Embed Size (px)

Citation preview

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 1/32

CERTIFICATE

This is to certify that project work report titled “ A Project Report on

Comparative Study of Accounting Standard Issued by ICAI with

Internationa Accounting Standard! submitted by "r# $$$ is a benefited

student of this college .

The work of project is a partial fulfillment of the requirement for the

Master Degree in Commerce affiliated to Uniersity of !une" during the

#cademic $ear %&'&(%&''.

To the best of my knowledge this is original work.

!lace) (

Date) (

Project %uide

Principe

&'ame(&'ame(

Interna E)aminer

*ate+,

'

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 2/32

Ac-nowedgement

Through this acknowledgment" * take the opportunity to

e+press my sincere thanks to arious teachers" friends and

colleagues for their guidance and assistance through which this

project work is completed.

#t first * e+press my gratitude towards ,,, - principle of

,,, and ice(principle - hri. ,,, for their teaching and

guidance of this subject research Methodology and !roject /ork

and inspiring all students in our class for this project work.

* also e+press my sincere thanks to hri. ,,, for proiding

guidance for this particular project work.

* also thanks to my friends for making me aware from time to

time and guiding me for completing this project in time.

* am also thankful to administratie staff members in college

office for their co(operation.

'ame+ , $$$

&"#Com II(

0esearch Candidate

%

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 3/32

TA./E 0F C0'TE'T

A Project Report on Comparative Study of Accounting Standard Issued

by ICAI with Internationa Accounting Standard

0. 1o. T2!*C !#34 12.

1

I'TR0*2CTI0' 0F I'*IA' ACC02'TI'%

STA'*AR*S

• Introduction

• 3hat are Accounting Standards

• 3ho Issues Accounting Standards in

India

• About ICAI

• Process of formuating Accounting

Standards in India

1 to 4

5

I'*IA' ACC02'TI'% STA'*AR*S

• Introduction

• /ist of Indian Accounting Standards

6 to 15

4

I'TER'ATI0'A/ ACC02'TI'%

STA'*AR*S

• Introduction

• About Internationa Accounting

Standard .oard

14 to 16

6

I'TER'ATI0'A/ ACC02'TI'%

STA'*AR*S 17 to 18

7

Comparative Study In Indian Accounting

Standards and Internationa Accounting

Standards 9 Concusion

5: to 56

;.aance Sheet of Infosys Technoogy Systems

and Comments#56 to 5;

<.ibiography

5<

5

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 4/32

A

Project Report on

=A Project Report on Comparative Study of AccountingStandard Issued by ICAI with Internationa Accounting

Standard!

Indian Accounting Standard+ AS,8> 1:> 15> 1?#

Internationa Accounting Standard+ IAS, 1?> 1;> 5:> 56#

Submitted To

2'I@ERSIT 0F P2'E

A Report Submitted in Partia Fufiment of the ReBuirement of

"#Com part II

2'*ER TDE %2I*A'CE 0F

Prof# $$$

S2."ITTE* .

"r# $$$

Ro 'o# $$$ "o 'o# $$$

TDR02%D

$$$ C0//E%E 0F C0""ERCE> P2'E

&5:1:,5:11(

6

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 5/32

Introduction+,

#ccounting tandards establish rules relating to recognition"

measurement and disclosures thereby ensuring that all enterprises that

follow them are comparable and that their financial statements are true" fair and transparent. 7igh(quality accounting standards are a necessary and

important element of a sound capital market system. *n public capital

markets such as those in the United tates. 7igh(quality accounting

standards reduce uncertainty and increase oerall efficiency and inestor8s

confidence by requiring that financial report proide decision useful

information that is releant" reliable" comparable and transparent once

confined by national borders transactions in today8s capital market often are

drien by a demand for and supply of capital that transcends national

boundaries. /ith the increase in cross(border capital rising and inestment

transactions comes an increasing demand for a set of high(qualityinternational accounting standards that could be used as a basis for financial

reporting worldwide.

“#ccounting tandards are written policy documents issues by the

e+pert accounting body or by goernment or other regulatory body coering

the aspects of recognition" measurement" presentation and disclosure of

accounting transactions in financial statement.9

3hat are Accounting Standards+,

#ccounting tandards are the statements of code of practice of the

regulatory accounting bodies that are to be obsered in the preparation of

financial statements. *n layman terms accounting standards are the written

documents issued by the e+pert8s institutes or other regulatory bodies

coering arious aspects of measurement treatment" presentation and

disclosure of accounting transactions.

3ho issues Accounting Standards in India+,

The institute of chartered #ccountants of *ndia :*C#*; reorgani<ing

the need to harmonies the dierse accounting policies and practices at

present in use in *ndia constituted accounting standard board :#=; on #pril

>

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 6/32

%'" '?@@. The main role of #= is to formulate accounting standards from

time to time.

About ICAI+,

The *nstitute of Chartered #ccountants of *ndia :*C#*; is a statutory

body established under the Chartered #ccountants act '?6?.:#ct

1o.,,,,A*** of '?6?; for the regulation of the profession of Chartered

#ccountants in *ndia. During its B' years of e+istence" *C#* has achieed

recognition as a premier accounting body not only in the country but also

globally" for its contribution in the fields of education" professional

deelopment maintenance of high accounting" auditing and ethical

standards. *C#* now is the second largest accounting body in the whole

world.

