Embed Size (px)

Citation preview

AccountancyModule 1

Samitesh Brahma

Department of Humanities

Jorhat Engineering College

Module 1

✓ Concept and classification of accounts

✓ Double entry system of book keeping

✓ Golden rules of Debit and Credit

✓ Journal- Definition, advantages, Procedure of journalizing

✓ Ledger- Advantages, rules regarding posting, balancing of ledger accounts

✓ Trial Balance- Definition, objectives, procedure of preparation.

Meaning of Accounting

The American Institute of Certified Public Accountants defines

accounting as “the art of recording, classifying and summarizing in a

significant manner and in terms of money, transactions and events,

which are, in part atleast, of a financial character, and interpreting and

the results thereof. ”

Characteristics

1. Accounting is an art as well as science.

2. Recording of financial transactions only.

3. Classifying.

4. Summarizing.

5. Interpretation of results.

6. Communicating

NOTE: Recording, classifying and summarizing are termed as “Process of accounting” or “accounting cycle”

Objectives

1. To keep systematic record of business transaction

2. To calculate profit or loss

3. To know the exact reasons leading to net profit or net loss

4. To ascertain the financial position of business

5. To ascertain the operational performance.

6. To provide information to various parties

Functions

1. Maintaining complete and systematic records.

2. Communicating the financial results to various parties.

3. Protecting the assets of business.

4. Providing assistance to management

5. Compliance of legal needs.

Accounting CycleTransaction

Journal Entries

Posting in Ledger

Trail Balance

worksheet

Adjusting journal entries

Financial statements

Closing the books

The accounting cycle is a

collective process of

identifying, analyzing, and

recording the accounting

events of a company. It is a

standard 8-step process that

begins when a transaction

occurs and ends with its

inclusion in the financial

statements.

Figure: Accounting Cycle

Accounting Cycle1. Identify Transactions: An organization begins its accounting cycle with the identification of those transactions that

comprise a bookkeeping event. This could be a sale, refund, payment to a vendor, and so on.

2. Record Transactions in a Journal: Next come recording of transactions using journal entries. The entries are based on the

receipt of an invoice, recognition of a sale, or completion of other economic events.

3. Posting: Once a transaction is recorded as a journal entry, it should post to an account in the general ledger. The general

ledger provides a breakdown of all accounting activities by account.

4. Unadjusted Trial Balance: After the company posts journal entries to individual general ledger accounts, an unadjusted

trial balance is prepared. The trial balance ensures that total debits equal the total credits in the financial records.

5. Worksheet: Analyzing a worksheet and identifying adjusting entries make up the fifth step in the cycle. A worksheet is

created and used to ensure that debits and credits are equal. If there are discrepancies then adjustments will need to be

made.

6. Adjusting Journal Entries: At the end of the period, adjusting entries are made. These are the result of corrections made

on the worksheet and the results from the passage of time. For example, an adjusting entry may accrue interest revenue that

has been earned based on the passage of time.

7. Financial Statements: Upon the posting of adjusting entries, a company prepares an adjusted trial balance followed by the

actual formalized financial statements.

8. Closing the Books: An entity finalizes temporary accounts, revenues, and expenses, at the end of the period using closing

entries. These closing entries include transferring net income into retained earnings. Finally, a company prepares the post-

closing trial balance to ensure debits and credits match and the cycle can begin anew.

Branches of accounting

1. Financial accounting

2. Cost accounting

3. Management accounting

Accounting and Accountancy

Basis of

Distinction

Accounting Accountancy

1. Meaning It is concerned with recording,

classification and summarizing of

transactions.

It is a body of knowledge prescribing

certain rules or principles to be

observed while recording,

classification and summarizing of

transactions.

2. Scope It is narrow in scope. It is wider in scope.

3. Relation It depends in book- keeping. It depends on both book-keeping and

accounting.

4. Function Its main function is to ascertain the net

results and the financial position of the

business and to communicate them to

interested parties.

It includes the decision-making

function on the basis of information

provided by book-keeping and

accounting.

Transaction

An event involving some value between two or more entities. It can be a purchase of

goods, receipt of money, payment to a creditor, incurring expenses, etc. It can be a

cash transaction or a credit transaction.

Account

➢In actual practice, the individual transactions of like nature

are recorded, added and subtracted at one place. Such place is

customarily termed as an ‘Account’.

➢An account is a Ledger record in a summarized form, of all

the transactions that have taken place with the particular

person or things specified.

