Embed Size (px)

Citation preview

ALPHA BANK:

AGENDA 2010 REVISITED

Capital Markets Day

Bucharest, April 20, 2007

Retail Banking

G. Aronis, Executive General Manager

2

Strategic Emphasis on Retail Banking

Rationalize product offering

Apply sales oriented approach

Leverage on branch network: competitive advantage

Streamline multi-channel banking

Improve risk management

Centralize credit approval

Further enhance customer service quality

3

Action Plan is Already Paying Off in Household Lending

1.4 1.9 2.7 3.23.9

5.06.8

8.4

2003 2004 2005 2006

Consumer Credit Mortgages

(€ billion)

Mortgages & Consumer Credit Balances

5.36.9

9.411.6

30%CAGR 2004-2006

4

… Which is Further Evidenced by a Very Strong Q1 in 2007

208

126153 160

Q1 2004 Q1 2005 Q1 2006 Q1 2007Consumer Credit

(€ million)

385327320

174

Q1 2004 Q1 2005 Q1 2006 Q1 2007

Mortgages

(yoy growth)

(€ million)

(yoy growth)

21.4%4.6%

30%

83.9%2.2%

17.8%

5

… Setting the Stage for Meeting the 2010 Targets

3.2

2006 2010

Consumer Credit

8.4

2006 2010

Mortgages

CAGR 20% - 22%

CAGR 17% - 19%

(€ billion)

(€ billion)

6

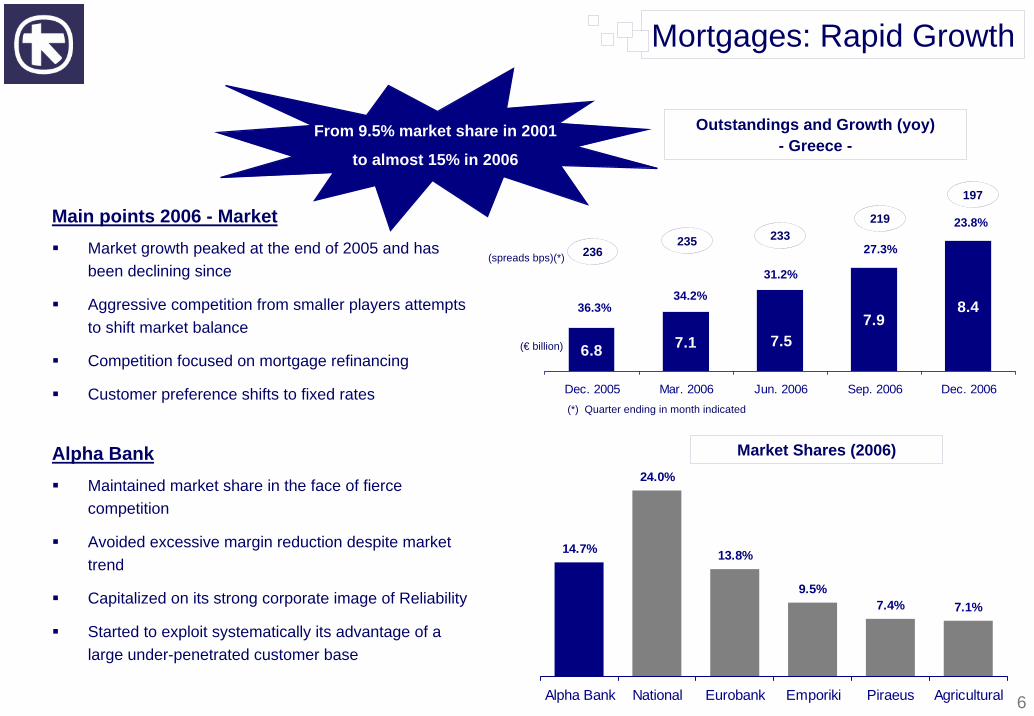

14.7%

24.0%

13.8%

9.5%7.4% 7.1%

Alpha Bank National Eurobank Emporiki Piraeus Agricultural

8.47.9

7.16.8 7.5

Dec. 2005 Mar. 2006 Jun. 2006 Sep. 2006 Dec. 2006

(spreads bps)(*)

Mortgages: Rapid Growth

(€ billion)

236

197

Outstandings and Growth (yoy)- Greece -

23.8%

Market Shares (2006)

(*) Quarter ending in month indicated

Main points 2006 - MarketMarket growth peaked at the end of 2005 and has been declining since

