Embed Size (px)

Citation preview

Page 1 of 28

Page 1 of 28

Advanced Financial Accounting

Sample Paper 3

2017 / 2018 Questions & Suggested Solutions

Page 2 of 28

NOTES TO USERS ABOUT SAMPLE PAPERS

Sample papers are published by Accounting Technicians Ireland. They are intended to provide guidance

to students and their teachers regarding the style and type of question, and their suggested solutions, in

our examinations. They are not intended to provide an exhaustive list of all possible questions that may

be asked and both students and teachers alike are reminded to consult our published syllabus (see

www.AccountingTechniciansIreland.ie) for a comprehensive list of examinable topics.

There are often many possible approaches to the solution of questions in professional examinations. It

should not be assumed that the approach adopted in these solutions is the only correct approach,

particularly with discursive answers. Alternative answers will be marked on their own merits.

This publication is copyright 2017 and may not be reproduced without permission of Accounting

Technicians Ireland.

© Accounting Technicians Ireland, 2017.

Page 3 of 28

INSTRUCTIONS TO CANDIDATES

PLEASE READ CAREFULLY

Candidates must indicate clearly whether they are answering the paper in accordance with the law

and practice of Northern Ireland or the Republic of Ireland.

In this examination paper the €/£ symbol may be understood and used by candidates in Northern

Ireland to indicate the UK pound sterling by candidates in the Republic of Ireland to indicate the

Euro.

Answer ALL THREE questions in Section A and TWO of the THREE questions in Section B. If

more than TWO questions is answered in Section B, then only the first TWO questions, in the

order filed, will be corrected.

Candidates should allocate their time carefully. All

workings should be shown.

All figures should be labelled, as appropriate, e.g. €’s, £’s, units etc.

Answers should be illustrated with examples, where appropriate.

Question 1 begins on Page 2 overleaf.

NOTE: This sample paper and solutions have been prepared to reflect the provisions of FRS

102

Page 4 of 28

SECTION A

Answer ALL THREE Questions in this Section

(The total marks for section A will be 60, made up of a theory question of 20 marks, a multiple choice

question of 15 marks and a further question of 25 marks)

QUESTION 1

(i) The Conceptual Framework for Financial Reporting provides a frame of reference that outlines

generally accepted theoretical principles for financial accounting.

(a) Explain briefly the purpose of the Framework. 6 marks

(b) A friend who has not studied accountancy has read the Conceptual Framework and

is confused by some of the terms and definitions discussed within. Prepare a note

setting out your understanding of three of the following four terms:

i. Going concern

ii. Accruals

iii. Asset

iv. Liability

6 marks

(ii) Define “Accounting Policies” and outline the circumstances under which an accounting

policy should be changed.

4 marks

Define “Accounting Estimates”and give examples of three items which are usually the subject

of accounting estimates.

4 marks

Total 20 marks

QUESTION 2

The following multiple choice question consists of TEN parts, each of which is followed by

FOUR possible answers. There is ONLY ONE right answer in each part.

Each part carries 1½ marks.

Requirement

Indicate the right answer to each of the following TEN parts. Total 15 Marks

N.B Candidates should answer this question by ticking the appropriate boxes on the special answer sheet

which is contained within the answer booklet.

Page 5 of 28

QUESTION 2 (cont’d)

BACKGROUND INFORMATION TO PARTS [1] – [5]

The following information relates to ROCK Ltd: £/€

Receivables at 1st

January 2016 ..................................... 60,000 Receivables at 31

st December 2016................................. 80,000

Payables at 1st

January 2016 ......................................... 75,000 Payables at 31

st December 2016..................................... 85,000

Inventory at 1st

January 2016 ........................................ 140,000 Inventory at 31

st December 2016 ................................... 170,000

Sales on credit for the year ended 31st

December 2016 ..... 1,800,000 Cash sales for the year ended 31

st December 2016........... 300,000

Purchases (all on credit) for the year ended 31st

December 2016 ................................................................................. 1,250,000 Bank overdraft at 31

