Embed Size (px)

Citation preview

An Industry Leader in Aluminium & Copper

September 2010

Hindalco Industries LimitedInvestor Presentation

2Hindalco Industries Limited: Investor Presentation

DisclaimerThis presentation may not be copied, published, distributed or transmitted. The information in this presentation is being provided by Hindalco Industries Limited (the

“Company”).

Any reference in this presentation to “Hindalco Industries Limited” shall mean, collectively, the Company and its subsidiaries. This presentation has been prepared for

informational purposes only. This presentation does not constitute a prospectus, offering circular or offering memorandum and is not an offer or invitation to buy or sell any

securities, nor shall part, or all, of this presentation form the basis of, or be relied on in connection with, any contract or investment decision in relation to any securities.

Furthermore, this presentation is not an offer of securities for sale in the United States, India or any other jurisdiction.

This presentation may contain forward-looking statements based on the currently held beliefs and assumptions of the management of the Company, which are expressed in

good faith and, in their opinion, reasonable. Forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results,

financial condition, performance, or achievements of the Company or industry results, to differ materially from the results, financial condition, performance or achievements

expressed or implied by such forward-looking statements. Given these risks, uncertainties and other factors, recipients of this presentation are cautioned not to place undue

reliance on these forward-looking statements. The Company disclaims any obligation to update these forward-looking statements to reflect future events or developments.

The Company, as such, makes no representation or warranty, express or implied, as to, and does not accept any responsibility or liability with respect to, the fairness,

accuracy, completeness or correctness of any information or opinions contained herein. The Company assumes no responsibility to publicly amend, modify or revise any

forward-looking statements, on the basis of any subsequent development, information or events, or otherwise. Unless otherwise stated in this presentation, the information

contained herein is based on management information and estimates. The information contained herein is subject to change without notice and past performance is not

indicative of future results. The Company may alter, modify or otherwise change in any manner the content of this presentation, without obligation to notify any person of such

revision or changes.

By attending this presentation you acknowledge that you will be solely responsible for your own assessment of the market and the market position of the Company and that

you will conduct your own analysis and be solely responsible for forming your own view of the potential future performance of the business of the Company.

Disclaimer

Our VisionStrategy –to build upstream

and buy downstream

ABG aspires to be in the Fortune 200 with a $65bn turnover by

FY15 and Hindalco expected to be the torchbearer..

Towards a new Hindalco

“To be a premiummetals major, Global

in size and reach, excelling in everything we do, and creating value for its

stakeholders”

4Hindalco Industries Limited: Investor Presentation

Hindalco : A promise delivered through stellar performance

Stronger NovelisStronger Novelis

Paradigm shift in focus – from volume driven to EBITDA drivenHigher premiums and permanent cost cutsWell positioned in emerging markets with strong growth fundamentalsOne of the world’s largest recyclers of aluminium – reduces costs and enables signficant reduction in energy consumptionSignficant market share in FRP with strong global market outlook

From turnaround to outperformer-

EBITDA of US$1bn

From turnaround to outperformer-

EBITDA of US$1bn

Existing Indian Operations

Existing Indian Operations

Asset sweating, Brownfield expansion on trackExploiting low cost baseIncreasing mix of VAP and domestic salesDominant market share

Better profitability

amongst peers

Better profitability

amongst peers

Focus on delivering expansion plans

Focus on delivering expansion plans

Well timed capacity increases – expected to be in the global best quartile for manufacturing costsSignificant progress achieved – reinforcing timely delivery capabilities

Ensures full coverage across the value chain

Ensures full coverage across the value chain

1. Novelis : Successful Turnaround Story

6Hindalco Industries Limited: Investor Presentation

Key themes

Industry: Improved aluminium sector fundamentals with a positive demand outlook

Novelis turnaround: Dual benefit of pricing power and cost cutting, coupled with strong liquidity

Way forward for Novelis: On the threshold of robust

growth I

III

II

7Hindalco Industries Limited: Investor Presentation

Global Economies : Showing on the road to recovery

Major emerging economies such as China and India have rebounded strongly from global downturn

7.9

6.0

2.4

1.4

10.3

9.3

(5.3

)

(0.7

)

US Europe China India

Q209 Q309 Q409 Q110 Q210

Global economic recovery continues …YOY % GDP growth rate from Q2 2009 to Q2 2010

(%)

Q2 2010 growth rates for Europe and India are estimates

… with improved sector outlook

(CY09-14)

4-8% 8-10% >10% 8%

4%

4%

7%

6%10%>10%3-5%

2-3%

6%

7%

10%

4-6%

10%

>15% 8-10%0%

Asia

N. America

Europe

S. America

Global

Can Sheet Automotive Industrial/ Electronics

Overall demand

I

8Hindalco Industries Limited: Investor Presentation

Novelis – Turnaround in operations

Uptick in volumes...

