Embed Size (px)

Citation preview

Building a prosperous and innovative Canada

AN INCLUSIVE INNOVATION AGENDA: THE STATE OF PLAY

June 14, 2016

Slow paced global growth and high volatility

Global recovery continues but fragility prevails Global growth revised down from Oct 2015: 2016: 3.2% from 3.6% 2017: 3.5% from 3.8% Low productivity growth

Emerging markets source of growth & new middle class Emerging markets will fuel nearly half of the growth through 2025 2.2 billion new middle class consumers by 2030 – cities in Asia, especially in China, will host largest markets

2

Global Forces Shaping a new context and Accelerating Change

G7 Declaration

A commitment to a low carbon economy

“Global growth remains moderate and below potential, while risks of weak growth persist”

Focus on international collaboration, domestic frameworks, and new investments in clean energy and clean technologies

Global demographic shifts underway Mass migration, aging population, vulnerabilities related to lack of inclusion & income inequality

Innovation to drive growth, improve lives of Canadians, and create jobs economy-wide

“Strengthen the global response to the threat of climate change,

in the context of sustainable development and efforts to

eradicate poverty, including by:

Holding the increase in the global average temperature to

well below 2 degree Celsius above pre-industrial levels”

Fourth Industrial revolution (e.g., digital manufacturing)

Exponential growth of connected devices By 2025 more than 50 billion connected devices in a world of 8 billion people Today 3 billion people connected to the Internet; 5 billion by 2025

No “traditional sectors” – all part of a technological transformation: manufacturing, natural resources, services

Autos a mobile platform and combination of digital, AI, software, advanced materials, fuel efficiency, manufacturing, & resources

A global INNOVATION RACE to lead in new technologies, high-end industries & capabilities

3

Disruptive technologies giving rise to a new Industrial Age

Potential economic impact of disruptive technologies in 2025 US$ trillion, annual

Innovation to drive growth – US, Germany, Australia

Targeting tech areas – UK

Prioritizing value-added industry/tech – Made in China 2025

Simplicity in support of innovation – Finland, Israel

Disruptive Tech: US$14 to $33 T by 2025 12 Technologies

Source: McKinsey, 2013

Technology changing the way people work & live, business lines & entire systems of production

The Canadian strengths and leading indicators

Solid Foundations Strong economic base

A leading open economy

A welcoming business environment

World-class research and universities

Highly educated workforce

Multicultural country, universal health care, clean, modern cities, high quality of life

4

Strengths Low inflation, interest rates, deficit

Led G7 in economic growth 2005-2014 (World Bank)

2nd most open G7 in trade and investment

Extensive market access – NAFTA, CETA

Best country in the G20 to do business – (Forbes & Bloomberg)

Lowest business tax costs G7 – 46% lower than US (KPMG)

Lowest business costs in the G7 for R&D intensive sectors

Soundest banking system in the world (WEF)

Most highly educated workforce among OECD

1st in life satisfaction G7 (OECD)

Leader in hosting international migrants – ranked 7th (UN) 70

80

90

Canada UK Germany Japan US France Italy

Social Progress Index – 2015

in the G7 and sixth overall in a 133 country study measuring social progress

Source: The Social Progress Imperative

1st

Strong “macro” conditions, yet Canada’s innovation metrics are not sufficiently world-leading

Drop in business R&D & low business sector ICT investment per-worker

Limited commercialization success

Lack of management capacity, serial entrepreneurs & anchor firms around innovation hubs

SME scale-up issues – limited participation in global markets

Need for better public-private innovation collaboration, interaction, partnerships

5

Worrying Trends Significant decline since 2001

A persistent innovation paradox

Adjusting to structural and cyclical challenges Aging of Canadians – 1 in 4 over 65 by 2031

Large oil price shock: from US$113 April 2011 to US$26 per barrel in Feb. 2016

High FDI in Canada but heavily relied on natural resources 60

65

70

75

80

85

90

95

100

1987 1992 1997 2002 2007 2012

Canadian Business Sector

Canadian Manufacturing Sector

US = 100

A widening productivity gap

0.80

1.26

1.02

0.80

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1992 1996 2000 2004 2008 2012

BERD Intensity

6

6 Areas for Action

ENTREPRENEURIAL AND CREATIVE SOCIETY

Foster a culture of innovation and entrepreneurship, build skills to embrace global changes, leverage Canada’s diversity and attract top global talent

1 GLOBAL SCIENCE EXCELLENCE

Support world-class research excellence from fundamental to applied science

2 WORLD LEADING CLUSTERS AND PARTNERSHIPS

3 Super clusters for business innovation and global reach, from idea generation to value creation

GROW COMPANIES & ACCELERATE CLEAN GROWTH

4 Develop start-ups and scale innovative, high impact small, medium and large firms, growing the next generation of job-creating global companies

COMPETE IN A DIGITAL WORLD

5 Harness the digital economy across sectors – infrastructure, broadband, ICTs, big and open data – to encourage digital adoption and strengthen competitiveness

EASE OF DOING BUSINESS

6 Enhance and align agile marketplace regulations and standards, enable market access so Canadian businesses can thrive globally

Globally connected and

competitive Canadian

companies creating value

and jobs for the middle class, including in

clean technology,

health sciences, advanced

manufacturing, digital

technology, resource

development and agri-food

Mobilizing Canadians for an Inclusive Innovation Agenda

Entrepreneurial and Creative Society

Canada has strengths in its people

7

Foster a culture of innovation and entrepreneurship, build

skills to embrace global changes, leverage Canada’s diversity and

attract top global talent

An environment conducive to entrepreneurship

2nd in Global Entrepreneur Index in 2015 Top 5 in access to training to start a business (OECD) Niches of social enterprises providing sustainable social solutions

A highly educated population

Highest percentage of population with a tertiary degree (54%) in the OECD Doubled the number of science and engineering PhDs per 100,000 population from 2006 to 2012 – 19th place to 17th Attracting top talent from abroad

10th in country capacity to attract talent (WEF) 3rd in foreign born doctorate holders (OECD) 8th most popular destination for international students Recognized for having world-leading researchers at Canadian universities

1

Canada has a long history of innovation— technological, SOCIAL, economic, CULTURAL and

political. Indeed, Canada itself has been called a bold experiment in DIVERSITY and MULTICULTURALISM.

