Embed Size (px)

Citation preview

André Maggi

Participações

S.A. (Amaggi)

Financial Statements as of

December 31, 2020

KPDS 796991

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

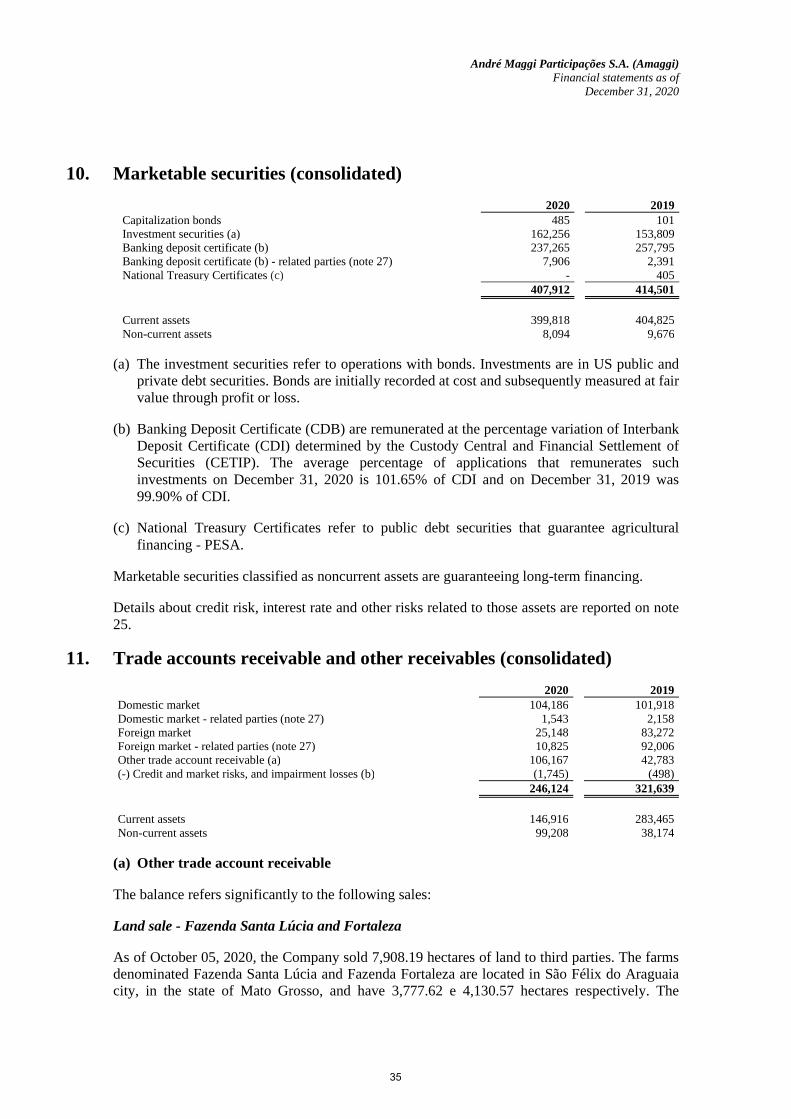

Content

Management report 3

Independent auditor’s report 4

Statements of financial position 9

Statements income 10

Statements of comprehensive income 11

Statements of changes in equity 12

Statements of cash flows 13

Notes to the financial statements 14

2

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

Shareholders,

We are pleased to submit for consideration of the financial statements of the André Maggi Participações S.A., for the financial year ended 31 December 2020, compared to 2019, with Independent Auditors ' report on the financial statements and related notes.

These documents, which were prepared in accordance with accounting practices adopted in Brazil, including the pronouncements issued by the Accounting Pronouncements Committee - CPC and the International Financial Reporting Standards - IFRS issued by the International Accounting Standards Board - IASB by on December 31, 2020, and contains all data necessary for the analysis of activities and performance of the Company during the year.

The management is grateful to everyone who contributed to the results achieved, especially our team of employees for the commitment and dedication to the suppliers and service providers for the quality and timeliness and to customers by credibility in our work

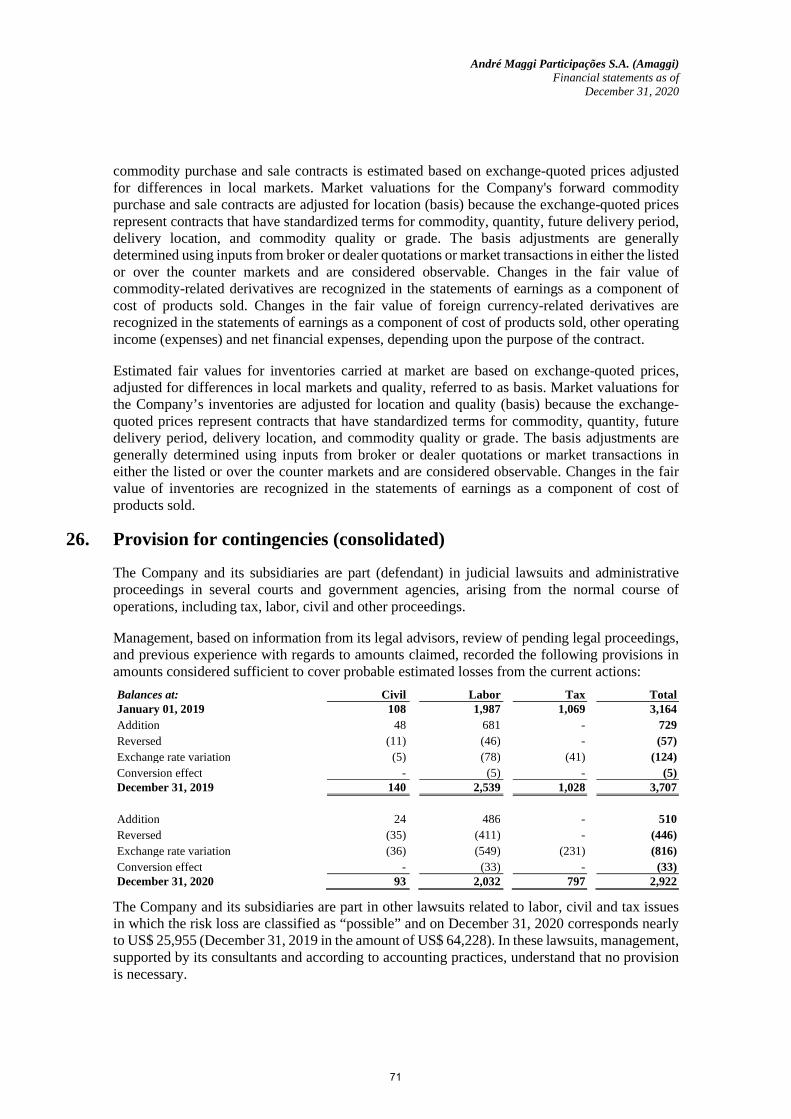

We are at your disposal for any further clarifications that may be judged necessary.

Cuiabá - MT, March 08, 2021.

Directors.

3

KPMG Auditores Independentes, uma sociedade simples brasileira e firma-membro da rede KPMG de firmas-membro independentes e afiliadas à KPMG International Cooperative (“KPMG International”), uma entidade suíça.

KPMG Auditores Independentes, a Brazilian entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

KPMG Auditores Independentes

Avenida Presidente Vargas, 2.121

Salas 1401 a 1405, 1409 e 1410 - Jardim América

Edifício Times Square Business

14020-260 - Ribeirão Preto/SP – Brasil

Independent Auditor’s Report on the Individual and

Consolidated Financial Statements

To

The Board of Directors and Shareholders of

André Maggi Participações S.A. (Amaggi)

Cuiabá – MT

Opinion

We have audited the individual and consolidated financial statements of André Maggi Participações S.A. (“the Company”), respectively referred to as Parent and Consolidated, which comprise the statement of financial position as at December 31, 2020, the statements of income and other comprehensive income, changes in equity and cash flows for the year then ended, and notes, comprising significant accounting policies and other explanatory information.

In our opinion, the accompanying individual and consolidated financial statements present fairly, in all material respects, the individual and consolidated financial position of the André Maggi Participações S.A. as at December 31, 2020, and of its individual and consolidated financial performance and its individual and consolidated cash flows for the year then ended in accordance with Accounting Practices Adopted in Brazil and with International Financial Reporting Standards (IFRS), issued by the International Accounting Standards Board (IASB).

Base for opinion

We conducted our audit in accordance with Brazilian and International Standards on Auditing. Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the Individual and Consolidated Financial Statements section of our report. We are independent of the Company and its subsidiaries in accordance with the relevant ethical requirements included in the Accountant Professional Code of Ethics (“Código de Ética Profissional do Contador”) and in the professional standards issued by the Brazilian Federal Accounting Council (“Conselho Federal de Contabilidade”) and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

4

KPMG Auditores Independentes, uma sociedade simples brasileira e firma-membro da rede KPMG de firmas-membro independentes e afiliadas à KPMG International Cooperative (“KPMG International”), uma entidade suíça.