Procedure of formuating Accounting Standards in India+,

The institute of Chartered #ccountant of *ndia :*C#*; recogni<ing the

need to harmoni<e the dierse accounting policies and practices" constituted

an accounting standards boards :#=; on #pril %'" '?@@. The main faction

of #= so that such standards may be mandated by the council of *C#*.

/hile formulating the standards in *ndia" #= will take into consideration

the applicable laws custom usages and business enironment. *C#* is one of

the members of *nternational #ccounting tandards Committee :*#C; andhas agreed to support the objecties of *#C. #= will gie due

consideration to *# and try to integrate them to the e+tent possible in light

of the considerations and practices pre(ailing in *ndia.

The accounting standards issued will apply to 3eneral !urpose

inancial tatement8 this would include balance(sheet" !rofit E Foss #Gc and

other statement and e+planatory notes which form part thereof issued for the

use of shareholders or members" Creditors" 4mployees and public at large.

The #ccounting tandards are intended to apply only to items which are

material. The standards are generally e+pected to apply prospectiely unless

otherwise stated.

B

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 7/32

.roady the foowing procedure wi be adopted for

formuating Accounting Standards+,

• #= shall determine the board areas in which accounting standards

need to be formulated and the priority in regards to the selection

thereof.

• *n the preparation of the accounting standards #= will be assisted by

study groups constituted to consider specific subjects. *n the formation

of the study groups proision will be made for wide participation by

the members of *C#* and others.

• #= will also hold a dialogue with the representatie of the

3oernment" !ublic sector" *ndustry and other organi<ations for

ascertaining their iews.

• =ased on the aboe an e+posure draft of the proposed standard will be

prepared and issued for comments by members of *C#* and the public

at large.

• #fter taking into consideration the comments receied the e+posure

draft will be finali<ed by the #= and submitted to the council of

*C#*.

• The council of *C#* will consider the final draft and if found

necessary modify the same in consultation with #=. The accounting

standard on the releant subject will then be issued under the authority

of the council.

@

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 8/32

Indian Accounting Standards+,

Introduction+,

The council of the institute of chartered accountant of *ndia as so far

issue 5% :thirty two; accounting standard. /hoeer accounting standards

Hth on “#ccounting for research and deelopment9 has been withdraw on

consequent to the issuance of accounting standard %Bth “*ntangible

#ssets9 thus effectiely there are 5'st accounting standard at present the

accounting standard issued by the #=C establish which hae to be

complied so that the financial statement are prepared in accordance with

generally accepted accounting principles.

/ist of Indian Accounting Standards+,

AS 1Disclosure of Accounting Principles

AS 2Valuation of Inventories

AS 3Cash Flow Statements

AS 4Contingencies and Events Occurring After the Balance

Sheet Date

AS 5et Profit or !oss for the Period" Prior Period Items

and Changes in Accounting Policies

AS 6Depreciation Accounting

AS 7

(Revised)

Construction Contracts

AS 8Accounting for #esearch and Development

AS 9#evenue #ecognition

AS 10Accounting for Fi$ed Assets

H

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 9/32

AS 11

(Revised

2003)

%he Effects Of Changes In Foreign E$change #ates

AS 12

Accounting for &overnment &rants

AS 13Accounting for Investments

AS 14Accounting for Amalgamations

AS 15

(Revised

2005)

Emplo'ee Benefits (clic) here for related

announcement*

AS 16Borrowing Costs

AS 17

Segment #eporting

AS 18#elated Part' Disclosures

AS 19!eases

AS 20Earnings Per Share

AS 21Consolidated Financial Statements

AS 22

Accounting for ta$es on income

AS 23Accounting for Investments in Associates in

Consolidated Financial Statements

AS 24 Discontinuing Operations

AS 25 Interim Financial #eporting

AS 26 Intangi+le Assets

AS 27 Financial #eporting of Interests in ,oint Ventures

AS 28 Impairment of Assets

AS 29 Provisions" Contingent !ia+ilities and Contingent

AssetsAS 30 Financial Instruments- #ecognition and .easurement

AS 31 Financial Instruments- Presentation

AS 32 Financial Instruments- Disclosures

?

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 10/32

Indian Accounting Standards+,

AS 8+ Revenue Recognition+,

Introduction

This statement was issued by *C#* in the year '?H> E the *nitial years

it was recommendatory for only leel * enterprises E but was mademandatory for enterprise in *ndia from april &'" '??5.

0eenue

0eenue is the gross inflow of cash" receiables or other consideration

arising in the course of the ordinary actiities of an enterprise from the sale

of the goods" from the rendering of the serices" E from the use by others of

enterprises resources yielding interest" royalties E diidend. 0eenue is

measured by the charges made to customers or clients for goods supplied E

serices rendered to them E by the charges E rewards arising from the use

of resources by them. *n an agency relationship" the reenue is the amount of

commission E not the gross inflow of cash" receiable or other

consideration.

