Embed Size (px)

Citation preview

Robert M. “Kinney” Poynter, CPAExecutive Director, National Association of State Auditors, Comptrollers, and Treasurers (NASACT)

David A. VaudtChairman, Governmental Accounting Standards Board

Michele Mark LevineDirector, Technical Service Center, GFOA

Accounting and Auditing Year in Reviewwww.gfoa.org • #GFOA2018

112th Annual ConferenceMay 6-9, 2018 • St. Louis, Missouri

Moderator/Speakers:

10:30 – 12:10 • May 7, 2018 • Room Hall 5

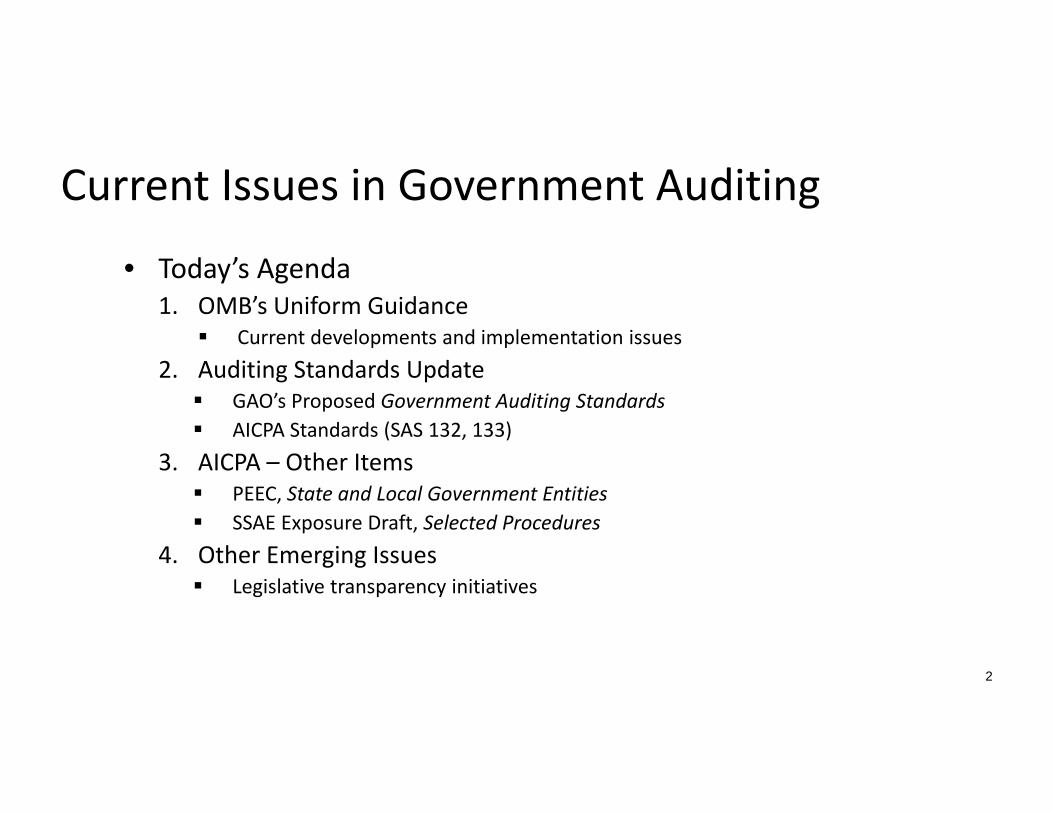

Current Issues in Government Auditing

• Today’s Agenda1. OMB’s Uniform Guidance

Current developments and implementation issues2. Auditing Standards Update GAO’s Proposed Government Auditing Standards AICPA Standards (SAS 132, 133)

3. AICPA – Other Items PEEC, State and Local Government Entities SSAE Exposure Draft, Selected Procedures

4. Other Emerging Issues Legislative transparency initiatives

2

Uniform Guidance Implementation – Current Developments

• OMB released M‐17‐26 on June 15, 2017– Reduces burden for federal agencies

• OMB issued latest round of FAQs in July 2017– 24 new FAQs bringing total to 122

• 2018 Compliance Supplement– A “skinny supplement”

• President’s Management Agenda – March 2018• Draft 2019 SF‐SAC (Data Collection Form) – April 2018• Proposed Rule change expected in summer 2018

3

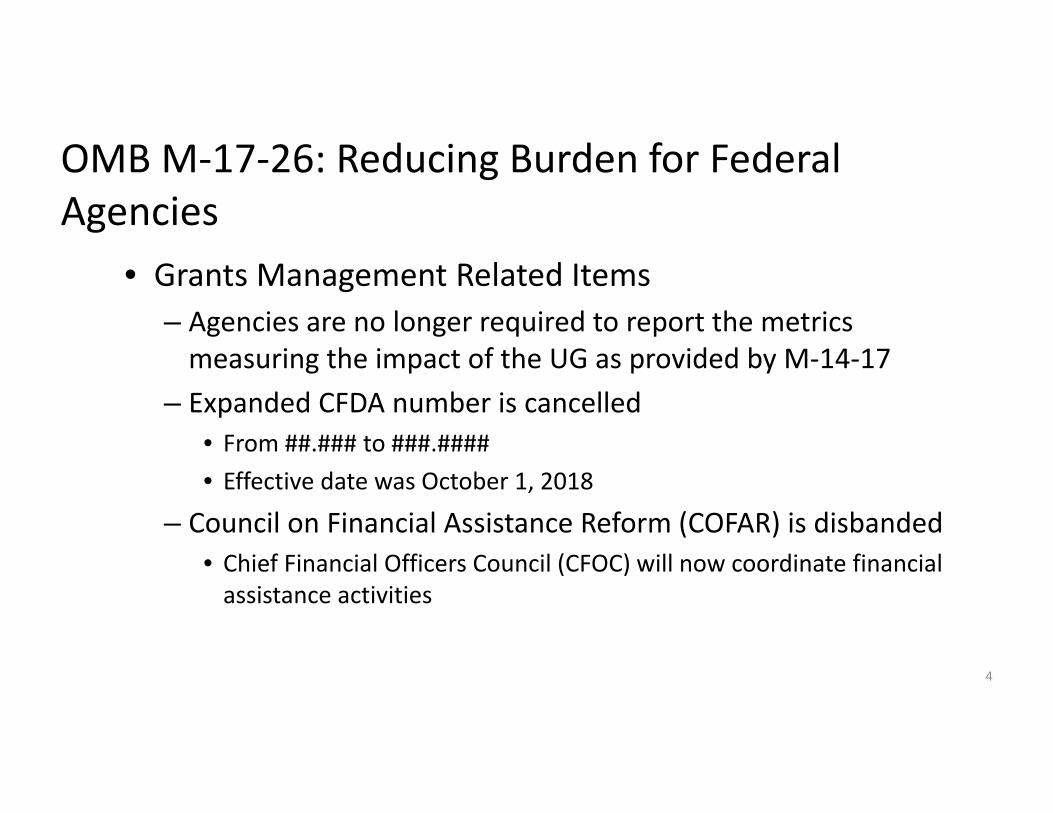

OMB M‐17‐26: Reducing Burden for Federal Agencies

• Grants Management Related Items– Agencies are no longer required to report the metrics measuring the impact of the UG as provided by M‐14‐17

– Expanded CFDA number is cancelled• From ##.### to ###.####• Effective date was October 1, 2018

– Council on Financial Assistance Reform (COFAR) is disbanded• Chief Financial Officers Council (CFOC) will now coordinate financial assistance activities

4

Implementation Issue: Corrective Action Plan on Auditee Letterhead

• New FAQ 200.511‐1– Addresses the auditee’s responsibility for preparing the Summary Schedule of Prior Findings and the Corrective Action Plan

– Now specifies that “the auditee must submit the corrective action plan on auditee letterhead”

• Causing some states problems, especially local government audits

5

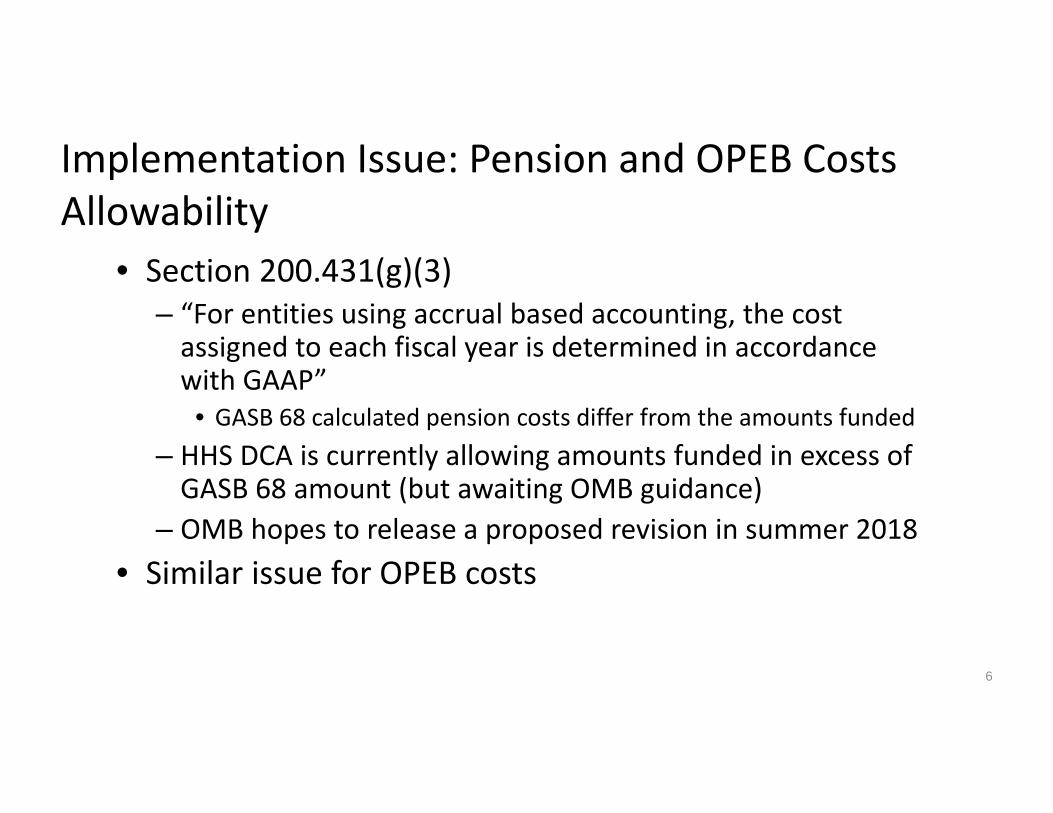

Implementation Issue: Pension and OPEB Costs Allowability

• Section 200.431(g)(3)– “For entities using accrual based accounting, the cost assigned to each fiscal year is determined in accordance with GAAP”

• GASB 68 calculated pension costs differ from the amounts funded– HHS DCA is currently allowing amounts funded in excess of GASB 68 amount (but awaiting OMB guidance)

– OMB hopes to release a proposed revision in summer 2018• Similar issue for OPEB costs

6

Current Developments: Testing SFA Cluster as Major

• U.S. Department of Education (ED)– Section 487(c) of the Higher Education Act of 1965 (HEA) requires that each

Title IV participating institution submit a financial and compliance audit “on at least an annual basis”

• Conflicts with UG when SFA cluster is not selected as a major program – ED issued memo on August 5, 2016

• If Title IV programs are low risk, institutions should “contact their respective School Participation Division.”

