Embed Size (px)

Citation preview

Chapter 7

Analytical Study of Organized Retail Outlets in Mumbai Metro

Division

7.1 Introduction

7.2 Retailing in Mumbai - Zonal Classification

7.3 Upcoming Supply Analysis

7.4 Rental Profile in Mumbai City

7.5 Research framework

7.6 Analyses of Sampling Profile

7.7 Analyses of the impact of organized retail sector in Mumbai

City

7.8 Testing of Hypotheses

7.9 Summary of the Study

7.10 Conclusion

332

Chapter 7

Analytical Study of Organized Retail Outlets in Mumbai Metro

Division

7.1 Introduction

Mumbai bears the tag of being the financial capital of the country and contributes

around 5 per cent of the country's GDP. The city is home to important financial

institutions like the Reserve Bank of India, the Bombay Stock Exchange and the

National Stock Exchange. Besides being the entertainment capital of the country, the

city has rich cosmopolitan demographics. These factors also ensure that the city

remains foremost in terms of the real estate development. The region referred to as

Mumbai Metropolitan Region (MMR), covers the city of Thane and Navi Mumbai

along with Mumbai city.

Mumbai, which houses the first Mall in the country, has a total organised retail stock

of 8.72 mn.sq.ft. and will witness 11.26 mn.sq.ft. of new retail development over the

next 3 years319

. The city is home to some of the most prominent and successful malls

in the country and the retail rentals are amongst the most expensive in the world.

While the size of the consumer market in the city is particularly large, the pace of

retail real estate development has outgrown the organised retail business over the last

4-5 years. This situation, coupled with the global financial crisis in 2008, forced

319

www.indiaretailing.com

333

retailers to curtail their expansion plans and put some large retailers on the brink of

bankruptcy. While the confidence of the retailers was shaken, the mall projects in the

city were stalled due to poor liquidity. Retail and commercial projects of the city were

on a negative list of the institutional lenders which made situation worse for

commercial real estate segment. While the situation has improved since mid 2009, the

retail space vacancy across the city still remains high. Many mall projects have been

marred because of poor design and also high concentration of malls in particular

catchment area. Taking cognizance of the poor demand situation, some malls with

high vacancy have started leasing space to office occupiers instead of waiting for

retailers.

Mumbai currently has 8.72 mn. sq.ft. of major operational mall space in the city.

These malls are spread all over the city, stretching from Nariman Point in South

Mumbai to Bhayander in the Western Suburbs and Kalyan in the Central Suburbs.

The city of Mumbai is divided into 4 zones: Island City, Western Suburbs, Central

Suburbs and Navi Mumbai. The malls in these zones have been analyzed and their

characteristics have been studied in order to provide a thorough examination of mall

space in Mumbai.

7.2 Retailing in Mumbai - Zonal Classification

Table 7.1

Zonal Classification of Retailing in Mumbai

S.No. Zone Locations

1 Island City Nariman Point, Haji Ali, Worli, Lower Parel,

Dadar, Mahim

2. Western Suburbs Bandra, Santacruz, Andheri, Goregaon, Malad,

Borivali, Dahisar, Mira Road- Bhayander stretch

3. Central Suburbs Matunga, Chembur, Ghatkopar, Mulund, Thane,

Kalyan, Bhandup

4. Navi Mumbai Airoli, Vashi, Kharghar

Source: Knight Frank Research.

334

As mentioned in table no 7.1 which shows the zonal classification in Mumbai. Retail

is an age old trade in the city of Mumbai. It has undergone considerable shift in the

last past decade and more radical changes are foreseen. Mumbai being a commercial

capital of India keeps vibrating with trade and commerce activities of all shapes and

forms. It’s been seen that retailing in Mumbai has undergone into drastic changes in

the last few years. The rising consumerism and increasing purchasing power of the

customer has led to significant growth of organized retail market in Mumbai. The

distribution of the Mumbai region on the basis of zonal aspects has been mentioned in

table no 4.1 which provides a clear idea of the location.

7.2.1 Island City

As mentioned in the table, the Island City zone of Mumbai encompasses all of South

Mumbai, Worli to Nariman Point, as well as Prabhadevi, Dadar and Mahim. The

major micro-markets covered in the Island City are Nariman Point, Worli-Prabhadevi,

Lower Parel and Haji Ali-Kemps Corner. Some of the major malls in the zone include

High Street Phoenix located at Lower Parel and Atria Mall located at Worli.

Since the Island City is considered to be a fairly up market residential area, there are a

large number of national and international brands present here. Two out of the three

major highstreets that were covered in this study are present in this zone, further

enhancing this zone's exclusive status.

Crossroads, the first mall in the country, located at Haji Ali was shut down and

bought by the Future Group in 2006 to convert it into office space with some amount

of retail space as well. The initially unorganised retail space has now been organised

and is referred to as SoBo (South Bombay) Central Mall, having a built up area of 0.1

mn. sq.ft. This name of the retail space was given as recently as 2009. Currently, there

is just a fraction of the space that is used commercially, with the majority comprising

retail space. This zone saw the development of a new mall called Palladium, which is

the newest part of the High Street Phoenix Mall at Lower Parel. It is referred to as

335

Phase 3, came into operation in 2009 and has a built up area of approximately 0.2 mn.

sq.ft.

The Island City only accounts for 15 percent of the major operational malls in

Mumbai with a total built up area of 1.3 mn. sq.ft. As mentioned earlier, owing to the

large volume of organised retail in this zone, there is a lack of dependence on mall

space. Furthermore, the average mall vacancy is only 4 percent since there are only 5

major malls in the Island City. With a smaller number of malls in the zone, it is

unlikely that any of them would operate without full capacity.

7.2.2 Western Suburbs

Some of the major micro-markets falling under the Western Suburbs include

Santacruz, Linking Road in Bandra, Andheri, Malad, Goregaon and Kandivali. All of

the major operational malls in this zone were covered, like Infinity Mall, Inorbit Mall

and Oberoi Mall.

In the last twelve months, only one new mall entered this zone- V Souk Mall located

in Kandivali West with a built up area of 0.2 mn. sq.ft320

. However, 2008 saw a

massive influx of mall space in this zone. Major malls that came into operation then

were Oberoi Mall, Mega Mall, Crystal Point Mall and Thakur Mall. The dominant

micro-markets in the Western Suburbs are Andheri (west) and Malad (west) with

these 2 micro-markets accounting for 6 large malls. A reason for this could be the lack

of organised retail in these spaces and hence the need for large malls. Another reason

could be the fact that a lot of individuals in these areas have an income higher than

individuals in the smaller micro-markets and therefore mall space is necessary.

Similar to the Island City, no major operational malls have been shut down in the last

twelve months. The Western Suburbs account for 43 percent of mall space in

Mumbai, the maximum of all the four zones. In all, this zone covers over 3.7 mn.

sq.ft. of operational mall space, with Oberoi Mall, situated in the micro market of

320

Devasahayam, Madona, ‘Big Deal’, Praxis Quarterly Journal on Management, August, Vol.2, No.2,

1998.

336

Goregaon, having more than 0.6 mn. sq.ft. of mall space. This zone has the most

number of malls as well, housing 14 major operational malls. The vacancy rates in

this zone are a lot higher than what was witnessed in the Island City. Here, the

average mall vacancy is around 21 per cent, primarily due to the fact that a lot of the

malls became operational within the last 2-3 years and have not found enough

retailers yet. Some of the older malls, like Inorbit Mall designed by K Raheja

Corporation and Growel's 101 designed by Garuel and Weil, have a 0 percent

vacancy.

7.2.3 Central Suburbs

The major micro-markets that were taken into consideration while studying the

Central Suburbs are Matunga, Chembur, Ghatkopar and Mulund. The micro-markets

of Thane and Kalyan, although normally considered an independent zone, were

clubbed along with the Central Suburbs. Over the past year, the major malls that

became operational in this zone were K Star Mall in Chembur with a built up area of

0.16 mn. sq.ft., and R City Mall in Ghatkopar having a built up area of 0.45 mn. sq.ft.

Both malls are retail only projects, containing multiplexes on the top floor. Similar to

the Island City and Western Suburbs, no major operational malls were shut down

during the last twelve months. Thane is an extremely dominant micro-market in this

zone. This is because Thane has seen major development in terms of residential real

estate. The micro-market has exponentially grown towards the Ghodbunder Road

with large scale residential projects coming up in the last few years. The rising

residential catchment has created a need for quality retail space and hence this micro-

market has seen an influx of new malls. Central Suburbs come second to the Western

Suburbs in terms of area occupied in Mumbai, accounting for 27 per cent of the total

stock in the city. The Central Suburbs have mall spaces aggregating to 2.4 mn. sq.ft.

but also have a high average mall vacancy, measuring approximately 29 per cent. This

is far higher than any of the other zones in Mumbai. A reason for this high vacancy

could be poor planning and designing of some of these malls. With poor designs,

people do not necessarily visit the full mall as it gets very complicated for them to

find their way around.

337

Retailers were unwilling to occupy a space which is difficult for consumers to get to

and hence those stores remain vacant. This is a possible explanation for the unusually

high vacancy rate in the Central Suburbs.

