Embed Size (px)

Citation preview

ANCHORAGE ~~su , ~ EST ATE :i~

4

~ ~~ARCH A51 vol. 2 RT no. 1 Spring 1 1979 ~ Copy 2 )

VOLUME II, NO. 1 - SPRING 1979

c z

-) .J

lw 2 )~

GRAPHICS ON PAGES 12, 27, 28, & 43 BY DEGLER'S ART & DESIGN

:( !

(

J3or·

~ANCHORAGE '-· ..... -~.:-..... ::.,_ •. _ •.•.•• :::::::::::...~.---=::::::----......--_,-=::::=;-_

REAL ESTATE RESEARCH REPORT

VOLUME II, NO. 1 - SPRING 1979

U t!.~~~ I~!"'%J'' '"'"' 1 r;,_ l\: ': '. " •' : .· ::, [:· \f( ~~ -~. ~ wr~ ~ ·"""'"' r, "r:- 1 1 r:: r. A ~'(

~...,_-,~~ '',t\ l!,)}:~ .. ' " .. '. . - - - . . - '·-· "~ \.. '\.

NOT TO LEAVE LIBEt\RY

Published Semiannually by the Anchorage Real Estate Research Committee

283 Muldoon Raad Box 209

Anchorage, Alaska 99504

The contributors to this report are solely responsible for statements or interpretations contained herein. We make no warranty, express or implied, and assume no legal liability or responsibility for the accuracy of this data.

No reproductions or quotations of any part of this report permitted without special authorization in writing.

ARERC

INTRODUCTION

Volume 1 of the Anchorage Real Estate Research Report contained a substantial amount of background information on the residential real estate industry in Anchorage. This edition of the Report introduces several new tapies to our publication.

The first-ever index of residential construction costs in Anchorage has been developed by Rob Gamel for the Real Estate Research Committee. This section will be updated every six months so that trends can be identified and analyzed.

Ali of the current surveys of vacancy rates in Anchorage are somewhat deficient. To overcome the shortcomings of the various surveys, the Committee is in the process of developing its own madel to determine vacancy rates and trends in Anchorage. lt is hoped that the results of this survey will be available for pu bi ication in the next edition.

This issue of the Report includes an index of classified advertising of rentai housing for trre past two years. This index was developed by Al Robinson and presents additional information about vacancies in Anchorage. The new graph depicting vacancies reported by the Joint Military Housing Referral Office at Elmendorf Air Force Base was prepared by Rob Gamel.

Other new contributions to this issue include mortgage interest rate trends by Bob Sullivan and utility costs by John Ramzy.

Of course, ali of our regular features have been updated and, in many cases, supplemented. The hard work of ali the committee members has again resulted in a most valuable source of information for the Anchorage real estate community.

Severa! tapies of particular interest will be included in the next edition of the Anchorage Real Estate Research Report. The Planning Department of the Municipality of Anchorage has conducted an exhaustive study of housing stock (by type), by grid square, from 1975 to the present. We look forward to publishing the results of their study. Drs. Husky and Ender have been developing projections of demand for residential housing through 1985, which we hope to include in the next issue.

As you can see, the next Report will contain much timely information and original research. Please mail your subscription renewal early so you are assured of a copy. Volume 1 was completely sold out, and many people were not able to obtain a copy. We appreciate the continued support and interest of our subscribers, who make this Reportpossible.

SUBSCRIPTION APPLICATION

Name ______________________________________________________________________________ _

Address ________________________________________________________________ _

City -----------------------------------State -------------------- Zip ---------------

Regular one-year subscription (including one copy of Spring and Fall issue): $50.00

Mail check to: Anchorage Real Estate Research Committee No. of Subscriptions Requested: ____ _ 283 Muldoon Road, Box 209, Anchorage, AK 99504

-

ARERC

ANCHORAGE REAL ESTA TE RESEARCH COMMITTEE

A nonprofit commuity group organized to develop and distribute factual information on trends in real estate, construction and related activities in the Anchorage area.

CHAIRMAN Robert W. Sullivan

Alaska Mutual Savings Bank

REPORT COORDINATOR John W. Ramzy

Professional Realty, lnc.

EDITOR Angie Dugick

Cook lnlet Region, lnc.

CONSULTANTS

Richard L. Ender, Ph.D. Urban Observatory University of Alaska

Lee Huskey, Ph.D. 1 nstitute of Social and

Econom ic Research

BUSINESS & ECONOMIC CONDITIONS Mary Lou Couch Alaska Pacifie Bank

Robert R. Richards Alaska Pacifie Bank

RESIDENTIAL CONSTRUCTION ACTIVITY

E. Allen Robinson Department of Housing and

Urban Development

CONSTRUCTION COSTS H. Robert Gamel Gamel Homes, 1 ne.

H. Derrell Smith Alaska Statebank

RESIDENTIAL SALES ACTIVITY Bob Baer Totem Realty

VACANCY E. Allen Robinson Department of Housing

and Urban Development

ii

James H. Hubert Federal Home Loan Bank

of Seattle

Robert R. Richards Alaska Pacifie Bank

UNSOLDINVENTORY Abe Love Home Federal Savings & Loan

MORTGAGE LOAN ACTIVITY J im Smith First Federal Savings & Loan Association

MORTGAGE INTEREST RATE TRENDS Robert W. Sullivan Alaska Mutual Savings Bank

UTILITIES John W. Ramzy Professional Realty

EMPLOYMENT TRENDS & COST OF LIVING E. Allen Robinson -Department of Housing

and Urban Development

ORGANIZATION, MARKETING & SALES Carole Bangs Security Title & Trust Company of Alaska

ARERC

H. Derrell Smith Vice President Alaska Statebank 310 Eas.t Northern Lights Blvd. Anchorage, Alaska 99503 279-7637

James L. (J im) Smith Vice President First Federal Savings & Loan Association 813 West Northern Lights Blvd. Anchorage, Alaska 99503 274-6561, ext. 228

iv

Robert W. (Bob) Sullivan Vice President Alaska Mutual Savings Bank P.O. Box 1080 Anchorage, Alaska 99510 274-3561

Barbara Withers Regional Economist-Pianning Department Municipality of Anchorage Pouch 6-650 Anchorage, Alaska 99502 264-4866

l_

ARERC

SUBSCRIBERS TO ANCHORAGE REAL ESTATE RESEARCH REPORT

Alaska Bank of Commerce Alaska Housing Finance Corporation Alaska and the Milepost Alaska Appraisal & Research Corporation Alaska Mutual Savings Bank Alaska Pacifie Bank Alaska Pacifie Ventures Alaska Statebank Alaska Resource Library Alaska Title Guaranty Alaska USA Federal Credit Union Alaska Valuation Service, lnc. Alley-Haeg, 1 ne. The Aleut Corporation Allison & Associates Enterprises Amfac Mortgage Corporation American Realtors Anchor Mortgage Consultants, 1 ne. Anchorage Times Publishing Co., lnc. Appraisal Company of Alaska Arctic First Federal j im A. Arnesen Bank of Montreal Beneficiai Standard Properties, lnc. Besse Engineering, lnc. John R. Boo ney Wayne C. Booth, J r. William P. Bredsen, j r. Burr, Pease & Kurtz, lnc. Business Communications, lnc. Cablecom-General, lnc. Carr-Gottstein Properties, 1 ne. Century 21 - Heritage Homes Coast Mortgage Company Colonial Realty, lnc. Columbia Enterprises Consolidated Services, lnc. Cook lnlet Region, lnc. E. N. Courtney Reginald K. Curtiss Delta Companies State of Alaska

Division of Economie Enterprise Ellison & Ellison Realtors Federal Home Loan Bank of Seattle Federal Home Loan Mortgage Corporation Federal National Mortgage Association First Federal Savings & Loan First Escrow Services of Alaska First National Bank of Anchorage First National Bank of Oregon G & P Services, 1 ne. Gamel Homes, lnc.

v

Avrn S. Gensburg Ward S. Hastings Duane Heyman Hickel lnvestment Company Home Federal Savings & Loan I.M.I. ISER Iowa Appraisal and Research Corporation 1 nvestment Center, 1 ne. The 1 nvestment Corporation Leland P. james Kaiser Cement & Gypsum Corporation Philip Kraus Landmark Realty Lawyers Title lnsurance Agency, lnc. Herbert Lee Lehman Brothers, Kuhn Loeb Marty Loken McDonald's Food Services, lnc. john W. MacCarthy john McMahan Associates, lnc. MGIC Management Consulting Service Management and Planning Services Marston Real Estate Marston - South The Massart Company Massey & Company, lnc. William M. Mehner Merrill Lynch Relocation Management William E. Morrison The Mortgage Corporation Multiple Listing Service, lnc. NANA Construction Co., lnc. NCP Development National Bank of Alaska Nova Real Estate, lnc. Pacifie National Bank of Washington Peoples Bank & Trust Company Pendragon House, lnc. Polar Realty Priee Waterhouse & Co. Professional Realty, lnc. Rainier National Bank Real Estate Appraiser Real Estate Services Corporation Restaurant Corporation of Alaska Seattle First National Bank Security National Bank Security Title & Trust Co. of Alaska Bill Schreck Showcase Realty & 1 nvestments Simpson, Usher & jones, lnc.

ARERC

Harold Smith Spenard Builders Supply Spokane Mortgage Company State of Alaska

Division of Land and Water Stateside Enterprises, lnc. Swain Williams Kenneth F. Swartz Tarn Construction, lnc. Target, 1 ne. Real tors Ticor Mortgage lnsurance Co. Totem Realty, lnc. United Bank Alaska United Lumber Co., lnc. University of Alaska-Library

University of Alaska Center for Cross Cultural Studies

Unwin, Scheben, Korynta and Huette Valley lnvestments Verex Assurance, 1 ne. WGM, lnc. Wakeland, Norene and McDowell, lnc. Washington Mortgage Co., lnc. Wohlforth & Flint Jack White Company Western Enterprises Yorkvest Limited Arthur Young & Co. Yukon Realty, lnc.

This list may not include ali subscribers si nee it is revised on a continuing basis.

vi

ARERC

TABLE OF CONTENTS

1 ntroduction .............. .

Anchorage Real Estate Research Committee

Subscribers to ARERC

Table of Contents ...

Index of Charts and Graphs

Municipality of Anchorage Maps

Anchorq,ge Business and Economie Conditions

Residential Construction ....

Residential Construction Costs

Residential Sales Activity

Rentai Vacancy Trends

Unsold lnventory

Mortgage Loan Activity

Mortgage lnterest Rate Trends

Utilities ...

Employment

Cost of Living .

vii

ii

v

vii

viii

3

8

16

21

31

38

40

42

44

48

50

-

ARERC

INDEX OF CHARTS AND GRAPH~

Location of Municipality of Anchorage

Municipality of Anchorage (Map)

Building Permit Trends ....

