Embed Size (px)

DESCRIPTION

Project is on analysis of unsecured loan

Citation preview

CHAPTER 1INTRODUCTION

INTRODUCTION

This project report deals with the analysis of unsecured loan (personal loan) at SBH bank, Latur. The analysis includes the main emphasis on the share of personal loan in the total unsecured loan of the SBH bank as well as it comprises with the defaulters of the personal loan. The data collected for the years of 2009, 2010, &2011.The project also focuses on the reasons for the rejection of the loan proposal of the customers & the reasons for the defaulter of the loan. The case study about rejection of loan proposals & defaulter of loan gives practical point of view. The project includes the requirements of documents for the loan proposal & eligibility criteria for the same.

Unsecured loans which are usually carrying greater risk comprises of:-

Personal loan Credit card

Unsecured loans are characterized by:-

Higher interest rates and Offer higher margin than secured advances

1.2 IMPORTANCE OF TOPIC

The main aim of this project is to understand the importance of the unsecured loan from the point of view of the banker as well as the customer .The project also looks towards the risk factor behind issuing unsecured loan.The SBH Bank is recognized bank for its services to the customer so the study of the SBH Banks policy for the recovery of the defaulters loan amount (NPA) is also important for the researcher.

1.3 SELECTION OF TOPIC

As compare to the secured loans like car loan, home loan etc the unsecured loan is very risky to issue because they don’t need any security lag behind for the recovery if customer not being able to repay the loan. This loan is issued on the basis of credit rating of the customer. Another aspect of unsecured loan is that it yields high returns than that of others. Since, it possesses the high risk; the rate of interest of unsecured loans is higher than others.SBH Bank is the leading bank in the banking sector. There must be interested & curious part for the researcher to understand the SBH Banks performance in this sector.

1.4 OVERVIEW OF THE BANKING SECTOR

“In 1949, two major actions were taken which was very important from the point of view of structural reforms in banking sector. Firstly, the banking regulation act was passed. It gave extensive regulatory powers to reserve bank of India (RBI) over the commercial banks. Another development of no less importance was the nationalization of the RBI.”

In the early 1990s, the government embarked on a policy of liberalization, licensing a small number of private banks. These came to be known as New Generation tech-savvy Banks, and included Global Trust bank (the first of such new generation banks to be set up), which later amalgamated with Oriental Bank of Commerce, Axis Bank (earlier as State Bank of India),ICICI Bank and SBH Bank this move along with the rapid growth in the economy of India, reutilized the banking sector in India, which has seen rapid growth with strong contribution from all the three sectors of banks, namely government bank, private bank and foreign banks.

Liberalization and de-regulation process started in 1991-92 has made sea chances in the banking system. From a totally regulated environment, we have gradually moved into a market driven competitive system. The pace of chances gained momentum in the last few years. Globalization would gain greater speed in the coming years particularly on account of expected opening up of financial services under WTO. Four trends change the banking industry world over, viz.

1.Consolidation of players through mergers and acquasitions.

2.Globalization of operations

3.Development of new technology

4.Universalization of banking

One of the concerns is quality of bank lending. Most significant challenge before banks is the maintenance of rigorous credit standards, especially in an environment of increased competition for new and existing clients.

Experience has shown us that worst loans are often made in the best of times. Compensation through trading gains is not going to support the banks forever. Large scale efforts are needed to upgrade skills in credit risks measuring, controlling and monitoring as also revamp operating procedures. Credit evaluation may have shift from cash flow based analysis to “borrower account behavior”. Corporate lending is already undergoing changes.

In Indian context, there has been a close relationship between industry and political parties; industry being the major source of funding for elections. In such a scenario consern or favour for industry or particular industrial groups gets appropriately addressed by the political executive while designing or framing policies.

