Embed Size (px)

Citation preview

ABBL › B.P. 13 L-2010 Luxembourg › Tel.: (352) 46 36 60-1 › Fax: (352) 46 09 21 › [email protected] › www.abbl.lu

Association des Banques et Banquiers, Luxembourg

The Luxembourg Bankers’ Association

Luxemburger Bankenvereinigung

2008 Annual Report

uarantee described above is provided to retroactively take account of the rights accrued in previous years. For all employees in service on 31 December 2007, the first assessmen

1.

Table of contents

Message from the Chairman 3

Financial markets and securities regulation 8

Post-trade / Clearing & settlement 12

Banking supervision 14

Evolution of the IFRS 16

XBRL 16

SEPA: The first year 17

The Payment Services Directive (PSD) 20

Bank account switching 20

ICT Security 21

The European Savings Directive 22

The fight against money laundering: Recent developments 24

Implementation of the data protection legislation 28

VAT: New reporting obligations for the financial sector 30

Private Banking Group, Luxembourg 31

Retail Banking Group 32

Introduction of the single statute 33

Social elections in 2008 34

Freedom of movement of persons & Immigration 35

Survey on the social situation in the banking sector 36

Collective employment agreement 41

Communicating in times of crisis 42

The identity of the ABBL evolves 44

Promoting social responsibility 45

ABBL events in 2008 46

LFF: Raising the profile 46

IFBL 48

AGDL: Deposit guarantee 52

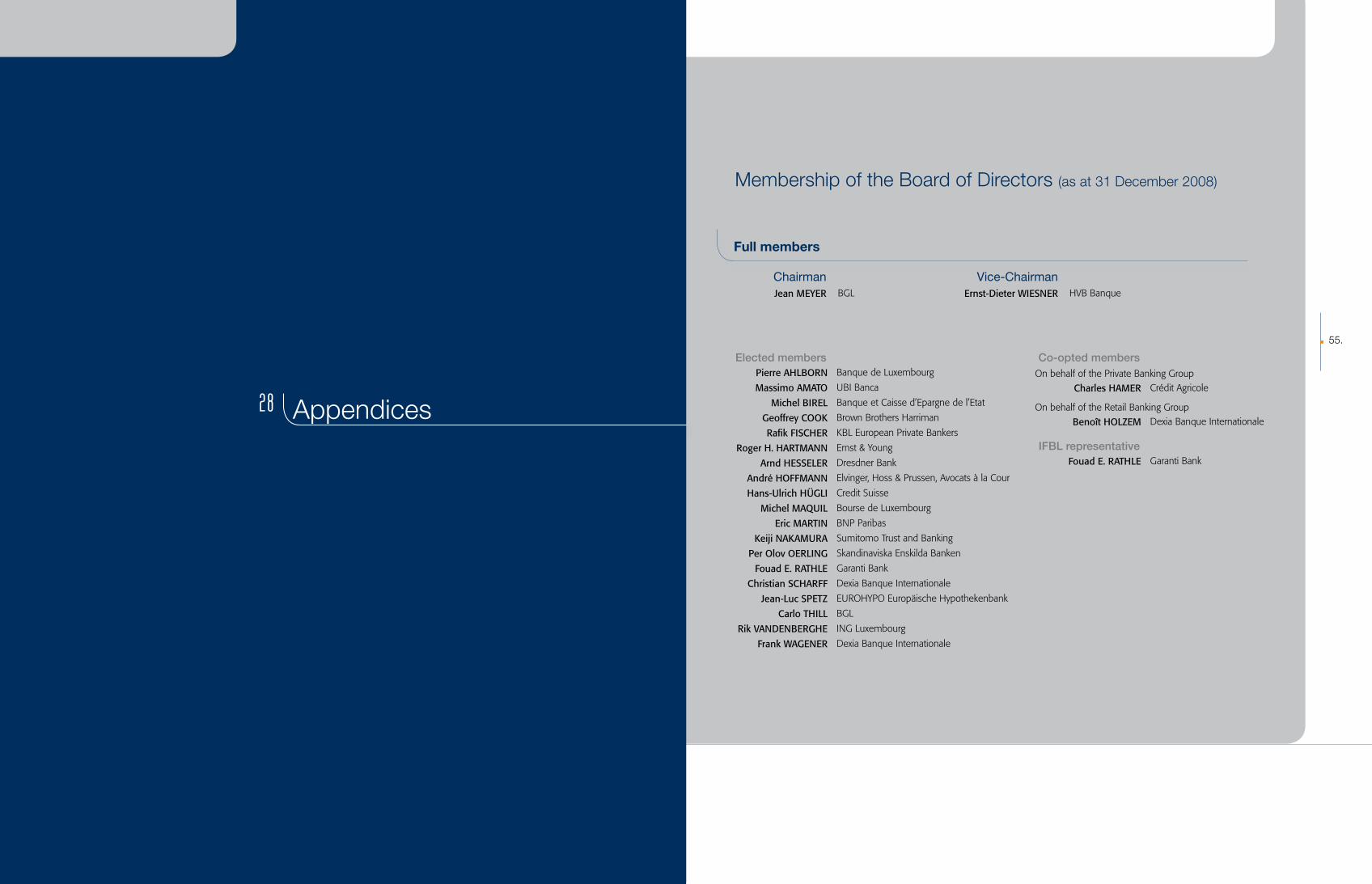

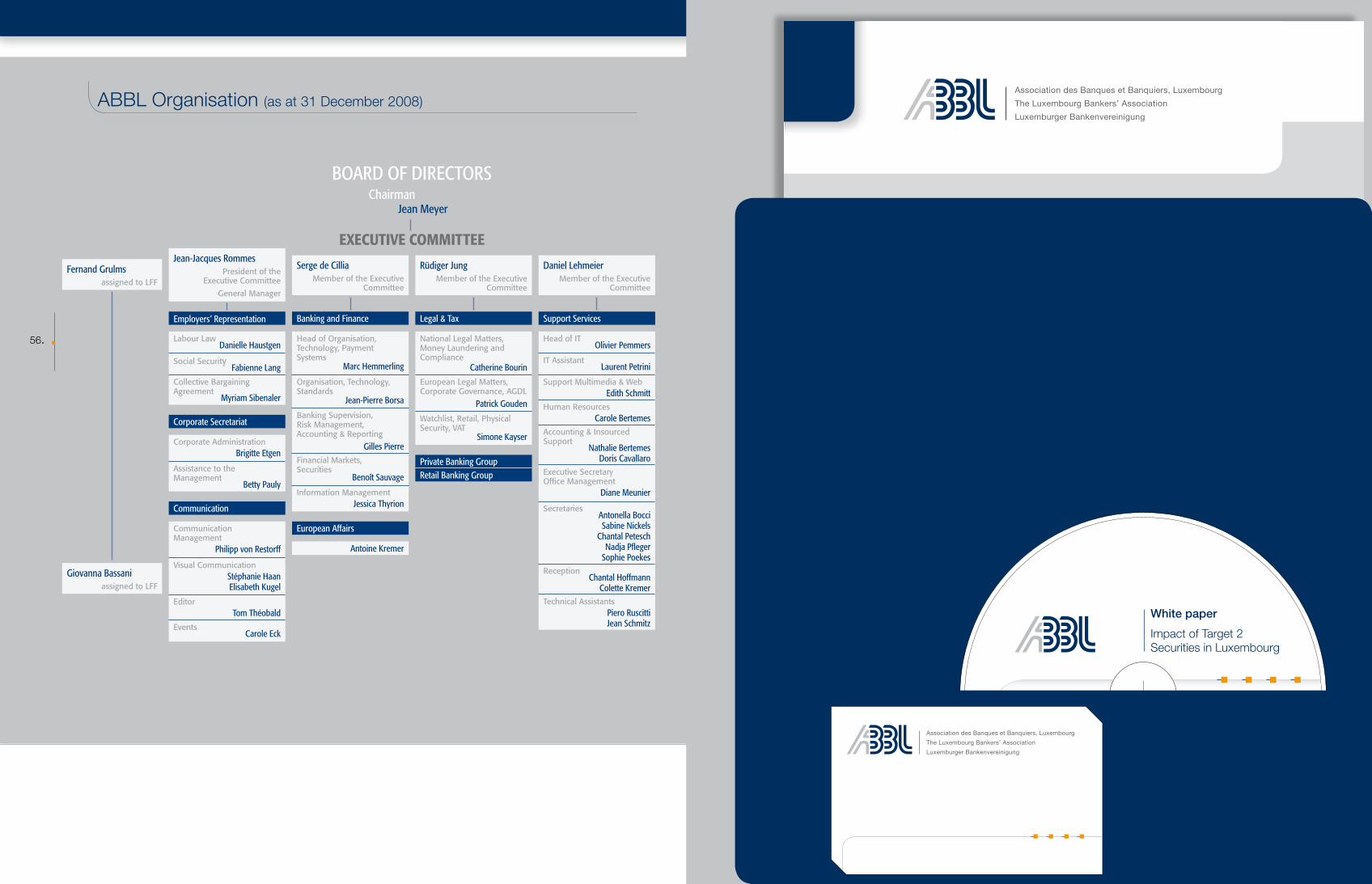

Appendices 54

Accounting & Reporting

Banking supervision & Professional obligations

Client protection

Clusters

Communication

Financial markets & services

Legal & Tax

Payment systems & IT

Social affairs & Employers’ representation

Training

www.abbl.lu

1

2

3

4

5

6

7

8

9

10

12

11

13

14

15

16

17

18

19

20

21

23

22

24

25

26

27

28

page

3.

