Embed Size (px)

Citation preview

An ageing populationThe untapped potential for hospitality and leisure businesses

Contents

2 of 19

3 Section one: Introduction4 UK consumer behaviour

5 Consumer attitudes

6 Consumer loyalty

7 The customer journey

8 Section two: The sector’s perspective9 Operators’ attitudes

10 Building relationships with consumers

11 Future plans for the sector

12 Section three: The North West13 Operators’ attitudes: The North West

14 Building relationships: The North West

15 Future plans for the North West

16 Section four: Strategies for success17 Case study: Premier Inn

18 Key takeaways

19 About the author

Critical has taken every reasonable care in the preparation of the content of this research. All information that it contains is provided in good faith.We make no representations or warranties about the information providedthrough this research. Critical accepts no liability whatsoever for any for errors or omissions nor for any direct, indirect, special or otherconsequential loss or damage of whatever kind, resulting from whatevercause, through the use of any information obtained either directly orindirectly from this research.

Section one: Introduction

Expectations of businesses and consumers

One fifth of UK income in the hospitality and leisureindustry is generated from the over 65s; yet, only 5% of businesses operating within the sector consider over 65s to be their most important demographic in terms of revenue, with many focusing on 35-44 year olds instead.

Despite this contradiction, one quarter of businessesrecognise that the proportion of turnover received fromover 65s has increased in the last five years and 86%expect their turnover amongst this age group to increase or remain the same.

Evidence suggests that with high levels of disposableincome and more free time, the older demographic (65+)is spending more than other age groups across a broadrange of UK hospitality and leisure services.

Understanding the demographics

Those aged 18-34 rated products and services highest,while consumers aged 55 and over provided the lowestratings. Products and services that are tailored to aspecific age group received lower ratings, with the olderage groups again marking these services lower.

It is encouraging to read that 94% of businesses believethey are engaged or highly engaged with the over 65s;however, in light of the above consumer statistics, itappears there is still some work to be done by hospitalityand leisure businesses hoping to fully benefit from thepower of the ‘Grey Pound’.

The digital revolution

There is clear evidence that consumers across all agegroups are using digital channels more than they were fiveyears ago to search for information about the productsand services in the sector.

Internet search engines and online customer reviews haveseen the highest level of growth, whilst in-shop travelagents and traditional TV and print advertising haveexperienced the least.

Companies are using digital media more than they did fiveyears ago, mainly via social media, their own websites andSearch Engine Optimisation; however, with those aged 65years and over more likely to access traditional channelsthan other age groups – including editorial placementsand print advertising – the sector’s digital revolution maybe moving too quickly for its more senior audience.

Our research covers a sample of 564 UK hospitality andleisure businesses across leisure, food and drink, travel,hotels and professional sports, as well as 1,100 consumersof varying ages, incomes and geographies across the UK.

By exploring the thoughts of customers and businessesalike, we hope to highlight the industry’s attitudes towardsdifferent audience demographics and demonstrate howhospitality and leisure operators can find opportunities totarget their markets more effectively.

Across the UK, a large opportunity exists for hospitality and leisure businessesto target consumers aged over 65; however, at present, much of this potentialremains untapped.

65+This age group is spending more than others across a broad range of UK hospitality and leisure services.

Mike SaulHead of Hospitality and Leisure

3 of 19

Bought food froma restaurant/bar

Watchedprofessional sport

Gambled (highstreet or online)

Visited a theme park

Paid to play golf

Other activity

UK holiday

Visited cinemaor theatre

Health club or gym

Booked a holiday abroadusing a UK travel operator

UK hotel

?