st December 2016 ............................ 60,000

Taxation liability at 31st

December 2016 .......................... 70,000 Accrued expenses at 31

st December 2016........................ 25,000

Prepaid expenses at 31st

December 2016......................... 30,000

[1] The receivable days outstanding at 31st

December 2016 (to the nearest day) was: -

(a) 12 days

(b) 14 days

(c) 16 days

(d) 18 days

[2] The payables days outstanding at 31st

December 2016 (to the nearest day) was: -

(a) 23 days

(b) 24 days

(c) 25 days

(d) 26 days

[3] The current ratio at 31

st December 2016 (assuming no other current assets or liabilities), to two

decimal points, was: -

(a) 1.65 :1

(b) 1.17 :1

(c) 1.04 :1

(d) 0.16 :1

Page 6 of 28

Question 2 cont’d

[4] The inventory turnover (to two decimal places) for the year ended 31st

December 2016 was: -

(a) 8.06 times

(b) 7.87 times

(c) 7.35 times

(d) 1.18 times

[5] The gross profit margin for the year ended 31

st December 2016, to one decimal point was:

(a) 32.2 % (b) 38.6 % (c) 41.9 % (d) 44.3 %

[6] FRS 102 provides that a complete set of Financial Statements comprises the following:

(a) A Statement of Comprehensive Income and a Statement of Financial Position.

(b) A Statement of Comprehensive Income, a Statement of Financial Position and A

statement of Changes in Equity.

(c) A Statement of Comprehensive Income, a Statement of Financial Position, a statement of Changes in Equity and A Statement of Cash Flows. (d) A Statement of Comprehensive Income, A Statement of Financial Position, A

statement of Changes in Equity and A Statement of Cash Flows, and notes to the

Financial Statements.

[7] FRS 102 states that a business should prepare its financial statements on the basis that the business

is a going concern: -

(a) if it is being liquidated

(b) if it has ceased trading

(c) if the directors have no realistic alternative but to liquidate the entity or to cease trading

(d) only if none of the above situations exist

[8] Under the provisions of the Companies Acts there must be shown in a note to the accounts:

(a) the average number of people employed during the year

(b) the number of people employed on the first day of the year

(c) the number of people employed on the last day of the year

(d) the number of new employees employed during the year

Page 7 of 28

Question 2 cont’d

[9] Partners drawings are: -

(a) charged against the partners in their capital accounts

(b) charged against the partners in their current accounts

(c) credited to the partners in their capital accounts

(d) credited to the partners in their current accounts

[10] Payments by a lessee in an operating lease are:-

(a) charged in the lessee’s Statement of Comprehensive Income on the reducing balance

basis

(b) credited in the lessee’s Statement of Comprehensive Income on the reducing balance

basis

(c) charged in the lessee’s Statement of Comprehensive Income on the straight line basis

(d) credited in the lessee’s Statement of Comprehensive Income on the straight line basis

Page 8 of 28

QUESTION 3

CABLE Ltd., is a furniture company with an authorized share capital of

£/€3,000,000, comprised of 6,000,000 ordinary shares of 50 pence/cent each. The following trial:

balance was extracted as at 31st

December 2016

£/€’000 £/€’000

Ordinary share capital.................................................................... 2,200 Share premium account ................................................................. 180 General reserve .............................................................................. 260 Retained earnings balance at 1 January 2016 ................................ 74 8% debenture stock........................................................................ 250 Leasehold premises at cost ............................................................ 3,900 Leasehold premises – accumulated depreciation at 1 January 2016..... 500 Plant and machinery at cost ........................................................... 820 Plant and machinery – accumulated depreciation at 1 January 2016.... 320 Motor vehicles at cost.................................................................... 300 Motor vehicles – accumulated depreciation at 1 January 2016 ........... 80 Receivables.................................................................................... 169 Payables ........................................................................................... 95 Bank............................................................................................... 120 Sales............................................................................................... 4,500 Sales returns..................................................................................... 79 Opening inventory ......................................................................... 180 Purchases ........................................................................................ 2,400 Purchases returns ........................................................................... 160 Administration expenses................................................................ 450 Distribution expenses..................................................................... 340 Bankinterest .................................................................................. 60 Deposit interest received................................................................ 35 Debenture interest.......................................................................... 10 Interim ordinary dividend paid ...................................................... 66

.................................................................................................

8,774 8,774

ADDITIONAL INFORMATION

(1) Goods purchased on 28th

December 2016 for £/€70,000 had not been accounted for or

included in the physical stock count at 31st

December 2016.

(2) Closing inventory, as per the physical stock count at 31st

December 2016 was

£/€220,000.

(3) Training grants of £/€20,000 in respect of training sales staff were due to the company at 31st

December 2016.

Page 9 of 28

QUESTION 3(Cont’d.)

