Embed Size (px)

Citation preview

Analyst Professional Development Seminar

NASBO Staff:

Stacey Mazer

Brian Sigritz

Kathryn White

2

www.nasbo.org

Leah Wavrunek

Lauren Cummings

Brukie Gashaw

www.nasbo.org

3

www.nasbo.org

Current Economic and Fiscal Situation for States

4

www.nasbo.org

5

State Fiscal Overview

Fiscal 2016 -- 6th consecutive annual increase in general fund spending and revenues

Most states: continued stability and slow growth▫ Less midyear cuts and budget gaps▫ Most states ended fiscal 2015 with revenues above projections or on target

Common theme in State of States of need to create jobs, grow the economy, and provide opportunity for all to succeed▫ Many said need to prioritize transportation, education, and workforce training to

achieve this goal

Some states are facing difficult budget environments due to various issues

Fiscal improvements over the last several years have not returned states to normal patterns of growth

www.nasbo.org

6

Major Challenges to State Budgets: 2016+ Revenues and spending have yet to surpass pre-recession highs

after accounting for inflation

▫ Revenue growth projected to be modest in fiscal 2016

Future economic growth

Health care costs

Pensions and retiree health care

Infrastructure

Certain states impacted by oil price declines, federal cuts, tax related issues, long-term liabilities, slow economic growth, etc.

Federal uncertainty

Debt service levels around 5%, very manageable

www.nasbo.org

Current Fiscal Situation:Indicators

7

www.nasbo.org

8

Slow Budget Growth Continues

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

-8

-6

-4

-2

0

2

4

6

8

10

12

General Fund Expenditure Growth (%)

%

*Average

*38-year historical average annual rate of growth is 5.5 percent *Fiscal 2015 numbers are estimated; fiscal 2016 are recommended Source: NASBO Spring 2015 Fiscal Survey of States

www.nasbo.org

9

States Direct Most New Spending to K-12 and Medicaid

K-12

Higher Ed

Public Ass

ist.

Medica

id

Correcti

ons

Transp

ortatio

n

All Other

-2

0

2

4

6

8

10

12$10.2

$2.6

$0.1

$9.2

$1.8

-$0.7

$6.4

FY 2016 Recommended General Fund Spending Changes by Category

($ in

Bill

ions

)

Source: NASBO Spring 2015 Fiscal Survey

www.nasbo.org

10

Fiscal 2015 GF Revenue Below Pre-Recession Peak After Inflation

FY 2007 FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016$500

$550

$600

$650

$700

$750

$800

$655$680

$626$610

$650

$669

$716$728

$755

$778$772*

General Fund Revenue: FY 2007-FY 2016

Source: NASBO Spring 2015 Fiscal Survey of States; Fiscal 2016 numbers are recommended*Aggregate revenue levels would need to total $772 billon in fiscal 2015 to be equivalent with real 2008 revenue levels.

www.nasbo.org

11

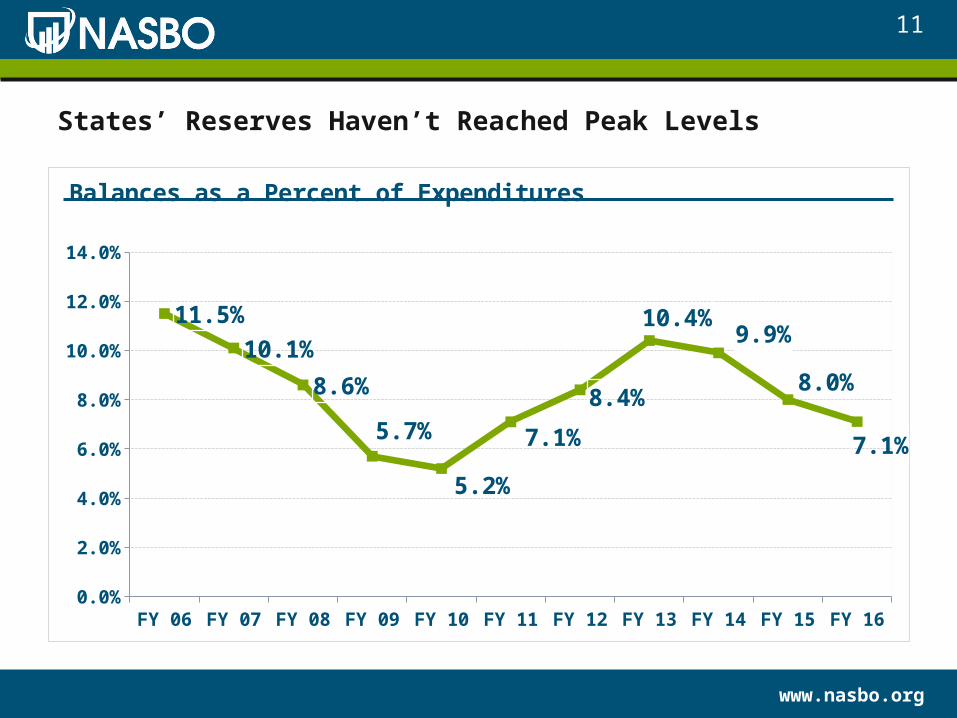

States’ Reserves Haven’t Reached Peak Levels

FY 06 FY 07 FY 08 FY 09 FY 10 FY 11 FY 12 FY 13 FY 14 FY 15 FY 160.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