Age 18-34 Age 35-54 Age 55-64 Age 65 and over

353 466 499 556

76 105 111 133

507 640 545 878

1,672 3,187 3,438 5,419

147 276 202 173

275 563 523 527

188 378 367 284

248 515 292* 578*

97 231 99* 396*

61 182 160 423

125 256 109 216

Hospitalityand leisure

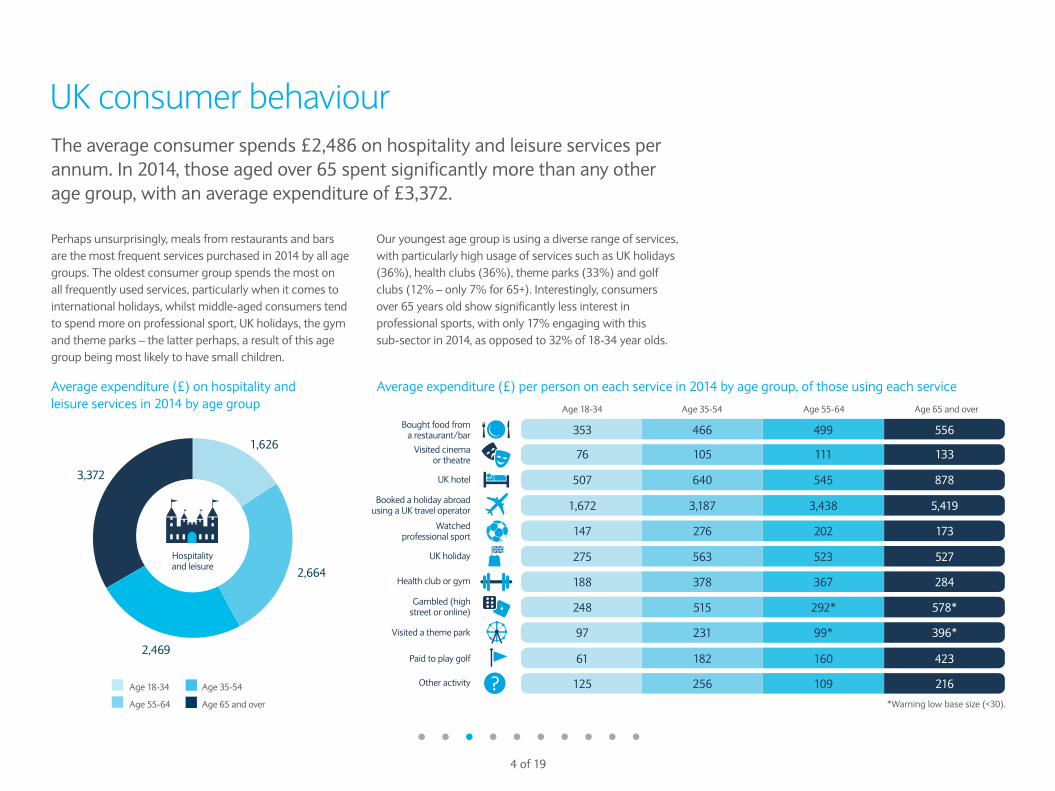

UK consumer behaviour

Perhaps unsurprisingly, meals from restaurants and bars are the most frequent services purchased in 2014 by all agegroups. The oldest consumer group spends the most on all frequently used services, particularly when it comes tointernational holidays, whilst middle-aged consumers tendto spend more on professional sport, UK holidays, the gymand theme parks – the latter perhaps, a result of this agegroup being most likely to have small children.

Our youngest age group is using a diverse range of services,with particularly high usage of services such as UK holidays(36%), health clubs (36%), theme parks (33%) and golfclubs (12% – only 7% for 65+). Interestingly, consumersover 65 years old show significantly less interest inprofessional sports, with only 17% engaging with this sub-sector in 2014, as opposed to 32% of 18-34 year olds.

1,626

2,664

2,469

3,372

The average consumer spends £2,486 on hospitality and leisure services perannum. In 2014, those aged over 65 spent significantly more than any otherage group, with an average expenditure of £3,372.

Average expenditure (£) per person on each service in 2014 by age group, of those using each serviceAverage expenditure (£) on hospitality andleisure services in 2014 by age group

*Warning low base size (<30).

Age 18-34 Age 35-54

Age 55-64 Age 65 and over

4 of 19

In general, our results show that consumers have apositive attitude toward hospitality and leisure operators.Those aged between 18-34 were particularly reassuring,with 44% rating the sector positively. Less encouraging is the over 65 age group, however, with only 19%providing a positive rating for the sector as a whole.

The products and services offered by hospitality andleisure operators in general ranked highly, with 75% of 18-34 and 71% of 35-54 year olds rating them as excellentor good. Slightly lower down the scale, the 55-64 year oldsand over 65s score products and services as excellent or good at 64% and 67% respectively.

Products for specific age groups

Interestingly, when consumers were asked to evaluateproducts and services offered for their particular agegroups, positivity levels fell. 18-34 year olds are still mostlikely to rate services highly, with 67% ranking these as excellent or good; however, the 55-64 year olds andover 65s yet again show signs of dissatisfaction with only 56% and 59% rating services as excellent or good, in that order.

