Embed Size (px)

Citation preview

Affordable Care Act

ABC’s of the ACA

Transforming Healthcare: Surfing the Tsunami of Change

October 24, 2014

Donna OrbanCertified Marketplace Navigator

Learning ObjectivesExplain the Health Insurance

Marketplace from consumer perspective

Describe demographics of Marketplace consumers

Look at enrollment by the numbers

Learning ObjectivesDescribe key provisions of the

ACA. Describe the history of the

Affordable Care Act (ACA).Describe the implementation

of ACA beginning in 2009.

Marketplace ExchangeIt’s like a mall for health insurance! What does is mean for consumers?

The Health Insurance Marketplace

Easier to Buy Insurance• Insurance Exchanges allow people

to compare plans, apples to apples• Families and individuals receive tax

credit, depending upon income, to help pay for health insurance coverage

• Marketplaces offer multiple Qualified Health Plans from participating providers

• Ability to find coverage to fit your individual needs• Marketplaces provide basic

information on:• Plan premiums• Deductibles• Out-of-pocket costs

Premium Tax Credits

Must not be eligible for “affordable” job based coverage that meets Minimum Essential Coverage

Household income must be between 100% and 400% of Federal Poverty Level for household size

Expansion of State Health Insurance Programs

http://kff.org/health-reform/state-indicator/state-activity-around-expanding-medicaid-under-the-affordable-care-act

Olympics of Healthcare Coverage

The Silver plan is set up so that 70% of medical costs are covered through the provider. With cost-sharing reductions the amount listed below is what the provider and the government will pay for out-of-pocket health services:

If your income is 100-150% of the FPL, the actual coverage of a Silver plan is 94%

If your income is 150-200% of the FPL, the actual coverage of a Silver plan is 87%

If your income is 200-250% of the FPL, the actual coverage of a Silver plan is 73%

Only Silver Plan = Cost Sharing Reductions

Marketplace Enrollment & DemographicsHow many individuals have new comprehensive insurance and what do they look like?

Enrollment by the NumbersFrom Oct 1, 2014 through the extension

deadline April 19, 2015: 8,019,763 people selected Marketplace

plans More than 4.8 million additional

individuals enrolled in Medicaid and CHIP About 3.8 million people, including

nearly 1.2 million young adults (18 – 34), enrolled during the final reporting period, which began March 2 and concluded on April 19

http://aspe.hhs.gov/health/reports/2014/MarketPlaceEnrollment/Apr2014/ib_2014Apr_enrollment.pdf

Marketplace Demographics

Of the more than 8 million who enrolled in Marketplace plans:

54 % are female and 46 % are male 34% are under age 35 28 % are between the ages of 18-34 65 % selected a Silver Plan; 20% Bronze 85% selected a plan with financial

assistance

http://aspe.hhs.gov/health/reports/2014/MarketPlaceEnrollment/Apr2014/ib_2014Apr_enrollment.pdf

Marketplace Demographics 62.9 % of those reporting are white 16.7 % are African American 10.7% are Latino 7.95 are Asian 1.3% are multiracial 0.3% American Indian/Alaska Native 0.1% Native Hawaiian/Pacific Islander

http://aspe.hhs.gov/health/reports/2014/MarketPlaceEnrollment/Apr2014/ib_2014Apr_enrollment.pdf

Marketplace DemographicsTotal Oklahoma Marketplace Enrollment =

69,221 (bottom 7 states for enrollment)

70.1 % of those reporting are white 9.0 % are African American 7.5 % are Latino 6.8% are Asian 3.4 % are multiracial 3.1 % American Indian/Alaska Native 0.1% Native Hawaiian/Pacific Islander

http://quickfacts.census.gov/qfd/states/40000.html

Patient Protection and Affordable Care ActTransforming the Delivery and Business of Healthcare

Major Tenants of ACA Payment reform Quality Delivery system redesign

Who does it impact?o Everyone!

