Embed Size (px)

Citation preview

Annual Report for

31 May 2017

Advantage Asia Pacificex Japan Dividend

Advantage Asia Pacific ex Japan Dividend

TRUST DIRECTORY

Manager

AmFunds Management Berhad

9th

&10th

Floor, Bangunan AmBank Group

55 Jalan Raja Chulan

50200 Kuala Lumpur

Board of Directors

Raja Teh Maimunah Raja Abdul Aziz

Mustafa Mohd Nor

Tai Terk Lin

Sum Leng Kuang

Goh Wee Peng

Investment Committee

Sum Leng Kuang

Tai Terk Lin

Mustafa Mohd Nor

Zainal Abidin Mohd Kassim

Trustee

Deutsche Trustees Malaysia Berhad

Auditors and Reporting Accountants

Ernst & Young

Taxation Adviser

Deloitte Tax Services Sdn Bhd

Advantage Asia Pacific ex Japan Dividend

CONTENTS

1 Manager’s Report

10 Independent Auditor’s Report to the Unitholders

13 Statement of Financial Position

14 Statement of Comprehensive Income

16 Statement of Changes in Equity

17 Statement of Cash Flows

18 Notes to the Financial Statements

37 Statement by the Manager

38 Trustee’s Report

39 Directory

1

MANAGER’S REPORT

Dear Unitholders,

We are pleased to present you the Manager’s report and the audited accounts of Advantage Asia

Pacific ex Japan Dividend (formerly known as AmAdvantage Asia Pacific ex Japan Dividend)

(“Fund”) for the financial year ended 31 May 2017.

Salient Information of the Fund

Name Advantage Asia Pacific ex Japan Dividend (formerly known as AmAdvantage Asia

Pacific ex Japan Dividend) (“Fund”)

Category/

Type

Feeder Fund (Equity)/Income and Growth

Name of

Target Fund

HSBC Global Investment Funds – Asia Pacific ex Japan Equity High Dividend

Objective The Fund seeks to provide income* and Long-term** capital growth by investing in

the Target Fund which has an investment focus in Asia Pacific ex Japan equities.

Note: *Income distribution (if any) will be paid via cheque or reinvested as

additional units.

** Long term means the investment horizon should at least be five (5) years.

Duration The Fund was established on 1 August 2012 and shall exist for as long as it appears

to the Manager and the Trustee that it is in the interests of the unitholders for it to

continue. In some circumstances, the unitholders can resolve at a meeting to

terminate the Fund.

Performance

Benchmark

MSCI AC Asia Pacific ex Japan Index

(obtainable from: www.aminvest.com)

Income

Distribution

Policy

Subject to availability of income, distribution is paid at least once a year.

Breakdown

of Unit

Holdings by

Size

For the financial year under review, the size of the Fund stood at 8,620,755 units.

Size of holding As at 31 May 2017 As at 31 May 2016

No of units

held

Number of

unitholders

No of units

held

Number of

unitholders

5,000 below - - - -

5,001-10,000 - - - -

10,001-50,000 - - - -

50,001-500,000 - - - -

500,001 above 8,620,755 1 11,009,221 1

2

Fund Performance Data

Portfolio

Composition

Details of portfolio composition of the Fund for the financial years as at 31 May are

as follows:

FY

2017

%

FY

2016

%

FY

2015

%

Foreign collective investment scheme 95.94 97.78 95.68

Cash and others 4.06 2.22 4.32

Total 100.00 100.00 100.00

Note: The abovementioned percentages are calculated based on total net asset

value.

Performance

Details

Performance details of the Fund for the financial years ended 31 May are as follows:

FY

2017

FY

2016

FY

2015

Net asset value (RM)* 13,184,956 13,404,958 19,523,029

Units in circulation* 8,620,755 11,009,221 14,923,729

Net asset value per unit (RM)* 1.5294 1.2176 1.3082

Highest net asset value per unit (RM)* 1.5739 1.3544 1.3871

Lowest net asset value per unit (RM)* 1.1946 1.1328 1.1540

Benchmark performance (%) 30.78 -5.04 19.34

Total return (%)(1)

28.07 -2.25 13.04

- Capital growth (%) 25.61 -6.84 8.88

- Income distribution (%) 2.46 4.59 4.16

Gross distribution (sen per unit) 3.00 6.00 5.00

Net distribution (sen per unit) 3.00 6.00 5.00

Management expenses ratio (%)(2)

0.63 0.14 0.89

Portfolio turnover ratio (times)(3)

0.78 0.21 0.38

* Above prices and net asset value per unit are shown as ex-distribution.

Note:

(1) Total return is the actual return of the Fund for the respective financial years

computed based on the net asset value per unit and net of all fees.

(2) Management expense ratio (“MER”) is calculated based on the total fees and

expenses incurred by the Fund divided by the average fund size calculated on a

daily basis. The MER increased by 0.49% as compared to 0.14% per annum for

the financial year ended 31 May 2016 mainly due to increase in expenses.

(3) Portfolio turnover ratio (“PTR”) is calculated based on the average of the total

acquisitions and total disposals of investment securities of the Fund divided by the

average fund size calculated on a daily basis. The PTR increased by 0.57 times

(>100.0%) as compared to 0.21 times for the financial year ended 31 May 2016

mainly due to increase in investing activities.

3

Average Total Return (as at 31 May 2017)

Advantage Asia Pacific

ex Japan Dividend(a)

%

MSCI AC AP

ex-Japan(b)

%

One year 28.07 30.78

Three years 12.27 14.00

Since launch (1 August 2012) 11.61 13.75

Annual Total Return

Financial Years/Period Ended

(31 May)

Advantage Asia Pacific

ex Japan Dividend(a)

%

MSCI AC AP

ex-Japan(b)

%

2017 28.07 30.78

2016 -2.25 -5.04

2015 13.04 19.34

2014 9.41 13.11

2013(c)

9.79 11.17

(a) Source: Novagni Analytics and Advisory Sdn Bhd.

(b) MSCI AC Asia Pacific ex-Japan Index (obtainable from: www.aminvest.com)

(c) Total actual return for the financial period from 1 August 2012 (date of

commencement) to 31 May 2013.

The Fund performance is calculated based on the net asset value per unit of the Fund.

Average total return of the Fund and its benchmark for a period is computed based on

the absolute return for that period annualised over one year.

Note: Past performance is not necessarily indicative of future performance and

that unit prices and investment returns may go down, as well as up.

Fund

Performance

For the financial year under review, the Fund registered a return of 28.07%

comprising of 25.61% capital growth and 2.46% income distribution.

Thus, the Fund’s return of 28.07% has underperformed the benchmark’s return of

30.78% by 2.71%.

As compared with the financial year ended 31 May 2016, the net asset value

(“NAV”) per unit of the Fund increased by 25.61% from RM1.2176 to RM1.5294,

while units in circulation have decreased by 21.70% from 11,009,221 units to

8,620,755 units.

The line chart below shows comparison between the annual performances of

Advantage Asia Pacific ex Japan Dividend and its benchmark, MSCI AC AP ex-

Japan, for the financial period/years ended 31 May.

(Forward)

4

Note: Past performance is not necessarily indicative of future performance and

that unit prices and investment returns may go down, as well as up.

Target Fund

Performance

Fund Performance Review of the Target Fund – HSBC Global Investment

Funds – Asia Pacific ex Japan Equity High Dividend (AS) (the “Target Fund”)

Period

Return in USD

as at 31 May 2017

1 month 2.56%

3 months 6.94%

6 months 15.61%

1 year 25.24%

3 years (annualized) 2.75%

5 years (annualized) 6.90%

Since Inception (annualized) 7.12%

Launch Date: 5 November 2004

Source: HSBC Global Asset Management, data as at 31 May 2017

Past performance is not indicative of future performance

Over one year, the Target Fund progressed by +25.24% in USD terms.

December 2016

The Target Fund delivered a negative absolute return but outperformed the

benchmark in December mainly due to stock selection calls in technology and

financials. Australian and Hong Kong financials were prominent among the top

positive contributors to performance in December, benefitting from a steepening in

the yield curve. The non-holding of Chinese ecommerce giant Alibaba worked well

as it fell as a US Government statement that its site offers an unacceptable level of

fake goods. On the downside, Indiabulls Housing Finance was impacted by the

5

negative effects of demonetization. Sands China fell along with other Macau casino

stocks which were hit by new lower limits on ATM withdrawals.

January 2017

The Target Fund delivered a positive absolute return and outperformed the

benchmark in January mainly due to strong stock selection calls in India, Korea,

Taiwan and Australia. Positive sentiment around Cairn India continued. Samsung

Electronics also pushed higher along with DRAM prices, as the production of higher

spec Chinese smartphones is contributing to lower than usual DRAM inventory

levels. Bank of China (“BOC”) (Hong Kong) continued to rise as it is expected to

benefit from a steepening of the yield curve. BHP Billiton, our largest position in the

materials sector, gained on rising prices for steel and other base metals. Taiwan-listed

Delta Electronics is another beneficiary of the push for higher specification

smartphones for which it supplies various components. On the down-side, the non-

holding of Alibaba hurt as the e-commerce giant released stronger than expected

quarterly results on the back of sharp improvements in online marketing revenue.

