Embed Size (px)

Citation preview

Altron Group2010 Interim results

Agenda

Altron group overview Robert Venter

Altron group financial results Alex Smith

Operational reviews:

Altech Craig Venter

Bytes Rob Abraham

Powertech Norbert Claussen

Altron – Outlook Robert Venter

Volumes flat with growth coming from cost cutting and efficiencies obtained over last 18 months

Encouraging improvement in EBITDA margins

Further improvement in group’s working capital management

Bytes and Powertech show significant improvement in profits and margins

Altech experienced difficult market conditions, particularly in East Africa and Altech UEC

Strong rand continues to impact the group

Increased competition from foreign entry into local markets

Second 6 months anticipated to be stronger at Altech

Continued external focus on selective acquisitions

Group overview

Financial summary(for the 6 months ended 31 August 2010)

R millions Aug 10 Aug 09 % change

Revenue 11 724 12 055 (3%)

EBITDA 988 951 4%

EBITDA margin 8.4% 7.9%

Adjusted diluted HEPS (cents) 105 100 5%

Return on capital employed 18.4% 19.9%

Revenue: 4 788 1%

EBITDA: 507 12%

EBITDA margin: 10.6% 12.2%

Headline earnings: 201 29%

Adjusted dilutedheadline earnings: 218 25%

ROE: 21.7% 29.2%

ROCE: 31.3% 41.2%

*

Subsidiary company results (for the 6 months ended 31 August 2010)

*listed on JSE

62%

(R millions)

*shareholding

Revenue: 3 797 (5%)

EBITDA: 270 23%

EBITDA margin: 7.1% 5.5%

Headline earnings: 91 102%

Adjusted dilutedheadline earnings: 98 63%

ROE: 7.6% 4.0%

ROCE: 10.8% 8.5%

*

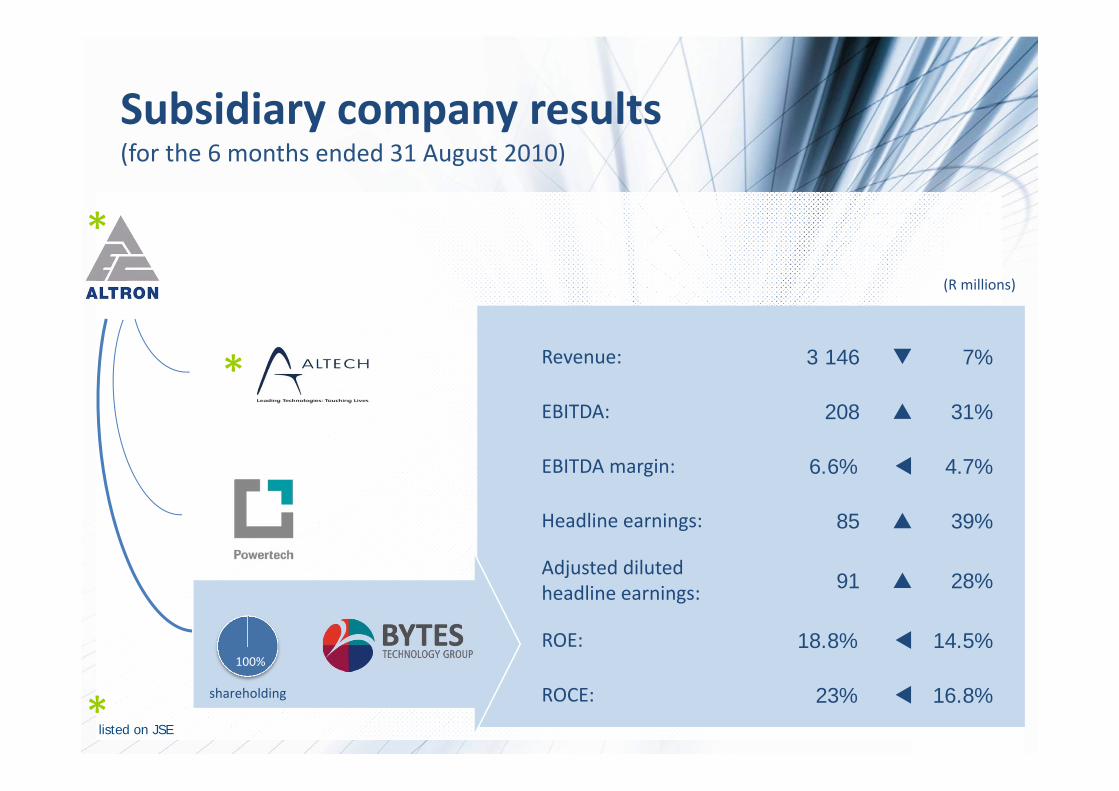

Subsidiary company results (for the 6 months ended 31 August 2010)

