Embed Size (px)

Citation preview

2013 Financial Institutions ConferenceAccounting for SBA Loan Sales

© 2013 Crowe Horwath LLP 2Audit | Tax | Advisory | Risk | Performance

Learning Objectives Understand accounting issues related to sale of SBA loans Understand how to account for sale of SBA loan including, recording of

servicing asset associated with sale as well as gain recognition Understand impact of Basel III on treatment of mortgage servicing assets

© 2013 Crowe Horwath LLP 3Audit | Tax | Advisory | Risk | Performance

Why SBA Loan Sales? Increase in volume Investors willing to pay high premium for guaranteed loans because only risk

is prepayment risk Changes in loan sales agreements from SBA Accounting guidance dictating whether transfer constitutes sale is

relevant to other areas such as participation loan sales Regulators tend to encourage lending to small businesses and SBA

allows financial institutions to make these loans with limited risk

© 2013 Crowe Horwath LLP 4Audit | Tax | Advisory | Risk | Performance

Transfers of Financial Assets ASC 860, “Transfers and Servicing” (formerly FAS 140 as amended by

FAS 166) establishes accounting treatment for transfers of financial assets

Financial Asset – Cash, evidence of ownership interest in entity, or contract that conveys to one entity a right to do either of the following: Receive cash or another financial instrument from second entity Exchange other financial instruments on potentially favorable terms with

second entity Transfer – Conveyance of noncash financial asset by and to someone

other than issuer of financial asset Includes: selling receivable, putting receivable into securitization trust, posting

receivable as collateral Excludes: Origination of receivable, settlement of receivable, restructuring of

receivable into security in troubled debt restructuring

© 2013 Crowe Horwath LLP 5Audit | Tax | Advisory | Risk | Performance

Conditions for Sale Accounting In order to be able to account for transfer as a sale all of the following

conditions must be considered: Transferred assets have been isolated, beyond reach of transferor Transferee has right to pledge or exchange assets Transferor does not maintain effective control

If transaction does not meet conditions for sales accounting treatment, it would be considered secured borrowing

© 2013 Crowe Horwath LLP 6Audit | Tax | Advisory | Risk | Performance

Conditions for Sale Accounting (cont.) Effective control: Transferor has not given up effective control if agreement both entitles and

obligates transferor to repurchase or redeem sold portion before maturity Agreement that provides transferor with both unilateral ability to cause holder

to return specific financial assets and more-than-trivial benefit attributable to that ability, other than through cleanup call

Agreement that permits transferee to require transferor to repurchase transferred financial assets at price that is so favorable to transferee that it is probable that transferee will require transferor to repurchase them

Considerations when deciding if control has been surrendered: Is transferee consolidated by transferor? What is transferor’s continuing involvement in transferred asset? Are there any arrangements or agreements made contemporaneously with,

or in contemplation with transfer? Are there recourse provisions?

© 2013 Crowe Horwath LLP 7Audit | Tax | Advisory | Risk | Performance

Participating Interest In order to be eligible for sale accounting, financial asset cannot be

divided into components unless it meets definition of participating interest

Participating interest has each of the following characteristics: From date of transfer, it represents proportionate (pro rata) ownership interest

in entire financial asset From date of transfer, all cash flows received from entire financial asset are

divided proportionately among participating interest holders in amount equal to their share of ownership

Rights of each participating interest holder (including transferor in its role as participating interest holder) have same priority, and no participating interest holder’s interest is subordinated to interest of another participating interest holder

No party has right to pledge or exchange entire financial asset unless all participating interest holders agree to pledge or exchange entire financial asset

© 2013 Crowe Horwath LLP 8Audit | Tax | Advisory | Risk | Performance

Would the following examples meet sales accounting criteria? Scenario 1 - Sales agreement contains clause indicating transferor may force

transferee to sell back sold portion of participation loan at any time No Transferor would not have given up “effective control”

