Embed Size (px)

Citation preview

An Overview of the Housing and Economic Crisis – and Why There Is More Pain to Come

T2 Accredited Fund, LPTilson Offshore Fund, Ltd.

T2 Qualified Fund, LP

February 1, 2010

The latest version of this presentation is regularly updated at www.valueinvestingcongress.com

T2 Partners Management L.P. Manages Hedge Funds and Mutual Funds

and is a Registered Investment Advisor

145 E. 57th Street, 10th FloorNew York, NY 10022

(212) [email protected] www.T2PartnersLLC.com

The collapse of the U.S. housing market, the world’s largest debt market, is the defining economic event of our lifetimes. This presentation explores what happened and why, where we are today, and what the future likely holds.

For More Details, See Our Book:More Mortgage Meltdown

Tilson Mutual Funds

The Tilson Mutual Funds (www.tilsonmutualfunds.com) follow a long-term-oriented, value-based investment strategy, seeking to identify stocks that are trading at a substantial discount to their intrinsic value. The Tilson Focus Fund (TILFX) seeks maximum capital appreciation, while the Tilson Dividend Fund (TILDX), while also seeking capital appreciation, seeks to generate current income from dividends and selling covered calls. An investor should consider the investment objectives, risks, and charges and expenses of the Funds before investing. The prospectus contains this and other information about the Funds. A copy of the prospectus is available at www.tilsonmutualfunds.com/tilsonprospectus.pdf or calling the fund directly at 888-484-5766. The prospectus should be read carefully before investing.

Investment in the Funds is subject to investment risks, including, without limitation, market risk, management style risk, sector focus risk, foreign securities risk, nondiversified fund risk, portfolio turnover risk, credit risk, interest rate risk, maturity risk, investment-grade securities risk, junk bonds or lower-rated securities risk, derivative instruments risk and real estate securities risk.

The Tilson Mutual Funds are distributed by Capital Investment Group, Inc., Member FINRA/SIPC, 17 Glenwood Ave, Raleigh, NC, 27603. There is no affiliation between the Tilson Mutual Funds, including its principals, and Capital Investment Group, Inc.

Attend the Next Value Investing Congress on May 4-5 in Pasadena, CA

Register at www.valueinvestingcongress.com

Confirmed speakers include:• Bruce Berkowitz, Fairholme Capital• John Burbank, Passport Capital• Eric Sprott, Sprott Asset Management• Mohnish Pabrai, Pabrai Investment Funds• Paul Sonkin, Hummingbird Value Funds• Thomas Russo, Gardner, Russo & Gardner• David Nierenberg, The D3 Family Funds• Lloyd Khaner, Khaner Capital• J. Carlo Cannell, Cannell Capital• Guy Spier, Aquamarine Fund• Patrick Degorce, Thélème Partners• Richard Vogel, Alatus SA• Amitabh Singhi, Surefin Investments• Whitney Tilson & Glenn Tongue, T2

Partners

Subscribe to Value Investor Insight and SuperInvestor Insight

What Happened?

9

For the Second Half of the 20th Century, Housing Was a Stable Investment

Sources: Robert J. Shiller, Irrational Exuberance, Princeton University Press 2000, Broadway Books 2001, 2nd edition, 2005, also Subprime Solution, 2008, as updated by the author at http://www.econ.yale.edu/~shiller/data.htm; Lawler Economic & Housing Consulting.

100

125

150

175

200

225

250

275

300

1950

1954

1958

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

Rea

l Hom

e Pr

ice

Inde

x (1

890=

100)

ShillerLawler

Trend Line

10

…And Then Housing Prices Exploded

Sources: Robert J. Shiller, Irrational Exuberance: Second Edition, as updated by the author; Lawler Economic & Housing Consulting.

100

125

150

175

200

225

250

275

300

1950

1954

1958

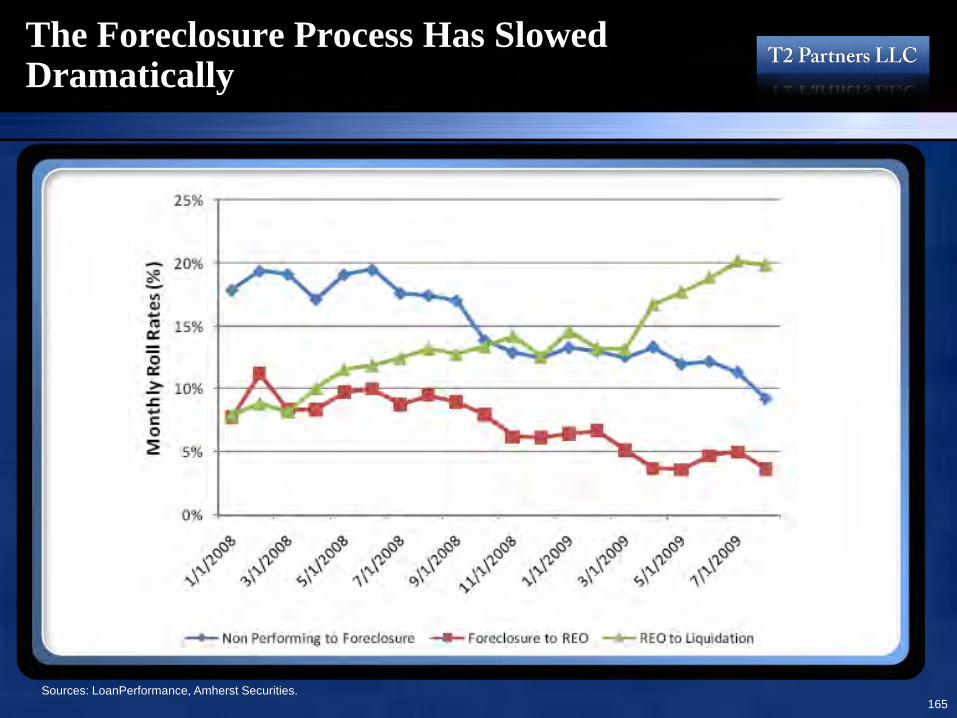

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

Rea

l Hom

e Pr

ice

Inde

x (1

890=

100)

ShillerLawler

Trend Line

HousingBubble

11

Prices Exploded Because the Borrowing Power of a Typical Home Purchaser More Than Tripled from 2000-2006

Source: Amherst Securities.

$0

$100,000

$200,000

$300,000

$400,000

Jan-95 Jan-96 Jan-97 Jan-98 Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08

Pre-Tax IncomeBorrowing Power

3.3x in January 2000

9.2x in January 2006

Factors contributing to the ability to borrow more and more were:

1. Lenders were willing to allow much higher debt-to-income ratios

2. Interest-only mortgages (vs. full amortizing)3. No money down4. Low- and no-documentation loans, which led

to widespread fraud5. Slowly rising income6. Falling interest rates

12

Americans Have Borrowed Heavily Against Their Homes Such That the Percentage of Equity Has Fallen Below 50% for the First TimeThere still appears to be substantial equity protecting the debt – but this is misleading. Given that 1/3 of homes have no mortgage (i.e., 100% equity), the remaining homes have only 16% equity. A further 10% decline in home prices would, on average, leave little equity cushion to support U.S. mortgage debt.

Source: Federal Reserve Flow of Fund Accounts of the United States.

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

1945 1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

Mor

tgag

e D

ebt (

Bn)

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Equity as a %

of Hom

e Value

1945Mortgage Debt: $18.6 billionEquity: $97.5 billion

Q309Mortgage Debt: $10.3 trillionEquity: $7.9 trillion

13

Housing Became Unaffordable in Many Areas Using a Typical 30-Year Fixed-Rate Mortgage, Which Led Many Borrowers to Take Exotic Mortgages

Sources: NAHB/Wells Fargo Housing Opportunity Index, which measures percentage of households that could afford the average home with a standard mortgage.

0

10

20

30

40

50

60

70

80

Q1 199

6

Q1 199

7

Q1 199

8

Q1 199

9

Q1 200

0

Q1 200

1

Q1 200

2

Q3 200

4

Q3 200

5

Q3 200

6

Q3 200

7

Hou

sing

Opp

ortu

nity

Inde

x

Riverside, CALos Angeles, CASan Diego, CA

14

There Was a Dramatic Decline in Mortgage Lending Standards from 2001 through 2006

• In 2005, 29% of new mortgages were interest only — or less, in the case of Option ARMs — vs. 1% in 2001

• In 1989, the average down payment for first-time home buyers was 10%; by 2007, it was 2%

• The sale of new homes costing $750,000 or more quadrupled from 2002 to 2006. The construction of inexpensive homes costing $125,000 or less fell by two-thirds

7474

76

81

83

84

81

68

70

72

74

76

78

80

82

84

86

2001 2002 2003 2004 2005 2006 2007

Com

bine

d Lo

an to

Val

ue (%

)

1% 1%

3%

9%

14%

17%

8%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

2001 2002 2003 2004 2005 2006 2007

Perc

ent o

f Orig

inat

ions

33%

39%

45%

49%

56%

63%65%

0%

10%

20%

30%

40%

50%

60%

70%

2001 2002 2003 2004 2005 2006 2007

Perc

ent o

f Orig

inat

ions

0% 0%

1%

4%

8%

11%

5%

0%

2%

4%

6%

8%

10%

12%

2001 2002 2003 2004 2005 2006 2007

Perc

ent o

f Orig

inat

ions

Combined Loan to Value 100% Financing

Limited Documentation 100% Financing & Limited Doc

Sources: Amherst Securities, LoanPerformance; USA Today (www.usatoday.com/money/economy/housing/2008-12-12-homeprices_N.htm).

Why Did It Happen?

16

Among the Many Causes of The Great Housing Bubble, Two Stand Out

1. The lenders making crazy loans didn’t care if the homeowner ended up defaulting for two reasons:

– They didn’t hold the loan, but instead sold it to someone else. It was eventually bought by a Wall Street firm, which packaged it with thousands of other mortgages in a Residential Mortgage-Backed Security (RMBS), which was then sliced into numerous tranches that were sold to investors around the world. This entire process was extraordinarily profitable for all involved, especially the Wall Street firms and the rating agencies;

– Or, if they did plan to hold the loan, they assumed home prices would keep rising, such that homeowners could either refinance before loans reset or, if the homeowner defaulted, the losses (i.e., severity) would be minimal.

2. The entire system – real estate agents, appraisers, mortgage lenders, banks, Wall St. firms and rating agencies – became corrupted by the vast amounts of quick money to be made

There were many other reasons, of course – a bubble of this magnitude requires what Charlie Munger calls “lollapalooza effects”

– Regulators and politicians were blinded by free market ideology and/or the dream that all Americans should own their homes, causing them to fall asleep at the switch, not want to take the punch bowl away and/or get bought off by the industries they were supposed to be overseeing

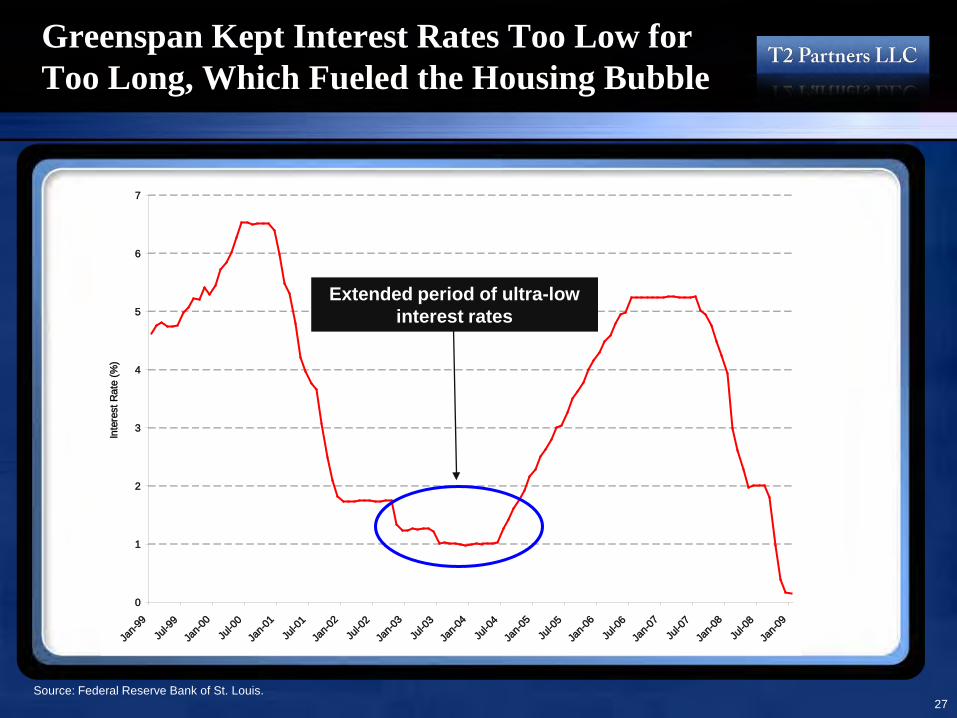

– Debt became increasingly available and acceptable in our culture– Millions of Americans became greedy speculators and/or took on too much debt– Greenspan kept interest rates too low for too long– Institutional investors stretched for yield, didn’t ask many questions and took on too

much leverage– In general, everyone was suffering from irrational exuberance, driven by the money

being made

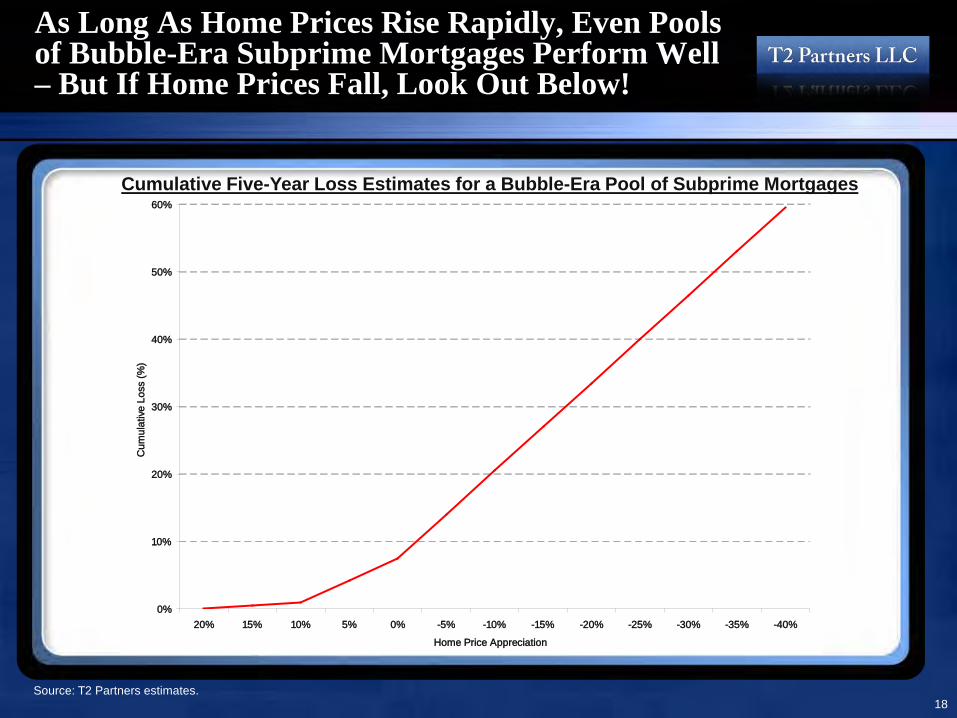

When Home Price Appreciation Slows, Loss Severity Skyrockets

Sources: LoanPerformance; OFHEO; Deutsche Bank; “Who's Holding the Bag?”, Pershing Square presentation, 5/23/07.

