Embed Size (px)

Citation preview

Summer Training Report

On

“An Insight into the Indian Capital Market”

At

Kolkata, West Bengal

Prepared by:

Vasundhara Kedia

Enrollment No. 10111161

PGPM

Under the Guidance of

Mr. Rohit Pasari (Cluster Manager) Mr. Krishnendu Ghosh

Industry Guide Faculty Guide

As a Partial Fulfilment of PGPM

At

Globsyn Business School, Kolkata

An Insight Into the Indian Capital Market

ACKNOWLEDGEMENT

This project work has been made possible through the direct and indirect cooperation of various people for whom I wish to express my appreciation and gratitude.

I would specially like to mention about my Industry guide, Mr. Santanu Basu ( Zonal Broking Head- East) and Mr. Rohit Pasari ( Cluster Manager- Business Development) of Karvy Stock Broking Ltd., whom I owe a profound sense of obligation and respect for guiding me and playing a pivotal role right from the start till the completion of this project. I also thank them for motivating and encouraging me to refine the work done at every stage.

My grateful appreciation is also extended to Professor Krishnendu Ghosh (Faculty Guide & Mentor, Globsyn Business School) and cordially thank him for his support and inculcating in me the focus and also for his ever enriching suggestions.

I would also take this opportunity to thank all my senior colleagues in KSBL for their unlisted encouragement, timely support and suggestions.

Page 2

An Insight Into the Indian Capital Market

DECLARATION

I, Vasundhara Kedia, hereby declare that this project entitled “An Insight into the Indian Capital Market,” submitted by me under the guidance of Mr. Rohit Pasari (Cluster Manager- Business Development, KSBL) and Professor Krishnendu Ghosh ( Faculty Guide & Mentor at Globsyn Business School) is my own work. The report has been prepared in partial fulfilment of requirements towards the Summer Internship Project at Karvy Stock Broking Ltd., Kolkata. I further declare that this dissertation has not been submitted earlier to any other university or institution for the award of any other degree or diploma.

………………………………………

Vasundhara Kedia

PGPM 11

Enrollment No. 10111161

Date-

Place-

Page 3

An Insight Into the Indian Capital Market

TABLE OF CONTENTS

PAGE NO.

1. Introduction to Karvy Stock Broking Ltd................................................ 5

2. Work done during Summer Training Program....................................... 15

3. Design............................................................................................................ 17

4. Introduction to The Indian Capital Market.............................................. 19

5. Legal Framework and Regulatory Bodies................................................ 67

6. Participants in the Indian Capital Market................................................ 73

7. Reforms in the Indian Capital Market...................................................... 77

8. Stock Exchanges in India............................................................................ 83

9. Risk and Risk Management in Indian Capital Market........................... 110

10. Presentation & Analysis of Data

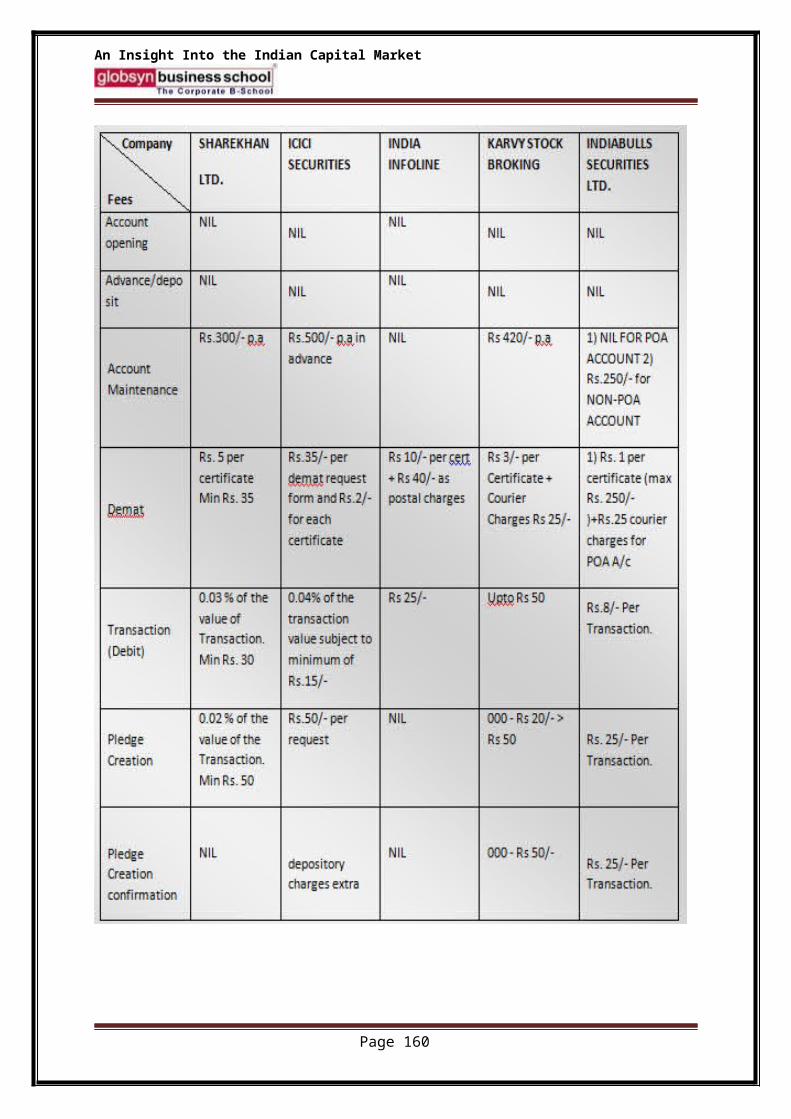

a) Comparative study of KSBL.................................................................... 108

b) Sensex v/s Nifty........................................................................................... 115

c) Sensex vis-à-vis International Markets.................................................... 137

d) Analysis of Indian Capital Market........................................................... 143

11. Recommendations..................................................................................... 148

12. Summary & Conclusions.......................................................................... 156

BIBLIOGRAPHY

Page 4

An Insight Into the Indian Capital Market

INTRODUCTION TO THE COMPANY

Page 5

An Insight Into the Indian Capital Market

“Success is a journey, not a destination.” If we look for examples to prove this quote then we can find many but there is none like that of Karvy. Back in the year 1981, five people created history by establishing Karvy and company which is today known as Karvy, the largest financial service provider of India.

Vision of Karvy:

To achieve & sustain market leadership, Karvy shall aim for complete customer satisfaction, by combining its human and technological resources, to provide world class quality services. In the process Karvy shall strive to meet and exceed customer’s satisfaction and set industry standards.

Mission statement:

“Our mission is to be a leading and preferred service provider to our customers, and we aim to achieve this leadership position by building an innovative, enterprising , and technology driven organization which will set the highest standards of service and business ethics.”

Company overview:

Karvy was established as ‘Karvy & Co.’ by five chartered accountants during the year 1979-80, and then its work was confined to audit and taxation only. Later on it diversified into financial and accounting services during the year 1981-82 with a capital of Rs.150000. It achieved its first milestone after its first investment in technology. Karvy became a known name during the year 1985-86 when it forayed into capital market as registrar.

Evolution of KARVY:

In 1982, a group of Hyderabad based practicing chartered accountants started KARVY consultant Ltd, with a capital of Rs.150,000 offering auditing and taxation services initially, later, it forayed into the registrar activities and into financial services.

KARVY- the letter in the work K,A,R,V,Y stands for 5 directors names.

K – Mr.Kutumba Rao.v. A- Mr. Ajay kumar.k. R- Mr.Ramakrishna.M.S. V-Mr.singh Y-Mr.Yugandhur

They along with, KARVY’s strong work ethic and professional background leverage with information technology enable it to deliver to the individual.

It is well said that success is a journey not a destination and we can see it being proved by Karvy. Under this section we will see that how this ‘Karvy & Co.’ of 1980 became “Karvy” of 2008. Karvy blossomed with the setting up of its first branch at Mumbai during the year 1987-88. The turning point came in the year 1989 when it decided to enter into one of the not

Page 6

An Insight Into the Indian Capital Market

only emerging rather potential field too i.e. stock broking. It added the feather of stock broking into its cap. At the same time it became the member of Hyderabad Stock Exchange through associate firm Karvy Securities Ltd and then Karvy never looked back, it went on adding services one after another, it entered into retail stock broking in the year 1990. Karvy investor service centers were set up in the year 1992. Karvy which already enjoyed a wide

network through its investor service centers, entered into financial product distribution services in the year 1993. One year more and Karvy was now dealing into mutual fund services too in the year 1994 but it didn’t stopped there, it stepped into corporate finance and investment banking in the year 1995.