February 2017

The Target Fund delivered a positive absolute return but underperformed the

benchmark in February due to stock selection calls in Hong Kong, China, Taiwan and

Australia. IndiaBulls Housing Finance was a strong contributor as concerns over the

negative impacts of demonetization have abated. Indonesian mining services and

heavy machinery distributor United Tractor rallied on firmer coal prices, which is a

boost to its key clients. China Construction Bank rose as earnings in the banking

sector continues to improve. On the downside, BHP Billiton was subject to some

profit taking after trading at an 18-month high in January, and was also trading lower

due to the softening in iron ore prices. HSBC was also a detractor as its quarterly

results were below expectations. Sector allocation effects were negative for

benchmark-relative performance in February. The overweight to energy and telecoms

were the key detractors, while the overweight to financials was favourable.

March 2017

The Target Fund delivered a positive absolute return and outperformed the

benchmark in March mainly due to strong stock selection calls in India, Hong Kong

and Korea. Indiabulls Housing Finance outperformed due to government

announcements to support affordable housing which should lead to improvement in

the growth outlook for housing finance companies. Cairn India continued to trade

higher in March following better than expected results in February.

Samsung Electronics rose on rising DRAM (memory) and display prices. Taiwan-

listed convenience store operator President Chain Store surged in March as an

improved product mix at its stores is driving margins higher and offsetting increases

in operating expenditure. We have recently been adding to the technology selectively

on a strong outlook for internet and hardware. We have also been finding good value

in consumer staples. These purchases are being funded from profit taking mainly in

industrials and energy. Country allocation effects were negative for benchmark-

relative performance in March mainly as a result of the overweight to New Zealand,

which lagged the broader region.

6

April 2017

The Target Fund delivered a positive absolute return and underperformed the

benchmark in April as strong stock selection calls in Taiwan, Korea and consumer

staples were offset by detracting stock selection in India, China and energy. Taiwan

technology hardware supply chain names contributed positively, reinforced by the

trend towards higher spec smartphones. Convenience store operator, President Chain

Store, also fared well as it executes it strategy to higher margin fresh foods. On the

downside, the underweight to Chinese internet and gaming names like Alibaba and

Tencent detracted as these sectors have continued to achieve strong sales momentum.

The overweight to BHP Billiton also detracted on the back of the recent weakening of

the iron ore price. Sector allocation effects were negative for benchmark-relative

performance in April, mainly owing to the overweight to telecoms which was the

worst performing sector.

May 2017

The Target Fund delivered a positive absolute return and performed in line with the

benchmark in May. Strong stock selection in Hong Kong and India was offset by

detracting selection in Korea, China and Singapore. Our holdings of Australian banks

NAB and Commonwealth detracted as the sector was hit a new Government levy

announced in the new budget. Similarly, our non-holding of Westpac and ANZ was

positive for performance. Australian supermarket operator Woolworths detracted on

more intense competitive pressures. Early childhood educational game manufacturer

VTech surged on stronger than expected results and a rise in its dividend pay-out

ratio. Bank of China (“BOC”) Hong Kong also rallied after releasing solid results.

Country allocation effects were negative for benchmark-relative performance in May

mainly due to the underweight in the Chinese internet sector, which pays out a lower

than average dividend but has been rallying lately. The portfolio remains most

overweight to Taiwan, Hong Kong, telecoms, consumer staples and energy. This is

where we are finding the best opportunities when considering attractive valuation for

the profitability on offer and the prospective dividend yield.

Source: HSBC Global Asset Management (Singapore) Limited, as at 31 May 2017

Has the Fund

achieved its

objective?

For the year under review, the fund is in line with its stated objective to provide

income and long-term capital growth by investing in the Target Fund which has an

investment focus in Asia Pacific ex Japan equities.

Strategies

and Policies

Employed

Strategies and Policies of the Target Fund

The Target Fund seeks long-term capital growth and a high level of income by

investing primarily in a diversified portfolio of investments in equity and equity

equivalent securities of companies which have their registered office in and with an

official listing on a major stock exchange or other Regulated Market of any Asia

Pacific country (excluding Japan) as well as companies which carry out a

preponderant part of their economic activities in the Asia Pacific region (excluding

Japan), that offer short-term sustainable dividend yields above the market average

and/or the potential for dividend growth above the market average over the short-

term. As the sub-fund will seek to invest in companies throughout the Asia Pacific

region (excluding Japan), these can be both companies with a registered office in, and

with an official listing in developed markets, and also those in emerging Asian

countries.

7

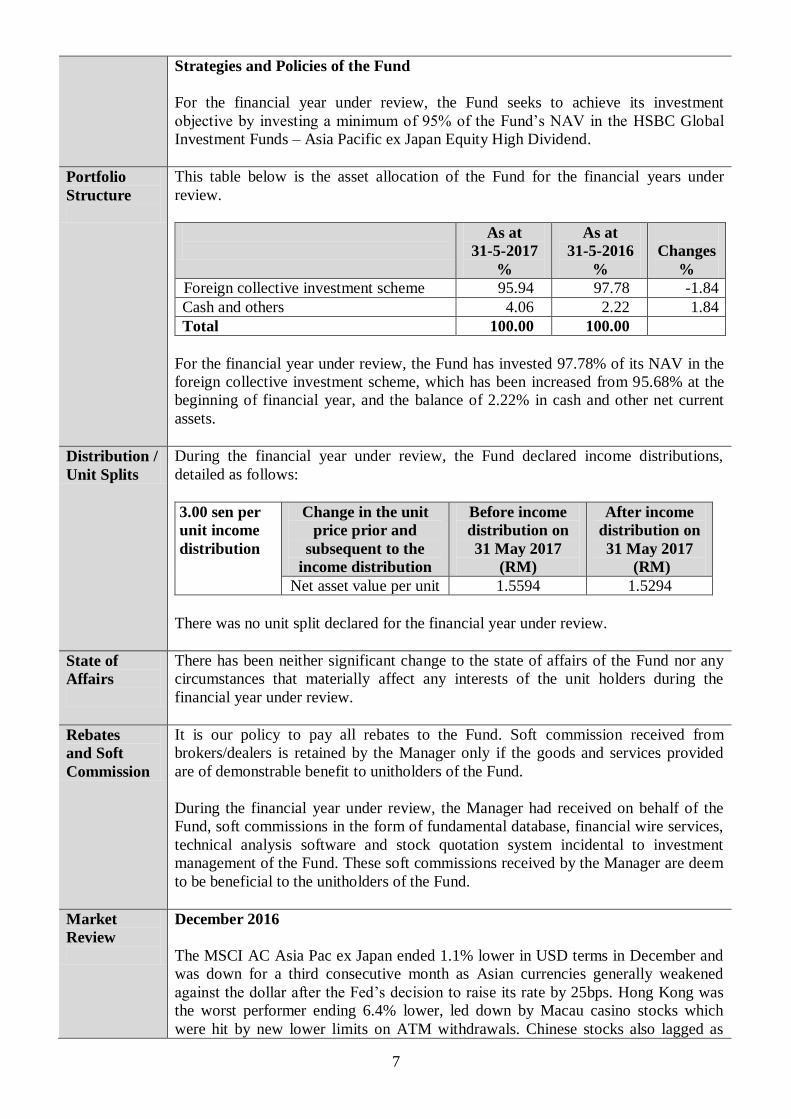

Strategies and Policies of the Fund

For the financial year under review, the Fund seeks to achieve its investment

objective by investing a minimum of 95% of the Fund’s NAV in the HSBC Global

Investment Funds – Asia Pacific ex Japan Equity High Dividend.

Portfolio

Structure

This table below is the asset allocation of the Fund for the financial years under

review.

As at

31-5-2017

%

As at

31-5-2016

%

Changes

%

Foreign collective investment scheme 95.94 97.78 -1.84

Cash and others 4.06 2.22 1.84

Total 100.00 100.00

For the financial year under review, the Fund has invested 97.78% of its NAV in the

foreign collective investment scheme, which has been increased from 95.68% at the

beginning of financial year, and the balance of 2.22% in cash and other net current

assets.

Distribution /

Unit Splits

During the financial year under review, the Fund declared income distributions,

detailed as follows:

3.00 sen per

unit income

distribution

Change in the unit

price prior and

subsequent to the

income distribution

Before income

distribution on

31 May 2017

(RM)

After income

distribution on

31 May 2017

(RM)

Net asset value per unit 1.5594 1.5294

There was no unit split declared for the financial year under review.

State of

Affairs

There has been neither significant change to the state of affairs of the Fund nor any

circumstances that materially affect any interests of the unit holders during the

financial year under review.

Rebates

and Soft

Commission

It is our policy to pay all rebates to the Fund. Soft commission received from

brokers/dealers is retained by the Manager only if the goods and services provided

are of demonstrable benefit to unitholders of the Fund.

During the financial year under review, the Manager had received on behalf of the

Fund, soft commissions in the form of fundamental database, financial wire services,

technical analysis software and stock quotation system incidental to investment

management of the Fund. These soft commissions received by the Manager are deem

to be beneficial to the unitholders of the Fund.