The assumption of perpetually rapidly rising home prices led lenders to give virtually anyone a loan because even if they defaulted, the home could simply be resold with little or no loss.

17

18

As Long As Home Prices Rise Rapidly, Even Pools of Bubble-Era Subprime Mortgages Perform Well – But If Home Prices Fall, Look Out Below!

Source: T2 Partners estimates.

0%

10%

20%

30%

40%

50%

60%

20% 15% 10% 5% 0% -5% -10% -15% -20% -25% -30% -35% -40%Home Price Appreciation

Cum

ulat

ive L

oss

(%)

Cumulative Five-Year Loss Estimates for a Bubble-Era Pool of Subprime Mortgages

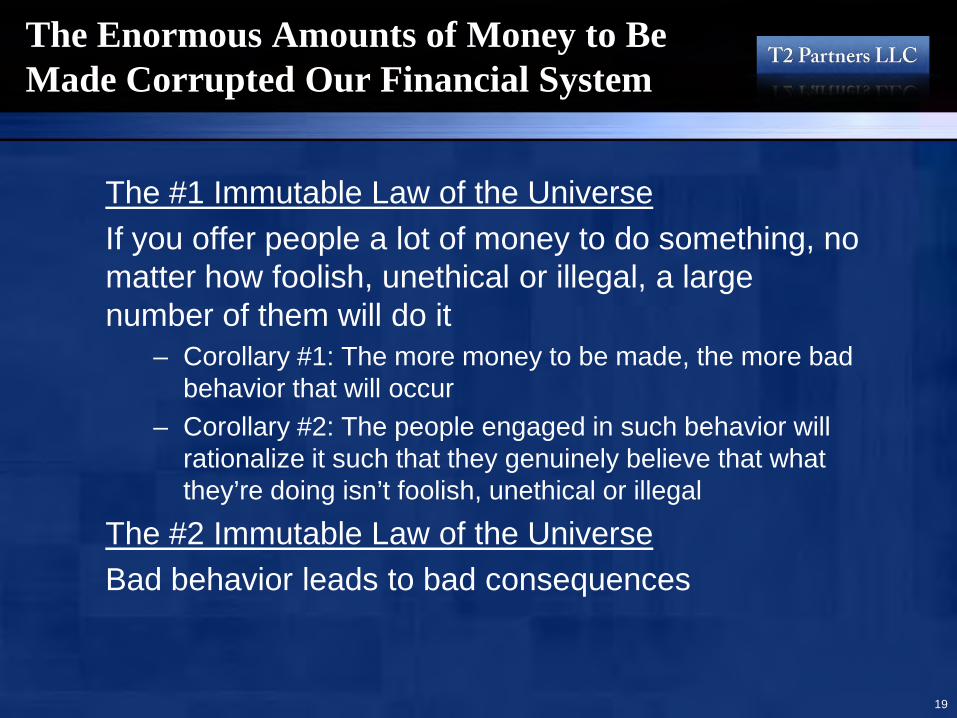

The Enormous Amounts of Money to Be Made Corrupted Our Financial System

The #1 Immutable Law of the UniverseIf you offer people a lot of money to do something, no matter how foolish, unethical or illegal, a large number of them will do it

– Corollary #1: The more money to be made, the more bad behavior that will occur

– Corollary #2: The people engaged in such behavior will rationalize it such that they genuinely believe that what they’re doing isn’t foolish, unethical or illegal

The #2 Immutable Law of the UniverseBad behavior leads to bad consequences

19

20

Deregulation of the Financial Sector Led to a Surge of Compensation, Leverage and Profits

Source: Ariell Reshef, University of Virginia; Thomas Philippon, NYU; Wall St. Journal, 5/14/09.

Ratio of Financial Services Wages to Nonfarm Private-Sector Wages, 1910-2006

21Sources: Federal Reserve, BEA, as of Q2 2007, GMO presentation.

Low Debt Era Rising Debt Era

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

51 54 57 60 63 66 69 72 75 78 81 84 87 90 93 96 99 02 05

Fina

ncia

l Pro

fits

as P

erce

nt o

f GD

P

100%

150%

200%

250%

300%

350%

Total Debt as Percent of G

DP

Dec-

Total Debt

Financial Profits

Over the Past 30 Years, We Have Become a Nation Gorged in Debt – To The Benefit of Financial Services Firms

Profits and Wages in the Financial Sector Soared from 1980 Onward

Source: Moody’s Economy.com, NY Times, 12/18/08. 22

23

Wall Street Firms Were Making a Fortune Securitizing Loans

• Among the most profitable areas for Wall Street firms was producing Asset-Backed Securities (ABSs) and Collateralized Debt Obligations (CDOs)

• To produce ABSs and CDOs, Wall Street needed a lot of loan “product”

• Mortgages were a quick, easy, big source• It is easy to generate higher and higher volumes of

mortgage loans: simply lend at higher loan-to-value ratios, with ultra-low teaser rates, to uncreditworthy borrowers, and don’t bother to verify their income and assets (thereby inviting fraud)

• There’s only one problem:

DON’T EXPECT TO BE REPAID!

Mortgages Were Pooled into RMBSs, Tranches of Which Were Pooled into CDOs

This is an example of a “Mezzanine CDO.” A “High-Grade CDO” would select collateral primarily from the A and AA tranches mixed with ~25% senior tranches from other, often mezzanine, CDOs

Note: Asset-based securities backed by home mortgages are called Residential Mortgage-Backed Securities (RMBS), those backed by commercial real estate loans are called Commercial Mortgage-Backed Securities (CMBS), etc. Source: Citigroup, All Clogged Up: What’s Ailing the Financial System, 2/13/08.

Loss rates of, say, 20%, in the underlying RMBS’s can lead to catastrophic losses for a CDO

Equity

BBB

BBB

BBB

BBB

BBB

BBB

BBB

BBB

BBB

BBB

BBB

BBB

BBB

Equity

BBB

Equity

A

BBB- ABBB

A

A

A

AA

AA

AA

AAA

AAA

AAA

SuperSenior

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

RMBS CDO Composition CDO Rating

24

A Case Study of Wall StreetCompensation Run Amok:Stan O’Neal, Dow Kim & the Mortgage Team at Merrill Lynch

Source: On Wall Street, Bonuses, Not Profits, Were Real, NY Times, 12/18/08.

25

The Rating Agencies Were Making a Fortune Rating Structured Finance Products

$10.00

$20.00

$30.00

$40.00

$50.00

$60.00

$70.00

2003 2004 2005 2006

Moody’s Stock Price Reflected Its Surge in Profits

Source: Yahoo! Finance.26

Greenspan Kept Interest Rates Too Low for Too Long, Which Fueled the Housing Bubble

0

1

2

3

4

5

6

7

Jan-9

9Ju

l-99

Jan-0

0Ju

l-00

Jan-0

1Ju

l-01

Jan-0

2Ju

l-02

Jan-0

3Ju

l-03

Jan-0

4Ju

l-04

Jan-0

5Ju

l-05

Jan-0

6Ju

l-06

Jan-0

7Ju

l-07

Jan-0

8Ju

l-08

Jan-0

9

Inte

rest

Rat

e (%

)

Source: Federal Reserve Bank of St. Louis.27

Extended period of ultra-low interest rates

Background on the U.S. Housing Market

29

There Was a Surge of Toxic Mortgages From 2000 to Mid-2007

Source: Inside Mortgage Finance, published by Inside Mortgage Finance Publications, Inc. Copyright 2009.

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Orig

inat

ions

(Bn)

Conforming, FHA/VAJumboAlt-ASubprimeSeconds

30

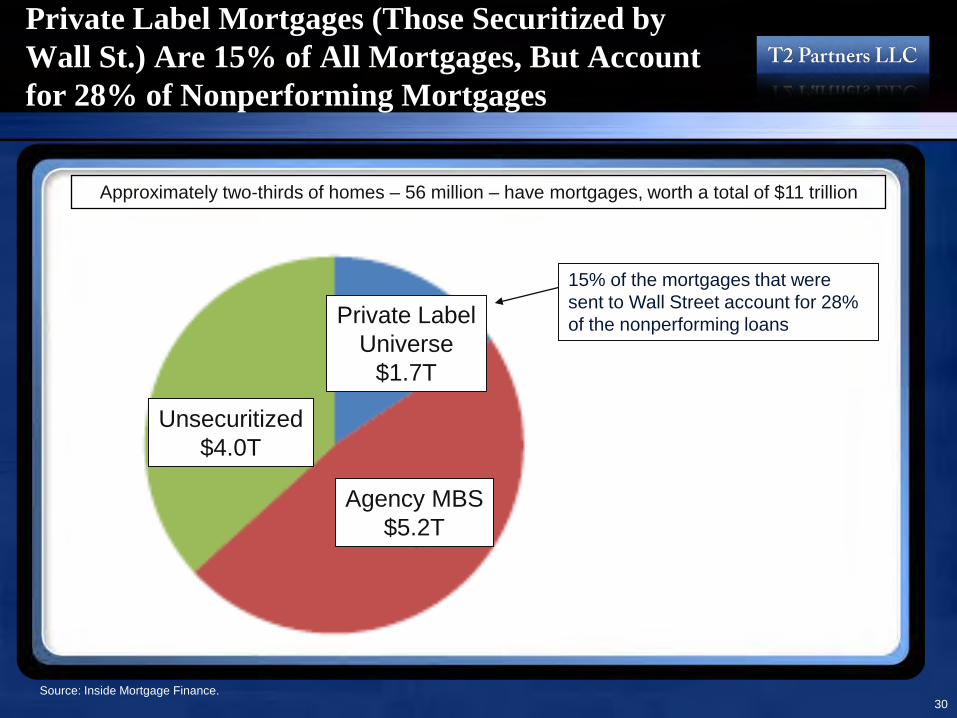

Private Label Mortgages (Those Securitized by Wall St.) Are 15% of All Mortgages, But Account for 28% of Nonperforming Mortgages

15% of the mortgages that were sent to Wall Street account for 28% of the nonperforming loans

Source: Inside Mortgage Finance.

Approximately two-thirds of homes – 56 million – have mortgages, worth a total of $11 trillion

Agency MBS$5.2T

Private LabelUniverse

$1.7T

Unsecuritized$4.0T

31

More Than 14% of Mortgages on 1-to-4 Family Homes Were Delinquent or in Foreclosure as of Q3 2009

Source: National Delinquency Survey, Mortgage Bankers Association; T2 Partners estimates. Note: Delinquencies (30+ days) are seasonally adjusted.

4%

6%

8%

10%

12%

14%

16%

Per

cent

age

of H

ome

Loan

s

32

All Types of Loans Are Seeing a Surge in Delinquencies, Led by Subprime

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

Q1 199

9

Q3 199

9

Q1 200

0

Q3 200

0

Q1 200

1

Q3 200

1

Q1 200

2

Q3 200

2

Q1 200

3

Q3 200

3

Q1 200

4

Q3 200

4

Q1 200

5

Q3 200

5

Q1 200

6

Q3 200

6

Q1 200

7

Q3 200

7

Q1 200

8

Q3 200

8

Per

cent

Non

curr

ent

Alt AOption ARMJumboSubprimePrimeHome Equity Lines of Credit

Sources: Amherst Securities, LoanPerformance; National Delinquency Survey, Mortgage Bankers Association; FDIC Quarterly Banking Profile;T2 Partners estimates. Note: Prime is seasonally adjusted.

An Examination of Subprime, Prime and Alt-A Loans

34

The Decline in Lending Standards Led to a Surge in Subprime Mortgage Origination

Source: Reprinted with permission; Inside Mortgage Finance, published by Inside Mortgage Finance Publications, Inc. Copyright 2009.

10% 9%9%

10%9%

10%10%

7% 7%8%

18%

20%20%

8%

$0

$100

$200

$300

$400

$500

$600

$700

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Originations(Bn)

0%

5%

10%

15%

20%

25%

% ofTotal

35

$0

$5

$10

$15

$20

$25

$30

$35

Jan-0

6Apr-

06Ju

l-06

Oct-06

Jan-0

7Apr-

07Ju

l-07

Oct-07

Jan-0

8Apr-

08Ju

l-08

Oct-08

Jan-0

9Apr-

09Ju

l-09

Oct-09

Jan-1

0Apr-

10Ju

l-10

Oct-10

Loan

s w

ith P

aym

ent S

hock

(Bn)

Sources: LoanPerformance, Deutsche Bank; slide from Pershing Square presentation, How to Save the Bond Insurers, 11/28/07.

The Wave of Resets from Subprime Loans Is Mostly Behind Us

We are here

36Sources: Amherst Securities.