Jean Meyer

Chairman of the ABBL

Viewed from the end of 2007, the year 2008 was not forecasted as a period of all evils for the financial world nor for the real economy.

I suspected that 2008 would not be a tremendous year, but who would have imagined that we would be running into a real nightmare 10 month later. The problem with crises of this dimension is that they are not foreseen and finally not foreseeable, because we just refuse to accept that such disasters can occur. We tend to believe that a catastrophe of the like of 1929 cannot happen again in today’s well functioning world. The phenomenon is known as disaster myopia; the tendency to underestimate the probability of disastrous outcomes espe-cially for low-frequency events last experienced in a distant past. Obviously, the risk of falling victim to this syndrome is especially high in periods of economic well-being and stability.

Warren Buffet once said that “nothing sedates rationality like large doses of effortless money”.

There were obviously signs which could have discomforted us. We were certainly not at ease when commodities reached unprecedented levels with the barrel of oil coming to a record price of 147 USD, when gold hit a ceiling of 1.000 USD and the Euro shot up to its highest level with an exchange rate to the Dollar of 1,60.

As a matter of fact, what we became used to calling the “financial turmoil” for a little bit more than a year turned into a deep financial crisis in September, when the American authorities decided to let Lehman Brothers fall thereby opening the Pandora box. Confidence had been weak even before this obvious mistake. It pretty much vanished into thin air in the second half of September. The collapse of one of the world’s most prestigious investment banks appeared to be the first domino piece in a number of successive failures in the financial industry.

Investors now had every reason to be pessimistic, which entailed bearish stock markets in which the value of financial industry shares dropped to historically low levels. They were not the only ones, as financial markets began to announce a generalised economic crisis, first in the US, and then shortly afterwards here in Europe.

Message from the Chairman

4. 5.

Bankers were, and still are, frequently blamed for the crisis, and it is hard to deny that among the many mistakes that have led to the economic breakdown, the failure of banks to manage risk adequately is a prominent one. But as a matter of fact, the financial industry had acted in conformity with rules and market practices, as every other entrepreneur would have done. It contributed to economic wealth and years of growth for all economic actors. In return, the collapse of confidence in the financial industry had immediate effects on the worldwide economic system.

In the European financial industry, the Benelux countries were the first to be hit for the simple reason that their economies are the most open to other countries. The difficulties at Fortis and Dexia threatened the economies of all three Benelux countries and even that of France. Here in Luxembourg their systemic importance for all economic actors, for the State and for the financial centre, is of such importance that our authorities did not really have a choice other than deciding to insure their survival at all costs. The Luxembourg government showed its capability for strong and quick action in the interest of our country. But the rescue measures for banks were not limited to these two institutions. Indeed, most European countries had to sup-port their banking industry within a few weeks, in order to avoid a run on bank accounts and a complete collapse of the banking system. Iceland, which was particularly dependent on its highly leveraged banks, did not have the means to avoid the failure of Kaupthing, Landsbanki and Glitnir. The subsidiaries of those three banks in Luxembourg had to ask for a suspension of payments and triggered our national deposit guarantee scheme, the AGDL.

Unfortunately, not all European action was well coordinated in that period. In order to avoid the withdrawal of cash from bank accounts, different European states began to raise the minimum limits of their deposit guarantee schemes in total disorder. When the European finance ministers finally decided to change the directive on deposit guarantees, Luxembourg raised the minimum guaran-teed amount to 100’000 € per capita. This change only came into effect on 1 January 2009, and the Luxembourg deposit guarantee scheme (AGDL) only adapted its statutes on February 18.

In terms of reputation, all banks and bankers have enormously suffered in October and November of last year. It has been decades since confidence in the banking system has been this low. Even here in Luxembourg, where banks have contributed to the country’s exceptio-nal wealth, the credibility of banks reached close to zero.

On the other hand, more than ever, the public and the press wanted explanations and they tried to understand what was happening: why governments had to spend so much money on the banking system, what was the risk borne by depositors and tax payers, and what would be the impact on

the country’s well-being? It was a period when the ABBL had to face public interrogation. “Crisis communication” became the Secretariat’s main activity. The remaining resources were often dedicated to the management of the deposit guarantee scheme and its payout to the customers of Kaupthing, Glitnir and Landsbanki.

Unfortunately, there were more bad news to come. When in December 2008 the Madoff scandal was exposed in the United States, Luxembourg once more came under attack from France, because French investors appeared to have lost their money with Madoff through Luxembourg-based funds. Luxembourg for Finance (LFF), ALFI and the ABBL had to res-pond to questions concerning the liability of depository banks of Luxembourg investment funds. While this question is legally indeed a very tricky one, the foreign press was quick to conclude that Luxembourg legislation offers less guarantees than others in Europe and, more specifically, less than French legislation. This is obviously not true, but again the financial cen-tre had to be on the defensive, only weeks after it was accused by French politicians of being a tax haven responsible for the financial crisis in general.

During this awful autumn in 2008, the Luxembourg financial centre learned a number of practical lessons, of which it was theoretically aware before: Our reputation, even if it is strong with global professionals, is systematically under attack for political reasons. Whether it be the European pass-port for management companies of UCITS, the architecture for European supervision, the tax regime on savings, there are numerous technical issues behind attacks on the reputation of our financial centre. It is of the utmost importance for Luxembourg not to stay on the defensive indefinitely. The creation of Luxembourg for Finance in January 2008 was the right move towards a proactive de-fence of our reputation. We need to advocate our skills and our institutional advantages throughout the world. It appears logical that we should begin by focusing on our European neighbours and partners. By enhancing our credibility in Europe, we make ourselves less vulnerable to attacks in the numerous technical fields where we must defend our interests. We will certainly have to adapt to the new regulation that is going to come as a consequence of the financial crisis. But this is something we have always done very successfully. The real adaptation that lies ahead of us concerns adequate communication towards European politics, business, and the general public. The ABBL will stay committed to PROFIL and LFF in order to win this strategic battle.

Viewed from Luxembourg, in this spring 2009, the financial crisis seems not to have been enough. The Swiss banking system and the strong banking secrecy that made it the private banking centre of the world, came into serious trouble in the wake of the UBS affair, in which the bank was accused by the US of helping thousands of US citizens to evade and cheat US

7. 6.

taxes. This scandal brought plenty of arguments to the opponents of financial centres world-wide who continuously attack secrecy, an alleged lack of transparency and the EU withhol-ding tax system.

The recent action taken by the G20 in London demonstrated clearly that this is an uneven fight of the big nations versus the small ones and that we will have to continue, as we always did, to defend and argument in favour of the privacy rules in which we and all our customers believe.

Confronted with the blackmail of being put on an official blacklist of so called “tax havens”, Switzerland, Luxembourg and Austria agreed to cooperate in tax matters along the lines of OECD standards. Our banking secrecy remains as such. but changes will be brought in as far as cooperation on demand between tax administrations is concerned when tax offenses are under inquiry.

We are convinced that such a concession had to be made in order to avoid the infamy of a blacklist. We also believe that by doing so, our government has acted wisely and strategically. The ABBL will not change its position, refusing an automatic exchange of information that would put at risk our private banking activities.

The bad news of the end of 2008 are reflected in the figures presented by banks in their accounts. Results before provisions are down 9%. On top of that, we must expect careful provisioning in 2008, and the CSSF foresees a shrinking of net results of more than 50%. This will have a direct impact on State revenues, as banks pay 70% of companies’ income tax in Luxembourg. Finally, the total assets under management in Luxembourg investment funds lost 25% of their value in one year.

Due to the government’s interventions, I do not believe that things will turn to catastrophe in 2009. But we must expect the revenues on interest margin and commissions to be lower than in 2008. In other words, just as the rest of the economy, the Luxembourg financial industry will certainly suffer from the general economic crisis, and will live through a very difficult year 2009.

In this context, we will experience enhanced pressure on costs. Very obviously, the nego-tiation for a new collective employment agreement as of 2010 will have to take into account the fact that little growth can be expected from our financial centre for some time. There is, of course, a direct link between cost control and employment. The financial sector in Luxem-bourg has so far proven to be very resistant to the turmoil that began in the autumn of 2007. It has continuously employed new people until the beginning of 2009. We must fear, however,

that the situation on the employment front will deteriorate in the months to come. This is one reason why the ABBL has launched a specific “job market” platform with a view to match available persons with available jobs between our members.

