Embed Size (px)

Citation preview

Corporate Reporting of C t G d Ta means of Corporate Governance and Transparency

Presented by

Abdul Rahim Suriyawww.arsuriya.comwww.arsuriya.com

Seminar Objectives

To provide participants an

overview of expectations ofoverview of expectations of

stakeholders with regard to

i f ti t b i l d dinformation to be included

in the Annual Report;

k f l h l l k To make familiar with voluntary disclosures in Pakistan

To highlight areas for improvement to make Corporate R ti t t dReporting more transparent; and

To achieve excellence in annual corporate reporting by applying best practices around the worldapplying best practices around the world

2

Take awaysTake aways

B th d f thi i By the end of this session ,

Appreciate the importance of annual reports

you should be able to:

pp p pas tool for business decision making

Guide management in developing the annual Guide management in developing the annual reports with changing expectations of stakeholders.

Corporate Reporting –a means of Corporate Governance and Transparency

Corporate Reportingof Corporate Governance and Transparency

Co po ate epo t gWhat framework is

followed ?

What are the best practices locally and internationally?

Corporate Reporting –a means for Corporate Governance and

The accounting data are communicated

Transparency

The accounting data are communicatedthrough Financial Statements

Corporate Governance is communicatedCorporate Governance is communicatedthrough Annual Report.

The Challenge: Balance Conflicting Interests Between h dthe Company and Investors

Company seeks to :

Investors seek to:

Include information on

Reduce scope of disclosure to maintain competitive strengths

business risks

Compare actual results ith th l

Unwillingness to provide information on development prospects

with the plan

Information on corporate governanceprospects governance

Disclose additional historic informationinformation

have increased the focus on both the role of the Board and its effectiveness in executing its

responsibilitiesresponsibilities.

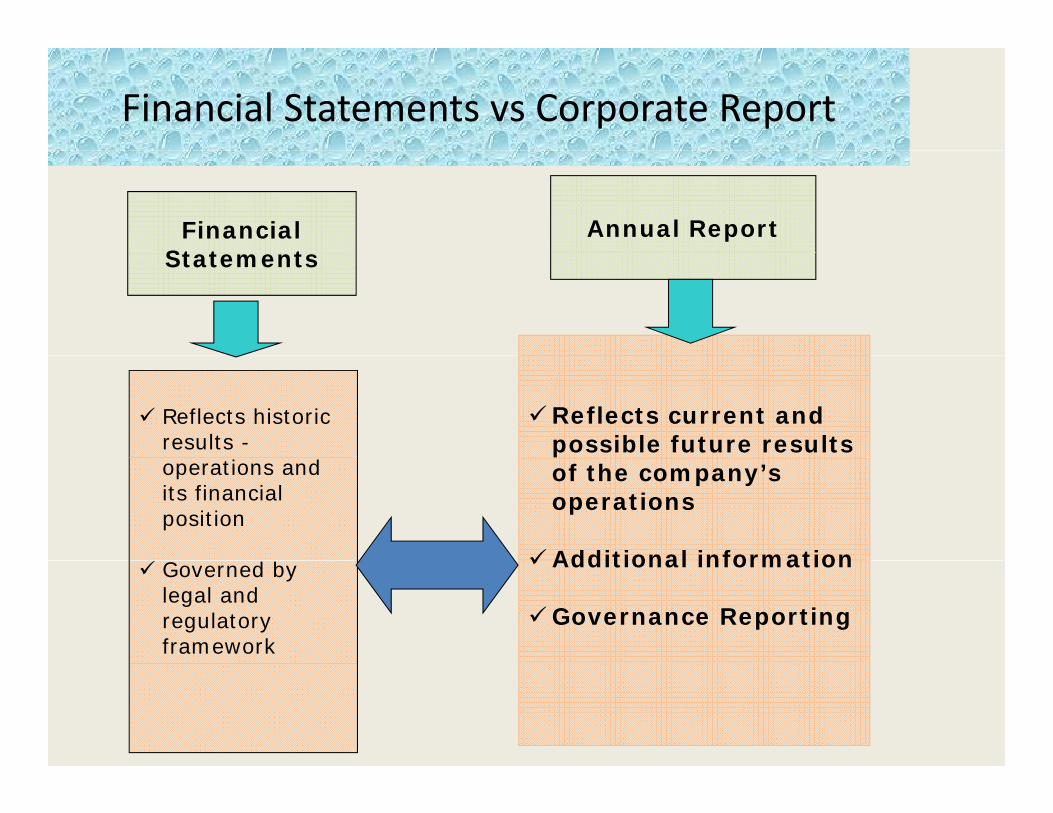

Financial Statements vs Corporate Report

FinancialSt t t

Annual ReportStatements

Reflects historic results -

Reflects current and possible future results

operations and its financial position

of the company’s operations

Additional information Governed by legal and regulatory framework

Additional information

Governance Reporting

ANNUAL REPORT

is it specifically required by law

Annual Report‐

International Standard on Auditing # 720

“ An entity ordinarily issues on an annual y ybasis a document which includes its audited financial statements together audited financial statements together with the auditor’s report thereon. This document is frequently referred to as document is frequently referred to as the “annual report”.