Karvy’s strategy has always been being the first entrant in the market. Karvy again hit the limelight by becoming the first registrar in the country to be awarded ISO 9002 in the year 1997. Then it stepped into the other most happening sector i.e. IT enabled services by establishing its own BPO units and at a gap of just 1 year it took the path of e-Business through its website www.karvy.com . Then it entered into insurance services in the year 2001 with the launch of its retail arm “Karvy- The Finapolis: your personal finance advisor”. Then in the year 2002 it launched its PCG (Private Client Group) which looks after its High Networth Individuals .and maintain their portfolio and provides them with other financial services. In the year 2003, it commenced secondary debt and WDM trading.

It was a decade which saw many Indian companies going global. So, why should the largest financial service provider of India should lag behind? Hence, Karvy launched “Karvy Global

Page 7

An Insight Into the Indian Capital Market

Services Limited” after entering into a joint venture with Computershare, in Australia the year 2004. The year 2004 also saw Karvy entering into commodities marketing through Karvy Comtrade Ltd.

Year 2005 saw Karvy establishing a separate branch for its insurance services under the head “Karvy Insurance Broking Ltd” and in the same year, after being impressed with the rapid growth of Karvy Stock Broking Limited, PCG group of Hong Kong acquired 25% stake at KSBL. In the year 2006, Karvy entered into one of the hottest sector of present time i.e. real estate through Karvy Realty & Services (India) Ltd. Hence, we can see now Karvy being established as the largest financial service provider of the country.

KARVY GROUP – 11 RENOWNED ENTITIES :

The first securities registry to receive ISO 9002 certification in India. Registered with SEBI as Category I Registrar, is Number 1 Registrar in the Country. The award of being ‘Most Admired’ Registrar is one among many of the acknowledgements we received for our customer friendly and competent services.

Karvy stock broking ltd. Consists of five units namely stock broking services, depository participant, advisory services, distribution of financial products, advisory services and private client groups.

It is registered with SEBI as a category 1 merchant banker. Its clientele includes leading corporate, State Governments, foreign institutional investors, public and private sector companies and banks, in Indian and global markets.

Page 8

An Insight Into the Indian Capital Market

Karvy insurance broking ltd is also a part of Karvy Stock Broking Ltd. At Karvy Insurance Broking Limited both life and non-life insurance products are provided to retail individuals, high net-worth clients and ulfillin.

The company provides investment, advisory and brokerage services in Indian Commodities Markets. And most importantly, it offers a wide reach through our branch network of over 225 branches located across 180 cities.

Karvy Global is a leading business and knowledge process outsourcing Services Company offering creative business solutions to clients globally. It operates in banking and financial services, insurance, healthcare and pharmaceuticals, media, telecom and technology. It has its sales and business development office in New York, USA and the offshore global delivery center in Hyderabad, India.

Karvy Realty (India) Limited is engaged in the business of real estate and property services offering:

Buying/ selling/ renting of properties

Identifying valuable investments opportunities in the real estate sector

Facilitating financial support for real estate and investments in properties

Real estate portfolio advisory services

Page 9

An Insight Into the Indian Capital Market

Karvy Computershare Private Limited is a joint venture between Computershare, Australia and Karvy Consultants Limited, India in the registry management services industry. Computershare, Australia is the world’s largest and only global share registry providing financial market services and technology to the global securities industry. Karvy Corporate and Mutual Fund Share Registry and Investor Services business, India’s No. 1 Registrar and Transfer Agent and rated as India’s “Most Admired Registrar” for its overall excellence in volume management, quality processes and technology driven services.

KDMSL is emerging as a leading service provider in the areas of E-governance processing, insurance back office processing, record keeping, back office for BFSI clientele and is in pursuit to establish credentials in the areas of Telecom processing, Data management requirements of large corporate.

KDMSL is striving to achieve leadership position by tapping the Indian retail sector boom, through a combination of our extensive branch network and proprietary IT backbone. Needless to say, KDMSL is run as an independent outfit with seasoned professionals on board, who have decades of expertise in the industry.

KDMSL is a fully owned subsidiary of Karvy Stock Broking Limited (KSBL), incorporated in April 2008 and is head quartered at Hyderabad.

Karvy Fortune is a correlate opportunity from India’s foremost financial services provider, Karvy. It offers complete Karvy’s spectrum of financial products. Karvy fortune gives the opportunity to associate with “Karvy Family” as Franchisee, Remisser, E– Franchisee or as an Independent Financial Advisors.

Page 10

An Insight Into the Indian Capital Market

In its ambition to emerge as a complete financial advisor, KARVY has recently launched its personal financial planning wing, KARVY Financial Planning. It proposes to cater all advice to its customer pertaining to personal finance.

With India emerging as a strong market, the investments avenues have also increased, to advice our customers the right avenue according to their suitability.

Our vision is “To cater to the unique needs and requirements of the mass affluent by providing complete financial solutions and thereby enabling them to transform their dreams into reality.”

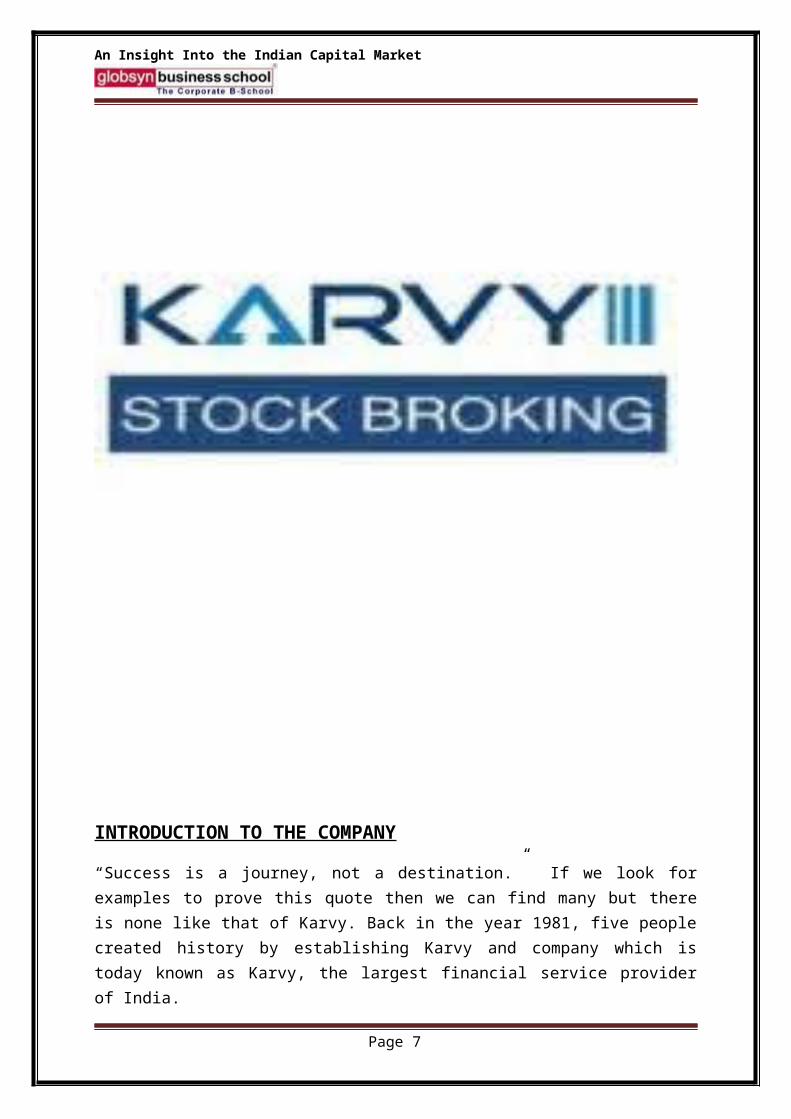

ORGANISATION STRUCTURE OF KARVY :

Page 11

An Insight Into the Indian Capital Market

Talking about the organization structure, the board of directors as the supreme governing body. The chairman being Mr. C Parthasarthy, Mr. M Yugandhar as the managing director and M S Ramakrishna as the Executive Director.

The Board of Directors head the Karvy Group, Karvy Computershares limited, Karvy Investors Services Ltd., Karvy Comtrade, Karvy Stock Broking Ltd., and Karvy Global Services Ltd.

Karvy group being the flagship company looks after the functional departments such as corporate affairs, group human resources, finance & accounting, training & development, technology services and corporate quality.

Page 12

An Insight Into the Indian Capital Market

Facilities Offered by KSBL :

Free online stock-broking and attractive margin funding options

Life time free demat account

Free online commodities broking account

Free Mutual Fund transactions to an unlimited extent ,including unlimited SIP transactions

Application in IPOs with attractive loan options for applications

Loans against securities

Daily equity market research reports and calls through SMS

Access to research reports on Mutual Fund, IPO sand Insurance

Regular portfolio statement for better planned future investments

Free financial advise on portfolio allocation in various asset classes

Free subscription of ‘KARVYF FinaPolis’ magazine

If there are disputes in the case of orders placed over phone, how can they be resolved?

Orders over the telephone can be placed only through designated telephone numbers. We have a voice recording system to record all orders placed over the telephone. We will ask for customer ID details before processing the order. Still, if a dispute arises, the voice recording would be the final proof for settling the dispute.