We’re not two years shy of our 150th birthday by accident. We didn’t get here by revolution or upheaval,

but neither have we clung unduly to the status quo.

The Governor General of Canada His Excellency the Right Honourable David Johnston

June 9, 2015

Entrepreneurial and Creative Society

There are skills and competency gaps Youth scores continue to drop in each cycle for all indicators

7th in reading (6th in 2009) 13th in math (10th in 2009) 10th in science (8th in 2009)

48% of Aboriginal people had a PSE compared to 65% of non-Aboriginal Lower proportion of women enrolment in STEM

Experiencing signs of skills mismatches between competencies needed and qualifications

Poor performance in over-qualification and under-qualification in jobs (selected OECD countries)

OECD PISA Scores for Canada 2000-2012

Gaps in equity of education

8

Canada has a larger proportion of adults at the lowest proficiency levels in all three skill levels compared to OECD average

Improve performance on the skills of tomorrow - Digital skills needs

Bottom 5th in adults with ICT and problem solving skills with tertiary degrees (OECD)

510

515

520

525

530

535

540

2000 2003 2006 2009 2012

Math

Reading

Science

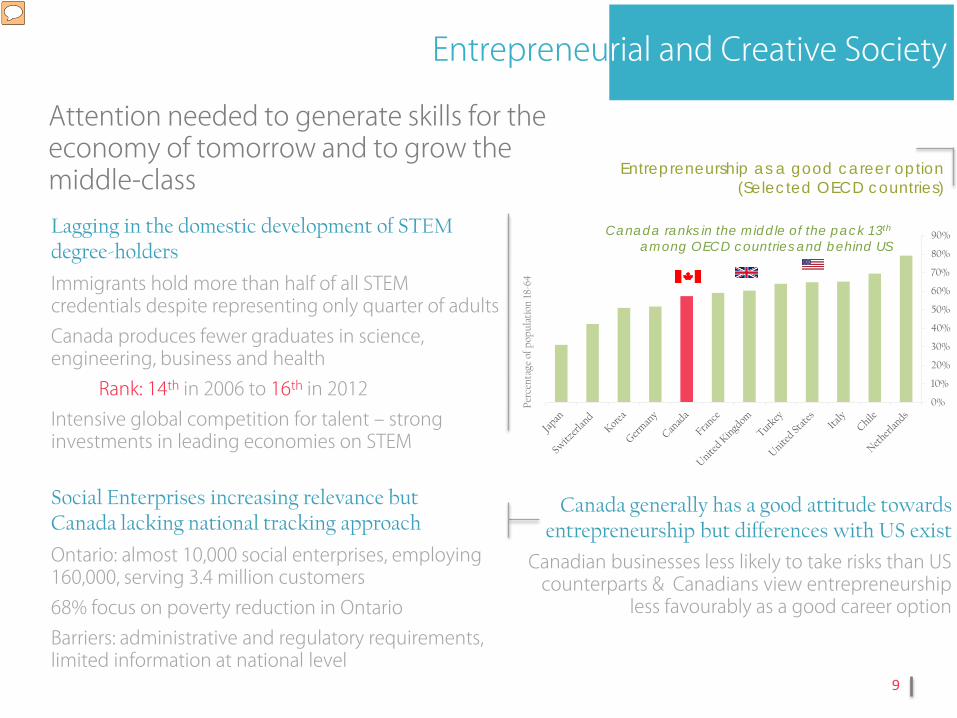

Canada generally has a good attitude towards entrepreneurship but differences with US exist

Attention needed to generate skills for the economy of tomorrow and to grow the middle-class Lagging in the domestic development of STEM degree-holders

Immigrants hold more than half of all STEM credentials despite representing only quarter of adults Canada produces fewer graduates in science, engineering, business and health

Rank: 14th in 2006 to 16th in 2012 Intensive global competition for talent – strong investments in leading economies on STEM

9

Entrepreneurial and Creative Society

Social Enterprises increasing relevance but Canada lacking national tracking approach

Ontario: almost 10,000 social enterprises, employing 160,000, serving 3.4 million customers 68% focus on poverty reduction in Ontario Barriers: administrative and regulatory requirements, limited information at national level

Canadian businesses less likely to take risks than US counterparts & Canadians view entrepreneurship

less favourably as a good career option

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

Perc

enta

ge o

f pop

ulat

ion

18-6

4

Entrepreneurship as a good career option (Selected OECD countries)

Canada ranks in the middle of the pack 13th among OECD countries and behind US

THE COMMONWEALTH SCIENTIFIC AND INDUSTRIAL RESEARCH ORGANISATION INNOVATION FUND co-invests in spin-offs from researchers involved with the government, universities, or other publicly funded research bodies. The private sector also contributes investment to the fund. (A$70M) INSPIRING ALL AUSTRALIANS IN DIGITAL LITERACY AND STEM is a measure in the Innovation Strategy that has ten sub-initiatives. Some of these initiatives include: Little Scientists (A$4M) engages children with fun experiments, Let’s Count(A$4M) engages parents and children in early concepts of mathematics, Early Learning STEM Australia (A$6M) is a series ofapps to foster interest in science, Massive Open Online Course to teach teachers digital literacy, Peripatetic (travelling) ICT teachers for one term ICT lessons in disadvantaged schools, and a series of science/coding competitions. (A$65M)

Entrepreneurial and Creative Society

10

International examples

AUSTRALIA

UNITED KINGDOM

SOCIETY CAPITAL supports charities and social enterprises with affordable financial support to grow their social impact. Itoperates on ROI model and has ten areas of focus. The Big Society Trust was set up using funds that had been dormant for fifteen years or longer. Over five years Big Society Capital will be capitalised with £600 M from dormant bank accounts and four UK banks.