Aggressive competition from smaller players attempts to shift market balance

Competition focused on mortgage refinancing

Customer preference shifts to fixed rates

Alpha BankMaintained market share in the face of fierce competition

Avoided excessive margin reduction despite market trend

Capitalized on its strong corporate image of Reliability

Started to exploit systematically its advantage of a large under-penetrated customer base

235 23327.3%

219

31.2%

34.2%36.3%

From 9.5% market share in 2001

to almost 15% in 2006

7

Mortgages: The Way Forward

Sales &

Market Share Growth

Regular offering of innovative productsEmphasis in maintaining existing portfolioContinuous advertising Cross-selling through promotional offers, direct marketingStaff performance evaluation & incentives Further growth of direct sales (i.e. sales agreements with developers, brokers, etc)

Efficiency

Business Process

Re-engineering

Full centralization of credit approval & operationsReview of collections operationsSimplification of branch operations to increase productivity

8

Consumer Loans

Consumer Loans Disbursements

Outstanding Balances have doubled in the last two years (€2.2 vs €1.1 billion)

Focus on improving / transforming the business

Highly competitive environment

Emphasis on balance transfer programs

New entries

0

100

200

300

400

Q1/03Q2/03

Q3/03Q4/03

Q1/04Q2/04

Q3/04Q4/04

Q1/05Q2/05

Q3/05Q4/05

Q1/06Q2/06

Q3/06Q4/06

Q1/07(est)

(€ million)

Market Overview Alpha Bank

Personal Loans

Market leading customer propositions(All in One - Effie award)

Multi channel lender (Branch Network - Direct mail –SMS Gate – Telemarketing )

Development through diversification of our strategic business model in order to focus and approach quantity and quality loan volumes among middle size auto dealers

Expansion with full installation of Bank’s sales representatives all over Greece (starting with large cities)

Auto Loans

9

Maintain a profitable growth modelRetain and grow our market share Maintain low rates in delinquencies flows and arrears level

Personal Loans72%

Retail Factoring -

Other17%

Auto Loans11%

Auto Loans14%

Retail Factoring -

Other11%Personal

Loans75%

Personal Loans76%

Retail Factoring -

Other9%

Auto Loans15%

Outstanding Balance Origination

2004 2005 2006

Growing in the most profitable segment

2005 2006 change

107 147

1,880

782

1,360

37.3%

38.3%

778

NII (€ mn)

Average Balance (€ mn)

Spread (bps)

Consumer Loans

Key Initiatives Consumer Loans Business Results

10

Consumer Credit Risk: Quality is Top Priority

0.5%

1.0%

1.5%

2.0%

Dec-04 Mar-05 Jun-05 Sep-05 Dec-05 Mar-06 Jun-06 Sep-06 Dec-06

Prob

abili

ty

Ten scorecards for credit applications of new customers

Internal rating system, based on behavioral data

Application fraud detection tool

Overall acceptance rate at 63% in line with prudent credit policy

Credit strategies for each type of distribution channel risk

(Instant credit, Auto loans, Branches, Merchants)

Delinquencies on a declining trend (flow rates charts)

0.5%

1.0%

1.5%

2.0%

Dec-04 Mar-05 Jun-05 Sep-05 Dec-05 Mar-06 Jun-06 Sep-06 Dec-06

Pro

babi

lity

Flow Rates Credit Cards(Probability to default 4 months forward)

Flow Rates Consumer Loans(Probability to default 4 months forward)