Given that 94% of businesses are confident that theirbusiness is engaged or highly engaged with the over 65s,these lower scores could suggest that more needs to bedone to ensure proactive businesses are communicatingtheir offering effectively, across multiple audiences.

Percentage of consumers rating hospitality and leisureproducts and services aimed at their age group asexcellent or good

The hospitality and leisure industry is considered much more positively thanothers in the UK, with 48% of all respondents stating that the sector providesbetter products than other service industries.

Consumer attitudes

Age

18-34

67% 60% 56% 59%

Age

35-54Age

55-64Age

65 and over

5 of 19

According to our research, 30% of all consumers are loyal to certain hospitality and leisure companies, whereas 40%feel they have no loyalty at all. Interestingly, the top fourcompanies that consumers felt most loyal to were hotels –perhaps proving that loyalty is encouraged through multipleconsumer touch-points across a longer timeframe.

One of the least important factors driving loyalty for those aged 18-64 is the quality of food provided by leisureoperators; however, this is the fourth most importantfactor for the oldest age group with 13% seeing this as a key reason for repeat custom.

When looking to attract consumers for the first time, goodvalue for money is the top priority for all age groups –significantly for those aged between 35-64. Interestingly,consumers in the 18-34 and over 65 age brackets look forthe same top three factors when deciding to use a companyfor the first time: value for money, recommendation andquality of product.

With such similar preferences across the age groups,companies may not need to shift their offering radically inorder to suit their target audiences. Hospitality and leisurecompanies may prefer to explore how they are marketingtheir deals and reviews to ensure their messages reachdifferent age demographics.

Top three reasons for consumer loyalty across the age groups

Loyalty is significantly higher among the over 65s (41%) and lowest for 18-34year olds (19%), suggesting that – as can be expected – consumers are likelyto return to brands over time.

Consumer loyalty

Age 18-34 Age 35-54 Age 55-64 Age 65 and over

3 2 2 2Value for money/price

1 1 1 1The level of service

2 3 3 3Rewards/incentives/loyalty scheme

6 of 19

Percentage of consumers using the internet for different hospitality and leisure services (%) by age profile

The customer journey

It is a positive sign that all ages are interacting with onlineservices across the sector, bucking some assumptions that older generations are failing to engage with digitalchannels. Unexpectedly, online bingo – which haspreviously been associated with an older age group – has a much higher following among those aged 18-34,showing how online services have the potential to shifttraditional audience demographics.

Across the age groups, our research shows thatconsumers are also using the internet to research thesector, with internet search engines topping the list as themost popular way to search for information on hospitalityand leisure services. In fact, four of the top five sources ofinformation included digital media: search engines, onlinecustomer reviews and forums, direct email, and onlinetravel agencies.

Perhaps unsurprisingly, social media is the least popularsource of information for the over 65s, with only 2% of respondents in this age category engaging with thechannel. Interestingly, however, only 8% of over 65s areinclined to visit in-store travel agents. This low figureproves that, despite a lack of social media engagement,the older generation is beginning to become more digital-savvy and look for more instant and convenient ways toaccess information on the sector.

The majority of consumers are happy to book hotels, holidays, cinema ticketsand restaurants using the internet, with 72% of all consumers using theinternet to make hotel reservations.

Made a hotelreservation

Boughttheatre tickets

Bought tickets forprofessional sport

Gambling/gaming

Played bingo

Made a restaurantreservation

Booked aholiday abroad

Boughtlottery tickets

Boughtcinema tickets

Booked a UK holiday

Age 18-34 Age 35-54 Age 55-64 Age 65 and over

62% 78% 80% 69%

60% 68% 70% 62%

48% 61% 68% 51%

57% 56% 48% 32%

41% 52% 50% 49%

43% 53% 44% 42%

30% 43% 32% 25%

33% 35% 31% 19%

29% 23% 13% 6%

15% 13% 3% 2%

7 of 19

Section two: The sector’s perspective

Despite this statistic, 35-44 year olds are seen as the mostimportant age group in terms of revenue – perhaps as aresult of this age group usually taking families along withthem. With one fifth of all UK hospitality and leisure incomegenerated from the over 65s, however, it seems that thisdemographic is somewhat overlooked as a key priority foroperators in the sector.