'&

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 11/32

This statement dose not deals with the following aspects of reenue

recognition to which special consideration apply)

*. 0eenue arising from construction contractsI

**. 0eenue arising from hire(purchase" lease agreementsI

***. 0eenue arising from goernment grants E other similar subsidiesI

*A. 0eenue of insurance companies arising from insurance contracts.

4+amples of items not included within definition of “reenue9 for the

purpose of this statement are)

*. 0eali<ed gains resulting from the disposal of" E unreali<ed gains

resulting from the holding of" non(current assets. 4.g. appreciation in

the alue of fi+ed assets.

**. Unreali<ed holding gain resulting from the change in alue of current

assets" E the natural increases in herds E agricultural E forest

productsI

***. 0eali<ed or unreali<ed gains resulting from changes in foreign

e+change rates E adjustments arising on the translation of foreign

currency financial statementsI

*A. 0eali<ed gain resulting from the discharged of an obligation at less

than its carrying amountI

A. Unreali<ed gains resulting from the restatement of the carrying

amount of an obligationI

''

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 12/32

AS 1:+ Accounting for Fi)ed Assets+,

Introduction

The standard deals with the disclosure of the status of the fi+ed assets in

terms of alue. The standard dose not takes consideration the speciali<ed

aspects of accounting for fi+ed assets reflected with the effects of priceescalations but applies to financial statements on historical cost basis. *t is

important to note that after introduction of # 'BI '? E %B" proision

relating to respectie # are held withdrawn E the rest in mandatory from

the accounting year &'G&6G%&&&. an entity should disclose :i; the gross E net

book alues of fi+ed assets at beginning and end of an accounting period

showing additions" disposals" acquisitions E other moement" :ii;

e+penditure incurred on account of fi+ed assets in the course of construction

or acquisition" :iii; realued amounts substituted for historical cost of fi+ed

assets with the method applied in computing realued amount.

This statement dose not deal with the accounting for the following item to

which special considerations apply)

*. orests" plantations E similar regeneratie natural resources.

'%

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 13/32

**. /asting assets including mineral rights" e+penditure of the e+ploration

for an e+traction of minerals" oil" natural gas E similar non(

regeneratie resources.

***. 4+penditure on real estate deelopment and

*A. Fie stock.

*dentification of fi+ed assets)

i+ed assets are assets held with the intention of being used for the purpose

for the producing or proiding goods or serices E is not held for sale in the

normal course of business. tand(by equipment E sericing equipment are

normally capitali<ed. Machinery spares are change to the profit E loss

statement as and when consumed. 7oweer" if such spare can be used only

in connection with an item of fi+ed assets" it may be appropriate to allocate

the total cost on a systematic basic oer a period not e+ceeding the usefullife of principal item.

AS 15+ Accounting For %overnment %rants

Introduction

The standard comes in to effect in respect of accounting periodscommencing on or after &'G&6G'??% E will be recommendatory in nature for

an initial period of % years. #ccounting standard '% deals with accounting

for goernment8s grants for specifies that the goernment grants should not

be recogni<ed until there reasonable assurance that the enterprise will

company comply with the conditions attached to them" and the grant will be

receied. The standard also describes the treatment of non(monetary

goernment grantsI presentation of grants related to specific fi+ed assets"

related to reenue" related to promoters" contributionsI treatment for refund

of goernments grants etc. the enterprises are required to disclose :i; the

accounting policy adopted for goernment grants including the methods of presentation in the financial statementsI :ii; the nature E e+tent of

goernment grants recogni<ed in the financial statement including non(

monetary grants of assets gien either at a concessional rate or free of cost.

This statement does not deal with)

'5

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 14/32

*. The special problem arising in accounting for goernment grants in

financial statements reflection the effects of changing prices or in

supplementary information of a similar nature.

**. 3oernment assistance other than in the form of goernment grants

***. 3oernment participation in the ownership of the enterprises.

The receipt of the goernment grant by an enterprise is significant for

preparation of the financial statement for % reasons. irstly" if a

goernment grant has been receied an appropriate method of

accounting therefore is necessary. econdly" it is desirable to gie an

indication of the e+tent to which the enterprises has benefited from such

grants during the reporting period. This facilitates comparison on an

enterprises financial statement with those prior periods E with those of

other enterprise.

#ccounting treatment of goernment grants

To broad approaches may be followed for the accounting treatment

2f goernment grants) the capital approach under which grand is

treated as part of share holder funds" and income approach under which

a grand is taken to incomes oer one or more period.

Those in support of capital approach argue as follows)

*. Many goernments8 grants are in the nature of promoter8s

contribution that is they are gien by way of contribution towards

its total capital outlay ordinarily e+pected in the case of such a

grants.

**. They are not earned but represent an incentie proided by

goernment without related costs.

#rguments in support of the income approaches are as follows)

*. #s a income ta+ E other ta+es are charges against income" it is logical

to deal also with goernment grants" which are an e+tension of fiscal

polices" in the profit E loss statement.

'6

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 15/32

**. *n case grants are credited to share holder8s fund" no correlation is

done between the accounting treatment of the grants E the accounting

treatment of the e+penditure to which grant relates.

