Embed Size (px)

Citation preview

1

Analysis of Financial Statements

Profitability

Dr. Clive Vlieland-Boddy

2

3

What is Profitability?

• Is it always all about “success?”

• Or about achieving what is expected or perhaps better than expected!.

• Is it about goals being achieved!

• Or about managing risk and minimising these?

• Profit means that revenues are higher than costs. But by how much..

• Is it always just about $$$$$$$$$....

4

Profit Mastery Content

Steps to Building Value

� Effective Strategy

� Effective Planning.

� Managing Cash Flow

� Managing Growth

� Ensuring Sustainability

5

Improving Profitability can be achieved by:

• Selling More

• Selling at a better margin

• Better use of Capital Structures

• More efficient use of assets (Ryanair Vs BA)

• Maintaining a competitive advantage.

• Developing core competitances.

6

But what is Profitability? How do we measure it?

It is how successful the business is.

• But how do we assess that?

• Yes. we can evaluation of the Income Statement.

• We can make a comparison of results

• But we need to know what we are going to measure.

7

The road to

improve profits

8

Profitability • Profit is the number one objective of all

firms • Profitability measures look at how much

profit the firm generates • Although we talk about CSR and the

environment, until a business is profitable how can it afford to be environmentally friendly?

• However, we must accept that sustainability is vital and “PROFITS” must be linked to that goal.

9

Profitability Ratios

10

Profitability Ratios

• Profitability measures look at how much profit the firm generates from sales or from its capital assets

• Different measures of profit – gross and net

– Gross profit – effectively total revenue (turnover) – variable costs (cost of sales)

– Net Profit – effectively total revenue (turnover) – variable costs and fixed costs (overheads)

11

Profitability Ratios

1. Gross Profit Margin

2. Net Profit Margin

3. Return on Assets

4. Return on Equity

5. Return on Capital Employed

12

Gross Profit Margin

• The percentage that a company makes on selling products after taking into account the direct costs of that sale.

• This is the Gross Profit as a percentage of Sales.

• This Is by far the most important profitability ratio.

13

Profitability Ratios Profitability Ratios

Gross Profit Margin

Gross Profit

Net Sales

Gross Profit Margin

Gross Profit

Net Sales

Indicates the efficiency of operations and firm pricing

policies.

Income Statement / Balance Sheet

Ratios

Profitability Ratios

14

Gross Profitability

• The higher the better

• Enables the firm to assess the impact of its sales and how much it cost to generate (produce) those sales

• A gross profit margin of 45% means that for every £1 of sales, the firm makes 45p in gross profit

15

Gross Profit %

Gross Profit

Revenues

= 12,400 = 13%

97,500

16

Gross Profit Margin

Total Gross Margin Dollar Amount Percentage

Net Sales $100 100%

Cost of Goods Sold - 40 - 40

Gross Profit Margin $ 60 60%

Unit Gross Margin

Unit Sales Price $1.00 100%

Unit Cost of Goods Sold - 0.40 - 40

Unit Gross Profit Margin $0.60 60%

17

Comparing Business Models Let’s compare Maxi with Mini Maxi Mini Net Sales $321,062 $205,853 Cost of Sales $130,455 $ 67,947 Gross Profit $190,607 $137,906 Gross Margin 59% 67%

Which one has a more profitable business model?

18

Gross Profit or Margin %

• Definitely the most important ratio.

• Tells us how management are controlling the business.

• However there may be external influences.

19

Example 1 • Company has Sales of $12,500,000 and Cost of

Goods Sold (COGS) of $7,500,000. This means that the Gross Profit is $5,000,000 ($12.5m-7.5m)

Its Gross Margin or Profit Ratio is

5,000,000 = 40%

12,500,000

If 2009 was 39.7% and 2008 was 39.3%

20

Profitability Ratio Comparisons Profitability Ratio Comparisons

Company Industry

40.0% 40.1%

39.7 40.8

39.3 40.6

Company Industry

40.0% 40.1%

39.7 40.8

39.3 40.6

Year

2010

2009

2008

Gross Profit Margin

The Company has a good and improving Gross Profit Margin inline with the industry

21

Key Factors Affecting the Gross Profit Margin

• Price per unit sold

• Cost of Goods Sold per unit

• Mix of the goods and services sold (i.e. the “product mix”)

22

Other ratios of Income/ Expenditures

• It is also useful to compare items of expenditure as a percentage of Income.