KPMG Auditores Independentes, a Brazilian entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the individual and consolidated financial statements of the current period. These matters were addressed in the context of our audit of the individual and consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

Measuring the fair value of term commodity contracts See Notes 6.c and 25.d to the individual and consolidated financial statements. Key audit matter How our audit addressed this matter The Company and its subsidiaries maintain derivative financial instruments to hedge their exposures to the risks of changes in commodity prices. All gains or losses arising from derivative financial instruments are recognized at fair value.

The fair value for forward commodity purchase and sale contracts are estimated based on exchange-quoted prices adjusted for differences in local markets. Market valuations for the Company's forward commodity purchase and sale contracts are adjusted for location (basis) because the exchange-quoted prices represent contracts that have standardized terms for commodity, quantity, future delivery period, delivery location, and commodity quality or grade. In some cases, the basis adjustments are unobservable because they are supported by little to no market activity.

Due to the assumptions used in estimated the fair value of forward commodity purchase and sale contracts have a significant risk of resulting in a material adjustment to the financial statements, we consider this a significant matter for our audit.

.

Our audit procedures included, but were not limited to:

We evaluated the Company´s accountingpolicies and guidelines including itsmark-to-market policy and fair valuegovernance policy relating to long termcommodity contracts, and assessed thesepolicies in relation to applicableframework requirements and currentmarket practice in the applicationthereof;

We evaluate the terms of the contractsand contract amendments with theCompany’s counterparties for a sampleof contracts;

We tested the valuation of allindividually material long-term contractsand a sample of individually immaterialcontracts.

For each of the aforementioned contracts:

We tested whether the classification andaccounting adopted were based on theCompany's policies and guidelines, aswell on the applicable frameworkrequirements;

We tested the valuation of each contract,by assessing the ability of the model toaccurately capture the risks of theunderlying contract, testing theobservable market inputs to third partyderived data sources, evaluating otherassumptions in the model, and testing themathematical integrity of the model;

We also tested the consistency ofapplication of the valuationmethodologies across the portfolio;

We understood and evaluated themethodology employed to derive forward price curves for a sample of commoditiesand discount curves for a sample ofcontracts. For forward price curve, wetested the observable inputs to third partysourced data, and corroborated thereasonableness of unobservable inputs by

5

KPMG Auditores Independentes, uma sociedade simples brasileira e firma-membro da rede KPMG de firmas-membro independentes e afiliadas à KPMG International Cooperative (“KPMG International”), uma entidade suíça.

KPMG Auditores Independentes, a Brazilian entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

comparing to available data sources, including consensus forecasts for long term prices;

We also evaluated whether the derivedcurves were internally consistent. Wetested the mathematical integrity of theprice curve models and that they wereappropriately applied to the contracts.For discount curves, we tested theobservable inputs to third party sourceddata, and corroborated thereasonableness of unobservable inputs by comparing to available data sources,including credit ratings of the contractingparties determined by external creditrating agencies. We tested whether thetenors of the discount curves wereconsistent with the underlying contracts;

We also assessed the adequacy of therelated disclosures in the notes to thefinancial statements.

Based on the audit procedures above summarized, we consider that the measurement of commodity contracts’ fair value, as well as the respective disclosures, are appropriate, in the context of the financial statements taken as a whole, for the year ended December 31, 2020.

Measurement of the fair value of biological assets See Notes 6.i and 13 to the consolidated financial statements. Key audit matter How our audit addressed this matter The Company and its subsidiaries measured their biological assets, which correspond mainly to the cultivation of agricultural products (soybeans, corn and cotton), based on their fair value less costs to sell.

The estimated fair value is based on assumptions, mainly related to the total estimated harvest area, expected productivity, average price of sales, and exchange rate.

Due to the assumptions used in estimated the fair value of biological assets have a significant risk of resulting in a material adjustment to the financial statements, we consider this a significant matter for our audit.

Our audit procedures included, but were not limited to:

Evaluation, with the assistance of our corporate finance experts, of theassumptions used to determine the fair value of biological assets based oncomparison of assumptions used to estimated the fair value withobservable data market, as well as sensitivity analysis of the significantassumptions used; and

Evaluation of the disclosures in the financial statements regarding thepresentation of relevant information related to this matter.

Based on the audit procedures above summarized, we consider that the balance of biological assets, as well as the respective disclosures, are appropriate, in the context of the financial statements taken as a whole, for the year ended December 31, 2020.

6

KPMG Auditores Independentes, uma sociedade simples brasileira e firma-membro da rede KPMG de firmas-membro independentes e afiliadas à KPMG International Cooperative (“KPMG International”), uma entidade suíça.

KPMG Auditores Independentes, a Brazilian entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

Responsibilities of Management for the Individual and Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of the individual and consolidated financial statements in accordance with Accounting Practices Adopted in Brazil and with International Financial Reporting Standards (IFRS), issued by the International Accounting Standards Board (IASB) and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the individual and consolidated financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company and its subsidiaries or to cease operations, or has no realistic alternative but to do so.

Auditors’ Responsibilities for the Audit of the Individual and Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the individual and consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Brazilian and international standards on auditing will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with Brazilian and international standards on auditing, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

– Identify and assess the risks of material misstatement of the individual and consolidated financial statements,whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain auditevidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a materialmisstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion,forgery, intentional omissions, misrepresentations, or the override of internal control.

– Obtain an understanding of internal control relevant to the audit in order to design audit procedures that areappropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of theCompany’s internal control.

– Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates andrelated disclosures made by management.

– Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based onthe audit evidence obtained, whether a material uncertainty exists related to events or conditions that may castsignificant doubt on the Company and its subsidiaries’ ability to continue as a going concern. If we conclude thata material uncertainty exists, we are required to draw attention in our auditors’ report to the related disclosures inthe individual and consolidated financial statements or, if such disclosures are inadequate, to modify ouropinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors’ report.However, future events or conditions may cause the Company and its subsidiaries to cease to continue as a goingconcern.

– Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, andwhether the individual and consolidated financial statements represent the underlying transactions and events ina manner that achieves fair presentation.

– Obtain sufficient appropriate audit evidence regarding the financial information of the entities or businessactivities within the Group to express an opinion on the consolidated financial statements. We are responsiblefor the direction, supervision and performance of group audit. We remain solely responsible for our auditopinion.

7

KPMG Auditores Independentes, uma sociedade simples brasileira e firma-membro da rede KPMG de firmas-membro independentes e afiliadas à KPMG International Cooperative (“KPMG International”), uma entidade suíça.

KPMG Auditores Independentes, a Brazilian entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity.

We communicate with management among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

Ribeirão Preto, March 08, 2021

KPMG Auditores Independentes CRC 2SP-027611/F

Fernando Rogério Liani Accountant CRC 1SP229193/O-2

8

André Maggi Participações S.A. (Amaggi)

Statements of financial position

Years ended December 31, 2020 and 2019

(In thousands of US Dollars)

Assets Note 2020 2019 2020 2019 Liabilities Note 2020 2019 2020 2019

Cash and cash equivalents 9 472,487 180,657 11 21 Accounts payable to suppliers 21 403,258 274,421 - 2 Marketable securities 10 399,818 404,825 - - Loans and financing 22 932,123 556,414 - - Trade accounts and others receivables 11 146,916 283,465 - - Advances from customers 23 186,890 64,426 - - Leases receivable 1,817 1,212 - - Taxes payable 6,175 11,599 2 2 Inventories 12 604,826 470,168 - - Current taxes liabilities 11,023 25,939 - - Biological assets 13 187,295 189,319 - - Salaries and vacation payable 28,683 29,087 5 7 Advances to suppliers 14 541,980 345,364 - - Derivative financial instruments 25 1,129,485 148,039 - - Recoverable taxes 15 69,275 84,812 - - Securities brokerage operations 3,618 679 - - Current taxes assets 16 24,384 30,933 - - Leases payable 24 885 2,511 - - Loans granted 17 7 37,764 - - Dividends payable 30,311 25,548 30,046 25,380 Securities brokerage operations 408,332 56,479 - - Others accounts payable 22,879 9,235 250 347 Derivative financial instruments 25 1,174,011 134,921 - - Total current liabilities 2,755,330 1,147,898 30,303 25,738 Prepaid expenses 13,663 37,540 2 5 Other credits 1,776 6,846 - - Accounts payable to suppliers 21 - 46,125 - - Non-current assets held for sale 4,448 - - - Loans and financing 22 1,564,825 1,595,716 - - Total current assets 4,051,035 2,264,305 13 26 Advances from customers 23 - 181 - -

Taxes payable 510 4,213 - - Marketable securities 10 8,094 9,676 - - Derivative financial instruments 25 88,570 14,082 - - Trade accounts and others receivables 11 99,208 38,174 - - Provision for contingencies 26 2,922 3,707 - - Advances to suppliers 14 7,102 4,706 - - Deferred income and social contribution taxes 18 333,058 391,765 - - Recoverable taxes 15 8,082 17,578 - - Leases payable 24 1,869 12,113 - - Current taxes assets 16 766 34,276 - - Total non-current liabilities 1,991,754 2,067,902 - - Loans granted 17 9,644 17,007 - - Derivative financial instruments 25 81,968 38,362 - - Total liabilities 4,747,084 3,215,800 30,303 25,738 Prepaid expenses - 34 - - Other credits 18,600 28,084 - - Equity 28Deferred income and social contribution taxes 18 5,048 364 329 326 Capital 447,583 447,583 447,583 447,583 Biological assets 13 11,181 11,951 - - Legal reserve 50,362 42,455 50,362 42,455 Investments 19 208,803 211,393 1,490,237 1,334,842 Equity valuation adjustments 238,862 241,602 238,862 241,602 Investment properties 17,826 17,826 - - Cumulative translation adjustments (108,873) (85,807) (108,873) (85,807) Property, plant and equipment 20 1,858,905 1,993,882 47 64 Goodwill on capital transactions (483) (483) (483) (483) Intangible assets 19,740 20,577 - - Participation of variation in controlled capital 87,636 87,636 87,636 87,636 Total non-current assets 2,354,967 2,443,890 1,490,613 1,335,232 Profit retention reserve 745,236 576,534 745,236 576,534

Total shareholders' equity 1,460,323 1,309,520 1,460,323 1,309,520

Non-controlling interests 198,595 182,875 - -

Total equity 1,658,918 1,492,395 1,460,323 1,309,520

Total assets 6,406,002 4,708,195 1,490,626 1,335,258 Total equity and liabilities 6,406,002 4,708,195 1,490,626 1,335,258

The notes are an integral part of these financial statements.