23% of businesses say that their income from customersaged over 65 has increased in the last five years, with only7% saying that it has decreased, and 53% stating that it has remained the same. 17% of operators were unsure how this demographic was affecting their turnover.

Challenging perceptions

44% of all operators said that our oldest age category tendsto spend less on leisure services than younger customersdo; an assumption which contradicts our earlier statistic,showing that consumers over 65 spend more on averagethan any other age group.

This perception from operators may be a result of thoseaged over 65 benefiting from cheaper, off-peak leisure deals during the day or school-terms, whilst youngerdemographics are, typically, at work. The exception to this is in the hotel and travel sectors where 38% and 44% ofoperators, respectively, said that over 65s tend to spendmore than the average customer.

Our research shows that almost three quarters (72%) of businesses in the hospitalityand leisure sector expect those aged over 65 to spend the same or more on services over the next five years, with 65% expecting disposable income to plateau or increase.

Operators’ (%) most important age group in terms of revenue

18-24 years

20%

37%

13%

9%

5%

10%

25-34 years 35-44 years 45-54 years 55-64 years 65 yearsand over

All of these

4%

8 of 19

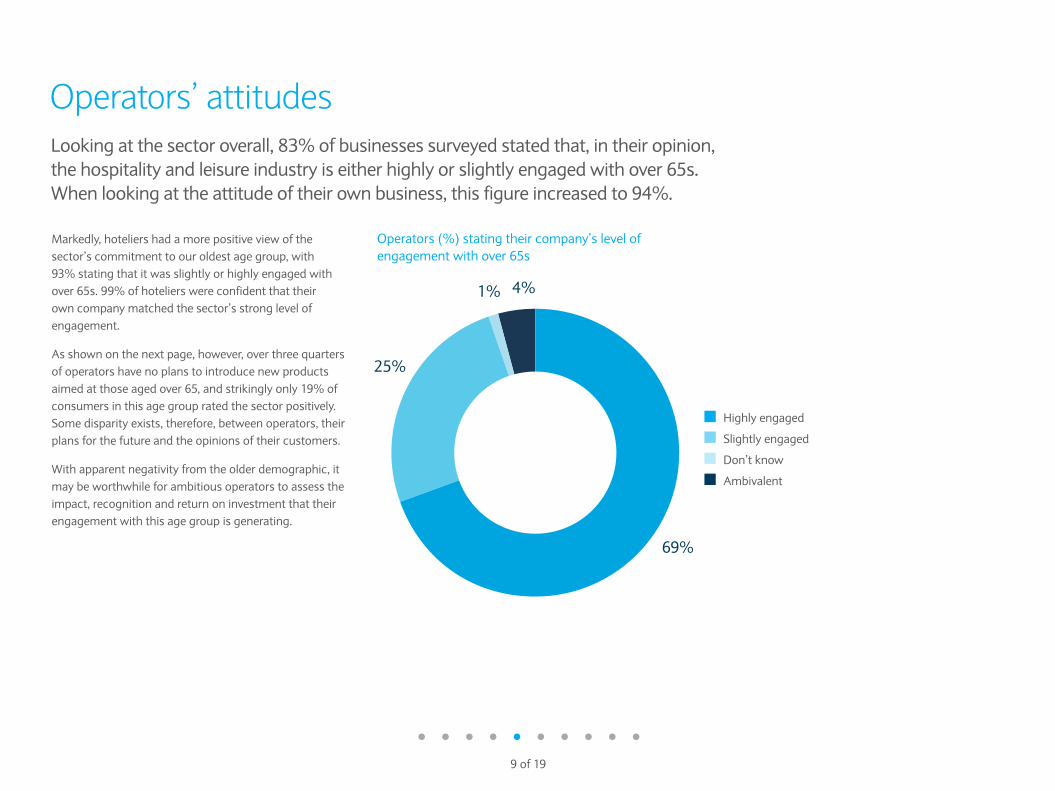

Markedly, hoteliers had a more positive view of thesector’s commitment to our oldest age group, with 93% stating that it was slightly or highly engaged withover 65s. 99% of hoteliers were confident that their own company matched the sector’s strong level ofengagement.

As shown on the next page, however, over three quartersof operators have no plans to introduce new productsaimed at those aged over 65, and strikingly only 19% ofconsumers in this age group rated the sector positively.Some disparity exists, therefore, between operators, theirplans for the future and the opinions of their customers.