1978 Planning Districts (Map)

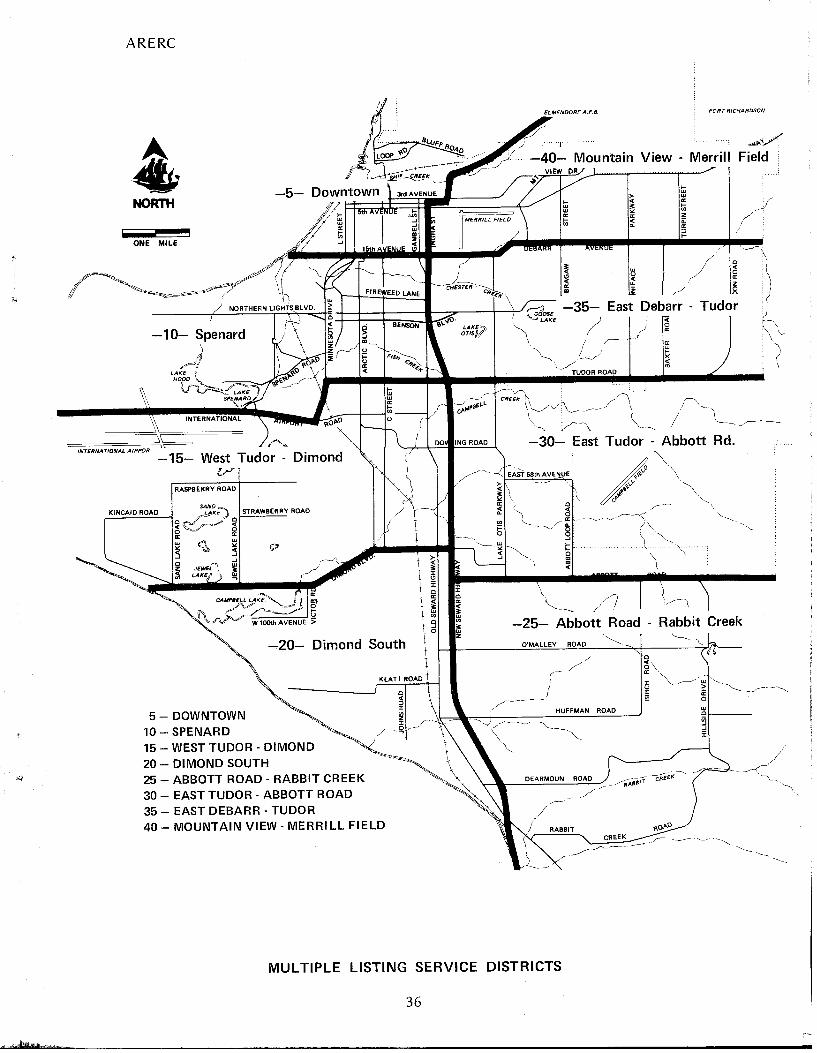

Multiple Listing Service Districts #5, 10, 15, 20, 25, 30, 35 and 40

Multiple Listing Service Districts# 100 and# 102 ..... .

2

12

14

23

24

Percentage of Ali Sold Residential Properties by Priee Range

Monthly Closed Sales as a Percent of Annual Closed Sales

Vacancy Trends in Residential Housing

. . . . . . . . . . . . . . . . . . . . . . . . 27

Mortgage lnterest Rate Trends

viii

28

33

43

• • r..· ~ ••• : .. : .:.• ~= ~(

.. .. . . .. .. . . . . . . . ..

t:J

D

: .

.·· ...... 1

' . •"' , . . . .. ..

~

~

oO •

;,?.$Jo•G3

PT. BARROW

ALASKA

\ Anchorage ~

,#

FAIRBANKS

•

MUNICIPALITY OF ANCHORAGE

. .. 1 • . . . . . . •' . . . . . . .. ·

. . . . . . . . . . . ... : . ... . . . . . . ': ... . . ·.· .. . ··' , . .. . . :: ..

:' :. •.i 1- =-· .... ••• t-".: .. 1-'e.t.•P.

, ...... ~ . . . .. .

\ : ·:··r ' . .. . ,,.,

Hl KAN

-... ,

)> ;;o m ;;;o (")

ARERC

1"= 10 Miles o Palmer

••; ~~klutno -••••••••••••••••••••1

Anchorage (City)

Metropoliton Areo

(,

(,'(.

(;~ '(.ù

MUNICIPALITY OF ANCHORAGE

2

~'J ~\

~~ ov ~

1 1 1 1 1 1 1 1 1

1 1 -1

1 1 1 1 1 1 1 1 1 1 1 1

! 1

••••••• ..1 1 1 ..

ARERC

BUSINESS AND ECONOMIC CONDITIONS

1

~ 3

ARERC

BUSINESS AND ECONOMIC CONDITIONS

The Anchorage economy as a whole remained stronger than expected in 1978, with employment increasing 2% to 3%. Although other measures of the Anchorage economy indicated an aggregate drop of about 5% in 1978 from the previous year; the level of the Anchorage economy was about 10% above its 1976 mark and more than one-half above levels of pre-pipeline years. lt is expected that 1979 will bring moderate increases in ali sectors of the Anchorage economy as normal growth patterns resume.

Looking to the past, the Anchorage economy ,accelerated rapidly in 1974 and 1975 in anticipation of and during trans-Alaska pipeline construction, followed by a very slow rate of growth at a sustained high level in 1976. ln 1977, however, the growth of the Anchorage economy considerably exceeded most expectations and, therefore, the decline experienced in 1978 was anticipated and should be viewed in its proper perspective.

One of the reasons for the 1978 decline is th at the Anchorage economy has a definite cyclical natur~ whereby highs, lows and plateaus occur in business activity from year to year. These business cycles are present in some form in virtually ali economies. The reasons for the cyclical nature of the Anchorage economy are basically twofold. First of ali, despite the fact that Anchorage has approximately half of the jobs in the state, the entire economy of Alaska is tiny, with the smallest gross state product in the nation. Furthermore, although Anchorage has about one-half of the statewide population, Alaska as a whole is still the smallest of the fifty states. Secondly, Anchorage as a major beneficiary of Alaska's economie growth, will fi nd its future dependent on a series of major, disjointed statewide events, some of which may not even occur and ali of which have timeframes impossible to predict. Examples of such events include construction of a gas pipeline, a petrochemical complex and an oil refinery, additional oil and gas exploration, coal development, hydroelectric projects, Native corporation investments, extension of the Alaska Railroad and the proposed capital move.

Because Anchorage serves as the financial and service center for the rest. of Alaska, it has a slightly different employment mix than the state as a whole. Of ali the jobs in An'chorage, almost one-half is in the distributive industries, more Ahan one-third are in government, and fourteen percent are in the basic industries. Also, Anchorage is headquarters for nearly two-thirds of ali the jobs in Alaska's construction and trade and service industries, and about one-half of ali the Federal government jobs in Alaska. With such a concentration of jobs in these important sectors, it is clear that Anchorage will continue to prosper from Alaskan economie development in general.

REAL ESTA TE TRENDS

ln Anchorage, nonresidential building permit values feil by one-half, returning to near the $70 million level of 1974. This represents a reaction to market conditions following the recent surge of office building construction in the Anchorage area. The Anchorage office space absorption rate feil by about one-quarter in 1978, returning to its 1976 level of about 350,000 square feet. lt is estimated that the value of new commercial construction in the Anchorage area will fall significantly in 1979 from 1978, primarily in response to high inventories. Currently there are over 300,000 square feet of office space available in the Anchorage area, which is about equal to or slightly more than the 1978 absorption rate. Further, there is a possibility that future rents could decline in the office building market which could limit the potential return to investors. This possibility, combined with the high cost of funds, could discourage some new construction.

The Anchorage home-building industry was extremely effective in keeping housing supply in line with demand during 1978. As a result, most real estate market statistics reflect a healthy Anchorage market condition.

Total dwelling units authorized by building permits in 1978 decreased by almost one-third from 1977's record year of 4,877 units. Residential building permit values dropped below their 1977 record to about $150 million, but remained above the values for any other previous year. Signs of strength were reported by the Anchorage Multiple Listing Service where, for the first three-quarters of 1978 the average number of residential sales per week increased and the average number of days required to sell a home decreased. Also, the rate of growth in the average selling priee increased from 1977's rate of growth.

4

~ ....

ARERC

On the other hand, the MLS sales to new listings ratio for the first three-quarters dropped from 58% in 1977 to 50% in 1978, and the rate of growth in sales was only half as fast as the rate of increase in new listings. lnve.ntories also increased substantially in 1978 above previous years.

ln Fesponse to potential oversupply and waning demand, new Anchorage multifamily building permits dropped substantially. The Anchorage apartment vacancy rate rose to record levels in 1978, reflecting some workers leaving Alaska in response to inadequate job opportunities, and sorne movements of households from apartments into first homes. Furthermore, apartment rents have increased less than bui'lding and maintenance costs, which diminishes the economie incentive for multifamily construction.

Conventional mortgage interest rates rose above 10% to new highs in 1978. Nonetheless, consumers were undaunted by the higher rates and responded favorably to the new higher lending limits announced late last year by FNMA and FHLMC. Furthermore, an awareness of the effects of inflation combined with high equity accumulation apparently encouraged many Anchorage residents to continue upgrading. This investment mentality seemed to outweigh consumer sensitivity to rising priees and interest rates.

1 nterest rates for home financing are expected to continue weil above 1 0% in 1979. Whether or not they rise further or fall depends entirely on the anti-inflationary effectiveness of federal fiscal and monetary policies. As of December 1978, there was no sign that inflation was under control. Nevertheless, a slowing U.S. economy accompanied by the expectation of tighter fiscal policies gives cause for hope that interest rates may start to subside in the latter half of 1979. Although interest rates remain high, there should be no shortage of funds.

The foregoing presents an unclear picture for the Anchorage real estate market. The data indicate that so far during the post-pipeline slowdown, housing demand has remained stronger than expected because upgrading demand and the aforementioned investment mentality have offset rising priees and the interest rate effects of a generally lackluster economy. There is a general consensus among those in the real estate industry that these relationships will continue in 1979. A cautious approach on the part of both builders and financial institutions is expected to continue in 1979, with probably little change in Anchorage housing starts from their level in 1978.

CONSTRUCTION TRENDS

The pace of Alaska's construction industry has subsided statewide, and 1979 should bring a lever of activity similar to that experienced in 1978. Large expenditures in the government sector once again will supply a major portion of the activity and may in fact induce a small employment increase.

Anchorage's level of activity in the construction industry, Alaska's largest basic industry, is a function of expansion both elsewhere in the private sector as weil as in government projects. Regardless of the future composition of Alaska's economie growth, the construction industry will benefit to sorne degree. However, the magnitude of growth in Alaska's construction industry will depend on both the rate of increase in government spending and the level of expansion in the private industries. If it is recognized that tighter fiscal postures could be assumed by ali levels of government, thereby suggesting slower increases in government spending, and that rates of growth in private industries are tied directly to government policies, then it is clear that the future of the construction industry in Alaska wm be affected both directly and indirectly by government actions.

TOURISM

Concerning the visitor industry, 1978 turned in an outstanding performance and ali prospects indicate continued growth in the future. Anchorage, the state's largest city, is visited by about three-quarters of ali Alaska travelers. Promotional air fares, increased tour ship traffic and more hotel room availability ali contributed to the 49th state's popularity with visitors.

1978 was the strongest visitor season in Alaska's history. Anchorage counted about 700,000 visitors in 1978, a 1 0% to 15% increase from the previous year. This compares with about 630,000 in 1977 and about 583,000 in 1976. Air travel increased nationwide, and Alaska, where more than 80% of the visitors arrive via commercial airliner, was no exception. Total air passenger traffic at the Anchorage International Airport reached three million for the first time, increasing almost 5% above 1977, despite a strike during the key

5

ARERC

summer season by one major carrier which may have discouraged additional increases. New promotional air fares attracted more travelers to Alaska, partly because the minimum seven-day required stay is less than the average ni ne da ys spent by most Alaska vi si tors.

Anchorage's hotels expanded capacity in 1978. The Hotel Captain Cook added a third tower providing an additional 200 rooms, bringing the downtown Anchorage major hotel room total up to 1 ,500. Furthermor~, Calista Corporation soon will open its new $39-million, 41 0-room hotel to be managed by Sheraton Corporation.

ln the future, if the dollar sustains its decline,abroad and if travel throughout the contine,ntal United States increases in priee, then Alaska as a whole will gain in popularity by comparison, especially in combination with new promotional air fares and tour packaging as weil as the increasing capabilities of Alaska visitor accommodations. However, du ring this year in Anchorage, air travel increases should slow to about 3% in view of the lack of major new economie events which have attracted business travelers in the recent past.

DISTRIBUTIVE INDUSTRIES

The distributive industries also play a major role in the Anchorage economy. Distributive industry employment in Anchorage declined about 1% in 1978, reflecting the general continuing slowdown in the economy. Nonetheless, the large distributive sector accounted for about 48% of ali the jobs in Anchorage. For 1979, the level of activity is expected to increase slightly.