ICURE PILOT PROGRAMME (based on US I-Corps) offers university researchers with commercially promising ideas up to£50,000 to ‘get out of the lab’ and validate their ideas in the marketplace. (£3.2M)

INNOVATION CORPS provides entrepreneurship training for federally-funded scientists and engineers by pairing them up withbusiness mentors to test their business models. (US$30M, 2016) STEM MASTER TEACHER CORPS is designed to increase the number of STEM teachers in school districts that have historicallynot done well in STEM. It aims to have 10,000 Master Teachers by 2017. (US$1B) CHALLENGE.GOV includes technical, scientific, and creative competitions where the US government seeks innovative solutionsfrom the public for social innovations. Since 2010, over 600 competitions have been launched, over 250,000 people participated. (US$220M has been awarded) SOCIAL INNOVATION FUND combines public and private resources to grow promising community-based solutions for threepriority areas: economic opportunity, healthy futures, and youth development. It provides US$1-5M grants annually for up to fiveyears. In its first two years it allocated US$95M, leveraged an additional US$250M of private funds, and supported 150 projects in100 cities.

UNITED STATES

11

Global Science Excellence Support world-class research excellence from fundamental to applied science

Canada has strengths in science performance

Life sciences and biomedical research & technologies Environmental sciences & technologies Energy sciences & technologies ICT research and technologies

Strong capabilities & breakthroughs in key fields

World-leading education and universities

1st in the OECD for overall spending in higher education at 3% of GDP (OECD) 3rd for the number of universities in the top 30 university rankings – top cited publications (OECD) Top 4 among OECD countries in fields such as psychology, neuroscience and economics (OECD)

Global recognition of research

9th in top cited publications among OECD countries* 6th in the Thomson Reuters’ 2015 rankings of the most highly cited researchers**

Dr. Arthur McDonald (Canadian) won the 2015 Nobel Prize in Physics. His work tracking neutrinos from the sun is a discovery that changes the basic understanding of physics

The National Microbiology Lab in Manitoba created the first Ebola vaccine for humans, a discovery that will save millions of lives

World leading discoveries in glioblastoma, one of the most

deadly and difficult to treat brain cancers

2

* Top 10 % highly cited publications ** Top 1% highly cited publications

Declining investment in knowledge production and diffusion

Canada’s higher education R&D intensity has been declining and is at the same level as in 2003 – competitors increasing investments

7th* in 2014 from 3rd in 2006 – higher education R&D expenditure as % GDP (OECD) 22nd on government performed R&D (0.15%) in 2014 below OECD average (0.26%) (GOVERD)

12

Global Science Excellence

0.45

0.68 0.71

0.65

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

Canadian businesses not sufficiently commercializing S&T and innovation research

Canada last in G7 countries for share of triadic patents** Universities lagging US counterparts in patents issued, licences executed and new start-ups Lower percentage of researchers in the business sector (OECD countries) 12th in the percentage of researchers working in the business sector 22nd in absorbing talent in 2012 out of 43 countries

Much of Canada’s post-secondary institutions (PSI) and federal labs infrastructure needs to be modernised

Canada’s Higher Education R&D Intensity (as a % of GDP)

*Ranking data is 2014 or latest available** Patents filed in Japan, Europe, and US

Lower number of university graduates in key disciplines and a gender gap

Dropping in the generation of university graduates in key disciplines

20th (from 11th in 2006) of 27 countries in 2012 in engineering grads per 100,000 of population 9th of 27 countries in 2012 in science grads per 100,000

13

Global Science Excellence

Fewer women pursuing science & engineering fields of studies

20th out of 28 countries in share of female Canadians science & engineering PhD graduates 17% of scientific publication authored by women in Canada – US 24%

Even though Canada doubled the number of science & engineering PhDs per 100,000 population from 2006 to 2012, Canada lags leading OECD countries (e.g., Germany, Australia, UK)

World-leading research excellence will continue to be a critical foundation to innovation performance

Australia’s National Innovation & Science Agenda will spend A$1.1 billion 2016-19

The UK’s Science & Innovation Strategy will spend £6 billion 2014-21

The President’s 2016 Budget proposes US$67 billion for applied research

Finland allocated €1.8 billion to R&D in 2016-17

China - the OECD projects that funding of R&D will surpass the US by 2019

14

Global Science Excellence

THE ISRAEL SCIENCE FOUNDATION is Israel's predominant source of competitive grants for funding basic research. Itpromotes science excellence and basic research. It focuses on sciences and technology, life sciences and medicine, and humanities and social sciences. ($213M, 2015) LIFE SCIENCES FUND promotes and accelerates the growth of Israel’s Biotechnology industry, an area in which Israelpossesses a competitive advantage but the private sector considers high risk. ($220M) KAMIN serves as an additional bridge between pre-commercial research and industrial research. KAMIN offers theopportunity for academic groups whose research is no longer eligible for basic research funds to continue in their work for up to two years. Grants may be 85 to 90 percent of the approved budget and the remainder of the R&D costs are to be borne by the research institute.

ISRAEL

UNITED KINGDOM

THE GLOBAL CHALLENGES RESEARCH FUND supports cutting-edge research to address problems faced by developingcountries. The fund is administered through delivery partners including the Research Councils and national academies. (£1.5B over 5 years)THE INTELLIGENT MOBILITY FUND will provide £50-100M into early-stage innovations, focusing on transportation ofthe future. It aims to turn Britain into the “smart transport Silicon Valley”.

