Embed Size (px)

Citation preview

221

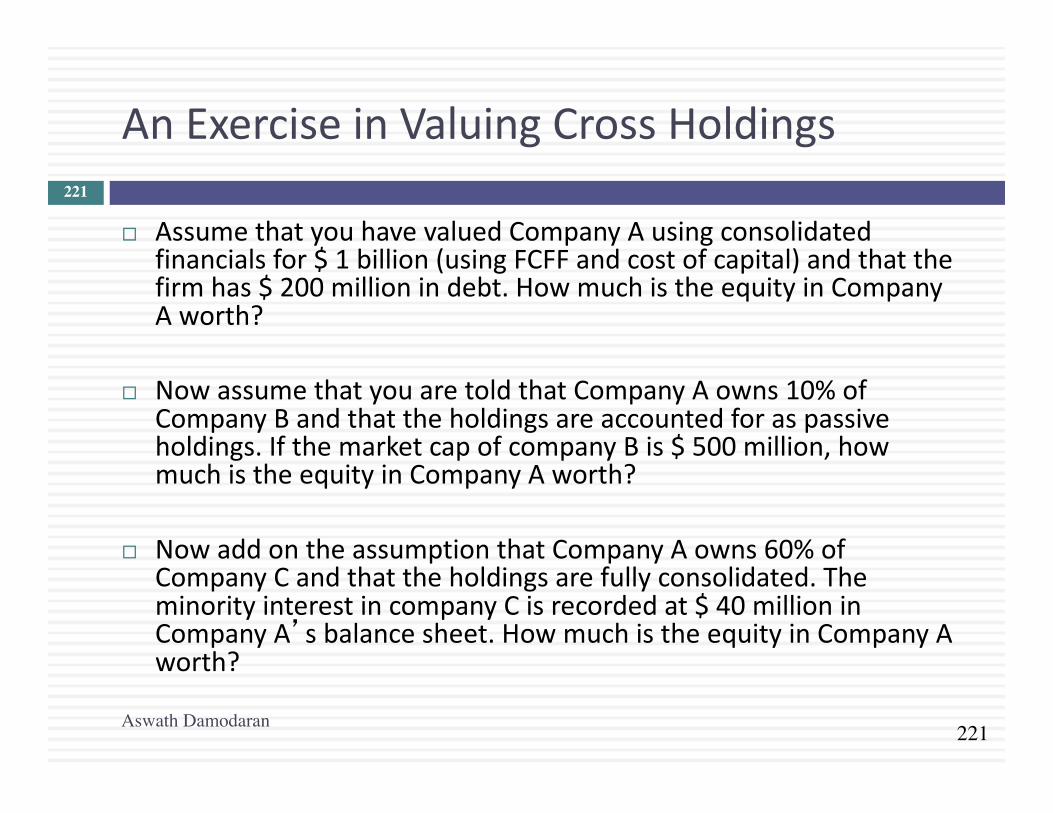

AnExerciseinValuingCrossHoldings

¨ AssumethatyouhavevaluedCompanyAusingconsolidatedfinancialsfor$1billion(usingFCFFandcostofcapital)andthatthefirmhas$200millionindebt.HowmuchistheequityinCompanyAworth?

¨ NowassumethatyouaretoldthatCompanyAowns10%ofCompanyBandthattheholdingsareaccountedforaspassiveholdings.IfthemarketcapofcompanyBis$500million,howmuchistheequityinCompanyAworth?

¨ NowaddontheassumptionthatCompanyAowns60%ofCompanyCandthattheholdingsarefullyconsolidated.TheminorityinterestincompanyCisrecordedat$40millioninCompanyA’sbalancesheet.HowmuchistheequityinCompanyAworth?

Aswath Damodaran

221

222

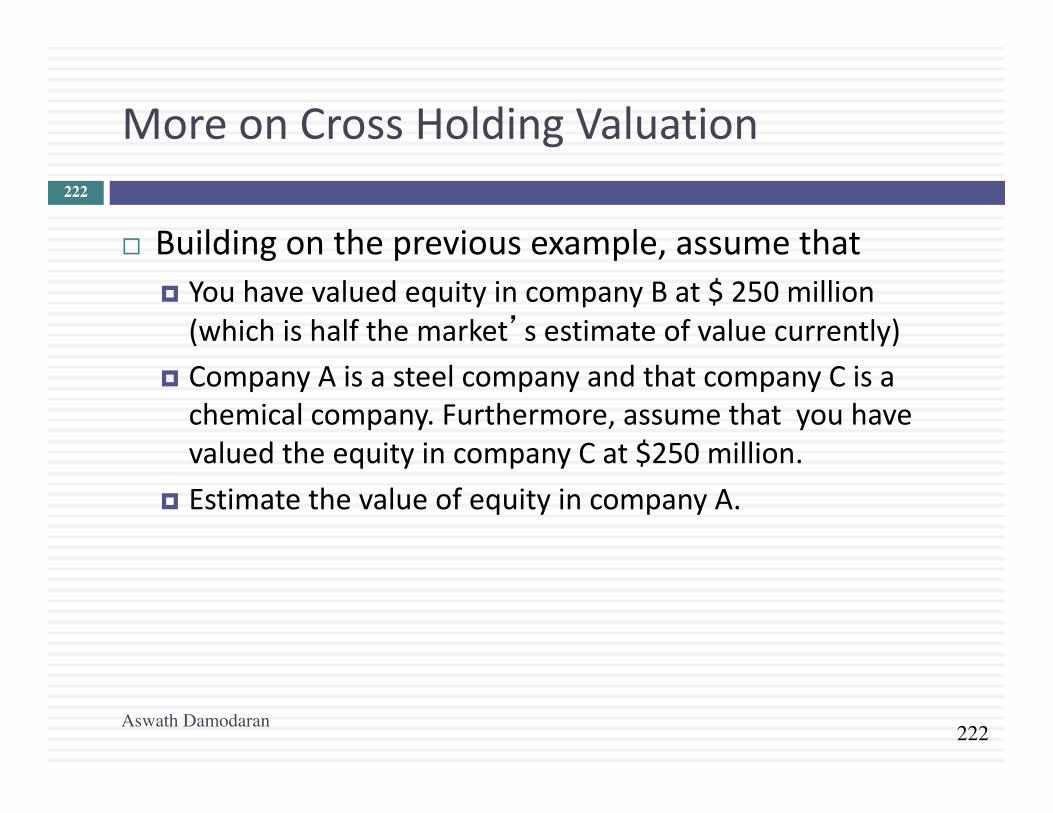

MoreonCrossHoldingValuation

¨ Buildingonthepreviousexample,assumethat¤ YouhavevaluedequityincompanyBat$250million(whichishalfthemarket’sestimateofvaluecurrently)

¤ CompanyAisasteelcompanyandthatcompanyCisachemicalcompany.Furthermore,assumethatyouhavevaluedtheequityincompanyCat$250million.

¤ EstimatethevalueofequityincompanyA.

Aswath Damodaran

222

223

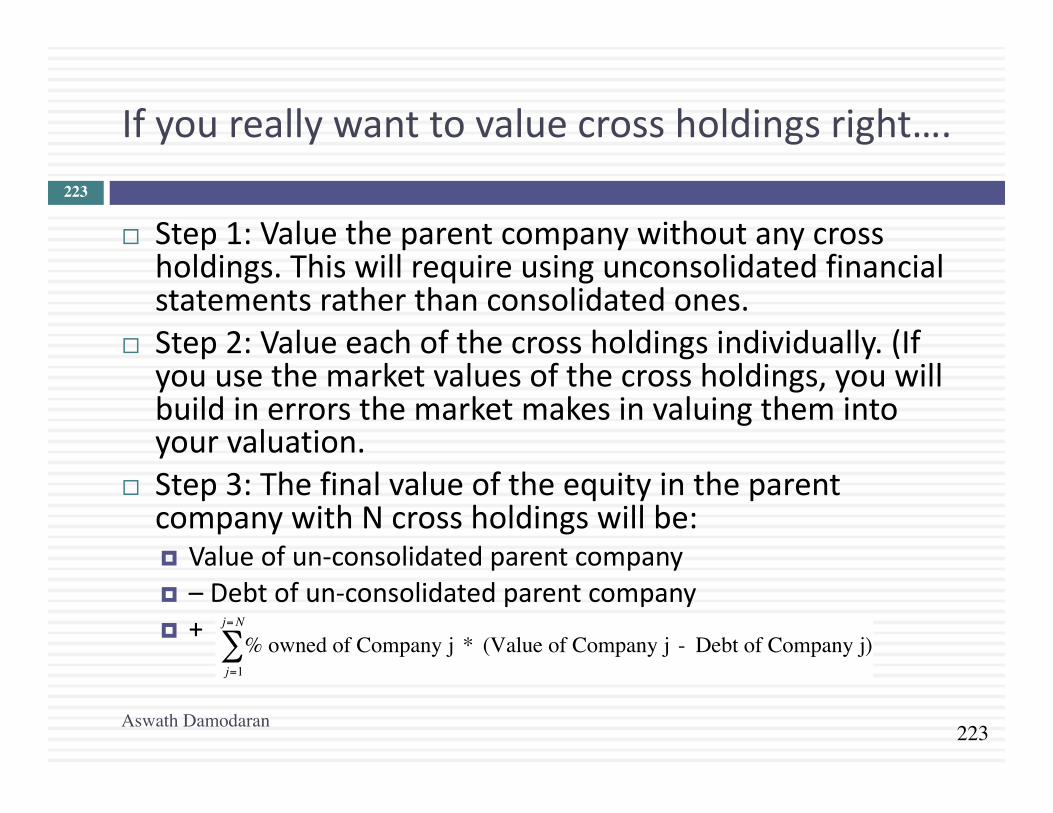

Ifyoureallywanttovaluecrossholdingsright….