• E.g. say advertising or Research & Development.

• How does this compare to previous years and does an increase affect revenues.

• How does it compare to what competitors spend as a percentage of revenues.

23

Net Profit Margin

• The profit margin tells you how much profit a company makes for every $1 it generates in revenue or sales.

• Profit margins vary by industry, but all else being equal, the higher a company's profit margin compared to its competitors, the better.

24

Profitability Ratios Profitability Ratios

Net Profit Margin

Net Profit after Taxes

Net Sales

Net Profit Margin

Net Profit after Taxes

Net Sales

Indicates the firm’s profitability after taking account of all

expenses and income taxes.

Income Statement / Balance Sheet

Ratios

Profitability Ratios

25

The Calculation of Net Profit Margin

• Net Income After Taxes ÷ Total Revenue

• = Net Profit Margin

26

Example 2 • Company has Net Profits after taxes of $512,500

with sales of $12,500,000. Its Net Margin Ratio is

512,500 = .041%

12,500,000

If 2009 was 4.9% and 2008 was 9%

27

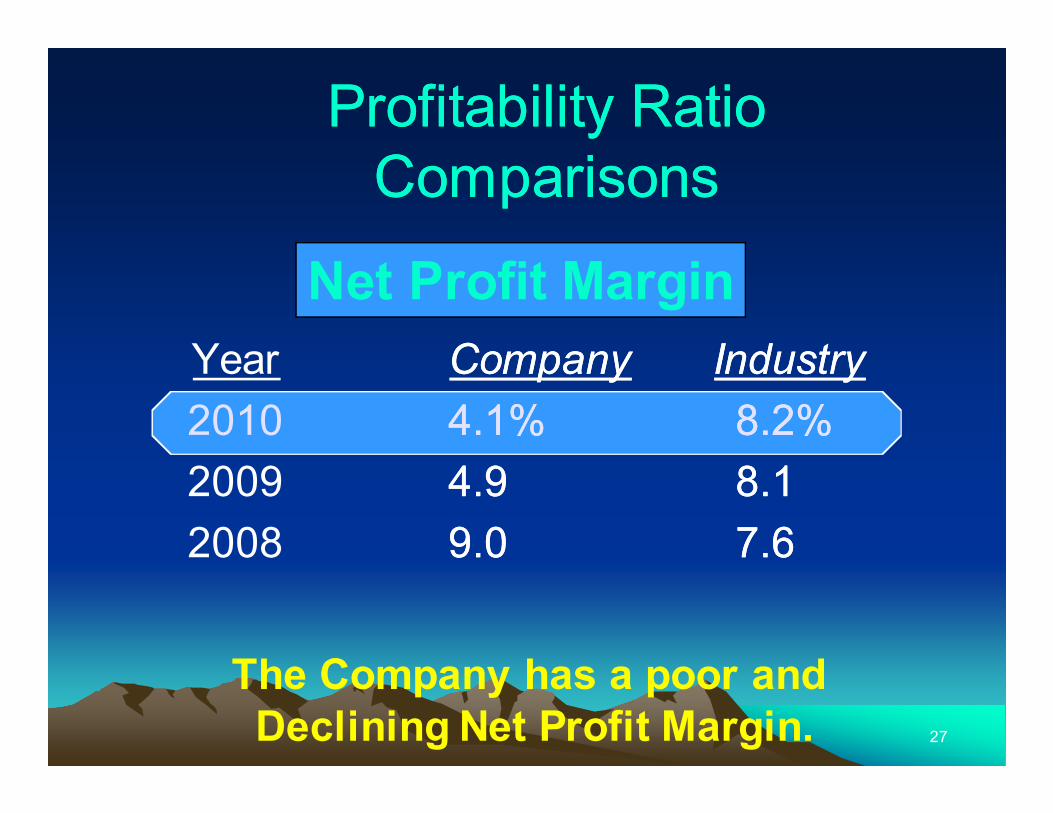

Profitability Ratio Comparisons

Profitability Ratio Comparisons

Company Industry

4.1% 8.2%

4.9 8.1

9.0 7.6

Company Industry

4.1% 8.2%

4.9 8.1

9.0 7.6

Year

2010

2009

2008

Net Profit Margin

The Company has a poor and Declining Net Profit Margin.