THE NEWTON FUND aims to develop science and innovation partnerships that promote the economic development andsocial welfare of partner countries. The Fund focuses on building innovation and science expertise, creating research collaborations, and developing innovation solutions to development problems. (£735M 2014-21 / partner countries match the resources) WORLD-CLASS LABORATORY CAPITAL is for maintaining and refreshing existing UK science infrastructure. It isallocated to partners to be spent at their discretion, to retain the UK’s global science excellence. (£3B 2016-21) THE EIGHT GREAT TECHNOLOGIES INITIATIVE supports areas of science strengths in the UK. They are big data andenergy-efficient computing, satellites and commercial applications of space, robotics and autonomous systems, synthetic biology, regenerative medicine, agri-science, advanced materials and nanotechnology, and energy. (£600M, 2012)

International examples

15

SWEDISH RESEARCH COUNCIL funds basic research in natural sciences, technology, medicine, the humanities andsocial sciences. (SEK 5.5B, 2014) SWEDISH RESEARCH COUNCIL FOR ENVIRONMENT, AGRICULTURAL SCIENCES AND SPATIAL PLANNING (FORMAS) supports basic and needs-driven research in the fields of environment, land-based industries and spatialplanning. (SEK 1.12B, 2014) SWEDISH RESEARCH COUNCIL FOR HEALTH, WORKING LIFE AND WELFARE (FORTE) supports and initiates basicand needs-driven research in the fields of the labour market, work organisation, work and health, public health, welfare, the social services and social relations. (SEK 512M, 2014) SWEDISH GOVERNMENTAL AGENCY FOR INNOVATION SYSTEMS (VINNOVA) funds needs-driven research in thefields of technology, transport, communications and working life. (SEK 2.4B, 2014)

SWEDEN

NORWAY

BIOMEDICAL RESEARCH INVESTMENT The Norwegian Research Council announced in 2015 four largeinvestments in biomedical research. The investments will focus on supporting research in sequencing and precision medicine, national biobanks, brain research and clinical research. (NOK 255 M)

International examples

Global Science Excellence

Nanotechnology, additive manufacturing, energy storage, autonomous vehicles, robotics, regenerative medicine, genomics, quantum computing, big data analytics, advanced materials

World Leading Clusters and Partnerships

16

Super clusters for business innovation and global reach,

from idea generation to value creation

3 Canada has important clusters and regional innovation Leading clusters in key economic sectors

Automotive – ON represents the 2nd largest automotive producing region in North America – 5 OEMs, 11 vehicle assembly lines in 8 assembly plants, 3 engine plants, over 730 auto parts suppliers and a network of research and facilities Aerospace – Montréal region one of the 3 leading aerospace hubs along with Seattle and Toulouse with OEM, leading suppliers & research institutes ICT – Waterloo region a leading cluster in North America home to 1,000 technology companies, leading universities, developing and attracting top talent – one of the world’s top regions for tech start-ups Life science – Presence across Canada – BC home to one of the largest biotech sectors in North America with the University of BC ranking in the top 10 in North America for patentable research Food Processing – 2nd largest manufacturing industry in Canada - $2 billion annually in capital expenditures Energy & natural resources – large and diverse resources throughout Canada – lead energy research in AB, agri-food in SK, clean water technology in ON, cleantech BC, ON, QC, Atlantic Canada

Transformative technologies reinvigorating industrial capabilities

– Enhances regional and industryperformance, including job creation,

innovation, and new business formation

Geographic concentrations of interconnected companies, suppliers,

service providers, firms in related industries, & research institutions – They

compete but also cooperate

CLUSTERS

Canada could improve in partnerships and in business-led clusters

Canada’s ranking in the state of cluster development is declining

20th in 2015 from 16th in 2008 Germany 3rd (2015) from 10th (2008) UK 8th (2015) from 15th (2008)

17

More partnerships needed between research facilities and industry - building critical mass

Limited success in attracting new R&D from MNEs* - % of BERD funded from foreign-owned constant over last 5 years (around 35%) 9th in OECD in HERD funded by business (behind Korea and Germany)

World Leading Clusters and Partnerships

Canada’s top 25 firms’ expenditures in R&D are declining

Last among G7 countries in the number of firms in the top 1000 global R&D firms with only 10

*Multinational Enterprises

18th in 2013 OECD countries

Number of triadic patents per million population

19th in 2015 fell from 7th in

2010

WEF ranking of countries with extensive university-industry R&D collaboration

9th in 2013 Government funding of business R&D (OECD) 4th indirect support 25th direct support

Need for balance – more than 85% of government support to business R&D is indirect

18

World Leading Clusters and Partnerships

Business sophistication requires higher levels of R&D investment and partnerships

29th in terms of high-tech exports as a % of total trade (Global Innovation Index – 2015) Last in G7 countries in the export of ICT (OECD)

Canada not well-integrated into global value chain

Canada ranked among the lowest in terms of its GVC participation – last among G7 countries (OECD - 2009 latest data) Canada’s GVC participation driven by primary inputs – need to complement with higher end products and services

Canada not leading in value chain participation, business innovation & high-tech exports

Low levels and ranking in high tech exports

23rd in capacity to innovate (WEF) 29th in firm-level technology absorption (WEF)

Relatively small market size – less attractive to test technologies High BERD-intensive sectors are in decline Heavy reliance on tax incentives to incentivize business R&D Need for experienced TALENT to drive and manage growth – a race for talent Limited density & capabilities

The Landscape

Building Capabilities through Clusters and Partnerships

Build CRITICAL MASS and enhance commercialization outcomes

Create self-sustaining technical centres of excellence and strengthen value chains

Bring the best talents and capabilities from the public and private sector

Proving ground for cutting-edge technology testing & application

19

World Leading Clusters and Partnerships

NATIONAL NETWORK FOR MANUFACTURING INNOVATION scales up advanced manufacturing technologies andprocesses. The initial network consists of 15 institutes targeting key technologies and it aims to expand to 45 by 2024. The government has provided an initial investment of US$600M, which has been met by nearly US$1.2B of private investment.Each institute is unique and led by experts in the field. The institutes have attracted over 800 companies, universities, and non-profits as members of the National Network for Manufacturing Innovation.

ENERGY REGIONAL INNOVATION CLUSTERS PROGRAM in which the DOE is leading six other federal agencies to help USregions develop innovation zones. Regions compete for funds.

