services directly to

a debtor with no intention of trading the receivable. They are included in non-current assets, except for maturities within 12 months of the balance sheet date. Loans and receivables include term deposits with the original maturity above three months.

(3) Held-to-maturity investments

Held-to-maturity investments are non-derivative financial assets with fixed or determinable payments

and fixed maturities that the entity has the positive intention and ability to hold to maturity. During this financial year, the entity did not hold any investments in this category.

(4) Available for sale financial assets

Available for sale financial assets are non-derivatives that are either designated in this category or not classified in any of the other categories. They are classified as either current or non-current assets,

depending on the period of time the entity expects to hold them, which is usually the maturity date.

Initial recognition and measurement

Purchases and sales of financial assets at fair value through profit and loss, held-to-maturity and

available for sale (except cash and cash equivalents) are recognised on trade date - the date on which the entity commits to purchase or sell the asset. Loans and term deposits are recognised at settlement date. Financial instruments are initially recognised at fair value. For all financial assets not carried at fair value through profit and loss transaction costs are added to the fair value at initial recognition.

Financial instruments are derecognised when the rights to receive cashflows from the investments have expired or the entity has transferred substantially all risks and rewards of ownership to another party.

Subsequent measurement

Financial assets at fair value through profit and loss are subsequently carried at fair value with gains and losses arising changes in the fair value being included in the statement of financial performance in the period in which they arise.

Loans and receivables and held-to maturity investments are carried at amortised cost using the effective interest method.

Available for sale financial assets are subsequently carried at fair value. Gains and losses arising from changes in the fair value being recognised in the fairs value reserve. Interest on available for sale

Annual accounts of the SESAR Joint Undertaking 2016

15

financial assets calculated using the effective interest method is recognised in the statement of financial performance.

The entity assesses at each balance sheet date whether there is objective evidence that a financial asset is impaired and whether an impairment loss should be recorded in the statement of financial performance.

1.3.5. Pre-financing amounts

Pre-financing is a payment intended to provide the beneficiary with a cash advance, i.e. a float. It may be split into a number of payments over a period defined in the particular contract, decision, agreement or

basic legal act. The float or advance is either used for the purpose for which it was provided during the period defined in the agreement or it is repaid. If the beneficiary does not incur eligible expenditure, he has the obligation to return the pre-financing advance to the entity. The amount of the pre-financing may

be reduced (wholly or partially) by the acceptance of eligible costs (which are recognised as expenses).

Pre-financing is, on subsequent balance sheet dates, measured at the amount initially recognised on the balance sheet less eligible expenses (including estimated amounts where necessary) incurred during the period.

1.3.6. Receivables and recoverables

As the EU accounting rules require a separate presentation of exchange and non-exchange transactions,

for the purpose of drawing up the accounts, receivables are defined as stemming from non-exchange transactions and recoverables are defined as stemming from exchange transactions (when the entity receives value from another entity without directly giving approximately equal value in exchange).

Receivables from exchange transactions meet the definition of financial instruments and are thus classified as loans and receivables and measured accordingly (see 1.3.4 above).

Recoverables from non-exchange transactions are carried at original amount (adjusted for interests and penalties) less write-down for impairment. A write-down for impairment is established when there is

objective evidence that the entity will not be able to collect all amounts due according to the original terms of the recoverables. The amount of the write-down is the difference between the asset's carrying amount and the recoverable amount. The amount of the write-down is recognised in the statement of

financial performance.

1.3.7. Cash and cash equivalents

Cash and cash equivalents are financial instruments and include cash at hand, deposits held at call or at

short notice with banks, and other short-term highly liquid investments with original maturities of three months or less.

1.3.8. Provisions

Provisions are recognised when the entity has a present legal or constructive obligation towards third parties as a result of past events, it is more likely than not that an outflow of resources will be required

to settle the obligation, and the amount can be reliably estimated. Provisions are not recognised for future operating losses. The amount of the provision is the best estimate of the expenditure expected to be required to settle the present obligation at the reporting date. Where the provision involves a large number of items, the obligation is estimated by weighting all possible outcomes by their associated

probabilities ('expected value' method).

1.3.9. Payables

Included under accounts payable are both amounts related to exchange transactions such as the purchase of goods and services and non-exchange transactions related e.g. to cost claims from beneficiaries, grants or other EU funding.

Annual accounts of the SESAR Joint Undertaking 2016

16

Where grants or other funding is provided to the beneficiaries, the cost claims are recorded as payables for the requested amount when the cost claim is received. Upon verification and acceptance of the

eligible costs, the payables are valued at the accepted and eligible amount.

Payables arising from the purchase of goods and services are recognised at invoice reception for the original amount and corresponding expenses are entered in the accounts when the supplies or services are delivered and accepted by the entity.

1.3.10. Accrued and deferred income and charges

Transactions and events are recognised in the financial statements in the period to which they relate. At

year-end, if an invoice is not yet issued but the service has been rendered, the supplies have been delivered by the entity or a contractual agreement exists (e.g. by reference to a contract), an accrued income will be recognised in the financial statements. In addition, at year-end, if an invoice is issued but

the services have not yet been rendered or the goods supplied have not yet been delivered, the revenue will be deferred and recognised in the subsequent accounting period.

Expenses are also accounted for in the period to which they relate. At the end of the accounting period, accrued expenses are recognised based on an estimated amount of the transfer obligation of the period.

The calculation of accrued expenses is done in accordance with detailed operational and practical guidelines issued by the Accounting Officer which aim at ensuring that the financial statements provide a faithful representation of the economic and other phenomena they purport to represent. By analogy, if a

payment has been made in advance for services or goods that have not yet been received, the expense will be deferred and recognised in the subsequent accounting period.

1.4. STATEMENT OF FINANCIAL PERFORMANCE

1.4.1. Revenue

Revenue comprises gross inflows of economic benefits or service potential received and receivable by the

entity, which represents an increase in net assets, other than increases relating to contributions from owners.

Depending on the nature of the underlying transactions in the statement of financial performance it is

distinguished between:

(i) Revenue from non-exchange transactions

Revenue from non-exchange transactions are taxes and transfers because the transferor provides

resources to the recipient entity without the recipient entity providing approximately equal value directly in exchange.

Transfers are inflows of future economic benefits or service potential from non-exchange transactions, other than taxes. The entity shall recognise an asset in respect of transfers when the entity controls the resources as a result of a past event (the transfer) and expects to receive future economic benefits or

service potential from those resources, and when the fair value can be reliably measured. An inflow of resources from a non-exchange transaction recognised as an asset (i.e. cash) is also recognised as revenue, except to the extent that the entity has a present obligation in respect of that transfer (condition), which needs to be satisfied before the revenue can be recognised. Until the condition is met

the revenue is deferred and recognised as a liability (pre-financing received).

(ii) Revenue from exchange transactions

Revenue from the sale of goods and services is recognised when the significant risk and rewards of

ownership of the goods are transferred to the purchaser. Revenue associated with a transaction involving the provision of services is recognised by reference to the stage of completion of the transaction at the

reporting date.

Annual accounts of the SESAR Joint Undertaking 2016

17

1.4.2. Expenses

Expenses are decreases in economic benefits or service potential during the reporting period in the form of outflows or consumption of assets or incurrence of liabilities that result in decreases in net assets/equity. They include both the expenses from exchange transactions and expenses from non-exchange transactions.

Expenses from exchange transactions arising from the purchase of goods and services are recognised when the supplies are delivered and accepted by the entity. They are valued at original invoice amount. Furthermore, at the balance sheet date expenses related to the service delivered during the period for

which an invoice has not yet been received or accepted are recognised in the statement of financial performance.

Expenses from non-exchange transactions account for the majority of the entity's operating expenses.

They relate to transfers to beneficiaries and can be of three types: entitlements, transfers under agreement and discretionary grants, contributions and donations. Transfers are recognised as expenses in the period during which the events giving rise to the transfer occurred, as long as the nature of the transfer is allowed by regulation or an agreement has been signed authorising the transfer; any eligibility

criteria have been met by the beneficiary; and a reasonable estimate of the amount can be made.

When a request for payment or cost claim is received and meets the recognition criteria, it is recognised as an expense for the eligible amount. At year-end, incurred eligible expenses due to the beneficiaries

but not yet reported are estimated and recorded as accrued expense.

1.5. CONTINGENT ASSETS AND LIABILITIES

1.5.1. Contingent assets

A contingent asset is a possible asset that arises from past events and of which the existence will be

confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly

within the control of the entity. A contingent asset is disclosed when an inflow of economic benefits or service potential is probable.

1.5.2. Contingent liabilities

A contingent liability is a possible obligation that arises from past events and of which the existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity; or a present obligation that arises from past events but is not recognised

because: it is not probable that an outflow of resources embodying economic benefits or service potential will be required to settle the obligation or, in the rare circumstances where the amount of the obligation cannot be measured with sufficient reliability.

1.6. CONTRIBUTIONS FROM MEMBERS

The contributions from the Members of the joint undertakings (JU) form the funding of the JU and are

treated as contributions from owners. An owner in this context does not mean an owner in the sense of owning shares (no shares are issued) of the JU but rather in the sense of political interest and governance of the JU by exercising the voting rights linked to these contributions.

1.6.1. Financial contributions

Financial contributions are contributions of Members made in cash in order to provide funding of the operational or administrative needs of the JU. The financial contributions are recognised in the net assets

in the period in which the right to receive the payment was established.

Annual accounts of the SESAR Joint Undertaking 2016

18

1.6.2. In-kind contributions

Members other than the EU (i.e. 'Private Members') can also contribute resources other than cash, e.g. laboratory equipment, specialised staff, etc. These in-kind contributions consist of the costs incurred by Private Members in implementing indirect actions.

The Regulation distinguishes between two types of in-kind contributions: (1) In-kind contributions to

operational activities (IKOP) and (2) in-kind contributions to additional activities (IKAA).

The IKOP represents in-kind contributions made to the JU linked to its work plan and co-financed by the EU. The IKOP are recognised in the net assets of the JU in the period when the conditions for Members'

contributions stipulated by the Regulation were met.

The expenses related to the IKOP incurred in the financial year are recognised in the statement of financial performance. At year-end, incurred IKOP not yet reported are estimated and recorded as other

liabilities ('Contributions of Members to be validated').

The IKAA relate to contributions linked to implementing additional activities outside the work plan of the JU that contribute to the objectives of the JU. Because the outflow of resources related to those activities is outside of control of the JU, the contributions are not recognised in the financial statements of the JU.

Annual accounts of the SESAR Joint Undertaking 2016

19

2. NOTES TO THE BALANCE SHEET

ASSETS

2.1. INTANGIBLE ASSETS

EUR '000

Gross carrying amount at 31.12.2015 2 171 Gross carrying amount at 31.12.2016 2 171

Accumulated amortisation at 31.12.2015 (2 040) Amortisation charge of the year (94) Accumulated amortisation at 31.12.2016 (2 134)

NET CARRYING AMOUNT at 31.12.2016 36 NET CARRYING AMOUNT at 31.12.2015 131

The heading comprises software with depreciation rate 25 % and includes also software and developments made under the contract with Eurocontrol.

