Embed Size (px)

Citation preview

African Emergence –

The rise of the phoenix

kpmgafrica.com

b | African Emergence

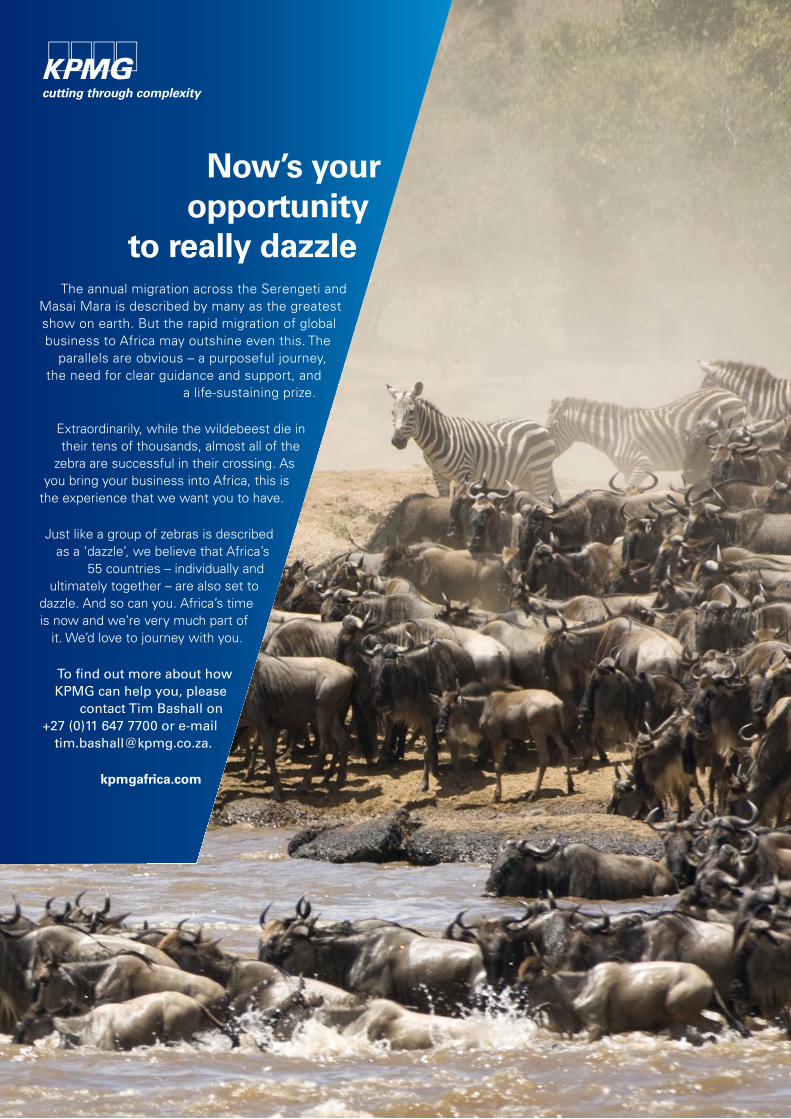

Now’s your opportunity

to really dazzleThe annual migration across the Serengeti and

Masai Mara is described by many as the greatest show on earth. But the rapid migration of global business to Africa may outshine even this. The

parallels are obvious – a purposeful journey, the need for clear guidance and support, and

a life-sustaining prize.

Extraordinarily, while the wildebeest die in their tens of thousands, almost all of the

zebra are successful in their crossing. As you bring your business into Africa, this is

the experience that we want you to have.

Just like a group of zebras is described as a ‘dazzle’, we believe that Africa’s

55 countries – individually and ultimately together – are also set to

dazzle. And so can you. Africa’s time is now and we’re very much part of

it. We’d love to journey with you.

To find out more about how KPMG can help you, please

contact Tim Bashall on +27 (0)11 647 7700 or e-mail

kpmgafrica.com

The rise of the phoenix | 1

Contents

A message from Moses Kgosana | Senior Partner, KPMG Africa Limited 2

A message from Yunus Suleman | Chairman, KPMG Africa Limited 4

Opinion piece | Foreign Direct Investment in Africa 7

Sources 21

KPMG in Africa 22

Contacts 24

2 | African Emergence

The rise of the phoenix | 3

A message from Moses KgosanaWe live in an interconnected world. What we do has an impact on others and what they do has an impact on us. This truth is embodied in the African philosophy of Ubuntu – literally meaning ‘humanity’ and encapsulating the understanding that “I am what I am because of who we all are”. There is huge strength in this. While the economic value of investment in Africa is becoming increasingly self-evident, unexpected value from Africa is also now revealing itself through fundamental truths such as this. We like to think of this whole context as ‘Economic Ubuntu’.

How fitting, therefore, that the World Economic Forum on Africa is once again bringing together business, political, academic and other leaders of society to shape global, regional and industry agendas. As always, the delegates list reads like a “Who’s Who in Africa”, including from among the most prominent leaders and significant movers-and-shakers. A powerful combination.

Realising the significant investment opportunities that exist in Africa – in fact, some of the best in the world at present – is up to all of us, working together: government and business, with a common sense of purpose and commitment to uplifting the communities which look to us. Our interconnectedness is one of Africa’s greatest drawcards – and the continent is clearly ‘open for business’. Investors are looking for a share of Africa’s abundant resources and the burgeoning population is ready. Africa is ready to move forward but the required investments are massive.

There is a lot of discussion (and some very specific actions) regarding Foreign Direct Investment in Africa. KPMG is pleased to play an active part in this dialogue, including through this specially prepared publication. We are passionate about Africa and the business opportunities that abound, believing that these are sought by savvy investors who expect global standards in an African context.

Our own interconnectedness allows us to readily bring our people together and deliver on the synergies that this presents. Through high impact initiatives such as the KPMG Africa Conversation Series, we regularly contribute to the journey our clients and other key stakeholders are taking across Africa. Our research across 19 African countries (including comparisons to several other countries beyond Africa) on the causes of complexity in business today and how these are being confronted is proving invaluable to informed discussions about doing business in Africa.

Taking this position still further forward, I invite you to watch ‘Invest Africa’ on CNBC-Africa every Wednesday at 20:30 (CAT), which KPMG is proud to be the title sponsor of. This exciting new programme launches on 16 May 2012, with a discussion that recognises the importance of the World Economic Forum on Africa meeting in Addis Ababa this week.

I trust that you will find particular value in this publication. Foreign Direct Investment plays a key role in global business in a number of ways. Please give us your feedback. Through understanding what our stakeholders most value – and want – we are able to continuously position ourselves to best serve you across this magnificent continent and anywhere else in the world where your interests shine.

Moses Kgosana Senior Partner, KPMG Africa Limited

4 | African Emergence

The rise of the phoenix | 5

A message from Yunus SulemanMuch has often been said about ‘putting your money where your mouth is’ – showing support for something you believe in through your actions, and especially the giving of money. Arguably, not enough emphasis is typically placed on ‘putting your mouth where your money is’ – sharing experiences, leading by example and revealing the philosophies – and the power – of responsible capitalism.

This is where the World Economic Forum comes in. Committed to improving the state of the world, the engagement that the World Economic Forum facilitates with business, political, academic and other leaders of society is second-to-none. KPMG salutes the World Economic Forum and is proud to be associated with this outstanding organisation. It is particularly encouraging to see the growing interest in Africa as a credible and highly relevant economically viable destination.

Africa is described as being ‘investment hungry’. In fact, it currently has an insatiable appetite for growth. The needs are everywhere – from roads, power stations and the myriad of other infrastructural essentials to privately owned profit-oriented investments across sectors, borders and markets. All of this requires money – and there simply isn’t enough within the continent itself.

Foreign Direct Investment (FDI) is an essential component of Africa’s sustainable, positive future. And it’s good for the investors too – there is undoubtedly money to be made in Africa, recognised today as one of the world’s most attractive high growth markets. Understanding FDI, what it means to Africa as much as to the global investor, accessing these funds and securing the desired returns are all very much part of today’s Africa story.

In this thought provoking publication, we are seeking to make a robust contribution to the essential conversations regarding FDI in Africa. This is a passion of ours, recognising that FDI is a key trigger point for so much else of what we all desire for Africa and her people. The win-win is that the investor scores too – which needs to be profitably, sustainably and responsibly.