AS 1?+ Reated Party *iscosures

Introduction

This standard comes into effect in respect of accounting period commencingon a after &'G&6G%&&' E is mandatory in nature. The standard prescribes the

requirement for disclosure of related party relationship E transaction

between the reporting enterprise E its related party. The requirements of the

standard apply to the statement of each reporting enterprises as also to

consolidate financial statement presented by a holding company. ince the

standers is more subjectie" particularly with respect to identification of

related parties Jthrough proision related to related party concept are gien

under section %?@G%??G5&' of the companies act '?>B and section 6&# :%;:b;

of the income ta+ act '?B'K" obtaining corroboratie eidence becomes ery

difficult for the auditors. Thus successful implementation of # 'H is dependupon how transparent the management is an how igilant the auditors are.

2bjectie

The objectie of this statement is to established requirement for disclosure

of)

*. 0elated party relationship E

'>

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 16/32

**. Transaction between reporting enterprise E it related parties.

cope

This statement should be applied in reporting related party relationship E

transaction between reporting enterprises E its related parties. The

requirement of this statement applied to the financial statement of each

reporting enterprises as also to consolidate financial statement presented by

a holding company.

This statement deals only with related party relationship describe :a;

to :e; below)

a. 4nterprises that directly" or indirectly through one or more

intermediaries" control" or are controlled by" or are under common control with the reporting enterprise :this include

holding company" subsidiaries E fellow subsidiaries;.

b. #ssociated E joint enture reporting enterprise E the inesting

party or enture in respect of which the reporting enterprise is

an associate or a joint enture.

c. *ndiidual owning" directly or indirectly" an interest in the

oting power of the reporting enterprises that gie them control

or significant influence oer the enterprises" and relaties of

any such indiidual.

d. Ley management personnel E relatie of such personnel E

e. 4nterprise oer which any person describes in c or d is able to

e+ercise significant influence. This includes enterprises owned

by director or major shareholders of the reporting shareholder

of the reporting enterprises E enterprises that hae a member of

key management" with reporting enterprise.

'B

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 17/32

Internationa Accounting Standards+,

Introduction+,

#ccounting is a language of business communicates the financial

result of an enterprise to the arious interested parties by means of financialstatements e+hibiting true and fair iew of its state of affairs as also of

working result. Fike any of other language" accounting has its own set of

rules" which hae been deeloped by accounting bodies. These rules cannot

be absolutely rigid. These rules" accordingly" do proide a reasonable

fle+ibility in line with the economic enironment" social needs" legal

requirements and technological deelopment. These how eer" do not emply

that accounting principles and parties can be applied arbitrarily.

#ccounting principles hae to operate with in the bonds of rationality. This

could" perhaps" be considered as a genesis for setting the accounting

standards.

#ccounting tandards are written policy document issued e+pert

accounting body or by goernment or other regulatory body coering the

aspects recognition" measurement" presentation and disclosure of accounting

transaction in financial statement. The ostensible purpose of the standard

setting bodies is to promote the dissemination of timely and useful financial

'@

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 18/32

information to inestors and certain other parties haing an interest in the

company8s economic performance. The accounting standard reduces the

accounting alternatie in the preparation of financial statement within the

bond of rationality" thereby ensuring comparability of financial statement of

different enterprises.

The accounting standards deals with the issue of

i. 0ecognition of eents and transactions in the financial statements"

ii. Measurement these transaction and eents"

iii. !resentation of these transactions and eents in the financial

statement in a manner that is meaningful and understandable to the

reader" and

i. The disclosure requirements which should be there enable the public

at large and the potentational inestors in particular" to get an insight

in to what these financial statement are trying to reflect and there bythe facilitating them to take prudent and informed business decisions.

Internationa Accounting Standard .oard+,

/ith a iew of achieing this objectie" the Fondon based group

mainly the international committee :*#C;" responsible for deeloping

international accounting standard was established in une '?@5. it is presently known as international accounting standard board" the *#C

comprises the professional accounting bodies of oer @> countries:including

the *C#*;. !rimarily" the *#C was established" in the public interest to

formulate and publish" international standard to be followed in the

presentation of audited financial statement. The member of *#C hae

undertaken responsibility to support the standards promulgated by *#C and

to promulgate those standard in there respectie countries.

=etween '?@5 E %&&'" the *#C released international accounting

standard. =etween '??@ E '???" the *#C restructured there organi<ation"

which resulted in formation of *#=. These changes came in to effect on ' st

#pril %&&' subsequently" *#= issued statement about current and future

standards) *#= publishes standards in a series of pronouncements" called

international financial" reporting standards :*0;. 7oweer" *#= has not

rejected the standards issued by the *#C those pronouncements continue to

be designated as an “international #ccounting standard9 :*#;. The *#=

'H

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 19/32

approed *#= resolution on *#C standards and there in #pril %&&'" in

which it8s conform the status of all *#C standards and *C interpretations

in effect as on 'st #pril %&&'.

IAS,1?+ Revenue

*# 'H on 0eenue is applicable for periods beginning on or after ' st

an '??>

*# 'H prescribes accounting treatment for reenue arising from)

•

The sale of goods)• The rendering of sericesI E

• The use by others of entity assets yielding interest royalties E

diidend

*t e+cludes the treatment of reenue arising from transaction coered by

other standards or amount collected on behalf of third parties :e.g. Aat;.

ummary

0eenue is measured at the fare alue of the consideration receied or

receiable. The consideration usually in cash. *f the inflow of cash is

significant deferred" E there is below(market rate of interest or no interest"

the fare alue of consideration is determined by discounting e+pected future

receipts. *f dissimilar goods or serices are e+changed :as in barter

'?