Turnaround driven by a number of cost cutting initiatives…

Restructuring globally across the Company to reduce labour and overhead costs through capacity and staff reductions

– Reduced manpower by 11%

Annual cost savings of US$140m achieved ahead of schedule

Transfer of production facilities to low-cost regions – relocation of Rogerstone facility to Hirakud

Proactive risk management for commodity pricing, foreign exchange and interest rate risks

746756

632 605 650693

649716

263

231199200

124

5388

127

500

550

600

650

700

750

800

Q2FY09 Q3FY09 Q4FY09 Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY110

50

100

150

200

250

300Shipments (kt) Adjusted EBITDA (US$mn)

116 201 88 191 289 307 323 353

Adjusted EBITDA/ton (US$)

II

9Hindalco Industries Limited: Investor Presentation

Novelis – Convergence of Adj. EBITDA and EBITDA

Over time, Novelis has witnessed a gradual convergence between EBITDA and adjusted EBITDA

213

(124)

(1,868)

214 413 434

264

164

263231

199

200124

5388127

(2,000)

(1,500)

(1,000)

(500)

0

500

Q2FY09 Q3FY09 Q4FY09 Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY11

EBITDA (US$mn) Adjusted EBITDA (US$mn)

II

Novelis’ strong risk management practices combined with the termination of certain ceiling contracts have led to a gradual

convergence of EBITDA and adjusted EBITDA numbers

10Hindalco Industries Limited: Investor Presentation

Novelis shipments – sustained improvement across markets

Automotive

Industrial

Cans

Automotive

Industrial

Cans

Automotive

Industrial

Cans

Automotive

Industrial

Cans

North America Europe

South America Asia

246 254 258 243274 278

Q4 Q1 Q2 Q3 Q4 Q1

II

1018999755737

Q4 Q1 Q2 Q3 Q4 Q1

188 185203 188

227 232

Q4 Q1 Q2 Q3 Q4 Q1

889460603315

Q4 Q1 Q2 Q3 Q4 Q1

Shipments (kt)

Segment income (US$mn)

85 81

9384

86 90

Q4 Q1 Q2 Q3 Q4 Q1

49382636119

Q4 Q1 Q2 Q3 Q4 Q1

86130 139 134 129 146

Q4 Q1 Q2 Q3 Q4 Q1

4441394838

3

Q4 Q1 Q2 Q3 Q4 Q1

Shipments (kt)

Segment income (US$mn)

Shipments (kt)

Segment income (US$mn)

Shipments (kt)

Segment income (US$mn)

Current trend in Aluminium demand Novelis’ Shipments Novelis’ Segment Income

11Hindalco Industries Limited: Investor Presentation

Global Leader in Aluminium Recycling

Novelis is one of the world’s largest recyclers of aluminium

− 9 plants on 4 continents

Aluminium recycling only requires 5% of energy used to produce primary aluminium

Aluminium recycling avoids 95% of GHG emissions of primary aluminium smelting

Novelis recycled 40 billion cans in FY2009

− Reduced the need for primary aluminium by 530,000 metric tons

− Saved 73 million MMBTUS

− Avoided 5 million tonnes of GHG emissions

Recycling drives low cost position; positions the cans as environmentally preferred package

II

12Hindalco Industries Limited: Investor Presentation

Sustained turnaround with strong liquidity

Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY11

Cash and cash equivalents Availability under the ABL facility

$446$555

$634

$1,026 $1,051

Strong liquidity (Mn)

Strong liquidity: Now focuses on strategic capital allocation decision

Excess cash may be utilized by Novelis towards future capex (the Company recently announced Pinda Project in Brazil)