28

Net Profit Margin Trend Analysis Comparison

Net Profit Margin Trend Analysis Comparison

Trend Analysis of Net Profit Margin

4

5

6

7

8

9

10

2008 2009 2010

Analysis Year

Ratio Value (%)

Company

Industry

29

Example 3

• Better Buys sells 100,000 widgets at $5 each.

• It generates a total of $500,000 in revenues.

• The company's cost of goods sold is $2 per widget.

• Therefore 100,000 widgets at $2 each is equal to $200,000 in costs.

• This results in a gross profit of $300,000 ($500k revenue - $200k cost of goods sold).

• The Gross Profit Margin of 60%. (300,000 divided by 500,000......

30

Example 3

• If its operating expenses were $180,000, this would leave a Pre Tax Profit of $120,000. Subtracting the tax bill of $50,000, we are left with a net profit of $70,000.

• Net Profit Margin would be 14% (70,000 divided by 500,000)

31

Caution

• This is the standard version of Net Profit Margin.

• Many will adapt this.

• Must ensure that you are consistent

32

Shareholder Expectations

33

Investors

Provide the capital

34

What do Investors want in Return

• Expect a minimum %.

• Expect a sustainable business with growth potential

• Expect good CSR.

35

SO...

• Management must ensure that they meet shareholder expectations.

• That they invest the funds to generate in excess of the expected returns that the shareholders want.

• Therefore the cost of capital being what the shareholders demand must be used as the minimum return that management must achieve from its investments.

36

Return on Investment

37

Return On Investment

• This is the relationship of investment to the return that it makes.

• This can be evaluated either before of after tax.

• Before tax taxes account of the fact that tax is normally outside the control of management.

• It also takes account of the earning power not how financed.

38

The 3 Key Ratios for ROI

• ROE (Return on Equity)

• ROA (Return on Assets)

• ROCE (Return on Capital Employed)

39

Return on Equity

• Reports the percentage of income earned for each dollar invested by the owners of an entity.

• Computed as Net Income divided by Average Total Shareholders Funds.

• This tells us how efficiently we use our invested capital.

• As most of Equity is Retained Earnings, ROE measures how efficiently management uses that accumulated profit to make more money

