Embed Size (px)

Citation preview

An Introduction to RIIAThought-Leadership and Best Practices

© 2014. Retirement Income Industry Association. All rights reserved.Retirement Income Industry Association®, RIIA®, is the owner of the RIIA® logo, a registered collectivemembership mark and trademark/service mark; the owner of RIIA's Retirement Management Analyst(sm),RMA(sm), and logo, a certification mark and the owner of the RMA curriculum; and the owner of RIIAMarket Insight(sm), RMI(sm), and logo, a service mark. Retirement Income Industry Association®, RIIA®, isalso the owner of the “View Across the Silos(sm),” “Household Balance Sheet View(sm)” “HouseholdBalance Sheet Benchmark(sm),” “Retirement Policy Statement(sm)” and Retirement Management Journal(sm),RMJSM, and logo, a service mark of RIIA® (Collectively, "Marks, Logos and Property"). Only RIIA®, itsauthorized members and/or certified persons, in compliance with usage guidelines, may use the Marks,Logos and Property. The Marks, Logos and Property may not be copied, imitated, or used, in whole orin part, without the prior written permission of RIIA®.

History of RIIA’s Founders

• Rational Investors: 1996-2001

• Mass-Customized Investment Advice over the Internet

• Sold to S&P in 1999

• Retirement Engineering: 2001-2006

• Intent to create a new industry

• Pricing income in terms of $/lb.

• RIIA: 2006-Present

• The View Across the Silos: Thought-Leadership

• The RMA designation: Best Practices

Founding Members (2006)

Alliance BernsteinAmerican CenturyAVIVA NARDeloitte ConsultingGenworth FinancialGreenwich AssociatesIbbotson/MorningstarFundQuestFranklin TempletonING U.S. Financial ServicesLipper, a Reuters CompanyMassMutualMcElroy, Deutsh, Mulvaney & CarpenterMercer HR ServicesMerrill Lynch/Bank of AmericaMetLifeMFS Investment Management

Nationwide FinancialOppenheimer FundsPLANSPONSORRBC Insurance/Royal Bank of CanadaRetirement Engineering, Inc.The 401(k)Company/SchwabThe Phoenix CompaniesRussell Investment GroupSymetra FinancialUBS Global Asset ManagementWealth2KWells Fargo

• Institutional Members

• 86 since 2006, 44 active now, including:

• TIAA-CREF, New York Life, MassMutual, Prudential,

Challenger, JPMorgan, Morgan Stanley, Bank of

America/Merrill Lynch, BNY/Mellon, BlackRock,

• Individual Members

• about 1,000 since 2006

• 5,000 members on LinkedIn Group

• RMA Certificate Holders

• about 100 since 2010

• In 2014 the RMA designation will be taught at 5

Universities: BU, TTU, SSU, NSU and FIU

RIIA Today

Thought-Leadership

• Board Members

• Special Advisors to the Board

• Conference Keynote Speakers

• Retirement Management Journal Authors

• Virtual Learning Center Webinars Speakers

• Retirement Management Analyst Curriculum Book Authors

• RIIA Market Insight Research Consortium Members

Thought-Leadership: Board Members

Regular Board Members

•Chip Castille, BlackRock

•Adam Bryan, DTCC

•Karen Wimbish, Wells Fargo

•Bill Hunter, Bank of America/Merrill Lynch

•Ron Mastrogiovanni, HVS

•Ed O’ Connor, Morgan Stanley

•Tim Murphy, Investors Capital

•Anand Rao, PwC

•Rob Capone, BNY/Mellon

•Jan Gundersen, TIAA-CREF

Former Board Members:

•Peng Chen, Morningstar/DFA

•Tom Johnson, MassMutual/NewYork Life

•Sri Reddy, Prudential Financial

At Large Members:

Joan Boros, Esq.

Elvin Turner, Esq.

Stephen Saxon, Esq.