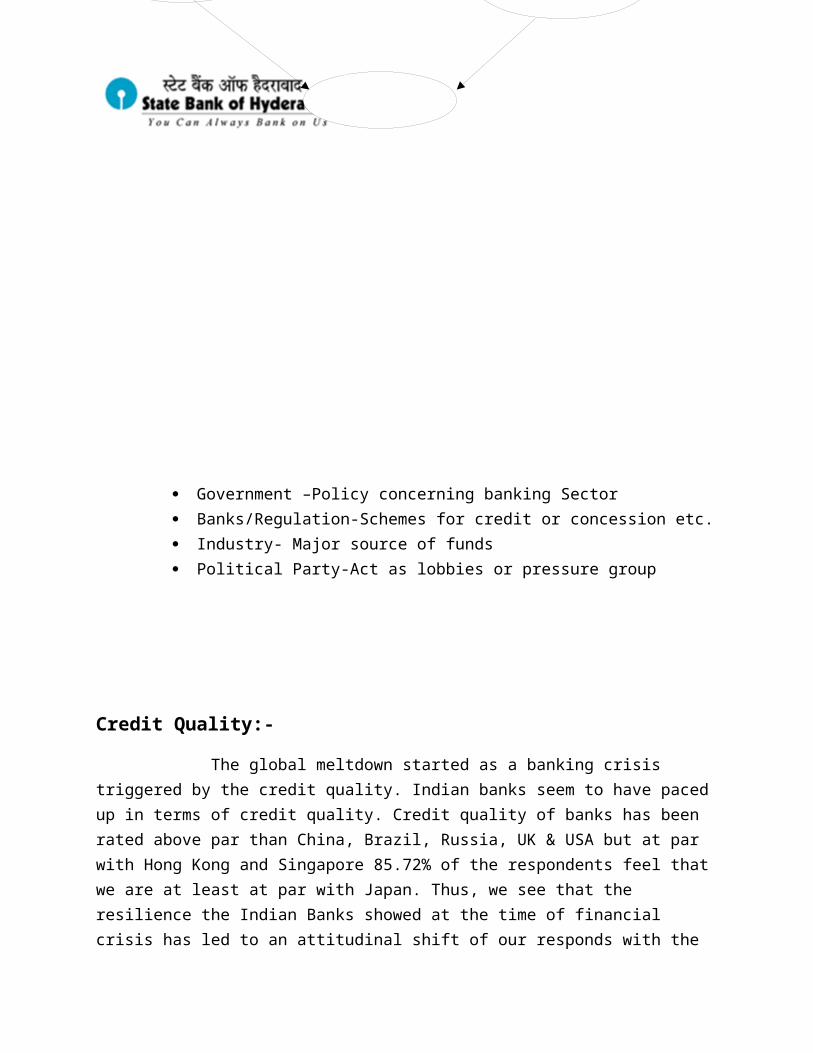

Bank-Industry Interface Reflecting Political Factor:-

Government –Policy concerning banking Sector Banks/Regulation-Schemes for credit or concession etc. Industry- Major source of funds Political Party-Act as lobbies or pressure group

GOVERNMENT

BANKS/

REGULATOR

POLITICAL PARTY

INDUSTRY

Credit Quality:-

The global meltdown started as a banking crisis triggered by the credit quality. Indian banks seem to have paced up in terms of credit quality. Credit quality of banks has been rated above par than China, Brazil, Russia, UK & USA but at par with Hong Kong and Singapore 85.72% of the respondents feel that we are at least at par with Japan. Thus, we see that the resilience the Indian Banks showed at the time of financial crisis has led to an attitudinal shift of our responds with the past survey indicating credit quality of Indian banks being below par than that US and UK.

Currently, India has 88 scheduled commercial banks (SCBs)-28 public sector banks (that is with the Government of India holding a stake), 29 private banks (these do not have government stake; they may be publically listed and traded on stock exchanges) and 31 foreign banks. They have combined network of over 53,000 branches and 17,000 ATMs. According to a report by ICRA limited, a rating agency, the public sector banks hold over 75 percent of total asset of banking industry, with the private and foreign banks holding 18.2% and6.5% respectively.

The Indian banking sector is poised to become the world’s third largest in asset size over the next 14 years, a report released recently said. “The domestic banking industry is set for an exponential growth in the coming years with its assets size poised to touch USD 28,500 billion by the turn of the 2025 from the current asset size of USD 1,350 billion (2010)” says an IBA-FICCI-BCG report titled “being five star in productivity-roadmap for excellence in Indian Banking, prepared for the Indian banks association.

“It is noteworthy that in the recent past bank lending did not take place as fast as the deposits had grown. Consequently credit –deposits ratio which stood at 80.8 on 30th March 1976 declined to 72.4 as on 27th March 2010.”

CHAPTER -2

PROFILE OF STATE BANK OF HYDERABAD

2.1 INTRODUCTION OF THE BANK

State Bank of Hyderabad (SBH) is an associate bank of State Bank of India (SBI), and is one of the scheduled banks in India. The Bank's Head Office is situated at Gunfoundry Area, in Hyderabad, India. SBH has over 1,200 branches and about 12,800 employees. Assets are in excess of Rupees 767 billion. It is now the largest Associate Bank of State Bank of India.

The bank has performed well in the past decades, winning several awards for its banking practices.[1] Shri Pratip Choudhary is the current Chairman and Sri. M Bhagavantha Rao is the current Managing Director

2.2 HISTORY OF THE BANK

Vision Statement of the Bank:-

To be a vibrant, forward looking, techno-savvy, customer centric bank serving diverse sections of the society, enhancing shareholders’ and employees’ value while moving towards global presence.

The bank originated as the central bank of the erstwhile Nizam state under the name, Hyderabad State Bank. It was established on 8 August 1941 under the Hyderabad State Bank Act, 1941, during the reign of the last Nizam of Hyderabad, Mir Osman Ali Khan. The bank managed the Osmania Sicca, the currency of Hyderabad state, which covered the present-day Telangana region of Andhra Pradesh, Hyderabad-Karnataka of Karnataka and Marathwada of Maharashtra. (At the time a number of the princely states had their own currencies.) The bank also carried out commercial banking. The Bank opened its first branch at Gunfoundry, Hyderabad on 5 April 1942. After Partition, on September 17, 1948 the Indian Army conducted Operation Polo, a “police action” that annexed Hyderabad to India.

In 1953, the bank absorbed, by merger, the Mercantile Bank of Hyderabad, which Raja Pannalal Pitti had founded in 1935. (Other accounts give year of founding as 1946 and that of merger as 1952). In the same year, the Bank started conducting government and Treasury business as agent for the Reserve Bank of India.

In 1956 the Reserve Bank of India took over the bank as its first subsidiary and renamed it State Bank of Hyderabad. The Subsidiary Banks Act was passed in 1959, so on 1 October 1959 it and the other banks of the princely states became subsidiaries of SBI.

2.3 PRODUCT & SERVICES

PRODUCTS:-

Deposits Loans Investment/Insurance Cards Online Services Wealth Management Money Transfer Bank Accounts

SBHs wide product range includes loans for purchase and construction of aresidential unit, purchase of land, home improvement loans, non residential premieses loans for professionals and loan against property,while its flexible repayment options include step up repayment facility (SURF) and flexible loan installment plan (FLIP).

SERVICES:- Property Solutions Insurance Corporate Net Banking Cash Management FX Online SME Services Online Taxes Custodial Services

SBH also provide wide range of services for his customers. Other than this SBH provides various other services for its priority customers for more conveniences and satisfaction.