Between November 1977 and November 1978, the Anchorage Consumer Priee 1 nd ex increased 1 0.5%. The outlook for 1979 sees the Anchorage inflation rate dropping from its 1978 rate to about 9%, reflecting anticipated national trends.

Throughout 1978 the cast of funds for both Alaska banks and Alaska borrowers increased substantially. ln january 1978, Alaska banks were paying 7.5% on six-month, large certificates of deposits. ln December 1978, the rate was 10.5%. Loan rates rose also, with the U.S. prime rate increasing from 7.75% at the first of the year to 11.75% at the end of 1978. Nonetheless, total bank loans continued to increase faster than deposits. Likewise, the loan to deposit ratio for ali Alaska banks increased from 59% in 1974 to 75% in 1978 as Alaska financial institutions responded to strong loan demand from Alaska bu si nesses.

Anchorage retail trade remained about even overall in 1978, although rates of growth varied a great deal for individual businesses within the industry. Also, many Anchorage retailers either expanded or relocated in 1978. According to a national survey, per household Anchorage retail sales were al most $19,000 in 1977. For 1979, sorne ri se is expected in Anchorage retail sales as the economy resumes its normal growth trends following the post-pipeline slowdown.

ln the transportation industry, freight handled by the Alaska Railroad was down 4% through October from the same period of the previous year. General cargo, coal and petroleum products handled by the railroad were down. At the Port of Anchorage, although general cargo increased 2% through November of 1978, total tonnage decreased 5%, primarily due to declining petroleum shipments resulting from Tesoro Alaska's Nikiski to Anchorage pipeline. Concerning incoming freight in vans, flats, and containers, 1977 and 1978 were years of virtually no growth at the Port of Anchorage. However, the more than 850,000 tons of in corn ing freight was more th an double ab ove its 1973 lev el.

Total freight handled at the Anchorage 1 nternational Airport dropped 2% from 1977 du ring 1978, returning to a level, nonetheless, weil above any other previous year with the exception of 1977. Also, incoming air freight, a more accurate reflection of the local Anchorage economy, increased 6% from the previous year.

Generally the outlook for Alaska's distributive industries in 1979 will be very similar to the pattern set in 1978. There are no new major economie developments expected to spur large increases in the supportive industries, but there also are not any anticipated negative events to bring about significant declines.

The growth of Anchorage supportive industries depends in the long run upon expansion of the basic sector and government. Therefore, the outlook for Anchorage's distributive industries reflects the future prospects for the basic industries which remain difficult to predict because of the many political uncertainties facing Alaska.

6

ARERC

GOVERNMENT

The other major employer in Anchorage is government. lncluding the uniformed military, about 45% of the jobs in Anchorage are supplied by government. A net increase in total government employment is expected in 1979.

Government spending plays a major role in the Alaska economy, and the high level of public expenditures prevented a severe post-pipeline downturn. The State of Alaska Fiscal Year 1979 budget of $1.5 bill ion is 27% ab ove the year be fore. Although the state budget is expected to continue increasing, it should do so at a decelerating rate given the current political situation.

With the exception of Fairbanks, where the demand for public services has slowed following the heavy impact made initially by trans-Alaska pipeline construction activity, local governments appear to be continuing their expansions. The Municipality of Anchorage has planned $98 million in capital expenditures for 1979, a 48% increase from 1978. However, in the fall of 1978, Anchorage voters approved less than one-third of a $126-million bond package. lt is difficult to tell if the spending contrais represented citizen resistance to increased government expenditures or if the bonding proposais were unacceptable for other reasons. The Anchorage 1979 total budget of $287 mill ion represents a 19% increase from the year before, and the general fund budget of $96 million is 7% above the preceding year.

Late in 1976 Alaska voters mandated that the capital be moved from Juneau to Willow. However, in November of 1978, voters declined to support the general obligation bond issue designed to finance 28% of the capital relocation costs. Furthermore, the voters passed an initiative requiring thatall bondable costs of the relocation be made clear and approved by the voters, with no funds spent on the relocation prior to such voter approval. Since the original legislation required that the move begin by 1980, it is unclear at this time what course of events will take place next.

Clearly, the high level of government expenditures will contribute to the Alaska economy as a whole and Anchorage will be no exception.

ln conclusion, 1979 is expected to be another year of adjustment for the Anchorage economy to post-pipeline levels of activity.

7

8

NOIL3IlHLSN03 'IVILN:IGIS:IH

ARERC

RESIDENTIAL CONSTRUCTION

Despite a flurry of activity in the three months of August through October in both single family and the smaller size multifamily housing structures, units authorized by building permits in the last two months of 1978 d ropped off considerably. The net effect was a total of 1 ,586 authorizations on the second half of the year compared with 1,703 in the first half. The grand total of 3,289 units authorized in 1978 was a decline of nearly a third from 1977's record year of 4,877 units. lt was still weil above the first year of oil pipeline activity, when 2,822 units were authorized in 1974.

Most of the past year's decline was in larger multifamily structures of 5 or more units, falling by 757 units, or 52.9 percent, due to the increasing rentai vacancy rate. The decrease in smaller multifamily housing (2- to 4-family structures) was 29.3 percent; in single family units it was off 23.7 percent; and in mobile homes the new connections were down only 4.7 percent. The year of 1978 was thus one of adjustment to the unusually active building period of 1975-77.

9

ARERC

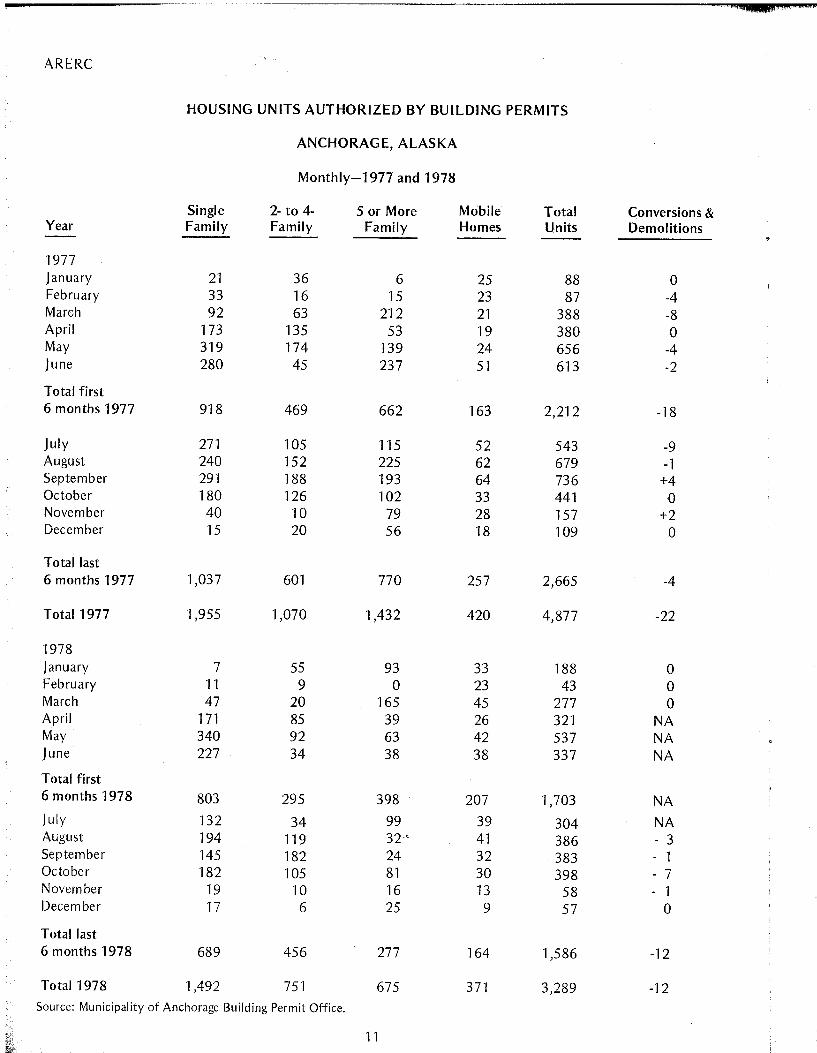

HOUSING UNITS AUTHORIZED BY BUILDING PERMITS

ANCHORAGE, ALASKA

Annually-1970 to 1978

NUMBER OF DWELLING UNITS (NOT PERMITS)

Single 2- to 4- 5 or More Year Family Family Family

1970 1,4003 ~

1,6003

1971 1,385 1,665 1972 1,445 1,506 1973 1,402 684 1974 1,798 1,024 1975 1,827 2,183 1976 1,269 2,216 1977 1,955 1,070 1,432 1978 1,492 751 675

1 Mobile home hook-ups. 2conversions may be plus or mi nus; data for 1970-7 5 are for City only. 3Estimated.

Mobile Total Hones1 Units

NA 3,0003

NA 3,0503

NA 2,951 NA 2,086 NA 2,822 NA 4,010 453 3,938 420 4,877 371 3,289

Conversions & Demolitions2

-59 -39 -63 -54 -41 -12 -46 -22 -12

Source: Municipality of Anchorage Building Permit Office; prior to 1976, City and Borough building departments.

Note: Effective January 1, 1976, ali building permits were issued by the Municipality of Anchorage as a result of the merger of the City of Anchorage and the Greater Anchorage Area Borough on September 15, 1975. Ali land use permits issued for Eagle River, Chugiak, Girdwood, and Portage areas (where building permits are not required) are included in single-family units from J uly 1972 through April 1976; beginning in May 19.76 they are reported by number of units of each type (single family, multifamily, and mobile homes).

10

ARERC

HOUSING UNITS AUTHORIZED BY BUILDING PERMITS

ANCHORAGE, ALASKA

Monthly-1977 and 1978

Single 2- to 4- 5 or More Mobile Total Conversions & Year Family Family Family Homes Units Demolitions

1977 January 21 36 6 25 88 0 February 33 16 15 23 87 -4 March 92 63 212 21 388 -8 April 173 135 53 19 380 0 May 319 174 139 24 656 -4 June 280 45 237 51 613 -2

Total first 6 months 1977 918 469 662 163 2,212 -18

July 271 105 115 52 543 -9 August 240 152 225 62 679 -1 September 291 188 193 64 736 +4 October 180 126 102 33 441 0 November 40 10 79 28 157 +2 December 15 20 56 18 109 0

Totallast 6 months 1977 1,037 601 770 257 2,665 -4

Tota11977 1,955 1,070 1,432 420 4,877 -22

1978 January 7 55 93 33 188 0 February 11 9 0 23 43 0 March 47 20 165 45 277 0 April 171 85 39 26 321 NA May 340 92 63 42 537 NA June 227 34 :58 38 337 NA

Total first 6 months 1978 803 295 398 207 1,703 NA July 132 34 99 39 304 NA August 194 119 32·· 41 386 - 3 September 145 182 24 32 383 - 1 October 182 105 81 30 398 - 7 November 19 10 16 13 58 - 1 December 17 6 25 9 57 0

Totallast 6 months 1978 689 456 277 164 1,586 -12

Total1978 1,492 751 675 371 3,289 -12 Source: Municipality of Anchorage Building Permit Office.