Mathew P. Fink, retired ICI

Thought-Leadership: Special Advisors

Academic Advisors including:•Shlomo Benartzi, UCLA•Zvi Bodie, Boston University•Jeff Brown, University of Illinois•Michael Finke, Texas Tech University•Larry Kotlikoff, Boston University•David Laibson, Harvard University•Annamaria Lusardi, Dartmouth College•Moshe Arye Milevsky, Ph.D.,York University•Olivia Mitchell, Wharton School, University of Pennsylvania•Wade Pfau, American College•Meir Statman, Santa Clara University•Jack VanDerhei, Temple University and EBRI Fellow•Stephen Zeldes, Columbia University

Thought-Leadership: Special Advisors

Executive Advisors, including:

•Hans Carstensen, retired Chairman, AVIVA

•Farrell Dolan, retired, Fidelity

•Keith B Jarrett, Chairman, Rockport Funding, LLC

•Jerry Kenney, Merrill Lynch/Blackrock

•Louis Lataif, Boston University School of Management

•Sandra Timmermann, Gerontologist and founder of the MetLife Mature

Market Institute

Thought-Leadership: Special Advisors

Practicing Advisors, including:

•Mitch Anthony, Advisor Insights, Inc.

•John Mulligan, CFP®,CIMA, AIFA, RMA

•Anna Rappaport, FSA, MAAA, Anna Rappaport Consulting

•Chuck Robinson, Northwestern Mutual Wealth Management

•Sheldon H. Smith, Esq, Partner, Holme Roberts & Owen LLP

•Don Trone, Strategic Ethos

•Jarrod Upton

Thought-Leadership: Officers

• Francois Gadenne, Co-founder, Chairman of the Board

• Al Turco, Co-founder, Counsel to the Board

• Udo Frank (retired Allianz Global Investors), Treasurer

• Joan Boros, Secretary

• David Ehrenthal, Business Unit Director, Membership Services

• Deborah Burkholder, Business Unit Director, Events

• Robert Powell, Business Unit Director, Publications

• Elvin Turner, Business Unit Director, Research

• Francois Gadenne, Business Unit Director, Education

• Marcia Mantell, Business Unit Director, Consumer

Thought-Leadership: Keynote Speakers

• 2006: Meir Statman

• 2007: Ray Kurzweil

• 2008: Ray Burham, David Warsh

• 2009: Bruce Sterling, Howard Bloom

• 2010: Sam Khoury, Buddy Donohue, Marsh Carter

• 2011: Doug Short, Charlie Baker, VDH, Clint Watts

• 2012: Frank Casey, Tim Garrett, Herb Meyer

• 2013: Michael Kitces, Michael Lane

• 2014: David Blanchett, Sandy Timmermann, Bill Baldwin

Thought-Leadership: RMJ Authors

Since Spring 2011 issue, 64 RMJ papers from authors including:•Shlomo Benartzi•Steve Sexauer•Laurence B. Siegel•Michael Finke•Wade Pfau•Matt Grove•Harry Markowitz•Anna Rappaport•David Blanchett•Michael Zwecher•Peng Chen•Michael Kitces•Helen Simon

Thought-Leadership: VLC Speakers

• Two webinars per months, with speakers such as:• Michael Finke, Ph.D., CFP® - Ph.D. Coordinator and Associate Professor

of Personal Financial Planning at Texas Tech University• Sarah Holden, Senior Director of Retirement & Investor Research at the

Investment Company Institute (ICI).• Andrew Blumberg , Group Director, DTCC Analytic Reporting for

Annuities• Dennis Gallant, President of GDC Research• Zachary S. Parker, CFP, MBA, 1st Vice President – Income Distribution &

Product Strategy, Securities America• Stan “The Annuity Man” Haithcock - nationally recognized annuity expert

and annuity critic• Michael Kitces - Partner and Director of Research for Pinnacle Advisory

Group• Dana Anspach, Principal, Sensible Money, LLC

Thought-Leadership: RMA Governance Board

• Al Turco, Esq., McElroy, Deutsch, Mulvaney & Carpenter,LLP

• Joan Boros, Esq., Stradley Ronon Stevens & Young, LLP

• Harold Evensky, Evensky & Katz

• Patrick Fitzgerald

• Francois Gadenne

• Craig Adamson, LPL Financial, LLC

• Michael Finke, Ph.D. Texas Tech University

• Lawrence Ford

• Ruth Ann Murray, Boston University, Metropolitan College

• Zachary Parker, Securities America, Inc.

