Embed Size (px)

Citation preview

Rating Report │ 5 February 2020 fitchratings.com 1

Supranationals

Africa

African Export-Import Bank (Afreximbank)

Key Rating Drivers Rating Affirmed: The ‘BBB-’ rating of African Export-Import Bank (Afreximbank) is driven by the bank’s intrinsic features, including its strong level of solvency and liquidity, both of which assessed at ‘a-’ by Fitch Ratings. The solvency assessment reflects ‘Strong’ capitalisation and a ‘Moderate’ risk profile. The ‘High Risk’ business environment in which the bank operates translates into a three-notch negative adjustment to our assessment of its solvency and liquidity, resulting in an overall intrinsic rating of ‘bbb-’.

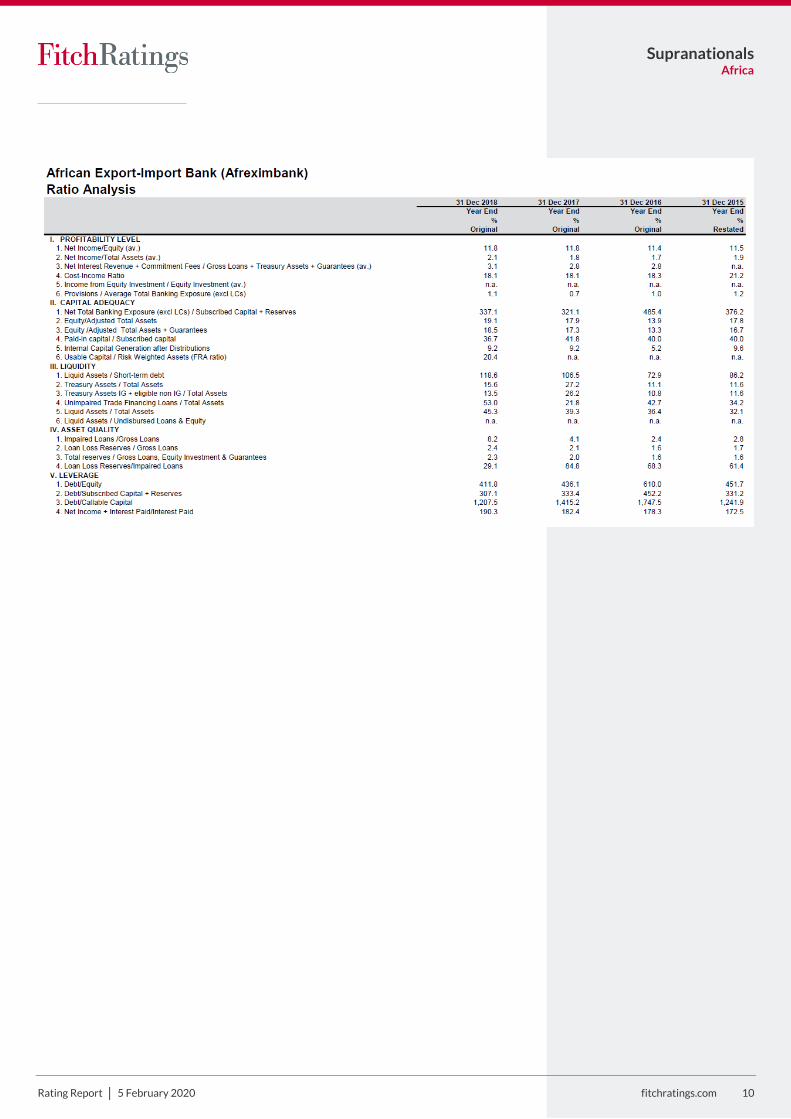

Strong Capitalisation: Afreximbank’s strong capitalisation is underpinned by an equity-to-adjusted assets and guarantees ratio of 18.5% as of end-2018, a strong and improving ratio since 2016 (13.2%). Fitch’s usable capital-to-risk-weighted assets (FRA) ratio was 20.4% at end-2018, a ‘Moderate’ level. Fitch expects both ratios to remain at similar levels over the medium term, as higher lending growth is broadly matched by increase in equity.

Moderate Credit Risk: Non-performing loans (NPLs), as reported by the bank, moderated to 3.0% in 2018 from 4.1% in 2017. However, loans accounted in Stage 3 under IFRS, were significantly higher, at 8.2% as of end-2018, highlighting delays on loan repayments. The credit quality of the bank’s portfolio is very weak with a weighted average credit rating of borrowers of ‘B-’. This is partly offset by credit risk mitigants (including credit insurance and cash collaterals) which provide an uplift of three notches above the average rating of loans to ‘BB-’.

PCS Revised Down: The agency has revised its assessment of Afreximbank’s preferred creditor status (PCS) to ‘Low’ from ‘Moderate’. In line with Fitch’s own approach to assess PCS, this reflects the significant increase in the share of non-sovereign loans in total loan portfolio (81% as of end-2018 from 45% in 2016) and repayment delays, of over 90 days, on a loan to an African central bank in 2018 and the subsequent restructuring of this loan in 1H19.

High Risk Business Environment: The ‘High Risk’ assessment of the business environment chiefly reflects Afreximbank’s strategy, characterised by a rapid growth in its banking portfolio in high-risk countries. The importance of the bank’s public mandate is assessed as ‘moderate’ balancing its strong relationship with African sovereigns’ authorities and focus on supporting trade in Africa against its limited size, especially compared with regional peer African Development Bank (AfDB, AAA/Stable).

Moderate Shareholder Support: Fitch also revised up the support assessment of Afreximbank, to ‘bb’, on the back of an improvement in the credit rating of two key shareholders, Egypt (B+/Stable) and Russia (BBB/Stable). The use of credit risk mitigants on callable capital provides a one-notch uplift, resulting in a support capacity assessment of ‘bb+’. Support propensity is assessed as ‘Moderate’ resulting in an overall support assessment of ‘bb’.