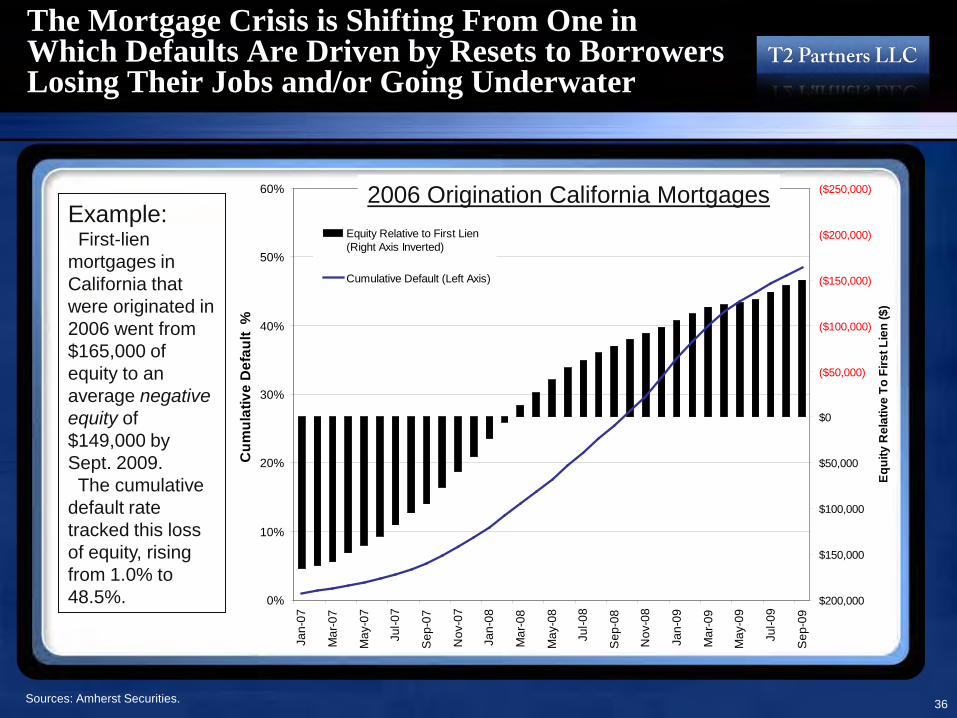

The Mortgage Crisis is Shifting From One in Which Defaults Are Driven by Resets to Borrowers Losing Their Jobs and/or Going Underwater

Example:First-lien

mortgages in California that were originated in 2006 went from $165,000 of equity to an average negative equity of $149,000 by Sept. 2009. The cumulative

default rate tracked this loss of equity, rising from 1.0% to 48.5%. 0%

10%

20%

30%

40%

50%

60%

Jan-

07

Mar

-07

May

-07

Jul-0

7

Sep

-07

Nov

-07

Jan-

08

Mar

-08

May

-08

Jul-0

8

Sep

-08

Nov

-08

Jan-

09

Mar

-09

May

-09

Jul-0

9

Sep

-09

Cum

ulat

ive

Def

ault

%

($250,000)

($200,000)

($150,000)

($100,000)

($50,000)

$0

$50,000

$100,000

$150,000

$200,000

Equi

ty R

elat

ive

To F

irst L

ien

($)

Equity Relative to First Lien(Right Axis Inverted)

Cumulative Default (Left Axis)

2006 Origination California Mortgages

37

The Mortgage Meltdown Has Moved Beyond Subprime to Five Other Areas

Sources: Federal Reserve Flow of Funds Accounts of the United States, IMF Global Financial Stability Report October 2008, Goldman Sachs Global Economics Paper No. 177, FDIC Quarterly Banking Profile, OFHEO, S&P Leverage Commentary & Data, T2 Partners estimates.

$0.0 $0.5 $1.0 $1.5 $2.0 $2.5 $3.0 $3.5 $4.0 $4.5 $5.0

CDO/ CLO

Other Consumer

Construction & Development

Option ARM

Auto

Credit Card

Home Equity

Jumbo Prime

High-Yield / Leveraged Loans

Subprime

Commercial & Industrial

Other Corporate

Alt-A

Commercial Real Estate

Prime Mortgage

Amount Outstanding (Trillions)

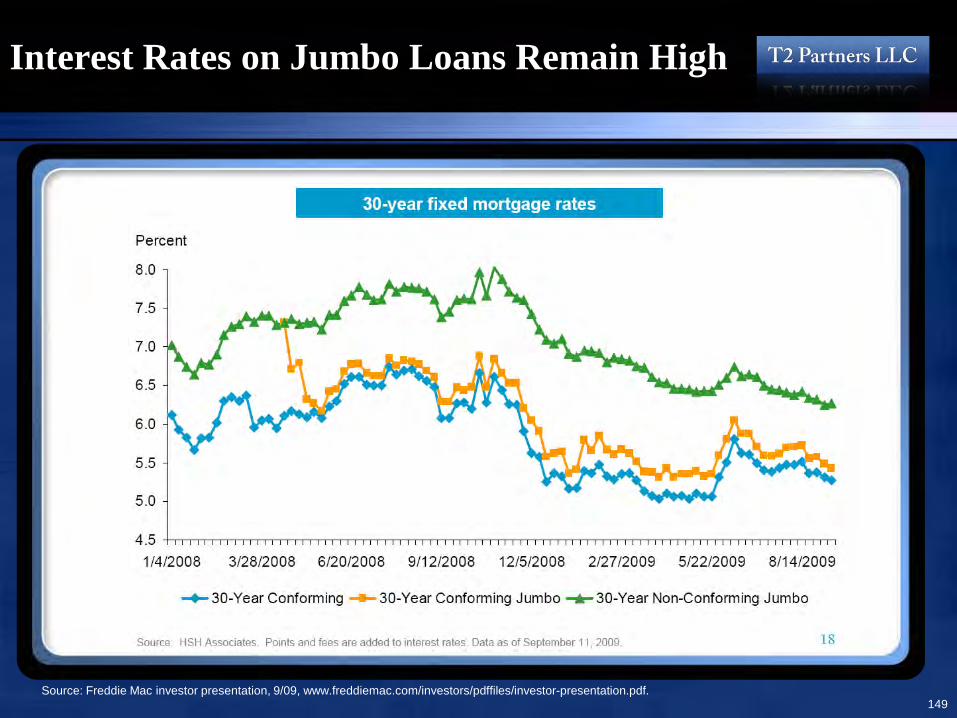

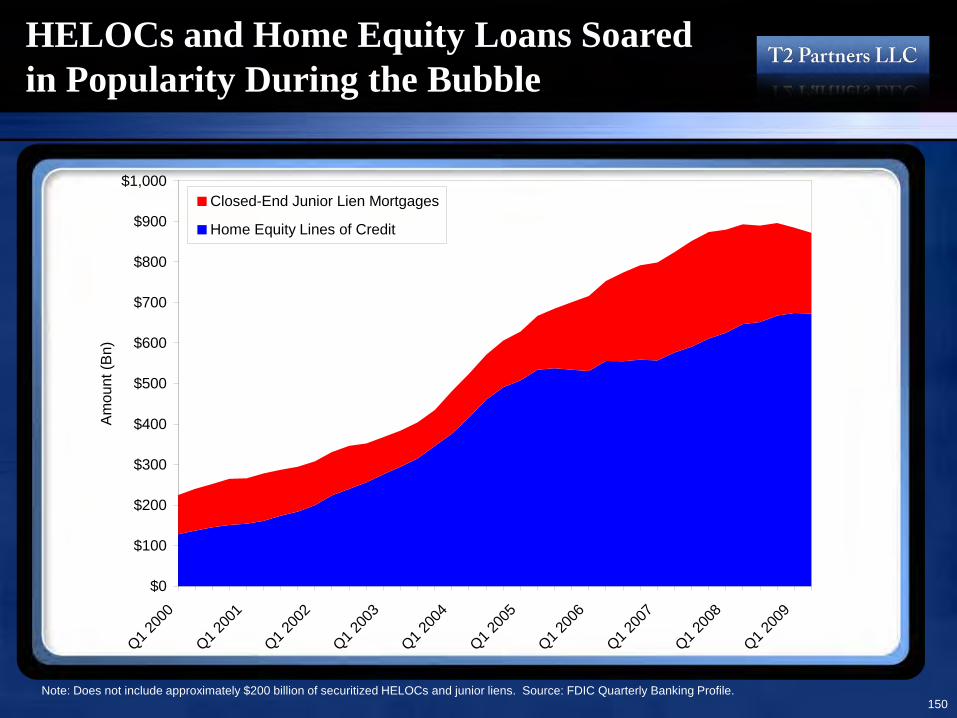

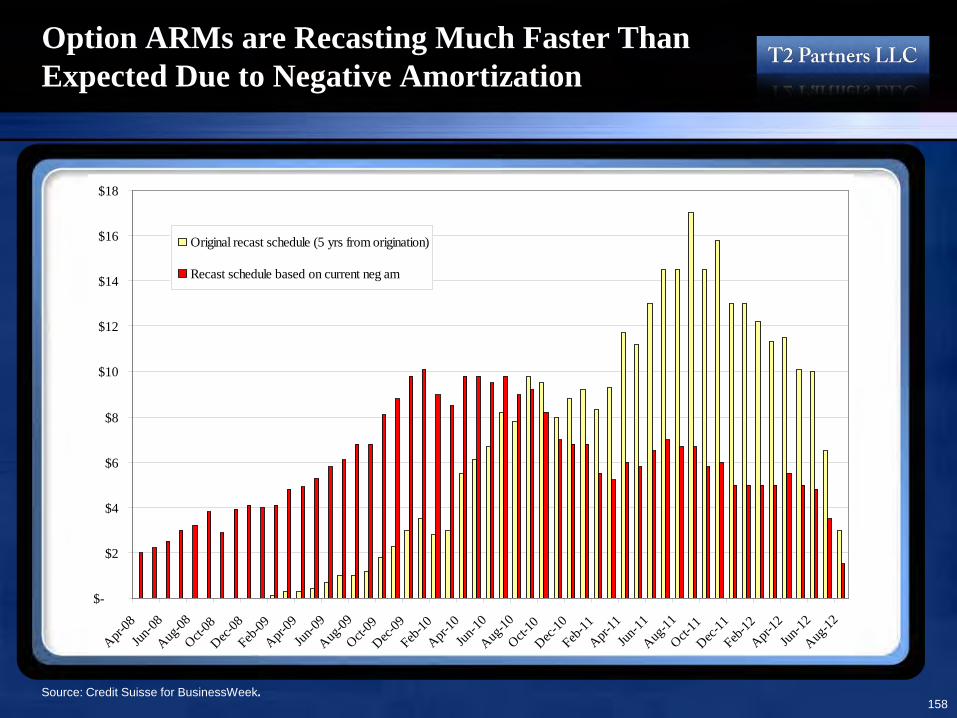

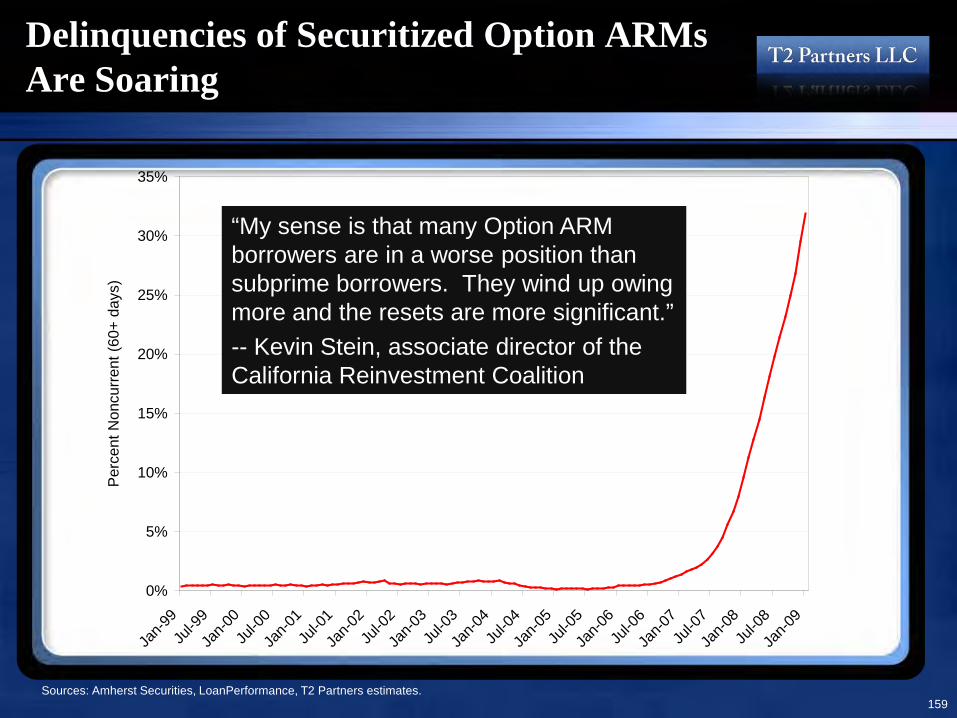

For further details about Jumbo Prime, HELOCs and Option ARMs, see the Appendix

Subprime is only a small part of the problem

38

Delinquencies of Prime and Alt-A Mortgages Are Soaring

Source: New York Times, 5/24/09.

39

Delinquencies of Prime Mortgages Are Soaring

Source: Mortgage Bankers Association National Delinquency Survey.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Q1 199

9

Q3 199

9

Q1 200

0

Q3 200

0

Q1 200

1

Q3 200

1

Q1 200

2

Q3 200

2

Q1 200

3

Q3 200

3

Q1 200

4

Q3 200

4

Q1 200

5

Q3 200

5

Q1 200

6

Q3 200

6

Q1 200

7

Q3 200

7

Q1 200

8

Q3 200

8

Per

cent

Non

curr

ent (

60+

days

)

40

Fannie Mae and Freddie Mac Serious Delinquencies Are Soaring

Note: Serious delinquencies are loans that have missed three or more consecutive payments (90+ days).Source: Company filings.

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

5.0%

Fannie

Freddie

41

Freddie Mac’s Delinquency Rate by Vintage Underscores the Decline in Lending Standards

* Represents the cumulative transition rate of loans to a default event, and is calculated for each year of origination as the number of loans that have proceeded to foreclosure, acquisition or other disposition events, excluding liquidations through voluntary pay-off, divided by the number of loans in our single-family mortgage portfolio. Excludes certain Structured Transactions. Source: Company filing.

Total Single-Family Portfolio Cumulative Default Rates* by Book Year

42

There Is a Surge of Notices of Default and Foreclosures Among the GSEs

Prime Notices of Default

Subprime Notices of Default

Prime ForeclosuresSubprime Foreclosures

Source: The Field Check Group.

43

The Foreclosure Problem Is No Longer Only a Bubble State Phenomenon

Source: New York Times, 5/24/09.

