Embed Size (px)

Citation preview

Support document: Internet banking functionality for South African Generation-Y users

Examples of functionality innovation demonstrated by early-

adopter banks

1. Personal financial management (PFM)

Barclays Bank in the United Kingdom is one of the early adopters of the money management

functionality. According to (Niemeyer 2011), Barclaycard, the credit card division of

Barclays bank, has implemented a secure website named; Mybarclaycard. Mybarclaycard

allows users to manage their credit card spending online. Upon login, users are able to see:

1. A visual representation of their card

2. Automatic categorisation of their spending, and even assign more familiar categories

to these

3. Graphical representation of their spending patterns, from which they can select the

best manner to view this information

Fig 1.1. Spending graphs and detailed breakdown of expenditure - Mybarclaycard

User are able to view their spending patterns in different

types of graphs, and also gain an in-depth analysis of their

spending by selecting to view their spending breakdown

according to specific categories.

Support document: Internet banking functionality for South African Generation-Y users

2

2. Multi-device banking

This growing need for mobility and instant utility from users has led to the recent explosion

of mobile technologies like responsive design and the development of mobile applications,

commonly known as “apps”. Responsive design, also known as adaptive design, allows a

site to automatically format to a range of screen sizes, from desktop to smartphone, and any-

thing in between. The navigation, design and layout gracefully shift and resize without

breaking, which ensures a site is always usable, on whatever device the user views it on

(Kissoyan 2012). A number of organisations have started adopting this manner of design;

Jyske bank is one of them. Figure 2.1 below depicts how the organisation’s website renders

the responsive interface across devices of varying sizes.

Fig 2.1 Jyske bank’s responsive website rendered on desktop, tablet and smartphone devices

The banking industry in South Africa has recently began to make great progress in the mobile

app sphere, with 3 out of the 5 biggest banks in South Africa recently launching apps that

simplify the transactional banking needs of their customers. As a support channel to the

Internet banking offering, FNB, Standard Bank and Nedbank offer their customers the ability

to perform key transactional tasks like viewing balances, making payments, transferring

money, buying pre-paid airtime on the go, all from the convenience of their smart device.

Support document: Internet banking functionality for South African Generation-Y users

3

Fig 2.2: Examples of transactional mobile apps from FNB, Standard Bank and Nedbank

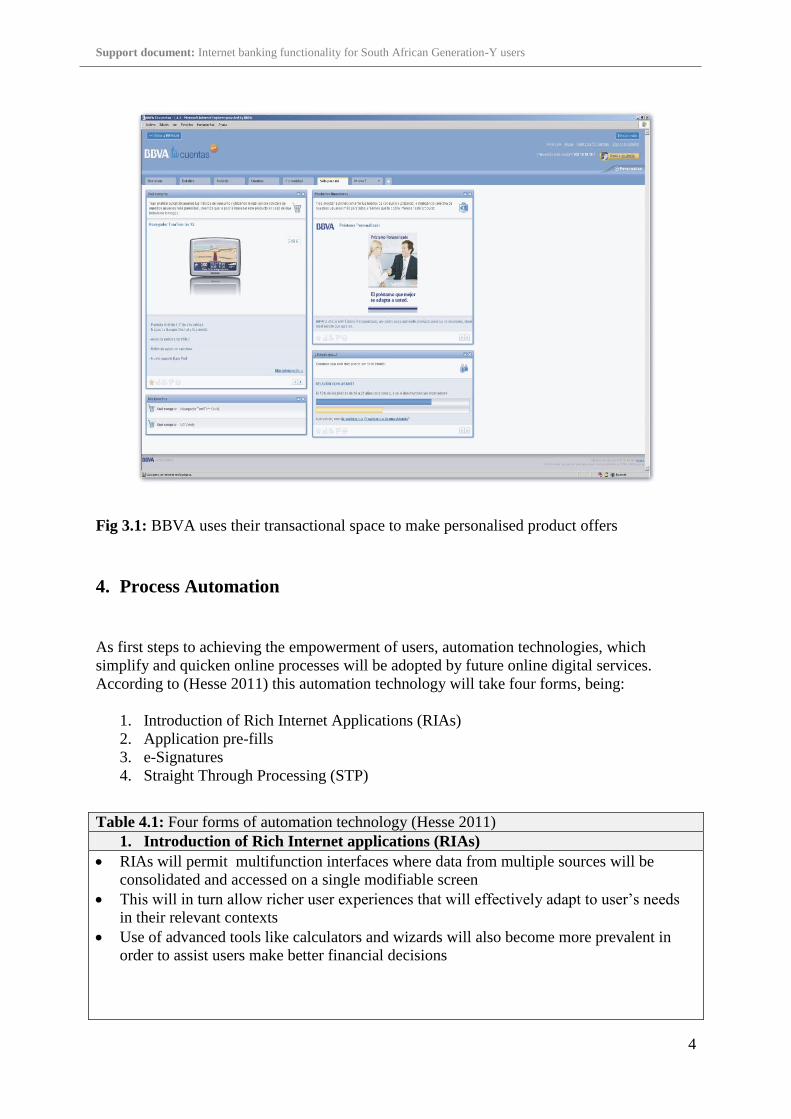

3. Personalisation

Hesse (2011) foresees that organisations will make use of available customer information to