7.2.4 Navi Mumbai

The major micro-markets that fall under the Navi Mumbai zone are Airoli, Vashi and

Kharghar. There are only 6 major operational malls in this zone. Of the 6 major malls,

Inorbit Mall became operational in 2009 and has a very low vacancy rate; it is purely

a retail project. All the other 5 malls opened up in 2007-2008, hence all the malls in

this zone are relatively new malls. There were no major operational malls that shut

down in the last twelve months. Vashi is clearly the dominant micro-market in this

zone, housing 5 out of the 6 major malls. With the formation of Navi Mumbai, Vashi

was one of the major areas in that zone as it was seen as an entry point for commercial

activity. With an increase in commercial activity, there was a subsequent increase in

residential demand. And with an increase in commercial as well as residential demand

in that micro-market, the retail activity was forced to gather pace. Hence, more malls

are noticed in Vashi than any other micro-market in Navi Mumbai. Navi Mumbai has

relatively new malls and hence it only accounts for 15 percent of the total retail space

in Mumbai, covering 1.28 mn. sq.ft. of mall space. Vacancy in Navi Mumbai is also

relatively low, at 19 per cent average mall vacancy. This number translates to

approximately 237,000 sq.ft. of total mall vacancy in the zone. One reason behind this

vacancy could be the size of the malls. Most of the malls in Navi Mumbai are

relatively small in size, hence it is not possible to house tenants of all product

categories. Retailers do not wish to be a part of malls that cannot house other product

categories since that mall will not offer the consumers a complete shopping

experience. Hence, some retailers are hesitant to enter these malls and this could be a

potential reason behind the vacancy.

338

7.3 Upcoming Supply Analysis

Mumbai is set to witness a staggering 11.26 mn. sq.ft. of fresh retail space in the next

three years - 2010 to 2012321

. A possible reason behind such a huge amount of retail

space entering the market could be the fact that during the recent economic crisis, a

number of projects were stalled by developers. Now, with the economy on a sounder

foot, developers are keen to finish those stalled projects along with building new

projects. Hence the city is set to witness a great influx of retail space in the next three

years. There was an estimation of 11.26 mn. sq.ft., but approximately 7.4 mn. sq.ft.

was available by the end of 2010. There was another estimation of 3.1 mn. and 1.6

mn. This was set to come up by the end of 2011 and 2012 respectively and gradually

was achieved.

The Central Suburbs of Mumbai should experience maximum supply infusion over

the next three years. The zone would account for almost 7 mn. sq.ft. of retail space,

roughly 62 per cent of the total upcoming retail space in Mumbai. The micro-market

of Thane, which has been considered to be a part of the Central Suburbs, would be

accountable for 1.93 mn. sq.ft. of retail space. Thane has recently experienced a great

infrastructural boost and enhanced connectivity which has made projects easier to

develop. This could be a factor behind the relatively higher number of scheduled

projects. One major project planned to come up by 2011 is by Sheth Developers. The

mall will be called Viva City with a built up area of 800,000 sq.ft.

The Western Suburbs are the next most favoured destination for upcoming malls. Yet,

this zone still accounts for only 20 per cent of the upcoming retail space in Mumbai

with a total built up area of 2.26 mn. sq.ft. This shows how greatly the Central

Suburbs dominate the imminent mall space. The largest project in Western Suburbs

should be witnessed in the micro-market of Malad (west), where a 400,000 sq.ft.

project should be completed by end of 2011. Even though there are as many as 14

malls coming up in the Western Suburbs, none of them have a particularly large built

up area. The average size of all the 14 major upcoming malls is around 160,000 sq.ft.

321

Devasahayam, Madona, ‘Big Deal’, Praxis Quarterly Journal on Management, August, Vol.2, No.2,

1998.

339

so it is clear that the 400,000 sq.ft. project is by far the largest. Navi Mumbai accounts

for only 13 per cent of imminent retail space in Mumbai, with a total built up area of

approximately 1.4 mn. sq.ft. A major project that is scheduled to be developed by

2010 will be in the micro-market of Kharghar. The Green Valley Home Developers

are planning on building the Glomax Mall which will have a built up area of 350,000

sq.ft. Another key project will be witnessed in the Vashi micromarket, where Fantasia

Nano Shopping will be developed by Haware Builders and will occupy a total space

of 250,000 sq.ft. This project developed in 2010 and also have a small portion of

commercial space.

The Island City too experiences a very low built up area of upcoming retail space.

There are only 3 projects scheduled to come up in the next 5 years (2010-2015) in this

zone and hence the Island City accounts for only 620,000 sq.ft. or 6 percent of the

total upcoming supply. A possible reason behind this surprisingly low amount of

upcoming mall space could be the fact that the Island City has a large proportion of

organised retail.

Table 7.2

Supply Lag in Mumbai

S.No Year

Anticipated

Supply

(mn.sq.ft.)

Actual

Supply

(mn.sq.ft.)

Supply

Withdrawn

(mn.sq.ft.)

Supply

Stalled/Deferred

(mn.sq.ft.)

1 2006 4.64 0.36 - 4.28

2 2007 7.33 1.05 0.83 7.50

3 2008 3.67 3.13 1.37 2.10

4 2009 8.02 2.93 - 7.03

Source : Knight Frank India Research (Mumbai) 2002, ‘Searching for space’, Praxis Business Line,

January.

From analyzing Table 7.2, it is clear to understand that the Anticipated Supply for any

particular year, very rarely turns into the Actual Supply.

340

The years 2006 and 2007 were particularly difficult for developers, as 4.28 mn. sq.ft.

and 7.50 mn. sq.ft. of retail space respectively, was stalled or deferred. Although 2008

saw an Actual Supply of 3.13 mn. sq.ft., there was still approximately 3.47 mn. sq.ft.

of supply that was withdrawn or stalled. In 2009 there were greater delays in retail

projects where 75 per cent of the anticipated supply was stalled or deferred;

approximately 6 mn. sq.ft. of the anticipated 8 mn. sq.ft. failed to enter the market.

The above-mentioned Dreams Mall in Bhandup, which is highly anticipated amongst

consumers, had to reschedule its opening from 2008 to 2010. While the reasons for all

these delays vary from a lack of funds, to poor planning and designing, the fact

remains that retail projects are very often delayed.

7.4 Rental Profile in Mumbai City

While considering the anchor tenant rentals across the zones in Mumbai, it is clear

that their average monthly rentals range from Rs. 41-89/sq.ft. per month. While this is

not a very large range, it is also worth noting that rentals in the Island City are

considerably higher than rentals in Navi Mumbai. It stems from the value of property

in the two zones, with the Island City containing significantly higher property values

than Navi Mumbai. This scenario is evident while looking at the Vanilla tenant rentals

as well. The average monthly rentals range from Rs. 97267/sq.ft. per month322

. Once

again, the Island City has the highest rentals with Navi Mumbai having the lowest

rentals. It is also worth mentioning that anchor tenants in the Island City pay almost

the same amount of rent as vanilla tenants do in Navi Mumbai. This proves the

disparity between the two zones and clearly indicates where the property prices are

higher. brief look at the floor-wise variations between anchor and vanilla tenants

makes it clear that stores on the lower levels command much higher rentals than

stores on the higher levels. This is only normal with the lower level floors attracting a

significantly larger footfall than the upper level stores. This variation is clearly

noticed in anchor as well as vanilla tenants, with the same theory applying to both.

Vanilla tenants on the lower levels of malls are amongst the highest rent payers of all

322

Kannan, S., ‘Huge potential awaits retailing’, Business line, Thursday, September 1, 2001.

341

the tenants in the malls, with their small stores generally attracting the highest

footfalls in the mall. While observing Mumbai, as a whole, the rental values in malls

have actually appreciated by around 9 percent during the period March 2009-

February 2010. This is relatively surprising since during the same period, the national

average saw prices depreciate by around 30 percent. This proves that even though the

rest of the country was forced to slash prices due to low turnover from malls, Mumbai

was still functioning normally, with prices not only remaining constant but even rising

in certain micro-markets.

Retailing has now become a key growth area. There has been an attitude change in the

way the Indian consumer thinks about shopping. What, were and how they buy is now

the big question. Over the last decade, there has been a significant evolution in his

psyche, a change that has been carefully recorded and documented by behavioral

pundits. Although it is most noticeable in large metros, its impact is also seen in small

towns. The change was kicked off by the economic liberalization of the 1900's and

accelerated by the media (cable) boom following the Gulf War, when the radical

explosion in media images exposed the Indian consumer to the lifestyle enjoyed in

more affluent countries. Earlier, it was the lack of consumer culture along with low

incomes that prevented the development of such formats. But economic growth has

now triggered off a spending spree, with India's middle and high-in-come population

suddenly realizing that they have enough disposable income to go for the good times.

As the low-income base shrinks, there is an ever- increasing expansion of the higher

income groups, with a corresponding demand for consumer goods that allows the

deeper penetration of high quality and higher priced products. The early indicators of

this revolution are the mushrooming of better quality retail outlets, a profusion of

brands and various product options. The Indian consumer who can discern a clear

value propositions and unbeatable ranges at unbeatable prices served to him on a

platter. The retail industry is now beginning to evolve. Traditionally, most retailers

have very localized operations but this nature of the industry is fast changing with the

awareness that sources must be developed and a proper merchandising system put in

place. The pace of transformation has accelerated and today India has over 12 million

retail outlets. As a phenomenon, retail marketing has a radical impact and can bring in

342

new technologies, systems and mindsets. It can improve overall labor, productivity

and employment, all in the name of providing the consumer with a better range of

products at better prices in a better ambience. The nature of the economic system

(capitalism, socialism) in a country has a direct impact on the retailer’s business.

Therefore, a retailer should have a thorough a2understanding of the various economic

factors of a country that would influence their operations and profitability. Some of

the economic factors that affects the retailer are – Gross domestic product, rate

of inflation, purchasing power, interest rates, tax levels, employment growth etc.

higher growth rate of GDP (in real terms) implies that consumers have more income

and hence, they spend more, resulting in higher sales and more profits for retailers.

On the other hand, increase in inflation leads to a decrease in the purchasing power of

the consumers. The economic reforms of the1990’s have resulted in higher economic

growth than that observed in the previous decade.