Rating Sensitivities Solvency Metrics: Improvement in solvency stemming from stronger capitalisation could be rating positive. Weaker-than-expected capital payments, higher-than-anticipated loan growth or failure to reduce Stage 3 loans as a share of gross loans would be rating negative.

Liquidity Profile: Improvement in liquidity profile on the back of higher coverage of short-term debt by liquid assets or improvement in the share of ‘AAA’-‘AA’ treasury assets would be rating positive. Weakened coverage of short-term debt by liquid assets, decline in the share of ‘AAA’-‘AA’ treasury assets or deterioration in access to capital markets and other source of liquidity can result in a lower liquidity assessment, and put pressure on overall rating.

Ratings

Long-Term IDR BBB-

Short-Term IDR F3

Outlook Long-Term IDR Stable

Financial Data

African Export-Import Bank (Afreximbank)

Dec 18 Dec 17

Total assets (USDm) 13,419 11,914

Equity to adj. assets and guarantees (%)

18.5 17.3

Fitch’s usable capital/ risk-weighted assets (FRA, %)

20.4 n.a.

Average rating of loans & guarantees

B- B-

Impaired loans (% of total loans)

8.2a 4.1

b

5 largest exposures to total exposure (%)

27.2 28.1

Share of non-sovereign exposure (%)

80.7 70.9

Net income/equity (%) 11.8 11.8

Average rating of key shareholders

BB BB-

a Stage 3 loans as per IFRS 9 accounting standards. Impaired loans reported by the bank were 3% in 2018. b Restated from 2.5% after adoption of IFRS9 Source: Fitch Ratings, Afreximbank

Applicable Criteria

Supranational Rating Criteria (May 2019)

Related Research

Preferred Creditor Status (October 2018)

Fitch Ratings 2020 Outlook: Supranationals (December 2019)

Support for Supranationals: What Is the Cost for Sovereigns? (November 2019)

Analysts Khamro Ruziev, CFA

+44 20 3530 1813

Enrique Bernardez

+44 20 3530 1964

Rating Report │ 5 February 2020 fitchratings.com 2

Supranationals

Africa

Business Environment Afreximbank is a multilateral development bank (MDB) established in 1993 by AfDB to finance and promote intra- and extra-African trade. The bank provides loans, guarantees and advisory services to sovereigns and private-sector entities domiciled within AfDB’s member states in Africa. As part of Afreximbank’s strategy to diversify its shareholder base, it has increased the number of member states to 52 in 2019 (2016: 44) and attracted private shareholders (financial institutions and others). Afreximbank’s head office is in Egypt and it also has offices in Cote d’Ivoire, Nigeria, Uganda and Zimbabwe.

The bank differs from other Fitch-rated MDBs due to its profit-driven business model and mixed shareholder base. Afreximbank focuses on granting trade finance loans, typically self-liquidating, short-term (less than 12 months) facilities, most of which are secured by collaterals. Some of the payment risk is transferred to OECD-based off-takers. These fairly low-risk activities help mitigate the high-risk environment in which the bank operates.

Afreximbank operates in high-risk business environment, which translates into a three-notch downward adjustment over its solvency and liquidity assessment, both of which assessed ‘a-’.

Business Profile

Fitch assesses Afreximbank’s business profile as ‘high risk’, primarily reflecting the bank’s ‘high-risk’ strategy and governance risks.