Trading Package of Karvy Online:

I-Zone ‘+’ : One-Stop Registration for Investment Zone

Equities & Derivates (NSE / BSE)

Mutual FundsAll major AMCs)

IPOs & DP services (NSDL/CDSL)

Commodities (NCDEX & MCX)

Facilities:

Page 13

An Insight Into the Indian Capital Market

Live market news

Quality research live on the trading screen

Top analysts providing inputs on strategies and recommendations

Alert facility for tracking

Seamless integration between bank, broking, mf and DP Accounts

Comprehensive net worth statement

Live tracking of investments

Corporate news a click away

Streaming quotes and news from the exchange on your desktop

Links to existing Karvy relations:

Offline Broking ID – The same UCC would be allotted for the I-Zone account.

Offline Mutual Fund Code – The existing Offline Folios if held singly in the name of Sole / First Applicant would be available for display in the online Login of the client. The portfolio would be updated on a daily basis. However, online transactions can be executed in such offline folios only after conversion of such offline folios to online folios. For conversion the client needs to provide one letter to each AMC in whose scheme he/she has invested mentioning the offline Folio number.

Demat ID –If the client already holds a demat account with Karvy where the holder(s) in demat is same as applicants in the I-Zone form and in the same sequence, the existing demat account can be connected to the I-Zone account. All IPO bids, in such case, would be placed in the name of joint holders as in demat account.

Page 14

An Insight Into the Indian Capital Market

WORK DONE DURING SUMMER TRAINING

PROGRAM

WORK DONE DURING SUMMER TRAINING PROGRAM :

Page 15

An Insight Into the Indian Capital Market

Engaged in:

1. Selling Discounted Brokerage Plans to Active Clients.

2. KYC Updation of Clients Inactive/Never Traded/Dormant from 2009 and before

3. Making inactive clients from 2010 and after resume trading.

4. Handling Client Grievances- meeting clients and enabling Inactive HNI Clients resume activity.

5. Client interaction with respect to Physical Contract Note wherein, the client e-mail was invalid thus creating ECN issue.

6. Attending and briefing Interns from other B-Schools with respect to the project & job role.

7. Assisting Industry Guide in preparing his Clusters’ Employee KRA Evaluation.

Page 16

An Insight Into the Indian Capital Market

RESEARCH DESIGN

DESIGN

Page 17

An Insight Into the Indian Capital Market

Research can be defined as a scientific and systematic search for pertinent information on a specific topic. Research is a careful investigation of inquiry especially through search for new facts in any branch of knowledge. In simple terms, research refers to search for knowledge. Research comprises defining and redefining problems, formulating hypothesis or suggested solutions collecting, organizing and evaluating data, making deductions and reaching conclusions and at last carefully testing the conclusion to determine whether they fit the formulating hypothesis.

Research methodology is away to systematically solve the research problem. It may understand as a science of studying how research is done scientifically. In it, we study the various steps that are generally adopted by the researcher in study of his research problem along with logic behind them.

A Research design is a framework or blueprint for conducting the research of a project. It details the procedures necessary for obtaining the information needed. A research design lays the foundation for conducting the project.

Secondary Data was largely used for the purpose of data interpretation and analysis.

For the purpose of the review, research has been defined as doctoral dissertations, papers published in academic journals, books (including expository, but excluding obviously popular books) and working papers or occasional unpublished papers (where such information was available) on Indian capital markets. I have reviewed articles published in the popular media such as financial dailies, business magazines and other popular magazines and journals. I have also reviewed dissertations for Masters’ degrees, reports of government committees or commissions, seminar and conference papers. I have also included publications in foreign journals. It is possible that, in the process, the list of works reviewed may have excluded some excellent works published in popular media or included some sub-standard works published in academic journals.

Page 18

An Insight Into the Indian Capital Market

OVERVIEW

The past decade in many ways has been remarkable for securities market in India. It has grown exponentially as measured in terms of amount raised from the market, number of stock

Page 19

An Insight Into the Indian Capital Market

exchanges and other intermediaries, the number of listed stocks, market capitalization, trading volumes and turnover on stock exchanges, and investor population. Along with this growth, the profiles of the investors, issuers and intermediaries have changed significantly. The market has witnessed several institutional changes resulting in drastic reduction in transaction costs and significant improvements in efficiency, transparency, liquidity and safety. In a short span of time, Indian derivatives market has got a place in list of top global exchanges. In single stock futures category, the Futures Industry Association (FIA) placed NSE in second position in the year 2000.

INTRODUCTION

The market for long-term securities like bonds, equity stocks and preferred stocks is divided into primary market and secondary market. The primary market deals with the new issues of securities. Outstanding securities are traded in the secondary market, which is commonly known as stock market or stock exchange. In the secondary market, the investors can sell and buy securities. Stock markets predominantly deal in the equity shares. Debt instruments like bonds and debentures are also traded in the stock market. Well-regulated and active stock market promotes capital formation. Growth of the primary market depends on the secondary market. The health of the economy is reflected by the growth of the stock market.

Companies raise funds to finance their projects through various methods. The promoters can bring their own money or borrow from the financial institutions or mobilize capital by issuing securities. The funds may be raised through issue of fresh shares at par or premium, preference shares, debentures or global depository receipts. The main objectives of a capital issue are given below:

To promote a new company To expand an existing company To diversify the production To meet the regular working capital requirements To capitalize the reverses

Securities markets provide a channel for allocation of savings to those who have a productive need for them. As a result, the savers and investors are not constrained by their individual abilities, but by the economy’s abilities to invest and save respectively, which inevitably enhances savings and investment in the economy.

MARKET SEGMENT

Page 20

An Insight Into the Indian Capital Market

The securities market has two interdependent and inseparable segments: the primary and the secondary market. The primary market provides the channel for creation of new securities through issuance of financial instruments by public companies as well as Governments and Government agencies and bodies whereas the secondary market helps the holders of these financial instruments to sale for exiting from the investment. The price signals, which subsume all information about the issuer and his business including associated risk, generated in the secondary market, help the primary market in allocation of funds. The primary market issuance is done either through public issues or private placement. A public issue does not limit any entity in investing while in private placement, the issuance is done to select people. In terms of the Companies Act, 1956, an issue becomes public if it results in allotment to more than 50 persons. This means an issue resulting in allotment to less than 50 persons is private placement.

There are two major types of issuers who issue securities. The corporate entities issue mainly debt and equity instruments (shares, debentures, etc.), while the governments (central and state governments) issue debt securities (dated securities, treasury bills). The secondary market enables participants who hold securities to adjust their holdings in response to changes in their assessment of risk and return. They also sell securities for cash to meet their liquidity needs. The exchanges do not provide facility for spot trades in a strict sense. Closest to spot market is the cash market in exchanges where settlement takes place after some time. Trades

Page 21

An Insight Into the Indian Capital Market

taking place over a trading cycle (one day under rolling settlement) are settled together after a certain time. All the 23 stock exchanges in the country provide facilities for trading of corporate securities. Trades executed on NSE only are cleared and settled by a clearing corporation which provides novation and settlement guarantee. Nearly 100% of the trades in capital market segment are settled through demat delivery. NSE also provides a formal trading platform for trading of a wide range of debt securities including government securities in both retail and wholesale mode. NSE also provides trading in derivatives of equities, interest rate as well indices. In derivatives market (F&O market segment of NSE), standardized contracts are traded for future settlement. These futures can be on a basket of securities like an index or an individual security. In case of options, securities are traded for conditional future delivery. There are two types of options – a put option permits the owner to sell a security to the writer of options at a predetermined price while a call option permits the owner to purchase a security from the writer of the option at a predetermined price. These options can also be on individual stocks or basket of stocks like index.

Two exchanges, namely NSE and the Stock Exchange, Mumbai (BSE) provide trading of derivatives of securities. Today the market participants have the flexibility of choosing from a basket of products like:

• Equities

• Bonds issued by both Government and Companies

• Futures on benchmark indices as well as stocks

• Options on benchmark indices as well as stocks

• Futures on interest rate products like Notional 91-day T-Bills, 10 year notional zero

Page 22

An Insight Into the Indian Capital Market

HISTORY OF INDIAN CAPITAL MARKET

HISTORY OF INDIAN CAPITAL MARKET

Page 23

An Insight Into the Indian Capital Market

The history of the Indian capital markets and the stock market, in particular can be traced back to 1861 when the American Civil War began. The opening of the Suez Canal during the 1860s led to a tremendous increase in exports to the United Kingdom and United States. Several companies were formed during this period and many banks came to the fore to handle the finances relating to these trades. With many of these registered under the British Companies Act, the Stock Exchange, Mumbai, came into existence in 1875.

It was an unincorporated body of stockbrokers, which started doing business in the city under a banyan tree. Business was essentially confined to company owners and brokers, with very little interest evinced by the general public. There had been much fluctuation in the stock market on account of the American war and the battles in Europe. Sir Premchand Roychand remained a kingpin for many years.