11.5%

10.1%

8.6%

5.7%

5.2%

7.1%

8.4%

10.4%9.9%

8.0%

7.1%

Balances as a Percent of Expenditures

www.nasbo.org

12

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

$0

$5

$10

$15

$20

$25

$30

$35

$40

0

10

20

30

40

50

20

28

35

22

9 813

72 3 1

16

37 37

18

5 2 4

13

41 39

23

811

811

Enacted Budget Cuts Made After the Budget Passed

Number of states Amount of reduction

$ In

Mill

ions

Num

ber o

f Sta

tes

Recession ends

Recession ends

Recession ends

Midyear Budget Cuts Relatively Minimal in Fiscal 2015 at $2B

Source: NASBO Spring 2015 Fiscal Survey *Fiscal 2015 midyear cuts are ongoing

www.nasbo.org

13

Critical Challenges

www.nasbo.org

14

www.nasbo.org

15

www.nasbo.org

16

Higher Education Funding

States to Colleges: Prove You’re Worth It▫- July 28, 2015 (Stateline)

More States Grade Public Colleges on Performance▫June 23, 2015 (CNBC)

www.nasbo.org

17

State Severance Tax Revenue as a Percentageof Total State Tax Collections

Alaska

North

Dak

ota

Wyo

ming

New M

exico

Wes

t Virg

inia

Mon

tana

Texas

Louis

iana

Okla

hom

a0

20

40

60

80 72.4

53.8

39

18.512.7 11.5 10.9 8.9 7.5

Fiscal 2014

%

Source: U.S. Census Bureau

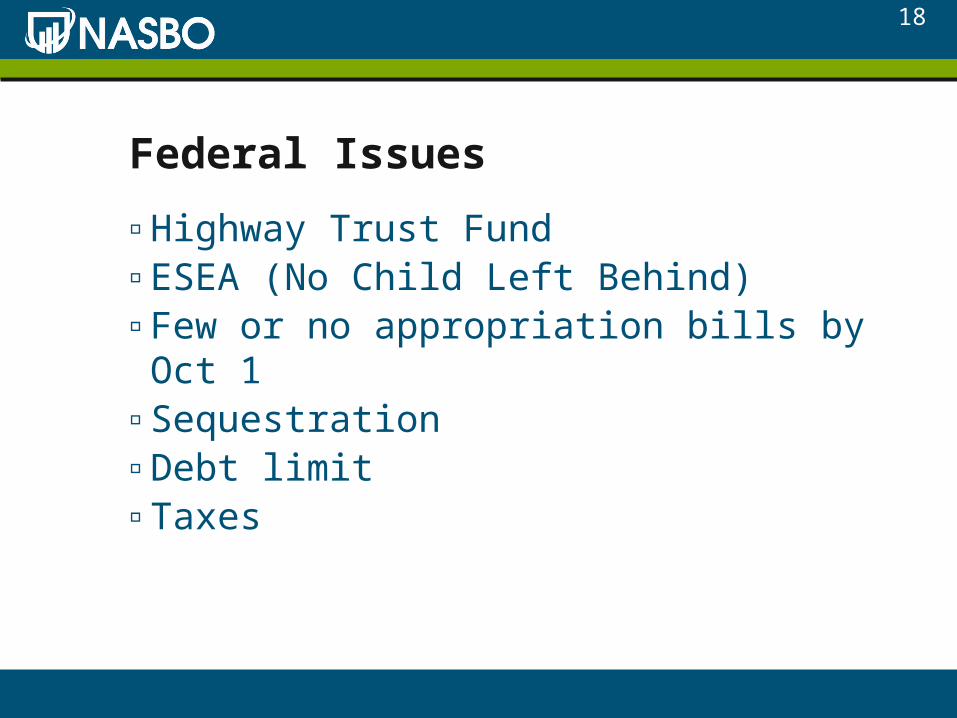

Federal Issues

▫Highway Trust Fund▫ESEA (No Child Left Behind)▫Few or no appropriation bills by Oct 1▫Sequestration ▫Debt limit ▫Taxes