11

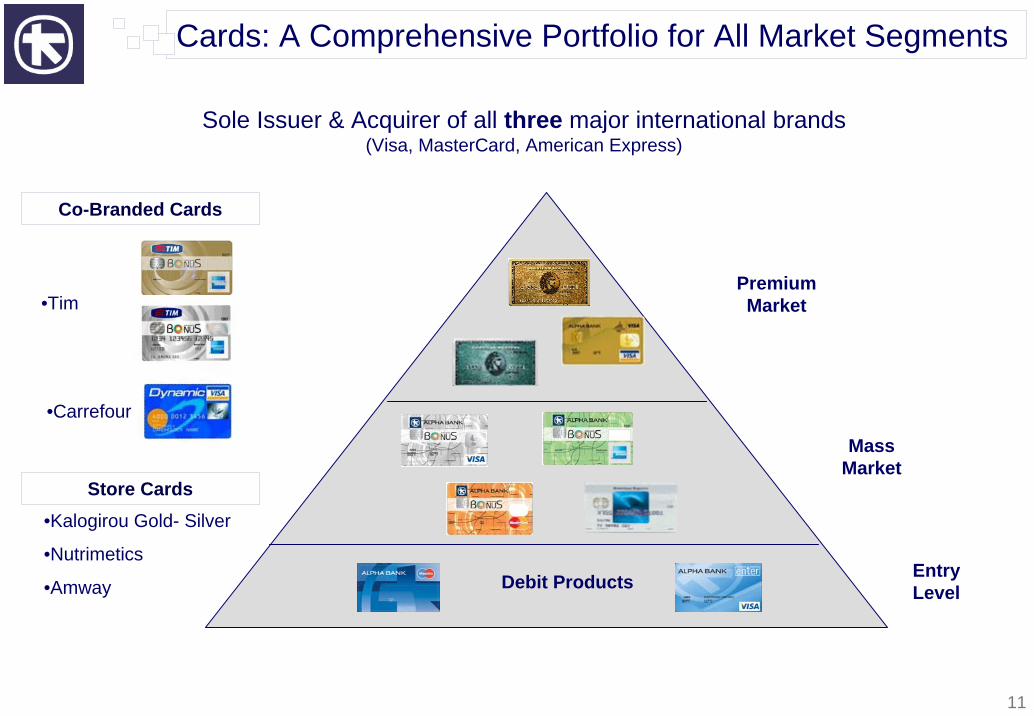

Sole Issuer & Acquirer of all three major international brands(Visa, MasterCard, American Express)

Cards: A Comprehensive Portfolio for All Market Segments

Debit Products

Premium Market

Mass Market

Entry Level

•Kalogirou Gold- Silver

•Nutrimetics

•Amway

•Tim

•Carrefour

Co-Branded Cards

Store Cards

12

AMEX37%

MASTERCARD14%

VISA49%

Growth focus on credit through carefully designed portfolio mix

Business growth outpacing the market (9.4% in balances vs. market 3.2%)

The largest Visa Issuer in the country

Sole American Express issuer

Cards: Fast Growing Business

MASTERCARD16%

AMEX22%

VISA62%

9.1% growth in 2006 while maintaining premium in commissions over competition

One of the largest merchant networks (110,000 merchants – 45,000 POS)

Sole acquirer of American Express products

EMV rollout on-going

Acquiring Market Share 28%

Acquiring Business by Brand€1.75 billion in 2006

Credit Cards In Force by Brand1 million cards (year end 2006)

Issuing Market Share 20%(Billed Business and CIF)

13

Continuous increase in revenues and balances

High retainable spreads (900 bps)

(€ million)2005 2006 %

change

117.0

77.3

39.7

Average Card Balance 845.2 950.0 12.4%

13.9%

17.9%138.0

86.2

51.8

11.5%

30.5%

14.6%

Total Income

- NII

- Commissions

Gross Revenue Margin

Cards: Fast Growing Business

Innovative Product Development

Value proposition reinforcement with latest technology chip based loyalty schemes

Customer Segmentation – niche segments

Increase penetration though cross selling

Accelerate sales through more efficient use of alternative channels

Key ActionsHigh Profitable Sector

Card Business Income

14

The BonuS Loyalty / Reward Scheme

Leading Private Retail Bank

Leading Car Rental Agency

Leading Greek Airline

Leading Grocery Retailer

LeadingMobile Phone

Operator

LeadingFuel Retailer

Instant rewardsPoints collectionOne scheme for allTechnologically innovativeFocussed on customer insight

Customer Loyalty – Merchant Loyalty – Card Loyalty

Scheme Partners Other Participating Merchants

15

Instant rewardsRelevant promotionsConvenience & Simplicity

Generate higher turnoverAcquire new customersHigher business profileBetter customer knowledge

Increased credit card volumes, spend & activationReduced attritionStrengthening the AcquiringbusinessGreater value to merchants