Changes that may impact familieso Financial Protectiono Easier Access to Health Insuranceo Tax Credits

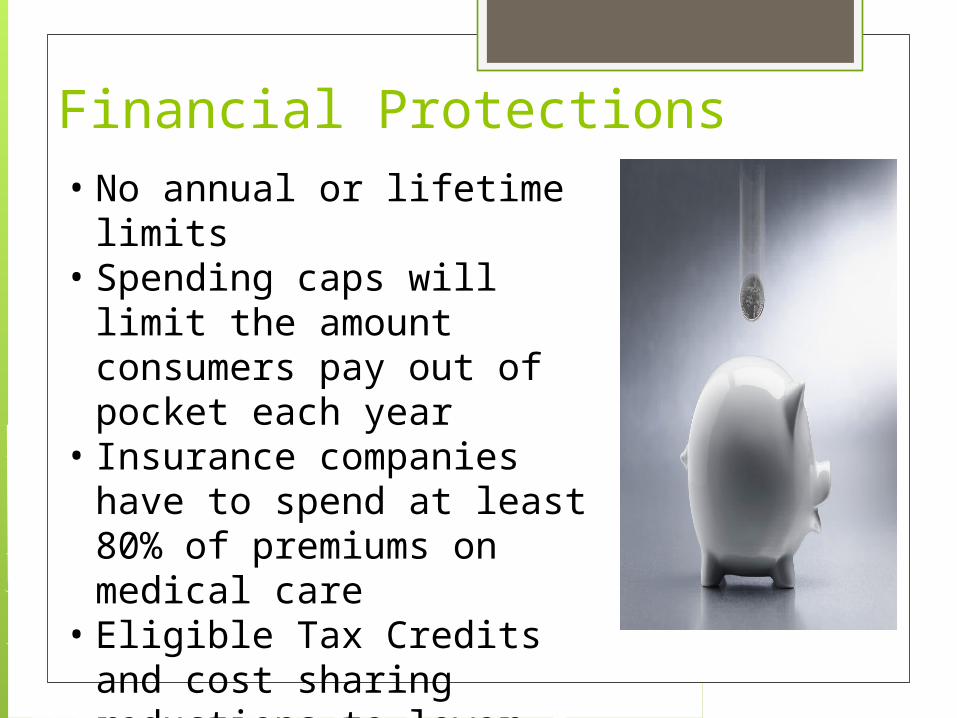

Financial Protections• No annual or lifetime

limits• Spending caps will limit

the amount consumers pay out of pocket each year

• Insurance companies have to spend at least 80% of premiums on medical care

• Eligible Tax Credits and cost sharing reductions to lower cost of healthcare

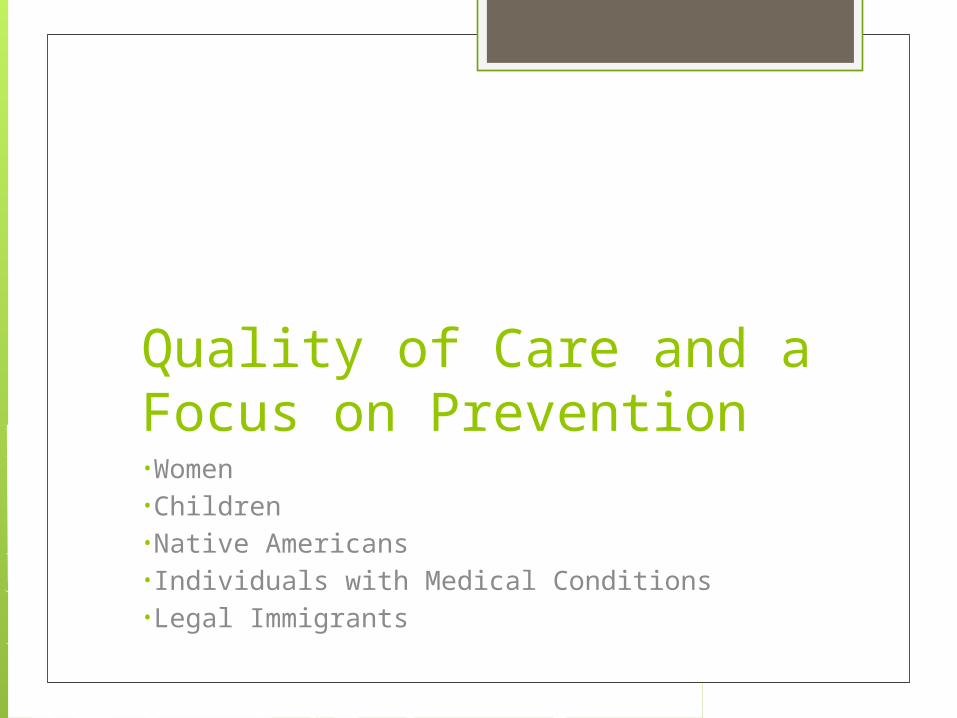

Quality of Care and a Focus on Prevention•Women•Children•Native Americans•Individuals with Medical Conditions•Legal Immigrants