personalise the financial website experience for customers. He outlines 4 different levels this

type of functionality will materialise in. Available customer information will be used to

personalise:

1. The website content

2. The website’s navigation

3. The website’s presentation

4. Products being marketed to users

A tab on BBVA’s transactional website is dedicated to personalised product offers

The website can make personalised offers for both financial and non-financial

products (e.g. The customer is sold a GPS navigator as seen on the below example,

rather than a credit card offered by the bank)

Because of the website ability to also customise the content, the user can at any point

disable or remove this sales tab should they wish not to be marketed to

Support document: Internet banking functionality for South African Generation-Y users

4

Fig 3.1: BBVA uses their transactional space to make personalised product offers

4. Process Automation

As first steps to achieving the empowerment of users, automation technologies, which

simplify and quicken online processes will be adopted by future online digital services.

According to (Hesse 2011) this automation technology will take four forms, being:

1. Introduction of Rich Internet Applications (RIAs)

2. Application pre-fills

3. e-Signatures

4. Straight Through Processing (STP)

Table 4.1: Four forms of automation technology (Hesse 2011)

1. Introduction of Rich Internet applications (RIAs)

RIAs will permit multifunction interfaces where data from multiple sources will be

consolidated and accessed on a single modifiable screen

This will in turn allow richer user experiences that will effectively adapt to user’s needs

in their relevant contexts

Use of advanced tools like calculators and wizards will also become more prevalent in

order to assist users make better financial decisions

Support document: Internet banking functionality for South African Generation-Y users

5

2. Application Pre-fill

Pre-fills will search internal and external databases in real time and return customer

information for ease of use in advice tools and application processes

This will dramatically reduce applications and transacting time for banking customers

3. eSignatures

eSignatures will replace legally binding handwritten signatures to indicate approval or

finalisation of an online transaction

This will in return minimise the time and effort required to complete online transactions

4. Straight through processing (STP)

This means that transactions will automate from start to finish, allowing users to complete

transactions without any human intervention from the organisation itself regardless of any