➢All accounts are divided into two parts:

1. Left side of an account is called Debit side

2. Right side of an account is called Credit side

Classification of accounts

Classification on accounts

Personal Accounts Impersonal Accounts

Real Accounts Nominal Accounts

Classification of accounts

✓ Personal accounts – the accounts which relate to an individual, firm, company or

an institution.

✓Example: Bank account, Capital Account, Drawings account, etc.

✓ Real accounts- the accounts of all those things whose value are measured in

terms of money and which are properties of the business (assets).

✓Example: Cash account, furniture account, goodwill account, etc.

✓ Nominal accounts- the accounts which includes the accounts of all expenses or

loss and incomes or gains.

✓Example: Salaries paid, rent paid, bad debts, etc.

Note: When any word (as a prefix or as a suffix ) is added to a nominal account, it becomes a personal account

Classification of Personal accounts

Personal Accounts

Natural personal accountsArtificial personal

accounts

Representative personal

accounts

Classification of personal accounts

1. Natural personal accounts – accounts of human beings.

Example: drawings account, debtors account, creditors account, Ram’s account.

2. Artificial personal accounts- accounts do not have physical existence as

human beings.

Example: any firm’s account, any institution’s account, etc.

3. Representative personal accounts- accounts represents a group of persons.

Example: salaries outstanding account, prepaid insurance account, etc.

Classification of Real accounts

Real Accounts

Tangible Real Accounts Intangible Real Accounts

Classification of Real accounts

1. Tangible real accounts – accounts of those things which can be

touched, felt, measured, purchased, sold, etc.

Example: Cash account, furniture account, land account, etc.

2. Intangible real accounts – accounts which cannot be touched, but

their value can be measured in terms of money.

Example : goodwill account, copyrights account, patents account, etc.

Golden rules of debit and credit

Types of account Golden rules

1. Personal account Debit - the receiver

Credit - the giver

2. Real account Debit - what comes in

Credit – what goes out

3. Nominal account Debit – the expenses or losses

Credit – the incomes or gains

Rules of Debit and Credit

Assets Liabilities

Increase Decrease Increase Decrease

Debit Credit Credit Debit

Expenses/Loses Capital

Increase Decrease Increase Decrease

Debit Credit Credit Debit

Revenue/Gain

Increase Decrease

Credit Debit

Double Entry system

Every business transaction has a two- fold effect and that it affects two

accounts in opposite directions and if a complete record were to be

made of each transaction, it would be necessary to debit one account

and credit another account. It is this recording of the two-fold effect of

every transaction that has given rise to the term double entry system.

Principles or characteristics of double entry system

1. Every business transaction affects two accounts

2. Recording of both personal and impersonal aspects.

3. Recording is made according to certain specified rules.

4. Preparation of trail balance

Stages of double Entry System

1. Original Record (Journal)

2. Classification (Ledger)

3. Summary ( Trial Balance)

Advantages of Double Entry System

1. Scientific system

2. Complete record of every transaction

3. Preparation of trail balance

4. Preparation of trading and P&L Account

5. Knowledge of financial position of the business

6. Legal approval

7. Helps management in decision making

Journal- Books of original entry

✓It is a book of original entry in which the transactions are recorded

first of all, as and when they take place.

✓Transactions are originally recorded in a chronological (day-to-day)

order.

✓Journal is sub-divided into a number of Sub-Journals known as special

purpose subsidiary books.

✓The subsidiary books may be

1. Cash Book 5. Sales Return Book

2. Purchases Book 6. Bills Receivable Book

3. Sales Book 7. Bills Payable Book

4. Purchases Return Book 8. Journal Paper

Features or characteristics of a journal

i. Journal is a book in which the transactions are recorded for the first

time, as and when they take place.

ii. A journal is only a book of primary entry.

iii. A journal is a daily accounting record.

iv. It maintains the identity of each transactions and provides a

complete picture of the same in one entry.

v. Each entry in the journal is followed by a brief explanation of the

transaction which is called ‘Narration’.

vi. In journal, transactions are recorded in a chronological order.

Functions of a journal

i. To keep a chorological record of all transactions.

ii. To analyze each transactions into debit and credit aspects by using

double entry system of book keeping.

iii. To provide a basis for posting into ledger.

iv. To maintain the identity of each transaction by keeping a complete

record of each transaction qt one place on a permanent basis.