Thought-Leadership: RMA Authors

• Beth Allan

• Dana Anspach

• Brian Barnier

• David Blanchett

• Jason Branning

• Brent Burns

• April Caudill

• Larry Cohen

• Harold Evensky

• Michael Finke

• Jeremy Fletcher

• Ray Grubbs

• Stephen Huxley

• Cliff Jurdi

• Paul Kaplan

• Mitzi Lauderdale

• Chris Leone

• Michael Lonier

• David Macchia

• Brett Machtig

• Aaron Minney

• Steve Mitchell

• John Mulligan

• Wade Pfau

• Paul Samuelson

• Jack Sharry

• Doug Short

• Al Turco

• Elvin Turner

• Alain Valles

• George Wilbanks

• Michael Zwecher

• Francois Gadenne

Thought-Leadership: Research Committee

• Kathleen Beichert, SVP, OppenheimerFunds

• David Blanchett, Morningstar Investment Management

• Andrew Blumberg, DTCC, Analytic Reporting for Annuities

• Ron Bush, Brightwork Partners, LLC

• Larry Cohen, Strategic Business Insights

• Matt Greenwald, Mathew Greenwald & Associates

• Lilah Koski, Koski Research

• Louis Lombardi, PwC

• Kim McSheridan

• Lisa Plotnick

• Anna Rappaport

• Linda Schwartz, TIAA-CREF

• Jack Tatar, GEM Research Solutions

The Evolution of RIIA’s Conferences

A Time to Present Best PracticesRFC14: The Art and Science of the Retirement Policy StatementRSC14: Retirement Opportunities are the beginning of great enterprisesRFC 13: Practical Solutions in an Uncertain WorldRSC13: The Household Balance Sheet View

A Time to Ask The Right QuestionsRFC12: What does it take to be a top retirement income advisor?RSC12: What can Defined Contribution and Retail Distribution learn from one another after five years of independent product and process development?RFC11: Are We Rome or Byzantium?RSC11: The Future of Retirement Income Solutions and Delivery:

The Retirement Puzzle in an Age of Uncertainty

A Time to Define the ProblemsAMAD10: Making Powerful Connections to Advance Retirement Income SecurityRSC10: New Products, New Communications, New Technologies, New ProcessesAMAD09: Traditional Retirement Planning Failed: How Will A New Approach Work?IIR09: The New Normal as Seen from the View Across The Silos

A Time to Present Best PracticesRFC14: The Art and Science of the Retirement Policy StatementRSC14: Retirement Opportunities are the beginning of great enterprisesRFC 13: Practical Solutions in an Uncertain WorldRSC13: The Household Balance Sheet View

A Time to Ask The Right QuestionsRFC12: What does it take to be a top retirement income advisor?RSC12: What can Defined Contribution and Retail Distribution learn from one another after five years of independent product and process development?RFC11: Are We Rome or Byzantium?RSC11: The Future of Retirement Income Solutions and Delivery:

The Retirement Puzzle in an Age of Uncertainty

A Time to Define the ProblemsAMAD10: Making Powerful Connections to Advance Retirement Income SecurityRSC10: New Products, New Communications, New Technologies, New ProcessesAMAD09: Traditional Retirement Planning Failed: How Will A New Approach Work?IIR09: The New Normal as Seen from the View Across The Silos