Retail, India's largest industry is driven by the markets' ability to provide better

products in a comfortable ambience at affordable prices. The growth of large multi-

brand apparel outlets is one result. These outlets are usually 20,000-50,000 sq ft in

size, have their own parking space, and separate counters for perfumes, accessories,

men's wear, women's clothing and children’s clothing. Some stores also have toys,

books, home wear, footwear and music. Some of these retailers have begun to develop

a private label brand, to supplement their range and improve their margins. These

have become significant brands in their own right. Similar departmental stores/multi

brand outlets are likely to develop into a significant format in the Indian market

over the next decade. The players who can make organized retailing an integral part

of India will be the ones who reap the benefits at the end of the change process. The

industry however will have to work in tandem with the government and manufactures

to build a more positive environment for retail and cater to the demand for better

products and retailing from India's first generation of demanding cash rich consumer

An important aspect of the current economic scenario in India is the emergence of

organized retail. There has been considerable growth in organized retailing business

in recent years and it is poised for much faster growth in the future. Major industrial

houses have entered this area and have announced very ambitious future expansion

343

plans. Transnational corporations are also seeking to come to India and set up retail

chains in collaboration with big Indian companies. However, opinions are divided on

the impact of the growth of organized retail in the country. Concerns have been raised

that the growth of organized retailing may have an adverse impact on retailers in the

unorganized sector. It has also been argued that growth of organized retailing will

yield efficiencies in the supply chain, enabling better access to markets to producers

(including farmers and small producers) and enabling higher prices, on the one hand

and, lower prices to consumers, on the other. In the context of divergent views on the

impact of organized retail, it is essential that an in-depth analytical study on the

possible effects of organized retailing in India is conducted. There has been a creeping

internationalization of retailing over the recent period. As home markets have become

crowded and with opportunities in emerging markets rising, modern retailers from

developed countries have been turning to new markets.

Expansion of Organized Retail by Format

There has been an expansion of organized retail in terms of the different modern retail

formats.

The total number of organized retail outlets rose from 3,125 covering an area of 3.3

million sq. ft. in 2001 to 27,076 with an area of 31 million sq. ft. in 2007. Small-sized

single-category specialty stores dominated the organized retail in the beginning with

almost two-thirds of total space in 2001. Departmental stores came next with nearly a

quarter of total space and supermarkets accounting for the balance of about 12 per

cent of organized retail space. There were no hypermarkets in India in 2001. Specialty

stores are still the most common modern retail format with over a half of total modern

retail space in 2007. Supermarkets and department stores, occupied nearly an equal

space of 15-16 per cent each in 2007. In 2006, India had about 75 large-sized

hypermarkets carrying a tenth of the total modern retail space in the country. This

format is expected to gain more prominence in the future. To understand this growth

structure the researcher conducted an analytical study of the organized retail outlets in

Mumbai region.

344

Empirical Study

There has been fascinating changes in the Indian retail sector in the past, these

changes prompted attention of the researcher and to give a analytical thought. After

referring various written materials, consulting with various academicians and the

research guide the researcher finally selected the aforesaid topic for scientific

exploration. The researcher selected Mumbai city to conduct the research because the

city is the financial capital and changes first take place in this city and also the city

has mixed consumers.

The research concentrated on various multiple formats of organized retail outlets that

exist in the city varying from supermarkets, hypermarkets, malls, specialty stores,

departmental stores and discount stores and so on. The conceptual definition of all the

formats is provided for avoiding possible ambiguities in terms of terminology.

Source: Statistical analysis of Primary data.

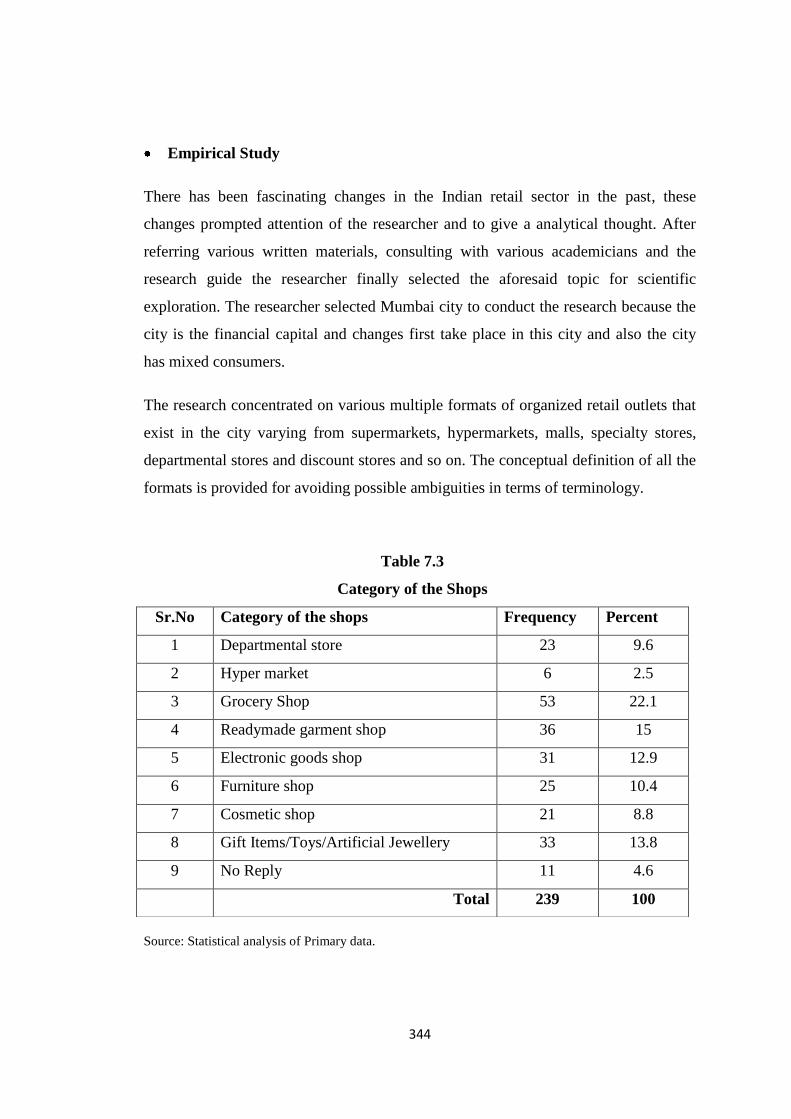

Table 7.3

Category of the Shops

Sr.No Category of the shops Frequency Percent

1 Departmental store 23 9.6

2 Hyper market 6 2.5

3 Grocery Shop 53 22.1

4 Readymade garment shop 36 15

5 Electronic goods shop 31 12.9

6 Furniture shop 25 10.4

7 Cosmetic shop 21 8.8

8 Gift Items/Toys/Artificial Jewellery 33 13.8

9 No Reply 11 4.6

Total 239 100

345

Graph 7.1

Categories of the Shops

The researcher conducted a research with organized retailers in Mumbai and the

results put in tabular form. The above Table 7.3 graph 7.1 shows that there are all

categories of shops in the organized section the market is evenly distributed with

various category shops but the maximum people belonged to grocery shop with 53

numbers and 22.1 percentage followed by readymade garment shop with 36 number

and 15 percentage. There is also presence of electronic good shop with 31 numbers

and 12.9 percent, furniture shops with 25 numbers 10.4 percent and even retailers

with cosmetics with 21 numbers 8.8 percent and gift and artificial jewelery categories

with 33 numbers and 13.8 percent have equal share in the market. This shows that

gradually organized outlets in Mumbai are capturing the market with every category

keeping the demand and needs of the consumers and therefore have been popular with

categories like grocery, readymade garments, electronic but after shift in the economy

a special category developed belonging to gift items/toys/artificial jewelery.

0

20

40

60

23

6

53

36 31 25 2133

11 Frequency

346

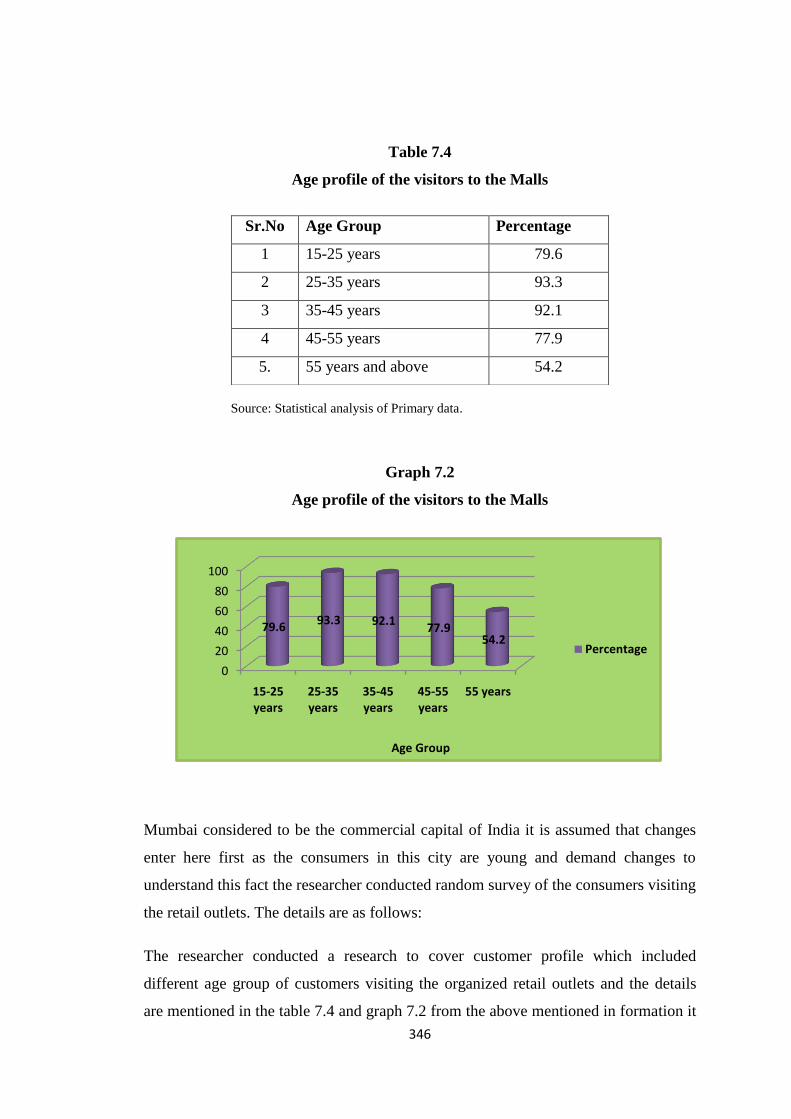

Table 7.4

Age profile of the visitors to the Malls

Source: Statistical analysis of Primary data.