18

Revenue Issues

▫Revenues recovering slowly compared to past recession

▫Greater volatility▫April windfall▫Gaming becoming limited

19

www.nasbo.org

20

Background on State Spending Trends

www.nasbo.org

21

Source: NASBO State Expenditure Report

www.nasbo.org

22

Total State Expenditures by FunctionEstimated Fiscal 2014

Elementary & Secondary Edu-

cation19.5%

Higher Education10.1%

Public Assistance1.4%

All Other32.4%

Corrections3.1%

Transportation7.7%

Medicaid25.8%

Source: NASBO State Expenditure Report

www.nasbo.org

23

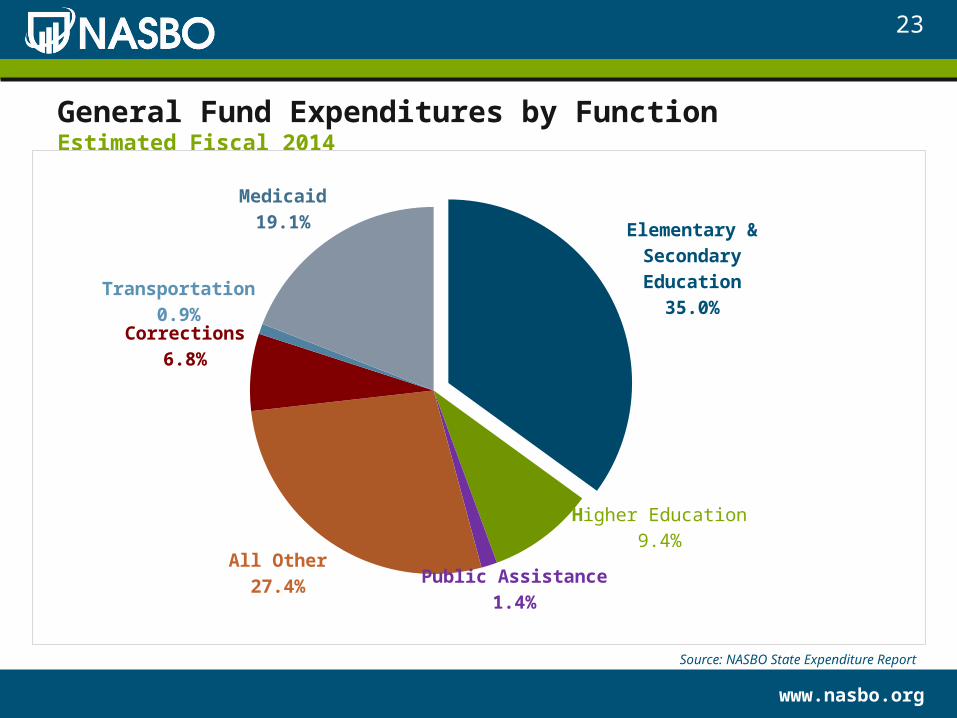

General Fund Expenditures by FunctionEstimated Fiscal 2014

Elementary & Secondary Ed-

ucation35.0%

Higher Education9.4%

Public Assistance1.4%

All Other27.4%

Corrections6.8%

Transportation0.9%

Medicaid19.1%

Source: NASBO State Expenditure Report

www.nasbo.org

24

Federal Funds Expenditures by FunctionEstimated Fiscal 2014

K-129.9%

Higher Education3.7%

Public Assistance2.6%

All Other25.0%

Corrections0.1%

Transportation7.7%

Medicaid51.0%

Source: NASBO State Expenditure Report

www.nasbo.org

25

Revenue Sources in the General Fund (Percentage)

Sales 31%

Personal Income 42%

Corporate Income 6%

Gaming 1%

Other Taxes & Fees 20%

Estimated Fiscal 2014

Source: NASBO State Expenditure Report

www.nasbo.org

Outlook

26

www.nasbo.org

27

State Fiscal Outlook

42 states recommended general fund spending increases in FY 2016, but growth still below average

Revenue growth projected to remain slow in fiscal 2016

Uncertainty remains concerning federal spending decisions and ACA implementation

Tough competition for general funds

Dealing with infrastructure, long-term liabilities

States will continue to make some painful choices

www.nasbo.org

28

Decision Making

You make important decisions in the public arena. Public policy decision making shapes our lives in many ways.

Analyze what processes are followed in public policy decision making by government officials at all levels, from elected officials to mainstream managers.

Analyze how the processes themselves impact the outcomes. How are important decisions made?

29

Relationships

Critical: your reputation, interaction, building of trust

While sunshine laws and rules governing open meetings are the norm, decisions are often made based on understandings and agreements forged between individuals in informal settings.

30

Don’t let emotions get in the way…

Pitfalls of groupthink

In large scale public policy endeavors, the involvement of groups is absolutely essential.

However, as shown with the Challenger launch decision, groupthink can also adversely affect organizational success.

32

33