What is OTHER INFORMATION as per IAS #720p

Financial and non‐financial information other than: financial statements and auditor’s report

Auditors’ duty for additional information IAS # 720as per IAS # 720

Auditor’s opinion does not cover other informationp

Auditor has no specific responsibility.Auditor has no specific responsibility.

Auditor shall read the other information to identify ymaterial inconsistencies

When to obtain the other information ?

preferably prior to the date of the auditor’s report.

Where Code of Corporate Governance talks about Annual Report‐talks about Annual Report

CCG requires that Annual report should contain:

the names of the non executive, executive and independent director(s)

details of the aggregate remuneration separately of executive and non executive directors

The names of members of the committees of the board The names of members of the committees of the board

All trades in the shares carried out by its directors, executivesAll trades in the shares carried out by its directors, executives and their spouses and minor children

Objectives of BCR Award

1- To encourage and give recognition to ll i l t ti excellence in annual corporate reporting

2- To promote corporate accountability transparency

Criteria for best reports in Pakistan

Criteria for 2012 is

www.icap.org.pkwww icmap com pkwww.icmap.com.pk

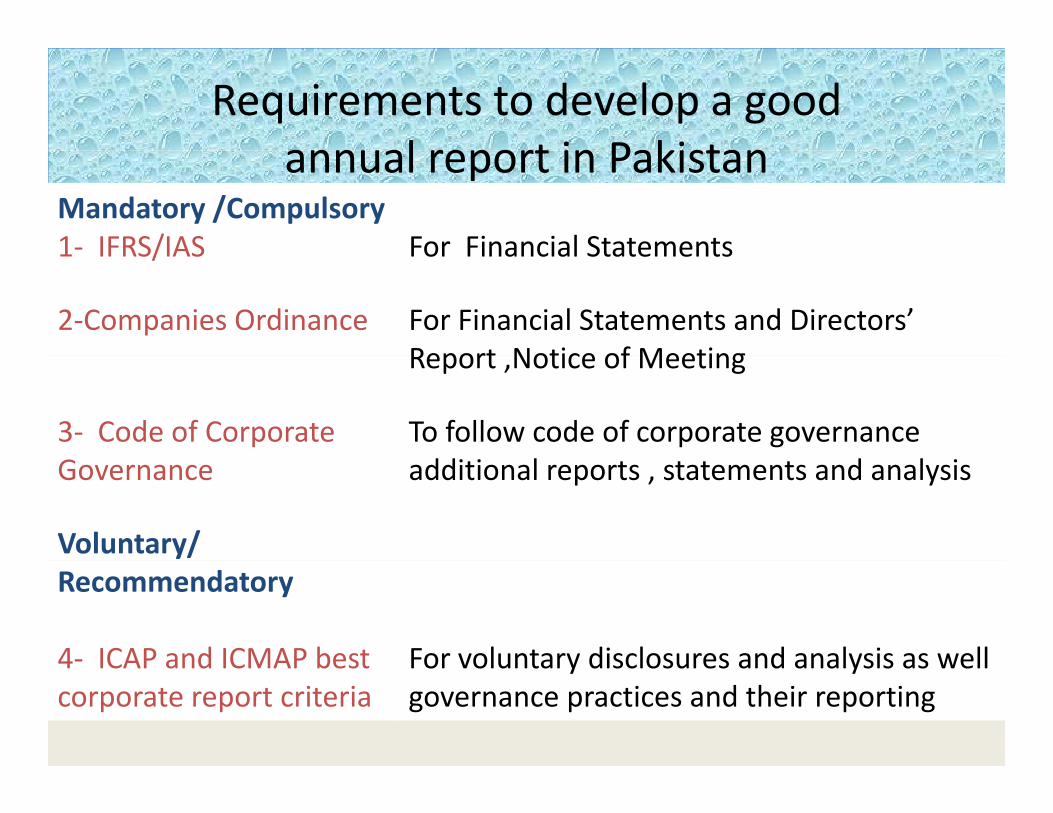

Requirements to develop a good annual report

The ‘Criteria’ not only comprise of mandatory requirement

Encourages to adopt best practice being followed all practice being followed all over the world