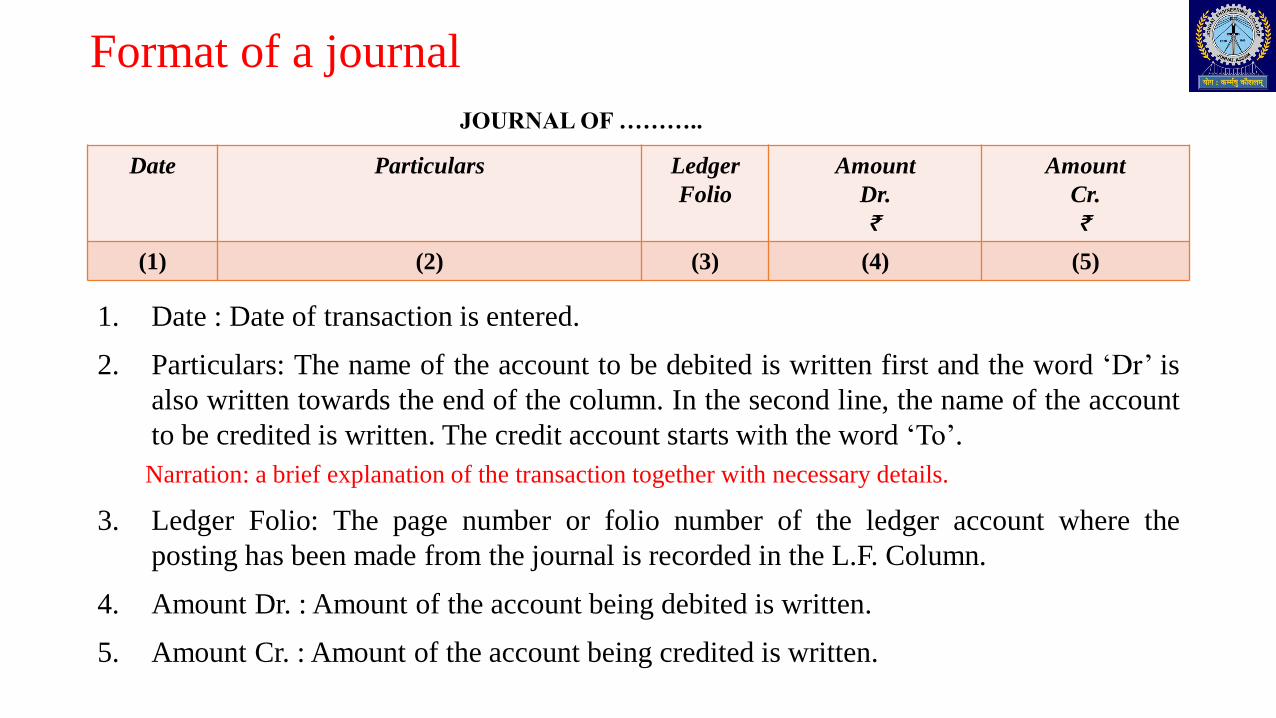

Format of a journal

Date Particulars Ledger

Folio

Amount

Dr.

₹

Amount

Cr.

₹

(1) (2) (3) (4) (5)

1. Date : Date of transaction is entered.

2. Particulars: The name of the account to be debited is written first and the word ‘Dr’ is

also written towards the end of the column. In the second line, the name of the account

to be credited is written. The credit account starts with the word ‘To’.

Narration: a brief explanation of the transaction together with necessary details.

3. Ledger Folio: The page number or folio number of the ledger account where the

posting has been made from the journal is recorded in the L.F. Column.

4. Amount Dr. : Amount of the account being debited is written.

5. Amount Cr. : Amount of the account being credited is written.

JOURNAL OF ………..

Rules of Journalising

1. Personal accounts

E.g.,

a. paid ₹20,000/- to Mr. ABC

b. Received ₹ 50,000/- from Mr. XYZ

Particulars Amount

Dr.

Credit

Cr.

Mr. ABC Dr 20,000

To Cash A/c

(Cash paid to Mr. ABC)

20,000

Particulars Amount

Dr.

Credit

Cr.