11

ARERC

NO. PERMITS AUTHORIZED

5,000 --

4,000 --

3,000 -

-2,000 -

-1,000 -

-0

TOTAL HOUSING UNITS AUTHORIZED BY BUILDING PERMITS Anchorage, Alaska Area

3,000

Il

1 1970

1970 ·1978

4,010 ,-

3,938 r--ï ~

3,050 2,951

2,822 ~

r---i r--;

2,086 ,..-,

1 1 1 1971 1972 1973 1974 1975 1976

COMPARISON OF BUILDING PERMIT ACTIVITY 1977 and 1978 INCREASE/DECREASE

(+ %) (- %)

4,877 r-----1

1977

Single Family Permits 2 -4 Family Permits

1977 1,955

3,289 r---1

1978

~ 1978Z//lZ/h4;2 7T//~ /ZJ 1977~ 1,070

19787/;~5VA

Multi-Family Permits -

1977 1,432

(- 29.8%)

(-23.7%)

12

(- 29.8%)

Mobile Home Hookups

1977~ 1978~

(-11.7%)

ARERC

TOTAL HOUSING UNITS AUTHORIZED 1

BY BUILDING PERMITS AND PUBLIC CONTRACTS IN SELECTED ALASKAN URBAN AREAS 2

ANNUALLY-1970 TO 1978

Anchor- Fair- Ketch-Year age banks3 juneau ikan Kodiak Sitka Kenai Sol dot na Homer Total

1970 3,000 4 444 157 94 NA 18 17 11 6 3,747 1971 3,0504 348 221 147 23 19 23 4 12 3,847 1972 2,951 439 441 119 93 41 22 16 11 4,133 1973 2,086 446 274 178 31 82 13 11 17 3,138

1974 2,822 594 122 107 43 104 25 37 35 3,889 / 1975 4,010 1,051 154 107 143 64 100 87 13 5,789 1976 3,938 998 281 117 74 136 161 138 60 5,903 1977 4,877 1,561 429 175 239 159 267 177 117 8,001 1978 3,289 806 351 104 203 121 160 69 92 5,195

1978 (by month)

Jan 188 27 8 5 10 6 4 2 251 Feb 43 19 29 13 4 25 0 0 0 133 Mar 277 36 21 14 7 11 1 6 3 376

INTi

Apr 321 138 37 6 11 5 14 5 5 542 May 537 160 56 15 45 4 28 18 29 892 -June 337 129 44 10 7 12 35 10 11 595 July 304 125 31 7 6 10 29 10 5 527

Aug 386 79 25 14 10 12 12 13 11 562 Sept 383 43 35 7 21 6 28 3 7 533 Oct 398 36 19 6 30 24 8 3 13 537 Nov 58 12 24 4 49 1 1 0 150 Dec 57 2 22 3 3 5 0 0 5 97

11ncludes mobile homes, additions, and conversions where reported. 21ncludes city and borough area combined for alllisted areas except Kenai Peninsula Borough. 3Excludes many mobile homes brought into the area, most of them outside the cities of Fairbanks and North Pole. 4Estimated.

NA-Not available.

Source: Builcting permit issuing offices.

13

ARERC

• NORTH

ONE MILE

KINCAID ROAD ~SAND

~ ~ 0 0 a: a:

~ ~ ....

STRAWBERRY ROAD

SAND LAKE

Ç>

"' §

il li i

0 ;:

a: 0 .. a: ~ .. "' ~ '3 "' 0 ~

z

RABBIT CREEK

CHUGIAK

EAGLE RIVER

ELMENDDRF A.F.B . FORT RICHARDSON

.... w w a: .... "' z a: a: ~ ....

~ """TI/ONI = / ·9

~ li'

; ,~ j t(~ ffi .... x .. .,

·~···· ~

/ \ . Î --- ~.~/ '-----~-

·~

\ ·~

.. v

----./~ -~-~~·~ § )~

',\

cl ~ ·········· \ ."--; HILLSlDË '< .

~ ABBOTT

~. /Î

~~ O'MALLEY ROAD ~

r//

1 HUFFMAN ROAD

~ ~"-.._

/ . ....---(

,4 • \ DEARMOUN ROAD ;t...-;As8ÎT c "---._ '\

1978 ANCHORAGE PLANNING DISTRICTS ~-~·~~

( ""'- ~ . ./'.----- ~-)~ GIFÙ>WOOD/ALYESKA ---~

/

14

1

ARERC ARE1

J ULY 1, 1978 SUBCOMMUNITY HOUSING UNITS FROM BUILDING PERMITS

Single Multi- Mobile Family Duplex Family Home Other

Government Hill 147 146 1,078 1,371 North Mountain View 740 168 1,214 222 2,344 Fairview/Downtown 1 '735 481 3,738 142 286 6,382 South Mountain View 1,863 500 1,531 1 '134 100 5,128 lnlet View/Turnagain 1,368 259 432 54 16 2,129 Spenard 3,356 867 5,288 1,476 140 11 '127 Lake Otis 2,609 382 1,258 10 245 4,504 North Muldoon 2,087 460 1 '113 1,422 5,082 South Muldoon 2,539 352 696 586 4,173 Abbott Loop 1,445 126 702 541 2,814 Sand Lake 3,547 526 1,705 134 5,912 Campbeii/Kiatt 1,297 124 215 873 2,509 O'Malley /Hillside 3,635 67 90 2 3,794 Oceanview 910 45 65 15 1,035

Total 27,278 4,503 19,125 6,611 787 58,304

Source: Municipality of Anchorage.

15

9L

SLSO:l NOIL:lflliLSNO:l 'IVILN3GIS3ll

ARERC

RESIDENTIAL CONSTRUCTION COSTS

This section marks the beginning of an attempt to develop reliable information regarding residential construction costs in Anchorage. Current plans are to update this survey every six months.

A uniform set of house plans was sent to 11 local builders. They were asked to develop a cast estimate for these plans according to specifie guidel ines.

Five of the 11 builders responded to the survey. Together, these five builders built a total of 250 homes du ring 1978. One builder built less than 10 houses; three built between 10 and 30 houses; and one built more than 30 houses. The average was 15 to 25 houses.

The final construction cast of $96,650 as weil as each line item represents an average of ali the costs submitted.

17

ARERC

INSTRUCTIONS TO BUILDERS

GUIDELINES FOR CO~TING OUT ARERC PLANS

1. The purpose of this survey is to determine as accurately as possible the average component costs of building a rather typical "Aiaskan box"; i.e., a garage under split entry with an unfinished downstairs.

2. We have included a material takeoff from Spenard Builders Supply which includes trusses, windows and doors to aid you in this pricing area.

3. The plans reproduced are a few years old, so we ask that you priee them out according to current building requirements, such as smoke detectors, etc.

4. A special note: please use current priees as of January 1, 1979. For the purposes of this survey, assume that no extra costs would be incurred for winter construction. Therefore, in figuring flat work for example, do not add in heat charges for winter construction.

5. We have tried to make notations on the plans listing the most common construction methods utilized today, such as asphalt versus concrete driveways, 5/8" vs. W' subfloor, T-11 siding and a few others. Because most builders still use 2x4 wall construction rather than 2x6, we retained the 2x4 design.

20

ARERC

RESIDENTIAL SALES ACTIVITY

21

ARERC

RESIDENTIAL SALES ACTIVITY

Statistics summarizing Anchorage area residential sales for each calendar year have been completed and are presented in the attached tables. Figures include the Mat-Su Borough, as many residents of that Borough commute to Anchorage and are a part of that market. ln addition, because of the statistical information available, a very minimum number of non-Anchorage, Mat-Su sales are included, but these have little or no bearing on the total picture.

The figures regarding residential sales have been obtained from Multiple Listing Service, lnc. Presently, 184 real estate agencies and over 1,500 agents in the Anchorage area report sales to the MLS. lt is estimated that over 90 percent of the total residential sales in Anchorage are reported to MLS, and are thus included in the statistics presented here.

The latest available data from MLS have been used. Revisions of data occur in each edition of the MLS due to the fact that some sales do not close and this information needs to be incorporated into the data. These revisions are most prevalent in data published during the most recent six months, and do not significantly affect older data.

22

ARERC

• NORTH

ONE MILE

.t"-... INTERNATIONAL AIRPOR

-15- West Tudor - Dimond u-r

RASPBERRY ROAD

KINCAID ROAD SAND ;Y.ÏcË)