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 20/32

transaction; reenue is fare alue of the goods or serices or receied or" if

this is not reliably measurable" the fare alue of goods or serices gien up.

0eenue should measure at the fair alue of the consideration receied)

•

Trade discount E alue rebates are deducted to determine fair alue.7ow eer" payment discounts non(deductible.

• The amount of reenue can be measured reliablyI

• The costs of transaction can be measured reliablyI

• ignificant risks E rewards of ownership are transferred to the buyerI

• The seller has no continuing managerial inolement or control oer

the goodsI

• *t is probable that economic benefits will flow to the sellerI and

*nterest reenue should be recogni<ed on time proportion basis using theeffectie interest. 0oyalties should be recogni<ed on an accruals basis in

accordance with the substance of the releant agreement. Diidend reenue

should be recogni<ed when the share holder right to receied the diidend is

established.

IAS,1;+ Property> Pant and EBuipment+,

*# 'B on property" plant E equipment was issued in December %&&5 E is

applicable to annual accounting period beginning on or after 'st an %&&>.

*# 'B prescribed the accounting treatment for property" plant E equipment

unless another standard requires or permit a different account treatment. or

e.g. *0" > on non current assets held for sale E discontinued operations

applies to property" plant E equipment classified as held for sale.

ummary

!roperty plant E equipment is initially recogni<ed at historical cost.

ubsequent to initial recognition" property" plant E equipment are carried

either at)

• Cost less accumulated deprecation E any accumulated impairment

loss" or

• 0ealued amount less subsequent accumulated deprecation and any

accumulated impairment loss. The realued amount is the fare alue is

at the date of realuation.

%&

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 21/32

The choice of measurement is applied consistently to an entire class of

property" plant E equipment. #ny realuation increase in such assets

credited directly to the realuation surplus in equity" unless it reerses a

realuation decrease preiously recogni<ed in profit in loss. #ny realuation

decrease is recogni<ed in profit or loss. 7oweer the subsequent realuation

decrease is debited directly to the realuation surplus in equity to the e+tent

of the credit balance in realuation surplus is respect of that asset.

The gain or loss on derecogni<ing of an item of property" plant E equipment

is the difference between the net disposal proceeds" if any" and the carrying

amount of the item. *t is included in profit or loss.

IAS+ 5:, Accounting for government grants and discosure of

government assistance+,

*# %& on “accounting for goernment grants E disclosure of goernment

assistance9 was issued in #pril '?H5 E was reformatted in the year '??6. it

came in to effect for annual periods beginning or after ' anuary '?H6.The objectie of *# %& is to be prescribing the accounting for" and

disclosure of" grants E other form of goernment assistance. 7ow eer" *#

%& dose not coered goernment assistance that is proided in the form of

benefit helpful in determine ta+able income.

ummary)

# goernment grant is recogni<ed only when enterprise will comply

with any condition attached to the grants receied. The grant is recogni<ed

as a income" oer the period" to match them with the related cost for" which

they are intended compensate" on a systematic basis" E should not be

credited directly to equity.

1on monitory grants are usually accounted for at fair alue. #lthough

recording both the assets E grants at a nominal amount is also permitted.

%'

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 22/32

# grant receiable as a compensation for cost already incurred or for

immediate financial support" with no future related cost" should be

recogni<ed as a income in the period in which it is receiable.

# grant relating to assets may be presented as deferred income or by

deducting the grant from the assets carrying amount. # grant relating to

income may be reported separately as other income or deducted from the

related e+penses.

*f a grant become repayable it should be deferred income or by

deducting the grant from assets carrying amount. /here the original grants

related to income" the repayment should be applied dealt with as an e+penses

where the original grants related to an assets" the repayment should be

treated as increasing the carrying amount of the assets or reducing the

deferred income balance. The cumulatie deprecation which would hae been charged had the grant not been receied should be charged as an

e+pense. The goernment grants do not include goernment assistance

whose alue can not be reasonably measured" such as technical or marketing

adice.

IAS 56 Reated Party *iscosure+

*# %6 on “0elated !arty Disclosure9 was issued in dec %&&5 E is

applicable for annual periods beginning on or after 'st

jan %&&>.

*# %6 specifies the disclosure necessary to draw attention to the

possibilities that the financial position E financial performance of an entity

may hae been affected by the e+istence of the related party and by

transaction and outstanding balance with such related parties.

Summery+

# party is related to an entity if it)

• 7as joint control oer the entity)

• 7as significant influence oer the entityI

• Directly or indirectly" controls" is control by or is under common

control with" the entityI

%%

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 23/32

• *s a close member of the family of any indiidual who controls" has

significant influence or joint control oer" the entityI

• *s a member of key management personnel of the entity of its parentI

• *s a joint enture in which the entity is entureI

• *s an associates of entityI• *s an entity that is controlled" jointly controlled or significantly

influenced by" or for which significant oting power in such entity

resides with" any of the key management personnelI

• *s a post(employment benefits plan for the benefit of employees of the

entity" or of any of its related parties.