I am aware that this year’s Chairman’s message does not appear to be an optimistic one. It would have been naïve to portray things in any other light. But pessimism, on the other hand, is not an alternative. The strengths of our financial centre remain intact in comparison to our competitors. Luxembourg has shown to be relatively resistant to the tremendous exogenous shock that we have experienced. Our authorities were reactive, our staff remained committed, and our results were less bad than others. This is why I am convinced that Luxembourg will continue to have a financial centre after this crisis with the same relative importance than the one it had before. We will learn from this crisis, not only as an industry, but also as a country. More than ever, it is important for our professio-nals to stick together and to prepare the future of a well-governed financial centre. More than ever, we all need an ABBL to defend us and to be our guide.

Executive Committee

From left to right:

Daniel Lehmeier Jean-Jacques Rommes (General Manager) Rüdiger Jung Serge de Cillia

7.

9. 8.

benefits of the management company passport, which would be detrimental to clients. This approach was working well until large countries turned a deaf ear to the arguments of specialists of cross-border fund management and opted for the full passport. The UCITS IV Directive was scheduled to be approved by the European Parliament early in 2009.

Ongoing projects

The most important ongoing projects comprise the UCITS IV package of amendments, the two European Parliament reports on hedge funds and private equity, and the European Commission position on MiFID article 65 (the revision of pre- and post-trade transparency obligations for instruments other than shares).

Concerning UCITS IV, 2008 was a year of negotiation to solve basically one issue: the organisation of the man-agement company passport and the supervision of fund activities. There was a clash of two approaches: the one supported inter alia by Luxembourg is that of the partial passport; the other, which is strongly defended by large EU countries, is the full passport. The evolution of the dossier took place in three phases. At first, internal discus-sions were held at the European Commission level until July. Then, a draft regulation was presented together with a mandate to CESR (Commission of European Securities Regulators) to advise on how to solve the management company passport and supervision. In a third and final stage, the European Council (under French presidency) forced a “compromise” practically at the same time that CESR issued its advice. Together with other associations, the ABBL tried to warn regulators against an unbalanced trade-off between good supervision and the hoped-for

If one were able to set aside the financial turmoil that was spreading throughout the year, 2008 could have been considered a calm year from a financial market regulation perspective; especially since the launch of the Financial Service Action Plan and its 42 regulatory measures that concluded the EU-wide implementation of the Markets in Financial Instruments Directive (MiFID) already saw comple-tion in 2007.

However, such a perspective does not take into account all the work undertaken in the implementation of MiFID, up to and ever since 1 November 2007. Here, it is fitting to once more underline the fact that MiFID has not only become a well-established success, but also that the financial industry has managed to implement such a huge package of legislation in such a short time. Moreover, the afore-mentioned perspective does not fully take into account the magnitude of the ongoing discussions at European level on financial regulation projects that have marked the past year, and therefore constituted substantial areas of work for the ABBL. Taking a pragmatic approach, these projects may be classified in three categories: ongoing projects, new ideas and “crisis management issues”.

Financial markets and securities regulation

Partial or full passport for the management company

In simplified terms, a UCITS (Undertaking for Collective Investment in Transferable Securities) is composed of several actors: the fund (the clients’ assets), the depositary bank, the supervisory au-thorities, the asset manager and the management company (MC).

• Under the theory of the partial passport, in order to guarantee an optimal supervision of the clients’ assets, the management com-pany (the fund’s coordinating organ) and the depositary bank shall be in the same mem-ber state as the fund. This solution offers the supervisory authority an easy direct access to the funds/assets. The asset management,

for its part, could be delegated outside the fund’s country.

• The full passport theory, on the other hand, assumes that the focal point is not the fund but the MC, which can delegate the differ-ent functions wherever it pleases and in any member state. Concretely, this would mean having asset management in country A, de-positary in country B, and fund in country C; other functions could be spread elsewhere as well. The fact that the supervisory authority is the one of the MC implies that each member state’s authorities have to coordinate multilat-erally to perform the supervision of the funds’ activities and its assets.

1

1842 Luxembourg joins the German Customs Union (“Zollverein”) and adopts the thaler as currency

1839 First Treaty of London: Luxembourg independence is officially confirmed

11. 10.

European Commission has set up numerous and highly active working groups. Two of the most prominent initiatives are a controversial regulation proposal for rating agencies (issued in the last quarter of the year) and the creation of a pan-European clearinghouse for over-the-counter deriva-tives on credit default swaps, for which the European Commission proposed (in November 2008) a tight schedule of implementation with the aim to be operational by the end of the first quarter of 2009.

“Crisis management issues”

There were actually very few regulatory initiatives sched-uled for 2008, but with the intensification of the financial turmoil and the resulting public and political demands, the situation changed rather drastically. There are now 2 levels of actions. Firstly, on the international level, there are the commitments of various bodies like IOSCO, the FSF, the G20, the Basel Committee, the IIF, the IMF, and the IASB, which have served as focal points for high level regulatory and political initiatives. These initiatives will drive the agenda for the coming months and years in financial regulation, calling for, amongst other things, increased transparency, improved supervisory structures, regulation for financial actors that are currently not regulated, improved financial infrastructures (notably in post-trade), and a deleveraging of financial institutions. Secondly, at European level, the

New ideas

The European Commission opened the way for three new areas of potential regulation:

n the creation of a pan-European regime for private invest-ment (mostly for collective investment vehicles)

n a study on the need to create a European framework for open-ended real estate funds

n and the most controversial issue: the “substitute products call for evidence”

In this latter project, the European Commission assumes that retail investment schemes are perfectly substitut-able. For example, a fund or a structured product delivers the same benefits to a retail investor as a unit linked life insurance and vice versa. They should therefore require the same regulation, whatever the intermediary or prod-uct. With the MiFID as a clear benchmark, no need to specify that this idea is strongly contested. The European Commission is scheduled to deliver a white paper on the issue early in 2009.

2008 also saw the European Parliament issue two reports on hedge fund and private equity, and their interactions with the economy and their impact on regulation. After a rather alarming start, yet thanks to the efforts of all stakeholders, including the ABBL, the outcome of the two reports can now be regarded as being pragmatic. They ask for a review of regulations where it was deemed most appropriate, i.e. risk management (credit arranged with banks) and trans-parency directive (in line with the review of the directive, the report asked for a lowering of the disclosure of the holding threshold from 5% to 3%). In these reports, both hedge funds and private equity funds are no longer considered as an ideal de facto scapegoat for apparent financial regulation failures or the financial turmoil. Moreover, positive aspects were also given some consideration, such as the fact that such funds are providers of credit to small and medium companies.

Draft regulation of credit rating agencies

The draft regulation requires that agencies are registered in the EU, and that ratings used for supervisory purposes can only be those issued by registered agencies. The draft also proposes to introduce organisational ar-rangements to prevent conflicts of interests at agency level, and to improve the quality of ratings. Although the proposal is paved with good intentions, it is, as most rushed regula-tions, likely to become a problem child, the chief reasons being that the major agencies are US based and that some key regulations in the prudential field have given ratings a prominent role.

1856 Establishment of the “Caisse d’Epargne de l’Etat” and “Banque Internationale à Luxembourg” (BIL), the latter on the basis of the inflow of foreign capital

1847 Monetary reform: Luxembourg franc becomes accounting money / the thaler is maintained

13. 12.

Beyond this important project there are also other initiatives that need to be mentioned. Firstly, the Code of Conduct implementation, which is delivering its results, even if a little bit slower than initially expected by the rather optimistic December 2008 ECOFIN conclusions. Then, following a demand by the ECOFIN, CESR and the ECB reworked the draft standards they tentatively issued in 2005, transform-ing them into a less controversial set of recommendations addressed to the supervisory authorities. 2008 was also the year of the “Oxera Survey” for some banks. The former is a study launched by the European Commission on the cost of post-trade. There is, of course, also the ongo-ing project to establish a pan-European clearinghouse for over-the-counter traded derivatives on credit default swaps. Finally, 2008 saw the publication of the second FISCO and Legal Certainty Group report on the tax proce-dure and on the legal barriers to a more efficient functioning of post-trade activities. The ABBL has been very active in all of these dossiers thanks to the help and commitment of the members of its Securities Committee.

For some years now, post-trade has been a field to which the European institutions pay particular attention. They have realised that improving the more glamorous, until 2008 at least, area of front trade (trading rooms, client servicing…) cannnot fully come into its own until the pipes and plumb-ing that support it are working properly. This is why 2008 was once again a year full of activities in the post-trade world.

The Target 2 Securities (T2S) project of the European Central Bank (ECB), scheduled to be in place for 2013, counts among the most important projects. The first part of the year was dedicated to the consultation period on the “User Requirements Documents” (URD for short). The ABBL, together with the Banque Centrale du Luxembourg, coordinated the efforts to analyse and review the 800 and plus page document and to put forth a Luxembourg per-spective. Then, after a review period and the commitment of infrastructures, the ECB Board of Governors officially launched the development phase of the project in mid-July 2008.

Post-trade / Clearing & settlement

ABBL White Paper on T2S

With the help of the contribution of Carlo Matagne, the Chairman of its Securities Committee, the ABBL has determined that Target 2 Securities represents a key project for the financial centre. The ABBL published, in collaboration with Carlo Matagne (BCEE) and Olivier Maréchal (Deloitte), a white paper describing the project and analysing its impacts for Luxembourg’s financial actors. The paper’s findings were corroborated by interviews with key private and public stake-holders. The white paper was presented at a conference in late November and has become the starting point of a strategy to prepare the Luxembourg financial centre for the introduc-tion of T2S.