I trust that you’ll enjoy reading this piece and, with my fellow Partners across the world, would welcome the opportunity of discussing any aspect of this further with you. We are committed to Africa, starting with an advocacy role of realistically promoting the very many positive influences, actions and outcomes that are shaping Africa today in so many ways.

Yunus Suleman Chairman, KPMG Africa Limited

6 | African Emergence

The rise of the phoenix | 7

Opinion piece

This opinion piece centres on Foreign Direct Investment (FDI) and trade in Africa. The discussion is – where applicable – structured around the following three mega-trends: natural resources, (including mining, oil, gas and agriculture), consumer demand and infrastructure.

Q: What has changed in Africa’s fundamentals over the past decade or more that is driving investment higher? How has investment in Africa changed over the past decade or more in terms of the sectors targeted?

A: Africa is increasingly able to draw attention from the global stage in terms of attracting investment. Taking a step back in time, as the 1980s drew to a close, several geopolitical convergences conspired to create a new and challenging space for African countries. The most fundamental of these shifts was the collapse of the Soviet Union and the liberation of its east Europe buffer. It was not perhaps so much the collapse of the Soviet empire as the disintegration of the bi-polar Superpower configuration that spawned a so-called “Cold War” and an intense competition between the West (mainly the United States) and the Soviets for influence in just about every nook and cranny on the planet.

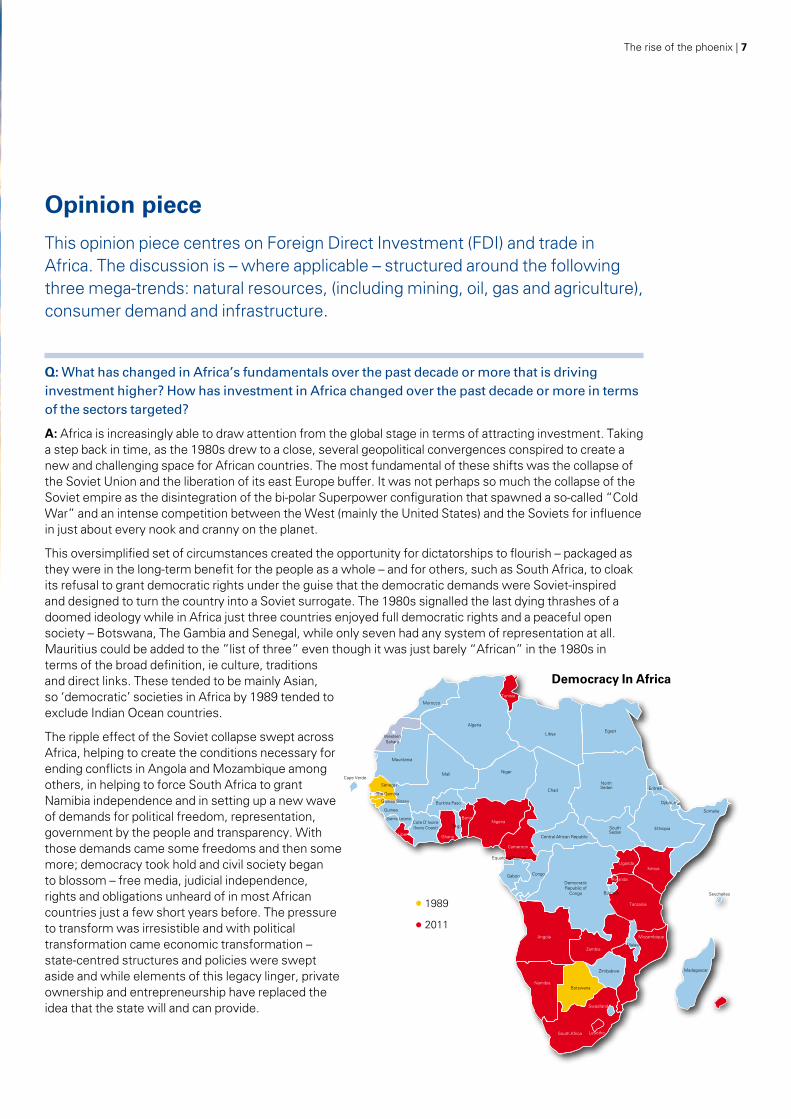

This oversimplified set of circumstances created the opportunity for dictatorships to flourish – packaged as they were in the long-term benefit for the people as a whole – and for others, such as South Africa, to cloak its refusal to grant democratic rights under the guise that the democratic demands were Soviet-inspired and designed to turn the country into a Soviet surrogate. The 1980s signalled the last dying thrashes of a doomed ideology while in Africa just three countries enjoyed full democratic rights and a peaceful open society – Botswana, The Gambia and Senegal, while only seven had any system of representation at all. Mauritius could be added to the ”list of three” even though it was just barely “African” in the 1980s in terms of the broad definition, ie culture, traditions and direct links. These tended to be mainly Asian, so ‘democratic’ societies in Africa by 1989 tended to exclude Indian Ocean countries.

The ripple effect of the Soviet collapse swept across Africa, helping to create the conditions necessary for ending conflicts in Angola and Mozambique among others, in helping to force South Africa to grant Namibia independence and in setting up a new wave of demands for political freedom, representation, government by the people and transparency. With those demands came some freedoms and then some more; democracy took hold and civil society began to blossom – free media, judicial independence, rights and obligations unheard of in most African countries just a few short years before. The pressure to transform was irresistible and with political transformation came economic transformation – state-centred structures and policies were swept aside and while elements of this legacy linger, private ownership and entrepreneurship have replaced the idea that the state will and can provide.

North Sedan

South Sedan

Democracy In Africa

1989

2011

That in turn created opportunities for outsiders to invest in and take a share of the growing demands for goods and services in several key countries and to take a share of the wealth potential generated by an expanded and expanding infrastructure network not only on a country-by-country basis, but across the continent. In addition, the massive resources of the continent, its oil, minerals, and other raw materials were suddenly more available and accessible than at any time during the so-called “Cold War” era and that too sparked massive foreign extraction investment that more lately has turned to downstream beneficiation, as well as leaving a more lasting impact.

The interconnection between economic growth, social development and political freedom quickly became more obvious and demands for political freedom were now accompanied by expectations of economic and social improvement. By 2011, an additional 18 countries complied with the requirements of a full electoral democracy – including some major new members since 1989:

• South Africa, Nigeria, Ghana, Kenya, Tanzania, Mozambique, Angola, Uganda, Benin, Seychelles, Mauritius, Rwanda, Namibia, Zambia, Liberia, Lesotho Tunisia, and Cameroon.

Several others were considered partially free or semi-democratic, but with restrictions and problems:

• Zimbabwe, Morocco, the Republic of Congo, DRC, Algeria, Ethiopia, Malawi, Eritrea, and Gabon – many of these with significant investment potential despite the obvious political risks.

It was not only the number of countries that were now embracing democratic practice, it was in many cases the quality of the countries and their investment potential. South Africa freed of sanctions, Nigeria with its vast population and massive potential free of military rule and the constant threat of coups, Kenya the hub that opened East Africa sparking reform in Tanzania, Uganda and, following its horrific experiences in 1994, Rwanda. The Arab Spring has added significantly to Africa’s future investment potential and while Libya, South Sudan and Sudan are likely to continue with internal political struggles and limited democracy, they too hold tremendous potential. Egypt is expected to begin to fly a lot sooner.

All of this drives higher investment from companies and countries seeking a foothold in Africa and looking to take a share of the tremendous wealth and potential that has yet to be unlocked. What we have seen to date is the tip of the proverbial iceberg – the continent has much more to offer and investments will continue to flow.

When looking at the last decade or more, some of the key reasons for increased investment in Africa over the period have been a favourable outlook for economic growth, improving business environments, market-driven reforms in many cases done with guidance from the International Monetary Fund (IMF), and a general lowering in the sovereign risk profile of African countries. In many cases also, as more economic data on countries became available, it became easier to measure (and with a greater degree of certainty) the economic risk of investing in African countries, and made it possible to monitor this risk on a continuous basis. In many cases too, an improving political climate paved the way for a reduction in economic risk. Improved government policies have allowed better scope for the private sector to grow. Macroeconomic policies became increasingly targeted at stability, enhancing the ability of many African countries to deal with short-term shocks. Massive debt relief under the IMF-World Bank’s Heavily Indebted Poor Countries (HIPC) debt relief initiative and the Multilateral Debt Relief Initiative (MDRI) paved the way for governments to divert funding used for debt service payments to spending on infrastructure. With 26 African countries having qualified for debt relief under the IMF/World Bank debt relief initiatives as of December 2011, and as a result of improved fiscal policies, African governments’ debt metrics in many instances look much healthier than that of their European counterparts. Furthermore, as the IMF has noted quite accurately, during the first decade of this century, sub-Saharan Africa’s economic growth performance surpassed the global average, in both good times and bad.

