Embed Size (px)

Citation preview

ACC7017 Accounting Decision Making

Management Control System

Week 8: 27 November 2021

Learning Objectives:

At the end of this session, students will be able to:

• Understand the purpose of management control system and issues in decision-making process

• Understand cash budget and budgetary system

• Understand the how budget is used as performance evaluation tool

• Understand the relevant costing or differential costing, and short-run alternative choice decisions

Management Control System

• Management accounting: provide information to management to assist in formulating & implementing strategy

• Management control activities: prepare budgets & evaluate performance

• Accounting function plays an important role in strategy formulation & implementation through • capital budgeting• operational budgeting

• sales budgeting• production budgeting

• cash budgeting• performance evaluation

Why Cash Budget is Important?What role does it plays?

Capital Budgeting (For information only)

• process of identifying, evaluating & selecting projects that require commitments of large sums of funds & generate benefits into future

• 3 steps:• Project identification & definition• Evaluation & selection• Monitoring & review

• Techniques: • Payback period• Return on investment• Net present value• Internal rate of return

• Forecasting future cash flows to be generated from investment taking into consideration of discount rate for determining present value

• Risks: political, economic & financial

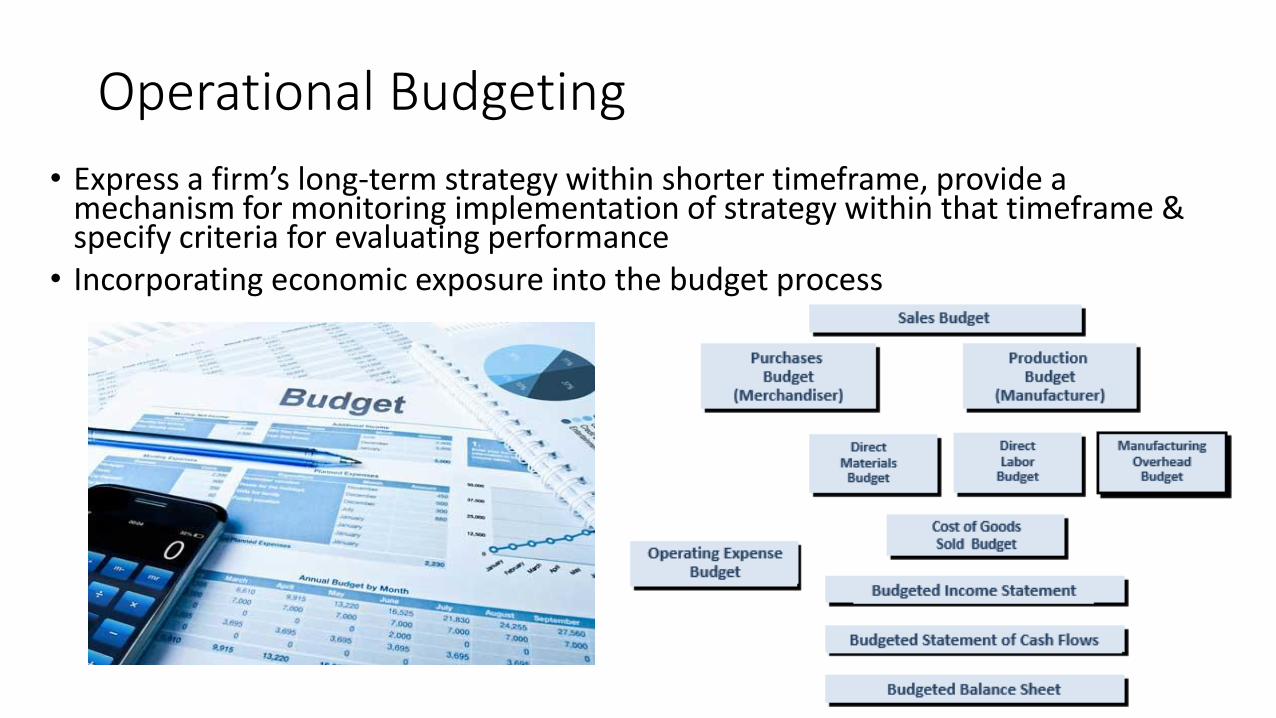

Operational Budgeting

• Express a firm’s long-term strategy within shorter timeframe, provide a mechanism for monitoring implementation of strategy within that timeframe & specify criteria for evaluating performance

• Incorporating economic exposure into the budget process

Cash Budget

• Useful to evaluate the cash position of a Company

• To plan where to get the source of funds if there is a shortfall of cash required

• To optimise cash for investments etc.