2

1893 Establishment of the first branch of a foreign bank (Sogenal, France)

1919 Franc becomes sole legal currency / establishment of “Banque Générale du Luxembourg” (BGL), first Belgian bank in Luxembourg

White paperImpact of Target 2 Securities in Luxembourg

15. 14.

On 1 October 2008, the European Commission proposed a revision of the Capital Requirements Directive through co-decision procedure. The new directive aims to update EU rules on capital requirements for banks designed to reinforce the stability of the financial system, reduce risk exposure and improve supervision of banks that operate in more than one EU country. Under the new rules, banks will be restricted from lending beyond a certain limit to any one party, while national supervisory authorities will have a better overview of the activities of cross-border banking groups.

The main changes proposed are as follows:

n Improving the management of large exposures

Banks will be restricted from lending beyond a certain limit (150 million € or 25% of own funds, whichever is higher) to any one party. As a result, in the inter-bank market, banks will not be able to lend or place money with other banks beyond a certain amount, while borrowing banks will ef-fectively be restricted in how much and from whom they can borrow.

n Improving supervision of cross-border banking groups

Colleges of supervisors will be established for banking groups that operate in multiple EU countries. The rights and responsibilities of the respective national supervisory authorities will be made clearer and their cooperation will become more effective.

In order to draw lasting lessons from the financial crisis, the European Commission set up, in November 2008, the independent High Level Group on Financial Supervision chaired by Jacques de Larosière. The group will make recommendations to the Commission on strengthening European supervisory arrangements covering all financial sectors, with the objective of establishing a more efficient, integrated and sustainable European system of supervi-sion and also of reinforcing cooperation between European supervisors and their international counterparts. The group will present a report to the European Commission in view of the European Council of Spring 2009.

As requested by the ECOFIN Council of 14 May 2008, the European Commission is currently preparing a White Paper on early Intervention to deal with ailing banks as a means of enhancing crisis handling. The main focus of the White Paper will be on assessing the current range of crisis prevention / resolution / stabilisation tools available to au-thorities and should be complemented by additional tools. Publication is expected for mid 2009.

n Improving the quality of banks’ capital

There will be clear EU-wide criteria for assessing whether ‘hybrid’ capital, i.e. including both equity and debt, is eligi-ble to be counted as part of a bank’s overall capital – the amount of which determines how much the bank can lend.

n Improving liquidity risk management

For banking groups that operate in multiple EU countries, their liquidity risk management – i.e. how they fund their operations on a day-to-day basis – will also be discussed and coordinated within colleges of supervisors. These pro-visions reflect the on-going work at the Basel Committee on Banking Supervision and the Committee of European Banking Supervisors (CEBS).

n Improving risk management for securitised products

Rules on securitised debt – the repayment of which de-pends on the performance of a dedicated pool of loans – will be tightened. Firms (known as originators) that re-pack-age loans into tradable securities will be required to retain some risk exposure to these securities, while firms that in-vest in the securities will be allowed to make their decisions only after conducting comprehensive due diligence. If they fail to do so, they will be subject to heavy capital penalties.

The EU Council has reached a compromise on the Commission’s proposal, which is currently being examined by the European Parliament. The vote on the directive is expected in early April 2009.

Banking supervision3

1927 Establishment of the Luxembourg Stock Exchange (Bourse de Luxembourg)1921 Economic Union with Belgium /

Luxembourg adopts Belgian franc

17. 16. 16.

At the beginning of 2008, the CSSF made the use of the eXended Business Reporting Language (XBRL) manda-tory for both COREP (Common solvency ratio Reporting) and FINREP (Financial Reporting) reportings. During 2008, banks in Luxembourg, assisted by the ABBL and by XBRL Luxembourg, succeeded in migrating to this new standard on schedule, while delivering high quality data as requested by the CSSF. The knowledge and experience acquired as well as the XBRL solutions put into place by banks dur-ing this project will ease the future burden of the expected increase in data to be reported to supervisors and other authorities.

On 13 October 2008, the IASB adopted amendments of IAS 39 “Financial Instruments: Recognition and Measurement” and of IFRS 7 “Financial Instruments: Disclosures”.

The amendments to IAS 39 introduce the possibility of re-classifications for companies applying International Financial Reporting Standards (IFRS), which were already permit-ted under US Generally Accepted Accounting Principles (GAAP) in rare circumstances. The amendments to IFRS 7

XBRL

Having been successfully launched on 28 January 2008, the SEPA project is celebrating its first birthday in 2009.

As a quick reminder, in January 2008, over 4300 banks in 31 countries, representing roughly 95 percent of pay-ment volume in Europe, took a historical first step towards the established of a Single Euro Payments Area (SEPA) by launching the SEPA Credit Transfer Scheme (SCT) for euro payments.

In Luxembourg, more than 50 banks have now adhered to the scheme as direct members as well as indirect mem-bers of one of the SEPA compliant Clearing and Settlement Mechanisms (CSM).

Yet, after 12 months of operations, a mere 1.5% of the credit transfer operations are SEPA compliant in Europe.

Despite of this slow uptake, Luxembourg is very well po-sitioned as model student, with an average of 30% of the SEPA “EBA Clearing” traffic.

One of the most important features of the new credit transfer instrument, was the common use of IBAN and BIC as single account identifier in the SEPA space. Contrary to many other SEPA countries, Luxembourg customers have been accustomed to using such IBAN and BIC codes ever since 2002.

SEPA: The first yearEvolution of the IFRS

introduce additional disclosure requirements linked to these reclassifications in order to ensure full transparency for us-ers of financial statements.

The IASB’s approach fully achieves the objectives set out by the ECOFIN Council of 7 October, i.e. to place EU com-panies at the same level as their competitors as far as re-porting rules are concerned. The amendments were made applicable as of the third quarter of 2008, as requested by the ECOFIN.

The ABBL, as a founding member of XBRL Luxembourg, fully supported the creation of XBRL Europe, whose mis-sion is the promotion and harmonization of the use of XBRL in pan-European projects, and to be the European institu-tions’ interlocutor. Different working groups are already focusing on the harmonisation of the COREP/FINREP report-ings, which will ease the burden of multinational groups.

4 6

5

1939 Establishment of the ABBL by the following banks:

Banque Commerciale Banque Générale de Luxembourg Banque Internationale à Luxembourg Crédit Anversois Crédit Industriel d’Alsace et de Lorraine Crédit Lyonais Alfred Levy & Cie. La Luxembourgeoise Société Générale Alsacienne de Banque Union Financière Luxembourgeoise

1939 Joined the ABBL (only current members)

BGL Dexia Banque Internationale à Luxembourg Société Générale Bank & Trust

1929 Law on holding companies (Holding 29) / First quotation on the Luxembourg Stock Exchange

1934 Creation of a special authorisation for the profession of banker

ABBL Founding Convention

19. 18.

That is the reason why the ABBL organized in 2008 various seminars and “ABBL meets members” in order to inform on the impacts of SEPA and of the Payment Services Directive (PSD). The ABBL will continue doing so during 2009.

During 2008, the ABBL actively took part in discussions relative to the “SEPA Direct Debit Scheme” (SDD) at EPC level.

The rulebook for this particular scheme is now available, but needs some enhancements regarding the adherence process and the e-mandate feature.

Concomitantly, the Luxembourg banking community began discussions on the implementation of an SDD scheme at national level.

The ABBL, which acts as the “National Adherence Support Organization (NASO)”, has started preparatory work for the SDD adherence process at EPC level.

The SEPA project, coordinated in Luxembourg by the ABBL, was initiated by the European banking industry back in 2002 with a self-regulatory approach.

In this context, the decision taking bodies of the EPC (European Payments Council) have defined the technical standards required to build the new European Payment Systems.

The Luxembourg financial sector’s interests are represented by the ABBL and by representatives of its member banks at various levels at the EPC: Plenary, Project Management Forum, SEPA Payment Scheme working group, Legal sup-port group, Standardization support group, Cards working groups and Cash working groups.

What are the next steps ?

SEPA is on track and open for business with its first prod-uct: The SEPA Credit Transfer.

In 2009, banks will continue to adhere to the SCT scheme, with the aim to provide complete coverage for whatever type of customer and wherever their account is held.

At the same time, additional efforts will be necessary to convince customers themselves - in particular the corpo-rate community and public administrations – of the benefits that SEPA holds for them.