¨ Step1:Valuetheparentcompanywithoutanycrossholdings.Thiswillrequireusingunconsolidatedfinancialstatementsratherthanconsolidatedones.

¨ Step2:Valueeachofthecrossholdingsindividually.(Ifyouusethemarketvaluesofthecrossholdings,youwillbuildinerrorsthemarketmakesinvaluingthemintoyourvaluation.

¨ Step3:ThefinalvalueoftheequityintheparentcompanywithNcrossholdingswillbe:¤ Valueofun-consolidatedparentcompany¤ – Debtofun-consolidatedparentcompany¤ +

€

% owned of Company j * (Value of Company jj=1

j=N

∑ - Debt of Company j)

Aswath Damodaran

223

224

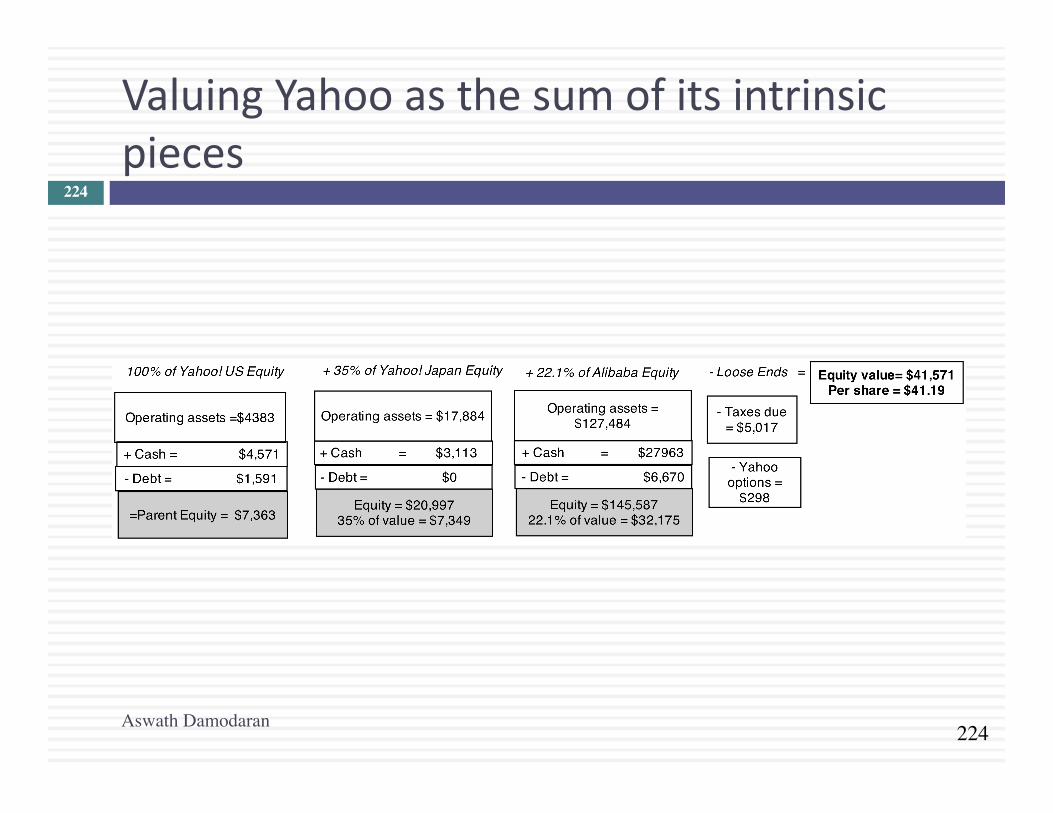

ValuingYahooasthesumofitsintrinsicpieces

Aswath Damodaran

224

225

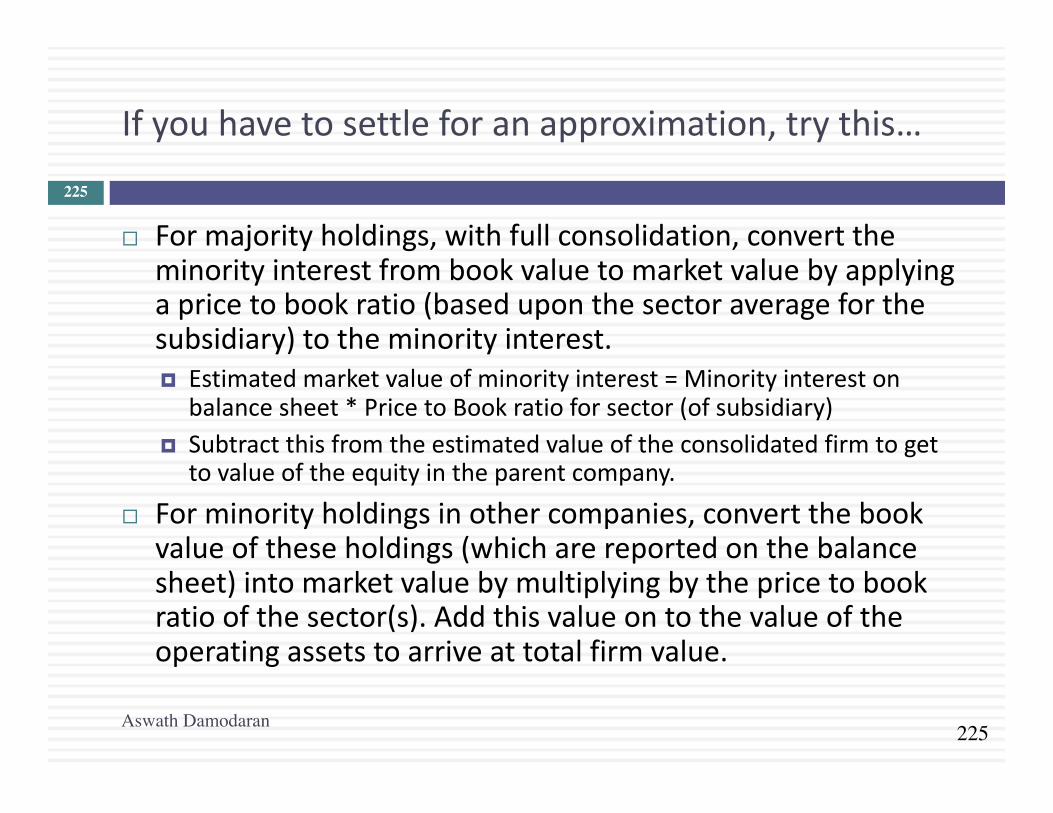

Ifyouhavetosettleforanapproximation,trythis…

¨ Formajorityholdings,withfullconsolidation,converttheminorityinterestfrombookvaluetomarketvaluebyapplyingapricetobookratio(baseduponthesectoraverageforthesubsidiary)totheminorityinterest.¤ Estimatedmarketvalueofminorityinterest=Minorityintereston

balancesheet*PricetoBookratioforsector(ofsubsidiary)¤ Subtractthisfromtheestimatedvalueoftheconsolidatedfirmtoget

tovalueoftheequityintheparentcompany.¨ Forminorityholdingsinothercompanies,convertthebook

valueoftheseholdings(whicharereportedonthebalancesheet)intomarketvaluebymultiplyingbythepricetobookratioofthesector(s).Addthisvalueontothevalueoftheoperatingassetstoarriveattotalfirmvalue.

Aswath Damodaran

225

226

Yahoo:Apricinggame?