2.2. PROPERTY, PLANT AND EQUIPMENT

EUR '000

Buildings Furniture and

vehicles

Computer hardware

Other Total

Gross carrying amount at

31.12.2015

592 170 12 60 834

Additions 8 2 – – 10 Disposals – – (2) (2) (4)

Gross carrying amount at 31.12.2016

600 172 10 59 841

Accumulated depreciation at

31.12.2015

(472) (98) (9) (48) (627)

Depreciation charge of the year (128) (19) (1) (7) (155) Disposals – – 2 2 4 Accumulated depreciation at

31.12.2016

(600) (117) (9) (53) (778)

NET CARRYING AMOUNT at

31.12.2016

– 56 2 5 63

NET CARRYING AMOUNT at 31.12.2015

119 73 3 12 208

Included under the heading 'Buildings' are materials and works related to the partitioning and set up of the SJU office space.

Included under the heading 'Other' is technical equipment that was presented in 2015 annual accounts under the heading 'Computer Hardware & Technical Equipment'.

2.3. PRE-FINANCING

EUR '000

31.12.2016 31.12.2015 Non-current pre-financing 40 840 –

Current pre-financing 35 971 61 884 Total 76 810 61 884

Provisional annual accounts of the SESAR Joint Undertaking 2016

20

The outstanding pre-financing was reduced by kEUR 26 602 of estimated (cut-off) expenses for on-going or ended projects without validated cost claims on 31.12.2016. The remaining portion of the cut-off

expenses is recorded in 'contributions to be paid to Members' (see note 2.6) and in accrued charges (see note 2.7).

For all pre-financing amounts open at 31.12.2016 a case-by-case assessment has been performed and all the pre-financing that was considered unlikely to be cleared in the course of 2016 was classified as

non-current pre-financing.

The significant increase of the non-current pre-financing, is due to the fact that 2016 was the first year when pre-financing was given to SESAR 2020 projects. In 2015 all the pre-financing related to SESAR1

projects was presented under current pre-financing, because the SESAR1 projecs were foreseen to finish their activities by 31/12/2016 at the latest.

2.4. EXCHANGE RECEIVABLES & NON-EXCHANGE

RECOVERABLES

At 31. 12. 2016 SJU did not have any balances related to non-current receivables and recoverables. All

the amounts are current and can be split as follows:

2.4.1. Receivables from exchange transactions

EUR '000

31.12.2016 31.12.2015 Customers 40 – Deferred charges relating to exchange transactions 9 354 Central treasury liaison accounts 54 146 –

Others 53 65 Total 54 247 419

The significant increase in current receivables from exchange transactions is the effect of the use of the

central treasury of the Commission since 01.11.2016. A corresponding decrease is noted in cash and cash equivalents. See note 2.5 for further details.

2.5. CASH AND CASH EQUIVALENTS

EUR '000

31.12.2016 31.12.2015 Current accounts 17 10 129 Total 17 10 129

Following the appointment of the Accounting Officer of the Commission as the Accounting Officer of SJU, the treasury of SJU was integrated into the Commission's treasury system. All payments and receipts are processed via the Commission's treasury system and registered on intercompany accounts which are presented under the heading exchange receivables (see note 2.4).

The amounts remaining under this heading relate to bank charges for the closure of the old SJU bank accounts that will be deducted in 2017 (kEUR 6) and a fixed amount of bank guarantees and safe charges (kEUR 11).

EUR '000

Note 31.12.2016 31.12.2015

Current

Recoverables from non-exchange transactions 3 4

Receivables from exchange transactions 2.4.1 54 247 419

Total 54 250 423

Annual accounts of the SESAR Joint Undertaking 2016

21

LIABILITIES

2.6. PAYABLES AND OTHER LIABILITIES

EUR '000

31.12.2016 31.12.2015 Contribution in-kind from Members to be validated 118 382 240 039

Contribution to be paid to Members 49 782 63 754 Current payables 55 675 10 705 Sundry payables 501 4 Total 224 339 314 503

Included under the sub-heading 'contribution in-kind to be validated' are the in-kind contributions from Members related to on-going or ended projects without a validated cost statement at 31.12.2016. The sub-heading 'contributions to be paid to Members' comprises the estimated EU contribution to those

projects. The amounts of contributions were estimated on a case-by-case basis using the best available information on the projects at 31.12.2016. The increase of the amounts compared to 2015 is due to new projects that started under the SESAR2020 program in 2016.

The main components of current payables are liabilities to suppliers (kEUR 50 166) and to Member States (kEUR 4 703). The increase in current payables relates to the closure of SESAR1 program. In line with the rules applicable to SESAR1 those amounts will be paid when the final financial statements are received from the Members.

2.7. ACCRUED CHARGES AND DEFERRED INCOME

The SJU does not have any deferred income. All the amounts included under this heading related to

accrued charges and are as follows:

EUR '000

31.12.2016 31.12.2015 Accrued charges 18 375 11 583

Accrued charges are the amounts estimated by the Authorising Officer of costs incurred for services and

goods delivered in year 2016 but not yet invoiced or processed by the end of the year. Included under this heading are estimated amounts related to demonstration activities (kEUR 10 457), exploratory research (kEUR 4 802), amounts related to staff (kEUR 377) and other administrative expense

(kEUR 2 084). The portion of the estimated accrued charges which relates to pre-financing paid has been recorded as a reduction of the pre-financing amounts (see note 2.3). It should be noted that the estimated contributions of Members are recorded under other liabilities (see note 2.6).

Annual accounts of the SESAR Joint Undertaking 2016

22

NET ASSETS

2.8. CONTRIBUTIONS FROM MEMBERS

The total contribution from Members amounted to kEUR 1 563 940 (2015: kEUR 1 264 774) at 31.12.2016. The details of the cash contributions and in-kind contributions by the type the funding programme and by Member are as follows:

2.8.1. SESAR1: Research and Innovation funding programme (FP7) and Framework Programme on Trans-European networks (TEN-T) for 2007-2013

EUR '000

EU Eurocontrol Industry Members Total

Cash In kind Cash In kind Cash In kind Cash In kind

A. Running Costs 23 990 – 20 407 – 25 478 – 69 875 – Previous years 17 050 – 19 617 – 25 478 – 62 145 –

Current year 6 940 – 790 – – – 7 730 - B. Operational costs (R&D Projects) 573 146 – 104 861 302 441 – 456 828 678 007 759 288 Previous years 505 086 – 92 249 236 521 – 368 773 597 335 605 294

Current year 68 060 – 12 613 65 920 – 88 513 80 673 154 433 Adjustments – – – – – (439) – (439) BALANCE AS AT 31.12.2016 597 136 – 125 268 302 441 25 478 456 847 747 883 759 288 BALANCE AS AT 31.12.2015 522 136 – 111 865 236 521 25 478 368 773 659 480 605 294

Contribution in cash/kind in % 79.84 % 0.00 % 16.75 % 39.83 % 3.41 % 60.17 % 100 % 100 % Total contribution in % 39.62 % 28.38 % 32.00 % 100 %

Voting rights % 32.33 % 30.86 % 26.91 % 90 %*

* The rules of distribution of voting rights are defined in Article 4 of the Regulation. Based on this article the representative of civil users of airspace, designated by their representative organisation at

European level has at least 10 % of the voting rights in the Administrative Board of SJU. This organisation is not a member of SJU and does not provide any financial or in-kind contributions to the joint undertaking.

2.8.2. SESAR2020: Research and Innovation funding programme for 2014-2020 (Horizon 2020)

At 31.12.2016 the contributions to SESAR2020 amounted to kEUR 56 769. The entire amount was contributed by the European Union to the operational activities of the joint undertaking. The distribution of voting rights remains the same as under SESAR1.

Annual accounts of the SESAR Joint Undertaking 2016

23

3. NOTES TO THE STATEMENT OF FINANCIAL PERFORMANCE

NON-EXCHANGE REVENUE

3.1. RECOVERY OF EXPENSES

EUR '000

2016 2015 Recovery of expenses 299 1

This heading is composed of the operating expenses recovered from beneficiaries during the year.

3.2. EXCHANGE REVENUE

EUR '000

2016 2015 Interest revenue 1 24 Property, plant and equipment related revenue – 6 Administrative revenue 55 1

Foreign exchange gains 1 2 Total 57 32

EXPENSES

3.3. OPERATING COSTS

Included under this heading are operating expenses incurred in relation to all programme activities that were performed in 2016 (estimated works achieved) and expenses related to contracts for industrial

support, legal, financial & management support, experts, launch of specific technical activities and the Programme Support Office (PSO) of Eurocontrol.

The part of the operating costs related to on-going or ended projects without any validated cost claims

(or equivalent) available at 31 December, was estimated using the best information available at the time of the preparation of the annual accounts. The estimation is based on the case-by-case assessment of completion which ensures that only costs that reflect the services or work performed by 31 December are included in the operating costs of the year. Depending on the availability of information at the time of the

preparation of the annual acounts, the estimates are based on reports of services or work performed or costs incurred to date as a proportion of the estimated total costs of the projects ('pro-rata temporis').

The break-down of the operating costs between operating costs incurred on the basis of validated cost

claims (or equivalent) and estimated operating costs is given in the table below. It should be noted that in line with the accounting rules the portion of the estimated cost also includes a revision of accounting estimates made in the previous periods.

EUR '000

Note 2016 2015 Operating costs incurred (validated cost claims)

234 979 125 148

Operating costs estimated 2.6, 2.7 (86 420) 151 945 Total 148 559 277 093

Annual accounts of the SESAR Joint Undertaking 2016

24

The decrease of the operating costs compared to last year is the combined effect of phasing out of SESAR1 and a start up phase of SESAR2020.

3.4. STAFF COSTS

These expenses include all staff related costs such as salaries, social security, insurances, secondments and other staff costs.

3.5. OTHER EXPENSES

EUR '000

2016 2015 External IT services 1 838 1 129

External non IT services 930 646 Property, plant and equipment related expenses 923 1 025 Communications & publications 420 274

Missions 253 265 Office Supplies & maintenance 173 181 Expert expenses 33 16

Other 21 19 Training Costs 18 32 Total 4 609 3 587

Operating lease expenses related to the SESAR JU offices of kEUR 463 are included under the

sub-heading 'property, plant and equipment related expenses'.

Amounts committed to be paid during the remaining term of this lease contract until February, 2025 include rent and related charges and are as follows:

EUR '000

Future amounts to be paid

< 1 year 1- 5 years > 5 years Total

Buildings 466 2 449 1 569 4 484

4. OTHER SIGNIFICANT DISCLOSURES

4.1. OUTSTANDING COMMITMENTS NOT YET EXPENSED

EUR '000

31.12.2016 31.12.2015 Outstanding commitments not yet expensed 156 693 162 273

The outstanding commitments not yet expensed comprises the budgetary RAL ('Reste à Liquider') less related amounts that have been included as expenses in the 2016 statement of financial performance.

The budgetary RAL is an amount representing the open commitments for which payments and/or de-commitments have not yet been made. This is the normal consequence of the existence of multi-annual programmes.