Requirements to develop a good annual report in Pakistanannual report in Pakistan

Mandatory /Compulsory1‐ IFRS/IAS For Financial Statements1 IFRS/IAS For Financial Statements

2‐Companies Ordinance For Financial Statements and Directors’ Report Notice of MeetingReport ,Notice of Meeting

3‐ Code of Corporate To follow code of corporate governance Governance additional reports , statements and analysis

Voluntary/ Recommendatory

4‐ ICAP and ICMAP best For voluntary disclosures and analysis as well4 ICAP and ICMAP best corporate report criteria

For voluntary disclosures and analysis as well governance practices and their reporting

Criteria for judging Best Annual Reports

ELIGIBILITY

From 2012, all Annual Reports will be considered for this competition; however, annual reports not containing a clean audit report would be subject to a deduction of a maximum of 5 marksof 5 marks.

Highlights of ADDITIONAL DISCLOSURES IN THE BCR CRITERIA 2012 ‐

NOTE : THESE ARE NOT PART OF LAWNOTE : THESE ARE NOT PART OF LAW However items written in red color are those which were subsequently

Directors’ Report

incorporated in CCG 2012

• Nature of business including business model discussions

• Management's objectives and strategies ‐addressing threats and opportunities of market

trendstrends

• Significant changes in an entity’s objectives and strategies from the previous period or periods

• The relationship between :• The relationship between :

the entity’s results ,

management’s objectives and

management’s strategies for achieving those objectives.

Highlights of ADDITIONAL DISCLOSURES IN THE BCR CRITERIA 2012

Description of the entity's most significant:• Resources, including an analysis of liquidity, cash flows, financing arrangements, human capital;

• Capital structure including any inadequacies in the capital structure and plans to address suchthe capital structure and plans to address such inadequacies;

• Significant changes in financial position liquidity• Significant changes in financial position, liquidity and performance compared with those of the previous period;previous period;

Highlights of ADDITIONAL DISCLOSURES IN THE BCR CRITERIA 2012

• Risks, including strategic, commercial operational and financial risks;

• Plans and strategies for mitigating these risks andPlans and strategies for mitigating these risks and potential opportunities; and

• The significant relationships that the entity has• The significant relationships that the entity has with stakeholders, how those relationships are likely to affect the performance and value of thelikely to affect the performance and value of the entity, and how those relationship are managed

Highlights of ADDITIONAL DISCLOSURES IN THE BCR CRITERIA 2012IN THE BCR CRITERIA 2012

• Comparison of the entity's financial and non‐fi i l f ffinancial performance from:

th l t d the last year and

d i ti f th f t t i l di description of the future prospects, including whether the performance may be indicative of the future performanceof the future performance

Highlights of ADDITIONAL DISCLOSURES IN THE BCR CRITERIA 2012

• Forward looking informationgin narrative or quantitative

form including projectionsform including projections

or forecasts

• Explanation as to how the performance of thep p

entity meets/exceeds and why it was short of

forward looking disclosures made in the priorforward‐looking disclosures made in the prior period( applicable from 2013)

Highlights of ADDITIONAL DISCLOSURES IN THE BCR CRITERIA 2012IN THE BCR CRITERIA 2012

• Description of critical performance measures and indicators ‐‐‐‐against stated objectives of the entity and

• whether the indicators used currently will continue to be relevant in the future

• Human resource management policies including preparation of a succession planpreparation of a succession plan

Highlights of ADDITIONAL DISCLOSURES IN THE BCR CRITERIA 2012IN THE BCR CRITERIA 2012

• Analysis of the prospects of the entity including targets for financial and non‐financial measures and explanation as to why the results from performance measures have changed or how the indicators have changedchanged or how the indicators have changed

M k h i f i f bl f• Market share information preferably from an independent source

• Description of energy saving measures taken ‐‐‐‐

h h i l i h l ihow the company is planning to overcome the escalating energy crisis

Highlights of ADDITIONAL DISCLOSURES IN THE BCR CRITERIA 2012

Specific Disclosures encouraged in Financial Statements

there are 14 marks , out of that 12 marks are awarded based on

specific disclosures like

• Cash flow statement based on Direct Method

• Disclosure of fair value of property, plant & equipment

• Summary of significant/ material assets or immovable Summary of significant/ material assets or immovable

property

Highlights of ADDITIONAL DISCLOSURES IN THE BCR CRITERIA 2012IN THE BCR CRITERIA 2012

Stakeholders’ Information6 years data for6 years data for • Cash flow statement• Vertical and Horizontal analysis• Ratios

( CCG doesn’t suggest any specific ratios, CCG only asks for KEY OPERATING and FINANCIAL DATA)and FINANCIAL DATA)

• Comments on the results of the analysis of ratios, cash flows and financial statements

Statement of Value Added and how distributed with graphical presentationpresentation

Investors’ Related section on the corporate website

Highlights of ADDITIONAL DISCLOSURESIN THE BCR CRITERIA 2012IN THE BCR CRITERIA 2012

Report Presentation p• Theme on the cover• Effectiveness of photographs and their relevance• Effectiveness of charts and graphic for Financial

Statements• Calendar of major events during the year• Comprehensiveness of corporate information and

address for correspondence e g website emailaddress for correspondence e.g. website, email addresses and telephone Nos.