On its way to fuel Greater Hindalco growth

Visibly sustained turnaround in Operating and Financial Performance

649

746716

693650

756

632 605

263231

199

88

200

12453

127

500

600

700

800

Q2FY09 Q3FY09 Q4FY09 Q1F10 Q2FY10 Q3FY10 Q4FY10 Q1FY110

100

200

300

400

FRP Shipments (LHS) Adjusted EBITDA (RHS)

FRP

Ship

men

ts (k

t)

41 44 43 40 41 41 3642

Interest, net (US$ mn)

Adjusted EB

ITDA

(US$m

n)

II

13Hindalco Industries Limited: Investor Presentation

Novelis today III

High end products focusContinues to build on its strong market position in FRPMajority of product portfolio comprised of premium productsMarket leader in can recycling with strong technology focus

Inventory controlSignificant reduction in inventory through effective supply chain management

Worldwide assets and expertise provide unique capabilities to regional/ global customers

1

2

34

5

6

De-risked business modelSimple converter business (LME pass through)

Well Balanced geographic mixOver 33% revenues from emerging markets

Effective Risk ManagementStrong controls and systems in place to reduce volatility

Cost initiativesRelocation of facilities to low-cost regions Greater application of Novelis technology for global projects

Novelis’ initiatives and multi-pronged strategy have successfully enabled it to turnaround operations

14Hindalco Industries Limited: Investor Presentation

Novelis going forward III

Novelis is on the threshold of robust growth, with plans to exceed $1B of Adjusted EBITDA per annum going forward

“One Novelis” Drive Efficiencies and Reduce Costs

Expand and further consolidate leadership position

Build on Novelis’ focused business model to become a fully integrated global company

Strategic &Opportunistic Investments

Reduce overall cost base and improve manufacturing efficiency

Leverage and streamline procurement

Standardize financial and IT platforms

Greater application of Novelis technology for global projects (such as Tata Motors)

Governed by operating efficiency gains and IRR hurdle rates

Explore potential opportunities and identify optimum option for deployment of excess cash reserves

Achieve plant optimization in developed markets

Emerging markets and brownfield expansion focus

Pinda Project in Brazil

15Hindalco Industries Limited: Investor Presentation

Strong Outlook for FRP ProductsFRP growth worldwide from 2010 to 2015 (kt)

967222

343639

3383,088

16,493

22,090

10,000

12,000

14,000

16,000

18,000

20,000

22,000

24,000

2010 Asia MENA West. Europe East. Europe S. America N. America 2015

Areas of focus

III

Focusing capex on growing economies; Europe & N.A to return to pre-recession levels

16Hindalco Industries Limited: Investor Presentation

Novelis continues to be strong player in global can business

Beverage can portfolio – Immune to economic downturn~58% can body stockRecycling – Go Green initiativeNovelis bought over 40bn cans in FY10

Novelis – Dominant player in global can business

FY09 – Can shipments – 1,557 KT FY10 – Can shipments – 1,580 KT

Advantages of the CanCans have considerable advantages over bottles in

all relevant areas for retail and industry

Branding Freshness

Variety Logistics

16%

3%6%

4%

17%

45%9%Beverage cans Foil & Packaging

Industrial Transport

Construction Lithography

Others

10%

2%4%

8%

15%

54%

7%Beverage cans Foil & Packaging

Industrial Transport

Construction Lithography

Others

Steady increase in contribution by beverage can segment

FY08

FY10

III

2. Continued impressive performance of Indian operations

18Hindalco Industries Limited: Investor Presentation

Key themes

IIIndustry : Improved Domestic aluminium sector fundamentals with a positive demand outlook

Focused growth of Indian operations – All round improvement in Al

Copper business: Steady margins despite decline in TcRc rates, with good by-product realizations; situation expected to improve

I

III

II

19Hindalco Industries Limited: Investor Presentation

Hindalco at the forefront of the explosive growth in India

Large scope for metal consumption to rise from current levels

End user segments have a strong/positive outlook – i.e. Power, Transport, Construction, Industrial etc

Rising per capita consumption of Al in India

Strong metal sector growth – Al consumption and Cu consumption

India: Strong growth in end user industries

390

435

FY10 Q1 FY11 Q1

11.5%

Aluminium consumption (kt)

Copper consumption (kt)