Increasingly, investors have become aware not only of the risks of investing in Africa, but the risk of not investing in the continent. They have become more focused on where in Africa to invest, as opposed to whether to invest or not. Increased awareness of the potential size of the African consumer market, and a number of significant discoveries of oil and minerals in recent years which have again highlighted the natural resources potential, have all played their role to attract additional investment to the continent. Concurrently, an increased interest from foreigners and local governments alike to address the continent’s infrastructure challenges has seen increased investment in roads, rails and ports.

8 | African Emergence

The rise of the phoenix | 9

We expect to continue to see very strong investment in the oil and gas sectors in Africa. The discovery of oil off the coast of Ghana in 2007 again excited key global energy players and once more hinted at the enormous resource potential of Africa. Additional recent discoveries of gas off the coasts of Tanzania and Mozambique further endorsed the appeal of investment in Africa’s energy potential and in March this year Kenya discovered some oil, although the commercial viability still needs to be determined. Whereas at the end of 2010, Africa had 120 billion barrels of proven oil reserves, it is projected that another 100 billion barrels of oil are offshore Africa, only waiting to be discovered. Furthermore, enormous agricultural potential exists on the continent – while at the same time two recent global food price increases have highlighted the vulnerability of the world’s population.

Although Africa’s oil, gas, mineral and metal endowment will remain important drawcards for investment on the continent, increasingly focus has shifted to the potential contained in the size of and growth in Africa’s consumer market. Consumer-facing companies ranging from clothing, to food, telecommunications and to retail banking all have extensive strategies in various stages of play on the continent. Increased investment in construction and manufacturing is expected to continue to take place across Africa. As Africa continues to invest in its infrastructure, notably addressing the problem of insufficient energy supplies, the cost of manufacturing should decline. African economies continue to diversify and, in this regard, have also realised that although its domestic manufacturing sector may not be able to compete on a global basis, it could compete on a regional African basis, and be well employed serving a regional African market, and even creating a regional footprint.

Q: Which sectors have dominated Africa’s FDI inflows over the past decade? Which African countries have received the highest levels of FDI? How is Africa competing in terms of investment relative to other High Growth Markets (HGM) in Asia and Latin America?

A: By and large, FDI into Africa has followed the oil over the past decade. As such, the top six oil producers in Africa – Nigeria, Algeria, Angola, Libya, Egypt and Sudan – are all among the top eight recipients of FDI on the continent despite some of them being very challenging places in which to do business. Other African FDI frontrunners are South Africa, Morocco and Tunisia: in contrast to the abovementioned countries, these three economies are not rich in oil, but their strength lies in their diversification, and they have therefore been able to attract FDI in other sectors of the economy. South Africa has by far the largest stock of inward FDI in Africa, followed by the next two largest economies on the continent, Egypt and Nigeria.

10 | African Emergence

In terms of comparing Africa with other HGMs, as a whole, Africa received an average of $51.1bn worth of FDI inflows p.a. since 2004. This is well below China, but around double as much as what was received by India and Brazil. As a percentage of GDP though, Africa received an impressive 4% worth of FDI during the 2004-10 period. Not many regions of the world can compete with this.

1 This suggests that FDI/GDP in Africa is perhaps only high because of Africa’s relatively low GDP (per capita). This is particularly evident if we take a high-income region such as Europe. According to UNCTAD data, developed economies in Europe’s FDI/GDP from 2001-10 was 3.1%, compared to 3.7% for Africa. However, these European countries’ FDI per capita averaged $883 p.a. during the 2001-10 period compared to Africa’s $44 p.a. So, the benefit per person in Africa is much lower, even though its FDI/GDP ratio is higher.

Even though its FDI/GDP is high, Africa’s FDI inflows per capita are still low compared to most emerging market economies1. It is also well below the FDI per capita in developed nations, as shown in the graph below on the right. In a regional context, Northern, Central and Southern Africa perform much better than West and East Africa. While the first three perform better than ‘Developing Asia’, FDI per capita in East and West Africa remain very low. In East Africa in particular, FDI per capita was in the region of only $20 p.a. over the past few years.

The rise of the phoenix | 11

In terms of stocks of FDI, Africa’s stock of inward FDI has risen substantially since the late-1990s – from $110bn at the end of 1998 to $554bn at the end of 2010. Despite this increase, it is still fairly low compared to other HGMs. For example, the FDI stock in China on its own was $578.8bn at the end of 2010, while Brazil had $472.6bn worth of FDI. As shown in the accompanying graph, Africa is also not catching up with the regions ahead of it, such as East Asia and South America, as these regions’ FDI inflows are also generally higher than that of Africa.

However, improvements in the business, political and macroeconomic environments across the continent have made African economies more attractive than ever before. On the downside, African countries and regions, with some exceptions – Rwanda comes to mind – continue to be less competitive than some other HGM preferred investment destinations. This is perhaps precisely because of its relatively young democracies and the lack of such restrictions in other HGMs. While many African countries are likely to continue with exploitative labour and social practices, the space for this is closing rapidly in Africa, and since many Asian and Latin American competitors do not have similar political considerations, African output is likely to remain lower. Political considerations are not the only issues: shortfalls in education and training, skills shortages, ‘brain drains’ and a lack of resources for basic healthcare are also key inhibitors of African competitiveness. Red tape, over-restrictive labour laws and other administrative and governance issues such as corruption and mismanagement are likely to remain higher in Africa than in some other HGMs, but not in perpetuity and improvements are on-going in all aspects of governance. These issues will hinder, not prevent a growing African contribution to global investment opportunities. Nor is the investment decision always so apparently simple. The DRC, Ivory Coast, the Republic of Congo, Sudan, South Sudan, Libya, Egypt, Tunisia, Morocco and others offer investment opportunities, but with significantly higher risk in some cases. Political risk remains one of the determinants in assessing investment potential and such an assessment would obviously include a particular risk appetite/profile and the risk/reward equation. There are places where political risk may be high but where the return on investment is sufficiently high to justify taking on such high political risk. These are not issues that can be resolved in theory; they need an individual assessment of risk and what risk is worth what potential reward.

12 | African Emergence

Q: What are the general trends in trade flows into and out of Africa? How does Africa compare to other HGMs in terms of export growth? What will be the key dynamics of African trade in 2012 and beyond?

