Embed Size (px)

Citation preview

AN EVALUATION OF THE RISK-RETURN HYPOTHESIS

A STUDY OF SECURITY MARKET PERFORMANCE

by

ROBERT OWEN KIRBY, B.S., M.S.

A DISSERTATION

IN

BUSINESS ADMINISTRATION

Submitted to the Graduate Faculty of Texas Tech University in Partial Fulfillment of the Req[uiramants for

the Degree of

DOCTOR OF BUSINESS ADMINISTRATION

Approved

Accepted

Au^u^t, 197'4 i^uA

Td

fOoXZ

ACKNOWLEDGMENTS

I realize that it would be impossible to thank

everyone who aided ma in the preparation of this disserta

tion. However, I would like to recognize four individuals

who ware especially helpful. Let ma state my sincere

appreciation to Dr. William P. Dukes, my major professor,

for his untiring efforts in directing my research through

two drafts and innumerable corrections. I also am indebted

to Dr. Oswald D. Bowlin and Dr. Virgil T. Dock for thair

helpful criticisms concerning the content and cohasivanass

of the final copy. In addition, I am especially apprecia

tive of my wife, Pat, for her dedicated effort in typing,

editing, and proofreading.

11

TABLE OF CONTENTS

ACKNOWLEDGMENTS ii

LIST OF TABLES V

LIST OF FIGURES vi

I. INTRODUCTION 1

Statement of the Problem 2

Purpose of the Dissertation 3

Need for the Research 5

Organization of tha Study 8

II. REVIEW OF RELATED RESEARCH 10

University of Chicago Canter for Research in Security Prices 10

Closely Related Research 12

Sharpe's Empirical Research 13

Other Related Research 15

III. METHOD OF RESEARCH 26

The Data 26

The Market Index 27

Tha Risk Measure 28

Tha Index Modal of

Portfolio Theory 29

Measures of Return 31

Arithmetic Mean 32

Geometric Mean 33

Pure Yield 34

iii

The Market Periods 36

Tha Risk and Return Classes 39

Test of Hypothesis 40

Portfolio Returns 40 f

Pure Yields 43

rV. THE FINDINGS 45

Relationship Batwaan Risk and Return 45

Summary of tha Relationship

Batwaan Risk and Return 63

Long-Run Relationship 66

Pure Yield Performance 68

Summary of tha Relationship Batwaan Risk and Pura Yields . . . . 77

Relationship of Beta Coefficients 81 Distribution of Beta Coefficients 82

Beta as a Predictor of Return 85

V. SUMMARY, CONCLUSIONS, AND

IMPLICATIONS 90

Summary 90

Conclusions 91

Implications 94

Recommendations for

Future Research 96

BIBLIOGRAPHY 99

APPENDIX 106

iv

LIST OF TABLES

Table Page

1. Comparisons of Arithmetic Mean Portfolio Returns and Beta Coefficients by Market Periods 46

2. Comparison of Arithmetic Mean Portfolio Returns in Which There was a Significant Differanca . . . . 53

3. Performance Comparisons of Geometric Mean Portfolio Returns and Beta Coefficients by Market Periods 56

4. Comparison of Gaomatric Mean Portfolio Returns for Which There was a Significant Difference in Performance 62

5. Performance Comparisons Based on Pura Yields by Market Periods 69

6. Distribution of Sub-Pariod Beta Coefficients for 25 Stock Portfolios 7/6/62-5/22/70 83

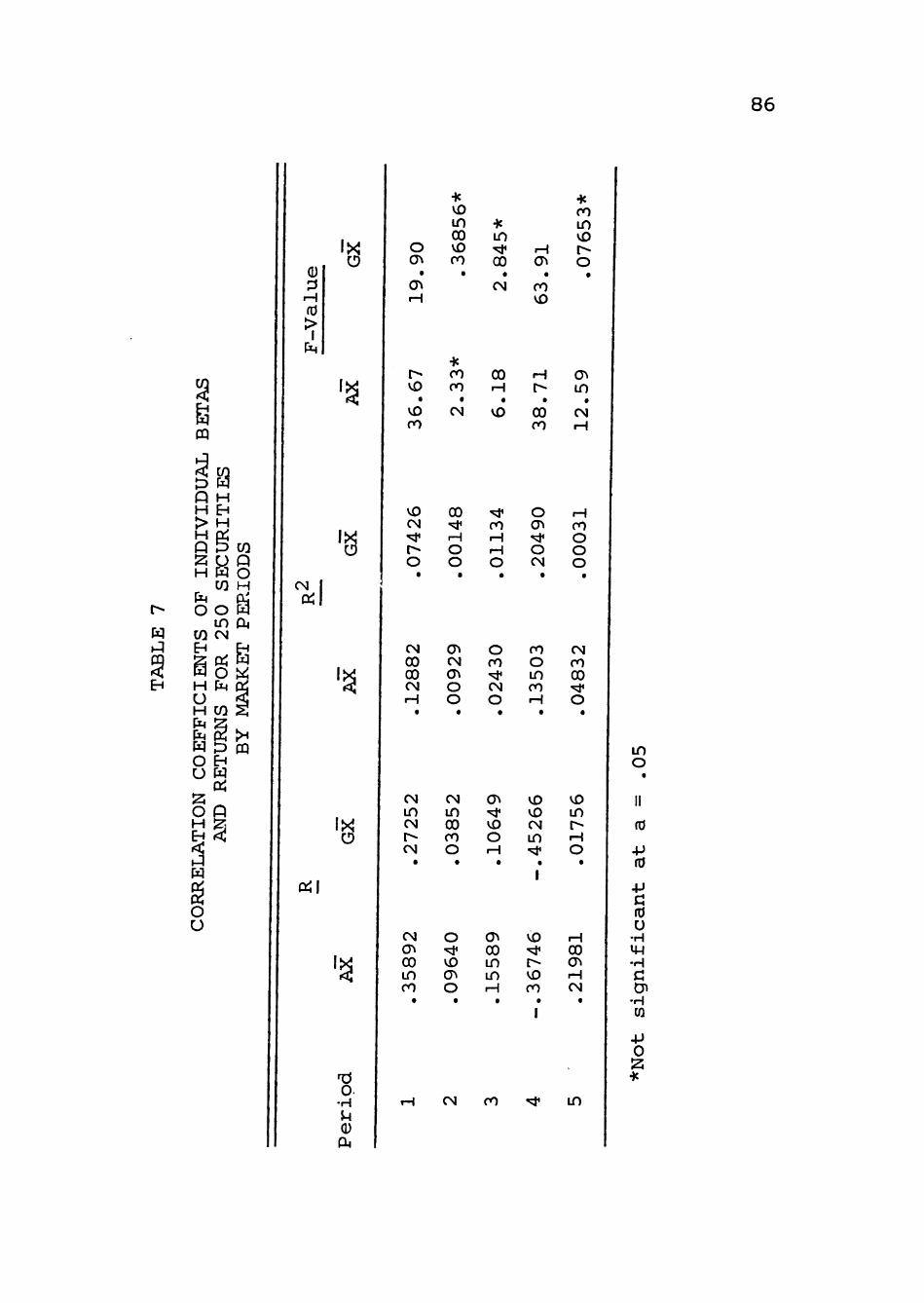

7. Correlation Coafficiants of Individual Betas and Returns for 250 Securities by Market Periods 86

8. Correlation Coafficiants of Portfolio Betas and Returns by Market Periods 88

LIST OF FIGURES

Figure Page

1. Standard and Poor's 500 Average 1962-1970 38

2. Performance as Measured by tha Portfolio Possibility Line 72

3. Performance as Measured by tha Portfolio Possibility Line Whan the Borrowing and Landing Rates Differ 81

VI

CHAPTER I

INTRODUCTION

One of tha best documented propositions of invest

ment theory is that investors, on tha average, can realize

a higher rata of return by assuming greater risks. Con

sistent with this thesis is a long standing theory in

economics which hypothesizes that a positive relationship

exists batwaan a security's risk and its return (i.e.,

the greater tha risk or uncertainty of tha return, the

greater tha average return or risk premium). A common

objective of most investors is tha maximization of return,

and many baliava that tha means of acquiring greater returns

is to invest in securities that ara thought to be mora

risky.

Sauvain [61, p. 117] states that maximizing returns

by investing in low grade securities is based on what ha

calls tha "hypothesis of increasing returns." The theory

states that "in tha entire universe of investments the

rates of net return realized by all investors over long

time periods tends to increase with increasing poorness of

grade." Intuitively this type of relationship is expected.

Investors demand high rates of return as an inducement to

invest in risky assets whara lass risky investments ara

acceptable at lower rates of return. Investors who desire

high average returns must incur high risks and, simulta

neously, andura an increased chance of loss.

Investors frequently base thair decisions to buy

on tha supposition that risk and return ara positively

related. A rational investor obviously will not walcoma

risk for its own sake. Thus, tha only economic justifica

tion for an investor to acquire a mora risky asset is that

the return is baliavad to increase as soma function of tha

increase in risk. Tha fact that common stocks have pro

vided investors with a greater rata of return than bonds,

over extended periods of time, would land soma support to

this belief.

Statement of tha Problem

It has generally bean recognized that there is,

or should be, some trada-off batwaan risk and return.

Recently a substantial body of literature has evolved

giving explicit attention to tha assessment of risk and

tha rata of return on equity securities. Tha problem,

however, is that various thaoratical and empirical studies

have uncovered conflicting results. Data can be collactad

to show that risk and return ara related in a positive

manner, high risk securities tending to reward the investor

with higher returns. In similar fashion, empirical avidanca

is available to show that such a relationship does not

exi st.

In tha event that high risk securities do not reward

investors with greater returns, as tha general theory

seams to imply, than individuals who adhere to the thesis

unknowingly make sub-optimal investments. Presumably tha

quality of investment decisions can ba improved if results

from current empirical research ara made available to

investors as to whether or not, or to what extant, the

risk-raturn tradeoff has existed in tha past. Although

tha same relationship between risk and return may not

exist in tha future, it nonathalass can provide insight

pertaining to tha historical presumptions of investors.

Most of tha research in tha literature supports tha risk-

raturn thesis. However, there have bean enough studies

undertaken during tha past tan years which question various

aspects of tha general relationship to kaap tha subject

viable.

Purpose of tha Dissertation

The purpose of this dissertation is to determine

whether or not common stocks charactarizad by a high dagraa

of systematic risk afford an investor a higher rata of

return than securities with low systematic risk under

identifiable market trends.

To determine tha empirical relationship between

risk and return tha analysis is focused on two risk-raturn

evaluations. First, a comparison of returns is made for

securities in tan risk classifications over four different

market periods, tha derivation of which is explained in

Chapter III, to datarmine the pattern of returns relative

to the level of risk. The objective is to datarmina if

there is a diffarance in tha returns of the tan risk

classifications, and if so, batwaan which groups of

securities is the laval of returns different. Second, tha

relationship between risk and return is examined to investi

gate tha incramants in security returns. An explanation

of performance using pura yield as a measure is also

presented in Chapter III. Tha objactive of this procedure

is to examine security performance in terms of tha return

par unit of risk and to datarmina a relative performance

ranking for tha tan risk classes under market conditions

that advance and decline.