Who and How the ACA helps…

Women Insurance companies can

no longer deny women insurance because of a pre-existing conditions such as: Breast or Cervical Cancer Pregnancy or C-Section Domestic Abuse

Insurers can no longer charge women more than men for the same coverage

Who and How the ACA helps…

Native Americans Permanently authorizes

the Indian Health Care Improvement Act and: Improves access to 1.9

million Native Americans served by Indian Health Services

Cost sharing reductions avail 100-300% FPL

AN/AI can enroll monthly

Who and How the ACA helps…

People with medical conditions People with a disability or

mental illness can work part-time and still qualify for Medicaid

Mental healthcare must be covered just like physical health care

Insurers cannot refuse or charge more to cover those individuals with pre-existing conditions

Who and How the ACA helps…

Chronic Health Problems No longer deny individuals

Insurance due to pre-existing conditions or for participating in a clinical trial

No yearly or lifetime limits on coverage

All Marketplace insurance plans will cover children’s vision and dental

Young adults can stay on their parents’ plan until age 26 Coverage is available even if child

is married or has own child (child and spouse are not covered)

Who and How the ACA helps…

Legal Immigrants Eligible for:

Purchasing health insurance from the State Exchange (2014) with no waiting periods

Premium tax credits, cost-sharing reductions, temporary high-risk pools, and “basic health plans” offered by a state

Reforming HealthcareHow long has the U.S. been seeking change in healthcare?

This is not a new concept…The Heritage Foundation was one of the strongest early backers of an individual mandate.The “central element in the Heritage proposal is a two-way commitment between government and citizens. Under this ‘social contract’ the federal government would agree to make it financially possible… for every American family to purchase at least a basic package of medical care including catastrophic insurance. In return, government would require, by law, every head of household acquire at least a basic health plan for his or her family.”

Historical ReviewA Presidential Overview

Franklin Roosevelt- Healthcare is a fundamental human right

Harry Truman- Single Payer Insurance System

Dwight Eisenhower- Allow small companies to pool resources to expand coverage

John F. Kennedy- Universal single payer with national health budget, no consumer cost-sharing

Richard Nixon- Minimum levels of coverage

Lyndon B. Johnson- Medicare and Medicaid Enacted

Gerald Ford- Avoidance of duplicate services

Jimmy Carter- Focus on cost containment, minimum package of benefits, new public corporation created to sell coverage

Ronald Reagan- 1st major expansion of Medicare benefits, ceiling on out-of-pocket costs

George Bush- Healthcare tax credits, purchasing pools, manage fraud and abuse in Medicare

George W. Bush- Prescription drug coverage for Medicare

Bill Clinton- Universal coverage, employer and individual mandates, managed competition

Barack Obama- Patient Protection and Affordable Care Act

Do these terms sound familiar???

human right pool resources Single Payer Universal single payer Minimum levels cost containment ceiling on out-of-pocket

costs tax credits, purchasing pools employer and individual

mandates Prescription drug coverage

By the numbers…What does our health and our healthcare cost???

Rising Healthcare Costs

Healthcare Spending

Healthcare Spending vs. Health OutcomesWe spend so much… You think we’d be healthier…

How much do you go to the Doctor???