100%

(R millions)

*

shareholding

*listed on JSE

100%

Revenue: 3 146 7%

EBITDA: 208 31%

EBITDA margin: 6.6% 4.7%

Headline earnings: 85 39%

Adjusted dilutedheadline earnings: 91 28%

ROE: 18.8% 14.5%

ROCE: 23% 16.8%

*

Subsidiary company results (for the 6 months ended 31 August 2010)

*

(R millions)

shareholding

*listed on JSE

Contribution per subsidiary

Revenue* EBITDA* Headline earnings

Aug 10

Aug 09

* Revenue & EBITDA excludes Corporate & Financial and includes forex losses / gains

R270m 27%

R507m 52%

R208m 21%

R219m 23%

R578m 60%

R159m 17%

R91m 30%

R123m 39%

R85m 27%

R13m 4%

R45m 15%

R175m 60%

R61m 21%

R12m 4%

R3 797m 32%

R4 788m 41%

R3 146m 27%

R3 981m 33%

R4 732m 39%

R3 374m 28%

Improve existing operationsExpand organicallyAcquire and disposeAllocate capital

Strategic philosophies

Strategic alliances

Ownership of Intellectual Property

Annuity income

Value added servicesMarket leadership / Critical mass

Quality / Sustainability of Income

Superior human capital

Global expansion in niche marketsBlack Economic Empowerment

Increase shareholder value

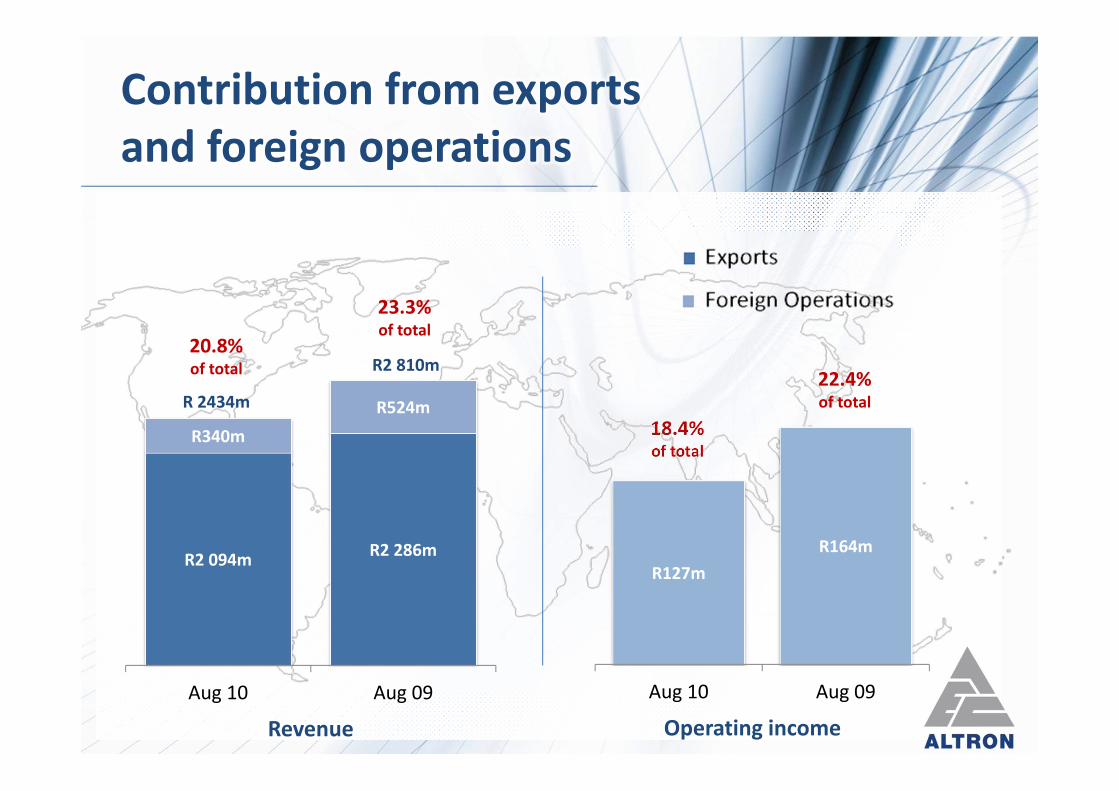

R2 094m R2 286m

R340mR524m

Aug 10 Aug 09

Contribution from exports and foreign operations

20.8%of total

23.3%of total

18.4%of total

22.4%of totalR 2434m

R2 810m

Revenue Operating income

R127mR164m

Aug 10 Aug 09

Annuity incomefor 12 months to Feb 09 (R m)

Annuity incomefor 12 months to Feb 10 (R m)

Annuity incomeFor 6 months to Aug 10 (R m)

6 809 74% 7 422 81% 3 926 82%

2 805 46% 2 822 47% 1 491 47%

1 617 17% 1 238 17% 618 16%

11 231 45% 11 482 51% 6 035 51%

Annuity based services

EBITDA

‐

100

200

300

400

500

600

700

H12006

H22006

H12007

H22007

H12008

H22008

H12009

H22009

H12010

H22010

H12011

Altech

‐

50

100

150

200

250

300

H12006

H22006

H12007

H22007

H12008

H22008

H12009

H22009

H12010

H22010

H12011

Bytes

‐

100

200

300

400

500

600

700

H12006

H22006

H12007

H22007

H12008

H22008

H12009

H22009

H12010

H22010

H12011

Powertech