0 STRAWBERRY ROAD

~~~ ~ a:

~ ~ 0 _,

-20- Dimond South

5- DOWNTOWN 10- SPENARD 15 -WEST TUDOR - DIMOND 20- DIMOND SOUTH 25- ABBOTT ROAD- RABBIT CREEK 30- EAST TUDOR - ABBOTT ROAD 35- EAST DEBARR- TUDOR

KLATTROAD

0

~ a:

40- MOUNT AIN VIEW- MERRILL FIELD

ELMENDORF A.F.B.

r· ....,_'./

-40- Mountain View - Merrill Field

~

... w w a: t; z 0: a: ::J ...

z / East Debarr

CRE~ ' /~ . '-.._ _/'./ i\__ ---- \

\, V\ \_

/ \ 0

~ '\ R

Tudor

-30- East Tudor - Abbott Rd .

~ /0 -25- Abbott Road - Rabbit Creek

O'MALLEY ROAD

/

r/ 1

. ./- - HUFFMAN ROAD

{<01'0

CREEK ___r-. ____..... . .....__ -~

~-/'-·~--- ....______---- ..___ / /

MULTIPLE LISTING SERVICE DISTRICTS

23

ARERC

~·

1

102 MAT-SU

BOROUGH

100 EAGLE RIVER

MULTIPLE LISTING SERVICE DISTRICTS

24

ARERC

12/31/1978 12/31/1977 12/31/1976 12/31/1975

SUMMARY STATISTICS-ANCHORAGE MULTIPLE LISTING SERVICE

ANNUAL SALES STATISTICS*

Average Market Average Listing Priee

Average Sales Priee Time Sold (Days)

$80,719 73,428 66,665 59,722

$79,869 72,577 65,609 58,965

53 55 60 50

*Statistics computed as of December 31 each year.

Average Selling Priee

No. of Sales

Total Volume Residential Closed

$

TOTAL RESIDENTIAL SALES STATISTICS (January 1 through December 31)

1978 1977 1976

79,869 $ 72,577 $ 65,609

2,864 2,579 1,895

$228,746,832 $187,176,172 $124,330,744

Average Listing Priee

Houses Not Sold

$86,660 76,683 73,278 67,264

1975

$ 58,965

1,606

$94,699,226

FINANCING METHOD BY PERCENT OF TOTAL RESIDENTIAL MARKET

State and FHA Federal VA Conventional Assumption M iscellaneous

1978 3.60% 24.09% 51.60% 10.71% 10.00% 1977 1.52% 26.79% 52.34% 8.41% 10.94% 1976 2.26% 27.46% 48.60% 12.70% 8.98% 1975 4.08% 26.58% 42.02% 13.13% 14.19%

WEEKL Y SALES VOLUME

J an.-Dec. 1978 jan.-Dec. 1977 jan.-Dec. 1976 Jan.-Dec. 1975

Average Sales Per Week 55 50 36 31

Total Residential Listings 1,441 994 677 457

Weeks of Listings of lnventory 26.2 19.9 18.9 14.7

RESIDENTIAL SALES STATISTICS

1978 1977 1976 1975

Average Sales Priee $81,875 $73,815 $66,812 $59,516

% lncrease Over Previous Year 10.9% 10.5% 12.26% N/A

*These figures include Anchorage, Eagle River, and Chugiak sales statistics only.

25

ARERC

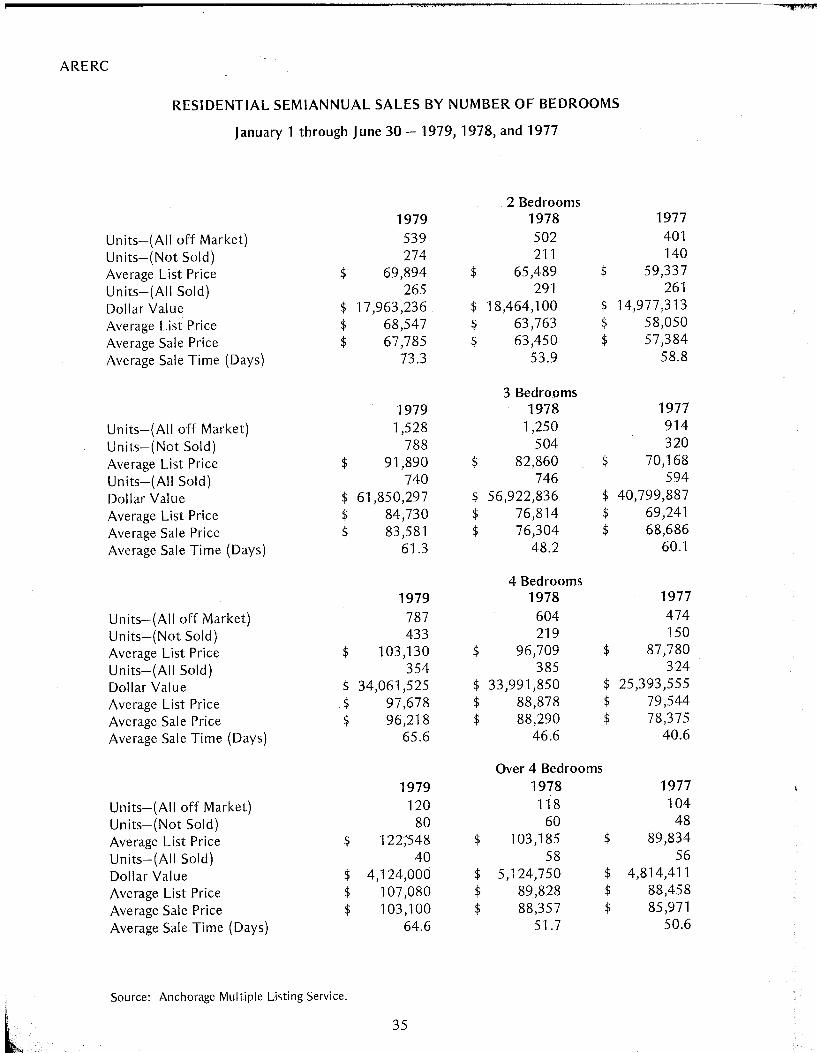

RESIDENTIAL SALES BY NUMBER OF BEDROOMS 1978, 1977 AND 1976

-1978- -1977- -1976-2 Bedrooms

Units-(AII off Market) 1,074 855 803 Units-(Not Sold) 523 337 382 Average List Priee $ 66,916 $ 59,937 $ 61,834 Units-(AII Sold) 551 ... 518 421 Dollar Value $ 35,715,902 $ 30,956,729 $ 23,444,785 Average List Priee $ 65,664 $ 60,402 $ 56,408 Average Sale Priee $ 64,820 $ 59,762 $ 55,688 Average Sale Time (Days) 57.14 61.31 71.1

-1978- -1977- -1976-3 Bedrooms

Units-(AII off Market) 2,743 2,103 1,647 Units-(Not Sold) 1,274 828 772 Average List Priee $ 85,655 $ 74,225 $ 71 '163 Units-(AII Sold) 1,469 1,275 875 Dollar Value $115,988,622 $ 90,643,063 $ 55,781,708 Average IJ.5t Priee $ 79,701 $ 71,749 $ 64,670 Average Sale Priee $ 78,957 $ 71,092 $ 63,750 Average Sale Time (Days) 52.99 56.88 58.9

-1978- -1977- -1976-4 Bedrooms

Units-(AII off Market) 1,386 1,071 933 Units-(Not Sold) 650 386 418 Average List Priee $ 100,192 $ 90,786 $ 82,892 Units-(AII Sold) 736 685 515 Dollar Value $ 66,963,708 $ 56,767,069 $ 38,220,501 Average List Priee $ 91,917 $ 84,008 $ 75,665 Average Sale Priee $ 90,983 $ 82,871 $ 74,214 Average Sale Time (Days) 50.30 47.58 55.4

-1978- -1977- -1976-Over 4 Bedrooms

Units-(AII off Market) 253 206 186 Units-(Not Sold) 145 105 102 Average List Priee $ 106,048 $ 97,967 $ 92,744

~ Units-(AII Sold) 108 101 84 Dollar Value $ 1 0,078,600 $ 8,809,311 $ 6,883,750

•,>

Average List Priee $ 95,044 $ 89,674 $ 83,671 Average Sale Priee $ 93,320 $ 87,220 $ 81,949 Average Sale Time (Days) 55.10 54.83 53.40

Source: Anchorage Multiple Listing Service.

26

ARERC

l-~~--~

PERCENT AGE OF ALL SOLO RESIDENTIAL PROPERTIES BY PRICE RANGE 1978

E·9.3%

D-22.2%

c. 31.4%

A· UN DER $54,~99 8 · $55,000 TO $69,999 C · $70,000 TO $84,999 D · $85,000 TO $99,999 E · $100,000 TO $124,999 F · $125,000 AND OVER

27

8·23.6%

IV 00

11.00

10.00

9.00

8.00

• • • • 7.00

. . /

1/ t/

6.00

5.00

4.00

"'

MONTHLY CLOSED SALE AS A PERCENT OF ANNUAL CLOSED SALES COMPARISONS 1976_1977 __ 1978 ••

• • 1 ' •

,

IX \ .. ·· • • 1

/ •• ----.!--_ • 1

•• f">( • • ~,~ ' •• • 1 ' • • • ' . ' • ,. 1 •• ' ,. 1 . . . . .

1-- ... , v "'

. .

.1/ ~,o." 1 • • '\ ...... ,.. . . . ... ......... r-------- •' • . • • •

1 •

1 •

~{ 1 \ 1 '1

----- ~- -- ----

• . •

• ~ . ' . ' . ',·

't ~ ., . ', . '

': ' ' ~·· . ' ' ' ~',, ' ~

• • •

.... \ • . • • . • • • • • • .

---3.00 JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC

)> ;;c 1"1'1 ;;tl (')

ARERC

PROFILE OF RESIDENTIAL SALES ACTIVITY ANNUAL STATISTICS-1975, 1976, 1977, 1978

Anchorage Multiple Listing Service*

J anuary 1 to December 31, 1978 J anuary 1 to December 30, 1977 Average

Percent of Average Listing

Average Average Listing Sale Time- Priee-

Unit %Total Dollar %Sales Listing Selling Priee Houses Sold Houses Not

District Sales Market Volume Activity Priee Priee Received Median Sale (Da ys) Sold

En tire District 2,864 100.00 228,746,832 52.49 80,719 79,869 98.94 78,750 53.2 86,660

5 34 1.18 2,625,500 69.38 75,602 77,220 102.13 69,500 38.8 84,566

10 179 6.25 14,822,950 55.59 83,928 82,809 98.66 76,500 42.7 89,877

15 435 15.18 34,432,915 60.08 79,712 79,156 99.30 78,450 51.9 84,707

20 364 12.70 31,618,763 51.19 87,509 86,864 99.26 84,600 63.8 96,266

25 278 9.70 27,147,910 49.46 98,739 97,654 98.90 95,000 60.3 111,679

30 118 4.12 9,388,662 56.19 80,228 79,564 99.17 81,000 51.1 81,234

35 713 24.89 56,434,371 66.26 79,960 79,150 98.98 80,500 44.8 89,541

40 146 5.09 10,136,492 59.10 70,427 69,428 98.58 67,750 41.2 79,486

100 256 8.93 19,963,075 47.76 78,947 77,980 98.77 79,625 59.6 84,749

102 253 8.83 16,596,694 38.33 67,027 65,599 97.86 65,000 60.5 74,840

J anuary 1 to December 30, 1977

En tire District 2,583 100.00 187,456,322 61.41 73,421 72,573 98.84 71,000 55.2 76,580

5 25 .96 1,808,000 64.10 74,806 72,320 96.67 65,500 78.4 69,385

10 194 7.51 13,837,825 67.59 72,320 71,328 98.62 67,500 58.5 79,519

15 394 15.25 27,829,838 69.00 71,230 70,634 99.16 68,500 52.8 76,803

20 352 13.62 27,348,920 57.32 78,679 77,695 98.74 76,000 69.0 82,950

25 282 10.91 23,993,568 63.51 86,149 85,083 98.76 82,664 56.7 95,371

30 127 4.91 9,092,250 53.13 72,248 71,592 99.09 73,900 48.7 71,402

35 725 28.06 53,473,781 75.52 74,474 73,756 99.03 73,500 44.8 79,560

40 133 5.14 7,959,200 65.19 60,898 59,843 98.26 58,000 47.3 64,487

100 161 6.23 11,253,500 54.57 70,681 69,897 98.89 70,500 60.0 76,481

102 119 4.60 7,140,650 36.50 60,614 60,005 98.99 56,950 66.0 65,271

January 1 to December 31, 1976

En tire District 1,895 100.00 124,330,744 53.09 66,665 65,609 98.41 66,000 60.5 73,278

5 27 1.42 1,672,900 35.52 63,212 61,959 98.01 60,000 67.8 80,797

10 165 8.70 10,785,563 65.47 66,582 65,367 98.17 63,000 94.8 72,739

15 334 17.62 22,104,362 57.68 66,533 66,180 99.46 65,500 65.8 71,482

20 223 11.76 16,461,500 43.38 74,997 73,818 98.42 73,500 70.6 78,845

25 166 8.75 13,213,476 46.89 81,303 79,599 97.90 76,950 65.2 89,792

30 111 5.85 7,398,335 53.62 67,794 ·'-66,651 98.31 67,500 61.0 67,476

35 529 27.91 34,126,830 61.65 65,568 64,511 98.38 62,500 44.7 72,151

40 92 4.85 5,030,522 55.08 55,695 54,679 98.17 55,000 51.9 58,989

100 122 6.43 7,396,850 51.47 61,872 60,629 97.99 64,000 46.2 69,633

102 54 2.84 2,783,045 37.76 51,993 51,537 99.12 48,750 68.6 72,251

*See footnote on following page.

29

&

' 1

A

ARERC

january 1 to December 31, 1975*

Entire District 1 ,606. 100.00 94,699,226 56.70 59,722 58,965 98.73 58,000 50.3 67,264 5 19 1.18 1,074,100 44.18 58,447 56,531 96.72 51,500 58.4 71,485 10 149 9.27 8,658,750 57.75 59,232 58,112 98.10 58,000 41.4 65,563 15 271 16.87 16,016,292 57.05 59,714 59,100 98.97 58,000 49.9 63,752 20 173 10.77 11 '124,855 49.28 64,393 64,305 99.86 65,200 55.7 72,663 25 174 10.83 11,867,063 52.25 69,289 68,201 98.43 67,750 63.7 84,540 30 70 4.35 4,167,925 60.86 59~912 59,541 99.38 61,500 40.2 66,352 35 465 28.95 27,427,718 69.50 59,827 58,984 98.58 57,000 42.9 70,607 40 121 7.53 6,263,700 51.05 52,342 51,766 98.89 50,000 59.8 58,570 100 108 6.72 5,648,923 56.84. 53,015 52,304 98.65 53,250 52.6 59,062 102 24 1.49 1,087,300 35.82 46,679 45,304 97.05 45,000 75.0 55,625

*Multiple Listing districts 101 and 103 through 106 are in other areas of the State, and thus were excluded from these statistics. Also, because of the higher number of non-MLS brokers in the excluded districts, the reported data in those districts are not considered to be representative of actual sales activity. Since these small districts were not included, columns such as"% of the Total Market" total slightly less than 100% and "Unit Sales" do not add.

The districts referred to above are depicted on pages 23 and 24.

30

ARERC

RENTAL VACANCY TRENDS

31

î" 1

ARERC

RENTALVACANCYTRENDS