This approach is different from the majority of

previous research in that tha risk-raturn relationships

ara examined over market periods that ara charactarizad by

a specific trend. Unlike other studies in which tha

returns from common stocks ara computed over extended

time periods, tha methodology that is employed in this

dissertation examines tha performance of equity securities

in specific market periods that advance or decline. In

addition to tha four specific market periods, a fifth

period is considered in order to examine tha long run

relationship between risk and return for tha total eight

year period.

The major portion of related research has evaluated

security performance over a typical two, thraa, or five

year holding period, disregarding tha parformanca character

istics of securities under specific market trends, while

assuming that tha risk measure remained relatively constant

over time. Any insight, tharafora, relating to tha actual

parformanca of securities under different market conditions

would ba useful information for both tha individual investor

and the professional investment manager attempting tha

construction and maintenance of efficient portfolios. It

is baliavad that a segmented approach, considering security

performance over a specific market trend, provides mora

information for investors than simply knowing tha par

formanca patterns of equity securities over extended periods

of time in tha past.

Naad for tha Research

An opinion held by most writers in the field of

investment theory saams to ba that investors, in general,

have an aversion to risk. In order to avoid a risky

security, investors indirectly pay a premium in tha sansa

of accepting lower returns from securities of low risk.

In this respect, there is an implication that securities

which are charactarizad by a high degree of risk actually

reward the investor with a greater return. Although thara

is a lack of total agreement with this statement, tha

majority of researchers tend to hold this opinion.

A statement by Hirschlaifar [28, p. 117] seems

typical of tha literature on risk and return.

There will ordinarily be a positive premium on risk. That is, expected risky yields will be higher than sura yields. . . . That tha market does pay positive risk premiums is a statement that many people claim has in fact baan rafutad. However, I baliava that tha weight of tha avidanca indicates that risky madias of investment do in fact have higher expectad yields than secure madias.

Qnpirical research has generally shown that tha

actual risk-raturn relationships ara consistent with this

statement. For example, studies by Fisher and Lorie [23]

and Soldofsky and Millar [l2] propose that high quality

fixed income securities typically reward tha investor

with a lower return than mora speculative bonds or common

stocks. When tha comparison is made, however, batwaan

relative degrees of riskiness, vis-a-vis a sura return,

the findings become somewhat incongruous. Consider, for

•example, the following statement by Morton [52, p. 13].

During tha past faw years tha view has baan promulgated that common stocks having tha greatest price fluctuations will produce tha largest gain to tha investor. Academic theories and statistical studies have baan advanced in support of this thesis and soma mutual funds driving at "parformanca" appear to have baan guided by it. Tha basic assumptions of this theory ara: (1) that investors who take tha greater risk will make tha greater profit, and (2) that risk consists of and is measured by

instability, volatility in market price about the average. . . . Thara is simply no ground in reason or axparianca for tha belief that tha industries or companies with tha greater risk actually earn mora than those with lass risk.

Richardson \j>9, p. 99] supprts the findings of Morton in

the following statement.

. . . tha notion that investors, on average, can realize higher returns by taking greater risks can have no practical validity in investment decision-making. As it now stands, tha risk-reward theory must ba regarded as a rather arbitrary, academically inspired concept of what investing is all about.

Although conflicting avidanca can ba found in the

literature regarding tha risk-raturn tradeoff, tha position

taken by Sauvain [ 1, p. 117] might ba more appropriate.

Most theorists in investments and many practical investment managers baliava that in tha entire universe of security investment tha rates of net return realized by all investors over long periods of time tend to increase with increasing riskiness of securities. Thara ara logical reasons why thara should ba such a relationship of risk and returns and thara is good empirical evidence that it exists, but until tha data ara mora conclusive we shall regard it as a hypothesis.

Obviously much of the dissimilarity in tha findings

can be traced to tha specific methodology employed by tha

researcher. Specifically, tha surrogate for risk appears

to be tha most critical consideration. This problem is

unduly complicated since thara is limited agraamant among

both academicians and practitioners as to what measure

constitutes tha bast surrogate for risk. A second variable

that undoubtedly has a bearing on the findings is tha

8

market period used in tha respective analyses. The time

periods vary depending on tha date of the research and may

to some extant bias tha results. For this reason, it

appears that continued research will be required to keep

market participants abreast of the currant tradeoff under

market conditions that ara continually changing.

In addition to tha academic value of continued

research into tha risk-raturn hypothesis, tha findings

should also prove useful for tha practitioner. Investment

managers attempting to construct optimal portfolios through

diversification techniques would surely find tha results

of current empirical research informative. In the avant

that tha actual tradeoff between risk and return is

different from that which is normally expected, or that

certain groups of securities display unique return

characteristics, tha construction and balancing of optimal

portfolios bacoma extremely complicated. In this respect,

it would appear that tha quality of investment decisions

can be improved if tha most currant empirical evidence is

made available to decision makers concerning tha relationship

between risk and return.

Organization of tha Study

In attempting to present empirical evidence relating

to the nature of tha risk-raturn hypothesis, it is necessary

to develop and interpret a large amount of data. For this

reason only summary data related to tha subject of this

dissertation are presented in the main text.

Chapter II presents a concentrated review of

closely related research in the area of security performance

describing tha conclusions and research methodology

employed by the respective authors.

Chapter III describes tha data that ware used in

this analysis and tha related methodology and research

design that was developed to permit an examination of the

risk-return hypothesis for the period of study. Tha

measures of risk and return used in this research ara

introduced along with the determination of tha market

periods and tha development of tha respectiva risk classes.

Chapter IV presents the general findings of tha

analysis as they apply to tha objective of this dissertation.

Information is presented to examine and evaluate security

performance as wall as a summary review of these data

as they applied to tha risk-raturn hypothesis.

Chapter V presents a summary and conclusions with

implications and possible explanations for the findings.

CHAPTER II

REVIEW OF RELATED RESEARCH

During tha past twenty years, an extraordinary

amount of empirical research has bean conducted in tha

area of security performance. Throughout this period

many davalopmants have occurred in tha theory pertaining

to tha stock market and the way in which participants

currently view invastmant theory. Tha modifications have

occurred primarily because of axtansiva empirical research

and theoretical innovations in thraa areas: (1) tha

publication of Harry Markowitz's article on portfolio

theory [45], and tha subsequent work of William F. Sharpa

[62]; (2) tha extensive research and developmant of

efficient market theory and tha related implications for

security analysis; and (3) tha developmant of comprahansiva

data files and computer technology which make extensive

empirical research feasible.

University of Chicago Canter for Research in Security Prices

Tha Canter for Research in Security Prices, which

was established at tha University of Chicago in 1960

through an initial grant from tha brokerage firm of Merrill,

Lynch, Pierce, Fanner & Smith Inc., has become the most

10

11

prolific source of research on the security market since

its inception. Either through direct research effort by

the center itself, and its directors Lawrence Fishar and

James H. Loria, or in tha davalopmant of its data bank,

tha center has become involved either directly or indirectly

in much of tha published research in tha area of security

performance. As an indication of tha significant role

played by tha canter in research activities related to

security market parformanca. Jamas Lorie and Richard

Brealey, while compiling a collection of articles for a

recant publication [43], found that approximately half

of the thirty-savan articles selected for inclusion in

their readings book ware in one way or another connected

with tha canter. Tha articles ware either authored by

persons directly associated with the canter, based on its

data bank, or originally presented in working paper form

at the canter's semiannual meetings.

Over tha years tha number of articles appearing

for publication, dealing with a variety of topics related

to the stock market and security performance, has increased

steadily. This is not surprising since many people ara

interested in tha stock market, and perhaps an even greater

number have aspirations of future invastmant. To review

the literature to data on all related research would be

an insurmountable task; therefore, only tha mora recant

publications and findings, which relate specifically to

12

the topic of this dissertation, ara mentioned in this

review.

Closely Related Research

During tha past faw years a number of studies have

been undertaken to investigate what Morton [Sl] called

tha "performance invastmant strategy." Although consider

able differences exist in tha methodology employed by tha

various studies, such as data samples, time periods,

statistical techniques, and risk surrogates, tha principle

objective of each author was tha same, to investigate soma

aspect of tha risk-raturn hypothesis.

One of tha first major projects undertaken by tha

Center for Research in Security Prices was a comprahansiva

study of tha rates of return on common stock listed on

tha New York Stock Exchange for tha period 1926-1960. Tha

research was coordinated and directed by Fishar and Loria

who later published thair findings [23]. Tha objective of

thair analysis was to compare tha rates of return for

common stocks over twenty-two different time periods

under a variety of invastmant strategies. Return data

were presented for individuals of different tax brackets

under various assumptions concerning the rainvastmant of

dividends. The article was the first comprahansiva study

on the parformanca of securities listed on tha New York

Stock Exchange over an extended period of time. These

13

data indicated that on the average the rates of return on

common stocks have exceeded the average rates of return

on all classes of fixed income securities. According to

the authors the findings of tha research was "news" in

that tha relatively high rates of return on equity securi

ties surprised many investors.

A second article by Fishar and Loria [24] provided

additional information relative to their former study,

and extended their earlier analysis through 1965. Although

minor changes were made in the methodology, mainly the

number and length of time periods, tha results for tha

most part confirmed their earlier findings. A majority

of the original rates of return remained unchanged in tha

second study and provided empirical avidanca to support

the theory that investors seem to require additional

return to compensate for an increased exposure to risk.

Sharpa's Empirical Research

A theoretical modal introduced by William F. Sharpa

[63] in which he davalopad a market equilibrium theory of

asset prices under conditions of risk was tha forerunner

of a number of articles that examined tha risk-return

hypothesis. Sharpe's view was that tha market price of

a security was a function of two variables: (1) tha price

of time, or tha pura rate of interest; and (2) tha price

of risk, i.e., the additional return that is related to

14

the level of risk exposure. The author constructed a market

model which proposed that the relationship between tha

magnitude of tha risk and axpactad return is depicted by

a linear relationship.

In an empirical test of his model, Sharpa [65]

compared tha risk and return measures for thirty-four

mutual funds over the tan year period 1954-1963. Average

holding period returns were computed for each of tha funds

and tha standard deviation of returns was employed as tha

measure of risk. Utilizing a regression technique, Sharpa

concluded that there was significant correlation between

tha risk and return variables, through which ha was able

to depict an "intarmadiata line" as his estimate of the

linear relationship batwaan an asset's laval of risk and

its expected return.

In another study, Sharpa [67] investigated the

relationship batwaan tha rata of return and tha "volatility"

of mutual funds. Using volatility as tha measure of risk,

which is also raprasantad as a rasponsivanass measure, ha

concluded that there appears to be some additional return

for tha investor who held a mora aggressive fund relative

to the investor who dasirad to hold a defensive portfolio.