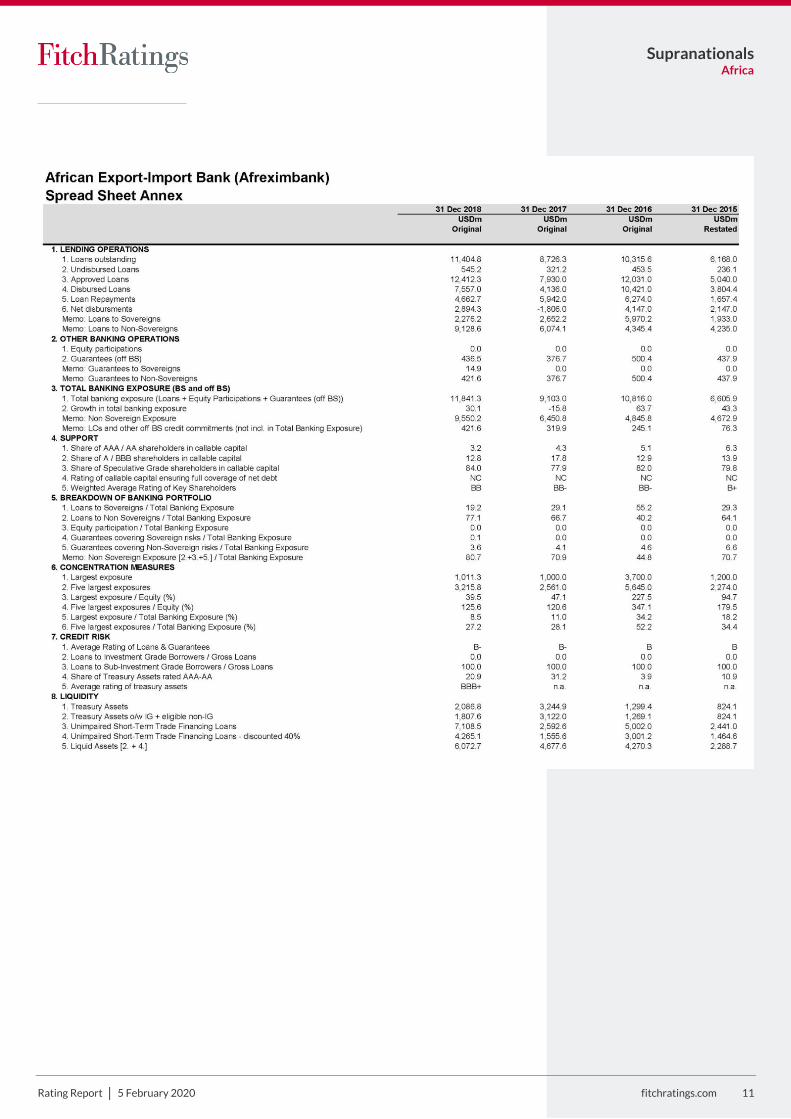

The banking portfolio, which comprises loans and guarantees, was USD11.8 billion at end-2018. Afreximbank’s banking portfolio has grown significantly over the past five years, following the increase in its capitalisation. The bank’s loan facilities are mainly extended under Line of Credit, Syndication and Direct Financing programmes, which together accounted for about 90% of total loan approvals in 2018.

Afreximbank’s strategy is deemed ‘High Risk’, reflecting a rapid growth of its banking portfolio in high-risk countries of operations. This also reflects high exposure to non-sovereign borrowers, whose share increased from 45% in 2016 to 81% of the bank’s portfolio due to increase in loan disbursements to private-sector entities and the repayment of all Countercyclical Trade Liquidity Facility (COTRALF) loans. The agency expects the non-sovereign exposure to account for two-thirds of the banking portfolio over the rating horizon.

Fitch considers Afreximbank’s quality of governance as ‘High Risk’. This assessment reflects the risk of fast and ample disbursements to a limited number of key shareholders, as happened when the COTRALF programme was implemented

1. The bank’s overall governance structure

is similar to most sub-regional peers, consisting of general assembly of shareholders. The board of directors is delegated most of power and selects the president in charge of running the bank’s daily operations. The board also approves all loans made by the bank and its risk management policies.

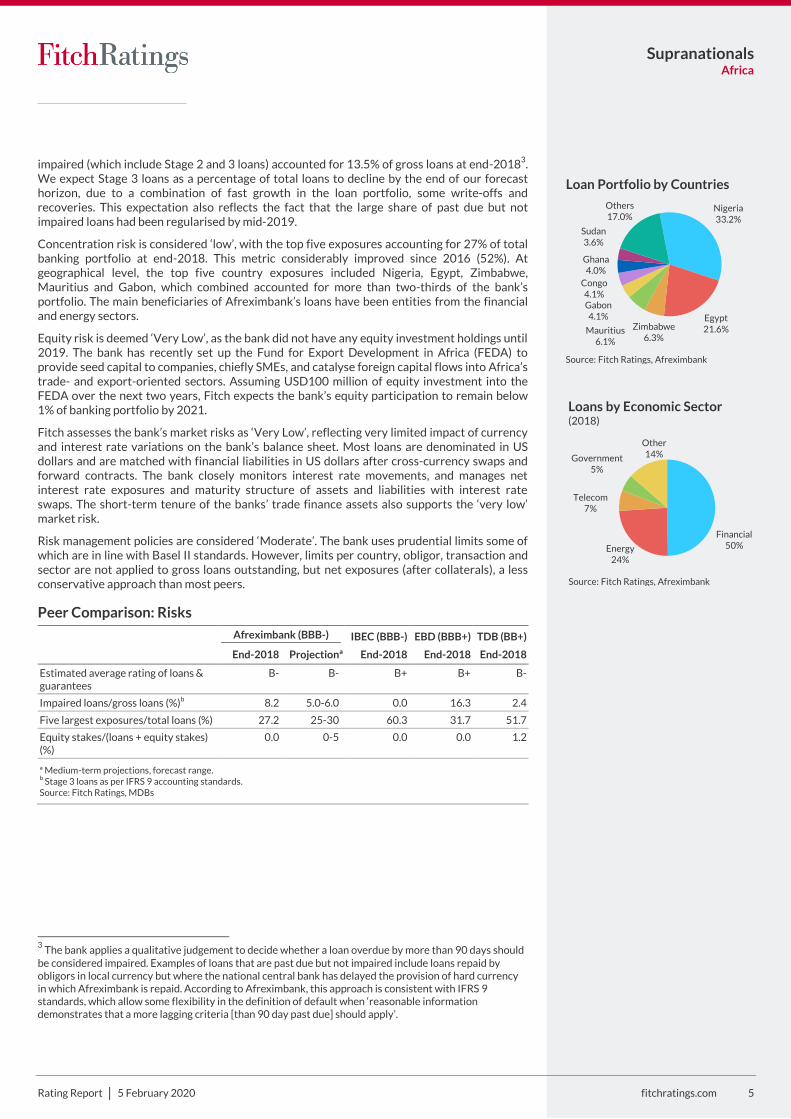

Loans are mostly concentrated in northern and western Africa, primarily Nigeria (33% of total loan portfolio at end-2018), Egypt (21.6%) and Zimbabwe (6.3%). Loan exposures spread across various sectors. However, borrowers from the financial, energy and telecommunication sectors are the main beneficiaries, accounting for 89% of total loan approvals.

The importance of the bank’s public mandate is considered as ‘Medium Risk’. This assessment reflects Afreximbank’s strong relationship with governments of African member states, as evidenced by regular and ongoing capital increases. The assessment also takes into account the bank’s ambitious 2017-2021 development objectives. The assessment is moderated by the limited size of the bank focused on promoting and financing trade in the continent, especially compared with AfDB, which has a broader development mandate.