Consolidated Company Consolidated Company

9

André Maggi Participações S.A. (Amaggi)

Statements income

Years ended December 31, 2020 and 2019

(In thousands of US Dollars)

Consolidated CompanyNote 2020 2019 2020 2019

Net revenue 29 4,564,686 4,765,255 - - Changes in fair value of biological assets 13 61,061 25,974 - - Cost of goods and services 31 (4,000,351) (4,337,633) - - Gross profit 625,396 453,596 - -

Selling expenses 32 (101,087) (121,653) - - Administrative expenses 33 (89,627) (108,249) (274) (363) Impairment losses of receivables 34 (2,587) (4,563) - -Net other operating income (expenses) 34 (36,409) (9,806) - -Equity interest gain (loss) in subsidiaries 19 6,764 11,477 275,335 131,672 Income from operating activities 402,450 220,802 275,061 131,309

Financial revenues 35 516,383 310,408 - - Financial expenses 35 (526,886) (337,329) - - Exchange rate variation (net) 35 (60,801) 14,242 (2) 8 Net financial income (expenses) 35 (71,304) (12,679) (2) 8

Net income before taxes 331,146 208,123 275,059 131,317

Income tax and social contribution - deferred 18 63,422 (1,007) 3 7 Income tax and social contribution - current 18 (70,691) (46,734) - -

Net income for the year 323,877 160,382 275,062 131,324

Net income for the yearControlling interests 275,062 131,324 275,062 131,324 Non-controlling interests 48,815 29,058 - - Net income for the year 323,877 160,382 275,062 131,324

The notes are an integral part of these financial statements.

10

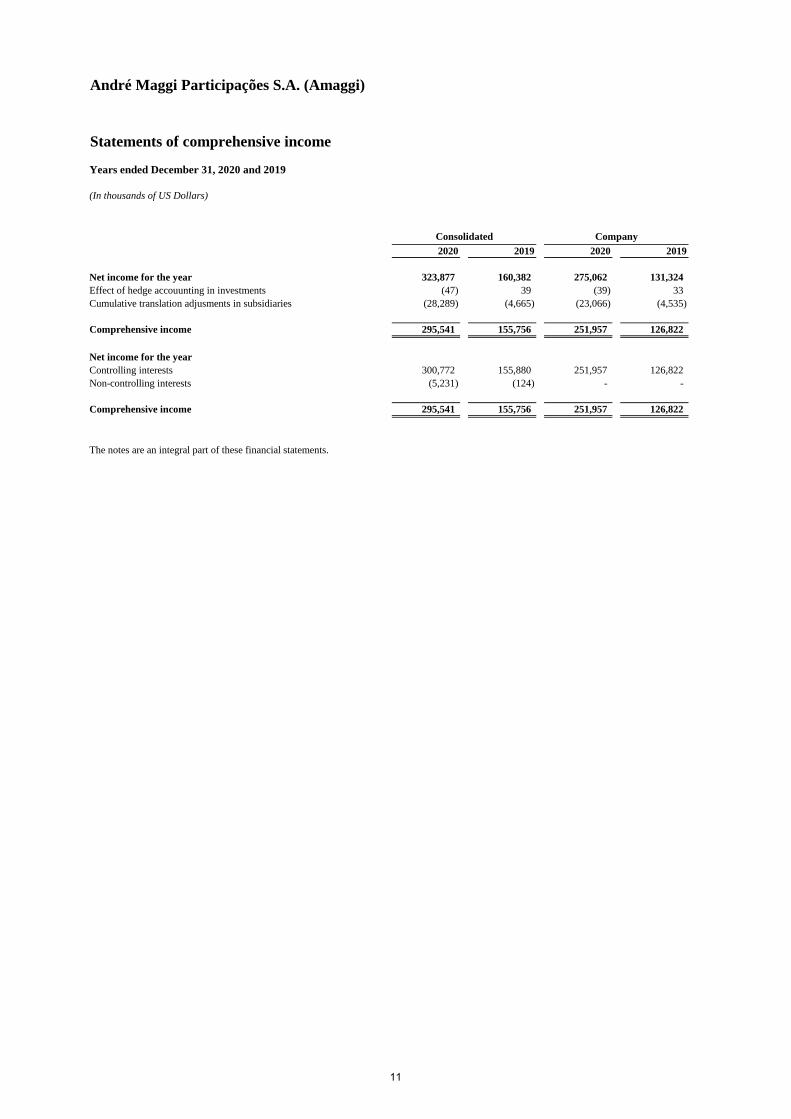

André Maggi Participações S.A. (Amaggi)

Statements of comprehensive income

Years ended December 31, 2020 and 2019

(In thousands of US Dollars)

2020 2019 2020 2019

Net income for the year 323,877 160,382 275,062 131,324 Effect of hedge accouunting in investments (47) 39 (39) 33Cumulative translation adjusments in subsidiaries (28,289) (4,665) (23,066) (4,535)

Comprehensive income 295,541 155,756 251,957 126,822

Net income for the yearControlling interests 300,772 155,880 251,957 126,822 Non-controlling interests (5,231) (124) - -

Comprehensive income 295,541 155,756 251,957 126,822

The notes are an integral part of these financial statements.

Consolidated Company

11

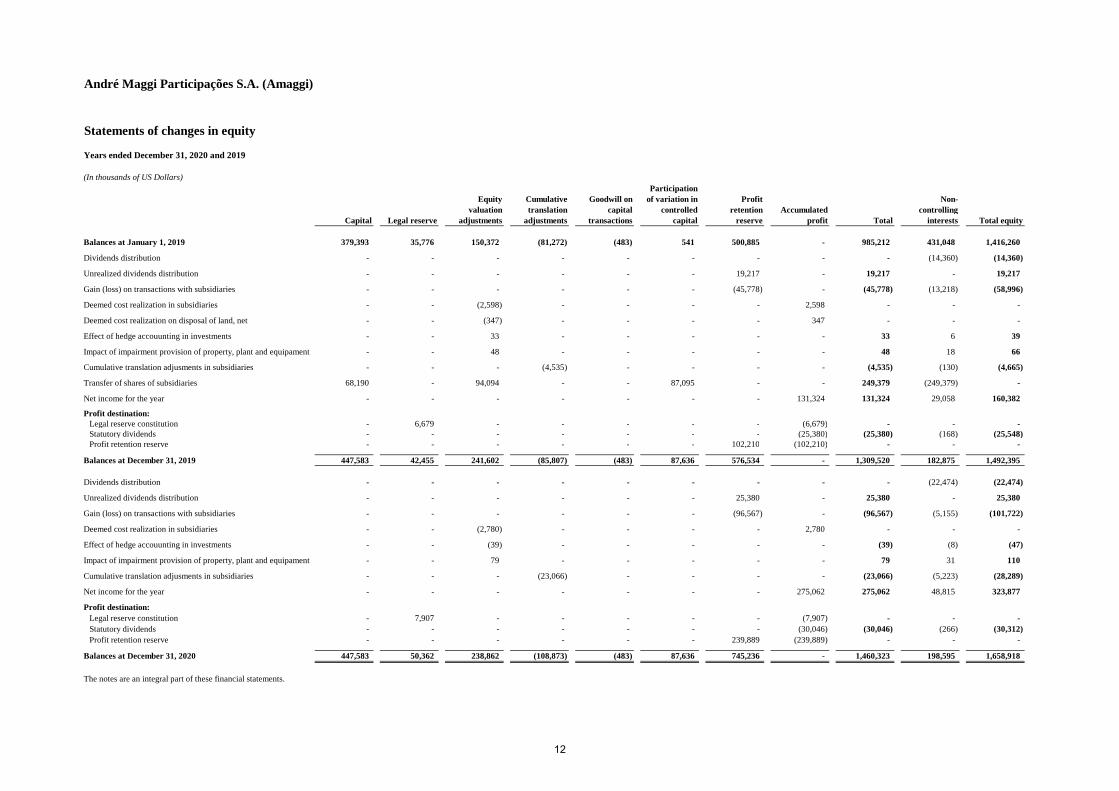

André Maggi Participações S.A. (Amaggi)