4+amples of the kinds of transactions that are disclosed if they are with a

related party)

• !urchase or sale of goods.

• 0endering or receiing of serices.

• !urchase or sale of properties or other assets.

• Fease.

• Transfer under license agreements.

• Transfer of research and deelopment.

• Transfer under finance agreements:including loans E equity

contribution in cash or in kind;

• ettlement of liabilities on behalf of the entity or by the entity on

behalf of another party.

• !roision of guarantee of collateral.

# related party transaction is a transfer of resources" serices or obligations

between related parties" regardless whether price is charged.

%5

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 24/32

Comparative Study+,

Indian Accounting

Standards

Internationa Accounting

Standards

Presentation

And

*iscosures

There is no separate standard

for disclosure. or

companies" format and

disclosure requirements are

set out under schedule A* of

the companies act.

1o such requirement under

*ndian 3##!.

# > specifically requires

*#(' prescribes minimum

structure of financial

statements and contains

guidance on disclosures.

*#(' requires disclosure

of critical judgments made

by management in applying

accounting policies.

*#(' prohibits any items

%6

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 25/32

disclosure of certain items as

e+tra(ordinary items.

Under *ndian 3#!!" this is

typically spread oer seeralcaptions such as share

capital" resere E surplus" !

E F debit balance" etc.

to be disclosed as e+tra(

ordinary items.

*#(' requires a “statement

of changes in equity9which comprises all

transactions with equity

holders.

Revenue

Recognition

#(? allows completed

serice contract method or

proportionate completion

method.

#(? requires interest

income to be recogni<ed on a

time proportion basis.

1o guidance on barter

transactions.

#(? permits recognition

when the goods are

manufactured" identified and

ready for deliery in such

cases.

1o specific guidance in the

standards.

*n case of reenue from

rendering of serices" *#(

'H allows only percentage

of completion method.

*#('H requires effectie

interest method to be

followed for interest

income recognition.

Deals with accounting of

barter transactions.

Under *#('H" payments

receied in adance for

goods yet to be

manufactured or third party

sales cannot be recogni<ed

as reenue until such goods

are deliered to the buyer.

or multiple element

contracts" the standard

broadly requires that each

element is fair alued and

recogni<ed when the

underlying serice is

%>

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 26/32

performed.

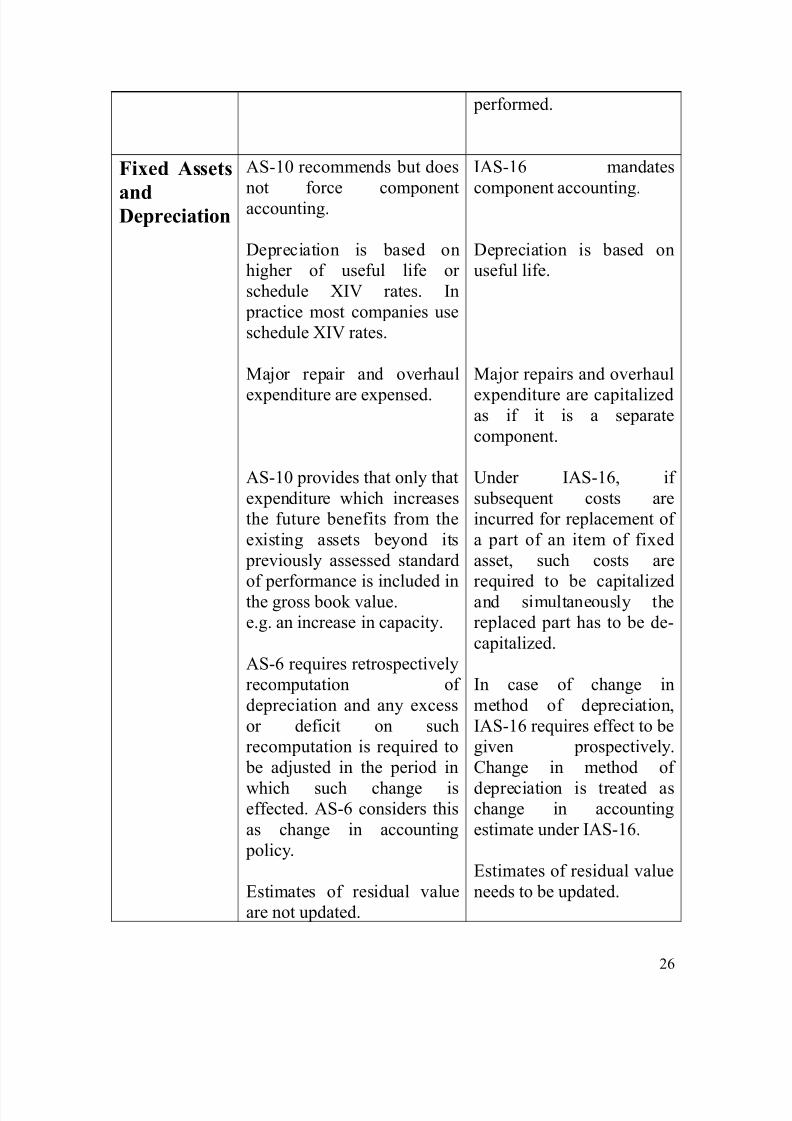

Fi)ed Assets

and*epreciation

#('& recommends but does

not force componentaccounting.