‐

200

400

600

800

1 000

1 200

1 400

H12006

H22006

H12007

H22007

H12008

H22008

H12009

H22009

H12010

H22010

H12011

Altron

Rm Rm

Rm Rm

Altron's progress in terms of meeting its B‐BBEE Vision 2012 targets has been published in Altron Vision 2012 Progress Report

Empowerdex ratings confirmed Bytes’ position as number one empowered ICT company in South Africa

Bytes group obtained average B‐BBEE score of 90.98 to be rated a Level 2 contributor on DTI scorecard for 2010 (customers can claim 156%)

Altech’s consolidated verification achieved Level 3 contributor status with 76.14 points

Powertech’s major operations have been rated and reflect Level 3 contributor ratings

Altron ranked #1 countrywide survey for skills development by FM/Empowerdex

B‐BBEE transformation progress

Financial resultsAlex SmithChief Financial Officer: Altron

Group income statement ‐ highlights

R millions Aug 10 Aug 09 % change

Revenue 11 724 12 055 3%

Operating profit before capital items 691 731 5%

EBITDA 988 951 4%

EBITDA margin 8.4% 7.9%

Net investment income (35) (43)

Capital items (24) (50)

Foreign exchange losses/gains (27) (96)

Taxation (216) (234)

Headline earnings per share (cents) 99 93 6%

Adjusted diluted headline earnings per share (cents)* 105 100 5%

* Adjusted for the amortisation of intangible assets

Impact of appreciating rand

6 months to Aug 10

R m

EBITDA 507 208 270 988

EBITDA margin 10.6% 6.6% 7.1% 8.4%

Forex losses 10 12 12 27

Effect of translation of foreign ops 10 5 1 16

Adjusted EBITDA 527 225 283 1 031

Adjusted EBITDA margin 11.0% 7.2% 7.5% 8.8%

Effect of translation is difference between current year results translated at average

rates for half year, versus average rate for prior half year

Adjusted & diluted headline earnings

R millions Aug 10 Aug 09

Headline earnings 312 293

Amortisation of intangibles (net of tax and minorities)

‐ Altech 10 7

‐ Bytes 6 9

‐ Powertech 15 15

Adjusted headline earnings 343 324

Dilution adjustments

‐ Aberdare (8) 0

‐ Altech Alcom Matomo 0 (2)