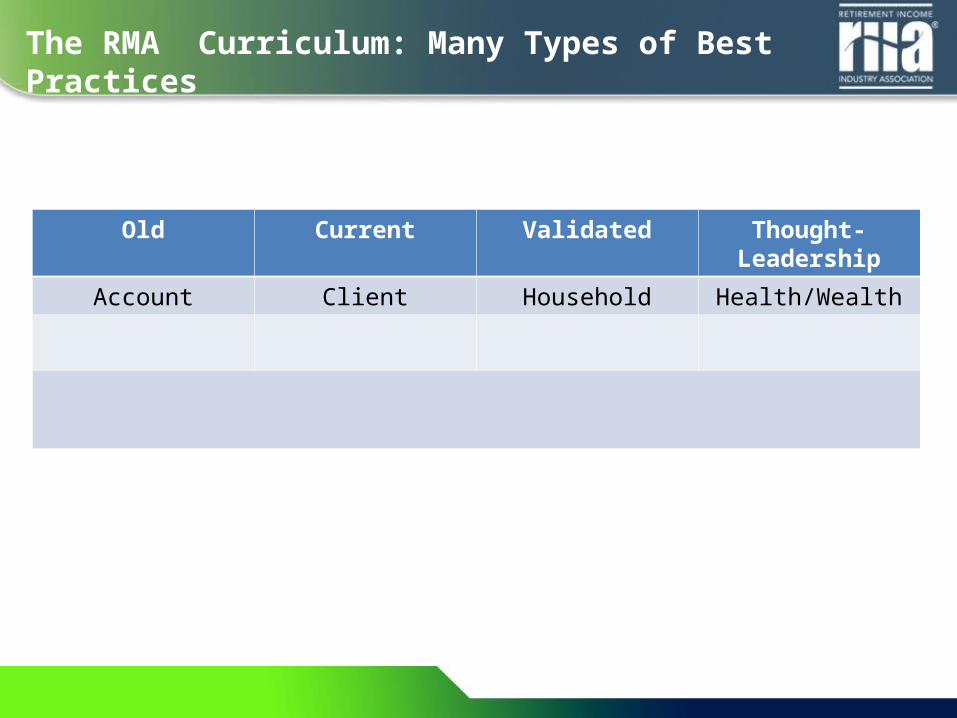

The RMA Curriculum: Many Types of Best Practices

Old Current Validated Thought-Leadership

The RMA Curriculum: Many Types of Best Practices

Old Current Validated Thought-Leadership

Account Client Household Health/Wealth

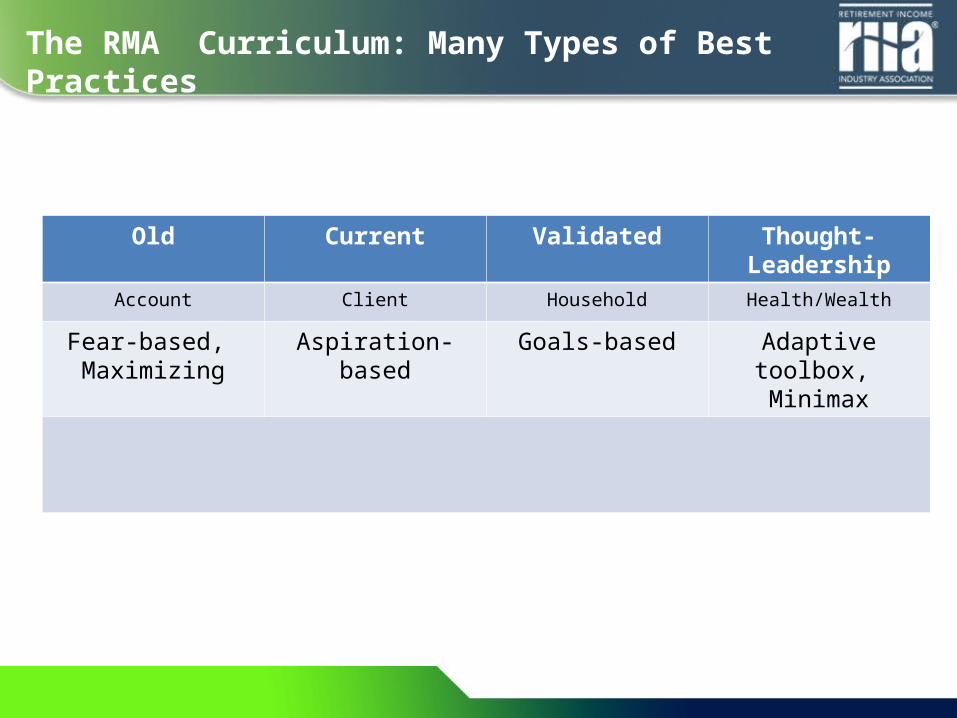

The RMA Curriculum: Many Types of Best Practices

Old Current Validated Thought-LeadershipAccount Client Household Health/Wealth

Fear-based, Maximizing

Aspiration-based Goals-based Adaptive toolbox, Minimax

The RMA Curriculum: Many Types of Best Practices

Old Current Validated Thought-LeadershipAccount Client Household Health/Wealth

Fear-based, Maximizing

Aspiration-based Goals-based Adaptive toolbox, Minimax

Vocabulary Test for Data Input in Software Programs

Personal Mastery of Professional Planning Skills

The RMA Curriculum: Many Types of Best Practices

Old Current Validated Thought-Leadership

Probability First(Expert Models of “Known Risks”)

Safety First(Holistic Checklists for “Uncertainty”)

Vocabulary Test for Data Input in Software Programs

Personal Mastery of Professional Planning Skills

The RMA Curriculum: Many Types of Best Practices

Old Current Validated Thought-Leadership

Probability First(Expert Models of “Known Risks”)

Safety First(Holistic Checklists for “Uncertainty”)

AUMs / Readiness(Financial Literacy)

AUMs / Fundedness(Risk Literacy)

Vocabulary Test for Data Input in Software Programs

Personal Mastery of Professional Planning Skills

The RMA Curriculum: Many Types of Best Practices

Old Current Validated Thought-Leadership

Probability First(Expert Models of “Known Risks”)

Safety First(Holistic Checklists for “Uncertainty”)

AUMs / Readiness(Financial Literacy)

AUMs / Fundedness(Risk Literacy)

Risk Profile / Salary Replacement Household Balance Sheet(Assets, Liabilities, Risk Exposures)