A secondary conclusion was that tha risk-raturn tradeoffs

which ware computed for various portfolios in ona period

were surprisingly similar in later periods.

15

Other Related Research

In a doctoral dissertation presented at Indiana

University in 1966, Shannon Pratt [ 58] proposed a method

ology to test tha proposition that high risk securities,

as measured by variability of returns in a historic market

period, tend to provide tha investor with a higher return

than did low risk securities. Tha returns on five port

folios of different risk classes, for holding periods of

one to seven years over tha period 1929-1959, ware examined

to determine if investors ware compensated according to

their risk exposure. Tha expected relationship should

show an increase in tha returns for each risk class, or

portfolio, as tha risk increases. Calculating holding

period returns in the conventional way and employing

standard deviation of returns as the measure of risk,

Pratt concluded that those securities which had been

characterized by high risk in tha historic period continued

to remain risky in the future periods. Portfolio returns,

in general, did increase as tha risk became greater;

however, tha returns for tha fifth risk class were lower

than risk class four.

Another interpretation of thasa results by Braalay

[ll, pp. 48-5l] not only raised questions about tha laval

of returns for tha high risk classes, but also pointed out

that the returns did not necessarily increase as a strict

16

linear function of the risk. Investors who have taken

increased risks do seam to have bean compensated, on the

average, by soma increase in return; however, tha question

is raised about whether or not tha increment in return

is sufficient to keep tha "price of risk reduction""^

unchanged.

Support for a similar conclusion is found in a

study by Douglas [20]. Ha examined annual returns and

variance of returns for 616 securities over tha period

1947-1963 in an attempt to datarmina whether or not tha

market places a positive price on risk-bearing. His

findings reveal that investors who take tha greater risk

tend to receive a somewhat higher return, although questions

can again be raised about the level of returns for tha

high risk securities relative to tha returns from securi

ties of low risk.

Sharpa and Cooper [68] proposed a methodology

similar to that of Pratt's in their research to examine

tha risk-raturn relationship. Their objective was to

determine if high risk securities, as measured by high

levels of nondivarsifiabla risk over historic market periods,

tend to exhibit a similar risk in tha subsequent period

and at the same time provide tha investor with high returns.

A risk factor was calculated for each of tha 1,572 securities

For a definition of this term sea Sharpa [ 66, p. 84]

17

in their sample over tha preceding sixty-month period, and

then each security was sorted into risk-return classes on

the basis of thair respective risk. This procedure was

repeated for each year of tha 1931 through 1967 market

period.

The measure of risk employed by tha authors is

"market sensitivity," a term which thay use to denote tha

slope of tha regression equation relating price changes on

a security or a portfolio to a market index. Deviating,

somewhat, from previous research, the measure of parformanca

used in the analysis excluded tha dividend yield as a

determinant of beta for individual securities. In thair

opinion, the major portion of variation in returns is

attributable to changes in price, the dividend yield

remaining relatively constant over time. On this basis

it would make little difference in measuring performance

and calculating beta coafficiants if tha dividend yield

were omitted.

To test tha importance of excluding dividends as

a determinant of parformanca, the return measures for each

security ware calculated by both procedures. Betas ware

computed for both returns and than regressed against each

other. The results ware vary similar and resulted in the

following regression aq[uation:

Beta = .004 + .997 (Market Sensitivity)

The Coefficient of Determination (R^) = .996

18

The results confirmed that as a practical matter,

dividend yield could ba excluded in calculating tha per

formance measure, and that "market sensitivity" was a

suitable substitute for the mora traditional method of

calculating beta.

The conclusions of Sharpa and Cooper's research

indicate that thara is substantial stability in the risk

characteristics of individual stocks, and that securities

believed to ba of tha highest risk in tha historic period

have a tendency to remain tha most risky in future periods,

and to soma extant provide tha investor with greater

returns.

Black, Jensen, and Scholas [6], and Soldofsky [lO]

uncovered a similar relationship between risk and return.

The first study, which dealt mora specifically with testing

the capital asset pricing modal, also constructed risk-

return classes on the basis of beta and monthly returns.

Using historic observations that ranged from twanty-four

to sixty months to determine tha appropriate risk classifi

cation of each security and accepting tha assumption of

beta stability, tha authors proceeded to rank securities

on the basis of thair calculated risk and compared tha

returns for tha various portfolio classifications.

The second study utilizes a classification procedure

based on invastmant advisory service ratings to group

securities and evaluates thair performance. Corporate

19

bonds, preferred, and common stocks ware evaluated and

comparisons made between risk and return for holding periods

of five, eight, and sixteen years. In this study savanty-

five industrial stocks ware classified into six quality

classes for comparison of risk and return.

The general conclusion of the two research efforts

was that high risk securities, on tha average, seam to

reward the investor with high returns, although both

studies tend to question the level of tha increase in

returns relative to the increase in risk.

In related research specifically devised for testing

tha Capital Asset Pricing Modal, Jacob [29], Millar and

Scholas [49], and Blume and Friend [s] concluded that tha

relationship between risk and return appeared linear and

positively related. However, tha question was again raised

about the laval of tha increase in return relative to tha

increase in risk.

Wagner and Lau [77] evaluated tha returns on diver

sified random porfolios of one to twenty securities for

holding periods of five and tan years over tha total market

period of 1960-1970. The major thrust of their research

was to determine how diversification can be used to offset

the individual riskiness of securities. The results of

their study confirmed that high risk portfolios, on tha

average, performed significantly better than low risk

portfolios. However, thair research ravaalad that in some

20

periods, e.g., 1965-1970, the returns from risky portfolios

were not high enough to preserve tha expected linear

relationship that is believed to prevail batwaan risk and

return.

An article published in January of 1974 by Robert A.

Levy [36] examined tha relationship between risk and return

by investigating tha ability of beta coefficients to predict

security returns. Using weakly returns for 500 securities

over tha period 1960-1970, Levy computed a ona year

historical beta to classify securities into deciles or

portfolios for return comparisons over tha following

calendar year.

Portfolio ona was constructed to consist of those

securities with tha 50 lowest betas; tha second portfolio

consisted of the next 50 lowest beta securities, at cetera.

Return comparisons ware made for each of the nine test

periods (calendar years) to datarmine tha relative par

formanca. Levy hypothesized that high risk securities

will return mora than low risk securities whan tha market

trend is up, and will lose more than low risk securities

when tha market trend is down. In other words, betas and

returns should ba positively correlated in bullish markets,

negatively correlated in bearish markets, and uncorralated

in a flat market. Results from tha analysis on the nine

calendar years supported his hypothesis in four periods.

In two periods an opposite hypothesis was supported; two

21

periods show insignificant performance; and one period

depicted negative correlation in a flat market.

In an extension of the analysis Levy examined the

ability of beta to predict single security returns over

specific market periods in which tha Standard and Poor's

500 Index exhibited either bearish or bullish trends.

Tha market periods used in this part of tha analysis ware

as follows:

Bear Market Periods

12/29/61 - 6/22/62

2/11/66 - 10/07/66

11/29/68 - 5/22/70

Bull Market Periods

6/22/62 - 2/11-66

10/07/66 - 11/29/68

5/22/70 - 12/31/70

The results of tha analysis confirmed, for tha

most part, that security returns and betas ara associated

in tha manner expected but not without soma reservations.

The correlation coafficiants for the bear market periods

ware -.31, -.22, and -.40 with a significant "t" statistic

in each case. In tha bull market periods the coafficiants

were .06, .10, and .04 but tha "t" statistic was only

significant in the second period.

22

Results were also tabulated for portfolio returns

and betas in an effort to evaluate the ability of betas

to predict returns. Tha results ware similar to tha former

analysis only much stronger at the portfolio laval. The

correlation coefficients for tha tan portfolios in tha

bear market periods ware -.91, -.93, and -.95 with signifi

cant "t" statistics in all periods. In tha bull market

periods, the coafficiants ware .45, .42, and .29 with only

the second period "t" statistic significant.

The conclusion reached by Levy was that beta

coefficients are axcallant predictors of return when the

market trend was bearish, but tha test results proved

inconclusive during the' bull market periods.

Two authors in particular tend to refute tha

generally accepted proposition of a positive relationship

between risk and return. Morton [52] and Richardson £59]

have concluded that thara is no reason to believe that

investors who take greater risks will necessarily ba

rewarded with higher returns.

Evaluating the returns on Standard and Poor's

industrial stocks for tha years 1956-1968 and using price

volatility as tha measure of risk, Morton concludes that

tha proposition that high volatility means high profits

has no substance in theory or fact. Tha period from

1956-19J65 was used to datarmina the risk of each security

23

which Morton calculates by means of a "market-price ratio."

Yields were determined from tha thraa year holding period

of 1965 through 1968. Each security was grouped according

to its risk, and a regression was performed relating yields

to the market-price ratios. The results indicate that there

was no statistically significant relationship between tha

two variables.

Morton contends that investors ara confused between

the relation of risk to "ax ante" or anticipated return

and the relationship of risk to "ax post" returns. Data

are available to show that tha "ax ante" expectation of a

positive relationship batwaan risk and return is, in fact,

unsupported. Tha actual return on a security that is

realized by tha investor is not necessarily commansurata

with tha associated risk.

Richardson offers a similar conclusion in discussing

soma limitations of tha empirical avidanca offered by

fellow researchers. Richardson, focusing on a lack of

conclusive data and inconsistencies of developing logic

in the risk-raturn hypothesis, developed an interesting

and logically concaivad investment strategy based on how

Tha "markat-prica ratio" is calculated by dividing the highest yearly average market price by tha lowest yearly average in tha 10 year base period (e.g., if a security had an average yearly low price of $10 in 1958 and an average yearly high price of $40 in 1965, tha ratio would be 4).

24

investors should react if the hypothesis had any practical

validity. He contends that if investors, on the average,

can realize higher returns by taking greater risks invest

ment funds would pour increasingly into low quality, high

risk securities. Such a strategy would tend to raise tha

price of low grade high risk securities relative to high

grade low risk securities. Such a strategy has not developed

in tha industry thus far, and thara is no indication that

such a change in investment activities is currently under

way. His conclusion is that tha findings to data in support

of tha risk-raturn hypothesis should ba regarded as

inconclusive.

Although the risk-raturn' hypothesis is not accepted

in total, a preponderance of research generally accepts

the concept. Most studies have concluded that a linear

relationship is an approximation of tha association between

risk and return. With tha exception of Levy, limited

research has been undertaken to datarmina the relationship

between risk and return over market periods of specific

trend. Tha major portion of related research examined tha

risk-raturn relationships over extended time periods dis

regarding market trend considerations. Levy's research

considered specific market trends but was limited, for tha

most part, to an evaluation of tha laval of correlation

between tha two variables for tha purpose of determining

the ability of beta to predict return.