With apparent negativity from the older demographic, itmay be worthwhile for ambitious operators to assess theimpact, recognition and return on investment that theirengagement with this age group is generating.

Operators’ attitudesLooking at the sector overall, 83% of businesses surveyed stated that, in their opinion,the hospitality and leisure industry is either highly or slightly engaged with over 65s.When looking at the attitude of their own business, this figure increased to 94%.

Operators (%) stating their company’s level ofengagement with over 65s

69%

25%

4%1%

Highly engaged

Slightly engaged

Don’t know

Ambivalent

9 of 19

Building relationships with consumers

With older customers more likely to remain loyal toparticular brands, alongside only 59% of over 65s ratingservices tailored for them as excellent or good, the abovestatistic could highlight a need for operators to adopt amore bespoke approach to their senior audiences.

Indeed, with 94% of businesses stating that they areengaged with those aged over 65, it is striking that only30% have products and services related to thisdemographic and poses the question: what else areoperators doing to engage with this audience?

When encouraging an older customer to use theircompany for the first time, businesses perceive the most important factors to be strong customer service,reputation and value for money. This is a positive result, as it parallels our survey’s consumer results, discussedin section one of this report.

30% of companies have specific products and services aimed at the over 65s,with leisure operators and travel businesses improving on this statistic at 45%and 43% respectively.

Factors perceived by operators (%) to encourage firsttime custom from consumers aged 65+

58%Customer service/reputation

51%Pricing/rewards/value

41%Product/service offered

15%Advertising/reviews/editorials

10 of 19

Not considered before

Compromise current positioning

Lack of skills/resources/fundingto cater to this age group

About to sell the business/retire

Previously tried to targetwith little success

Already have enough products/services in place

Don't target specific groups

See little financial opportunityin this age group

Less/no demand for our products/services with this age group

37%

31%

28%

28%

22%

19%

12%

11%

1%

Future plans for the sector

On average, 15% of investment from all companies will be used to meet the needs of those over 65. Over threequarters (76%) of all operators have no plans to introduceany new products or services aimed at this demographic.Delving into the more positive responses, 29% of leisurespecific businesses do have plans to introduce furtheroptions for our oldest age category.

Top reasons given for not introducing new products and services to those aged over 65 include having notconsidered this before, already having enough products in place, experiencing less demand from that particularage group and seeing little financial opportunity.

For those that have tailored their offering, the mostpopular methods are providing bespoke products (69%),age-related vouchers (68%) and age-specific facilities(65%). Direct marketing to the over 65s is also popular,with 55% of those businesses opting for this approach.

Engaging your audience

With regards to marketing, printed media remains the thirdmost popular channel for hospitality and leisure companies,with 34% using this medium, coming closely behind onlineadvertising (39%) and company websites (47%). In light ofearlier discussion around consumer preferences, thesemarketing preferences should be somewhat effective incapturing the attention of the older audience.

Of the companies we surveyed, 83% are planning investment over the nextfive years, with one fifth planning major investment.

Reasons given by operators (%) for not introducing more productsand services for customers aged over 65 in the next five years

11 of 19

12 of 19

18-24 years

33%

25-34 years 35-44 years 45-54 years 55-64 years 65 yearsand over

All of these

1%

15%

10%9%

16%

10%

Section three: The North West

On average, consumers living in the North West spend£3,139 on hospitality and leisure services per annum.

Similar to national statistics, 35-44 years old are seen as the most important age group in terms of revenue for companies in the North West, with only 9% ofoperators considering the over 65s as the most important group.

Positively, one quarter of businesses say that theirproportion of turnover from the over 65s has increased in the last five years, and only 2% believe that theirproportion of turnover amongst over 65s has fallen.

A high proportion (89%) expect their company’s turnoveramongst over 65s will increase or remain the same in thenext five years, with only 6% expecting it to decrease.

43% of businesses across the North West believe that spend per customer is lower amongst those aged 65 and over, whereas 32% think that this age group is spending more.

Operators’ (%) most important age group, in terms of revenue, across the region

13 of 19

Operators’ attitudes: The North West

When asked about their own company’s level of engagement, the majority (87%) believe they are highly engaged or engaged with the over 65s. Althoughthis figure is slightly lower than the national average, it remains a strong result for the region’s operators.