Graph 7.2

Age profile of the visitors to the Malls

Mumbai considered to be the commercial capital of India it is assumed that changes

enter here first as the consumers in this city are young and demand changes to

understand this fact the researcher conducted random survey of the consumers visiting

the retail outlets. The details are as follows:

The researcher conducted a research to cover customer profile which included

different age group of customers visiting the organized retail outlets and the details

are mentioned in the table 7.4 and graph 7.2 from the above mentioned in formation it

Sr.No Age Group Percentage

1 15-25 years 79.6

2 25-35 years 93.3

3 35-45 years 92.1

4 45-55 years 77.9

5. 55 years and above 54.2

0

20

40

60

80

100

15-25 years

25-35 years

35-45 years

45-55 years

55 years

79.693.3 92.1

77.954.2

Age Group

Percentage

347

is been observed that there has been subsequent division of the crowd visiting the

outlets, but the major crowd belongs to the youngsters in the age bracket 25-35 and

the middle age group in the age bracket 35-45 its been observed that the customer

base beyond the age group of 55 occasionally visit malls. Therefore it is confirmed

that the age group 25-35 and 35-45 consisting of that the young people going to

college and the middle age group office going to college and the middle age group

goers patronized the organized retail outlets they seems to be influencing the market

as they are the major chunk of productive consumers.

Table 7.5

Types of Products displayed in the store in Malls

Sr.No Product category Response Percent

1 Branded 192 80

2 Ubranded 54 22.5

3 Private 58 24.2

Total 304 127.7

Source: Statistical analysis of Primary data.

Graph 7.3

Types of Products displayed in the store in Malls

0

20

40

60

80

100

120

140

160

180

200

Branded Ubranded Private

192

54 58

Product category

Response

348

Table 7.5 graph 7.3 gives a clear idea of products being displayed by the outlets. The

researcher took three categories and the results were that maximum outlets believe in

having branded goods in order to attract maximum consumers. It also justifies the

popularity of the organized outlets in comparison to unorganized outlets. The

researcher also unfolded that there is a section which also maintains unbranded

category and goods from private labels in order to maintain a balance in the turnover

and to have a regular flow of consumers belonging to lower middle class and lower

class who also happens to be attracted towards organized retail outlets. The survey

also revealed a fact that in Mumbai the consumers of the entire category differ in their

choice according to their needs; therefore the retailers have to stock branded

unbranded products. The survey also revealed a fifty eight percent of retailers relying

on private goods that is because a few of the shopkeepers have their own workshops

as well as marketing showrooms wherein their own products are displayed for sale

and sometimes they either directly purchase from the local distributors depending

upon their requirements.

Purchase Pattern

The purchasing pattern followed in Mumbai have a combination of the various

options available to the shopkeepers and that he decides on the basis of the their

requirements they depend on three sources directly from the companies, local

distributors and from the wholesalers. Following table provides the information about

their purchasing patterns:

Table 7.6

Area of purchases made by Retailers in the Malls

Sr.No Purchases Made Response Percent

1 Whole-sale dealer 179 74.6

2 Local distributors 94 39.2

3 Directly from the companies 118 49.2

Total 391 163.0

Source: Statistical analysis of Primary data.

349

Graph 7.4

Area of purchases made by Retailers in the Malls

Table 7.6 Graph 7.4 unfolds a major confusion of modern organized retailers in the

area of the buying the goods from and the researcher through the research justifies

that maximum retailers buy their goods from the wholesaler and further directly from

the companies as it has been mentioned earlier that they maintain branded goods. In

order to maintain stock for the local consumers at affordable price the retailer also

buys goods from the local distributors but at minimum amount.

Inventory Stock Maintenance

Inventory Stock Management is an important aspect of material management. It refers

to the stock of items which are held for sale. It covers the areas such as period of the

inventory which is normally maintained. It is important to maintain enough stock in

order to meet the demands of the consumers. The researcher tried to find out the

system followed by the organized retailers in inventory management the details are

put up below:

0 50 100 150 200

Whole-sale dealer

Local distributors

Directly from the companies

179

94

118

Response

350

Table 7.7

Maintaining stock of Inventory

Source: Statistical analysis of Primary data.

Graph 7.5

Maintaining stock of Inventory

Table 7.7 and Graph 7.5 unfold the inventory management of the retailers. Out of

total two hundred forty shops surveyed there was one hundred seventy one positive

reply who believed in maintaining stock of inventory to serve the consumers better

further sixty seven respondents believed in not maintaining the stock according to

them this will block their working capital and they further had practice of taking order

and then going for supply.

Sr.No Option Response Percent

1 Yes 171 71.3

2 No 67 27.9

3 No Reply 2 0.8

Total 240 100

0

50

100

150

200

Yes No No Reply

171

67

2

Response

351

The researcher was keen in knowing the policy of the retailers in maintaining the

stock turnover period he surveyed around two forty retailers and the results are put up

as below:

Table 7.8

Period of Inventory

Sr.No Period of Inventory No of Retailers Percent

1 1-3 months 59 24.6

2 3-6 months 24 10

3 6-9 months 8 3.3

4 > 9 months 81 33.8

5 No Reply 68 28.3

Total 240 100

Source : Statistical analysis of Primary data.

Graph 7.6

Period of Inventory

59

24

8

81

68

Frequency

1-3 months

3-6 months

6-9 months

> 9 months

No Reply

352

Table 7.8 and Graph 7.6 majority of shops 33.8 percent keep the stocks for more than

nine months therefore it can be seen that the retailers believe in maintaining stock for

longer period in order to avoid fluctuation in demand. Out of the total 59 retailers with

24.6 percent believed in rotating their inventory in one to three months thus it can be

inferred that these shops maintain fast moving consumer goods whose demand keep

shifting according to the time and 24 retailers with 10 percent rotate within three to

six months maintaining a steady and regular demand. The researcher also found it

difficult to get no reply from sixty eight retailers who choose to remain silent.

Thus with this survey the researcher concluded that the retailer in order to be

successful, face competition and bring in consumer satisfaction maintains stock of

inventory.

Customer Footfalls

Indian organized retail outlets have started making a remarkable impact on the

economy and gradually it started making an impact on consumer’s behavior. The

development of malls has specially created a change in the pattern of lifestyle of the

modern era consumer. This shift has been absorbed more in urban cities like Mumbai.

There is a gap between the customers visiting the malls and making purchases.

Mumbai consumer’s behavior pattern also differs during weekdays and weekends.

The researcher in order to understand this change conducted a survey and the results

put up as follows.

Table 7.9

Customer footfalls during Weekdays in the Malls

Sr.No Particulars Customer footfalls Percent

1 Up to 100 113 47.1

2 Up to 200 80 33.3

3 No Response 47 19.6

Total 240 100

Source: Statistical analysis of Primary data.

353

Graph 7.7

Customer footfalls during Weekdays in the Malls

The growth of the retail outlets is understood by the footfalls especially during

weekdays and weekends. According to table no 7.9 and Graph 7.7 shows that during

week days there are about 113 customers up to a range of 100 and 80 customers in the

category of up to 200.

Table 7.10

Customer footfalls during Weekends in Malls

Sr.No Particulars Customer footfalls Percent

1 Up to 100 65 27.1

2 101 to 200 112 47.7

3 201 to 300 11 4.6

4 301 to 400 3 1.3

5 No Response 49 20.4

Total 240 100

Source: Statistical analysis of Primary data.

113

80

47

Customer footfalls

Up to 100

Up to 200

No Response

354

Graph 7.8

Customer footfalls during Weekends in Malls

Table 7.10 and graph 7.8 shows the footfalls during weekends. Out of 240

respondents 49 respondents decided not to respond but according to the rest of

respondents the maximum footfalls during weekends is between 101-200 with 112

respondents confirming the category 65 respondents confirming upto 100.

This shows that in Mumbai the footfalls of consumers during weekdays and weekends

are almost similar.

Promotional Methods

This ‘P’ of marketing plays a very important role in today’s competitive business

world; It is been absorbed that in order to pull the consumer to the retail shop it is

very important to contact them with appropriate offers. The urban consumers a very

choose therefore it is important pull them with basic offers. . In this category an array

of offers are given to the prospects so that a competitive market environment can be

created and the details show below of contacting them on regular bases give an

interesting scenario.

020406080

100120

65112

113

49Customer footfalls

355

Table 7.11

Methods Followed by Retailers to contact customers on regular bases

Source : Statistical analysis of Primary data.

Graph 7.9

Methods Followed by Retailers to contact customers on regular bases

In table 7.11 and Graph 7.9 data pertaining to various promotional scheme offered by

retailers are presented. The most popular is festival offer (With discount) where 47.7

percent retailers thought in Mumbai consumers rush to the outlets more during festive

season which runs throughout the year, especially during ganapati, diwali and

christmas. This is followed by normal discount schemes with 22.5 percent of them

Sr.No Name of Promotional Schemes Frequency Percent

1 Discounts 54 22.5

2 Seasonal Sales 51 21.3

3 Exchange offer (with old) 18 7.5

4 Festival offer (discount) 112 47.7

5 Gifts with every purchase 24 10

6 Discount on Bulk Purchase 3 1.3

7 Any other 20 8.3

Total 282 100

020406080

100120

54 5118

112

243 20

Frequency

356

being optimistic in maintain the regular flow of consumers to their outlets, the

retailers were of the opinion that that today to pull the customers to their shops it is

important to provide them the discount schemes on regularity basis. In the

competitive environment where consumer has become so very choose the other most

popular offer shown in the table is seasonal sales with 21.3 percent. The analysis also

shows a unique feature which has developed more in the recent past that is banded

packs (buy one get one free) offers with 10 percent retailers opting for this scheme.