3.8%

160

166

FY10 Q1 FY11 Q1

Electrical & Electronics

Building & Construction

Consumer Durable

Automobile & Transport

Industrial Machinery

Packaging

I

Insulated from global pressures due to exposure to Power sector in India – accounts for c.48% of aluminium usage in India

20Hindalco Industries Limited: Investor Presentation

Indian Al operations – robust growth prospects

Alumina (kt) Metal (kt)

Higher alumina and metal production on he back of Brownfield expansions… increased volumes of downstream value added products

Wire rod (kt) FRP (kt) Extrusions (kt)

1,237

1,307

FY09 FY10

6%

523

555

FY09 FY10

6%

75

92

FY09 FY10

23%

182

205

FY09 FY10

13%

36

39

FY09 FY10

8%

II

21Hindalco Industries Limited: Investor Presentation

Cost control initiatives launched proactively ahead of the global downturn have helped

The Company has been able to maximize production output at Hirakud, which has access to captive coal

Costs to reduce further as Greenfield projects come on stream

Hindalco: Low cost positionHindalco Aluminium smelters are in the best quartile (25th percentile)

on cost Further set to benefit from Hirakud Cost Advantage

Hindalco’s Indian aluminium operations ranked amongst the lowest cost producers of aluminium globally

0

500

1,000

1,500

2,000

2,500

3,000

1% 25% 41% 52% 63% 75% 85% 94% 100%

Hirakud Business Operating Costs

Renukoot Business Operating Costs

% of World Production

Site Operating Cash Cost Curve

100

94

FY09 FY10

Aluminium conversion cost (Rs/t, Indexed)

29.0

28.0

28.5

27.0

707580859095

100105110115120

FY10Q1 FY10Q2 FY10Q3 FY10Q426.0

26.5

27.0

27.5

28.0

28.5

29.0

29.5

95

102

100

114

86

107

110

84

102 99

104

86

Hirakud

Renukoot

Hirakud sharein output (%)

Overall

US$/ t

II

The only smelter which uses captive coal and power

22Hindalco Industries Limited: Investor Presentation

VAP to drive margins

Hindalco expects to increase VAP going forward and maintain its dominant market share going forward

Healthier product-mix and geographic mix (kt)

60% 57 %

43%40%

FY09 FY10

VAP

Primary

6%521 555

82%69%

18%31%

FY09 FY10

Exports

Domestic

521 555

VAP sales: One of the key drivers for Hindalco’s sales in IndiaKey brands commanding significant market share; has 53% market share in domestic Rolled Products sales*Increasing downstream applications in India; Hindalco’s well balanced product portfolio would consolidate market leader positionHigh margins further enhanced with duty protection

VAP: Key driver for Hindalco’s downstream operations

Key Brands

Hindalco’s downstream products command market premium with significant market share in India

II

Hindalco has a dominant market share in FRP

23Hindalco Industries Limited: Investor Presentation

Al Railway Wagon in India

New initiatives undertaken by Hindalco

Hindalco has pioneered new range of futuristic value added product range with a potential to improve margins

II

Development of Aluminium hoods & roof

Al. Swing Arm

Aluminisation in Automotives

Al Roofing's for Construction Al Bicycle Frames

Al Boats

24Hindalco Industries Limited: Investor Presentation

Hindalco: Long on Alumina

China’s dependence is positive for Hindalco’s long alumina position

II

Contract alumina prices up from 12-12.5% of LME historically to 13-13.5% in 2009 and to 14-15% in 2010

8.110.8

16.4 16

2.3

18

1980 1990 2000 2010

ROW China

China increasingly dependent on ROW for its alumina requirement

Rising Alumina cost further adds to Chinese costs

Global Alumina Third Party Market (mn tons)

Alumina Aluminium

1.5 0.6

Hindalco 2010: Integrated Upstream Operations

mtpa

Upstream

Alumina Aluminium

3.0 1.4

Upstream

Hindalco 2012: Integrated Global Upstream Operations

Going forward Hindalco will be long in Alumina

Delinking of Alumina prices from the LME and introduction of spot price would benefit Hindalco’s long alumina position

25Hindalco Industries Limited: Investor Presentation

A cost effective “Upstreaming” strategyMining acquisitionStrategic alliances/partnership

Long Term feedstock securitisation

By-Products value extractionValue added downstreaming

Value Chain Enhancement

Global ScaleTop Quartile Cost Curve

Global Cost Competitiveness

Jetty /port infrastructure to overcome locational disadvantageSourcing Mix optimisationRegional redistribution points