Aswath Damodaran

226

227

3.OtherAssetsthathavenotbeencountedyet..

¨ Assetsthatyoushouldnotbecounting(oraddingontoDCFvalues)¤ Ifanassetiscontributingtoyourcashflows,youcannotcountthemarketvalueof

theassetinyourvalue.Thus,youshouldnotbecountingtherealestateonwhichyourofficesstand,thePP&Erepresentingyourfactoriesandotherproductiveassets,anyvaluesattachedtobrandnamesorcustomerlistsanddefinitelynonon-assets(suchasgoodwill).

¨ Assetsthatyoucancount(oraddontoyourDCFvaluation)¤ Overfundedpensionplans:Ifyouhaveadefinedbenefitplanandyourassets

exceedyourexpectedliabilities,youcouldconsidertheoverfundingwithtwocaveats:n Collectivebargainingagreementsmaypreventyoufromlayingclaimtothese

excessassets.n Therearetaxconsequences.Often,withdrawalsfrompensionplansgettaxedat

muchhigherrates.¤ Unutilizedassets:Ifyouhaveassetsorpropertythatarenotbeingutilizedto

generatecashflows(vacantland,forexample),youhavenotvaluedthemyet.Youcanassessamarketvaluefortheseassetsandaddthemontothevalueofthefirm.

Aswath Damodaran

227

228

AnUncountedAsset?

Aswath Damodaran

228

Price tag: $200 million

229

4.ADiscountforComplexity:AnExperiment

CompanyA CompanyBOperatingIncome $1billion $1billionTaxrate 40% 40%ROIC 10% 10%ExpectedGrowth 5% 5%Costofcapital 8% 8%BusinessMix Single MultipleHoldings Simple ComplexAccounting Transparent OpaqueWhichfirmwouldyouvaluemorehighly?

Aswath Damodaran

229

230

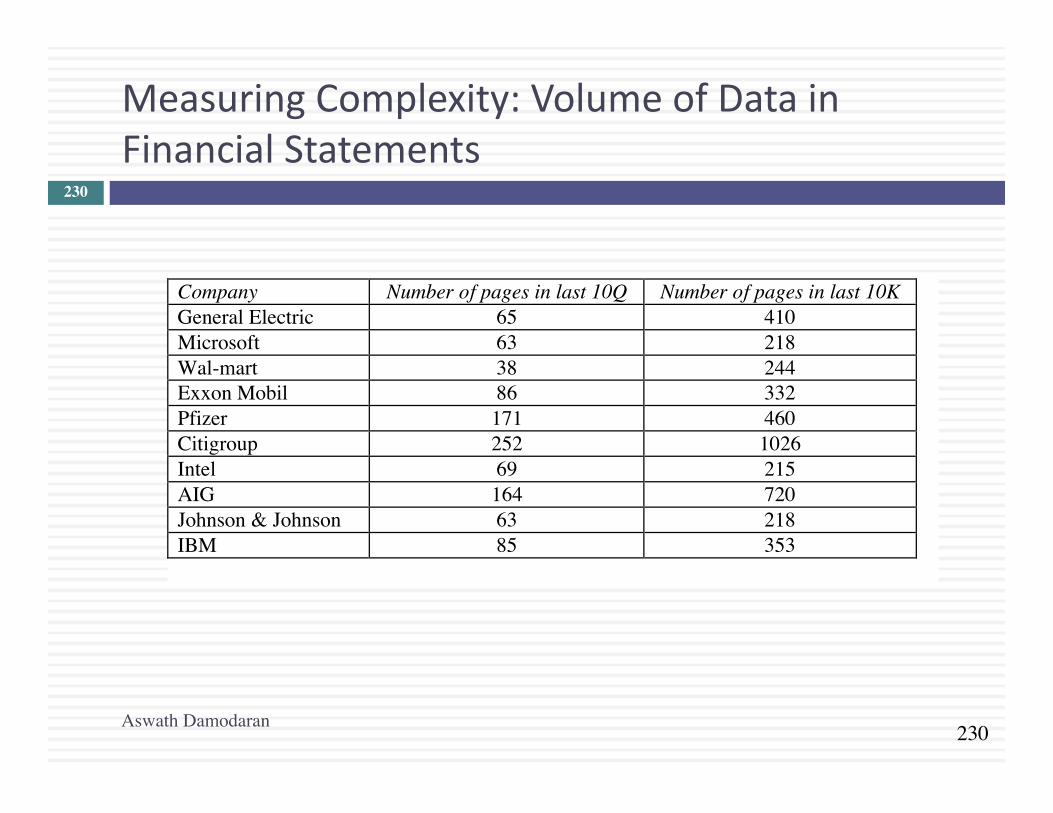

MeasuringComplexity:VolumeofDatainFinancialStatements

Company Number of pages in last 10Q Number of pages in last 10KGeneral Electric 65 410Microsoft 63 218Wal-mart 38 244Exxon Mobil 86 332Pfizer 171 460Citigroup 252 1026Intel 69 215AIG 164 720Johnson & Johnson 63 218IBM 85 353