15 States With the Highest Prime Mortgage Foreclosure Rates

44

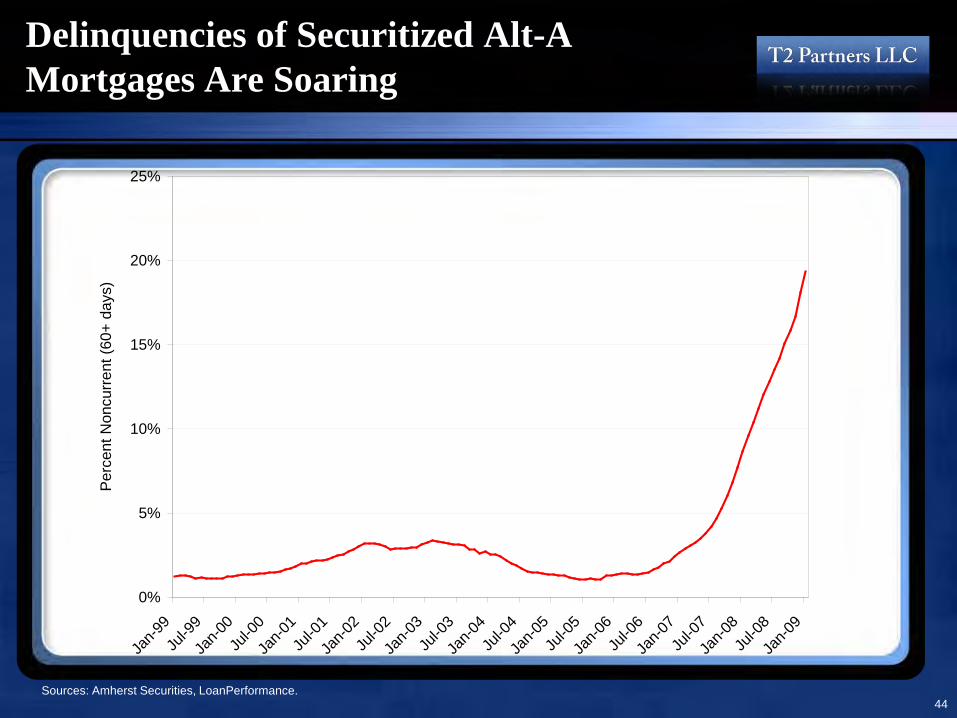

Delinquencies of Securitized Alt-A Mortgages Are Soaring

Sources: Amherst Securities, LoanPerformance.

0%

5%

10%

15%

20%

25%

Jan-9

9Ju

l-99

Jan-0

0Ju

l-00

Jan-0

1Ju

l-01

Jan-0

2Ju

l-02

Jan-0

3Ju

l-03

Jan-0

4Ju

l-04

Jan-0

5Ju

l-05

Jan-0

6Ju

l-06

Jan-0

7Ju

l-07

Jan-0

8Ju

l-08

Jan-0

9

Per

cent

Non

curr

ent (

60+

days

)

45

Alt-A Delinquencies By Vintage Show the Collapse in Lending Standards in 2006 and 2007

Sources: Amherst Securities, LoanPerformance.

0%

5%

10%

15%

20%

25%

30%

0 5 10 15 20 25 30 35 40 45 50 55 60

Months of Seasoning

Per

cent

Non

curr

ent (

60+

days

)

2007 2006

2005

2004

2003

46

There Are $2.4 Trillion of Alt-A Mortgages --And Their Resets Are Mostly Ahead of Us

$0

$1

$2

$3

$4

$5

$6

$7

$8

$9

$10

Jan-1

0Ju

l-10

Jan-1

1Ju

l-11

Jan-1

2Ju

l-12

Jan-1

3Ju

l-13

Jan-1

4Ju

l-14

Jan-1

5Ju

l-15

Am

ount

(Bn)

$0$50

$100$150

$200$250

$300

Estim

ated Cum

ulative Reset A

mount (B

n)

We are here

Sources: Credit Suisse, LoanPerformance.

NOTE: This chart only shows resets for a small fraction of Alt-A loans, but is representative of all of them.

47

Two Waves of Losses Are Behind Us…But Three Are Looming

Losses Mostly Behind Us• Wave #1: Borrowers committing (or the victim of) fraud, as well as

speculators, who defaulted quickly. Timing: beginning in late 2006 (as soon as home prices started to fall) into 2008. Mostly behind us.

• Wave #2: Mostly subprime borrowers who defaulted when their mortgages reset due to payment shock. Timing: early 2007 (as two-year teaser subprime loans written in early 2005 started to reset) to the present. Now tapering off as low interest rates mitigate payment shock.

Losses Mostly Ahead of Us• Wave #3: Prime loans (most of which are owned or guaranteed by the

GSEs) defaulting due to job loss and home price declines (i.e., underwater homeowners). Timing: started to surge in early 2008 to the present.

• Wave #4: Jumbo prime, second lien and HELOCs (most of which are on banks’ books) defaulting due to job loss and home price declines/ underwater homeowners. Timing: started to surge in early 2008 to the present.

• Wave #5: Losses among loans outside of the housing sector, the largest of which will be in the $3.5 trillion area of commercial real estate. Timing: started to surge in early 2008 to the present.

48

Why Won’t the System Collapse Again?

Given that the three looming waves are much larger than the two that are mostly behind us, why won’t they trigger a collapse of our financial system similar to what happened in late 2008?

Answer: Last year’s collapse was triggered in part by the magnitude of the losses, but also because of the suddenness. Financial institutions can withstand even large losses if they trickle in over time because they can offset losses each quarter with profits earned during the quarter – but this isn’t possible if losses are sudden.

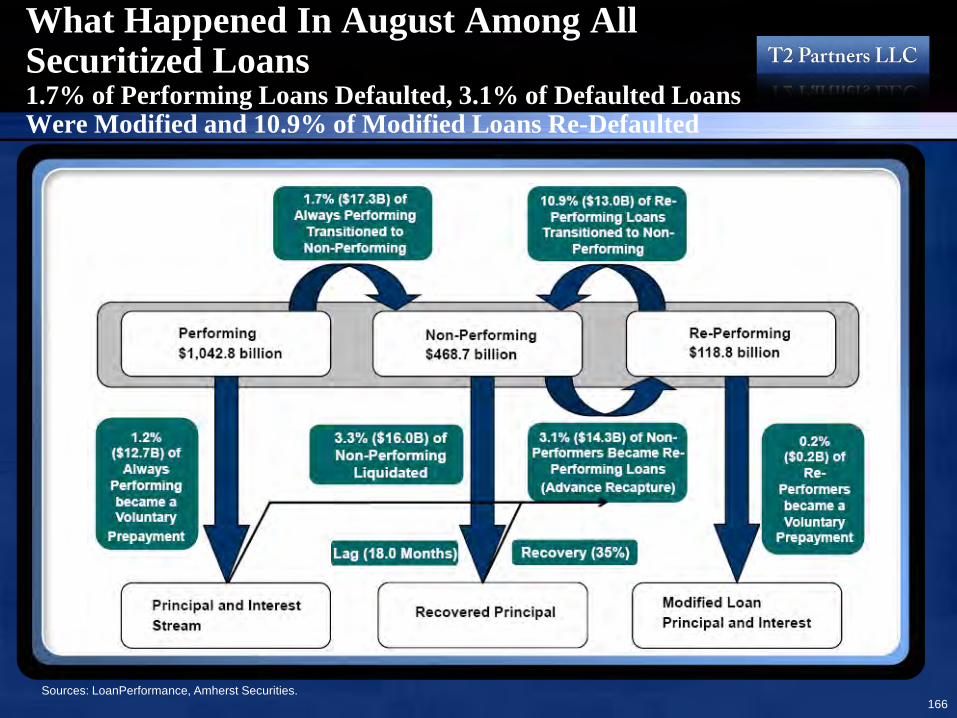

The suddenness of last year’s losses was due in part to rapidly rising defaults, especially among subprime mortgages, but in fact, realized losses were still quite low. The real culprit was the fact that most subprime loans had been securitized into RMBSs and CDOs, turning them into tradable debt instruments.

According to GAAP accounting rules, traded instruments like stocks and bonds have to be marked to market, and in only a few months in 2008, the market price for hundreds of billions of dollars of AAA-rated RMBS and CDO securities went from close to 100 cents on the dollar to the 20-30 cent range (even though the underlying pools of mortgages hadn’t yet realized much in the way of losses). This required every institution holding these securities to immediately book enormous losses, which caused many of them to collapse.

Why did Merrill Lynch, Citigroup, Lehman and Bear Stearns fall, but Wells Fargo didn’t? Because Wells had almost nothing on its balance sheet that had to be marked to market.

Big mark to market losses are now behind us, so it’s unlikely that there will be any sudden shocks to the system. Instead, hundreds of billions of dollars of additional losses from trillions of dollars of bad loans will be realized over many, many years.

This is both good news and bad news: the good news is that while future losses will surely bankrupt many banks, especially smaller ones exposed to commercial real estate, they likely won’t threaten the system because banks are earning so much money currently that most should be able to outrun their losses.

The bad news is that very high losses will plague our financial system for many years to come –our best guess is current extremely high levels for another two years, and then slowly declining for three more years before finally returning to normal levels in five years. This drip torture of high losses every quarter, year after year, will likely keep banks extremely cautious in their lending, making robust economic growth unlikely.

49

The Housing Crisis is Shifting in a Number of Ways

First Stage of Collapse1. Subprime & fraudulent loans

account for most defaults

2. Defaults driven by loans resetting

3. Defaults mainly in sand and rust states

4. Mark-to-market losses due to bad loans being securitized

5. Little government intervention

Current Stage1. Prime, Alt-A and other loans to

better borrowers drive defaults

2. Defaults driven by job losses and underwater mortgages

3. Defaults occurring across a broad swath of the country

4. Losses from on-balance-sheet loans (not marked to market)

5. Massive government intervention

Current Status of the Housing Market

51

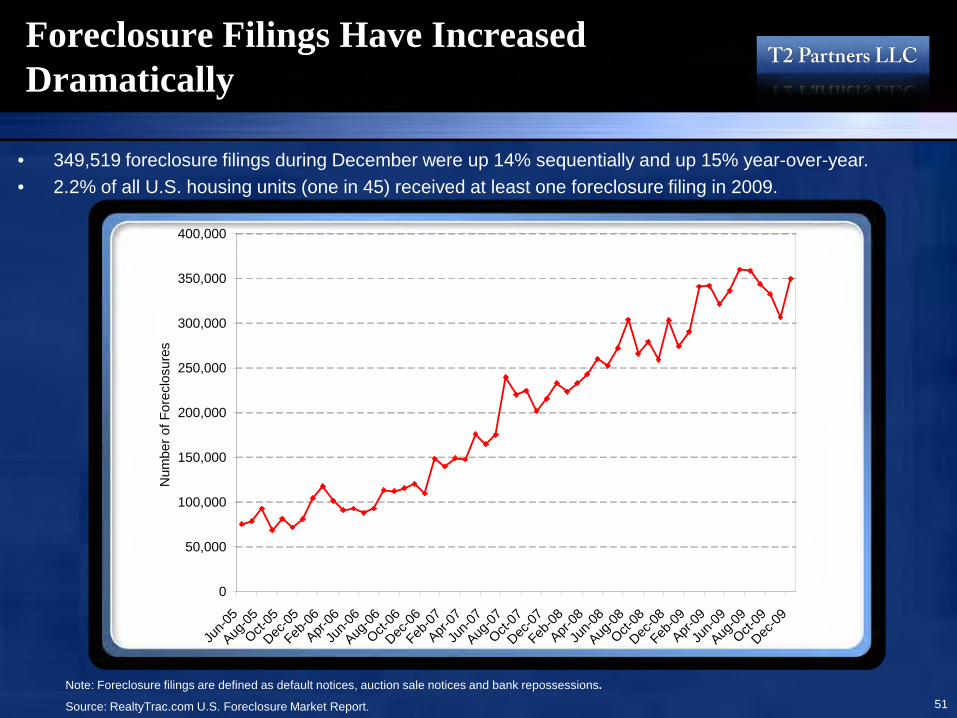

Foreclosure Filings Have Increased Dramatically

• 349,519 foreclosure filings during December were up 14% sequentially and up 15% year-over-year.• 2.2% of all U.S. housing units (one in 45) received at least one foreclosure filing in 2009.

Note: Foreclosure filings are defined as default notices, auction sale notices and bank repossessions.

Source: RealtyTrac.com U.S. Foreclosure Market Report.

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

Jun-0

5

Aug-05

Oct-05

Dec-05

Feb-06

Apr-06

Jun-0

6

Aug-06

Oct-06

Dec-06

Feb-07

Apr-07

Jun-0

7

Aug-07

Oct-07

Dec-07

Feb-08

Apr-08

Jun-0

8

Aug-08

Oct-08

Dec-08

Feb-09

Apr-09

Jun-0

9

Aug-09

Oct-09

Dec-09

Num

ber o

f For

eclo

sure

s

52

The Delinquency and Foreclosure Problem Has Spread Far Beyond the Bubble States

Source: LPS Applied Analytics, WSJ 10/22/09.

Credit Suisse Predicts More Than 6 Million Additional Foreclosures by the End of 2012

Sources: Credit Suisse, 9/08; http://calculatedrisk.blogspot.com 53

This chart is quite dated, but accurately shows how the foreclosure crisis is shifting away from subprime.

54

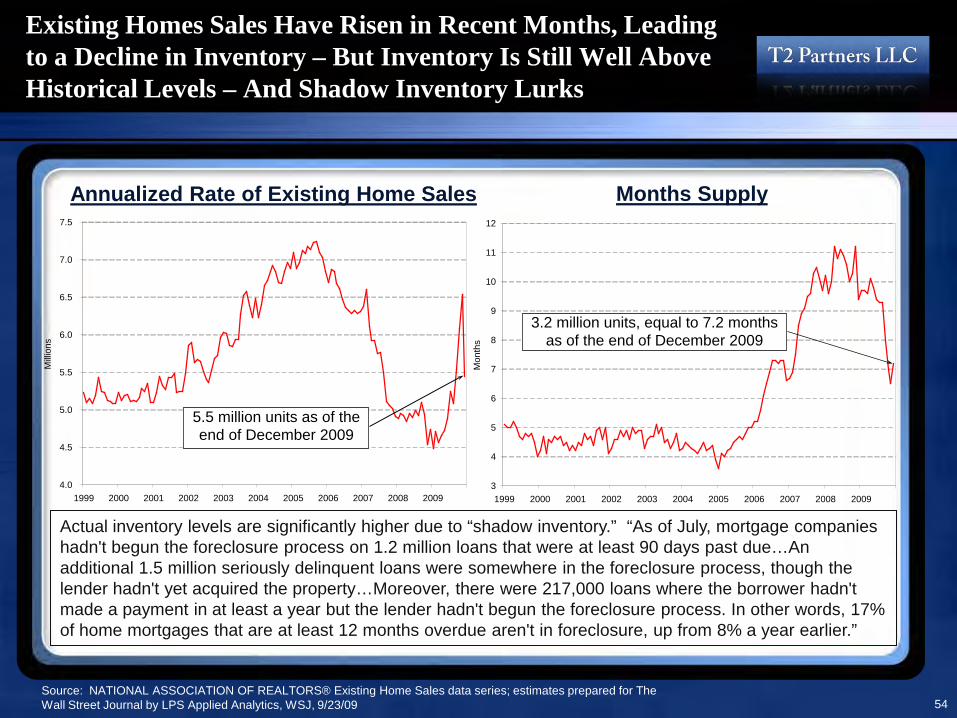

Existing Homes Sales Have Risen in Recent Months, Leading to a Decline in Inventory – But Inventory Is Still Well Above Historical Levels – And Shadow Inventory Lurks

Source: NATIONAL ASSOCIATION OF REALTORS® Existing Home Sales data series; estimates prepared for The Wall Street Journal by LPS Applied Analytics, WSJ, 9/23/09

Months SupplyAnnualized Rate of Existing Home Sales

Actual inventory levels are significantly higher due to “shadow inventory.” “As of July, mortgage companies hadn't begun the foreclosure process on 1.2 million loans that were at least 90 days past due…An additional 1.5 million seriously delinquent loans were somewhere in the foreclosure process, though the lender hadn't yet acquired the property…Moreover, there were 217,000 loans where the borrower hadn't made a payment in at least a year but the lender hadn't begun the foreclosure process. In other words, 17% of home mortgages that are at least 12 months overdue aren't in foreclosure, up from 8% a year earlier.”