outstanding requirements or minor account restrictions detected

This will automatically translate to less visits to the branch

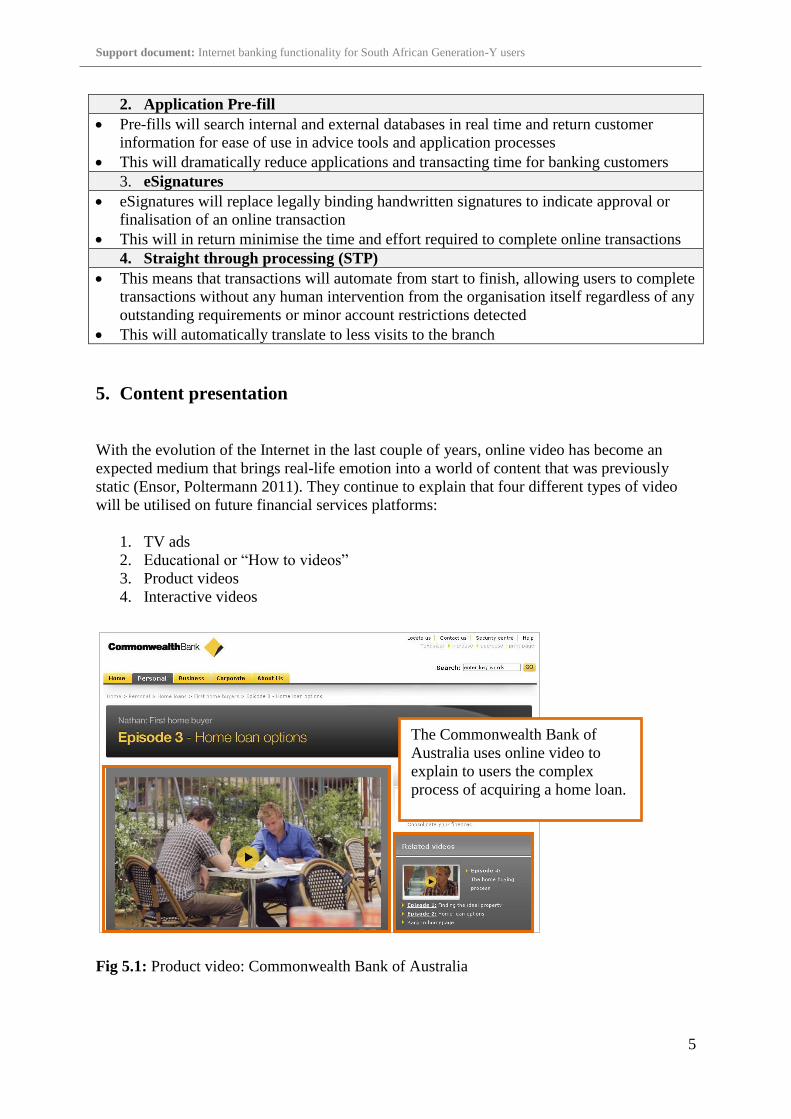

5. Content presentation

With the evolution of the Internet in the last couple of years, online video has become an

expected medium that brings real-life emotion into a world of content that was previously

static (Ensor, Poltermann 2011). They continue to explain that four different types of video

will be utilised on future financial services platforms:

1. TV ads

2. Educational or “How to videos”

3. Product videos

4. Interactive videos

Fig 5.1: Product video: Commonwealth Bank of Australia

The Commonwealth Bank of

Australia uses online video to

explain to users the complex

process of acquiring a home loan.

Support document: Internet banking functionality for South African Generation-Y users

6

Fig 5.2: Educational video: Easy Credit financial services provider

6. Human Touch

A case study by Montez (2012) depicts a human touch innovation recently implemented by

Bank Hapoalim. The bank is one of Israel’s largest, with approximately 300 branches. In a

country of an estimated 7.5 million people, Hapoalim’s Internet banking platform has more

than 1 million users, showing its significance in this market.

In early 2011, the bank introduced a new service, called Poalim Connect, which was aimed at

providing customers who mostly or entirely use digital channels with the ability to

communicate with a personal banker, or an extended team of bankers during working hours.

The introduction of this functionality has led to a number of successes being witnessed by the

bank. The bank has witnessed improved customer satisfaction for both human and digital

touch points. When Poalim Connect customers, were surveyed, 92% of the respondents were

satisfied with the service they received from the personal banking team through the interface,

85% were satisfied with Poalim Connect, and 77% would recommend the service to others.

Moreover, customer engagement increased, with more than 25,000 meetings having been

scheduled by bankers, and over 50 000 online conversations already held with banking

customers.

The adviser on the Easy Credit

website changes her advice based on

the data the user fills in.

Support document: Internet banking functionality for South African Generation-Y users

7

7. Social banking

Naidu (2010) suggests that banks that engage with social media ultimately win more

customers and increase profits. She continues that although transacting on social media

platforms is still shunned upon by most Internet banking users, the reluctance of use can be

compared to the beginning stages of Internet banking. She outlines that very similar concerns

of trust and security were raised, and based on the use of Internet banking today; these

concerns have observably been overcome.

Locally, FNB has recently joined ranks to become one of the selected financial institutions

worldwide to offer customers banking functionalities through the social networking website,

Facebook. By linking their cellphone banking profile, with their Facebook profile, FNB

customers have access to basic transactional capabilities, without having to start a separate

browsing session.

The contact panel allows users to connect with

bankers via SMS, email or online chat.

Support document: Internet banking functionality for South African Generation-Y users

8

Fig 7.1: Transactional banking within Facebook – FNB

8. References

Ensor, B & Poltermann, S 2011, Using video to drive online financial services sales,

Forrester Research Inc, Cambridge, Massachusetts

Hesse, A 2011, Next-generation digital financial services - Make it simple, ubiquitous,

personal, empowering, and reassuring, Forrester Research Inc, Cambridge, Massachusetts

Kissoyan, V 2012, To App or not to App? Why responsive design is key to your mobile

strategy, viewed 1 May 2012, http://www.lokion.com/lokion/to-app-or-not-to-app-why

responsive-design-is-key-to-your-mobile-strategy/

Montez, T 2012, Case study: Hapoalim Injects a human touch into digital banking, Forrester

Research Inc, Cambridge, Massachusetts

Naidu, P 2010, Social media and its application within the banking industry, MSc Thesis,

University of Pretoria

Users have access to basic

transactional capabilities, without

having to exit the Facebook platform.

Support document: Internet banking functionality for South African Generation-Y users

9

Niemeyer, V 2011, Case Study: How Barclaycard helps customers manage their spending,

Forrester Research Inc, Cambridge, Massachusetts