51% of companies in the North West expect that thedisposable income of those aged 65 and over will eitherstay the same or increase over the next five years.

With such positive expectations, it is promising to see that companies across the region are engaging with the older age group – even if catering for a youngeraudience remains their key priority.

Two thirds (66%) of operators in the region say that the hospitality andleisure sector as a whole engages well with the over 65s.

Operators (%) stating their company’s level ofengagement with over 65s across the region

69%

18%

4%

4%5%

Highly engaged

Slightly engaged

Don’t know

Ambivalent

Neglectful

14 of 19

72%

44%

34%Product/service offered

15%Advertising/reviews/editorials

Pricing/rewards/value

Customer service/reputation

Building relationships: The North West

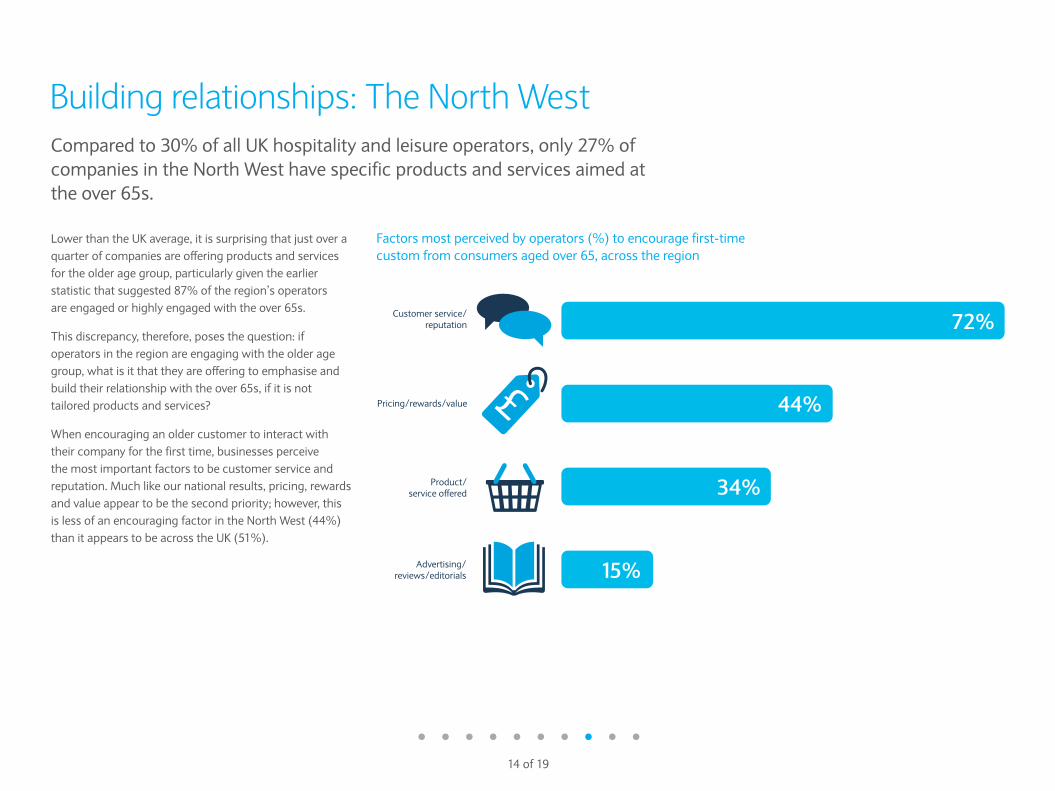

Lower than the UK average, it is surprising that just over aquarter of companies are offering products and servicesfor the older age group, particularly given the earlierstatistic that suggested 87% of the region’s operators are engaged or highly engaged with the over 65s.

This discrepancy, therefore, poses the question: ifoperators in the region are engaging with the older agegroup, what is it that they are offering to emphasise andbuild their relationship with the over 65s, if it is not tailored products and services?

When encouraging an older customer to interact withtheir company for the first time, businesses perceive the most important factors to be customer service andreputation. Much like our national results, pricing, rewardsand value appear to be the second priority; however, this is less of an encouraging factor in the North West (44%)than it appears to be across the UK (51%).

Compared to 30% of all UK hospitality and leisure operators, only 27% ofcompanies in the North West have specific products and services aimed atthe over 65s.

