Embed Size (px)

Citation preview

May 2013

Achmea Investor Presentation

“The leading Dutch insurance Company with strong brands, multi-channel distribution strategy, well diversified product range and a conservative investment profile”

414807_Roadshow 2013.ppt

1

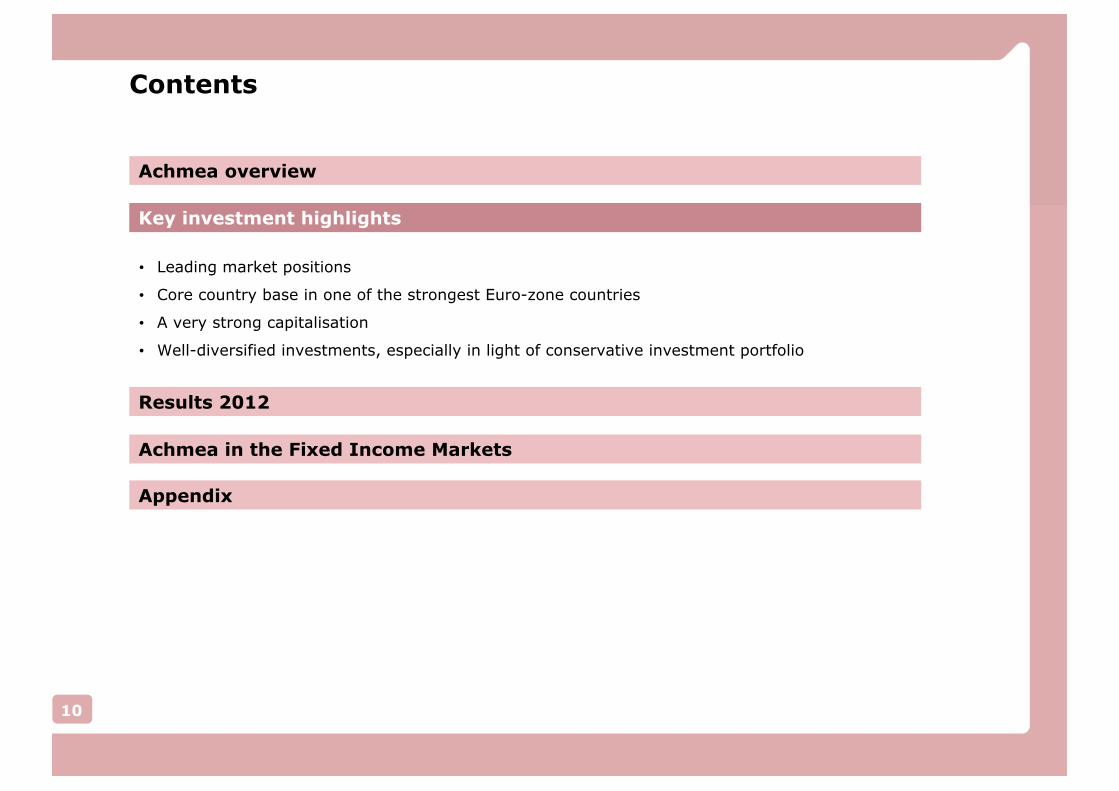

Contents

Achmea overview

Key investment highlights

Results 2012

Achmea in the Fixed Income Markets

• Leading market positions

• Core country base in one of the strongest Euro-zone countries

• A very strong capitalisation

• Well-diversified investments, especially in light of conservative investment portfolio

Appendix

414807_Roadshow 2013.ppt

2

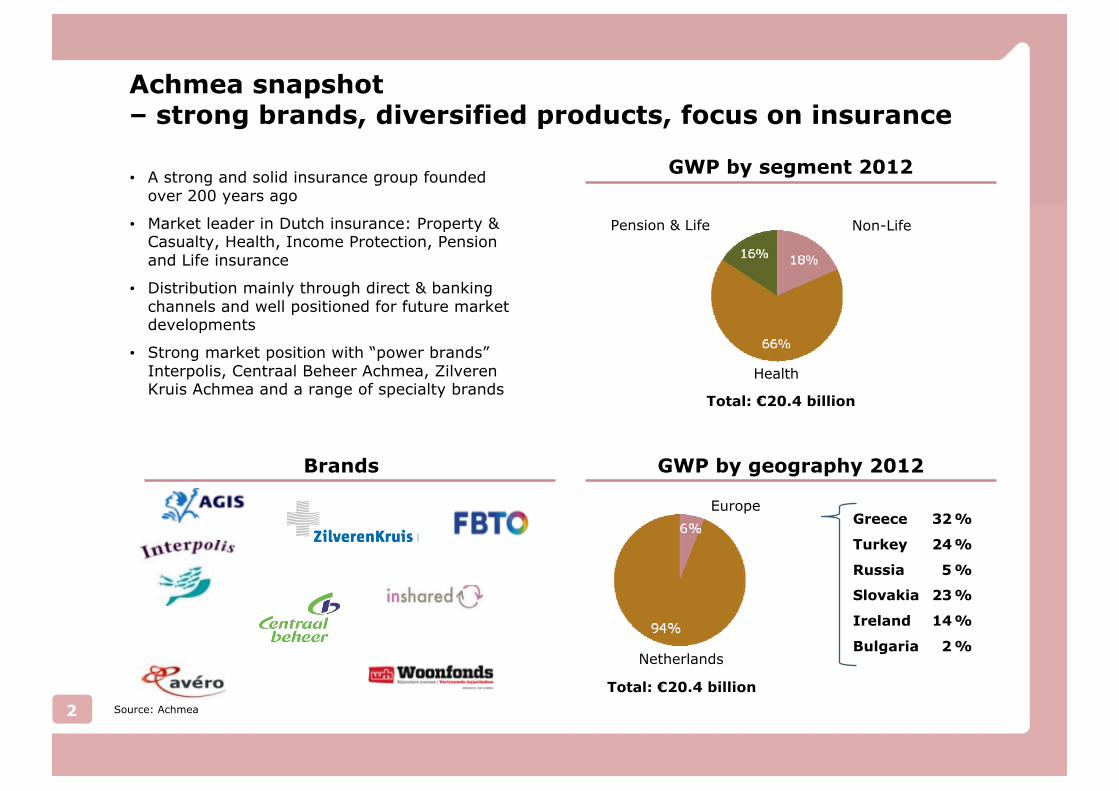

Achmea snapshot – strong brands, diversified products, focus on insurance

• A strong and solid insurance group founded over 200 years ago

• Market leader in Dutch insurance: Property & Casualty, Health, Income Protection, Pension and Life insurance

• Distribution mainly through direct & banking channels and well positioned for future market developments

• Strong market position with “power brands”Interpolis, Centraal Beheer Achmea, Zilveren Kruis Achmea and a range of specialty brands

Netherlands

Europe

Health

Pension & Life Non-Life

GWP by segment 2012

GWP by geography 2012

Total: €20.4 billion

Total: €20.4 billion

Greece 32 %

Turkey 24 %

Russia 5 %

Slovakia 23 %

Ireland 14 %

Bulgaria 2 %

Brands

Source: Achmea

414807_Roadshow 2013.ppt

3

Ownership structure – stability through two cornerstone shareholders

ACHMEA ASSOCIATION

65.3%

RABOBANK NETHERLANDS

29.2%

OTHER5.5%

PREFERENCESHAREHOLDERS

ACHMEA TUSSENHOLDING

5.5%

ORDINARYSHARES94.5%

Source: Achmea

414807_Roadshow 2013.ppt

4

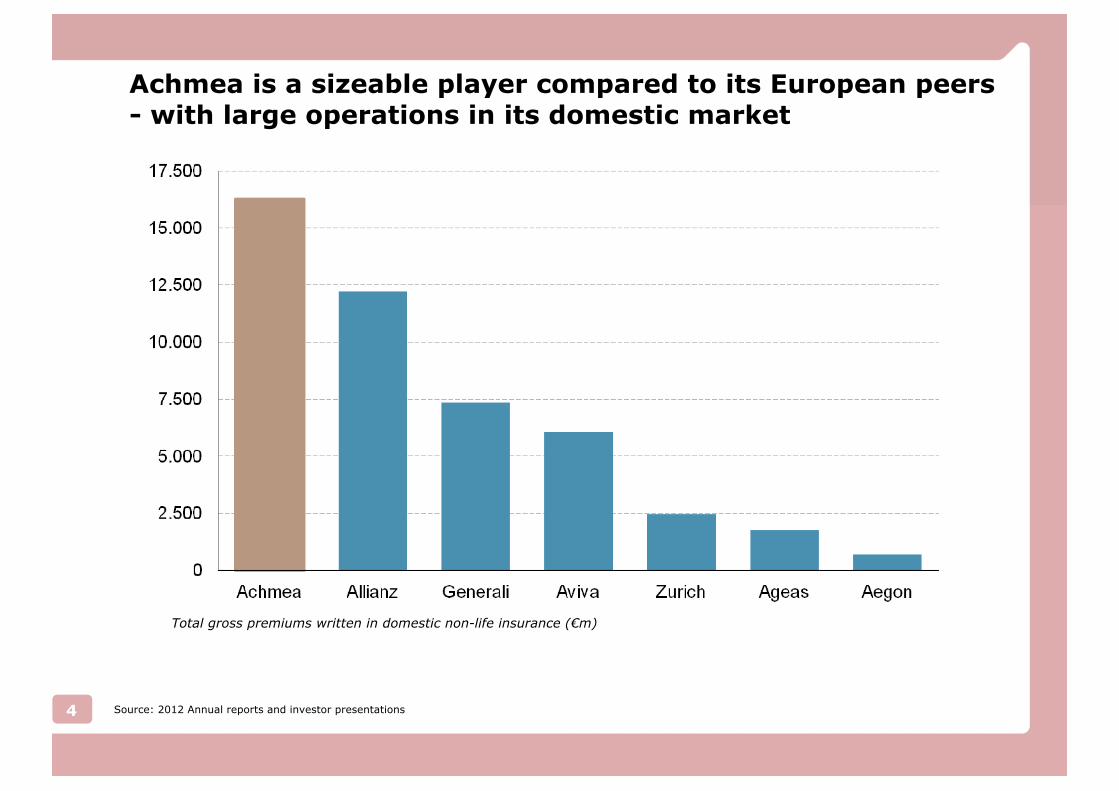

Achmea is a sizeable player compared to its European peers- with large operations in its domestic market

Source: 2012 Annual reports and investor presentations

Total gross premiums written in domestic non-life insurance (€m)

414807_Roadshow 2013.ppt

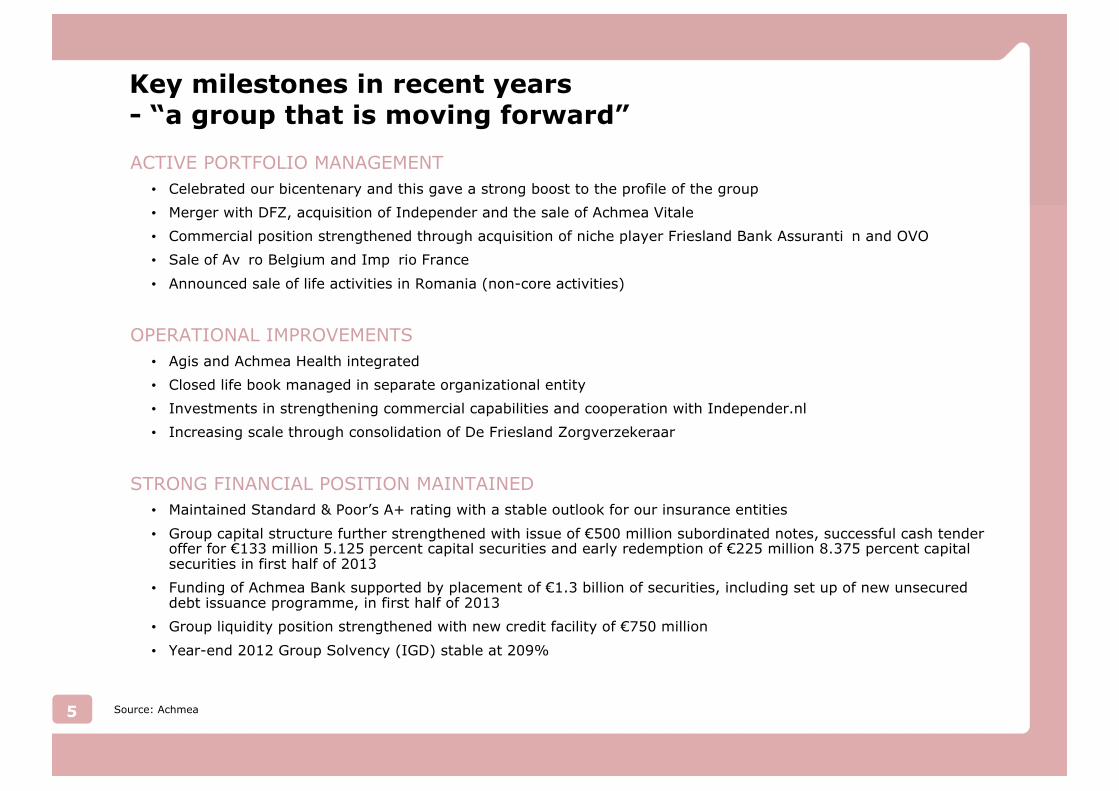

ACTIVE PORTFOLIO MANAGEMENT

• Celebrated our bicentenary and this gave a strong boost to the profile of the group

• Merger with DFZ, acquisition of Independer and the sale of Achmea Vitale

• Commercial position strengthened through acquisition of niche player Friesland Bank Assurantiën and OVO

• Sale of Avéro Belgium and Império France

• Announced sale of life activities in Romania (non-core activities)

OPERATIONAL IMPROVEMENTS

• Agis and Achmea Health integrated

• Closed life book managed in separate organizational entity

• Investments in strengthening commercial capabilities and cooperation with Independer.nl

• Increasing scale through consolidation of De Friesland Zorgverzekeraar

STRONG FINANCIAL POSITION MAINTAINED

• Maintained Standard & Poor’s A+ rating with a stable outlook for our insurance entities

• Group capital structure further strengthened with issue of €500 million subordinated notes, successful cash tender offer for €133 million 5.125 percent capital securities and early redemption of €225 million 8.375 percent capital securities in first half of 2013

• Funding of Achmea Bank supported by placement of €1.3 billion of securities, including set up of new unsecured debt issuance programme, in first half of 2013

• Group liquidity position strengthened with new credit facility of €750 million

• Year-end 2012 Group Solvency (IGD) stable at 209%

5 Source: Achmea

Key milestones in recent years- “a group that is moving forward”