• Complete and accessible annual report on the website • Definition and glossary of terms

Highlights of ADDITIONAL DISCLOSURESIN THE BCR CRITERIA 2012

Corporate GovernanceCorporate Governance • Timely authorization by Board of Directors within 30

daysdays

• Organization Chart

• The Board structure and its committees• The Board structure and its committees

• Chairman of the Board other than the CEO

N f ti di t i di ti th i• Name of non‐executive directors, indicating their independence, with at least one independent non‐executive director having relevant industry experienceexecutive director having relevant industry experience

Highlights of ADDITIONAL DISCLOSURES IN THE BCR CRITERIA 2012IN THE BCR CRITERIA 2012

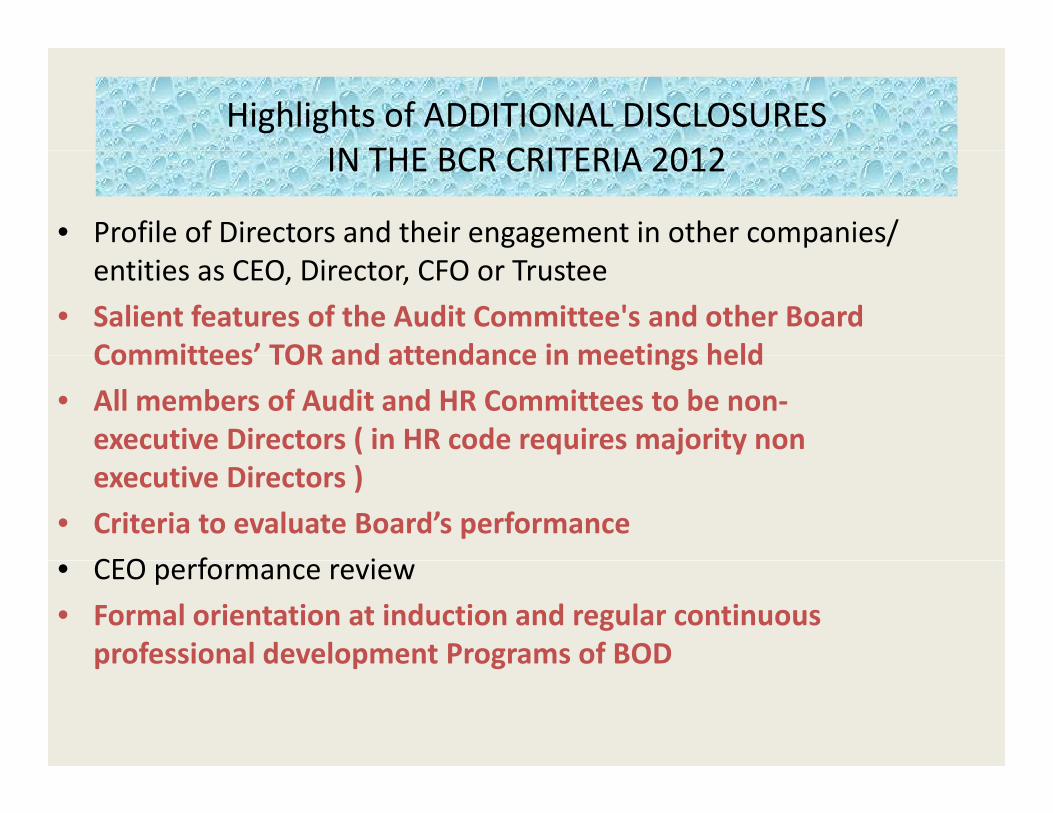

• Profile of Directors and their engagement in other companies/ entities as CEO, Director, CFO or Trustee

• Salient features of the Audit Committee's and other Board Committees’ TOR and attendance in meetings heldCommittees TOR and attendance in meetings held

• All members of Audit and HR Committees to be non‐executive Directors ( in HR code requires majority non executive Directors )

• Criteria to evaluate Board’s performance

CEO f i• CEO performance review

• Formal orientation at induction and regular continuous professional development Programs of BODprofessional development Programs of BOD

BEST SUSTAINABILITY REPORT AWARD

CCG requires BOD to consider REPORT on CSRN E i th f t ti i P ki t New Era in the eve of corporate reporting in Pakistan.