Service level differentiationQuality edge

Cost effective brown field expansionStrategic advantage through technologyAsset sweating

Drivers

Leadership in domestic market offering better realisation

Supply Chain Reengineering

Capital Efficiency

Key focus areas

Steps taken by Hindalco to strengthen copper business III

1

2

3

4

5

6

Transforming the copper business into a globally competitive smelting value chain

26Hindalco Industries Limited: Investor Presentation

999

182 333

1,043

170 298

DAP (kt) Cathode (kt) Sulfuric Acid (kt)

FY09 FY10

Copper Operations - Good performance despite tough market conditions

Sustained improvement in key parameters like recovery and energy consumptionEnergy-mix : more usage of petcoke and LNGRatio of VAP to cathode production up from 37% to 53%DAP production increased significantly

12%

Cathode (kt)

Copper Cathode cost w/o any credits (c/lb, indexed)100

73

FY09 FY10

4%7%56,450

49,600

FY09 FY10

14%

Overall production down 19% to 57kt due to conscious idling of Mt. Gordon

Nifty production (tons)

448

166

72

(89)

440

(60)

Sales (US$mn) EBIDTA (US$mn) PAT (US$mn)

FY09 FY10

Performance at ABML (US$mn)

III

27Hindalco Industries Limited: Investor Presentation

Strong financial performance (standalone)

68

181132 163 182 196

820 847

1,0691,155

1,1751,126

1,4011,530

1,836

2,037

2,1992,122

(100)

100

300

500

700

900

1,100

1,300

1,500

Q4FY09 Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY110

500

1,000

1,500

2,000

2,500Sales (US$mn) EBITDA (US$mn) LME prices (US$)

8% 21% 12% 14% 15%

EBIDTA Margin (%)

Exchange Rate: US$1: INR46

17%

3. Expansion Projects : Aggressively focused on delivery with calibrated financial closure on course

29Hindalco Industries Limited: Investor Presentation

Robust project pipeline – backbone to deliver growth future growth

Total land requirement of c.4,000 acres for the project. Application for acquisition of private land has been submittedWater drawl clearance received for 55 MCM and DFR is complete

US$ 2,174 mnQ1 FY14JharkhandAluminium

c.1,387 Acres of land registered in name of company, process forbalance land is in progressWater drawl agreement to draw upto10.42 cusecs obtained

US$ 1,304 mnQ1 FY14Aditya Refinery

Q2FY12

Q3FY12

Q2FY12

Timing – Expected Completion

US$ 1,217 mn

US$ 2,000 mn

US$ 2,000 mn

Project Cost (US$mn)

Detailed Engg-59% Complete for smelter & 25 % complete for CPPMajor approvals received. Forest land stage I clearance received. Permission to start project site consolidation activities received. Stage II clearance is progressing

Aditya Aluminium

Basic Engg-100 % Complete, Detailed Engg-92% CompletedAll statutory clearances have been obtainedMore than 5000 people working at site. Major Contractors like L & T, Simplex, GDC mobilized fully at site

Utkal Alumina

Basic Engg-94 % Complete, Detailed Engg-60% CompleteMajor approvals in placeOrders for all major, long delivery equipment placedMore than 10,000 people at site. Major Contractors like L&T, BHEL, Rohan Builders etc have been mobilized fully

Mahan Aluminium

CommentsProject

Exchange Rate: US$1: INR46

30Hindalco Industries Limited: Investor Presentation

Update on Project : Greenfield

% committed

6,578 acres3,328 acres3,750 acresLand spread

Q2FY12Q3FY12Q2FY12Expected Completion

Capex ramp up (US$mn)

US$ 1,217 mnUS$ 2,000 mnUS$ 2,000 mnProject Cost (US$mn)

1,500 ktpa359 ktpa smelter900MW power plant

359 ktpa smelter900MW power plant

Scope

RefinerySmelterSmelterNature

Mahan aluminium, Madhya Pradesh Aditya aluminium, Orissa Utkal alumina, Orissa

57%83%

%committedat time of

QIP

%committed

current

49%66%

%committedat time of

QIP

%committed

current

66% 82%

%committedat time of

QIP

%committed

current

370522

28344

2010 2011 2012 2013

217

924

522300

2010 2011 2012 2013

109

630870

337

2010 2011 2012 2013

Key Benefits

Well timed capacity increase

Lower Production Cost

Lower Capex Cost ( on a per

ton basis)