Statements of changes in equity

Years ended December 31, 2020 and 2019

(In thousands of US Dollars)

Balances at January 1, 2019 379,393 35,776 150,372 (81,272) (483) 541 500,885 - 985,212 431,048 1,416,260

Dividends distribution - - - - - - - - - (14,360) (14,360)

Unrealized dividends distribution - - - - - - 19,217 - 19,217 - 19,217

Gain (loss) on transactions with subsidiaries - - - - - - (45,778) - (45,778) (13,218) (58,996)

Deemed cost realization in subsidiaries - - (2,598) - - - - 2,598 - - -

Deemed cost realization on disposal of land, net - - (347) - - - - 347 - - -

Effect of hedge accouunting in investments - - 33 - - - - - 33 6 39

Impact of impairment provision of property, plant and equipament - - 48 - - - - - 48 18 66

Cumulative translation adjusments in subsidiaries - - - (4,535) - - - - (4,535) (130) (4,665)

Transfer of shares of subsidiaries 68,190 - 94,094 - - 87,095 - - 249,379 (249,379) -

Net income for the year - - - - - - - 131,324 131,324 29,058 160,382

Profit destination:Legal reserve constitution - 6,679 - - - - - (6,679) - - - Statutory dividends - - - - - - - (25,380) (25,380) (168) (25,548) Profit retention reserve - - - - - - 102,210 (102,210) - - -

Balances at December 31, 2019 447,583 42,455 241,602 (85,807) (483) 87,636 576,534 - 1,309,520 182,875 1,492,395

Dividends distribution - - - - - - - - - (22,474) (22,474)

Unrealized dividends distribution - - - - - - 25,380 - 25,380 - 25,380

Gain (loss) on transactions with subsidiaries - - - - - - (96,567) - (96,567) (5,155) (101,722)

Deemed cost realization in subsidiaries - - (2,780) - - - - 2,780 - - -

Effect of hedge accouunting in investments - - (39) - - - - - (39) (8) (47)

Impact of impairment provision of property, plant and equipament - - 79 - - - - - 79 31 110

Cumulative translation adjusments in subsidiaries - - - (23,066) - - - - (23,066) (5,223) (28,289)

Net income for the year - - - - - - - 275,062 275,062 48,815 323,877

Profit destination:Legal reserve constitution - 7,907 - - - - - (7,907) - - - Statutory dividends - - - - - - - (30,046) (30,046) (266) (30,312) Profit retention reserve - - - - - - 239,889 (239,889) - - -

Balances at December 31, 2020 447,583 50,362 238,862 (108,873) (483) 87,636 745,236 - 1,460,323 198,595 1,658,918

The notes are an integral part of these financial statements.

Total

Non-controlling

interests Total equityLegal reserve

Profit retention

reserveAccumulated

profitCapital

Equity valuation

adjustments

Cumulative translation

adjustments

Goodwill on capital

transactions

Participation of variation in

controlled capital

12

André Maggi Participações S.A. (Amaggi)

Statements of cash flows

Years ended December 31, 2020 and 2019

(In thousands of US Dollars)Company

Note 2020 2019 2020 2019Cash flows from operating activities

Net income for the year 323,877 160,382 275,062 131,324

Adjustment to:Depreciation 20 85,141 79,567 17 17 Amortization 710 1,374 - - Residual cost on disposal of property, plant and equipment 6,283 6,455 - - Residual cost on disposal of intangible 383 - - - Income from sale of property, plant and equipment (4,850) (1,437) - - Deferred taxes 18 (63,422) 1,007 (3) (7) Equity interest gain (loss) in subsidiaries 19 (6,764) (11,477) (275,335) (131,672) Provision for contingencies 64 672 - - Interest incurred on loans and financing 22 99,058 106,883 - - Other financial expenses 6,493 3,739 - - Exchange variation on loans and financing 22 (79,513) (27,943) - - Other exchange variations (18,525) (1,986) 14 (7) Changes in fair value of biological assets 13 (61,061) (25,974) - - Realization of biological assets on cost 31 30,802 24,131 - - Net income of impairment of property, plant and equipment 479 (69) - - Realization of added value on investments 2,204 2,249 - - Income from unrealized derivatives (26,717) 27,217 - - Income tax and social contribution 18 70,691 46,734 - - Credit and market risks, and impairment losses 2,587 4,564 - - Provision (reversion of) for inventory losses 12 5,660 (1,053) - - Net realizable value of inventories 12 (88,149) 9,164 - - Update on land sell receivables 34 (11,803) - - - Tax credits (2,731) (35,389) - - Gains from other investments - (1,768) - -

270,897 367,042 (245) (345) (Increase) decrease on assets

Trade accounts and others receivables 136,821 (76,770) - - Leases receivable (521) 700 - - Inventories (54,395) 103,045 - - Biological assets 33,146 (23,306) - - Advances to suppliers (202,302) 192,317 - - Recoverable taxes (32,556) (31,951) - - Current taxes assets (15,314) (3,691) - - Securities brokerage operations (351,853) (54,038) - - Prepaid expenses 23,911 (34,861) 3 (2) Other credits 4,309 (729) 338 72

Increase (decrease) on liabilitiesAccounts payable to suppliers 157,848 83,425 (2) 2 Advances from customers 122,042 (229,313) - - Taxes payable (4,221) 7,862 - - Salaries and vacation payable 1,966 (2,429) (1) - Securities brokerage operations 2,939 (15,602) - - Leases payable 607 90 - - Other accounts payable 13,990 (5,714) (103) (73)

Cash provided by (utilized in) from operations 107,314 276,077 (10) (346)

Interest paid 22 (95,101) (112,562) - - Taxes paid on profit (2,053) (2,410) - -

Net cash flow provided by (utilized in) operating activities 10,160 161,105 (10) (346)

Cash flow from investing activitiesIncrease on investments (46,299) (51,298) - - Decrease on investments - 16 - - Dividends and interests of own capital received 2,415 4,265 - 356 Proceeds from sale of property, plant and equipment 10,422 3,141 - - Acquisition of property, plant and equipment (54,918) (126,646) - (12) Acquisition of intangible (284) (530) - - Marketable securities 3,682 (16,015) - - Loans granted to related parties 17 (5,009) (17,838) - - Loans received 17 - 3,401 - - Loans received from related parties 17 46,756 17,923 - -

Net cash flow provided by (utilized in) investing activities (43,235) (183,581) - 344

Cash flows from financing activitiesFinancial funding 22 1,598,871 1,641,195 - - Payments of loans and financing 22 (1,161,289) (1,579,310) - - Payments of loans and financing to related parties 22 (936) (6,327) - -

Payments of lease liabilities (1,309) (2,294) - - Payments of lease liabilities to related parties (185) (293) - -

Transaction costs related to loans and financing 22 (2,208) (3,380) - - Dividends paid (87,554) (70,724) - -

Net cash flow provided by (utilized in) financing activities 345,390 (21,133) - -

Increase (decrease) in cash and cash equivalents 312,315 (43,609) (10) (2)

Statements of increase (decrease) in cash and cash equivalentsCash and cash equivalents on January 1 9 158,686 202,295 21 23 Increase (decrease) in cash and cash equivalents 312,315 (43,609) (10) (2)

Cash and cash equivalents on December 31 9 471,001 158,686 11 21

The notes are an integral part of these financial statements.

Consolidated

13

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

Notes to the financial statements

(In thousands of U.S. Dollars)

1. Reporting entity

André Maggi Participações S.A., hereinafter referred to as “Company”, and its subsidiaries,jointly designated in this report as "Amaggi", is composed by many entities that act in differentsegments of the economy: commodities trading, agriculture, grains crushing, fluvialtransportation, electric power generation and administration of ports.

Company operational headquarters is located in André Antônio Maggi Avenue, 303, City ofCuiabá, State of Mato Grosso. Its operations are located in Brazil, Argentina and Paraguay.

These consolidated financial statements comprise the Company and its subsidiaries (togetherreferred to as the “Amaggi”).

André Maggi Participações S.A. is a holding and its operations consists in investing directly inAmaggi Exportação e Importação Ltda. and Agropecuária Maggi Ltda.

a. Considerations concerning COVID-19

At March 11, 2020, the World Health Organization (WHO) declared the outbreak of COVID-19 as a pandemic, leading government authorities worldwide to impose restrictions to contain the spread of the virus. Such restrictions have had significant impacts on the global economy.

In Brazil, as all over the world, the government authorities implemented several measures to prevent and contain the pandemic, as well as to mitigate the respective impacts on economy.

The Company management did not identify significant impacts on its operations, maintaining its production forecasts and sales. The agribusiness production chain is considered an essential activity and the operation was not stopped during the isolation period.

Government assistance measure

Government authorities implemented several economic and financial assistance measures to prevent and contain the pandemic, with the purpose of mitigate the respective impacts on economy. One of the measures adopted in operations was the suspension of the term for payment of taxes and federal contributions.

The Company has been monitoring and analyzing the measures taken by government to mitigate the crisis impacts.