Market

Review

December 2016

The MSCI AC Asia Pac ex Japan ended 1.1% lower in USD terms in December and

was down for a third consecutive month as Asian currencies generally weakened

against the dollar after the Fed’s decision to raise its rate by 25bps. Hong Kong was

the worst performer ending 6.4% lower, led down by Macau casino stocks which

were hit by new lower limits on ATM withdrawals. Chinese stocks also lagged as

8

tighter liquidity conditions prevailed after a bond yields rose, while the real estate

sector fared badly on softening residential sales data. Indonesia was the best

performing market (up 5.4% in USD terms), rising sharply near month end as Fitch

revised its credit outlook to positive. Against the trend of other currencies, the Rupiah

was firmer against USD. Australia also fared well as its banks and resource stocks

have continued to rally since the US election results. India had a volatile month,

finally ending down slightly. This reflected the muddled impact of its

demonetization, where consumption and manufacturing have been hit and bank rates

have dropped on tepid loan growth. Despite the impeachment of President Park over

corruption, the Korean market still ended the month higher.

January 2017

The MSCI AC Asia Pac ex Japan started the year on a strong note, ending January

5.8% higher in USD terms, with all countries and sectors finishing in positive

territory in USD terms. Continuing the trend from H2 2016, cyclicals generally

outperformed defensive sectors indicating risk appetite was still strong. Hong Kong

and Chinese stocks were buoyed better than expected. Q4 Gross Domestic Product

(“GDP”) and a gradual easing of the liquidity squeeze that occurred in December.

Korea was also a solid performer reflecting the appreciation of the Won as foreign

investments rose following the upbeat guidance from Samsung Electronics, which

comprises 21% of the KOSPI index market cap. India added 4.3% in January with the

Goods and Services Tax scheduled to be rolled out from July following the resolution

of pending issues. Taiwan added 5.0% as the tech sector surged.

February 2017

The MSCI AC Asia Pacific ex Japan continued its strong start to the year in February

rising 3.4% in USD terms in February. All Asian markets ended the month higher,

except the Philippines. India was the best performing market gaining 6% in February

led by a credible Union Budget, corporate action by some index heavyweights, and

receding concerns about growth due to demonetization. Taiwan was 4% higher, led

by Apple supply chain names. The Philippines declined 1.3% in USD terms in part

due to a weaker Peso, rising inflation, political noise and a mixed earnings season.

March 2017

The MSCI AC Asia Pac ex Japan added another 3.1% in USD terms in March. All

Asia Pac ex Japan markets ended the month higher, except New Zealand. India was

the best performing market for a second consecutive month gaining 6% as confidence

was boosted by the success of the incumbent government Bharatiya Janata Party

(“BJP”) in the Uttar Pradesh state elections and the encouraging progress on the

passage of GST legislation. Korea shrugged off geopolitical concerns of its region

and performed strongly on the back of rises in the IT and telecom sectors. Upgrades

in semiconductor and display demand and prices helped in particular. Indonesia’s

Jakarta Composite Index reached an all-time high in March as foreign investors

became net buyers of the market after heavy outflows in the previous 6 months. The

Asian region more broadly continues to be buoyed by solid economic data from

China as well.

April 2017

The MSCI AC Asia Pac ex Japan continued its year to date surge adding another

1.6% in USD terms in April. All countries recorded positive absolute returns in USD

terms, except Australia partly due to the AUD weakening 2% vs USD. The

9

Philippines, Malaysia and Indonesia were the top performing markets. Earnings

expectations and positive sentiment around tax reforms led the rally in the

Philippines. All three markets witnessed significant positive foreign flows. China also

fared well with stronger Q1 2017 nominal GDP data, improving profitability in the

industrial sector and easing fears of capital outflow CNY depreciation. The Indian

market was buoyed by strong domestic flows and also encouraging forecasts for the

upcoming monsoon season. Sector-wise, technology was the standout largely due to a

strong showing from Chinese and Korean tech hardware names.

May 2017

The MSCI AC Asia Pac ex Japan continued its unbroken run for 2017, rising 2.7% in

USD terms (up 18% year to date). All countries except Australia recorded positive

absolute returns in USD terms, with Korea and China being the top performing

markets. In South Korea, President Moon Jae-in was elected and earnings revision

continues to be positive. China was buoyed by a few factors including reassurance

from the People’s Bank of China (“PBOC”) that efforts reduce leverage in the

economy should not destabilize it. A stronger Yuan Renminbi (“RMB”) and robust

southbound flows on the stock connect also helped. The market seemed to shrug off

Moody’s downgrade of China’s sovereign rating. Singapore was boosted by its

financials as investors are positive on higher rates benefitting the banks margins.

Philippines continued its run up led by outperformance of the property sector. India

stayed also positive due to generally positive corporate earnings and a continuation of

the reform agenda. Australian banks were hit hard after the Government introduced a

new levy on banks as part of its latest budget.

Source: HSBC Global Asset Management (Singapore) Limited, as at 31 May 2017

Market

Outlook

Asian economies stand to benefit from the synchronized pickup in global economic

growth. While there is still uncertainty around issues like potential trade barriers, we

expect earnings growth to remain strong against the backdrop of a stronger global

economy. Prospects for a continued re-rating of Asian equity markets remain

positive. Key risks are local currency volatility and a more aggressive rate hike cycle

in the US. Macro indicators suggest a stable Chinese economy which continues to

grow at a solid pace. There are potential positive catalysts on the horizon around

ongoing economic and structural reforms which should help support economic

growth. In India, the Government’s reform agenda is incrementally adding to the

country’s growth potential and attractiveness as a destination for capital. The ongoing

recovery in the economy and improving earnings growth prospects will be key

catalysts going forward. With subsiding macro concerns around Korea, we should see

capital returning to the market, while Taiwan continues to benefit from the strong

tech cycle. ASEAN’s steady growth momentum should support ongoing interest in

these markets. Valuations in Asia Pac ex Japan remain attractive on a price-to-book

basis.

Source: HSBC Global Asset Management (Singapore) Limited, as at 31 May 2017

Kuala Lumpur, Malaysia

AmFunds Management Berhad

7 July 2017

Independent auditors’ report to the unitholders of

Advantage Asia Pacific ex Japan Dividend

(formerly known as AmAdvantage Asia Pacific ex Japan Dividend)

Report on the audit of the financial statements

Opinion

Basis for opinion

Independence and other ethical responsibilities

Information other than the financial statements and auditors’ report thereon

Our opinion on the financial statements of the Fund does not cover the other information

and we do not express any form of assurance conclusion thereon.

In connection with our audit of the financial statements of the Fund, our responsibility is

to read the other information and, in doing so, consider whether the other information is

materially inconsistent with the financial statements of the Fund or our knowledge

obtained in the audit or otherwise appears to be materially misstated.

We have audited the financial statements of Advantage Asia Pacific ex Japan Dividend

(formerly known as AmAdvantage Asia Pacific ex Japan Dividend) (“the Fund”), which

comprise the statement of financial position as at 31 May 2017, the statement of

comprehensive income, statement of changes in equity and statement of cash flows for

the year ended, and notes to the financial statements, including a summary of significant

acounting policies, as set out on pages 13 to 36.

In our opinion, the accompanying financial statements give a true and fair view of the

financial position of the Fund as at 31 May 2017, and of its financial performance and its

cash flows for the year then ended in accordance with Malaysian Financial Reporting

Standards and International Financial Reporting Standards.

We conducted our audit in accordance with approved standards on auditing in Malaysia

and International Standards on Auditing. Our responsibilities under those standards are

further described in the Auditor’s Responsibilities for the Audit of the Financial

Statements section of our report. We believe that the audit evidence we have obtained is

sufficient and appropriate to provide a basis for our opinion.

We are independent of the Fund in accordance with the By-Laws (on Professional Ethics,

Conduct and Practice) of the Malaysian Institute of Accountants (“By-Laws”) and the

International Ethics Standards Board for Accountants’ Code of Ethics for Professional

Accountants (“IESBA Code”), and we have fulfilled our other ethical responsibilities in

accordance with the By-Laws and the IESBA Code.

The Manager is responsible for the other information. The other information comprises

information in the Annual Report, but does not include the financial statements of the

Fund and our auditors’ report thereon.

10

Independent auditors’ report to the unitholders of

Advantage Asia Pacific ex Japan Dividend

(formerly known as AmAdvantage Asia Pacific ex Japan Dividend) (cont’d.)

Responsibilities of the Manager and the Trustees for the financial statements

Auditor’s responsibilities for the audit of the financial statements

As part of an audit in accordance with the approved standards on auditing in Malaysia

and International Standards on Auditing, we exercise professional judgment and maintain

professional skepticism throughout the planning and performance of the audit. We also:

Identify and assess the risks of material misstatement of the financial statements

of the Fund, whether due to fraud or error, design and perform audit procedures

responsive to those risks, and obtain audit evidence that is sufficient and

appropriate to provide a basis for our opinion. The risk of not detecting a material

misstatement resulting from fraud is higher than for one resulting from error, as

fraud may involve collusion, forgery, intentional omissions, misrepresentations,

or the override of internal control.

Obtain an understanding of internal control relevant to the audit in order to design

audit procedures that are appropriate in the circumstances, but not for the purpose

of expressing an opinion on the effectiveness of the Fund’s internal control.

The Trustee is responsible for ensuring that the Manager maintains proper accounting

and other records as are necessary to enable true and fair presentation of these financial

statements.

Our objectives are to obtain reasonable assurance about whether the financial statements

of the Fund, as a whole are free from material misstatement, whether due to fraud or

error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a

high level of assurance, but is not a guarantee that an audit conducted in accordance

approved standards on auditing in Malaysia and International Standards on Auditing will

always detect a material misstatement when it exists. Misstatements can arise from fraud

or error and are considered material if, individually or in the aggregate, they could

reasonably be expected to influence the economic decisions of users taken on the basis of

these financial statements.