4.2. RELATED PARTIES

The related parties of the SJU are the participants of the JU and key management personnel of these entities. Transactions between these entities take place as part of the normal operations of SJU and as

this is the case, no specific disclosure requirements are necessary for these transactions in accordance with the EU accounting rules.

Provisional annual accounts of the SESAR Joint Undertaking 2016

25

4.3. KEY MANAGEMENT ENTITLMENTS

The highest ranked civil servant of SESAR JU is the Executive Director, who executes the role of the Authorising Officer.

31.12.2016 31.12.2015 Executive Director AD 14 AD 14

The Executive Director is remunerated in accordance with the Staff Regulation of the European Union that is published on the Europa website and which is the official document describing the rights and the

obligation of all officials of the EU. The Executive Director has not received any preferential loans from SESAR JU.

5. FINANCIAL INSTRUMENTS DISCLOSURES

5.1. CURRENCY RISKS

Exposure of the SJU to currency risk at year end

At 31.12.2016 the ending balances of financial assets and financial liabilities did not include any material

amounts quoted in different currencies than euro.

5.2. CREDIT RISK

Financial assets that are neither past due nor impaired

At 31.12.2016 the financial assets are entirely composed of receivables and recoverables that are neither past due nor impaired.

Financial assets by risk category

At 31.12.2016 the financial assets are composed of receivables and recoverables against entities without external credit rating who never defaulted in the past. They also include immaterial amounts on current accunts in ING Bank Belgium (kEUR 16) and City Bank Belgium (kEUR 1).

5.3. LIQUIDITY RISK

Maturity analysis of financial liabilities by remaining contractual maturity

The financial liabilities entirely compose of accounts payable. All the accounts payable have a remaining contractual maturity of less than 1 year.

Annual accounts of the SESAR Joint Undertaking 2016

26

REPORTS ON THE IMPLEMENTATION OF

THE BUDGET

It should be noted that due to the rounding of figures into thousands of euros, some financial data in the tables below may appear not to add-up.

Annual accounts of the SESAR Joint Undertaking 2016

27

CONTENTS

1. BUDGETARY PRINCIPLES, STRUCTURE AND IMPLEMENTATION ......................28

2. RESULT OF THE IMPLEMENTATION OF THE BUDGET ..................................... 31

3. RECONCILIATION OF ECONOMIC RESULT WITH BUDGET RESULT ................... 32

4. IMPLEMENTATION OF BUDGET REVENUE .................................................... 33

5. IMPLEMENTATION OF BUDGET EXPENDITURE .............................................. 36

6. COMMITMENTS OUTSTANDING ................................................................. 48

7. GLOSSARY ............................................................................................. 51

Annual accounts of the SESAR Joint Undertaking 2016

28

1. BUDGETARY PRINCIPLES, STRUCTURE AND IMPLEMENTATION

1.1. Budgetary principles

The budget of the SJU has been established in compliance with the principles of unity, budget accuracy, annuality, equilibrium, unit of account, universality, specification, sound financial management and transparency (as set out in Title II of the SJU Financial Rules).

Principles of unity and budget accuracy

This principle means that no revenue shall be collected and no expenditure effected unless booked to a line in the budget of SJU. No expenditure may be committed or authorised in excess of the appropriations

authorised by the budget. An appropriation may be entered in the budget only if it is for an item of expenditure considered necessary.

Principle of annuality

The appropriations entered in the budget shall be authorised for a financial year which shall run from 1

January to 31 December.

Principle of equilibrium

The SJU is responsible for the development phase of the SESAR Programme which, following the

extension of the SJU in June 2014 is expected to last until 2024. SESAR is a multi-annual programme and in this respect, the programme will be characterized during its life by an expected imbalance between revenues and expenditure. Considering the nature of the SJU Work Programme, the Administrative Board

adopted its first Budget in 2008 introducing the following interpretation with regard to the principle of equilibrium:

'For the SJU the principle of equilibrium shall apply for the totality of the foreseen period for the development phase. That means that the total budget revenue of the foreseen lifetime of the SJU shall be

in balance with the total budget expenditure of the same period. However, at no point of the existence of the SJU must cumulative commitment appropriations exceed the cumulative amount of revenue appropriations.'

Principle of unit of account

The budget shall be drawn up and implemented in euro and the accounts shall be presented in euro.

Principle of universality

Total revenue shall cover total payment appropriations and all revenue and expenditure shall be entered in full without any adjustment against each other.

Principle of specification

Appropriations shall be earmarked for specific purposes at least by title and chapter.

Principle of sound financial management

Appropriations shall be used in accordance with the principle of sound financial management, namely in accordance with the principles of economy, efficiency and effectiveness.

Principle of transparency

The budget shall be established and implemented and the accounts presented in accordance with the principle of transparency. The budget and any amending budgets shall be published on the internet site

of the SJU within four weeks of their adoption and shall be transmitted to the Commission and the Court of Auditors.

Annual accounts of the SESAR Joint Undertaking 2016

29

1.2. Structure and presentation of budged

The budget of the SJU consists of a statement of revenue and a statement of expenditure with administrative and operational appropriations for commitments and payments. Following the extension of the SJU until 2024 and in view of the establishment of the next SESAR Programme in parallel to the existing first Programme until the end of 2016, the Administrative Board introduced in 2014 the

presentation of the Budget in two separate sections:

Section 1 ('SESAR1'):

Revenues, Commitments, Payments and the Running Cost of the Joint Undertaking related to the first

Programme 2007-2016 under FP7/TEN-T funding are presented here. It should be noted that the European Union commitment revenues – EUR 700 million – were received by the SJU and that all funds related to the Programme had been committed towards the Members by the end of 2013. In term of

revenues, an amount of EUR 13.4 million was recognised and validated as Cash Contribution from Eurocontrol but due to technical issues this contribution will be part of the 2017 Budget.

Section 2 ('SESAR2020'):

Revenues, Commitments and Payments related to the second SESAR Programme 2014-2024 under

HORIZON-2020 funding are presented here. It should be noted that Section 2 of the 2016 Budget was still exclusive of any Running Costs and that no detailed provisions for the Contributions of Members other than the European Union were available. For the same reason, no in-kind contributions in relation

to SESAR2020 had been included into Annex I and II of the Budget yet.

1.3. Highlights of the budgetary implementation

Overall in 2016, budget execution of commitment and payment appropriations reached 98.0 % and 65.1 % respectively (for SESAR1: 96.0% and 52.2% and for SESAR2020: 99.2% and 88.3%). The overall implementation rate was influenced mainly by delays or incomplete invoicing by non-Members and, on

the other side, the SJU's continuous effort to keep the Running costs at the minimum necessary.

Administrative and Staff expenditure (='Running Costs' only under SESAR1 Programme)

Staff expenditure includes all staff related costs such as salaries, social security, taxes, insurances, mission costs, recruitment, secondments and interim support.

Administrative expenditures include the administrative costs such as office supplies (printing, copiers, translation, publications, consumable office material), utilities (water, electricity, telecommunications costs), office rental and associated charges, legal, financial and fiscal expertise for administrative needs

and all insurances not related to staff as well as expenses incurred for the activities of the Administrative Board .This post furthermore includes the procurement, rental and maintenance of IT equipment, furniture and other technical facilities. The IT infrastructure including on-site and remote support is provided mainly by Eurocontrol as part of its services to the SJU.

Unlike for operational expenditure below, appropriations for Running Costs (Titles 1 and 2 of the SJU Budget) are non-differentiated appropriations, i.e. initial Commitment and Payment Appropriations must match.

As in previous years, in 2016 the implementation rate for commitments was high (96.0%) and amounts related to IT services, rental of the building and secondments from Members, amongst others, were carried forward to the next year, mainly due to a contractually fixed time-lag in the invoicing process with

Members . This explains why the implementation rate for Payments 2016 (75.4%), like in all previous years, is considerably lower, an effect which will be counterbalanced with the payments on the last RAL for SESAR1 in 2017.

Operational expenditure

Regarding SESAR 1 operational costs, the execution rate on the commitment appropriations reached 96.1% and on payment appropriations 49.6%. The unused payment appropriations ( EUR 154 million) will cover amounts related to costs incurred during 2015 (claimed and recognised in 2016 but payments

foreseen with the Final Financial Statements) and 2016 (to be claimed in 2017).

Annual accounts of the SESAR Joint Undertaking 2016

30

Regarding SESAR2020 operational costs , the commitment execution rate reached 99.2 %. The total unused appropriations amounted to EUR 500 are an additional (non-H2020 funds) assigned entitlement

for Drone geo-fencing demonstrations activities carried-forward to 2017.

The payment appropriations include EUR 16.5 million for Pre-Financing and interim payments under the first Exploratory Research call launched in 2015 and EUR 40 million for Pre-Financing payments of the First Industrial Research call launched in 2016. The execution rate of payments is 88.3%. The unused

payment appropriations (EUR 6.6 million) were carried-forward to 2017.

Detailed information regarding the budget implementation is provided in the 'Report on the Budgetary and Financial management' of the year.

Annual accounts of the SESAR Joint Undertaking 2016

31

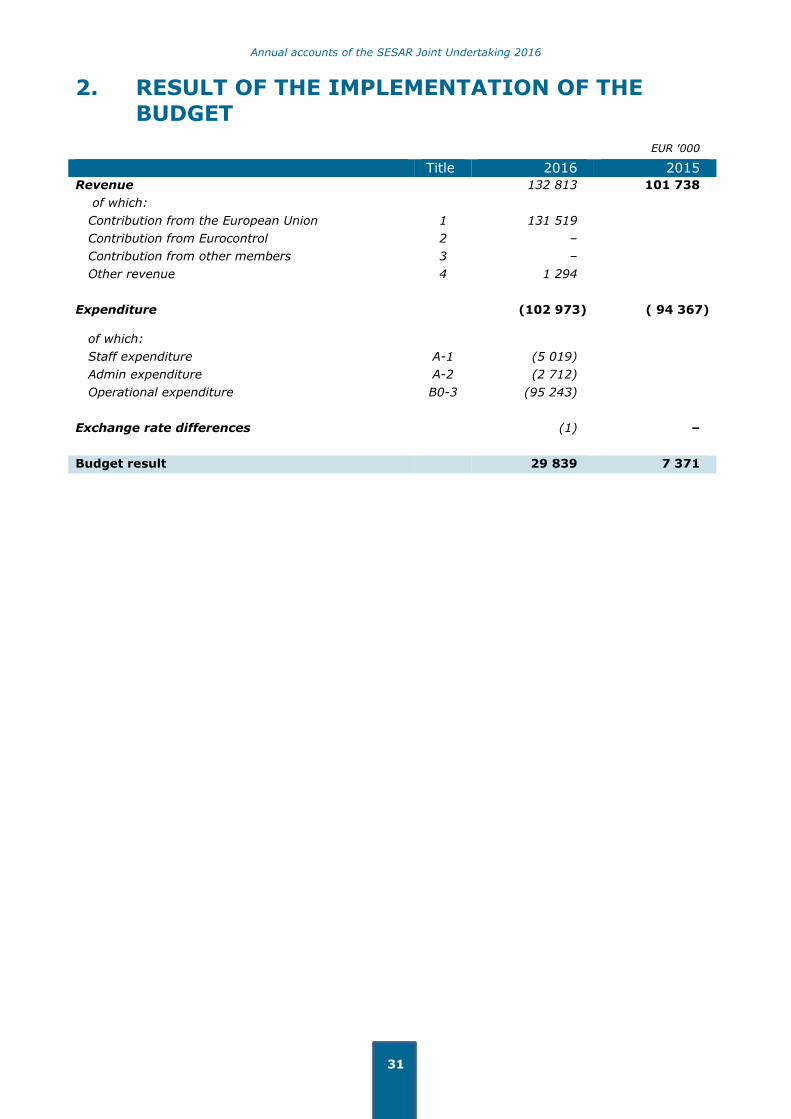

2. RESULT OF THE IMPLEMENTATION OF THE BUDGET

EUR '000

Title 2016 2015

Revenue 132 813 101 738

of which:

Contribution from the European Union 1 131 519

Contribution from Eurocontrol 2 –

Contribution from other members 3 –

Other revenue 4 1 294

Expenditure (102 973) ( 94 367)

of which:

Staff expenditure A-1 (5 019)

Admin expenditure A-2 (2 712)

Operational expenditure B0-3 (95 243)

Exchange rate differences (1) –

Budget result 29 839 7 371

Annual accounts of the SESAR Joint Undertaking 2016

32

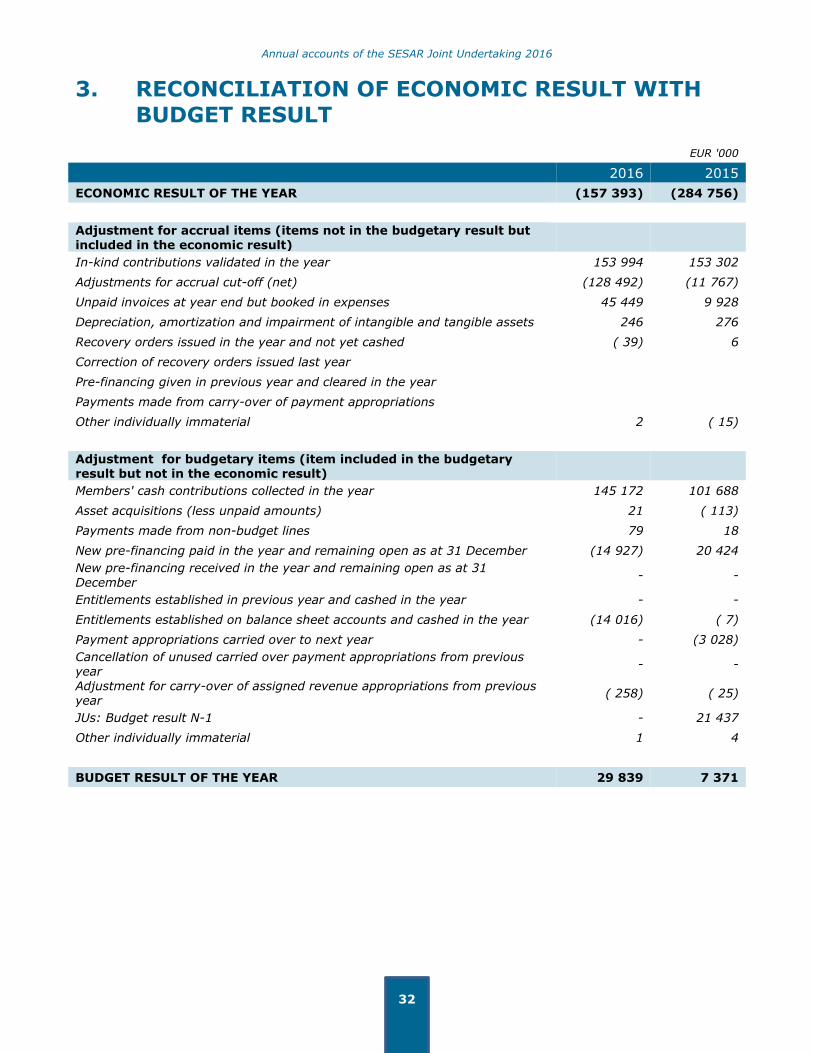

3. RECONCILIATION OF ECONOMIC RESULT WITH BUDGET RESULT

EUR '000

2016 2015

ECONOMIC RESULT OF THE YEAR (157 393) (284 756)

Adjustment for accrual items (items not in the budgetary result but included in the economic result)

In-kind contributions validated in the year 153 994 153 302

Adjustments for accrual cut-off (net) (128 492) (11 767)

Unpaid invoices at year end but booked in expenses 45 449 9 928

Depreciation, amortization and impairment of intangible and tangible assets 246 276

Recovery orders issued in the year and not yet cashed ( 39) 6

Correction of recovery orders issued last year

Pre-financing given in previous year and cleared in the year

Payments made from carry-over of payment appropriations

Other individually immaterial 2 ( 15)

Adjustment for budgetary items (item included in the budgetary result but not in the economic result)

Members' cash contributions collected in the year 145 172 101 688

Asset acquisitions (less unpaid amounts) 21 ( 113)

Payments made from non-budget lines 79 18

New pre-financing paid in the year and remaining open as at 31 December (14 927) 20 424

New pre-financing received in the year and remaining open as at 31

December - -

Entitlements established in previous year and cashed in the year - -

Entitlements established on balance sheet accounts and cashed in the year (14 016) ( 7)

Payment appropriations carried over to next year - (3 028)

Cancellation of unused carried over payment appropriations from previous year

- -

Adjustment for carry-over of assigned revenue appropriations from previous year

( 258) ( 25)

JUs: Budget result N-1 - 21 437

Other individually immaterial 1 4

BUDGET RESULT OF THE YEAR 29 839 7 371

Annual accounts of the SESAR Joint Undertaking 2016

33

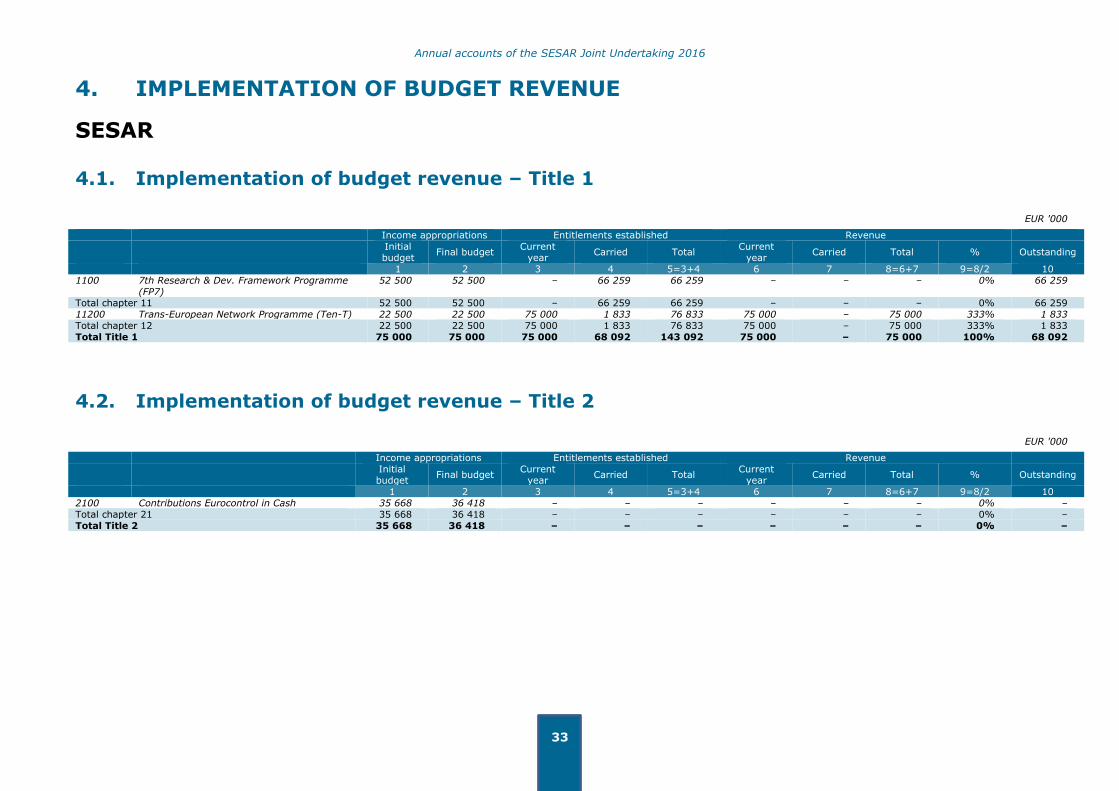

4. IMPLEMENTATION OF BUDGET REVENUE

SESAR

4.1. Implementation of budget revenue – Title 1

EUR '000

Income appropriations Entitlements established Revenue

Initial budget

Final budget Current

year Carried Total

Current year

Carried Total % Outstanding

1 2 3 4 5=3+4 6 7 8=6+7 9=8/2 10 1100 7th Research & Dev. Framework Programme

(FP7) 52 500 52 500 – 66 259 66 259 – – – 0% 66 259

Total chapter 11 52 500 52 500 – 66 259 66 259 – – – 0% 66 259 11200 Trans-European Network Programme (Ten-T) 22 500 22 500 75 000 1 833 76 833 75 000 – 75 000 333% 1 833 Total chapter 12 22 500 22 500 75 000 1 833 76 833 75 000 – 75 000 333% 1 833 Total Title 1 75 000 75 000 75 000 68 092 143 092 75 000 – 75 000 100% 68 092

4.2. Implementation of budget revenue – Title 2

EUR '000

Income appropriations Entitlements established Revenue

Initial budget

Final budget Current

year Carried Total

Current year

Carried Total % Outstanding

1 2 3 4 5=3+4 6 7 8=6+7 9=8/2 10 2100 Contributions Eurocontrol in Cash 35 668 36 418 – – – – – – 0% – Total chapter 21 35 668 36 418 – – – – – – 0% – Total Title 2 35 668 36 418 – – – – – – 0% –