• Starting point: Identify what are cash and non-cash items in the financial statements

• Practice: Berjaya Food Group

January February March

Budgeted unit sales 10,000 12,000 15,000

Price per unit 25$ 25$ 25$

Budgeted sales revenue 250,000$ 300,000$ 375,000$

Receipts from December sales 30,000$

Receipts from January sales 175,000 72,500$

Receipts from February sales 210,000 87,000$

Receipts from March sales 262,500

Total cash receipts 205,000$ 282,500$ 349,500$

January: .70 × $250,000 = $175,000 and .29 × $250,000 = $72,500

February: .70 × $300,000 = $210,000 and .29 × $300,000 = $87,000

March: .70 × $375,000 = $262,500

Cash Receipts BudgetAll sales are on account. Jones’ collection pattern is: 70% collected in month of sale, 29% collected in month after sale, 1% will be uncollectible.

Accounts receivable on December 31 is $30,000, all of which is collectible.

January February March

Material purchases (lbs.) 43,500 38,400 31,100

Cost per pound 0.90$ 0.90$ 0.90$

Total cost 39,150$ 34,560$ 27,990$

Payables from December 18,000$

January purchases 19,575 19,575

February purchases 17,280 17,280

March purchases 13,995

Total payments in month 37,575$ 36,855$ 31,275$

½ × $39,150 = $19,575

½ × $34,560 = $17,280

½ × $27,990 = $13,995

Cash Payments for MaterialsMaterials used in production cost $0.90 per pound. One-half of a month’s purchases are paid for in the

month of purchase; the other half is paid for in the following month.

No discount terms are available. The accounts payable balance on Dec 31 is $18,000.

With just a bit more information, we will be able to prepare a comprehensive cash budget.

We need the information below to complete the cash budget for Jones Company:

▪ Has a $100,000 line of credit at its bank, with a zero balance on

January 1.

▪ Maintains a $20,000 minimum cash balance.

▪ Borrows at the beginning of a month and repays at the end of a

month.

▪ Pays interest at 12 percent when a principal payment is made.

▪ Pays a $77,000 cash dividend in January.

▪ Purchases equipment costing $118,245 in February and $196,540

in March.

▪ Has a $25,175 cash balance on January 1.

Comprehensive Cash Budget

January February March

Beginning cash balance 25,175$ 20,000$ 33,950$

Cash receipts 205,000 282,500 349,500

Cash available 230,175$ 302,500$ 383,450$

Cash payments:

Materials budget 37,575$ 36,855$ 31,275$

Labor budget 12,800 16,200 9,400

Manufacturing OH budget 62,800 66,200 59,400

S&A expense budget 25,000 26,000 27,500

Equipment purchases 0 118,245 196,540

Dividends 77,000 0 0

Total cash payments 215,175$ 263,500$ 324,115$

Balance before financing 15,000$ 39,000$ 59,335$

Borrowing 5,000 0 0

Principal repayment 0 (5,000)

Interest 0 (50)

Ending cash balance 20,000$ 33,950$ 59,335$

Comprehensive Cash Budget

To maintain the $20,000 cash balance, the company must

borrow $5,000 from its line of credit at the end of the month.

$5,000 × .12 × 1/12 = $50

The company does not need to borrow money at the end of

February. The $5,000 loan must be repaid along with interest of $50

($5,000 x 0.12 x 1/12).

Case Study (Flip Classroom Group 1)

Prepare a Cash Budget based on the following case:

Rashford Sportswear is a custom imprinter that began operations six months ago. Sales have exceeded management’s most optimistic projections. Sales are made on account and collected as follows: 50% in the month after the sale is made and 45% in the second month after sale. Merchandise purchases and operating expenses are paid as follows:

In the month during which the merchandise is purchased or the cost is incurred 75%

In the subsequent month 25%

Cash on hand August 31 is estimated to be RM40,000. Collections of August 31 accounts receivable were estimated to be RM20,000 in September and RM15,000 in October. Payments of August 31 accounts payable and accrued expenses in September were estimated to be RM24,000.