25

The objective of this dissertation is not only to

examine tha pattern of returns for tha ten risk classifi

cations, but also to datarmine the specific origin of any

difference in returns for any two risk classes over

specific market periods that advance and decline. In

addition an investigation is made of tha increase in

returns relative to tha increase in risk. Tha purpose of

this analysis is to examine tha question of whether or not

the risk-return tradeoff is proportionate among tha various

risk classifications. This question has bean raised by

a number of rasaarchars and is unsettled even among those

who currently accept tha risk-raturn hypothesis.

CHAPTER III

METHOD OF RESEARCH

Tha Data

The data examined in this dissertation consisted

of 250 New York Stock Exchange securities for which complete

data were available for tha eight-year period considered

in this analysis. Following an earlier attempt to calculate

the performance data based on monthly returns, it was

believed that the reliability of tha research could be

improved if a greater number of observations was used.

Due in part to tha relatively short length of time covered

by ona of the market periods, a decision was made to base

the research on weekly closing prices and dividend data.

To procure the weakly data tha securities ware

screened from an Investment Statistics Laboratory (ISL)

data tape which, for the most part, was complete through

1969. In order to update tha tape through June, 1970, the

end of the fourth market period, price and dividend data

were manually collected from ISL books and merged into tha

original data sat to fill gaps and extend tha data tape

to cover the eight-year market period that was used for

the research.

26

27

The Market Index

The index of market performance that was used in

the analysis was calculated from tha weakly closing price

of the "Standard and Poor's Composite Stock Index."

Dividends were excluded in computing tha parformanca of tha

index, dua mainly to tha problem of determining tha weak

in which tha dividend should ba included. In measuring

performance, tha most accepted technique is to consider

both aspects of return, price appreciation and dividend

yield. However, Sharpa and Cooper [68, p. 49] state that

most variation in tha return of equity securities is

attributable to changes in price while tha dividend yield

remains relatively constant over time. This would infer

that dividends could ba excluded in tha calculation of

the performance measure and have a minimal affect on tha

results.

The Standard and Poor's Composite Stock Index was

selected as the measure of market performance dua to its

size and tha variety of securities it contains. Although

other indexes could have baan selected, tha decision was

made to use this index on tha basis of its repeated use

in related research throughout tha literature.

28

The Risk Measure

Following tha initial studies of Markowitz [45]

and Tobin [ 75] , literature on tha subject of risk expanded

rapidly. Tha advantage of representing soma element of

risk, as well as returns of an investment alternative,

has by now been widely accepted.

Markowitz and Tobin originally suggested variance

as the appropriate measure of risk in representing tha

undesirable aspect of an investment decision. As port

folio theory davalopad/ most of the authors showed a

preference for variance as tha proxy for risk. Foremost

of thasa was William F. Sharpa, who, while focusing on a

limitation of variance, tha high cost of its derivation,

was able to reduce the complexity of computing tha risk

for a portfolio. By proposing certain assumptions about

securities and thair relationship to tha market, Sharpa

[62] , was able to develop a surrogate for variance that

greatly simplified tha measure of risk for a diversified

portfolio. Tha proposed measure, which has baan referred

to throughout the literature as tha "beta value,"

"systematic risk," "rasponsivanass coefficient,"

"volatility" or "coefficient of non-diversifiabla risk,"

has grown in popularity over tha past tan years.

The measure of risk that was used in this disserta

tion was the coefficient of non-diversifiabla risk, or

29

what is more commonly called tha beta coefficient in

Sharpa' s index modal .•

In recant years academicians have shown a praferanca

for using beta as a measure of portfolio risk.^ It was

for this reason, in part, that beta was used as the proxy

for risk in this dissertation. The other reason was that

tha risk classes, explained later, which ware used in

evaluating tha risk-raturn hypothesis resembled a wall

diversified portfolio and ware constructed from a ranking

of the beta coafficiants of each security.

Tha Index Modal of Portfolio Theory

Sharpa [62], drawing from Markowitz [45], suggested

that tha return from a risky asset can ba represented

through a linear relationship with market factors and the

individual characteristics of the asset. Tha general

relationship can ba stated as follows:

Where: R-jt ~ return on security j in time period t.

a . = constant, tha return axis intercept.

Saa for example the comments of Block [7], and tha articles by Levy [36] , [37] , Sharpa [62] , Black, Jensen, and Scholas [6], Traynor [76], and Sharpa and Cooper [68] .

30

bj = tha slope of tha regression line

relating R.^ to changes in I (defined

as COV (Rj/I) / VAR (I)).

I^ = the value of I (market factor) in

time period t. Generally raprasantad

as the return of a market index,

ejt = a random variable with a mean of

zero and a variance of V ..

It is also assumed that tha a-'s ara independent of tha

level of I^ (i.e., COV (a.,I.) = 0), and is characteristic

of a unique aspect of security j.

By rewriting aquation (1) in terms of expected

returns tha expression becomes.

E(Rj^) = aj + bj (E(I^)) (2)

and the variance of (R.) can ba expressed as:

Vj = bj(I) + Vaj (3)

When tha risk of a security is stated as in

equation (3) it becomes clear that tha measure of total

variability is an additive function of two components.

The first term in (3), bTV(I), represents tha

portion of variability attributable to a security's

relationship with tha market index which cannot ba diversi

fied away, the "systematic risk." The second term in (3),

31

Vej, represents a measure of the unique characteristics

of a security and is independent of market factors, tha

"unsystematic risk." Since V(I) is tha same for all

securities, bj alona will represent tha relative systematic

risk of security (j).

The variance for a portfolio of n securities can

then, be datarminad by tha following equation:

n n V(Rp) = ZX.b.-^^d) + ZlX^a. (4)

^ j=l J J j=l J J

Where: R = tha distribution of portfolio returns.

X. = tha proportion of tha portfolio

invested in tha j security.

Sharpe [66j shows that tha "unsystematic risk"

(Ve .) of a security can ba substantially reduced or

neutralized by diversification to tha point that it can

be omitted in evaluating the riskiness of a well diversified

portfolio. This leads to tha conclusion that tha second

term in (4) can be dropped, leaving tha first term which

will serve as a reasonably good approximation of portfolio

variance. Tha result, tha "beta coefficient," now saams

to be tha most widely discussed measure of portfolio risk.

Measures of Return

The conceptual definition of a security's return

employed in this dissertation is tha holding period return

32

as defined by Latane and Tuttle [ 34, p. 59] . In this

context, the measure is considered to ba a "relative gross

return" calculation. It considers all benefits that are

likely to accrue to the investor over the holding period,

relative to what was originally invested.

The holding period return is calculated as follows:

"PR Pt Pt Pt ^ ^

Where: D. = tha dividend to be received during

period t.

P^ = the price at tha beginning of period t

P.^1 = tha price at tha end of period t+1.

Arithmetic Mean

The return data for each security were annualized

before a comparison of returns was made batwaan different

risk classes. The data were converted on the basis of the

following equation:

n

tir'-j R . = \ \_i -1/ (N) = \ ^ ^ J " / (N) (6) aj

Where: ^aj ~ arithmetic mean annualized HPR for

security (j) in market periods (1-4).

33

n Z HPR . = sum of the weakly holding period t=l -

returns for security (j) in each

market period,

n = number of observations par market

period.

N = number of weeks par year.

Geometric Mean

Performance data ware also computed by using a

geometric mean of tha holding period returns for each

security. Levy and Kripotos [38, p. 28] raised doubt about

tha use of an arithmetic average in dealing with security

performance. The authors questioned tha usa of tha arith

metic mean because:

The arithmetic average of price relatives assumes an equalization of tha amount invested in each component stock every time the average is computed. What is naadad is a measure which reflects continual equalization disregarding time intervals. . . . A geometric average weights each security equally, tha investment in each security is continually evened up, and a given percentage change in the price of ona stock has an identical effect on the average.

The geometric mean is defined as tha "n"^"" root of tha

product of "n" numbers.

GX = V (HPR^) (HPR2)"(HPR^) (7)

Holding period returns were computed in tha conventional

way, and tha geometric mean of these returns was used to

34

compute the individual performance data for each security.

The geometric mean weekly holding period return, minus 1

times (N), annualized returns for this part of tha analysis.

All weakly return data ware converted into annual aqiaiyalants

so that tha HPR's, which ware computed from market periods

of different length, could be stated and compared on a

common annual basis.

Pure Yield

A third measure of return was used in tha analysis

for tha purpose of evaluating the incremental increase in

return par unit of risk. (Questions have baan raised by a

number of researchers about tha increase in return relative

to the increase in risk. In order to investigate this

aspect of the risk-raturn hypothesis, a direct analysis

was made to datarmina if the increase in return was

sufficient to keep tha "price of risk reduction" unchanged.

The return measure that was davalopad to permit an analysis

of this concept was tha "pura yield."

The pure yield was calculated following tha basic

approach of Traynor [76]. Tha following aquation defines

Treynor's index of portfolio parformanca in terms of the

pura yield.

^p - r Py = • \ - (8)

35

Where: R^ = average return on portfolio (p).

r = riskless rate of interest. Represented

by tha average yield on Treasury Bills

for the period of this analysis.

B = beta coefficient of portfolio (p). p

Treynor's parformanca measure is essentially an

adaptation of the Capital Asset Pricing Model (CAPM) and

provides a convenient standard for measuring parformanca.

In equation form tha (CAPM) can be represented as follows:

E(R ) = R^ + B (E(Rm) - R^) P r p r

(9)

Where: E(R ) = expected return on a portfolio.

R- = a riskless rata of interest.

B = beta coefficient on a portfolio.

E(Rm) = expected return on a stock index.

Essentially the modal hypothesizes that tha axpactad return

on a portfolio should exceed tha riskless rate by an amount

proportionate to tha magnitude of beta. If stated in terms

of tha return above tha riskless rata, tha risk premium

on a portfolio should increase proportionately to tha

increase in beta.

Eq[uation (8) states tha return in excess of tha

riskless rata, or the risk premium, in terms of the

associated level of risk. Thus, the pura yield provides

36

a direct comparison for determining performance for

portfolios of different risk.

Pure yields could not be computed for individual

securities because of tha problem encountered in normalizing

whan a security has either a zero or a negative beta. This

problem was not prevalent whan computing a portfolio's

pure yield as tha negative or zero beta of a single stock

would "wash out" whan combined with a group of securities.

Tha Market Periods

The base period for this study encompassed 412

weeks of stock market activity for tha period July, 1962,

through June, 1970. Weakly prices and dividends ware used

in determining tha parformanca data for each security so

that tha number of observations involved in calculating

tha performance variables for tha different market period

could ba increased. This was dona in an effort to generate

reliable measures of risk and return. Because tha ranking

criteria used in this analysis was dependent on tha beta

coefficient of each security, it was important that thair

values ba determined by an adequate number of observations.

This was particularly important to this research since

In an earlier attempt to datarmina tha beta coefficients using monthly observations, it was found that many of the securities in tha shorter market periods had betas that ware not significantly different from zero as measured by a "t" statistic.

37

the second market period included only eight and ona-half

months of stock market activity. Although a required

minimum number of observations is not expressed in tha

literature, most of tha related research employs a range 5

of twanty-four to sixty observations.