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Mill

ions

5.5 million units as of the end of December 2009

3

4

5

6

7

8

9

10

11

12

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Mon

ths

3.2 million units, equal to 7.2 months as of the end of December 2009

55

Thanks to Massive Government Stimulus (Mainly the FHA & the $8,000 First-Time Homebuyers Tax Credit), Sales from June-Sept. 2009 Were Higher Than 2008, But This May Not Last

Source: Mark Hanson Advisors.

Note how seasonal home sales are

56

Thanks to Massive Government Stimulus (Mainly the FHA & the $8,000 First-Time Homebuyers Tax Credit), Sales from June-Sept. 2009 Were Higher Than 2008, But This May Not Last

Source: Mark Hanson Advisors.

Note how seasonal home sales are

Organic sales are highly seasonal, while distressed sales are have fallen in recent months due to loan mods

57

Inventory is Moving at the Low End, But As the High End Tips Over, Sales Are Falling and Inventories Are Ballooning

Sources: JP Morgan; CA Assoc. of Realtors (left chart); National Assoc. of Realtors via Moody’s Economy.com, WSJ 6/22/09 (right chart).

Months Inventory in CA By Home Price

Another example: based on the rate of sales over the seven months ending in May 2009, there is five years of housing inventory in Greenwich, CT

Sudbury, MA (July data)

Months ofPrice Inventory>$250K 6$250-500 8$500-750 5$750-1M 14$1M+ 51

58

Defaults Are Massively Outpacing Liquidations, So the Inventory Overhang Continues to Worsen

Note: This data is based on approximately 28 million loans. Total first-time defaults are running at 300,000/month.Source: First American CoreLogic Loan-Level Servicing Data, Amherst Securities.

First time defaults

Liquidations

59

Defaulted Mortgages Are Taking Longer to Liquidate, Adding to the Inventory Overhang

Source: First American CoreLogic Loan-Level Servicing Data, Amherst Securities.

60

Cure Rates Have Fallen Such That Once a Homeowner Misses Two Payments, A Foreclosure Is Almost Inevitable

Source: Loan Performance, Amherst Securities.

61

The Current “Housing Overhang” Is 7 Million Homes –Which Doesn’t Include Any New Defaults, Which Are Running at Approximately 300,000/Month!

Source: Mortgage Bankers Association, Loan Performance, Amherst Securities.

62

Shadow Inventory for Each of the 20 Cities in the Case-Shiller Index

Note: Notice of Default data is incomplete or missing for many cities.Source: www.trulia.com, Amherst Securities.

Outlook for Housing Prices

64

Home Prices Were in an Unprecedented Freefall Until A Slight Bounce in Q209

Sources: Standard & Poor’s, OFHEO Purchase-Only Index, NATIONAL ASSOCIATION OF REALTORS® Existing Home Sales data series.

100

120

140

160

180

200

220

Q1 200

0

Q3 200

0

Q1 200

1

Q3 200

1

Q1 200

2

Q3 200

2

Q1 200

3

Q3 200

3

Q1 200

4

Q3 200

4

Q1 200

5

Q3 200

5

Q1 200

6

Q3 200

6

Q1 200

7

Q3 200

7

Q1 200

8

Q3 200

8

Q1 200

9

S&P/Case-Shiller U.S. National Home Price IndexS&P/Case-Shiller 20-City CompositeOFHEO Purchase-Only IndexNAR Median Sales Price of Existing Homes

65

Home Prices Look Affordable Due to Price Declines and Ultra-Low Interest Rates

Source: Case-Shiller, Bureau of Labor Statistics, Amherst Securities.

0

100

200

300

400

500

600

700

800

Inde

x Va

lue

Date

CASE SHILLER USA (1975 = 100)

Modeled Home Prices - Interest Only

Modeled Home Prices - 30yr Fully Amortizing

S C Shill B f L b St ti ti Bl b A h t S iti

66

The Housing Affordability Index Shows Houses Are Now Affordable

14

16

18

20

22

24

26

1989

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

Mor

tgag

e P

aym

ent o

n M

edia

n P

riced

Hom

e as

% o

f Fam

ily In

com

e

Before concluding that houses are cheap, however, there are three big caveats: first, low rates are only available to those who qualify for conforming mortgages, which doesn’t help millions of homeowners or potential homeowners who have spotty credit histories or are underwater on their current mortgages. Second, with low enough interest rates, almost anything looks affordable; if rates rise, houses won’t look so reasonably priced based on these metrics. Finally, in light of the severe economic downturn, average income may fall for quite some time.

Source: NATIONAL ASSOCIATION OF REALTORS® Housing Affordability Index.

67

Home Prices Need to Fall Another 5-10% to Reach Trend Line

Sources: Robert J. Shiller, Irrational Exuberance: Second Edition, as updated by the author; Lawler Economic & Housing Consulting, T2 estimates.

100

125

150

175

200

225

250

275

300

1950

1954

1958

1962

1966

1970

1974

1978

1982

1986

1990

1994

1998

2002

2006

2009

Rea

l Hom

e Pr

ice

Inde

x (1

890=

100)

ShillerLawler

Trend Line

HousingBubble

68

GMO’s Study of Bubbles Shows That All of Them Eventually Return to Trend Line34 Have Returned to Trend; the Only Exception, British Housing, Is On Its Way

StocksS&P 5001920-1932

0.3

0.8

1.3

1.8

2.3

20 21 22 23 24 25 26 27 28 29 30 31

Det

rend

ed R

eal P

rice

Trend Line

S&P 5001946-1984

0.0

0.5

1.0

1.5

2.0

2.5

46 50 54 58 62 66 70 74 78 82

Det

rend

ed R

eal P

rice

Trend Line

Japan vs. EAFE ex-Japan1981-1999

0.00.51.01.52.02.53.0

81 83 85 87 89 91 93 95 97 99

Rel

ativ

e R

etur

n

Trend Line

S&P 5001992-October 2008

0.8

1.2

1.6

2.0

2.4

92 94 96 98 00 02 04 06 08

Det

rend

ed R

eal P

rice

Trend Line

CurrenciesU.S. Dollar1979-1992

0.81.01.21.41.61.82.0

79 81 83 85 87 89 91

Cum

ulat

ive

Ret

urn

U.K. Pound1979-1985

0.80.91.01.11.21.31.4

79 80 81 82 83 84

Cum

ulat

ive

Ret

urn

Japanese Yen1983-1990

0.80.91.01.11.21.31.4

83 84 85 86 87 88 89 90C

umul

ativ

e R

etur

n

Japanese Yen1992-1998

0.80.91.01.11.21.31.4

92 93 94 95 96 97

Cum

ulat

ive

Ret

urn

CommoditiesGold1970-1999

0

400

800

1200

1600

2000

70 74 78 82 86 90 94 98

Rea

l Pric

e

Crude Oil1962-1999

0

20

40

60

80

62 66 70 74 78 82 86 90 94 98

Rea

l Pric

e

Nickel1979-1999

0

50

100

150

200

250

79 81 83 85 87 89 91 93 95 97

Rea

l Pric

e

Cocoa1970-1999

0100200300400500600

70 74 78 82 86 90 94 98

Rea

l Pric

eSource: GMO LLC. Note: For S&P charts, trend is 2% real price appreciation per year. Source: GMO. Data through 10//10/08.* Detrended Real Price is the price index divided by CPI+2%, since the long-term trend increase in the price of the S&P 500 has been on the order of 2% real.

12 ExamplesGMO calls this “the greatest sucker’s rally in history”

69

The Biggest Danger is That Home Prices Overshoot on the Downside, Which Often Happens When Bubbles Burst

S&P 500 1927-1954

S&P 500 1955-1986

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

2.50

1927 1930 1933 1936 1939 1942 1945 1948 1951 1954

Det

rend

ed R

eal S

&P

500

Sto

ck P

rice

Inde

x

-59%

Overrun: 59%Fair Value to Bottom: 1.5 Years

Fair Value to Fair Value: 23 Years

0.00

0.25

0.50

0.75

1.00

1.25

1.50

1.75

2.00

2.25

1955 1957 1959 1961 1963 1965 1967 1969 1971 1973 1976 1978 1980 1982 1984 1986

Det

rend

ed R

eal S

&P

500

Sto

ck P

rice

Inde

x

-45%

Overrun: 45%Fair Value to Bottom: 7 Years

Fair Value to Fair Value: 12 Years

Source: GMO LLC, T2 Partners calculations.

70

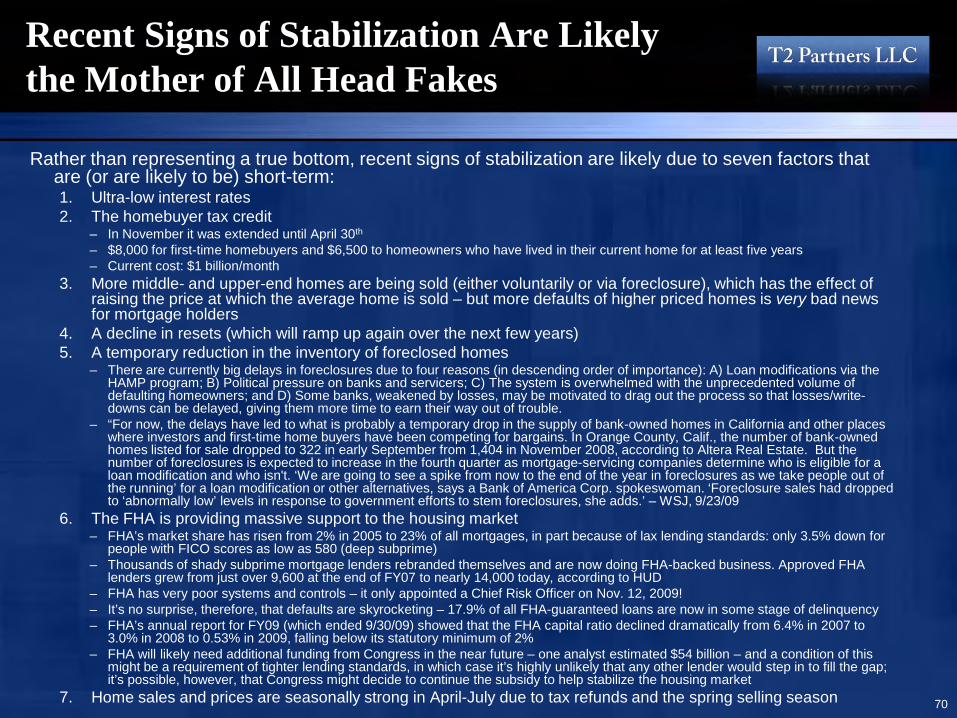

Recent Signs of Stabilization Are Likely the Mother of All Head Fakes

Rather than representing a true bottom, recent signs of stabilization are likely due to seven factors that are (or are likely to be) short-term:1. Ultra-low interest rates2. The homebuyer tax credit

– In November it was extended until April 30th

– $8,000 for first-time homebuyers and $6,500 to homeowners who have lived in their current home for at least five years– Current cost: $1 billion/month

3. More middle- and upper-end homes are being sold (either voluntarily or via foreclosure), which has the effect of raising the price at which the average home is sold – but more defaults of higher priced homes is very bad news for mortgage holders

4. A decline in resets (which will ramp up again over the next few years)5. A temporary reduction in the inventory of foreclosed homes

– There are currently big delays in foreclosures due to four reasons (in descending order of importance): A) Loan modifications via the HAMP program; B) Political pressure on banks and servicers; C) The system is overwhelmed with the unprecedented volume of defaulting homeowners; and D) Some banks, weakened by losses, may be motivated to drag out the process so that losses/write-downs can be delayed, giving them more time to earn their way out of trouble.