Healthcare Spending Realities

Delivering Healthcare Services

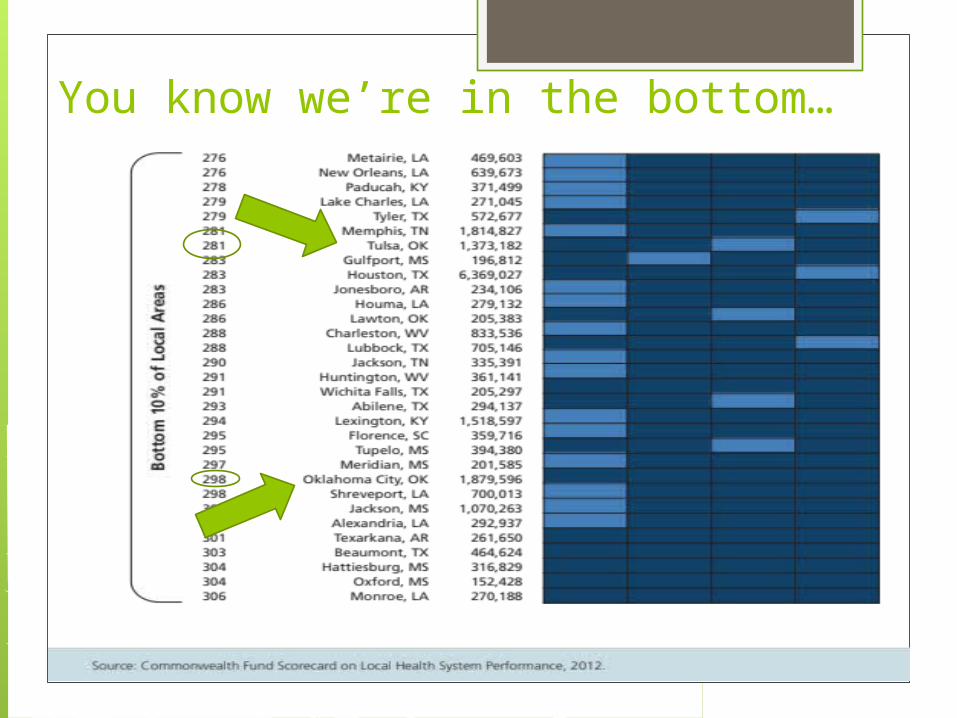

You know we’re in the bottom…

Payment ReformIndividual Financial Protections80/20 RuleMore Transparency of Healthcare Systems

More Financial Protections• Insurers must justify premium

increases• ACA limits insurance companies

overhead costs (administration and marketing)

• Allows individuals and small businesses to get better rates because they are in a bigger pool

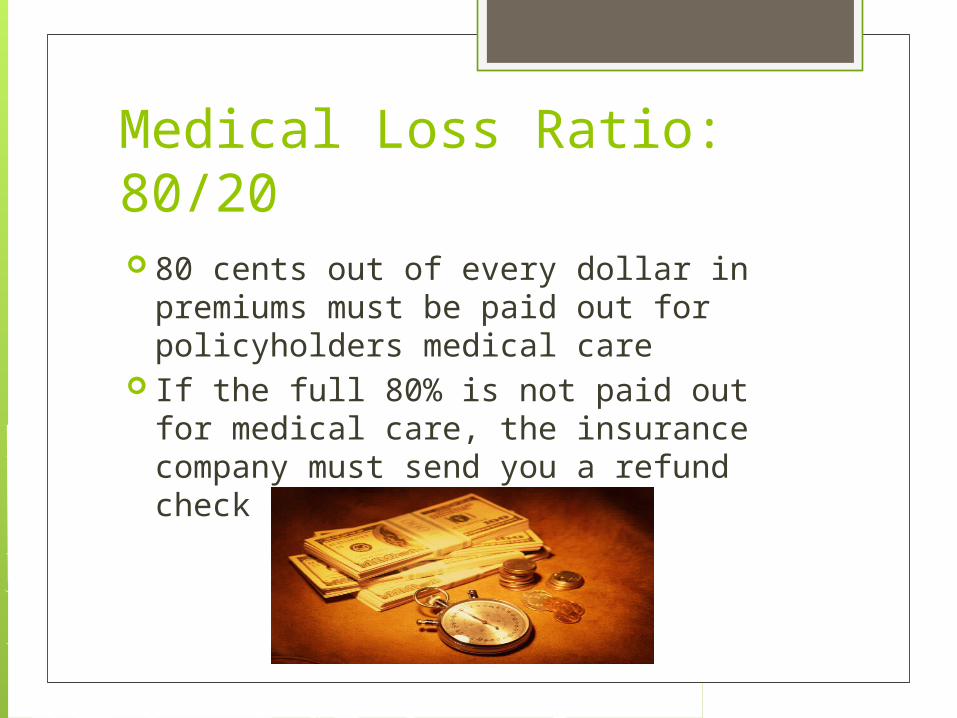

Medical Loss Ratio: 80/20 80 cents out of every dollar in premiums

must be paid out for policyholders medical care

If the full 80% is not paid out for medical care, the insurance company must send you a refund check every year

Protecting Women’s Health

Prevention and Wellness No deductibles or

copayments for preventative services

Grants for community wellness programs

National standards for restaurant nutrition labeling

Incentives for doctors to improve patient’s health

The Patient and Doctor Have Control Insurance plans will have to cover essential

services: Preventative care Hospitals Physicians Prescription Drugs Substance Abuse Dental and Vision for: Children Maternity Care