Cash A/c Dr 50,000

To Mr. XYZ

(Cash received from Mr. XYZ)

50,000

Narration

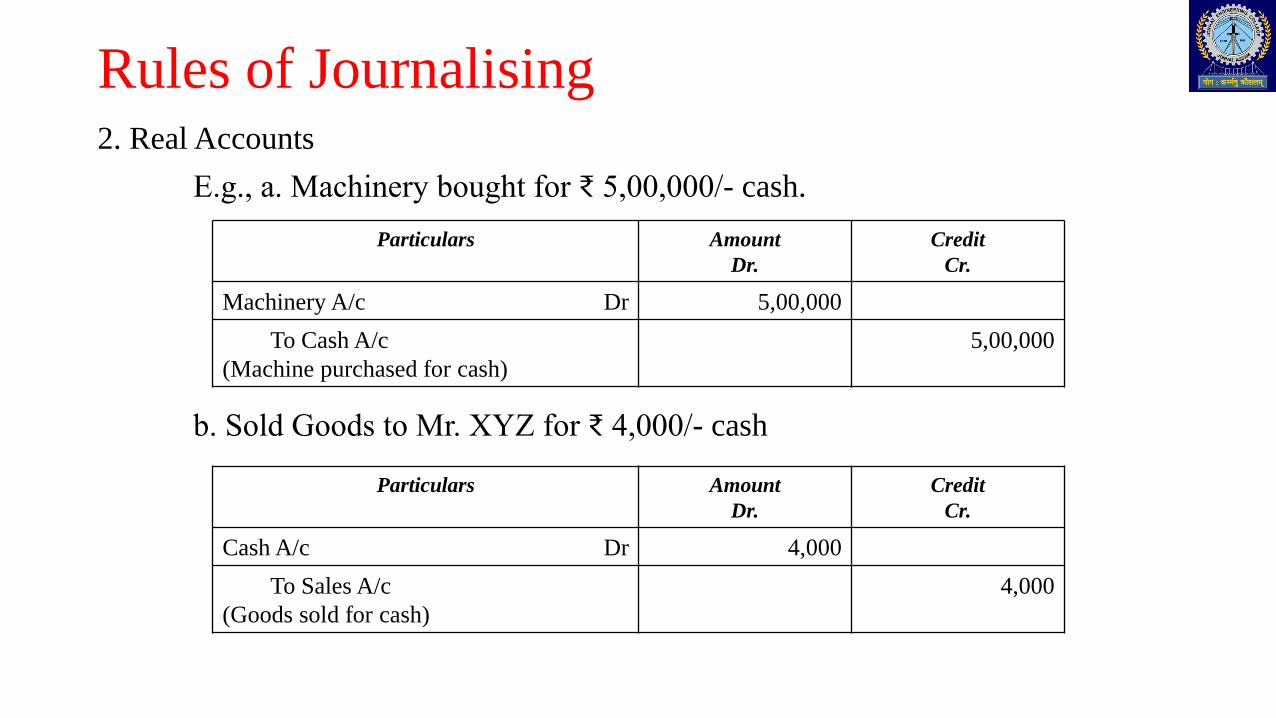

Rules of Journalising2. Real Accounts

E.g., a. Machinery bought for ₹ 5,00,000/- cash.

b. Sold Goods to Mr. XYZ for ₹ 4,000/- cash

Particulars Amount

Dr.

Credit

Cr.

Machinery A/c Dr 5,00,000

To Cash A/c

(Machine purchased for cash)

5,00,000

Particulars Amount

Dr.

Credit

Cr.

Cash A/c Dr 4,000

To Sales A/c

(Goods sold for cash)

4,000

Rules of Journalising

3. Nominal Accounts

E.g., a. ₹ 20,000/- paid for salary

b. ₹ 3000/- received for commission

Particulars Amount

Dr.

Credit

Cr.

Salary A/c Dr 20,000

To Cash A/c

(Salary paid)

20,000

Particulars Amount

Dr.

Credit

Cr.

Cash A/c Dr 3,000

To Commission A/c

(Commission received)

3,000

Important considerations1. If, in the transaction relating to purchase or sale of goods, the name

of the purchaser or seller is not given, it is considered as a cash

transaction.

Example: ‘Goods sold for ₹ 50,000.’

2. If, in the transaction relating to purchase or sale of goods, the name

of the purchaser or seller is given along with cash, it is considered as

a cash transaction.

Example: ‘Goods sold to XYZ for cash.’

3. If, in the transaction relating to purchase or sale of goods, the name

of the purchaser or seller is given and it is not stated whether it is a

cash or credit transaction, it is considered to be a credit transaction.