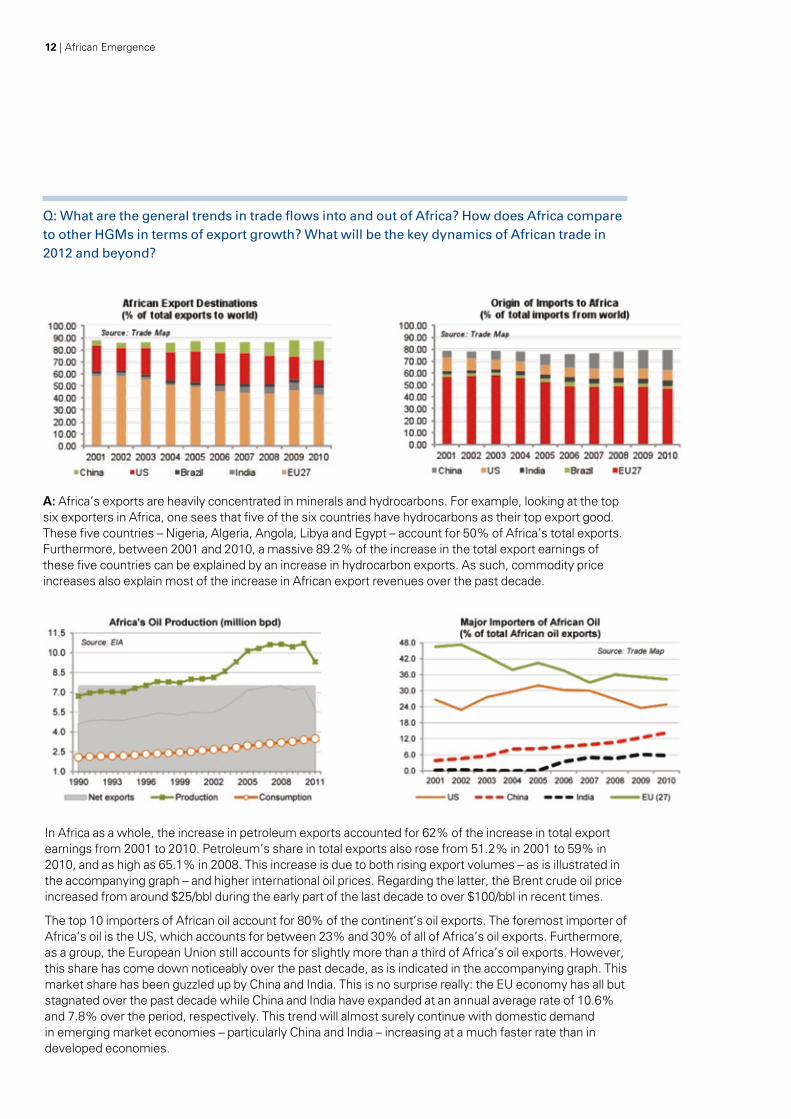

A: Africa’s exports are heavily concentrated in minerals and hydrocarbons. For example, looking at the top six exporters in Africa, one sees that five of the six countries have hydrocarbons as their top export good. These five countries – Nigeria, Algeria, Angola, Libya and Egypt – account for 50% of Africa’s total exports. Furthermore, between 2001 and 2010, a massive 89.2% of the increase in the total export earnings of these five countries can be explained by an increase in hydrocarbon exports. As such, commodity price increases also explain most of the increase in African export revenues over the past decade.

In Africa as a whole, the increase in petroleum exports accounted for 62% of the increase in total export earnings from 2001 to 2010. Petroleum’s share in total exports also rose from 51.2% in 2001 to 59% in 2010, and as high as 65.1% in 2008. This increase is due to both rising export volumes – as is illustrated in the accompanying graph – and higher international oil prices. Regarding the latter, the Brent crude oil price increased from around $25/bbl during the early part of the last decade to over $100/bbl in recent times.

The top 10 importers of African oil account for 80% of the continent’s oil exports. The foremost importer of Africa’s oil is the US, which accounts for between 23% and 30% of all of Africa’s oil exports. Furthermore, as a group, the European Union still accounts for slightly more than a third of Africa’s oil exports. However, this share has come down noticeably over the past decade, as is indicated in the accompanying graph. This market share has been guzzled up by China and India. This is no surprise really: the EU economy has all but stagnated over the past decade while China and India have expanded at an annual average rate of 10.6% and 7.8% over the period, respectively. This trend will almost surely continue with domestic demand in emerging market economies – particularly China and India – increasing at a much faster rate than in developed economies.

The rise of the phoenix | 13

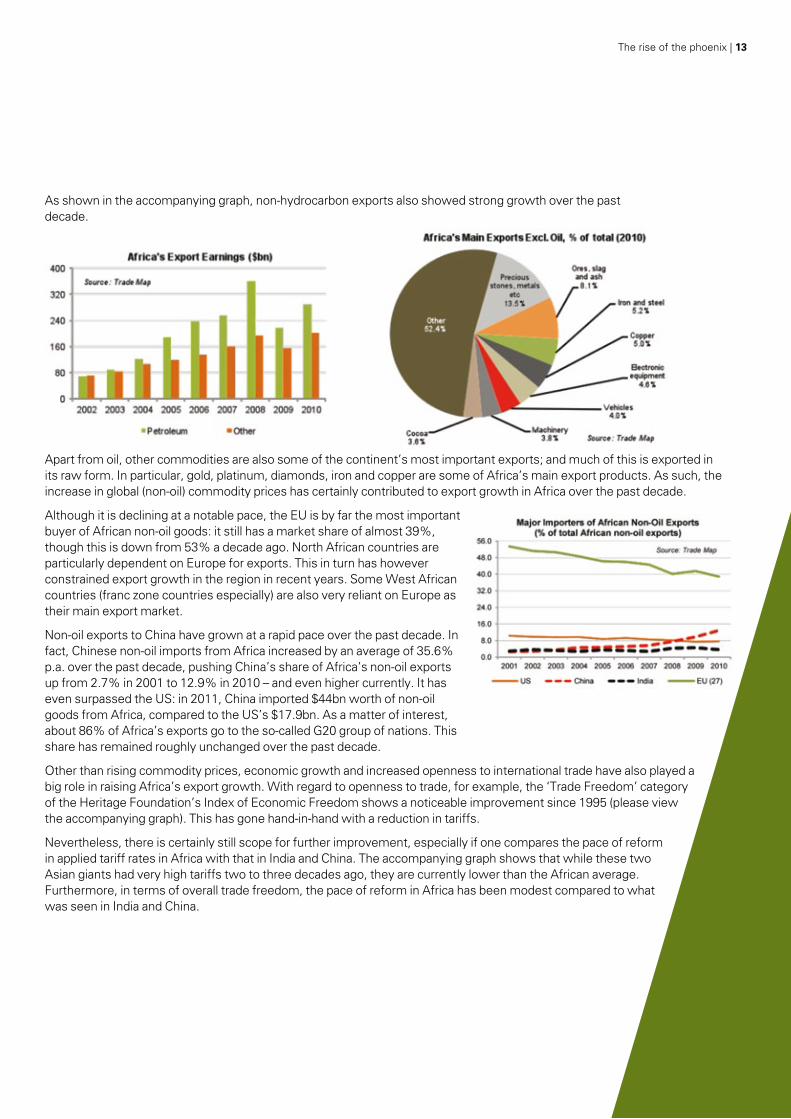

As shown in the accompanying graph, non-hydrocarbon exports also showed strong growth over the past decade.

Apart from oil, other commodities are also some of the continent’s most important exports; and much of this is exported in its raw form. In particular, gold, platinum, diamonds, iron and copper are some of Africa’s main export products. As such, the increase in global (non-oil) commodity prices has certainly contributed to export growth in Africa over the past decade.

Although it is declining at a notable pace, the EU is by far the most important buyer of African non-oil goods: it still has a market share of almost 39%, though this is down from 53% a decade ago. North African countries are particularly dependent on Europe for exports. This in turn has however constrained export growth in the region in recent years. Some West African countries (franc zone countries especially) are also very reliant on Europe as their main export market.

Non-oil exports to China have grown at a rapid pace over the past decade. In fact, Chinese non-oil imports from Africa increased by an average of 35.6% p.a. over the past decade, pushing China’s share of Africa’s non-oil exports up from 2.7% in 2001 to 12.9% in 2010 – and even higher currently. It has even surpassed the US: in 2011, China imported $44bn worth of non-oil goods from Africa, compared to the US’s $17.9bn. As a matter of interest, about 86% of Africa’s exports go to the so-called G20 group of nations. This share has remained roughly unchanged over the past decade.