1 In December 2015, Afreximbank initiated the two-year COTRALF programme under which it provided hard-currency loans to few central banks of member states to ease the implication of adverse conditions in commodity markets and the impact of terrorist acts in many African states. As a result, the total assets doubled to USD14 billion at mid-2017 from USD7.1 billion at end-2015, putting pressure on concentration and capitalisation metrics. By mid-2018, all COTRALF loans were fully repaid.

Intrinsic Rating Assessment

Indicative value Assessment

Solvency a-

Liquidity a-

Business environment -3 notches

Intrinsic rating bbb-

Source: Fitch Ratings

0%

20%

40%

60%

80%

100%

2016 2017 2018

Line of credit Syndications

Direct financing Others

Source: Fitch Ratings, Afreximbank

Loans by Types of Programme

West49%

North25%

South11%

East10%

Source: Fitch Ratings, Afreximbank

Geographical Distribution of Outstanding Loans in Africa(2018)

Central5%

Rating Report │ 5 February 2020 fitchratings.com 3

Supranationals

Africa

Operating Environment

Fitch considers Afreximbank’s operating environment as ‘High Risk’ in line with regional peers. The bank operates in low- and middle-income African countries with low credit quality, weak business environment and high political risk.

We estimate the average rating of Afreximbank’s countries of operation at ‘B’, which is within the ‘High Risk’ threshold as per Fitch’s Supranationals Rating Criteria.

The income per capita of the countries of operation is also considered ‘High Risk’. Half of the 52 African member states are low income, with average GDP per capita at USD2,397, which is lower than that of peers: International Bank for Economic Co-operation (IBEC, USD10,931), Eurasian Development Bank (EDB, USD5,211) and Eastern and Southern African Trade and Development Bank (TDB, USD2,766).

Political risk and business climate in country of operations, including Egypt (B+/Stable), where the bank is headquartered, are considered as ‘High Risk’. Egypt experienced several political and civil unrests over the past decade, resulting in deterioration of its rankings in the World Bank’s governance indicators.

Operational support from countries of operations is deemed ‘Low Risk’. Afreximbank is exempt from direct taxes and benefits from various immunities and privileges common to MDBs. It also benefits from some form of support by African authorities in relation to resolving non-payment of loans by private-sector borrowers. In 2016, the Zimbabwe State Asset Management Company (ZAMCO) acquired non-performing loans of private-sector borrowers in order to repay Afreximbank. At the height of 2017 currency crisis, the central banks of Nigeria and Egypt arranged foreign-exchange (FX) swaps and eased FX translation of local-currency deposits for the repayment of private-sector loans to the bank.

Solvency Afreximbank’s solvency is assessed at ‘a-’, reflecting primarily moderate risk profile of the bank and Fitch’s expectation that the bank will maintain its strong capital base over the rating horizon.

Capitalisation

The strong capitalisation assessment is driven by the ‘Strong’ equity-to-adjusted assets and guarantees ratio and ‘Moderate’ FRA ratio.

Afreximbank’s capital base has more than doubled since 2015, following shareholders’ decision in June 2018 to increase the bank’s paid-in capital by USD1 billion by 2021. By end 2019, the bank secured nearly 90% of its capital increase target, which resulted in an improvement in equity-to-adjusted assets and guarantees ratio (2018: 18.5% vs 2016: 13.3%). However, the bank’s capitalisation ratio remains weaker than that of peers.

The bank’s FRA ratio, a ratio of capitalisation newly introduced by Fitch, was 20.4% at end-2018. The bank’s usable capital, including shareholders’ equity and 10% of ‘AAA’-‘AA’ callable capital (USD28 million), totalled USD2.6 billion at end-2018. Risk-weighted assets totalled USD12.6 billion, lower than unweighted total assets of USD13.4 billion reflecting low weights assigned to investment-grade treasury assets

2.

Due to heavy focus on trade financing, Afreximbank has enjoyed high earnings over the last decade. The bank’s net income more than doubled since 2015, to USD276 million in 2018, on the back of increasing short-term trade finance operations. At end-2018, internal capital generation (return on equity after distribution) averaged 9.2%, the highest across the Africa-focused MDBs. Strong profitability also reflects a low cost-to-income ratio (2018: 18% and 2017: 18%).

Fitch expects the equity-to-assets and guarantees and FRA ratios to moderate and remain at ‘Strong’ and ‘Moderate’ levels, respectively, over the forecast horizon. High lending growth and increase in the bank’s guarantee operations will be match by the capital increase. The bank plans to issue depositary receipts, which has been factored in our forecast.

2 Risk-weighted assets include loans, guarantees, equity investment and other assets which are weighted according to risk of those assets. Weights are inspired by the Basel Committee’s Standard Approach.

Source: Fitch Ratings

Low risk operating environment

High risk business profile

Low risk business profile

High risk operating environment

TDB, BOAD, Afreximbank, EBID, IBEC

CAF

AfDB AsDB, IaDB, IBRD

NADB, IsDB

Business Environment

0

20

40

60

80

100

2015 2016 2017 2018

(%)

Afreximbank TDB

IBEC EDB

Source: Fitch Ratings

Equity/Adj.Assets & Guarantees

0

20

40

60

80

Afreximbank TDB EDB

(%)

Source: Fitch Ratings

FRA Ratio(2018)

Rating Report │ 5 February 2020 fitchratings.com 4

Supranationals

Africa

In 2018, Afreximbank, like many other MDBs, adopted IFRS 9 standards to account for loan loss impairment, replacing the IAS39 incurred loss approach with forward-looking expected credit loss approach. This led to an increase in total impairment allowance (which now covers loans, interest receivables, treasury investments, guarantees and letter of credit) by USD129.9 million (to USD311.6 million on 1 January 2018 from USD181.7 million under the IAS39 standard at end-2017), and a corresponding decline in retained earnings.