Company’s adopted measures

The Company adopted several measures and protocols to preserve the safety of all people involved in its operational context, following the orientations of local and international health authorities.

14

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

Also in March, the Company created the Crisis Committee for COVID-19 to continuously assess the general situation, update preventive measures and risk minimization actions, as well as to coordinate the execution of actin plans. Among the actions taken, the main ones were:

• Distribution of gel alcohol in all areas of the company;

• Intensification of hygiene and cleaning, in addition to hiring a company to perform sanitization on the Company's facilities, in case of a positive result COVID-19;

• Suspension of travel, events and training, adopting electronic means of communication;

• Work at home for administrative areas;

• Increase in the number of buses and disinfection of these vehicles with 70º alcohol;

• Temperature measurement of employees and third parties;

• Access control to the facilities, by sending a prior checklist;

• Work leave for employees over 60, pregnant women, young apprentices and interns;

• Distribution of reusable masks to employees;

• Reinforcement of communication to guide and comply with containment measures, such as posters, communicated via e-mail and guidance by the leaders;

• Acquisition of rapid tests for COVID-19.

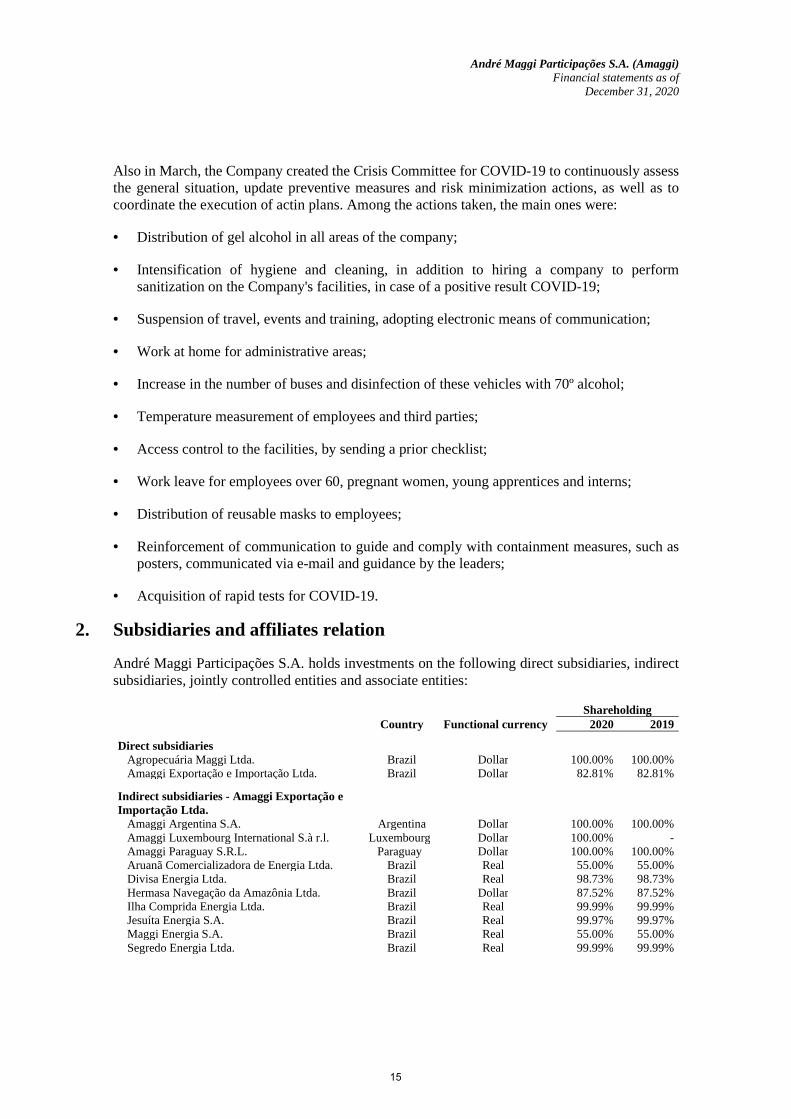

2. Subsidiaries and affiliates relation

André Maggi Participações S.A. holds investments on the following direct subsidiaries, indirect subsidiaries, jointly controlled entities and associate entities:

Shareholding Country Functional currency 2020 2019

Direct subsidiaries Agropecuária Maggi Ltda. Brazil Dollar 100.00% 100.00% Amaggi Exportação e Importação Ltda. Brazil Dollar 82.81% 82.81%

Indirect subsidiaries - Amaggi Exportação e Importação Ltda.

Amaggi Argentina S.A. Argentina Dollar 100.00% 100.00% Amaggi Luxembourg International S.à r.l. Luxembourg Dollar 100.00% - Amaggi Paraguay S.R.L. Paraguay Dollar 100.00% 100.00% Aruanã Comercializadora de Energia Ltda. Brazil Real 55.00% 55.00% Divisa Energia Ltda. Brazil Real 98.73% 98.73% Hermasa Navegação da Amazônia Ltda. Brazil Dollar 87.52% 87.52% Ilha Comprida Energia Ltda. Brazil Real 99.99% 99.99% Jesuíta Energia S.A. Brazil Real 99.97% 99.97% Maggi Energia S.A. Brazil Real 55.00% 55.00% Segredo Energia Ltda. Brazil Real 99.99% 99.99%

15

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

Shareholding Country Functional currency 2020 2019 Indirect subsidiaries - Agropecuária Maggi Ltda.

Amaggi Pecuária Ltda. Brazil Real 91.24% 91.24% Companhia Agrícola do Parecis - CIAPAR Brazil Dollar 100.00% 100.00%

Jointly controlled entities Amaggi Louis Dreyfus Zen-Noh Holdings S.A. Brazil Dollar 33.33% 33.33% Carguero Inovação Logística e Serviços S.A. Brazil Real 50.00% 50.00% Navegações Unidas Tapajós S.A. Brazil Dollar 50.00% 50.00% Rio Madeira Administração de Bens Ltda. Brazil Real 50.00% 50.00%

Associates Terminal de Granéis do Guarujá S.A. Brazil Real 33.00% 33.00%

Agropecuária Maggi Ltda.

It’s a limited entity domiciled in the city of Cuiabá, state of Mato Grosso, Brazil. Its activities consist on the production and commercialization of agricultural products, mainly soybean, corn and cotton and seeds production and processing.

Amaggi Exportação e Importação Ltda.

It’s a limited entity domiciled in the city of Cuiabá, state of Mato Grosso, Brazil and its main objectives are the commodities trading, mainly soybean exportation, seed processing, fertilizers importation and commercialization, extraction and commercialization of crude and degummed soybean oil and soybean meal. Substantial part of its exportation is performed through Amaggi International Ltd.

Amaggi Argentina S.A.

Headquarters and operations are located in the city of Buenos Aires, state of Buenos Aires, Argentina. Its activities consist in the trading of soybean, corn, wheat, sorghum and barley.

Amaggi Luxembourg International S.à r.l.

Headquarters and operations are located in the city of Luxembourg, Luxembourg. The constitution of the company occurred on December 2020 and its main activity consists in the issuance of representative debt securities.

Amaggi Paraguay S.R.L.

Headquarters and operations are located in the city of Ciudad del Este, state of Alto Paraná, Paraguay. Its activities consist in the trading of soybean, corn and wheat.

Aruanã Comercializadora de Energia Ltda.

Headquarters and operations are located in the city of Cuiabá, state of Mato Grosso, Brazil. Its activities consists is the trading of electric power.

16

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

Divisa Energia Ltda.

Headquarters is located in the city of Cuiabá, state of Mato Grosso, Brazil, but its activities are located in the city of Campos de Júlio, state of Mato Grosso, Brazil. Its activities consist in the electric power generation and commercialization in Brazil’s territory, with the authorization of the competent legal authorities.

Hermasa Navegação da Amazônia Ltda.

Headquarters is located in the City of Cuiabá, state of Mato Grosso, Brazil, but its activities are located in the Brazilian states of Rondônia, Amazonas and Pará. Its activities consists, mainly, is the rendering of services of fluvial navigation, transportation, storage and transshipment of grains, substantially to related parties.

Ilha Comprida Energia Ltda.

Headquarters is located in the city of Cuiabá, state of Mato Grosso, Brazil, but its activities are located in the city of Sapezal, state of Mato Grosso, Brazil. Its activities consist in the electric power generation and commercialization in Brazil’s territory, with the authorization of the competent legal authorities.

Jesuíta Energia S.A.

Headquarters is located in the city of Cuiabá, state of Mato Grosso, Brazil. Its activities consists is the electric power generation and commercialization in Brazil’s territory, with the authorization of the competent legal authorities. The Company is on stage of review of its basic project approved.

Maggi Energia S.A.

Headquarters is located in the city of Cuiabá, state of Mato Grosso, Brazil, but its activities are located in the city of Sapezal, state of Mato Grosso, Brazil. Its activities consist in the electric power generation and commercialization in Brazil’s territory, with the authorization of the competent legal authorities.

Segredo Energia Ltda.

Headquarters is located in the city of Cuiabá, state of Mato Grosso, Brazil, but its activities are located in the city of Sapezal, state of Mato Grosso, Brazil. Its activities consist in the electric power generation and commercialization in Brazil’s territory, with the authorization of the competent legal authorities.