Sir Phiroze Jeejeebhoy was another who dominated the stock market scene from 1946 to 1980. His word was law and he had a great deal of influence over both brokers and the government. He was a good regulator and many crises were averted due to his wisdom and practicality. The BSE building, icon of the Indian capital markets, is called P.J. Tower in his memory.

The planning process started in India in 1951, with importance being given to the formation of institutions and markets The Securities Contract Regulation Act 1956 became the parent regulation after the Indian Contract Act 1872, a basic law to be followed by security markets in India. To regulate the issue of share prices, the Controller of Capital Issues Act (CCI) was passed in 1947.

The stock markets have had many turbulent times in the last 140 years of their existence. The imposition of wealth and expenditure tax in 1957 by Mr. T.T. Krishnamachari, the then finance minister, led to a huge fall in the markets. The dividend freeze and tax on bonus issues in 1958-59 also had a negative impact. War with China in 1962 was another memorably bad year, with the resultant shortages increasing prices all round. This led to a ban on forward trading in commodity markets in 1966, which was again a very bad period, together with the introduction of the Gold Control Act in 1963.

The markets have witnessed several golden times too. Retail investors began participating in the stock markets in a small way with the dilution of the FERA in 1978. Multinational companies, with operations in India, were forced to reduce foreign share holding to below a certain percentage, which led to a compulsory sale of shares or issuance of fresh stock. Indian investors, who applied for these shares, encountered a real lottery because those were the days when the CCI decided the price at which the shares could be issued. There was no free pricing and their formula was very conservative.

The next big boom and mass participation by retail investors happened in 1980, with the entry of Mr. Dhirubhai Ambani. Dhirubhai can be said to be the father of modern capital markets. The Reliance public issue and subsequent issues on various Reliance companies generated

Page 24

An Insight Into the Indian Capital Market

huge interest. The general public was so unfamiliar with share certificates that Dhirubhai is rumoured to have distributed them to educate people.

Mr. V.P. Singh’s fiscal budget in 1984 was path-breaking for it started the era of liberalization. The removal of estate duty and reduction of taxes led to a swell in the new issue market and there was a deluge of companies in 1985. Mr. Manmohan Singh as Finance Minister came with a reform agenda in 1991 and this led to a resurgence of interest in the capital markets, only to be punctured by the Harshad Mehta scam in 1992. The mid-1990s saw a rise in leasing company shares, and hundreds of companies, mainly listed in Gujarat, and got listed in the BSE. The end- 1990s saw the emergence of Ketan Parekh and the information, communication and entertainment companies came into the limelight. This period also coincided with the dotcom bubble in the US, with software companies being the most favoured stocks. There was a meltdown in software stock in early 2000. Mr. P Chidambaram continued the liberalization and reform process, opening up of the companies, lifting taxes on long-term gains and introducing short-term turnover tax. The markets have recovered since then and we have witnessed a sustained rally that has taken the index over 13000.

Several systemic changes have taken place during the short history of modern capital markets. The setting up of the Securities and Exchange Board (SEBI) in 1992 was a landmark development. It got its act together, obtained the requisite powers and became effective in early 2000. The setting up of the National Stock Exchange in 1984, the introduction of online trading in 1995, the establishment of the depository in 1996, trade guarantee funds and derivatives trading in 2000, have made the markets safer. The introduction of the

Fraudulent Trade Practices Act, Prevention of Insider Trading Act, Takeover Code and Corporate Governance Norms, are major developments in the capital markets over the last few years that has made the markets attractive to foreign institutional investors. This history shows us that retail investors are yet to play a substantial role in the market as long-term investors. Retail participation in India is very limited considering the overall savings of households.

Investors who hold shares in limited companies and mutual fund units are about 20-30 million. Those who participated in secondary markets are 2-3 million. Capital markets will change completely if they grow beyond the cities and stock exchange centers reach the Indian villages. Both SEBI and retail participants should be active in spreading market wisdom and empowering investors in planning their finances and understanding the markets.

Page 25

An Insight Into the Indian Capital Market

Page 26

An Insight Into the Indian Capital Market

Financial markets facilitate the reallocation of savings from savers to entrepreneurs. Savings are linked to investments by a variety of intermediaries through a range of complex financial products called “securities” which is defined in the Securities Contracts (Regulation) Act, 1956 to include shares, bonds, scrips, stocks or other marketable securities of like nature in or of any incorporate company or body corporate, government securities, derivatives of securities, units of collective investment scheme, interest and rights in securities, security receipt or any other instruments so declared by the central government.

It is not that the users and suppliers of funds meet each other and exchange funds for securities. It is difficult to accomplish such double coincidence of wants. The amount of funds supplied by the supplier may not be the amount needed by the user. Similarly, the risk, liquidity and maturity characteristics of the securities issued by the issuer may not match preference of the supplier. In such cases, they incur substantial search costs to find each other. Search costs are ulfillin by the intermediaries who match and bring the suppliers and users of funds together. These intermediaries may act as agents to match the needs of users and suppliers of funds for a commission, help suppliers and users in creation and sale of securities for a fee or buy the securities issued by users and in turn, sell their own securities to suppliers to book profit. It is, thus, a misnomer that securities market disintermediates by establishing a direct relationship between the savers and the users of funds. The market does not work in a vacuum; it requires services of a large variety of intermediaries. The disintermediation in the securities market is in fact an intermediation with a difference, it is a risk-less intermediation,

Page 27

An Insight Into the Indian Capital Market

where the ultimate risks are borne by the savers and not the intermediaries. A large variety and number of intermediaries provide intermediation services in the Indian securities market. The securities market has essentially three categories of participants, namely the issuers of securities, investors in securities and the intermediaries and products include equities, bonds and derivatives. The issuers and investors are the consumers of services rendered by the intermediaries while the investors are consumers (they subscribe for and trade in securities) of securities issued by issuers.

In pursuit of providing a product to meet the needs of each investor and issuer, the intermediaries churn out more and more complicated products. They educate and guide them in their dealings and bring them together. Those who receive funds in exchange for securities and those who receive securities in exchange for funds often need the reassurance that it is safe to do so. This reassurance is provided by the law and by custom, often enforced by the regulator. The regulator develops fair market practices and regulates the conduct of issuers of securities and the intermediaries so as to protect the interests of suppliers of funds. The regulator ensures a high standard of service from intermediaries and supply of quality securities and non-manipulated demand for them in the market.

The past decade in many ways has been remarkable for securities market in India. It has grown exponentially as measured in terms of amount raised from the market, number of stock exchanges and other intermediaries, the number of listed stocks, market ulfillingion, trading volumes and turnover on stock exchanges, and investor population. Along with this growth, the profiles of the investors, issuers and intermediaries have changed significantly. The market has witnessed fundamental institutional changes resulting in drastic reduction in transaction costs and significant improvements in efficiency, transparency and safety.