Annual accounts of the SESAR Joint Undertaking 2016

34

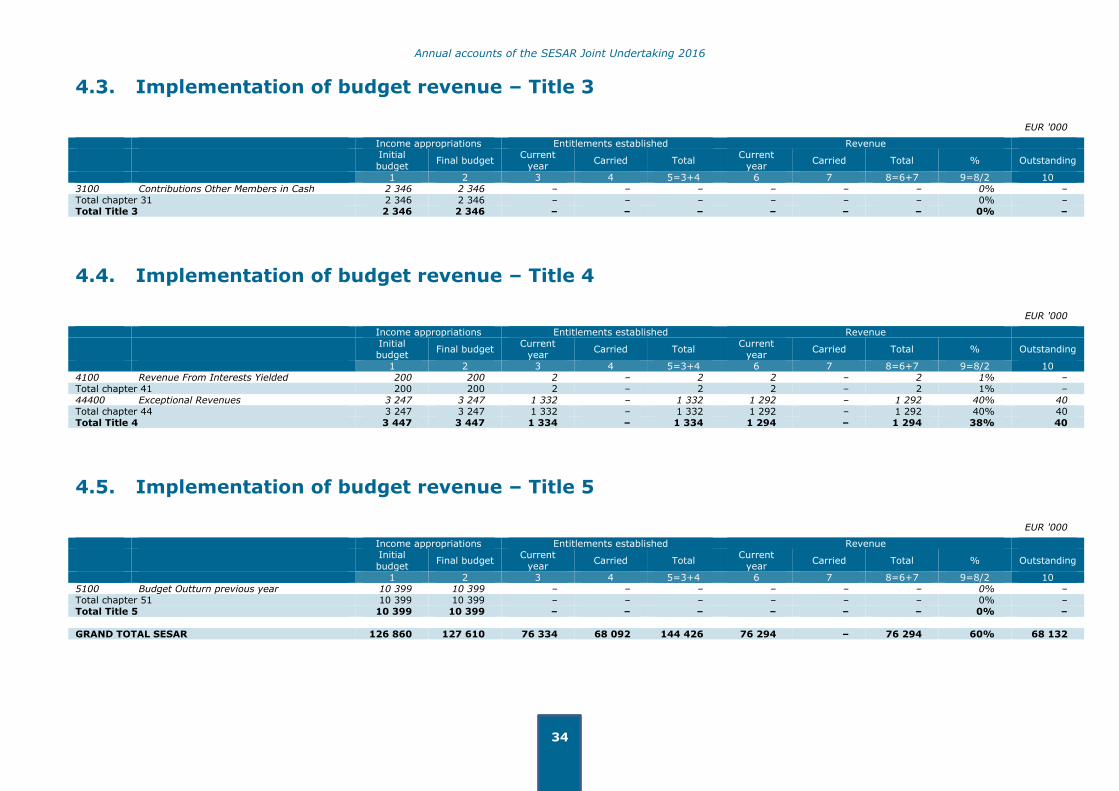

4.3. Implementation of budget revenue – Title 3

EUR '000

Income appropriations Entitlements established Revenue

Initial

budget Final budget

Current

year Carried Total

Current

year Carried Total % Outstanding

1 2 3 4 5=3+4 6 7 8=6+7 9=8/2 10 3100 Contributions Other Members in Cash 2 346 2 346 – – – – – – 0% – Total chapter 31 2 346 2 346 – – – – – – 0% – Total Title 3 2 346 2 346 – – – – – – 0% –

4.4. Implementation of budget revenue – Title 4

EUR '000

Income appropriations Entitlements established Revenue

Initial budget

Final budget Current

year Carried Total

Current year

Carried Total % Outstanding

1 2 3 4 5=3+4 6 7 8=6+7 9=8/2 10 4100 Revenue From Interests Yielded 200 200 2 – 2 2 – 2 1% – Total chapter 41 200 200 2 – 2 2 – 2 1% – 44400 Exceptional Revenues 3 247 3 247 1 332 – 1 332 1 292 – 1 292 40% 40 Total chapter 44 3 247 3 247 1 332 – 1 332 1 292 – 1 292 40% 40 Total Title 4 3 447 3 447 1 334 – 1 334 1 294 – 1 294 38% 40

4.5. Implementation of budget revenue – Title 5

EUR '000

Income appropriations Entitlements established Revenue

Initial budget

Final budget Current

year Carried Total

Current year

Carried Total % Outstanding

1 2 3 4 5=3+4 6 7 8=6+7 9=8/2 10 5100 Budget Outturn previous year 10 399 10 399 – – – – – – 0% – Total chapter 51 10 399 10 399 – – – – – – 0% – Total Title 5 10 399 10 399 – – – – – – 0% – GRAND TOTAL SESAR 126 860 127 610 76 334 68 092 144 426 76 294 – 76 294 60% 68 132

Annual accounts of the SESAR Joint Undertaking 2016

35

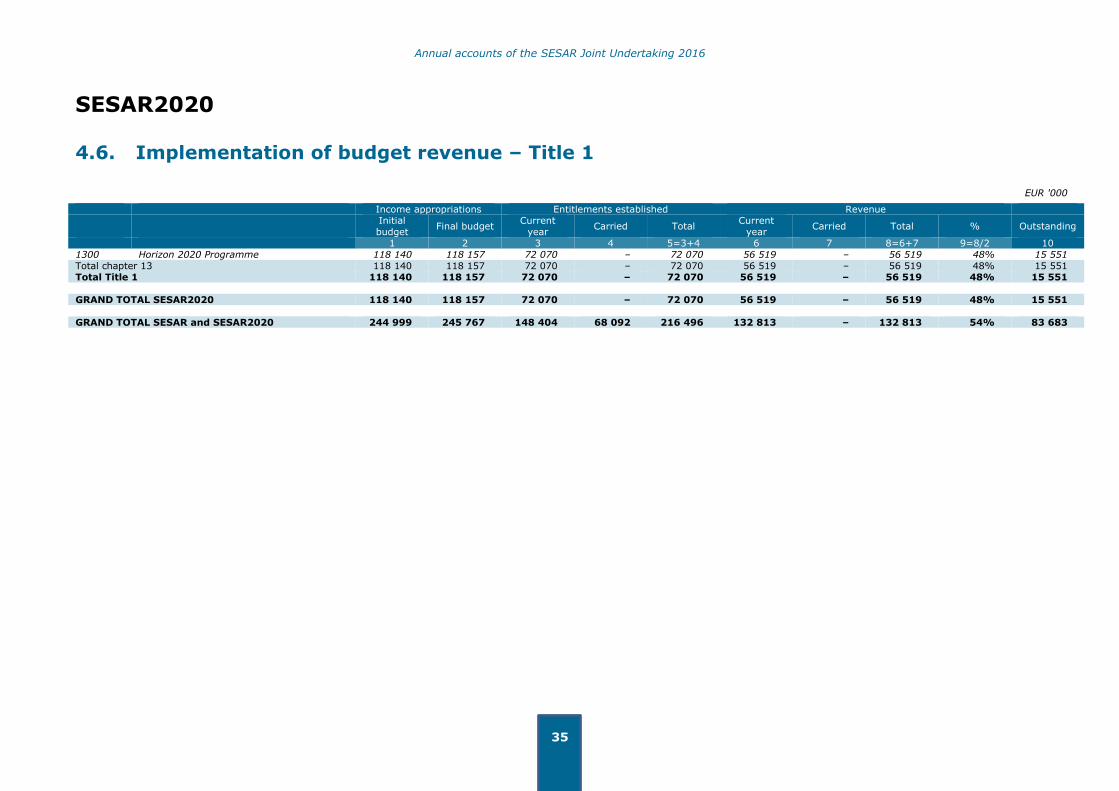

SESAR2020

4.6. Implementation of budget revenue – Title 1

EUR '000

Income appropriations Entitlements established Revenue

Initial budget

Final budget Current

year Carried Total

Current year

Carried Total % Outstanding

1 2 3 4 5=3+4 6 7 8=6+7 9=8/2 10 1300 Horizon 2020 Programme 118 140 118 157 72 070 – 72 070 56 519 – 56 519 48% 15 551 Total chapter 13 118 140 118 157 72 070 – 72 070 56 519 – 56 519 48% 15 551 Total Title 1 118 140 118 157 72 070 – 72 070 56 519 – 56 519 48% 15 551 GRAND TOTAL SESAR2020 118 140 118 157 72 070 – 72 070 56 519 – 56 519 48% 15 551 GRAND TOTAL SESAR and SESAR2020 244 999 245 767 148 404 68 092 216 496 132 813 – 132 813 54% 83 683