Raw Material Coverage

Greater Integration

Exchange Rate: US$1: INR46

31Hindalco Industries Limited: Investor Presentation

Progress of Key Projects

Basic Engineering – 100% and Detailed Engineering – 92% completed

Statutory approvals – obtained

Site progress – c.5,000 people working at site; major contractors have been mobilized; 87% of Piling work completed; RCC, structural fabrication – 33% complete; Tankages erection – under progress

Power plant – Erection of BTG units under progress

Financial closure achieved -Syndication launched for US$1,087mn against which a response received for c. US$2,391mn and Documentation completed

Utkal Alumina

Basic Engineering – 94% and Detailed Engineering – 60% completed

Statutory approvals – major approvals in place

Site progress – c.10,000 people working at site;

Smelter - Site Grading –55% complete; structural - under progress

Power plant – 5 boiler units, 4 ESP units, 2 power units completed, First chimney 88 m completed, second chimney 40 m completed

Financing - DFR completed, preliminary discussion with banks for financing has commenced and Banks are willing to underwrite entire fund requirement

Mahan Aluminium

Detailed Engineering – 59% completed for smelter and 25% complete for CPP

Statutory approvals – major approvals in place - Forest land stage I clearance received.

Site progress – c.10,000 people working at site;

Smelter - Site Grading –65% complete; structural - under progress. R & R houses-30 % houses completed

Financing - DFR completed, financing being launched shortly

Aditya Aluminium

Bauxite Mine & Refinery

Exchange Rate: US$1: INR46

32Hindalco Industries Limited: Investor Presentation

Update on Project : Brownfield

Nature and Scope – Expansion of the VAP facility to 600 ktpa. The expansion is expected to cost c.$300mProgress – recently conceivedProject Schedule - To be completed by Q3FY13

Pinda, Brazil

Nature and Scope – Transfer of Novelis UK can factory to IndiaProgress - 98 % dismantling completed. Containers are being dispatched and some have arrived in India. Cold and Hot Mill – orders placed with vendors (Achenbach and ABB). Site office developed for project team. Site Grading and Boundary Wall Construction in progress. 165 persons working at site.Project Schedule – To be completed by Q2FY12

FRP, Hirakud, Orissa

Smelter Expansion - Capacity increase from 161 to 213 KTPA through addition of 80 Pots of 235 kA. The plan is to expand the capacity to 360 KTPower Plant Expansion - Capacity to increase to 467.5 MW by addition of 100 MWProgress - DCPL has been engaged as the EPCM consultant . Basic Engineering by GAMI-LOT A & B –Basic Engineering documents recd. 3rdLot also in final stage. Orders placed for 100 MW turbine/generator and boilers. Enquiries for FTP, Rectifier station, PTM have been floated. Orders to be placed by end August. Site grading 80 % completed.Project Schedule - 30 pots to be commissioned by Dec’2011 & balance 50 pots by Mar’2012.

Hirakud, Orissa

HIRAKUD, ORISSAHIRAKUD, ORISSA PINDA, BRAZIL

33Hindalco Industries Limited: Investor Presentation

Project Capital expenditure and financing need

391

1,217

2,000

2,000

5,217

3,652

1,174

0

1,000

2,000

3,000

4,000

5,000

6,000

Utkal Alumina Mahan Aluminium Aditya Aluminium Total Project Finance Equity contribution

Project spending for key projects (US$mn)

70%

Exchange Rate: US$:INR 1:46

Already spent

Treasury

Post the successful QIP transaction, Hindalco is well positioned to raise additional debt for its planned projects… Hindalco has over US$1 bn in Treasury

Impressive financial performance with upward momentum in profitability

35Hindalco Industries Limited: Investor Presentation

Strong financial performance (consolidated*)

121305 332 362 413 459

2,759 2,807

3,250 3,267

3,595 3,6591,401

1,530

1,836

2,037

2,1992,122

0

1,000

2,000

3,000

4,000

5,000

6,000

Q4FY09 Q1FY10 Q2FY10 Q3FY10 Q4FY10 Q1FY110

500

1,000

1,500

2,000

2,500Sales (US$mn) EBITDA (US$mn) LME prices (US$)