414807_Roadshow 2013.ppt

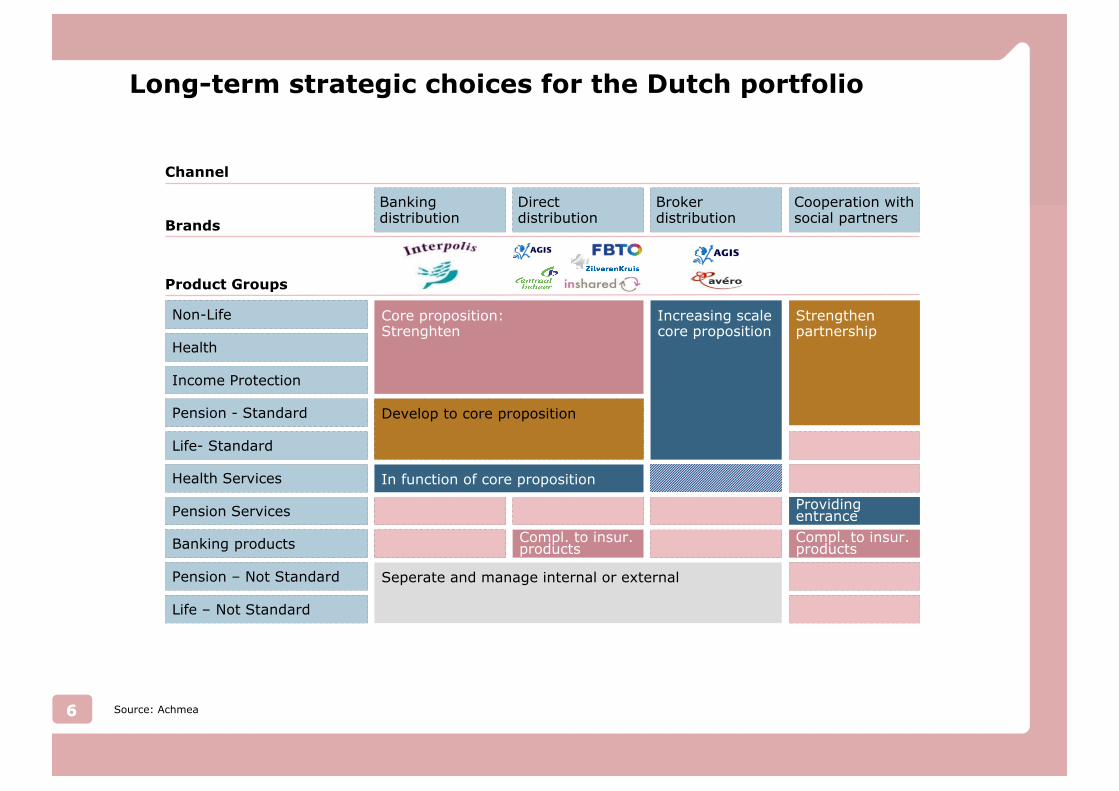

Seperate and manage internal or external

Compl. to insur. products

In function of core proposition

Develop to core proposition

Core proposition: Strenghten

Directdistribution

Brokerdistribution

Bankingdistribution

Cooperation with social partners

Channel

Product Groups

Increasing scale core proposition

Strengthen partnership

Providing entrance

Compl. to insur. productsBanking products

Health Services

Pension Services

Life – Not Standard

Pension – Not Standard

Pension - Standard

Life- Standard

Non-Life

Health

Income Protection

Brands

66 Source: Achmea

Long-term strategic choices for the Dutch portfolio

414807_Roadshow 2013.ppt

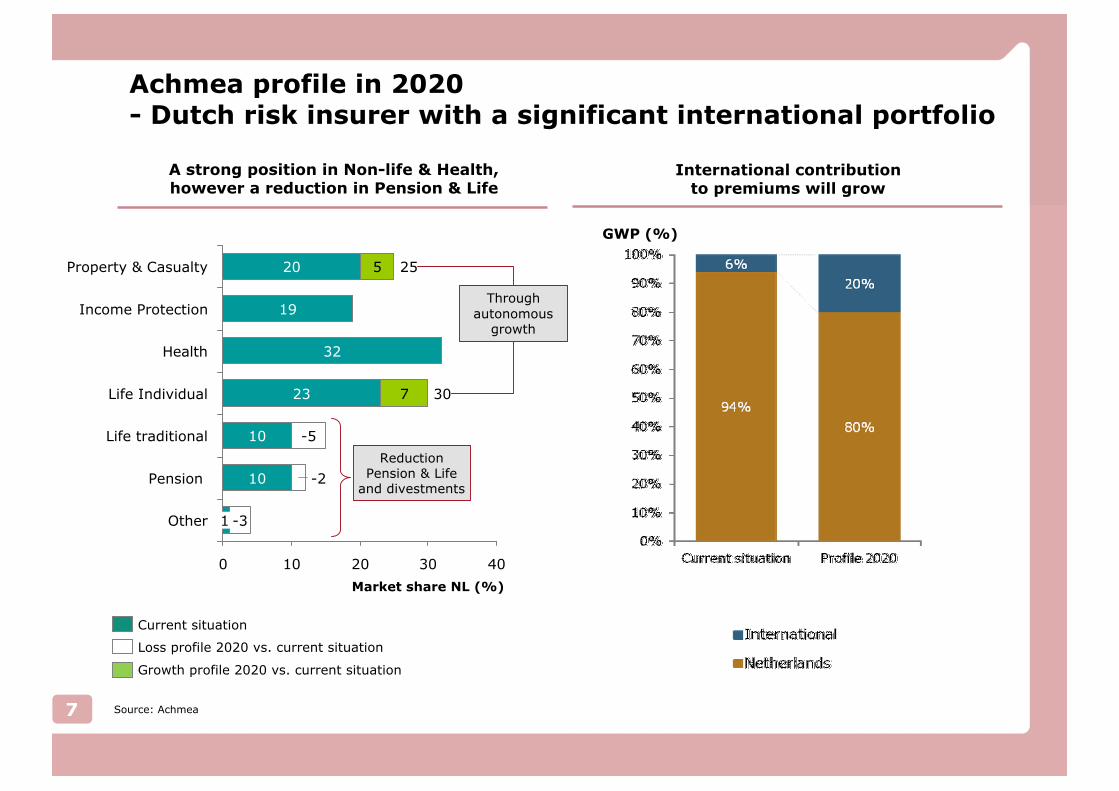

Market share NL (%)

403020100

Other 1 -3

Pension 10 -2

Life traditional 10 -5

Life Individual 3023 7

Health 32

Income Protection 19

Property & Casualty 2520 5

Through autonomous

growth

Reduction Pension & Life

and divestments

Growth profile 2020 vs. current situation

Current situation

Loss profile 2020 vs. current situation

A strong position in Non-life & Health, however a reduction in Pension & Life

International contribution to premiums will grow

Source: Achmea7

GWP (%)

Achmea profile in 2020- Dutch risk insurer with a significant international portfolio

414807_Roadshow 2013.ppt

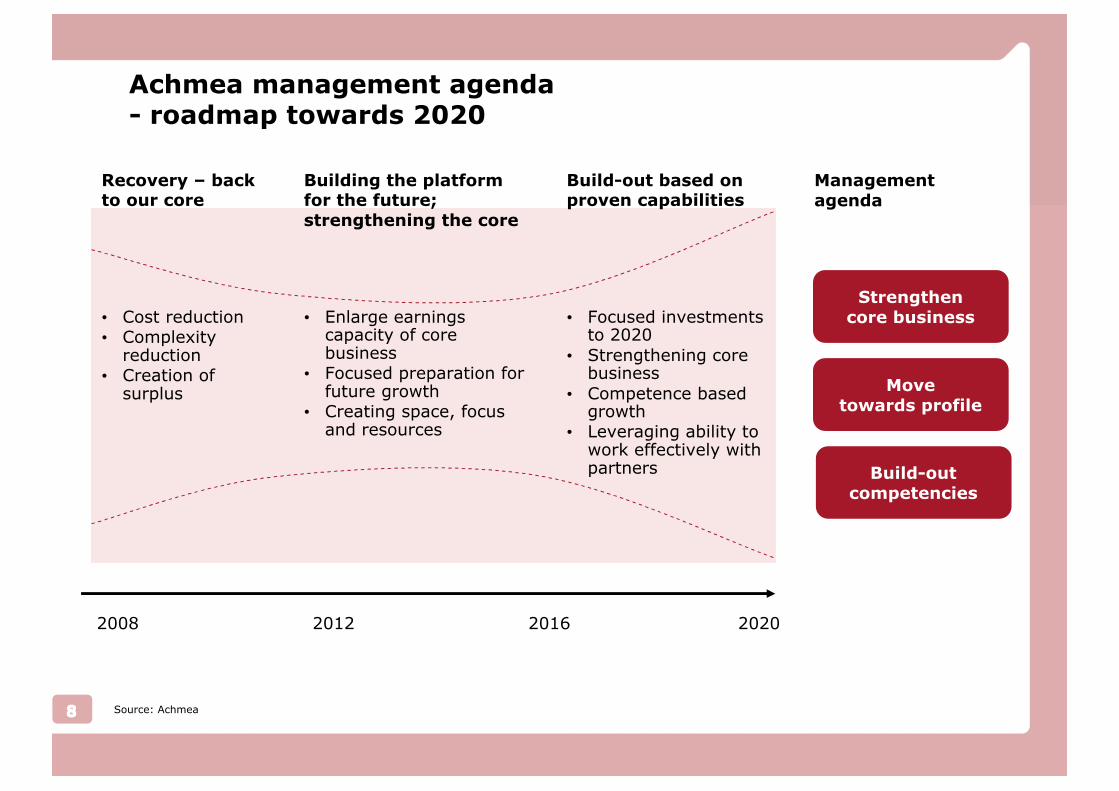

Achmea management agenda- roadmap towards 2020

202020122008 2016

Recovery – back to our core

• Cost reduction• Complexity

reduction• Creation of

surplus

Building the platform for the future; strengthening the core

• Enlarge earningscapacity of core business

• Focused preparation for future growth

• Creating space, focus and resources

Build-out based on proven capabilities

• Focused investments to 2020

• Strengthening core business

• Competence based growth

• Leveraging ability to work effectively with partners

88 Source: Achmea

Managementagenda

Versterken van het huidige bedrijf

Strengthencore business

Movetowards profile

Build-outcompetencies

414807_Roadshow 2013.ppt

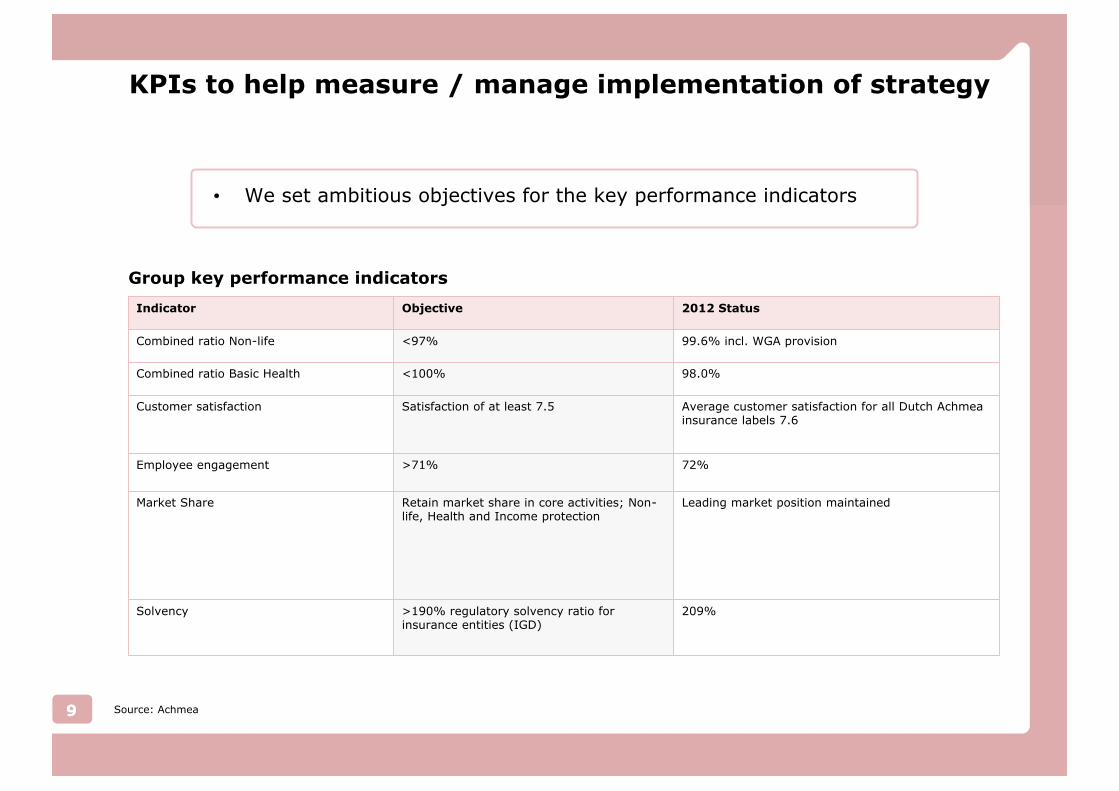

Indicator Objective 2012 Status

Combined ratio Non-life <97% 99.6% incl. WGA provision

Combined ratio Basic Health <100% 98.0%

Customer satisfaction Satisfaction of at least 7.5 Average customer satisfaction for all Dutch Achmea insurance labels 7.6

Employee engagement >71% 72%

Market Share Retain market share in core activities; Non-life, Health and Income protection

Leading market position maintained

Solvency >190% regulatory solvency ratio for insurance entities (IGD)

209%

Group key performance indicators

• We set ambitious objectives for the key performance indicators

99 Source: Achmea

KPIs to help measure / manage implementation of strategy

414807_Roadshow 2013.ppt

10

Contents

Achmea overview

Key investment highlights

Results 2012

Achmea in the Fixed Income Markets

• Leading market positions

• Core country base in one of the strongest Euro-zone countries

• A very strong capitalisation

• Well-diversified investments, especially in light of conservative investment portfolio