To gain an insight as to how securities from

different risk classes perform under advancing and declining

market conditions, tha base period for this research was

segmented into four subpariods. Tha subpariods ware

determined by examining the Standard and Poor's 500 Average

for extended periods of time in which tha general trend of

tha index either advanced or declined (saa Figure 1). This

lad to the determination of the following market periods.

Market Periods

1

2

3

4

Weeks

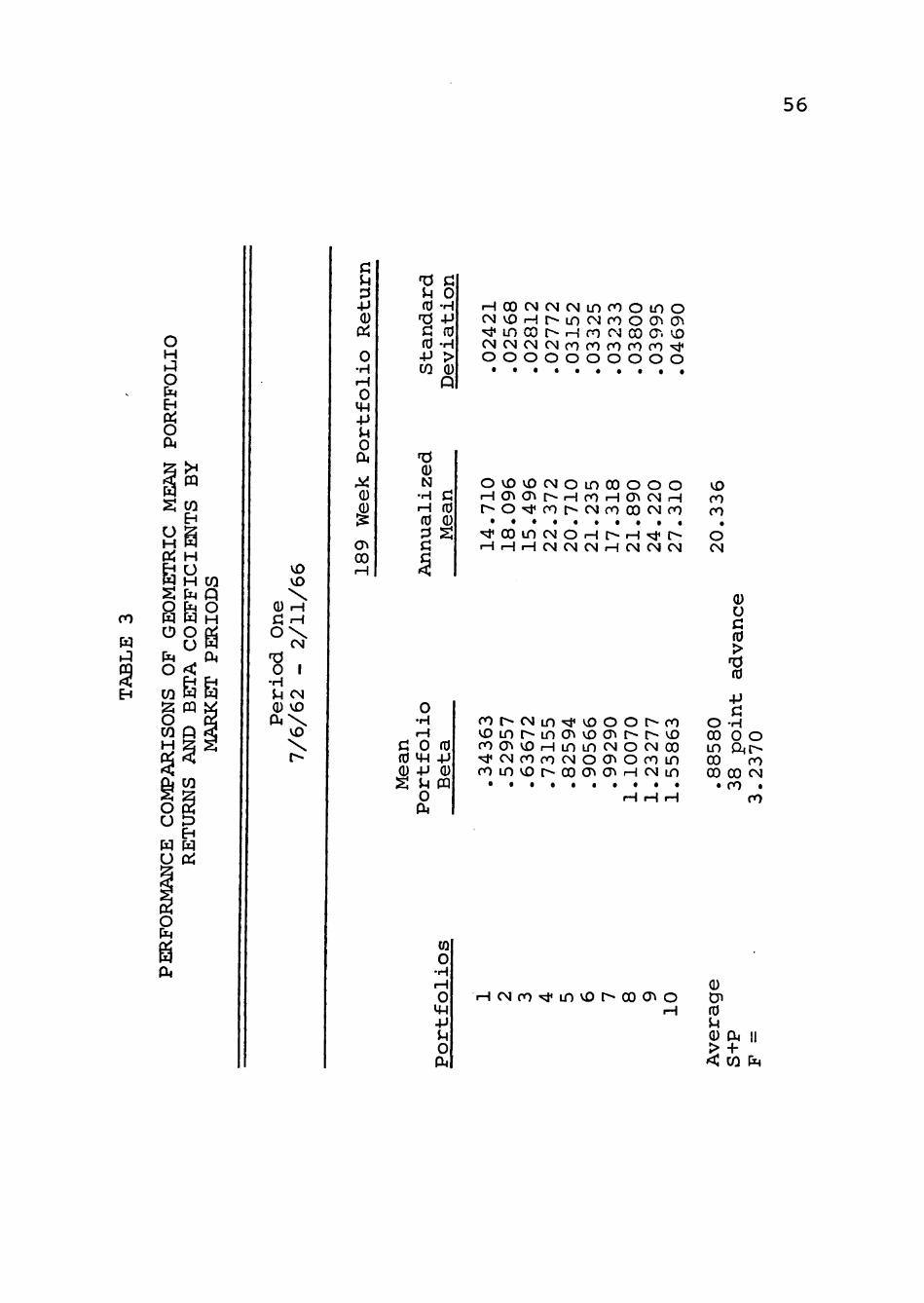

7/6/62 - 2/11/66

2/11/66 - 10/7/66

10/7/66 - 11/29/68

11/29/68 - 5/22/70

Duration (Weeks)

189

34

112

77

Trend

UP

DOWN

UP

DOWN

Data were also available to examine tha long run relation

ship batwaan risk and return by calculating parformanca over

For example saa tha studies by Black, Jansan, and Scholas [6] , Sharpa and Coopar [68] , Pratt [58] , and Levy [36] .

38

STANDARD & POOR'S 500 AVERAGE

1962-1970

Source : F o r b e s , August 15 , 1973 , p . 96

F igure 1

39

the entire eight year period. This was done as the fifth

market period over tha following inclusive dates.

Market Duration Period Weeks (Weeks) Trend

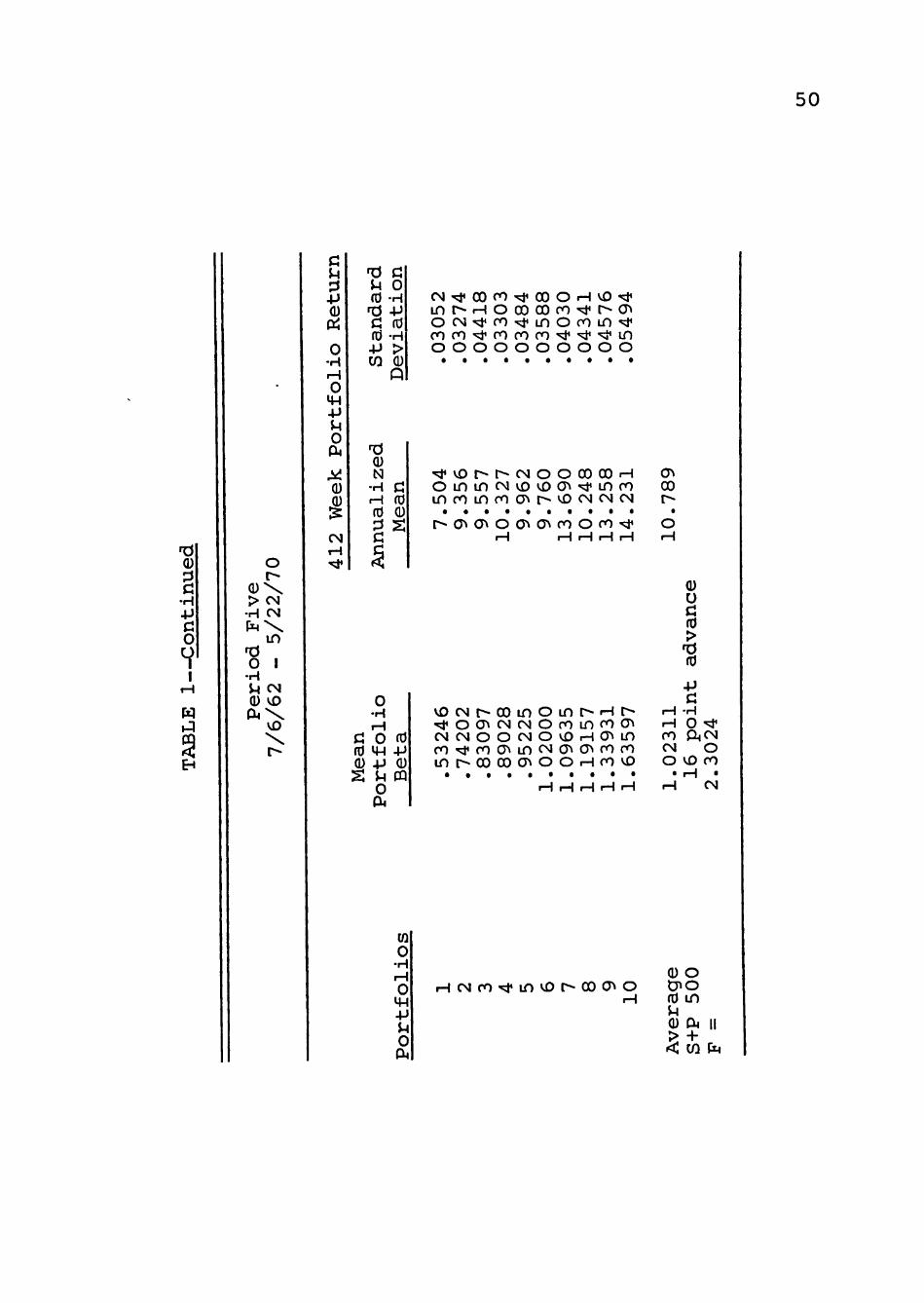

5 7/6/62 - 5/22/70 412 UP

- Tha Risk and Return Classes

To examine the nature of the risk-raturn hypothesis,

tha performance data used in tha analysis ware divided

into dacilas in each of tha four market periods. Tha

division was accomplished by comparing tha risk measure

of each security. Beta coafficiants were calculated for

all securities in each of the market periods, and than

each security was rank-ordarad from the lowest to tha

highest beta value. The arrays ware partitioned into risk

classes (deciles) such that risk class one contained the

twenty-five securities with tha lowest betas while tha

nine remaining classes became identified with succassivaly

higher betas. Since tha composition of each risk class

was determined solely by tha magnitude of tha beta

coefficients for tha raspactiva securities, and the size of

tha sample was large, each group of securities comprising

the ten risk classifications was analogous to a portfolio

containing twanty-fiva securities.

To datarmina tha returns for each risk class, tha

weekly holding period returns from tha securities within

40

each portfolio ware calculated as described earlier. Tha

mean holding period return for every security in each

market period was calculated and annualized so that for

any risk class there ware twanty-fiva return observations.

A diversified portfolio with a high beta value is

more risky than a portfolio with a low beta value. In

accordance with tha risk-return hypothesis tha high risk

portfolio should also provide a greater return. Portfolios

with varying degrees of risk can easily be constructed

by combining stocks of similar risk as outlined above.

Securities with high betas should have high returns on the

average and ware combined to represent a high risk portfolio

Low beta securities ware similarly combined to represent

a low risk portfolio. This strategy should provide low

returns, on tha average, but with much lass risk exposure.

Test of Hypothesis

Portfolio Returns

Evidence relating to tha actual tradeoff batwaan

the various portfolios in the four market periods was

obtained by examining the test results of tha following

null hypothesis:

(A) There is no significant diffarance between tha

mean returns for tha tan risk classes within

each market period.

41

The ultimate objective in testing the null hypoth

esis was to determine if there ware significant differancas

in tha risk-raturn tradeoffs within market periods, i.e.,

do high risk securities provide higher returns compared to

low risk securities under advancing or declining market

conditions.

