Embed Size (px)

Citation preview

n by the FinAnciAl stAtements review committee

te

Ch

niC

al

Financial Reporting disclosuresSHEDDING LIGHT ON AN ENTITY’S PERFORMANCE

The Committee noted that approximately 37% entities accounted for FGCs issued as contingent liabilities in accordance with MFRS 137 “Provisions, Contingent Liabilities and Contingent Assets”. Where it had been assessed that an outflow of cash is not probable, these FGCs were disclosed as contingent liabilities. MFRS 137 does not apply to financial instruments (including guarantees) that are within the scope of MFRS 139 “Financial Instruments: Recognition and Measurement” (MFRS137.2).

These corporate guarantees are FGCs that meet the definition of financial liabilities and shall be recognised and measured in accordance with MFRS 139. FGCs are initially measured at fair value which take into consideration the probability, extent and expected timing of an outlay of cash by the guarantor due to a default by the borrower.

After initial recognition, FGCs shall be measured at the higher of the best estimate of the amount required to settle the obligation in accordance with MFRS 137 and the amount initially recognised

FINANCIAl reporting serves as a fundamental medium of communication between an entity and its stakeholders. Management and the Board of Directors are entrusted with the assets of an entity and financial reports illustrate how effective they have been in managing these assets to drive performance. By observing how management has exercised professional judgement in determining what is important and how to disclose it, stakeholders are able to gauge the quality of an entity’s management.

In providing guidance to members on good financial reporting, the Financial Statements Review Committee (“FSRC” or “the Committee”) wishes to highlight deficiencies arising from their review of financial statements of public-listed entities for the period from July 2015 to June 2016.

finanCial Guarantee ContraCts (fGCs)

Typically, a parent entity issues corporate guarantees to financial institutions to secure credit facilities extended to subsidiary companies.

82 accountants today | Nov 2016 - Feb 2017

finAnCiAl reporting disClosures

less where appropriate, cumulative amortisation is recognised (MFRS 139.47(c)).

MFRS 4 “Insurance Contracts” can only be applied if an issuer of FGCs has previously asserted explicitly that it regards such contracts as insurance contracts and has used accounting applicable to insurance contracts; hence, the issuer may elect to apply MFRS 139 or MFRS 4 to such contracts. The issuer may make that election contract by contract, but the election for each contract is irrevocable (MFRS 139.2(e)).

Where the issuer has the option to apply MFRS 4 but does not elect to do so, the issued FGCs shall be accounted for in accordance with the provisions of MFRS 139 (MFRS 139.2(e)).

The Committee wishes to reiterate that there should be clear and consistent application of the accounting policy, accompanied with the respective disclosure requirements covered by MFRS 7 “Financial Instruments: Disclosures” or MFRS 4 accordingly.

CaPital manaGement

An entity is required to provide sufficient information to enable stakeholders to evaluate the entity’s objectives, policies and processes for managing capital (MFRS 101.134). Such disclosure communicates important information about the entity’s capital strategy. As each entity has different definitions of what it manages as capital, an entity is required to disclose qualitative

and quantitative information to illustrate what it manages as capital (MFRS 101.135).

However, approximately 21% of the financial statements reviewed did not have summary quantitative data about what is being managed as capital. The disclosures should reflect the information provided internally to the entity’s key management personnel. An example of how the disclosure requirements are met is illustrated in IG10 of MFRS 101.

liquidity risk disClosures

Commonly, an entity only discloses the contractual undiscounted cash flows for the principal amount of the term loans but fails to factor in the contractual undiscounted interest cash flows in respect of the loans with approximately 21% of reviews performed displaying this error.

MFRS 7 “Financial Instruments: Disclosures” requires the disclosure of a maturity analysis for non-derivative financial liabilities that shows the remaining contractual maturities (MFRS7.39(a)). This should include all cash flows expected from the financial liability based on the contractual terms, including any interest payable. Therefore, total contractual undiscounted cash flows for term loans (including interest) is unlikely to be equal to the carrying amount of the term loans in the statement of financial position.