The Manager is responsible for the preparation of the financial statements of the Fund

that give a true and fair view in accordance with Malaysian Financial Reporting

Standards and International Financial Reporting Standards. The Manager is also

responsible for such internal control as the Manager determines is necessary to enable the

preparation of financial statements of the Fund that are free from material misstatement,

whether due to fraud or error.

If based on the work we have performed, we conclude that there is a material

misstatement of this other information, we are required to report that fact. We have

nothing to report in this regard.

11

Independent auditors’ report to the unitholders of

Advantage Asia Pacific ex Japan Dividend

(formerly known as AmAdvantage Asia Pacific ex Japan Dividend) (cont’d.)

Other matters

Ernst & Young Wan Daneena Liza Bt Wan Abdul Rahman

AF: 0039 No. 2978/03/18(J)

Chartered Accountants Chartered Accountant

Kuala Lumpur, Malaysia

7 July 2017

Evaluate the overall presentation, structure and content of the financial statements

of the Fund, including the disclosures, and whether the financial statements of the

Fund represent the underlying transactions and events in a manner that achieves

fair presentation.

We communicate with the Manager regarding, among other matters, the planned scope

and timing of the audit and significant audit findings, including any significant

deficiencies in internal control that we identify during our audit.

This report is made solely to the unitholders of the Fund, as a body, and for no other

purpose. We do not assume responsibility to any other person for the content of this

report.

Evaluate the appropriateness of accounting policies used and the reasonableness

of accounting estimates and related disclosures made by the Manager.

Conclude on the appropriateness of the Manager’s use of the going concern basis

of accounting and, based on the audit evidence obtained, whether a material

uncertainty exists related to events or conditions that may cast significant doubt

on the Fund’s ability to continue as a going concern. If we conclude that a

material uncertainty exists, we are required to draw attention in our auditors’

report to the related disclosures in the financial statements or, if such disclosures

are inadequate, to modify our opinion. Our conclusions are based on the audit

evidence obtained up to the date of our auditors’ report. However, future events or

conditions may cause the Fund to cease to continue as a going concern.

12

Advantage Asia Pacific ex Japan Dividend

(formerly known as AmAdvantage Asia Pacific ex Japan Dividend)

STATEMENT OF FINANCIAL POSITION

AS AT 31 MAY 2017

2017 2016

Note RM RM

ASSETS

Investment 4 12,649,239 13,107,221

Deposits with financial institutions 5 462,144 333,831

Amount due from Manager 6 341,541 -

Cash at banks 480,203 2,757

TOTAL ASSETS 13,933,127 13,443,809

LIABILITIES

Amount due to Manager 6 - 28,191

Amount due to Target Fund Manager 7 477,331 -

Amount due to Trustee 8 904 875

Distribution to be reinvested 258,623 -

Sundry payables and accrued expenses 11,313 9,785

TOTAL LIABILITIES 748,171 38,851

EQUITY

Unitholders’ capital 11(a) 8,659,493 11,087,246

Retained earnings 11(b)(c) 4,525,463 2,317,712

TOTAL EQUITY 11 13,184,956 13,404,958

TOTAL EQUITY AND LIABILITIES 13,933,127 13,443,809

UNITS IN CIRCULATION 11 8,620,755 11,009,221

NET ASSET VALUE PER UNIT

− EX DISTRIBUTION 152.94 sen 121.76 sen

The accompanying notes form an integral part of the financial statements.

13

Advantage Asia Pacific ex Japan Dividend

(formerly known as AmAdvantage Asia Pacific ex Japan Dividend)

STATEMENT OF COMPREHENSIVE INCOME

FOR THE FINANCIAL YEAR ENDED 31 MAY 2017

2017 2016

Note RM RM

INVESTMENT INCOME/(LOSS)

Distribution income 195,688 443,990

Interest income 7,997 16,175

Net gain/(loss) from investment:

− Financial assets at fair value through profit or

loss (“FVTPL”) 9 2,325,654 (956,589)

Other unrealised foreign exchange loss (223) -

Gross Income/(Loss) 2,529,116 (496,424)

EXPENDITURE

Manager’s fee − current financial year 6 (34,789) (56,910)

Manager’s fee − over provision in prior financial year 6 - 60,173

Trustee’s fee 8 (10,000) (10,479)

Auditors’ remuneration (6,000) (6,000)

Tax agent’s fee (3,500) (3,500)

Custodian’s fee (50) -

Other expenses 10 (8,403) (5,625)

Total Expenditure (62,742) (22,341)

NET INCOME/(LOSS) BEFORE TAX 2,466,374 (518,765)

LESS: INCOME TAX 13 - -

NET INCOME/(LOSS) AFTER TAX 2,466,374 (518,765)

OTHER COMPREHENSIVE INCOME - -

TOTAL COMPREHENSIVE INCOME/(LOSS) FOR THE

FINANCIAL YEAR 2,466,374 (518,765)

Total comprehensive income/(loss) comprises the following:

Realised income 1,695,334 1,071,271

Unrealised gain/(loss) 771,040 (1,590,036)

2,466,374 (518,765)

14

Advantage Asia Pacific ex Japan Dividend

(formerly known as AmAdvantage Asia Pacific ex Japan Dividend) (cont’d.)

STATEMENT OF COMPREHENSIVE INCOME

FOR THE FINANCIAL YEAR ENDED 31 MAY 2017

2017 2016

Note RM RM

Distributions for the financial year:

Gross/net distributions 14 258,623 630,135

Gross/net distributions per unit (sen) 14 3.00 6.00

The accompanying notes form an integral part of the financial statements.

15

Advantage Asia Pacific ex Japan Dividend

(formerly known as AmAdvantage Asia Pacific ex Japan Dividend)

STATEMENT OF CHANGES IN EQUITY

FOR THE FINANCIAL YEAR ENDED 31 MAY 2017

Unitholders’ Retained Total

capital earnings equity

Note RM RM RM

At 1 June 2015 16,056,417 3,466,612 19,523,029

Total comprehensive loss for

the financial year - (518,765) (518,765)

Creation of units 11(a) 1,817,701 - 1,817,701

Reinvestment of distribution 11(a),14 630,135 - 630,135

Cancellation of units 11(a) (7,417,007) - (7,417,007)

Distribution 14 - (630,135) (630,135)

Balance at 31 May 2016 11,087,246 2,317,712 13,404,958

At 1 June 2016 11,087,246 2,317,712 13,404,958

Total comprehensive income for

the financial year - 2,466,374 2,466,374

Creation of units 11(a) 8,006,643 - 8,006,643

Cancellation of units 11(a) (10,434,396) - (10,434,396)

Distribution 14 - (258,623) (258,623)

Balance at 31 May 2017 8,659,493 4,525,463 13,184,956

The accompanying notes form an integral part of the financial statements.

16

Advantage Asia Pacific ex Japan Dividend

(formerly known as AmAdvantage Asia Pacific ex Japan Dividend)

STATEMENT OF CASH FLOWS

FOR THE FINANCIAL YEAR ENDED 31 MAY 2017

2017 2016

Note RM RM

CASH FLOWS FROM OPERATING AND

INVESTING ACTIVITIES

Proceeds from sale of investment 9,193,392 5,697,197

Distributions received 195,688 443,990

Interest received 7,997 16,175

Manager’s fee paid (34,296) (20,559)

Trustee’s fee paid (9,971) (10,582)

Tax agent’s fee paid (3,290) (3,500)

Custodian’s fee paid (50) -

Payments for other expenses (13,084) (13,059)

Purchase of investment (5,932,649) (1,082,000)

Net cash generated from operating and

investing activities 3,403,737 5,027,662

CASH FLOWS FROM FINANCING ACTIVITIES

Proceeds from creation of units 7,660,739 1,817,701

Payments for cancellation of units (10,458,717) (7,677,744)

Net cash used in infinancing activities (2,797,978) (5,860,043)

NET INCREASE/(DECREASE) IN CASH AND

CASH EQUIVALENTS 605,759 (832,381)

CASH AND CASH EQUIVALENTS AT

BEGINNING OF FINANCIAL YEAR 336,588 1,168,969

CASH AND CASH EQUIVALENTS AT

END OF FINANCIAL YEAR 942,347 336,588

Cash and cash equivalents comprise:

Deposits with financial institutions 5 462,144 333,831

Cash at banks 480,203 2,757

942,347 336,588

The accompanying notes form an integral part of the financial statements.

17

Advantage Asia Pacific ex Japan Dividend

(formerly known as AmAdvantage Asia Pacific ex Japan Dividend)

NOTES TO THE FINANCIAL STATEMENTS

1. GENERAL INFORMATION

2. BASIS OF PREPARATION OF FINANCIAL STATEMENTS

Standards effective during the financial year

Standards issued but not yet effective

Effective for

financial periods

beginning on or after

MFRS 9: Financial Instruments

MFRS 15: Revenue From Contracts With Customers

Advantage Asia Pacific ex Japan Dividend (“the Fund”) was established pursuant to a Deed dated

16 April 2012 as amended by Deeds Supplemental thereto (“the Deed”), between AmFunds

Management Berhad as the Manager, Deutsche Trustees Malaysia Berhad as the Trustee and all

unitholders. By a supplemental Deed dated 23 October 2015, the Fund has changed its name from

AmAdvantage Asia Pacific ex Japan Dividend to Advantage Asia Pacific ex Japan Dividend.