Vacancies in the Anchorage area's rentai housing have continued to increase since m id-1978. This trend is evident from two measures. The former weekly and recently semi-monthly counts of apartment vacancies taken by phone by the Joint Military Referral Office at Elmendorf Air Force Base show an overall increase in vacancies from nearly 14 percent at the end of June to al most 22 percent at the end of December 1978. This sample of low, median, and high rent apartments has been broadened from 3,222 to 4,001 units currently. As indicated in the following table, the lower rent apartments have been about one-fourth empty in the last two months of 1978. Sizeable vacancy increases were also recorded in December in both the medium and higher rent groups of apartments.

The same upward trend has been noted in a count of classified ads in the Sunday edition of the Anchorage Times. Ali family type units, both homes and apartments (furnished and unfurnished} have been counted as number of ad listings only, not the number that may be vacant. This rough measure, however, exhibits broad trends. Compared to a total listing cou nt of around 700 in late June 1978, this figure grew to over 800 in nearly ali the Sundays of November and December. By January 7, 1979, the total exceeded 900 for the first time. These ad counts over the past few years have typically shown some decline in the summer months when more construction activity usually occurs.

The Anchorage Real Estate Research Committee is currently developing its own methodology for determining vacancy rates. We hope to include this information in the next volume of the Report.

32

ARERC

1

1

V AC ANCY TRENDS IN RE~ This chart indicates the trend of rentai housing vacancies as reported by the Joint Military Housing Referral Office at Elmendorf Air Force Base. The weekly reports have been averaged on a monthly basis. From October 1974 to the end of 1977, these vacancy rates were reported in two rentai categories; the lower rent apartments below $300 per month, and the medium and high rent apartments combined at rents of $300 or more. Beginning in January 1978, these last two categories were separately reported so that the low, medium and high rent apartments are in distinct rentai groups. There is some overlapping, however, of rent ranges between unit sizes. The three rentai categories as of January 1978 are as follows:

Low Medium High

0-&1-BR

$150-$299 $300-$375 $376 & Over

2-BR

$200-$300 $301-$400 $401 & Over

3-BR

$225-$350 $351-$465 $466 & Over

Source: Joint Military Housing Referral Office, Elmendorf Air Force Base

Low Medium to High Medium High

4-BR

$300-$390 $391-$500 $501 & Over

" 1 \

r

1

1 \ 1 \ 1

1 \ 1

1

1

r

1

1 1

1

A 1 V

/ --,.,...., -

/ -...,.-" /""- _,

1 ------"

/ ' 1 / ' / "-- - "'"\ 1 ' .) ' _. ,__...--

------L-~~~--~--~--r-~---.==~--~~r=~~-r--~=-~~~~---r--,---r-~~~---r--,--r--1-

O::T AOV JJli:: .JAN !PB !1tf~ !14Y ZN .70L Al6 5éP (1J (Vol

7S 75 7.5" '7.5 76 76 76 7b 7(o 76 76 76 70 70 76

33

~ RESIDENTIAL HOUSING

1 1

.,.

.. 1

1 1

!""

-

r--, /'\ 1 " / \ 1 '-/

\ 1 \ 1

1 \_-/

...... J - ....._ 1

.... " 1 \ 1 \ 1 \ 1 \ 1 1 1 \__..}

1 1 1

1

1

1 1

/

r

/~ . \ /. \

:\ 1 ' 1 • 1 •

r·-\ fi. J

/ .. •' \ 1 •. 1 . 1 \ ' ' ,

' .. i \ :\ 1 . 1 \.· ;/ \, i : •/ v \f 1

1 1 1 \ /~\ 1 v \ 1

\ 1 \ r----J

\ 1 \ 1

..;

, ..

;> dr )ov ZfC Jw tEB ~~AR k ,~y Jo# JUL JJ26 .:JP d71Jav z>k ~N lb JAR k- kr .bN dvL Aas stP h kûv tEe ~ 76 70 76 '11 77 7'7 1'7 77 77 77 77 '7'7 77 77 77 78 79 78 78 78 ?8 78 78 '78 78 76 78

34

r-~-·~M··-----

ARERC 1 1978 ANCHORAGE CIVILIAN RENT AL HOUSING VACANCY RATES

1978 Low Medium High Average

Jan. 6 3.5 13.1 12.6 8.3% 13 4.1 13.6 17.4 9.5% 20 13.4 13.0 17.2 13.9% 27 14.3 13.7 16.1 14.4%

Feb. 3 14.5 14.5 17.2 15.0% 10 16.3 14.5 16.6 15.7% 17 16.4 13.4 17.4 15.5% 24 16.2 11.0 14.1 14.1%

Mar. 3 16.2 11.5 15.7 14.5% 10 14.9 10.5 16.8 13.7% 17 14.7 8.7 21.9 13.9% 24 14.7 9.9 18.1 13.7% 31 14.2 11.5 15.2 13.4%

Apr. 7 17.1 15.9 7.8 15.1% 14 15.7 14.2 9.2 14.1% 21 15.8 9.5 12.5 13.1% 28 13.4 9.5 14.5 13.3%

May 5 14.1 11.7 15.2 13.5% 12 14.9 10.4 16.1 13.5% 19 14.7 10.1 19.9 14.0% 26 14.2 11.2 21.0 14.3%

June 2 13.9 9.6 18.1 13.2% 16 15.0 8.8 18.3 13.4% 30 15.0 10.0 17.7 13.8%

July 28 11.8 7.5 17.5 11.1

Aug. 11 12.9 9.7 19.7 12.9

Sept. 1 22.7 9.1 11.1 15.7 15 18.1 9.5 15.9 14.4

Oct. 7 17.5 10.2 15.9 14.5 14 22.3 9.8 16.2 16.4 20 21.9 9.0 15.2 15.5 27 22.3 10.1 13.8 15.8

Nov. 4 25.4 8.8 13.4 16.5 17 25.4 9.3 13.3 16.7

Dec. 15 24.9 14.9 17.3 19.4 29 26.8 16.1 22.2 21.8

Annual Average- 1978 16.4 11.2 16.0 14.4

1 Rent ranges by unit size (number of bedrooms) are as follows:

0- & 1-BR 2-BR 3-BR 4-BR

Low $150-$299 $200-$300 $225-$350 $300-$390

Medium $300-$375 $301-$400 $351-$465 $391-$500

High $376 & Over $401 & Over $466 & Over $501 & Over

Source: joint Military Housing Referral Office, Elmendorf Air Force Base.

35

ARERC

CLASSIFIED AD LISTINGS FOR RENT IN ANCHORAGE TIMES

SELECTED DATES, 1977-1978

Monthly Average Mobile

Homes Efficiencies Apts. Furn. Apts. Unfurn. Total Total Homes

May 29, 1977 42 13 162 ,. 161 378 378 7

june5, 1977 49 9 165 200 423 391 10 june 12, 1977 53 6 163 154 376 14 june 19, 1977 48 6 157 192 403 12 june 26, 1977 65 12 134 154 365 11

july 17,1977 45 10 153 162 370 364 6 j uly 24, 1977 32 12 140 145 329 6 july31,1977 55 8 161 171 395 14

August 7, 1977 41 11 162 167 381 379 15 August 14, 1977 53 11 145 159 360 13 August 21, 1977 51 16 136 165 368 9 August 28, 1977 54 13 166 173 406 20

September 4, 1977 42 12 182 149 385 380 11 September 11, 1977 49 9 181 167 406 11 September 18, 1977 50 15 167 157 389 14 September 25, 1977 46 7 143 146 342 21

October 2, 1977 54 15 203 180 452 469 18 October 9, 1977 69 11 195 180 455 28 October 16, 1977 77 13 174 189 453 15 October 23, 1977 81 14 186 202 483 16 October 30, 1977 65 17 179 243 504 14

November 6, 1977 62 15 196 228 501 530 15 November 13, 1977 65 25 184 246 520 17 November 20, 1977 70 20 184 269 543 14 November 27, 1977 71 22 212 253 558 20

December 4, 1977 77 25 231 304 637 567 34 December 11, 1977 69 34 221 282 606 26 December 18, 1977 73 25 210 244 552 23 December 25, 1977 66 16 184 208 474 12

j anuary 1, 1978 66 19 206 258 549 615 19 ,. J anuary 8, 1978 63 23 222 310 618 23 J anuary 15, 1978 61 22 226 324 633 22 January22, 1978 53 23 236 306 618 25 j anuary 29, 1978 65 25 253 318 661 23

February 5, 1978 71 24 262 314 671 620 17 February 12, 1978 69 25 215 292 601 22 February 19, 1978 83 21 201 283 588 12

Mareil 5, 1978 74 34 236 291 635 584 16 March 12, 1978 64 26 239 284 613 11 March 26, 1978 57· 22 186 240 505 12

36 "-"'TI!ilfft ~""hiNm· Ph

ARERC

CLASSIFIED AD LISTINGS FOR RENT IN ANCHORAGE TIMES

SELECTED DATES, 1977-1978 (conti nued) Monthly

Average Mobile

Homes Efficiencies Apts. Furn. Apts. Unfurn. Total Total Homes

April 2, 1978 56 21 225 272 574 543 13

April 9, 1978 67 19 211 285 582 17

April 16, 1978 64 14 207 211 496 28

April 23, 1978 64 7 217 263 451 18

April 30, 1978 70 19 249 277 615 23

May 7, 1978 69 14 271 280 634 604 18

May 14, 1978 57 15 273 297 642 17

May 21, 1978 35 13 235 264 547 26

May 28, 1978 64 18 239 273 594 22

june 4, 1978 81 16 281 291 669 630 24

june11,1978 62 15 270 288 635 16

june 18,1978 72 8 263 265 608 25

June 25, 1978 74 11 250 276 611 16

july2, 1978 82 16 258 272 628 680 21

july9, 1978 95 17 297 284 693 21

july16, 1978 86 19 289 303 697 19

j uly 23, 1978 90 11 275 324 700 19

j uly 30, 1978 97 13 258 316 684 16

August 6, 1978 86 15 308 318 727 711 22

August 13, 1978 69 13 293 298 673 27

August 20, 1978 101 10 268 305 684 17

August 27, 1978 116 16 308 320 760 15

September 3, 1978 89 23 272 335 719 710 20

September 10,1978 95 21 292 320 728 16

September 17, 1978 76 14 255 318 663 19

September 24, 1978 89 17 273 354 733 23

October 1, 1978 101 27 276 318 722 739 30

October 8, 1978 107 25 276 304 712 27

October 15, 1978 89 21 273 307 690 25

October 22, 1978 113 17 297 320 747 37

October 29, 1978 105 21 330 370 826 50

November 5, 1978 106 28 323 345 802 802 39

November 12, 1978 104 20 307 333 764 36

November 19, 1978 138 27 326 322 813 33

November 26, 1978 154 26 305 346 831 34

December 3, 1978 136 26 338 362 862 808 28

December 10, 1978 142 23 320·- 368 853 29

December 17, 1978 132 21 318 366 837 28

December 24, 1978 102 12 279 278 671 29

December 31, 1978 120 28 333 338 819 25

37

8f

..

XHOLN3ANIG'IOSN11

::nt3~V

ARERC

UNSOLDINVENTORY

ANCHORAGE TOTAL CONSTRUCTION ACTIVITY AS OF DECEMBER 31, 1978

Single-Family Construction (1-4 units), excluding condominiums

Number: 996 Percent Sold: 56% Percent U nsold:

Condominiums

Number: 612 Percent Sold: 35% Percent Unsold:

Multi-Family (over 4-plex)

Number: 29 projects 377 units

44%

65%

This sample was kept on a simple basis in arder to facilitate ease of data acquisition and to insure maximum response from those institutions which participate in construction lending. Virtually alllending institutions with offices in Anchorage responded to the questionnaire.

Questionnaires were sent to ali banks, savings and loans, mutual savings banks, credit unions and mortgage companies in Anchorage. Twenty institutions, representing ali major lenders, responded to the survey. Although it is very difficult to quantify, it is estimated that this sample represents over 90% of construction activity in Anchorage during 1978.