Vocabulary Test for Data Input in Software Programs

Personal Mastery of Professional Planning Skills

The RMA Curriculum: Many Types of Best Practices

Old Current Validated Thought-Leadership

Probability First(Expert Models of “Known Risks”)

Safety First(Holistic Checklists for “Uncertainty”)

AUMs / Readiness(Financial Literacy)

AUMs / Fundedness(Risk Literacy)

Risk Profile / Salary Replacement Household Balance Sheet(Assets, Liabilities, Risk Exposures)

Investment Allocations(Risky Assets Diversification = Upside)

Retirement Allocations(Upside, Floor, Longevity, Reserves)

Vocabulary Test for Data Input in Software Programs

Personal Mastery of Professional Planning Skills

The RMA Curriculum: Many Types of Best Practices

Old Current Validated Thought-LeadershipAccount Client Household Health/Wealth

Fear-based, Maximizing

Aspiration-based Goals-based Adaptive toolbox, Minimax

Probability First(Expert Models of “Known Risks”)

Safety First(Holistic Checklists for “Uncertainty”)

AUMs / Readiness(Financial Literacy)

AUMs / Fundedness(Risk Literacy)

Risk Profile / Salary Replacement Household Balance Sheet(Assets, Liabilities, Risk Exposures)

Investment Allocations(Risky Assets Diversification = Upside)

Retirement Allocations(Upside, Floor, Longevity, Reserves)

Investment Policy Statement Retirement Policy Statement

Vocabulary Test for Data Input in Software Programs

Personal Mastery of Professional Planning Skills

Best Practices to Retirement Policy Statement

1- Buying “Lifestyle Time” for clients

- “Fundedness” , Investment-based, Goals-based, Product-based

2- Finding the relevant Assets, Liabilities and Risks with the

“Household Balance Sheet View(sm)”

3- Transitioning from Asset Allocations to “Retirement Allocations”

- Mitigating risk exposures: “First Build a Floor…”. - Optimizing Performance: “… Then Expose to Upside(sm)”.