Illustrated below is an example of how the disclosures should be made:

carrying amount

contractual cash flows under 1 year 1-2 years 3-5 years More than

5 years

Trade payables 5,000 5,000 5,000 - - -

other payables 2,000 2,000 2,000 - - -

Term loans 16,900 18,000 3,000 5,000 5,000 5,000

bank overdraft 2,000 2,000 2,000 - - -

25,900 27,000 12,000 5,000 5,000 5,000

Financial guarantee contracts*

NIL 7,000 7,000 - - -

* The disclosure represents the maximum amount that is required to be settled in the event of a <triggering event>.

Nov 2016 - Feb 2017 | accountants today 83

te

Ch

niC

al

finAnCiAl reporting disClosures

oPeratinG seGments

The FSRC finds that certain disclosures required by MFRS 8 “Operating Segments” are omitted in the financial statements. For instance, approximately 16% of the financial statements reviewed did not have disclosures relating to the entity’s major customers.

If revenues from transactions with a single external customer amount to 10% or more of an entity’s revenue, the entity is required to disclose the following:

(i) The fact that there are customer(s) whose transactions amount to 10% or more of the entity’s revenue;

(ii) The total amount of revenue from each customer identified in (i); and

(iii) The identity of the segment(s) reporting the revenues

However, the entity need not disclose the identity of the major customer(s) nor the amount that each segment reports from the said customer(s) (MFRS 8.34). An example of how this disclosure requirement is met is illustrated via IG6 of MFRS 8.

These disclosures are necessary to enable stakeholders to gauge the entity’s extent of reliance on its major customers.

ConClusion

Above all, the FSRC wishes to reiterate that the responsibility for the preparation of financial statements under the Companies Act 1965 lies with the entity’s management and Board of Directors.

Whilst the auditor plays an important role in enhancing the credibility of the financial statements, this role would be further enhanced with the entity’s management and Board of Directors engaging with the auditors throughout the financial reporting process. This is especially crucial in

light of the enhanced auditor reporting requirements becoming effective from December 2016 onwards.

Parties in the financial reporting ecosystem should not treat financial reports as just another item to tick off their annual to-do-list. Instead, all parties should take the opportunity to engage stakeholders by enhancing the quality of financial reporting and providing comprehensive credible information on the financials of an entity. n

The Financial statements review Committee (“FSRC” or “the Committee”) of the Institute was set up with the aim of upholding the quality of financial reporting of entities listed on Bursa Malaysia.

The Committee reviews audited financial statements and audit reports that are prepared by or are the responsibility of members of MIA, for the purpose of determining compliance with statutory and other requirements, approved accounting standards and approved auditing standards in Malaysia.

84 accountants today | Nov 2016 - Feb 2017

n by the FinAnciAl reportinG stAndArds implementAtion committee

te

Ch

niC

al

MFrs 13 became effective for annual periods beginning on or after 1 January 2013, and this has had a significant impact on the financial statements of financial institutions (“FIs”). Auditors of FIs highlighted two pertinent implementation issues in relation to MFRS 13 which are as follow:

Determining the significance of a particular input to the fair value measurement of loans and advances, as well as deposits from customers; and

Reflecting the effects of credit risk and non-performance risk, as well as other adjustments in determining the fair value of derivatives.

In response to these concerns, the FRSIC Secretariat carried out a survey in relation to the above to better understand the current practices of FIs in Malaysia, and received responses from seven major FIs in Malaysia.

FAIr vAlUe hIerArchy DIScloSUre oF loAnS AnD ADvAnceS AnD DePoSItS From cUStomerS

Paragraph 97 of MFRS 13, among others, requires - for each class of assets and liabilities not measured at fair value in the statement of financial position but for

which the fair value is disclosed - an entity to disclose the level of the fair value hierarchy within which the fair value measurements are categorised in their entirety (i.e. Level 1, 2 or 3).

In relation to this, paragraph 73 of MFRS 13 states that “in some cases, the inputs used to measure the fair value of an asset or a liability might be categorised within different levels of the fair value hierarchy. In those cases, the fair value measurement is categorised in its entirety in the same level of the fair value hierarchy as the lowest level input that is significant to the entire measurement. Assessing the significance of a particular input to the entire measurement requires judgement, taking into account factors specific to the asset or liability. Adjustments to arrive at measurements based on fair value, such as costs to sell when measuring fair value less costs to sell, shall not be taken into account when

WE TAKE A LOOK AT THE IMPLEMENTATION issues on the application of MFRS 13 “Fair Value Measurement” by financial institutions in Malaysia.

fair value issues affeCtinG fis

86 accountants today | Nov 2016 - Feb 2017

fAir vAlue issues AffeCting fis

determining the level of the fair value hierarchy within which a fair value measurement is categorised”.