Factors most perceived by operators (%) to encourage first-timecustom from consumers aged over 65, across the region

15 of 19

Not considered before

55%

About to sell the business/retire 7%

Already have enough products/services in place

15%

Less/no demand for our products/services with this age group

25%

See little financial opportunityin this age group

41%

Compromise current positioning

37%

Previously tried to targetwith little success 30%

Don't target specific groups

16%Lack of skills/resources/fundingto cater to this age group

7%

Future plans for the North West

Of this planned investment, on average 18% will be used to meet the needs of over 65s in the North West.

Just over a third of operators (37%) have plans to introduce products or services aimed at the over 65s,which is significantly higher than the national average(21%); however, the fact remains that almost 60% ofbusinesses have no plans to introduce any tailoredpackages for their older audience.

The main reasons given for not doing so are the perceptionthat they ‘already have enough products/services in place’and a perceived ‘lack of demand for products and servicesfrom this age group’.

Across the region, company websites and onlineadvertising are the most commonly used marketingchannels used by businesses, with 35% of operatorscommunicating with their audiences in this way. Socialmedia usage is the third most popular at 33%, which isclose to the UK average of 32%.

85% of companies in the North West are planning some form of investmentover the next five years to meet their business needs. Three in ten (30%) areplanning a major investment.

Reasons given by operators in the region (%) for not introducing moreproducts and services for customers aged over 65 in the next five years

Section four: Strategies for success

16 of 19

Hospitality and leisure operators have adopted a range of strategies andtechniques to improve their appeal to different age groups. Below are a fewconsiderations for successful interaction with the over 65s.

Personalised conversations with your whole audience

This research demonstrates the differences inpreference and buying habits of a range of age

groups. How confident are you that you really knowyour customers and understand their specific likesand dislikes? Successful use of big data means youcan have specific conversations with each of yourdemographics that are entirely relevant to them.

Capitalise on loyaltyBrand loyalty in the hospitality and leisure sector isstrong, and increases with age. What are you doing to further incentivise your audience to ensure they

are loyal to your brand throughout their lives?

Don’t underestimate the spending potential of the over 65 age group

The research suggests that the majority of operatorsare focusing their attention on the 35-44 age group,

but the over 65s spend more per head. With anincreasingly ageing population, there is significant

potential for businesses to capitalise on the spendingpower of this audience.

Now’s the time to actDon’t wait to act on this information –

building stronger relationships with the olderdemographic now will stand you in good

stead for the future.

Review your product or service offering Consumers were less satisfied with the products and services offered for their specific age groups,

particularly the over 65s. Is there potential toreposition your offering to target a greater share of the ‘Grey Pound’? Small changes can increase your appeal to this audience, look to emphasise

these in your product design and marketing going forward.

Multi-channel futureConsumers are increasingly using the internet for

various stages of the purchasing journey; ensuringyour business makes this process as easy as possiblewill be of long-term benefit. But don’t overlook the

more traditional marketing channels. The over 65s arestill inclined to be influenced by print advertising and

editorials so be sure to vary your approach across age groups to achieve maximum effect.

Customer first approach

Russell Braterman, Premier Inn Brand Marketing Director,says the single most important factor in driving thesepositive statistics is the company’s commitment tocustomer service. Excellence in guest care is at the heartof Premier Inn’s philosophy and this means consideringthe requirements of all visitors to the group’s 650+ hotels – be they elderly, business travellers, families or any otherdemographic.

Premier Inn is a budget brand, but the product is designedto offer value aligned with excellent service at all pointsin the customer journey. The chain has invested heavilyin social media and its market-leading Twitter teamresponds to challenges and issues faced by customers in real time, providing care and support for any onlinebooking challenges. The 24-hour reception means thatwhatever time guests arrive, there will be personal supportto welcome them to the hotel. The provision of tea andcoffee facilities in rooms and free Wi-Fi, whilst not uniqueto Premier Inn, are added touches which help improve theoverall guest experience.

Appealing to specific demographics

Whilst Premier Inn does not deliberately target anyparticular demographics, there are certain elements of their offering that appeal more to specific audiences.

The new higher bed design is easier to get in and out of for example, and has received strong feedback from olderguests. The provision of sofabeds in rooms has also beenapplauded by older guests, for providing an alternative and accessible place to relax. The 24-hour reception appealsto this demographic because, as evidenced elsewhere in thereport, they prefer direct human interaction to self-serving.