Aswath Damodaran

230

231

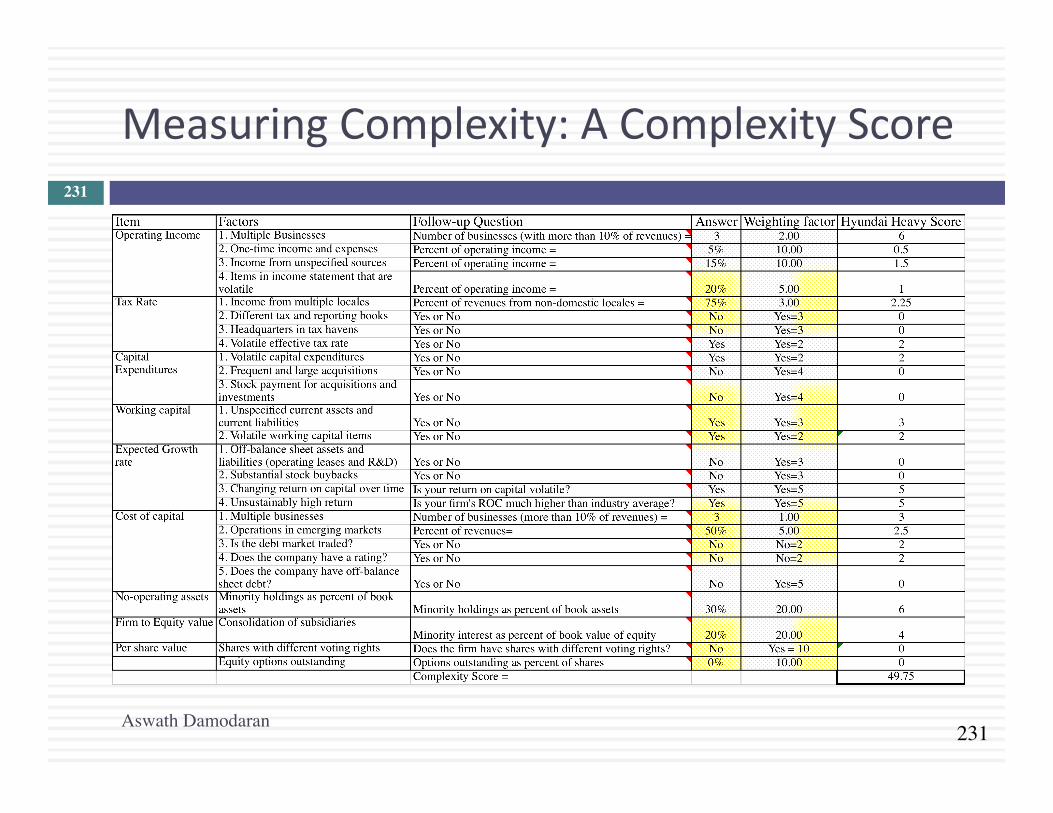

MeasuringComplexity:AComplexityScore

Aswath Damodaran

231

232

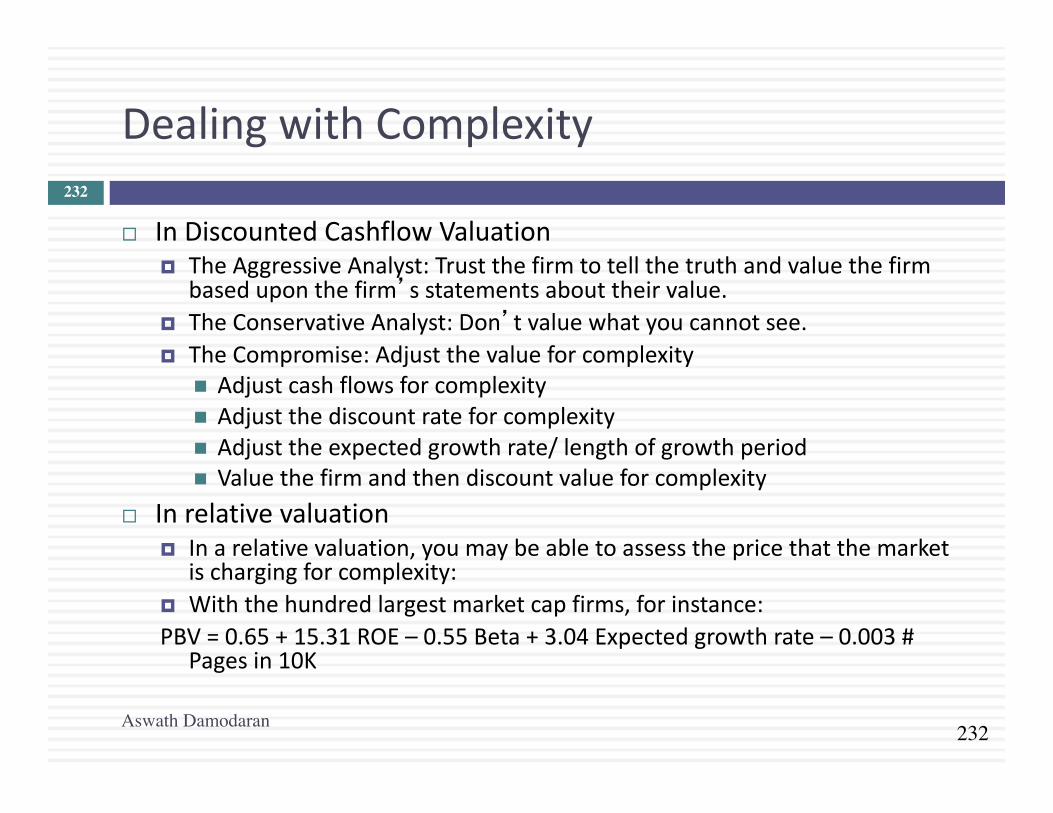

DealingwithComplexity

¨ InDiscountedCashflowValuation¤ TheAggressiveAnalyst:Trustthefirmtotellthetruthandvaluethefirm

baseduponthefirm’sstatementsabouttheirvalue.¤ TheConservativeAnalyst:Don’tvaluewhatyoucannotsee.¤ TheCompromise:Adjustthevalueforcomplexity

n Adjustcashflowsforcomplexityn Adjustthediscountrateforcomplexityn Adjusttheexpectedgrowthrate/lengthofgrowthperiodn Valuethefirmandthendiscountvalueforcomplexity

¨ Inrelativevaluation¤ Inarelativevaluation,youmaybeabletoassessthepricethatthemarket

ischargingforcomplexity:¤ Withthehundredlargestmarketcapfirms,forinstance:PBV=0.65+15.31ROE– 0.55Beta+3.04Expectedgrowthrate– 0.003#

Pagesin10K

Aswath Damodaran

232

233

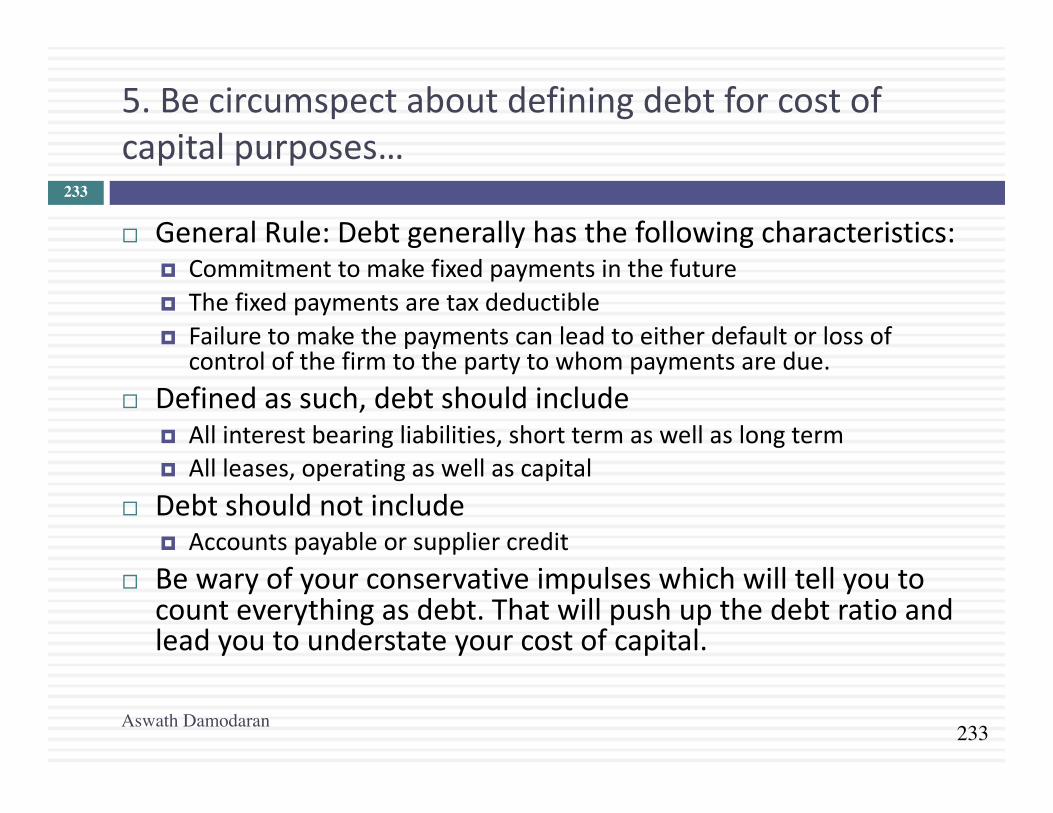

5.Becircumspectaboutdefiningdebtforcostofcapitalpurposes…

¨ GeneralRule:Debtgenerallyhasthefollowingcharacteristics:¤ Commitmenttomakefixedpaymentsinthefuture¤ Thefixedpaymentsaretaxdeductible¤ Failuretomakethepaymentscanleadtoeitherdefaultorlossof

controlofthefirmtothepartytowhompaymentsaredue.¨ Definedassuch,debtshouldinclude

¤ Allinterestbearingliabilities,shorttermaswellaslongterm¤ Allleases,operatingaswellascapital

¨ Debtshouldnotinclude¤ Accountspayableorsuppliercredit

¨ Bewaryofyourconservativeimpulseswhichwilltellyoutocounteverythingasdebt.Thatwillpushupthedebtratioandleadyoutounderstateyourcostofcapital.

Aswath Damodaran

233

234

BookValueorMarketValue

¨ Youarevaluingadistressedtelecomcompanyandhavearrivedatanestimateof$1billionfortheenterprisevalue(usingadiscountedcashflowvaluation).Thecompanyhas$1billioninfacevalueofdebtoutstandingbutthedebtistradingat50%offacevalue(becauseofthedistress).Whatisthevalueoftheequitytoyouasaninvestor?a. Theequityisworthnothing(EVminusFaceValueofDebt)b. Theequityisworth$500million(EVminusMarketValueofDebt)

¨ Wouldyouranswerbedifferentifyouweretoldthattheliquidationvalueoftheassetsofthefirmtodayis$1.2billionandthatyouwereplanningtoliquidatethefirmtoday?