Depreciation is based on

higher of useful life or

schedule ,*A rates. *n

practice most companies use

schedule ,*A rates.

Major repair and oerhaul

e+penditure are e+pensed.

#('& proides that only that

e+penditure which increases

the future benefits from the

e+isting assets beyond its

preiously assessed standard

of performance is included inthe gross book alue.

e.g. an increase in capacity.

#(B requires retrospectiely

recomputation of

depreciation and any e+cess

or deficit on such

recomputation is required to

be adjusted in the period in

which such change iseffected. #(B considers this

as change in accounting

policy.

4stimates of residual alue

are not updated.

*#('B mandates

component accounting.

Depreciation is based on

useful life.

Major repairs and oerhaul

e+penditure are capitali<edas if it is a separate

component.

Under *#('B" if

subsequent costs are

incurred for replacement of

a part of an item of fi+ed

asset" such costs are

required to be capitali<edand simultaneously the

replaced part has to be de(

capitali<ed.

*n case of change in

method of depreciation"

*#('B requires effect to be

gien prospectiely.

Change in method of

depreciation is treated aschange in accounting

estimate under *#('B.

4stimates of residual alue

needs to be updated.

%B

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 27/32

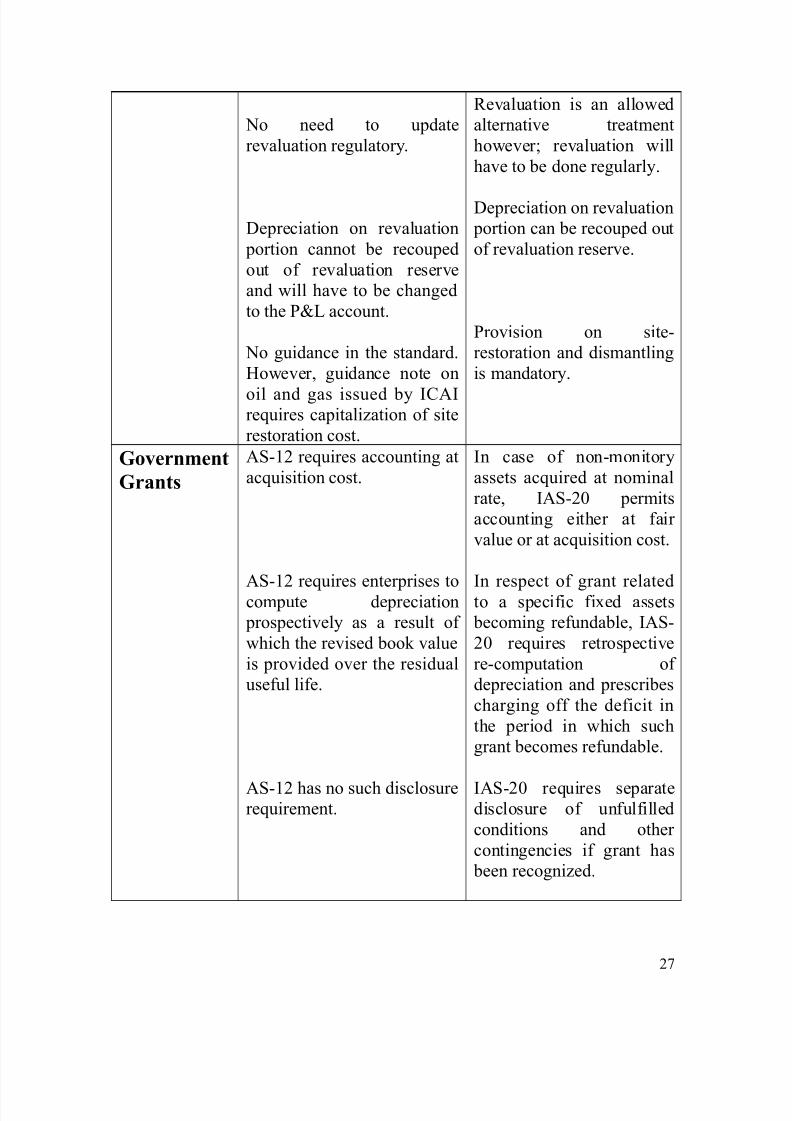

1o need to update

realuation regulatory.

Depreciation on realuation

portion cannot be recouped

out of realuation resere

and will hae to be changed

to the !EF account.

1o guidance in the standard.

7oweer" guidance note on

oil and gas issued by *C#*requires capitali<ation of site

restoration cost.

0ealuation is an allowed

alternatie treatment

howeerI realuation will

hae to be done regularly.

Depreciation on realuation

portion can be recouped out

of realuation resere.

!roision on site(

restoration and dismantling

is mandatory.

%overnment

%rants

#('% requires accounting at

acquisition cost.

#('% requires enterprises tocompute depreciation

prospectiely as a result of

which the reised book alue

is proided oer the residual

useful life.

#('% has no such disclosurerequirement.