Despite the increase in impairment charges and provisions, Fitch expects the bank’s internal capital generation (ICG) to range from 8% to 10% by 2021 (2018: 9.2%). ICG is supported by high margins on non-cash collateralised trade finance loans and low cost to income level.

Peer Comparison: Capital Ratios and Profitability

Afreximbank (BBB-) IBEC (BBB-) EDB (BBB+) TDB (BB+)

End-2018 Projectionª End-2018 End-2018 End-2018

Equity/adjusted assets & guarantees (%)

18.5 15-20 71.7 46.9 21.5

Usable capital/risk-weighted assets (FRA, %)

20.4 15-20 n.a. 64.7 23.2

Net incomeb/average equity 9.2 8-10 -3.4 3.9 9.3

ª Medium-term projections, forecast range b Net income after distribution Source: Fitch Ratings, MDBs

Risks

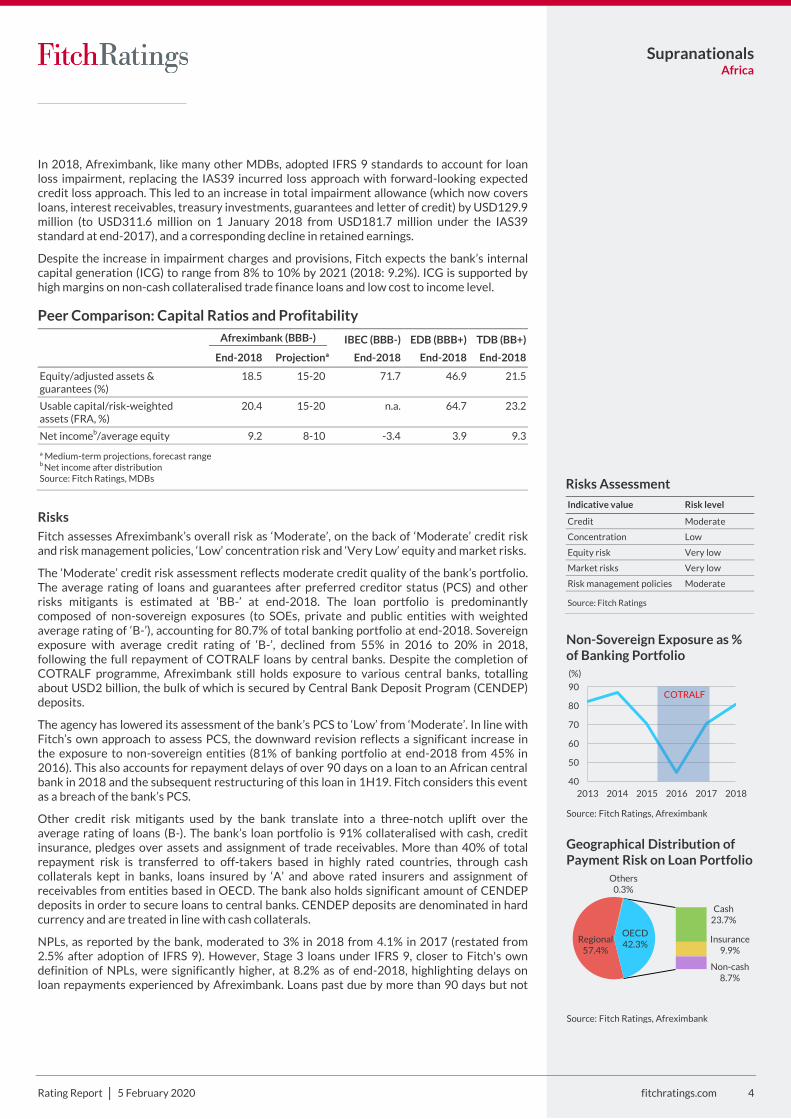

Fitch assesses Afreximbank’s overall risk as ‘Moderate’, on the back of ‘Moderate’ credit risk and risk management policies, ‘Low’ concentration risk and ‘Very Low’ equity and market risks.

The ‘Moderate’ credit risk assessment reflects moderate credit quality of the bank’s portfolio. The average rating of loans and guarantees after preferred creditor status (PCS) and other risks mitigants is estimated at ‘BB-’ at end-2018. The loan portfolio is predominantly composed of non-sovereign exposures (to SOEs, private and public entities with weighted average rating of ‘B-’), accounting for 80.7% of total banking portfolio at end-2018. Sovereign exposure with average credit rating of ‘B-’, declined from 55% in 2016 to 20% in 2018, following the full repayment of COTRALF loans by central banks. Despite the completion of COTRALF programme, Afreximbank still holds exposure to various central banks, totalling about USD2 billion, the bulk of which is secured by Central Bank Deposit Program (CENDEP) deposits.

The agency has lowered its assessment of the bank’s PCS to ‘Low’ from ‘Moderate’. In line with Fitch’s own approach to assess PCS, the downward revision reflects a significant increase in the exposure to non-sovereign entities (81% of banking portfolio at end-2018 from 45% in 2016). This also accounts for repayment delays of over 90 days on a loan to an African central bank in 2018 and the subsequent restructuring of this loan in 1H19. Fitch considers this event as a breach of the bank’s PCS.

Other credit risk mitigants used by the bank translate into a three-notch uplift over the average rating of loans (B-). The bank’s loan portfolio is 91% collateralised with cash, credit insurance, pledges over assets and assignment of trade receivables. More than 40% of total repayment risk is transferred to off-takers based in highly rated countries, through cash collaterals kept in banks, loans insured by ‘A’ and above rated insurers and assignment of receivables from entities based in OECD. The bank also holds significant amount of CENDEP deposits in order to secure loans to central banks. CENDEP deposits are denominated in hard currency and are treated in line with cash collaterals.