2.4 ORGANIZATIONAL CHART

ORGANISATION CHART OF THE COMPANY

CHART OF DEPARTMENTS

2.5 KEY BUSINESS AREA OF OPERATION

STATE BANK OF HYDRABAAD

RETAIL BANKING

CORPORATE BANKING

RURAL BANKING

1. Retail Banking:-

The Retail Banking Group of the SBH Bank is responsible for products and services for retail customers and small enterprises including various credit products, liability products, distribution of third party investment and insurance products and transaction banking services.

2. Corporate Banking:- The corporate banking division provides comprehensive and customized financial solutions to the banks corporate customers. This segment offers a complete range of corporate banking products including rupee and foreign currency debt, working capital credit, structured financing, syndication and transaction banking products and services.

A. Small and medium enterprises:- SBH Bank believes in the franchise model for the small enterprises segment and has significantly enhanced its franchise this segment. As matter of strategy, the bank has focused on customer convenience in transaction banking services, as well as working capital loans to suppliers or dealers of large corporations, and clusters of small enterprises that have a homogeneous profile.

B. Project Finance:- The Indian economy is witnessing resurgence in investment activity with companies undertaking both brown field and green field expansions across sectors like infrastructure, oil & gas, manufacturing, etc. SBH bank is uniquely positioned to meet the funding requirements of companies by leveraging its domestic and overseas presence to offer innovative financing solutions. The key to its project finance proposition is its constant endeavor to add value to the project through financial structuring to ensure back ability of such project. These services are backed by strong due diligence and structuring skills and extensive relationships with various international sponsors and consultants. Equal emphasis is laid on ensuring marketable debt structuring.

3. Rural Banking:-

Under its rural banking strategy, SBH has adopted a holistic approach to the financial services needs of various segments of the rural population, by delivering a comprehensive product suite encompassing credit, transaction banking, deposit, investment and insurance, through a range of channels. Rural delivery channels include branches, internet kiosks, franchisees and micro finance institution partners. The rural economy represents a large latent demand for financial services including credit products, savings products, investment products and risk mitigation products like insurance. However, the delivery of financial services in rural areas presents a set of unique challenges.

2.6 ADVANTAGES OF SBH BANK

Pioneers of Housing Finance in India with over 33 years of lending experience.

Widest range of home loan & deposit products.

Vast network of over 283 interconnected offices which includes 3 international offices.

Most experienced and empowered personal to ensure smooth & easy processing.

Online loan application facility at www.sbh.com and across the counter services for new deposits, renewals & repayments.

Counseling and advisory services for acquiring a property.

Flexible loan repayment options.

Free & safe document storage.

CHAPTER - 3REVIEW OF LITERATURE

3.1 CONCEPT OF USECURED LOAN

Meaning of Unsecured Loan:-

An ‘unsecured loan’ is a loan that is not backed by collateral finance collateral. It is also known as a “signature loan” or “personal loan”. Unsecured loans are based solely upon the borrower’s credit rating. As a result, they are often much more difficult to get than asecured loan, which also factors in the borrower’s income.

However, an unsecured loan is considered much cheaper and carries less risk to the borrower. However, when an “unsecured loan” that is not backed by collateral, AKA “signature loan” or “personal loan” is granted, it does not necessarily have to be based on a credit score. For example, if your friend loans you money without any collateral finance collateral, meaning something of worth that can be repossessed if the loan isn’t repaid, then your credit score has zero to do with it, but rather the value of your friendship is at stake. Therefore the real meaning of an unsecured loan is that it is not backed by any object of value and is loaned to you based on your good name.

For financial institutional purposes, they may want to look at your credit score because they are not your friends and it is strictly a business transaction, therefore your good name may be associated with your historical payment history on prior debt, reflecting in your credit score. There are three types of unsecured loans. First there is a personal unsecured loan, meaning a loan that you individually are responsible for the repayment of, second is an unsecured business loan which leaves the business responsible for the repayment, and finally there is an unsecured business loan with a personal guarantee. With latter, although the borrower is the business, you as an individual will be payer of last resort if the business default on the loan.

3.2 DEFINITIONS

1] “Loan that establishes consumer credit that is granted for personal use; usually unsecured and based on the borrower’s integrity and ability to pay called personal loan.”

2] “A personal loan is an unsecured loan, meaning the borrower does not put up any collateral or security to guarantee the repayment of the loan. For this reason personal loans tend to carry high interest rates. If a borrower owns a home, a lower interest rate alternative is a home equity loan. However, this option requires that the borrower put up his or her home or other real estate property as collateral.

3] “An amount given to an individual to use for personal benefit that must be paid off at a specified time is called as personal loan.

4] “Unsecured loans are sometimes called ‘signature loans’ because the bank has nothing nut your signature – they can’t take possession of your house, car, or other belongings. However, they can report you to the credit reporting companies and ding up your credit.

5] “Loan extended only on the basis of the borrower’s financial position, creditworthiness, credit history, and general reputation. The borrower signs a promissory note but does not pledge any specific asset(s) as collateral. It is also called character, good faith loan, or signature loan.

3.2 INSIGHT INTO PERSONAL LOAN

Personal Loan:-

Personal loan is an all-purpose loan, which is given in most cases without any kind of security like car, home, shares etc.

Lenders:-

Most nationalized, foreign, and co-operative banks offers personal loans. Besides banks, some other finance companies and financial institutions also offer them.

Lending Rates:-

Lending rates differ for different financiers and currently range from 17 to 32 percent.

Minimum & maximum amount that can be issued as a personal loan:-

Personal loan are available in the range of Rs.50000 to 15 lack.

Tenure Possible:-

The period varies widely; some lenders usually permit repayment up to a maximum of 60 months. However most lenders restrict the lending to a maximum period of 36 months.