Development of nuclear family resulted in losing the impact of bulk purchases

therefore there is very small percentage which offers discount on bulk purchases.

Therefore it shows that to retain the consumers the retailer mostly follow the above

mentioned schemes regularly. This also helps the retailers to ascertain their

credentials.

Advertising and Publicity techniques

The competitive environment prevailing today requires consumers to be loyal. The

consumer of today requires awareness information and persuasion. The retailer

follows this marketing strategy which includes advertising and publicity through the

data analysis is presented in the following table.

Table 7.12

Publicity methods followed by retailers

Sr.No. Publicity methods Response Percent

1 Print Media 59 24.6

2 Outdoor Advertising (Banner/Hoarding) 28 11.7

3 Electronic media 6 2.5

4 Mouth to mouth publicity 30 12.5

5 Internet 96 40

6 Distribution of pamphlets 7 2.9

Total 226 100

Source : Statistical analysis of Primary data.

357

Graph 7.10

Publicity methods followed by retailers

Table 7.12 and graph 7.10 shows the detailed information about the various publicity

strategies used by the retailers. The most popular methodology in the modern era

being through Internet. This shows that most of the retailers are technology friendly

and believe in capturing maximum consumers in minimum time. The other area being

the traditional method print media with 24.6 percent as the retailers wants to reach to

every remote area where there is no internet connection. The print media being

cheaper in cost and has huge frequency in reaching maximum consumer at minimum

cost.

Further it has also been observed that most of the retailers believe in Personal touch in

marketing, therefore their publicity focus also has been to mouth to mouth publicity

with 12.5 percent.

The analysis also shows that there is less inclination towards distribution of pamphlets

with 2.9 percent in modern society. This result further highlights the fact that the

consumer does not get convinced merely by getting pamphlets. Therefore to attract

modern consumer the retailers have to do something unique to be on the top on mind

of the consumer.

0 20 40 60 80 100

Print Media

Outdoor Advertising …

Electronic media

Mouth to mouth publicity

Internet

Distribution of pamphlets

59

28

6

30

96

7

Response

358

Technology in Business

Technology plays very important role in the growth development and upliftment of

the organization. Further the basic difference in the growth of organized retails apart

from the unorganized retails is the technology used by the organized outlets. Mumbai

being the commercial capital and the mushrooming of MNCs have resulted in flowing

of the latest technologies. Technology basically refers to the degree of automation

being used by the retailers. The retailer in order to find out the usage of technology

concentrated areas like:

i. Credit card system

ii. Bar coding

iii. Computerized billing etc.

Following tables give a clear cut view of the various types of usage of technology.

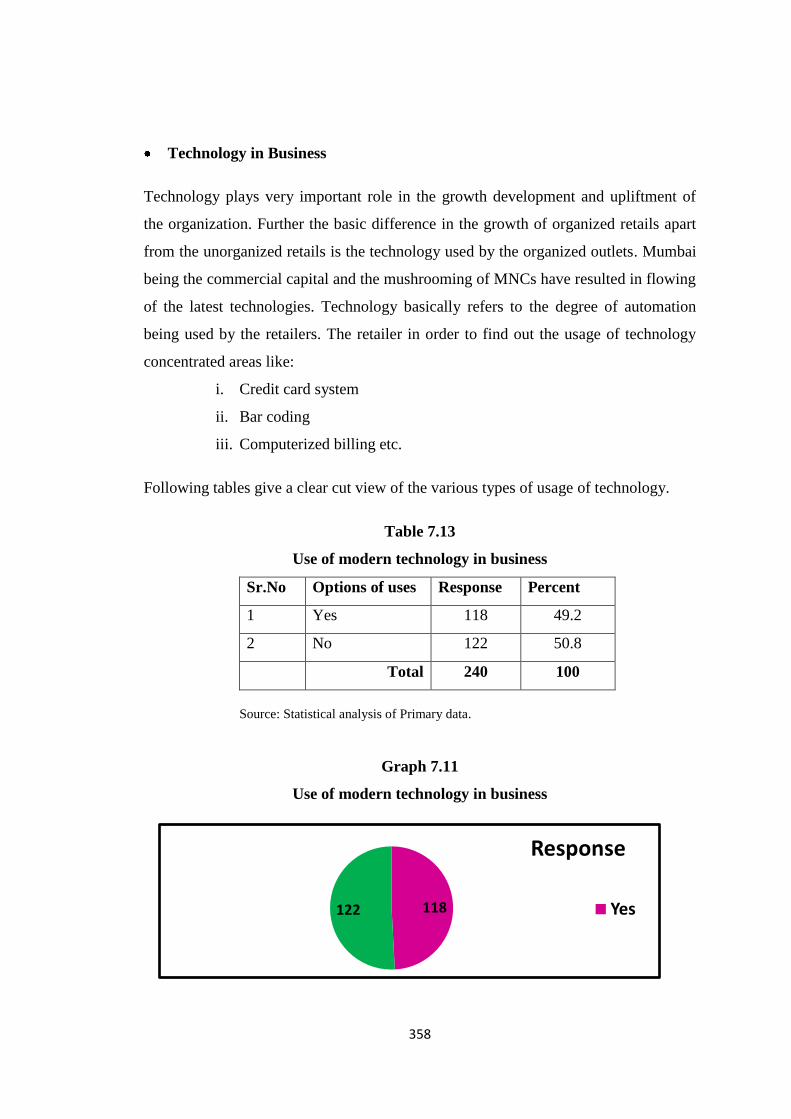

Table 7.13

Use of modern technology in business

Sr.No Options of uses Response Percent

1 Yes 118 49.2

2 No 122 50.8

Total 240 100

Source: Statistical analysis of Primary data.

Graph 7.11

Use of modern technology in business

118122

Response

Yes

359

As per the Table 7.13 and Graph 7.11 out of total two hundred forty retailers surveyed

there were around 50.8 percent of the responders who said they do not use any

modern technologies in their shop and 49.2 percent were very optimistic in stating

that they follow the trend and believe in serving the consumer with modern

technology. They further stated that using latest technology has made their work more

systematic and they are able to maintain proper records. According to the retailers

using the modern technology though initially costed on their budget but in the long

run it has become cost effective.

Table 7.14

Systems used in the shop

Source : Statistical analysis of Primary data.

Graph 7.12

Systems used in the shop

Sr.No Systems Used Response Percent

1 ERP 89 37.1

2 SAP/Tally 33 13.8

3 Bar coding and scanners 89 37.1

4 Credit card payments 9 3.8

5 Computerized billing 3 1.3

Total 223 100

0 20 40 60 80 100

ERP

SAP/Tally

Bar coding and scanners

Credit card payments

Computerized billing

89

33

89

9

3

Response

360

Table 7.14 and Graph 7.12 reveals that most of the retailers who follow the modern

technology have ERP (37.1 percent) Bar coding and scanners (37.1 percent) as most

prominent systems further followed by SAP/Tally (13.8 percent). It has been absorbed

that due to hacking and computer crimes being more prominent in the recent past the

retailers are hesitant to use those systems, therefore resulting in least response.

Human Resource Management

Retailing being a dynamic and growth oriented industry does require effective

management of human resources that organizational objectives and individual

objectives can be balanced effectively. The activities to be performed by the

employees working in a retail organization are very comprehensive and vary from

organization to organization but commonly used practices are followed by most of the

retailers in order to protect and nurture the talents of the human resources in the work

place. The researcher during the research found out that the retailers try to maintain a

balance between modern and traditional techniques in conducting human resource

management techniques, further it also has been found out that there is no

professional approach in maintaining human resource. The retailers mostly rely on

family members or close relatives. In order to justify this statement the researcher

conducted survey into the following human resource management areas:

i. Methods of Recruitment and Selection.

ii. Training of the employees.

iii. Facilities provided to the employees.

Recruitment and Selection of the employees

This is an important area in the process of human resource management since the

business depends on efficient manpower. The survey brought to the notice that

selection of staff is basically by maintaining traditional approach that is because in the

business of retail trust plays an important role.

361

Table 7.15

Method used for selection of employees

Sr.No Name of the methods Response Percent

1 Personal Contacts 146 60.8

2 Advertisement in Newspaper 25 10.4

3 Family Member 110 45.8

4 Any Other 18 7.5

Total 240 100

Source: Statistical analysis of Primary data.

Graph 7.13

Method used for selection of employees

As per the data presented in Table 7.15 and Graph 7.13 it is clearly evident that most

of the retailers believe in having their own family members into their business with

45.8 percent favoring it. This could reduce their expenses on the selection process and

further in Mumbai most of the retailers manage family business. There is also one

more area which is very strongly accepted by the retailers that is personal contacts

with 60.8. According to the result put in the table this is the area which is sought more

by the retailers, the personal contacts were distant relatives or people brought from

0%

20%

40%

60%

80%

100%

146 25 110 18

Response

362

native who come to Mumbai in search of livelihood. Appointment through

advertisements is not much preferred with 10.4 percent of the retailers opting for it.

This shows employee selection till date in retailing depends on personal contacts due

to trust factor in business.

Method followed in Training and development

All type of jobs require training and development of the employees for their efficient

performance therefore all the employees, new or old should undergo this process from

time to time. Further, in Mumbai the way retail outlets are developing and emerging it

becomes imperative for the organized retail outlets in the city to systematically

introduce planned training programmes aiming to increase the knowledge, skills,

abilities and aptitude of the employees to perform the new competitive task

effectively and efficiently. The researcher concentrated on two areas, on the job and

off the job he therefore with the help of the survey tried to find out the systems

followed by the retailers in Mumbai metro region the results are given below:

Table 7.16

The system followed by the retailers for training of employees

Source: Statistical analysis of Primary data.