40

Example • Company has profits after tax of $512,500

with assets of $12,200,000

512,500 = .042%

12,200,000

If 2009 was 6% and 8.1% in 2008

41

Example • Company has profits after tax of $512,500

with total Equity (Shareholders funds) of $6,400,000

512,500 = .08%

6,400,000

If 2009 was 6% and 8.1% in 2008

42

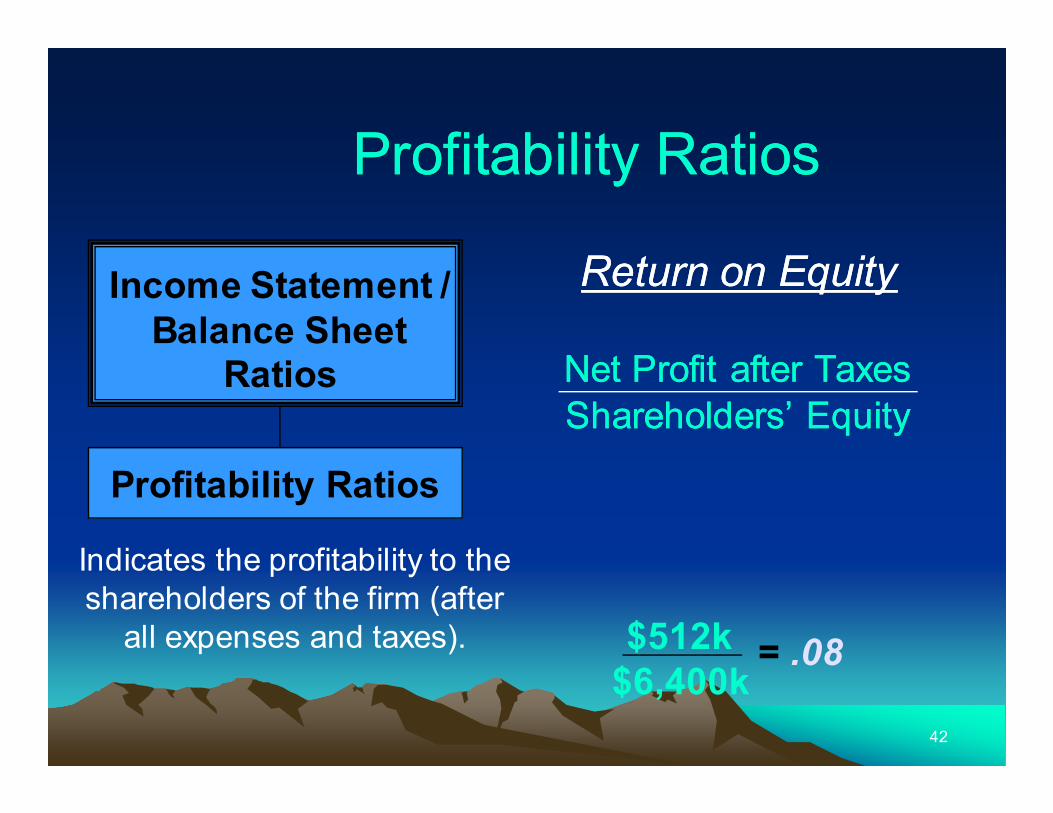

Profitability Ratios Profitability Ratios

Return on Equity

Net Profit after Taxes

Shareholders’ Equity

Return on Equity

Net Profit after Taxes

Shareholders’ Equity

Indicates the profitability to the shareholders of the firm (after

all expenses and taxes).

Income Statement / Balance Sheet

Ratios

Profitability Ratios

$512k $6,400k

= .08

43

Profitability Ratio Comparisons

Profitability Ratio Comparisons

Company Industry

8.0% 17.9%

9.4 17.2

16.6 20.4

Company Industry

8.0% 17.9%

9.4 17.2

16.6 20.4

Year

2010

2009

2008

Return on Equity

The Company has a poor and declining Return on Equity.

44

Return on Equity Trend Analysis Comparison

Return on Equity Trend Analysis Comparison Trend Analysis of Return on Equity

7.0

10.5

14.0

17.5

21.0

2008 2009 2010

Analysis Year

Ratio Value (%)