Appendix

414807_Roadshow 2013.ppt

11

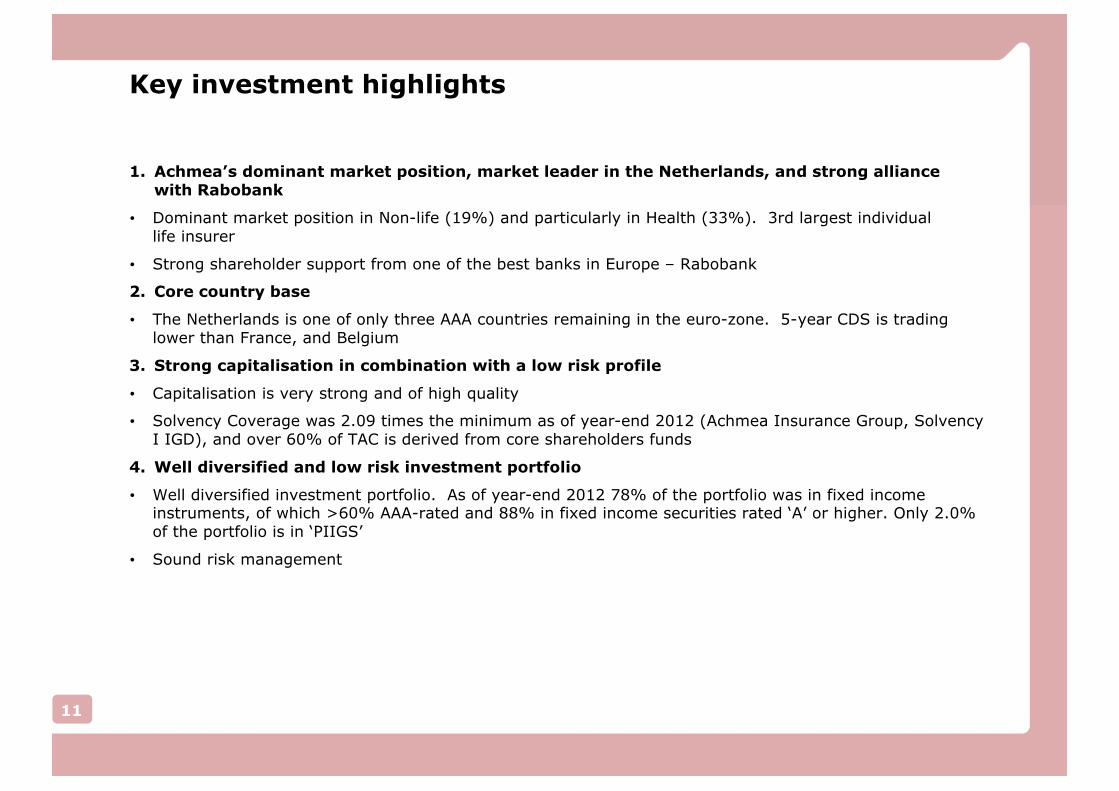

Key investment highlights

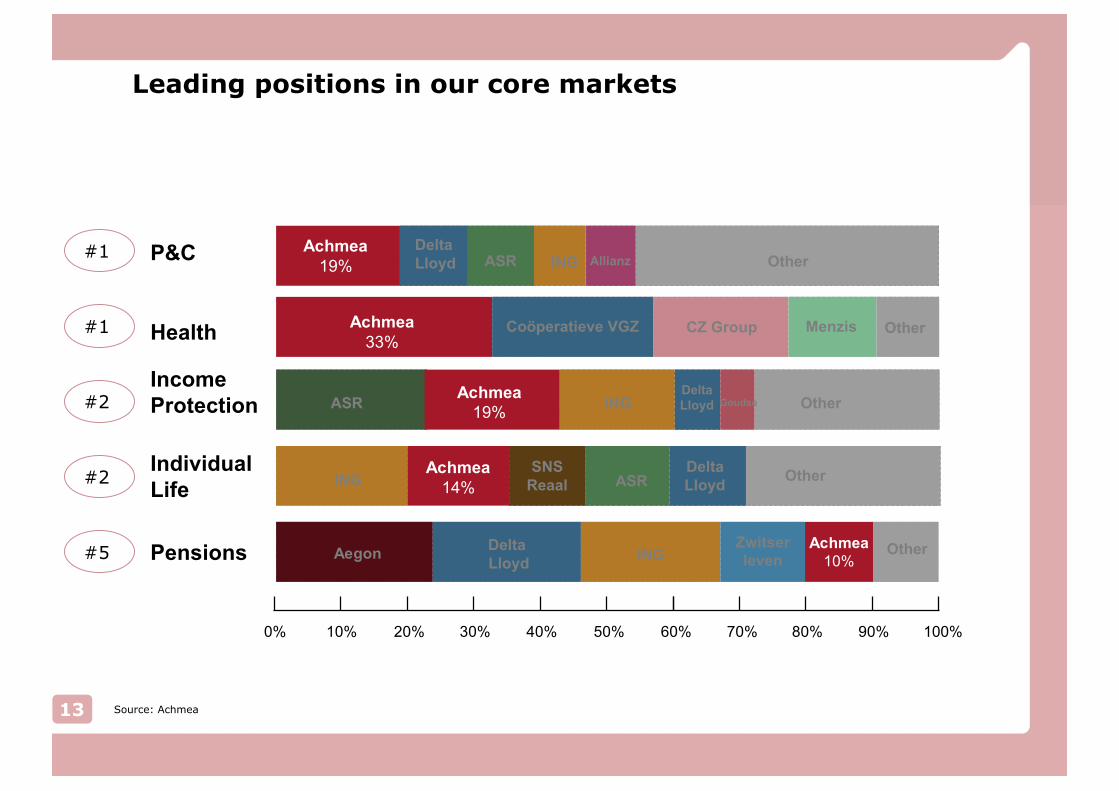

1. Achmea’s dominant market position, market leader in the Netherlands, and strong alliance with Rabobank

• Dominant market position in Non-life (19%) and particularly in Health (33%). 3rd largest individual life insurer

• Strong shareholder support from one of the best banks in Europe – Rabobank

2. Core country base

• The Netherlands is one of only three AAA countries remaining in the euro-zone. 5-year CDS is trading lower than France, and Belgium

3. Strong capitalisation in combination with a low risk profile

• Capitalisation is very strong and of high quality

• Solvency Coverage was 2.09 times the minimum as of year-end 2012 (Achmea Insurance Group, Solvency I IGD), and over 60% of TAC is derived from core shareholders funds

4. Well diversified and low risk investment portfolio

• Well diversified investment portfolio. As of year-end 2012 78% of the portfolio was in fixed income instruments, of which >60% AAA-rated and 88% in fixed income securities rated ‘A' or higher. Only 2.0% of the portfolio is in ‘PIIGS’

• Sound risk management

414807_Roadshow 2013.ppt

12

Contents

Achmea overview

Key investment highlights

Results 2012

Achmea in the Fixed Income Markets

• Leading market positions

• Core country base in one of the strongest Euro-zone countries

• A very strong capitalisation

• Well-diversified investments, especially in light of conservative investment portfolio