Example: ‘Goods sold to ABC’

Illustration 1

2021 Amount (₹)

Feb. 1 M/s XYZ Stores started business with cash 50,000

3 Purchased goods for cash 20,000

5 Purchased goods from Mr. A for cash 12,000

8 Purchased goods from Mr. B 8,000

10 Sold goods for cash 5,000

11 Sold goods to Mrs. C for cash 10,000

13 Sold goods to Mr. D 7,000

20 Withdrew cash from office for personal use 2,000

27 Paid wages 1,500

28 Paid rent 6,500

28 Paid salary to Mr. Q 3,000

28 Received commission 4,000

Enter the following transactions in the Journal of M/s XYZ Stores.

Illustration 1

Solution

Date Particulars L.F. Amount

Dr.

₹

Amount

Cr.

₹

Feb 1’21 Cash A/c Dr. 50,000

To Capital A/c 50,000

(Being Cash brought into the business by M/s XYZ Stores as capital)

Feb 3’21 Purchase A/c Dr. 20,000

To Cash A/c 20,000

(Being Goods purchased for cash)

Feb 5’21 Purchase A/c Dr. 12,000

To Cash A/c 12,000

(Being Goods purchased for cash)

Total c/f 82,000 82,000

Journal of M/s XYZ Stores

Illustration 1

Solution

Date Particulars L.

F.

Amount

Dr.

₹

Amount

Cr.

₹

Total b/f 82,000 82,000

Feb 8’21 Purchase A/c Dr. 8,000

To Mr. B 8,000

( Being Goods purchased from Mr. B on credit )

Feb 10’21 Cash A/c Dr. 5,000

To Sales A/c 5,000

(Being Sold goods for cash)

Feb 11’21 Cash A/c Dr. 10,000

To Sales A/c 10,000

(Being Sold goods for cash)

Total c/f 1,05,000 1,05,000

Journal of M/s XYZ Stores

Illustration 1

Solution

Date Particulars L.F

.

Amount

Dr.

₹

Amount

Cr.

₹

Total b/f 1,05,000 1,05,000

Feb 13’21 Mr. D Dr. 7,000

To Sales A/c 7,000

( Being Goods sold to Mr. D on credit )

Feb 20’21 Drawings A/c Dr. 2,000

To Cash A/c 2,000

( Being the Amount withdrawn for personal use)

Feb 27’21 Wages A/c Dr. 1,500

To Cash A/c 1,500

(Being the Wages Paid)

Total c/f 1,15,500 1,15,500

Journal of M/s XYZ Stores

Illustration 1

Solution

Date Particulars L.F. Amount

Dr.

₹

Amount

Cr.

₹

Total b/f 1,15,500 1,15,500

Feb 28’21 Rent A/c Dr. 6,500

To Cash A/c 6,500

( Being the Paid Rent)

Feb 28’21 Salary A/c Dr. 3,000

To Cash A/c 3,000

(Being The Salary Paid)

Feb 28’21 Cash A/c Dr. 4,000

To Commission Received A/c 4,000

(Being Commission received)

Total ₹ 1,29,000 1,29,000

Journal of M/s XYZ Stores

Ledger

✓According to L.C. Cropper, “The book which contains a classified and

permanent record of all the transactions of a business is called the Ledger.”

✓A ledger in accounting refers to a book that contains different accounts

where records of transactions pertaining to a specific account is stored.

✓It is also known as the book of final entry or principal book.

Distinction between ‘Books of Original Entry’ and ‘Ledger’

Journal or Books of Original Entry Ledger

1 Transactions are entered in a chorological

order, as and when they take place

Transactions are recorded in analytical order, i.e.,

all the transactions pertaining to a particular

account are contained at one place in the Ledger.

2 Full details of a transaction are narration are

recorded in these books.

Full details of a transactions are not recorded in

the ledger.

3 Final Accounts cannot be prepared with the

help of books of original entry.

Final accounts can be prepared with the help of

Ledger balances.

4 The process of recording entries in the books

of original entry is called ‘journalizing’

The process of recording entries in the ledger is

called ‘posting’.

5 Page number of the ledger, i.e., Ledger Folio

(L.F.) is written in these books.

Page number of the Journal or subsidiary books,

i.e., Journal Folio (J.F) is written in Ledger

6 Accuracy of these books cannot be tested. Accuracy of the ledger accounts is tested by

preparing a trail Balance

Format of ledger

Dr. Name of Account Cr.

Date Particulars J.F. Amount

₹

Date Particulars J.F. Amount

₹

1 2 3 4 1 2 3 4

As, shown above, there are four columns on each side of an account-

1. Date:- The date of the transaction is recorded in this column.

2. Particulars:- Each transaction affects two accounts. The name of the other account which is

affected by the transactions is written in this column.