Annual accounts of the SESAR Joint Undertaking 2016

36

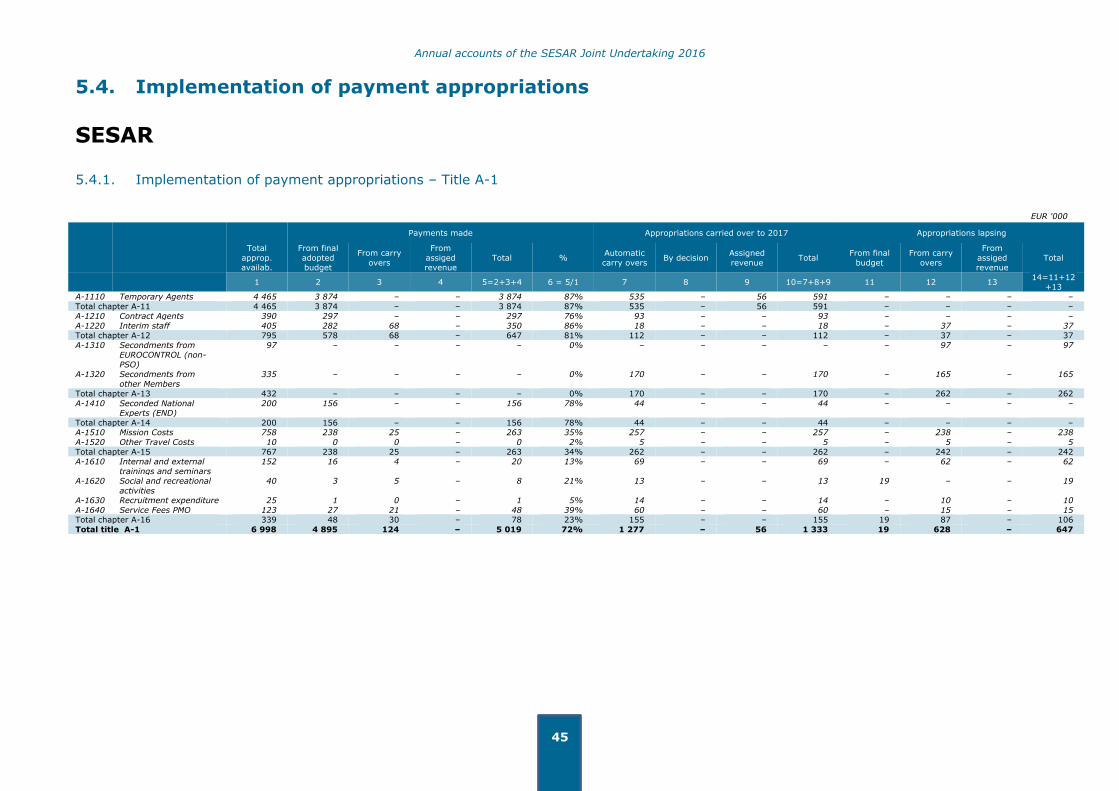

5. IMPLEMENTATION OF BUDGET EXPENDITURE

5.1. Breakdown & changes in commitment appropriations

SESAR

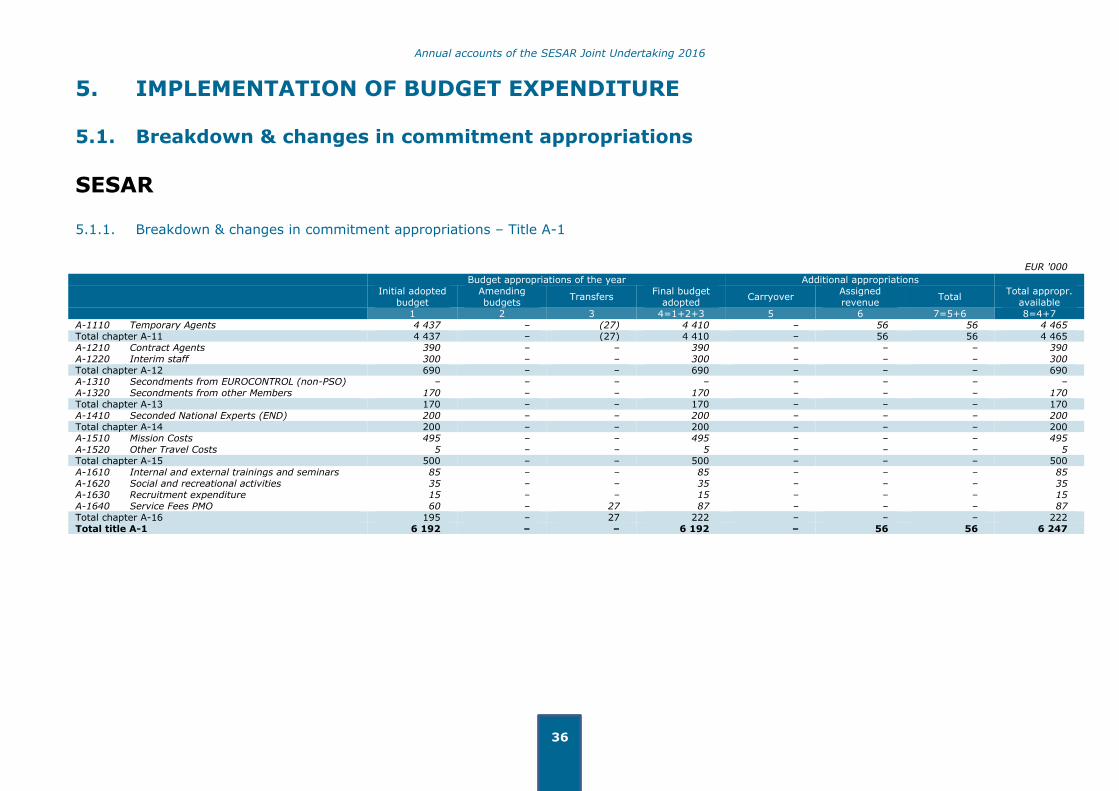

5.1.1. Breakdown & changes in commitment appropriations – Title A-1

EUR '000

Budget appropriations of the year Additional appropriations

Initial adopted

budget Amending budgets

Transfers Final budget

adopted Carryover

Assigned revenue

Total Total appropr.

available 1 2 3 4=1+2+3 5 6 7=5+6 8=4+7

A-1110 Temporary Agents 4 437 – (27) 4 410 – 56 56 4 465 Total chapter A-11 4 437 – (27) 4 410 – 56 56 4 465 A-1210 Contract Agents 390 – – 390 – – – 390 A-1220 Interim staff 300 – – 300 – – – 300 Total chapter A-12 690 – – 690 – – – 690 A-1310 Secondments from EUROCONTROL (non-PSO) – – – – – – – – A-1320 Secondments from other Members 170 – – 170 – – – 170 Total chapter A-13 170 – – 170 – – – 170 A-1410 Seconded National Experts (END) 200 – – 200 – – – 200 Total chapter A-14 200 – – 200 – – – 200 A-1510 Mission Costs 495 – – 495 – – – 495 A-1520 Other Travel Costs 5 – – 5 – – – 5 Total chapter A-15 500 – – 500 – – – 500 A-1610 Internal and external trainings and seminars 85 – – 85 – – – 85 A-1620 Social and recreational activities 35 – – 35 – – – 35 A-1630 Recruitment expenditure 15 – – 15 – – – 15 A-1640 Service Fees PMO 60 – 27 87 – – – 87 Total chapter A-16 195 – 27 222 – – – 222 Total title A-1 6 192 – – 6 192 – 56 56 6 247

Annual accounts of the SESAR Joint Undertaking 2016

37

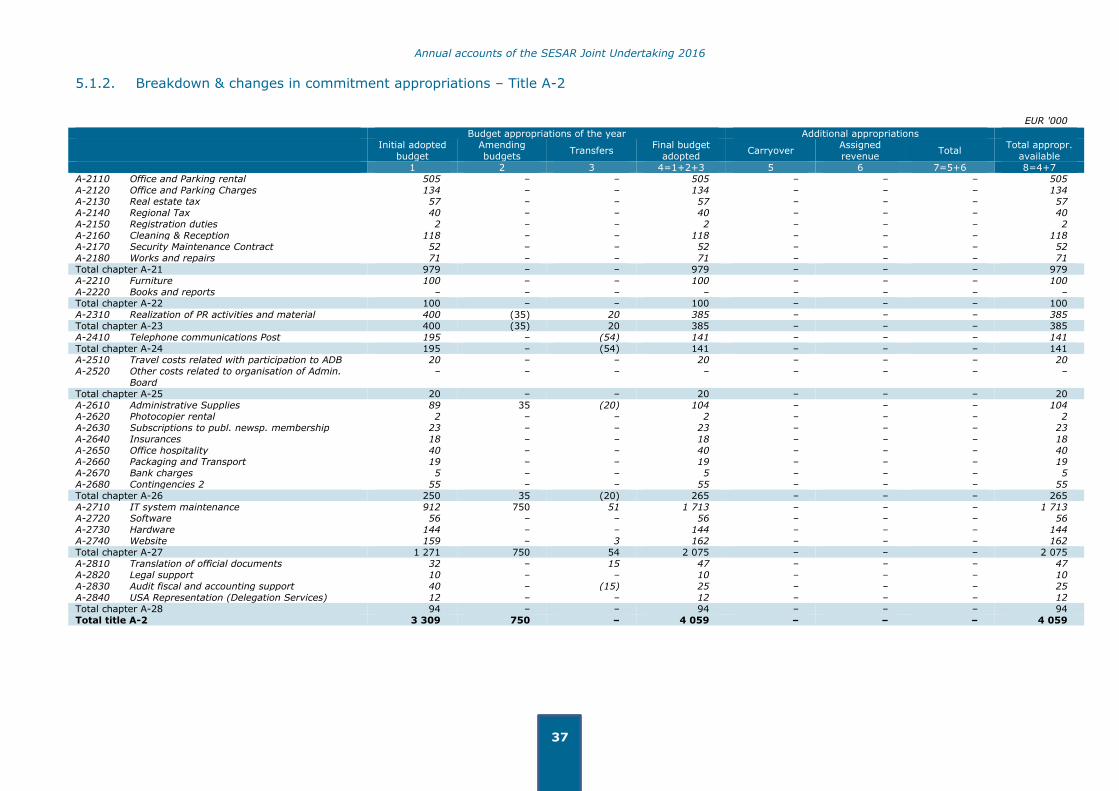

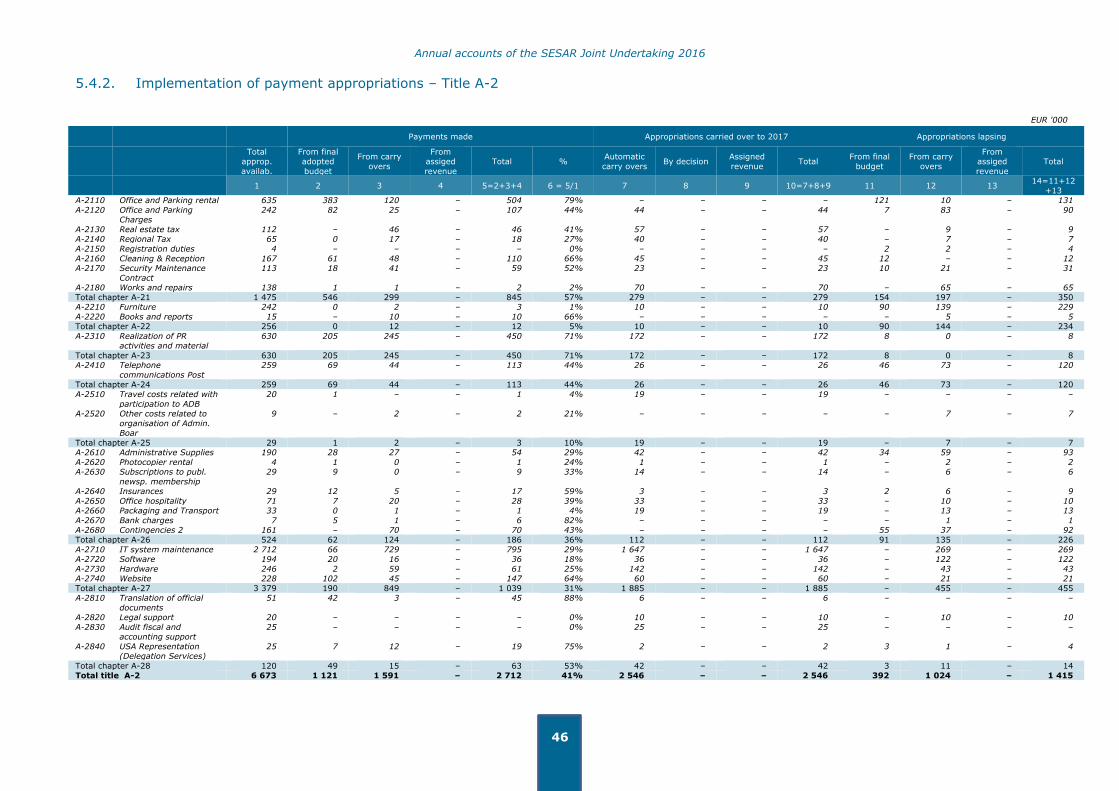

5.1.2. Breakdown & changes in commitment appropriations – Title A-2

EUR '000

Budget appropriations of the year Additional appropriations

Initial adopted

budget Amending budgets

Transfers Final budget

adopted Carryover

Assigned revenue

Total Total appropr.

available

1 2 3 4=1+2+3 5 6 7=5+6 8=4+7 A-2110 Office and Parking rental 505 – – 505 – – – 505 A-2120 Office and Parking Charges 134 – – 134 – – – 134 A-2130 Real estate tax 57 – – 57 – – – 57 A-2140 Regional Tax 40 – – 40 – – – 40 A-2150 Registration duties 2 – – 2 – – – 2 A-2160 Cleaning & Reception 118 – – 118 – – – 118 A-2170 Security Maintenance Contract 52 – – 52 – – – 52 A-2180 Works and repairs 71 – – 71 – – – 71 Total chapter A-21 979 – – 979 – – – 979 A-2210 Furniture 100 – – 100 – – – 100 A-2220 Books and reports – – – – – – – – Total chapter A-22 100 – – 100 – – – 100 A-2310 Realization of PR activities and material 400 (35) 20 385 – – – 385 Total chapter A-23 400 (35) 20 385 – – – 385 A-2410 Telephone communications Post 195 – (54) 141 – – – 141 Total chapter A-24 195 – (54) 141 – – – 141 A-2510 Travel costs related with participation to ADB 20 – – 20 – – – 20 A-2520 Other costs related to organisation of Admin.