Similarly, for another key demographic, the opportunity toautomatically link hotel stays directly to personal expenseclaims through the Business Account Card appeals tothose travelling for work.

A motivated workforce

Premier Inn’s parent company, Whitbread, has a focus onthe ‘customer heartbeat’ and this wider values frameworkruns through much of the hotel chain’s employee agenda.Premier Inn operates a number of key initiatives to ensureits employees, ‘bring their best selves to work’, creating a‘culture of high performance delivered by nice people’.Front line staff come from all age groups and backgroundsand are involved in the decision-making process, creatinga unified sense of purpose. Colleague reward schemescelebrate excellent customer service and drive a strongaspirational culture.

Additionally, Premier Inn aims to recruit 50% of staff for new openings from amongst the local long-termunemployed, giving these individuals training anddevelopment opportunities which, in turn, pays off in their commitment to the company and a strong desire to deliver for the customer.

Focused marketing

As a brand, Premier Inn has a diverse audience, but alwaysties back to its core customer commitment. This meansthat specific campaigns can target a certain demographic,as The Lego Movie ad break takeover achieved withfamilies last year, whilst still ensuring brand awarenessacross all their demographics.

Premier Inn was voted the number one hospitality and leisure brand, across allage groups, by the 1,000-plus consumers surveyed for this report. What dothey do that generates this pan-generational brand recognition?

Case study: Premier Inn

17 of 19

Key takeaways• One fifth of UK income in the hospitality and leisure industry is generated from the over 65s –

an estimated £37bn in 2014

• Despite this, the sector could be missing out on at least a further £16bn by underestimating the spending power of the older generation

• The over 65s spend an average of £3,372 per annum on hospitality and leisure, compared to£2,486 across all age groups

• Brand loyalty increases with age. 41% of those aged 65 and over were loyal to particular brands,compared to 19% of those aged 18-34

• 94% of hospitality and leisure operators surveyed thought they engaged with the over 65s, but only 5% see them as the most important age group

• Over 83% of operators expect to invest in their business in the next five years, but only 15% of the planned investment will be used to meet the needs of the over 65s.

To find out more about how Barclays can support your business, please call 0800 015 4242* or visit barclays.com/corporatebanking

Figures based on research conducted by Critical, on behalf of Barclays, between January-February 2015. 564 hospitality and leisure businesses were interviewed, as well as 1,100 consumers.

*To maintain a high quality of service, your call may be monitored or recorded for training and security purposes. Calls to 0800 numbers are free of charge, when calling from a UK landline. Charges may apply when using a mobile phone or when calling from abroad. Lines are open from 8am to 6pm Monday to Friday.

18 of 19

About the authorFor further information and to find out how our sector specialist team can support your business, please contactMike Saul, Head of Hospitality and Leisure.

Mike is Head of the UK-based Hospitality and Leisure team atBarclays. With over 30 years of experience, he and his teamsupport a wide-ranging client base with their dedicated specialistapproach, industry knowledge and sector-specific products and services.

Mike Saul Head of Hospitality and LeisureBarclays

M: 07775 540800*[email protected]

*Please note: this is a mobile phone number and calls will be charged in accordance with your mobile tariff.

No part of this publication may be reproduced or stored in a retrieval system, in any form or by any means, electrical, mechanical, photocopying or otherwise, without the prior consent of the publishers. The views and forecasts presentedin this report represent independent findings and conclusions drawn from a study by Critical. Critical can accept no responsibility for any investment decision made on the basis of this information or for any omissions or inaccuracies thatmay be contained in this report. This report has been produced in good faith and independently of any operator or supplier to the industry. We trust that it will be of significant value to all readers.

The views expressed in this report are the views of third parties, and do not necessarily reflect the views of Barclays Bank PLC nor should they be taken as statements of policy or intent of Barclays Bank PLC. Barclays Bank PLC takes noresponsibility for the veracity of information contained in third party narrative and no warranties or undertakings of any kind, whether expressed or implied, regarding the accuracy or completeness of the information given. Barclays BankPLC takes no liability for the impact of any decisions made based on information contained and views expressed in any third party guides or articles.

Barclays is a trading name of Barclays Bank PLC and its subsidiaries. Barclays Bank PLC is authorised by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority(Financial Services Register No. 122702). Registered in England. Registered number is 1026167 with registered office at 1 Churchill Place, London E14 5HP.

April 2015.

19 of 19