The BonuS Loyalty / Reward Scheme

BonuS achieves a win-win-win situation between all participants …

Merchants

6 Partners, 100+ Retailers

Customers

360,000 customers/cards to date

Alpha Bank

Amex, Visa, MasterCard

16

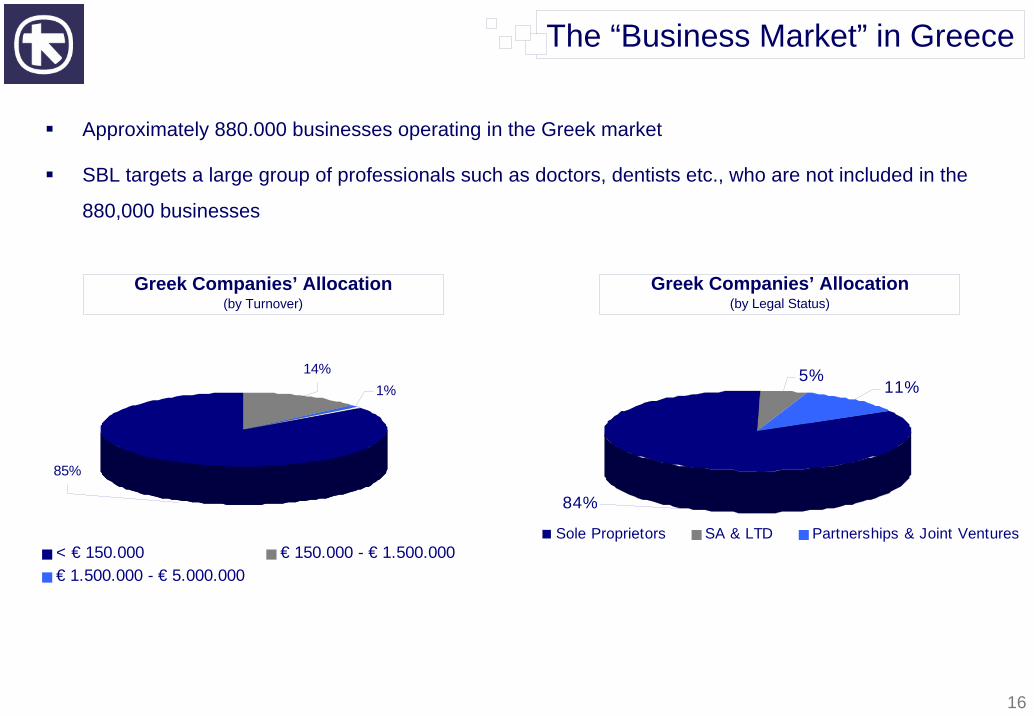

Approximately 880.000 businesses operating in the Greek market

SBL targets a large group of professionals such as doctors, dentists etc., who are not included in the

880,000 businesses

14%1%

85%

< € 150.000 € 150.000 - € 1.500.000€ 1.500.000 - € 5.000.000

84%

5%11%

Sole Proprietors SA & LTD Partnerships & Joint Ventures

The “Business Market” in Greece

Greek Companies’ Allocation(by Turnover)

Greek Companies’ Allocation(by Legal Status)

17

Customer Segmentation– Establishment of Small Business Financing Division, targeting:

• Small Businesses (turnover up to €2.5 million or credit limits of up to €1 million) and • Self-Employed Professionals

Advertising – Launch of a new Advertising Campaign focused on SBL– Targeted Promotional Activities (direct marketing)

Targets and performance evaluation for key products New Product Development

Small Business Lending

545 658 818 900 1,017

2,904 2,908 2,901 2,9092,928

534578 576 565 555

Dec. 2005 Mar. 2006 June 2006 Sept. 2006 Dec. 2006

New loan facilities to businesses with turnover up to € 1 millionSpreads (quarter ending in month indicated)

Growing use of alternative channels – Emphasis on third party salesforce– Collaboration with the Credit Guarantee Fund

of Small & Very Small EnterprisesCentralization of operations

– Standardized process – Effective credit administration support

Small business advisors in Branches

Specialised department to handle financing for pleasure boats

Key Drivers For Success

Small Business Loans (credit limits < 1 million) Outstanding and Growth

3,473 3,726 3,9263,562 3,801

18

Offer an array of privileges and potentialsFull complement of competitive deposit accounts with high cross – selling potential

- Alpha 1|2|3 Youth Line: Build loyalty to future active customers (children & young people) and increase cross – selling potentials to guardians

- Alpha Payroll: Dynamic launch of new competitive product to increase deposit market share. Develop new long standing relationships and Cross – selling potential

- E-Savings: Drive digital innovation capitalizing on Alpha’s predominant Web Banking position

Deposit & Investment Products: Dynamic & Innovative Approach

25.0%22.0%21.3%

19.4%

115

10393

79

2004 205 2006 2010F

Market Share in Non-Money Market Mutual FundsGross Revenue Margin (quarter ending in month indicated)

Deposit Products

Investment Products

Develop Integrated Investment Solutions for Customers’ ProfilesDeliver wealth management solutions to satisfy the increasing risk appetite of retail investors