Survey findingsThe majority of respondents classify both

loans and advances, as well as deposits from customers, at Level 2. Such classification is determined by the significant inputs to the valuation techniques used to measure fair values. The respondents view the significant inputs as interest rates and counterparty credit risks.

Review of Financial Statements of Financial Institutions in Malaysia

Following the survey findings above, the

FRSIC Secretariat then carried out a review of financial statements of the licensed FIs in Malaysia other than those that have responded (a total of 7 FIs) to the survey. The review encompasses financial statements of 25 local and foreign FIs. The findings of the review are summarised in the diagram 1.

The review reveals that there are mixed practices by the 25 local and foreign FIs on the fair value hierarchy of loans and advances, as well as deposits from customers.

Review of Financial Statements of Financial Institutions in the UK, Australia and Hong Kong

The FRSIC Secretariat also performed a jurisdiction review of the top banks in the UK, Australia and Hong Kong and this is summarised in the diagram 02.

0

3

Loans and advances to customers

Deposits from customers

6

9

12

Level 2

Level 3

Some level 2, some level 3

CA approximates FV

4

0

1

UK Australia Hong Kong

2

3 Level 2

Some level 2, some level 3

CA approximates FV

Level 2

Level 3

Some level 2, some level 3

CA approximates FV

0

1

UK Australia Hong Kong

2

3

4

No

YesCVA

DVA

0 2 3 5 6

Quarterly

Monthly

Intraday pre-deal

DVA

CVA

0 2 3 5 6

diagram 1

0

3

Loans and advances to customers

Deposits from customers

6

9

12

Level 2

Level 3

Some level 2, some level 3

CA approximates FV

4

0

1

UK Australia Hong Kong

2

3 Level 2

Some level 2, some level 3

CA approximates FV

Level 2

Level 3

Some level 2, some level 3

CA approximates FV

0

1

UK Australia Hong Kong

2

3

4

No

YesCVA

DVA

0 2 3 5 6

Quarterly

Monthly

Intraday pre-deal

DVA

CVA

0 2 3 5 6

diagram 2deposits from customers

0

3

Loans and advances to customers

Deposits from customers

6

9

12

Level 2

Level 3

Some level 2, some level 3

CA approximates FV

4

0

1

UK Australia Hong Kong

2

3 Level 2

Some level 2, some level 3

CA approximates FV

Level 2

Level 3

Some level 2, some level 3

CA approximates FV

0

1

UK Australia Hong Kong

2

3

4

No

YesCVA

DVA

0 2 3 5 6

Quarterly

Monthly

Intraday pre-deal

DVA

CVA

0 2 3 5 6

loans and advances to customers

Nov 2016 - Feb 2017 | accountants today 87

te

Ch

niC

al

fAir vAlue issues AffeCting fis

The majority of top banks in the UK and Australia classify deposits from customers at Level 2 and loans and advances at Level 3. In contrast, the majority of top banks in Hong Kong state that the carrying amount of those balances approximate fair values. This may be due to different market conditions in these countries as compared to Malaysia, where the pricing in a more developed market is driven by customers’ individual ratings or credit quality.

Feedback received from the FRSIC Annual Forum with Finance Leaders of Financial Institutions in Malaysia

The findings of the survey as well as the review of financial statements of financial institutions in Malaysia and those of UK, Australia and Hong Kong were presented at the FRSIC Annual Forum with Finance Leaders of Financial Institutions in Malaysia. The feedback received on the findings is as follows:

Base financing rate (BFR) or base lending rate (BLR) is used as the input in the fair value measurement of loans and advances.

Homogenous financing such as housing loans and hire purchase will be classified at Level 2 as the banks use BLR or BFR in determining the fair value of these loans.