Sr.No System of training Frequency Percent

1 on the job 89 37.1

2 off the job training 89 37.1

3 No Response 62 25.8

Total 240 100

363

Graph 7.14

The system followed by the retailers for training of employees

In Table 7.16 and Graph 7.14 out of two hundred forty retailers surveyed 25.8

percentage of responders were not very clear of the system followed by them

therefore they decided to remain silent. Further out of 179 responders it has been

found out that there is a balance between on the job (37.1 percent) and off the job

(37.1 percent) system being followed by them. This shows that the retailers in

Mumbai have tried to maintain both traditional (Job Rotation etc) as well as modern

techniques (Universities and Training Centers etc) and followed the principle of learn

by doing.

Facilities to the employees

Facilities represent a substantial part in any organization, it is equally important to the

organization and the employees. Hence it becomes imperative for the HR department

of any retail business to have clear cut policy guidelines which could benefit both the

employee and the organization.

Since the survey was of organized retail outlets it was found that areas like annual

salary and fringes were considered the most. It was also seen that these benefits were

differing from shop to shop.

89

89

62

0 20 40 60 80 100

on the job

off the job training

No Response

Frequency

364

The results further gives a clear idea of the system followed by most of the organized

retailers in Mumbai and further their popularity.

Table 7.17

Facilities provided by the retailers to employees

Graph 7.15

Facilities provided by the retailers to employees

Name of facilities provided to employees Response Percent

Annual Salary Increment 118 49.2

Bonus 19 7.9

Fringes 120 50

Medical facilities 50 20.8

Casual Leave 22 9.2

Annual Leave (Earned Leave) 5 2.1

Total 334 100

Source: Statistical analysis of Primary data.

0

50

100

150

118

19

120

5022 5 Response

365

Table 7.17 and Graph 7.15 provide information pertaining to the facilities provided to

the employees in the organized outlets in Mumbai. The result shows that the retailers

provide quite number of facilities to the employees like annual salary increment (49.2

percent) bonus (7.9 percent) Fringes (50 percent) based on performance medical

facilities (20.8 percent) casual leave (9.2 percent) and further few also followed the

system of annual leave (2.1). The results show that most of the concentrated on annual

salary increment and fringes, it also shows that the retailers do provide medical

facilities to their employees. Therefore from the results it is quite evident that

organized retails follow the proper system of human resource development

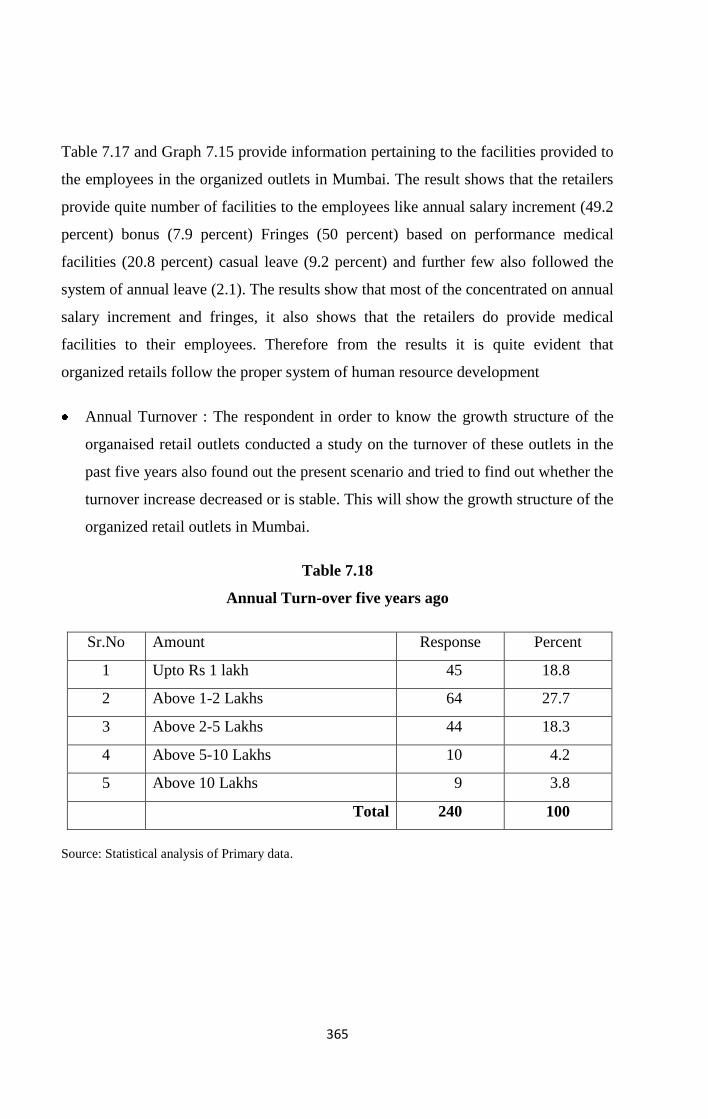

Annual Turnover : The respondent in order to know the growth structure of the

organaised retail outlets conducted a study on the turnover of these outlets in the

past five years also found out the present scenario and tried to find out whether the

turnover increase decreased or is stable. This will show the growth structure of the

organized retail outlets in Mumbai.

Table 7.18

Annual Turn-over five years ago

Sr.No Amount Response Percent

1 Upto Rs 1 lakh 45 18.8

2 Above 1-2 Lakhs 64 27.7

3 Above 2-5 Lakhs 44 18.3

4 Above 5-10 Lakhs 10 4.2

5 Above 10 Lakhs 9 3.8

Total 240 100

Source: Statistical analysis of Primary data.

366

Graph 7.16

Annual Turn-over five years ago

Table 7.18 and Graph 7.16 show the annual turnover in the last five years out of 240

respondents 45 respondents were of the opinion that their annual turnover is about one

lakh and 64 respondents replied it is between one to two lakhs with 44 responding that

it is between two to five lakhs and 10 were of the opinion that it is between five to ten

lakhs only there were 9 respondents who felt that there turnover is above ten lakhs.

The researcher believes that due to the infancy stage of the retail business in Mumbai

the turnover has been little less but the impact of globalization will gradually make

the difference in the future.

45

64

44

10

9

0 10 20 30 40 50 60 70

Upto Rs 1 lakh

Above 1-2 Lakhs

Above 2-5 Lakhs

Above 5-10 Lakhs

Above 10 Lakhs

Response

367

Table 7.19

Annual Turn-over now

Sr.No Amount Response Percent

1 Upto Rs 1 lakh 28 11.7

2 Above 1-2 Lakhs 43 17.9

3 Above 2-5 Lakhs 68 28.3

4 Above 5-10 Lakhs 21 8.8

5 Above 10 Lakhs 21 8.8

Total 240 100

Source : Statistical analysis of Primary data.

Graph 7.17

Annual Turn-over now

Further the researcher wanted to know the present status of these retailer therefore

Table 7.19 and Graph 7.17 shows the present picture of these retailers it is 28

respondents still feel that there turnover is still upto one lakh and 43 respondents

replied it is still maintaining between one to two lakhs with gradual increase in the

quantity of respondents in this category, 68 responding that it is between two to five

28

43

68

21

21

Response

Upto Rs 1 lakh

Above 1-2 Lakhs

Above 2-5 Lakhs

Above 5-10 Lakhs

Above 10 Lakhs

368

lakh and 21 were of the opinion that it is between five to ten lakhs only there were

further 21 respondents who felt that there turnover is above ten lakhs.

This shows that the organized retail outlets are gradually picking pace in Mumbai.

Therefore the change in economy and the change in consumer behavior has gradually

brought the difference in the annual turnover of the retailers.

To understand this researcher made an attempt to ascertain the annual turnover of the

organized retail outlets in the last five years. Since absolute figures of the annual sales

were not possible to obtain, therefore it is ascertain on the basis of the percentage.

Following table gives a clear scenario of the growth of the organized retail outlets.

Table 7.20

Annual turnover increased or decreased in the last five years

Sr.No

Response Percent

1 Increased 96 40

2 Decreased 88 37.7

3 Remained Same 13 5.4

4 No Reply 43 17.9

Total 240 100

Source : Statistical analysis of Primary data.

369

Graph 7.18

Annual turnover increased or decreased in the last five years

Table 7.20 and Graph 7.18 present picture of the growth of organized retail outlets in

Mumbai. The respondent surveyed 240 respondents to find out whether the annual

turnover in the last five years have increased or decreased or has remained the same

43 respondents decided to remain silent with no response 13 respondents felt that

there turnover has remained the same but the major difference could be seen when 96

respondent said there has been relative increase in the annual turnover and 88

respondents said there has been decrease. This study shows a conclusion that for

many retailers the development of organized outlets has been blessing by giving them

good turnover. Further the decrease can be covered in the future by systematically

handling the consumers

7.8 Testing of Hypotheses

Ho: Males and female opine equally that development of organized retail outlets

have reduced their visits to unorganized sectors.

0

10

20

30

40

50

60

70

80

90

100

Increased Decreased Remained Same

No Reply

9688

13

43

Response

370

H1: More female opine that development of organized retail outlets have

reduced their visits to unorganized sectors.

Mumbai a commercial capital and presence of an equal combination of gender

therefore there is least gender discrimination. The researcher wanted to find out

has the development of organized retail outlets reduced the visit of the

population to unorganized sector, to get a clear idea this result the researcher

wanted in gender wise and therefore framed a hypothesis. For testing this

hypothesis the researcher took parameter on the basis gender which justified the

opinion of women that it is the development of organized retail outlets that has

reduced their visits to unorganized outlets. Chi Square test is used on the various

primary survey and the results have been put up in the tabular form given

below:

Table 7.21

Calculation showing data of response on development of organized outlets

reduced visit to unorganized outlets

Source: Analysed from primary data.