NPLs, as reported by the bank, moderated to 3% in 2018 from 4.1% in 2017 (restated from 2.5% after adoption of IFRS 9). However, Stage 3 loans under IFRS 9, closer to Fitch's own definition of NPLs, were significantly higher, at 8.2% as of end-2018, highlighting delays on loan repayments experienced by Afreximbank. Loans past due by more than 90 days but not

Risks Assessment

Indicative value Risk level

Credit Moderate

Concentration Low

Equity risk Very low

Market risks Very low

Risk management policies Moderate

Source: Fitch Ratings

40

50

60

70

80

90

2013 2014 2015 2016 2017 2018

Source: Fitch Ratings, Afreximbank

Non-Sovereign Exposure as % of Banking Portfolio

COTRALF

(%)

Others0.3%

Cash23.7%

OECD42.3%

Geographical Distribution of Payment Risk on Loan Portfolio

Source: Fitch Ratings, Afreximbank

Regional57.4%

Insurance9.9%

Non-cash8.7%

Rating Report │ 5 February 2020 fitchratings.com 5

Supranationals

Africa

impaired (which include Stage 2 and 3 loans) accounted for 13.5% of gross loans at end-20183

. We expect Stage 3 loans as a percentage of total loans to decline by the end of our forecast horizon, due to a combination of fast growth in the loan portfolio, some write-offs and recoveries. This expectation also reflects the fact that the large share of past due but not impaired loans had been regularised by mid-2019.

Concentration risk is considered ‘low’, with the top five exposures accounting for 27% of total banking portfolio at end-2018. This metric considerably improved since 2016 (52%). At geographical level, the top five country exposures included Nigeria, Egypt, Zimbabwe, Mauritius and Gabon, which combined accounted for more than two-thirds of the bank’s portfolio. The main beneficiaries of Afreximbank’s loans have been entities from the financial and energy sectors.

Equity risk is deemed ‘Very Low’, as the bank did not have any equity investment holdings until 2019. The bank has recently set up the Fund for Export Development in Africa (FEDA) to provide seed capital to companies, chiefly SMEs, and catalyse foreign capital flows into Africa’s trade- and export-oriented sectors. Assuming USD100 million of equity investment into the FEDA over the next two years, Fitch expects the bank’s equity participation to remain below 1% of banking portfolio by 2021.

Fitch assesses the bank’s market risks as ‘Very Low’, reflecting very limited impact of currency and interest rate variations on the bank’s balance sheet. Most loans are denominated in US dollars and are matched with financial liabilities in US dollars after cross-currency swaps and forward contracts. The bank closely monitors interest rate movements, and manages net interest rate exposures and maturity structure of assets and liabilities with interest rate swaps. The short-term tenure of the banks’ trade finance assets also supports the ‘very low’ market risk.

Risk management policies are considered ‘Moderate’. The bank uses prudential limits some of which are in line with Basel II standards. However, limits per country, obligor, transaction and sector are not applied to gross loans outstanding, but net exposures (after collaterals), a less conservative approach than most peers.

Peer Comparison: Risks

Afreximbank (BBB-) IBEC (BBB-) EBD (BBB+) TDB (BB+)

End-2018 Projectionª End-2018 End-2018 End-2018

Estimated average rating of loans & guarantees

B- B- B+ B+ B-

Impaired loans/gross loans (%)b 8.2 5.0-6.0 0.0 16.3 2.4

Five largest exposures/total loans (%) 27.2 25-30 60.3 31.7 51.7

Equity stakes/(loans + equity stakes) (%)

0.0 0-5 0.0 0.0 1.2

ª Medium-term projections, forecast range. b Stage 3 loans as per IFRS 9 accounting standards.

Source: Fitch Ratings, MDBs

3

The bank applies a qualitative judgement to decide whether a loan overdue by more than 90 days should be considered impaired. Examples of loans that are past due but not impaired include loans repaid by obligors in local currency but where the national central bank has delayed the provision of hard currency in which Afreximbank is repaid. According to Afreximbank, this approach is consistent with IFRS 9 standards, which allow some flexibility in the definition of default when ‘reasonable information demonstrates that a more lagging criteria [than 90 day past due] should apply’.

Egypt21.6%

Gabon4.1%

Congo4.1%

Ghana4.0%

Sudan3.6%

Others17.0%

Source: Fitch Ratings, Afreximbank

Loan Portfolio by Countries

Zimbabwe6.3%

Mauritius6.1%

Nigeria33.2%

Energy24%

Other14%

Source: Fitch Ratings, Afreximbank

Loans by Economic Sector (2018)

Financial50%

Telecom7%

Government5%

Rating Report │ 5 February 2020 fitchratings.com 6

Supranationals

Africa

Liquidity

Peer Comparison: Liquidity

Afreximbank (BBB-) IBEC (BBB-) EDB (BBB+) TDB (BB+)

End-2018 Projectionª End-2018 End-2018 End-2018

Liquid asset/short-term debt (%) 119 70-100 169 227 78

Share of treasury assets rated ‘AA-’ & above (%)

20.9 18-23 3.9 22.0 0

ª Medium-term projections, forecast range Source: Fitch Ratings, MDBs

Liquidity Buffer

Afreximbank’s liquidity buffer is ‘Moderate’, with liquid assets accounting for 1.2x short-term debt at end-2018. This metric has improved following a surge in trade finance loans with maturities less than 12 months (which Fitch considers as liquid assets after applying a discount) to USD7.1 billion in 2018 from USD2.6 billion in 2017. The agency expects liquid assets to short-term debt to fall below 1.0x reflecting the strong growth in lending operations.

Quality of Treasury Assets

The quality of liquid assets is ‘Moderate’, with the share of ‘AA-’ and above rated treasury assets accounting for 21% of total treasury assets at end-2018. About 87% of treasury assets, which include short-term deposits and money market placements, are kept with investment-grade financial institutions, making Afreximbank comparable to its peers: IBEC (66% at end-2018), TDB (59%) and EDB (99%).