Amaggi Pecuária Ltda.

Headquarters is located in the city of Cuiabá, state of Mato Grosso, Brazil. Its activities consist in the activity of livestock in the purchase and resale, breeding of cattle and breeding animals in semi-confinement and confinement for cutting.

Companhia Agrícola do Parecis - CIAPAR

Headquarters is located in the city of Campo Novo do Parecis, state of Mato Grosso, has by

17

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

purpose the production and commercialization of agricultural products, however, discontinued its activity of agricultural production, and currently leases a significant area of its arable lands to parent company Agropecuária Maggi Ltda., which has become its main source of revenue.

Carguero Inovação Logística e Serviços S.A.

It is a joint venture in conjunction with Louis Dreyfus Company Brasil S.A., headquarters are located in the city of São Paulo, state of São Paulo. Its activities consists in development and licensing of digital platforms (software’s) for control and management of multimodal transports of freight, freight’s agency and operations.

Amaggi Louis Dreyfus Zen-Noh Holdings S.A.

It’s a joint venture in conjunction with Louis Dreyfus Company Brasil S.A. and Zen-Noh Grain Brasil Holdings Ltda., headquarters and operations are located in the city of São Paulo, state of São Paulo, Brazil. Its activities consists mainly of investments in others entities with own resources.

Navegações Unidas Tapajós S.A.

It’s a joint venture with Bunge Alimentos S.A., headquarters is located Cuiabá, state of Mato Grosso, Brazil. Its activities consists mainly at rendering of services of fluvial navigation and port operations for handling dry bulk cargo.

Rio Madeira Administração de Bens Ltda.

It’s controlled in conjunction with Nilto Costa Alves, and headquarters are located in the city of São Paulo, state of São Paulo, Brazil but its operations are located in the city of Porto Velho, state of Rondônia, Brazil. Its activities consist in the trading and administration of land.

Terminal de Granéis do Guarujá S.A.

Headquarters and operations are located in the city of Guarujá, state of São Paulo, Brazil. It operates as a marine terminal to receive, store and load grains (corn, soybeans and their sub products).

3. Basis of preparation

a. Statement of compliance

The financial statements have been prepared in accordance with International Financial Reporting Standards - IFRS issued by the International Accounting Standards Board - IASB.

The financial statements, accompanied by the independent auditor’s report were authorized for issuance by the Board of Directors on March 05, 2021. After issuance, only shareholders may change the financial statements.

Details of the Company and its subsidiaries significant accounting policies are presented in note 6.

18

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

All the relevant information to the financial statements, and only them, are being disclosure, and correspond to those used by Administration in its management.

b. Basis of measurement

The financial statements have been prepared based on the historical cost basis except for the following items which are measured on an alternative basis on each reporting date:

• Derivative financial instruments measured at fair value;

• Non-derivative financial instruments measured at fair value through profit or loss;

• Biological assets measured at fair value less expenses to sell; and

• Inventories of commodities of trading companies which are evaluated at marked values less selling expenses.

4. Functional currency

The Company's management after analysis of their operations and business, especially with regard to the factors to determine its functional currency, concluded that the US Dollar ("US$" or "Dollars") is its functional currency. This conclusion is based on the analysis of the following indicators:

• Currency that most influences the prices of goods and services marketed by the Company;

• Currency of the country whose competitive forces and regulations mainly determine the selling price of its products and services;

• Currency that most materially influence the material and other costs of providing goods or services; and

• Currency in which they are obtained substantially funds from financing activities.

5. Use of estimates and judgments

In the preparation of these financial statements, management has made judgments, estimates and assumptions that affect the application of the Company and its subsidiaries accounting policies and reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates.

Estimates and assumptions are reviewed on an ongoing basis. Reviews of accounting estimates are recognized prospectively.

a. Judgments

Information about judgments made in applying accounting policies that have the most significant effect on the amounts recognized in the financial statements are included in the following notes:

• Note 2 and 6.a - Consolidation: determining whether the Company and its subsidiaries has the control about on investee; and

19

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

• Note 6.o - Lease: determining whether an arrangement contains a lease.

b. Assumptions and estimation uncertainties

Information about uncertainties on assumptions and estimates that have a significant risk of resulting in a material adjustment within the next financial year are included in the following notes:

• Note 6.i and 13 - Determining the fair value of biological assets on the basis of significant unobservable inputs;

• Note 18.a - Deferred tax assets: availability of future taxable profit against which tax losses carried forward can be utilized;

• Note 19 - Determining goodwill on investments: main assumptions regarding recoverable amounts;

• Note 19 - Impairment test of intangible assets and goodwill: key assumptions underlying recoverable amounts, including the recoverability;

• Note 20 - Useful life of property, plant and equipment: expected use of the asset under certain conditions of use;

• Note 25 - Determination of fair value of derivative financial instruments: sensitivity of the model to inputs and observable assumptions; and

• Note 26 - Provisions for contingencies: main assumptions about the probability and magnitude of outflows.

6. Significant accounting policies

The accounting policies set out below have been applied consistently to all periods reported in these consolidated and individual financial statements.

a. Basis of consolidation

(i) Controlled entities

The Company and its subsidiaries control another entity when is exposed, or have the rights, on the variable income if this entity and has the ability to affect this income exercising its power over the entity. The financial statements of controlled entities are included in the consolidated financial statements from the date the control begins and they are maintained until the date the control no longer exists.

In the Company's individual financial statements, the financial information of subsidiaries is recognized using the equity method.

(ii) Investments in associates and joint ventures

Associates are those entities in which the Company and its subsidiaries, directly or indirectly, has significant influence, but not control, over the financial and operating policies.

20

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

Jointly ventures are those entities whose activities the Company and its subsidiaries have joint control, established by contractual agreements and requiring unanimous consent on the strategic financial and operating decisions.

The investments on associates and joint ventures are accounted by equity method on the consolidated and individual financial statements and are initially recognized by cost plus transaction costs. After initial recognition, consolidated financial statements include the participation on profit or loss and other comprehensive income of the investee until the date that significant influence or shared control exists.

The consolidated financial statements include the profit or loss and other comprehensive income of equity accounted investees, after adjustments to align its accounting policies with those of the Company and its subsidiaries, from the date that significant influence or joint control begins until the date that significant influence or joint control ceases.

When the Company and its subsidiaries share of losses exceeds its interest in an equity-accounted investee, the carrying amount of the investment, including any long-term interests that form part thereof, is reduced to zero, and the recognition of further losses is discontinued except to the extent that the Company and its subsidiaries have an obligation or has made payments on behalf of the investee.

(iii) Transactions eliminated on consolidation

Intragroup balances and transactions, and any unrealized profit or loss arising from intragroup transactions, are eliminated during the preparation of the consolidated financial statements.

Unrealized gains arising from transactions with equity-accounted investees are eliminated against the investment on the extent of the Company and its subsidiaries interest in the investee.

Unrealized losses are eliminated in the same way as unrealized gains, but only to the extent that there is no evidence of impairment.

(iv) Business combination

Business combinations are recorded using the acquisition method when control is transferred to the Company and its subsidiaries. The consideration transferred is generally measured at fair value, as well as identifiable net assets acquired. Any goodwill arising in the transaction is tested annually for impairment. Gains on an advantageous purchase are recognized immediately in the result. The transaction costs are recorded in the income statement as incurred, except for costs related to the issuance of debt or equity instruments.

b. Foreign currency

Foreign currency transactions

Transactions in foreign currency (other than the functional currency), are translated into the respective functional currency of the Company and its subsidiaries at exchange rates in the dates of the transactions.

Monetary assets and liabilities denominated in foreign currencies at the reporting date are translated into the functional currency at the exchange rate at that date.

21

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

Non-monetary assets and liabilities denominated in foreign currencies that are measured at fair value are translated into the functional currency at the exchange rate at the date that the fair value was determined. Foreign currency differences are generally recognized in profit or loss.

c. Financial instruments

(i) Recognition and initial measurement

The trade account receivable and debt securities issued are initially recognized when they are originated. All other financial assets and liabilities are recognized initially when the Company and its subsidiaries becomes part of the contractual provisions of the instrument.

A financial asset (unless it is a trade receivable do not contain a significant financing component) or financial liability at its fair value plus, in the case of a financial asset or financial liability not at fair value through profit or loss, transaction costs that are directly attributable to the acquisition or issue of the financial asset or financial liability. A trade receivable that does not contain a significant financing component is initial recognized by its transaction price.

(ii) Classification and subsequent measurement

Financial instrument

After initial recognition, financial asset is classified as measured: amortized cost, fair value through other comprehensive income (FVOCI) - for debt instrument, fair value through other comprehensive income (FVOCI) - for equity instrument; or fair value through profit or loss (FVTPL).

The financial assets are not subsequent reclassified to their initial recognition unless the Company changes its business model for managing financial assets, in which case all financial assets affected are reclassified on the first day of the reporting period after the change in the business model.

A financial asset is measure by amortized cost if attend both conditions below and not be designated as fair value through profit or loss (FVTPL):

• Is maintained within a business model whose purpose is to maintain financial assets to receive cash flows; and

• Their contractual terms generate, at specific dates, cash flows that are only related to the payment of principal and interest on the outstanding principal amount.