The “Retirement Policy Statement“ as a protective process

Should You become an RMA?

Appendices

PwC

The RMA Curriculum: Full Range of Stakeholders

The RMA’s Arc of Development started with DC, moved to Relationship Advisors and returned to both DC and Retail Transactional Advisors

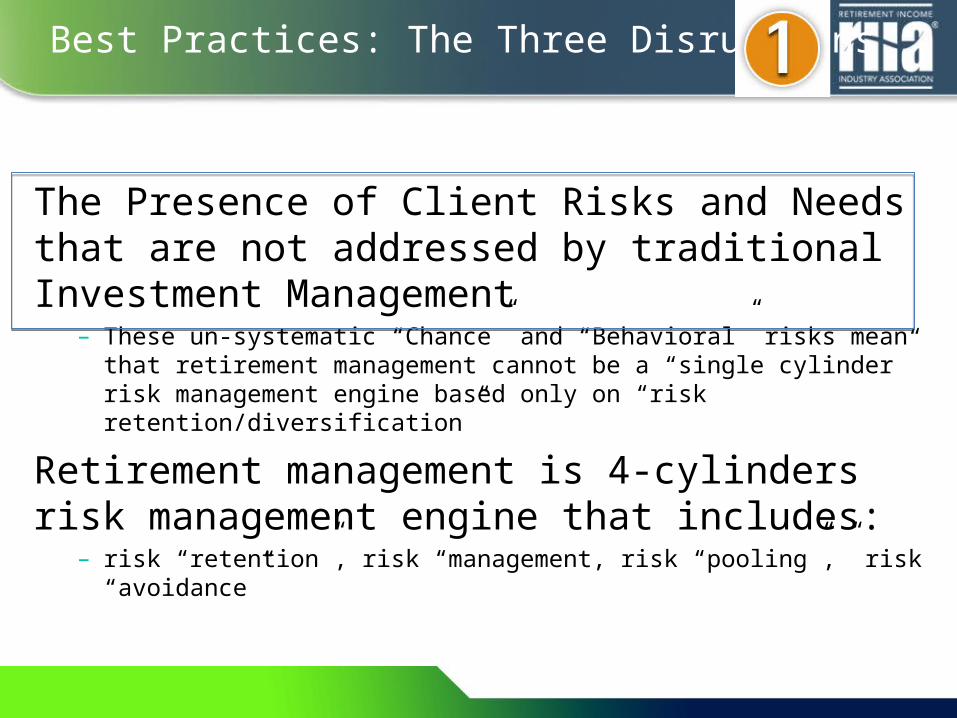

Best Practices: The Three Disruptions

The Presence of Client Risks and Needs that are not addressed by traditional Investment Management

– These un-systematic “Chance” and “Behavioral” risks mean that retirement management cannot be a “single cylinder” risk management engine based only on “risk retention/diversification”

Retirement management is 4-cylinders risk management engine that includes:

– risk “retention”, risk “management, risk “pooling”,” risk “avoidance”

The Client’s View: A Staged Retreat?

Best Practices: The Three Disruptions

Solutions that exist Outside of the traditional Business Models.•The traditional business model is “gathering assets.” •The business model of retirement is “paying a monthly check”

Incremental thinking and misunderstood adoptions will not “move the needle”.

DCDB Retail

Income Statement Planning

Household Balance Sheet Planning

Retirement Planning Best Practices by Primary Client Channel

RIIA 2005: The Vision of the View Across the Silos

Best Practices: The Three Disruptions

Academic Justifications and Practice Validations expand beyond the traditional focus on Wealth•Traditional financial management is a special case of the larger financial framework that has been developed and formalized since the 1950s.