Clear appeals process if your claim is denied

Delivery System Redesign•Buying Health Insurance•Improving the Healthcare Workforce•Local Efforts for Improvement

Changing the System of Healthcare Delivery Physician Incentives for quality

coordinated care Funding for pilot projects in evidenced-

based medicine Enhanced payments for primary care

physicians and general surgeons Use of Health Informatics Expansion of State Medicaid services

Improving the Healthcare Workforce The ACA will provide loan

repayments and scholarships for students who work in underserved areas

The ACA offers grant opportunities for health programs at colleges and universities to increase the racial diversity of the healthcare workforce

Shared Responsibilities of the ACAFederal, Business, and Individual Responsibilities

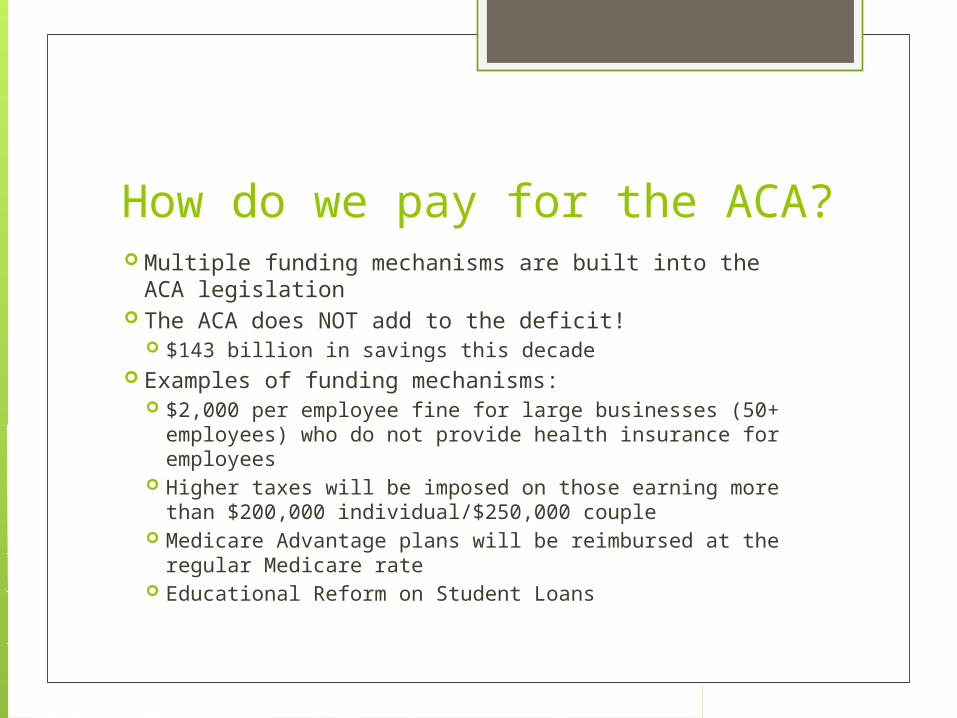

How do we pay for the ACA? Multiple funding mechanisms are built into the ACA

legislation The ACA does NOT add to the deficit!

$143 billion in savings this decade Examples of funding mechanisms:

$2,000 per employee fine for large businesses (50+ employees) who do not provide health insurance for employees

Higher taxes will be imposed on those earning more than $200,000 individual/$250,000 couple

Medicare Advantage plans will be reimbursed at the regular Medicare rate

Educational Reform on Student Loans

Federal Government Pays for 100% of Medicaid expansion

from 2014-2016 Pays for 90%-95% of Medicaid

expansion in 2017 and beyond Shares in costs of tax credits and

premium subsidies

Businesses Large employers (50+ employees) may

have to pay a penalty if they do not provide coverage AND one or more of their employees receives an insurance premium subsidy

Taxes on insurance companies that offer very high cost plans “Cadillac plans”

Fee or taxes on producers of some medical equipment and pharmaceuticals

Individuals U.S. citizens and legal residents must purchase health

insurance or pay a penalty Penalties are phased in for those who do not purchase

health insurance Exemptions granted for:

AI/AN Populations Hardship Exemptions Religious objections Those without coverage for less than 3 months Undocumented workers Incarcerated individuals Or, if the lowest cost plan exceeds 8% of income

Tax changes for some high-income individuals

Questions???For more information contact:Donna Orban, CRS [email protected]