• Same guidance applied for FY 2017 audits– ED issued guidance on March 29, 2018 regarding FY 2018 single audits

• Public and non‐profit entities with institutions participating in the Title IV programs that submit a Single Audit that does not include the Student Financial Assistance Cluster as a major program will no longer be required to notify their respective School Participation Division of the low‐risk assessments

• The impact on year three testing requirements (after two years of low risk assessments) for fiscal year 2019 audits and beyond is still under review

7

Current Developments: Securing Student Information

• ED is also adding a new special test and provision on Securing Student Information – ED considers IHEs to be financial institutions under the Gramm‐Leach‐Bliley

Act (GLBA)– Plans to issue in 2018 Compliance Supplement

• Audit Objectives– Determine whether the IHE designated an individual to coordinate the information security

program; performed a risk assessment that addresses the three areas noted in 16 CFR 314.4 (b) and documented safeguards for identified risks

• Suggested Audit Procedures a. Verify that the IHE has designated an individual to coordinate the information security

programb. Obtain the IHE risk assessment and verify that it addresses the three required areas noted in

16 CFR 314.4 (b)c. Obtain the documentation created by the IHE that aligns each safeguard with each risk

identified from step b above, verifying that the IHE has identified a safeguard for each risk

8

2018 Compliance Supplement

• OMB will be issuing the Compliance Supplement every two years– Future issue date would be January– 2018 Compliance Supplement will be a “skinny” version (approx. 35 pages) to address major changes from 2017

• “Skinny” version was expected in February 2018• Federal agencies would use 2018 to take a hard look at their compliance requirements

– Practical transition issues• What will be auditors’ responsibilities in 2018?

9

President’s Management Agenda

• Issued March 20, 2018– Contains various cross‐agency priority (CAP) goals

• Results‐Oriented Accountability for Grants– Seeks to rebalance compliance efforts with a focus on results – Standardize grant reporting data and improve data collection in ways that will increase efficiency, promote evaluation, reduce reporting burden

– Measure progress and share lessons learned and best practices to inform future efforts, and support innovation to achieve results

10

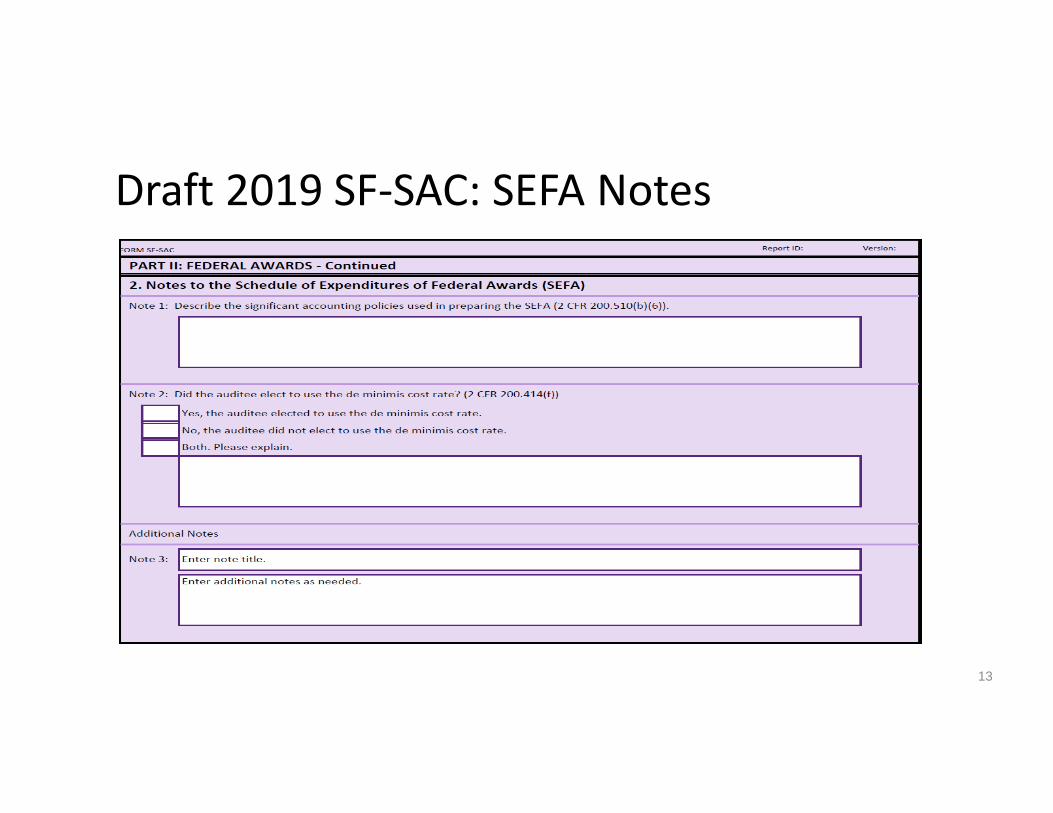

Draft 2019 SF‐SAC (Data Collection Form)

• Published for comments in Federal Register on April 3, 2018– Comment period ends June 4, 2018– Should be used for audits covering fiscal periods ending in 2019, 2020 or 2021.

• Audits with FY ending prior to January 1, 2019 must use the appropriate year form

– New form is designed to enable streamlined reporting (a DATA Act goal)

11

Draft 2019 SF‐SAC (Data Collection Form)

• New items:1. Notes to the Schedule of Expenditures of Federal

Awards (SEFA) (Part II, item 2)2. Written communications (management letters) issued

to the auditee (Part III, item 2(f))3. Text of the audit findings (Part III, item 5)4. Corrective action plan (Part IV)5. Auditee certification statement (Part V, item 1) 6. Auditor statement (Part V, item 2)

12

Draft 2019 SF‐SAC: SEFA Notes

13

Draft 2019 SF‐SAC: Audit Findings

14

Draft 2019 SF‐SAC: Corrective Action Plan

15

AUDIT STANDARDS UPDATE

16

Government Auditing Standards

• “Yellow Book” or• Generally Accepted Government Auditing Standards (“GAGAS”)

17

GAO’s Government Auditing Standards

• Exposure Draft issued April 6, 2017– First proposed changes since 2011– Comment period ended July 6, 2017– Why Issued?

• Represents a modernized version that takes into account developments in the accounting and auditing professions

• Intended to reinforce principles of transparency and provide a framework for high quality government audits

– Effective date: to be determined– Anticipated issue date: 2018– http://gao.gov/yellowbook/overview

18

GAO’s Government Auditing Standards

• Some of the key proposed changes:1. New format and organization of GAGAS2. Independence threats related to preparing records and

financial statements3. Independence guidance related to three‐party

arrangements4. Independence guidance related to professional services

in government5. GAGAS qualification for CPE requirement

19

GAO’s Government Auditing Standards

• Key proposed changes (cont.):6. CPE guidance for 24‐hour and 56‐hour requirements7. Peer review requirements8. Internal control: financial audits, examination

engagements, and performance audits9. New requirements for waste10. Standards for reviews of financial statements

20

GAO’s Government Auditing Standards

• Independence Threats: Preparing Accounting Records and Financial Statements (3.89)– Any services performed by auditors related to preparing accounting records and FS, other than those defined as impairments, create significant threats to auditors’ independence

– Auditors should:• Document the threats and safeguards applied to eliminate and reduce threats to an acceptable level OR

• Decline to perform the service

21

GAO’s Government Auditing Standards

• New Requirements for Waste– For financial audits, examination engagements, and performance audits,

standards are expanded to require that auditors perform audit procedures to ascertain the potential effect on the audit objectives if they become aware of waste (6.16, 7.18, 8.69)

• Auditors are required to report when waste has occurred that is material or has a significant effect on the audit objectives for financial audits, examination engagements, and performance audits (6.35, 7.41, 9.32)

• Auditors are required to communicate in writing waste that does not have a material or significant effect on the audit objectives but warrants the attention of those charged with governance for financial audits, examination engagements, and performance audits (6.39, 7.42, 9.33)

22

GAO’s Government Auditing Standards

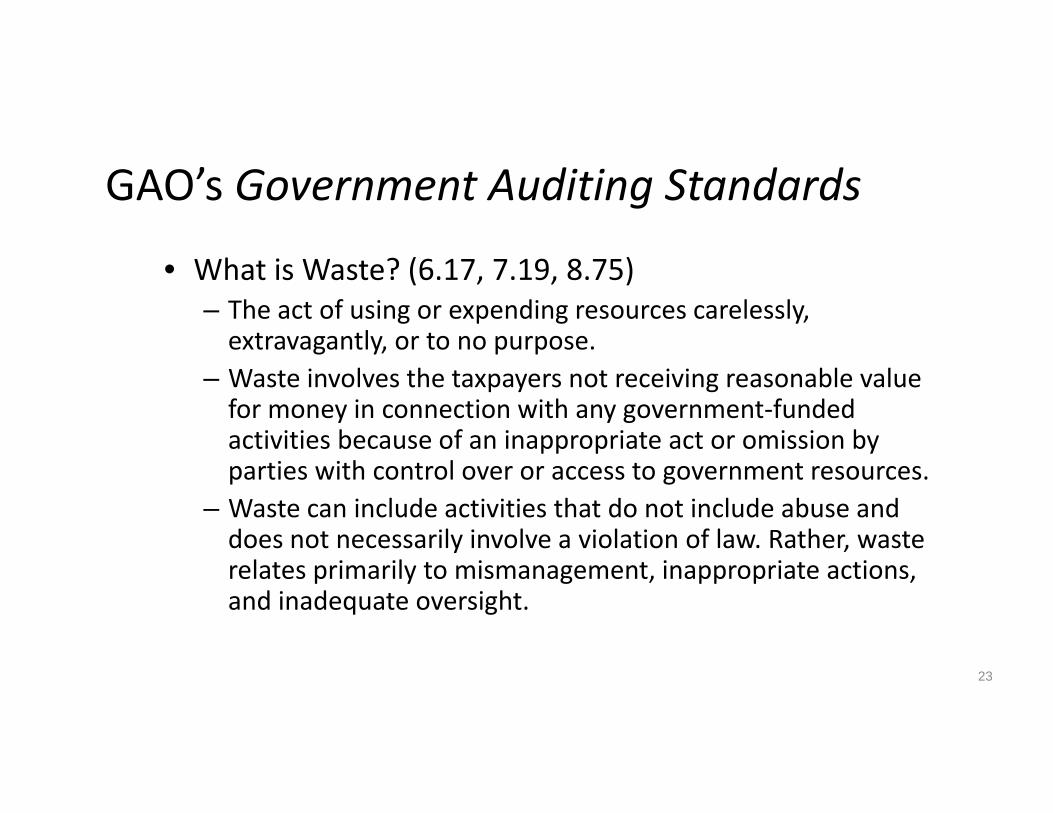

• What is Waste? (6.17, 7.19, 8.75)– The act of using or expending resources carelessly, extravagantly, or to no purpose.