Appendix

414807_Roadshow 2013.ppt

Menzis

80%70%60%50%40%30%20% 100%90%10%0%

Income Protection ASR ING

DeltaLloyd

Individual Life

ASRING

Delta Lloyd

Health

ING

CZ Group

Pensions Aegon

ASR INGP&C Delta Lloyd Allianz

Leading positions in our core markets

Other

Other

Other

Other

Other

Achmea33%

Achmea19%

Achmea19%

Zwitserleven

Achmea14%

Coöperatieve VGZ

Delta Lloyd

SNSReaal

Achmea10%

Goudse

DeltaLloyd

Source: Achmea

#1

#1

#2

#2

#5

13

414807_Roadshow 2013.ppt

14

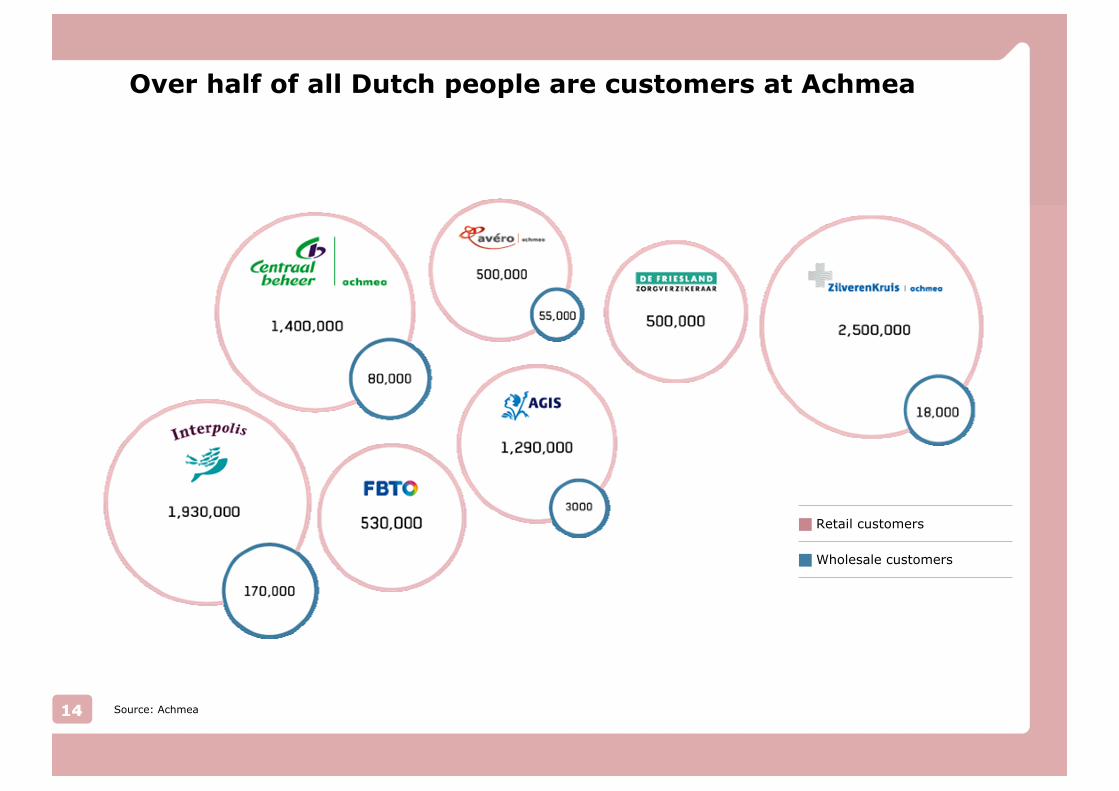

Over half of all Dutch people are customers at Achmea

g Retail customers

g Wholesale customers

14 Source: Achmea

414807_Roadshow 2013.ppt

15

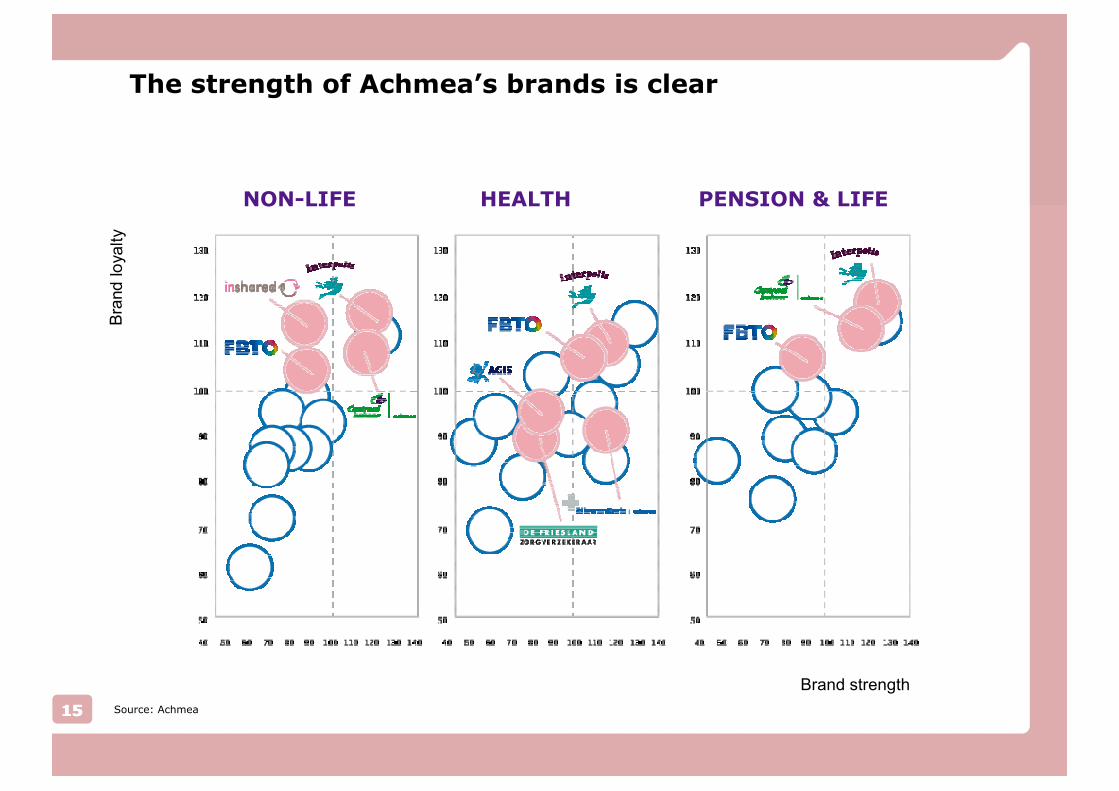

The strength of Achmea’s brands is clear

NON-LIFE HEALTH PENSION & LIFE

Bra

nd

loy a

lty

Brand strength

15 Source: Achmea

414807_Roadshow 2013.ppt

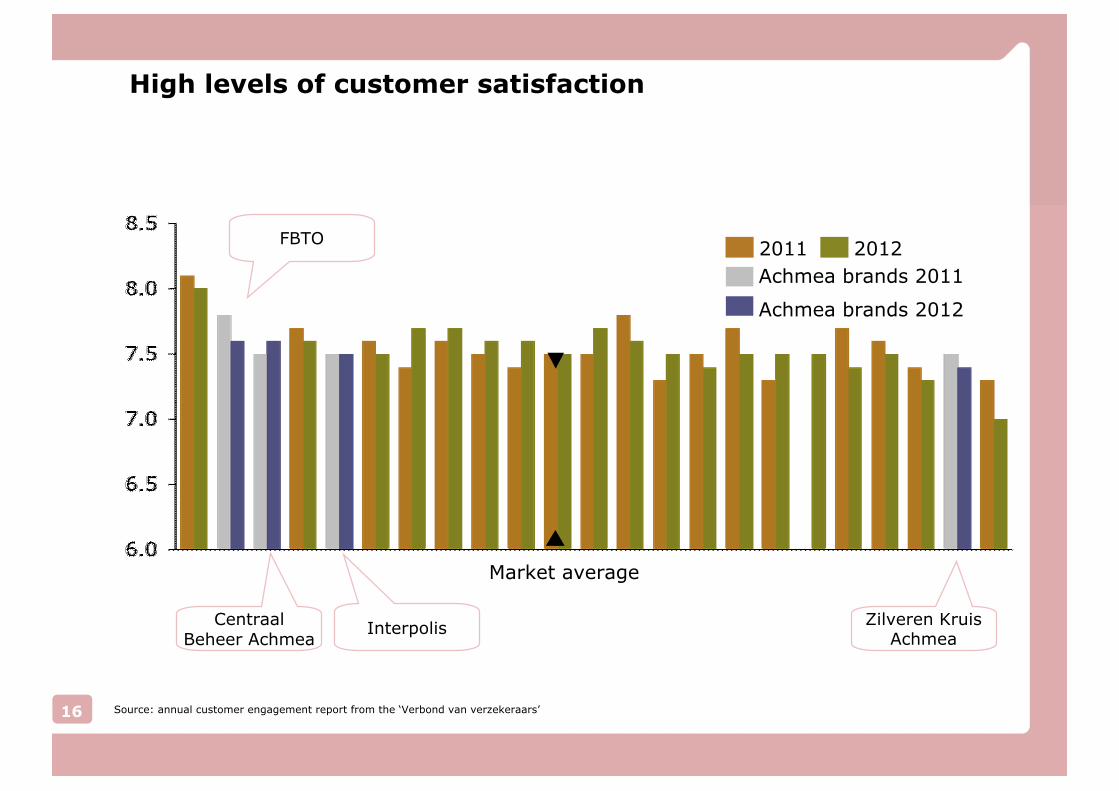

Achmea brands 2011

High levels of customer satisfaction

Market average

2011 2012FBTO

Achmea brands 2012

16 Source: annual customer engagement report from the ‘Verbond van verzekeraars’

Centraal Beheer Achmea

InterpolisZilveren Kruis

Achmea

414807_Roadshow 2013.ppt

17

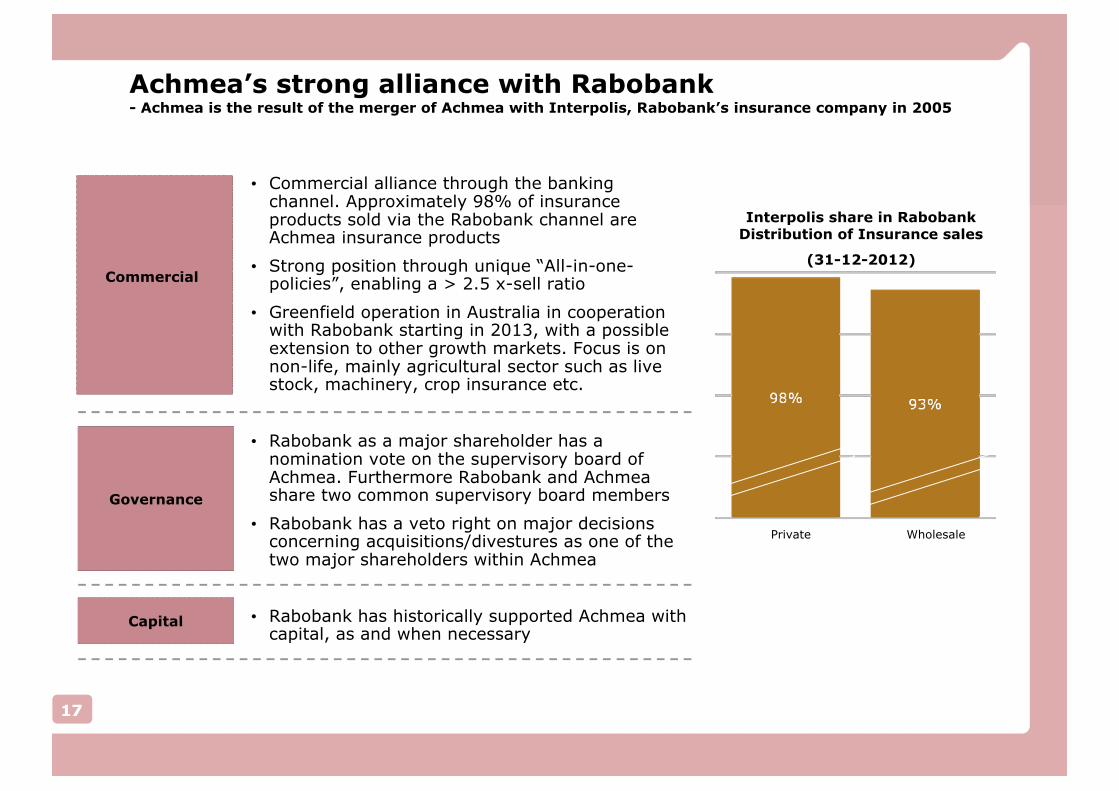

Achmea's strong alliance with Rabobank- Achmea is the result of the merger of Achmea with Interpolis, Rabobank’s insurance company in 2005

• Commercial alliance through the banking channel. Approximately 98% of insurance products sold via the Rabobank channel are Achmea insurance products

• Strong position through unique “All-in-one-policies”, enabling a > 2.5 x-sell ratio

• Greenfield operation in Australia in cooperation with Rabobank starting in 2013, with a possible extension to other growth markets. Focus is on non-life, mainly agricultural sector such as live stock, machinery, crop insurance etc.

• Rabobank as a major shareholder has a nomination vote on the supervisory board of Achmea. Furthermore Rabobank and Achmea share two common supervisory board members

• Rabobank has a veto right on major decisions concerning acquisitions/divestures as one of the two major shareholders within Achmea

• Rabobank has historically supported Achmea with capital, as and when necessary

WholesalePrivate

Interpolis share in Rabobank Distribution of Insurance sales

(31-12-2012)Commercial

Governance

Capital

17

414807_Roadshow 2013.ppt

18

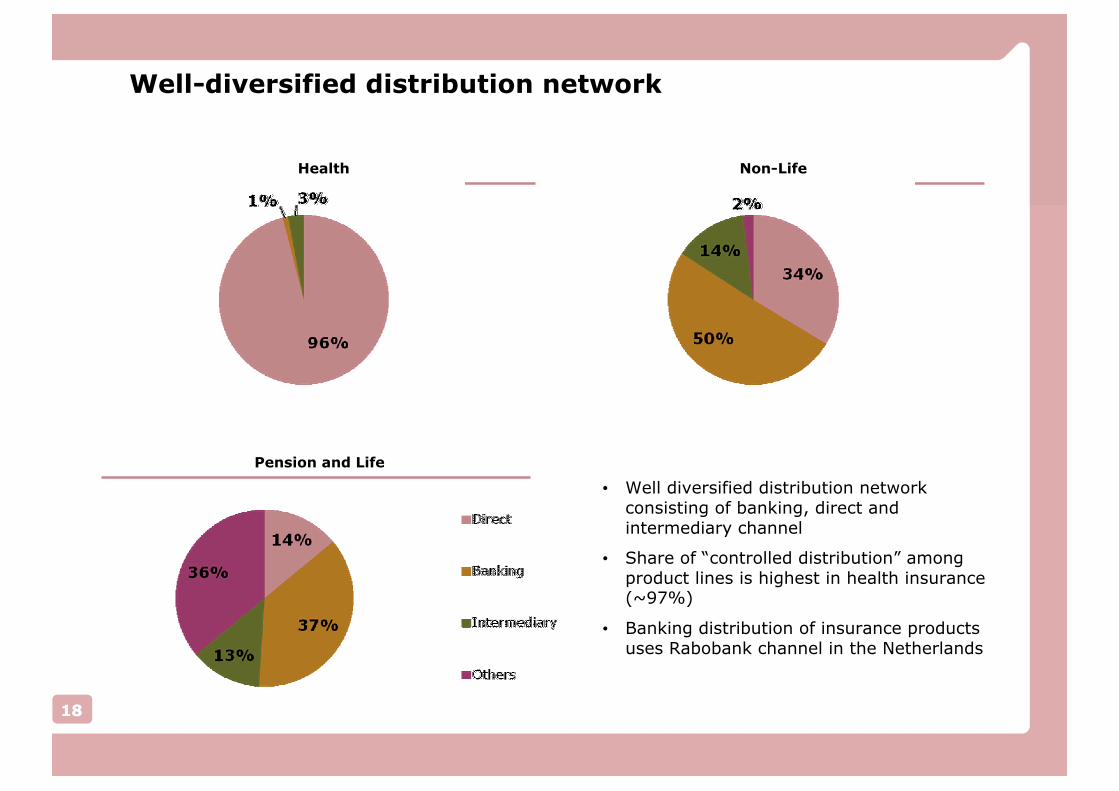

Well-diversified distribution network

Health Non-Life

Pension and Life

18

• Well diversified distribution network consisting of banking, direct and intermediary channel

• Share of “controlled distribution” among product lines is highest in health insurance (~97%)

• Banking distribution of insurance products uses Rabobank channel in the Netherlands

414807_Roadshow 2013.ppt

19

Contents

Achmea overview

Key investment highlights

Results 2012

Achmea in the Fixed Income Markets

• Leading market positions

• Core country base in one of the strongest Euro-zone countries

• A very strong capitalisation

• Well-diversified investments, especially in light of conservative investment portfolio

Appendix

414807_Roadshow 2013.ppt

20

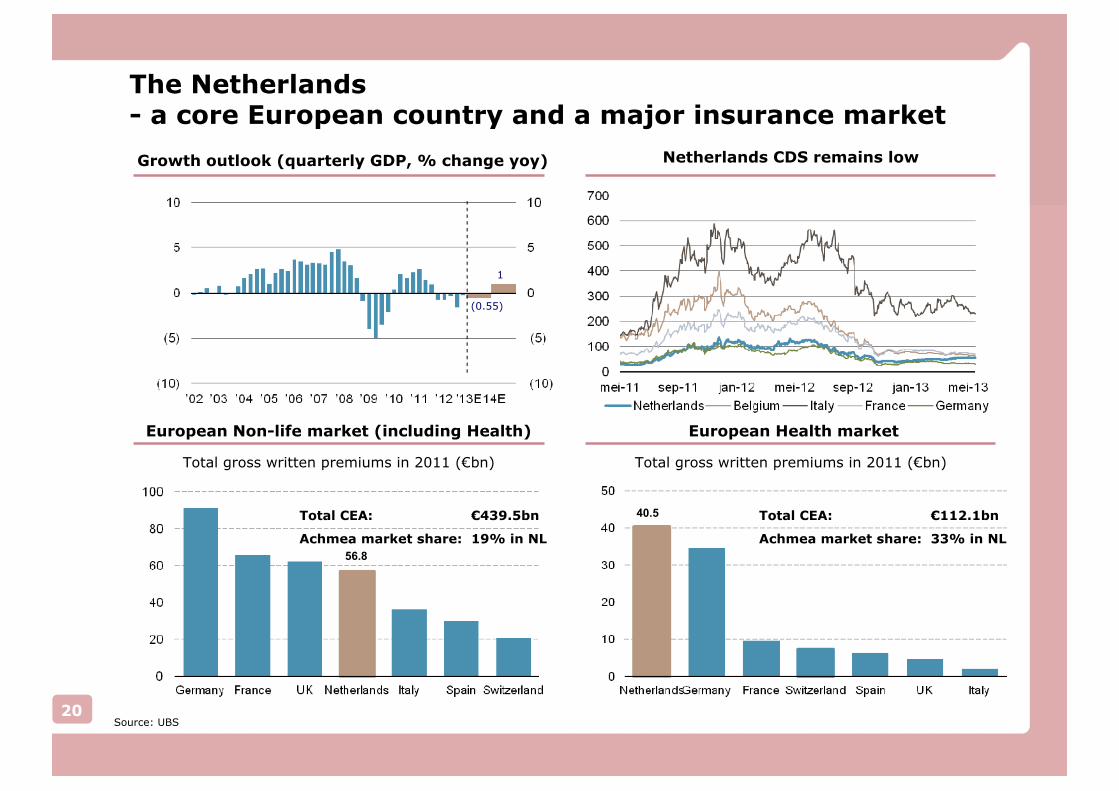

Netherlands CDS remains low

European Non-life market (including Health)

Total gross written premiums in 2011 (€bn)

Total CEA: €439.5bn

Achmea market share: 19% in NL

European Health market

Total gross written premiums in 2011 (€bn)

Growth outlook (quarterly GDP, % change yoy)

The Netherlands- a core European country and a major insurance market

(0.55)

1

Total CEA: €112.1bn

Achmea market share: 33% in NL

Source: UBS

56.8

40.5

414807_Roadshow 2013.ppt

21

Contents

Achmea overview

Key investment highlights

Results 2012

Achmea in the Fixed Income Markets

• Leading market positions

• Core country base in one of the strongest Euro-zone countries

• A very strong capitalisation

• Well-diversified investments, especially in light of conservative investment portfolio