Scenario 2 - Transferor will always pay itself its own share of each payment collected for participation loan before paying transferee No Cash flows are not being shared proportionately

Scenario 3 - Transferee is prohibited from selling its own share of participation without first obtaining permission from transferor It depends… If transferor includes language that permission will “not be unreasonably

withheld” this would generally not indicate transferor has not given up control

© 2013 Crowe Horwath LLP 9Audit | Tax | Advisory | Risk | Performance

Back to SBA Loan Sales… Transfer of guaranteed portion and retained unguaranteed portion now typically

meet definition of participating interest on transfer date based on revised SBA agreements but keep this guidance in mind when evaluating sales for appropriate accounting treatment

An exception: if agreement transfers guaranteed portion at par and transferring lender agrees to pass interest through to party obtaining guaranteed portion at less than contractual interest rate Viewed as interest only strip, which would preclude sales accounting

treatment

© 2013 Crowe Horwath LLP 10Audit | Tax | Advisory | Risk | Performance

Accounting TreatmentRecording Transaction Servicing asset – If benefits of servicing are expected to more than adequately

compensate servicer for performing servicing, servicer books intangible servicing asset

Interest only strip – If seller retains no interest in loan but will receive beneficial interest (interest-only), this interest should be recorded as interest only strip

To calculate gain on sale: 1. Allocate previous carrying amount (e.g., deferred fees and costs) of entire financial

asset between participating interest sold and participating interest held by transferor based on relative fair value at date of transfer

2. Calculate proceeds from sale including servicing asset and interest only strip3. Recognize gain as difference between proceeds as calculated in #2 above and carrying

value of financial asset sold as calculated in #1 above

© 2013 Crowe Horwath LLP 11Audit | Tax | Advisory | Risk | Performance

Allocating Fair Value – Simple Example Sold portion – In general, fair value is assumed to be price paid by buyer Retained portion – Fair value will consider fact that rate received will be

less than what would have been required for similar loan given lack of guarantee of retained portion

Example – Entity A is selling 75% SBA guaranteed portion of loan to Entity B for

$250,000 Current principal balance of loan is $310,000 and calculated fair value for

25% retained portion is $75,000

Fair Value

% of Total Fair Value

Sold Portion $250,000 77%Retained Portion 75,000 23%Total $325,000

© 2013 Crowe Horwath LLP 12Audit | Tax | Advisory | Risk | Performance

Calculating Carrying Amount – Simple Example Entity A is selling 75% SBA guaranteed portion of loan to Entity B for $250,000 Principal balance of loan is $310,000 and calculated fair value for 25% retained

portion is $75,000 Fees earned by originator, net of costs total $2,000 One-time guarantee fee for loan (3% of amount guaranteed) totaled $6,975 and

calculated servicing asset was $3,200 Total carrying amount is calculated:

Allocation between retained and sold portion:Carrying Amount

% of Total Fair Value

Sold Portion 242,531 77%Retained Portion 72,444 23%Total 314,975

Loan amount $ 310,000 Net Origination Fees (2,000)SBA Fees 6,975 Total $ 314,975

© 2013 Crowe Horwath LLP 13Audit | Tax | Advisory | Risk | Performance

Calculate Gain - Example Entity A is selling 75% SBA guaranteed portion of loan to Entity B for

$250,000 Principal balance of loan is $310,000 Calculated fair value for 25% retained portion is $75,000 Calculated servicing asset was $3,200

Proceeds from sale $ 250,000 Servicing asset 3,200 Total proceeds $ 253,200

Less allocated carrying amount of sold portion (242,531)Gain on sale $ 10,669

© 2013 Crowe Horwath LLP 14Audit | Tax | Advisory | Risk | Performance

Journal Entries Entry to record transaction would appear as follows:

Retained portion on Entity A’s books is $72,444 and would be accreted to 25% of contractual payments due from borrower, assuming all payments are made as agreed