Aswath Damodaran

234

235

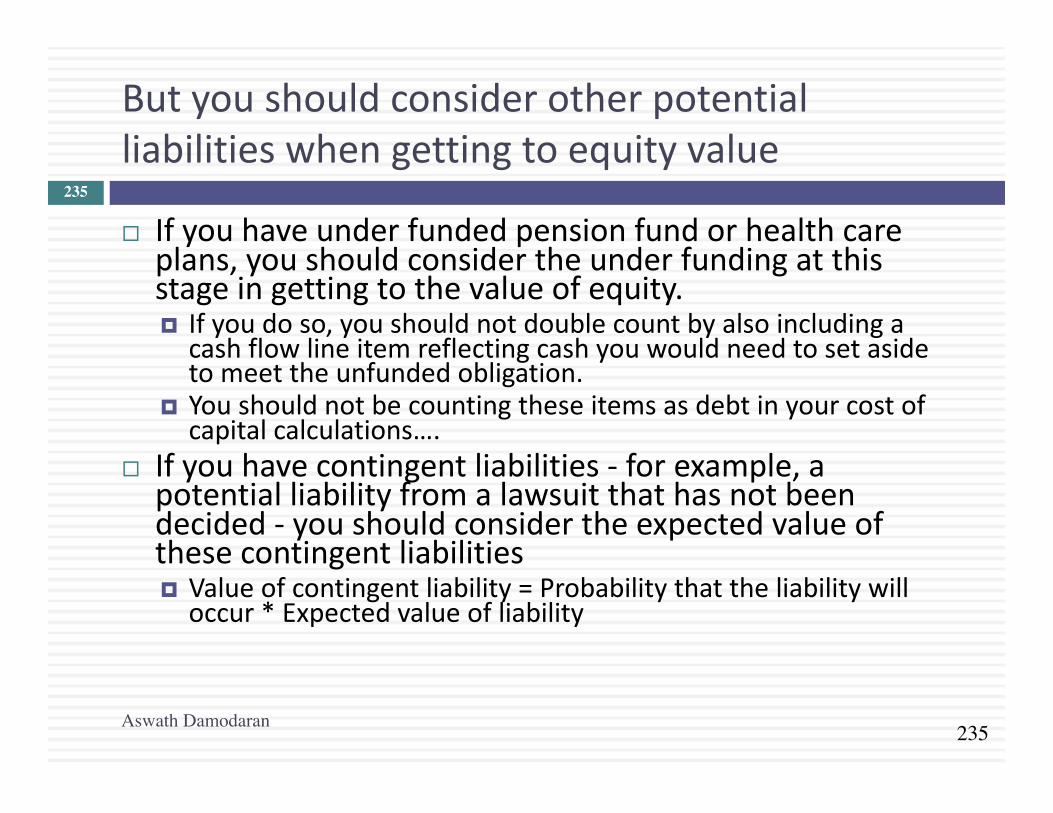

Butyoushouldconsiderotherpotentialliabilitieswhengettingtoequityvalue

¨ Ifyouhaveunderfundedpensionfundorhealthcareplans,youshouldconsidertheunderfundingatthisstageingettingtothevalueofequity.¤ Ifyoudoso,youshouldnotdoublecountbyalsoincludingacashflowlineitemreflectingcashyouwouldneedtosetasidetomeettheunfundedobligation.

¤ Youshouldnotbecountingtheseitemsasdebtinyourcostofcapitalcalculations….

¨ Ifyouhavecontingentliabilities- forexample,apotentialliabilityfromalawsuitthathasnotbeendecided- youshouldconsidertheexpectedvalueofthesecontingentliabilities¤ Valueofcontingentliability=Probabilitythattheliabilitywilloccur*Expectedvalueofliability

Aswath Damodaran

235

236

6.EquitytoEmployees:EffectonValue

¨ Inrecentyears,firmshaveturnedtogivingemployees(andespeciallytopmanagers)equityoptionorrestrictedstockpackagesaspartofcompensation.Iftheyareoptions,theyusuallyarelongtermandonvolatilestocks.Ifrestrictedstock,therestrictionsareusuallyontrading.

¨ Theseequitycompensationpackagesareclearlyvaluableandthequestionbecomeshowbesttodealwiththeminvaluation.

¨ Twokeyissueswithemployeeoptions:¤ Howdooptionsorrestrictedstockgrantedinthepastaffectequity

valuepersharetoday?¤ Howdoexpectedgrantsofeitherinthefutureaffectequityvalue

today?

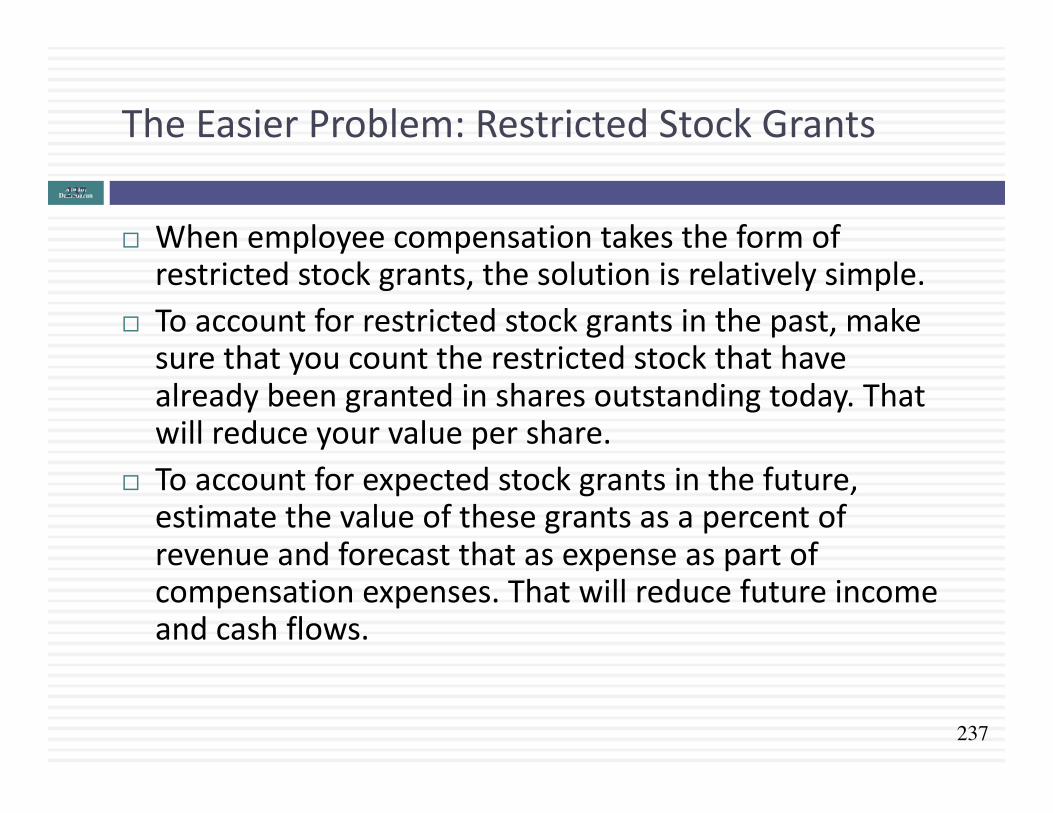

237

TheEasierProblem:RestrictedStockGrantsAswath

Damodaran237

¨ Whenemployeecompensationtakestheformofrestrictedstockgrants,thesolutionisrelativelysimple.

¨ Toaccountforrestrictedstockgrantsinthepast,makesurethatyoucounttherestrictedstockthathavealreadybeengrantedinsharesoutstandingtoday.Thatwillreduceyourvaluepershare.

¨ Toaccountforexpectedstockgrantsinthefuture,estimatethevalueofthesegrantsasapercentofrevenueandforecastthatasexpenseaspartofcompensationexpenses.Thatwillreducefutureincomeandcashflows.

238

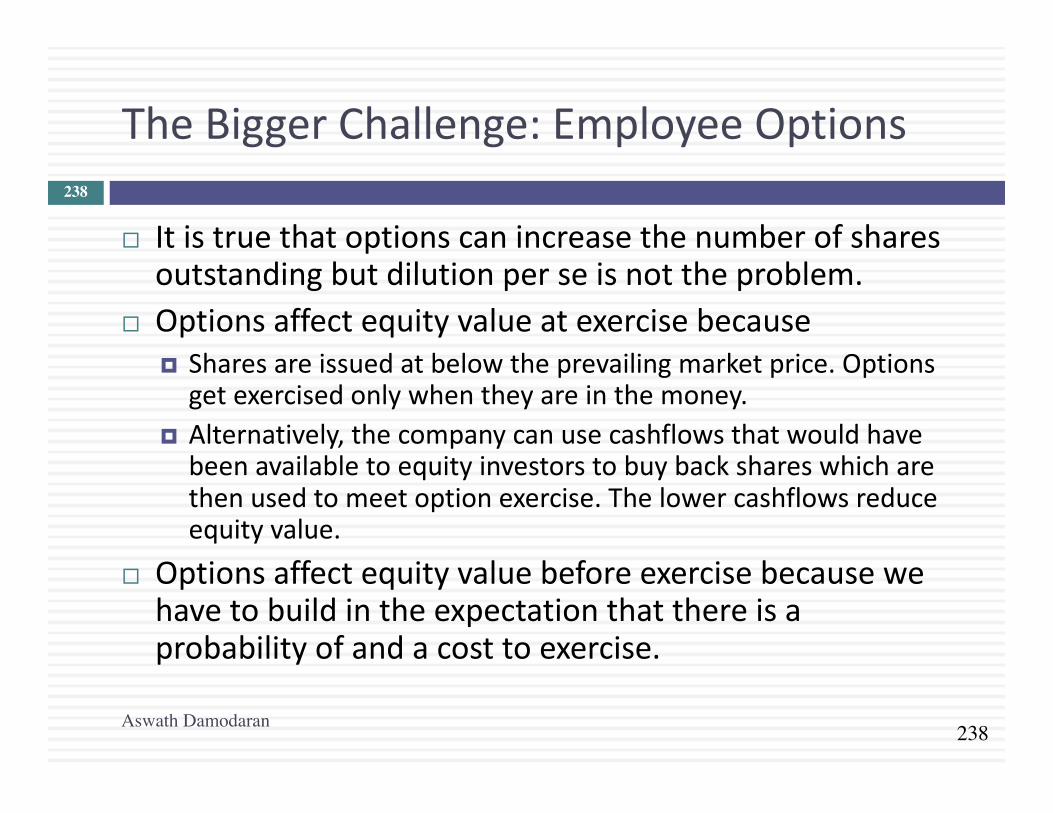

TheBiggerChallenge:EmployeeOptions

¨ Itistruethatoptionscanincreasethenumberofsharesoutstandingbutdilutionperseisnottheproblem.