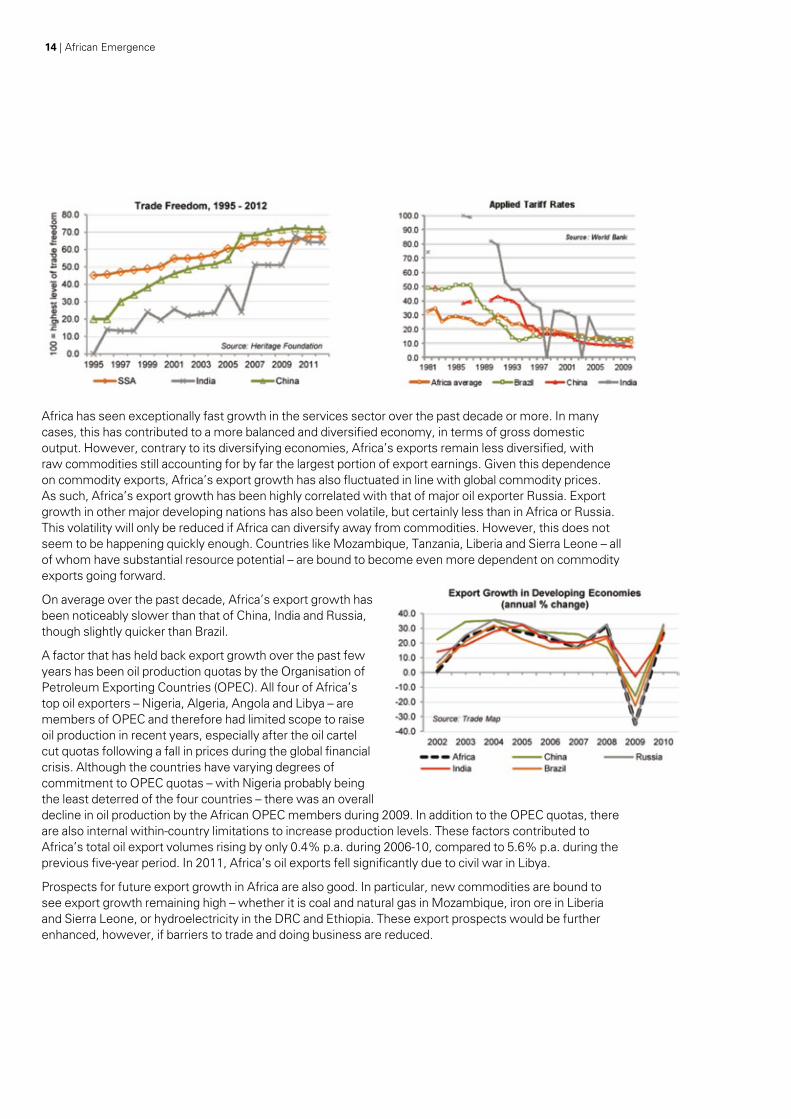

Other than rising commodity prices, economic growth and increased openness to international trade have also played a big role in raising Africa’s export growth. With regard to openness to trade, for example, the ‘Trade Freedom’ category of the Heritage Foundation’s Index of Economic Freedom shows a noticeable improvement since 1995 (please view the accompanying graph). This has gone hand-in-hand with a reduction in tariffs.

Nevertheless, there is certainly still scope for further improvement, especially if one compares the pace of reform in applied tariff rates in Africa with that in India and China. The accompanying graph shows that while these two Asian giants had very high tariffs two to three decades ago, they are currently lower than the African average. Furthermore, in terms of overall trade freedom, the pace of reform in Africa has been modest compared to what was seen in India and China.

14 | African Emergence

Africa has seen exceptionally fast growth in the services sector over the past decade or more. In many cases, this has contributed to a more balanced and diversified economy, in terms of gross domestic output. However, contrary to its diversifying economies, Africa’s exports remain less diversified, with raw commodities still accounting for by far the largest portion of export earnings. Given this dependence on commodity exports, Africa’s export growth has also fluctuated in line with global commodity prices. As such, Africa’s export growth has been highly correlated with that of major oil exporter Russia. Export growth in other major developing nations has also been volatile, but certainly less than in Africa or Russia. This volatility will only be reduced if Africa can diversify away from commodities. However, this does not seem to be happening quickly enough. Countries like Mozambique, Tanzania, Liberia and Sierra Leone – all of whom have substantial resource potential – are bound to become even more dependent on commodity exports going forward.

On average over the past decade, Africa’s export growth has been noticeably slower than that of China, India and Russia, though slightly quicker than Brazil.

A factor that has held back export growth over the past few years has been oil production quotas by the Organisation of Petroleum Exporting Countries (OPEC). All four of Africa’s top oil exporters – Nigeria, Algeria, Angola and Libya – are members of OPEC and therefore had limited scope to raise oil production in recent years, especially after the oil cartel cut quotas following a fall in prices during the global financial crisis. Although the countries have varying degrees of commitment to OPEC quotas – with Nigeria probably being the least deterred of the four countries – there was an overall decline in oil production by the African OPEC members during 2009. In addition to the OPEC quotas, there are also internal within-country limitations to increase production levels. These factors contributed to Africa’s total oil export volumes rising by only 0.4% p.a. during 2006-10, compared to 5.6% p.a. during the previous five-year period. In 2011, Africa’s oil exports fell significantly due to civil war in Libya.

Prospects for future export growth in Africa are also good. In particular, new commodities are bound to see export growth remaining high – whether it is coal and natural gas in Mozambique, iron ore in Liberia and Sierra Leone, or hydroelectricity in the DRC and Ethiopia. These export prospects would be further enhanced, however, if barriers to trade and doing business are reduced.

The rise of the phoenix | 15

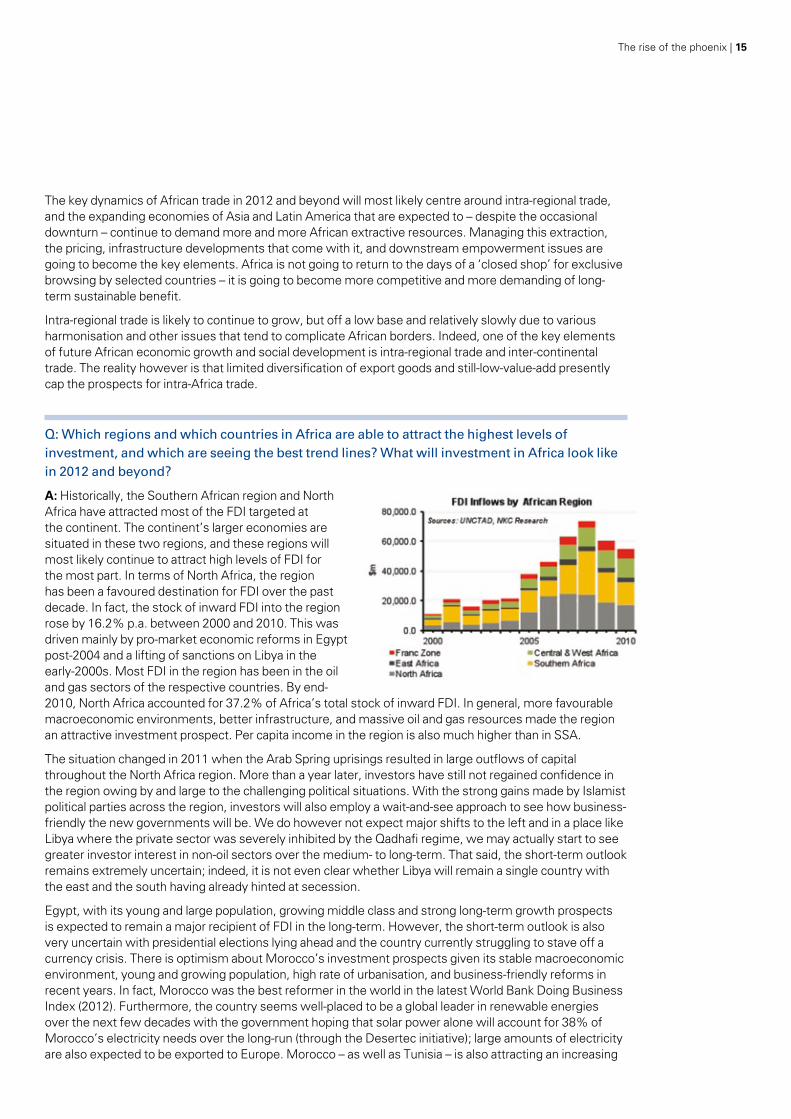

The key dynamics of African trade in 2012 and beyond will most likely centre around intra-regional trade, and the expanding economies of Asia and Latin America that are expected to – despite the occasional downturn – continue to demand more and more African extractive resources. Managing this extraction, the pricing, infrastructure developments that come with it, and downstream empowerment issues are going to become the key elements. Africa is not going to return to the days of a ‘closed shop’ for exclusive browsing by selected countries – it is going to become more competitive and more demanding of long-term sustainable benefit.

Intra-regional trade is likely to continue to grow, but off a low base and relatively slowly due to various harmonisation and other issues that tend to complicate African borders. Indeed, one of the key elements of future African economic growth and social development is intra-regional trade and inter-continental trade. The reality however is that limited diversification of export goods and still-low-value-add presently cap the prospects for intra-Africa trade.

Q: Which regions and which countries in Africa are able to attract the highest levels of investment, and which are seeing the best trend lines? What will investment in Africa look like in 2012 and beyond?