– Waste involves the taxpayers not receiving reasonable value for money in connection with any government‐funded activities because of an inappropriate act or omission by parties with control over or access to government resources.

– Waste can include activities that do not include abuse and does not necessarily involve a violation of law. Rather, waste relates primarily to mismanagement, inappropriate actions, and inadequate oversight.

23

AICPA ASB Update

• New Audit Standards– SAS No. 132 (February 2017)– SAS No. 133 (July 2017)

• Recent Exposure Drafts– Auditor Reporting– Auditor’s Responsibilities Relating to Other Information in Annual Reports

– Omnibus Statement 2018

24

AICPA SAS No. 132 – Going Concern

• The Auditor’s Consideration of an Entity’s Ability to Continue as a Going Concern– Issued on February 22, 2017– Supersedes SAS 126 (same title) – Effective date:

• Audits of financial statements for periods ending on or after December 15, 2017, and

• Reviews of interim financial information for interim periods beginning after fiscal years ending on or after December 15, 2017

– Primary objective is to consider the accounting provisions of FASB Update 2014‐15 & GASB 56

• What is the auditor’s responsibility?

25

AICPA SAS No. 132 – Going Concern

• Significant changes include:– Auditor’s Objectives and Related Conclusions

• Clarifies that the auditor’s objectives include separate determinations and conclusions with respect to:

– The appropriateness of management’s use of the going concern basis of accounting in the preparation of the financial statements; and

– Whether substantial doubt about an entity’s ability to continue as a going concern for a reasonable period of time exists, based on the audit evidence obtained.

26

AICPA SAS No. 133 – Exempt Offering Documents

• Auditor Involvement with Exempt Offering Documents– Issued on July 26, 2017 – AU‐C section 945

• Does not amend or supersede any existing guidance– Effective date:

• For exempt offering documents with which the auditor is involved that are initially distributed, circulated, or submitted on or after June 15, 2018

– Includes private placement offerings, exempt public offerings and municipal securities offerings

– Goal is to determine whether info in the offering document could undermine the credibility of the F/S and the auditor’s report thereon

27

AICPA SAS No. 133 – Exempt Offering Documents

• Key Provisions:– Includes performance requirements when the auditor is involved with an exempt offering document

– Involvement is determined by a two‐benchmark model:• The auditor’s report on F/S or the auditor’s review on interim financial information is included or incorporated by reference in an offering document

• The auditor performs one or more “triggering” specified activities

28

AICPA SAS No. 133 – Exempt Offering Documents

• “Triggering events” include:– Assisting the entity in preparing information included in the offering document

– Reading a draft of the offering document at the entity’s request – Issuing a comfort letter– Participating in due diligence discussions – Issuing an attestation report on information relating to the exempt offering

– Providing written agreement for the use of the auditor’s report in the offering document

– Updating the auditor’s report for inclusion in the offering document

29

AICPA SAS No. 133 – Exempt Offering Documents

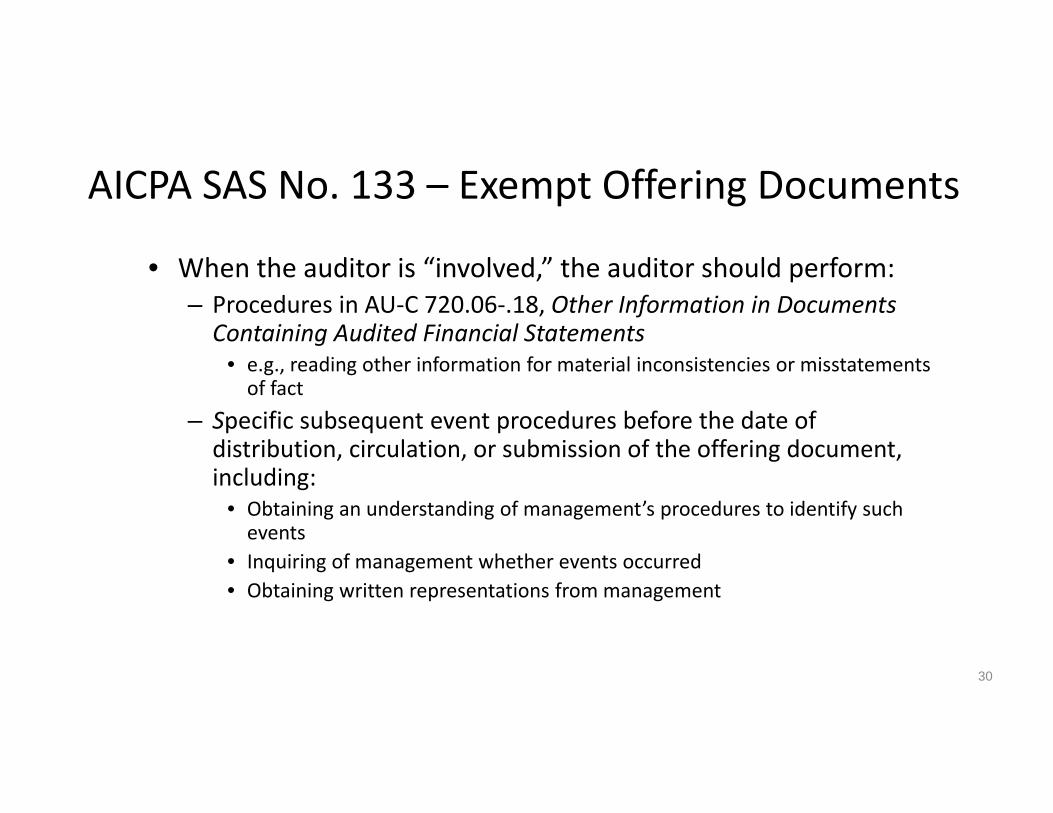

• When the auditor is “involved,” the auditor should perform:– Procedures in AU‐C 720.06‐.18, Other Information in Documents Containing Audited Financial Statements

• e.g., reading other information for material inconsistencies or misstatements of fact

– Specific subsequent event procedures before the date of distribution, circulation, or submission of the offering document, including:

• Obtaining an understanding of management’s procedures to identify such events

• Inquiring of management whether events occurred• Obtaining written representations from management

30

AICPA ED ‐ Auditor Reporting

• The four proposed auditor reporting SASs include:– Forming an Opinion and Reporting on Financial Statements;– Communicating Key Audit Matters in the Independent Auditor’s Report;

– Modifications to the Opinion in the Independent Auditor’s Report; and

– Emphasis‐of‐Matter Paragraphs and Other‐Matter Paragraphs in the Independent Auditor’s Report

• If adopted as proposed, effective dates would be for audits of financial statements for periods ending on or after June 15, 2019

31

AICPA ED ‐ Auditor Reporting

• Key changes:– Moving the opinion to the first paragraph– Adding an affirmative statement about the auditor’s independence and compliance with ethical responsibilities

– New Section • AU‐C 701, Communicating Key Audit Matters in the Independent Auditor’s Report

• Required for issuers (of securities); however, might be required by nonissuers if required by law, regulation, or contractual agreement (e.g., included in the terms of the audit engagement)

32

AICPA – Other Items

• AICPA Proposed SSAE: Selected Procedures– Exposure Draft issued Sept. 1, 2017

• Comments were due December 1, 2017• A new engagement type; different than AUP

– Addresses a market gap that exists between a “verifier” and “adviser”• Proposed standard would:

– Provide flexibility by not requiring the specified parties to either establish the procedures or agree to the sufficiency of the procedures

» Practitioner may determine the procedures– No requirement to either request an assertion or disclose in the report when the assertion is not obtained

– No requirement for the practitioner to restrict the use of the report

33

AICPA – Other Items

• AICPA Professional Ethics Division: State and Local Government Entities– Exposure Draft issued July 7, 2017

• Formerly Entities Included in State and Local Government Financial Statements (ET sec. 1.224.020)

• Addresses a member’s (of the AICPA) independence with respect to entities that are required to be included in a state or local government’s financial reporting entity

34

AICPA – Other Items• AICPA Professional Ethics Division: State and Local Government Entities (cont.)– Makes use of terms downstream, upstream and brother‐sister entities

• Downstream: refers to those entities that are “below” the f/s attest client in its organization structure

– e.g., financial statement attest client is the primary government, funds and component units to be evaluated are those required to be included in the primary government’s financial reporting entity

• Upstream: refers to those entities that are “above” the f/s attest client– e.g., financial statement attest client is a fund or component unit

• Bother‐sister: refers to other funds and component units that the member does not provide attest services to but are included in the same upstream financial reporting entity as the financial statement attest client

35

OTHER EMERGING ISSUES

36

Increasing Transparency: The Continuing Story

• FFATA (2006)– Ongoing monthly reporting of federal awards and contracts at prime/first‐tier sub levels

• DATA (2014)– Amends FFATA

• GREAT (2018)– Proposed legislation to further DATA

37

DATA Act: Timeline/Deadlines

• May 2015– Establish data standards

• May 2017– Federal agencies must report spending data using data standards

• August 2017– OMB must report Section 5 pilot results

• May 2018– Federal agencies must post spending data in machine‐readable formats

38

DATA Act: Section 5 Pilot

• A pilot program shall be established to develop recommendations for the:– Use of standardized reporting elements across the Federal government