Repayment:-

Issuing post dated cheques for entire tenure of the contract does repayment of the loan. The amount of post-dated cheques would be EMI. Some lenders also permit repayment option by way of standing instruction to your bank account or deduction at source from your salary every month.

3.4 CREDIT RATING/SCORING

Credit rating is a system card issuers use to help determine whether to give you credit. Information about you and your credit experiences, such as your bill paying history, the number and type of accounts you have, late payment, collection actions, outstanding debt, and the age of your accounts, is collected from your credit application and your credit report. Using a statistical program, creditors compare this information to the credit performance of consumers with similar profits.

A credit scoring system awards points for each factor that helps predict who is most likely to repay a debt. A total number of points, a credit score, help you to predict how creditworthy you are, that is, how likely it is that you will repay a loan and make the payment when due.

How do I improve my credit rating/score?

Improving your credit rating can be a confusing and tedious process. If you are seeking to “repair your credit”, you will have to consider the following resources, which delivers to “do-it-yourself” approach to credit repair. Ventura is recognized as a leading authority on credit related subjects. This 263- page paperback can be purchased online only $7.95, considerably cheaper than other “credit repair kits” (many of which are not reputable). You may also find the following free resources to be beneficial.

If you would prefer to have a third party assist you with improving your credit rating, consider utilizing Lexngton law firm. While regular credit repair work by Lexngton law firm requires a monthly payment of at least $ 75 per month, internet users are now being allowed, in limited numbers, to participate in the client program at only $ 35 per month! Client includes the same proven service as the regular retainer, but requires that you conduct most communications with the firm by email. By using the internet to save on expensive staffing, Lexngton is able to pass along a significant bargain. Lexngton claims to provide the lowest cost, most effective, credit repair option available in the United States.

3.5 NPA (NON PERFORMING ASSET)

Those are the asset for which interest is overdue for more than 180 days. In simple words, an asset (or a credit facility) becomes non-performing when it ceases to yield income. As a result, banks do not recognize interest income on these assets unless it is actually received. If interest amount is already credited on an accrual basis in the past years, it should be reversed in the current year’s account if such interest is still remaining uncollected.

Once an asset falls under the NPA category, banks are required by the Reserve Bank of India (RBI) to make provision for the uncollected interest on these assets. For the purpose they have to classify their assets based on the strength and on collateral securities into:

Standard Assets:- This is not a non-performing asset. It does not carry more than normal risk attached to the business.

Substandard Assets:- It is an asset, which has been classified as non-performing for a period of less than two years. In this case the current net worth of the borrower or the current market value of the security is not enough to ensure recovery of the debt due to the bank. The classification of substandard assets should not be upgraded (to standard assets) merely as a result of rescheduling of the payments. (Rescheduling indicates change in payment schedule by the borrower or by the banker) There must be a satisfactory performance for two years after such rescheduling.

Doubtful Assets:- It is an asset, which has remained non-performing for a period exceeding two years.

Loss Assets:- It is an asset identified by the bank, auditors or by the RBI inspection as a loss asset. It is an asset for which no security is available or there is considerable erosion in the realizable value of the security. (If the realizable value of the security as assessed by bank, approved values or RBI is less than 10% of the outstanding, it is known as considerable erosion in the value of asset.) As a result even though there may be some salvage or recovery value, its continuance as bankable asset is not warranted.

3.6 ENVIRONMENTAL THREAT AND OPPORTUNITIES

ENVIRONMENTAL NATURE OF IMPACT ON PERSONAL FACTOR IMPACT LOAN

Inflation There is an impact of inflation on growth Rate of personal loan because demand will decrease.

Competitor It has an impact on it if competitor lending loan at less interest rate then it will affect

the growth of personal loan of bank.

RegulatoryRBI which regulate the banking policy has an impact on growth of personal loan of bank.

Defaulter Defaulter increase the NPA of bank.

Political No significant impact on bank.

Social culture standard of living of Urban & Suburban area is changing, demand for loan also increasing.

3.7 RECOVERY OF LOANS

We keep reading about SBH using third party agencies to recovery money. This is a right you given them when you sign up for a personal loan with them. In the event of a default, SBH bank shall, at the cost of the borrower, hire one or more persons to collect the borrower’s dues and to quote them, SBH bank may (for such purposes) furnish to such person(s) such information, facts and figures pertaining to the borrowers as SBH bank deems fit. SBH bank may also delegate to such person(s) the right and authority to perform and execute all acts, deeds, matters and things connected there with, or incidental there to as SBH bank deems fit.

In other words, SBH can send a person or a group of persons to your office or residence asking you to pay your loan. SBH also has the right to contact your employees and ask them to deduct the amount payable from your salary and remit the same to SBH bank. The deductions may be of an amount, which SBH bank decides. So if your salary is 15,000 a month and you’ve taken a loan of Rs.20,000 SBH bank can, hypothetically ask your employer to deduct Rs.15,000 from your salary and send it to SBH, leaving you with nothing to run your home with. Whenever they do this or not is entirely their choice. You give them the right to do this, when you take a personal loan from SBH.

The borrower’s shall not have, or raise/create, any objections to such deductions. No law or contract governing the borrower’s and borrower employer prevent or restricts in any manner the aforesaid right of SBH bank to require such deduction and payment by the borrower employer to SBH bank. In other words, you cannot object.

Their terms and conditions further state, provided however that in the event the said amounts so deducted are insufficient to repay the outstanding borrower dues to SBH bank in full, the unpaid amounts remaining due to SBH bank shall be paid by the borrower’s in such manner as SBH bank may in its sole discretion decide and the payment shall be made by the borrower’s accordingly.