Access to Capital Markets and Alternative Sources of Liquidity

Afreximbank’s liquidity profile is enhanced by the short duration of the loan portfolio (average maturity of 19 months at end-2018) as well as its access to additional liquidity sources.

The bank is not a frequent issuer in international bond markets compared to some other MDBs, which regularly issue debt securities in multiple currencies and in various jurisdictions. However, it benefits from its access to various undrawn credit lines from commercial banks and development institutions. Moreover, it has recently built access to well-diversified non-equity funding sources, including CENDEP deposits and depositary receipts mechanism. The access to alternative sources of liquidity, in Fitch’s view, moderately enhances the bank’s overall liquidity profile.

Shareholders’ Support Fitch has revised up Afreximbank’s support rating to ‘bb’ from ‘bb-’ at its previous review on the back of an improvement in the credit quality of its key shareholders.

Peer Comparison: Shareholder Support

Afreximbank (BBB-) IBEC (BBB-) EDB (BBB+) TDB (BB+)

End-2018 Projectionª End-2018 End-2018 End-2018

Coverage of net debt by callable capital

NC NC NC BBB NC

Average rating of key shareholders BB BB BBB- BBB BB

Propensity to support (notch adjustment)

Moderate (-1)

Moderate (-1)

Weak (-2) Strong (0) Moderate (-1)

a Medium-term projections. Source: Fitch Ratings, MDBs

Afreximbank has a diverse shareholder base, which has expanded over the past few years. The ownership of capital split between four classes of shareholders, with Class A shares owned by African sovereigns and multilateral development institutions, Class B shares by African

Liquidity Assessment

Indicative value Risk level

Liquidity buffer Moderate

Quality of Treasury Assets Moderate

Access to Cap Markets & alt. sources of liquidity

Moderate (+1 notch)

Source: Fitch Ratings

0

100

200

300

400

500

600

2015 2016 2017 2018

(%)

Afreximbank

TDB

IBEC

Source: Fich Ratings

Liqud Assets to Short-term Debt

AAA7%

AA14%

A50%

BBB16%

below BBB13%

Source: Fitch Ratings, Afreximbank

Breakdown of Treasury Assets by Ratings

Rating Report │ 5 February 2020 fitchratings.com 7

Supranationals

Africa

financial institutions and private investors, Class C shares by non-African institutions, and Class D shares by private investors. Class D shares are backed by freely tradable depositary receipts, which were issued and listed in the Stock Exchange of Mauritius in October 2017.

Capacity to Provide Extraordinary Support

The revision of extraordinary support assessment to ‘bb’ primarily reflects an improvement in the credit quality of shareholders. An upgrade of the sovereign ratings of Egypt and Russia (BBB/Stable) in 2019, resulted in a ‘BB’ average rating of key shareholders, one notch up from ‘BB-’ at the previous review. The credit quality of key-shareholders is also supported by AfDB’s shareholding: as a founder shareholder with permanent seat on the board, AfDB has a vested interest to support Afreximbank despite the decline in its share in the bank’s subscribed capital (to 3.3% in 2018 from 6.0% in 2009).

The bank’s callable capital is partially supported by medium-term credit risk mitigation instruments (covering 71% of total callable capital), particularly insurance policies issued by highly rated insurance providers based in OECD countries. This would enable the bank to call the insurance in the event of a default of a shareholder on its callable commitments. Fitch views this mechanism as beneficial to the bank’s support capacity assessment, leading to an uplift of one notch over the average rating of key shareholders, to ‘BB+’.

Propensity to Provide Extraordinary Support

The propensity of the bank’s shareholders to provide support is considered ‘Moderate’, translating into a negative one notch adjustment below the support capacity. This assessment reflects the relative small size of Afreximbank’s portfolio (USD11.8 billion at end-2018) relative to the size of the economies in which it operates

4.

Fitch’s support propensity assessment also factors in the fact that the board of directors can call capital as and when necessary to finance growth in operations and recapitalise the bank. Such a call becomes mandatory when the capital adequacy ratio falls close to 4%, in line with Basel guideline. This differentiates Afreximbank from the bulk of other Fitch-rated MDBs, which can only call capital when unable to repay a short-term liability. The bank has never resorted to callable capital and maintains it as an additional buffer.

4 Afreximbank operates in 52 African states, whose total GDP is estimated at USD2.3 trillion according to data collected from IMF WEO Database October 2019.

AAA3.3%

AA0.1%

A5.9%

BBB10.7%

BB and below80.0%

Source: Fiitch Ratings, Afreximbank

Shareholders by Ratings

Rating Report │ 5 February 2020 fitchratings.com 8

Supranationals

Africa

Rating Report │ 5 February 2020 fitchratings.com 9

Supranationals

Africa

Rating Report │ 5 February 2020 fitchratings.com 10

Supranationals

Africa

Rating Report │ 5 February 2020 fitchratings.com 11

Supranationals

Africa

Rating Report │ 5 February 2020 fitchratings.com 12

Supranationals

Africa

The ratings above were solicited and assigned or maintained at the request of the rated entity/issuer or a related third party. Any exceptions follow below.