A: Historically, the Southern African region and North Africa have attracted most of the FDI targeted at the continent. The continent’s larger economies are situated in these two regions, and these regions will most likely continue to attract high levels of FDI for the most part. In terms of North Africa, the region has been a favoured destination for FDI over the past decade. In fact, the stock of inward FDI into the region rose by 16.2% p.a. between 2000 and 2010. This was driven mainly by pro-market economic reforms in Egypt post-2004 and a lifting of sanctions on Libya in the early-2000s. Most FDI in the region has been in the oil and gas sectors of the respective countries. By end-2010, North Africa accounted for 37.2% of Africa’s total stock of inward FDI. In general, more favourable macroeconomic environments, better infrastructure, and massive oil and gas resources made the region an attractive investment prospect. Per capita income in the region is also much higher than in SSA.

The situation changed in 2011 when the Arab Spring uprisings resulted in large outflows of capital throughout the North Africa region. More than a year later, investors have still not regained confidence in the region owing by and large to the challenging political situations. With the strong gains made by Islamist political parties across the region, investors will also employ a wait-and-see approach to see how business-friendly the new governments will be. We do however not expect major shifts to the left and in a place like Libya where the private sector was severely inhibited by the Qadhafi regime, we may actually start to see greater investor interest in non-oil sectors over the medium- to long-term. That said, the short-term outlook remains extremely uncertain; indeed, it is not even clear whether Libya will remain a single country with the east and the south having already hinted at secession.

Egypt, with its young and large population, growing middle class and strong long-term growth prospects is expected to remain a major recipient of FDI in the long-term. However, the short-term outlook is also very uncertain with presidential elections lying ahead and the country currently struggling to stave off a currency crisis. There is optimism about Morocco’s investment prospects given its stable macroeconomic environment, young and growing population, high rate of urbanisation, and business-friendly reforms in recent years. In fact, Morocco was the best reformer in the world in the latest World Bank Doing Business Index (2012). Furthermore, the country seems well-placed to be a global leader in renewable energies over the next few decades with the government hoping that solar power alone will account for 38% of Morocco’s electricity needs over the long-run (through the Desertec initiative); large amounts of electricity are also expected to be exported to Europe. Morocco – as well as Tunisia – is also attracting an increasing

16 | African Emergence

amount of FDI in the manufacturing industry. Meanwhile, Algeria, despite all its potential, will likely struggle to attract significant amounts of FDI due to a trend towards economic nationalism over the past few years.

With SSA expected to see strong growth over the next decade while North Africa still recovers from the political upheaval in 2011, we expect to see an increase in SSA’s share in total African FDI over the next decade. The degree to which this shift occurs will, to a large extent, depend on the political environments and the economic policy direction in North Africa over this period; with stable political and economic backdrops, North Africa can certainly continue being a major recipient of FDI in the long-run. Within the confines of SSA, we believe the sharpest acceleration in inward FDI will be experienced by the East and the West African regions. For one, both the East and West African regions are expected to boast with a number of the fastest growing economies in the world over the medium-term. In the West African grouping, Nigeria and Ghana stand out with excellent economic growth prospects, while in the East African selection, Tanzania, Uganda, and Ethiopia are projected to show strong expansion in coming years.

All things considered, if there is a list of countries that offer significant potential reward and should be preferred investment destinations in Africa, then those countries include Nigeria, Egypt, Kenya, Angola, South Africa, Zambia, Rwanda, and – depending on risk appetite – Zimbabwe, the DRC, Ivory Coast, and even Ethiopia are possible destinations, though the latter country perhaps presents more political risk may be apparent at first. Morocco too may be a preferred investment destination, although it has relatively high political risk. Mozambique and Ghana have also seen their investment move to a substantially higher level in recent years, and are seen as offering value to investors in certain areas. In 2010, with oil coming on stream in Ghana in that year, the country even managed to pull in higher FDI inflows than South Africa.

Q: How much has Africa started to invest in its own future? Which are the African countries that are the key investors on the continent? Which African companies are leading this drive?

A: Although interest from the West in Africa continues, and interest from Asia remains almost guaranteed, the increase in investment in Africa from within its own borders makes for the most interesting story. According to data from the United Nations Conference on Trade and Development (UNCTAD), intra-regional FDI in Africa remains limited in terms of both volumes and diversity. Nevertheless, the organisation states that there is “some evidence that intra-regional FDI is beginning to emerge in non-natural resource related industries”. In this regard, UNCTAD states that harmonisation of Africa’s regional trade agreements could help Africa move closer to its intra-regional FDI potential. UNCTAD estimates that intra-regional African FDI accounts for only 5% of the total FDI in Africa in terms of value, and 12% in terms of number of projects. Intra-regional Africa FDI offers enormous opportunities, and we believe that there is a fundamental shift taking place with African countries becoming more proactive in investing on the continent. That said, like intra-regional trade, intra-regional African investment is still taking ‘baby steps’.

In terms of intra-African investment, South Africa has played a large role, although there has been some well-founded critique that South African firms have been slow off the starting blocks in Africa, with the continent’s largest economy not using its entrepreneurial drive and its “home” advantage to its fullest extent. It is estimated that of the $554bn invested in Africa, South Africa has only contributed about 4%. Nevertheless, more than 80 Johannesburg Stock Exchange listed companies operate in Africa, and across a very diverse range of sectors: mining (Anglogold Ashanti and Goldfields), retail (Massmart, Pick ‘n Pay, Shoprite, Woolworths, Tiger Brands), telecommunications (MTN, Vodacom), and banking (Standard Bank, FNB), to name but a few. What is perhaps more interesting though are the underlying trendlines. South African direct investment in the rest of Africa has increased much more rapidly than the rate of increase in the country’s overall outward FDI since the 1990s. According to South African Reserve Bank data, whereas in the late 1990s only about 5% of South Africa’s outbound FDI was directed to Africa, by 2008, more than 20% of South Africa’s outbound FDI was targeted at the African continent.

The rise of the phoenix | 17

Although South Africa’s FDI outflows to the continent by far eclipses those of Kenya and Nigeria, these two economies are nevertheless important foreign investors in their respective regions. East Africa’s largest economy, Kenya, has for a long time seen relatively high outflows of FDI to its neighbours Uganda and Tanzania. Kenya is considered East and Central Africa’s hub for financial services, with its banking sector among the most developed in SSA. According to the World Bank, about 11 multinational and Kenyan-owned banks use Kenya as a hub to expand their operations into the East African Community (EAC). Furthermore, UNCTAD figures show that Kenya’s oil marketer KenolKobil had the second highest greenfield investment in Uganda in 2010 – worth $1.7bn in coal and gas projects. Kenya has also invested in the retail space of neigbouring countries. Nakumatt, one of the most prominent companies operating in Kenya’s retail space, is also the biggest supermarket chain in East Africa according to the Financial Times. The company has 40 outlets in Kenya, Uganda and Rwanda. Plans are also underway to open an outlet in Tanzania, while the company is embarking on a feasibility study regarding the entrance to other markets such as Burundi, Zambia, South Sudan, the DRC, Nigeria, Botswana, and Malawi. These FDI outflows from Kenya to the region are by any measure still very small, but it is believed that they will continue to show an increase over time. Increasing integration of the EAC and closer trade ties, and a combined effort from the region’s governments to invest in infrastructure and, specifically also regional infrastructure, will pave the way to higher regional trade and investment.

Similarly, another economic powerhouse, Nigeria, is an active regional investor. Africa’s second largest economy especially targets the financial services sectors of other African countries with its FDI outflows. Nigerian banks have a reputation of bringing in innovative services to neighbouring countries in West Africa, and many of the leading banks have an extensive presence throughout the region. More recently, the ambitious plans of Nigerian cement manufacturer Dangote have made headlines around the world. In April this year, the Financial Times reported that Aliko Dangote, Africa’s richest man, plans to list his multibillion dollar cement business on the London Stock Exchange next year. The reason for the listing is to finance the planned rapid expansion on the continent. Apart from Nigeria, where Dangote has three plants and 70% market share, the company has contracts to construct factories in eight other African countries.

Nevertheless, outside of South Africa, North Africa has been by far the most important source of FDI outflows from Africa since 2000. Most of these North Africa FDI outflows go to other Arab countries and Europe, but some of these flows are directed at Africa. Of the $29.4bn increase in outward FDI in Africa excluding South Africa since 2000, North Africa accounted for 69%. This in turn was due to a large increase in foreign investment by Libya and to a lesser extent by Egypt.