REGIONAL INNOVATION STRATEGIES PROGRAM creates and expands cluster-focused proof-of-concept andcommercialization programs and early-stage seed capital through the i6 Challenge and the Seed Fund Support (SFS) Grant competition. (US$15M)

UNITED STATES

International examples

FRAUNHOFER SOCIETY undertakes applied research with the objective to reinforce the competitive strength of the regionaland national economies. Fraunhofer aims to promote innovation, accelerate technological progress, disseminate knowledge and help to train the future generation of scientists and engineers, providing a conduit to link governments, industry and research institutes. Fraunhofer carries out research in hundreds of technology fields and makes the results available as patents, licenses, and in the form of research projects commissioned by industry. More than 70 percent of Fraunhofer’s contract research revenue is derived from contracts with industry and from publicly financed research projects. (€2.1B annually) GERMANY

CATAPULT CENTRES are a network of centres designed to transform the UK's capability for innovation in specific areas andhelp drive future economic growth. The UK's businesses, scientists and engineers work side by side on late-stage R&D. Each Catapult Centre specialises in a different area of technology. The centres focus on: cell and gene therapy, compound semiconductor applications, digital, energy systems, future cities, high value manufacturing (a network of another seven centres), medicines discovery, offshore renewable energy, precision medicine, satellite applications, and transport systems. The centres are funded by core public funding, private contracts, and public-private partnership projects. The government aims to have 30 Catapults by 2030.

KNOWLEDGE TRANSFER NETWORKS were established to foster better collaboration between science, creativity andbusiness. The KTN program has specialist teams covering all sectors of the economy – from defence and aerospace to biotechnology and robotics. KTN has helped thousands of businesses secure funding to drive innovation.

UNITED KINGDOM

20

STARTUP DELTA works with the 13 innovation hubs in the Netherlands to create one single hub. It tackles capital, talentand networking problems that hinder growth of startups. It is comprised of people from across government, enterprise and research community.

NETHERLANDS

International examples

INNOVATION CONNECTIONS INITIATIVE drives industry-led collaborations between researchers and SMEs. TheInitiative matches grants to support graduate and postgraduate research placements in businesses, matches grants for industry researchers to be placed in publicly funded research organizations, and identifies opportunities to access R&D testing facilities and training. (A$18M) AUSTRALIA

IRELAND

GREEN WAY is a cleantech cluster in Dublin. This cluster brings together the public sector, academia,industry and consumers, to stimulate clean-economic growth. According to EY, Cleantech has the potential to boost Irish GDP by between €2.4B and €3.9B by 2020, while adding up to 80,000 jobs in the process. Thecluster was founded by a group of municipalities, higher education institutes and industry representatives. Its network has expanded to include multinational organizations, and is connected to clusters in San Jose, Silicon Valley, and Beijing.

World Leading Clusters and Partnerships

Grow Companies & Accelerate Clean Growth

21

Develop start-ups and scale innovative, high impact small,

medium and large firms, growing the next generation of job-creating global companies

4 Growth and job creation is about firms and their pathway to success

SMEs contribution to jobs and exports is significant

SMEs account for 90% of private sector employment and for 99% of businesses – 1.1 million enterprises 10% of SMEs exported goods or services (2011), accounting for 40% of exports

Leading exporter among OECD countries

4th of 24 OECD countries in average value of exports by enterprise

An improving venture capital market

Canada’s start-up rate higher than in the US

3rd among OECD countries in terms of the value of VC investments relative to GDP, lagging only to Israel and the US

Significant expertise & potential in clean technologies

Growing and active clean technologies firms

Cleantech companies (almost 800) employ more than 50,000 and about 80% of them export (Analytica Advisors) Canada’s cleantech industry revenue over $11 billion in 2014 (Analytica Advisors) 7th in Cleantech Innovation Index 62% of Canada’s electricity generation from renewable sources 4th (OECD) – Government R&D budget spent on energy and the environment (11.3%)

76.9% 75.6%

10% 8.5%

7.5% 10.0%

5.7% 5.9%

2007 2015

us

EUROPE

ASIA OTHERS

us

EUROPE

ASIA OTHERS

22

Grow Companies & Accelerate Clean Growth

Canada has proportionally fewer large firms, with fewer employees and lower revenues

More SMEs need to grow into larger globally oriented firms

Top 100 Canadian firms were responsible for more than 60% of exports in 2012; this compares to less than 40% in France, Germany, and the US

While Canadian VC is high, the average deal size still significantly lags the US – less than half

These smaller deal sizes may not be sufficient for companies in later stages looking to scale up Canadian VC is more heavily weighted in seed/early stages than many other countries – less on scale-up 13th in the contribution of later stage VC financing to total VC financing

Canadian Merchandise Exports

Only 83 firms with revenue in the range of $500 million to $999 million 169 companies in the billion-dollar range

Constant dependence on US market with limited footprint in emerging markets

Source: Statistics Canada

0% 1% 2% 3% 4%

Canada

United Kingdom

France

OECD Average

Germany

United States (2013)

Denmark

Switzerland (2012, 2004)