Pioneer unique investment products to domestic market

- Alternative Investments

- Mutual Funds with preservation of capital product range

- Emerging Market Mutual Funds

Offer Bundled/Life Event propositions

Further increase market share and average management fees

Asset Management

185 298 341856 1,168 1,379

2,309

3,1003,637

Dec. 04 Dec. 05 Dec. 06

Discretionary Advisory Prime Brokerage

3,350

4,566 5,356

20% 2007-2010 CAGR

Alpha Private Bank

(bps)

(€ million)

19

3.0 4.0

14.6 14.6

10.113.3

5.2

4.24.4

5.1 Private Banking andInstitutional Money

Mutual Funds

Time Deposits plusAlpha Bank Bonds

Savings and SightDeposits (Domestic)

Deposits (abroad)

€ 37.3 bn

€ 41.2 bn

Stable funding base

Successful placement of Alpha Bank bonds with retail

Still high liquidity preference despite low returns

Gradual shift to higher margin investment products

Financial planning advisory services for mass affluent customers (> € 60,000)

Customer Assets

31.7%

(3.2%)

8.1%

10.4%

Investment Balances

Liquidity

Transaction Balances

Dec. 2005 Dec. 2006

From Deposits to Investments

CAGR 2007-2010

10% - 14%

20

A New Banking Experience

Approach

Targets the Mass Affluent segment• Market size* : € 20 bln• No. Clients* : 200,000

Mass Affluent Market (60-300)**Levels of Wealth

HNW

Retail

Mass Affluent

(300+)**

(0-60)**

** amounts in thousands €

ALPHAPrime Goal• 20% of market size• Presence in approx. 120 Branches • 140 Investment Advisors

• The establishment of long term relationships with clients• Specialized personnel in selected branches (Investment Advisors)• Excellence in customer experience (Convenience & Flexibility)• Specialized area in the Branch hosting the Service

• Specially designed Investment Offering with products targeting the specific market aiming at higher profitability

• Specially designed Banking Offering enriched with preferential terms• Use of the Private Banking infrastructure (Sales Approach, Back Office, IT, MIS-

Client Profitability, Specialized Intranet Applications)• Use of a specialized call center• Continuous training of Investment Advisors

Offering & Infrastructure

Present Status & Future Deployment

• 30 Branches already operational aiming at a total of 70 Branches operational by the end of 2007

• Full deployment by mid 2008*source: ALPHA PRIVATE BANK estimates

21

Bancassurance: Significant Growth Opportunities

Sale of Insurance subsidiary to AXA

Long term (20 years) cooperation agreement in Bancassurance

Agreement covers both Greek and SE Europe operations

Benefit form the support and expertise of one of the major international insurance companies

Redesign of products – processes – personnel training

5.9 6.4

>30

2005 2006 Target 2010

Substantial margin for increase in insurance cross selling ratio for Consumer Credit, Mortgages and SME loans

Substantial margin for increase in Pensions –Savings

Target to achieve € 30 million in insurance fees by 2010 (Bank and Asset Management)

Insurance Fees & Commissions

(€ million)

CAGR 2007

-2010

~50%

22

Retail Branch Network (Greece): Types, Size & Distribution

2006 2007

Athens and suburbs 171 180

Salonica 37 42

Other areas 167 173

Total 375 395

Ideal Country size

Strong urban concentration

GIS optimized (next slide)

TRANSACTIONS

INDIVIDUALS Prime Banking(selected branches)

SMALL ENTERPRICES (selected branches)

Non - Teller Branches are currently under consideration

BRANCH STRUCTURE: A modular approach

Key PointsBranches per Area

23

Retail Branch Network (Greece): Planning

Demographic data Economic data

Product specific data

ANNUAL GOALS

Competition data

BRANCHES & STAFF DISTRIBUTION

Geographical Information Systems &

Methodology

24

Retail Branch Network (Greece): Annual Targets & Evaluation

ANNUAL TARGETS are set for:

• Deposits (per category)

• Loans (per category)

• Mortgages

• Credit cards

• Prime & Private Banking

• Bonds & Mutual Funds

• Insurance (per category)

• Bancassurance

• Small Enterprises attracted

• Per product methodology

• GIS optimized

• Goals are reevaluated if necessary

• Performance is monthly monitored

• Products are weighted according to their importance

• Specific product campaigns are launched during the year if necessary

Branch Evaluation is currently based on annual goals

achievement

APPLICABLE within 2007

A more detailed evaluation to be based on:

• Impairments

• Spreads

• Quality of Service (complains, internal audit reports, etc.)

ALPHA BANK:

AGENDA 2010 REVISITED

Capital Markets Day

Bucharest, April 20, 2007