(4) Depreciation is to be charged as follows:

Leasehold premises ........... 2% on cost

Plant and machinery .......... 10% on cost

Motor vehicles................... 20% on cost

Depreciation on leasehold premises and plant and machinery should be included as part of

administration expenses and depreciation of motor vehicles should be included as part of

distribution expenses.

(5) The charge for corporation tax for the year ended 31st

December 2016 is estimated at 50% of

the profit before tax.

(6) A final dividend of 5 pence/cent per share was paid to the ordinary shareholders on 31

December 2016 however this payment has not yet been recorded in the accounts.

(7) Half year debenture interest to be provided for.

Requirement

(a) Prepare, in accordance with FRS 102, the Statement of Comprehensive Income of CABLE Ltd.,

for the year ended 31st

December 2016 in as far as the information provided permits.

N.B. You are NOT required to prepare a Statement of Financial Position or notes to the accounts. You are required to submit workings to show the make-up of the figures in the

Statement of Comprehensive Income.

20 Marks

(b) Prepare a Statement of Changes in Equity for the year ended 31 December 2016.

3 Marks

Presentation: 2 marks

Total: 25 Marks

Page 10 of 28

Premises..................................................... 250,000 50,000 200,000 Plant and machinery .................................. 130,000 65,000 65,000 Furniture and fittings ................................. 25,000 5,000 20,000

405,000 120,000 285,000

Geoff.........................................................

Henry ........................................................ 80,000

70,000

Ian.............................................................

Partners Current Accounts

70,000 220,000

Geoff......................................................... 16,000 Henry ........................................................ (20,000) Ian............................................................. 10,000

6,000 Profit for the year (not yet divided between the partners) 88,000

Current liabilities

Payables....................................................

26,000

Loan from Simon...................................... 13,000 39,000

Total capital and liabilities 353,000

SECTION B

Answer TWO of the THREE questions in this Section QUESTION 4

Geoff, Henry and Ian are in partnership sharing profits and losses in the ratio 4:2:2. The partners

receive a salary of £/€5,000, £/€6,000 and £/€7,000 each and are entitled to interest on the balance on

their capital accounts at 5% per annum. Ian is entitled to a guaranteed share of profits, in addition to his

salary and interest on capital, of £/€6,000 any deficiency to be borne by Geoff and Henry equally.

The following is the draft balance sheet of the partnership as at 31 December 2016 (before the profit for

the year has been divided between the partners).

DRAFT Statement of Financial Position as at 31st

DECEMBER 2016

Cost Accumulated Net Book

Depreciation Amount

£/€ £/€ £/€

Non-current Assets

Current Assets Inventory .................................................. 30,000 Trade receivables...................................... 26,000

Bank.......................................................... 12,000

68,000

................................................................... 353,000

Partners Capital Accounts

Page 11 of 28

QUESTION 4 (Cont’d.)

Adjustment is required in respect of the following items:

(1) Depreciation for the year has not been provided. It should be provided for as follows:

Premises ..................... £/€5,000 Plant and machinery ..... £/€26,000 Furniture and fittings..... £/€5,000

(2) Wages and salaries of £/€14,000 have not been provided for at the year end.

(3) Rent amounting to £/€7,000 has been prepaid at the year end.

Requirement

You are required to prepare:

(a) a statement setting out the adjustments required to the profit for the year arising out of items

(1) to (3) above;

3 Marks

(b) a statement setting out the appropriation of the adjusted profit between the partners;

3 Marks

(c) the current accounts of the partners;

4 Marks

(d) the revised balance sheet after dealing with parts (a) to (c) above.

8 Marks

Presentation: 2 marks

Total: 20 Marks

Page 12 of 28

QUESTION 5

JEWEL Limited, a car rental company, had revenue of £/€4,500,000 and made a net profit before

taxation of £/€350,000 for the year ended 31st

December 2016, as per the draft accounts.

During a review of the draft accounts you ascertain the following:

(1) A customer who owed the company £/€80,000 at 31

st December 2016 has gone into

receivership in January 2017 and is unlikely to be able to pay any part of the debt.

(2) A government grant of £/€50,000 to help meet the cost of wages and salaries to train staff was

treated as deferred income at 31st

December 2016.

(3) Inventory which cost £/€175,000 was found to be damaged and it is estimated that it has a net

realisable value of £/€125,000.

(4) On 6

th January 2017 goods costing £/€60,000 were received which had been ordered from a

supplier on 20th

December 2016.