‐ Dilutive options – Altech (2) (4)

Adjusted diluted headline earnings 333 318

R millions Aug 10 Aug 09

Total non‐current assets 5 719 5 235

Current assets 5 374 5 818

Cash balances 1 273 1 338

Total assets 12 366 12 391

Shareholders’ equity 4 664 4 506

Minority interests 1 414 1 384

Non‐current liabilities 908 1 305

Current liabilities 5 380 5 196

Total equity and liabilities 12 366 12 391

Summarised balance sheet

Cash flow statementR millions Aug 10 Aug 09

Operating activities

Cash generated by operations 1 013 956

Changes in working capital 31 127

Net investment expense (45) (43)

Tax paid (230) (227)

Cash available from operating activities 769 813

Dividends paid, including to minority shareholders (449) (533)

Investment activities (395) (574)

Financing activities (108) 97

Net funds utilised (183) (197)

Cash and cash equivalents at the end of period 1174 1180

Translation of foreign cash (17) (12)

Cash and cash equivalents at the end of period 974 971

58 48 46 39 43 43

5357 55

57 56 51

‐85 ‐89‐81 ‐77 ‐81 ‐80

Feb 07 Feb 08 Feb 09 Aug 09 Feb 10 Aug 10

Working capital26

21

18

Accounts receivable days

Inventory days

Accounts payable days

Net working capital days

16

R1 625mR1 989mR1 598mR1 567m Net working capital

19

14

R1 784m R1 488m

R22 336mR24 768mR21 431mR17 126m RevenueR12 055m R11 724m

Altech results Craig VenterCEO

Altech financial summary

R millions Aug 10 Aug 09 % change

Revenue 4 788 4 732 1

EBITDA 507 578 (12)

EBITDA margin 10.6% 12.2%

Adjusted diluted headline earnings 218 291 (25)

Altech divisional reviewR millions

Aug 10revenue

% growth Comments

Autopage Cellular 2 819 2 Subscriber clean‐out (lower margin). ARPU maintained.

Netstar 473 9 Continued strong growth in Fleet Management.

Tech Concepts 26 85 Stable performance, transforming from Tier 2 to Tier 1 ISP.

East Africa 314 21 East Africa remains growth engine for Altech. Lower bandwidth charges. Timing of SEACOM bandwidth sales (now all sold). Carrying cost of satellite connectivity.

Alcom 152 (12) Solid performance on back of new projects.

Fleetcall 32 19 Stable growth.

UEC 544 (9) DTT delays and uncertainty on technology standards.Improved 2nd half.

AAD 142 (6) Electronics industry under pressure.

Isis 61 13 Strengthened position with existing customers.

ACS 151 29 Continued positive growth trend, e‐Security and POS terminals .

West Africa 99 (8) Rand exchange effect. Maintained market share. Expanded product lines and services capacity.

NuPay 56 55 Strong performance.

Group eliminations (82)

Total 4 788 1

Altech – the way forward

Significantly improved performance expected for 2nd half

Adverse factors specific to 1st half will not recur

Diversify income base within TMT sector through globalisation, M&A activity and convergence opportunities

Transform Telecoms business by moving ATC up the value chain

Expand Multi‐media division’s converged services offering through continued investment in and development of innovative technologies

Strengthen leadership position in East Africa

Invest in human capital development and skills retention

Focus on optimisation of margins, cost structures, working capital and cash flow

Our journey from a telecommunications and technology company to converged services group continues…

Bytes results

Rob AbrahamCEO

1st half focus

Reorganise management team and streamline operations

Deploy performance excellence plans with reviews

Emphasis on financial results (profit and cash)

Turn around underperformers (Retail ATM, BDS UK, Intelleca)

Energise and develop our people

Customer service and brand recognition

Agree an acquisitions plan and strategy for future growth

R millions Aug 10 Aug 09 % change

Revenue 3 146 3 374 (7)

EBITDA 208 159 31

EBITDA margin 6.6% 4.7%

Adjusted diluted headline earnings 91 71 28

Bytes financial summary

CompanyAug 10revenue

% growth

Comments

Systems Integration 380 20 Profits substantially improved ‐ new business focus

Managed Solutions 365 (14) Performance slightly ahead of expectation – Retail ATM turnaround complete ☺ Good pipeline of business expected to materialise in 2nd half

