Embed Size (px)

Citation preview

AARP CA-2 Instructor Training

December 2016

Thank you!

You Make a Difference!

Training Materials

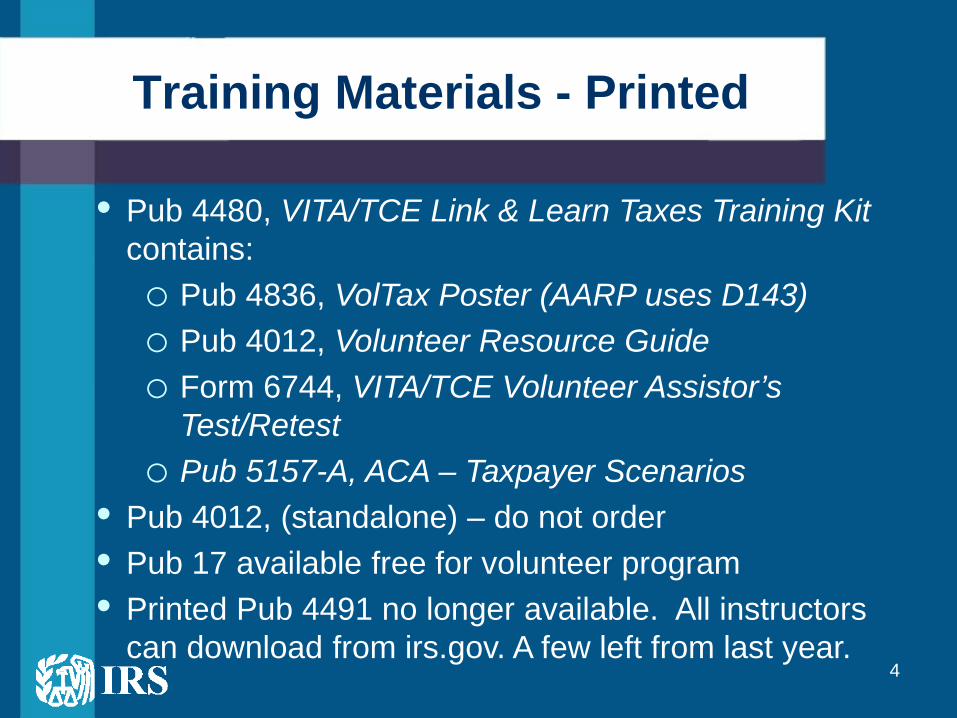

Training Materials - Printed

4

• Pub 4480, VITA/TCE Link & Learn Taxes Training Kit contains: o Pub 4836, VolTax Poster (AARP uses D143) o Pub 4012, Volunteer Resource Guide o Form 6744, VITA/TCE Volunteer Assistor’s

Test/Retest o Pub 5157-A, ACA – Taxpayer Scenarios

• Pub 4012, (standalone) – do not order • Pub 17 available free for volunteer program • Printed Pub 4491 no longer available. All instructors

can download from irs.gov. A few left from last year.

5

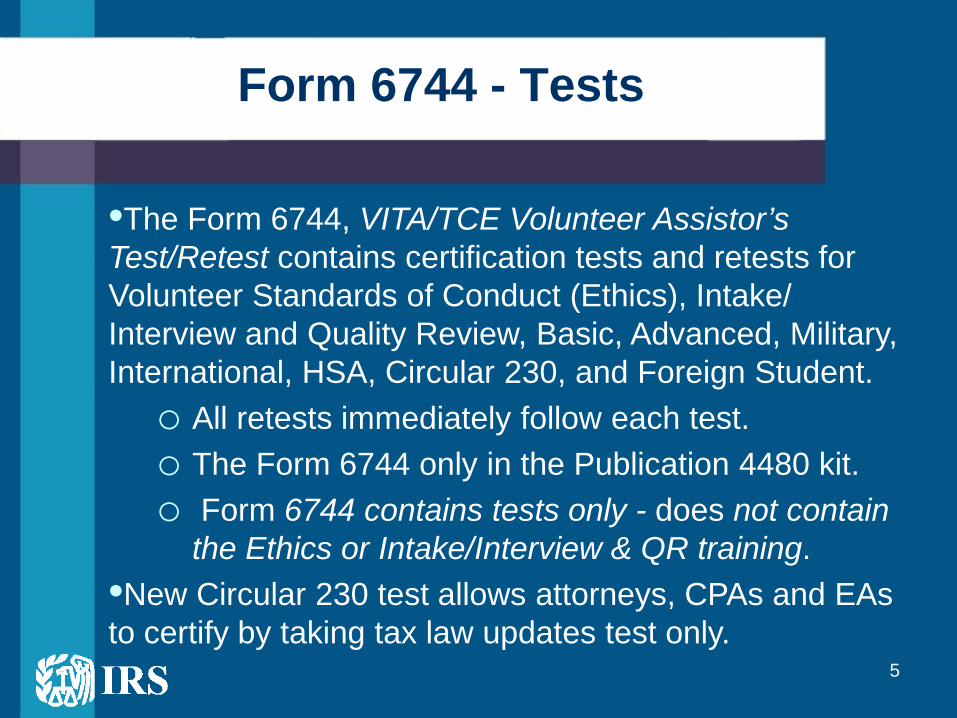

•The Form 6744, VITA/TCE Volunteer Assistor’s Test/Retest contains certification tests and retests for Volunteer Standards of Conduct (Ethics), Intake/ Interview and Quality Review, Basic, Advanced, Military, International, HSA, Circular 230, and Foreign Student. o All retests immediately follow each test. o The Form 6744 only in the Publication 4480 kit. o Form 6744 contains tests only - does not contain

the Ethics or Intake/Interview & QR training. •New Circular 230 test allows attorneys, CPAs and EAs to certify by taking tax law updates test only.