4.4% 10.9% 10.2% 11.1% 11.5%

EBIDTA Margin (%)

Exchange Rate: US$1: INR46

12.5%

* Consolidated: comprises Hindalco standalone and Novelis results

36Hindalco Industries Limited: Investor Presentation

Debt Position (Consolidated)

* Hindalco Repayment Schedule includes Hindalco Standalone Debt consisting of secured loans & unsecured foreign currency loan and Novelis Loan Recourse; does not include working capital loansExchange Rate : US$1: INR 46

1011

354 3041418

61 173 234 448 763540

1,000

2,000

3,000

Debt (30 Jun 2010) 2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

Secured Loan Novelis Loan Recourse

2,631

2416 16

2,414

16145

0

1,000

2,000

3,000

Debt (30 June 2010) Within 1 yr 2 years 3 years 4 years 5 years After 5 years

US$

in m

n

Repayment schedule

US$

in m

n

Novelis

Hindalco

• Over 90% of debt back-ended

Repayment schedule*

• Repayment of Novelis loan commences in FY12

Favourable Market Outlook

38Hindalco Industries Limited: Investor Presentation

Robust world consumption for Al post rebound in 2010

2010E Consumption

Sustained robust demand for Aluminium over the next few years

Projected primary aluminium consumption by region (in MMT)

China

Europe

North America

Asia w/o China, India and Russia

Latin AmericaIndia

RussiaRest of World

14.0%

2%

0%

12%

7%

-13%

-19%

-25%

16%

6%

7%

14%

6%

9%

8%

7%

15%

3.4%

3.6%

4.6%

3.1%

4.7%

4.2%

0.4%2009 Actual2010 Forecast2011E

2009 Global demand growth rate: -4%

2010 Global demand growth rate: 11% (2010 ex-China: 8%)

2011 Global demand growth rate: 8%(2011 ex-China: 4%)

China

Europe

North America

Asia w/o China, India and Russia

Latin America

India

Russia

Rest of World

Source: Industry Reports

39Hindalco Industries Limited: Investor Presentation

50

100

150

200

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10

1 yr contango Storage + Financing cost

Robust world consumption for Al post rebound in 2010

Positive Outlook for Aluminium to continue with China and India aluminium demand consumption to outpace production

21,43423,148

25,000

20,87919,306

12,84615,025 16,115 17,600

18,93416,60514,446

2009 2010E 2011E 2012E 2013E 2014E

Production ConsumptionChina India

1,588 1,5971,439

1,563 1,636 1,712 1,755 1,7981,5501,503

1,3041,473

2009 2010E 2011E 2012E 2013E 2014E

Production Consumption

Regional Premiums close to all time highs due to paucity of aluminium in the physical markets One year contango still higher than storage costs (US$/T)

Source: Industry reports

Contango flat for last one year

0%

100%

200%

300%

400%

500%

May-09 Jul-09 Sep-09 Nov-09 Jan-10 Mar-10 May-10

Midwest Japan Europe

China was a net exporter of aluminium in June 2010 for the first time since 2008 – production was at record levels

Source: Industry reports

Source: Industry reports Source: Industry reports

40Hindalco Industries Limited: Investor Presentation

Drivers for consumption growth in India in place

Industrial 7%

Others17%

Power48%

Transportation15%

Construction13%

Robust growth outlook…

Consumption by various industry segments…

…to continue to drive Aluminium consumption

Source: Aluminium Association of India

Source: Industry reports

…is expected to continue showing robust demand

Generation capacity to increase by 68,869 MW in 2007-12

− Privatization of electricity T&D and emphasis on improving existing infrastructure to strengthen domestic aluminium demand

Increased use of aluminium in automobile and two-wheeler manufacturing to further bolster domestic demand

Underpenetration in India also augurs well for future demand

− Per capita consumption 1.1 kg in 2009 as compared 10-25 kg in developed European countries and USA

1.08 1.21 1.281.45

1.681.85

2.07

0.86 0.96

2004

2005

2006

2007

2008

2009

2010

E

2011

E

2012

E

2013

E

2014

E

9.06.7 7.2

8.49.99.4

7.5

0

4

8

12

FY05 FY06 FY07 FY08 FY09 FY10 FY11

Source: Office of Economic Advisor (India), IMF, Industry reports

Industrial Production growth (%)GDP growth (%)