18 | African Emergence

Libya, mainly through its sovereign wealth fund, made significant investments outside of Libya’s borders since 2007. According to UNCTAD, outward FDI averaged $3.07bn during the 2007-10 period, most of which was made in 2007-08. Libya was also the largest foreign investor from the African continent prior to its civil war – when looking at FDI outflows from Africa, to all destinations. On average during 2007-10, Libyan FDI outflows accounted for 34% of Africa’s total FDI outflows. Much of these investments were made by the Libyan Investment Authority (LIA), a sovereign wealth fund that was established in 2006 with the goal of managing the country’s massive amount of saved oil revenues, and investing these funds in financial assets. According to the Sovereign Wealth Fund Institute, the LIA was worth $65bn at the end of 2010.

One branch of the LIA, called the Libya Africa Portfolio for Investments (LAP), specialises in investing on the African continent. In a bid to diversify its revenue base, the LAP invested in the energy, communications, and tourism sectors of various countries. According to the Sovereign Wealth Fund Institute, the LAP had $5.2bn in capital late in 2010, with significant holdings in the following companies:

• OiLibya

• Afriqiyah Airways

• Sahel-Saharan Investment and Trade Bank (BISC)

• LAP Green Network

• Libyan Arab African Investment Trade Company

• Libyan African Portfolio.

A report by Global Witness shows that the vast majority of the LIA portfolio is held in Europe and North America with roughly one-eighth of it held in emerging and other markets. As far as Africa is concerned, it seems that Libya has a notable presence in West Africa and the Sahel region (in Northern Africa).

We expect the post-Qadhafi government to review its foreign holdings. It may also decide to redirect some African investments to more developed economies, a move that has been made more likely by the nationalisation of the Libyan-owned telecommunications company Zamtel by the Zambian government. Furthermore, we expect the LIA to use its funds to restore Libya’s infrastructure after the civil war rather than investing heavily overseas. As such, outward FDI is expected to be relatively low over the medium-term. Once infrastructure has been rebuilt, there is certainly scope for the Libyan government to increase its presence in other African countries significantly over the long-term given the growth potential of African economies.

Like Libya, Algeria is another North African country with a massive amount of foreign exchange reserves, which in turn gives it the financial means to become a large investor on the continent. However, as yet, this has not been realised. The economy does not have much of a private sector, with the government – and the state-owned oil and gas giant, Sonatrach – dominating the economy. Sonatrach, in turn, is also the major foreign investor, with operations in a number of countries, including Tunisia, Mauritania and Libya. Egyptian investments abroad mostly go to Europe and other Middle East North Africa (MENA) countries. The activities of the major commercial banks in Egypt mainly focus on the domestic market only, though they are starting to expand their regional African presence. For example, the National Bank of Egypt, the largest bank in the country, expanded its reach to Sudan last year.

The rise of the phoenix | 19

Meanwhile, in the telecommunications industry, Orascom Telecom has a presence in Algeria (operating as Djezzy with a 56% market share in that country), Central African Republic (Telecel), Burundi (Leo), and Zimbabwe (Telecel: 20% market share). During 2011, there was a dip in outward FDI by Egyptian companies, possibly due to a lack of liquidity in the aftermath of the Egyptian uprising. However, this is likely to pick up once again in line with the projected recovery of the Egyptian economy.

Finally, Morocco has also become an increasingly important source of FDI for Africa, particularly in the telecoms sector. Maroc Telecom has expanded its reach to Mauritania, Burkina Faso, Gabon, and Mali. In the financial sector, Attijariwafa Bank has also been a large investor across West Africa and the Maghreb. The bank has a presence in Tunisia, Mauritania, Senegal, Mali, Burkina Faso, Ivory Coast, Republic of Congo, Gabon, and Cameroon. Meanwhile, BMCE Bank also has a large presence in Africa via its shareholding in Bank of Africa (BOA). BOA is present in 21 African countries. BMCE has also made it one of its key strategies to increase its presence in African countries further. In fact, earlier this year, its chairman stated: “We aim to cover all African countries within 10 to 15 years”. Another major bank, Banque Centrale Populaire (BCP), also has a presence in Africa, with subsidiaries in Guinea and the Central African Republic.

Q: From a company perspective, where are the key gateways to the continent situated? Which gateway should be used when investing on the continent, considering different company focuses? What would be the best strategy for entering Africa in terms of key investment and trade corridors? South Africa tends to be emotionalised as the gateway to Africa, but to what extent does this hold true? Are we seeing a change here, a shift, and if so is this shift incremental or fundamental?

A: The “gateway” to Africa idea is a little outdated. Entry into African markets depends on the nature of the investment. Practically, there is no single “gateway” to Africa no matter how much Brand South Africa may believe South Africa fulfils this need. There are now several “gateways” including South Africa, but Nigeria, Kenya, Egypt, Mauritius and others represent no less an opportunity.

Nigeria offers significant potential and it along with Angola, Kenya, perhaps Egypt at a later stage, and South Africa are and will remain the key entry points into Africa over the next decade. Ghana is a potential additional West Africa entry point, but as in all cases it is the nature of the proposed business that would play a key role in determining an entry point. Other issues such as skills base, availability and cost of labour and ease of doing business would be other considerations. Infrastructure gaps, specifically transport, communications, power generation and reliability and port congestion are also factors that are often problematic in Africa and less so elsewhere in the developing world.

There is reliable empirical evidence to suggest that in the space of a few years South Africa will no longer be the largest economy on the continent. Nigeria is expected, with several others, to close the gap. Africa is the opportunity and the gateways are many.

Q: Has the creation of trade blocs in Africa been conducive to trade - ie, have we seen any real benefit from the creation of trade blocs to trade? To what extent are the African trade blocs successful and to what extent is it only a pipe dream? Is the East African trade bloc (and others) really happening, or will it remain only a ‘long shot’? What is the overall situation around trade blocs on the continent?

A: Continental Free Trade Area a long way off

The African Union (AU) idea of a Continental Free Trade Area (CFTA) is sound in theory and essential for African growth and development, but 2017 is an unrealistic target date.

Africa is currently working – or not – to cement a number of regional FTAs with varying degrees of success and in most cases there is significant work still to be done. An FTA without a multilateral

Customs Agreement and Revenue Sharing formulae running concurrently is not particularly effective or efficient in promoting cross-border and intra-regional trade.

Several of these regional FTAs or co-operation agreements – SADC, COMESA, ECOWAS, EAC, among others, are incomplete in one way or another (institution-building

the most significant weakness) after years of talks, treaties, discussions and setbacks.

COMESA is a mix-match of countries that belong to other regional groupings at the same time, SADC is characterised by massive economic inequalities (eg, Lesotho – South Africa)

and a reluctance by member states to relinquish financial controls (a common Africa-wide issue), while the EAC is new and working through several internal issues. The combination of

these three regional groupings into a single entity is the first crucial step in the AU’s plan but, while essential in theory, in practice there are still too many issues to be resolved and a two-

year deadline is not realistic.

Part two of the AU plan is that other regional groupings – also within a very short timeframe – will follow the example of the SADC/COMESA/EAC combination treaty and join with other regional

groupings in their neighbourhood. Part three is that once we have five or six “super-regional groupings”, they will forge a new treaty to combine all into the CFTA. Although sound in theory and

essential for overall African growth, regional co-operation arrangements confront a number of key problems, many of which have yet to be resolved after years of discussion. These include:

The fact that most African states are young and reluctant to surrender any sovereignty

The economic disparities between neighbouring states, let alone distant ones, are massive

Many regimes are and are likely to remain politically unstable

Regime changes in one country could well result in demands to renegotiate agreements not yet completed by the previous regime

A continental wide FTA would require significant institution-building and policy-making capacity – precisely the issues lacking in most regional arrangements.

The list could be longer but those are the important considerations. At many levels, regional and even a continental wide FTA is desirable and ultimately beneficial to all, provided it has very strong institutions, has wide-ranging powers stripped from individual states, and most important a coherent, highly qualified and extremely effective policy-making mechanism given that it is making policy for an entire continent with significant individual inequalities.