Board – – – – – – – –

Total chapter A-25 20 – – 20 – – – 20 A-2610 Administrative Supplies 89 35 (20) 104 – – – 104 A-2620 Photocopier rental 2 – – 2 – – – 2 A-2630 Subscriptions to publ. newsp. membership 23 – – 23 – – – 23 A-2640 Insurances 18 – – 18 – – – 18 A-2650 Office hospitality 40 – – 40 – – – 40 A-2660 Packaging and Transport 19 – – 19 – – – 19 A-2670 Bank charges 5 – – 5 – – – 5 A-2680 Contingencies 2 55 – – 55 – – – 55

Total chapter A-26 250 35 (20) 265 – – – 265 A-2710 IT system maintenance 912 750 51 1 713 – – – 1 713 A-2720 Software 56 – – 56 – – – 56 A-2730 Hardware 144 – – 144 – – – 144 A-2740 Website 159 – 3 162 – – – 162 Total chapter A-27 1 271 750 54 2 075 – – – 2 075 A-2810 Translation of official documents 32 – 15 47 – – – 47 A-2820 Legal support 10 – – 10 – – – 10 A-2830 Audit fiscal and accounting support 40 – (15) 25 – – – 25 A-2840 USA Representation (Delegation Services) 12 – – 12 – – – 12 Total chapter A-28 94 – – 94 – – – 94 Total title A-2 3 309 750 – 4 059 – – – 4 059

Annual accounts of the SESAR Joint Undertaking 2016

38

5.1.3. Breakdown & changes in commitment appropriations – Title B-3

EUR '000

Budget appropriations of the year Additional appropriations

Initial adopted

budget Amending budgets

Transfers Final budget

adopted Carryover

Assigned revenue

Total Total appropr.

available

1 2 3 4=1+2+3 5 6 7=5+6 8=4+7 B3-100 Studies / Development conducted by the SJU 26 685 0 – 26 686 703 298 1 001 27 686 Total chapter B3-1 26 685 0 – 26 686 703 298 1 001 27 686 B3-300 Studies / Development conducted by the

members – – – – – 1 278 1 278 1 278

Total chapter B3-3 – – – – – 1 278 1 278 1 278 Total title B-3 26 685 0 – 26 686 703 1 576 2 279 28 964 GRAND TOTAL SESAR 36 185 750 – 36 936 703 1 631 2 334 39 270

SESAR2020

5.1.4. Breakdown & changes in commitment appropriations – Title B-3

EUR '000

Budget appropriations of the year Additional appropriations

Initial adopted

budget Amending budgets

Transfers Final budget

adopted Carryover

Assigned revenue

Total Total appropr.

available 1 2 3 4=1+2+3 5 6 7=5+6 8=4+7

B3-100 Studies / Development conducted by the SJU 61 638 500 – 62 138 – – – 62 138 Total chapter B3-1 61 638 500 – 62 138 – – – 62 138 B3-300 Studies / Development conducted by the

members – – – – – – – –

Total chapter B3-3 – – – – – – – –

Total title B-3 61 638 500 – 62 138 – – – 62 138 GRAND TOTAL SESAR2020 61 638 500 – 62 138 – – – 62 138 GRAND TOTAL SESAR and SESAR2020 97 823 1 250 – 99 074 703 1 631 2 334 101 408

Annual accounts of the SESAR Joint Undertaking 2016

39

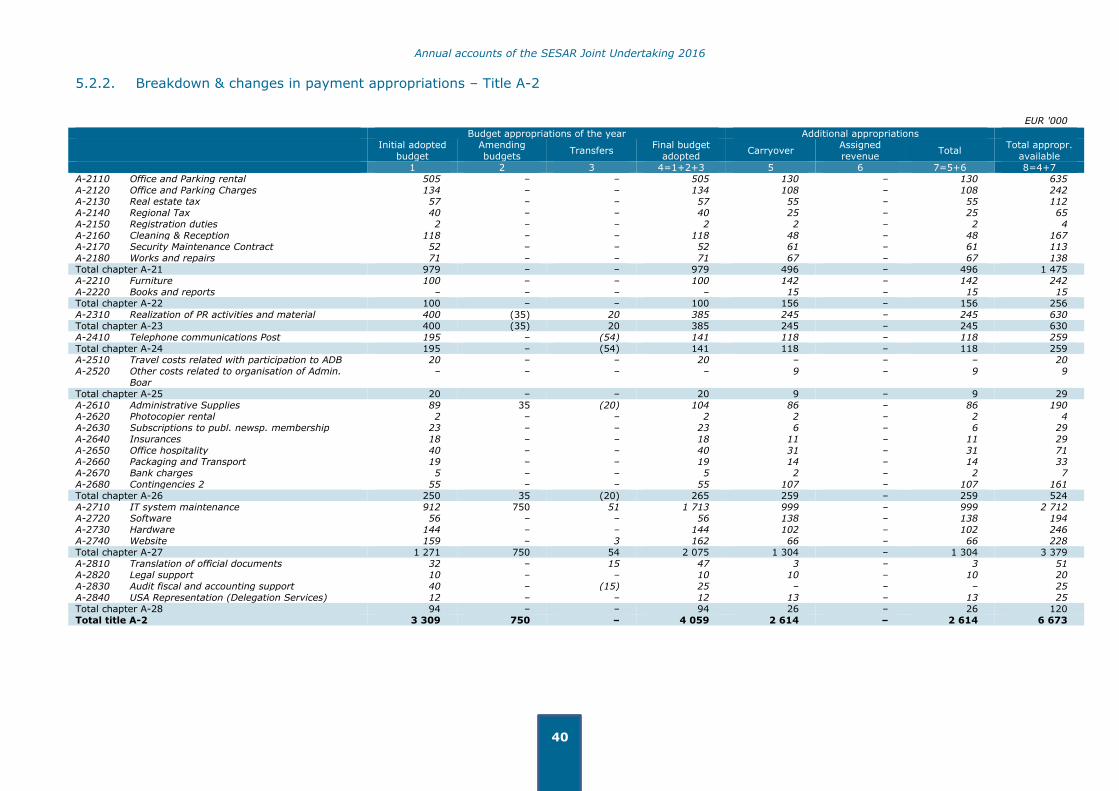

5.2. Breakdown & changes in payment appropriations

SESAR

5.2.1. Breakdown & changes in payment appropriations – Title A-1

EUR '000

Budget appropriations of the year Additional appropriations

Initial adopted

budget Amending budgets

Transfers Final budget

adopted Carryover

Assigned revenue

Total Total appropr.

available 1 2 3 4=1+2+3 5 6 7=5+6 8=4+7

A-1110 Temporary Agents 4 437 – (27) 4 410 – 56 56 4 465 Total chapter A-11 4 437 – (27) 4 410 – 56 56 4 465 A-1210 Contract Agents 390 – – 390 – – – 390 A-1220 Interim staff 300 – – 300 105 – 105 405 Total chapter A-12 690 – – 690 105 – 105 795 A-1310 Secondments from EUROCONTROL (non-PSO) – – – – 97 – 97 97 A-1320 Secondments from other Members 170 – – 170 165 – 165 335 Total chapter A-13 170 – – 170 262 – 262 432 A-1410 Seconded National Experts (END) 200 – – 200 – – – 200 Total chapter A-14 200 – – 200 – – – 200 A-1510 Mission Costs 495 – – 495 263 – 263 758 A-1520 Other Travel Costs 5 – – 5 5 – 5 10 Total chapter A-15 500 – – 500 267 – 267 767 A-1610 Internal and external trainings and seminars 85 – – 85 67 – 67 152 A-1620 Social and recreational activities 35 – – 35 5 – 5 40 A-1630 Recruitment expenditure 15 – – 15 10 – 10 25 A-1640 Service Fees PMO 60 – 27 87 36 – 36 123 Total chapter A-16 195 – 27 222 117 – 117 339 Total title A-1 6 192 – – 6 192 751 56 807 6 998

Annual accounts of the SESAR Joint Undertaking 2016

40

5.2.2. Breakdown & changes in payment appropriations – Title A-2

EUR '000

Budget appropriations of the year Additional appropriations

Initial adopted

budget Amending budgets

Transfers Final budget

adopted Carryover

Assigned revenue

Total Total appropr.

available

1 2 3 4=1+2+3 5 6 7=5+6 8=4+7 A-2110 Office and Parking rental 505 – – 505 130 – 130 635 A-2120 Office and Parking Charges 134 – – 134 108 – 108 242 A-2130 Real estate tax 57 – – 57 55 – 55 112 A-2140 Regional Tax 40 – – 40 25 – 25 65 A-2150 Registration duties 2 – – 2 2 – 2 4 A-2160 Cleaning & Reception 118 – – 118 48 – 48 167 A-2170 Security Maintenance Contract 52 – – 52 61 – 61 113 A-2180 Works and repairs 71 – – 71 67 – 67 138 Total chapter A-21 979 – – 979 496 – 496 1 475 A-2210 Furniture 100 – – 100 142 – 142 242 A-2220 Books and reports – – – – 15 – 15 15 Total chapter A-22 100 – – 100 156 – 156 256 A-2310 Realization of PR activities and material 400 (35) 20 385 245 – 245 630 Total chapter A-23 400 (35) 20 385 245 – 245 630 A-2410 Telephone communications Post 195 – (54) 141 118 – 118 259 Total chapter A-24 195 – (54) 141 118 – 118 259 A-2510 Travel costs related with participation to ADB 20 – – 20 – – – 20 A-2520 Other costs related to organisation of Admin.