Appendix

414807_Roadshow 2013.ppt

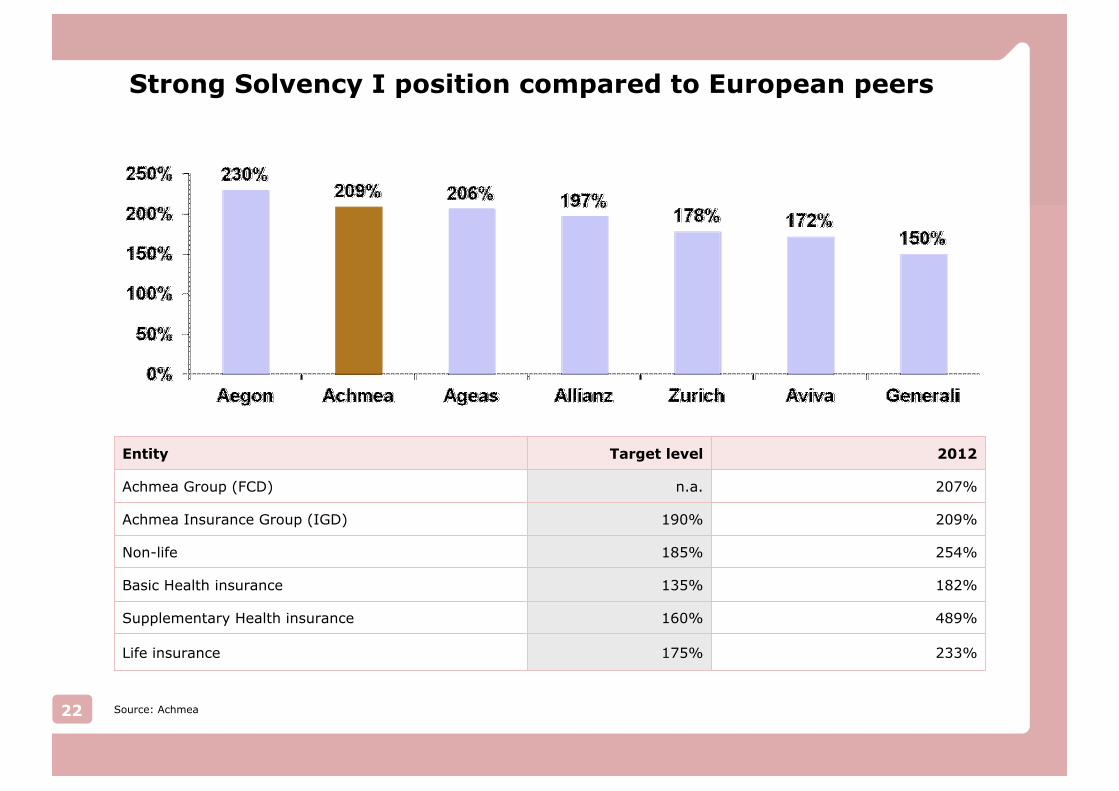

Strong Solvency I position compared to European peers

Entity Target level 2012

Achmea Group (FCD) n.a. 207%

Achmea Insurance Group (IGD) 190% 209%

Non-life 185% 254%

Basic Health insurance 135% 182%

Supplementary Health insurance 160% 489%

Life insurance 175% 233%

22 Source: Achmea

414807_Roadshow 2013.ppt

23

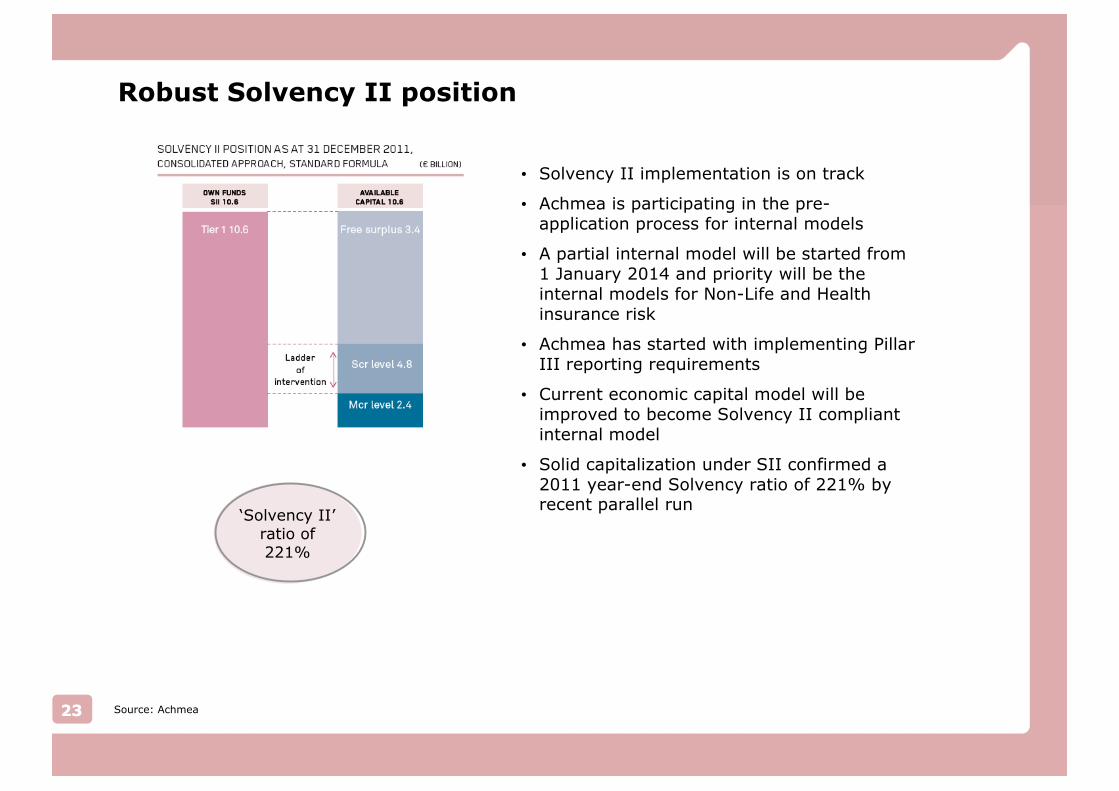

Robust Solvency II position

• Solvency II implementation is on track

• Achmea is participating in the pre-application process for internal models

• A partial internal model will be started from 1 January 2014 and priority will be the internal models for Non-Life and Health insurance risk

• Achmea has started with implementing Pillar III reporting requirements

• Current economic capital model will be improved to become Solvency II compliant internal model

• Solid capitalization under SII confirmed a 2011 year-end Solvency ratio of 221% by recent parallel run

23 Source: Achmea

‘Solvency II’ratio of 221%

414807_Roadshow 2013.ppt

24

High quality of capital with low double leverageQuality of capital

(31 December 2012)Composition of capital (31 December 2012)

Long-term debt(€0.8 bn)

Hybrid capital (€1.3 bn)

Core capital(€9.0 bn)

Tangible equity(€8.7 bn)

VOBA(€0.2 bn)

Other intangibles(€0.3 bn)

Goodwill(€1.2 bn)

• Double leverage as of 31 December 2012 is 104%

Allocation of IFRS capital 2012

Total: €11.1 billion

Holding

International

Other

Banking

Health

Pension & Life

Non-life

Net internal cash

Source: Achmea

414807_Roadshow 2013.ppt

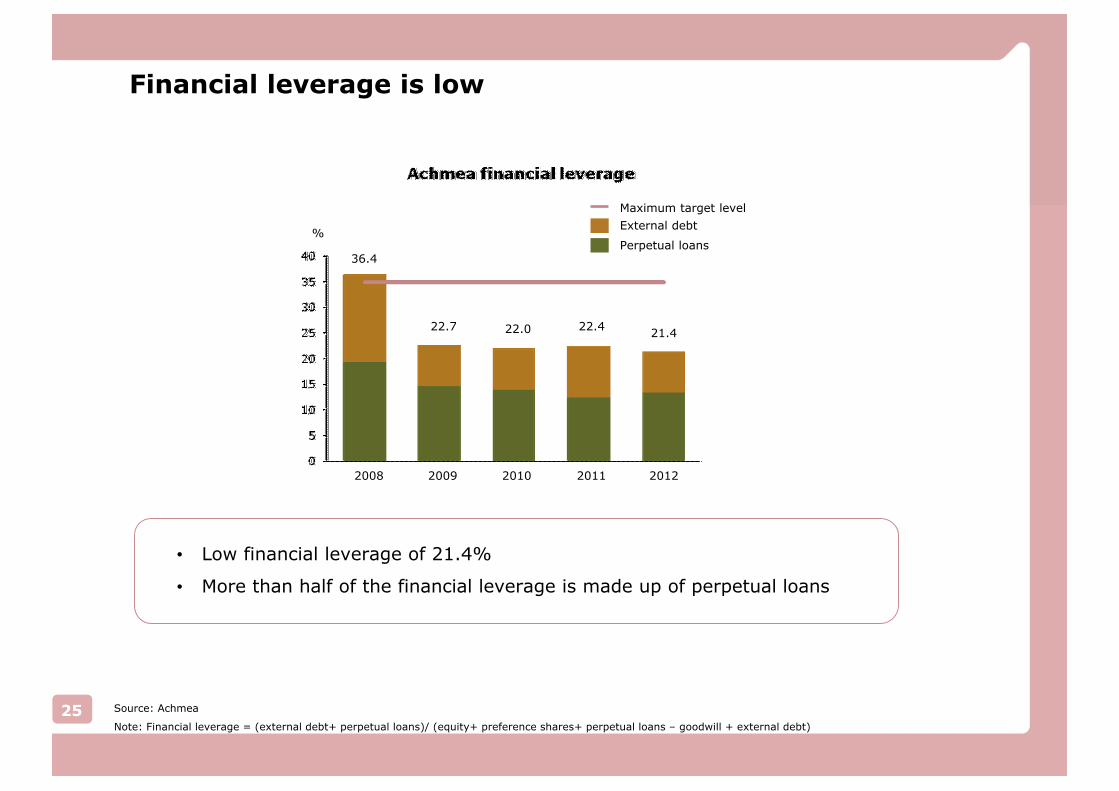

Financial leverage is low

• Low financial leverage of 21.4%

• More than half of the financial leverage is made up of perpetual loans

2011

22.4

2010

22.0

2009

22.7

2008

36.4Perpetual loans

External debt

Maximum target level

%

2012

21.4

25 Source: Achmea

Note: Financial leverage = (external debt+ perpetual loans)/ (equity+ preference shares+ perpetual loans – goodwill + external debt)

414807_Roadshow 2013.ppt

26

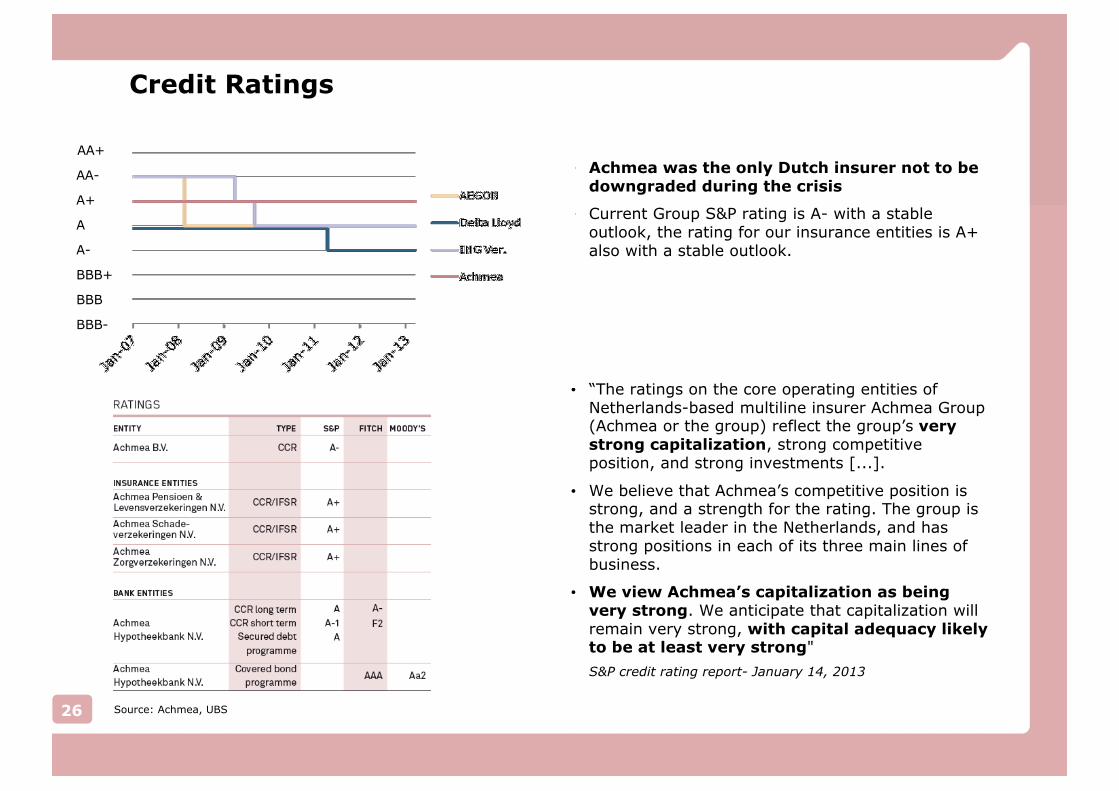

Credit Ratings

• Achmea was the only Dutch insurer not to be downgraded during the crisis

• Current Group S&P rating is A- with a stable outlook, the rating for our insurance entities is A+ also with a stable outlook.

• “The ratings on the core operating entities of Netherlands-based multiline insurer Achmea Group (Achmea or the group) reflect the group's very strong capitalization, strong competitive position, and strong investments [...].

• We believe that Achmea's competitive position is strong, and a strength for the rating. The group is the market leader in the Netherlands, and has strong positions in each of its three main lines of business.

• We view Achmea's capitalization as being very strong. We anticipate that capitalization will remain very strong, with capital adequacy likely to be at least very strong"

S&P credit rating report- January 14, 2013

Source: Achmea, UBS

AA+

AA-

A

A-

BBB+

A+

BBB

BBB-

414807_Roadshow 2013.ppt

27

Contents

Achmea overview

Key investment highlights

Results 2012

Achmea in the Fixed Income Markets

• Leading market positions

• Core country base in one of the strongest Euro-zone countries

• A very strong capitalisation

• Well-diversified investments, especially in light of conservative investment portfolio

Appendix

414807_Roadshow 2013.ppt

28

16%

11%

9%1%

62%

2%

AAA AA A BBB >BBB Not rated

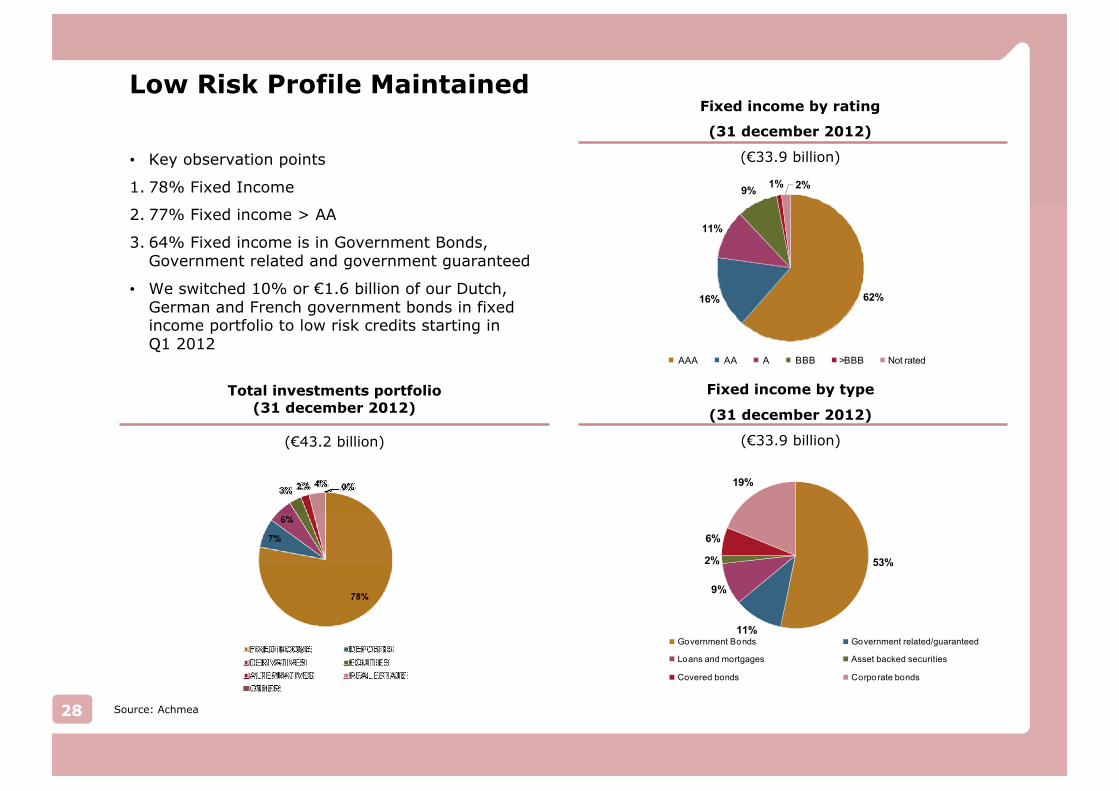

• Key observation points

1. 78% Fixed Income

2. 77% Fixed income > AA

3. 64% Fixed income is in Government Bonds, Government related and government guaranteed