– Elimination of unnecessary duplication in financial reporting, and

– Reduction of compliance costs for recipients• Two work streams dealing with procurement and financial assistance

39

DATA Act: Section 5 Pilot• Report issued on August 10, 2017• Key findings on financial assistance (six pilot areas)

– Consolidated Federal Financial Reporting (FFR, SF 425) • Grant recipients entering FFR info systematically through one entry point with that information being shared electronically from that point forward, would reduce recipient burden and improve data accuracy

– Analysis found that allowing grantees to submit their complete FFR one time and through a single entry point (HHS’s Payment Management System) instead of multiple entry points was very productive

– This built on previous inconclusive findings from testing by the Recovery and Transparency Board

40

DATA Act: Section 5 Pilot

• Key findings (cont.)– Single Audit

• If grant recipients do not have to report the same info on duplicative forms (SEFA and SF‐SAC), but rather allow information reported once to be auto‐populated electronically, grant recipient’s burden would be reduced

– Majority of participants responded that the new SEFA template and FAC pilot reporting tool saves time and increases accuracy

– Revised SF‐SAC was published for comment in April 2018

41

DATA Act: Section 5 Pilot

• Report Recommendations – Pursue further standardization to increase opportunities to streamline reporting

– Seize opportunities to use information technology that can auto‐populate reporting fields from existing Federal sources

– Leverage information technology open standards to rapidly develop new tools

42

GREAT Act

• H.R. 4887 – The Grant Reporting Efficiency and Agreements Transparency (GREAT) Act– Introduced January 29, 2018– Continuation of the vision of the DATA Act– Requires data structure (taxonomy) to cover all the data elements required of recipients of federal funds

43

GREAT Act

• Requirements:– Establish government‐wide data standards for information related to federal awards reported by recipients of federal awards (within 1 year).

– Issue guidance to grantmaking agencies on how to utilize new technologies and implement new data standards into existing reporting practices with minimum disruption (within 2 years).

– Amends the Single Audit Act to provide for grantee audits to be reported in an electronic format consistent with the data standards (guidance to be issued within 2 years)

44

GASB Current Technical Agenda

Major Projects

Practice Issues

Pre-Agenda Research

Overview

Financial Reporting Model/Conceptual Framework

Public‐Private Partnerships

Revenue and Expense Recognition

Capitalization ofInterest Costs

Cloud Computing Arrangements

Conduit Debt

Equity Interest Ownership

Implementation Guides

Pre‐Agenda Research

www.gasb.org

GASB Final Standards

Newly Issued• GASB 87 – Leases• GASB 88 – Debt Disclosures• Implementation Guides: 2017‐3and 2018‐1

Previously Issued• GASB 75 – OPEB* • GASB 83 – AROs• GASB 84 – Fiduciary• GASB 85 – Omnibus• GASB 86 – Debt Extinguishment

* Not covered today

56

New Standards

57

GASB Statement No. 87Leases

Issued: June 2017Effective Date: Periods beginning after December 15, 2019

GASB 87: Leases• Establishes revised standards on lease accounting and reporting

• Eliminates capital and operating leases• Treats leases as intangible “right to use” asset and long term liability for lessee

• Effective for reporting periods beginning after December 15, 2019.

Earlier application is encouraged.

59

Excluded from Scope• Excluded from scope of GASB 87

– Leases for:• Intangibles (includes computer software)

– Exception ‐ Sublease of the intangible right‐to‐use a leased tangible asset

• Biological assets• Inventory

– Leases where underlying asset is financed with conduit debt• Exception ‐ underlying asset and conduit debt reported by lessor

– Service concession agreements– Supply contracts

60

What is a Lease?Definition of a lease:

A contract that conveys the right to use another entity’s nonfinancial asset (the underlying asset) as specified in the contract for a period of time in an exchange or exchange‐like transaction

• Contract – legally enforceable (written or oral)• Right to use underlying asset –

– Obtain present service capacity – Determine nature and manner of use

• Nonfinancial asset –– Land, buildings, equipment; not securities

61

Lease Term

Period during which lessee has:– Noncancelable right to use underlying asset,– Plus periods* where

• Lessee or lessor has option to extend (if exercise is reasonably certain), and

• Lessee or Lessor has option to terminate (if notexercising is reasonably certain)

– Includes fiscal funding clauses

* Factor into expected future lease payments 62

Exceptions• Short term lease – A lease that, at its beginning, has a maximum

possible term under the contract of 12 months or less, including all options to extend– Recognize revenue or expense when payments are due– No revenue or expense during rent holidays

• Contracts that transfer ownership – A contract whereby a lessee will become owner of the underlying asset at end of contract term and that contains no termination options (except fiscal funding clauses reasonably certain not to be exercised)– Account for as a financed purchase of the underlying asset

63

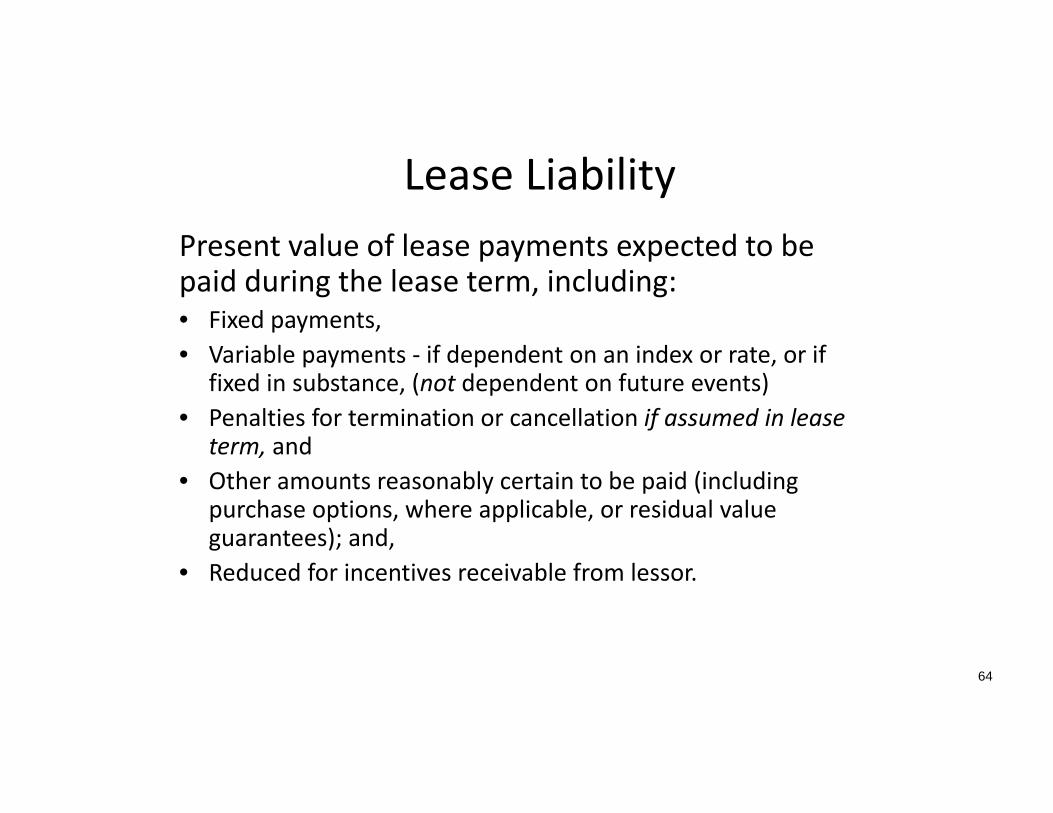

Lease LiabilityPresent value of lease payments expected to be paid during the lease term, including:• Fixed payments, • Variable payments ‐ if dependent on an index or rate, or if

fixed in substance, (not dependent on future events)• Penalties for termination or cancellation if assumed in lease

term, and• Other amounts reasonably certain to be paid (including

purchase options, where applicable, or residual value guarantees); and,

• Reduced for incentives receivable from lessor.

64

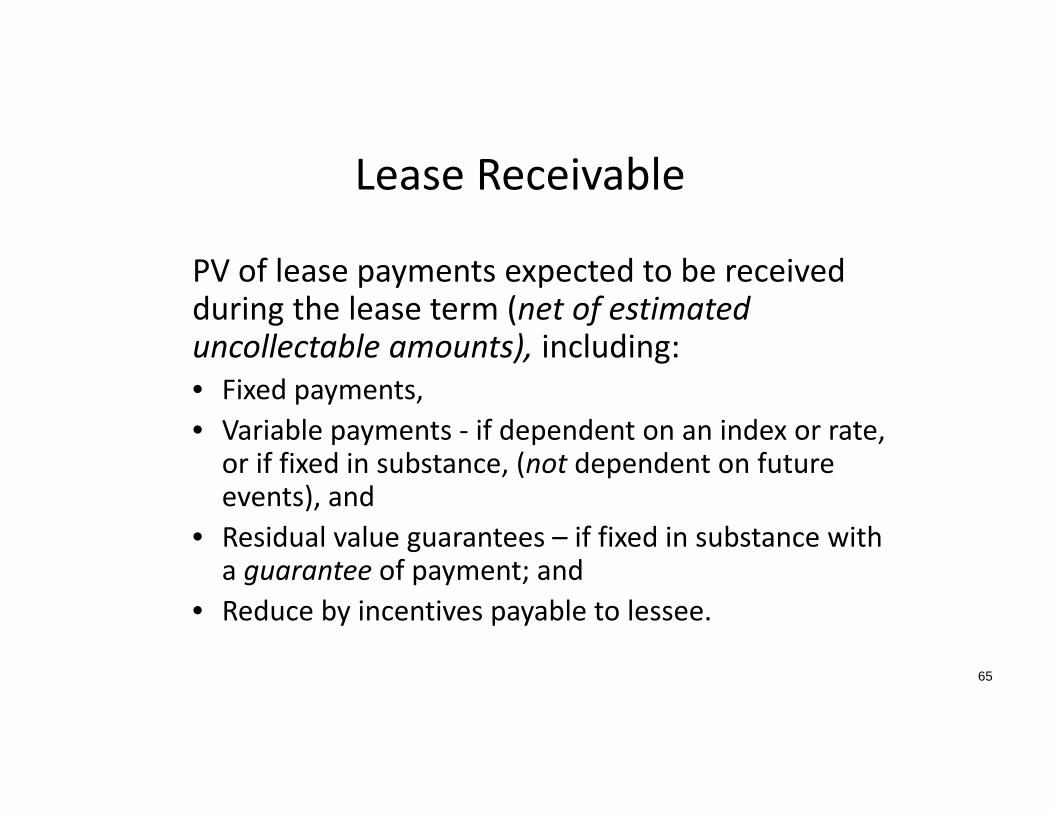

Lease Receivable

PV of lease payments expected to be received during the lease term (net of estimated uncollectable amounts), including:• Fixed payments,• Variable payments ‐ if dependent on an index or rate, or if fixed in substance, (not dependent on future events), and

• Residual value guarantees – if fixed in substance with a guarantee of payment; and

• Reduce by incentives payable to lessee.