Document Solutions 915 (1) Xerox division performed strongly. NOR Paper and LaserCom below par ‐better 2nd half anticipated

Connect 271 5

Outsource ‐ rock solid, strong performanceCommunications ‐ re‐energised ‐ satisfactory 1st halfIntelleca – poor performance, now restructured and reorganised, recovery dependent on new business development in medium accounts

Healthcare Solutions 99 15 Another excellent performance ‐ better than expectation. Investment in new offerings underway

People Solutions 42 15 Profitable growth, considerably better than previous year

International Operations 1 092 (20) BDS UK turned around, refocused and re‐energisedSoftware Services ‐ strong performance, better than anticipated

Bytes Namibia 11 12 Satisfactory performance

Group Eliminations (29)

Total 3 146 (7) Efficiency gains fueled 31% EBITDA improvement

Bytes divisional review

Sustain strong cash generation and excellent working capital

management achieved in 1st half

Implement growth plan

Leverage cross sell opportunities

East Africa (possibly green fields)

UK ‐ progress acquisition opportunities

South Africa ‐ continue to focus on operational excellence

Our vision – to be recognised as the best IT company in Africa

Our mission – to help our customers do great work

Bytes – the way forward

Powertech resultsNorbert ClaussenCEO

Powertech financial summary

R millions Aug 10 Aug 09 % change

Revenue 3 797 3 981 (5%)

EBITDA 270 219 23%

EBITDA margin 7.1% 5.5%

Adjusted diluted headline earnings 98 60 63%

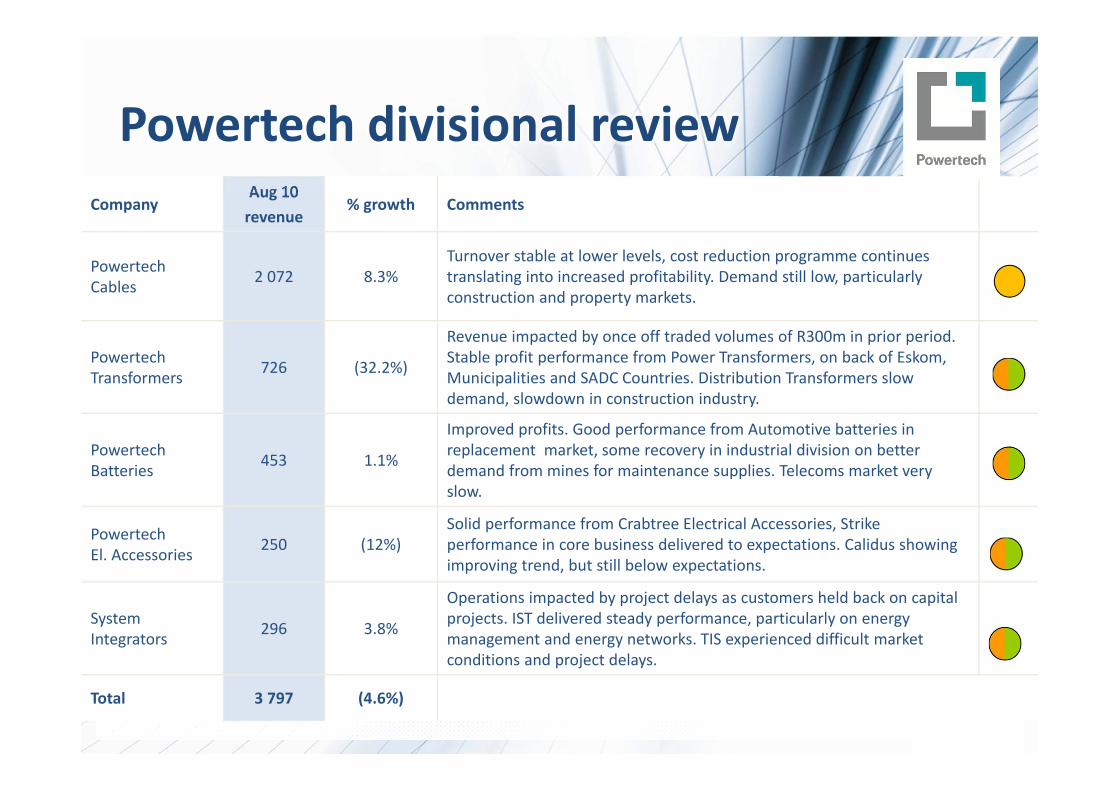

CompanyAug 10revenue

% growth Comments

Powertech Cables 2 072 8.3%

Turnover stable at lower levels, cost reduction programme continues translating into increased profitability. Demand still low, particularly construction and property markets.