Euro Area (13)

Sepa Area (31)

315m Population 504m

17m Corporates 25m

6-7k Banks 9k

11 ACH Schemes 20+

14+ Card Schemes 18+

4-6m POS 6-7m

240k ATMS 339k

50bn Electronic Transactions

73bn

Euro Area

EU 27

EEA

1945 Max Lambert, First ABBL Chairman

Creation of Luxembourg’s first banking supervisory authority, the “Commissariat aux banques”, Pierre Werner becomes its first Commissioner

1940 Luxembourg falls under German occu-pation / “Caisse d’Epargne de l’Etat” is liquidated, BIL and BGL are taken over by German banks / the ABBL suspends its activities

1944 German occupation ends / the ABBL resumes its activities

Different Country Implementation

• National | Local solutions• Different schemes, experiences,

standards,consumer protection laws• Different country implementations• No interoperability of national schemes• Cross-border complexity and risk

Harmonised SEPA

• Common solutions with additional optional services

• Common core payment instruments and experiences, consistent standards, application of harmonised consumer protection laws

• Improved interoperability• Harmonisation and consolidation• Reduced complexity, improved efficiency

Today

Tomorrow

Source: EPC

ACH: Automated Clearing HousePOS: Post OfficesATMS: Automatic Telling Machines

21. 20.

During 2008, the forthcoming transposition of the Payment Services Directive (PSD) has been a major dossier for the ABBL’s Banking and Finance Department. A working group reporting to the Payments, Information Systems & Standardisation Committee has been closely following the work done by an expert group put together by the Ministry of Finance. Several ABBL representatives participated in the reading of the initial text proposals elaborated by the Ministry, and a first opinion paper was issued during the consultation process starting in August 2008.

During 2008, the ABBL contributed, together with the EBF and under the chairmanship of the European Banking Industry Committee (EBIC), to the definition of the future basic principles on bank account switching that are to be implemented by banks in the member states by 1 Novem-ber 2009.

These principles were also discussed at the December ECOFIN meeting and made public by the European Com-mission, as well as by consumer and industry representa-tive bodies.

The Payment Services Directive (PSD)

Bank account switching

Another year has passed, and once more we witnessed the emergence of many new and varied security issues in the world of the web.

There were numerous incidents and reports this year, all over the world as well as in Luxembourg, that bore witness to the increasing professionalism of cyber-criminals and their sophisticated methods of attack (Trojan horses, phish-ing, pharming, DoS, Botnet, …), in particular on e-banking applications.

In order to deal with these issues related to internet security in an effective, efficient and coordinated manner, the ABBL set up a specific working group on “ICT Security” in 2007.

The first objective of this working group is to react and act quickly in urgent situations. This is why the group is study-ing the implementation of a Local Emergency Response Structure responsible for the financial sector. The future structure will work in close cooperation with public emer-gency response infrastructures.

Particularly in the banking sector, the importance of building secure software systems and using best practices and se-curity standardisation has been proven. While banks need to constantly improve both user and transaction authentica-tion technologies, clients should do their utmost to reduce the vulnerability of their computers.

In this area, the ABBL welcomed the decision of banks to migrate their authentications technologies. While some of them used parent company groupware technologies, others chose the applications that have now been made available by LuxTrust.

Finally, banks need to educate both their clients and their staff on the dangers involved in online banking and, impor-tantly, need to promote security reflexes.

In this respect, the ABBL continues to collaborate with CASES (Cyberworld Awareness and Security Enhancement Structure) of the Ministry of Economy on prevention cam-paigns that highlight the predominantly human nature of security weak.

The ABBL also took an active role in the development of publications by the Information Security Support Group (ISSG) of the EPC on subjects such as “Customer-to-bank security threat assessment” and “Customer-to-Bank Security Good Practices Guide”, amongst others.

Lastly, the ABBL joined the “IT Fraud working group”, a new working group set up by the EBF. This working group mainly focuses on the sharing of information and best practices between members. It also makes proposals and comments with regards to EU legislative initiatives on e-channels and IT fraud prevention, and cooperates with law enforcement (Europol, Interpol).

ICT Security

The ABBL also took an active part in the PSD Implementation Expert Group set up by the European Banking Federation with EACB and ESBG involvement. This expert group had an extensive dialogue with the European Commission throughout 2008 in order to clarify open points and guarantee compliance of the banking industry with the future laws entering into force in the 27 EU Member states as well as in the 3 EEA countries on 1 November 2009. At the end of 2008, an increasing number of member states disclosed their law proposals, allowing the Expert Group to assess the degree of harmonisation reached and to begin compiling an industry guide.

At the end of 2008, the ABBL’s Retail Banking Group deci-ded to constitute an ad hoc working group which will have to define the bank switching framework to be put in place in Luxembourg, as well as strategies on how to communi-cate on this consumer related issue.

7

8

9

1947 Ratification of the Benelux treaty / the ABBL organises its first training courses for bank personnel

1957 Treaty of Rome: establishment of the European Economic Community, establishing free movement of capital, goods & persons

1946 Joined the ABBL

Banque de Luxembourg

1948 Carlo Turk ABBL Chairman

1953 Jean d’Huart ABBL Chairman

23. 22.

The European Savings Directive1 0

According to Article 18 of the European Savings Directive (Directive 2003/48/EC), the European Commission is due to report to the Council on the operation of the directive every three years and to propose amendments that may be required. Thus, on 15 September 2008, a bit more than three years after the Savings Directive entered into force, the Commission, as requested by the ECOFIN of May 2008, issued its first report on the basis of informal con-sultations with tax authorities and market operators. As far as the transposition and implementation of the directive by members states is concerned the report found no major problems. In its economic evaluation, the Commission identified no major changes in the composition of savings incomes, nor did it identify an abandonment of products covered by the directive.

For countries having opted for the withholding tax regime, total interest payments amounted to about 4.5 billion € in 2006. As far as the automatic exchange of information is concerned, the Commission found that the data provided by member states and other jurisdictions covered con-tained “a critical number of missing values”. Thus, the total amount of interest payments made, for which information was exchanged, does not correspond to any amount of tax collected, given that tax regimes within member states dif-fer from each other. Indeed, there seems to be no evidence of the efficiency of the automatic exchange of information. Neither does the report provide an answer to whether the

automatic exchange of information provides any efficiency at all. However, according to Article 18, the Commission should have done precisely that: compare the efficiency of the automatic exchange of information system with the withholding tax system. Moreover, as clear proof of the ef-ficiency of a withholding tax system, the Commission need only have taken into account the fact that 19 out of 27 member states are now applying a withholding tax system domestically.

Strangely enough, even though Article 18 of the directive states that “on the basis of these reports, the Commission shall, where appropriate, propose to the Council any amendments …”, the Commission decided to elaborate the evaluation report and the proposals to improve the direc-tive in parallel. Thus, the Commission adopted amending proposals to the Savings Directive on 13 November 2008. Besides other refinements, these proposals cover three main areas:

1. Beneficial ownership

2. Definition of paying agent

3. Income included in the scope of the directive

1. For the ABBL, the confusion by the authors of the proposal of the terms “beneficial owner” and “tax payer” will lead to deteriorating customer relations. The European definition of the person who is a beneficial owner (as de-fined under the AML directives) does not match the various national definitions of “tax payer”. Besides being com-mon sense, it also makes sense, in terms of national tax laws, that the tax payer is the person who has received an income. It is also this person that has to file the tax return for the income in question. However, the beneficial owner, as identified besides the account holder according to AML directives, is in principle neither a customer of the bank, nor its creditor. For both systems, withholding tax and auto-matic exchange of information, this confusion of terms will carry the risk of double taxations, since persons who did not receive any income will be taxed, while persons who received an income should not be taxed. Tax administra-tions and investors will engage in interminable discussions on who has to finally pay taxes on a particular income.

2. The ABBL supports the European Banking Federation’s position that the concept of paying agent “upon receipt” does not work, and therefore does not agree with the Commission proposal to extend the scope of this concept.

3. Concerning the Commission’s proposal to extend the scope of income that is included, the ABBL believes that in the case of structured products, the term “innovative

financial product” is so meaningless as to be useless. Understanding the criterion of a “return ex ante” to mean that a return is fixed at issuance of the paper and that the customer exactly knows the return he will receive, notwith-standing interest rate changes as a result of market fluctua-tion, the ABBL agrees to the proposal, as the return can effectively be assimilated to an interest payment. Indeed, Luxembourg banks already apply the directive to the prod-ucts that should fall under the scope of the directive in the future. In terms of investment funds, it is important that the definition of investment fund should be kept large enough to include all collective investment vehicles established outside the EU.

Finally, the ABBL is convinced that a generalisation of the withholding tax system throughout Europe is the most ef-fective solution to make sure that countries can collect tax from their residents investing in other European countries. Once the withholding tax rate is increased to 35% in 2011 according to the directive, those countries that have opted for the withholding tax system will be clearly put in a com-petitive disadvantage.

1960 The ABBL together with other banking associations in Europe establish the European Banking Federation (EBF)

1959 Jean-Jacques Welbes ABBL Chairman

1962 Law defining the prerequisite conditions for access to the profession of banker

1961 Joined the ABBL

KBL European Private Bankers

25. 24.

n the FIU Circular 20/08 of 12 November 2008 on coopera-tion with the authorities

n the CSSF Circular 08/387 of 19 December 2008 on the fight against money laundering and terrorist financing

The new predicate offences of money laundering

Article 506-1 of the Penal Code contains a list of offences the proceeds of which may be considered to be the basis for money laundering and terrorist financing (predicate of-fences). The “first” law of 17 July 2008 has extended this list to encompass new offences, such as the counterfeit-ing and falsification of coins and banknotes, the use and disclosure of trade secrets or manufacturing secrets, theft without violence, bankruptcy, breach of trust, fraud and embezzlement, insider dealing and market manipulation, etc.