Retirement Management re-introduces minimum consumption in the financial equation •The goal of investment management is to expose the client’s wealth to upside potential subject to a risk profile.•The goal of retirement management is “First Build a (minimum consumption) Floor, Then Expose (to wealth growing) Upside”.

Best Practices: Ten Key Competencies

1- Working with both wealth and consumption needs

2- Focusing on the right client tiers: Fundedness

3- Selecting the proper client-matched, fundamental planning strategy

- Investment-based, (start with the portfolio)

- Goal-based, (start with the budget)

- Product-based, (start with the account)

4 - Developing the full household balance sheet

5- Planning with human, social and financial capital

6- Mapping risk exposures

7- Recommending risk management techniques allocations: Retirement Allocations

8- Selecting implementation process approaches

9- Recommending account locations and product selections

10- Reviewing the plan on a recurring schedule

PwC | RIIA | SBI

Fundedness Tools Overfunded Constrained Underfunded

Wealthy Households and Participants

Fundedness measures based on Financial Assets:C/FC, FC/C

Fundedness measures based on Financial Assets:C/FC, FC/CC’/FC, FC/C’

Fundedness measures based on Financial Assets:C/FC, FC/CC’/FC, FC/C’

Affluent Households and Participants

C’/FC, FC/C’ as well asFundedness measures based on HHBS:A/L

C’/FC, FC/C’ as well asFundedness measures based on HHBS:A/L

C’/FC, FC/C’ as well asFundedness measures based on HHBS:A/L

Mass Market Households and Participants

IF HHBS data incomplete, Fundedness measures based on a salary replacement ratio:

If HHBS data incomplete, Fundedness measures based on a salary replacement ratio::

If HHBS data incomplete, Fundedness measures based on a salary replacement ratio:

Are your tools, processes and products focused on the right client segment?

Investment Based Planning/Flooring Goals Based Planning/Flooring Product Based Planning

Best Practices: The Measures of “Fundedness”

Best Practices: The Household Balance Sheet

Best Practices Template: HHBS

PwC | RIIA | SBI

Fundamental Planning

StrategiesOverfunded Constrained Underfunded

High Net Worth Households and Participants

Investment-based planning(Generational Wealth)

Goal-based planning(Deferred Consumption)

Product-based planning(Best practices)

Affluent Households and Participants

Goal-based planning(Deferred Consumption)

Goal-based planning(Deferred Consumption)

Product-based planning(Best practices)

Mass Market Households and Participants

Product-based planning(Best practices)

Product-based planning(Best practices)

Product-based planning(Best practices)

A consistent conceptual framework across all stakeholder and client segments

Best Practices: Fundamental Planning Strategies

Best Practices: Mapping Risk Exposures

AssetAllocations

Retirement Allocations(Risk Management Techniques

Allocations)

Implementation Process Approaches

Stocks(60%)

Upside (risk retention)(60%)

Total Return

Bonds(30%)

Floor (risk management)(30%)

SWPsTime Segmentation

LaddersInsurance

- Longevity (risk pooling)(0%)

Insurance

Cash(10%)

Reserves (risk avoidance)(10%)

Cash

Best Practices: The Retirement Allocations

Retirement Allocations(Risk Management

Techniques Allocations)

Implementation Process Approaches

“Products that Wrap….

Upside (risk retention)(60%)

Total Return … The Market,

Floor (risk management)(30%)

SWPsTime Segmentation

LaddersInsurance

… The Market,…The Price of Income,

…The Household Balance Sheet,

… A Ladder,… The Mortality Credit,

Longevity (risk pooling)(0%)

Insurance … The Mortality Credit,

Reserves (risk avoidance)(10%)

Cash … Tax and/or Inflation.”

Mapping Products to Retirement Allocations

Better Understood,Better Managed,Better Protected.