Case Study (Flip Classroom Group 1)Rashford Sportswear’s income statement budget for each of the next two months, newly revised to reflect the success of the firm, follows:

September October

Sales RM42,000 RM54,000

Cost of goods sold:

Beginning inventory RM6,000 RM14,400

Purchases RM37,800 RM44,000

Cost of goods available for sale RM43,800 RM58,400

Less: Ending inventory (RM14,400) (RM20,600)

Cost of goods sold RM29,400 RM37,800

Gross profit RM12,600 RM16,200

Operating expenses RM10,500 RM12,800

Operating income RM2,100 RM3,400

Case Study (Flip Classroom Group 2)

The following budgeted income statement for Magnificent Uzbeks (MU) Sdn. Bhd. where you are the Financial Accountant.

APRIL

Sales RM224,000

Cost of goods sold* 153,600

Gross profit RM70,400

Operating expenses^ 35,200

Operating income RM35,200

*includes all product costs i.e. direct materials, direct labour and manufacturing overhead

^includes all period costs i.e. selling, general and administrative expenses

Case Study (Flip Classroom Group 2)

Additional information:

• 40% of sales are cash sales.

• 65% of credit sales will be collected one month after the sales, the 30% in the second month after the sales. The remaining will be bad debt.

• Depreciation represents RM12,800 of the estimated monthly operating expenses.

• Cost of goods sold and operating expenses are paid in the month incurred.

• Cash at April 1 2020 is RM22,400 and both accounts receivable of RM109,200 from March sales and RM21,504 from February sales will be collected in April.

• Capital expenditure of RM30,000 is expected to be made in April.

Based on the information given, prepare a cash budget for the month of April.

Performance Evaluation

• Monitoring an organisation’s effectiveness in fulfilling its objectives• Helps assess profitability of current operations • Identify areas that need closer attention• Allocate scarce resources efficiently

• High degree of subjectivity

• Factors required for a successful performance evaluation system:• Integration with overall business strategy• Feedback & review• Comprehensive measures• Ownership & support throughout the organisation• Fair & achievable measures• A simple, clear & understandable system

• Cultural differences might change how strategies to be implemented• US: managers involved in budgeting process & budget variances used as basis for evaluating performance &

determining rewards• Japan: budget variances view as providing information that can be used to improve performance • Mexico: authoritarian leadership style, no need to share information with subordinates & little faith in

participative management styles • Intolerance of uncertainty can lead managers to require short payback periods for capital investments

Opportunity cost vs Differential Cost

• Income forgone by choosing one alternative over another

• not recorded in the accounting records, but are relevant to decisions because they are a real sacrifice

• Will differ according to alternative activities being considered

• New Business????• The decision to accept additional business should be based on incremental costs and

incremental revenues. • Incremental amounts are those amounts that occur if the company decides to accept

the new business.

• Make or Buy????• The relevant cost of making a component is the cost that can be avoided by buying

the component from an outside supplier • Costs avoided must be greater than outside supplier’s price to consider buying the

component

• Continue or discontinue certain segment???• Effect on operation income and common fixed expenses

• Short-term allocation of scarce resources???• Fixed costs are not affected by this particular decision, so management can focus on

maximising total contribution margin

Making Decisions

Master Decker: Expansion Opportunities

• Determine the cash outflows and inflows for Decker Building, Stains and Cleaning Chemicals

• Determine the return on investment and payback period

• Discuss the expansion opportunities

• Advise the Company

Anwar Aluminum Works

• Determine the cash outflows and inflows for Renfrew Automotive and Evers Manufacturing

• Calculate the unit contribution and contribution margin rate

• Discuss should new customer orders be accepted

• Advise the Company

Revision

• Final Exam: • 5 mandatory questions on Short Term Decision

Making, Financial Statement Analysis, Cost Volume Profit, Activity Based Costing and Cash Budget.

• Each question carries 20 marks

• Online Exam (3 hours plus 30 minutes before exam time and 15 minutes after time ended to upload)

• Exam scripts to email to: [email protected]

Mind map of the module content