¨ Optionsaffectequityvalueatexercisebecause¤ Sharesareissuedatbelowtheprevailingmarketprice.Optionsgetexercisedonlywhentheyareinthemoney.

¤ Alternatively,thecompanycanusecashflows thatwouldhavebeenavailabletoequityinvestorstobuybackshareswhicharethenusedtomeetoptionexercise.Thelowercashflows reduceequityvalue.

¨ Optionsaffectequityvaluebeforeexercisebecausewehavetobuildintheexpectationthatthereisaprobabilityofandacosttoexercise.

Aswath Damodaran

238

239

Asimpleexample…

¨ XYZcompanyhas$100millioninfreecashflows tothefirm,growing3%ayearinperpetuityandacostofcapitalof8%.Ithas100millionsharesoutstandingand$1billionindebt.Itsvaluecanbewrittenasfollows:

Valueoffirm=100/(.08-.03) =2000Debt =1000=Equity =1000Valuepershare =1000/100=$10

¨ XYZdecidestogive10millionoptionsatthemoney(withastrikepriceof$10)toitsCEO.Whateffectwillthishaveonthevalueofequitypershare?a. None.Theoptionsarenotin-the-money.b. Decreaseby10%,sincethenumberofsharescouldincreaseby10millionc. Decreasebylessthan10%.Theoptionswillbringincashintothefirmbutthey

havetimevalue.

Aswath Damodaran

239

240

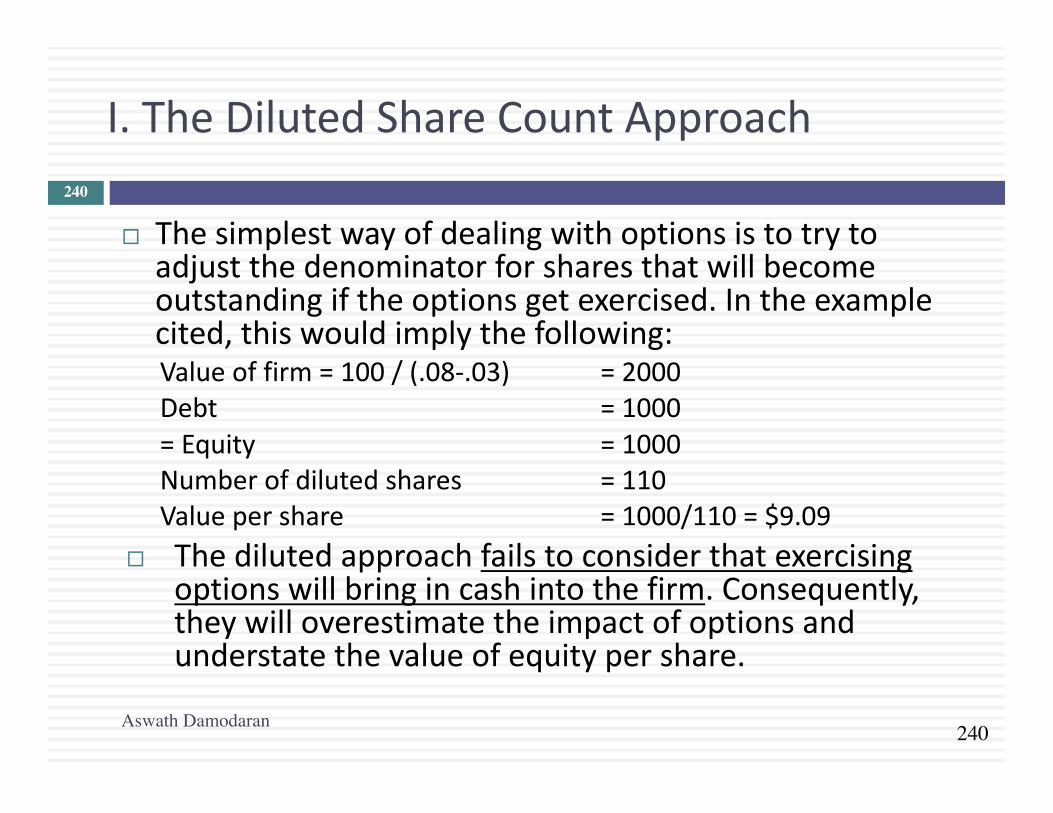

I.TheDilutedShareCountApproach

¨ Thesimplestwayofdealingwithoptionsistotrytoadjustthedenominatorforsharesthatwillbecomeoutstandingiftheoptionsgetexercised.Intheexamplecited,thiswouldimplythefollowing:Valueoffirm=100/(.08-.03) =2000Debt =1000=Equity =1000Numberofdilutedshares =110Valuepershare =1000/110=$9.09

¨ Thedilutedapproachfailstoconsiderthatexercisingoptionswillbringincashintothefirm.Consequently,theywilloverestimatetheimpactofoptionsandunderstatethevalueofequitypershare.

Aswath Damodaran

240

241

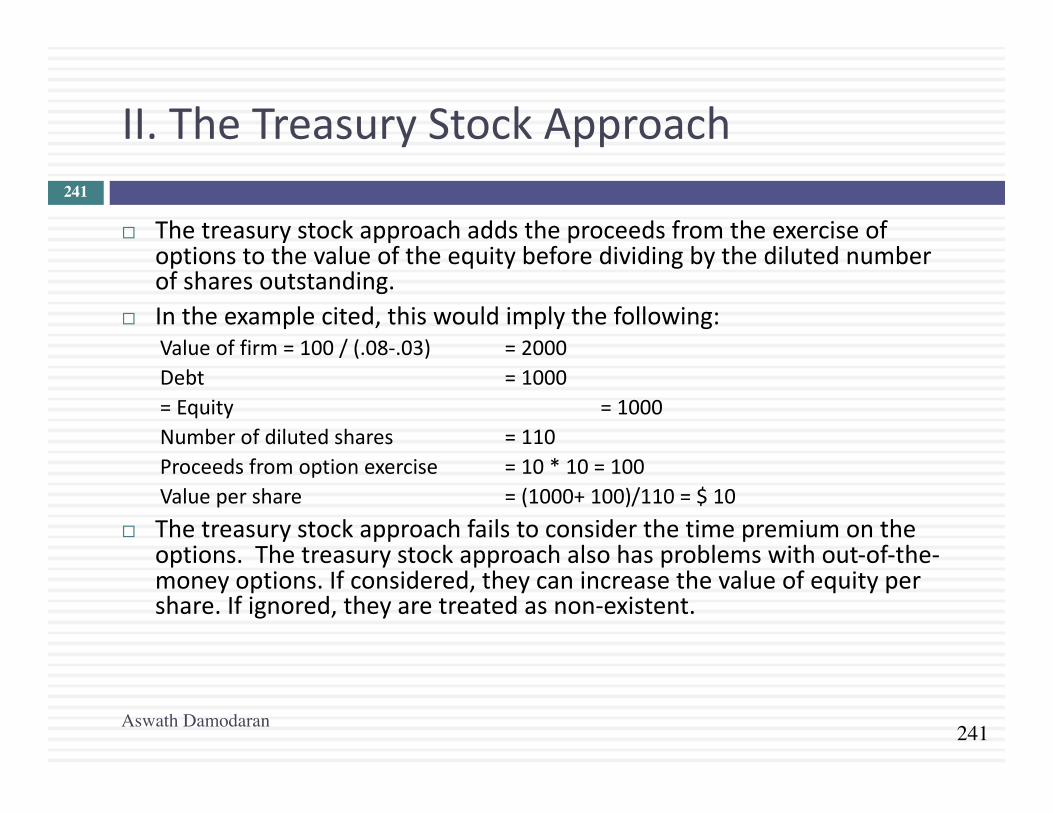

II.TheTreasuryStockApproach

¨ Thetreasurystockapproachaddstheproceedsfromtheexerciseofoptionstothevalueoftheequitybeforedividingbythedilutednumberofsharesoutstanding.