Financing with specific terms such as corporate loans tend to be classified at Level 3.

reFlectIng the eFFectS oF creDIt rISk AnD non-PerFormAnce rISk when DetermInIng the FAIr vAlUe oF DerIvAtIveS

When a derivative is not traded in an active market, its fair value is determined using a valuation technique (generally based on an income approach) as there is no observable market price for such instruments. A fair value measurement based on an income approach may include adjustments for liquidity, credit risk, or any other adjustments if these are based on assumptions that market participants would use.1

0

3

Loans and advances to customers

Deposits from customers

6

9

12

Level 2

Level 3

Some level 2, some level 3

CA approximates FV

4

0

1

UK Australia Hong Kong

2

3 Level 2

Some level 2, some level 3

CA approximates FV

Level 2

Level 3

Some level 2, some level 3

CA approximates FV

0

1

UK Australia Hong Kong

2

3

4

No

YesCVA

DVA

0 2 3 5 6

Quarterly

Monthly

Intraday pre-deal

DVA

CVA

0 2 3 5 6

diagram 3

0

3

Loans and advances to customers

Deposits from customers

6

9

12

Level 2

Level 3

Some level 2, some level 3

CA approximates FV

4

0

1

UK Australia Hong Kong

2

3 Level 2

Some level 2, some level 3

CA approximates FV

Level 2

Level 3

Some level 2, some level 3

CA approximates FV

0

1

UK Australia Hong Kong

2

3

4

No

YesCVA

DVA

0 2 3 5 6

Quarterly

Monthly

Intraday pre-deal

DVA

CVA

0 2 3 5 6

diagram 4

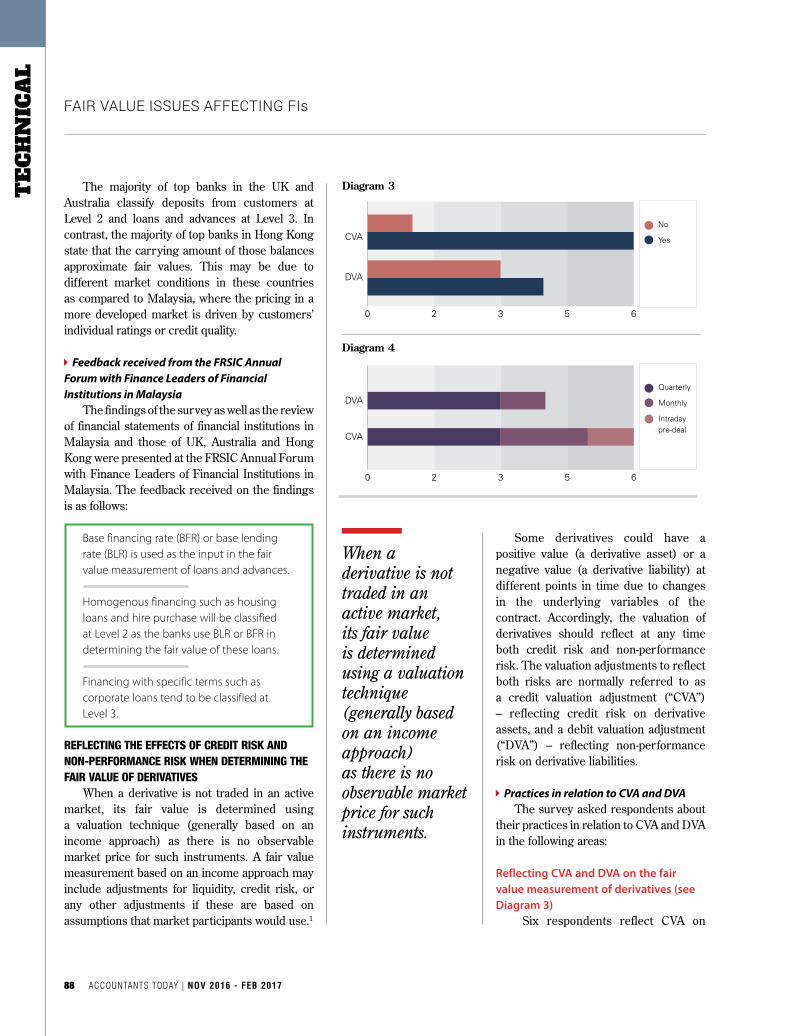

Some derivatives could have a positive value (a derivative asset) or a negative value (a derivative liability) at different points in time due to changes in the underlying variables of the contract. Accordingly, the valuation of derivatives should reflect at any time both credit risk and non-performance risk. The valuation adjustments to reflect both risks are normally referred to as a credit valuation adjustment (“CVA”) – reflecting credit risk on derivative assets, and a debit valuation adjustment (“DVA”) – reflecting non-performance risk on derivative liabilities.