So if your salary is 15000 and SBH has deducted the entire amount, now it has the right to decide when the rest of amount is payable and in that mode you are a defaulter.

1. Your fixed deposits are in peril:-Let’s say you have a fixed deposit account with SBH, which you opened to save for your daughter’s wedding. Now you’ve taken a personal loan of Rs. 20,000 to buy a scooter. If you’re in default of even a single installment, SBH has a right to deduct this amount from your fixed deposit account with them. They have a lien on all assets you have with them or their group companies. Since SBH direct share trading is also offered by SBH, if you have shares lying in their demat account, as per their terms and conditions, they can have access to these shares.

2. Communication is a one-way street here:-If SBH sends a notice to your home or office address, it is assumed that you received it. If you send a letter to SBH, unless it is received and acknowledged by SBH bank, it is not considered effective.

3. Right to choose jurisdiction:-If you go to court against SBH, as per the terms and conditions, you can only approach a court in Mumbai. SBH however reserves the right to file a suit against you anywhere in the country. We’re not sure how far this clause itself would stand in court since it infrings on the right of an individual to legal recourse.

4. SBH bank can publish names of defaulters in

newspapers or show them on TV or publish them notice:-

In case the borrower’s commits any default in repayment of principal amount of the facility or interest/charges due there on, SBH bank and/or the Reserve Bank of India (RBI) will have an unqualified right to disclose or publish the details of such default along with the borrower’s and/or its directors/parents/co-applicants, as applicable, as defaulters in such media as SBH bank and/or RBI may, in their absolute discretion, think fit.

SBH bank has the right to publish the name of a borrower who is in default, in any newspaper they choose or show it on television or publish it on the internet. This is again a right you give them when you take the personal loan. How would you like to open Times of India on Sunday morning and find your name published in it as the defaulter of a personal loan this clause also gives them the right to share you information with virtually anyone, if you’re in default of repaying your personal loan.

SBH bank has the absolute discretion to amend or supplement any of the loan terms at any time and will endeavor to give prior notice of fifteen days by email or put-up on the website as the case may be for such changes whenever feasible and such amended terms and conditions will there upon apply to and be binding on the borrower. Further, the loan terms shall also be subject to the changes based on guidelines/directions issued by the RBI to banks from time to time.

CHAPTER – 4

OBJECTIVES AND SCOPE

4.1 OBJECTIVE OF STUDY

1. To study the concept of unsecured loan and NPA.2. To understand the process, key issues in sanctions and disbursement.3. To study the concept of default and various reasons for defaulter.4. To find out the causes in rejection of cases.5. To study the various action taken by bank for the recovery of the loan.6. To study the impact of the environmental threat factor on the personal loan of SBH

bank with the help of ETOP model.

4.2 SCOPE OF THE STUDY

The scope of the project remains purely on the study of personal loan of STATE BANK OF HYDRABAAD with a view to know the assessment of the loan, how customer can assess the loan what are the interest rate, procedure can be known from this study. It also analyzes the defaulter in personal loan of SBH bank so that bank can take the precaution while the granting the loan.

CHAPTER - 5 PROCEDURE OF LOAN

PROCEDURE OF LOAN

SECTION 1

A loan without security- a personal loan is indeed issued without any security. And you do not

have to go to an agent in the vast disorganized sector to get one. Several banks and companies

would offer you this loan. The most striking feature of this type of loan is that the financer asks

no questions i.e. he is not interested in knowing what you intend to use the loan for. For your

point of you, it is convenient option compared to borrowing money from friends and relatives.

Personal loan issued in the range of Rs.15000 to Rs.10lakhs for a maximum period of 60 months,

include the categories of loans for educational purpose and holidays. Apart from these two

categories, these loan are typically taken to tide over an emergency when cash is urgently

required from a creditor who will not worry about securing his asset in the manner that a car

financer would.

Therefore the financer if doing perhaps a more check on your capability to repay than he might

even in the case of financing a home loan, for instance. Since financer perceive higher risk in this

category many follows a list of approved categories of borrowers. Interest rate is higher. All

other rates including service charges, post payment penalty are higher as well.

However, a personal loan may be a better choice than borrowing on your credit card, if you want

to keep your credit limit available for impulse purchases or an actual emergency requiring instant

purchasing power. Often borrowing money on your credit card carries a higher rate of interest

than a personal loan.

SECTION 2

After receiving the document from the customer the bank will decide how much loan will have to be approved to the customer based on the following calculation.

“If the customer is salaried person”

If the customer is salaried person the he will divided in the three category as below:

ELITE APPROVED OPEN MARKETBig companies (M&M, SIEMENS)

Limited companies Small companies

1. If the customer belongs to the ELITE group then the Loan amount will be approve him by applying the multiplier to his salary

Salary x 18 = Loan amount

2. If the customer belongs to the approved list category the loan amount will be approve him can be calculate as-

Salary x 12 = Loan amount

3. If the customer belongs to the open market list category the loan amount will be approve him can be calculate as-

Salary x 10 = Loan amount

“If the customer is self-employed”

If the customer is self-employed then loan amount will approve him can be calculate as-

Net Profit x 1.1 – obligation = Loan amount

(Obligation’s= daily expenses + previous loan amount)

Repayment

In this type if the customer has already taken the loan from the bank and he filed for new file for loan then the loan amount can be calculated as follows:-

Customer should have the paid EMI as,

Minimum EMI=9 and MAX=18

EMI amount x paid EMI (9 to 18)-obligation=Loan amount

SECTION 3

As after verifying all the document of the customer by the bank through the bank verifying agencies according the criteria mention the loan amount is disbursed.

Criteria Salaried Self-employed

Age 25yr – 58yr 25yr – 65yr

Net salary Net annual income Rs-

96000 p.a.