The Fund was set up with the objective to provide income and long term capital growth by

investing in the HSBC Global Investment Funds – Asia Pacific ex Japan Equity High Dividend

(“Target Fund”) which has an investment focus on Asia Pacific ex-Japan equities. Being a feeder

fund, a minimum of 95% of the Fund’s net asset value will be invested in the Target Fund, which

is a separate unit trust fund managed by HSBC Investment Funds (Luxembourg) S.A. (“Target

Fund Manager”). As provided in the Deed, the “accrual period” or financial year shall end on 31

May and the units in the Fund were first offered for sale on 1 August 2012.

The financial statements of the Fund have been prepared in accordance with Malaysian Financial

Reporting Standards (“MFRS”) as issued by the Malaysian Accounting Standards Board

(“MASB”) and are in compliance with International Financial Reporting Standards.

The financial statements of the Fund have been prepared under the historical cost convention,

unless otherwise stated in the accounting policies.

The adoption of MFRS which have been effective during the financial year did not have any

material financial impact to the financial statements.

As at the date of authorisation of these financial statements, the following Standards, which are

relevant to the Fund, have been issued by MASB but are not yet effective and have not been

adopted by the Fund.

1 January 2018

1 January 2018

18

MFRS 9 Financial Instruments

3. SIGNIFICANT ACCOUNTING POLICIES

Income recognition

Income tax

Functional and presentation currency

Foreign currency conversion

Income is recognised to the extent that it is probable that the economic benefits will flow to the

Fund and the income can be reliably measured. Income is measured at the fair value of

consideration received or receivable.

Distribution income is recognised when the Fund’s right to receive payment is established.

Interest income on short-term deposits is recognised on an accrual basis using the effective

interest method.

Current taxes are recognised in profit or loss except to the extent that the tax relates to items

recognised outside profit or loss, either in other comprehensive income or directly in equity.

Transactions in currencies other than the Fund’s functional currency (foreign currencies) are

recorded in the functional currency using exchange rates prevailing at the transaction dates. At

each reporting date, foreign currency monetary items are translated into Ringgit Malaysia at

exchange rates ruling at the reporting date. All exchange gains or losses are recognised in profit or

loss.

Functional currency is the currency of the primary economic environment in which the Fund

operates that most faithfully represents the economic effects of the underlying transactions. The

functional currency of the Fund is Ringgit Malaysia which reflects the currency in which the Fund

competes for funds, issues and redeems units. The Fund has also adopted Ringgit Malaysia as its

presentation currency.

MFRS 9 reflects International Accounting Standards Board’s (“IASB”) work on the replacement

of MFRS 139 Financial Instruments: Recognition and Measurement (“MFRS 139”). MFRS 9 will

be effective for financial year beginning on or after 1 January 2018. The Fund is in the process of

quantifying the impact of the first adoption of MFRS 9.

The Fund plans to adopt the above pronouncements when they become effective in the respective

financial periods. These pronouncements are expected to have no significant impact to the

financial statements of the Fund upon their initial application except as described below:

Current tax assets and liabilities are measured at the amount expected to be recovered from or

paid to the tax authorities. The tax rates and tax laws used to compute the amount are those that

are enacted or substantively enacted at the reporting date.

19

Statement of cash flows

Distribution

Unitholders’ capital

Financial assets

(i) Financial assets at FVTPL

The Fund adopts the direct method in the preparation of the statement of cash flows.

Cash equivalents are short-term, highly liquid investment that is readily convertible to cash with

insignificant risk of changes in value.

Distributions are at the discretion of the Fund. A distribution to the Fund’s unitholders is

accounted for as a deduction from realised reserve. A proposed distribution is recognised as a

liability in the period in which it is approved.

Subsequent to initial recognition, financial assets at FVTPL are measured at fair value.

Changes in the fair value of those financial instruments are recorded in ‘Net gain or loss on

financial assets at fair value through profit or loss’. Distribution revenue and interest earned

elements of such instruments are recorded separately in ‘Distribution income’ and ‘Interest

income’ respectively. Exchange differences, if any, on financial assets at FVTPL are not

recognised separately in profit or loss but are included in net gains or net losses on changes in

fair value of financial assets at FVTPL.

The unitholders’ capital of the Fund meets the definition of puttable instruments and is classified

as equity instruments under MFRS 132 Financial Instruments: Presentation (“MFRS 132”).

Financial assets are classified as financial assets at FVTPL if they are held for trading or are

designated as such upon initial recognition. Financial assets held for trading by the Fund

include foreign collective investment scheme acquired principally for the purpose of selling in

the near term.

The Fund determines the classification of its financial assets at initial recognition, and the

categories applicable to the Fund include financial assets at fair value through profit or loss

(“FVTPL”) and loans and receivables.

Financial assets are recognised in the statement of financial position when, and only when, the

Fund becomes a party to the contractual provisions of the financial instrument.

When financial assets are recognised initially, they are measured at fair value, plus, in the case of

financial assets not at fair value through profit or loss, directly attributable transaction costs.

20

(ii) Loans and receivables

Impairment of financial assets

(i) Loans and receivables carried at amortised cost

Financial liabilities

For investment in foreign collective investment scheme, fair value is determined based on the

closing net asset value per unit of the foreign collective investment scheme. The difference

between the cost and fair value is treated as unrealised gain or loss and is recognised in profit

or loss. Unrealised gains or losses recognised in profit or loss are not distributable in nature.

Financial assets with fixed or determinable payments that are not quoted in an active market

are classified as loans and receivables.

The carrying amount of the financial asset is reduced through the use of an allowance

account. When loans and receivables become uncollectible, they are written off against the

allowance account.

Financial liabilities are classified according to the substance of the contractual arrangements

entered into and the definitions of a financial liability.

On disposal of investment, the net realised gain or loss on disposal is measured as the

difference between the net disposal proceeds and the carrying amount of the investment. The

net realised gain or loss is recognised in profit or loss.

If in a subsequent period, the amount of the impairment loss decreases and the decrease can

be related objectively to an event occurring after the impairment was recognised, the

previously recognised impairment loss is reversed to the extent that the carrying amount of

the asset does not exceed its amortised cost at the reversal date. The amount of reversal is

recognised in profit or loss.

The Fund assesses at each reporting date whether there is any objective evidence that a financial

asset is impaired.

To determine whether there is objective evidence that an impairment loss on financial assets

has been incurred, the Fund considers factors such as the probability of insolvency or

significant financial difficulties of the debtor and default or significant delay in payments.

Subsequent to initial recognition, loans and receivables are measured at amortised cost using

the effective interest method. Gains and losses are recognised in profit or loss when the loans

and receivables are derecognised or impaired, and through the amortisation process.

If any such evidence exists, the amount of impairment loss is measured as the difference

between the asset’s carrying amount and the present value of estimated future cash flows

discounted at the financial asset’s original effective interest rate. The impairment loss is

recognised in profit or loss.

21

Classification of realised and unrealised gains and losses

Significant accounting estimates and judgments

The Fund’s financial liabilities are recognised initially at fair value plus directly attributable

transaction costs and subsequently measured at amortised cost using the effective interest method.

Financial liabilities, within the scope of MFRS 139, are recognised in the statement of financial

position when, and only when, the Fund becomes a party to the contractual provisions of the

financial instrument.

A financial liability is derecognised when the obligation under the liability is extinguished. Gains

and losses are recognised in profit or loss when the liabilities are derecognised, and through the

amortisation process.

Unrealised gains and losses comprise changes in the fair value of financial instruments for the

period and from reversal of prior period’s unrealised gains and losses for financial instruments

which were realised (i.e. sold, redeemed or matured) during the reporting period.

Realised gains and losses on disposals of financial instruments classified at fair value through

profit or loss are calculated using the weighted average method. They represent the difference

between an instrument’s initial carrying amount and disposal amount.

The Fund classifies its investment as financial assets at FVTPL as the Fund may sell its

investment in the short-term for profit-taking or to meet unitholders’ cancellation of units.

No major judgments have been made by the Manager in applying the Fund’s accounting policies.

There are no key assumptions concerning the future and other key sources of estimation

uncertainty at the reporting date, that have a significant risk of causing a material adjustment to

the carrying amounts of assets and liabilities within the next financial year.

The preparation of the Fund’s financial statements requires the Manager to make judgments,

estimates and assumptions that affect the reported amounts of revenues, expenses, assets and

liabilities, and the disclosure of contingent liabilities at the reporting date. However, uncertainty

about these assumptions and estimates could result in outcomes that could require a material

adjustment to the carrying amount of the asset or liability in the future.

22

4. INVESTMENT

2017 2016

RM RM

Financial assets at FVTPL

At cost:

Foreign collective investment scheme 10,603,284 11,832,529

At fair value:

Foreign collective investment scheme 12,649,239 13,107,221

Details of investment as at 31 May 2017 are as follows:

Fair

value as a

percentage of

Foreign collective Number Fair Purchase net asset

investment scheme of units value cost value

RM RM %

HSBC Global Investment

Funds – Asia Pacific ex

Japan Equity High

Dividend (“Target Fund”) 163,856 12,649,239 10,603,284 95.94

Excess of fair value over cost 2,045,955

2017 2016

% of % of

By country portfolio portfolio

Australia 18.9 18.4

China 18.4 18.2

Taiwan 15.9 14.4

Hong Kong 12.7 16.3

Korea 12.6 9.3

India 9.3 6.1

Indonesia 3.6 -

Singapore 3.4 7.9

(Forward)

A minimum of 95% of its net asset value will be invested in the Target Fund. However, the asset

allocation may be reduced due to creation of units at the point of reporting date. The ratio will be

adjusted back to the minimum level after the reporting period, if need be.