Company

Industry

45

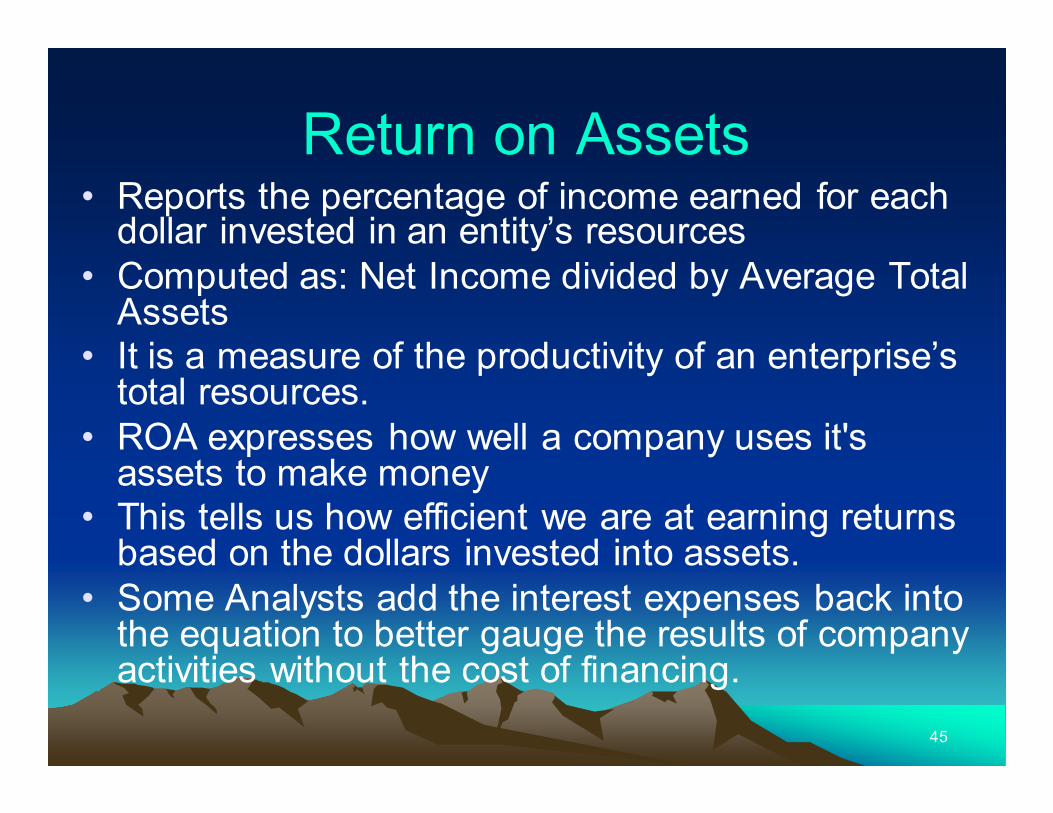

Return on Assets • Reports the percentage of income earned for each

dollar invested in an entity’s resources • Computed as: Net Income divided by Average Total

Assets • It is a measure of the productivity of an enterprise’s

total resources. • ROA expresses how well a company uses it's

assets to make money • This tells us how efficient we are at earning returns

based on the dollars invested into assets. • Some Analysts add the interest expenses back into

the equation to better gauge the results of company activities without the cost of financing.

46

Profitability Ratios Profitability Ratios

Return on Assets

Net Profit after Taxes

Total Assets

Return on Assets

Net Profit after Taxes

Total Assets

Indicates the profitability on the assets of the firm (after all

expenses and taxes).