65

Discount Rates for PV

• Lessee – discount rate is:– Rate charged by lessor, if determinable, or– Estimate of the rate that the lessee would have to pay to borrow the lease payment amounts during the lease term.

• Lessor – discount rate is the rate charged to the lessee.

66

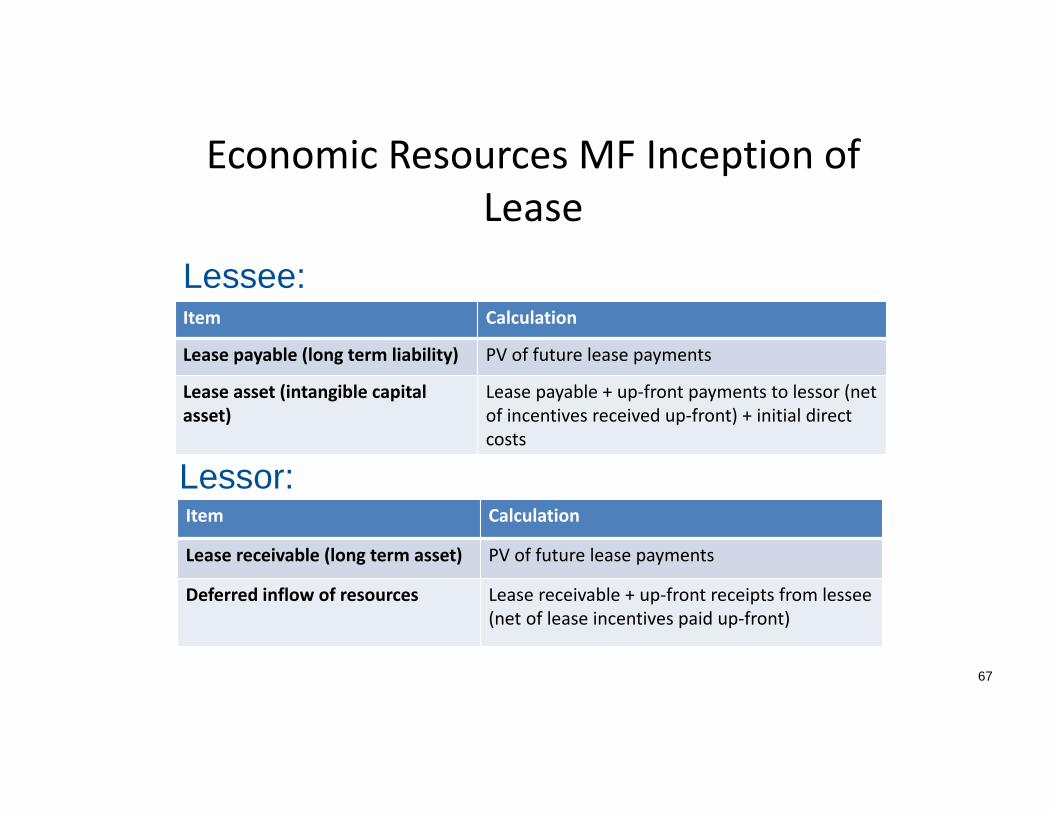

Economic Resources MF Inception of Lease

Item Calculation

Lease payable (long term liability) PV of future lease payments

Lease asset (intangible capital asset)

Lease payable + up‐front payments to lessor (net of incentives received up‐front) + initial direct costs

67

Item Calculation

Lease receivable (long term asset) PV of future lease payments

Deferred inflow of resources Lease receivable + up‐front receipts from lessee (net of lease incentives paid up‐front)

Lessor:

Lessee:

Economic Resources MFPeriodic Activity ‐ Lessee

Item Calculation

Lease payable ‐ Principal portion of lease payment

Interest expense Interest portion of lease payment

Amortization expense/ accumulatedamortization of lease asset

Systematic & rational allocation of lease asset over life of lease* (report with depreciation on other capital assets)

68

* Amortize over life of underlying asset instead if: 1) shorter or 2) purchase option reasonably certain of being exercised.

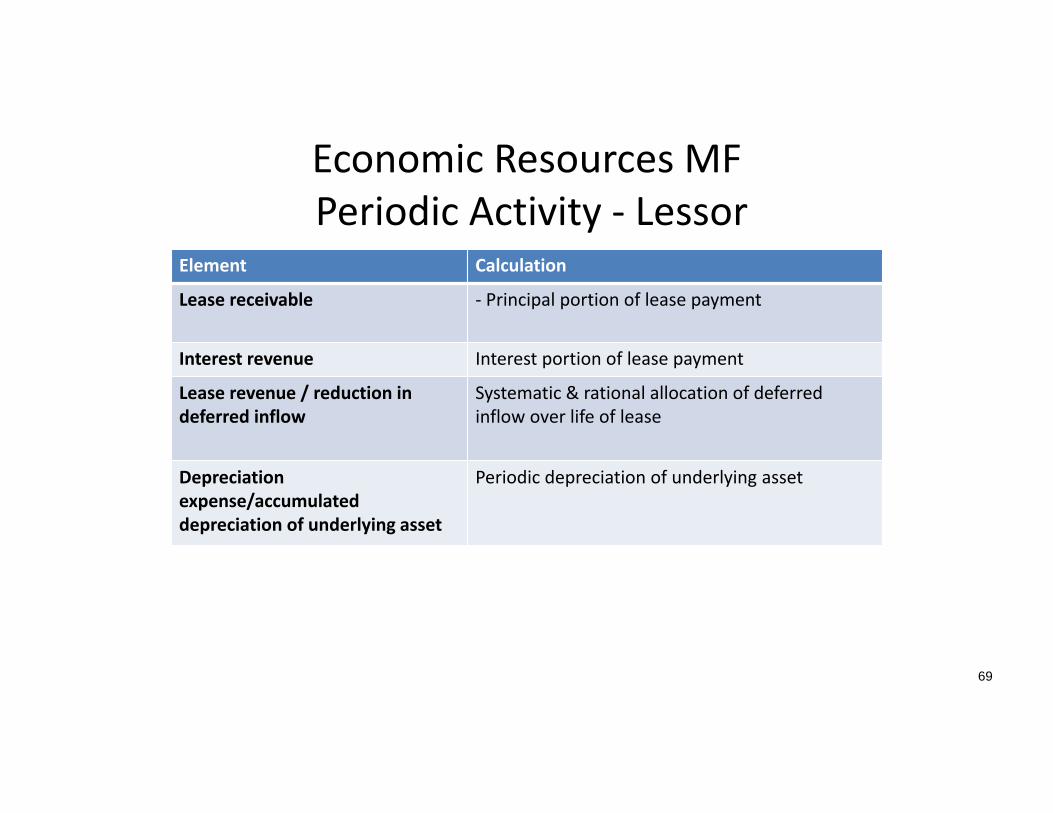

Economic Resources MFPeriodic Activity ‐ Lessor

Element Calculation

Lease receivable ‐ Principal portion of lease payment

Interest revenue Interest portion of lease payment

Lease revenue / reduction in deferred inflow

Systematic & rational allocation of deferred inflow over life of lease

Depreciation expense/accumulated depreciation of underlying asset

Periodic depreciation of underlying asset

69

Current Financial Resources MFInception of Lease

Lessee Lessor

Other Financing Source PV of future lease payments

Expenditure ‐ Capital PV of future lease payments

Lease Receivable PV of future lease payments + up‐front payments from lessee

Deferred Inflow of Resources PV of future lease payments + up‐front

payments from

70

Unchanged from Current Standards

Current Financial Resources MFPeriodic Activity

Lessee Lessor

Debt service expenditure Periodic lease paymentmade (separate principal

and interest)

Lease revenue / reduction in deferred inflow

Amortization of deferred inflows of resources

interest revenue Interest portion of lease payment received

lease receivable ‐Principal portion of lease payment received

71

Unchanged from Current Standards

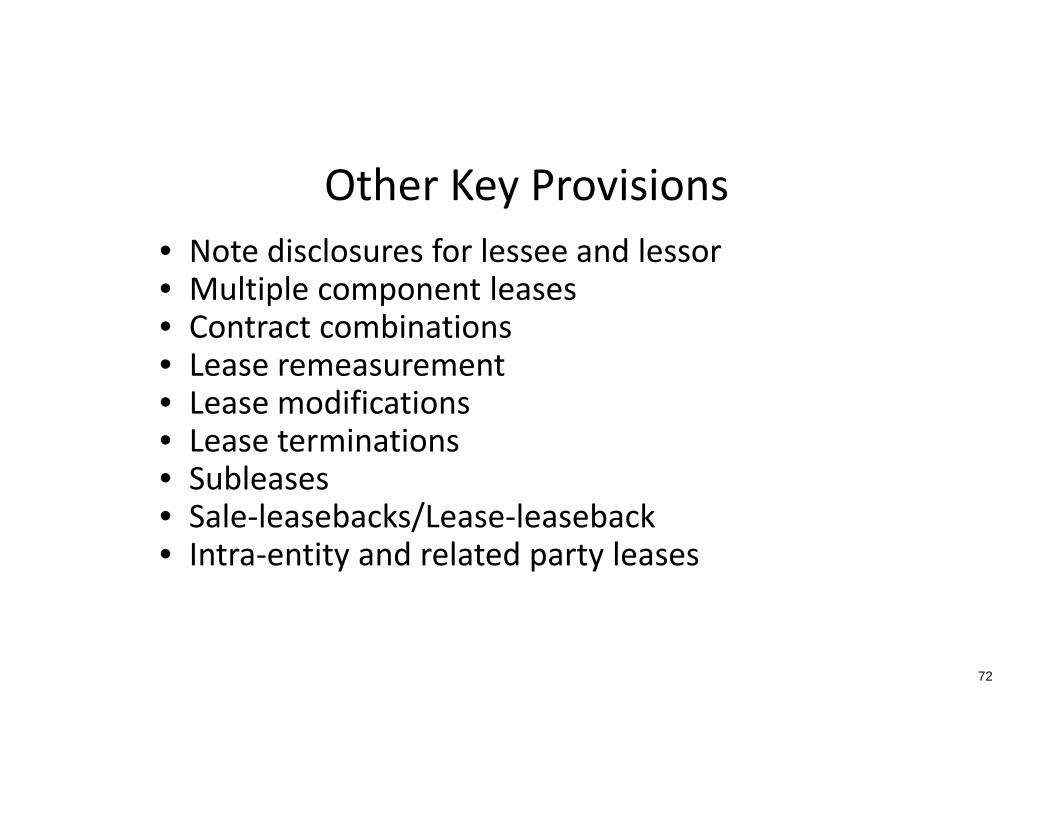

Other Key Provisions• Note disclosures for lessee and lessor• Multiple component leases • Contract combinations• Lease remeasurement• Lease modifications• Lease terminations• Subleases• Sale‐leasebacks/Lease‐leaseback • Intra‐entity and related party leases