3. Journal Folio or J.F. :- in this column, the page number of the Journal or subsidiary book from

which that particular entry is transferred, is entered.

4. Amount :- the amount pertaining to this account is entered in this column.

Rules of posting

1. All transactions relating to an account should be entered at one

place. In other words, two separate accounts should not be opened

for posting transaction relating to the same account.

2. The word ‘To’ is used before the accounts which appear on the debit

side of an account. Similarly, the word ‘By’ is used before the

accounts which appear on the credit side of an account.

3. If an account has been debited in the journal entry, the posting in the

ledger should also be made on the debit side of such account.

4. If an account has been credited in the journal entry, the posting in

the ledger should also be made on the credit side of such account.

Example : On 1st Jan 2021, sold goods for cash ₹ 10,000. Pass journal entry and post it into ledger.

Solution:

Journal entry:

Ledger account:

Date Particulars Amount ₹

Dr.

Credit ₹

Cr.

1/01/21 Cash A/c Dr 10,000

To Sales A/c

(Being Goods sold for cash)

10,000

Dr. Cash Account Cr.

Date Particulars J.F. Amount

₹

Date Particulars J.F. Amount

₹

1/01/21 To Sales A/c 10,000

Dr. Sales Account Cr.

Date Particulars J.F. Amount

₹

Date Particulars J.F. Amount

₹

1/01/21 By Cash A/c 10,000

Closing and balancing of accounts

1. Closing of Personal Accounts

If a personal account shows a debit balance, it indicates the amountowing from him. (↓)

If a personal account shows a credit balance, it indicates the amountowing to him. (↑)

The words ‘By balance c/d’ i.e., balance carried down are writtenagainst the amount of the difference. In the next accounting period, thebalance is brought down on the other side by witting the words ‘To balanceb/d’.

2. Closing of Real Accounts

Same as personal accounts.

3. Closing of Nominal Accounts

These accounts does not require balancing, as the main purpose ofopening nominal account is to ascertain the net profit or loss of the firm.

Trial Balance

➢Trial balance is the list of debit and credit balances, taken out from ledger. Italso includes the balances of cash and bank taken out from the cash book.

➢The statement prepared with the help of ledger balances, at the end offinancial year (or at any other date) to find out whether debit total agreeswith credit total is called Trail balance.

➢Account which shows no balance, i.e., whose debit and credit totals areequal, is not entered in the trail balance.

➢If the total of debit side of trial balance equals to that of credit side, it isproved that books are at least arithmetically correct and there are no errorsin the posting and balancing the ledger accounts.

Format

Trail Balance

As at ……..

Name of Accounts L.F. Balance Dr.

(₹)

Balance Cr.

(₹)

Points for preparing a Trail Balance: -

1. All Assets have debit balances. Their Balances should be shown on the debit

side of trail balance.

2. All liabilities have credit balances. Their balances should be shown on the credit

side of trail balance.

3. Capital account shows a credit balance.

4. Drawings account shows a debit balance.

5. All expenses and losses show debit balances.

6. All incomes and profits show credit balances.

7. Purchases account always shows a debit balance.

8. Purchases return account always shows a credit balance.

9. Sales account always shows a credit balance.

10. Sales return account always shows a debit balance.

IllustrationPrepare a Trail Balance from the following balances of M/s Dutta as at 31st March 2021: -

Name of Accounts ₹ Name of Accounts ₹

Opening Stock 20,000 Discount (Cr) 710

Purchases 85,000 Furniture 6,000

Purchases Returns 5,000 Machinery 62,000

Sales 1,60,000 Debtors 36,000

Sales Return 6,200 Creditors 12,750

Rent 1,200 Bills Receivable 4,600

Salaries 5,700 Bill Payable 2,500

Advertisement 880 Cash In hand 11,220

Commission Received 1,440 Bank Overdraft 10,000

Capital 50,000 Loan 6,000

Drawings 7,800 Interest on Overdraft 1,800

SolutionTrail Balance

As at 31st March 2021

Name of Accounts L.F. Balance Dr. (₹) Balance Cr. (₹)