To test the null hypothesis an application of

analysis of variance was used. Tests ware conducted to

determine if a significant diffarance existed between tha

mean returns of tha ten risk classes within each market

period. Tha test for hypothesis (A) was repeated five

times, once for each of tha four market periods and once

for tha total eight year period. An F-statistic was

calculated from tha parformanca data of tha tan portfolios

for each market period, and tha differancas ware determined

to be statistically significant if tha computed value of

F exceedad tha F-distribution value in the table for tha

appropriate degrees of freedom. If the computed F-valua

was greater than tha F-distribution value in tha table

than hypothesis (A) was rejected.

In tha avant that tha null hypothesis was rejected

in any or all market periods all that could be proven by

the analysis thus far was that a significant difference

existed batwaan tha mean returns of tha tan portfolios.

No information was available to show which portfolio

returns ware statistically different from all others.

42

To investigate the significant diffarance in port

folio returns tha Duncan Multiple Range Test^ was used to

determine batwaan which portfolios tha differancas occur.

The results of this test allowed conclusions to ba drawn

about significant differancas in tha mean returns of each

portfolio compared to all others for a given market period.

The return comparisons for each portfolio was made as

follows: 1 vs. 2, 3, 4, 10, 2 vs. 3, 4, 5, .... 10,

3 vs. 4, 5, 6, ... 10, at cetera, for a total of tan

replications. Tha test was conducted two times, once when

performance was measured by tha arithmetic mean holding

period return, and again whan parformanca was datarminad

by tha geometric mean return.

Results from tha Duncan Multiple Range Test provided

information to datarmina whether or not there was a

significant diffarance in tha mean returns of large groups

of securities as tha laval of risk increased in market

periods charactarizad by advancing and declining trends.

The Duncan test was selected to compare portfolio par

formanca since it appears frequently throughout tha litera

ture and is considered a good test for describing signifi

cant diffarance batwaan paired data.

For a discussion and explanation of tha Duncan Multiple Range Test, see Hicks [27, p. 31] .

43

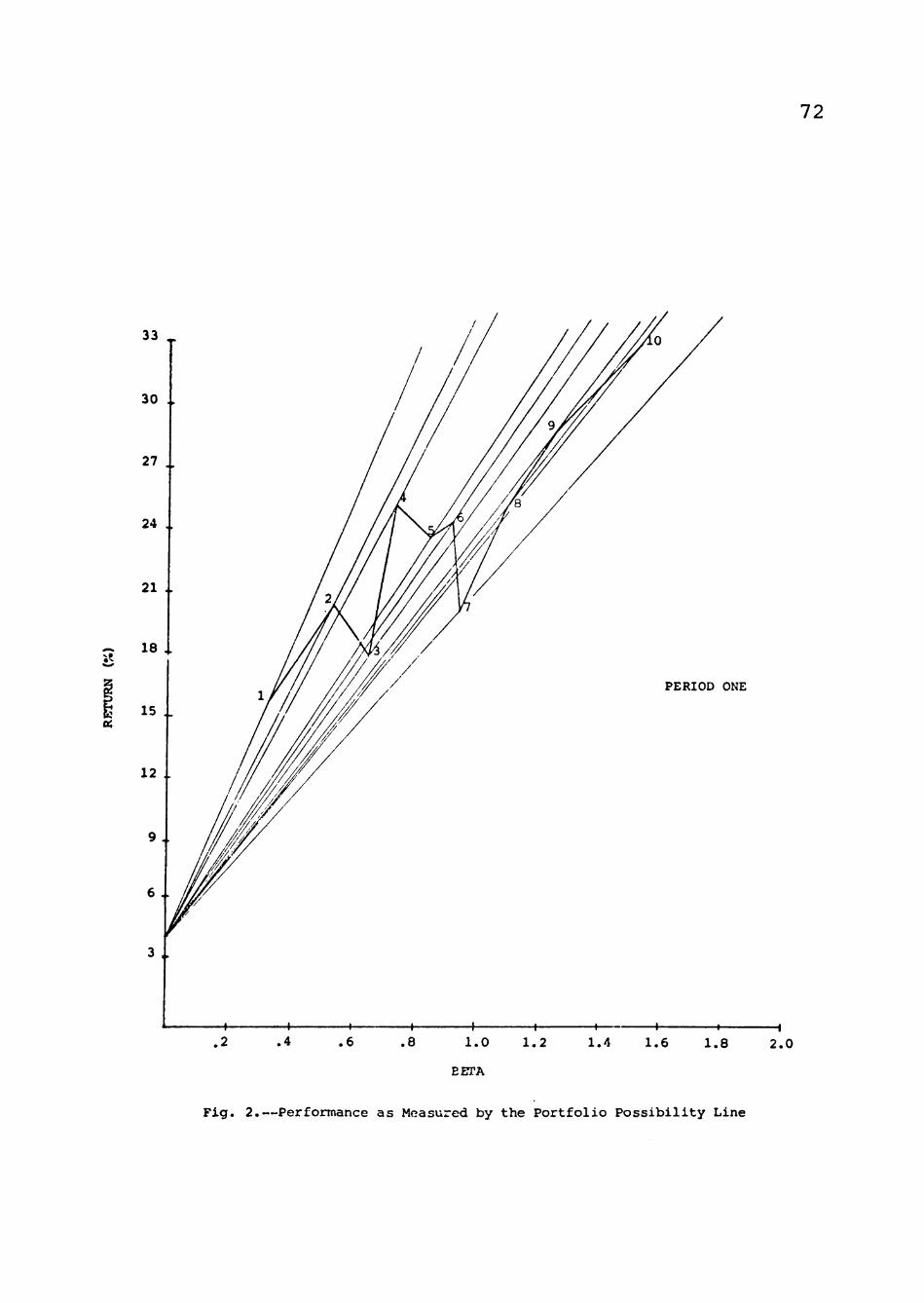

Pure Yields

In an attempt to disclose tha full nature of tha

relationship between risk and return for tha period of

study the analysis was extended to consider tha results

of the pure yield performance. The examination of portfolio

pura yields was made through a graphic presentation

following tha basic approach of Traynor [76]. A plot

which related portfolio returns to beta, above tha riskless

rata of interest, produced a relative ranking of tha

performance of each portfolio. Tha slope of tha "portfolio

possibility line" which represented tha measures of risk

and return for each portfolio reflected its relative

performance. Tha portfolio possibility line with tha

greatest slope pointed out tha portfolio whose parformanca

was best in terms of the return par unit of risk. If the

tradeoff between risk and return is identical, or if tha

price of risk reduction remained unchanged, tha portfolio

possibility line of each portfolio would plot tha same.

In subjecting tha data to tha aforamantionad

analysis it was baliavad that information could ba compiled

to provide a basis for determining tha actual relationship

7 Traynor uses tha term "portfolio possibility

line" to represent the risk and return tradeoff available to tha investor by combining different proportions of tha respective portfolio and tha riskless asset.

44

that existed between risk and return for tha period of

study.

CHAPTER IV

THE FINDINGS

Chapter II suggested that there is a lack of total

agreement regarding the relationship between a security's

risk characteristic and its return. Tha majority of

research indicates, however, that the predominant relation

ship is of a positive type. Risk and return ara, to soma

degree, positively correlated and return is expected to

increase as a function of risk. Tha implication of this

relationship is that as the riskiness of a portfolio

increases tha return will increase to compensate investors

for their greater risk exposure.

This chapter presents the research findings as thay

apply to the risk-raturn relationship described above.

The chapter is organized into three major sections:

(1) the relationship batwaan risk and return, (2) the pure

yield performance, and (3) tha relationship of beta

coefficients.

Relationship Between Risk and Return

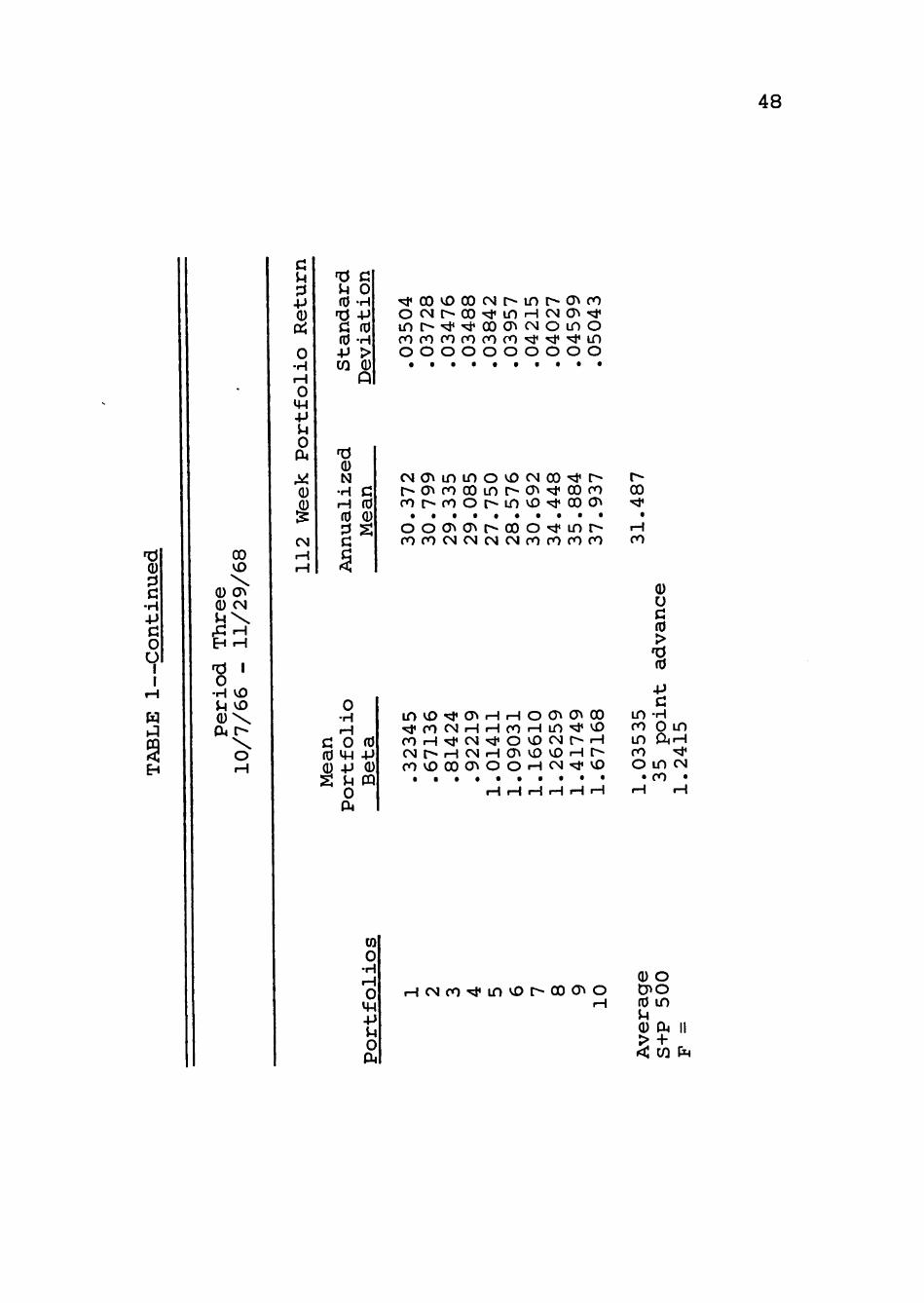

Table 1 presents summary data that describe tha

risk-return relationship for the ten portfolios over the

five market periods. The mean portfolio beta is paired

45

46

(A

Q) G O

vO vD \ rH rH

CVI

O I •H M CN 0 VD a 4 \

VO \

G U 7i 4J Q) Qd

O •H H O M-l +J U O

cu M

OS CX)