Powertech Transformers 726 (32.2%)

Revenue impacted by once off traded volumes of R300m in prior period. Stable profit performance from Power Transformers, on back of Eskom, Municipalities and SADC Countries. Distribution Transformers slow demand, slowdown in construction industry.

Powertech Batteries 453 1.1%

Improved profits. Good performance from Automotive batteries in replacement market, some recovery in industrial division on better demand from mines for maintenance supplies. Telecoms market very slow.

Powertech El. Accessories 250 (12%)

Solid performance from Crabtree Electrical Accessories, Strike performance in core business delivered to expectations. Calidus showing improving trend, but still below expectations.

System Integrators 296 3.8%

Operations impacted by project delays as customers held back on capital projects. IST delivered steady performance, particularly on energy management and energy networks. TIS experienced difficult market conditions and project delays.

Total 3 797 (4.6%)

Powertech divisional review

Total Powertech order bookFeb 2009 Aug 2009 Feb 2010 Aug 2010

Aberdare Cables R 515 m R 332 m R 365 m R 332 m

Transformers R 1 535 m R 1 070 m R 862 m R 1 169 m

Batteries R 25 m R 18 m R 13 m R 20 m

Industrial R 34 m R 24 m R 30 m R 28 m

Systems Integrators R 230 m R 230 m R 230 m R 214 m

Total R 2 339m R 1 674m R 1 500m R 1 763m

0

500

1000

1500

2000

2500

Feb 09 Aug 09 Feb 10 Aug 10

Market conditions remain challenging particularly in telecoms, building and construction industries

Cost and working capital management remain focus items for management

Utilities demand for electrical products showing improving trend

Market penetration for new Switchgear product to be a focus area in next 6 months

Increase marketing of basket of Powertech products over the next year, some success with gain of contracts at utilities and industry

Exploring opportunities for turnkey solutions to adress delays in infrastructure delivery

Powertech – the way forward

Cautiously Optimistic

Altron – the road aheadRobert VenterChief Executive

Source: McKinsey Global Institute report‐Lions on the move: The progress and potential of African economies

Source: McKinsey Global Institute report‐Lions on the move: The progress and potential of African economies

Customer alliances offer opportunities in Africa – banking and retail

Altech Stream East Africa remains significant growth driver for Altech

Growth in population and working age profile

Urbanisation and rise of middle class African consumer are stimulating consumer and infrastructure spending

Bytes already active in 26 countries and are planning to extend IT presence in East Africa in collaboration with Altech

NEPAD power projects aimed at boosting electrical power generation, distribution and transmission in Africa – opportunities for Powertech

Building on group’s existing footprint in Africa

Focus on Africa

Altron in Africa

Companies with operational presence Altech Bytes Powertech

R millions Exports Sales TotalAFRICA 872 1 082 1 954Kenya 56 440 497Namibia 149 191 340Mauritius 274 61 335Nigeria 20 217 237Botswana 94 70 164Mozambique 81 41 122Tanzania 33 14 47Uganda 2 42 45% of Altron revenue 4% 5% 9%

12 months to Feb 2010

Visibility remains limited and strong rand will continue to impact on translation of results of foreign operations, reduced exports and increased competition from imports

Despite indications that economic recovery is slowing down, prospects for the second half are positive given the expected turnaround in Altech’s performance and continued recovery from Bytes and Powertech

Powertech will require enhanced demand levels to drive growth in its businesses

Board remains optimistic that group is well positioned to capitaliseon future growth opportunities

Outlook

Questions

![988 hoffman[1]](https://img.dokumen.tips/doc/110x75/559b31c91a28abdb568b4569/988-hoffman1.jpg)