Page 28

An Insight Into the Indian Capital Market

CAPITAL MARKET AT A GLANCE

Page 29

An Insight Into the Indian Capital Market

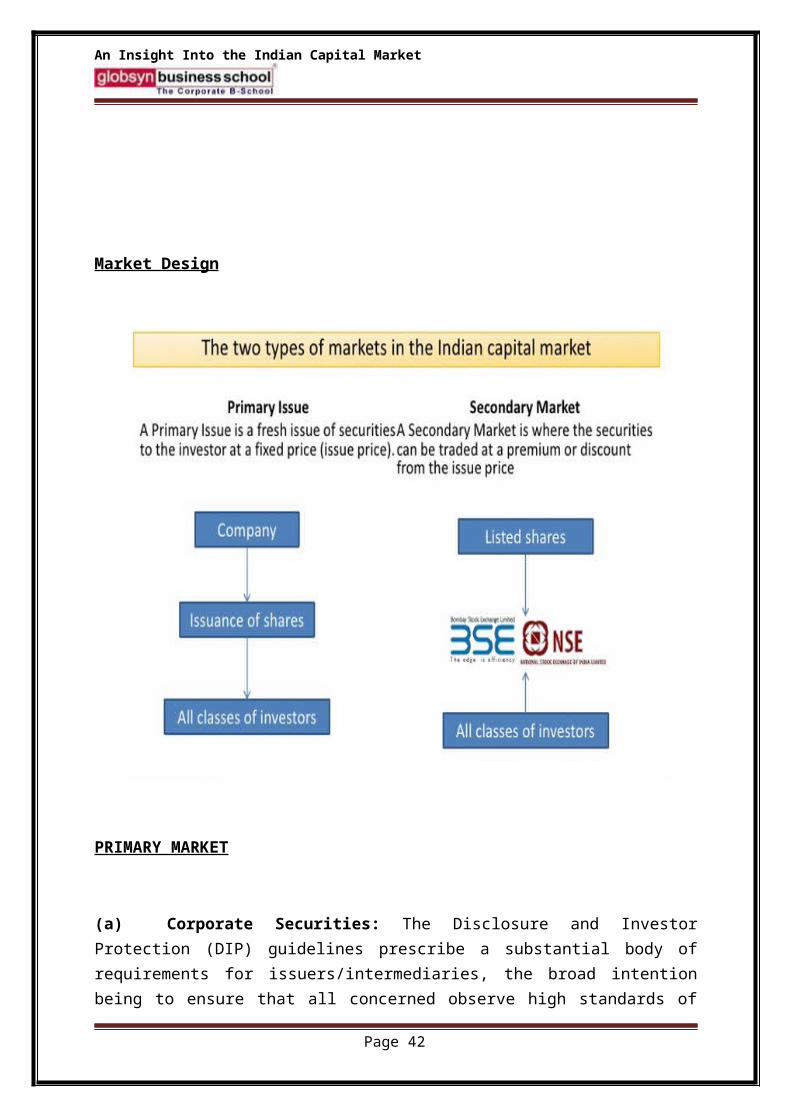

Market Design

PRIMARY MARKET

(a) Corporate Securities: The Disclosure and Investor Protection (DIP) guidelines prescribe a substantial body of requirements for issuers/intermediaries, the broad intention being to ensure that all concerned observe high standards of integrity and fair dealing, comply with all the requirements with due skill, diligence and care, and disclose the truth, whole truth and nothing but truth. The guidelines aim to secure fuller disclosure of relevant information about the issuer and the nature of the securities to be issued so that investors can take informed decisions. For example, issuers are required to disclose any material ‘risk factors’ and give justification for pricing in their prospectus. An unlisted company can access the market up to 5 times its pre-issue net-worth only if it has track record of distributable profits and net worth of Rs. 1 crore in 3 out of last five years. A listed company can access up to 5 times of its pre-issue net-worth. In case a company does not have track record or wishes to raise beyond 5 times of its pre-issue net-worth, it can access the market only through book building with minimum offer of 60% to qualified institutional buyers. Infrastructure companies are exempt

Page 30

An Insight Into the Indian Capital Market

from the requirement of eligibility norms if their project has been appraised by a public financial institution and not less than 5% of the project cost is financed by any of the institutions, jointly or severally, by way of loan and/or subscription to equity. The debt instruments of maturities more than 18 months require credit rating. If the issue size exceeds Rs. 100 crore, two ratings from different agencies are required. Thus the quality of the issue is demonstrated by track record/appraisal by approved financial institutions/credit rating/subscription by QIBs. The lead merchant banker discharges most of the pre-issue and post-issue obligations. He satisfies himself about all aspects of offering and adequacy of disclosures in the offer document. He issues a due diligence certificate stating that he has examined the prospectus, he finds it in order and that it brings out all the facts and does not contain anything wrong or misleading. He also takes care of allotment, refund and ulfilli of certificates. The admission to a depository for dematerialization of securities is a prerequisite for making a public or rights issue or an offer for sale. The investors, however, have the option of subscribing to securities in either physical form or dematerialized form. All new IPOs are compulsorily traded in I form. Every public listed company making IPO of any security for Rs. 10 crore or more is required to do so only in I form.

(b) Government Securities: The government securities market has witnessed significant transformation in the 1990s. With giving up of the responsibility of allocating resources from securities market, government stopped expropriating seigniorage and started borrowing at near – market rates. Government securities are now sold at market related coupon rates through a system of auctions instead of earlier practice of issue of securities at very low rates just to reduce the cost of borrowing of the government. Major reforms initiated in the primary market for government securities include auction system (uniform price and multiple price method) for primary issuance of T-bills and central government dated securities, a system of primary dealers and non-competitive bids to widen investor base and promote retail participation, issuance of securities across maturities to develop a yield curve from short to long end and provide benchmarks for rest of the debt market, innovative instruments like, zero coupon bonds, floating rate bonds, bonds with embedded derivatives, availability of full range ( 91-day and 382-day) of T-bills, etc.

Page 31

An Insight Into the Indian Capital Market

Page 32

An Insight Into the Indian Capital Market

Functions of Primary Market

The main service functions of the primary market are organization, underwriting and distribution. Origination deals with the origin of the new issue. The proposal is analyzed in terms of the nature of the security, the size of the issue, and timing of the issue and floatation method of the issue. Underwriting contract makes the share predictable and removes the element of uncertainty in the subscription. Distribution refers to the lead managers and brokers to the issue.

In the new issue market stocks are offered for the first time. The functions and the organization of the new issue market is different from the secondary market. In the new issue the lead mangers manage the issue, the underwriters assure to take up the unsubscribed portion according to his commitment for a commission and the bankers take up the responsibility of the collecting the application form and the money. Advertising agencies promote the new issue through advertising. Financial institutions and underwriter lend term loans to the company. Government agencies regulate the issue. The new issues are offered through prospectus. The prospectus is drafted according to SEBI guidelines disclosing the needed information to the investing public. In the bought out deal banks or a company buys the promoters shares and they offer them to the public at a later date. This reduces the cost of raising the fund. Private placement means placing of the issue with financial institutions. They sell shares to the investors at a suitable price. Right issue means the allotment of shares to the previous shareholders at a pro-ratio basis. Book building involves firm allotment of the instrument to a syndicate created by the lead managers. The book runner manages the issue. Norms are given by the SEBI to price the issue. Proportionate allotment method is adopted in the allocation of shares. Project appraisal, disclosure in the prospectus and clearance of the prospectus by the stock exchanges protect the investors in the primary market along with the active role played by the SEBI.

Page 33

An Insight Into the Indian Capital Market

Page 34

An Insight Into the Indian Capital Market

SECONDARY MARKET

(a) Corporate Securities: The stock exchanges are the exclusive centres for trading of securities. Though the area of operation/jurisdiction of an exchange is specified at the time of its recognition, they have been allowed recently to set up trading terminals anywhere in the country. The three newly set up exchanges (OTCEI, NSE and ICSE) were permitted since their inception to have nation-wide trading. The trading platforms of a few exchanges are now accessible from many locations. Further, with extensive use of information technology, the trading platforms of a few exchanges are also accessible from anywhere through the Internet and mobile devices. This made a huge difference in a geographically vast country like India.

(b) Exchange Management: Most of the stock exchanges in the country are organized as “mutuals” which was considered beneficial in terms of tax benefits and matters of compliance. The trading members, who provide brokering services, also own, control and manage the exchanges. This is not an effective model for self-regulatory ulfillingio as the regulatory and public interest of the exchange conflicts with private interests. Efforts are on to demutualise the exchanges whereby ownership, management and trading membership would be segregated from one another. Two exchanges viz. OTCEI and NSE are demutualised from inception, where ownership, management and trading are in the hands of three different sets of people. This model eliminates conflict of interest and helps the exchange to pursue market efficiency and investor interest aggressively.

I Membership: The trading platform of an exchange is accessible only to brokers. The broker enters into trades in exchanges either on his own account or on behalf of clients. No stock broker or sub-broker is allowed to buy, sell or deal in securities, unless he or she holds a certificate of registration granted by SEBI. A broker/sub-broker complies with the code of conduct prescribed by SEBI. Over time, a number of brokers – proprietor firms and partnership firms – have converted themselves into ulfillin. The standards for admission of members stress on factors, such as corporate structure, capital adequacy, track record, education, experience, etc. and reflect a conscious endeavor to ensure quality broking services.

(d) Listing: A company seeking listing satisfies the exchange that at least 10% of the securities, subject to a minimum of 20 lakh securities, were offered to public for subscription, and the size of the net offer to the public (i.e. the offer price multiplied by the number of securities offered to the public, excluding reservations, firm allotment and promoters’ contribution) was not less than Rs.100 crore, and the issue is made only through book building method with allocation of 60% of the issue size to the qualified institutional buyers.

Page 35

An Insight Into the Indian Capital Market

In the alternative, it is required to offer at least 25% of the securities to public. The company is also required to maintain the minimum level of non-promoter holding on a continuous basis. In order to provide an opportunity to investors to invest/trade in the securities of local companies, it is mandatory for the companies, wishing to list their securities, to list on the regional stock exchange nearest to their registered office. If they so wish, they can seek listing on other exchanges as well. Monopoly of the exchanges within their allocated area, regional aspirations of the people and mandatory listing on the regional stock exchange resulted in multiplicity of exchanges. The basic norms for listing of securities on the stock exchanges are uniform for all the exchanges. These norms are specified in the listing agreement entered into between the company and the concerned exchange. The listing agreement prescribes a number of requirements to be continuously complied with by the issuers for continued listing and such compliance is monitored by the exchanges. It also stipulates the disclosures to be made by the companies and the corporate governance practices to be followed by them.