The list is also extended to include any other offences punishable by deprivation of liberty or a detention order for a minimum of more than six months. As a consequence, murder and serious bodily harm, kidnapping, illegal confine-ment and hostage taking, theft, extortion, forgery, piracy, are henceforth also primary offences under the terms of the Penal code. Forgery of company accounts and abuse of company assets are also primary offences. It should

In 2008, two laws, a grand-ducal regulation, and two circu-lars on money laundering were published:

n the “first” law of 17 July 2008 on the fight against money laundering and terrorist financing, is a criminal law. It aims to extend the list of predicate offences in money laundering

n the “second” law of 17 July 2008 transposes two European directives into the Luxembourg law of 12 November 2004: Directive 2005/60/EC of the European Parliament and the Council of 26 October 2005 on the prevention of the use the financial system for the purpose of money laundering and terrorist financing, also known as “Third Directive”; as well as Directive 2005/70/EC of the Commission of 1 August 2006 laying down imple-menting measures for Directive 2005/60/EC as regards the definition of “politically exposed person” and the technical criteria for simplified customer due diligence procedures and for exemption on grounds of a financial activity conducted on an occasional or very limited basis. This law defines the obligations of customer due diligence that professionals must respect

n a Grand-Ducal regulation of 29 July 2008 established the list of third countries considered as having equivalent obligations in terms of the fight against money laundering and terrorist financing

The fight against money laundering: Recent developments

be noted that “fraud” only concerns offences in the Penal Code, which excludes tax fraud. Tax fraud as such (“es-croquerie fiscale”) is not included in the list of predicate offences of money laundering, since it is punishable by a minimum detention of one month only. However, it is to be stressed that the perpetration of this infringement generally presupposes that other criminal acts have been committed, in particular forgeries, which are primary offences of money laundering.

The new law requires the professional to file a declara-tion of suspicion with the State Prosecutor’s Office when it knows, suspects, or has good reasons to suspect the possibility that money laundering or terrorist financing took place, or was attempted, in particular due to the person concerned, his/her evolution, the origin of the assets, and the nature, the finality or the methods of the operation. There is no obligation for the professional to actively search for evidence of money laundering, neither to determine if those are sufficiently conclusive to be used as a base for an investigation, neither to qualify the facts, nor to prove their exactitude. This task is the responsibility of the competent legal authorities.

New professional obligations

The “second law” redefines the professional obligations and introduces a risk-based approach. The risk-based

approach must take into account the probability of certain risks occurring. All professionals must adopt their own risk-based approach, and they must each analyse their situa-tion by applying reasonable judgments on their business relations, in accordance with their type of business relation-ships, their customers, the services and products they offer and the countries with which they have dealings.

Professionals must apply customer due diligence measures when establishing a business relationship; when carry-ing out occasional transactions amounting to 15 000 € or more, whether the transaction is carried out in a single op-eration or in several operations which appear to be linked; when there is suspicion of money laundering or terrorist financing, regardless of any applicable derogation, exemp-tion or threshold; when there are doubts about the veracity or adequacy of previously obtained customer identifica-tion data. Customer due diligence measures include the identification of the customer and of the beneficial owner (a more precise definition of beneficial owner is provided), obtaining information on the business relationship, and con-stant monitoring of the business relationship (transactions, source of funds, updating data). Professionals are allowed to adapt the extent of such measures on a risk-sensitive basis depending on the type of customer, business rela-tionship, product or transaction. However, this increased freedom to evaluate the extent of obligations also implies an increased responsibility in relation to the decision taken

1 1

1965 Law on Soparfi / the titles bank and ban-ker become protected by Grand Ducal Decree

1966 Fuji Bank becomes the first Japanese bank in Luxembourg

1964 Jean d’Huart ABBL Chairman

1963 The first eurobond is launched in Luxembourg, deno-minated in euro-dollars / first quotation of eurobonds on the Luxembourg Stock Exchange

27. 26.

by professionals; indeed, they must be able to demonstrate that the extent of the measures is appropriate in relation to the risks of money laundering and terrorist financing.

Professionals may apply simplified customer due diligence with regards to:

n certain clients (financial institutions, listed companies whose securities are admitted to trading on a regulated market, beneficial owners of pooled accounts held by notaries or other legal professionals, Luxembourg public authorities, public authorities representing a low risk of money laundering, in particular European institutions)

n certain products or transactions (life insurance policies in respect of certain conditions, other products or trans-actions representing a low risk of money laundering in respect of technical criteria)

When professionals apply simplified customer due diligence measures, they must gather sufficient information to estab-lish whether the customer fulfils the necessary criteria to qualify for the exemption.

Professionals must perform enhanced customer due diligence measures in situations, which by their nature can present a higher risk of money laundering or terrorist financ-ing, in particular:

n when customers are not physically present for the identification

n in cross-border correspondent banking relationships with respondent institutions from third countries

n in transactions or business relationships with politically exposed persons. The law provides a definition of “politi-cally exposed persons”, that is “natural persons who are or have been entrusted with prominent public functions and immediate family members, or persons known to be close associates, of such persons”. This does not cover the persons residing in Luxembourg, nor the people who no longer occupy a prominent public function since more than a year

The law allows professionals to rely on third parties to per-form customer due diligence measures. The law introduces more flexibility, since “third parties” can henceforth be credit institutions, financial institutions, auditors, notaries, lawyers, in Luxembourg or in other Member States. The notion of “third parties” also includes the same professionals in third countries provided they fulfil certain conditions (mandatory professional registration, customer due diligence require-ments and record keeping requirements equivalent to those laid down in Directive 2005/60/CE).

The Grand-Ducal regulation of 29 July 2008 establishes a list of 16 third countries considered as having equivalent obligations with regards to the fight against money laun-dering and terrorist financing. In addition, institutions can delegate the implementation of due diligence measures to any other entity on a contractual basis in the context of outsourcing contracts. In each case, final responsibility for meeting those obligations still falls to professionals who rely on third parties. Appropriate copies of identification and verification data and any other relevant documentation re-garding the identity of the customer or the beneficial owner shall immediately be forwarded, on request, by the third party to the professional to whom the customer refers.

Finally, the law strengthens the obligation to cooperate with the authorities to which professionals are subject. In par-ticular, professionals, theirs directors and employees must promptly inform the Luxembourg authorities responsible for combating money laundering and terrorist financing when they suspect or have reasonable grounds to suspect that money laundering or terrorist financing is being or has been committed or attempted.

1968 The ABBL negotiates its first collective employment agreement for the banking sector / Discount Bank & Trust Company is the first Israeli bank to establish itself in Luxembourg

1969 Jean-Jacques Welbes ABBL Chairman

Wells Fargo Bank and Bank of America become the first US banks in Luxembourg

1968 Joined the ABBL

BNP Paribas Luxembourg1969 Joined the ABBL

Commerzbank International Crédit Agricole Luxembourg Private Bank

1967 Dresdner Bank becomes the first German bank to establish itself in Luxembourg / Uniao de Bancos Portugueses is the first Portuguese bank in Luxembourg

29. 28.

In October 2008, the ABBL published a document on the implementation of the data protection legislation, dealing with the specific aspects of surveillance at the workplace. This document summarises the proceedings of the ABBL Data Protection Working Group.

The law of 2 August 2002 on the protection of persons with regards to the processing of personal data imposed many new obligations on businesses, and their implemen-tation has not always been an easy matter. The purpose of the ABBL document is to analyse the different situations concerning surveillance in credit institutions and to help the latter to comply effectively with their obligations. Some clarifications are also given as to the practical application of the legislation, in particular following the simplification introduced by the law of 27 July 2007.

Credit institutions are governed by the legislation on data protection with respect to all “data processing” effected by them. The different types of processing which are li-able to be performed in a bank relate in particular to: the management of human resources, clients (including the effective beneficiaries and persons who represent the client: mandated agents, heirs, representatives of legal persons), potential clients and all other persons who are liable to be linked legally to the clientele (for example, guarantors), suppliers and intermediaries, public relations and contact

persons, shareholders, subscribers to units in investment funds/UCITS/SICAVs.

Before effecting any processing, the person responsible for such processing must make sure that certain rules are respected, notably in respect of the lawful and legitimate nature of the processing. They must then declare the processing (unless it is exempt from notification) to the National Commission for Data Protection (CNPD) or submit an application for prior authorisation for certain types of processing and make sure that the persons concerned are duly informed. Finally, they must ensure the security of the processed data.

Some types of processing must be authorised by the CNPD before they can be implemented. This applies in par-ticular to the processing for surveillance at the workplace and for other surveillance purposes. A prior authorisation is required for the following processing:

n surveillance of internet use

n surveillance of use of the e-mail system

n recording of telephone conversations to provide proof of transactions and commercial communications

n surveillance by camera at the workplace

It should be noted that, by a single decision of 22 June 2007, the CNPD has authorised access to surveillance systems which permit the management of physical access controls at the entrance to sites and buildings. The CNPD has also authorised the verification of working hours as part of the organisation of work based on flexible working hours, i.e. systems which permit management and verification of working hours and presence times at the workplace.