• We switched 10% or €1.6 billion of our Dutch, German and French government bonds in fixed income portfolio to low risk credits starting in Q1 2012

Total investments portfolio (31 december 2012)

(€43.2 billion)

Fixed income by rating

(31 december 2012)

(€33.9 billion)

Fixed income by type

(31 december 2012)

(€33.9 billion)

Low Risk Profile Maintained

53%

11%

9%

2%

6%

19%

Government Bonds Government related/guaranteed

Loans and mortgages Asset backed securities

Covered bonds Corporate bonds

Source: Achmea

414807_Roadshow 2013.ppt

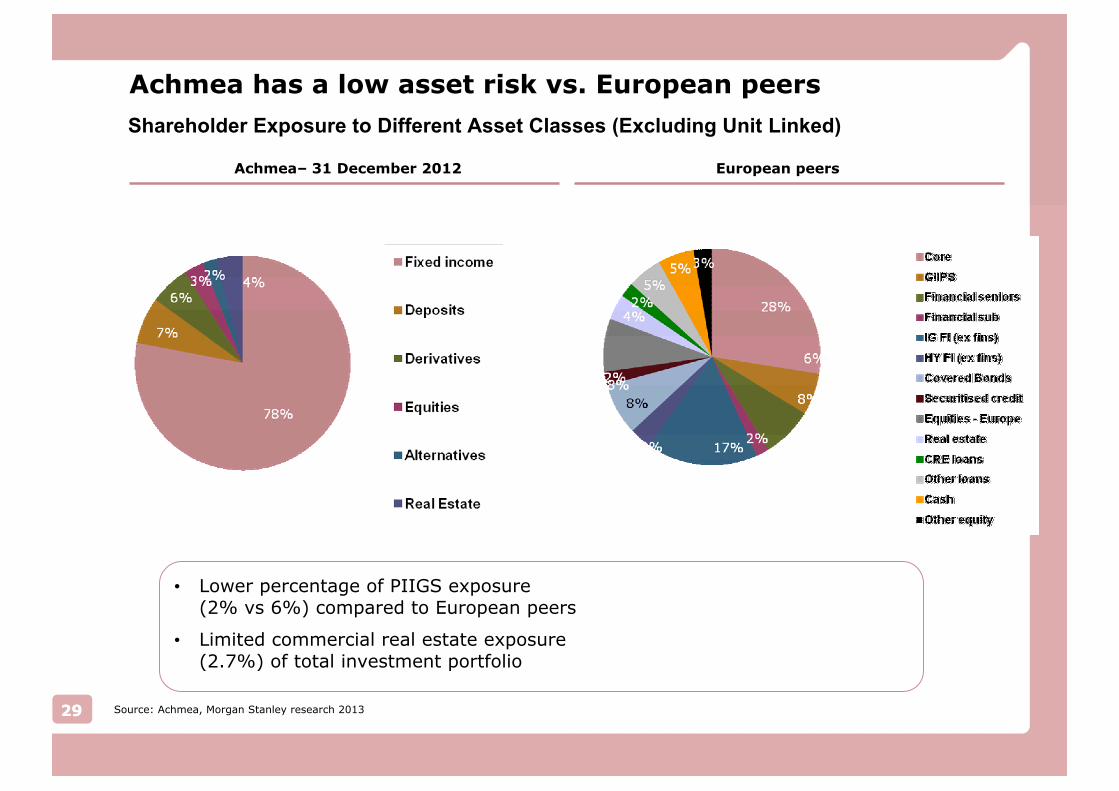

Achmea has a low asset risk vs. European peers

Shareholder Exposure to Different Asset Classes (Excluding Unit Linked)

29

European peersAchmea– 31 December 2012

29 Source: Achmea, Morgan Stanley research 2013

• Lower percentage of PIIGS exposure(2% vs 6%) compared to European peers

• Limited commercial real estate exposure(2.7%) of total investment portfolio

414807_Roadshow 2013.ppt

30

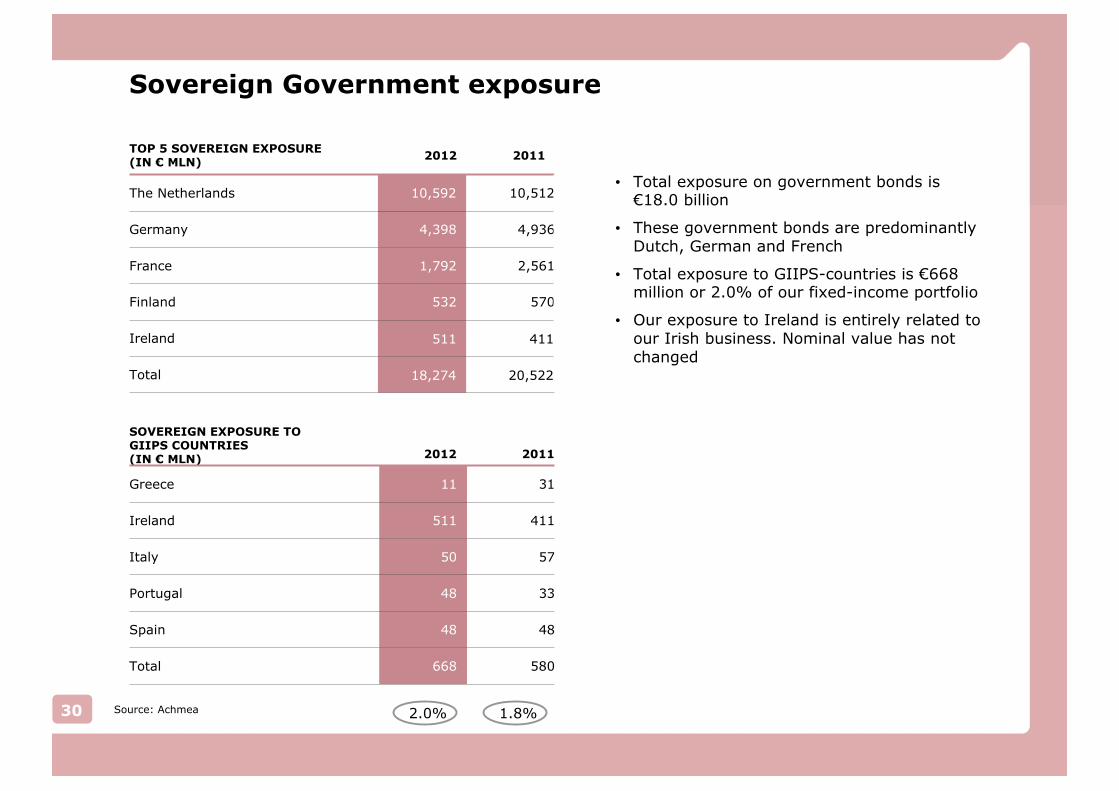

Sovereign Government exposure

• Total exposure on government bonds is €18.0 billion

• These government bonds are predominantly Dutch, German and French

• Total exposure to GIIPS-countries is €668 million or 2.0% of our fixed-income portfolio

• Our exposure to Ireland is entirely related to our Irish business. Nominal value has not changed

TOP 5 SOVEREIGN EXPOSURE (IN € MLN)

2012 2011

The Netherlands 10,592 10,512

Germany 4,398 4,936

France 1,792 2,561

Finland 532 570

Ireland 511 411

Total 18,274 20,522

SOVEREIGN EXPOSURE TO GIIPS COUNTRIES (IN € MLN) 2012 2011

Greece 11 31

Ireland 511 411

Italy 50 57

Portugal 48 33

Spain 48 48

Total 668 580

2.0% 1.8%Source: Achmea

414807_Roadshow 2013.ppt

31

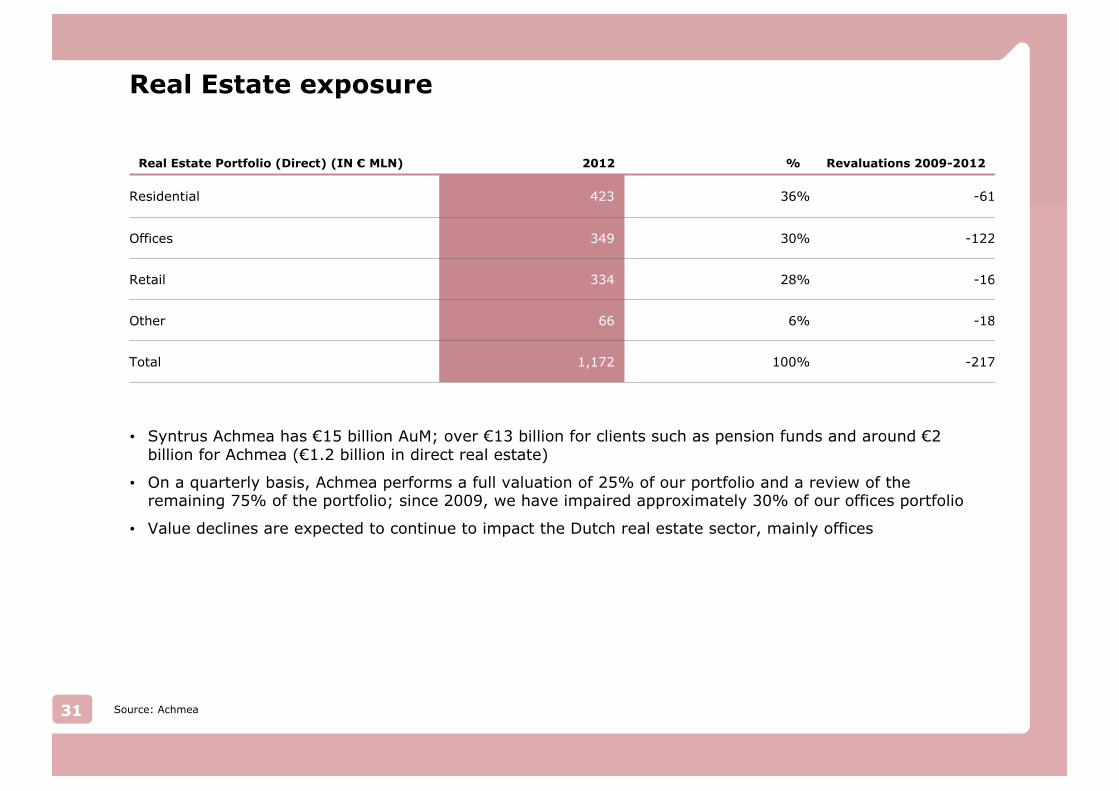

Real Estate exposure

Real Estate Portfolio (Direct) (IN € MLN) 2012 % Revaluations 2009-2012

Residential 423 36% -61

Offices 349 30% -122

Retail 334 28% -16

Other 66 6% -18

Total 1,172 100% -217

• Syntrus Achmea has €15 billion AuM; over €13 billion for clients such as pension funds and around €2 billion for Achmea (€1.2 billion in direct real estate)

• On a quarterly basis, Achmea performs a full valuation of 25% of our portfolio and a review of the remaining 75% of the portfolio; since 2009, we have impaired approximately 30% of our offices portfolio

• Value declines are expected to continue to impact the Dutch real estate sector, mainly offices

Source: Achmea

414807_Roadshow 2013.ppt

32

Contents

Achmea overview

Key investment highlights

Results 2012

Achmea in the Fixed Income Markets

• Leading market positions

• Core country base in one of the strongest Euro-zone countries

• A very strong capitalisation

• Well-diversified investments, especially in light of conservative investment portfolio

Appendix

414807_Roadshow 2013.ppt

33

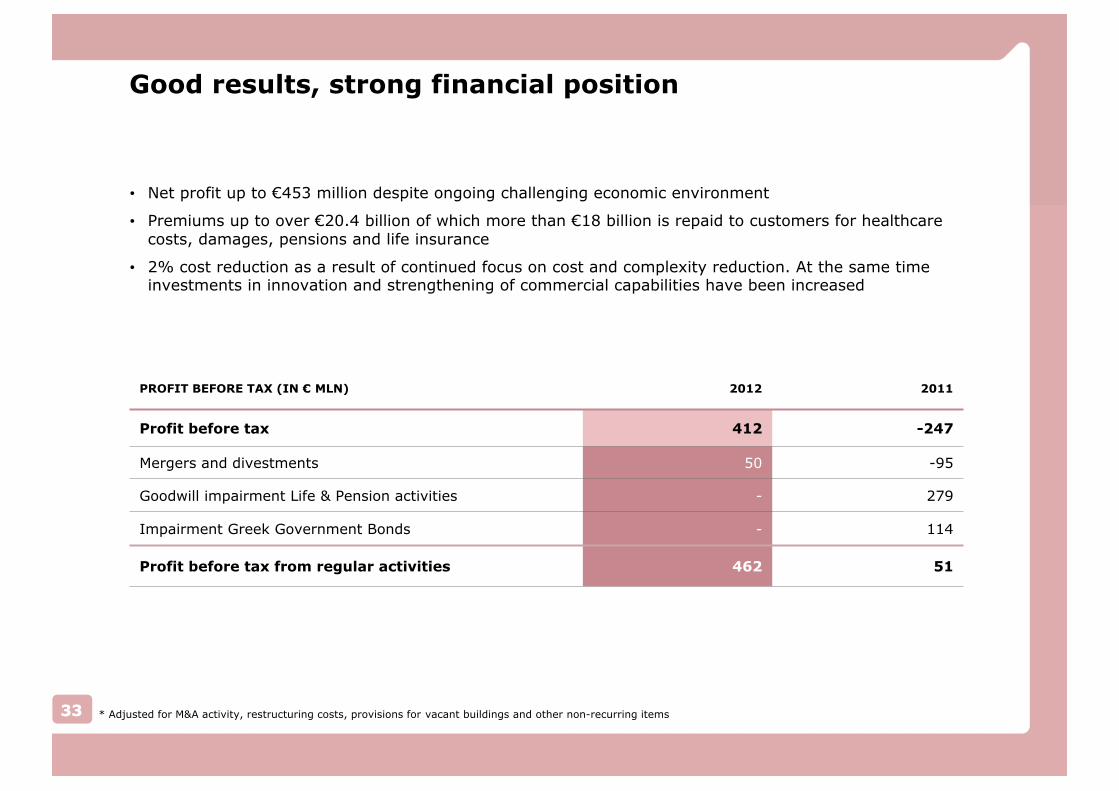

Good results, strong financial position

• Net profit up to €453 million despite ongoing challenging economic environment

• Premiums up to over €20.4 billion of which more than €18 billion is repaid to customers for healthcare costs, damages, pensions and life insurance

• 2% cost reduction as a result of continued focus on cost and complexity reduction. At the same time investments in innovation and strengthening of commercial capabilities have been increased