Sweden

Finland

Japan

Korea

Israel

2014

2006

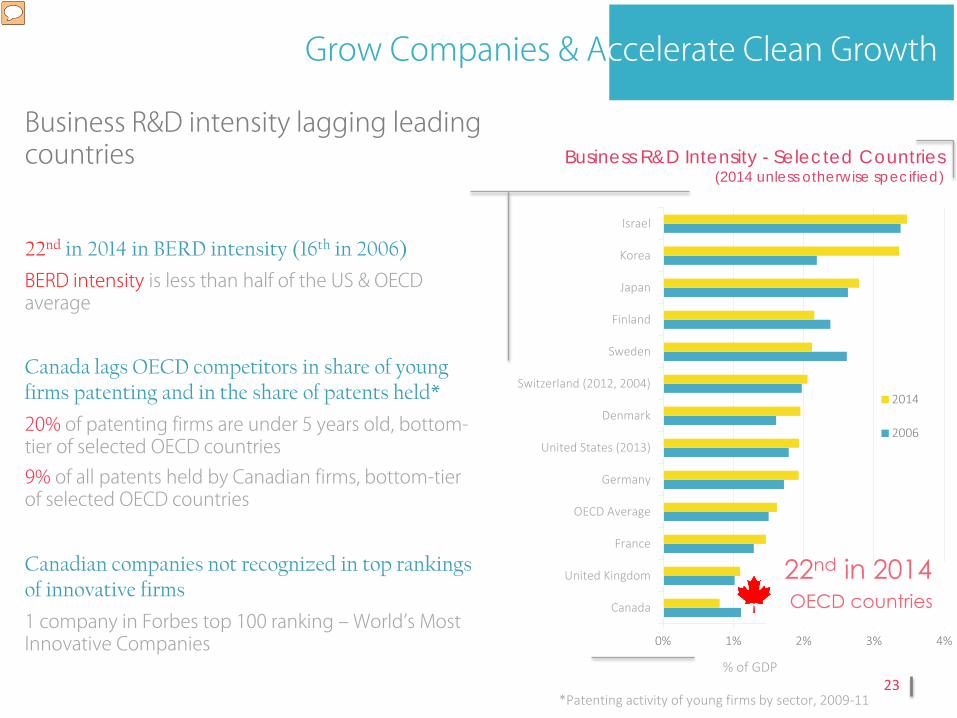

Business R&D intensity lagging leading countries

22nd in 2014 in BERD intensity (16th in 2006)

BERD intensity is less than half of the US & OECD average

23

Business R&D Intensity - Selected Countries (2014 unless otherwise specified)

22nd in 2014 OECD countries

% of GDP

Grow Companies & Accelerate Clean Growth

Canada lags OECD competitors in share of young firms patenting and in the share of patents held*

20% of patenting firms are under 5 years old, bottom-tier of selected OECD countries 9% of all patents held by Canadian firms, bottom-tier of selected OECD countries

Canadian companies not recognized in top rankings of innovative firms

1 company in Forbes top 100 ranking – World’s Most Innovative Companies

*Patenting activity of young firms by sector, 2009-11

24

Key competitors speeding up investment

Canadian cleantech firms face steep competition

China’s strategy to deploy cleantech across its economy has provided start-ups with a burgeoning market, preferential corporate tax rates and easy access to loans at low interest rates through the country’s state-owned development bank

Need to expand Canadian cleantech global presence

1.3% of cleantech global market share in 2014, a drop from 2.2% in 2005 (Analytica Advisors) Among the top 25 exporters, Canada’s global ranking fell from 14th to 19th (Analytica Advisors) 18th in 2014 in cleantech specific drivers (WWF)

Canada is last among G7 countries

0%

10%

20%

30%

Japan UnitedStates

Germany France UnitedKingdom

Italy Canada

Economies’ shares in environment-related patents, percentages, 2010-13

Source: OECD

Grow Companies & Accelerate Clean Growth

25

SMALL BUSINESS INNOVATION RESEARCH program encourages domestic small businesses to engage in federal R&D that hasthe potential for commercialization. It aims to stimulate technological innovation, meet US R&D needs, encourage entrepreneurship with socially and economically disadvantaged persons, and increase private sector commercialization. SBIR provides up to US$150,000 over six months for an organization to establish technical merit, and commercial potential. Successful companies may qualify for up to US$1M over two years to continue R&D.

ADVANCED RESEARCH PROJECTS AGENCY-ENERGY advances high-potential, high-impact energy technologies that are tooearly for private-sector investment. ARPA-E empowers America’s energy researchers with funding, technical assistance, and market readiness. It focuses on early-stage technologies from academia, industry, national labs, start-ups and small businesses. ARPA-E provides US$2-3M on average to each project and has supported over 400 projects.

ENERGY INNOVATION HUBS are integrated research centres combining basic and applied research with engineering toaccelerate scientific discovery in critical energy issues, such as nuclear reactors, solar, energy efficiency and storage and critical materials. (US$366M, 2010)CLEAN TECHNOLOGIES VOUCHERS are being provided by the DOE so that SMEs can use national labs and bring the nextgeneration of clean technologies to market. Each voucher is worth between US$50,000 and $300,000. (US$20M)

UNITED STATES

BRITISH BUSINESS BANK’S ENTERPRISE CAPITAL FUND partners with private venture capital firms to invest in high growthSMEs. This practice encourages VC firms to invest in SMEs. The Bank is owned by the UK government and has over £400M available to invest.

BRITISH BUSINESS BANK’S VENTURE CAPITAL CATALYST FUND for late stage venture capital funds to help banks beginmaking investments. This program was established in response to the 2008 financial crash. It has committed £71M in eightportfolios so far (e.g., cloud computing, mobile devices, B2B software, life sciences, Fintech and business analytics).

GROWTH HUBS are local public-private partnerships, led by the Local Enterprise Partnerships. They connect national and localbusiness to support start-ups and their scale. The UK has 39 hubs across the country. (£24M allocated for support over next two years) UK SMALL BUSINESS RESEARCH INITIATIVE (SBRI) The UK SBRI was established in 2001 with the goal to replicate thesuccess of the US SBIR in stimulating innovation and R&D. The UK program offers opportunities for SMEs to develop and demonstrate technology to public bodies. The UK increased the budget for SBRI to £100M in 2013/14 and to £200M in2014/2015.

UNITED KINGDOM

International examples Grow Companies & Accelerate Clean Growth

26

GERMANY

ENERGIEWENDE is the transition by Germany to a low carbon environment with an affordable energy supply. Goals ofthe transition include GHG reductions of 80–95% and a renewable energy target of 60% by 2050. Germany spends €1.5Bper year on energy research to solve the technical and social issues raised by the transition.

STRATEGIC ENERGY PLAN & FEED-IN TARIFF FOR RENEWABLE ENERGY sets out a support scheme to expand renewableenergy sources. In addition, the plan outlines a roadmap and measures for dissemination of innovations in cleantech across 37 technology areas and policy measures (collaboration, regulation reform, taxes & subsidies) to help support the development of the technologies through their lifecycle (present until 2050). JAPAN

DENMARK

STATE OF GREEN initiative aims to have Denmark independent of fossil fuels by 2050. It is a public-private partnershipfounded by the Danish Government, the Confederation of Danish Industry, the Danish Energy Association, the Danish Agriculture & Food Council and the Danish Wind Industry Association. It is focused on promoting and investing in 10 green sectors (e.g., sustainable transportation, solar & renewables, water, energy efficiency, and “intelligent energy”).