Net profit after tax-

Rs. 150000 p.a

Eligibility Employees of public ltd

Companies, private ltd.

Companies, Government

companies or MNC

Doctors, MBAs,

Architects, C.A..s,

Engineers, Traders,

Manufacturers

Years in current

job/profession

1 Year 3 Years

Years in current residence 1 Year 1 years

Document required for personal loan

DOCUMENT SALARIED SELFEMPLOYED

Latest 3 month bank statement Yes Yes

3 latest salary slip Yes -

Latest 2 year ITR with computation of

income/certified financials

- Yes

Proof of turnover(latest sales/ service tax

return)

- Yes

Proof of continuity in current job(form 16/

company appointment letter)

Yes -

Proof of continuity current profession

(IT return/ certificate of business continuity

issued by bank)

- Yes

Proof of identity Yes Yes

Proof of residence Yes Yes

Proof of office utility bill/ municipal tax

receipt

- Yes

Proof of qualification of highest degree

(for professional/ Govt Employees)

Yes Yes

Interest rate:-

The SBH bank provides the loan to the customer by imposing different type of interest rate on him.

Salaried-15.50% to 22.00%

Self-Employed Businessmen-17.50% to 22.00%

Self-Employed Profession-14.50% to 15.00%

Services charges for the SBH personal loan:-

1. Loan processing charges:-This is 2.5% of the loan amount. So for a personal loan of Rs. 50,000 you’ll pay Rs. 1,250.

2. Organizational charges:-This is 1% of the loan amount. So if an amount of Rs. 50,000 you’ll pay Rs. 500. This is to be paid along with the first repayment installment.

3. Cheque swap charges:-If you need to change the post-dated cheques issued to SBH bank, towards repayment of the personal loan, SBH will charge you Rs. 500.

4. Cheque bounce charges:-When a cheque is issued by you to SBH, bounces, you pay a penalty of Rs. 450.

5. Charges for late payment:-If you’re late in paying the installment due on the SBH personal loans, you’ll be charged 24% p.a on amount outstanding from date of default.

6. Interest rate can change:-SBH bank can change their interest rate on the personal loan, using its discretion or virtually change the interest rate anything they want in the terms and conditions.

7. Changing mode of repayment:-If you wish to change the mode of repayment of the SBH personal loan, this needs to be done with the permission of SBH bank. Stopping payments on post-dated cheques or otherwise cancelling or revoking mandates would be considered combined with a criminal intent according to the SBH terms and conditions.

CHAPTER – 6

RESEARCH METHODOLOGY

6.1 RESEARCH METHODOLOGY

Meaning of Research

Research in common parlance refers to a research for knowledge. The Advance Learner’s

Dictionary of Current English lays down the meaning of research as “a careful investigation or

inquiry especially through search for new facts in any branch of knowledge.”

Research methodology is an important tool in any research work. It acts as guideline and road in

completion of research. It is scientific search for data and information on as particular topic

research is search for knowledge.

Looking to the criticality of the subject and the inputs required for conducting research and for

arriving at logical conclusions, the following methodology or system was followed.

1) Primary Data.

2) Secondary Data.

1) Primary data: -

The information is gathered from the discussion with the employees/staff and from the

web site of the company.

2) Secondary data:-

The secondary data collected by

The sources of secondary data were -

The financial statements i.e. balance sheets and profit & loss accounts were obtained

from accounts department.

The information regarding loan collected from loan department and regarding Various

Schemes gathered from internet.

The statistical data regarding Loan sanctioned collected from loan account ledger from

accountant

CHAPTER -7

DATA ANALYSIS AND INTERPRETATION

7.1 PRESENTATION OF DATA IN GRAPH

From the balance sheet of the SBH bank we can observe that the contribution of personal loan to the total unsecured loan of the SBH bank in the years 2008, 2009, 2010 with the help of bar diagram:-

2008 2009 20100

5

10

15

20

25

30

Others Personal loan

Figures in corer

From the above diagram we can see that the personal loan contributes about 61.5% to the total unsecured loan of the bank in the year of 2008 and the contribution of personal loan is about 63.3% of total unsecured loan of the bank in the year of 2009 while in the year 2010 it is 67.3%.

From the above figure, the loan disbursement of unsecured loan in latur branch was increases near about 5% in the year of 2009 as compare to 2008 but for the year of 2010 this is 22%. This is because banks more emphasis on the unsecured loan (retail loan) particularly personal loan, which has high risk and high return.

Now we will see the Defaulter of the personal loan for the year of 2008, 2009, and 2010 can be seeing as bellow:-

Category 1 Category 2 Category 30

2

4

6

8

10

12

14

16

Defaulter Amt of Personal loan

Defaulter Amt of Personal loan

Figures in corer

From the above figure, we can see that for the year of 2008 the defaulters are low as compare to 2009 & 2010 but it was gradually increases with gradual increase in loan disbursements for the year 2009 & it is suddenly increases high for the year 2010 with sudden increase in the loan amount for 2010.

Now we will see that the defaulter case in personal loan i.e. NPA. For the year 2008 the NPA of SBH bank in personal loan is stood 44% & for the year 2009 is stood 46% while in the year 2010 it stood 53%.

Analysis:-

From the above figure, we can see that for the year of 2010 the defaulters are high as compared to the year of 2008 & 2009 that means the defaulters are increases highly for the year of 2010. From the above charts we can see that the defaulters for the year 2010 are increasing because of following reasons:

Bank increases the loan disbursement in personal loan in year 2010 compared to 2008 & 2009.

As interest rate increases the EMI also increases that affect the repayment capability of the borrower.

During this study I found that the bank who is aggressive player in retail loan segment has increased its personal loan disbursement.