Practices in relation to CVA and DVAThe survey asked respondents about

their practices in relation to CVA and DVA in the following areas:

Reflecting CVA and DVA on the fair value measurement of derivatives (see Diagram 3)

Six respondents reflect CVA on

When a derivative is not traded in an active market, its fair value is determined using a valuation technique (generally based on an income approach) as there is no observable market price for such instruments.

88 accountants today | Nov 2016 - Feb 2017

fAir vAlue issues AffeCting fis

and DVA on a particular day for new deals (in other words, intraday pre-deal) for collateral estimation and subsequent continuing valuation.

Active management of CVA and DVAThe majority of respondents do not

actively manage CVA and DVA which may indicate that such information is not used for risk management purposes.

Additional questions in relation to CVA

The survey also asked two additional questions in relation to CVA which are as follows:

Level at which CVA is booked Three respondents book CVA

at entity level while the remaining respondents book CVA either at desk or book level. It appears that the financial institutions reflect CVA for the purpose of financial reporting rather than using it in their daily operations for risk management purposes.

Reflecting CVA on collaterised derivatives

Collaterised derivatives are those derivatives where entities entered into collateral arrangements in order to limit the potential exposure. Three respondents record CVA on collaterised derivatives. Four respondents do not record CVA on such derivatives with one of them arguing that CVA is not required because collateral arrangements will mitigate the credit risk. n

1 KPMG (2013) “Fair Value Measurement: Questions and Answers”.

2 Paragraph 67 of MFRS 13.

their derivative assets while only four respondents reflect DVA on their derivative liabilities citing the following reasons for doing so: prevailing market practices, complying with accounting standards and group accounting policy, and reflecting the effects of credit risk and non-performance risk. The respondents who do not record such adjustments cited materiality and inherent model limitations as reasons not to reflect these adjustments.

Inputs used to determine CVA and DVAThe majority of respondents use

a mixture of market and historical data (“blended approach”) to calculate CVA. Examples of data being used to calculate CVA include interest rate curve, foreign exchange rate curve, published rating information by RAM Rating Services Berhad and collateral information. This also indicates that to a certain extent, market observable inputs are used in calculating CVA. In the absence of market observable data, unobservable inputs are used. MFRS 13 “Fair Value Measurement” requires entities to maximise the use of relevant observable inputs and minimise the use of unobservable inputs.2

Those respondents who reflect DVA on their derivative liabilities, use inputs such as credit default swap (“CDS”), secondary market data, blend data, probability of default (“PD”), loss given default (“LGD”), collateral information and risk rating information.

General methodology used to determine CVA and DVA

The majority of respondents who reflect CVA use mark-to-market approach to determine CVA. Half of respondents who reflect DVA also use mark-to-market approach.

Changes to CVA and DVA methodology used

More than half of the respondents expect changes in the existing CVA and DVA methodologies.

Frequency of recording of CVA and DVA (see Diagram 4)

Three respondents record CVA and DVA on a quarterly basis due to either significance of the amount or for the purpose of quarterly financial reporting. One respondent who only reflects CVA records it on a monthly basis following its group standard methodology, while another respondent records both CVA

Nov 2016 - Feb 2017 | accountants today 89

n by the public sector AccountinG committee

te

Ch

niC

al

What is mPsas?

The Federal government of Malaysia currently prepares its financial statements using modified cash accounting. As part of the Public Finance Reform Initiative under the Economic Transformation Programme (ETP), the financial statements of the Federal government will be prepared using the accrual basis of accounting.

As such, Malaysian Public Sector Accounting Standards (MPSAS) are issued to assist the implementation of accrual accounting in Malaysia. MPSAS is drawn from the International Public Sector Accounting Standards (IPSASs) issued by the International Public Sector Accounting Standards Board (IPSASB), an independent standard-setting board with the following goals and objectives:

i. Developing high-quality public sector financial reporting standards;

ii. Developing other publications for the public sector; and

iii. Raising awareness of IPSAS and the benefits of their adoption.