ENOVA is a public enterprise under the Ministry of Petroleum and Energy. Enova works with public and private enterprises to reduce consumption and increase power generation from renewable resources. Its objectives are to develop and introduce new energy and climate technologies in the market; create more efficient and flexible uses of energy; increase use of other energy carriers than electricity and natural gas for heating; increase use of new energy resources, including energy recovery and bioenergy; improving the functionality of markets for energy-efficient and environmentally friendly solutions, increase awareness in society of environmentally friendly solutions; and reducing greenhouse gas emissions in the transportation sector. To support these goals, in 2015, Enova supported 1,735 projects, which had an energy impact of 1.8 Terawatt hours and costs. (NOK 2.6B)

NORWAY

International examples

Grow Companies & Accelerate Clean Growth

Compete in a Digital World

27

Harness the digital economy across sectors – infrastructure, broadband, ICTs, big and open

data – to encourage digital adoption and strengthen

competitiveness

5 A well connected Canada with world-class digital infrastructure Most Canadians have access to some form of broadband and basic broadband coverage

94% of households have coverage at speeds of 5 Mbps 71% of households have access to speeds of 100 Mbps or faster 88% of Canadians and 98% of Canadian businesses are connected to the Internet Leading digital expertise, companies, and knowledge creation across Canadian cities and universities

Waterloo’s Quantum Valley is world leading, encompassing $100M+ investment fund for quantum technologies and state of the art R&D facilities, attracting top researchers – Perimeter Institute, the Institute for Quantum Computing, and Institute for Nanotechnology World leading companies in cyber security, technologies and services Capabilities in big data analytics (e.g., IBM), quantum computing, cloud technologies, robotics, AI

Leveraging skilled immigrants and providing economic opportunities

40% of ICT jobs are held by immigrants 2.7% unemployment rate for ICT immigrant professionals – in contrast to 7.2% unemployment for the total immigrant population 15+ (Digital Adoption Compass)

In 2014, Canada was the top export market for US computing services exports – US$4.4B of cloud computing services to Canada (US BEA)

$2,188

$4,279

$-

$1,000

$2,000

$3,000

$4,000

$5,000

Canada United StatesU

.S. D

olla

rs

28

Compete in a Digital World

Investment in ICT is low compared to competitors

Signs of concerns related to digital adoption and skills

Inadequate technology adoption

ICT investment per worker was 51% of that in the United States in 2013

Canada lagging in private sector investment per worker vis-à-vis the US on machinery and equipment and ICT 13th in ICT investment / GDP at 2.2% in 2013 – investment intensity was 70% of that of the top 5 performers (OECD) 48% of large firms are adopting big data in Canada compared to 76% in world (IDC 2012) Many SMEs not investing in cyber security technologies and services despite concerns

Need for skills and talent

Canada’s big data analytics talent gap estimated at 10,500-19,000 in 2014 (the Big Data Consortium) 20th as a share of data specialist in the economy (OECD) 40% of IT companies found it difficult to recruit professionals (CIRA)

Source: CSLS

29

Urban centres well connected but rural and remote areas not so much

Canada not fully maximizing online economic opportunities with a digital divide

97% of Canadians living in large population centres have access to 50-99 Mbps internet but only 26% in rural areas (CMR 2015) 26th in the OECD in wireless broadband subscriptions per 100 inhabitants

Not maximizing online opportunities

Internet’s contribution to the economy was 3% in Canada compared to 4.1% across the G20 (BCG) 77.5% of businesses have a website – 16th in the OECD (OECD)* 89% of Canadian SMEs do not sell their product or service online (CIRA) 20th in the OECD with 49.5% of individuals making online purchases 49% of IT companies are not equipped to compete globally (CIRA)

Compete in a Digital World

Infrastructure investments needed to facilitate high-speed corridors, support disruptive technologies and increasing usage

Declining performance – Top Global Exporters ICT Services (% of total exports)

0% 5% 10% 15%

ITA

CAN

ESP

SWE

BEL

NLD

FRA

CHN

GBR

USA

DEU

IND

IRL

Computer and information Communication

Canada 12th out of 37 countries in 2013 in % share of world ICT services exports from 7th in 2001 China has risen to 6th in the world in 2013 from 20th in 2001

*OECD does not include businesses with less than 10 employees

30

Compete in a Digital World

DATA61 is the largest data innovation group in Australia and supports a network of academia, corporations, startups, government agencies, investors and entrepreneurs. It researches big data and analytics; cybersecurity; imaging and visualisation; robotics, autonomous systems and sensing platforms; wireless and networks; data for decisions; and software engineering and UX design. (A$75M) DIGITAL MARKTPLACE was established to help ICT SMEs compete for contracts as the Marketplace breaks down tenders into individual components that are more manageable for SMEs to deliver. (A$5B a year)

AUSTRALIA

BROADBAND INFRASTRUCTURE investment over the next six-to-ten years for telecommunications carriers to build high-speed networks that will expand broadband to millions of rural residents. (US$9B) SMART CITIES initiative to invest in creating test beds for “Internet of Things” applications and developing new multi-sector collaborative models, collaborating with the civic tech movement and forging intercity collaborations, leveraging existing Federal activity, and pursuing international collaborations. The Department of Transportation has also pledged US$40M to help one city to fully integrate innovative technologies into its transportation network, such as self-driving cars, connected vehicles, and smart sensors. (US$160M) NETWORKING AND INFORMATION TECHNOLOGY RESEARCH AND DEVELOPMENT PROGRAM is a multi-agency effort for the coordination of US investment in ICT research. The program aims to accelerate progress in the advancement of computing and networking technologies and to support leading edge computational research in a range of fields, including, high-end computing systems and software, networking, human-computer interaction, health IT, and cybersecurity. (US$4.1B, 2015) OPEN DATA POLICY was established to increase public access to high value datasets in order to promote growth.

UNITED STATES

ICT FOR EVERYONE DIGITAL AGENDA is a set of policy objectives aimed at embedding the internet and digital technologies and skills across the population. Four strategic areas at an overarching level have been developed based on the perspective user: easy and safe to use, services that create benefit, the need for infrastructure and the role of ICT in societal development. Actionable items include, developing world class ICT infrastructure, promoting e-skills, empowering those with little exposure to ICT technologies, developing new digital services for businesses and citizens, and studying the impacts of ICT on societal development.