A debt instrument is measure by fair value through other comprehensive income (FVOCI) if attend both conditions below and not be designed as fair value through profit or loss (FVTPL):

• It is held within a business model whose purpose is to hold financial assets to collect contractual cash flows; and

• Their contractual terms generate, at specific dates, cash flows that are only related to the payment of principal and interest on the outstanding principal amount.

In the initial recognition of an investment in an equity instrument that is not held for trading, the

22

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

Entity may irrevocably choose to present subsequent changes in the fair value of the investment in other comprehensive income. This option is realized investment by investment.

All financial assets not classified as measured at amortized cost or to fair value through other comprehensive income (FVOCI), as described above, are classified as fair value through profit or loss (FVTPL). This includes all derivative financial assets. On initial recognition, the Company and its subsidiaries may irrevocably designate a financial asset that otherwise meets the requirements to be measured at amortized cost, to the fair value through other comprehensive income (FVOCI) and to the fair value through profit or loss (FVTPL) if this eliminates, or significantly reduces an accounting mismatch that would otherwise arise.

Financial instruments - Business model evaluation

The Company and its subsidiaries realize an assessment of the objectives of business's model which a financial asset is held in portfolio because it reflect the best way that the business is manage and the information are provided to the management. Information considered include:

• The policies and objectives set out for the portfolio and the practical operation of these policies. They include the question of whether management's strategy focuses on obtaining contractual interest income, maintaining a certain interest rate profile, matching the duration of financial assets with the duration of related liabilities or expected outflows of cash, or the realization of cash flows through the sale of assets;

• The form that the portfolio performance is assessed and reported to Company and its subsidiaries management;

• The risks that affect the performance of the business model (and the financial asset held in that business model) and the way those risks are managed;

• The form that the key management personnel are remunerated - for example, whether the compensation is based on the fair value of the assets managed or the contractual cash flows obtained; and

• The frequency, volume and timing of sales of financial assets in prior periods, the reasons for such sales and their expectations about future sales.

Transfers of financial assets to third parties in transactions that do not qualify for derecognition are not considered sales, consistent with the continued recognition of Company and its subsidiaries assets.

Financial assets held for trading or managed with performance measured at fair value are measure at fair value through profit or loss.

Financial assets - Evaluation from contract cash flow are exclusive payment of principal and interest

For the purposes of this valuation, the 'principal' is defined as the fair value of the financial asset at the initial recognition. 'Interest' is defined as a consideration for the time value of money and for the credit risk associated with the principal amount outstanding over a given period of time and for the other underlying risks and costs of borrowing (for example, liquidity risk and costs administrative costs), as well as a profit margin.

23

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

The Company and its subsidiaries consider the contractual terms of the instrument to assess if contractual cash flows are only principal and interest payments. This includes assessing whether the financial asset contains a contractual term that could change the timing or value of the contractual cash flows so that it would not meet that condition. In making this assessment, the Company and its subsidiaries considers:

• Contingent events that modify the value or timing of cash flows;

• terms that may adjust the contractual rate, including variable rates;

• prepayment and extension of the term; and

• Terms that limit the Company and its subsidiaries access to cash flows of specific assets (for example, based on the performance of an asset).

Financial assets - Subsequent measure and gains and losses

Financial assets at fair value through profit or loss (FVTPL)

These assets are measure subsequently at fair value. Net income, including interest or dividend income, is recognized in income.

Financial assets at amortized cost

These assets are measure subsequently at amortized cost using the effective interest method. The amortized cost is reduced by impairment losses. Interest income, the gains and losses of foreign exchange and impairment are recognize in the income statement. Any gain or loss on derecognition is recognized in profit or loss.

Debt instrument at fair value through other comprehensive income (FVOCI)

These assets are measure subsequently at fair value. Interest income calculated using the effective interest method, foreign exchange gains and losses and impairment are recognize in the income statement. Other net results are recognize in other comprehensive income (OCI). In derecognition, the accumulated result in other comprehensive income (OCI) is reclassified to the result.

Equity instrument at fair value through other comprehensive income (FVOCI)

These assets are measure subsequently at fair value. Dividends are recognize as a gain in profit or loss, unless the dividend represents a clear recovery of part of the cost of the investment. Other net income is recognize in other comprehensive income (OCI) and is never reclassified to income.

Financial liabilities - Classification, subsequent measure of gains and losses

Financial liabilities were classified as measured at amortized cost or to fair value though profit or loss (FVTPL). A financial liability is classified as measured at fair value through profit or loss if it is classified as held for trading, is a derivative or is designated as such at initial recognition. Financial liabilities measured at fair value though profit or loss (FVTPL) are measure at fair value and net income, including interest, is recognize in income. Other financial liabilities are measure subsequently at amortized cost using the effective interest method. Interest expense, exchange gains and losses are recognized in income. Any gain or loss on derecognition is also recognized in profit or loss.

24

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

(iii) Derecognition

Financial assets

The Company and its subsidiaries derecognizes a financial asset when the contractual rights to the asset's cash flows expire, or when the Company and its subsidiaries transfers contractual receivables to the contractual cash flows on a financial asset in a transaction in which substantially all the risks and benefits of ownership of the financial asset are transferred or in which the Company and its subsidiaries neither transfers nor maintains substantially all the risks and rewards of ownership of the financial asset and also does not retain control over the financial asset.

The Company and its subsidiaries carries out transactions in which it transfers recognized assets in the balance sheet, but maintains all or substantially all the risks and benefits of the transferred assets. In such cases, financial assets are not derecognized.

Financial liabilities

The Company and its subsidiaries derecognize financial liability when its contractual obligation is withdrawn, canceled or expired. The Company and its subsidiaries also derecognize a financial liability when the terms are modified and the cash flows of the modified liability are substantially different, in which case a new financial liability based on the modified terms is recognize at fair value.

In derecognition of a financial liability, the difference between the extinct book value and the consideration paid (including transferred assets that do not transit through the cash or assumed liabilities) is recognize in the income statement.

(iv) Financial instruments

The Company and its subsidiaries hold derivative financial instruments to hedge its foreign currency, interest rate risk exposures and commodity price.

The purpose of operations involving derivatives is always related to the operation of the Company and its subsidiaries and the reduction of their exposure to currency and market risks, duly identified by established policies and guidelines. The results obtained with these operations are consistent with the policies and strategies defined by the Company and its subsidiaries. All gains or losses arising from derivative financial instruments are recognized at fair value.

Derivatives are initially measured at fair value. Subsequent to initial recognition, derivatives are measured at fair value, and changes therein are generally recognized in profit or loss.

d. Capital

The Company share capital is composed only of common shares which are classified as shareholders' equity.

e. Earnings per share

Basic earnings per share are calculated based on the income for the year attributable to the Company's controlling shareholders and the weighted average of outstanding common shares in the respective year. The diluted earnings per share are calculated based on the mentioned average

25

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

of outstanding shares, adjusted by instruments that can potentially be converted into shares, with a dilution effect, in the years presented, pursuant to IAS 33 - Earnings per share.

f. Property, plant and equipment

(i) Recognition and measurement

Items of property, plant and equipment are measured at cost of acquisition or construction less accumulated depreciation and accumulated losses by impairment.

The cost of certain items of property as of January 1, 2008, anticipated date of the Company and its subsidiaries transition to the pronouncements of the IFRS was determined based on its fair value at that date.

Cost includes disbursements that are directly attributable to the acquisition of the asset. The cost of self-constructed assets includes the following:

• The cost of materials and direct labor;

• Any other costs directly attributable to bring the assets to a working condition for their intended use by management;

• Dismantling costs and the costs to restore the site on which the assets are located; and

• Capitalized borrowing costs on qualifying assets.

Purchased software that is an integrant part of the functionality of equipment is capitalized as part of that equipment.

When parts of an item of property, plant and equipment have different useful life, they are accounted for as separate items (major components) of property, plant and equipment.

Gains and losses on the disposal of an item of property, plant and equipment (the difference between the amount of the disposal and the carrying amount), are recognized in “net other operating income (expense)” in the “statements of comprehensive income”.

(ii) Subsequent costs

Subsequent costs are capitalized only when it is probable that the future economic benefits associated with the costs will flow to the Company and its subsidiaries. Ongoing repairs and maintenance are expensed as incurred.

(iii) Depreciation

Items of property, plant and equipment are depreciated on a straight-line basis in profit or loss over the estimated useful lives of each component. Land is not depreciated.

Items of property, plant and equipment are depreciated from the date that they are installed and are ready for use, or in respect of internally constructed assets, from the date that the asset is completed and ready for use.

26

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

Depreciation methods, useful lives and residual amounts are reviewed at each reporting date and eventual adjustments are recorded as changes in accounting estimates.

g. Impairment

(i) Non derivative financial assets

Financial instruments and contract assets

The Company and its subsidiaries recognize loss allowances for expected credit losses on:

• Financial assets measured at amortized cost; and

• Contract assets.

The Company and its subsidiaries measures loss allowances at an amount equal to lifetime expected credit losses, except for the following, which are measured at 12 months expected credit losses:

• Debt securities that are determined to have low credit risk at the reporting date; and

• Other debt securities and bank balances for which credit risk (i.e. the risk of default occurring over the expected life of the financial instrument) has not increased significantly since initial recognition.