By reason of the limited scope of application of cases in which processing for surveillance purposes is permitted, the following types of processing cannot be implemented:

Implementation of the data protection legislation

Any processing relating to surveillance at the workplace requires prior information of the employees concerned and of the staff representation bodies.

The fact of putting in place processing without having obtained prior authorisation from the CNPD, of implement-ing processing which is not justified for one of the reasons for which such processing may be held to be legitimate and of failing to inform the persons concerned, renders the employer liable for punishment under criminal law.

1 2

1972 Joined the ABBL

BHF-Bank International Citibank International plc, Luxembourg Branch HVB Banque Luxembourg

1971 Joined the ABBL

Dresdner Bank Luxembourg Banque BCP

1970 Creation of the international clearing company CEDEL (later Clearstream)

1970 Joined the ABBL

Deutsche Bank Luxembourg

n surveillance of employees with a view to verifying whether their conduct is liable to cause the employer to become liable in civil or criminal law

n permanent verification or monitoring of the performance of the members of staff

n processing of judicial data

n recording the telephone exchange of the business

31. 30.

On 12 February 2008, the European Council adopted a directive on the place of supply of services, resulting from the political agreement reached on the VAT package on 4 December 2007. This new legislation introduces major changes for the financial sector.

From 1 January 2010, with the entry into force of Directive 2008/8/EC, the new rules on the place of supply of services will require that business-to-business supplies of services will generally be taxed where the customer is established, rather than where the supplier is located, with certain ex-ceptions such as restaurant and transport services.

The directive introduces changes to recapitulative state-ments which currently deal only with intra-community transactions in goods. As from 1 January 2010, the new directive requires the listing of all supplies of cross-border services (other than exempt services). These recapitula-tive statements, which must include information on the VAT identification number of the B to B counterparties, explanations as to the legal basis for the application of VAT and the total value of the supplies, are transmitted by the tax authorities of the supplier via V.I.E.S. (VAT Information Exchange System) to the tax authorities of the receiver of the service. They will enable VAT administrations to monitor and control information in order to combat VAT fraud.

These new requirements will be burdensome and costly for financial institutions due to the necessary changes to IT systems. Accounting and reporting systems do not seem to be adapted, for the time being, to capture the data in question. In order to meet these new reporting obligations, the new systems will need to differentiate between taxable and exempt supplies, business and non-business clients, include information on the tax treatment of services banks render to businesses established in other member states, etc.

In addition, the European Commission adopted, in November 2008, a proposal in order to combat tax eva-sion connected with intra-community transactions. The new proposal speeds up the collection and exchange of information by reducing to one month both the frequency of recapitulative statements of intra-community transactions and the deadline for the exchange of information between tax administrations.

Created in 2007, the Private Banking Group, Luxembourg (PBGL) held its second Members’ Meeting on 19 June 2008. The PBGL constitutes the first business line cluster of the ABBL, and is composed of high-profile representatives of ABBL members active in the field of private banking.

In order to fulfil its missions, which include preparing the future evolution of private banking in Luxembourg as well as accompanying and promoting its further development, the Executive Board of the PBGL, chaired by Charles Hamer, set up a number of working groups.

Thus, the PBGL created a working group with the objective to obtain reliable statistics on the weight of private banking in Luxembourg. This was achieved with the help of a CSSF questionnaire.

The working group “Promotion” collaborates with Luxembourg for Finance (LFF) in determining target regions and cities for the promotion of Luxembourg private bank-ing abroad. Thus, the Private Banking Group accompanied LFF, amongst others, to China, Germany and Italy.

The cluster’s “Training” working group worked with the IFBL in developing a high-level international training programme in private banking. In this context, the PBGL and the IFBL presented, in January 2009, the Certified International Wealth Manager® diploma, an international qualification

VAT: New reporting obligations for the financial sector Private Banking Group, Luxembourg

which will be awarded by the Association of International Wealth Management (AIWM), Zurich, in cooperation with the ABBL and the IFBL.

In terms of strategy, the Private Banking Group based its work on the PricewaterhouseCoopers study on the re-positioning of Luxembourg private banking by 2015. The corresponding working group has been developing an action plan based on the study’s conclusions.

In 2008, the PBGL also set up a working group dealing with issues relating to the ECOFIN and to the European Savings Directive, a working group dealing with tax reporting with the aim to find a common provider for the tax reporting needs of member banks’ customers, as well as a working group on wealth planning.

Finally, the Private Banking Group also published a brochure on private banking in Luxembourg in 2008.

1 3 1 4

1973 Marcel Schleder ABBL Chairman

Union des Banques Suisses becomes first Swiss bank in Luxem-bourg / Christiania Bank is the first Scandinavian bank to establish itself in Luxembourg / Banco di Napoli International becomes the first Italian bank in Luxembourg / International Trade & Investment Bank is the first Arabic bank to establish itself in Luxembourg

1974 East-West United Bank becomes the first Russian bank in Luxembourg

1974 Joined the ABBL

J.P. Morgan Bank Luxembourg Mizuho Trust & Banking (Luxembourg) Mitsubishi UFJ Global Custody Nikko Bank (Luxembourg) Banque LBLux East-West United Bank

1973 Joined the ABBL

WestLB International M.M. Warburg & CO Luxembourg Norddeutsche Landesbank Luxembourg Hauck & Aufhäuser Banquiers Luxembourg UBS (Luxembourg)

1975 Joined the ABBL

Credem International (Lux)

1975 Georges Arendt ABBL Chairman

33. 32.

In October 2008, the ABBL created a new cluster called Retail Banking Group (RBG), which brings together ABBL members active in the field of retail banking. This cluster follows the launch of a first cluster on private banking in 2007. The RBG’s roles include defining initiatives and ac-tions to be taken in the retail banking profession as well as developing training programmes adapted to the needs of the profession.

In doing so, the Retail Banking Group closely follows the numerous initiatives taken by the European Commission, which is currently analysing the functioning and competi-tiveness of the European market for retail financial services. As a matter of fact, the Commission believes that this market is not entirely integrated yet and that a substantial number of competitive distortions still persist. There cur-rently exist a number of ongoing initiatives, notably in the fields of payments, bank accounts, personal and home loans, and financial literacy.

First and foremost, the Retail Banking Group is dealing with the common principles defined by the European Banking Industry Committee (EBIC) on bank account switching, which should enter into force in EU member states on 1 November 2009.

Retail Banking Group

The principles in question are aimed at helping consumers when transferring their account to another bank within the same member state. Banks will provide their clients with a mobility guide, which will explain the steps that need to be undertaken when switching bank accounts, by whom, and within what time frame. Compliance with these principles is to be controlled by national banking associations. The RBG will work to implement these principles at national level.

Moreover, in the coming months the RBG’s work will focus on the European Commission’s initiative on cross-border access to credit information. With this measure, the Commission plans to simultaneously encourage competi-tion in retail financial services markets as well as protect consumers from over-indebtedness. For this purpose, it has set up an expert group tasked with identifying legal and regulatory obstacles in accessing credit information, analys-ing the functioning of credit registers within the European Union, and presenting propositions aiming to lift the obsta-cles that have been identified. The RBG will attentively and critcially follow the Commission’s work.

Introduction of the single statute

The single statute for all employees in the private sector effectively abolishes the distinction between the definitions of “blue-collar” and “white-collar” workers. As of 1 January 2009, it has been implemented as one of the major reforms of social law in Luxembourg. The ABBL was a member of the employers’ delegation during the entire negotiations at political and administrative levels. The implications of the reform are far-reaching, including for the banking sector, which mainly occupies white collar workers.

The main changes introduced by the single statute can be summarized as follows:

n reduction of the period of continued salary payment for all companies to 13 weeks on average

n introduction of a single contribution rate for benefits in kind at 0.5%

n compulsory membership to the mutual scheme “Mutualité des Employeurs” for companies, thus covering the risks of continuation of salary, and reimbursment up to 80% of the fees

n introduction of a new system for the declaration of sala-ries to the Joint Social Security Centre

n administrative changes as a result of to the merger of the different health insurance schemes into a single National Health Fund and of the pension schemes into a single National Pension Fund

Since the beginning of the negotiations, as well as dur-ing the implementation procedure, the ABBL has been providing an overview on all hot topics under discussion in relation to the singe statute. Several information sessions were organized throughout 2008 in order to give HR staff the opportunity to meet attending experts who clarified dif-ferent aspects of the Law of 13 May 2008 and its practical application.

1 61 5

1976 Joined the ABBL

LBBW Luxembourg DZ Bank International Svenska Handelsbanken

1977 Albert Dondelinger ABBL Chairman

Creation of the public bank “Société Nationale de Crédit et d’Investissement” (SNCI)

1976 Joined the ABBL

Union Bancaire Privée (Luxembourg) Credit Suisse (Luxembourg) Société Européenne de Banque Banque Carnegie Luxembourg Danske Bank International Skandinaviska Enskilda Banken Swedbank

1977 Joined the ABBL

HSBC Trinkaus & Burkhardt (International) Landesbank Berlin International HSH Nordbank Securities

34.

uarantee described above is provided to retroactively take account of the rights accrued in previous years. For all employees in service on 31 December 2007, the first assessmen

35. 34.