72

Effective Date• Periods beginning after December 15, 2019• Apply retroactively

– Facts and circumstance of the lease in period of implementation (not inception of the lease)

• Remaining lease payments at beginning of period will become the future lease payments

– Restatement of beginning net position in period of implementation may be needed

• GASB implementation guide under development now– Scheduled release 2nd Quarter 2019 (ED 1st Quarter 2019)

• Begin analysis now73

GASB Statement No. 88 Certain Disclosures Related to Debt,including Direct Borrowings andDirect Placements

Issued: March 2018Effective Date: Periods beginning after June 15, 2018

GASB 88• Establishes new note disclosure requirements for long term debt, including direct borrowings and placements.

• Effective for reporting periods beginning after June 15, 2018. Earlier application is encouraged.

75

Purpose

• Many governments use bank loans or private placement of debt instead of accessing the bond market – Lower costs of issuance / complexity– relationship with local bank

• Accelerated payment requirements and other provisions of private debt expose governments to financial risks

• Inconsistent interpretation and application of disclosure requirements for such debt

76

Definition of Debt

• A liability that arises from a contractual obligation to pay cash (or other assets that may be used in lieu of cash) in one or more payments to settle an amount that is fixed at the date the contractual obligation is established.

• Excludes leases (except for contracts reported as a financed purchase of the underlying asset) and accounts payable.

77

Additional Disclosures

• Amount of unused lines of credit• Assets pledged as collateral for debt• Terms specified in debt agreements related to significant:

– Events of default with finance‐related consequences, – Termination events with finance‐related consequences, and – Subjective acceleration clauses.

78

Additional Disclosures (cont.)

• Separate information in debt disclosures for– Direct borrowings and direct placements of debt – Other debt

79

New GASB Implementation Guidance

80

Implementation Guide No. 2017-3, Accounting and Financial Reporting for Postemployment Benefits Other Than Pensions (and Certain Issues Related to OPEB Plan Reporting)

Issued: November 2017Effective Date: Periods beginning after June 15, 2017 (later effective dates for certain topics)

Implementation Guide 2017‐3• Comprised of 506 questions & answers

– 502 questions regarding employer OPEB (GASB 75/Cod. P50‐54)

– 4 questions regarding OPEB plans that arose after IG 2017‐2 was issued (GASB 74/Cod. Po50‐51)

– Less than 10% are truly “new” questions (no currently authoritative “predecessor questions” covering pension or OPEB)

– many are repeated under various classifications

82

Topics of New Questions

• Use of risk financing for OPEB when used for active employee health insurance

• Benefits other than OPEB provided through pension plan (life insurance, LT care)

• Administrative costs • Attribution periods for employees expected to “age out” of eligibility before retiring

• Employer fund balance classification for plans not administered through a GASB trust

83

Effective Dates

• Varied implementation dates:– Most – periods beginning after June 15, 2017– Actuarial valuation – for valuations as of December 15, 2017 or later

– Alternative measurement method – for financial statements including a NOL with a measurement date as of June 15, 2018 or later

– Earlier application encouraged once the related standard (GASB 75 or 74) is implemented

84

Implementation Guide No. 2018-1, Implementation Guidance Update - 2018 Issued: May 2018*Effective Date: Periods beginning after June 15, 2017 (certain questions effective periods beginning after June 15, 2018)

17 Questions & Answers ‐ Topics

9 New Q&A’s• Pension – 1• OPEB – 1• CAFR statistical section – 1• Regulated operations– 2• Tax abatements – 4

8 Clarifying* Changes• Deposits and investments – 2• Pensions – 2• Basic F/S and MD&A – 2• CAFR statistical section – 1• Tax abatements – 1* Non‐substantive changes

86

PensionNew:• Each plan member, as of the measurement date, should be counted as one in the denominator of the calculation of average expected remaining service lives. There should not be weighting.

87

OPEB

New:• The effects of ad‐hoc postemployment benefit changes for inactive members should be reported as a change in benefits in the schedule of changes in the net OPEB liability

88

CAFR Statistical SectionNew:• All types of debt outstanding during the 10‐year period

are included in debt capacity schedules, even if that type is no longer outstanding

Revised:• Clarifying change to Cod 2800.714‐4 (GASBIG 2015‐1,

Q9.24.4):• Defeased debt is excluded from debt capacity schedule,

beginning in the year of defeasance; but amounts outstanding in prior years should continue to be reported there.

89

Regulated OperationsNew:1. A utility that meets the requirements and elects to

apply regulated operations accounting (GASB COD Re10, Regulated Operations) should report period costs that are approved for recovery in future periods as regulatory assets rather than expenses.

2. The above would only apply where the regulatory rate setting applies to the entire operation.

90

Tax Abatements

4 New:• An agreement between a government and a developer in which the government provides tax revenue to a developer in exchange for construction of or improvement to an asset that will belong to the government is not an abatement.

91

Tax Abatements (continued)

• An agreement in which a government freezes the assessed value of a property for a period of time in exchange for the owner’s agreement not to change the property’s use during the period, is an abatement.

• The transferability of tax credits does not enter into the determination of whether the agreement creating them is an abatement.

92

Tax Abatements (continued)

• The amount disclosed for an abatement should be the reporting government’s reduction in tax revenues that result from an abatement agreement.

Revised:• Clarifying change to Cod T10.702‐1 (GASBIG 2016‐1,Q4.77)• Tax increment financing is not an abatement

– No agreement with taxpayer– No reduction in revenue

93

Review of Previously Issued Standards Not Yet Effective

94

GASB Statement No. 83Certain Asset Retirement Obligations

Issued: November 2016Effective Date: Periods beginning after June 15, 2018

What is an ARO?• Asset retirement obligation (ARO)

– Legally enforceable liability associated with the retirement of a tangible capital asset

• Retirement = sale, abandonment, recycling, other types of disposal, Permanent end of use, and

– Results from the normal operations of capital assets.

• Examples ‐ costs associated with:• Decommissioning nuclear reactors and medical imaging equipment

• Dismantling and removing sewage treatment plants and waste‐to‐energy plants

• Removal and disposal of wind turbines, solar farms96

Governmental funds

• No change from current accounting and reporting

• Recognize liabilities and expenditures for goods and services when received, to the extent due and payable

97

Economic Resources MF Determination of Recognition

Occurrence of external obligating event

Occurrence of internal obligating event

Recognize if liability is reasonably estimable

98

Source of potential obligation

Circumstances that trigger the obligation

Recognize when a liability is incurred and the amount is reasonably estimable.

Incurred if two events occurred:

External Obligating Events

Sources of ARO obligations:• Approval of laws and regulations establishing disposal requirements

• Creation of a legally binding contract• Issuance of a court judgment

99

Internal Obligating Events

Events that trigger obligations:

A. Acquisition Example: County acquires a power plant with a pre‐existing ARO Recognize : When asset is first acquired

B. Contamination (based on normal usage) Example: Nuclear medical imaging equipment, such as an MRI Recognize: When contamination first occurs – initial testing

100

Internal Obligating Events (cont.)Triggers, continued:

C. Pattern of usage Examples: logging, mining Recognize: when operations begin and some usable capacity

is consumed

D. Not based on usage Example: Wind turbines Recognize: when placed in service

E. Abandonment Example: power plant abandoned before completion Recognize: when abandoned

101

Recognition

• Recognize:– Credit an ARO liability – Debit ‐

• Deferred outflow of resources – Recognize as expense in a systematic and rational manner over useful life

• Expense– Abandonment before asset is ready for use

102

Initial Measurement

• Similar to pollution remediation requirements (Cod. P40, GASB 49)

• Best estimate of current value (not PV) of expected outlays (available evidence)

• Probability weighting of potential outcomes Like for pollution remediation

• If undetermined, use most likely amount in range of possible outcomes

103

Annual Remeasurement• Adjust for effects of inflation/deflation• Evaluate effect of all other relevant factors

– Changes in: • Price not attributable to inflation or deflation• Technology• Legal requirements• Type of equipment, facilities, or services that will be used to meet ARO

– Adjust estimated asset retirement outlays for these factors only if effects are significant