Opening Stock 20,000

Purchases 85,000

Purchases Returns 5,000

Sales 1,60,000

Sales Return 6,200

Rent 1,200

Salaries 5,700

Advertisement 880

Commission Received 1,440

Capital 50,000

Drawings 7,800

Discount (Cr) 710

Furniture 6,000

SolutionTrail Balance

As at 31st March 2021

Name of Accounts L.F. Balance Dr. (₹) Balance Cr. (₹)

Machinery 62,000

Debtors 36,000

Creditors 12,750

Bills Receivable 4,600

Bill Payable 2,500

Cash In hand 11,220

Bank Overdraft 10,000

Loan 6,000

Interest on Overdraft 1,800

Total 2,48,400 2,48,400

IllustrationPass journal entries for the following transactions and post them into ledger and prepare trial balance

2021 Amount (₹)

Jan 1 Ram & Shyam Constructions commenced business with cash 2,00,000

Jan 3 Purchased office furniture for cash 20,000

Jan 5 Purchased goods for cash 50,000

Jan 8 Purchased goods - from Vishal Trading Co. 25,000

from Mohan Steels 16,000

Jan 10 Returned goods to Vishal Trading Co. 5,000

Jan 14 Paid cash to Vishal Trading Co. in full settlement of their account, after deducting

5% cash discount

Jan 15 Sold goods for cash 40,000

Jan 18 Sold goods to Hero Limited, less 10% Trade discount 30,000

Jan 20 Ram & Shyam Constructions withdrew from business for personal use - Cash 10,000

Goods 4,000

Jan 21 Paid to Mohan Steels 7,800

Discount received 200

Jan 22 Received from Hero Limited 8,850

Discount allowed 150

Jan 25 Sold Goods to Hanjraj Ltd. For cash 12,000

Jan 28 Purchased goods from Pawan Brothers 24,000

Jan 31 Paid for Rent ₹ 2,000 and Salaries ₹4,000

Solution:

Journal of Ram & Shyam Constructions

Date Particulars L.F. Amount (Dr)

₹

Amount (Cr)

₹

Jan 1

2021

Cash A/c

To Capital A/c

(Stated business with cash)

Dr. 2,00,000

2,00,000

Jan 3 Furniture A/c

To Cash A/c

(purchased furniture for cash)

Dr. 20,000

20,000

Jan 5 Purchases A/c

To Cash A/c

(Purchased goods for cash)

Dr. 50,000

50,000

Jan 8 Purchases A/c

To Vishal Trading Co.

To Mohan Steels

(Goods purchased on credit)

Dr. 41,000

25,000

16,000

C/F 3,11,000 3,11,000

Journal of Ram & Shyam Constructions

Date Particulars L.F. Amount (Dr)

₹

Amount (Cr)

₹

B/F 3,11,000 3,11,000

Jan 10 Vishal Trading Co.

To Purchases Return A/c

(Goods returned )

Dr. 5,000

5,000

Jan 14 Vishal Trading Co.

To Cash A/c

To Discount Received A/c

(Cash paid and 5% discount received)

Dr. 20,000

19,000

1,000

Jan 15 Cash A/c

To Sales A/c

(Sold goods for cash)

Dr. 40,000

40,000

Jan 18 Hero Limited

To Sales A/c

(10% discount on goods bought)

Dr. 27,000

27,000

C/F 4,03,000 4,03,000

Journal of Ram & Shyam Constructions

Date Particulars L.F. Amount (Dr)

₹

Amount (Cr)

₹

B/F 4,03,000 4,03,000

Jan 20 Drawings A/c

To Cash A/c

To Purchases A/c

(Cash and Goods withdrew by owners )

Dr. 14,000

10,000

4,000

Jan 21 Mohan Steels

To Cash A/c

To Discount Received A/c

(Cash paid and 5% discount received)

Dr. 8,000

7,800

200

Jan 22 Cash A/c

Discount allowed A/c

To Hero Limited

(Cash received and discount allowed)

Dr.

Dr.