Income Statement / Balance Sheet

Ratios

Profitability Ratios

$512k $12,200k = .042

47

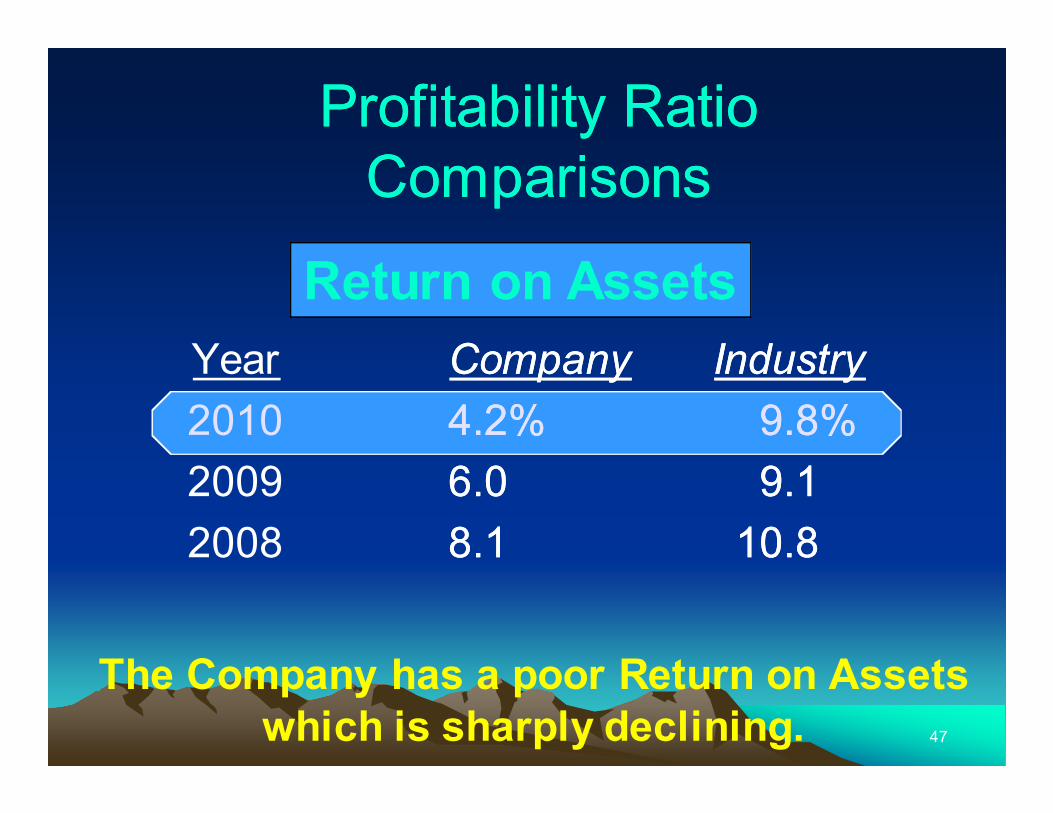

Profitability Ratio Comparisons

Profitability Ratio Comparisons

Company Industry

4.2% 9.8%

6.0 9.1

8.1 10.8

Company Industry

4.2% 9.8%

6.0 9.1

8.1 10.8

Year

2010

2009

2008

Return on Assets

The Company has a poor Return on Assets which is sharply declining.

48

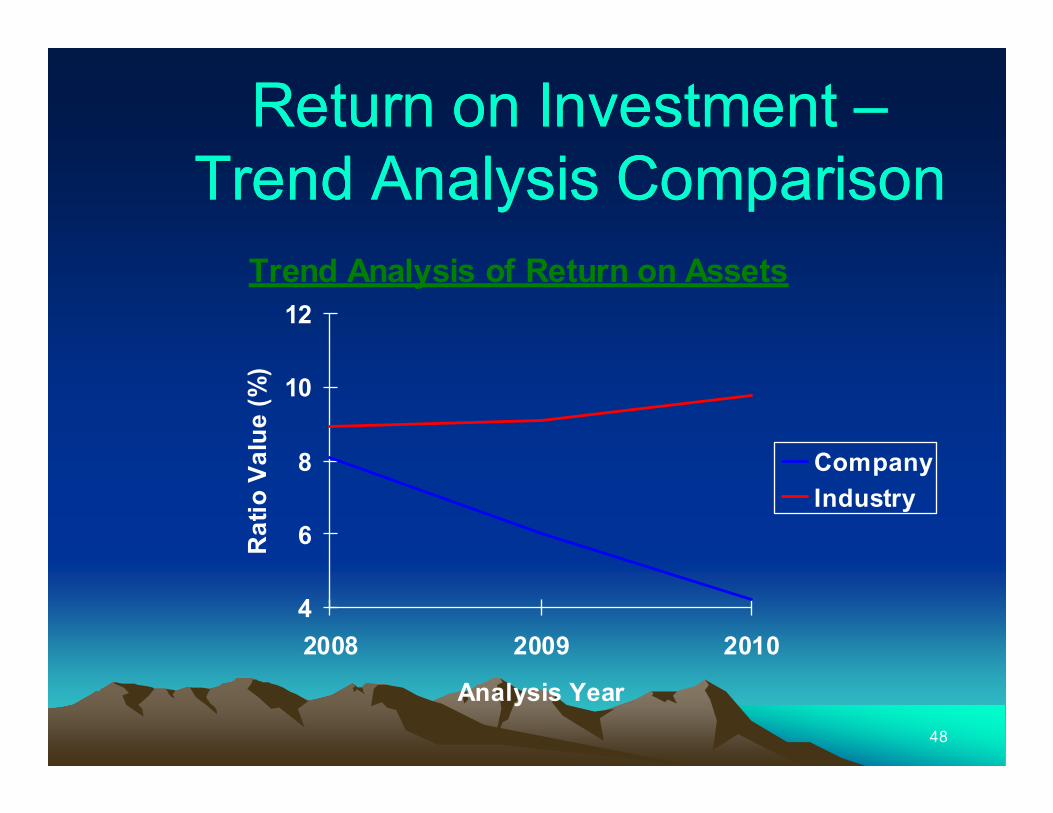

Return on Investment – Trend Analysis Comparison

Return on Investment – Trend Analysis Comparison

Trend Analysis of Return on Assets

4

6

8

10

12

2008 2009 2010

Analysis Year

Ratio Value (%)

Company

Industry

49

ROE Vs ROA • We can make the case that both tell us the same

thing, but that is not necessarily true as ROA tends to be the more volatile ratio.