ALL FITCH CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS AND DISCLAIMERS. PLEASE READ THESE LIMITATIONS AND DISCLAIMERS BY FOLLOWING THIS LINK: HTTPS://FITCHRATINGS.COM/UNDERSTANDINGCREDITRATINGS. IN ADDITION, RATING DEFINITIONS AND THE TERMS OF USE OF SUCH RATINGS ARE AVAILABLE ON THE AGENCY'S PUBLIC WEB SITE AT WWW.FITCHRATINGS.COM. PUBLISHED RATINGS, CRITERIA, AND METHODOLOGIES ARE AVAILABLE FROM THIS SITE AT ALL TIMES. FITCH'S CODE OF CONDUCT, CONFIDENTIALITY, CONFLICTS OF INTEREST, AFFILIATE FIREWALL, COMPLIANCE, AND OTHER RELEVANT POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE CODE OF CONDUCT SECTION OF THIS SITE. FITCH MAY HAVE PROVIDED ANOTHER PERMISSIBLE SERVICE TO THE RATED ENTITY OR ITS RELATED THIRD PARTIES. DETAILS OF THIS SERVICE FOR RATINGS FOR WHICH THE LEAD ANALYST IS BASED IN AN EU-REGISTERED ENTITY CAN BE FOUND ON THE ENTITY SUMMARY PAGE FOR THIS ISSUER ON THE FITCH WEBSITE.

Copyright © 2020 by Fitch Ratings, Inc., Fitch Ratings Ltd. and its subsidiaries. 33 Whitehall Street, NY, NY 10004. Telephone: 1-800-753-4824, (212) 908-0500. Fax: (212) 480-4435. Reproduction or retransmission in whole or in part is prohibited except by permission. All rights reserved. In issuing and maintaining its ratings and in making other reports (including forecast information), Fitch relies on factual information it receives from issuers and underwriters and from other sources Fitch believes to be credible. Fitch conducts a reasonable investigation of the factual information relied upon by it in accordance with its ratings methodology, and obtains reasonable verification of that information from independent sources, to the extent such sources are available for a given security or in a given jurisdiction. The manner of Fitch’s factual investigation and the scope of the third-party verification it obtains will vary depending on the nature of the rated security and its issuer, the requirements and practices in the jurisdiction in which the rated security is offered and sold and/or the issuer is located, the availability and nature of relevant public information, access to the management of the issuer and its advisers, the availability of pre-existing third-party verifications such as audit reports, agreed-upon procedures letters, appraisals, actuarial reports, engineering reports, legal opinions and other reports provided by third parties, the availability of independent and competent third-party verification sources with respect to the particular security or in the particular jurisdiction of the issuer, and a variety of other factors. Users of Fitch’s ratings and reports should understand that neither an enhanced factual investigation nor any third-party verification can ensure that all of the information Fitch relies on in connection with a rating or a report will be accurate and complete. Ultimately, the issuer and its advisers are responsible for the accuracy of the information they provide to Fitch and to the market in offering documents and other reports. In issuing its ratings and its reports, Fitch must rely on the work of experts, including independent auditors with respect to financial statements and attorneys with respect to legal and tax matters. Further, ratings and forecasts of financial and other information are inherently forward-looking and embody assumptions and predictions about future events that by their nature cannot be verified as facts. As a result, despite any verification of current facts, ratings and forecasts can be affected by future events or conditions that were not anticipated at the time a rating or forecast was issued or affirmed.

The information in this report is provided “as is” without any representation or warranty of any kind , and Fitch does not represent or warrant that the report or any of its contents will meet any of the requirements of a recipient of the report. A Fitch rating is an opinion as to the creditworthiness of a security. This opinion and reports made by Fitch are based on established criteria and methodologies that Fitch is continuously evaluating and updating. Therefore, ratings and reports are the collective work product of Fitch and no individual, or group of individuals, is solely responsible for a rating or a report. The rating does not address the risk of loss due to risks other than credit risk, unless such risk is specifically mentioned. Fitch is not engaged in the offer or sale of any security. All Fitch reports have shared authorship. Individuals identified in a Fitch report were involved in, but are not solely responsible for, the opinions stated therein. The individuals are named for contact purposes only. A report providing a Fitch rating is neither a prospectus nor a substitute for the information assembled, verified and presented to investors by the issuer and its agents in connection with the sale of the securities. Ratings may be changed or withdrawn at any time for any reason in the sole discretion of Fitch. Fitch does not provide investment advice of any sort. Ratings are not a recommendation to buy, sell, or hold any security. Ratings do not comment on the adequacy of market price, the suitability of any security for a particular investor, or the tax-exempt nature or taxability of payments made in respect to any security. Fitch receives fees from issuers, insurers, guarantors, other obligors, and underwriters for rating securities. Such fees generally vary from US$1,000 to US$750,000 (or the applicable currency equivalent) per issue. In certain cases, Fitch will rate all or a number of issues issued by a particular issuer, or insured or guaranteed by a particular insurer or guarantor, for a single annual fee. Such fees are expected to vary from US$10,000 to US$1,500,000 (or the applicable currency equivalent). The assignment, publication, or dissemination of a rating by Fitch shall not constitute a consent by Fitch to use its name as an expert in connection with any registration statement filed under the United States securities laws, the Financial Services and Markets Act of 2000 of the United Kingdom, or the securities laws of any particular jurisdiction. Due to the relative efficiency of electronic publishing and distribution, Fitch research may be available to electronic subscribers up to three days earlier than to print subscribers.

For Australia, New Zealand, Taiwan and South Korea only: Fitch Australia Pty Ltd holds an Australian financial services license (AFS license no. 337123) which authorizes it to provide credit ratings to wholesale clients only. Credit ratings information published by Fitch is not intended to be used by persons who are retail clients within the meaning of the Corporations Act 2001.

![Welcome [] · Zülküf Küçüközer TriangleCanvas.java import javax.microedition.lcdui.Graphics; import javax.microedition.lcdui.game.*; import javax.microedition.m3g.*;](https://img.dokumen.tips/doc/110x75/5d31f91d88c9937a3b8ccf67/welcome-zuelkuef-kuecuekoezer-trianglecanvasjava-import-javaxmicroeditionlcduigraphics.jpg)