Table 7.22

Chi-Square Test for impact of organized retail outlets on unorganized retail

outlets

Sr.No Response Sex Total

Male Female

1 Yes 237 (64.2%) 261 (73.7%) 498 (68.9%)

2 No 132 (35.8%) 93 (27.3%) 225 (31.1%)

369 (100%) 354 (100%) 723 (100%)

Value df

Asymp. Sig. (2-

sided)

Pearson Chi-Square 7.609(b) 1 .006

Continuity Correction(a) 7.172 1 .007

Source: Statistical analysis of primary data.

371

Chi Square test is applied to calculate the opinion of female who feel that due to

development of malls they totally have inclined to organized retail outlets and their

visit to unorganized outlets have been reduced, the researcher also tried to check the

frequency level of the increase. From Table 7.21 it is concluded that it is 261 (73.7

percent) of female respondent are of the opinion that malls have reduced their visit to

unorganized retail outlets. To this result Chi Square result in Table 7.22 gives an

indication of expected count less than 5 and the Pearson Chi Square result shows the

assume as .006 which is much less than the expected resulted. Thus Null hypothesis

that Males and female opine equally that development of organized retail outlets have

reduced their visits to unorganized sectors stands rejected. We conclude that more

female opine that development of organized retail outlets have reduced their visits to

unorganized sectors. Therefore the hypothesis stands to be authentic and it is proved.

Hypothesis 4

H0: Self employed, service class, Housewives and business class equally feel that

development of malls have created an impact on their budget.

H1: People from business feel that the development of malls has created an

impact on their budget.

Mumbai a city commercially viable and where there is assumption that

development is rapid. People belonging to business class have a belief that there

is an assumption that the development of the malls has created an impact on

their budget. The researcher wanted to find out has the development of

organized retail outlets have created an impact on their budget, to get a clear

idea an analysis is done taking the respondents belonging to various employment

parameters. Chi Square test is used on the various primary survey and the

results have been put up in the tabular form given below:

372

Table 7.23

Impact on the budget of consumers on the basis of Employment status

Source: Analysed from primary data.

Table 7.24

Chi-Square Test calculation on impact on the budget of consumers due to O.R

Value df

Asymp. Sig.

(2-sided)

Pearson Chi-Square 112.607(a) 10 .000

Likelihood Ratio 115.371 10 .000

Source: Statistical analysis of primary data.

Chi Square test is applied to calculate the opinion of people who belong to business

class on the development of malls and an impact on their budgets. From Table 7.23 it

is concluded that it is 36 (57.3%) of respondents belonging to business class feel that

there is an gradual impact on their budget due to the increase in malls in Mumbai. Chi

Square result in Table 7.24 gives an indication of expected count less than 5 and the

P-value shows the asymp as .000 which is much less than the expected count. Thus

Null hypothesis specifies that self employed, service class, housewives and business

class equally feel that development of malls have created an impact on their budget

stands rejected. We conclude that People from business feel that the development of

malls has created an impact on their budget. Therefore the hypothesis stands to be

authentic and it is proved.

S.No Response Employment Status Total

Self

Employed Service Business Retired

Not Employed

Currently

House-

wife

1 Yes,

Higher

spending

28 (45.2%) 162(48.9%) 36(57.3%) 8(15.7%) 95(57.2%) 31(67.4%) 360(49.8%)

2 Yes,

Lower

spending

15 (24.2%) 65(19.6%) 6(9.4%)

1(2.0%) 51(30.2%) 13(28.3%) 151(20.9%)

3 No 19(30.6%) 104(31.4%) 22 (34.4%) 42(82.4%) 23 (13.6%) 2(4.3%)

212

(29.3%)

Total 62 (100%) 331(100%) 64(100%) 51(100%) 169(100%) 46(100%) 723(100%)

373

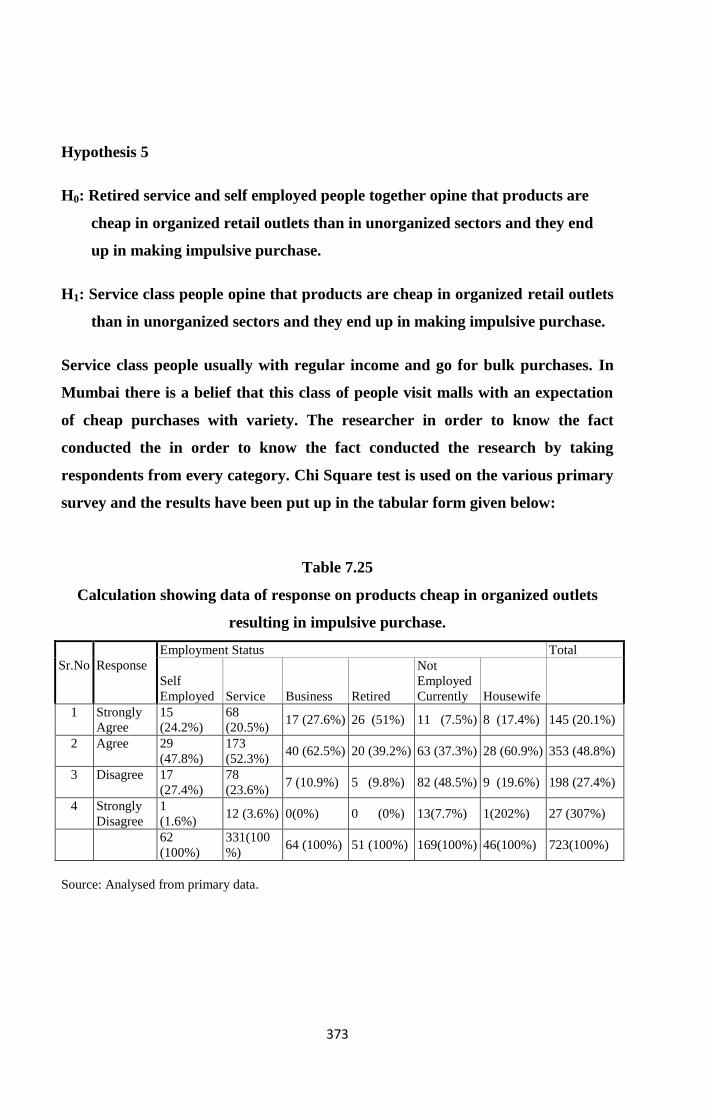

Hypothesis 5

H0: Retired service and self employed people together opine that products are

cheap in organized retail outlets than in unorganized sectors and they end

up in making impulsive purchase.

H1: Service class people opine that products are cheap in organized retail outlets

than in unorganized sectors and they end up in making impulsive purchase.

Service class people usually with regular income and go for bulk purchases. In

Mumbai there is a belief that this class of people visit malls with an expectation

of cheap purchases with variety. The researcher in order to know the fact

conducted the in order to know the fact conducted the research by taking

respondents from every category. Chi Square test is used on the various primary

survey and the results have been put up in the tabular form given below:

Table 7.25

Calculation showing data of response on products cheap in organized outlets

resulting in impulsive purchase.

Sr.No

Response

Employment Status Total

Self

Employed Service Business Retired

Not

Employed

Currently Housewife

1 Strongly

Agree

15

(24.2%)

68

(20.5%) 17 (27.6%) 26 (51%) 11 (7.5%) 8 (17.4%) 145 (20.1%)

2 Agree 29

(47.8%)

173

(52.3%) 40 (62.5%) 20 (39.2%) 63 (37.3%) 28 (60.9%) 353 (48.8%)

3 Disagree 17

(27.4%)

78

(23.6%) 7 (10.9%) 5 (9.8%) 82 (48.5%) 9 (19.6%) 198 (27.4%)

4 Strongly

Disagree

1

(1.6%) 12 (3.6%) 0(0%) 0 (0%) 13(7.7%) 1(202%) 27 (307%)

62

(100%)

331(100

%) 64 (100%) 51 (100%) 169(100%) 46(100%) 723(100%)

Source: Analysed from primary data.

374

Table 7.26

Chi-Square Test calculation on products cheap in organized outlets resulting in

impulsive purchase

Value df Asymp. Sig. (2-sided)

Value when

products are

cheap

Value when make

impulsive purchase df

Asymp. Sig. (2-

sided when

products are

cheap

Asymp.

Sig. (2-

sided)

Pearson Chi-

Square 107.998(a) 111.414(a) 15 .000 .000

Likelihood Ratio 107.892 89.525 15 .000 .000

Source: Statistical analysis of primary data.

Chi Square test is applied to calculate the assumption of why service class people visit

malls the most. From Table 7.25 it is concluded that it is 68 (20.5%) respondents

strongly agreed to this belief and 173 (52.3 %) of respondents agree to this fact .The

service class also feels that they end up in making an impulsive purchase due to the

products being cheap. Chi Square result in Table 7.26 gives an indication of expected

count less than 5 and the Pearson Chi Square result shows the asymp as .000 which is

much less than the expected count, therefore the hypothesis is proved further the

hypothesis also states that due to cheap products the service class people make an

impulsive purchases. Chi Square gives an indication of expected count less than 5 and

the Pearson Chi Square result shows the asymp as .300 which is less than the expected

count. Thus Null hypothesis that retired service and self employed people together

opine that products are cheap in organized retail outlets than in unorganized sectors

and they end up in making impulsive purchase stands rejected. We conclude that

Service class people opine that products are cheap in organized retail outlets than in

unorganized sectors and they end up in making impulsive purchase. Therefore the

hypothesis stands to be authentic and is proved.