'd G u o

(0 4J W 0

Q

13

N

G

o •H iH

c: o fd fd M^ 4-> <D -P Q) X UtA

o a*

m o

• H H 0

o

CM 00 CN CM vD iH • d* in CO cr> iH

r- CM in ro o LD ro 00 in CN CO o a» 00

ro CN 00 (T* vD CMCNCNCNcorororo O O O O O O O O O O

rOCMvOvO<r>(T><T>OOCMO f M r H r O " ^ ( T > C M r H r ^ r H v D C N O O i n r - C N H O v O - ^ C T *

v o c r » r ^ " ^ r O ' s t o i n o o c M r H H i H C N C N C M C N C M C M C O

r o r ^ c N i n ^ v D O O r ^ r o vDlnr^ lncJ^voo^r-r^vD rocT>vDHinincNOCNoo ' ;J 'CNrocoCMOCJ^O^OLn coinvor-oocr><r>rHCNLr)

i H C M r O - ^ i n v O t ^ O O C T ' O

CM 00 CN

• ro CN

0 u G fd >

fd

-p G

• H O ' ^ ftCN

OS

o 00 in 00 00 00

• ro in

0) o

fd in u Q) PK II

< CO P4

47

(D ? G

•H +» G O

I

rH

W

VD

go TJ r o

•H vD J-i VD

CM

G U J3 4J 0

cn o

• H H O

M-l • P U O QH M Q)

i en

-0 G U 0 fd -H TJ -P c fd fd -H 4J > W 0

rOOCT>(T»VDOO"^OOCNCM r - c N v O ' ^ r o i n c N i H C J N i n O O v O H ' ^ H v D H r - C N t H CM CN f O CO r o CO 'si' -^i LT) vO O O O O O O O O O O

0 N

- H C H fd fO 0

o •H iH

C O fd UH 0 4J

^ ^

fd

0

Ui O

• H rH

o MH • P O PU

CT>OvDinCTvCNOrorovD r * - o v D C j \ i n ' > * i n ( T > o o ^ O O O v D i ^ l n C 3 ^ c N ( 3 ^ r - r o

i n c M " ^ " ? t v D r H r o i n i n c N r o r o r O ' s j ' r O ' ^ r o r o c N r o

I I I I I I I i I I

00 CM 00 ^ vD r» CO ro r» ' 00 00 in C3 ro ro CO a> O '* O rH iH "^ ro (T> r^ ro in VD r^ 00 o

CM 00 'l' r^ VD in in -^ vD

ro in "^ ro CM -< r^ CN

• t • t

H rH rH CN

r H C M r O ' s t i n v D r - O O f T ' O

rH vD ro •

in ro I

r-ro '^ 00 o

0 G •H H o 0 'd

4J G •H O O Oicn

i> vD c^ ro •

0 O D^O fd in u 0 PU

< W PM

II

48

0

G •H +J G O U

I I

bH

00 VD

0 CJN 0 CM

Xi H EH H

•H iH 0 04

VD VD

O rH

G U :A • p 0 txi o •H H o

14H 4J O

TJ C J 0

fd -H d -p c fd fd -H •P > W 0

Q

' * O O v D O O C M r ^ i n t ^ C T > r o O C M r - 0 0 ' ^ L n r H C N C 3 ^ ' < * in r - "<* '<*00( r>cNOino r o r o r o r o r o r O ' ^ ' s f ^ i n O O O O O O O O O O

CU

M 0 0 ^

CN rH rH

TJ 0 N

•H C H fd fd 0

2 S c 1

0 -H H

c o fd fd m -p 0 4J 0

m

CO o

• H rH O m -p o Pl4

cNCTkininovDCMoO'^r--t^C3^rooOLn^^CJ^^OOro ro r - roOr - invD 's^OOCT*

oocT>CT»r^ooo - ^ i n r -rorocNCNCNCNrorororo

invO';j'CT>rHrHocrkcy^oo • < ; J < r O C M r H r H r O r H i n " ^ V D r O r H ' ^ C N ' ^ O v D C N r - r H C N t ^ r H C M r H C T v v D v D r H r -r O v D O O < T > O O r H C N ' « * v D

• • • • • • • • • * rH rH rH rH rH rH

rH CN ro "^

00

ro

in ro in ro

0

u G fd > 'd fd

+J G

•H 0 in ftrH

' ^ O in CN

* ro •

vD r^ 00 <3> o rH

0 O D > 0 fd in U 0 QA II

> + < W P4

49

0

G •H 4J G O

I

tA

O

in CN :3 CM 0 \ P4 i n

? •H 00 U VD 0 \

CN \

G U

4J 0

o •H rH o m -p

o

M 0

I

JH fd

f d -P

fd • P W 0

0 N

• H rH (d 0

o •H rH

c o fd fd UH 4J 0 -P 0 S SH ffl

O 04

CO O

•H rH

o ^ o 0*

CM rH VD O ^ o ro St* o o

VD ro 00 VD VD H O H vD r^ ro ro ro O O O

00 -^ (T> O O CN -^ ' ^ "^ ' ^

o o o

in o OS (N OS in •^ vD o o

i n O O O r - r O r H C M r o v D r o rHro in inmvDvDooOnH rHOr*rorHoovDcr»t^ in

• • • • • • . • • * cr>roooinvD"^c^r«cy>oo r H C M r H C N C M C M C N r O C M - « ; i ' I I I i I I I I I i

rHro(T»cr>vD'sj<Lnin<Hr^ rovD(T»rorHoOincNino O C M r - r O C N v D ( T > i n O C N r o v D v D ^ C M c r > O O r - ' * r o inr-oo(j>oorHCM-^cr>

rH rH rH rHrH rH

r H C M r o - ^ i n v D r - O O C ^ O

ro H ro

00* CM

I

VD O vD O

0 G

• H rH U 0

+J G

•H O ro 04O

ro vD O

• rH

0 O CHO fd in U

0 04

< Ui U4

II

M iior."-*. T ""

; : . « ^ L:^siA-:

50

0 :i G

•H 4J G o

vA

0 >

• H P4

O

CN CN

i n

O I •H SH CN 0 VD 04

VD \

G U

0 (Xi

O •H rH o m + j JH O

fd c: 4 0

fd -H fd -p c: fd fd -H •p > W 0

Q

CN">;l*COrO'^OOOrHvD'!;i ' inr-HOooooro-^t^cT* O C N ' ; l * r O " ^ i n O r O i n ' ; } * r o r O " « * r o r o r o ' v f ' ^ ' v i * i n O O O O O O O O O O

04

M Q) 0) 12 CM rH

fd 0 N

•H G rH fd fd 0 3 ^ c 5

o •H H

c o fd MH 0 4J S ^

o 04

fd

0

(0

o •H rH

o MH - P iH O 04

•^vDr^r-cMOOOOOOrH Oin incNvDvDcn ' ; f i n ro inroinro(T>r^vDCNCNCM

t ^ a > < T » O C r > ( T k r o O r O ' ^ r H rH rH rH rH

vDCNt^oo inOinc^rHr^ ' s d ' O C J ^ C N C N O r o i n r o c T * C M C N O O C N O v D r H C J ^ l n r o ^ r o C 7 » i n C M < T » ( 3 > r o r o i n r - o o o o c r > o o H r o v D

rH rH rH rH rH

cMrO'stinvDr-oocJ^O H

OS 00

ro CN

o

0 u G fd >

f d fd

• p G •H O '^J' ftCN

O VD ro

• H CM

0 O d^o fd i n u 0 04

< W PM

II

51

with its respective annualized arithmetic mean return and

standard deviation.

In market period one portfolio returns, in general,

conformed to tha expected relationship presented in tha

literature. These data indicated that high risk port

folios returned more than tha low risk portfolios. Returns,

for the most part, increased as the riskiness of tha

portfolios became greater. Tha exception was tha returns

from portfolios three and seven, which, in both instances,

were lower than tha returns of the preceding portfolios.

Returns differed significantly among tha tan portfolios

and generally in the direction anticipated. The computed

F-statistic was 5.19 for alpha = .05 compared to a critical

table value of 1.88 and, consequently, resulted in rejection

of the corresponding null hypothesis, which stated that

there was no significant diffarance batwaan tha mean returns

for the tan risk classes within each market period.

Results of tha Duncan Multiple Range Test, to

determine the specific origin of the differanca in returns,

yielded the following five homogeneous subsets:

4, 5, 6, 8, 9

2, 3, 5, 6, 7

2, 4, 5, 6, 7, 8

1, 2, 3, 7

9, 10

52

An interpretation of tha subsets is that no pair in each

of the five groups of portfolio returns differ by mora

than tha least significant range. In other words, no

statistically significant diffarance existed batwaan tha

returns of the portfolios comprising each of tha five

subsets. There was, however, a significant difference in

the returns of soma portfolios. It was this interpretation

of the range test with which the analysis was concerned.

Table 2 presents a summary of tha comparisons batwaan

those portfolios in which there was a statistically

significant difference in returns.