8.4 8.2 11.6 8.5 2.8 10.4 9.4

41Hindalco Industries Limited: Investor Presentation

Favorable Demand outlook: Reflected in Al forward prices

2,000

2,050

2,100

2,150

2,200

2,250

2,300

Sep-10 Dec-11 Mar-13 Jun-14 Sep-15

Last Price

1.6%

-0.9%

-13.6%-13.0%

12.0%

Aluminium Copper Nickel Lead Zinc

Source: Bloomberg (August 2010)

Aluminium forward price curve (US$/t) – Steadily rising 5 year forward curve price change (Sept 2010- Nov 2015)

Aluminium continues to be the only major non-ferrous metal with a double digit forward price growth (over a 5-year time horizon)

Recovery of US/ European markets and continued robust growth in Asia/ Latin America; China to witness acceleration phase in demand for AluminiumReduced production capacity, declining global aluminum inventories growing tightness in prime and value added products Launch of physical backed Aluminum Exchange Traded Funds (ETF)Wider application of Aluminum, especially in Auto and Industrial segments

Key Drivers for Aluminium Prices

Source: Bloomberg (August 2010)

Re-rating due to visibility of growth and focused strategy in place

43Hindalco Industries Limited: Investor Presentation

Well defined Growth drivers for Hindalco

Alumina Greenfield Projects Value Added Products

Long on Alumina - from 1.5 mtpa currently to 3 mtpa in the future

Amongst the largest producers of Specialty Alumina (expanding capacity to 350 kta) globally with a 90% domestic market share in India

JV in Cameroon in place to mine bauxite and set up alumina refinery

Greenfield projects expected to be in global best quartile for manufacturing costs

Scalability of Greenfield projects to provide uptick in margins in the future

Strong EBITDA profile for new projects to improve growthfundamentals and capital structure

Expansion of the Pinda projectwould increase emerging market exposure to over c.40%

Expects to increase mix of VAP and introduce futuristic value added product’s to provide further upsides to revenues and margins

To deliver high end products in Hirakud (Project Blue Fox)

Hindalco Today

Revenue (FY10) USD 12.9bn

EBITDA (FY10) USD 1.4bn

Hindalco Tomorrow

ABG aspires to be a $65bn turnover by FY15 and Hindalco expected to be the torchbearer..

44Hindalco Industries Limited: Investor Presentation

Towards Sustainable LeadershipDomestic operations Expansion Projects Novelis

Driver

User industries of aluminum have a bullish outlook Robust sector fundamentalsLong on AluminaIntroduction of new futuristic value added products (Al)New avenues for copper use

Financial closure on track for key Greenfield projectsGreenfield projects expected to be in global best quartile for manufacturing costsInfrastructure available for further scalability in the futureBrownfield capacity increase advantage

Improving product mix to drive margins and growthSuccessful relocation of Roger StoneConvergence of EBITDA and Adjusted EBITDALeader in Al Recycling

Highlight’s

Strategy

Sustainable growth Achieve potential Stabilize and transform

Strong risk management practices in placeLeading market share in VAPContinued focus on operational excellence for both Aluminum and CopperLow cost base and robust de-risked business model

Focus on timely delivery of planned projectsMaintain high quality of executionGreenfield projects will further sharpen the competitive positioningLow capex cost per ton with best in class operating capacities

Financial turnaround with continued operational improvementLeverage on high end technologyBrownfield expansion – Pinda project, Brazil

Price Leader Cost Leader Capability Leader

Seamless Global “One Metal” business

Thank You!

46Hindalco Industries Limited: Investor Presentation

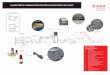

Hindalco’s Copper Operations - Focused Value Extraction in Copper

Ability to extract value from By-Products and Captive Infrastructure

Smelter

Phosphoric Acid Plant

Cu Anodes

Sulphuric Acid

RockPhosphate

Ammonia

Cu Conc.Refinery

Precious Metals Refinery

Cu Cathodes

Anode Slime

Silver(150 ktpa)

Di-Ammonium Phosphate(400 ktpa)

Gold(15 ktpa)

Phosphoric Acid

Captive All-Season Jetty Captive 135MW power plant Captive Oxygen Plant