375

7.9 Summary of the Study

Shopping in Malls has become the latest trend today. They are very popular among

people of all age groups. The reasons for their popularity are manifold. To begin with,

they sell all kinds of branded goods. People who opt for quality can get good products

here without much effort.

Furthermore, these Malls are not crowded and one can shop here with much comfort.

Shopping in these spacious places is indeed easy. Although they are crowded

sometimes, there is ample space for easy movement which makes shopping fun and a

memorable experience. To illustrate, since they are built in a large area they are very

spacious. In addition, climbing up and down the stairs can be avoided because of the

escalators as well as the lifts. Moreover, the malls not only sell commodities such as

garments, gadgets, cosmetics etc but also sell food items. In addition, there is a food

court on the top floor which sells various types of lip smacking food .These food

joints are obviously very much in demand by the teenagers.

Understanding these reasons the researcher tried to find out the range of popularity of

these malls and asked the respondents to rank the reasons of popularity in the scale of

1-5. The results are put up in tabular form given below.

376

Table 7.27

Rating for Reasons of popularity of Malls (1-5)

Source: Statistical analysis of Primary data.

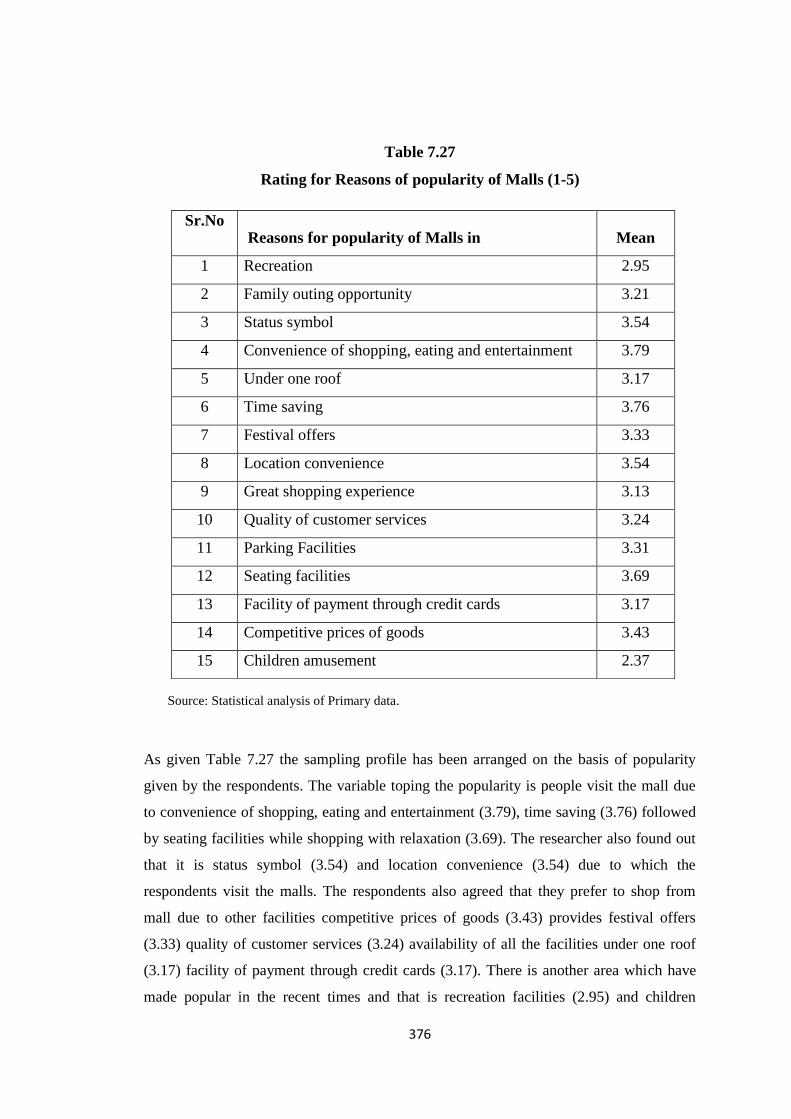

As given Table 7.27 the sampling profile has been arranged on the basis of popularity

given by the respondents. The variable toping the popularity is people visit the mall due

to convenience of shopping, eating and entertainment (3.79), time saving (3.76) followed

by seating facilities while shopping with relaxation (3.69). The researcher also found out

that it is status symbol (3.54) and location convenience (3.54) due to which the

respondents visit the malls. The respondents also agreed that they prefer to shop from

mall due to other facilities competitive prices of goods (3.43) provides festival offers

(3.33) quality of customer services (3.24) availability of all the facilities under one roof

(3.17) facility of payment through credit cards (3.17). There is another area which have

made popular in the recent times and that is recreation facilities (2.95) and children

Sr.No Reasons for popularity of Malls in Mean

1 Recreation 2.95

2 Family outing opportunity 3.21

3 Status symbol 3.54

4 Convenience of shopping, eating and entertainment 3.79

5 Under one roof 3.17

6 Time saving 3.76

7 Festival offers 3.33

8 Location convenience 3.54

9 Great shopping experience 3.13

10 Quality of customer services 3.24

11 Parking Facilities 3.31

12 Seating facilities 3.69

13 Facility of payment through credit cards 3.17

14 Competitive prices of goods 3.43

15 Children amusement 2.37

377

amusement (2.37). Due to the vast facilities people are diverting towards Shopping

Malls for the purpose of shopping of various products. One can shop for hours in air-

conditioned premises. Shopping Malls are getting more and more popularity mainly

among teenage youth. The researcher concluded that the modern generation slowly is

drifting towards malls due to time constrains.

The survey also throws light on the fact that shoppers do not shop exclusively at the

organized or the unorganized outlets. They shop at both outlets and the share of spending

varies from product to product. Even those who were interviewed at organized outlets,

declared that 43-46 per cent of their spending on vegetables, fruit, non-staple food items,

cooking oil and other packaged food items was from unorganized outlets. Table 7.28 and

Table 7.29 which clearly shows the ranking of organized and unorganized retail outlets

with the help of mean deviations.

On the whole, the sample shoppers at organized outlets make their spending on food and

grocery, and textiles and clothing at unorganized outlets. Similarly, consumers

interviewed at unorganized outlets also spend at organized outlets. The researcher

absorbed that on an average, the respondents spend their monthly shopping e at organized

outlets. The table below mentions the popularity of both the organized and unorganized

retail outlets on the basis of scales given.

To understand this researcher asked the respondents to rank the facilities provided by

both organized and unorganized retail outlets on 1-8 popularity scale. Further the results

collected are converted on mean deviations and presented in the Table 7.26 (ranking of

organized retail outlets) and 7.27 (Ranking of unorganized retail outlets).

378

Table 7.28

Ranks for Organized Retail Outlets

Sr.No. Particulars Mean

1 Display 5.62

2 Availability of all Brands 7.16

3 Status 5.95

4 Promotional Schemes 5.48

5 Financial Schemes 5.20

6 Sales person's interaction 5.56

7 Home Delivery 5.15

8 After sales services 5.60

Source: Statistical analysis of Primary data.

Table 7.28 shows the result of the popularity of organized retail outlets with the

consumers in Mumbai. It is basically the availability of all brands (7.16) due to which

the consumers visit organized retail outlets more. The organized retail outlets posses

the status (5.95) symbol a lot the consumer, are pulled towards them due to the

presentability of these outlets. Further it is the window display (5.62) which attract,

the consumers more to the outlets giving them the feel of touch and see. The

drawback of these outlets being lack of financial schemes (5.20) and home delivery

(5.15) due to which the unorganized outlets are popular in India and Mumbai.

379

Table 7.29

Rank for Un-Organized Retail Outlets

Sr.No. Particulars Mean

1 Proximity/Convenience 5.46

2 Trusted Brands 5.73

3 Trust worthiness of owner 5.58

4 Home delivery of all Products 4.39

5 Promotions 4.74

6 Availability of Financial Services 5.15

7 Hospitality provided by the owner 4.56

Source : Statistical analysis of Primary data.

Table 7.29 shows the result of the popularity of unorganized retail outlets with the

consumers in Mumbai. It is basically the trusted (5.73) due to which the consumers

visit unorganized retail outlets even today, Indian consumers make purchases only

after having confidence on the sellers because of their emotional attachment therefore

in spite of organized outlets moving fast in Mumbai still unorganized outlets are

popular due to trust worthiness on the owner (5.58). The consumers till date are

inclined towards the unorganized outlets due to the fact of proximity/convenience

(5.46), availability of financial service (5.15), home delivery (4.39) and most

importantly it is hospitality provided by the owner (4.56).

The results analyzed by the researcher clearly show an indication that it is both the

sectors that are equally surviving in Mumbai market with both sectors having their

own different place in the minds of the consumers.

7.10 Conclusion

The researcher made a sincere attempt to collect and analyze the data of retail outlets

in Mumbai and finally interpreted the same to arrive at the conclusion. The researcher

came to the conclusion that slowly and steadily organized retail outlets are capturing

the city but still there is an impact of unorganized outlets.

380

Furthermore the researcher was of the neutral view which rests on the possibility of

the co-existence of the organized and unorganized retailers in the country. Such co-

existence is justified largely by different combinations of benefits and conveniences

offered by each sector to its customers. While organized retail outlets offer

merchandise at cheaper prices and provide a convenient shopping environment,

unorganized retailers provide great convenience in the form of cash credit on goods

and home-delivery services. To justify this the researcher reviewed the report of AC

Nielsen presented in 2007, which focused on the buying behaviors of consumers from

organized and unorganized retail outlets, found that while penetration of grocery

retailing had occurred much more rapidly in processed, dry, and packaged foods,

household products and personal care items, for which supermarkets gain a cost

advantage due to economies of scale resulting from centralized procurement and

distribution, shoppers still mainly used wet markets and small vegetable stalls, where

they got low prices, credit, and personal service, for more frequent purchases of fresh

produce . Similarly, such different retail preferences for distinct categories of goods