(5) A customer of the company is suing the company for £/€600,000 damages on the basis that a car

which the customer rented from the company in December 2016 was mechanically deficient and

was the cause of the customer being involved in an accident which resulted in the customer

being badly injured. The company’s lawyers are unsure as to the company liability. The court case

will not take place until after the accounts are approved by the directors.

(6) Wages due to casual workers, who were recruited for the busy Christmas period, of

£/€17,000, were due at 31st

December 2016 and not yet accounted for.

Requirement

(a) Prepare the journal entries to show how each of the above items should be dealt with in the

final accounts for the year ended 31st

December 2016. You should use your understanding of FRS 102 in dealing with each item.

14 marks

(b) Compute the adjusted net profit before taxation for the year ended 31 December 2016

taking into account the adjustments made at [a] above.

4 marks

Presentation: 2 marks Total: 20 Marks

Page 13 of 28

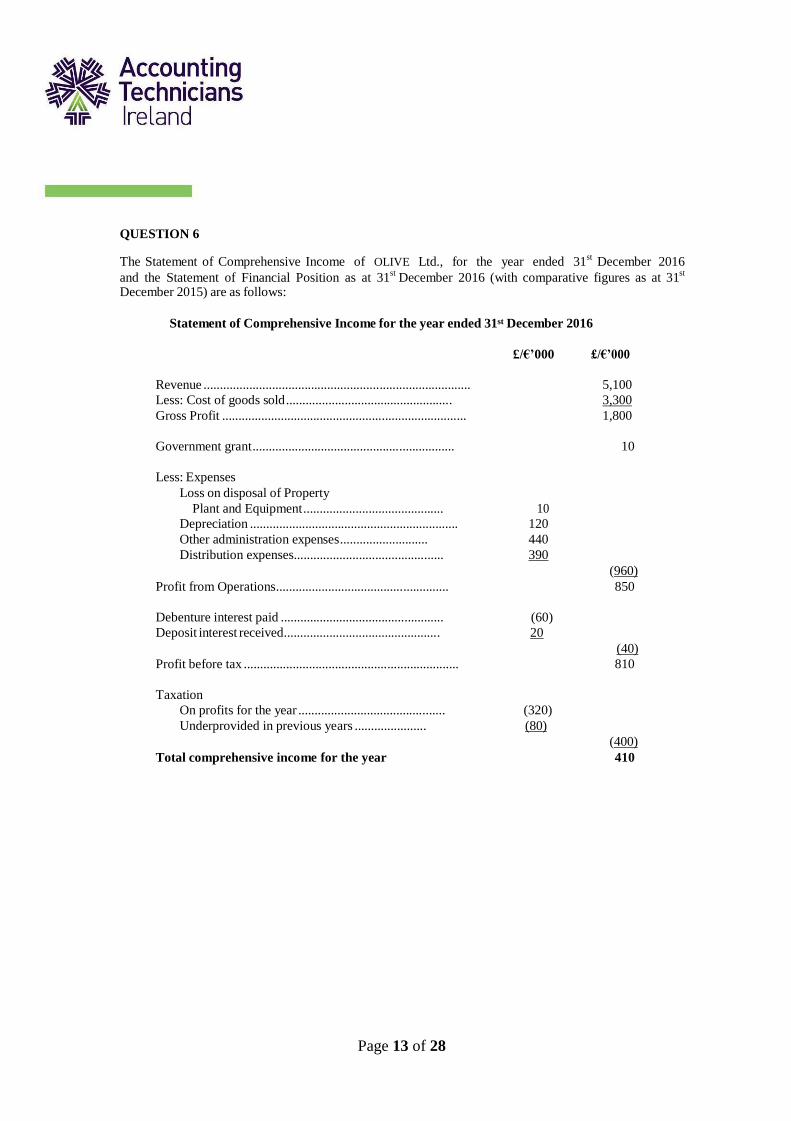

QUESTION 6

The Statement of Comprehensive Income of OLIVE Ltd., for the year ended 31st

December 2016

and the Statement of Financial Position as at 31st

December 2016 (with comparative figures as at 31st

December 2015) are as follows:

Statement of Comprehensive Income for the year ended 31st December 2016

£/€’000 £/€’000

Revenue .................................................................................. 5,100

Less: Cost of goods sold................................................... 3,300

Gross Profit ........................................................................... 1,800

Government grant.............................................................. 10