Encourage the corporate world to focus beyond single g p y gbottom line financial performance to triple bottom line :

• economic • economic, • environmental and • social performance

Sustainability Reporting in INDIA is mandatory for all listed companies for ye Dec31,2012

SECP has also issued draft guidline and soughtcomments on Sustainability Reporting .

WAY FORWARD

S t R t f A dit C itt • Separate Report of Audit Committee

• SWOT analysisy

• Sensitivity of EPS with changes in key variables

• Analysis of variation in results reported in Quarterly accounts

• Financial calendar of planned activities

• A disclosure statement by Directors on CONFLICT OF INTEREST

WAY FORWARD

• Investor relations and Shareholders engagement

• Governance Framework• Governance Framework

• Video presentation of CEO on Company’s website on:

financial results and performance

major products n projects accomplished n initiated

forward looking statement (Caterpillar vedio)

International Trends for more transparenciesE ample of AdidasExample of Adidas

New Contents• Responsibility Statement

• Listing of quantitative and qualitative resultsListing of quantitative and qualitative results

• Interview with CEO• Executive BoardExecutive Board• Supervisory Board• Supervisory Board Report

• Our share

International Trends for more transparenciesExample ofAdidasExample of Adidas

• Ten years over view ( in Pakistan 6 years data are disclosed )

• Glossary

Fi i l C l d f t • Financial Calendar of next year

• Internal Management System

• Business Performance

Ri k d t it R t• Risk and opportunity Report

• Subsequent Events and Outlook

International Trends for more transparenciesExample ofAdidasExample of Adidas

Responsibility Statement

This is signed by CEO ,CFO and Operation Directors

International Trends for more transparencies

Example of AdidasExample of AdidasListing of quantitative and qualitative results :

• Current year vs Targets set vs

t l k f t out look for next year_____________________

E l i f tiExamples information

• New products introducedShare price changes • Share price changes

• Borrowings • Capital expenditures

Sales and profitability increase • Sales and profitability increase

International Trends for more transparenciesExample of AdidasExample of Adidas

Interview with CEO- Questions asked were :2011 was the first year of strategic business plan 2015.Have the financials lived up to expectations?

News flow from the local players suggests that theChinese market will be difficult in 2012 What kind ofChinese market will be difficult in 2012. What kind ofvisibility do you have and do you expect momentum tocontinue?

Beyond your Olympic sustainability goals, have you other specific sustainability targets?

International Trends for more transparenciesExample of AdidasExample of Adidas

One of key 2015 goals is to achieve an operating margin ofy g p g g11%. In 2011, margins only modestly increased. Are youdisappointed with that?

Reebok has seen momentum slow and faces somechallenges with the end of the NFL license What are yourchallenges with the end of the NFL license. What are yourpriorities for continuing progress for the brand in 2012?

And how does your growing expertise in own retail play into making Adidas a success?

International Trends for more transparenciesExample of AdidasExample of Adidas

Executive Board

Our Executive Board is comprised of fourmembers who reflect the internationalmembers who reflect the internationalcharacter of our Group.

Each Board member is responsible for at leastone major function within the Group.

Profile of all these directors are also published Profile of all these directors are also published