8,850

150

9,000

Jan 25 Cash A/c

To Sales A/c

(Sold goods for Cash)

Dr. 12,000

12,000

C/F 4,46,000 4,46,000

Journal of Ram & Shyam Constructions

Date Particulars L.F. Amount (Dr)

₹

Amount (Cr)

₹

B/F 4,46,000 4,46,000

Jan 28 Purchases A/c

To Pawan brothers

(Bought goods on credit )

Dr. 24,000

24,000

Jan 31 Rent A/c

Salaries A/c

To Cash A/c

(Expenses paid in cash)

Dr. 2,000

4,000

6,000

Total 4,76,000 4,76,000

Ledger of Ram & Shyam Constructions

Dr. Cash Account Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 1 2021 To Capital A/c 2,00,000 Jan 3

2021

By furniture A/c 20,000

Jan 15 2021 To Sales A/c 40,000 Jan 5

2021

By Purchases A/c 50,000

Jan 22 2021 To Hero Limited 8,850 Jan 14

2021

By Vishal Trading Co. 19,000

Jan 25 2021 To Sales A/c 12,000 Jan 20

2021

By Drawing A/c 10,000

Jan 21

2021

By Mohan Steels 7,800

Jan 31

2021

By Rent A/c 2,000

Jan 31

2021

By Salaries A/c 4,000

Jan 31

2021

By balance C/d 1,48,050

2,60,850 2,60,850

Feb 1 2021 To Balance b/d 1,48,050

Dr. Capital Account Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 31 2021 To balance c/d 2,00,000 Jan 1 2021 By Cash A/c 2,00,000

Feb 1 2021 By balance b/d 2,00,000

Dr. Furniture Account Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 3 2021 To Cash A/c 20,000 Jan 31 2021 By balance c/d 20,000

Feb 1 2021 To Balance b/d 20,000

Dr. Purchases Account Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 5 2021 To Cash A/c 50,000 Jan 20 2021 By Drawings A/c 4,000

Jan 8 2021 To Vishal Trading Co. 25,000

Jan 8 2021 To Mohan Steels 16,000

Jan 28 2021 To Pawan Brothers 24,000

1,15,000

Dr. Vishal Trading Co. Cr.

Date Particulars J.F. Amount

(₹)

Date Particulars J.F. Amount (₹)

Jan 10 2021 To Purchases Return A/c 5,000 Jan 8 2021 By Purchases A/c 25,000

Jan 14 2021 To Cash A/c 19,000

Jan 14 2021 To Discount Received

A/c

1,000

25,000 25,000

Dr. Mohan Steels Cr.

Date Particulars J.F. Amount

(₹)

Date Particulars J.F. Amount (₹)

Jan 14 2021 To Cash A/c 7,800 Jan 8 2021 By Purchases A/c 16,000

Jan 14 2021 To Discount Received

A/c

200

Jan 31 2021 To balance c/d 8,000

16,000 16,000

Feb 1 2021 By balance b/d 8,000

Dr. Purchase Return Account Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 10 2021 By Vishal Trading Co. 5,000

Dr. Discount Received Account Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 14 2021 By Vishal Trading Co. 1,000

Jan 21 2021 By Mohan Steel 200

Dr. Sales Account Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 15 2021 By Cash A/c 40,000

Jan 18 2021 By Hero Limited 27,000

Jan 25 2021 By Cash A/c 12,000

Dr. Hero Limited Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 18 2021 To Sales A/c 27,000 Jan 22 2021 By Cash A/c 8,500

Jan 22 2021 By Discount Allowed A/c 150

Jan 31 2021 By balance c/d 18,000

27,000 27,000

Feb 1 2021 To balance b/d 18,000

Dr. Drawings account Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 20 2021 To Cash A/c 10,000 Jan 31 2021 By balance c/d 14,000

Jan 20 2021 To Purchases A/c 4,000

14,000 14,000

Feb 1 2021 To balance b/d 14,000

Dr. Discount Allowed Account Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 22 2021 To Hero Limited 150

Dr. Pawan Brothers Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 31 2021 By balance c/d 24,000 Jan 28 2021 By Purchases A/c 24,000

Feb 1 2021 By balance b/d 24,000

Dr. Salaries Account Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 31 2021 To Cash A/c 4,000

Dr. Rent Account Cr.

Date Particulars J.F. Amount (₹) Date Particulars J.F. Amount (₹)

Jan 31 2021 To Cash A/c 2,000

TRIAL BALANCE OF RAM & SHYAM CONSTRUCTIONS

As on 31st Jam 2021

Name of Accounts L.F. Dr. Balances (₹) Cr. Balances (₹)

Capital A/c 2,00,000

Mohan Steels 8,000

Hero Limited 18,000

Drawings A/c 14,000

Pawan Brothers 24,000

Cash A/c 1,48,050

Furniture A/c 20,000

Purchases A/c 1,11,000

Purchases return A/c 5,000

Sales A/c 79,000

Discount received A/c 1,200

Discount allowed A/c 150

Rent A/c 2,000

Salaries A/c 4,000

Total 3,17,200 3,17,200