If there is a problem in the sample, it lies in the area of multi-family units. Since it may not be uncommon for out-of-state institutions to finance construction of some of Anchorage's larger projects and since those institutions are unknown at this time, their totals are not included in these figures.

Because this report is not preceded by others with similar sampling techniques, it is difficult to draw sweeping conclusions. However, at !east one thing appears evident, single-family houses are still built in larger quantities than condominiums, and these houses seem to have better market acceptance as evidenced by the significantly greater proportion of houses sold as a percentage of total constructed when compared to condominiums.

39

ov

XLIAIL:JV NVO~ 3DVDLHOW

ARERC

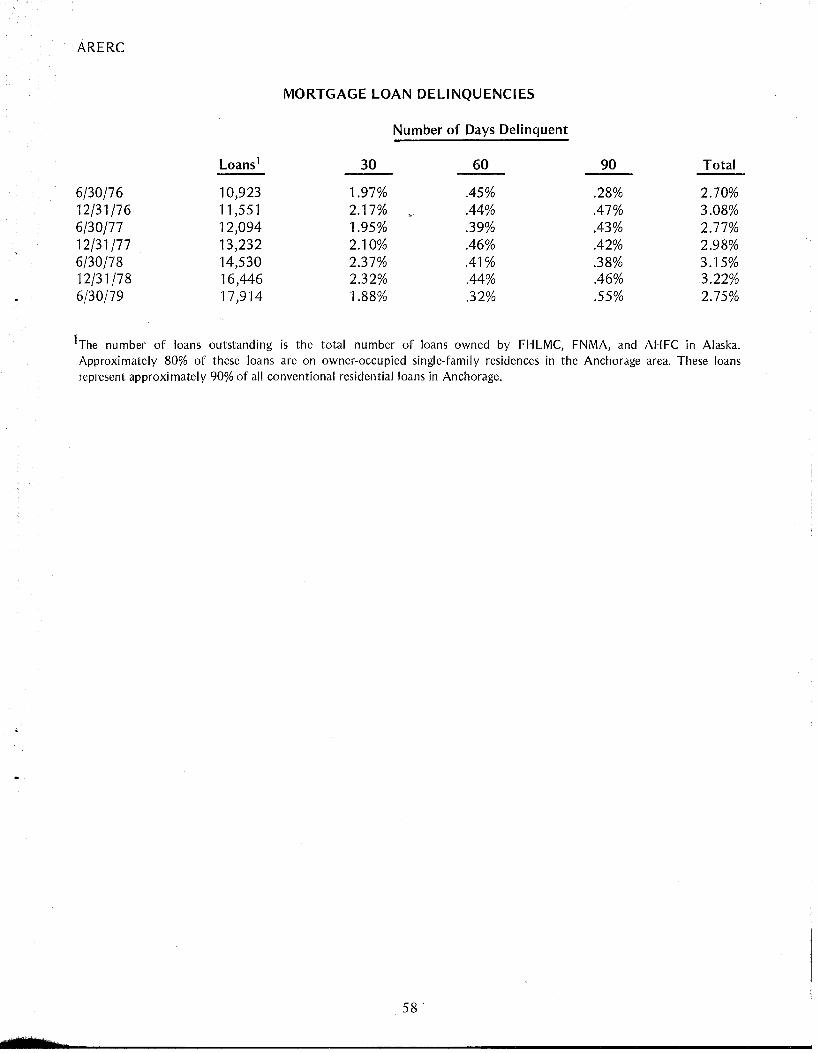

MORTGAGE LOAN DELINQUENCIES

Number of Days Delinquent

Loans1 30 60 90 Total

6/30/76 10,923 1.97% .45% .28% 2.70% 12/31/76 11 ,551 2.17% .44% .47% 3.08% 6/30/77 12,094 1.95% .39% .43% 2.77% 12/31/77 13,232 2.10% .46% .42% 2.98% 6/30/78 14,530 2.37% .41% .38% 3.15% 12/31/78 16,446 2.32% .44% .46% 3.22%

Total No. Number of Days Delinquent of Loans

Outstanding 30 60 90 Total

6/30/76 FHLMC 3,541 54 8 1 63 FNMA 4,640 116 25 12 153 AHFC2 . 2,742 __iL _16 _ _1_8 79

10,923 215 49 31 295

12/31/76 FHLMC 3,564 75 10 3 88 FNMA 4,782 126 29 12 167 AHFC2 3,205 _2Q_ _12_ ___12_ ...lQL

11 '551 251 51 54 356

·,: 6/30/77 FHLMC 3,564 67 7 4 78 !

FNMA 4,640 116 25 12 153 AHFC 2 3,890 53 15 36 104

12,094 236 47 52 335

12/31/77 FHLMC 3,467 86 8 5 99 FNMA 4,842 138 29 11 178 AHFC 2 4,923 ___ii_ _li_ -22._ 117

13,232 278 61 55 394

6/30/78 FHLMC 3,654 71 16 10 97 FNMA 5,220 184 24 10 218 AHFC2 5,656 89 19 35 143

14,530 344 59 55 458

12/31/78 FHLMC 3,742 87 15 12 114 FNMA 6,088 217 29 18 264 AHFC 2 6,616 _lL ___2_L 46 152 --

16,446 382 72 76 530

1 The nu mber of loans outstanding is the total number of loans owned by FHLMC, FNMA, and AHFC in Alaska. Approximately 80% of these loans are on owner-occupied single-family residences in the Anchorage area. These loans represent approximately 90% of ali conventional residentialloans in Anchorage.

2AHFC bases its delinquency statistics on seller/servicer reports which have monthly eut-off dates ranging from the 13th-20th of a mon th. Consequently AH FC reports its mortgage loan delinquencies on a 50-80-110 day basis.

41

ARERC

..

MORTGAGE INTEREST RATE TRENDS

""

42

ARERC

INTEREST RATE

11.00%

10.75%

10.50%

10.25%

10.00%

9.75%

9.50%

9.25%

9.00%

8.75%

8.50%

8.25%

8.00%

7.75%

7.50%

7.25%

7.00%

8.795

~ 8.750

~ t:::: ~ t:::;

~ t= ~ t::::

@] ~ t:::: ~ .--

~ == c::: .--

~ == t::::: ~ .--

~ ~ t:::=: =

~ t= c::: ~

CONVENTIONAL MORTGAGE LOAN INTEREST RATES Anchorage, Alaska

Period -12/31n6 thru 12/31/78

10.125

~ 9.971

~ ~ ~

9.435

~ 9~3

~ ~ ~6 ~ 9.008 ~ ~

~ ~ ~ ~ ~ ~ ~ 8.500 :>

~ ~ ~ ~ f= ~ ~ ~ ~ ,__

~ ~ ~ ~ -1

~ ;::::=

~ ~ ""=

~ ~ ~ ~ f= ~ 7.750 r-: f=

~ F= ~ ~ t::::

F== ~ ~ t:::: ~ .500 '--

~ ~ ~ = ~

t= ~ ~ ;;:::::: t== ~ ~ '-- = x

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ ~ f=

r-- ~ ~ :::::: ~ ~ f= ~ 12/31/76 6/30/77 -·· 12/31/77 6/30/78

Lege nd

~~-FNMA AHFC FHLMC

43

1~r ~ 10.797

~ ~ ~ ~ ~ ~ ~ ~ ~ ~ 8.750

~ ~ ~ ~ 1:::

~ ~ ~ ~

~ ~ ~ r--

~ ~ x;

~ r--

~ ~ ~ ~

~ ~ ~ r--

~ ~ ~ ~ r--12/31/78

Sub Notes: FHLMC rate includes 0.375% service fee

~

~ ~

~

~ ~

Yield shown is average yield

tt

S3I~I'II~fl

::::n13~v

ARERC

UTILITIES

Residents of Anchorage receive utility services from various providers, depending upon the service area in which they live:

Providers of utilities are:

Electricity Chugach Electric Association Municipality of Anchorage

Natural Gas Alaska Gas & Service

Water Central Alaska Utilities Municipality of Anchorage

Sewer Municipality of Anchorage

Refuse Anchorage Refuse Municipality of Anchorage

45

8t

LN3WXO'ldW3

::n.r:n1v

"" -< --,- o-_ ·~ ""-'"'-"' '"• _,-

441\j Sb :•11

ARERC

EMPLOYMENT TRENDS

ALASKA STATE AND ANCHORAGE

Annually, 1970-1977; Monthly, 1977-1978

Civilian Nonagricu ltural Nonagricultural Labor Force Wage & Salary An nuai Wage & Salary by Place of Employment by U nem ployment Employment by An nuai Residence Place of Work 1 Rate Place of Work3 Unemployment

Year Anchorage Anchorage Anchorage2 Alaska Total Rate Alaska

1970 49,024 42,000 6.7% 93,100 7.1% 1971 53,902 45,450 8.2 98,300 8.2 1972 57,535 48,250 8.9 104,200 8.3 1973 60,630 50,750 9.7 110,000 8.5 1974 58,661 58,700 6.8 128,200 7.0 1975 68,481 69,650 5.5 161,300 6.9 1976 73,436 73,100 6.8 171,700 6.7

1977 84,513 77,850 6.5 164,100 6.6 J anuary 72,150 7.2 152,100 8.1 February 72,700 8.3 154,800 8.8 March 73,700 7.7 158,500 7.3 April 75,450 7.3 163,600 6.4 May 78,150 7.0 168,300 7.3 June 80,500 6.0 172,400 6.2

J uly 79,900 5.6 171,800 5.2 August 81,600 5.2 172,600 5.4 September 82,900 5.2 171,900 5.3 October 80,750 5.9 166,000 5.7 November 78,900 6.5 160,100 6.4 December 77,600 6.7 156,900 6.9

1978 76,950 8.3 164,000 11.1 J anuary 74,100 8.4 151,600 12.0 February 74,450 8.1 153,000 11.8 March 74,900 9.5 155,700 12.8 April 75,850 9.1 159,400 12.1 May 77,950 9.0 165,300 12.1 June 79,500 8.6 171,600 11.4

July 77,650 7.9 176,000 10.0 August 78,350 7.5 179,300 9.5 September 80,800 7.5 173,300 9.4 October 78,750 7.4 166,000 10.2 November 76,100 7.9 160,500 11.1 December 75,200 8.3 156,600 11.4

1 Rounded to nearest 50. 2Based on Civilian Labor Force by Place of Residence. 3 Rounded to nearest 100.

Source: Research and Analysis Section, Employment Security Division, Alaska Department of Labor.

49

QÇ

~NIAI~ ~0 LSO:l

::nt::HIV

ARERC

ANCHORAGE CONSUMER PRICE INDEX

The second half of 1978 showed continually higher increases in the Anchorage Consumer Priee Index at annual rates exceeding the U.S. City average. ln November 1978, the Anchorage CPI increased to 194.7, up 10.5 percent from a year earlier. This is the first double digit increase since the pipeline boom period. The U.S. City average CPI in November 1978 was 202.0, which represents an annual rate of increase of 9.0

percent. These figures are index numbers with 1967 as a base of 100.

51

ARERC

CONSUMER PRICE INDEX 1

Annual Rate of Change Anchorage, Alaska ·and U. S. City Average

1974 to December 1978 (Anchorage, October 1967 = 100; U. S., 1967 = 100)

CPI Annual Rate of Change Anchorage U. S. Anchorage u. s. --

1974- Jan 125.6 139.7 7.9 7.4 Apr 129.9 143.9 8.8 10.1 J uly 134.2 148.0 11.5 11 .5 Oct 140.2 153.0 13.3 12.0

1975- Jan 142.9 156.1 13.8 11.7 Apr 150.0 158.6 15.5 10.2 July 153.8 162.3 14.6 9.7 Oct 157.4 164.6 12.3 7.6

1976- Jan 158.8 166.7 11.1 6.8 Apr 161.7 168.2 7.8 6.1 July 164.9 171.1 7.2 5.4 Oct 167.6 173.3 6.5 5.3

1977- Jan 169.4 175.3 6.7 5.2 Apr 172.6 179.6 6.7 6.8 J uly 177.4 182.6 7.6 6.7 Oct 177.3 184.5 5.8 6.5

1978- Jan 179.2 186.9 5.8 6.6 Apr 183.6 191.3 6.4 6.5 Mar 180.7 189.8 N.A. N.A. May 184.2 193.3 4.6 7.0 July 188.5 196.7 6.3 7.7 Sept. 193.2 199.3 9.8 8.3 Nov. 194.7 202.0 10.5 9.0

N.A.- Not applicable

1 Unrevised index for urban wage earners and clerical workers through April 1978; revised index for ali urban consumers beginning March 1978.

Source: Bureau of Labor Statistics, U. S. Department of Labor.

52

ALASKA HD

:1~4 tiORAGE A51 vol. 3 r ESTATE Fall

! ~!~~ 2 ARCH REPORT

-

,. ·.

,c

VOLUME rn- FALL 1979

,r-.._

1 J'

.....

7301

3 Fdc//

\AN CH_Q~R_A_GE ~--" """""'~'""'"""''""''"'"""~"'~·-·~~·--·-·-"-·--

REAL ESTATE RESEARCH REPORT

VOLUME ill - F ALL 1979

Published semiannually by the Anchorage Real Estate Research Committee

cjo Security Title 711 "H" Street

Anchorage, Alaska 99501

The contributors to this report are solely responsible for statements or interpretations contained herein. We make no warranty, express or implied, and assume no legal liability or responsibility for the accu racy of this da ta.

No reproductions or quotations of any part of this report permitted without special authorization in

writing.

'

ARERC

INTRODUCTION

The Anchorage Real Estate Research Report is fast becoming an "institution" in the real estate community. We thank our readers for their support and encouragement.

This volume of the Report contains information current through June 30, 1979. As always, the regular features have been updated and severa! new and enlightening research studies have been included. We are continuing our custom of not repeating duplicate data from volume to volume. Y ou will find prior years' data in Volumes 1 and Il. ··

Volume Ill includes two special studies that the Committee is particularly proud to be able to publish. This edition includes the first portion of a study conducted by Barbara Withers and Sandy Barto of the Municipality of Anchorage Planning Department. This is an analysis of ali of the housing stock in Anchorage and Eagle River/Chugiak. lt is an up-to-the-minute count of ali dwelling units, categorized by type and location, which has been verified through field checking. Subsequent issues of the Report will include further information on Anchorage housing stock and trends. Drs. Richard Ender and Lee Huskey have provided projections of housing demand in the Anchorage area for the next six years.