IPSASs are generally based on standards issued by the International Accounting Standards Board (IASB) with differences specific to the public sector environment. MPSASs are endorsed by the Government Accounting Standards Advisory Committee (GASAC) and approved by the Accrual Accounting Steering Committee (AASC) under the Accountant General’s Department.

Private seCtor entities

Entities in the private sector in Malaysia, on the other hand, adopt the three-tier financial reporting structure:1. Malaysian Financial Reporting

Standards (“MFRS”) for entities other than private entities and transitioning entities1. MFRSs are identical to IFRSs in all aspects other than the nomenclatures.

2. Financial Reporting Standards (“FRS”) for transitioning entities. FRS are adapted from IFRS with the following exceptions: a. in the FRS framework, IC

Interpretation 15 Agreements for the Construction of Real Estate will be withdrawn and FRS 2012004 Property Development Activities will continue to be the extant standard for accounting for property development activities;

b. in the FRS framework, there is no equivalent standard to IAS 41 Agriculture; and

c. in the FRS framework, there are two other local standards, i.e. FRS 2042004 Accounting for Aquaculture and IC Interpretation 201 Preliminary and Pre-operating Expenditure, in addition to FRS 201.

3. Private Entities Reporting Standards (“PERS”) or Malaysian

Understanding the Differences between

iN The NexT Few issues, mia will provide readers wiTh a series oF arTicles compariNg The Three FiNaNcial reporTiNg Frameworks iN malaysia, which are mpsas, mFrs aNd mpers. These arTicles will also assess The impacT oN aN eNTiTy ThaT moves From pers To aNy oF These Frameworks. sTay TuNed.