From the above figure it is also clear that the customer’s irresponsibility and insufficient information to the bank also paved the way towards increase in the defaulters list.

7.2 REASON FOR DEFAULTER

Default means the incapability of the borrower to make the repayment. The default may arise due to various reasons:-

The borrower may default without reason. Default due to death of the borrower. Bills pending with the debtors or govt. of the borrower. Absconding. Default due to financial crisis in the business of the borrower. Shut down of the business of the borrower etc.

These reasons or defaults are not in control of the bank. They are external and bank can’t predict them. It may sometimes so happen that the bank while issuing a loan may prove to be negligent while scrutiny of the borrower’s financial position or in deciding upon the limit of sanctioning of a loan. This may also lead to a default.

Loans are asset to the bank. The major profit is earned by way of interest on such loans. But in case of default no income is generated from such lending. Therefore they are also turned as non-performing assets.

We can say that the loss that is shown in the balance sheets stating loss from NPA is nothing but the loss from non-performing assert, which if wouldn’t have been defaulted would, definitely would have added to the profits of the bank. Therefore it is very important from banks point of view to take proper care while issuing a loan or while lending funds.

7.3 REASON FOR REJECTION

As a standard practice before agreeing to lend credit all banks and other finance providers does a credit check to see your credit score? The credit score helps them identify potential risks involved in lending you credit. Your score is identified by numerous factors such as your earnings, your outgoing expenditure, and your outstanding balance and arrears, which is mainly highlighted in your credit report. After an assessment of your credit score the creditors can see why and not one should be granted a loan.

Now we will see some of the common reason because of bank may reject the loan application of the customer:-

If the person has criminal Record.

If the person taken the loan from some other bank and he is defaulter of that bank.

If the person age is above 65 year.

If the person income is not sufficient to repay the loan amount.

7.4 CASE STUDIES

The reason for default can be well explained and understood with the help of few cases.

CASE-1

Customer Name - Mr. Ganesh Kumar.

Type of Loan -Personal Loan

Amount -Rs 4,00,000

Rate of Interest -20%

Here the Mr. Ganesh Kumar who had a small retail department outlet as his business. His average annual income was rupees three lack. He pays the income tax every year. He had been in this business from last twenty years so he has great goodwill to his name.

Reason for default

The party had taken a loan for the renovation of the shop. As the party had a business of general departmental store which was located far from city area. Also residents which were there prefer to go to the city area for bulk buying in the malls & big bazaar which would provide them good offers & discounts. As a result of this business hit badly & could not sustain.

Analysis:-

The client & bank should have taken the assurance of the future growth with this change & also the inflationary situation.

CASE-2

Customer Name - Mr Tushar Jadhav

Type of Loan -Personal Loan

Amount -Rs 5,00,000

Rate of Interest -18%

Here Mr Tushar Jadhav who was the area sales manager of VLC India ltd. His annual salary was rupees four lack and accordingly he pays the income tax every year. He has achieved a great success in his sector from last three year.

Reason for default:-

The party had taken a personal loan for the purchase of new car. The party had no contacts with the bank. The bank investigates the matter and found that he was untraceable & had a criminal record. They also found that the person who taken the loan has sold his car to other person and he was not the residence of the city.

Analysis:-

The basic problem here was that the bank had insufficient information about the borrower i.e. his past record, contacts etc. the scrutinizers did not gave due importance to the availability of such information and granted the loan without some concrete base. Overall we say an improper scrutiny of the proposal.

CASE-3

Customer Name -Mr. Manoj Patel

Type of Loan -Personal Loan

Amount -Rs 10,00,000

Rate of Interest -22%

Here Mr. Manoj Patel who was the owner of India Cement and Pipe Private Limited Company. His annual income was rupees ten lack and accordingly he pays the income tax every year. The party had the big & well established business of cement pipes since last twenty years.

Reason for default:-

The party had taken a loan for the purchase of capital assets like moldings machine, tools etc. After few days due to the major accident of his car he was under the ventilator & finally died. As a result the bank could not recover the dues.

Analysis:-

The basic problem here is that the bank should have taken the nominee of borrower for the loan. Due to such insufficient documentation the case was in default.

CASE-4

Customer Name -Mr. Ramesh Rathi

Type of Loan -Personal Loan

Amount -Rs 2,50,000

Rate of Interest -19%

Here, Mr. Ramesh Rathi having age twenty five is an employee of ABB limited company. His annual salary was rupees 1.5 lack. He has been working there as a temporary employee from last six months.

Reason for defaulter:-

The party had taken a loan for his personal use. After few days the person had lost his new job. Thus bank interest was not repaid in time. The bank extended the time period for repayment, but the payment still stands due. As a result there was no scope of recovery and thus case stands under the list of defaulter.

Analysis:-

The client should have taken note of his job assurance before taking a loan and also expected from the bank to scrutinize his job stability.

CASE-5

Customer Name -Mr. Harshal Sonone

Type of Loan -Personal Loan

Amount -Rs 2,00,000

Rate of Interest -21%

Here Mr. Harshal Sonone was a farmer. His annual income was rupees two lack. From last five years he had developed his farm effectively and he also had good transactions with the bank.

Reason for default:-

As the party has the agriculture as his business, had taken a personal loan for purchase of tractor for further development of his farm. But due to insufficient raining his business was badly affected and he was continuously unable to pay interest for 1 year.

Analysis:-

The basic problem here was that the bank had taken the risks while granting the loan, as his income is not that much to give him that much amount of loan.