Dr. Ender has also contributed an analysisofthe real purchasing power of the Anchorage consumer, which is most revealing.

For the first time ever, the Committee is publishing its own vacancy survey in addition to the information provided by the Elmendorf Housing Referral Office and the classified ad listings in the newspaper. lt is gratifying to note that these statistics and other sources support each other.

This edition again reflects the hard work and dedication of ali the Committee members. Without them, there would not be a Report.

Plans are already under way for a most exciting and informative Volume IV. We hope that you will take this opportunity to subscribe to the Report if you have not already done so.

SUBSCRIPTION APPLICATION

Name

Address ---------------------------------------------------------------------

City State ---------- ZIP ____ _

Regular one-year subscription (includes one copy of Spring and Fall issue, 1979): $50.00 _______ __

lndividual copies: {$25.00 per copy)

Vol. 1

\) oùi ';,0~

Vol. Il

Please indicate the volume and number of copies.

Mail check to: Anchorage Real Estate Research Report cfa Security Title & Trust Co. of Alaska 711 H Street Anchorage, Alaska 99501 Attn: Carole Bangs

Vol. Ill Vol. IV

----

ARERC

ANCHORAGE REAL ESTATE RESEARCH COMMITTEE

A nonprofit community group organized to develop and distribute factual information on trends in real estate, construction and related activities in the Anchorage area.

CHAIRMAN Robert W. Sullivan

Alaska Mutual Savings Bank

REPORT COORDINATOR John W. Ramzy

Professional Realty, lnc.

EDITOR Angie Dugick

Cook lnlet Region, lnc.

CONSUlTANTS

Richard L. Ender, Ph.D. Urban Observatory University of Alaska

Lee Huskey, Ph.D. lnstitute of Social and

Econom ic Research

BUSINESS & ECONOMIC CONDITIONS (Gu est Contributor) Lee Huskey, Ph.D. lnstitute of Social and Economie Research

ANCHORAGE INCOME ANAL YSIS Richard L. Ender, Ph.D. Urban Observatory University of Alaska

RESIDENTIAL CONSTRUCTION ACTIVITY E. Allen Robinson Department of Housing and

Urban Development

ANCHORAGE HOUSING STOCK Sandy Barto Municipality of Anchorage Planning Department

Barbara Withers Municipality of Anchorage Planning Department

MORTGAGE LOAN ACTIVITY Jim Smith First Federal Savings & Loan Association

ii

James H. Hubert Federal Home Loan Bank

of Seattle

Robert R. Richards Alaska Pacifie Bank

PROJECTIONS OF HOUSING DEMAND Richard L. Ender, Ph.D. Urban Observatory University of Alaska

Lee Huskey, Ph.D. lnstitute of Social and Economie Research

CONSTRUCTION COSTS H. Robert Gamel Gamel Homes, lnc.

H. Derrell Smith Alaska Statebank

RESIDENTIAL SALES ACTIVITY Bob Baer Totem Realty

VACANCY Judy Ponsford

E. Allen Robinson Department of Housing

and Urban Development

Terry Tyson Foster Appraisal Services

j'!

ARERC

CON DO CONVERSIONS John W. Ramzy Professional Real ty, 1 ne.

UNSOLDINVENTORY Abe Love Home Federal Savings & Loan

MORTGAGE INTEREST RATE TRENDS Robert W. Sullivan Alaska Mutual Savings Bank

iii

UTILITIES Jerry Ali ison Allison & Associates

EMPLOYMENT TRENDS & COST OF LIVING E. Allen Robinson Department of Housing

and Urban Development

ORGANIZATION, MARKETING & SALES Carole Bangs Security Title & Trust Company of Alaska

ARERC

ANCHORAGE REAL ESTATE RESEARCH COMMITTEE MEMBERS

Jerry Allison Allison & Associates P.O. Box 1466 Eagle River, Alaska

Bob Baer President-General Manager Totem Realty 724 East 15th Ave. Anchorage, Alaska 99501 272-0571

Carole Bangs Assistant Vice President Security Title & Trust Company of Alaska 711 H Street Anchorage, Alaska 99501 276-0909

Sandy Barto Demographer-Pianning Department Municipality of Anchorage Pouch 6-650 Anchorage, Alaska 99502 264-4254

Angela E. (Angie) Dugick Special Projects Coordinator Cook lnlet Region, lnc. Drawer 4-N Anchorage, Alaska 99509 274-8638

Richard L. (Rick) Ender, Ph.D. Director Urban Observatory University of Alaska 3221 Providence Drive Anchorage, Alaska 99504 263-1760

H. Robert (Rob) Gamel Vice-President-General Manager Gamel Homes, lnc. 750 East Fireweed Lane Anchorage, Alaska 99503 274-3679

James H. (Jim) Hubert Vice-President-Econom ist Federal Home Loan Bank of Seattle 600 Stewart Street Seattle, Washington 98101 (206) 624-3980

iv

Lee Huskey, Ph.D. Assistant Professor of Economies lnstitute of Social & Economie Research 707 A Street, Suite 206 Anchorage, Alaska 99501 278-4621

Abe Love Vice President Home Federal Savings & Loan Pouch 7008 Anchorage, Alaska 99501 272-1451

Judy Ponsford 3340 Checkmate Drive Anchorage, Alaska 99504 333-6606

John W. Ramzy Professional Realty, lnc. 507 West Northern Lights Blvd. Anchorage, Alaska 99503 279-8551

Robert R. (Bob) Richards Executive Vice President Alaska Pacifie Bank P.O. Box 420 Anchorage, Alaska 99510 276-3110

E. Allen (Al) Robinson Area Economist Department of Housing & Urban

Development-Anchorage Area Office 334 West 5th Ave. Anchorage, Alaska 99501 271-4183

H. Derrell Smith Vice President Alaska Statebank 310 East Northern Lights Blvd. Anchorage, Alaska 99503 279-7637

james L. (Jim) Smith Vice President First Federal Savings & Loan Association 813 West Northern Lights Blvd. Anchorage, Alaska 99503 274-6561, ext. 228

ARERC

Robert W. (Bob) Sullivan Vice President Alaska Mutual Savings Bank P.O. Box 1120 Anchorage, Alaska 99510 274-3561

Terry Tyson Real Estate Appraiser F oster Appraisal Services 118 East 1 nternational Airport Road Anchorage, Alaska 99502 276-5659

v

Barbara Withers Regional Economist-Pianning Department

· Municipality of Anchorage Pouch 6-650 Anchorage, Alaska 99502 264-4866

ARERC

SUBSCRIBERS TO ANCHORAGE REAL ESTATE RESEARCH REPORT

Alaska Bank of Commerce Alaska Brick Alaska Housing Finance Corporation Alaska & The Milepost Alaska Appraisal & Research Corporation Alaska Mortgage lnsurance Alaska Mutual Savings Bank Alaska Pacifie Bank Alaska Pacifie Construction Co. Alaska Pacifie Ventures Alaska Statebank Alaska Resource-Library Alaska Title Guaranty Alaska USA Federal Credit Union Alaska Valuation Service, lnc. Alaskan Real Estate Alley-Haeg, 1 ne. The Aleut Corporation Allison & Associates Enterprises Amfac Mortgage Corporation American Realtors Anchor Mortgage Consultants, lnc. Anchorage Board of Realtors Anchorage Times Publishing Co., lnc. Apartment Company Appleby Construction Co., Ltd. Appraisal Company of Alaska Arctic First Federal Area, lnc. Realtors J im A. Arnesen Bank of Montreal Baugh Construction & Engineering Co. Beneficiai Standard Properties, 1 ne. Besse Engineering, lnc. John R. Booney Wayne C. Booth, J r. Carl G. Boraiko, CCIM William P. Bredsen, Jr. Bowden Company Realtors Burr, Pease & Kurtz, lnc. Business Communications, lnc. CEDC Cablecom-General, lnc. Cablevision of Alaska, lnc. Carr-Gottstein Properties, 1 ne. J. B. Gottstein Co., 1 ne. Century 21-Heritage Homes Coalition for Econom ic Justice Coast Mortgage Co. Colonial Realty, lnc. Columbia Enterprises Consolidated Services, lnc. Continental Land lnvestments

vi

Cook lnlet Region, lnc. Al Courtney E. N. Courtney Reginald K. Curtiss Tom Degler Delta Companies Devaii/Wardwell Real Estate Dimond Center State of Alaska

Division of Economie Enterprise Dynamic Realty Eklutna, lnc. Eljim Realty Limited Ellison & Ellison Realtors Erickson & Hinchey Executive 1 ne., Real tors Federal Home Loan Bank of Seattle Federal Home Loan Mortgage Corporation Federal National Mortgage Association First Federal Savings & Loan First Escrow Services of Alaska First National Bank of Anchorage First National Bank of Oregon G & P Services, 1 ne. Gamel Homes Avrn S. Gensburg Hanson Realty-Century 21 Ward S. Hastings Joseph R. Henri Duane Heyman Hickel lnvestment Company Hollywood Apt. Co. Home Federal Savings & Loan Huffman Hills Development Co. I.M.I. 15ER Iowa Appraisal & Research Corporation lnvestment Center, lnc. The lnvestment Corporation Leland P. James Kaiser Cement & Gypsum Corporation Key Real Estate Co. Kelly-Gay 1 nvestments Chuck Kim Philip Kraus Landmark Realty John Lapagua Co. Lawyers Title 1 nsurance Age ney, 1 ne. Herbert Lee Lehman Brothers, Kuhn Loeb Marty Laken Z. J. Loussac Library Carl E. Luchsinger

ARERC

John W. MacCarthy David McCabe McDonalds Food Services, lnc. John McMahan Associates, lnc. Mat-Su Borough MGIC Management Consulting Service Management & Planning Services Marston Real Estate Marston Real Estate-South The Massart Company Massey & Company, lnc. William M. Mehner Merrill Lynch Relocation Management Modern Construction, lnc. William E. Morrison The Mortgage Corporation Mueller Enterprises Multiple Listing Service, lnc. NANA Construction Co., lnc. NCP Development National Bank of Alaska Noey & Associates, Ltd. Nova Real Esta te, 1 ne. PMI Mortgage lnsurance Co. Pacifie National Bank of Washington Benny W. Patterson Peoples Bank & Trust Co. Pendragon House, lnc. Polar Realty Priee Waterhouse & Co. Professional Realty, lnc. Rainier National Bank Real Estate Corner Real Estate Services Corporation Restaurant Corporation of Alaska Herbert Ross Royal Alaska Sales Seattle First National Bank Security National Bank