Less: Expenses

Loss on disposal of Property

Plant and Equipment........................................... 10

Depreciation ................................................................ 120

Other administration expenses........................... 440

Distribution expenses.............................................. 390

(960)

Profit from Operations..................................................... 850

Debenture interest paid .................................................. (60)

Deposit interest received................................................ 20

(40)

Profit before tax .................................................................. 810

Taxation

On profits for the year ............................................. (320)

Underprovided in previous years ...................... (80)

(400)

Total comprehensive income for the year 410

Page 14 of 28

Question 6 cont’d

Statement of Financial Position as at 31ST DECEMBER

2016 2015

£/€’000 £/€’000 £/€’000 £/€’000

Assets

Non current assets

Property, plant and equipment .............. 1,880 1,480

Current assets

Inventories ...................................................... 160 304

Receivables...................................................... 692 520

Bank.................................................................... 596 480

1,448 1,304

Total assets 3,328 2,784

Equity and Liabilities Capital

and reserves

Ordinary share capital................................ 1,100 1,000

Share premium account 100 ‐ Retained profits 970 720

2,170 1,720

Non current liabilities

Debenture stock .............................................. 350 200

Current liabilities

Payables............................................................ 448 384

Taxation............................................................ 320 480

Deferred income (govt grant) ................. 40 ‐

808 864

Total equity and liabilities 3,328 2,784

NOTES to the accounts:

(1) The profit on ordinary activities before taxation has been arrived at after charging:

Auditors remuneration............. 24

Directors remuneration............ 80

Depreciation ................................................... 120

Page 15 of 28

(2) Property plant and equipment:

During the year ended 31st

December 2016, OLIVE Ltd., sold for £/€40,000 an asset which cost it

£/€120,000 in 2013 and which had been depreciated by £/€70,000 at the date of sale. There

were no other sales of property plant and equipment during the year.

(3) A government grant of £/€50,000 relating to plant and equipment purchased during the year was

received.

(4) Dividends paid during the year amounted to £/€160,000.

Requirement

Prepare a Statement of Cash Flow for OLIVE Ltd., for the year ended 31

st December 2016, in accordance

with FRS 102.

18 marks

Presentation: 2 marks

Total: 20 Marks

Page 16 of 28

Accounting Financial Accounting

Sample Paper 3 – Suggested Solutions

NOTE: This sample paper and solutions have been prepared to reflect the provisions of FRS

100 – FRS 102

Page 17 of 28

Solution to question 1

(i)

(a)

The FRC developed the Conceptual Framework to provide guidance for the application of

generally accepted accounting principles to financial transactions. The principles of the

framework form the basis for the development of new accounting standards and the

assessment and revision where necessary of existing ones. The Framework is not an

accounting standard however new standards issued following the publication of the

Framework must be in line with the principles of the Framework. Going forward the

incidents of conflict between the Framework and accounting standards will reduce thus

leading to increased harmonisation in financial accounting regulations. However as the

Framework is not an accounting standard it cannot override the principles of an existing

accounting standard, where a conflict exists the principles as laid out in the standard

must be complied with.

The framework also provides very important definitions which were not previously

defined, including the definitions of such frequently used terms such as asset and

liability. This eliminates the need to provide such definitions in each standard thereby

decreasing the time it takes to develop and publish new standards.

Overall, the Framework promotes a more consistent regulatory environment which

should help not only standard setting bodies but also preparers of financial statements and

users of such financial information.

(b) Definitions

Going concern

Financial statements are normally prepared on the assumption that an entity is a going concern and will continue in operation for the foreseeable future. Foreseeable future is

considered to be twelve months from the date the financial statements are signed. In the event that management decide that it is no longer appropriate to prepare the financial statements on a going concern basis this must be disclosed.

Accruals

Financial statements, with the exception of the cash flow statement, are prepared on the

accruals basis of accounting where transactions are recognised in the period in which they

occur (are earned or accrued) irrespective of when the cash flow arising from these

transactions occurs.

Asset

An asset is a resource controlled by an entity as a result of past events and from which

future economic benefits are expected to flow to the entity. Future economic benefits

represent the potential to contribute to the cash flow of the entity. Examples of assets

include premises, equipment, receivables.

Page 18 of 28

Liability

A liability is a present obligation of the entity arising from past events, the settlement of

which is expected to result in an outflow of resources from the entity. Examples of liabilities

include payables, finance lease obligations, accruals.