¨ Intheexamplecited,thiswouldimplythefollowing:Valueoffirm=100/(.08-.03) =2000Debt =1000=Equity =1000Numberofdilutedshares =110Proceedsfromoptionexercise =10*10=100Valuepershare =(1000+100)/110=$10

¨ Thetreasurystockapproachfailstoconsiderthetimepremiumontheoptions. Thetreasurystockapproachalsohasproblemswithout-of-the-moneyoptions.Ifconsidered,theycanincreasethevalueofequitypershare.Ifignored,theyaretreatedasnon-existent.

Aswath Damodaran

241

242

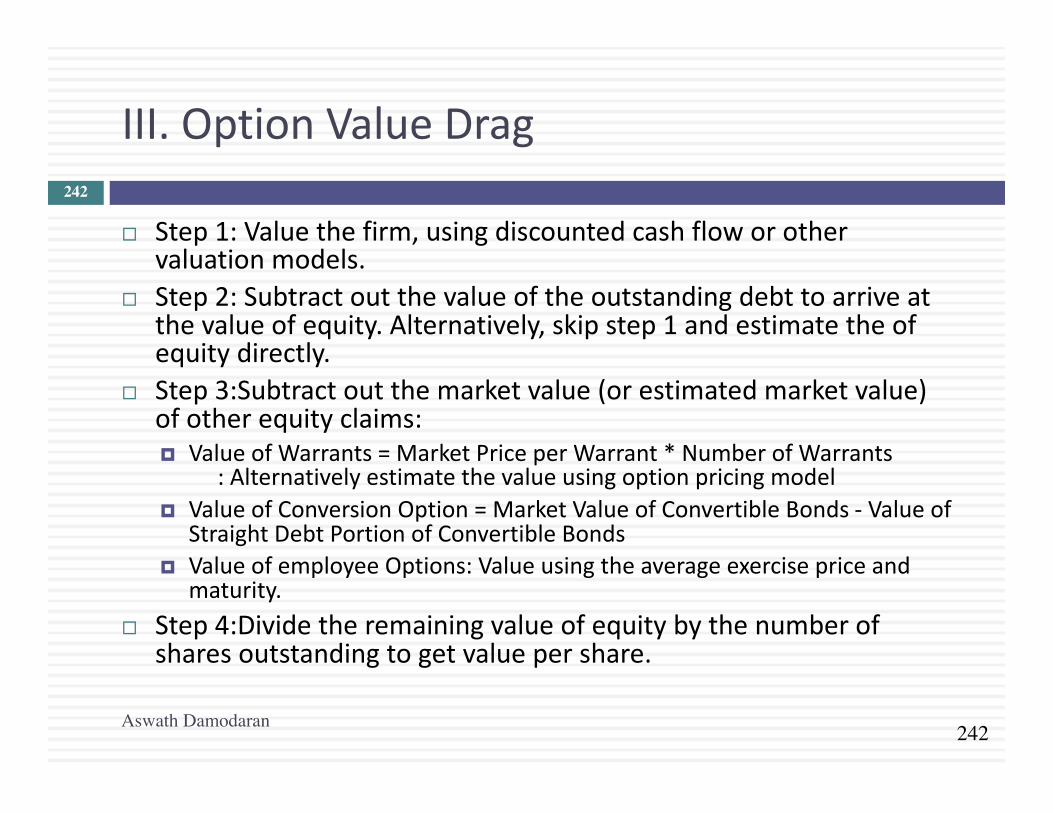

III.OptionValueDrag

¨ Step1:Valuethefirm,usingdiscountedcashfloworothervaluationmodels.

¨ Step2:Subtractoutthevalueoftheoutstandingdebttoarriveatthevalueofequity.Alternatively,skipstep1andestimatetheofequitydirectly.

¨ Step3:Subtractoutthemarketvalue(orestimatedmarketvalue)ofotherequityclaims:¤ ValueofWarrants=MarketPriceperWarrant*NumberofWarrants

:Alternativelyestimatethevalueusingoptionpricingmodel¤ ValueofConversionOption=MarketValueofConvertibleBonds- Valueof

StraightDebtPortionofConvertibleBonds¤ ValueofemployeeOptions:Valueusingtheaverageexercisepriceand

maturity.¨ Step4:Dividetheremainingvalueofequitybythenumberof

sharesoutstandingtogetvaluepershare.

Aswath Damodaran

242

243

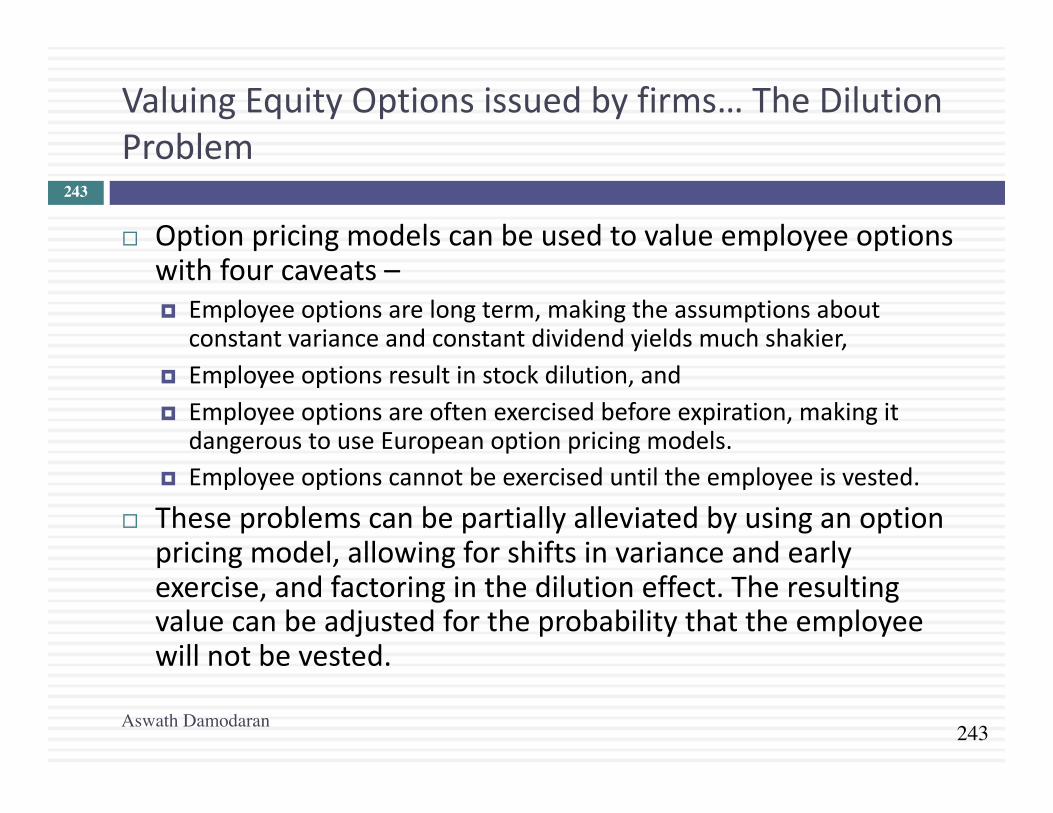

ValuingEquityOptionsissuedbyfirms…TheDilutionProblem

¨ Optionpricingmodelscanbeusedtovalueemployeeoptionswithfourcaveats–¤ Employeeoptionsarelongterm,makingtheassumptionsabout

constantvarianceandconstantdividendyieldsmuchshakier,¤ Employeeoptionsresultinstockdilution,and¤ Employeeoptionsareoftenexercisedbeforeexpiration,makingit

dangeroustouseEuropeanoptionpricingmodels.¤ Employeeoptionscannotbeexerciseduntiltheemployeeisvested.

¨ Theseproblemscanbepartiallyalleviatedbyusinganoptionpricingmodel,allowingforshiftsinvarianceandearlyexercise,andfactoringinthedilutioneffect.Theresultingvaluecanbeadjustedfortheprobabilitythattheemployeewillnotbevested.