SEBI has been issuing guidelines/circulars prescribing certain norms to be included in the listing agreement and to be complied with by the companies. A listed security is available for trading on the exchange. The stock exchanges levy listing fees – initial fees and annual fees – from the listed companies. It is a major source of income for many exchanges. A security listed on other exchanges is also permitted for trading. A listed company can voluntary delist its securities from non-regional stock exchanges after providing an exit opportunity to holders of securities in the region where the concerned exchange is located. An exchange can, however, delist the securities compulsorily following a very stringent procedure.

(e) Trading Mechanism: The exchanges provide an on-line fully-automated screen based trading system (SBTS) where a member can punch into the computer quantities of securities and the prices at which he likes to transact and the transaction is executed as soon as it finds a matching order from a counter party. SBTS electronically matches orders on a strict price/time priority and hence cuts down on time, cost and risk of error, as well as on fraud resulting in improved operational efficiency. It allows faster incorporation of price sensitive information into prevailing prices, thus increasing the informational efficiency of markets. It enables market participants to see the full market on real-time, making the market transparent. It allows a large number of participants, irrespective of their geographical locations, to trade with one another simultaneously, improving the depth and liquidity of the market. It provides full anonymity by accepting orders, big or small, from members without revealing their identity, thus providing equal access to everybody. It also provides a perfect audit trail, which helps to resolve disputes by logging in the trade execution process in entirety.

(f) Trading Rules: Regulations have been framed to prevent insider trading as well as unfair trade practices. The acquisitions and takeovers are permitted in a well defined and orderly manner. The companies are permitted to buy back their securities to improve liquidity and enhance the shareholders’ wealth.

Page 36

An Insight Into the Indian Capital Market

(g) Price Bands: Stock market volatility is generally a cause of concern for both policy makers as well as investors. To curb excessive volatility, SEBI has prescribed a system of price bands. The price bands or circuit breakers bring about a coordinated trading halt in all equity and equity derivatives markets nation-wide. An index-based market-wide circuit breaker system at three stages of the index movement either way at 10%, 15% and 20% has been prescribed. The movement of either S&P CNX Nifty or Sensex, whichever is breached earlier, triggers the breakers. As an additional measure of safety, individual scrip-wise price bands of 20% either way have been imposed for all securities except those available for stock options.

(h) Demat Trading: The Depositories Act, 1996 was passed to proved for the establishment of depositories in securities with the objective of ensuring free transferability of securities with speed, accuracy and security by

(a) making securities of public limited companies freely transferable subject to certain exceptions;

(b) ulfillingion the securities in the depository mode; and

I providing for maintenance of ownership records in a book entry form. In order to streamline both the stages of settlement process, the Act envisages transfer of ownership of securities electronically by book entry without making the securities move from person to person. Two depositories, viz. NSDL and CDSL, have come up to provide instantaneous electronic transfer of securities. At the end of March 2002, 4,172 and 4,284 companies were connected to NSDL and CDSL respectively. The number of I securities increased to 56.5 billion at the end of March 2002. As on the same date, the value of dematerialsied securities was Rs. 4,669 billion and the number of investor accounts was 4,605,588. All actively traded scrips are held, traded and settled in demat form. Demat settlement accounts for over 99% of turnover settled by delivery. This has almost eliminated the bad deliveries and associated problems. To prevent physical certificates from sneaking into circulation, it has been mandatory for all new IPOs to be compulsorily traded in dematerialized form. The admission to a depository for I of securities has been made a prerequisite for making a public or rights issue or an offer for sale. It has also been made compulsory for public listed companies making IPO of any security for Rs. 10 crore or more to do the same only in I form.

(i) Charges: A stock broker is required to pay a registration fee of Rs.5,000 every financial year, if his annual turnover does not exceed Rs. 1 crore. If the turnover exceeds Rs. 1 crore during any financial year, he has to pay Rs. 5,000 plus one-hundredth of 1% of the turnover in excess of Rs.1 crore. After the expiry of five years from the date of initial registration as a broker, he has to pay Rs. 5,000 for a block of five financial years. Besides, the exchanges collect transaction charges from its trading members. NSE levies Rs. 4 per lakh of turnover. The maximum brokerage a trading member can levy in respect of securities transactions is

Page 37

An Insight Into the Indian Capital Market

2.5% of the contract price, exclusive of statutory levies like SEBI turnover fee, service tax and stamp duty. However, brokerage charges as low as 0.15% are also observed in the market.

(j) Trading Cycle: Rolling settlement on T+3 basis gave way to T+2 from April 2003. The market has moved close to spot/cash market.

(k) Risk Management: To pre-empt market failures and protect investors, the regulator/exchanges have developed a comprehensive risk management system, which is constantly monitored and upgraded. It encompasses capital adequacy of members, adequate margin requirements, limits on exposure and turnover, indemnity insurance, on-line position monitoring and automatic disablement, etc. They also administer an efficient market surveillance system to curb excessive volatility, detect and prevent price manipulations. Exchanges have set up trade/settlement guarantee funds for meeting shortages arising out of nonfulfillment/partial fulfillment of funds obligations by the members in a settlement. A clearing corporation assures the counterparty risk of each member and guarantees financial settlement in respect of trades executed on NSE.

(l) Government Securities: The reforms in the secondary market include Delivery versus Payment system for settling scrip less SGL transactions to reduce settlement risks, SGL Account II with RBI to enable financial intermediaries to open custody (Constituent SGL) accounts and facilitate retail transactions in scrip less mode, enforcement of a trade-for-trade regime, settlement period of T+0 or T+1 for all transactions undertaken directly between SGL participants and up to T+5 days for transactions routed through NSE brokers, routing transactions through brokers of NSE, OTCEI and BSE, repos in all government securities with settlement through SGL, liquidity support to PDs to enable them to support primary market and undertake market making, special fund facility for security settlement, etc. As part of the ongoing efforts to build debt market infrastructure, two new systems, the Negotiated Dealing System (NDS) and the Clearing Corporation of India Limited (CCIL) commenced operations on February 15, 2002. NDS, facilitates screen based negotiated dealing for secondary market transactions in government securities and money market instruments, online reporting of transactions in the instruments available on the NDS and dissemination of trade information to the market. Government Securities (including T-bills), call money, notice/term money, repos in eligible securities, Commercial Papers and Certificate of Deposits are available for negotiated dealing through NDS among the members. The CCIL facilitates settlement of transactions in government securities (both outright and repo) on Delivery versus Payment (DvP-II) basis which provides for settlement of securities on gross basis and settlement of funds on net basis simultaneously. It acts as a central counterparty for clearing and settlement of government securities transactions done on NDS.

Page 38

An Insight Into the Indian Capital Market

Relationship between the Primary and Secondary Market

1. The new issues market cannot function without the secondary market. The secondary market or the stock market provides liquidity for the issued securities. The issued securities are traded in the secondary market offering liquidity to the stocks at a fair price.

2. The stock exchanges through their listing requirements, exercise control over the primary market. The company seeking for listing on the respective stock exchange has to comply with all the rules and regulations given by the stock exchange.

3. The primary market provides a direct link between the prospective investors and the company. By providing liquidity and safety, the stock markets encourage the public to subscribe to the new issues. The marketability and the capital appreciation provided in the

Page 39

An Insight Into the Indian Capital Market

stock market are the major factors that attract the investing public towards the stock market. Thus, it provides an indirect link between the savers and the company.

4. Even though they are complementary to each other, their functions and the organizational set up are different from each other. The health of the primary market depends on the secondary market and vice versa.

Page 40

An Insight Into the Indian Capital Market

CURRENT STATUS OF INDIAN CAPITAL

MARKET

CURRENT STATUS OF INDIAN CAPITAL MARKET

Page 41

An Insight Into the Indian Capital Market

Market ulfillingion and turnover

As on March 31, 2000, the Indian stock market had a market ulfillingion of over Rs 10 trillion ($ 230 billion) representing 58per cent of GDP. The annual trading volume in all the exchanges put together amounted to Rs 20 trillion (approximately twice the market ulfillingion). The average daily trading volume is about $2 billion and there are days on which the turnover is twice this level.

India has 9,871 listed companies; this number is second only to that of the United States. However, most of the trading volume is concentrated in a few hundred stocks, and even within this, the top hundred stocks account for a disproportionate share of the trading volume.

The Indian capital market is well-diversified in terms of ownership pattern and industry structure. Most of the top 50 companies are domestic private sector companies with no single family or business group accounting for a disproportionate share. There is no foreign owned corporation, public sector ulfillingi or newly ulfilling company in the top five stocks by market ulfillingion. Companies with a market ulfillingion of $1 billion or more are present in industries as diverse as software, petrochemicals, oil refining, consumer goods, telecom, banking, pharmaceuticals, and entertainment.

In the last few years, however, new economy stocks have shown rapid increase in their market ulfillingion and turnover. In the BSE 500 index covering the top 500 listed companies, new economy stocks account for about 49per cent of market ulfillingion and 50per cent of the average daily turnover.