(ii)

Accounting Policies

FRS 102 defines Accounting Policies as “the specific principles, bases, conventions, rules and

practices applied by an entity in preparing financial statements.”

An entity should change an accounting policy only if the change:

is required by a Standard or an Interpretation, or

results in the financial statements providing reliable and more relevant

information about the effects of transactions, other events or conditions

on the entity’s financial position, financial performance or cash flows.

Accounting Estimates

Accounting estimates involve judgements on the uncertainties inherent in business

activities which cannot be measured with precision but only estimated.

Examples of items may which require accounting estimates are:

Provision for bad and doubtful debts

Inventory obsolescence

Useful life of depreciable assets

Page 19 of 28

Solution to question 2

(1) C (80,000 *365 / 1,800,0000)

(2)

C

(85,000 * 365 / 1,250,000)

(3)

B

(170,000 +80,000+30,000)/(85,000+60,000+70,000+25,000)

(4)

B

(140,000 + 1,250,000 – 170,000) / ((140,000 + 170,000) /2)

(5)

C

(2,100,000 – (140,000 + 1250,000 – 170,000) = 880,000 *100/210,000

(6)

D

(7)

D

(8)

A

(9)

B

(10)

C

Page 20 of 28

Solution to question 3

Cable Ltd.

Statement of Comprehensive Income for the year ended 31 December 2016

£/€’000

Sales Revenue (W.1)

4,421

Cost of sales (W.2)

2,200

Gross profit

2,221

Other Income

20

Distribution costs (W.3)

(400) Administrative expenses (W.4) (610)

1,231

Interest received

35 Interest paid (W.5) (80)

Profit before tax 1,186

Tax expense

(593)

Profit on ordinary activities after tax

593

CABLE Limited

Statement of Changes in Equity for the year ended 31 December 2016

Share

Capita Share

Premiu Retained

earnings Genera

l

Total

£/€'000 £/€'000 £/€'000 £/€'000 £/€'000

As at 1 January 2016

2,200

180

74

260

2,714

Profit for the year 593 593

Ordinary dividends (w.6) (286) (286)

2,200 180 381 260 3,021

Page 21 of 28 AFA Sample Paper 3

Solution to question 3(cont ’ d)

Workings

(1) Sales revenue

£/€’000 £/€’000

Sales per T/B 4,500

Less: sales returns 79

4,421

(2) Cost of sales

Opening inventory 180

Purchases 2,400

Less : purchases returns (160)

2,240

Add : goods purchased on 28/12 70 2,310

2,490

Less : Closing Inventory

Per physical count (220)

Add : not accounted for (70)

(290)

2,200

(3) Distribution expenses

Per T/B

Depreciation : Motor Veh. 60

400

(4) Administrative expenses

Per T/B 450

Add : Depreciation : Premises 78

Plant and Mach. 82

(5) Interest paid

610

Bank overdraft interest 60

Debenture interest Paid 10

Due 10

20

80

Solution to question 3(cont ’ d)

Page 22 of 28 AFA Sample Paper 3

(6) Dividend

£/€’000

Interim dividend per trial balance 66

Final dividend paid 220

Total dividend 286

(7) Other Income

Training Grant receivable 20

Page 23 of 28 AFA Sample Paper 3

Solution to question 4

(a) Statement of adjusted profit for the year ended 31 December 2016

€/£ €/£

Net profit as per draft accounts 88,000

(1) Depreciation:

Leasehold Premises 5,000

Plant and Machinery 26,000

Furniture & Fittings 5,000

(36,000)

(2) Wages owing (14,000)

(3) Rent prepaid 7,000

Adjusted net profit 45,000

(b) Appropriation account for the year ended 31 December 2016

Net profit 45,000

Less:

Partner’s salaries

Geoff 5,000

Henry 6,000

Ian 7,000 (18,000)

Interest on capital Geoff 4,000 Henry 3,500 Ian 3,500 (11,000)

Appropriated as follows:

Geoff 8,000

Less: to meet guarantee (1,000)

Henry 4,000

Less: to meet guarantee (1,000)

Ian 4,000

Add: to meet guarantee 2,000

16,000

7,000

3,000

6,000

16,000

Page 24 of 28 AFA Sample Paper 3

Partners Current Accounts

Geoff Henry Ian Geoff Henry Ian

Balance b/d 20,000 Bal b/d 16,000 10,000

Salaries 5,000 6,000 7,000

Interest on capital 4,000 3,500 3,500

Share of profits 7,000 3,000 6,000 Balance c/d 32,000 26,500 Balance c/d 7,500

32,000 20,000 26,500 32,000 20,000 26,500 Balance b/d 7,500 Balance b/d 32,000 26,500