The Target Fund’s investment objective and policy are to seek long-term capital growth and a

high level of income by investing primarily in a diversified portfolio of investment in equity Asia

Pacific (ex-Japan region). As at the reporting date, the investment portfolio of the Target Fund is

made up as the following:

23

2017 2016

% of % of

portfolio portfolio

New Zealand 1.6 -

Malaysia 0.8 -

Cash and others 2.8 9.4

100.0 100.0

By sector

Financials 30.4 27.5

Technology 24.7 15.1

Telecommunications 10.1 14.4

Consumer staples 9.9 12.5

Energy 7.8 4.9

Materials 7.0 -

Industrials 3.5 12.3

Consumer discretionary 2.2 -

Real estate 1.1 -

Utilities 0.8 6.0

Cash and others 2.5 7.3

100.0 100.0

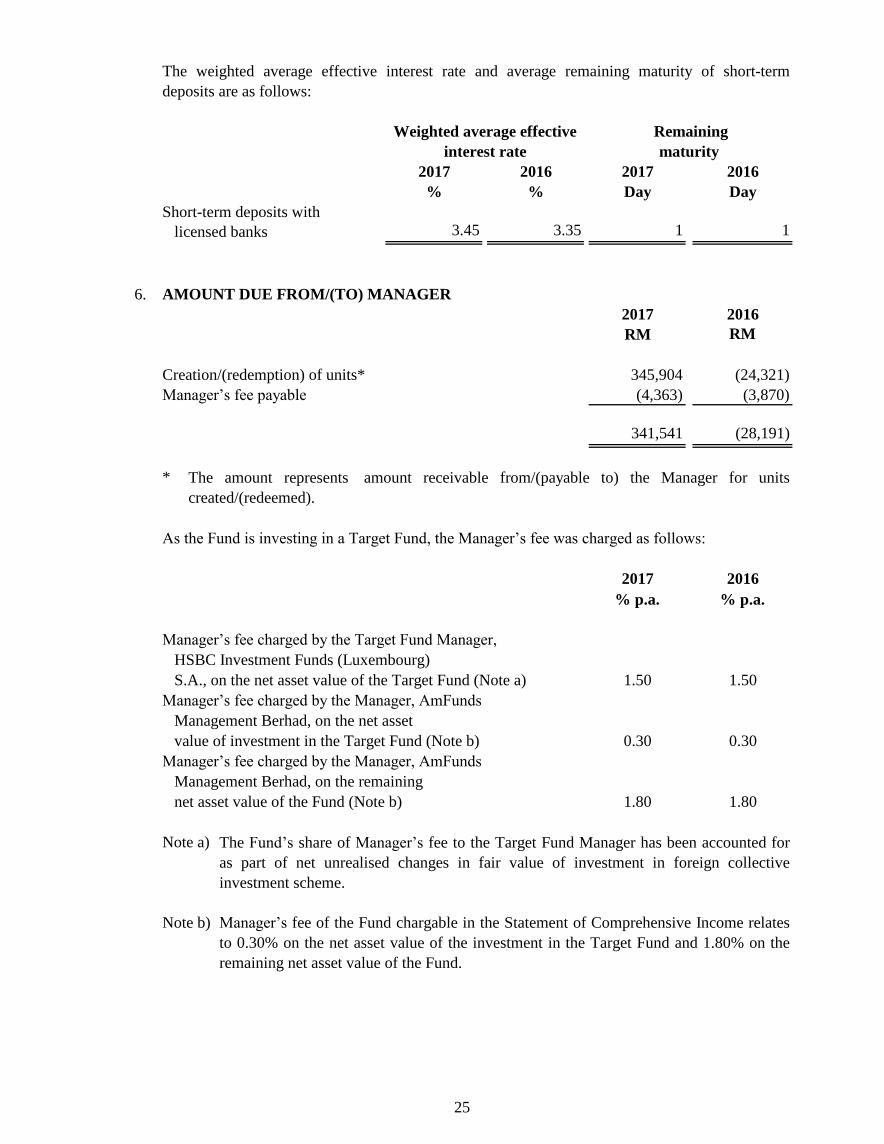

5. DEPOSITS WITH FINANCIAL INSTITUTIONS

2017 2016

RM RM

At nominal value:

Short-term deposits with licensed banks 462,100 333,800

At carrying value:

Short-term deposits with licensed banks 462,144 333,831

Details of deposits with financial institutions as at 31 May 2017 are as follows:

Carrying

value as a

percentage of

Maturity Nominal Carrying Purchase net asset

date Bank value value cost value

RM RM RM %

Short-term deposit with a licensed bank

01.06.2017 Public Bank

Berhad 462,100 462,144 462,100 3.51

24

2017 2016 2017 2016

% % Day Day

Short-term deposits with

licensed banks 3.45 3.35 1 1

6. AMOUNT DUE FROM/(TO) MANAGER

2017 2016

RM RM

Creation/(redemption) of units* 345,904 (24,321)

Manager’s fee payable (4,363) (3,870)

341,541 (28,191)

*

As the Fund is investing in a Target Fund, the Manager’s fee was charged as follows:

2017 2016

% p.a. % p.a.

Manager’s fee charged by the Target Fund Manager,

HSBC Investment Funds (Luxembourg)

S.A., on the net asset value of the Target Fund (Note a) 1.50 1.50

Manager’s fee charged by the Manager, AmFunds

Management Berhad, on the net asset

value of investment in the Target Fund (Note b) 0.30 0.30

Manager’s fee charged by the Manager, AmFunds

Management Berhad, on the remaining

net asset value of the Fund (Note b) 1.80 1.80

Note a)

Note b)

The Fund’s share of Manager’s fee to the Target Fund Manager has been accounted for

as part of net unrealised changes in fair value of investment in foreign collective

investment scheme.

interest rate

Weighted average effective Remaining

maturity

The amount represents amount receivable from/(payable to) the Manager for units

created/(redeemed).

Manager’s fee of the Fund chargable in the Statement of Comprehensive Income relates

to 0.30% on the net asset value of the investment in the Target Fund and 1.80% on the

remaining net asset value of the Fund.

The weighted average effective interest rate and average remaining maturity of short-term

deposits are as follows:

25

7. AMOUNT DUE TO TARGET FUND MANAGER

The normal trade credit period is three business days.

8. AMOUNT DUE TO TRUSTEE

9. NET GAIN/(LOSS) FROM INVESTMENT

2017 2016

RM RM

Net gain/(loss) on financial assets at FVTPL comprised:

− Net realised loss on sale of investment (434,741) (594,392)

− Net realised gain on foreign currency exchange 1,989,132 1,227,839

− Net unrealised gain/(loss) on changes in fair value

of investment 2,546,136 (2,617,149)

− Net unrealised (loss)/gain on foreign currency fluctuation

of investment denominated in foreign currency (1,774,873) 1,027,113

2,325,654 (956,589)

10. OTHER EXPENSES

The Manager’s fee, inclusive of GST, was overstated by RM62,903 for the period from 13 March

2015 to 19 June 2015. No adjustment was made to the Fund’s NAV as the impact was less than

0.5% to the Fund’s NAV. The amount was refunded to the Fund in the previous financial year.

The normal credit period in the previous and current financial years for creation and redemption

of units is three business days.

The normal credit period in the previous and current financial years for Manager’s fee payable is

one month.

Trustee’s fee is at a rate of 0.06% (2016: 0.06%) per annum on the net asset value of the Fund,

calculated on a daily basis, subject to a minimum fee of RM10,000 per annum.

The normal credit period in the previous and current financial years for Trustee’s fee payable is

one month.

Included in other expenses is Goods and Services Tax incurred by the Fund during the financial

year amounting to RM3,976 (2016: RM2,018).

The amount due to the Target Fund Manager was for the purchase of investment where settlement

was not due as at the financial year end.