mPsas, mfrs and mPers

90 accountants today | Nov 2016 - Feb 2017

understAnding tHe differenCes BetWeen MpsAs, Mfrs And Mpers

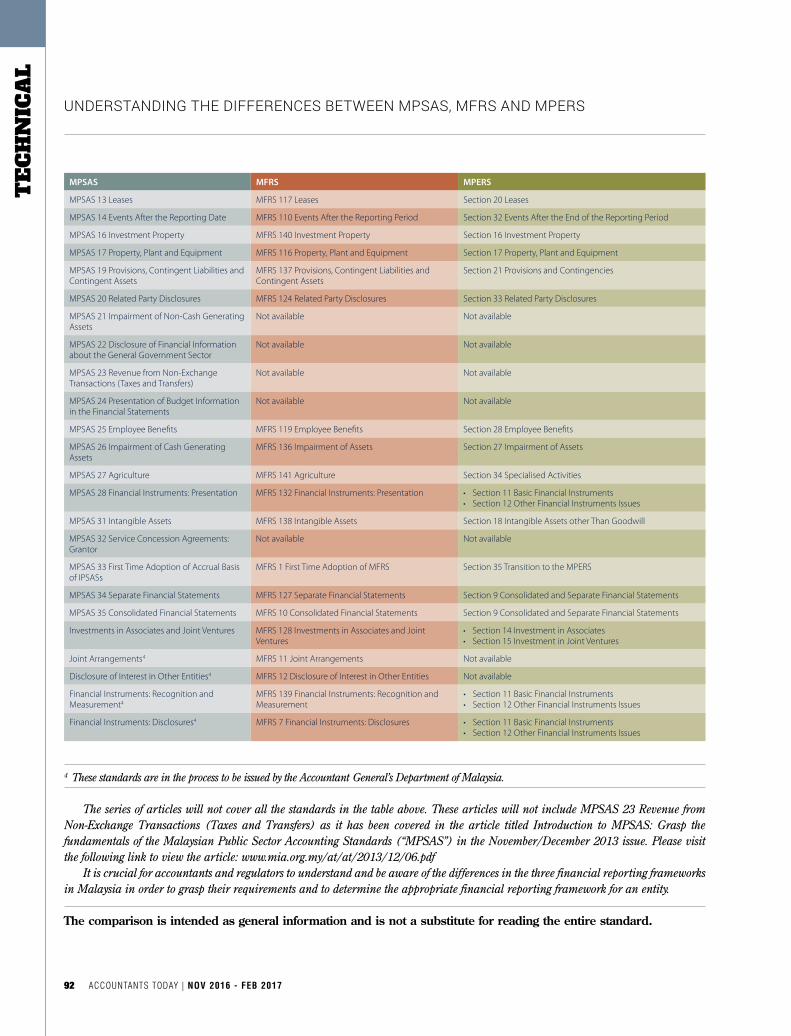

MPSAS3 MFRS MPERS

MPSAS 1 Presentation of Financial Statements MFRS 101 Presentation of Financial Statements • Section 3 Financial Statements Presentation• Section 4 Statement of Financial Position• Section 5 Statement of Comprehensive Income and Income

Statement• Section 6 Statement of Changes in Equity and Statement of

Income and Retained Earnings• Section 8 Notes to the Financial Statements

MPSAS 2 Cash Flow Statements MFRS 107 Statement of Cash Flows Section 7 Statement of Cash Flows

MPSAS 3 Accounting Policies, Changes in Accounting Estimates and Errors

MFRS 108 Accounting Policies, Changes in Accounting Estimates and Errors

Section 10 Accounting Policies, Estimates and Errors

MPSAS 4 The Effects of Changes in Foreign Exchange Rates

MFRS 121 The Effects of Changes in Foreign Exchange Rates

Section 30 Foreign Currency Translation

MPSAS 5 Borrowing Costs MFRS 123 Borrowing Costs Section 25 Borrowing Costs

MPSAS 9 Revenue from Exchange Transactions • MFRS 118 Revenue• MFRS 15 Revenue from Contracts with Customers

Section 23 Revenue

MPSAS 11 Construction Contracts MFRS 111 Construction Contracts Section 34 Specialised Activities

MPSAS 12 Inventories MFRS 102 Inventories Section 13 Inventories

Private Entities Reporting Standards (“MPERS”) for private entities2. MPERS is identical to the IFRS for Small and Medium Enterprises (SMEs), except for the requirements in relation to property development activities and consolidated and separate financial statements.FRS, MFRS and MPERS are

financial reporting frameworks that are applicable to companies incorporated under the Companies Act 1965 and fall under the purview of the Malaysian Accounting Standards Board (MASB).

ComParinG the frameWorks

In the next few issues, Accountants Today will publish a series of articles in relation to:a. comparison of the three financial

reporting frameworks in Malaysia, which are MPSAS, MFRS and MPERS; and

b. the impact on an entity that moves from PERS to any of these frameworks. The objectives of the comparison

between the three financial reporting frameworks are as follow:• To provide a quick insight

to practitioners (accountants and auditors) as well as both public sector and private sector stakeholders on information pertaining to financial reporting frameworks in the two sectors;

• Tohighlightsignificantdifferencesof the accounting requirements between the three frameworks;

• To assist regulators to decide onthe suitable financial reporting framework for an entity; and

• To create public awareness ofthe various financial reporting frameworks in Malaysia.The comparison will focus on the

significant requirements in MPSAS that are similar and different from the requirements in MFRS and MPERS in relation to (i) recognition, (ii) measurement; (iii) presentation and disclosures; and (iv) any relief for first-time adopters. The comparison will not discuss the relevant requirements in MFRS or MPERS that are not available in MPSAS. The list of MPSAS and its equivalent MFRS and MPERS are as follows:

1 Transitioning entities (“TE”) are entities that satisfy the following criteria:a. An entity that would otherwise be

subject to the application of MFRSs as its financial reporting framework and thereby be subject in particular to the application of MFRS 141 and/or IC Interpretation 15

b. An entity that consolidates or equity accounts another entity that has chosen to apply FRSs as its financial reporting framework.

2 A private entity is a private company, incorporated under the Companies Act 1965, that -a. is not itself required to prepare or lodge

any financial statements under any law administered by the Securities Commission or Bank Negara Malaysia; and

b. is not a subsidiary or associate of, or jointly controlled by, an entity which is required to prepare or lodge any financial statements under any law administered by the Securities Commission or Bank Negara Malaysia.