International Trends for more transparenciesExample f AdidasExample of Adidas

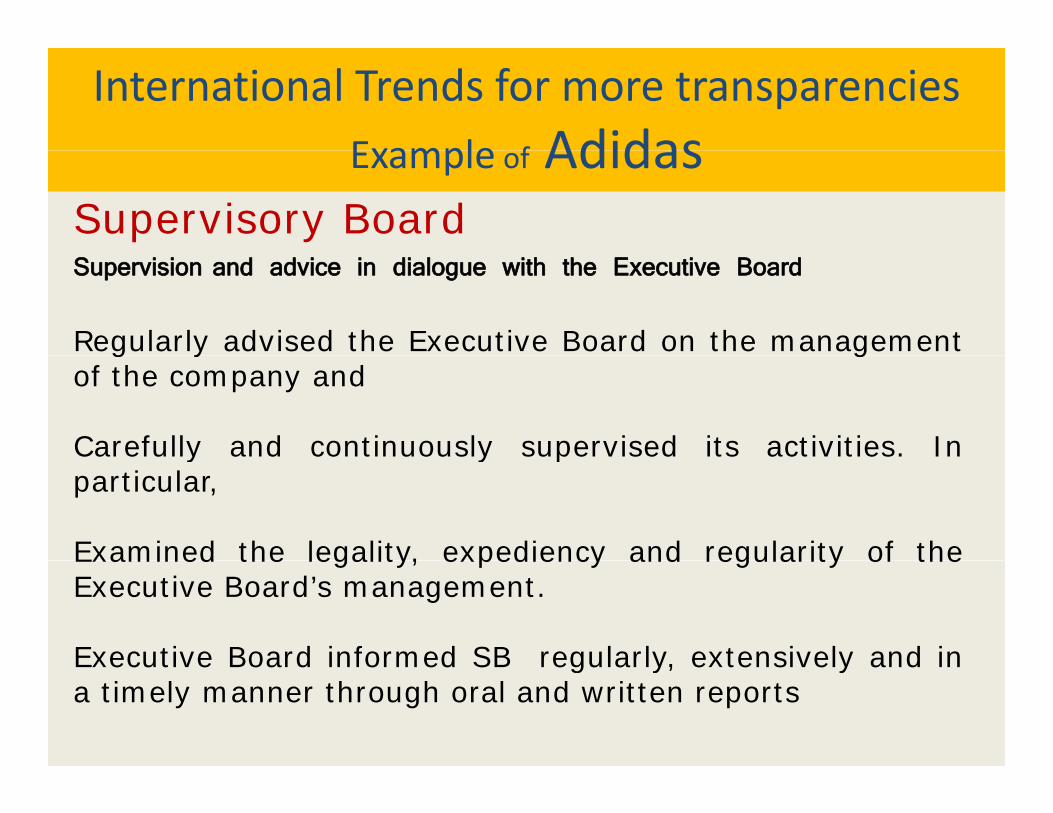

Supervisory BoardSupervision and advice in dialogue with the Executive Board

Regularly advised the Executive Board on the managementg y gof the company and

Carefully and continuously supervised its activities. Iny y pparticular,

Examined the legality, expediency and regularity of theExamined the legality, expediency and regularity of theExecutive Board’s management.

Executive Board informed SB regularly, extensively and inExecutive Board informed SB regularly, extensively and ina timely manner through oral and written reports

International Trends for more transparenciesf adidasof adidas

Supervisory Board

Executive Board presented at every Supervisory Boardmeeting at each quarter:

d l f l d i• development of sales and earnings,• employment situation as well as• business development of the individual markets were

presented by the

The Steering Committeegis authorized to pass resolutions on behalf of the entire Supervisory Board in particularly urgent cases.

International Trends for more transparenciesExample of AdidasExample of Adidas

OUR SHAREIn 2011 international stock market performance variedIn 2011, international stock market performance varied

Volatile markets due to :

the sovereign debt crisis in the euro and

l i l b l i slowing global economic.

The political unrest in the Middle East and NorthernAf i ll th d t ti th k dAfrica as well as the devastating earthquake andtsunami in Japan also weighed on financial markets.

International Trends for more transparencies

E l f AdidasExample of AdidasOUR SHARE

The adidas AG share clearly outperformed both indices,gaining 3% over the period which is due to

consistently strong financial results throughout 2011

rising confidence in the strategic business plan 2015,rising confidence in the strategic business plan 2015,

With further balance sheet improvements

�� ������ �� ������� � 25� ������ ��������

�������� �� ��� ����� ���� �� ��� 2012 A����� G������

M������.

International Trends for more transparenciesExample of AdidasExample of Adidas

Internal Management System :g yPrincipal financial goal ‐‐‐‐is maximizing operating cash flow.

Continually improving our top‐ and bottom‐line performance

Our planning controlling system is therefore designed toprovide a variety of tools to assess :

our current performance and to align future strategic and investment decision

to best utilize commercial and organizational opportunities

International Trends for more transparenciesExample of AdidasExample of Adidas

Internal Management System - matters discussed:• Operating cash flow as Internal Management Focus

• Operating margin as key performance indicator of operational progress

• Operating expense control

•Tight operating working capital management

•Capital expenditure targeted to maximize future returnsp p g

•Cost of capital metric used to measure investment potential

•Structured performance measurement system•Structured performance measurement system

•Management appraisal of performance and targets

International Trends for more transparenciesExample of AdidasExample of Adidas

Business Performance

Comments on analysis are covered in this section

Sales increased 13% as a result of double-digitgrowth.

Revenues grew 11% to € 13.344 billion from€ 11.990 billion in 2010.