Boar – – – – 9 – 9 9

Total chapter A-25 20 – – 20 9 – 9 29 A-2610 Administrative Supplies 89 35 (20) 104 86 – 86 190 A-2620 Photocopier rental 2 – – 2 2 – 2 4 A-2630 Subscriptions to publ. newsp. membership 23 – – 23 6 – 6 29 A-2640 Insurances 18 – – 18 11 – 11 29 A-2650 Office hospitality 40 – – 40 31 – 31 71 A-2660 Packaging and Transport 19 – – 19 14 – 14 33 A-2670 Bank charges 5 – – 5 2 – 2 7 A-2680 Contingencies 2 55 – – 55 107 – 107 161

Total chapter A-26 250 35 (20) 265 259 – 259 524 A-2710 IT system maintenance 912 750 51 1 713 999 – 999 2 712 A-2720 Software 56 – – 56 138 – 138 194 A-2730 Hardware 144 – – 144 102 – 102 246 A-2740 Website 159 – 3 162 66 – 66 228 Total chapter A-27 1 271 750 54 2 075 1 304 – 1 304 3 379 A-2810 Translation of official documents 32 – 15 47 3 – 3 51 A-2820 Legal support 10 – – 10 10 – 10 20 A-2830 Audit fiscal and accounting support 40 – (15) 25 – – – 25 A-2840 USA Representation (Delegation Services) 12 – – 12 13 – 13 25 Total chapter A-28 94 – – 94 26 – 26 120 Total title A-2 3 309 750 – 4 059 2 614 – 2 614 6 673

Annual accounts of the SESAR Joint Undertaking 2016

41

5.2.3. Breakdown & changes in payment appropriations – Title B-3

EUR '000

Budget appropriations of the year Additional appropriations

Initial adopted

budget Amending budgets

Transfers Final budget

adopted Carryover

Assigned revenue

Total Total appropr.

available

1 2 3 4=1+2+3 5 6 7=5+6 8=4+7 B3-100 Studies / Development conducted by the SJU 38 026 – – 38 026 703 298 1 001 39 027 Total chapter B3-1 38 026 – – 38 026 703 298 1 001 39 027 B3-300 Studies / Development conducted by the

members 41 959 10 399 (0) 52 357 – 1 278 1 278 53 635

Total chapter B3-3 41 959 10 399 (0) 52 357 – 1 278 1 278 53 635 Total title B-3 79 985 10 399 (0) 90 383 703 1 576 2 279 92 662 GRAND TOTAL SESAR 89 485 11 149 – 100 633 4 068 1 631 5 699 106 333

SESAR2020

5.2.4. Breakdown & changes in payment appropriations – Title B-3

EUR '000

Budget appropriations of the year Additional appropriations

Initial adopted

budget Amending budgets

Transfers Final budget

adopted Carryover

Assigned revenue

Total Total appropr.

available 1 2 3 4=1+2+3 5 6 7=5+6 8=4+7

B3-100 Studies / Development conducted by the SJU 24 200 (7 681) – 16 519 – – – 16 519 Total chapter B3-1 24 200 (7 681) – 16 519 – – – 16 519 B3-300 Studies / Development conducted by the

members 32 302 7 699 – 40 000 – – – 40 000

Total chapter B3-3 32 302 7 699 – 40 000 – – – 40 000

Total title B-3 56 502 18 – 56 519 – – – 56 519 GRAND TOTAL SESAR2020 56 502 18 – 56 519 – – – 56 519 GRAND TOTAL SESAR and SESAR2020 145 986 11 167 (0) 157 153 4 068 1 631 5 699 162 852

Annual accounts of the SESAR Joint Undertaking 2016

42

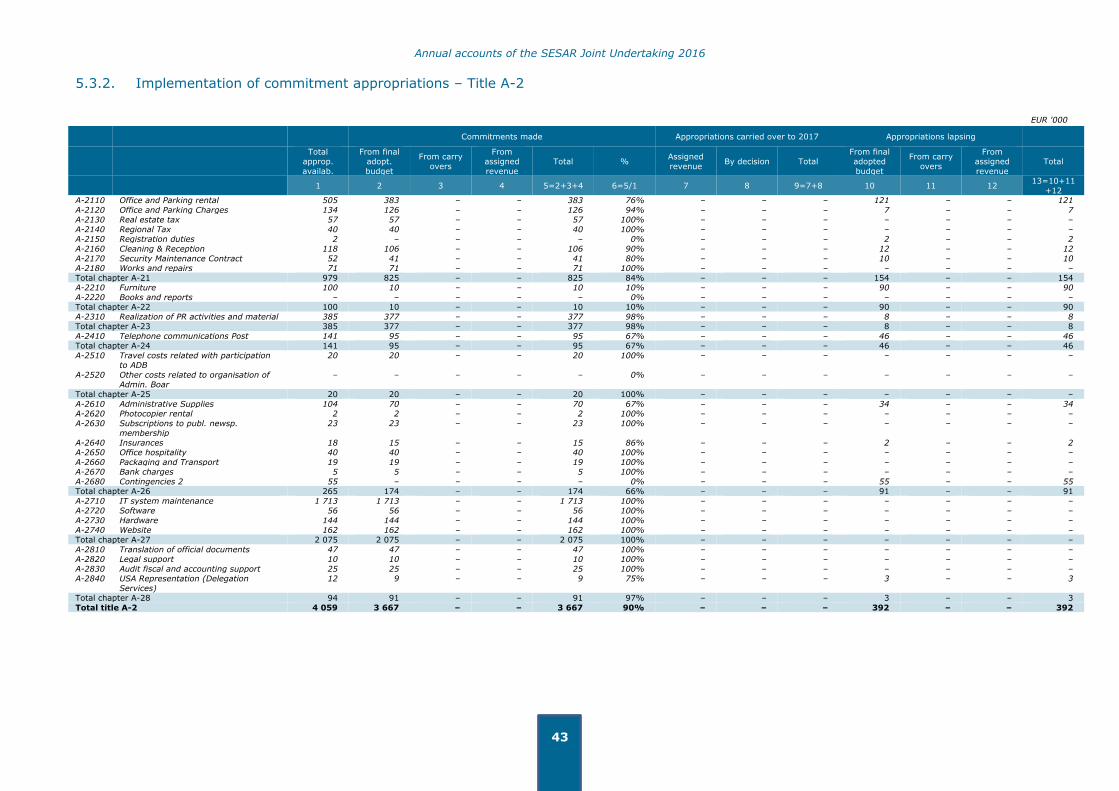

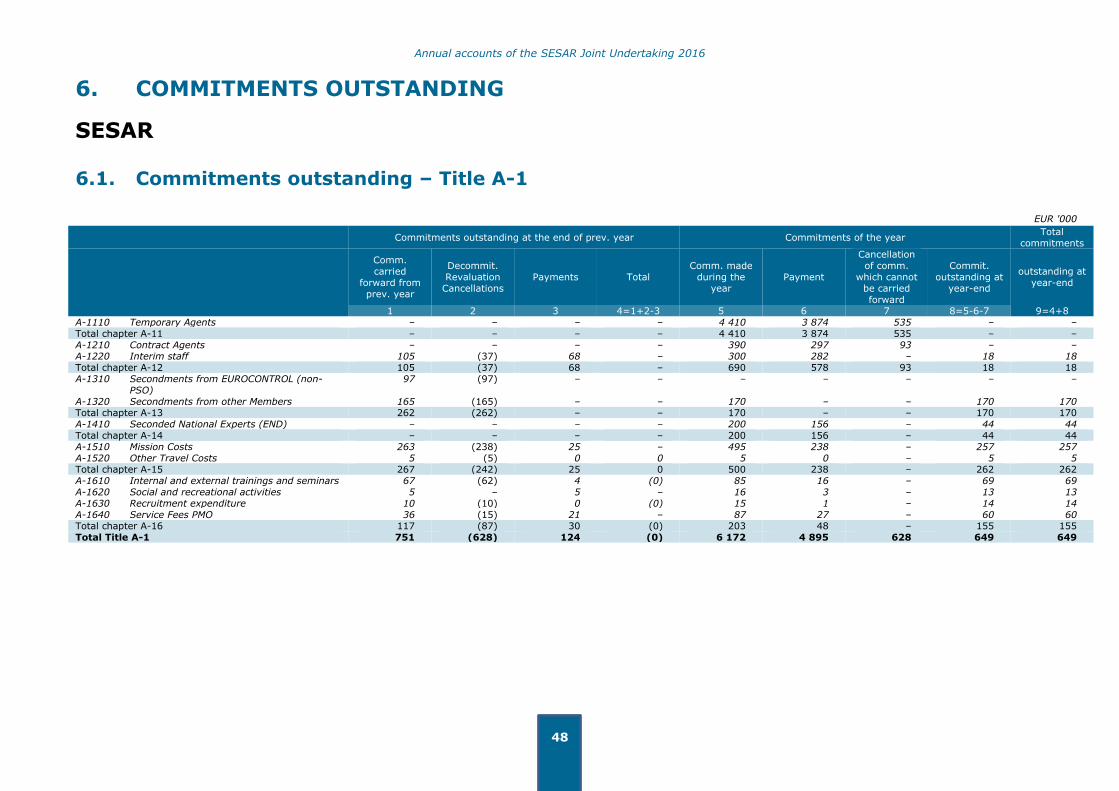

5.3. Implementation of commitment appropriations

SESAR

5.3.1. Implementation of commitment appropriations – Title A-1

EUR '000

Commitments made Appropriations carried over to 2017 Appropriations lapsing

Total

approp. availab.

From final

adopt. budget

From carry

overs

From

assigned revenue

Total % Assigned

revenue By decision Total

From final

adopted budget

From carry

overs

From

assigned revenue

Total

1 2 3 4 5=2+3+4 6=5/1 7 8 9=7+8 10 11 12 13=10+11

+12

A-1110 Temporary Agents 4 465 4 410 – – 4 410 99% 56 – 56 – – – –

Total chapter A-11 4 465 4 410 – – 4 410 99% 56 – 56 – – – – A-1210 Contract Agents 390 390 – – 390 100% – – – – – – –

A-1220 Interim staff 300 300 – – 300 100% – – – – – – – Total chapter A-12 690 690 – – 690 100% – – – – – – –

A-1310 Secondments from EUROCONTROL (non-PSO)

– – – – – 0% – – – – – – –

A-1320 Secondments from other Members 170 170 – – 170 100% – – – – – – – Total chapter A-13 170 170 – – 170 100% – – – – – – –

A-1410 Seconded National Experts (END) 200 200 – – 200 100% – – – – – – – Total chapter A-14 200 200 – – 200 100% – – – – – – –

A-1510 Mission Costs 495 495 – – 495 100% – – – – – – – A-1520 Other Travel Costs 5 5 – – 5 100% – – – – – – –

Total chapter A-15 500 500 – – 500 100% – – – – – – – A-1610 Internal and external trainings and

seminars

85 85 – – 85 100% – – – – – – –

A-1620 Social and recreational activities 35 16 – – 16 46% – – – 19 – – 19 A-1630 Recruitment expenditure 15 15 – – 15 100% – – – – – – –

A-1640 Service Fees PMO 87 87 – – 87 100% – – – – – – – Total chapter A-16 222 203 – – 203 91% – – – 19 – – 19

Total title A-1 6 247 6 172 – – 6 172 99% 56 – 56 19 – – 19

Annual accounts of the SESAR Joint Undertaking 2016

43

5.3.2. Implementation of commitment appropriations – Title A-2

EUR '000

Commitments made Appropriations carried over to 2017 Appropriations lapsing

Total

approp.

availab.

From final adopt.

budget

From carry

overs

From assigned

revenue

Total % Assigned

revenue By decision Total

From final adopted

budget

From carry

overs

From assigned

revenue

Total

1 2 3 4 5=2+3+4 6=5/1 7 8 9=7+8 10 11 12 13=10+11

+12 A-2110 Office and Parking rental 505 383 – – 383 76% – – – 121 – – 121

A-2120 Office and Parking Charges 134 126 – – 126 94% – – – 7 – – 7 A-2130 Real estate tax 57 57 – – 57 100% – – – – – – –

A-2140 Regional Tax 40 40 – – 40 100% – – – – – – – A-2150 Registration duties 2 – – – – 0% – – – 2 – – 2

A-2160 Cleaning & Reception 118 106 – – 106 90% – – – 12 – – 12

A-2170 Security Maintenance Contract 52 41 – – 41 80% – – – 10 – – 10 A-2180 Works and repairs 71 71 – – 71 100% – – – – – – –