3 MPSAS 6, 7, 8 and 15 is superseded by the upcoming standards in item 26, 27, 28 and 32 in the list respectively. MPSAS 10 Financial Reporting in Hyperinflationary Economies and MPSAS 18 Segment Reporting are not adopted by the Accountant General’s Department of Malaysia.

Nov 2016 - Feb 2017 | accountants today 91

te

Ch

niC

al

understAnding tHe differenCes BetWeen MpsAs, Mfrs And Mpers

4 These standards are in the process to be issued by the Accountant General’s Department of Malaysia.

The series of articles will not cover all the standards in the table above. These articles will not include MPSAS 23 Revenue from Non-Exchange Transactions (Taxes and Transfers) as it has been covered in the article titled Introduction to MPSAS: Grasp the fundamentals of the Malaysian Public Sector Accounting Standards (“MPSAS”) in the November/December 2013 issue. Please visit the following link to view the article: www.mia.org.my/at/at/2013/12/06.pdf

It is crucial for accountants and regulators to understand and be aware of the differences in the three financial reporting frameworks in Malaysia in order to grasp their requirements and to determine the appropriate financial reporting framework for an entity.

the comparison is intended as general information and is not a substitute for reading the entire standard.

MPSAS MFRS MPERS

MPSAS 13 Leases MFRS 117 Leases Section 20 Leases

MPSAS 14 Events After the Reporting Date MFRS 110 Events After the Reporting Period Section 32 Events After the End of the Reporting Period

MPSAS 16 Investment Property MFRS 140 Investment Property Section 16 Investment Property

MPSAS 17 Property, Plant and Equipment MFRS 116 Property, Plant and Equipment Section 17 Property, Plant and Equipment

MPSAS 19 Provisions, Contingent Liabilities and Contingent Assets

MFRS 137 Provisions, Contingent Liabilities and Contingent Assets

Section 21 Provisions and Contingencies

MPSAS 20 Related Party Disclosures MFRS 124 Related Party Disclosures Section 33 Related Party Disclosures

MPSAS 21 Impairment of Non-Cash Generating Assets

Not available Not available

MPSAS 22 Disclosure of Financial Information about the General Government Sector

Not available Not available

MPSAS 23 Revenue from Non-Exchange Transactions (Taxes and Transfers)

Not available Not available

MPSAS 24 Presentation of Budget Information in the Financial Statements

Not available Not available

MPSAS 25 Employee Benefits MFRS 119 Employee Benefits Section 28 Employee Benefits

MPSAS 26 Impairment of Cash Generating Assets

MFRS 136 Impairment of Assets Section 27 Impairment of Assets

MPSAS 27 Agriculture MFRS 141 Agriculture Section 34 Specialised Activities

MPSAS 28 Financial Instruments: Presentation MFRS 132 Financial Instruments: Presentation • Section 11 Basic Financial Instruments• Section 12 Other Financial Instruments Issues

MPSAS 31 Intangible Assets MFRS 138 Intangible Assets Section 18 Intangible Assets other Than Goodwill

MPSAS 32 Service Concession Agreements: Grantor

Not available Not available

MPSAS 33 First Time Adoption of Accrual Basis of IPSASs

MFRS 1 First Time Adoption of MFRS Section 35 Transition to the MPERS

MPSAS 34 Separate Financial Statements MFRS 127 Separate Financial Statements Section 9 Consolidated and Separate Financial Statements

MPSAS 35 Consolidated Financial Statements MFRS 10 Consolidated Financial Statements Section 9 Consolidated and Separate Financial Statements

Investments in Associates and Joint Ventures MFRS 128 Investments in Associates and Joint Ventures

• Section 14 Investment in Associates • Section 15 Investment in Joint Ventures

Joint Arrangements4 MFRS 11 Joint Arrangements Not available

Disclosure of Interest in Other Entities4 MFRS 12 Disclosure of Interest in Other Entities Not available

Financial Instruments: Recognition and Measurement4

MFRS 139 Financial Instruments: Recognition and Measurement

• Section 11 Basic Financial Instruments• Section 12 Other Financial Instruments Issues

Financial Instruments: Disclosures4 MFRS 7 Financial Instruments: Disclosures • Section 11 Basic Financial Instruments• Section 12 Other Financial Instruments Issues

92 accountants today | Nov 2016 - Feb 2017