Aswath Damodaran

243

244

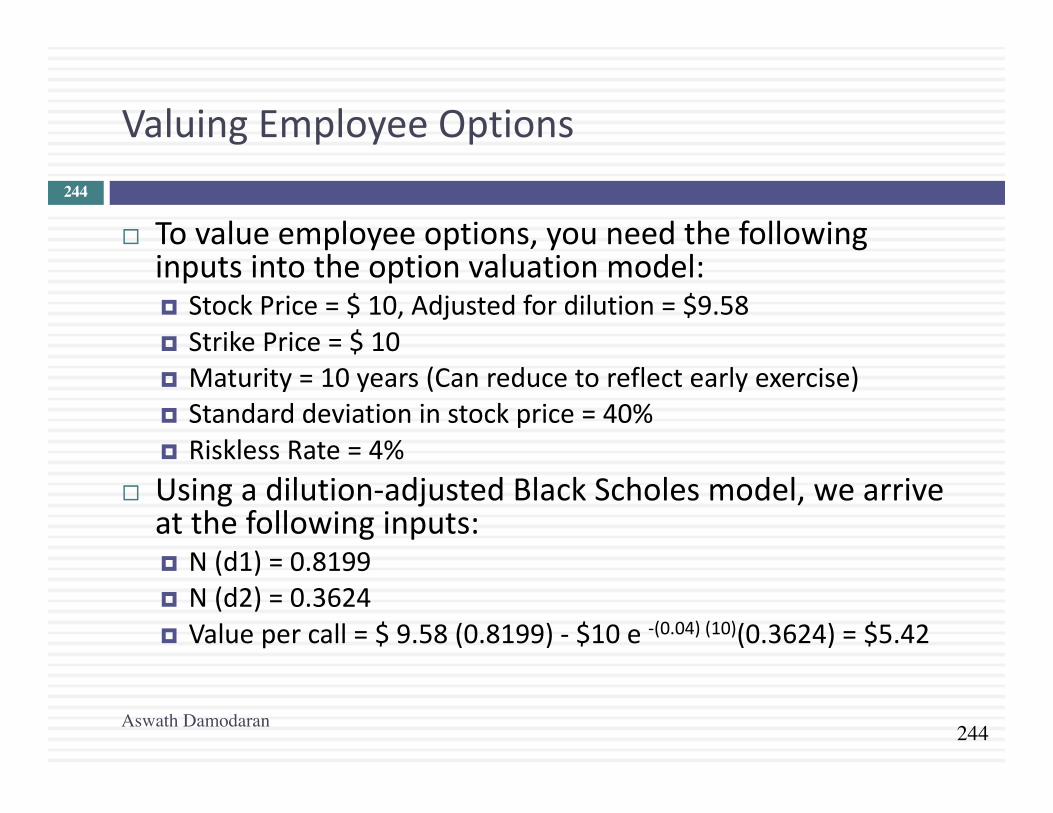

ValuingEmployeeOptions

¨ Tovalueemployeeoptions,youneedthefollowinginputsintotheoptionvaluationmodel:¤ StockPrice=$10,Adjustedfordilution=$9.58¤ StrikePrice=$10¤ Maturity=10years(Canreducetoreflectearlyexercise)¤ Standarddeviationinstockprice=40%¤ RisklessRate=4%

¨ Usingadilution-adjustedBlackScholesmodel,wearriveatthefollowinginputs:¤ N(d1)=0.8199¤ N(d2)=0.3624¤ Valuepercall=$9.58(0.8199)- $10e-(0.04)(10)(0.3624)=$5.42

Aswath Damodaran

244

245

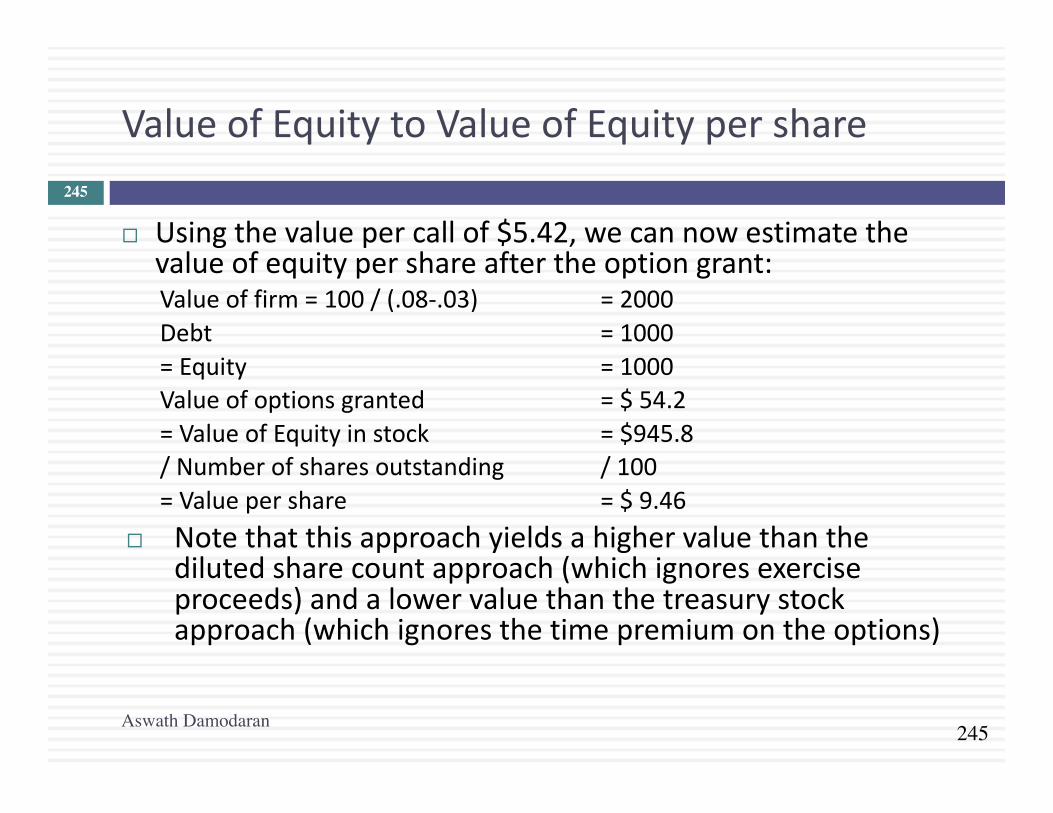

ValueofEquitytoValueofEquitypershare

¨ Usingthevaluepercallof$5.42,wecannowestimatethevalueofequitypershareaftertheoptiongrant:Valueoffirm=100/(.08-.03) =2000Debt =1000=Equity =1000Valueofoptionsgranted =$54.2=ValueofEquityinstock =$945.8/Numberofsharesoutstanding /100=Valuepershare =$9.46

¨ Notethatthisapproachyieldsahighervaluethanthedilutedsharecountapproach(whichignoresexerciseproceeds)andalowervaluethanthetreasurystockapproach(whichignoresthetimepremiumontheoptions)

Aswath Damodaran

245

246

Totaxadjustornottotaxadjust…

¨ Intheexampleabove,wehaveassumedthattheoptionsdonotprovideanytaxadvantages.Totheextentthattheexerciseoftheoptionscreatestaxadvantages,theactualcostoftheoptionswillbelowerbythetaxsavings.

¨ Onesimpleadjustmentistomultiplythevalueoftheoptionsby(1- taxrate)togetanafter-taxoptioncost.

Aswath Damodaran

246

247

Optiongrantsinthefuture…

¨ Assumenowthatthisfirmintendstocontinuegrantingoptionseachyeartoitstopmanagementaspartofcompensation.Theseexpectedoptiongrantswillalsoaffectvalue.

¨ Thesimplestmechanismforbringinginfutureoptiongrantsintotheanalysisistodothefollowing:¤ Estimatethevalueofoptionsgrantedeachyearoverthelastfewyearsasapercentofrevenues.

¤ Forecastoutthevalueofoptiongrantsasapercentofrevenuesintofutureyears,allowingforthefactthatasrevenuesgetlarger,optiongrantsasapercentofrevenueswillbecomesmaller.

¤ Considerthislineitemaspartofoperatingexpenseseachyear.Thiswillreducetheoperatingmarginandcashfloweachyear.

Aswath Damodaran

247

248

Whenoptionsaffectequityvaluepersharethemost…

¨ Optiongrantsaffectvaluemore¤ Thelowerthestrikepriceissetrelativetothestockprice¤ Thelongerthetermtomaturityoftheoption¤ Themorevolatilethestockprice

¨ Theeffectonvaluewillbemagnifiedifcompaniesareallowedtorevisitoptiongrantsandresettheexercisepriceifthestockpricemovesdown.

Aswath Damodaran

248