Furthermore, the law created a specific title for highly qualified employees for jobs which necessitate special knowledge or competences. This means that in normal circumstances,if a person is considered as highly qualified, the procedure for obtaining the title should be much faster.

The ABBL summarized the main features of the new law in a “Vademecum” that was sent to all its members in autumn 2008.

Social elections in 2008

On 12 November 2008, elections for new personnel del-egates took place in all Luxembourg companies with a staff of more than 15 workers. Social elections for personnel delegates take place every 5 years.

In view of these elections, the ABBL, together with other employers’ organisations, compiled and translated the ap-plicable legislation into English and German, and a CD-Rom with this information was distributed to all members of the ABBL. Parallel to this, a web page was launched featuring the relevant timetable, frequently asked questions and the necessary forms.

Finally, the ABBL invited its members to three conferences, in French, English and German, with a speaker from the Inspection du Travail et des Mines who provided a precise outline of the applicable procedure and who remained at the disposal of the members of the ABBL for any queries they had in relation to the staff delegate elections.

On 9 July 2008, the Luxembourg Parliament passed a long awaited new legislation on immigration, which promises simpler and faster procedures. This law came into force in October 2008.

Concerning EU citizens and citizens from assimilated coun-tries, the new law abolishes the former declaration of arrival for EU citizens, as well as their obligation to hold a staying permit (carte de séjour). EU citizens and members of their family gain the permanent right to stay after an uninter-rupted stay of 5 years in Luxembourg.

Concerning non-EU citizens, the legislator was sensitive to several proposals made by the ABBL.

As a matter of fact, the former categories of work permits (A, B, C, D) as well as the staying autorisation (autorisa-

tion de séjour) delivered by the local authorities have been abolished and replaced by one single title which indicates the type of authorisation that was granted to the person in question.

Freedom of movement of persons & Immigration1 7 1 8

1979 Georges Arendt ABBL Chairman

Bank of China establishes itself in Luxembourg

1981 Marcel Schleder ABBL Chairman

Law introducing the coordination of banking regulation on the basis of the 1st European Banking Directive / Banco mercantile de Sâo Paulo is the first Brazilian bank to establish itself in Luxembourg

1980 Joined the ABBL

IKB International BSI S.A., Luxembourg Branch Banque Hapoalim (Luxembourg)

1981 Joined the ABBL

Sanpaolo Bank

1979 Joined the ABBL

Bank of China (Luxembourg)

Result for the financial sector

Chamber of employees - Seat distribution

ALEBA

OGBL-L-SBA

FleDEL

LCGB-SESF

OGBL

LCGB

FNCTTFEL

SYPROLUX

ALEBA

5

1

36

2

16

52.36%

17.27%27.37%

3%

37. 36.

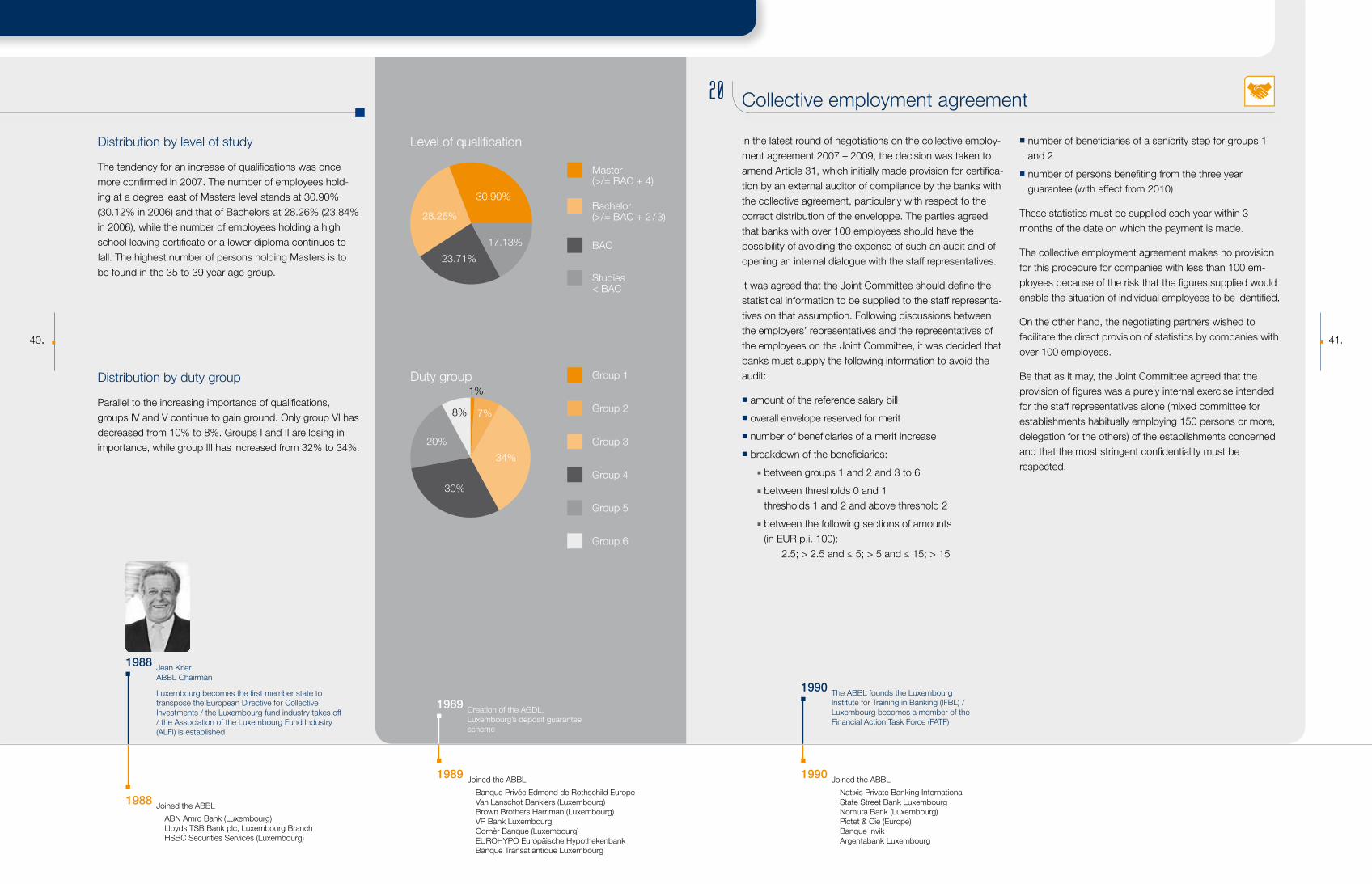

In 2008, the ABBL once more updated its annual study on the social situation in the banking sector, processing the most indicative data from the year 2007.

It is worth noting that the study was a considerable suc-cess in 2007. The level of participation has significantly increased, from 51.3% to 61.7%, thus covering 93.6% of our members’ employees compared with 79.1% in 2006.

The percentage of executive staff continues to increase and has currently reached 32.91%, while the rate of employees falling under the collective employment agreement keeps decreasing; in 2007, the latter represented 66.74% of the workforce.

Average length of service dropped from 7.9 to 7.39 years for men and from 9.4 to 8.11 years for women. The study concludes that the average age of employees has only marginally changed, amounting to 38.9 years of age for men (38.7 in 2006) and 37.0 for women (37.1 in 2006).

As to new recruitments, indefinite contracts now represent 81.31%, while only 18.69% of contracts were concluded on a fixed term basis.

Interim contracts declined from 3.08% in 2006 to 2.51% in 2007.

With 36.09% in 2007, Luxembourg residents continue to be the most represented population in terms of new recruits. New recruits from France have lost a little ground (from 32.55% to 30.53%), followed by Belgians (16.52%) and Germans (14.73%).

Survey on the social situation in the banking sector

21.0

8%15

.01%

10.4

0%6.

12%

15.1

5%15

.38%

1.40

% |

0.73

%

0 10

20

30

40

8.05

%6.

68%

OTHE

R

FRAN

CE

BELG

IUM

GERM

ANY

LUXE

MBO

URG

1 9

Place of residence of new recruits

Men

Women

1983 Establishment of the Luxembourg Monetary Institute (IML), taking over the responsibilities of the Commissioner for the Control of Banks

1984 Remy Kremer ABBL Chairman

The supervision of the financial sector is reorganised

1984 Joined the ABBL

Banque de Commerce et de Placements, Luxembourg Branch

1982 Law granting the Commissioner for the Control of Banks the right to suspend activities

1982 Joined the ABBL

Banco Bradesco Luxembourg Banco Popolare Luxembourg Nordea Bank Clearstream Banking

39. 38.

As to the country of origin of employees, there has been very little variation. There has only been a slight increase in the number of German, Luxembourg and French residents, while the number of Belgian residents has dropped slightly.