104

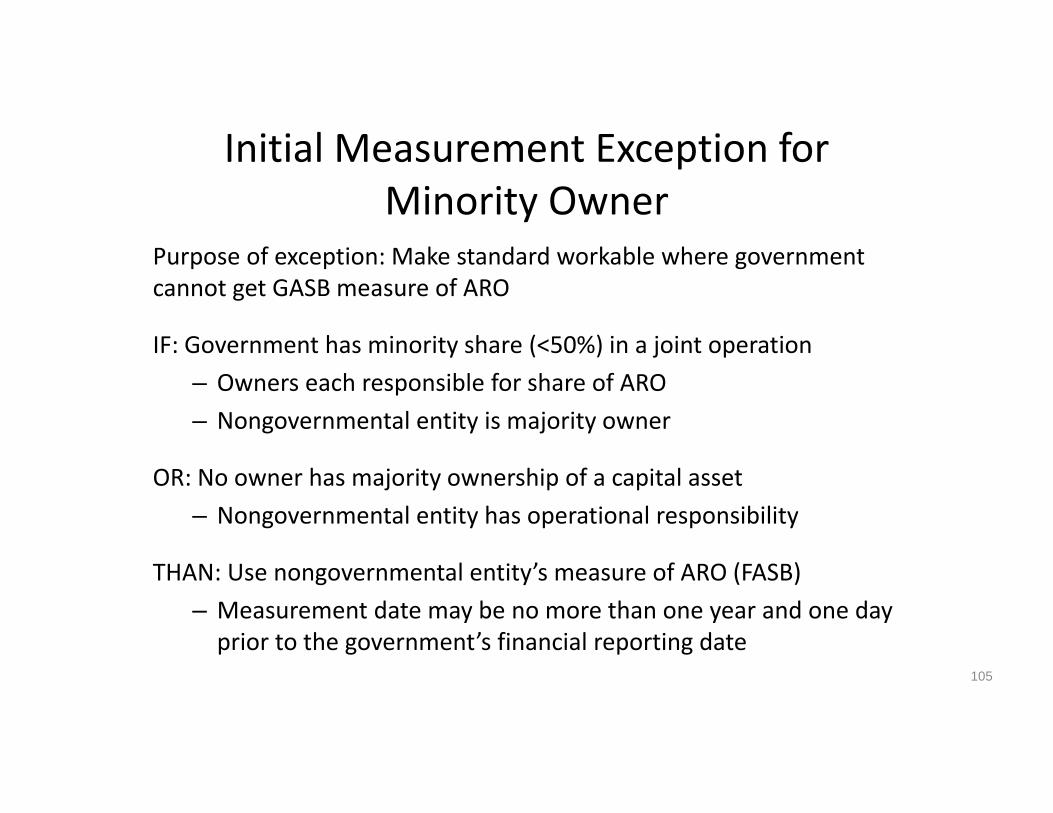

Initial Measurement Exception for Minority Owner

Purpose of exception: Make standard workable where government cannot get GASB measure of ARO

IF: Government has minority share (<50%) in a joint operation – Owners each responsible for share of ARO– Nongovernmental entity is majority owner

OR: No owner has majority ownership of a capital asset– Nongovernmental entity has operational responsibility

THAN: Use nongovernmental entity’s measure of ARO (FASB)– Measurement date may be no more than one year and one day prior to the government’s financial reporting date

105

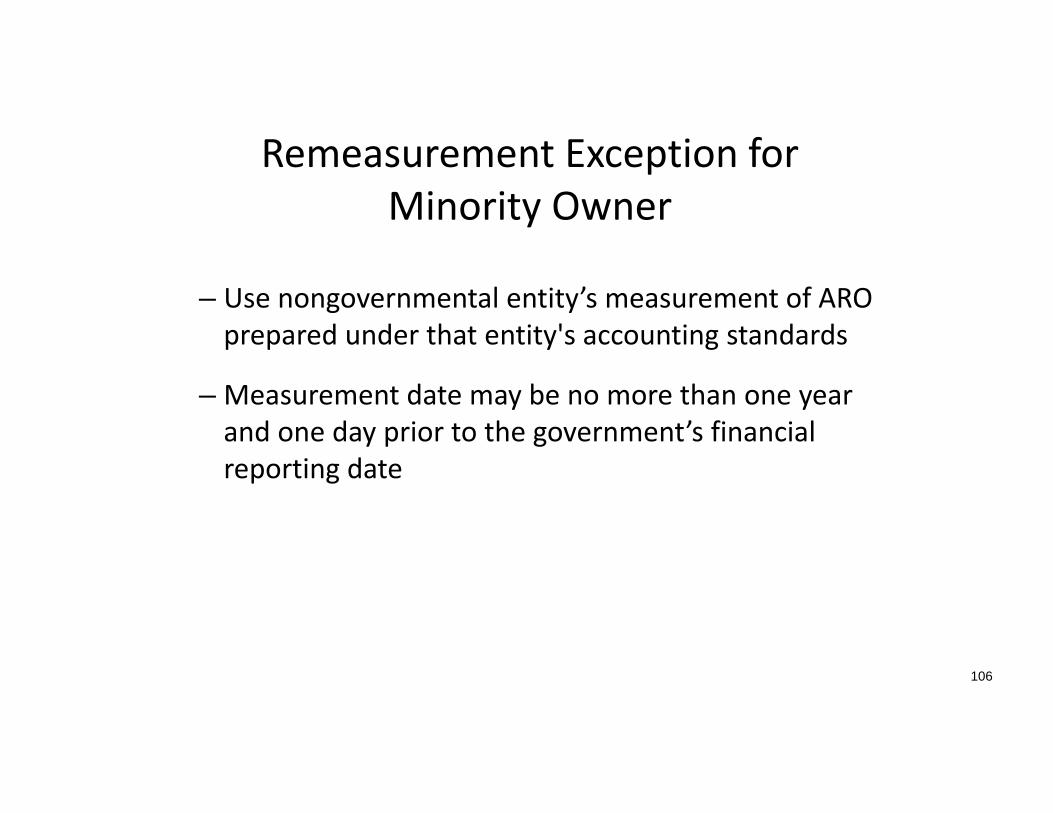

Remeasurement Exception for Minority Owner

– Use nongovernmental entity’s measurement of ARO prepared under that entity's accounting standards

– Measurement date may be no more than one year and one day prior to the government’s financial reporting date

106

Treatment of Changes in Estimate

• Prior to retirement of capital asset ‐– Prospective change in amortization

• After retirement of capital asset ‐– Immediate recognition

107

Expensing of Deferred Outflows

• If: deferred outflows were initially reported at the beginning of the asset’s useful life,– Than: recognize over the asset’s entire estimated useful life

• If: deferred outflows initially reported after asset was in service but before the end of its estimated useful life,– Than: recognize over the remaining life, starting from time of recognition

108

Financial Assurance Requirements

• Cannot offset restricted assets against the ARO• Disclose:

– How those requirements are being met– Amounts of assets restricted for payment (if not displayed separately)

109

Other Note Disclosures

• General description of ARO and associated assets, as well as the source of obligations

• Methods and assumptions used to estimate AROs• Estimated remaining useful life of associated assets

• Any liability for an ARO that has not been recognized only because it is not yet reasonably estimable (and the reason)

• If applicable, disclosures for minority share110

GASB Statement No. 84Fiduciary Activities

Issued: January 2017Effective Date: Periods beginning after December 15, 2018

Identification of Fiduciary Activities

1. Fiduciary component units:– PEB (pension and OPEB)– Other (non‐PEB)

2. Non‐CU pension and OPEB 3. Other fiduciary activities

112

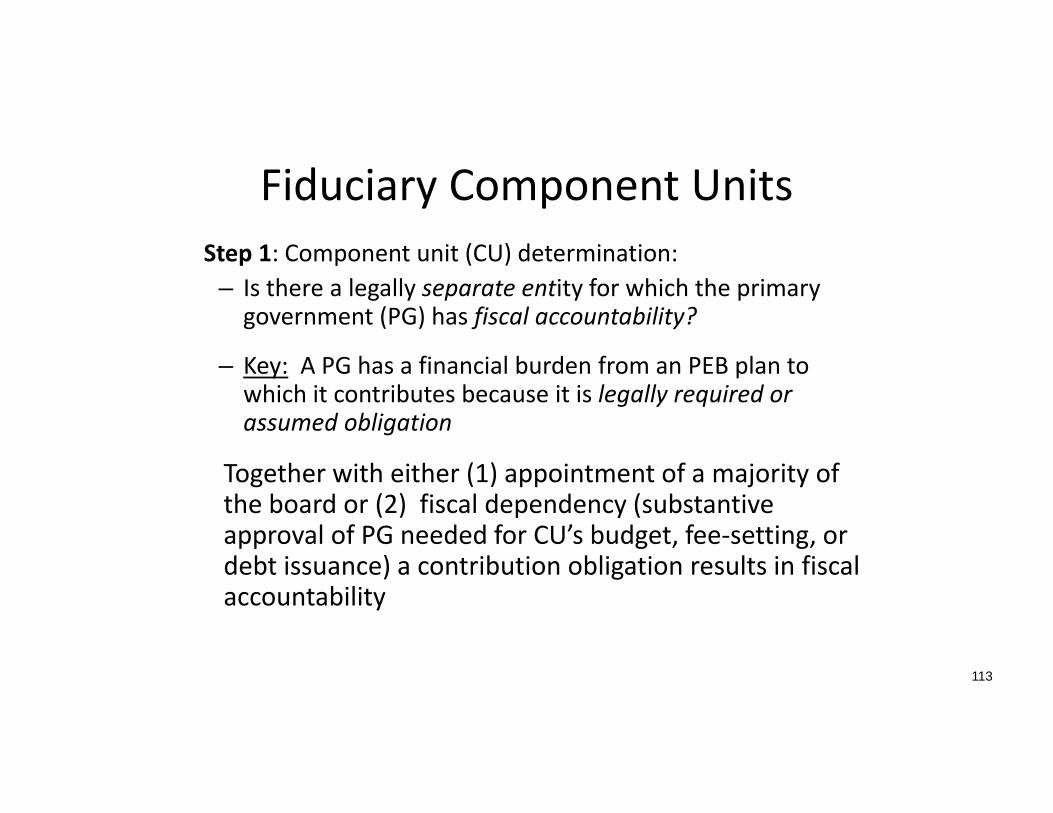

Fiduciary Component UnitsStep 1: Component unit (CU) determination:

– Is there a legally separate entity for which the primary government (PG) has fiscal accountability?

– Key: A PG has a financial burden from an PEB plan to which it contributes because it is legally required or assumed obligation

Together with either (1) appointment of a majority of the board or (2) fiscal dependency (substantive approval of PG needed for CU’s budget, fee‐setting, or debt issuance) a contribution obligation results in fiscal accountability

113

Fiduciary CUs ‐ PEBStep 2: for pension and OPEB CUsIs it a fiduciary CU? Yes, if it is:– A pension or OPEB plan administered through a

trust or = arrangement that meets the provisions of GASB 67 ¶ 3 for pensions or GASB 74 ¶ 3 for OPEB, (“GASB Trust”) or

– Pension or OPEB assets not held in a trust that meets the criteria, and the assets are contributed by entities not part of the PG’s reporting entity.

114

Fiduciary CUs – Non‐PEB

Step 2: for CUs that are not pension or OPEB

Is it a fiduciary CU? Yes, if the activity’s assets meet one or more of the following 3 criteria: 1. Assets are administered through a trust, and:

• The government is not a beneficiary, • Assets are dedicated to providing benefits to recipients in accordance with

benefit terms, and • Assets are legally protected from government’s creditors; or

115

Fiduciary CUs – Non‐PEB (cont.)