• ROE measures the return for $ invested by the shareholders.

• ROA measures the same thing but over the entire asset base not just Equity.

• In general, an ROA greater than the ROE is a sign of trouble.

• Remember that ROA includes the cost of financing. If ROA is greater than ROE, it means that financing is costing more than it makes.

50

ROI - perspectives

• ROE measures how much a company has earned on the funds invested by its shareholders (shareholder perspective)

• ROA shows how well a company’s funds were used, irrespective of the relative magnitudes of the sources of these funds (current liabilities, debt and equity)

• ROCE shows how much a company has earned on invested long-term funds (permanently employed capital = equity + LT debt)

51

• ROA is lowered by debt as interest expense lowers net income, which also lowers ROA.

• However, the use of debt lowers equity, and if equity is lowered more than net income, ROE would increase.

Effects of Debt on ROA and ROE

52

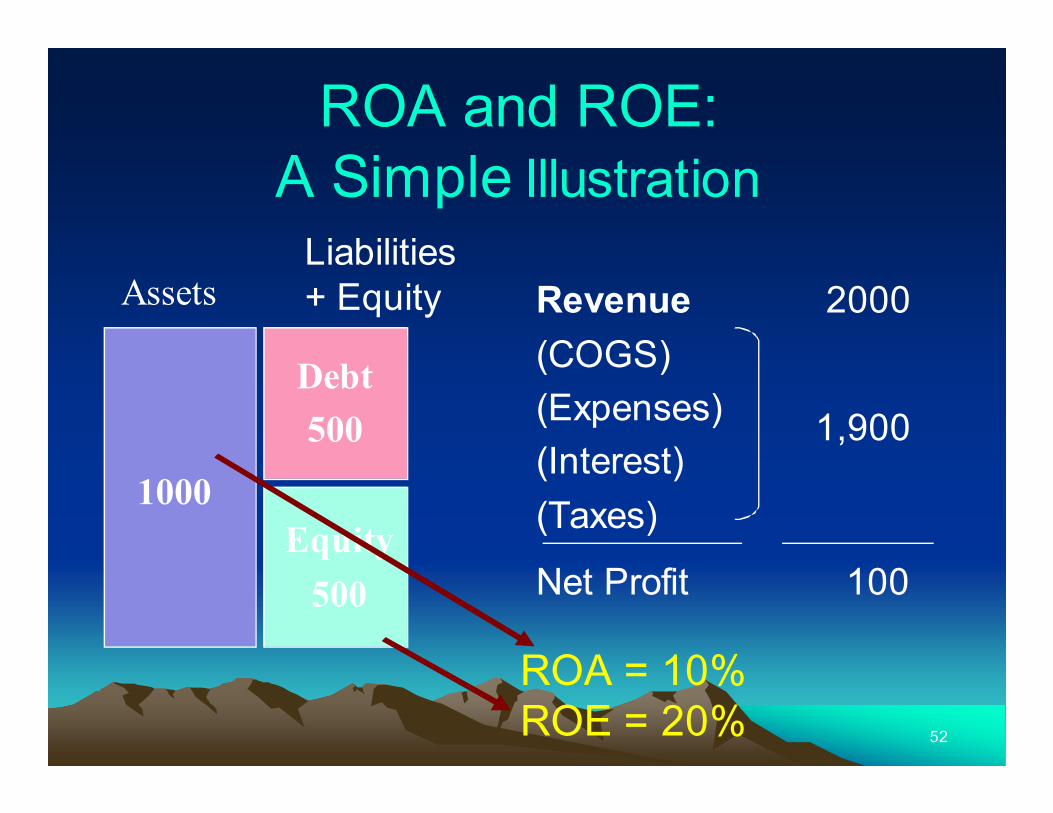

Debt

500

Equity

500

ROA and ROE: A Simple Illustration

Liabilities + Equity

Revenue 2000

(COGS)