Stock exchanges

India boasts of the oldest stock exchange in Asia – the Bombay Stock Exchange is 125 years old. There are 23 recognised exchanges spread across the country, but a process of consolidation is now under way. Many of the regional stock exchanges have started aligning themselves with one or both of the two large exchanges (the Bombay Stock Exchange and the National Stock Exchange) both of which have VSAT networks that give them a nation wide reach.

The National Stock Exchange is an unlisted for-profit company set up by some of the leading financial institutions of India. Most of the remaining stock exchanges are broker-owned (mutual) ulfillingio, but the Bombay Stock Exchange is actively considering ulfillingion. The Securities and Exchange Board of India (SEBI), the apex regulator of the capital market has regulations that mandate a minimum number of outside directors on the governing board and provide greater autonomy to the professional executives in the day-to-day running of the exchange.

Trading and settlement

Page 42

An Insight Into the Indian Capital Market

India’s stock exchanges are fully ulfillingi order driven or order-cum-quote driven systems. The country has made rapid strides towards a I trading environment on the basis of a competing depositories model. Investors have the choice of holding their stocks in physical or I form, but trading in the exchanges is in mandatory I mode in most important stocks. As of October 2000, about 98per cent of the trading in the stock exchanges is in I mode.

India has put in place a regulatory regime for internet trading of stocks. A large number of online brokers have started operations. More brokers are expected to follow when the exchanges put in place an ASP (Application Service Provider) model for online trading software. However, currently, the level of penetration of online trading is extremely small.

The stock exchanges currently run two parallel settlement systems. Practically all the trading takes place in the account period settlement system in which all trades during a weekly account period are netted off and the net obligations are settled five business days after the end of the period. The other unpopular system is that of rolling settlements where trades of each day are settled on a T+5 basis. SEBI is currently working on mandatorily shifting all stocks in a phased manner to the rolling settlement system. Further improvements in the settlement system to T+3 or beyond would have to wait for improvements in the payment system.

However, account period settlement does not give rise to significant systemic risks in India because of stringent end of day and intra-day margining systems. Put simply, the weekly settlement is regarded as akin to a one-week futures contract, and the systemic risk is taken care of by using futures style margining. The exchange imposes daily mark to market and initial margins on the brokers to eliminate settlement risk. Exchanges also have clearing houses to guarantee settlements on the exchange. As a result, there have been no settlement failures in the principal stock exchanges during the last five years.

Primary market

India enjoyed a major boom of IPOs in the mid 1990s. This hot IPO period came to an end in 1995-96 with a fall in the stock market and a downturn in the economy. Investors who subscribed at the height of the boom suffered significant losses, and the primary market has yet to recover from this debacle. In the late 1990s, moreover, the Indian corporate sector was in the midst of a structural transformation with the old economy companies stocks doing badly in the face of global competition while software companies delivered outstanding financial results. The stock market also rewarded the new economy stocks with high valuations. In this environment, it was difficult for most old economy companies to come to the market with a credible business plan. Software companies in India have used a stock market listing primarily to establish a valuation and create an acquisition currency as their large positive cash flows leave them with little need for additional funding.

At the same time, SEBI has been concerned about public capital raising by companies with no track record. Newly set up software companies, entertainment companies and internet

Page 43

An Insight Into the Indian Capital Market

companies with no tangible assets pose particular problems of valuation. In this situation, SEBI has moved half-way towards a QIB (Qualified Institutional Buyers) market for some of these stocks. This mandatory gatekeeping approach is discussed later in this paper. In 1999-2000, a total of Rs 78 billion was raised in the Indian capital market, of which about Rs 45 billion was in the form of equity and the balance in the form of debt.

Disclosure and corporate governance

India moved from a merit based regulation to a disclosure based regulation of the primary market with the establishment of the Securities and Exchange Board of India (SEBI) in 1992. The level of disclosure has increased progressively in recent years as SEBI has attempted to bring disclosure requirements up to international levels. This is an ongoing exercise.

In the field of continuing disclosure, listed companies are now required to disclose unaudited financial results on a quarterly basis, and there is now a subject these results to limited auditor review. The Accounting Standards Board set up by the accounting profession is engaged in a major exercise to bring Indian accounting standards on par with those of the IASC (International Accounting Standards Committee).

SEBI is now in the process of implementing the Corporate Governance Code framed by the Birla Committee through the listing agreement. Under this code, companies are required to have a minimum number of independent directors, and to have an audit committee.

Globalisation

India operates a rigorous system of exchange controls on the capital account. However, a window has been created for foreign portfolio investment. As on March 31, 2000, there were 506 Foreign Institutional Investors (FIIs) registered with SEBI. These FIIs had in the aggregate invested $11.23 billion in the Indian stock market; this represents about 5 per cent of the market ulfillingion.

Indian companies have also been allowed to issue shares outside the country in the form of GDRs (Global Depository Receipts) and ADRs (American Depository Receipts). From 1992-93 to 1998-99, Indian companies raised Rs 274 billion in this form. Any holder of ADRs and GDRs can convert these into the underlying domestic shares. However conversion in the opposite direction is not permitted.

Mutual funds

Page 44

An Insight Into the Indian Capital Market

As on March 31, 2000, there were 37 mutual funds registered with SEBI. This is in addition to the country’s largest and oldest mutual fund, the Unit Trust of India, which is not yet under SEBI’s regulatory purview. These mutual funds had floated a total of 330 different mutual fund schemes, which together controlled assets of Rs 1.1 trillion ($ 25 billion) representing about 11per cent of the market ulfillingion.

Investor population and profile

According to the investor survey carried out by the National Council of Applied Economic Research (NCAER) together with SEBI, about 8per cent of all households hold equity shares or debentures. This constitutes an investor base of 19 million individuals. Investors in mutual funds numbered about 23 million thanks mainly to the long established Unit Trust of India. Allowing for common ownership of shares and mutual funds, there are probably about 30 million direct and indirect investors in the Indian capital market.

The share of household financial savings that goes to the capital market is very small at around 3 per cent. This share had reached a level of 23 per cent in early 1990s towards the end of a long boom in the capital markets and has been steadily declining since then.

Derivatives market

India’s fledgling index futures market is less than six months old and the trading volume is far below even one per cent of the cash market volumes. Global experience suggests that the market may still be in the initial stage of low awareness and low acceptance, and that the market could pick up in coming months. There are also plans to introduce new derivative products.

Page 45

An Insight Into the Indian Capital Market

CLASSIFICATION OF INDIAN CAPITAL

MARKET

CLASSIFICATION OF INDIAN CAPITAL MARKET:

Page 46

An Insight Into the Indian Capital Market

PRIMARY MARKET

The primary is that part of the capital markets that deals with the issuance of new securities. Companies, governments or public sector institutions can obtain funding through the sale of a new stock or bond issue. This is typically done through a syndicate of securities dealers. The process of selling new issues to investors is called underwriting. In the case of a new stock issue, this sale is an initial public offering (IPO). Dealers earn a commission that is built into the price of the security offering, though it can be found in the prospectus.

The primary market for equity, which consists of both the ‘initial public offering’ (IPO)market and the ‘seasoned equity offering’ (SEO) markets, experienced considerable activity in 2005 and 2006 (Table 4.1). In 2006,Rs.30,325 crore of resources were raised onthis market, of which Rs.9,918 crore were made up by 55 companies which were listed for the first time (IPOs). The number of IPOs per year has risen steadily from 2002 onwards. A level of 55 IPOs in the year translates to roughly 4 IPOs every month. The mean IPO size, which was elevated in 2005, returned to Rs.180 crore, which is similar to the value prevalent in 2003. 4.3 The primary issuance of debt securities, as per SEBI, fell to a low of around Rs. 66 crore in 2006, which is one facet of the far-reaching difficulties of the debt market. Unlike equity securities, debt securities issued at previous dates are redeemed by companies every year. Hence, a year with a low issuance of fresh debt securities is a year in which the stock of outstanding debt securities drops. In addition to resource ulfillingi by the issuance of debt and equity securities, one of the most important mechanisms of financing that has been used by Indian firms is retained earnings, which are also a part of equity financing.

Page 47

An Insight Into the Indian Capital Market

New issue market instruments

The term initial public offering (IPO) slipped into everyday speech during the tech bull market of the late 1990s. Back then, it seemed you couldn’t go a day without hearing about a dozen new dotcom millionaires in Silicon Valley who were cashing in on their latest IPO. The phenomenon spawned the term siliconaire, which described the dotcom entrepreneurs in their early 20s and 30s who suddenly found themselves living large on the proceeds from their internet companies’ IPOs.

Selling Stock

An initial public offering, or IPO, is the first sale of stock by a company to the public. A company can raise money by issuing either debt or equity. If the company has never issued equity to the public, it’s known as an IPO.

Companies fall into two broad categories: private and public.

A privately held company has fewer shareholders and its owners don’t have to disclose much information about the company. Anybody can go out and incorporate a company: just put in some money, file the right legal documents and follow the reporting rules of your jurisdiction. Most small businesses are privately held. But large companies can be private too.