The reason for the rejection of loan file of a customer by the bank can be understood by the following case studies:-

CASE-1

Customer Name -Mr. Abhilash Patil

Type of Loan -Personal Loan

Mr. Abhilash Patil who is salaried person working with the Marksmen India Ltd he applied in the SBH bank for personal loan as per document required for the personal loan following documents are submitted by him.

a. PAN card b. Salary slipc. Light billd. Bank pass book

During the investigation it was found that

1. He has taken the home loan from the SBH bank loan in Baroda and he is the defaulter because his 7 cheques were bounced continuously in home loan of SBH bank.

2. He has lost the job.

Due to above reasons his file for the loan was rejected.

CASE-2

Customer Name -Mr. Prakash Dasharathrao Wadekar

Type of Loan -Personal Loan

Mr. Prakash Dasharathrao Wadekar who was civil contractor, and have lottery business. He applied personal loan in SBH bank.

As per document required for the personal loan following documents are submitted by him.

a. PAN card b. Light billc. Phone billd. IT returne. Income statementf. Bank pass book statement

During the investigation it was found that

1. He is defaulter of HDFC because he has not paid 10 EMI continuously.2. He has criminal record.3. He is suspended police officer.

Because of all above reason his file was rejected.

CASE-3

Customer Name -Mr. Gulabchand Bafna.

Type of Loan -Personal Loan

Mr. Gulabchand Bafna who was the businessman and have plywood & paints business. He had applied for personal loan in State Bank of Hyderabad.

As per document required for the personal loan following documents are submitted by him.

a. Income statementb. Bank pass book statement for last year.c. IT return.d. PAN card.

During the investigation it was found that

1. He has not paid the IT return for last two years.2. He has insufficient transaction with the bank.3. He is not accepted by the society for his creditworthiness.

Under such reasons his file for the loan was rejected by the bank.

CASE-4

Customer Name -Mr. Rohan Khandare

Type of Loan -Personal Loan

Mr. Rohan Khandare who was working in cement company. He has applied the personal loan in SBH bank. The documents required for the approval of the loan are:-

a. PAN card b. Salary slipc. Light billd. Bank pass book

During the investigation it was found that

1. He does not have the documents required by the bank.2. He does not any record or transaction with the bank.

Due to above reasons his file for the loan was rejected.

CASE-5

Customer Name -Mr. Jaspal Singh

Type of Loan -Personal Loan

Mr. Jaspal Singh who was salaried person with Micro manufacturing limited. He has applied the personal loan in SBH bank.

As per document required for the personal loan following documents are submitted by him.

a. Income statementb. Bank pass book statement for last year.c. IT return.d. PAN card.

During the investigation it was found that

1. He was going to retire in next month.2. He was also the defaulter in two financial institutions.

Because of this reasons his file was rejected.

CHAPTER 8

OBSERVATIONS AND FINDINGS

SUMMARY OF FINDINGS:-

From the above case studies of defaulters the following causes are extracted:-

1. Some parties does not the job assurance & also about their stability.2. Some of the parties do have the criminal record.3. Some of the future contingencies & uncertainties are not considered.4. Some of the parties do not have the capacity or capability to repay the loan & also the

EMI in time.

From the above case studies of rejections the following causes are extracted:-

1. The party has the bad past record still applying for the loan.2. Any suspended officer of the company applying for the loan.3. The party had submitted insufficient documents to the bank & expecting from the bank

to sanction the loan.4. The parties are defaulter of any other bank or institution.5. The party does not have any deposits or banking transactions with any other banks.

CHAPTER-9

CONCLUSIONS

Conclusion of case studies:-

After carrying out the case study and after speaking to some of the customers who are the borrower of the personal loan from the SBH bank we could conclude on following two parameters:-

Defaulters:-

The defaulters are increasing due to financial loses to businessmen, loss of job of the borrower, criminal record not checked by the bank, incorrect address provided by the borrower, lack of checking the credit history of the borrowers due to rush of completing year or month end target, lack of checking future business prospects while sanctioning unsecured loans (personal loans).

Rejections:-

The major reasons for rejections were lack of documentation (insufficient document provided by the borrower), credit history, lack of creditability, and lack of business with the bank.

Overall Conclusion:-

After carrying out the detail study and the information collected from the SBH bank the following conclusion were inferred.

There is growth in personal loan in year 2010 compared to 2009. The bank defaulter list of personal loan has increased in the year of 2010. Interest rate plays major role in the banks personal loan defaulter because as interest

rate increases the EMI also increases and hence sometimes customer are not repay the loan.

With reference to above cases, the customers are irresponsible of their liabilities, which is risk for bank.

CHAPTER-10

RECOMMENDATIONS AND SUGGESTION

After doing the analysis and study of the personal loan of the STATE BANK OF HYDRABAAD, I would like to suggest and recommend the following points:-

To resolve cases of defaulter to minimize the default amount. The bank should take proper care before giving the loan to the customer by the way of proper investigation of the customer record.

The loan amount should be sanctioned according to the capability of customer. The bank should regularly be in touch with the customer whenever there are chances in

the EMI,EMI date, increase in the interest rate, so that customer is aware of all these things.

Scrutinized weather all the required document are checked & submitted.

BIBLIOGRAPHY

BIBLIOGRAPHY

BOOKS REFERED:-

1. Indian Financial System – M.Y. Khan.

2. Economic environment of business by S.K.Misra & V.K.Puri.

3. Circular issued by RBI.

Website Referred :-

www.bankofhyderabad.com

1. www.rbi.com

2. www.timesofindia.com

3. www.google.com

![Loan note instrument - Big Society Capital · Dated [] 201[] LOAN NOTE INSTRUMENT relating to constituting up to £[] []% fixed rate unsecured loan notes, due 201[] between [] Limited](https://img.dokumen.tips/doc/110x75/5b62d3147f8b9a08478e0345/loan-note-instrument-big-society-capital-dated-201-loan-note-instrument.jpg)