Solution to Q4 continued overleaf

Page 25 of 28 AFA Sample Paper 3

Non-current assets

€/£ €/£ €/£

Leasehold Premises 250,000 55,000 195,000 Plant and machinery 130,000 91,000 39,000 Furniture & Fittings 25,000 10,000 15,000

405,000 156,000 249,000

Current Assets

Inventory 30,000 Receivables 26,000 Prepaid rent 7,000 Bank 12,000

75,000 324,000

Partners capital accounts Geoff

80,000

Henry 70,000 Ian 70,000

220,000

Partners current accounts

Geoff 32,000 Henry (7,500) Ian 26,500 51,000

Current liabilities Payables

26,000

Loan from Simon 13,000 Accrued wages and salaries 14,000

53,000 324,000

(d)

Statement of Financial Position as at 31 December 2016

Cost Accumulated

NBV Depreciation

Page 26 of 28 AFA Sample Paper 3

(3) Inventory (SOCI) 50,000

Inventory ( SOFP ) 50,000

(4)

Being reduction of inventory from cost to NRV

No adjustment ; a non adjusting event as per FRS 102

Solution to question 5

(a) Journal

Dr. Cr.

£/€ £/€

(1) Irrecoverable Receivable a/c (SOCI) 80,000

Receivable(SOFP) 80,000

Being write off of an irrecoverable receivable

(2) Deferred Income (SOFP) 50,000

Other Income (SOCI) 50,000

Being correction of mis‐posting;‐ Revenue grant posted in error to Deferred Grants

(5) Contingent liability, a possible but uncertain obligation, no provision required as per

FRS102. Show as a note to the accounts.

(6) Wages expense (SOCI) 17,000

Accrued expense (SOFP) 17,000

(Accounting for wages accrued due at year end not provided for)

(b) Adjusted net profit before tax

£/€ £/€

Profit before taxation per draft accounts 350,000

Adjustments :

(1) Irrecoverable Receivable (80,000)

(2) Training grant 50,000

(3) Inventory write off (50,000)

(6) Wages expense (17,000)

(97,000)

Adjusted net profit 253,000

Page 27 of 28 AFA Sample Paper 3

Cash generated from operations .......................................................... 1,006 Interest paid................................................................................................... (60) Income tax paid (w.1)................................................................................ (560)

Net cash flow from operating activities.............................................

386

Cash flow from investing activities:

Solution to question 6

OLIVE Ltd., Statement of Cash Flow for the year ended 31st December 2016

Cash flow from operating activities:

£/€’000 £/€’000

Profit on ordinary activities before interest 850

Adjustment for:

Government grant..........................................................................

(10)

Depreciation ............................................................................ 120

Loss on disposal of property plant and equipment ....... 10

Operating profit from working capital changes:

Decrease in inventories ........................................................... 144

Increase in receivables ................................................................

(172)

Increase in payables......................................................................

64

120

970

36

Purchases of property plant and equipment (w.2) ....... (570)

Proceeds of sale of property, plant and equipment....... 40

Interest received ......................................................................... 20

Net cash used in investing activities ................................................... (510) Cash flow from financing activities:

(124)

Proceeds from issue of shares (100+100) ................................ 200 Government grant received ....................................................... 50

Proceeds from long term borrowing ........................................ 150

Dividends paid ................................................................................

(160)

240

Net increase in cash and cash equivalents ....................................... 116 Cash and cash equivalents at beginning of year ............................ 480

Cash and cash equivalents at end of year ......................................... 596

Page 28 of 28 AFA Sample Paper 3

Solution to question 6 (Cont’d.)

WORKINGS

(1) Income tax paid

£/€’000

Due at 1st January 2016 .............................................. 480

Charge for year ........................................................... 400

880

Due at 31st December 2016 ........................................ 320

Income tax paid .......................................................... 560

(2) Purchase of property plant and equipment

£/€’000

Net book amount at 1st January 2016 ................ 1,480

Less: net book amount of sale

During year (£/€120,000 ‐ £/€70,000) ........... (50)

1430

Depreciation charge for year ................................. (120)

1310

Net book amount at 31st December 2016 ........ 1880

Purchases during year…………………… 570