– “For now, the delays have led to what is probably a temporary drop in the supply of bank-owned homes in California and other places where investors and first-time home buyers have been competing for bargains. In Orange County, Calif., the number of bank-owned homes listed for sale dropped to 322 in early September from 1,404 in November 2008, according to Altera Real Estate. But the number of foreclosures is expected to increase in the fourth quarter as mortgage-servicing companies determine who is eligible for a loan modification and who isn't. ‘We are going to see a spike from now to the end of the year in foreclosures as we take people out of the running’ for a loan modification or other alternatives, says a Bank of America Corp. spokeswoman. ‘Foreclosure sales had dropped to ‘abnormally low’ levels in response to government efforts to stem foreclosures, she adds.’ – WSJ, 9/23/09

6. The FHA is providing massive support to the housing market– FHA’s market share has risen from 2% in 2005 to 23% of all mortgages, in part because of lax lending standards: only 3.5% down for

people with FICO scores as low as 580 (deep subprime)– Thousands of shady subprime mortgage lenders rebranded themselves and are now doing FHA-backed business. Approved FHA

lenders grew from just over 9,600 at the end of FY07 to nearly 14,000 today, according to HUD– FHA has very poor systems and controls – it only appointed a Chief Risk Officer on Nov. 12, 2009!– It’s no surprise, therefore, that defaults are skyrocketing – 17.9% of all FHA-guaranteed loans are now in some stage of delinquency– FHA’s annual report for FY09 (which ended 9/30/09) showed that the FHA capital ratio declined dramatically from 6.4% in 2007 to

3.0% in 2008 to 0.53% in 2009, falling below its statutory minimum of 2%– FHA will likely need additional funding from Congress in the near future – one analyst estimated $54 billion – and a condition of this

might be a requirement of tighter lending standards, in which case it’s highly unlikely that any other lender would step in to fill the gap; it’s possible, however, that Congress might decide to continue the subsidy to help stabilize the housing market

7. Home sales and prices are seasonally strong in April-July due to tax refunds and the spring selling season

71

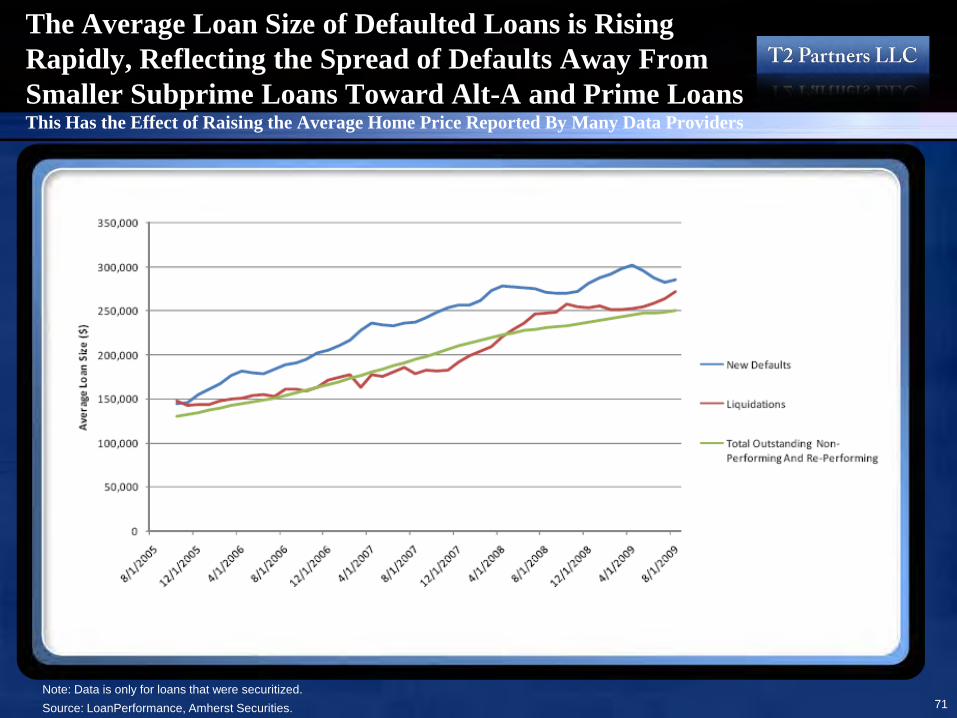

The Average Loan Size of Defaulted Loans is Rising Rapidly, Reflecting the Spread of Defaults Away From Smaller Subprime Loans Toward Alt-A and Prime LoansThis Has the Effect of Raising the Average Home Price Reported By Many Data Providers

Note: Data is only for loans that were securitized.Source: LoanPerformance, Amherst Securities.

72

Another Wave of Resetting Loans Is On the HorizonThe Last Wave Was Driven By Subprime Loans; This Time, It Will be Option ARMs

Source: Loan Performance, Amherst Securities.

0

5

10

15

20

Tota

l Loa

n Ba

lanc

e ($

Bil)

Option ARM Alt A Prime Subprime

We are here

73

Banks Are Selling Their REO, But Foreclosures Have Plunged By More Than Half, Ballooning the Inventory Pipeline

Source: Loan Performance, Amherst Securities.

0%

5%

10%

15%

20%

25%

Mon

thly

Rol

l Rat

es (%

)

Non Performing to Foreclosure Foreclosure to REO REO to Liquidation

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

REO 90 Days PLUS Foreclosure

Inventory Pipeline

Non-Performing to ForeclosureREO to Liquidation

Foreclosure to REO

90 Days & Foreclosure

REO

Monthly Roll Rates

74Source: HUD/FHA, through August 31, 2009, NY Times, 10/8/09; Commerce Department through Q3 09.

One Third of All New Single Family Home Sales Are Financed With FHA or VA Loans

FHA/VA Share of New SF Home Sales

0%

5%

10%

15%

20%

25%

30%

35%

40%

1988

Q1

1989

Q1

1990

Q1

1991

Q1

1992

Q1

1993

Q1

1994

Q1

1995

Q1

1996

Q1

1997

Q1

1998

Q1

1999

Q1

2000

Q1

2001

Q1

2002

Q1

2003

Q1

2004

Q1

2005

Q1

2006

Q1

2007

Q1

2008

Q1

2009

Q1

Number of FHA Loans Insured

75Source: HUD/FHA, through August 31, 2009, NY Times, 10/8/09.

FHA’s Loan Book Is a Rapidly Growing Disaster17.9% of Loans Are in Some Stage of Default; For 2007 Loans, It’s 32.4%

76

Existing Home Sales Are Highly Seasonal

Source: National Association of Realtors.

77

Existing Home Sales Are Highly Seasonal

Source: National Association of Realtors.

HPA Seasonality Coefficient -- Deviation From Mean

78

Home Prices Increased Every Month From May-October, then Fell in November

Source: S&P Case-Shiller 20-city index.

Sequential Home Prices March 2005-November 2009

-3.5%

-3.0%

-2.5%

-2.0%

-1.5%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

Mar-05

Jun-0

5

Sep-05

Dec-05

Mar-06

Jun-0

6

Sep-06

Dec-06

Mar-07

Jun-0

7

Sep-07

Dec-07

Mar-08

Jun-0

8

Sep-08

Dec-08

Mar-09

Jun-0

9

Sep-09

November 2009: -0.2%

79

…But They Always Bounce in the Spring and Summer!

Source: S&P Case-Shiller 20-city index.

Sequential Home Prices February 2000-November 2009

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

3.0%

Feb-00

Jul-0

0

Dec-00

May-01

Oct-01

Mar-02

Aug-02

Jan-0

3

Jun-0

3

Nov-03

Apr-04

Sep-04

Feb-05

Jul-0

5

Dec-05

May-06

Oct-06

Mar-07

Aug-07

Jan-0

8

Jun-0

8

Nov-08

Apr-09

Sep-09

Red circles represent April - June each year

80

Outlook for Housing Prices

• We think housing prices will reach fair value/trend line, down 40% from the peak based on the S&P/Case-Shiller national (not 20-city) index, which implies roughly a 10% further decline from where prices were as of the end of Q3 2009

• The key question is whether housing prices will go crashing through the trend line and fall well below fair value. This is possible, though unlikely because of continued massive government subsidies. In the long-term, housing prices will likely settle around fair value, but in the short-term prices will be driven both by psychology as well as supply and demand. The recent bounce in home prices has improved psychology, but the supply-demand trends are very unfavorable

– There is a huge mismatch between supply and demand, due largely to the tsunami of foreclosures. In addition, the “shadow” inventory of foreclosed homes already exceeds one year and there will be millions more foreclosures over the next few years, creating a large overhang of excess supply that will likely cause prices to overshoot on the downside, as they did in California

• Therefore, we expect housing prices to decline approximately 40% from the peak, bottoming in late 2010

• We are also quite certain that wherever prices bottom, there will be no quick rebound

– There’s too much inventory to work off quickly, especially in light of the millions of foreclosures over the next few years

– We don’t think the economy is likely to provide a tailwind, as we expect tepid economic growth at best for a number of years

81

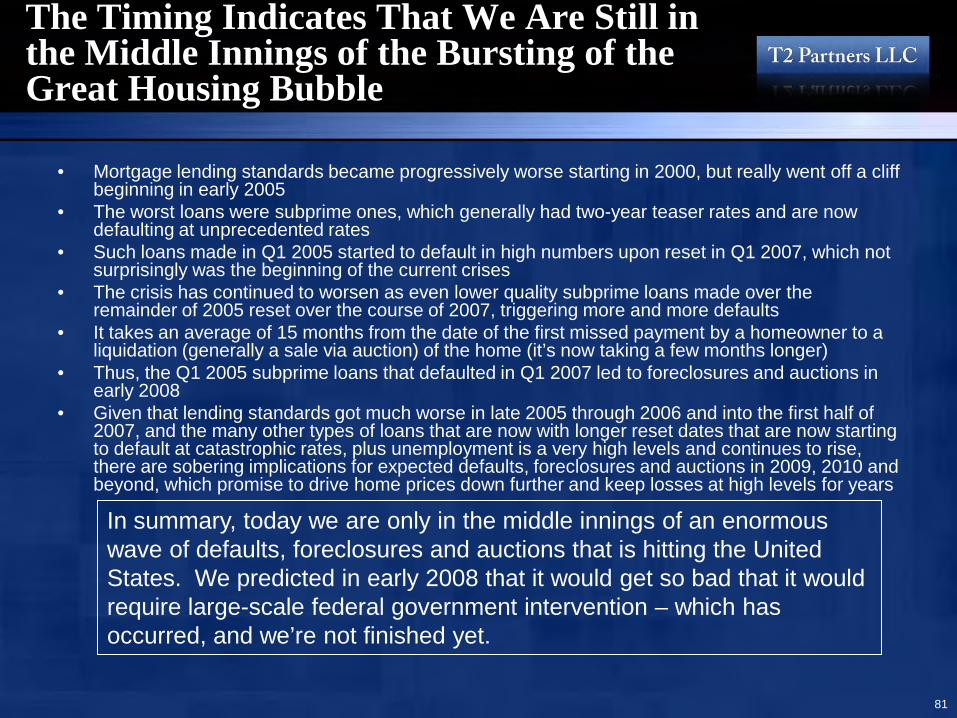

The Timing Indicates That We Are Still in the Middle Innings of the Bursting of the Great Housing Bubble

• Mortgage lending standards became progressively worse starting in 2000, but really went off a cliff beginning in early 2005

• The worst loans were subprime ones, which generally had two-year teaser rates and are now defaulting at unprecedented rates

• Such loans made in Q1 2005 started to default in high numbers upon reset in Q1 2007, which not surprisingly was the beginning of the current crises

• The crisis has continued to worsen as even lower quality subprime loans made over the remainder of 2005 reset over the course of 2007, triggering more and more defaults

• It takes an average of 15 months from the date of the first missed payment by a homeowner to a liquidation (generally a sale via auction) of the home (it’s now taking a few months longer)

• Thus, the Q1 2005 subprime loans that defaulted in Q1 2007 led to foreclosures and auctions in early 2008

• Given that lending standards got much worse in late 2005 through 2006 and into the first half of 2007, and the many other types of loans that are now with longer reset dates that are now starting to default at catastrophic rates, plus unemployment is a very high levels and continues to rise, there are sobering implications for expected defaults, foreclosures and auctions in 2009, 2010 and beyond, which promise to drive home prices down further and keep losses at high levels for years

In summary, today we are only in the middle innings of an enormous wave of defaults, foreclosures and auctions that is hitting the United States. We predicted in early 2008 that it would get so bad that it would require large-scale federal government intervention – which has occurred, and we’re not finished yet.

82

Future Losses Will Be Driven By Three Primary Factors

1. The economy• Especially unemployment

2. Interest rates• Ultra-low rates have helped mitigate some of the damage• But if the recent spike in rates continues, it could lead to an even greater surge

in defaults and losses3. Behavior of homeowners who are underwater

• Roughly one-fourth of homeowners with mortgages are currently underwater, some deeply so

• For many, it is economically rational for them to walk – leading to so-called “jingle mail” – but how many will actually do so?

• There is little historical precedent – we are in uncharted waters• As home prices continue to fall and more and more homeowners become

deeper and deeper underwater, they are obviously more likely to default, thereby creating a vicious cycle, but what exactly will the relationship be?

• Have millions of foreclosures led to a diminution of the stigma of defaulting and losing one’s home?

• Our best guess is that there will be rough symmetry: for homeowners 5% underwater, an additional 5% will default due to being underwater; 10% underwater will lead to 10% more defaults, and so forth…

Current Economic Situation

84

The Economy Rebounded at the End of 2009

Source: Bureau of Economic Analysis, 11/24/09; chart from Pershing Square presentation, 12/22/09.

5.7%

Q4’09

85

Financial Markets Are Stabilizing

Source: FRB, FDIC, Haver Analytics, Barclay’s Capital, 11/09; charts from Pershing Square presentation, 12/7/09.

86

The Stock Market Has Rallied DramaticallyThe S&P 500 Rose 68.2% from March 9, 2009 Through the End of the Year

Source: Bigcharts.com, 1/27/10.

On March 9, 2009, the S&P was down 55% from its peak only 17 months before, the largest decline since the Great Depression.

87

More Than 7 Million Jobs Have Been Lost SoFar in This Recession, Though the Monthly Rate of Losses Has Eased in Recent Months

Source: Bureau of Labor Statistics.

-1000

-800

-600

-400

-200

0

200

400

600

Jan-9

0

Jan-9

1

Jan-9

2

Jan-9

3

Jan-9

4

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Cha

nge

in N

onfa

rm P

ayro

ll Em

ploy

men

t (00

0s)

There have been job losses every month since

December 2007

125,000-150,000 jobs/month are required to absorb new entrants to the workforce and

prevent unemployment from rising

88

The Unemployment Rate Remains High, Registering 10% in December

Source: Bureau of Labor Statistics.

3%

4%

5%

6%

7%

8%

9%

10%

11%

Jan-7

0

Jan-7

3

Jan-7

6

Jan-7

9

Jan-8

2

Jan-8

5

Jan-8

8

Jan-9

1

Jan-9

4

Jan-9

7

Jan-0

0

Jan-0

3

Jan-0

6

Jan-0

9

Une

mpl

oym

ent R

ate

If part-time and discouraged workers are factored in, the unemployment rate would have been 17.3% in December. The labor force participation rate was 64.6%, the lowest in 22 years. The average work week was 33.2 hours. To return to the average of 33.8 hours would be the equivalent of nearly three million new jobs not created.

89

Chronic Unemployment Is Skyrocketing

Source: Labor Department, 1/8/10; WSJ, 10/3/09.

39.8%

90

The Average Weeks Unemployed is 29.1

Source: Labor Department, 1/8/10; WSJ, 10/3/09.

29.1

91

The Percentage of Unemployed Not on Temporary Layoff Has Risen to 53.4%

Source: Labor Department, 1/8/10; WSJ, 10/3/09.