Step 2 continued

2. Assets are not in a trust, but are:• Held for the benefit of individuals, • Not from the government’s provision of goods or services to those individuals,

and • The government does not have either administrative involvement with or

direct financial interest in the assets; or

116

Fiduciary CUs – Non‐PEB (cont)

Step 2 continued

3. Assets are not in a trust, but are:• Held for the benefit of organizations or other governments that are not part of

the government’s reporting entity, and• Not from the government’s provision of goods or services to those

organizations or other governments.

117

Administrative and Direct Financial Involvement

• A government has administrative involvement with assets if it:– Monitors compliance by subrecipients with program requirements,

– Determines eligibility, even if using grantor established criteria, or

– Can exercise discretion in allocation of funds.

• A government has direct financial involvement if, for example, it finances some program costs in accordance with matching requirements

118

Non‐CU Fiduciary Activities ‐Control of assetsStep 1: Does the government control the assets?

A government has control of assets if it:– Holds the assets, or – Has the ability to direct the use, exchange, or employment of the assets.

119

Control of Assets (cont.)–Use – expends or consumes an asset for benefit of specific individuals, organizations, or other governments

–Direct – designate a third party to perform a government’s fiduciary duties without assuming them

–Note: Control determination is unaffected by restrictions on use

120

Pension and OPEB ‐ Not CUsStep 2: for PEB plans:

Report as a fiduciary activity if it is:– A pension or OPEB plan administered through a

trust that meets the provisions of GASB 67 ¶ 3 for pensions or GASB 74 ¶ 3 for OPEB, or

– Pension or OPEB assets not held in a trust that meets the criteria, and the assets are contributed by entities not part of the PG’s reporting entity.

121

Non‐PEB Fiduciary Activities – Not CUs

Step 2: for fiduciary activities other than PEB plans:

Activities are fiduciary if meet both of these criteria:1. The assets are not derived from either:

• The government’s own‐source revenue, or• Government‐mandated nonexchange or voluntary

nonexchange transactions*, and

* Except if assets are derived from pass‐through grants for which the government does not have administrative or direct financial involvement.

122

Non‐PEB Fiduciary Activities – Not CUs

Step 2, continued

2. Assets are (one of the following):• In a trust of which the government is not a

beneficiary, dedicated to provide benefits per trust terms, and legally protected from the government’s creditors [GASB 84 ¶ 11(c)1], or

• For the benefit individuals but not derived from providing goods or services to those individuals, and the government has no administrative or direct financial involvement.

123

Fiduciary Fund Types• Four types of fiduciary funds

– Pension (and other employee benefit) trust funds– Investment trust funds– Private purpose trust funds– Agency Custodial funds

• Agency funds are replaced with custodial funds in GASB 84

• Custodial funds report assets not held in a trust.

124

Fiduciary Fund Types –Trusts (continued)

Pension (and other employee benefit) trust funds Pension and OPEB trusted plans Other employee benefit plans Trust complies with paragraph 11c(1) Contributions and earnings are irrevocable

Investment trust funds External portion of investment pools and individual

investment accounts Trust complies with paragraph 11c(1)

Private‐purpose trust funds All other trust activities Trust complies with paragraph 11c(1)

125

Liability Recognition• PEB – follow Pension and OPEB liability recognition standards

• Investment and private purpose trust funds and custodial funds – recognize when compelled to disburse resources:– Demand for the resources has been made, or– No further action or condition is required to be met to be entitled to receive the resources

• For example, tax collections on behalf of other governments

126

Reporting Requirements

• PEB ‐ follow Pension and OPEB reporting standards• Investment and private purpose trust funds and custodial funds – follow reporting requirements in GASB 84– Note: custodial funds now required to report a statement of changes in fiduciary net position

127

Custodial Funds Option• If resources held for three months or less

– Option to report single aggregated totals in custodial fund

• Additions • Deductions

– Example – County collects and remits property taxes to other taxing bodies

• Addition – Property taxes collected for other governments• Deduction – Property taxes remitted to other governments

128

Effective Date

• Periods beginning after December 15, 2019• Restate prior periods if practical, or report a restatement of beginning net position/fund balance

• GASB implementation guide under development now Scheduled release 2nd Quarter 2019 (ED 4th Quarter 2018)

129

‘Do Now’s

1. Review all current fiduciary funds 2. Identify where non‐fiduciary activities belong3. Determine impact on budget(s)4. Educate governing boards, others

130

GASB Statement No. 85Omnibus 2017

Issued March 2017Effective Date: Periods beginning after June 15, 2017

Topics• Addresses six topics:1. Blending component units (BTA reporting)2. Goodwill and negative goodwill3. Fair value measurement and application4. Employer accounting and reporting for pensions5. Employer accounting and reporting for OPEB 6. Reporting by OPEB plans

132

Topics 1 & 2 –Blending CUs and Goodwill

• BTAs may only blend component units (CUs) that satisfy criteria to be blended.

• Goodwill should be eliminated by:– Reclassifying positive amounts as deferred outflows, and – Adjusting net position for negative amounts.

133

Topic 3 – Fair Value Measurement & Application

• Real estate holdings of insurance entities should be reported as capital assets unless they meet definition of investments in GASB Cod. I50 Investments, paragraph 535.

• Use of amortized cost rather than fair value to report money‐market investments and interest‐earning investment contracts is an option not a requirement.

134

Topics 4 & 5 – Postemployment Benefits –Governmental Funds

• Measurement of Pension/OPEB in governmental funds– Liabilities to employees – measured as of the end of the reporting period

–Expenditures by defined benefit plans for the reporting period include:• Amounts payable to Pension/OPEB plan• Employer incurred costs of administering defined benefit plans not administered through a trust

135

Topics 4 & 5 – PEB – Governmental Funds (cont.)

• Treatment of on‐behalf PEB benefits payments in governmental funds– Employer should recognize expenditures for:

• Contributions to PEB plans, and benefit payments, made on the employer’s behalf by nonemployer contributing entities during the period, adjusted for

• Changes to the nonemployer contributing entities’ payables for the above (to the extent the payables would normally be liquidated with current resources).

136

Topics 5 & 6 – OPEB – Payroll Related Measures in RSI

• Payroll‐Related Measures in RSI – In OPEB Plan Statements (single employer or cost‐sharing plans):• Contributions to OPEB Plan based on pay – covered payroll• Contributions to OPEB Plan not based on pay – no payroll measure disclosed

– In Employer Statements:• Trust used

– Contributions to OPEB Plan based on pay – covered payroll– Contributions to OPEB Plan not based on pay – covered‐employee

payroll

• Trust not used ‐ covered‐employee payroll137

Topic 5 – OPEB – Employer‐Paid Member Contributions

• OPEB Plan should record as employeecontributions

• Employer should record as salaries, wages, or fringe benefits, not pension contributions

138

Topic 5 – OPEB –Alternative Measurement Method

• Increase in the number of simplified assumptions permitted– Expected point in time when employees will exit from active service

• Single assumed age or a single # of years worked– Employee turnover – probability of attaining length of service for eligibility for OPEB

• Expense in current period– Changes in proportion of collective TOL and NOL– Changes in proportion benefits paid by employer (v. nonemployer contributing entity)

139

Topic 5 – OPEB – Provided Through Private‐sector Plans

Same approach as for pension plans (GASB 78 Cod. P20.112) participating in cost‐sharing private‐sector plans• Recognition

– Expense – Required contributions for the reporting period– Liability – unpaid required contributions at end of reporting period

• Note disclosures (lots)• RSI – 10 year schedule of employer’s required contributions to each OPEB plan

140

GASB Statement No. 86Certain Debt Extinguishment Issues

Issued May 2017Effective Date: Periods beginning after June 15, 2017

Debt Extinguishment Using Only Existing Resources

New standard:1. Aligns accounting and reporting for debt defeasances using existing

resources with that for refunding,2. Changes accounting for prepaid insurance on defeased debt, and3. Requires disclosures related to risk of substitution of monetary

assets in defeasance escrow.

142

In‐substance Defeasance Cash and other monetary assets on hand ‐ notproceeds of refunding debt ‐ are deposited with an escrow agent in a trust– Deposit into trust is irrevocable– Use of trust assets is limited to principal & interest payments of defeased debt

– Trust assets are only monetary assets that are essentially risk‐free as to the amount, timing and collection of interest and principal

143

In‐substance Defeasance (cont.)Risk free as to ‐• Amount

– Fixed amounts denominated in same currency as the defeased debt is payable

• Timing– Principal and interest receipts from assets matched with those of defeased debt

• Callable securities do not qualify• Collection

– No credit risk• Only US treasury and treasury backed securities

144

Recognition Economic Resources:

+ =

– Reacquisition Price – Amount placed in escrow that, together with interest earnings, will be sufficient to pay the defeased debt.

– Net Carrying Value – Amount due at maturity +/‐ unamortized discount or premium, *prepaid insurance [new], and deferred inflows and outflows.

– Gain or Loss – Recognize, and report separately, in the period of the defeasance.

Current Resources: Escrow deposit is a debt service expenditure. 145

Reacquisition Price

Net Carrying Value*

(Defeased Debt)Gain or Loss

Note Disclosure• Period of defeasance

– General description of the transaction, such as:• Amount of debt extinguished• Amount placed in trust • Reasons for defeasance • Cash flows required to service the defeased debt

– New: Disclose if the substitution of essentially risk‐free monetary assets with monetary assets that are not essentially risk free is not prohibited

146

Note Disclosure (continued)• Subsequent periods

– Amount of in‐substance defeased debt that remains outstanding

– New: Disclose the amount of the above, if any, for which substitution of essentially risk free assets with assets that are not essentially risk free is notprohibited.

147

www.gfoa.org • #GFOA2018

112th Annual ConferenceMay 6-9, 2018 • St. Louis, Missouri

Questions:Speakers will take questions and comments. This session is being recorded, please utilize the microphone in the aisle to ask all questions.

Provide Feedback:Please take a few minutes to provide your feedback at www.gfoa.org/conf-eval

Discuss/Comment: Join the discussion at #GFOA2018

Speaker Contact Information:

R. Kinney Poynter, CPAEmail: [email protected]: 859-276-1147

David A. VaudtEmail: [email protected]: 203-956-5259

Michele Mark LevineEmail: [email protected]: 312-977-9700 Contact GFOA:

To contact GFOA about session topics please email [email protected]