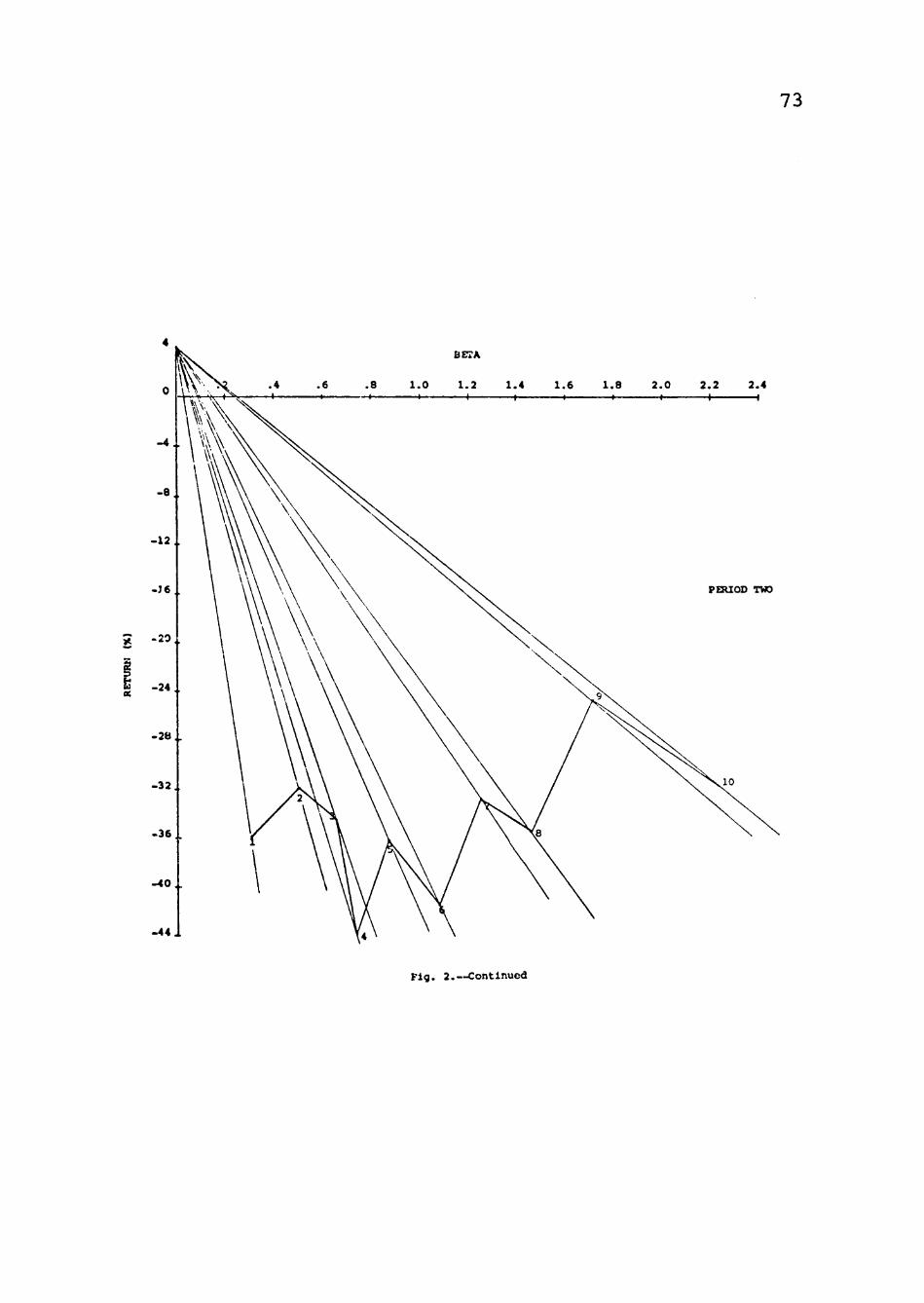

In market period two, a down market, returns did

not conform to tha expected relationship in which low

risk portfolios lose lass than high risk portfolios. Tha

highest negative returns ware shown for portfolios four

and six while the loss on the three lowest risk portfolios

averaged slightly mora, on tha average, than tha three

highest risk portfolios. For the period, returns did not

differ significantly among tha ten portfolios as avidancad

by a computed F-statistic of .97. Consacjuantly, tha

corresponding null hypothesis could not ba rejected. Tha

data ware not subjected to tha range test since no

®Tha value for the least significant ranges (LSR's) is found by referencing a Duncan's Table of Significant Ranges at alpha = .05, using N2 dagraas of freedom for tha error mean square (from an analysis of variance table) and p=2, 3, 4, 10.

53

TABLE 2

Market Period

COMPARISON OF ARITHMETIC MEAN PORTFOLIO RETURNS IN WHICH THERE WAS A

SIGNIFICANT DIFFERENCE

Referenca Portfolio

Portfolios That Vary Significantly From Reference Portfolio

-1 2 3 4 5 6 7 8 9 10

4, 5, 6, 8, 9, 10 9, 10 4, 8, 9, 10 1, 3, 10 1, 10 1, 10 9, 10 1, 3, 10 1, 2, 3, 7 1, 2, 3, 4, 5, 6, 7, 8

1 2 3 4 5 6 7 8 9 10

1 2 3 4 5 6 7 8 9 10

8, 10 8, 10 8, 10 10 10 10 10 1, 2, 3 10 1, 2, 3, 4, 5, 6, 7, 9

7, 9, 10 10

1 1, 2

54

significant difference was found between portfolio returns

for tha period.

A similar finding of no significant difference in

returns was found in the third market period, although

these data saamad to indicate that tha returns of tha two

lowest risk portfolios exceeded the return on portfolios

three through six. The computed F-statistic was 1.24

compared to tha table value of 1.88. Onca again, tha null

hypothesis could not ba rejected. Tharafora these data

were not subjected to analysis by the range test since

portfolio returns were not found to differ statistically

for the period.

In market period four, returns conformed, for tha

most part, to tha axpactad relationship whan the market

trend was down. Generally the lower risk portfolios lost

lass than tha higher risk portfolios although tha relation

ship was not totally consistent. Returns ware found to

differ significantly batwaan the ten portfolios, as evi

denced by a computed F-statistic of 4.03, and this fact

resulted in another rejection of tha null hypothesis.

The results of tha range test yielded three homo

geneous subsets within each of which thara was no signifi

cant diffarance in returns.

1, 2, 3, 4, 5, 6, 7, 9

4, 5, 6, 7, 8, 9

8, 10

55

Portfolios batwaan which thara is a significant differanca

in returns for tha period are presented in Table 2.

Results of tha analysis whan performance was

measured by the geometric mean holding period return tended

to support tha previous findings. In all but tha fifth

market period, discussed later, in which returns were

mixed, the high risk portfolios outperformed tha low risk

portfolios whan tha market trend advanced and low risk

portfolios lost lass whan tha market trend declined.

Parformanca was again datarminad to ba statistically

different in market periods ona and four. In addition,

performance in tha fifth market period was found to ba

not statistically different which conflicted with tha

finding in tha preceding analysis whan returns ware based

on tha arithmetic means.

Table 3 presents tha summary statistics that

described the gaomatric mean parformanca data for portfolio

classifications by market periods. If a comparison ware

made between tha arithmetic and gaomatric mean returns

the results would show that the values ware smaller with

the geometric calculations. This relationship is inherent

due to tha way in which a geometric mean is computed.

In market period one parformanca differed signifi

cantly batwaan tha tan portfolios. With tha exception of

the performance on portfolios two, four and seven, returns

increased steadily as tha risk became greater. Tha

56

ro W ^A

W

P (Xi

VD VD \

0 H G rH o\

CN f d o I

•H iH CN 0 VD 0 4 \

VD \

^

•P 0

o •H rH

o MH +) iH O 04

0

I 00

f d ^ fd

f d -p G fd •p W 0

f d 0 N

•H H fd 0

o •H rH

c o fd fd UH 4J 0 4J 0

o 04

Ui o

•H rH o m -p

o 04

r H o o c M C M C M i n r o o i n o cNvDHr^inc^JroocT^cTi "«* i n CO I> rH ro CJ CO a. 'vD CNCvJCMCMrorororOrO"";!* O O O O O O O O O O

O v D v D C M O i n O O O O O rHCTv(Tir^rHrOrHCy»CMrH r ^ O " ^ r o i > C N r o o O C N r o

• • • • • * . . . • " ^ o o i n c M O r H r - r H - ^ r ^ r H r H r H C M C N C N r H C M C N C M

r o r ^ c M L n " ^ v D O o r ^ r o vDinr- incnvDCTir-r-vD r O C T k v D r H i n i n C N O C M O O " 5 t C M r O r o c M O C r > O r o i n ro invDr-oo<7><T>>HCMin

• • • • • • • • • • rH rH rH

i- icNro"<sfinvDr>-oocr»o

VD ro ro .

o CN

0 U G fd > fd fd

-p G •H o o 04l>

ro CO 00 CM • ro •

ro

O 00 in 00

0

fd u 0 04

^

II

CO PM

57

f d 0 13 G •H +J G O

I ro

^A

VD VD \

o rH

vD VD

f d O

-H

04 rH rH \ CM

G U

•P 0

O •H rH o m 4J

0 04 M 0

I ro

f d u fd

f d -p c fd •p W 0

f d 0 N

•H H fd 0

o •H rH

c! o fd fd 4H -P 0 4J 0 S iH ffl

o 04

to o

•H rH O m •p iH o 04

r 0 O 0 ^ C J ^ v D 0 0 ' * 0 0 C M ^ M r ^ c N v D " ^ r o i r > c N r H ( T » i n O O v D H - ' ^ H v D H t ^ C N r H CMCNro ro ro ro^ "<s^LnvD O O O O O O O O O O

O r ^ v D ( T > C 7 > r H O O v D v O i n incNCNOCOrHrovDinr^ C N C O r O r o O ' i ^ l ^ v D v D C y i i n

ooror-r^(j\Lnr^rHCNjvD rororO'vt^ro^rO'^rO'* I I I I I I I I I I

OOCNoo-^vDr^rocNioO""* ror^"^ooooin(y>r^vDin ro ro ro cy> O "^ O

ro rH '^ in VD

ro OS l> 00 o

in " vD ro in •* ro CM r CN

H H H iH CM

rHCMro-^invDr-oocTkO

in o o •

o I

ro " « * 00 o

0 G •H rH O 0 fd

+J G •H o o OiH 00

vD OS en •

0 o d o fd in U 0 04

< Ui P'4

58

fd 0 G

•H 4J G O O

I I

ro

^A

00 VD \

0 OS 0 CN iH

•H iH 0 04

VD VD

G U J3 4J 0 (Xi

O •H rH O

MH 4J U O 04

M 0

fd U fd

fd

fd -P

w 0

fd 0 N

•H G rH fd fd 0

O •H H

C O fd MH 0 4J

04

fd

0

CQ O

•H H 0

MH

iH 0 04

" ^ O O v D O O C N r ^ - ^ t ^ C T ^ r o O C N r ^ 0 0 ' * L n r H C N ( 7 » ' « : t inr-^t>«:j«oocy»cMOino r o r o r o r o r o r o ^ ^ ^ i n O O O O O O O O O O

- " ^ C M v D o o o o j i n r o i n - ^ OCMCJ^^^'^J^^CJ^CJ^O(3^ r H r H ( T » C T » C T > ' s i < 0 0 C N ^ r O

r ^ r - L n i n r o « ^ i n o O r H CMCNCMCMCNCMCMrOrOrO

invD"«*CT>rHrHOCr»CT>00 • ^ r O C N r H r H r O r H i n - ^ v D r O r H ' s J < C M ' ^ O v D C M l > r H C N r * - r H C N r H a > V D V D r H r -r O V D O O C T k O O r H C N ' ^ v D

rH rH rH rH r^rH

r H C N r O ' ^ J ' i n v D t ^ O O C T i O

in

CN

CM

in ro in ro o

0 u G fd > fd fd

+j G •H O r>

in r-ro .

0 o d^o fd in U 0 04 < ui P4

59

f d 0

G •H 4J G O

I ro

W ^A

O r-

iH CM ;3 CM

PM i n

00 VD

f d o

•H iH 0 04 OS

CN \ rH

G u 0 •p

O •H rH 0