Gross margin decreased 0.3 percentage to 47.5%(2010: 47.8%), as the increase in input costs

International Trends for more transparenciesExample ofAdidasExample of Adidas

Business Performance

Comments and graphic presentation on : sales performance sales performance cost of sales marketing other operating expenses other operating expenses profitability with last year,

Graphic presentation of sales byGraphic presentation of sales by quarter, segment, region region, product category,

International Trends for more transparenciesExample of AdidasExample of Adidas

Business Performance

• Increase in assets fixed and current assets

• Liabilities growth

E it d t i i t i• Equity grows due to increase in net income

• Capital expenditure growth and its segment Capital expenditure growth and its segment and type classification in graphical form

T fi i li • Treasury – financing policy

Compulsory disclosures in respect of RISKdisclosures in respect of RISK

Companies Ordinance ‐‐ does not require any suchdi l

.

disclosure

Code of Corporate Governance –Code of Corporate Governance

• BOD to formulate significant policies which include Risk g pManagement

• Director’ Report shall outline along with future prospects ,risk and uncertainties surrounding the companycompany

Voluntary disclosures in respect of RISKdisclosures in respect of RISK

Best Corporate Report Award Criteria

.Description of the entity's most significant Risks, including strategic, commercial operational and financial risks and

Plan and strategies for mitigating these risks and potentialopportunities

Management Commentary

Risks, including strategic, commercial operational and financial risks;Risks, including strategic, commercial operational and financial risks;

Plan and strategies for mitigating these risks and potentialopportunities

More detailed discussions are provided in para 29,31,32 and 36

International Trends for more transparenciesExample of AdidasExample of Adidas

a separate Report is developed under the titleRisk and Opportunity ReportRisk and Opportunity Report

Explores and develops opportunities : to sustain earnings andg drive long term increase in share holder value to take certain risks to maximize business opportunities

This section include :This section include :

1.Risk and opportunity management Review

lPrinciplesSystem

2.Strategic and operational opportunities3.Financial opportunitiespp4.Management assessment of overall risks and opportunities5.Financing and Liquidity risk

International Trends for more transparenciesExample of AdidasExample of Adidas

Corporate opportunities

Strategic and Opportunities

Financial opportunities

Management assessment of overall risks and opportunities

International Trends for more transparenciesExample ofAdidasExample of Adidas

Subsequent Events and OutlookThis section include Forward looking statements for

• Sales and profitabilityp y

• Expected EPS

Operating working capital as a percentage to sales• Operating working capital as a percentage to sales

• Investment level

• Liquidity management

• Management to propose dividend

• Long strategic goals

International Trends for more transparenciesExample of AdidasExample of Adidas

Subsequent Events and Outlook

We forecast sales to increase at a ---rate on due to growth in theWholesale and Retail segments as well as in Other Businesses.g

Gross margin is expected to be around 47.5%.

Operating margin is forecasted to increase to a level approaching8.0%, driven by lower other operating expenses as a percentagef l A ltof sales. As a result

we project earnings per share to grow at a rate between 10% and15% to a level between € 3.52 and € 3.68.

International Trends for more transparenciesExample of AdidasExample of Adidas

Outlook - Forward looking statements These reflect Management’s current view with respect to thefuture development .

The outlook is based on estimates that we have made on thebasis of all the information available

These are subject to risks and uncertainties as described inthe Risk and Opportunity Report, which are beyond thecontrol

The adidas does not assume any obligation to update any forward-looking statements made in this Management Report g g pbeyond statutory disclosure obligations.

Best practice for CorporatebReporting by PWC

Few extracts from the Annual ReportFew extracts from the Annual Report

of FTSE 350 companies

Best practice for CorporateReporting by PWC

Subject Company Name

What is our approach to Governance Marks and Spencerpp

Chairman and CEO , Chairman’s independence

First Group plc, Prudential plc

independence

How does the Board demonstrate independence

Marks and Spencer

.

independence

Justification of independence Tesco plc , MITIE Group plc

Information and professional development

Kingfisher plc,Roll Royce

Best practice for CorporateReporting by PWCReporting by PWC

Subject Company Name

Access to independent advice National GridAccess to independent advice

Directors Performance Evaluation British American Tobaccob h lDebenhams plc

Going Concern Old Mutual Plc

.

Internal Control British Airways plc

Whistleblowing Wolseley plc

Whistleblowing

Dialogue with Institutional Shareholders

Wolseley plc

British Airways plc

What is our approach to governance?What is our approach to governance?

Example of Mark and spencerExample of Mark and spencer

We believe that good governance has four fundamentalWe believe that good governance has four fundamental

components:

• Leadership – clear and well communicated• Leadership – clear and well communicated

• Challenge – focused and effective

• Oversight active and comprehensive and• Oversight – active and comprehensive and

• Questioning – rigorous and sustained

What is our approach to governance?What is our approach to governance?