International examples

SWEDEN

31

International examples

GERMANY

HIGH TECH STRATEGY aims to accelerate scientific discoveries and their practical application to strengthen growth and prosperity. One area of the strategy, the digital economy and society commits Germany to: promoting the development and testing of innovative services, using big data technologies, provided by and for medium-sized enterprises, launched the “Trusted Cloud” initiative, an effort to promote innovative, secure and legally conformal cloud-based solutions, construction and expansion of complete coverage high-performance broadband networks, support the science sector in successfully managing the digital transformation, to strengthen digital scientific information infrastructure, and promote greater use of digital media in education and throughout people‘s entire lives. (€11 B – for entire strategy) DIGITAL AGENDA aims to guide the ongoing process of digitization. The agenda focuses on three core objectives: support the nationwide expansion of high-speed networks; enhance digital media literacy; and improve the security and safety of IT systems and services. The Agenda outlines seven measures for action, some of which include: digital infrastructure, the digital workplace, digital government and data protection.

INDUSTRIE 4.0 is a strategy aimed at developing the future of manufacturing, one where smart factories use information and communications technologies to digitise their processes. The aim of Industrie 4.0 is for German companies to maintain complete control over their entire value creation chains and related production processes. To achieve these ambitious goals, the German government is investing in research across government, academia, and business. (€200M)

5G STRATEGY was mentioned in the UK’s 2016 Budget. It commits the government to develop a strategy that would make the UK a world leader in the development of 5G by 2017. (£30M) GOVERNMENT DIGITAL STRATEGY sets out how the government will become digital by default, where many transactional and non-transactional services will be offered online by default. The strategy aims to improve departmental digital leadership, develop digital capability throughout the civil service, redesign transactional services to meet a new Digital by Default Service Standard, broaden the range of those tendering to supply digital services (including SMEs), remove unnecessary legislative barriers, and help third party organisations create new services and better information access for their own users by opening up government data and transactions.

DIGITAL ECONOMY STRATEGY aims to support innovative business projects and for digital companies to seize opportunities. The strategy also supports the Digital Catapult centre, the Open Data Institute and Tech City UK. (£30M) INSTITUTE ON CODING & COMPETITION will help in educating young people how to code more securely by having security principles built into their training. (£20M)

UNITED KINGDOM

Compete in a Digital World

Ease of Doing Business

32

Enhance and align agile marketplace regulations and

standards, enable market access so Canadian businesses can

thrive globally

6 Canada is globally recognized for its stability, rule of law and fiscal virtues

A world-leading business environment

2nd on Bloomberg’s best countries for business 3rd by the World Bank for time to start a businesses 3rd by the World Bank for ease of starting a businesses 7th in the OECD for low administrative burdens on start-ups

Strong foundations for innovation and competitiveness with strong IP protection, banks and market openness

1st in the OECD on the Global Competitiveness Index (GCI) for soundness of banks (WEF) 2nd in the G20 on the International Chamber of Commerce’s Open Market Index 8th in the OECD on the GCI for effectiveness of its taxation on incentives to invest 9th in the OECD on the GCI for IP protection

33

Canada international rankings on FDI procedures and rules have room to improve

There are global perceptions in need of response and branding

31st in FDI restriction index 2015 (OECD) 18th in product market regulation (OECD) 52th for the business impact of rules on FDI (WEF)

Need for better interprovincial trade frameworks

Negotiations under way to modernize the agreement on internal trade

Ease of Doing Business

Declining foreign demand for Canadian R&D

The percentage of GERD funded from abroad dropped from 17.4% in 2000 to 6% in 2014, 27th in the OECD The percentage of BERD financed from abroad went from 28% in 2000 to 11% in 2014, 16th in the OECD

Economy

Ease of Doing

Business Rank

Starting a Business

Dealing with Construction

Permits

Getting Electricity

Registering Property

Getting Credit

Singapore 1 10 1 6 17 19 NZ 2 1 3 31 1 1 Denmark 3 29 5 12 9 28 Korea 4 23 28 1 40 42 HK SAR, China 5 4 7 9 59 19 UK 6 17 23 15 45 19 US 7 49 33 44 34 2 Sweden 8 16 19 7 11 70 Norway 9 24 26 18 13 70 Finland 10 33 27 16 20 42 Taiwan, China 11 22 6 2 18 59 Macedonia 12 2 10 45 50 42 Australia 13 11 4 39 47 5 Canada 14 3 53 105 42 7 Germany 15 107 13 3 62 28

WORLD BANK EASE OF DOING BUSINESS RANKINGS 2015

34

International examples

CUTTINGREDTAPE.GOV.AU established to inform Australians on the progress of the cutting red-tape initiative. To date, the initiative has saved A$4.8B over two years. Throughout 2015, the government made 460 red-tape cutting decisions, which reduced compliance costs by A$2.5B a year.

COMMONWEALTH REGULATORY BURDEN MEASURE calculates the compliance costs of regulatory proposals on business, individuals and the community. For new regulations or when changing existing regulations, government agencies are required to use the Measure to quantify costs and cost offsets.

UNITED KINGDOM

THE CUTTING RED TAPE PROGRAMME allows business to tell the UK government how it can cut red tape and reduce bureaucratic barriers to growth and productivity within their sector. The programme also conducts proactive reviews, such as on house building, energy, waste, money-laundering, agriculture, and childcare. So far, 2,400 regulations have been scrapped and businesses will see £1.2B savings per year.

THE UK TRADE & INVESTMENT PLAN provides support for exporters to better engage with emerging markets and to increase foreign direct investment (FDI) in the UK. The plan provides specialist support, advice and access to trade and investment events overseas, increases the supply of inward investment opportunities. It hopes to increase UK exports to £1T by 2020 and increase FDI to £1.5T by 2020.

AUSTRALIA

Ease of Doing Business

Iu4-206/2016E-PDF 978-0-660-05904-4