PROFIT BEFORE TAX (IN € MLN) 2012 2011

Profit before tax 412 -247

Mergers and divestments 50 -95

Goodwill impairment Life & Pension activities - 279

Impairment Greek Government Bonds - 114

Profit before tax from regular activities 462 51

33 * Adjusted for M&A activity, restructuring costs, provisions for vacant buildings and other non-recurring items

414807_Roadshow 2013.ppt

34

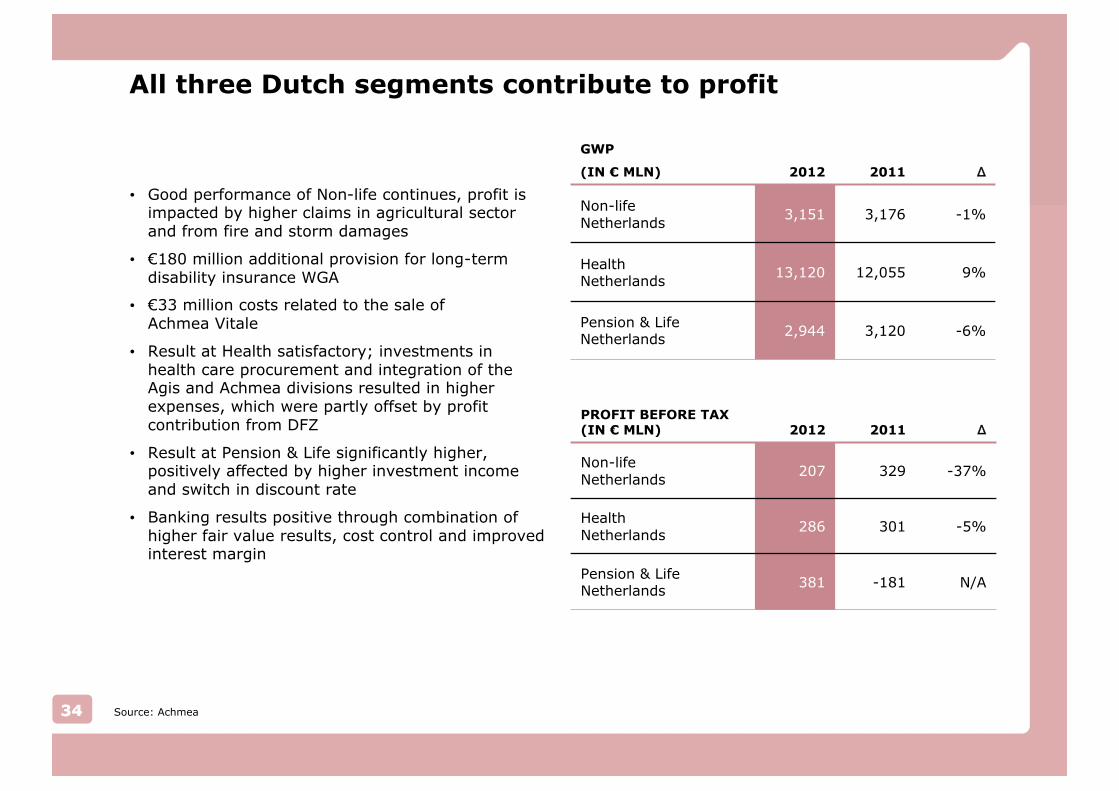

All three Dutch segments contribute to profit

• Good performance of Non-life continues, profit is impacted by higher claims in agricultural sector and from fire and storm damages

• €180 million additional provision for long-term disability insurance WGA

• €33 million costs related to the sale of Achmea Vitale

• Result at Health satisfactory; investments in health care procurement and integration of the Agis and Achmea divisions resulted in higher expenses, which were partly offset by profit contribution from DFZ

• Result at Pension & Life significantly higher, positively affected by higher investment income and switch in discount rate

• Banking results positive through combination of higher fair value results, cost control and improved interest margin

GWP

(IN € MLN) 2012 2011 �

Non-lifeNetherlands

3,151 3,176 -1%

HealthNetherlands

13,120 12,055 9%

Pension & LifeNetherlands

2,944 3,120 -6%

PROFIT BEFORE TAX (IN € MLN) 2012 2011 �

Non-lifeNetherlands

207 329 -37%

HealthNetherlands

286 301 -5%

Pension & LifeNetherlands

381 -181 N/A

34 Source: Achmea

414807_Roadshow 2013.ppt

35

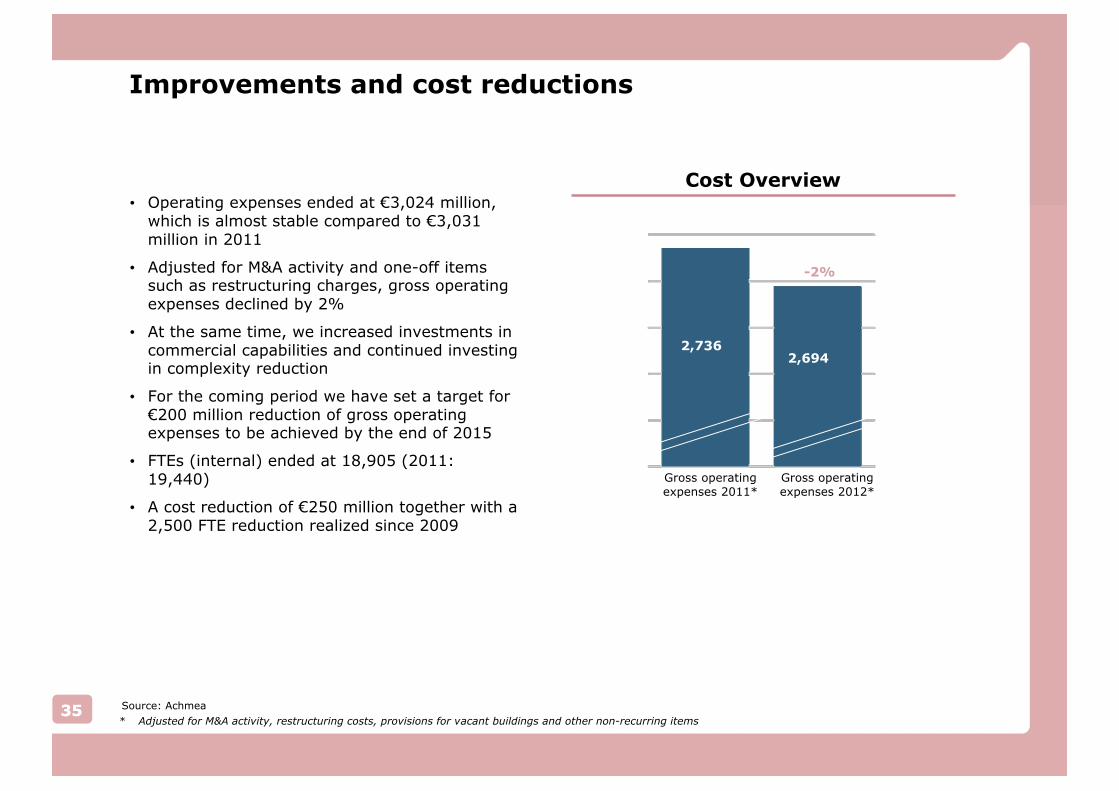

Improvements and cost reductions

• Operating expenses ended at €3,024 million, which is almost stable compared to €3,031 million in 2011

• Adjusted for M&A activity and one-off items such as restructuring charges, gross operating expenses declined by 2%

• At the same time, we increased investments in commercial capabilities and continued investing in complexity reduction

• For the coming period we have set a target for €200 million reduction of gross operating expenses to be achieved by the end of 2015

• FTEs (internal) ended at 18,905 (2011: 19,440)

• A cost reduction of €250 million together with a 2,500 FTE reduction realized since 2009

Cost Overview

2,6942,736

-2%

Gross operatingexpenses 2012*

Gross operatingexpenses 2011*

35* Adjusted for M&A activity, restructuring costs, provisions for vacant buildings and other non-recurring items

Source: Achmea

414807_Roadshow 2013.ppt

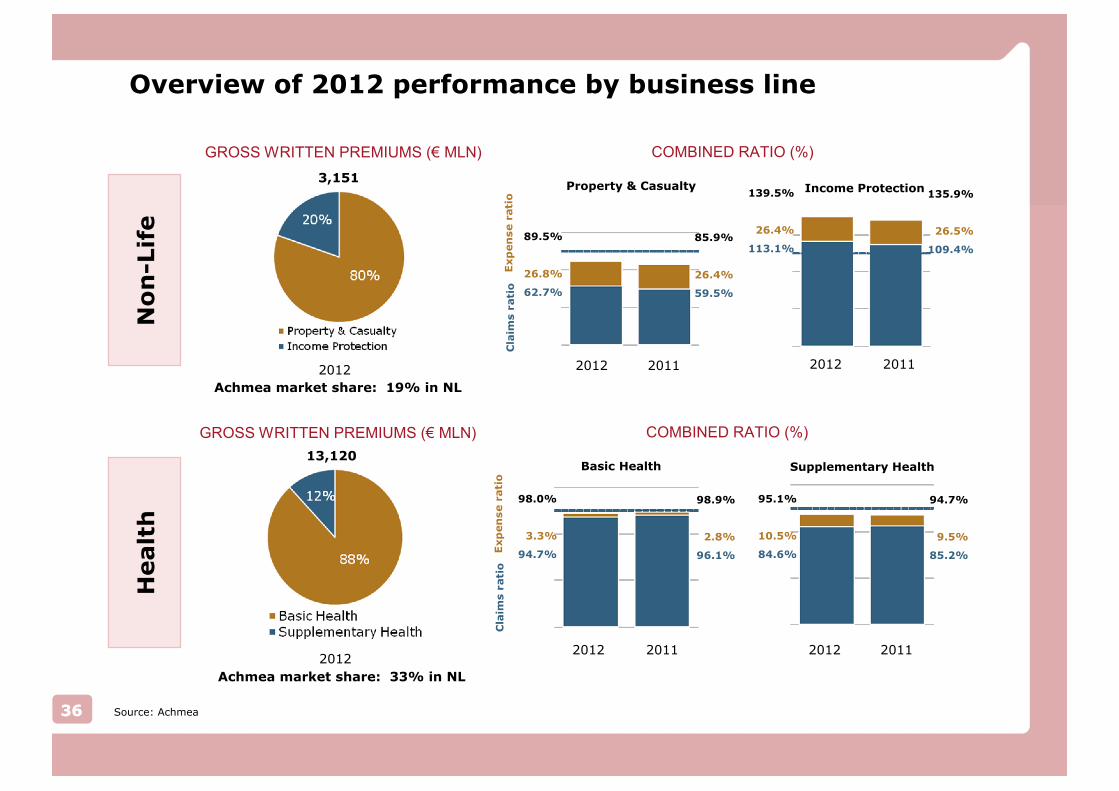

Overview of 2012 performance by business line

36

COMBINED RATIO (%)GROSS WRITTEN PREMIUMS (€ MLN)

2012

3,151

Cla

ims r

ati

oE

xp

en

se r

ati

o

2012 2011

Property & Casualty

2012 2011

Income Protection

89.5%

26.8%

62.7%

85.9%

26.4%

59.5%

139.5%

26.4%

113.1%

135.9%

26.5%

109.4%

COMBINED RATIO (%)GROSS WRITTEN PREMIUMS (€ MLN)

13,120

Cla

ims r

ati

oE

xp

en

se r

ati

o

2012 2011

Basic Health

2012 2011

Supplementary Health

98.0%

3.3%

94.7%

98.9%

2.8%

96.1%

95.1%

10.5%

84.6%

94.7%

9.5%

85.2%

2012

Achmea market share: 19% in NL

Achmea market share: 33% in NL

36

No

n-L

ife

Healt

h

Source: Achmea

414807_Roadshow 2013.ppt

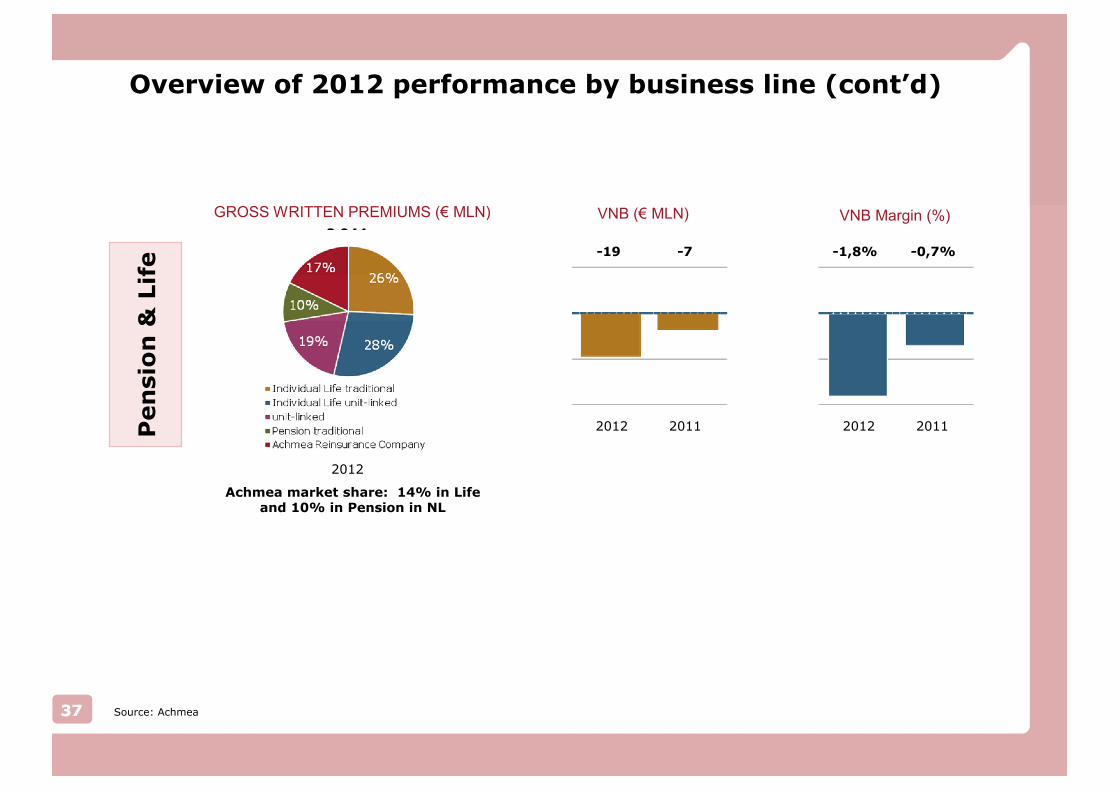

Overview of 2012 performance by business line (cont’d)

37

VNB Margin (%)VNB (€ MLN)GROSS WRITTEN PREMIUMS (€ MLN)