Page 48

An Insight Into the Indian Capital Market

It usually isn’t possible to buy shares in a private company. You can approach the owners about investing, but they’re not obligated to sell you anything. Public companies, on the other hand, have sold at least a portion of themselves to the public and trade on a stock exchange. This is why doing an IPO is also referred to as “going public.” Public companies have thousands of shareholders and are subject to strict rules and regulations. They must have a board of directors and they must report financial information every quarter. In the United States, public companies report to the Securities and Exchange Commission (SEC). In other countries, public companies are overseen by governing bodies similar to the SEC. From an investor’s standpoint, the most exciting thing about a public company is that the stock is traded in the open market, like any other commodity. If you have the cash, you can invest. The CEO could hate your guts, but there’s nothing he or she could do to stop you from buying stock.

Going public raises cash, and usually a lot of it. Being publicly traded also opens many financial doors:

Because of the increased scrutiny, public companies can usually get better rates when they issue debt.

As long as there is market demand, a public company can always issue more stock. Thus, mergers and acquisitions are easier to do because stock can be issued as part of the deal.

Trading in the open markets means liquidity. This makes it possible to implement things like employee stock ownership plans, which help to attract top talent.

Being on a major stock exchange carries a considerable amount of prestige. In the past, only private companies with strong fundamentals could qualify for an IPO and it wasn’t easy to get listed.

The internet boom changed all this. Firms no longer needed strong financials and a solid history to go public. Instead, IPOs were done by smaller startups seeking to expand their businesses. There’s nothing wrong with wanting to expand, but most of these firms had never made a profit and didn’t plan on being profitable any time soon. Founded on venture capital funding, they spent like Texans trying to generate enough excitement to make it to the market before burning through all their cash. In cases like this, companies might be suspected of doing an IPO just to make the founders rich. This is known as an exit strategy, implying that there’s no desire to stick around and create value for shareholders. The IPO then becomes the end of the road rather than the beginning.

SECONDARY MARKET:

Page 49

An Insight Into the Indian Capital Market

Outstanding securities are traded in the secondary market, which is commonly known as stock market or stock exchange. In the secondary market, the investors can sell and buy securities. Stock markets predominantly deal in the equity shares. Debt instruments like bonds and debentures are also traded in the stock market.

Dematerialization

Indian investor community has undergone sea changes in the past few years. India now has a very large investor population and ever increasing volumes of trades. However, this continuous growth in activities has also increased problems associated with stock trading. Most of these problems arise due to the intrinsic nature of paper based trading and settlement, like theft or loss of share certificates. This system requires handling of huge volumes of paper leading to increased costs and inefficiencies. Risk exposure of the investor also increases due to this trading in paper.

Some of these risks are:

Delay in transfer of shares.

Possibility of forgery on various documents leading to bad deliveries, legal disputes etc.

Possibility of theft of share certificates.

Prevalence of fake certificates in the market.

Mutilation or loss of share certificates in transit.

The physical form of holding and trading in securities also acts as a bottleneck for broking community in capital market operations.

The introduction of NSE and BOLT has increased the reach of capital market manifolds. The increase in number of investors participating in the capital market has increased the possibility of being hit by a bad delivery. The cost and time spent by the brokers for rectification of these bad deliveries tends to be higher with the geographical spread of the clients. The increase in trade volumes lead to exponential rise in the back office operations thus limiting the growth potential of the broking members. The inconvenience faced by investors (in areas that are far flung and away from the main metros) in settlement of trade also limits the opportunity for such investors, especially in participating in auction trading. This has made the investors as well as broker wary of Indian capital market. In this scenario dematerialized trading is certainly a welcome move.

What is Dematerialization?

Page 50

An Insight Into the Indian Capital Market

Dematerialization or “Demat” is a process whereby your securities like shares, debentures etc, are converted into electronic data and stored in computers by a Depository. Securities registered in your name are surrendered to depository participant (DP) and these are sent to the respective companies who will cancel them after “Dematerialization” and credit your depository account with the DP. The securities on Dematerialization appear as balances in your depository account. These balances are transferable like physical shares. If at a later date, you wish to have these “demat” securities converted back into paper certificates, the Depository helps you to do this.

Depository

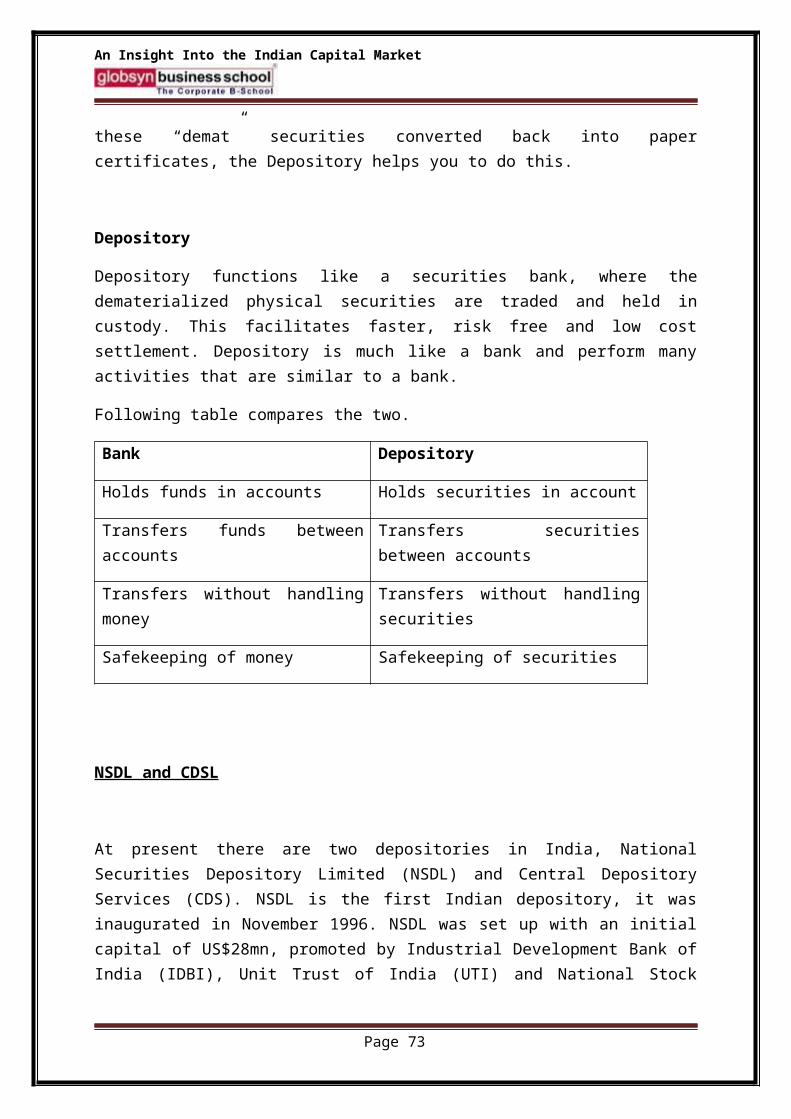

Depository functions like a securities bank, where the dematerialized physical securities are traded and held in custody. This facilitates faster, risk free and low cost settlement. Depository is much like a bank and perform many activities that are similar to a bank.

Following table compares the two.

Bank Depository

Holds funds in accounts Holds securities in account

Transfers funds between accounts Transfers securities between accounts

Transfers without handling money Transfers without handling securities

Safekeeping of money Safekeeping of securities

NSDL and CDSL

At present there are two depositories in India, National Securities Depository Limited (NSDL) and Central Depository Services (CDS). NSDL is the first Indian depository, it was inaugurated in November 1996. NSDL was set up with an initial capital of US$28mn, promoted by Industrial Development Bank of India (IDBI), Unit Trust of India (UTI) and National Stock Exchange of India Ltd. (NSEIL). Later, State Bank of India (SBI) also became a shareholder.

The other depository is Central Depository Services (CDS). It is still in the process of linking with the stock exchanges. It has registered around 20 DPs and has signed up with 40 companies. It had received a certificate of commencement of business from Sebi on February 8, 1999.

Page 51

An Insight Into the Indian Capital Market

These depositories have appointed different Depository Participants (DP) for them. An investor can open an account with any of the depositories’ DP. But transfers arising out of trades on the stock exchanges can take place only amongst account-holders with NSDL’s DPs. This is because only NSDL is linked to the stock exchanges (nine of them including the main ones-National Stock Exchange and Bombay Stock Exchange).

In order to facilitate transfers between investors having accounts in the two existing depositories in the country the Securities and Exchange Board of India has asked all stock exchanges to link up with the depositories. Sebi has also directed the companies’ registrar and transfer agents to effect change of registered ownership in its books within two hours of receiving a transfer request from the depositories. Once connected to both the depositories the stock exchanges have also to ensure that inter-depository transfers take place smoothly. It also involves the two depositories connecting with each other. The NSDL and CDS have signed an agreement for inter-depository connectivity.

Depositiory Participant