53.4%

92

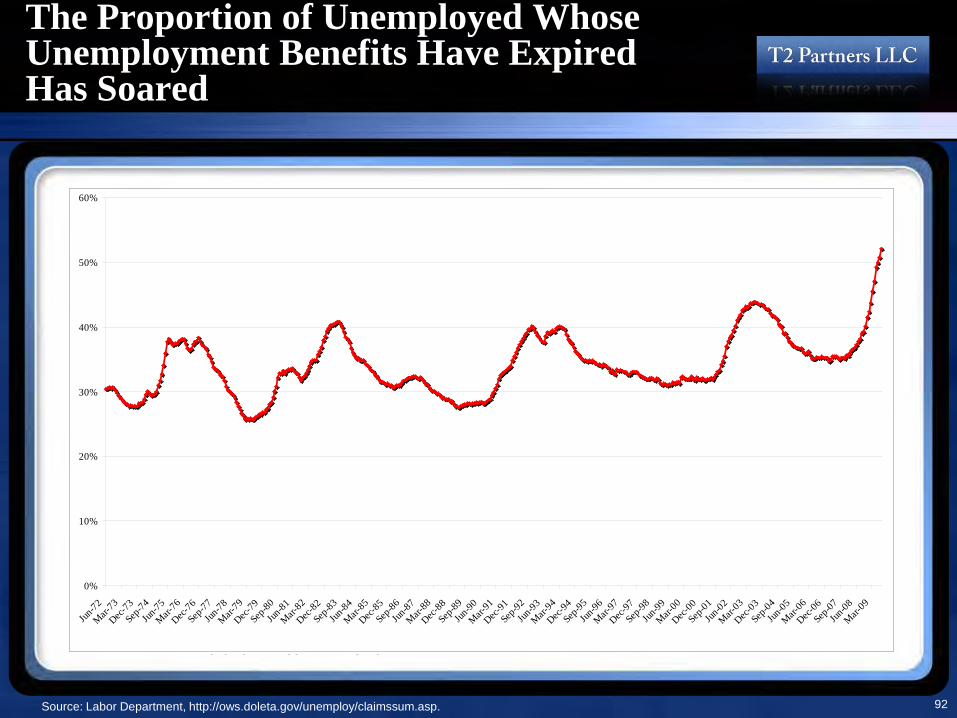

The Proportion of Unemployed Whose Unemployment Benefits Have Expired Has Soared

Source: Labor Department, http://ows.doleta.gov/unemploy/claimssum.asp.

0%

10%

20%

30%

40%

50%

60%

Jun-72

Mar-73

Dec-73Se

p-74Jun

-75

Mar-76

Dec-76Se

p-77Jun

-78

Mar-79

Dec-79Se

p-80Jun

-81

Mar-82

Dec-82Se

p-83Jun

-84

Mar-85

Dec-85Se

p-86Jun

-87

Mar-88

Dec-88Se

p-89Jun

-90

Mar-91

Dec-91Se

p-92Jun

-93

Mar-94

Dec-94Se

p-95Jun

-96

Mar-97

Dec-97Se

p-98Jun

-99

Mar-00

Dec-00Se

p-01Jun

-02

Mar-03

Dec-03Se

p-04Jun

-05

Mar-06

Dec-06Se

p-07Jun

-08

Mar-09

S D f L b h // d l / l / l i

93

There Are Now Six Unemployed People for Every Job Opening

Source: Bureau of Labor Statistics, NY Times, 9/27/09.

94

5.2% of All Jobs Have Disappeared, Worse Than Any Recession Since the Great Depression

Source: Bureau of Labor Statistics.

-5.5%

-4.5%

-3.5%

-2.5%

-1.5%

-0.5%

0 6 12 18 24 30 36 42 48Months after pre-recession peak

1948 1953 1958 1960 1969 1974 1980 1981 1990 2001 2007

2007-

95

Assuming Job Losses End Immediately (Unlikely) and Job Gains Average the Rate of the Most Recent Expansion, the Lost Jobs Won’t Be Restored Until 2016

Source: Labor Department, Wall St. Journal.

96

Consumer Confidence Has Rebounded Somewhat But Remains Low

Note: 1985=100. Source: The Conference Board (www.pollingreport.com/consumer.htm)

0

20

40

60

80

100

120

140

160

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Con

sum

er C

onfid

ence

Inde

x

Mortgage Equity Withdrawals of Roughly $400 Billion Annually During the Peak Bubble Years Fueled Unsustainable Consumer Spending

Source: www.calculatedriskblog.com/2009/05/mew-consumption-and-personal-saving.html.97

98

• As home prices have declined and other funding sources have dried up, millions of consumers have maxed out on home equity debt.

• In hot markets like California and Florida, a significant percentage of all consumers tapped into the value of their homes to help finance their new cars, according to CNW Marketing Research.

• Clearly this dynamic does not bode well for HELOC recovery rates or new car sales.

Many Borrowers Used Cash from Refinancings (Cash-Out Refis) and HELOCs to Buy New Cars

Source: New York Times 5/27/2008.

99

Total Consumer Credit Is Falling Sharply

Source: Federal Reserve Board, WSJ, 10/9/09.

Total Consumer Credit Outstanding(Change From Year Earlier)

Down $119 billion or 4.6% from its peak in 7/08. Down $12 billion in August, a 5.8% seasonally

adjusted annual rate, the seventh straight month of declines, the longest stretch since 1991.

Total Amount of Revolving and NonrevolvingConsumer Credit Outstanding

100

Household Credit Market Debt Outstanding Has Declined for the First Time Since This Was Measured Beginning in the Early 1950s

Source: St. Louis Fed.

101

The Percentage of Banks Tightening Standards for Consumer Loans Has Risen Sharply

Source: Federal Reserve Board Senior Loan Officer Opinion Survey on Bank Lending Practices, July 2009.

The U.S. Savings Rate Hit a 15-Year High of 6.9% in May, but Fell to 4.7% by NovemberThis is good news in the long run, but could be a severe economic headwind in the short run, given that consumer spending is 2/3 of GDP

Source: Paul Kedrosky’s blog, 6/26/09; http://paul.kedrosky.com/archives/2009/06/the_black_swan.html; www.bea.gov/newsreleases/national/pi/pinewsrelease.htm.102

Peaked

Household Liabilities as a Percentage of Disposable Income Remains Very High

Source: U.S. Federal Reserve, WSJ, 10/13/09.103

Peaked 1991: 90%

Peak: 138%

2000: 101%

Today: 129%

Private Domestic Investment Has Plunged

Source: WSJ, 10/13/09.104

Peaked

• “Of the 100 largest bond issues globally this year, only seven listed expansion, investment, capital expenditures or research and development as the purpose of the money-raising, according to Dealogic.”

• “In a recent survey conducted by the Conference Board, 51% of chief executives said they expect conditions in their industries to improve over the next six months, compared with 12% in the fourth quarter of 2008.”

105Sources: Federal Reserve, BEA, as of Q2 2007, GMO presentation.

Low Debt Era Rising Debt Era

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

51 54 57 60 63 66 69 72 75 78 81 84 87 90 93 96 99 02 05

Fina

ncia

l Pro

fits

as P

erce

nt o

f GD

P

100%

150%

200%

250%

300%

350%

Total Debt as Percent of G

DP

Dec-

Total Debt

Financial Profits

Over the Past 30 Years, We Have Become a Nation Gorged in Debt – To The Benefit of Financial Services Firms

Interest Rates

107

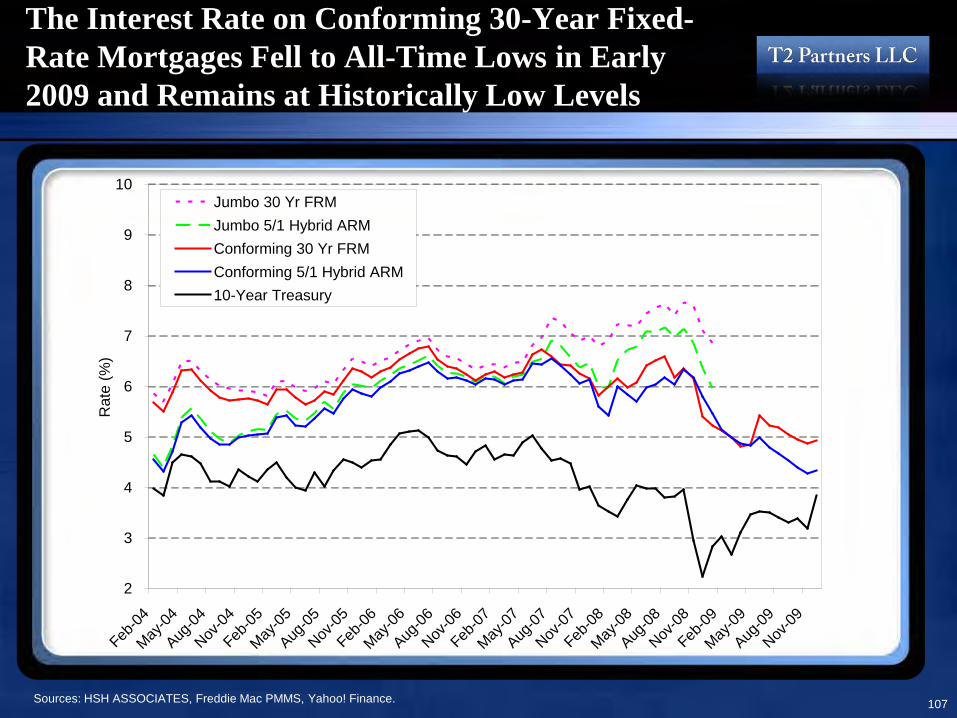

The Interest Rate on Conforming 30-Year Fixed-Rate Mortgages Fell to All-Time Lows in Early 2009 and Remains at Historically Low Levels

Sources: HSH ASSOCIATES, Freddie Mac PMMS, Yahoo! Finance.

2

3

4

5

6

7

8

9

10

Feb-04

May-04

Aug-04

Nov-04

Feb-05

May-05

Aug-05

Nov-05

Feb-06

May-06

Aug-06

Nov-06

Feb-07

May-07

Aug-07

Nov-07

Feb-08

May-08

Aug-08

Nov-08

Feb-09

May-09

Aug-09

Nov-09

Rat

e (%

)

Jumbo 30 Yr FRMJumbo 5/1 Hybrid ARMConforming 30 Yr FRMConforming 5/1 Hybrid ARM10-Year Treasury

108

Low Interest Rates Are Helping Stabilize the Housing Market

Sources: HSHAssociates.com; Ryan ALM via WSJ Market Data Group; Mortgage Bankers Association via Thomson Reuters; in the Wall St. Journal, 6/11/09 and 9/21/09.

(Conventional or nonconforming)

Roughly speaking, every 1% increase in mortgage rates reduces borrowing power by 10%

Underwater Homeowners

110

24% of Homeowners With a Mortgage Owe More Than the Home Is Worth, Making Them Much More Likely to Default

There Has Been a Dramatic Rise in Homeowners Who Are Underwater

In Bubble Markets, Far More Homeowners Are Underwater

Source: Zillow.com Q4 08 Real Estate Market Report; Moody's Economy.com, First American CoreLogic, T2 Partners estimates

Among people who bought homes in the past five years, 30%+ are underwater*

4%

6%

16%

20%

24%

0%

5%

10%

15%

20%

25%

Dec-06 Dec-07 Sep-08 Dec-08 Mar-09

Perc

ent U

nder

wat

er

Price Index Is % of Last 5 Yrsat Lowest Price Drop Purchasers Who

Metro Area Level Since Since Peak Are Under WaterNew York 2004-Q3 -15.2% 23.0%Los Angeles 2003-Q4 -32.0% 56.4%Boston 2002-Q2 -21.8% 27.8%Washington 2004-Q1 -24.8% 50.3%Miami 2004-Q1 -36.6% 65.1%San Francisco 2003-Q3 -27.8% 51.2%Atlanta 2004-Q4 -10.4% 23.2%San Diego 2002-Q4 -34.4% 63.9%Phoenix 2004-Q3 -37.7% 36.4%Las Vegas 2003-Q4 -41.8% 61.4%

* The actual figures are likely even worse, as this data doesn’t capture people who bought since 2003 and subsequently did a cash-out refi or after-the-fact second mortgage. 50% of all subprime and Alt-A loans in existence when the collapse happened were cash-out refis that carried a higher loan balance than the original purchase loan amount.

*

111

Certain Types of Loans Are Severely Underwater

Sources: Amherst Securities (January 2009), LoanPerformance, Standard & Poor’s.

73%

50%

45%

25%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Prime Alt A Subprime Option ARM

Per

cent

Und

erw

ater

Investment Outlook

113

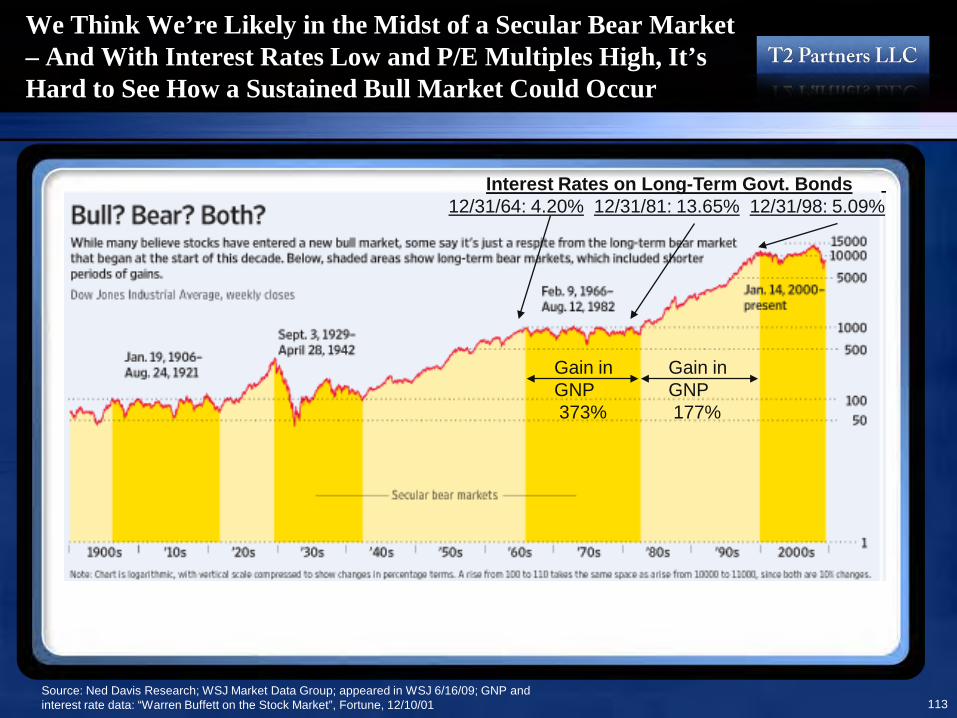

We Think We’re Likely in the Midst of a Secular Bear Market – And With Interest Rates Low and P/E Multiples High, It’s Hard to See How a Sustained Bull Market Could Occur

Source: Ned Davis Research; WSJ Market Data Group; appeared in WSJ 6/16/09; GNP and interest rate data: “Warren Buffett on the Stock Market”, Fortune, 12/10/01

Gain inGNP373%

Gain inGNP177%

Interest Rates on Long-Term Govt. Bonds12/31/64: 4.20% 12/31/81: 13.65% 12/31/98: 5.09%

114

Based on Inflation-Adjusted 10-Year Trailing Earnings, the S&P 500 at 20.8x Is Trading Above Its 130-Year Average of 16.3x

Source: Stock Market Data Used in "Irrational Exuberance" Princeton University Press, 2000, 2005, updated, Robert J. Shiller.