2012

2,944

2012

-1,8% -0,7%

20112012

-19 -7

2011

Achmea market share: 14% in Life and 10% in Pension in NL

37

Pen

sio

n &

Lif

e

Source: Achmea

414807_Roadshow 2013.ppt

38

Contents

Achmea overview

Key investment highlights

Results 2012

Achmea in the Fixed Income Markets

• Leading market positions

• Core country base in one of the strongest Euro-zone countries

• A very strong capitalisation

• Well-diversified investments, especially in light of conservative investment portfolio

Appendix

414807_Roadshow 2013.ppt

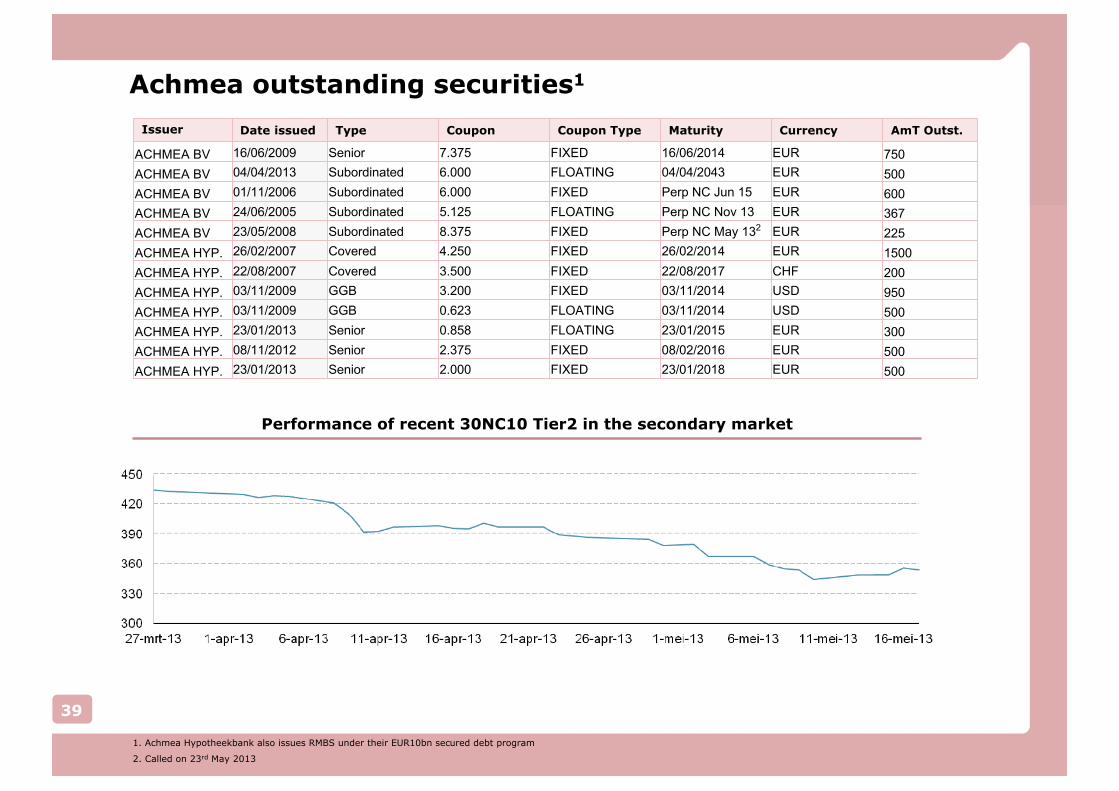

Issuer Date issued Type Coupon Coupon Type Maturity Currency AmT Outst.

ACHMEA BV 16/06/2009 Senior 7.375 FIXED 16/06/2014 EUR 750

ACHMEA BV 04/04/2013 Subordinated 6.000 FLOATING 04/04/2043 EUR 500

ACHMEA BV 01/11/2006 Subordinated 6.000 FIXED Perp NC Jun 15 EUR 600

ACHMEA BV 24/06/2005 Subordinated 5.125 FLOATING Perp NC Nov 13 EUR 367

ACHMEA BV 23/05/2008 Subordinated 8.375 FIXED Perp NC May 132 EUR 225

ACHMEA HYP. 26/02/2007 Covered 4.250 FIXED 26/02/2014 EUR 1500

ACHMEA HYP. 22/08/2007 Covered 3.500 FIXED 22/08/2017 CHF 200

ACHMEA HYP. 03/11/2009 GGB 3.200 FIXED 03/11/2014 USD 950

ACHMEA HYP. 03/11/2009 GGB 0.623 FLOATING 03/11/2014 USD 500

ACHMEA HYP. 23/01/2013 Senior 0.858 FLOATING 23/01/2015 EUR 300

ACHMEA HYP. 08/11/2012 Senior 2.375 FIXED 08/02/2016 EUR 500

ACHMEA HYP. 23/01/2013 Senior 2.000 FIXED 23/01/2018 EUR 500

39

Achmea outstanding securities1

Performance of recent 30NC10 Tier2 in the secondary market

1. Achmea Hypotheekbank also issues RMBS under their EUR10bn secured debt program

2. Called on 23rd May 2013

414807_Roadshow 2013.ppt

40

Contents

Achmea overview

Key investment highlights

Results 2012

Achmea in the Fixed Income Markets

• Leading market positions

• Core country base in one of the strongest Euro-zone countries

• A very strong capitalisation

• Well-diversified investments, especially in light of conservative investment portfolio

Appendix

414807_Roadshow 2013.ppt

41

Contact Details

For further information, please contact Achmea Investor Relations

Bastiaan Postma

+31 (0)6 13117581

Gül Poslu

+31 (0)6 20971758

Email: [email protected]

Internet: www.achmea.com

414807_Roadshow 2013.ppt

42

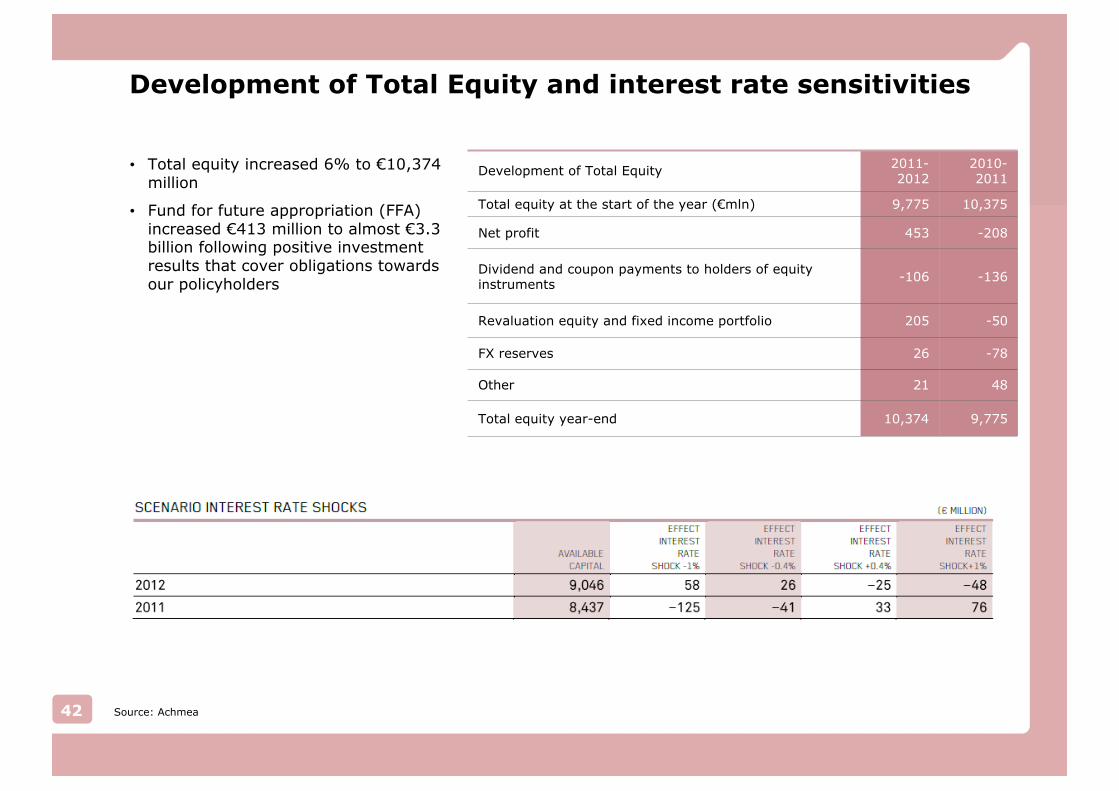

Development of Total Equity and interest rate sensitivities

• Total equity increased 6% to €10,374 million

• Fund for future appropriation (FFA) increased €413 million to almost €3.3 billion following positive investment results that cover obligations towards our policyholders

Development of Total Equity2011-2012

2010-2011

Total equity at the start of the year (€mln) 9,775 10,375

Net profit 453 -208

Dividend and coupon payments to holders of equity instruments

-106 -136

Revaluation equity and fixed income portfolio 205 -50

FX reserves 26 -78

Other 21 48

Total equity year-end 10,374 9,775

Source: Achmea

414807_Roadshow 2013.ppt

43

Disclaimer

The information and the opinions in this presentation have been prepared by Achmea B.V. (the "Company" or �Achmea") solely for use at a meeting regarding a proposed offering (the "Offering") of Notes of the Company (the "Notes"). This presentation and its contents are strictly confidential, are intended only for use by the recipient for information purposes only and may not be reproduced in any form or further distributed to any other person or published, in whole or in part, for any purpose. Failure to comply with this restriction may constitute a violation of applicable securities laws. By attending the meeting where this presentation is made, or by reading the presentation slides, you agree to be bound by the following limitations.

This presentation does not constitute or form part of, and should not be construed as, an offer to sell, or the solicitation or invitation of any offer to buy or subscribe for, Notes in any jurisdiction or an inducement to enter into investment activity in any jurisdiction. No part of this presentation, nor the fact of its distribution, should form the basis of, or be relied on in connection with, any contract or commitment or investment decision whatsoever. Any purchase of the Notes in the Offering should be made solely on the basis of the Base Prospectus and Final Terms to be prepared in connection with the Offering. This presentation is the sole responsibility of the Company and has not been approved by any regulatory authority.

The information contained in this presentation has not been independently verified. No representation, warranty or undertaking, expressed or implied, is or will be made by the Company, Deutsche Bank, HSBC, J.P.Morgan, RBS and UBS or any other investment bank involved with the Offering or their respective affiliates, advisors or representatives or any other person as to, and no reliance should be placed on, the truth, fairness, accuracy, completeness or correctness of the information or the opinions contained herein (and whether any information has been omitted from the presentation). Each of Deutsche Bank, HSBC, J.P.Morgan, RBS and UBS and any other investment bank involved with the Offering and, to the extent permitted by law, the Company and each of their respective directors, officers, employees, affiliates, advisors and representatives disclaims all liability whatsoever (in negligence or otherwise) for any loss however arising, directly or indirectly, from any use of this presentation or its contents or otherwise arising in connection with this presentation.

To the extent available, the industry, market and competitive position data contained in this presentation come from official or third party sources. Third party industry publications, studies and surveys generally state that the data contained therein have been obtained from sources believed to be reliable, but that there is no guarantee of the accuracy or completeness of such data. Accordingly, undue reliance should not be placed on any of the industry, market or competitive position data contained in this presentation.

This presentation and any materials distributed in connection with this presentation are not directed to, or intended for distribution to or use by, any person or entity that is a citizen or resident or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would require any registration or licensing within such jurisdiction.

The Notes have not been and will not be registered under the U.S. Securities Act of 1933 (the "Securities Act"), or under the securities laws of any state or other jurisdiction of the United States, and may not be offered or sold within the United States, or to, or for the account or benefit of, U.S. persons as defined in Regulation S under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act and in compliance with any applicable securities laws of any state or other jurisdiction of the United States. Achmea does not intend to register any portion of the Offering in the United States or conduct a public offering of securities in the United States.

The distribution of this presentation and other information in connection with the Offering in certain jurisdictions may be restricted by law and persons into whose possession this presentation or any document or other information referred to herein comes should inform themselves about and observe any such restrictions. Any failure to comply with these restrictions may constitute a violation of the securities laws of any such jurisdiction.

This presentation and any materials distributed in connection with this presentation include "forward-looking statements". These statements contain the words "anticipate", �will�, "believe", "intend", "estimate", "expect" and words of similar meaning. All statements other than statements of historical facts included in this presentation, including, without limitation, those regarding the Company�s financial position, prospects, growth, business strategy, plans and objectives of management for future operations (including statements relating to, among others, expected market growth, future market share, relations with the Company's shareholders, the impact of regulatory and other related developments, demographic changes, political and economic developments, competition, branch and/or sales network growth, funding plans, interest rates, net interest margin and other financial measures, product development, information technology and potential restructurings and reorganisations) are forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other important factors, including, without limitation, the risks and uncertainties to be set forth in the Prospectus, that could cause the actual results, performance or achievements of the Company to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. Such forward-looking statements are based on numerous assumptions regarding the Company's present and future business strategies and the environment in which the Company will operate in the future. These forward-looking statements speak only as at the date of this presentation. The Company cautions you that forward-looking statements are not guarantees of future performance and that its actual financial position, prospects, growth, business strategy, plans and objectives of management for future operations may differ materially from those made in or suggested by the forward-looking statements contained in this presentation. In addition, even if the Company's financial position, prospects, growth, business strategy, plans and objectives of management for future operations are consistent with the forward-looking statements contained in this presentation, those results or developments may not be indicative of results or developments in future periods. The Company does not undertake and expressly disclaims any obligation to review or confirm or to release publicly any updates or revisions to any forward-looking statements contained herein to reflect any change in the Company's expectations with regard thereto or any events that occur or conditions or circumstances that arise after the date of this presentation. The information and opinions contained in this presentation are provided as at the date of this presentation and are subject to change without notice.

This presentation is made to and is directed only at persons who (i) if in the European Economic Area, are persons who are "qualified investors" within the meaning of Article 2(1)(e) of the Prospectus Directive (Directive 2003/71/EC) (�Qualified Investors�); and (ii) if in the United Kingdom, are (a) persons who have professional experience in matters relating to investments who fall within the definition of "investment professionals" in Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the �Financial Promotion Order�) or (b) high net worth entities as defined in the Financial Promotion Order or (iii) other persons to whom it may otherwise lawfully be communicated falling within Article 49(2)(a) to (e) of the Financial Promotion Order or Article 43 of the Financial Promotion Order (all such persons in (i), (ii) and (ii) above together being referred to as �relevant persons�). Any person who is not a relevant person should not act or rely on this presentation or any of its contents. Any investment or investment activity to which this presentation relates is available only to and will only be engaged in with such persons.

Each of Deutsche Bank, HSBC, J.P.Morgan, RBS and UBS, and their respective affiliates are acting for the Company and no one else in connection with the matters referred to in this presentation and will not regard any other person as their respective clients in relation to such matters and will not be responsible to any other person for providing the protections afforded to their respective clients, or for providing advice in relation to such matters.