To achieve this board needs to:To achieve this board needs to:

i d d• Demonstrate independence

• Seek full information

• Act responsibly

Role of chairman and chief executiveRole of chairman and chief executive

Example of First group plca p e o st g oup p cThe chairman is responsible for:• Leadership• Timely and clear information• Effective communication• Managing the board• Managing the board• Regular evaluation of the performance of the board• Identify development needs of individual directors.• Effective contribution of Non‐ executive directors • constructive relations between executive and non‐executive

directorsdirectors.• Comprehensive induction program

Role of chairman and chief executiveRole of chairman and chief executive

Chief Executive Officer is responsible for:Chief Executive Officer is responsible for:

• Running the day to day business of the group

• Implementation of the policies and strategiesImplementation of the policies and strategies

• Day to day management of the executives

• Leading the development of senior management• Leading the development of senior management

• Ensuring that the chairman is kept appraised

• Indentifying and accessing opportunities for the• Indentifying and accessing opportunities for thegrowth and review performance of existingbusinessbusiness

Dialogue with institutional shareholdersDialogue with institutional shareholders

Example of British airways plcp y pThe company maintain regular contacts with its largerinstitutional shareholders through :g

its investor relation team,

meetings with the executive directors andmeetings with the executive directors and

annual institutional investor events.

The presentations are also available company’sThe presentations are also available company sinvestor relations website

Seven members of the boards attended the annualSeven members of the boards attended the annualinvestor day in March 2009.

Dialogue with institutional shareholdersDialogue with institutional shareholders

Example of British airways plcp y p

Private shareholder receive the company’sshareholder magazine twice a year and areshareholder magazine twice a year and areencourage to express their views and concerneither in person at the AGM or by emaileither in person at the AGM or by email.

h h d h b dThe main themes are reported to the boardand responded to by the chairman in hisdd h l laddress at the annual general meeting.

Constructive use of the AGMConstructive use of the AGM

Example of Marshals plcExample of Marshals plc• A presentation is made on the progress and performance of

the business prior to the formal business of the meetingp g

• The chairman of the audit, remuneration and nomination committee normally attend the AGM and are available to answer. All directors normally attend the meeting.

• The board welcomes question from shareholders who have an opportunity to raise issues informally or formally beforean opportunity to raise issues informally or formally before or at the AGM.

Constructive use of the AGMConstructive use of the AGM

Example of BP p l cExample of BP p.l.c. BP’s AGM enables share holders to:

ask questions

hear resulting discussion about performance

directors’ stewardship of the company.

vote on all matters (except procedural issues) vote on all matters (except procedural issues)are taken by a poll at the AGM,

Constructive use of the AGMConstructive use of the AGM

Example of BP p l cExample of BP p.l.c. • Voting level at the AGM increased to 64%,compared with 61% in 2007compared with 61% in 2007

• AGM was webcast• AGM was webcast

Th b h d i i• The webcast , speeches and presentations given atthe AGM are available to download at websitetogether with the outcome of voting on thetogether with the outcome of voting on theresolutions.

Whistle blowingWhistle blowing

Example from British American Tobacco p l cExample from British American Tobacco p.l.c.

• Whistle blowing policy and procedures bl ff i fid ienable staff, in confidence, to raise

concerns about possible improprieties in financial and other matters and to do so without fear of reprisal. p

• The Audit Committee receives regular reports on whistleblowing incidentsreports on whistleblowing incidents.

Local Example Governance FrameworkGovernance Framework

Engropolymer

Our governance framework is designed to ensure that the Company lives up to its core values and p y pprinciples, institutionalizing excellence in everything we do y g

The work of developing good CorporateThe work of developing good Corporate Governance is ongoing, and aims to incorporate standards universally practicedstandards universally practiced.

Local Example Governance FrameworkGovernance Framework

Improvements in good Corporate Governance have been continually focused upon.• The internal environment

• Internal Control Framework

• Risk Assessment

• Control Activities

• Review

• Salient features of Internal Audit Charter

• Directors• Directors

• Enterprise Risk Management (ERM) System

• Business Risks and Challenges

• Treasury Management and Financial Risks

• External validation of Corporate Governance

Local Example Stakeholder Engagement

EngropolymerEPCL k k h ld i l dEPCL takes stakeholder engagement very seriously, and understands that engaging with all our stakeholders is the only way to ensure that we remain a responsible corporate citizen d h iti i t ll t k h ldand have a positive impact on all our stakeholder groups.

Wider stakeholder community to include:y

• The mediaI t d h h ld• Investors and shareholders

• Suppliers , Customers• Host communitiesHost communities • Employees

.

The views expressed in this presentation are those of the presenter. p

Questions or comments?

![Solar system [suriya] slide show](https://img.dokumen.tips/doc/110x75/55509dceb4c90590208b4a47/solar-system-suriya-slide-show.jpg)