Cash $ 250,000Servicing Asset 3,200

Loans 242,531Gain on Sale 10,669

© 2013 Crowe Horwath LLP 15Audit | Tax | Advisory | Risk | Performance

Subsequent Accounting Servicing asset will be amortized in proportion to and over period of

estimated net servicing income and assessed for impairment based on fair value at each reporting date

Entries to record receipt of servicing income and amortization of servicing asset would be as follows:

Servicing asset would be measured for impairment on periodic basis If loan pays off early, remaining servicing asset would be recognized in

income statement upon payoff

Servicing asset amortization $ 30 Servicing asset $ 30

Cash $ 52 Servicing income $ 52

© 2013 Crowe Horwath LLP 16Audit | Tax | Advisory | Risk | Performance

Interest Only Strip Consideration If seller retains no interest in loan but will receive beneficial interest

(interest-only), this interest should be recorded as interest only strip If seller transfers only portion of loan, transaction will not meet definition

of participating interest (since cash flows are disproportionate) and would therefore not meet sales criteria As such, accounting would result in recording of secured borrowing

Interest only strips are recorded at fair value as they represent separate identifiable assets, not retained interest in assets sold

Transferor should include fair value of interest only strip when calculating proceeds from sale

© 2013 Crowe Horwath LLP 17Audit | Tax | Advisory | Risk | Performance

Interest Only Strip – Example Entity A originates loan and transfers 100% ($2,000,000) of loan to another entity

at par Entity A continues to service loans and will receive servicing fee of and beneficial

interest rate due to additional risk associated with unguaranteed portion At date of transfer, fair value of the loans, including servicing is $2,200,000 Fair value of servicing is $88,000 and fair value of interest only strip is $112,000 The entries to record transaction would be:

Proceeds from sale $2,000,000 Servicing asset 88,000Interest only strip 112,000Total proceeds $2,200,000

Less allocated carrying amount of sold portion 2,000,000Gain on sale $200,000

© 2013 Crowe Horwath LLP 18Audit | Tax | Advisory | Risk | Performance

Interest Only Strip Example (cont.) Journal entries to record sale:

Cash 2,000,000 Servicing asset 88,000 Interest only strip 112,000

Loan 2,000,000 Gain on sale of loan 200,000

© 2013 Crowe Horwath LLP 19Audit | Tax | Advisory | Risk | Performance

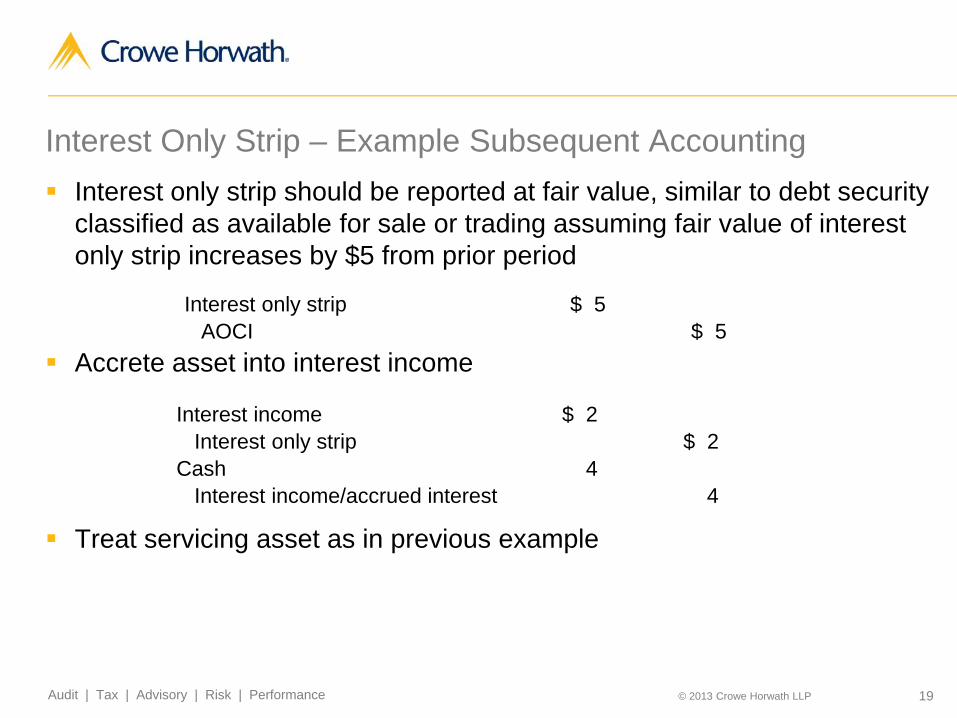

Interest Only Strip – Example Subsequent Accounting Interest only strip should be reported at fair value, similar to debt security

classified as available for sale or trading assuming fair value of interest only strip increases by $5 from prior period

Accrete asset into interest income

Treat servicing asset as in previous example

Interest only strip $ 5AOCI $ 5

Interest income $ 2Interest only strip $ 2

Cash 4Interest income/accrued interest 4

© 2013 Crowe Horwath LLP 20Audit | Tax | Advisory | Risk | Performance

Interest Only Strip Subsequent Accounting Impairment analysis Evaluate interest only strip for impairment according to ASC 320-10-35 Interest only strips are valued based on future cash flows Impairment concerns would come from prepayment risk as well as credit risk Fair value calculation would consider interest rates, prepayment rates, default

rates and future revenues/expenses Similar process to evaluating a debt security for OTTI

© 2013 Crowe Horwath LLP 21Audit | Tax | Advisory | Risk | Performance

Accounting for a Secured Borrowing When transfer does not meet definition of sale, transferor must account

for it as secured borrowing Assume Entity A originated loan for $350,000 and is selling 75% to Entity

B for $262,500 Sales agreement includes recourse provisions that do not allow sales

accounting treatment Entity A would make the following entries:

Loan $350,000 Cash $350,000

Cash 262,500 Secured borrowing 262,500

© 2013 Crowe Horwath LLP 22Audit | Tax | Advisory | Risk | Performance

Accounting for a Secured Borrowing (cont.) To record interest income/expense:

To record receipt of payment:

Accrued interest receivable 58Interest income 58

Interest expense 44Accrued interest payable 44

Cash 3,668 Accrued interest receivable 58 Loans 3,610

Accrued interest payable 44 Secured borrowing 2,707

Cash 2,751

© 2013 Crowe Horwath LLP 23Audit | Tax | Advisory | Risk | Performance

Regulatory Considerations In July 2013, Federal Reserve Board approved Basel III Regulatory

Capital and Market Risk Final Rule Mortgage servicing assets were not given favorable treatment and Final

Rule requires mortgage servicing assets that individually exceed 10% of common equity of tier 1 capital be deducted from that component of tier 1 capital

Likely to apply to SBA servicing assets as well If mortgage servicing assets exceed 15% of common equity component

of tier 1 capital they must be deducted from that component of tier 1 capital

Any mortgage servicing asset not deducted from capital would be risk-weighted 250% Current risk weight of servicing assets is 100%

Five-year phase-in commencing January 1, 2014

© 2013 Crowe Horwath LLP 24Audit | Tax | Advisory | Risk | Performance

Crowe Horwath LLP is an independent member of Crowe Horwath International, a Swiss verein. Each member firm of Crowe Horwath International is a separate and independent legal entity. Crowe Horwath LLP and its affiliates are not responsible or liable for any acts or omissions of Crowe Horwath International or any other member of Crowe Horwath International and specifically disclaim any and all responsibility or liability for acts or omissions of Crowe Horwath International or any other Crowe Horwath International member. Accountancy services in Kansas and North Carolina are rendered by Crowe Chizek LLP, which is not a member of Crowe Horwath International. © 2013 Crowe Horwath LLP