(Expenses)

(Interest)

(Taxes)

Net Profit 100

1000

Assets

ROA = 10% ROE = 20%

1,900

53

Debt

667

Equity

333

ROA and ROE The Impact of Increased Leverage

Liabilities + Equity

Revenue 2000

(COGS)

(Expenses)

(Interest)

(Taxes)

Net Profit 100

1000

Assets

ROA = 10%ROA = 10%ROA = 10%ROA = 10%

ROE = 30%ROE = 30%ROE = 30%ROE = 30%

54

Return on Capital Employed

• ROCE. Profit before interest and Tax / capital employed.

• This evaluated the effectiveness of the company to produce profits that compare with the total capital tied up in the busies. (Note this does not look at the market value of capital)

• This is a distorted ratio as Debt capital is normally much cheaper than Equity.

55

Return on Capital ROCE

• This shows return from the long term capital invested in the business.

EBIT

__________________

Average Capital Employed

Capital Employed is..

• Shareholders Funds + Debt Capital or

• Total Assets – Current Liabilities

• We are looking at how efficient management are at using the assets to generate profits from operating activities.

• Note this is normally book values!

• It could also be measured using EBIT less Tax.

56

57

Profitability & ROCE

• The higher the better

• Shows how effective the firm is in using its capital to generate profit

• A ROCE of 25% means that it uses every $1 of capital to generate 25 cents in profit

• Partly a measure of efficiency in organisation and use of capital

58

Capital employed

Assets Financing

Fixed assets

Equity

Net working capital LT Debt

Current assets Current liabilities

Capital employed C

apital employed

59

Income Statement: The Basics

• Everything on the Income Statement can be expressed as a percentage and compared to competitive companies.

• Everything on the Income Statement can be compared as a percentage to Net Sales or Revenues.

• We will return to this later in Common Sized Statements

60

Income Statement: The Basics

• Companies are valued based on the cash produced from “core” operations (or Operating Income).

• Focus your attention on the “core” business. What business is the company in? How much money did that business generate or cost?

61

Quality of earnings

• Is profit (and profit growth) sustainable?

• What is the impact of short term conditions ?

• What is the impact of ‘creative’ accounting changes ? – Changes in accounting policies

– Changes in accounting estimates

– Changes in consolidation scope

– Changes in interest %

– Exceptional sale of assets or business segments

– Other extraordinary operations

62

Taxes? Why do we look at pre-tax income?

• Companies have no control over taxes

• Taxes vary from state to state and country to Country.

• Taxes don’t show the true picture

• Various industries are taxed differently

• Tax credits skew year-to-year earnings

Taxes have their own line on the Income Statement.

63

Payout Ratio

• This is the % of Net Earnings that are paid out as dividends.

Dividends

__________

Net Income

64

Plough Back ratio • This is the % that the company retains of

Net Earnings to invest in the business.

Net Earnings – Dividends

_____________________

Net Earnings

65

Profitability

• Return on Capital Employed (ROCE) = Profit / capital employed x 100

• Be aware that there are different interpretations of what capital employed means – see http://www.bized.ac.uk/compfact/ratios/ror3.htm for more information!

66

Bye for now! I’m ready for some leisure time.

Please ensure you Prepare for next session

![EUROPEAN INSOLVENCY REGULATION, COMI AND · PDF fileEUROPEAN INSOLVENCY REGULATION, “COMI” AND ... Vlieland – Boddy [2005] EWCA ... relates generally to the unsecured balance](https://img.dokumen.tips/doc/110x75/5ab26a8f7f8b9a284c8d69a2/european-insolvency-regulation-comi-and-insolvency-regulation-comi-and-.jpg)

![Brexit: its impact on forum and law shopping · Malcolm Brian Shierson v Clive Vlieland-Boddy[2005] EWCA Civ 974 Mr Shierson divorced his wife and than moved from the UK to Spain,](https://img.dokumen.tips/doc/110x75/5e83354f1892dc5da02f0949/brexit-its-impact-on-forum-and-law-shopping-malcolm-brian-shierson-v-clive-vlieland-boddy2005.jpg)