Below is a list of current regional economic groupings including FTAs that operate with varying degrees of success, but where the average success is low:

• Economic Community of Central African States (ECCAS) – 15 member states

• Community of Sahel Saharan States (CEN-SAD) – 30 member states

• East African Community (EAC) – five member states

• Intergovernmental Authority on Development (IGAD) – seven member states

• Southern Africa Development Community (SADC) – 14 member states including suspended Madagascar

• Community of East and Southern Africa (COMESA) – 19 member states

• Economic Community of West African States (ECOWAS) – 15 member states

• Union of Arab Maghreb (UAM) – 5 member states.

Note: The total members of the above eight regional groupings is 110 – about twice the number of African states but that is because many states belong to more than one grouping. This presents opportunities for individual states to negotiate the best deal for themselves with various regional bodies.

20 | African Emergence

The rise of the phoenix | 21

SourcesAttijariwafa Bank

Banque Centrale Populaire

Bloomberg

Central Bank of Egypt

FDI Monitor

Financial Times, UK

Heritage Foundation

Global Witness

Investment Map

International Monetary Fund

International Telecommunication Union

Investment Map

Libyan Investment Authority

Maroc Telecom

NKC Independent Economists

Orascom Telecom

Organisation of Petroleum Exporting Countries

Reuters

Sonatrach

South African Reserve Bank

Sovereign Wealth Fund Institute

Trade Map

United Nations Conference on Trade and Development

US Department of State

US Energy Information Administration

World Bank

World Investment Report

22 | African Emergence

KPMG in Africa

As a High Growth Market of choice, Africa presents a number of opportunities for global investors. While the opportunities are numerous, the journey is challenging as it is a complex terrain to navigate.

KPMG has a clear commitment to serving our clients across Africa, supported by long-term investments, a clear pan-African strategy and business model (where we are globally connected while remaining locally relevant), with strong governance, and a robust African footprint. We have an in-depth geographical and sectoral knowledge of the continent, allowing us to help our clients successfully navigate their migration and growth in Africa.

Our focus is on working with our clients to filter the strategic opportunities and look to solid investment decisions.

At KPMG, we partner with our clients to take advantage of the opportunities in Africa while managing risks:

• Our forward-thinking, skilled professionals within our well-established footprint across Africa will assist you in harnessing the opportunities

• Our deep expertise and insight will help cut through the complexity of doing business in Africa to deliver informed opinions and value-adding solutions

• Our global mindset and local on-the ground knowledge and relationships is what businesses need to survive and thrive on this complex continent that is full of opportunity.

We use our global connectivity and local knowledge to assist businesses to flourish on this diverse continent. Our multi-disciplinary teams of experts boast an ideal blend of local knowledge, skills, sector specialists and international expertise to service multinational, regional and local clients — wherever they are based in Africa or the wider world.

At KPMG, we have the pan-African and in-country Strategic Corporate Intelligence to help our clients filter the strategic opportunities and focus on investment decisions particularly in the areas of greatest opportunity. We have a deep understanding of the complexities of the continent which enables us to help clients navigate the migration successfully.

At KPMG we help our clients cut through the complexity of doing business in Africa – we know the terrain, we know where to go and we know how to get there.

If you’re investing in Africa, we invite you to talk with us.

CAPE VERDE

The rise of the phoenix | 23

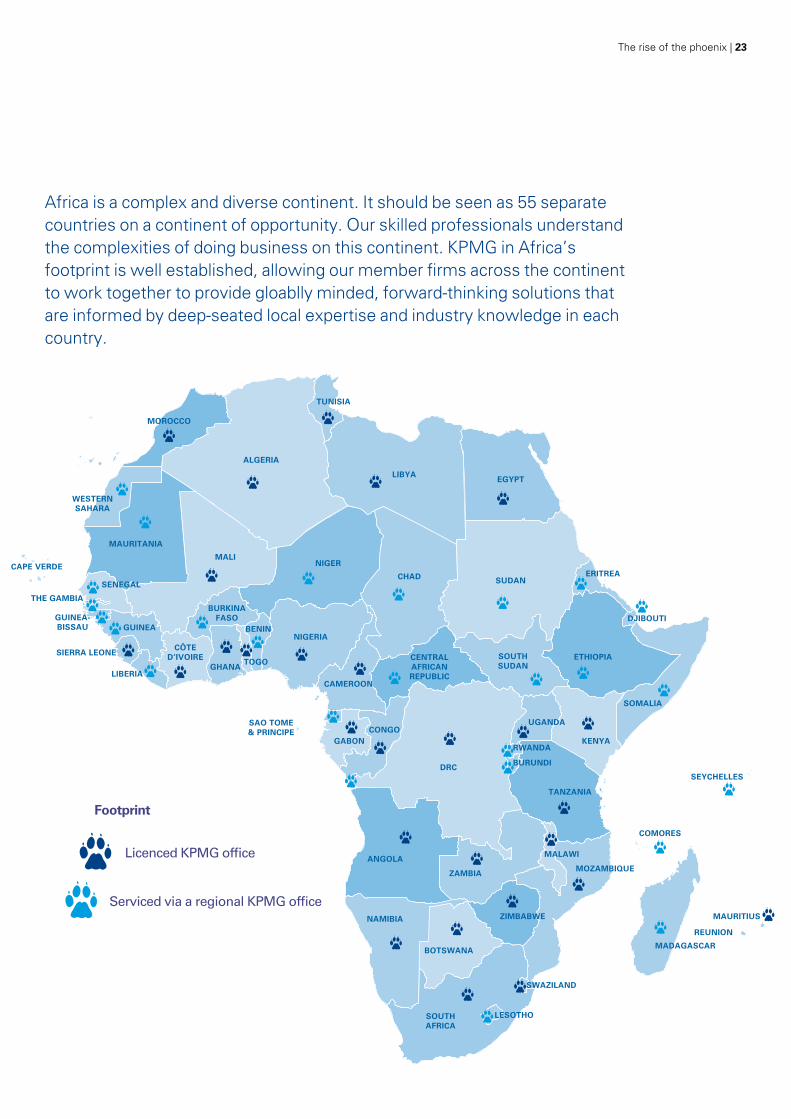

Licenced KPMG office

Footprint

Serviced via a regional KPMG office

Africa is a complex and diverse continent. It should be seen as 55 separate countries on a continent of opportunity. Our skilled professionals understand the complexities of doing business on this continent. KPMG in Africa’s footprint is well established, allowing our member firms across the continent to work together to provide gloablly minded, forward-thinking solutions that are informed by deep-seated local expertise and industry knowledge in each country.

SOUTHAFRICA

LESOTHO

SWAZILAND

MOZAMBIQUE

MADAGASCAR

NAMIBIA

BOTSWANA

ZIMBABWE

ANGOLA

ZAMBIA

MALAWI

DRC

TANZANIA

CONGOGABON

BURUNDI

RWANDA

UGANDA

KENYA

ETHIOPIA

SOMALIA

SOUTHSUDAN

SUDAN

EGYPTLIBYA

TUNISIA

ALGERIA

WESTERNSAHARA

MAURITANIA

MALINIGER

CHAD

CENTRALAFRICANREPUBLIC

CAMEROON

NIGERIABENIN

TOGOGHANA

CÔTED’IVOIRE

LIBERIA

SIERRA LEONE

GUINEAGUINEA-BISSAU

THE GAMBIA

SENEGALERITREA

BURKINAFASO

SAO TOME& PRINCIPE

REUNION

MAURITIUS

SEYCHELLES

COMORES

DJIBOUTI

CAPE VERDE

MOROCCO

24 | African Emergence

ContactsMoses Kgosana Senior Partner, KPMG Africa T: +27 11 647 8012 E: [email protected]

Yunus Suleman Chairman, KPMG Africa T: +27 11 647 6925 E: [email protected]

Tim Bashall Head of Strategy, KPMG Africa T: +27 11 647 7700 E: [email protected]

Seyi Bickersteth Senior Partner, KPMG Nigeria T: +234 12 805 984 E: [email protected]

Josphat Mwaura Senior Partner, KPMG Kenya T: +254 20 280 6000 E: [email protected]

Anthony Thunström COO, Project Africa T: +27 83 700 8862 E: [email protected]

24 | African Emergence

KPMG salutes the World Economic

Forum on driving positive change

kpmgafrica.com

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation. The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

© 2012 KPMG Services Proprietary Limited, a South African company and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. Printed in South Africa. MC8384

The opinions of the authors are not necessarily the opinions of KPMG.