26

11. TOTAL EQUITY

Total equity is represented by:

2017 2016

Note RM RM

Unitholders’ capital (a) 8,659,493 11,087,246

Retained earnings

− Realised income (b) 2,479,731 1,043,020

− Unrealised gain (c) 2,045,732 1,274,692

13,184,956 13,404,958

(a) UNITHOLDERS’ CAPITAL/UNITS IN CIRCULATION

Number of Number of

units RM units RM

At beginning of the

financial year 11,009,221 11,087,246 14,923,729 16,056,417

Creation during the

financial year 5,287,993 8,006,643 1,415,470 1,817,701

Distribution reinvested

(Note 14) - - 527,266 630,135

Cancellation during the

financial year (7,676,459) (10,434,396) (5,857,244) (7,417,007)

At end of the financial year 8,620,755 8,659,493 11,009,221 11,087,246

(b) REALISED – DISTRIBUTABLE

2017 2016

RM RM

At beginning of the financial year 1,043,020 601,884

Total comprehensive income/(loss) for the financial year 2,466,374 (518,765)

Net unrealised (gain)/loss attributable to investment held

and others transferred to unrealised reserve [Note 11(c)] (771,040) 1,590,036

Distributions out of realised reserve (Note 14) (258,623) (630,135)

Net increase in realised reserve for the

financial year 1,436,711 441,136

At end of the financial year 2,479,731 1,043,020

2017 2016

27

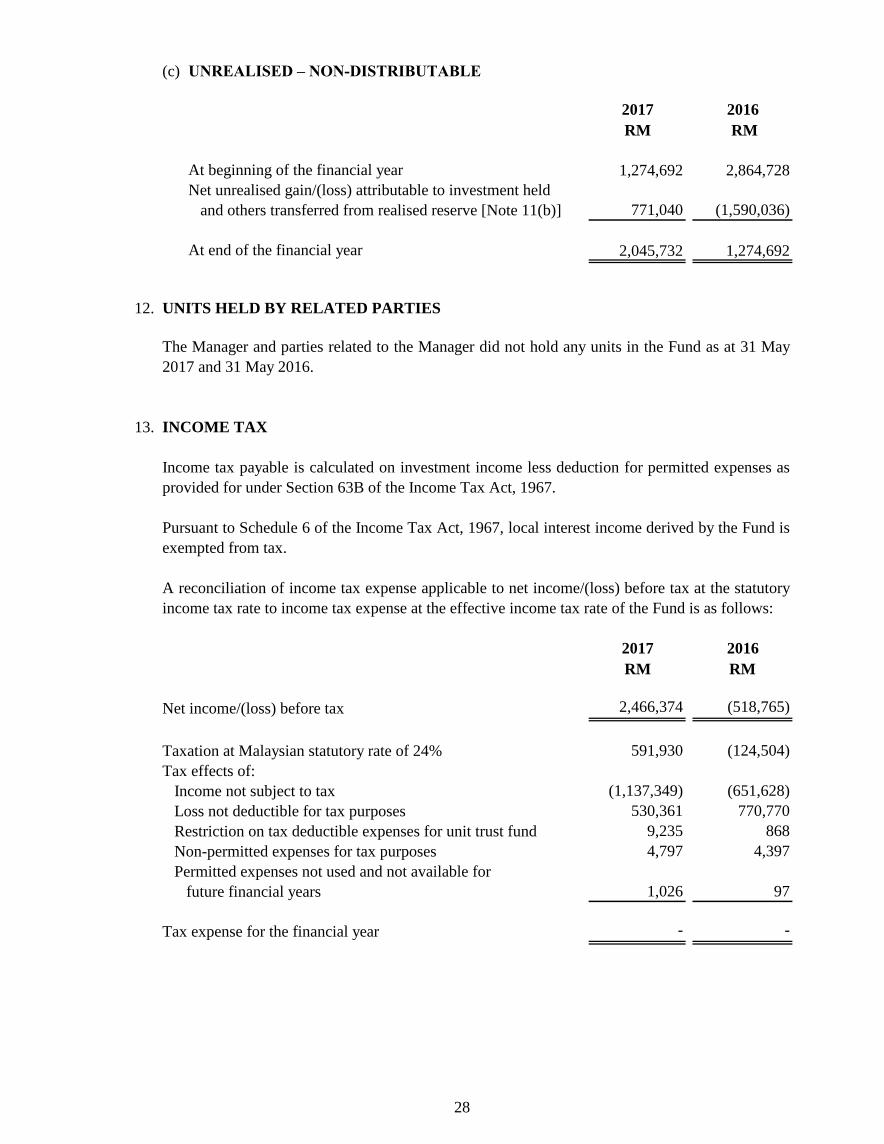

(c) UNREALISED – NON-DISTRIBUTABLE

2017 2016

RM RM

At beginning of the financial year 1,274,692 2,864,728

Net unrealised gain/(loss) attributable to investment held

and others transferred from realised reserve [Note 11(b)] 771,040 (1,590,036)

At end of the financial year 2,045,732 1,274,692

12. UNITS HELD BY RELATED PARTIES

13. INCOME TAX

2017 2016

RM RM

Net income/(loss) before tax 2,466,374 (518,765)

Taxation at Malaysian statutory rate of 24% 591,930 (124,504)

Tax effects of:

Income not subject to tax (1,137,349) (651,628)

Loss not deductible for tax purposes 530,361 770,770

Restriction on tax deductible expenses for unit trust fund 9,235 868

Non-permitted expenses for tax purposes 4,797 4,397

Permitted expenses not used and not available for

future financial years 1,026 97

Tax expense for the financial year - -

The Manager and parties related to the Manager did not hold any units in the Fund as at 31 May

2017 and 31 May 2016.

Income tax payable is calculated on investment income less deduction for permitted expenses as

provided for under Section 63B of the Income Tax Act, 1967.

Pursuant to Schedule 6 of the Income Tax Act, 1967, local interest income derived by the Fund is

exempted from tax.

A reconciliation of income tax expense applicable to net income/(loss) before tax at the statutory

income tax rate to income tax expense at the effective income tax rate of the Fund is as follows:

28

14. DISTRIBUTIONS

2017 2016

RM RM

Distribution income 67,662 171,619

Interest income 2,765 6,252

Net realised loss on sale of investment (434,741) -

Net realised gain on foreign currency exchange 685,679 474,605

321,365 652,476

Less: Expenses (62,742) (22,341)

Total amount of distributions 258,623 630,135

Gross/net distributions per unit (sen) 3.00 6.00

Distributions made out of:

− Realised reserve [Note 11(b)] 258,623 630,135

258,623 630,135

Comprising:

Distributions reinvested [Note 11(a)] - 630,135

Distributions to be reinvested 258,623 -

258,623 630,135

15. MANAGEMENT EXPENSE RATIO (“MER”)

2017 2016

% p.a. % p.a.

Manager’s fee 0.35 (0.02)

Trustee’s fee 0.10 0.06

Fund’s other expenses 0.18 0.10

Total MER 0.63 0.14

The Fund’s MER is as follows:

Distributions to unitholders declared on 31 May 2017 (declared on 25 May 2016 for the previous

financial year) are from the following sources:

29

16. PORTFOLIO TURNOVER RATIO (“PTR”)

17. SEGMENTAL REPORTING

18.

Target Fund Manager

RM %

HSBC Investment Funds (Luxembourg) S.A. 15,606,338 100.00

19. FINANCIAL INSTRUMENTS

(a) Classification of financial instruments

The above transactions were in respect of collective investment scheme. Transactions in these

investments do not involve any commission or brokerage.

The significant accounting policies in Note 3 describe how the classes of financial

instruments are measured, and how income and expenses, including fair value gains and

losses, are recognised. The following table analyses the financial assets and liabilities of the

Fund in the statement of financial position as by the class of financial instrument to which

they are assigned, and therefore by the measurement basis.

As stated in Note 1, the Fund is a feeder fund whereby a minimum of 95% of the Fund’s net asset

value will be invested in the Target Fund.

Transaction value

Details of transactions with the Target Fund Manager for the financial year ended 31 May 2017

are as follows:

The MER of the Fund is the ratio of the sum of annualised fees and expenses incurred by the

Fund to the average net asset value of the Fund calculated on a daily basis.

The PTR of the Fund, which is the ratio of average total acquisitions and disposals of investment

to the average net asset value of the Fund calculated on a daily basis, is 0.78 times (2016: 0.21

times).

As the Fund operates substantially as a feeder fund which invests primarily in the Target Fund, it

is not possible or meaningful to classify its investment by separate business or geographical

segments. A summary of the investment portfolio of the Target Fund is disclosed in Note 4.

TRANSACTIONS WITH THE TARGET FUND MANAGER

30

Loans and Financial Financial receivables liabilities at

assets at amortised amortised

at FVTPL cost cost Total

RM RM RM RM

Assets

Investment 12,649,239 - - 12,649,239

Deposit with financial

institution - 462,144 - 462,144

Amount due from Manager - 341,541 - 341,541

Cash at banks - 480,203 - 480,203

Total financial assets 12,649,239 1,283,888 - 13,933,127

Liabilities

Amount due to Target Fund

Manager - - 477,331 477,331

Amount due to Trustee - - 904 904

Distribution to be reinvested - - 258,623 258,623

Sundry payables and accrued

expenses - - 11,313 11,313

Total financial liabilities - - 748,171 748,171

Assets

Investment 13,107,221 - - 13,107,221

Deposit with financial

institution - 333,831 - 333,831

Cash at banks - 2,757 - 2,757

Total financial assets 13,107,221 336,588 - 13,443,809

Liabilities

Amount due to Manager - - 28,191 28,191

Amount due to Trustee - - 875 875

Sundry payables and accrued

expenses - - 9,785 9,785

Total financial liabilities - - 38,851 38,851

2016

2017

31

Income, expense, gains

and losses

2017 2016

RM RM

Net gain/(loss) from financial assets at FVTPL 2,325,654 (956,589)

Income, of which derived from:

- Distribution income from financial assets at FVTPL 195,688 443,990

- Interest income from loans and receivables 7,997 16,175

- Other unrealised foreign exchange loss (223) -

(b) Financial instruments that are carried at fair value

Level 1: quoted (unadjusted) prices in active markets for identical assets or liabilities;

Level 2:

Level 3:

Level 1 Level 2 Level 3 Total

RM RM RM RM

- 12,649,239 - 12,649,239

- 13,107,221 - 13,107,221

(c)

Deposits with financial institutions

Cash at banks

Amount due from/to Manager

Amount due to Target Fund Manager

other techniques for which all inputs which have a significant effect on the

recorded fair values are observable; either directly or indirectly; or

techniques which use inputs which have a significant effect on the recorded fair

value that are not based on observable market data.