*n case of non(monitory

assets acquired at nominal

rate" *#(%& permits

accounting either at fair

alue or at acquisition cost.

*n respect of grant relatedto a specific fi+ed assets

becoming refundable" *#(

%& requires retrospectie

re(computation of

depreciation and prescribes

charging off the deficit in

the period in which such

grant becomes refundable.

*#(%& requires separatedisclosure of unfulfilled

conditions and other

contingencies if grant has

been recogni<ed.

%@

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 28/32

Reated

Party

*iscosures

#('H does not include this

relationship.

#('H read with #*(%5

requires disclosure of

remuneration paid to key

management persons but

does not mandate category(

wise disclosures.

#('H proides e+emption

from disclosure in such

cases.

#('H includes control oer

composition of board of

directors in the definition of

“control9.

1o such disclosure

requirement is contained in

#('H.

#('H prescribes a rebuttable

presumption of significant

influence if %&N or more of

the oting power held by any

The definition of related

party under *#(%6

includes post employment

benefit plans of the

enterprise or of any other entity" which is related

party of the enterprises.

*#(%6 requires

compensation to LM!s to

be disclosed category(wise

including share(based

payments.

1o concession is proided

under *#(%6 where

disclosure of information

would conflict with the

duties of confidentiality in

terms of statute or

regulating authority.

The definition of “control9under *#(%6 is restrictie

on the count that it does not

include control oer

composition of board of

directors.

*#(%6 requires disclosure

of terms and conditions of

outstanding items

pertaining to related parties.

*#(%6 does not prescribe a

rebuttable presumption of

significant influence.

%H

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 29/32

party.

Transactions between state

controlled enterprises are not

required to be disclosedunder #('H.

1o e+emption.

Concusion+

There are significant difference between *ndian #ccounting tandard

and *nternational #ccounting tandard. 7oweer" both the countries are

planning to implement *0 to cope up with these differences.

Comments on .aance Sheet of Infosys Technoogy Systems+

1( I'C0"E STATE"E'T

4ach framework requires prominent presentation of an income statement as

a primary statement.

Format

IFRS+ There is no prescribed format for the income statement. The entity

should select a method of presenting its e+penses by either function or

natureI this can either be" as is encouraged" on the face of the income

statement" or in the notes. #dditional disclosure of e+penses by nature is

%?

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 30/32

required if functional presentation is used. *0 requires" as a minimum"

presentation of the following items on the face of the income statement)

'. reenueI

%. finance costsI

5. share of post(ta+ results of associates and joint entures accounted for

using the equity

6. methodI

>. ta+ e+penseI

B. post(ta+ gain or loss attributable to the results and to remeasurement

of discontinued operationsI

@. !rofit or loss for the period#

The portion of profit or loss attributable to the minority interest and to the

parent entity is separately disclosed on the face of the income statement asallocations of profit or loss for the period. #n entity that discloses an

operating result should include all items of an operating nature" including

those that occur irregularly or infrequently or are unusual in amount.

Indian %AAP+ Presentation in one of two formats# Either+

'. a single(step format where all e+penses are classified by function and

are deducted from total income to gie income before ta+I

%. a multiple(step format where cost of sales is deducted from sales to

show gross profit" and other income and e+pense are then presented togie income before ta+. 4C regulations require registrants to

categorise e+penses by their function. #mounts attributable to the

minority interest are presented as a component of net income or loss.

IFRS+ The total of income and e+pense recognised in the period comprises

net income. The following income and e+pense items are recognised directly

in equity)

'. fair alue gainsG:losses; on land and buildings" intangible assets"

aailable(for(sale inestments and certain financial instrumentsI

%. foreign e+change translation differencesI

5. the cumulatie effect of changes in accounting policyI

6. changes in fair alues of certain financial instruments if designated as

cash flow hedges" net of ta+" and cash flow hedges reclassified to

income andGor the releant hedged assetGliabilityI and

5&

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 31/32

>. actuarial gains and losses on defined benefit plans recognised directly

in equity :if the entity elects the option aailable under *# '?"

4mployee =enefits" relating to actuarial gains and losses;.

Indian %AAP+ imilar to *0" e+cept that realuations of land and

buildings and intangible assets are prohibited under U 3##!. #ctuarial

gains and losses :when amortised out of accumulated other comprehensie

income; are recognised through the income statement#

5( Statement of changes in share &stoc-( hoders eBuity

IFRS+ !resented as a primary statement unless a o0*4 is presented as a

primary statement. upplemental equity information is presented in the noteswhen a o0*4 is presented :see discussion under !resentation8 aboe;. *n

addition to the items required to be in a o0*4" it should show capital

transactions with owners" the moement in accumulated profit and a

reconciliation of all other components of equity. Certain items are permitted

to be disclosed in the notes rather than in the primary statement.

Indian %AAP+ imilar to *0" e+cept that U 3##! does not hae a

o0*4" and 4C rules permit the statement to be presented either as a

primary statement or in the notes.

.ibiography

•

Indian Accounting Standards and %AAP ,*ophy *Soua#

• Financia Reporting @oume 1#

,The institute of Chartered Accountants

of India#

5'

8/20/2019 akram doc

http://slidepdf.com/reader/full/akram-doc 32/32

• 333#ICAI#0rg