115

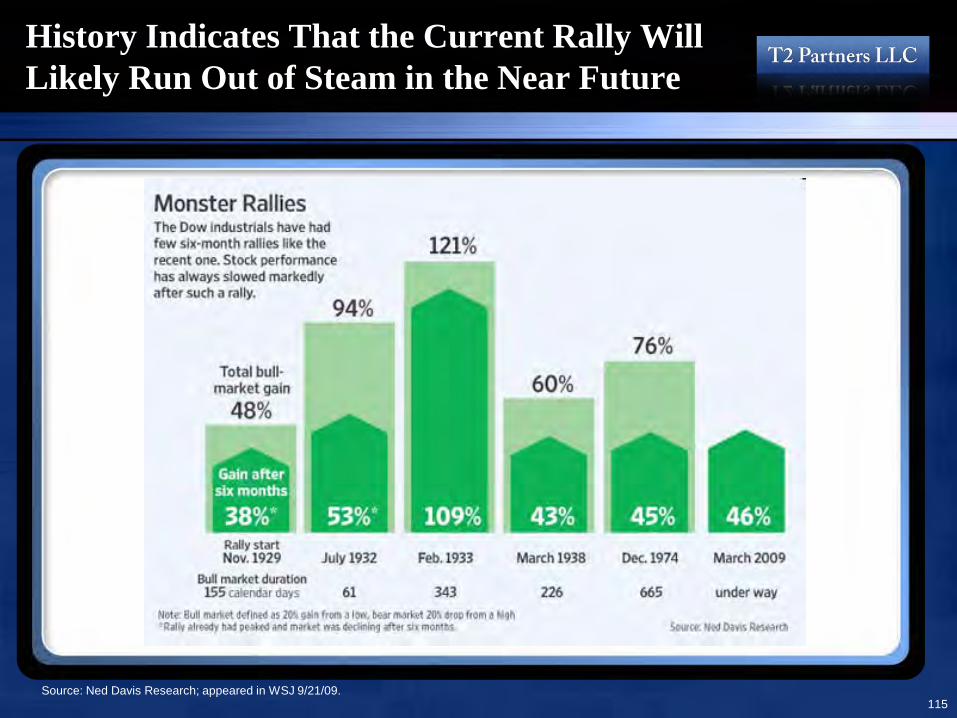

History Indicates That the Current Rally Will Likely Run Out of Steam in the Near Future

Source: Ned Davis Research; appeared in WSJ 9/21/09.

116

Where We Are Finding Opportunities10 Months Ago, We Were Playing Offense; Now We’re Playing Defense, As We Trim Our Longs, Add to Our Shorts and Shift Our Longs Toward Large, Dominant, Cash-Rich Companies

• Blue-chips. The stocks of some of the greatest businesses, with strong balance sheets and dominant competitive positions, are trading at their cheapest levels in years – due primarily to the overall market decline and weak economic conditions rather than any company-specific issues. In this category, we’d put Wal-Mart (which we own), Coca-Cola, McDonald’s, Altria, ExxonMobil, and Johnson & Johnson.

• Out of favor blue-chips. For somewhat more adventurous investors looking to buy great companies in the most out-of-favor sectors such as financials, retailers and healthcare, we own Berkshire Hathaway, Wells Fargo, American Express, Target and Pfizer. We also own Microsoft and Yahoo!. All are great businesses, but their stocks have suffered mightily thanks to the economic downturn. We think they’re good bets to rebound when things stabilize.

• Balance sheet plays. For investors who are comfortable with lower-quality businesses but want downside protection, there are many companies trading near or even below net cash on the balance sheet. Examples in our portfolio include digital media equipment company EchoStar Corp. and clothing retailer dELiA*s. Berkshire is the best of both worlds: a premier company but also a balance sheet play.

• Turnarounds. There are countless companies that have gotten clobbered by the economic downturn and are reporting dismal results – with stock prices to match. Investors in those that survive and return to anything close to former levels of profitability will be well rewarded – but picking these stocks isn’t easy. Among our holdings in this category are Wendy’s restaurants, Winn-Dixie supermarkets, Huntsman, a specialty chemical maker, Crosstex, a pipeline company, and Resource America, a specialty finance company.

• Special situations. This is somewhat of a catch-all category that, for us, includes Contango Oil & Gas, a stock that’s declined due to an aborted attempt to sell the company and the sharp drop in the price of natural gas.

• Mispriced options. Every once in a while we take a tiny position in a highly speculative situation – often where the stock price is below $1 – in which there’s a real chance that the outcome is zero, but also a decent chance, in our opinion, of making many multiples of our money. On an expected value basis, therefore, a small portfolio of such investments is attractive. Our holdings include a number of stocks and warrants of Special Purpose Acquisition Companies (SPACs), General Growth Properties, TravelCenters of America, Ambassadors International, Borders Group and PhotoChannel Networks.

Appendix(Many of these slides are out of date)

More Background Data on the Housing Market

Distressed Sales Have Fallen Due Mainly to Seasonal Factors

Sources: National Association of Realtors, NY Times, 6/9/09. 119

31% in June and July due to

seasonally strong organic sales.

This percentage is almost certain to rise in the off-

season

120

The Home Price-to-Rent Ratio Has Returned to Normal Levels

15

17

19

21

23

25

27

1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Med

ian

Hom

e Pr

ice

to M

edia

n G

ross

Ren

t

Source NATIONAL ASSOCIATION OF REALTORS® Existing Home Sales data series, U.S. Census Bureau, T2 Partners estimates.

The Housing Bubble Helped Many People Achieve the Dream of Home Ownership –Which is Now Turning Into a Nightmare

Source: Census Bureau.

60

61

62

63

64

65

66

67

68

69

70

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

Percentage of Households Owning Homes

%

121

The Percentage of Homes Listed for Sales Remains Near an All-Time High(Note that many more homes are vacant but not listed for sale)

Source: Census Bureau.122

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

Q1 195

6

Q4 195

9

Q3 196

3

Q2 196

7

Q1 197

1

Q4 197

4

Q3 197

8

Q2 198

2

Q1 198

6

Q4 198

9

Q3 199

3

Q2 199

7

Q1 200

1

Q4 200

4

Q3 200

8

Hom

e V

acan

cy R

ate

Home Vacancy Rate 1965-Q2 09

Housing Starts, Completions and Sales Are At or Near All-Time Lows

Source: Commerce Department, data through 9/09.123

A slight rebound in starts and sales in recent months

200

400

600

800

1000

1200

1400

1600

1800

2000

1970 1973 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009

Sea

sona

lly A

djus

ted

Ann

ual R

ate

(000

s)

StartsCompletionsNew Homes Sold

There Is an Enormous Inventory Glut of New HomesThe Average New Home Has Been on the Market for 12.9 Months

Source: Census Bureau, through 8/09.124

2

4

6

8

10

12

14

Jan-9

0

Jan-9

1

Jan-9

2

Jan-9

3

Jan-9

4

Jan-9

5

Jan-9

6

Jan-9

7

Jan-9

8

Jan-9

9

Jan-0

0

Jan-0

1

Jan-0

2

Jan-0

3

Jan-0

4

Jan-0

5

Jan-0

6

Jan-0

7

Jan-0

8

Jan-0

9

Med

ian

Age

(mon

ths)

Vacant Housing Stock Creates an Enormous Inventory Overhang

Source: Census BureauSource: Census Bureau, Moody’s Economy.com.

125

1.1-1.5 million excess units, equal to 2-3 years of existing home sales

Nearly 6% of Homes Built This Decade Are Vacant

Source: Census BureauSource: Census Bureau, through Q4 2008

126

5.9%

2.0%

April 2000 to presentMarch 2000 or earlier

Vacancy Rate By Date of Construction

Unlike Past Housing Downturns, New Home Sales Have Fallen Far More Than Existing Home Sales

Source: National Assoc. of Realtors (existing sales) and Census Bureau (new sales), both via Haver Analytics; chart from the New York Times, 6/27/09; manually updated through 8/09. 127

A slight rebound from March-August

New homes sales fell 76% from the peak; still down 69% through August

So Far, Few Loan Modifications Are Working

Source: Office of the Comptroller of the Currency and the Office of Thrift Supervision Mortgage Metrics

28.2%

52.1%

23.2%

36.7%

45.7%44.0%

49.8%

31.8%

46.1%

29.1%

0%

10%

20%

30%

40%

50%

60%

3 6 9 12Months Since Modification

Perc

ent o

f Mod

ified

Loa

ns 6

0+ D

ays

Del

inqu

ent

Q1 2008Q2 2008Q3 2008Q408

128

Banks Are Starting to Do Loan Modifications With Principal Reductions, Increasing the Chance of Success

Source: WSJ, 10/1/09.129

Most Loan Modifications Fail Because the Homeowner Is So Deep Underwater

Among foreclosures in California in May, the average amount owed was $412,000, yet the home was worth only $235,000. This means the homeowner was 43% underwater and the home price would have to rise 75% to equal the amount of the debt.

Source: The Field Check Group -- data provided by ForeclosureRadar.com.130

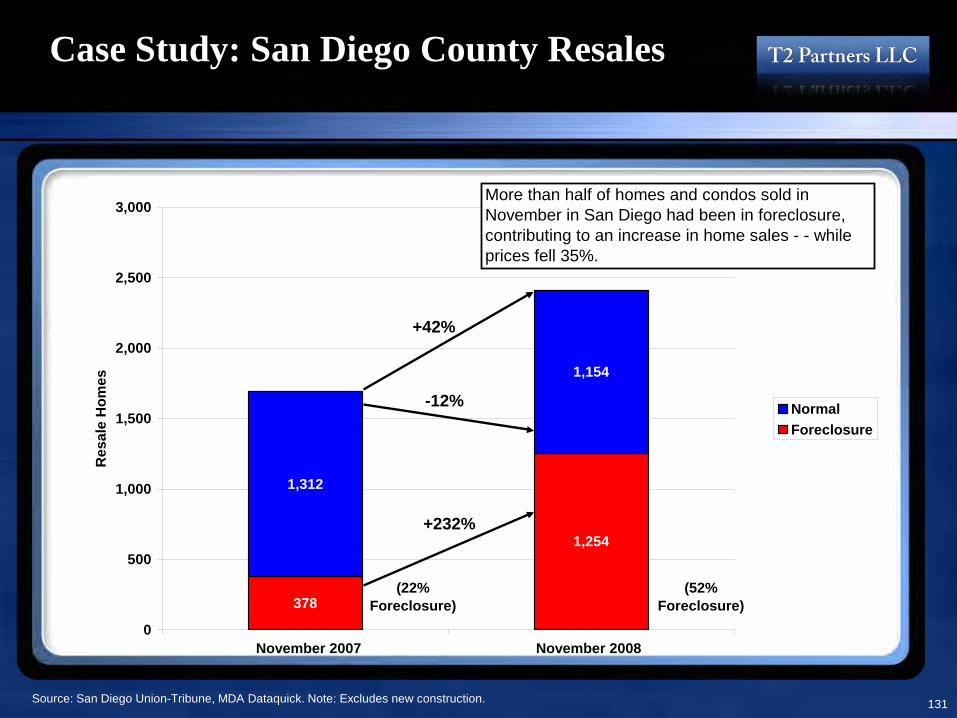

Case Study: San Diego County Resales

Source: San Diego Union-Tribune, MDA Dataquick. Note: Excludes new construction.

378

1,254

1,312

1,154

0

500

1,000

1,500

2,000

2,500

3,000

1/1/2007 1/1/2008

Res

ale

Hom

es

NormalForeclosure

+42%

-12%

+232%

More than half of homes and condos sold in November in San Diego had been in foreclosure, contributing to an increase in home sales - - while prices fell 35%.

November 2007 November 2008

(52% Foreclosure)

(22% Foreclosure)

131

Data on the Major Public Homebuilders

Debt-to-Equity Ratio ofMajor Homebuilders

Source: Census BureauSource: Company filings.

133

0.00 0.00

0.170.26

0.48 0.53 0.55 0.59 0.64

0.99

1.40

1.97

-0.5

0.0

0.5

1.0

1.5

2.0

NVR MDC TOL RYL MTH DHI LEN MHO PHM BHS KBH SPF BZH HOV

6.76

-11.98

Inventory-to-Equity Ratio ofMajor Homebuilders

Source: Census BureauSource: Company filings.

134

0.300.50

1.331.50 1.56 1.55

1.80

1.461.71

2.10

3.123.37

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

NVR MDC TOL RYL MTH DHI LEN MHO PHM BHS KBH SPF BZH HOV

8.74

-12.89

Price-to-Book Ratio ofMajor Homebuilders

Source: Census BureauSource: Company filings.

135

2.69

1.76

1.21

1.621.41

1.55

1.08

0.70

1.27

0.39

1.97

2.43

1.37

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

NVR MDC TOL RYL MTH DHI LEN MHO PHM BHS KBH SPF BZH HOV-3.09

Case Study: California, With a Focus on Sacramento

(California accounts for 10% of U.S. homes, but 33% of foreclosures – 43% by value)

137

Does the Recent Rise in Prices and Decline in the Percentage of Homes Sold Out of Foreclosure Mean California Has Bottomed?

Source: MDA Dataquick. Note: Includes new construction.

California

$0

$100

$200

$300

$400

$500

Jan-0

6

Apr-06

Jul-0

6

Oct-06

Jan-0

7

Apr-07

Jul-0

7

Oct-07

Jan-0

8

Apr-08

Jul-0

8

Oct-08

Jan-0

9

Apr-09

Jul-0

9

Med

ian

Hom

e P

rice

(000

s)

0%

10%

20%

30%

40%

50%

60%

70%

Foreclosure Resale %

138

Home Prices Crashed Through Trend Line in California, But Have Rebounded

Source: California Association of REALTORS ® . All rights reserved. www.rebsonline.com, T2 Partners estimates.

$0

$100

$200

$300

$400

$500

$600

Jan-7

9

Jan-8

1

Jan-8

3

Jan-8

5

Jan-8

7

Jan-8

9

Jan-9

1

Jan-9

3

Jan-9

5

Jan-9

7

Jan-9

9

Jan-0

1

Jan-0

3

Jan-0

5

Jan-0

7

Jan-0

9

Med

ian

Pric

e ($

000s

)

Median Sales Price4% Trend

139

Are We Seeing the Beginnings of a Bottom in Hard-Hit Markets Like Sacramento?

Source: NY Times, 5/4/09.

140

Home Prices in Sacramento More Than Tripled in Six Years – And Have Now Fallen 47%

Source: Zillow.com.

141