The following table shows an analysis of financial instruments recorded at fair value by the

level of the fair value hierarchy:

The Fund’s financial assets and liabilities at FVTPL are carried at fair value.

2017

The Fund uses the following hierarchy for determining and disclosing the fair value of

financial instruments by valuation technique:

Financial assets at FVTPL

2016

Financial assets at FVTPL

Financial instruments that are not carried at fair value and whose carrying amounts are

reasonable approximation of fair value

The following are classes of financial instruments that are not carried at fair value and whose

carrying amounts are reasonable approximation of fair value due to their short period to

maturity or short credit period:

32

Amount due to Trustee

Distribution to be reinvested

Sundry payables and accrued expenses

20. RISK MANAGEMENT POLICIES

Market risk

(i) Price risk

Percentage movements in

price by: 2017 2016

RM RM

-5.00% (632,462) (655,361)

+5.00% 632,462 655,361

(ii) Interest rate risk

Interest rate risk will affect the value of the Fund’s investments, given the interest rate

movements, which are influenced by regional and local economic developments as well as

political developments.

Market risk, in general, is the risk that the value of a portfolio would decrease due to changes in

market risk factors such as equity prices, interest rates, foreign exchange rates and commodity

prices.

Risk management is carried out by closely monitoring, measuring and mitigating the above said

risks, careful selection of investment coupled with stringent compliance to investment restrictions

as stipulated by the Capital Market and Services Act 2007, Securities Commission’s Guidelines

on Unit Trust Funds and the Deed as the backbone of risk management of the Fund.

The Fund is exposed to a variety of risks that include market risk, credit risk, liquidity risk, single

issuer risk, regulatory risk, country risk, management risk, and non-compliance risk.

There are no financial instruments which are not carried at fair values and whose carrying

amounts are not reasonable approximation of their respective fair values.

The result below summarized the price risk sensitivity of the Fund’s NAV due to movements

of price by -5.00% and +5.00% respectively.

Sensitivity of the Fund’s NAV (RM)

Price risk refers to the uncertainty of an investment’s future prices. In the event of adverse

price movements, the Fund might endure potential loss on its investment in the Target Fund.

In managing price risk, the Manager actively monitors the performance and risk profile of the

investment portfolio.

33

Parallel shift in yield curve by:

2017 2016

RM RM

+100bps (12) (8)

-100bps 12 9

(iii) Currency risk

Currencies other than the

Fund’s functional currency: 2017 2016

RM RM

-5.00% (632,470) (655,361)

+5.00% 632,470 655,361

2017 2016

Assets/(liabilities) dominated RM % of net RM % of net

in United States Dollar equivalent asset value equivalent asset value

Investment 12,649,239 95.94 13,107,221 97.78

Cash at bank 477,499 3.62 - -

Amount due to Target

Fund Manager (477,331) (3.62) - -

12,649,407 95.94 13,107,221 97.78

The result below summarised the interest rate sensitivity of the Fund’s NAV, or theoretical

value (applicable to money market deposit) due to the parallel movement assumption of the

yield curve by +100bps and -100bps respectively:

Currency risk is associated with the Fund’s assets and liabilities that are denominated in

currencies other than the Fund’s base currency. Currency risk refers to the potential loss the

Fund might face due to unfavorable fluctuations of currencies other than the Fund’s base

currency against the Fund’s base currency.

Sensitivity of the Fund’s NAV, or theoretical value

The result below summarised the currency risk sensitivity of the Fund’s NAV due to

appreciation/depreciation of the Fund’s functional currency against currencies other than the

Fund’s functional currency.

Sensitivity of the Fund’s NAV

The net unhedged financial assets and financial liabilities of the Fund that are not

denominated in Fund’s functional currency are as follows:

Domestic interest rates on deposits and placements with licensed financial institutions are

determined based on prevailing market rates.

34

Credit risk

Liquidity risk

Single issuer risk

Regulatory risk

Country risk

Credit risk is the risk that the counterparty to a financial instrument will cause a financial loss to

the Fund by failing to discharge an obligation. Credit risk applies to short-term deposits and

distributions receivables. The issuer of such instruments may not be able to fulfill the required

interest payments or repay the principal invested or amount owing. These risks may cause the

Fund’s investment to fluctuate in value.

The Fund, as a feeder fund, invests significantly all its assets in the Target Fund. The Target Fund

manages the risk by setting internal counterparty limits and undertaking internal credit evaluation

to minimise such risk.

For deposits with financial institutions, the Fund makes placements with financial institutions

with sound rating of P1/MARC-1 and above. Cash at banks are held for liquidity purposes and are

not exposed to significant credit risk.

Liquidity risk is defined as the risk of being unable to raise funds or borrowings to meet payment

obligations as they fall due. This is also the risk of the Fund experiencing large redemptions, when

the Investment Manager could be forced to sell large volumes of its holdings at unfavorable prices

to meet redemption requirements.

The risk of price fluctuation in foreign securities may arise due to political, financial and

economic events in foreign countries. If this occurs, there is a possibility that the net asset value of

the Fund may be adversely affected.

The Fund maintains a sufficient level of liquid assets, after consultation with the Trustee, to meet

anticipated payments and cancellation of units by unitholders. Liquid assets comprise of deposits

with licensed financial institutions and other instruments, which are capable of being converted

into cash within 5 to 7 days. The Fund’s policy is to always maintain a prudent level of liquid

assets so as to reduce liquidity risk.

Any changes in national policies and regulations may have effects on the capital market and the

net asset value of the fund.

The Fund, as a feeder fund, invests significantly all its assets in the Target Fund. The Target Fund

is restricted from investing in securities issued by any issuer in excess of a certain percentage of

its net asset value. Under such restriction, the risk exposure to the securities of any single issuer is

diversified and managed by the Target Fund Manager based on internal/external ratings.

35

Management risk

Non-compliance risk

21. CAPITAL MANAGEMENT

No changes were made in the objective, policies or processes during the financial years ended 31

May 2017 and 31 May 2016.

The primary objective of the Fund’s capital management is to ensure that it maximises

unitholders’ value by expanding its fund size to benefit from economies of scale and achieving

growth in net asset value from the performance of its investment.

The Fund manages its capital structure and makes adjustments to it, in light of changes in

economic conditions. To maintain or adjust the capital structure, the Fund may issue new or bonus

units, make distribution payment, or return capital to unitholders by way of redemption of units.

The specific risks associated to the Target Fund include market risk, securities risk, emerging

market risk, settlement and credit risks, regulatory and accounting standards risks, political risk,

custody risk and liquidity risk.

This is the risk of the Manager, the Trustee or the Fund not complying with internal policies, the

Deed of the Fund, securities law or guidelines issued by the regulators. Non-compliance risk may

adversely affect the investment of the Fund when the Fund is forced to rectify the non-compliance.

Poor management of the Fund may cause considerable losses to the Fund that in turn may affect

the net asset value of the Fund.

36

Advantage Asia Pacific ex Japan Dividend

(formerly known as AmAdvantage Asia Pacific ex Japan Dividend)

STATEMENT BY THE MANAGER

Kuala Lumpur, Malaysia

I, GOH WEE PENG, for and on behalf of the Manager, AmFunds Management Berhad, for

Advantage Asia Pacific ex Japan Dividend (formerly known as AmAdvantage Asia Pacific ex

Japan Dividend) do hereby state that in the opinion of the Manager, the accompanying statement of

financial position, statement of comprehensive income, statement of changes in equity, statement of

cash flows and the accompanying notes are drawn up in accordance with Malaysian Financial

Reporting Standards and International Financial Reporting Standards so as to give a true and fair

view of the financial position of the Fund as at 31 May 2017 and the comprehensive income, the

changes in equity and cash flows of the Fund for the financial year then ended.

7 July 2017

GOH WEE PENG

For and on behalf of the Manager

AmFunds Management Berhad

37

38

TRUSTEE’S REPORT

39

DIRECTORY

Head Office 9th Floor, Bangunan Ambank Group

55, Jalan Raja Chulan, 50200 Kuala Lumpur

Tel: (03) 2032 2888 Facsimile: (03) 2031 5210

Email: [email protected]

Postal Address AmFunds Management Berhad

P.O Box 13611, 50816 Kuala Lumpur

Related Institutional Unit Trust Agent

AmBank (M) Berhad Head Office

Company No. 8515-D 31st Floor, Menara AmBank

No. 8 Jalan Yap Kwan Seng, 50450 Kuala Lumpur

AmInvestment Bank Berhad Head Office

Company No. 23742-V 22nd

Floor, Bangunan AmBank Group

55 Jalan Raja Chulan, 50200 Kuala Lumpur

For more details on the list of IUTAs, please contact the Manager.

For enquiries about this or any of the other Funds offered by AmFunds Management Berhad

Please call 2032 2888 between 8.45 a.m. to 5.45 p.m. (Monday to Thursday),

Friday (8.45 a.m. to 5.00 p.m.)

Semi-Annual Report28 February 2015

03 2132 2888 | aminvest.com | [email protected]

AmFunds Management Berhad (155432-A)