Loss allowances for trade receivables and contract assets are always measured at an amount equal to lifetime expected credit losses.

When determining whether the credit risk of a financial asset has increased significantly since initial recognition and when estimating expected credit losses, the Company and its subsidiaries considers reasonable and supportable information that is relevant and available without undue cost or effort. This includes both quantitative and qualitative information and analysis, based on the Company and its subsidiaries historical experience and informed credit assessment and including forward-looking information.

Measurement of expected credit losses

Expected credit losses are a probability-weighted estimate of credit losses. Credit losses are measured as the present value of all cash shortfalls (i.e. the difference between the cash flows due to the Company and its subsidiaries in accordance with the contract and the cash flows that the Company and its subsidiaries expects to receive). Expected credit losses are discounted at the effective interest rate of the financial asset.

Financial assets with recovery problems

At each reporting date, the Company and its subsidiaries assesses whether financial assets carried at amortized cost and debt securities at fair value through other comprehensive income (FVOCI) are credit-impaired. A financial asset is “credit-impaired” when one or more events that have a detrimental impact on the estimated future cash flows of the financial asset have occurred. Evidence that a financial asset is credit-impaired includes the following observable data:

27

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

• Significant financial difficulty of the borrower or issuer;

• A breach of contract such as a default;

• The restructuring of a loan or advance by the Company and its subsidiaries in terms that would not be accepted under normal conditions;

• It is probable that the borrower will enter bankruptcy or other financial reorganization; or

• The disappearance of an active market for a security because of financial difficulties.

Presentation of allowance for expected credit loss in the statement of financial position

Loss allowances for financial assets measured at amortized cost are deducted from the gross carrying amount of the assets, for debt securities at fair value through other comprehensive income (FVOCI), the loss allowance is charged to profit or loss and is recognized in other comprehensive income (OCI).

(ii) Non-financial assets

At each reporting date, the Company reviews the carrying amounts of its non-financial assets (other than biological assets, investment property, inventories, contract assets and deferred tax assets) to determine whether there is any indication of impairment. If any such indication exists, then the asset’s recoverable amount is estimated. Goodwill is tested annually for impairment. For impairment testing, assets are grouped together into the smallest group of assets that generates cash inflows from continuing use that are largely independent of the cash inflows of other assets or CGUs. Goodwill arising from a business combination is allocated to CGUs or groups of CGUs that are expected to benefit from the synergies of the combination. The recoverable amount of an asset or CGU is the greater of its value in use and its fair value less costs to sell. Value in use is based on the estimated future cash flows, discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset or CGU. An impairment loss is recognized if the carrying amount of an asset or CGU exceeds its recoverable amount. Impairment losses are recognized in profit or loss. They are allocated first to reduce the carrying amount of any goodwill allocated to the CGU, and then to reduce the carrying amounts of the other assets in the CGU on a pro rata basis. An impairment loss in respect of goodwill is not reversed. For other assets, an impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortization, if no impairment loss had been recognized.

28

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

h. Inventories

Commodities of trading companies are adjusted to the market value (“mark to market”) less costs to sell. In order to perform the calculation of the fair value, trading companies use as reference the quotations and rates published by public sources that are related to the products and active markets in which the Company and its subsidiaries acts. Changes in the fair value of inventories are recognized in cost.

Other inventories are measured at the lower of cost and net realizable value. The cost of inventories is based on the moving weighted average. In the case of manufactured inventories and work in progress cost includes an appropriate share of production overheads based on normal operating capacity.

The cost of biological assets transferred to inventories is its fair value less expenses to sell at the date of harvest.

i. Biological assets

Biological assets are measured at fair value less costs to sell. Changes on fair value less costs to sell are recognized in profit or loss. Costs to sell include all costs that would be necessary to sell the assets, including transportation costs.

j. Advances to suppliers

The advances to suppliers with prices to be determined are update in accordance with the rates defined in the purchase agreement. Other advances are maintained by their original amount.

k. Short-term employee benefits

Short-term employee benefits obligations are measured on an undiscounted basis and are expensed as the related service is rendered. A liability is recognized for the amount expected to be paid under short-term cash bonus or profit-sharing plans if the Company and its subsidiaries has a present legal or constructive obligation to pay this amount as a result of past service provided by the employee, and the obligation can be estimated reliably.

l. Segment information

An operating segment is a component of the business of the Company and its subsidiaries. It performs business activities from which it can obtain revenues while incurring in expenses, including revenues and expenses with transactions with other components of the Company and its subsidiaries. All operating results are reviewed by the Executive Board of the Company and its subsidiaries for decisions regarding the resources to be allocated to the segment to be taken and to assess their performance for which individual financial information is available.

The Company and its subsidiaries operated the following reportable segments during the periods: (i) Agricultural production; (ii) Commodity trading; (iii) Navigation and (iv) Electric energy. The segments are aligned with the portfolio of products and services and reflect the structure used by management to assess the performance of the Company and its subsidiaries.

29

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

m. Revenue

(i) Agricultural goods sold

Operational revenue from sales of goods in the normal course of business is measured by the fair value of the consideration received or receivable. Revenue is recognized when there is convincing evidence that the control of assets have been transferred to the purchaser, and it is probable that the financial economic benefits will flow to the Company, that the related costs and potential return of goods can be reliably estimated, there is no continued involvement with the goods sold, and the amount of revenue can be reliably measured.

The timing of the transfer of risks and rewards varies depending on the individual terms of the sales agreement. For sales of the following products: soybean, gross and degummed soybean oil, soy meal, soybean hulls, corn, cotton, seeds and fertilizers, the transference usually occurs when the product is delivered to the client’s warehouse; however, in cases where the sells take place in foreign markets, the transferences are made when the shipment of the products occurs in the seller’s port.

(ii) Services and other revenue

Revenue from services rendered and supply of electric power is recognized in profit or loss in proportion to the stage of completion. Revenue is not recorded if there is significant uncertainty of its realization.

When two or more activities that generate revenues or when the delivery of selling products are done under the same agreement. The allocation of the revenue for the components is based on the relative fair value of each specific component.

n. Government grants

Grants that compensate the Company and its subsidiaries for expenses incurred are recognized in profit or loss as on a systematic basis in the periods that the expenses are recognized.

o. Leases

At the beginning of a contract, the Company assesses whether a contract is or contains a lease. A contract is, or contains a lease, if the contract transfers the right to control the use of an identified asset for a period of time in exchange for consideration. To assess whether a contract transfers the right to control the use of an identified asset, the Company uses the definition of lease in IFRS 16.

(i) As lessee

The Company recognizes a right-of-use asset and a lease liability on the lease start date. The right-of-use asset is initially measured at cost, which comprises the initial measurement value of the lease liability, adjusted for any lease payments made up to that of the start date, plus any initial direct costs incurred by the lessee and an estimate of costs to be incurred by the lessee in disassembling and removing the underlying asset, restoring the location in which it is located or restoring the underlying asset to the condition required by the lease terms and conditions, less any lease incentives received.

30

André Maggi Participações S.A. (Amaggi) Financial statements as of

December 31, 2020

The right-of-use asset is subsequently depreciated using the straight-line method from the start date to the end of the lease term, unless the lease transfers ownership of the underlying asset to the lessee at the end of the lease term, or if the cost of the right-of-use asset reflects that the lessee will exercise the purchase option. In this case, the right-of-use asset will be depreciated over the useful life of the underlying asset, which is determined on the same basis as that of property, plant and equipment. In addition, the right-of-use asset is periodically reduced by impairment losses, if any, and adjusted for certain remeasurements of the lease liability.

The lease liability is initially measured at the present value of lease payments that are not paid on the start date, discounted at the interest rate implicit in the lease or, if that rate cannot be determined immediately, at the Company's incremental borrowing rate.

The lease payments included in the measurement of the lease liability comprise the following:

• Fixed payments, including in-substance fixed payments;

• Variable lease payments that depend on an index or a rate, initially measured using the index or rate on the start date;

• Amounts expected to be payable by the lessee under residual value guarantees; and

• The exercise price of the purchase option if the lessee is reasonably certain to exercise that option, and payments of penalties for terminating the lease, if the lease term reflects the lessee exercising an option to terminate the lease.

The lease liability is measured at amortized cost, using the effective interest method. It is remeasured when there is a change in future lease payments resulting from a change in an index or a rate, if there is a change in the amounts that are expected to be paid in accordance with the residual value guarantee, if the Company changes its valuation of a purchase option that will be exercised, extension or termination or if there is a revised in-substance fixed lease payment.

When the lease liability is remeasured in this way, an adjustment corresponding to the carrying amount of the right-of-use asset is made is recorded in the income statement if the carrying amount of the right-of-use asset has been reduced to zero.

Leasing of low value assets

The Company has chosen not to recognize right-of-use assets and leases liabilities of low value assets and short-term leases. The Company recognizes lease payments associated with these leases as an expense on a straight-line basis over the lease term.

(ii) As lessor

At the beginning or in the modification of a contract that contains a lease component, the Company allocates the consideration in the contract to each lease component based on its independent prices.