Form 6744 - Tests

Other Training Materials

6

• Publication 4961, VITA/TCE Volunteer Standards of Conduct - Ethics Training. Available on Link & Learn.

• Publication 5101, Intake/Interview and Quality Review Training. Available on Link & Learn. Material should be included in AARP training.

• Publication 4942, Health Savings Accounts (electronic) • Link and Learn Taxes and the Practice Lab are

available. • Shipments of printed training materials, except for

Pub. 17, should be complete.

Other Training Materials

7

• Publication 4491-A, VITA/TCE Training Guide Consolidated Changes – new publication lists all updates to Pub. 4491

• Publication 4491-X (electronic) will contain any corrections to the training publications or updates to tax law made after December.

• Publication 4491-W, VITA/TCE Problems and Exercises,(electronic only).

• Go to VITA/TCE Central on Link & Learn for additional instructor resources.

Protecting Americans from Tax Hikes Act of 2015

(PATH Act)

9

PATH Act Legislation Changes

• Earned Income Tax Credit (EITC) expanded modifications made permanent

• Additional Child Tax Credit (ACTC) - the reduced earned income threshold for CTC made permanent at $3,000

• American Opportunity Tax Credit (AOTC) made permanent oEmployer Identification Number (EIN) of educational

institution required for taxpayers claiming the AOTC oEducational institutions required to report tuition &

expenses actually paid on Form 1098-T (2016-no penalty)

• 2015 law requires 1098-T to take education credits/deduction

10

PATH Act Legislation Changes

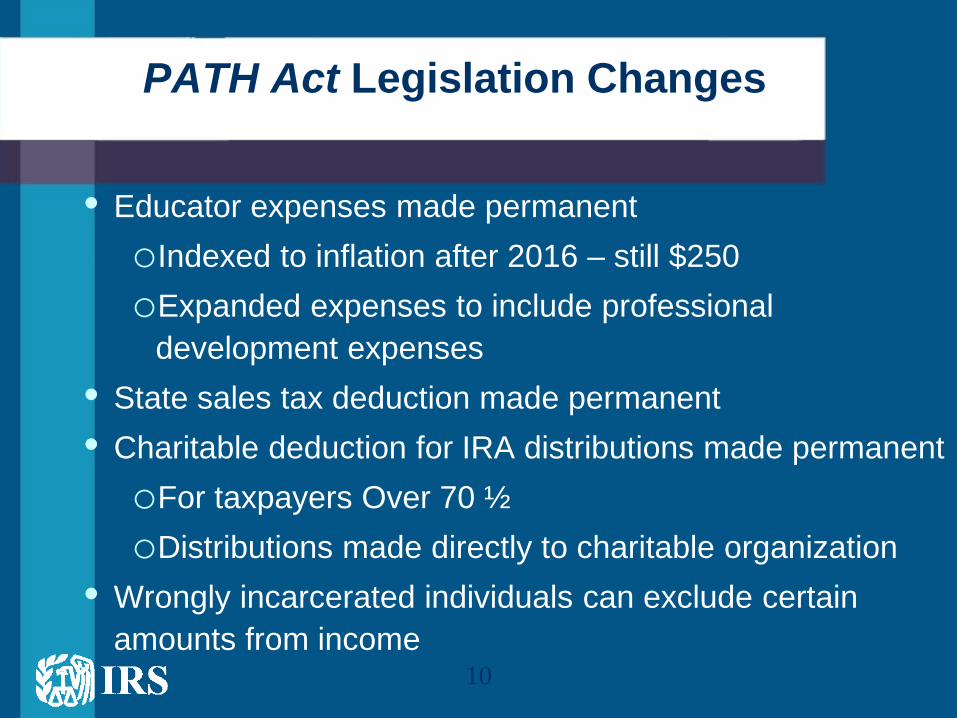

• Educator expenses made permanent oIndexed to inflation after 2016 – still $250 oExpanded expenses to include professional

development expenses • State sales tax deduction made permanent • Charitable deduction for IRA distributions made permanent oFor taxpayers Over 70 ½ oDistributions made directly to charitable organization

• Wrongly incarcerated individuals can exclude certain amounts from income

11

PATH Act Legislation Changes

Extended through 2016: • Exclusion from gross income of qualified

principal residence indebtedness • Mortgage insurance premiums deductible as

qualified residence interest • Deduction for qualified tuition & fees • Credit for nonbusiness energy property

(residential energy credit)

12

PATH Act Legislation Changes

Program Integrity • Various changes to refundable credits - EITC,

Child Tax Credit and American Opportunity Credit oRevised due dates oRefund holds oEnhanced penalties oIncreased due diligence

• Update to ITIN processes

13

PATH Act Legislation Changes

• Mandates IRS hold ALL refunds with Earned Income Tax Credit and Additional Child Tax Credit until February 15th oEntire refund will be held oReturns will be processed as normal – urge clients to

file as they have in past oImpacts all preparers and filing processes

• Additional screening for improper payments and income verification • W-2’s and 1099-MISC (Box 7) due by January 31st

14

PATH Act Legislation Changes

No Retroactive Claims of EIC, CTC and AOTC • Earned Income Credit oTaxpayer must have SSN by due date of return oQualifying child must have SSN by due date of

return • Child Tax Credit/American Opportunity Credit o Taxpayer must have SSN or ITIN by due date of

return o Child claimed/student must have SSN, ITIN or

ATIN by due date of return

15

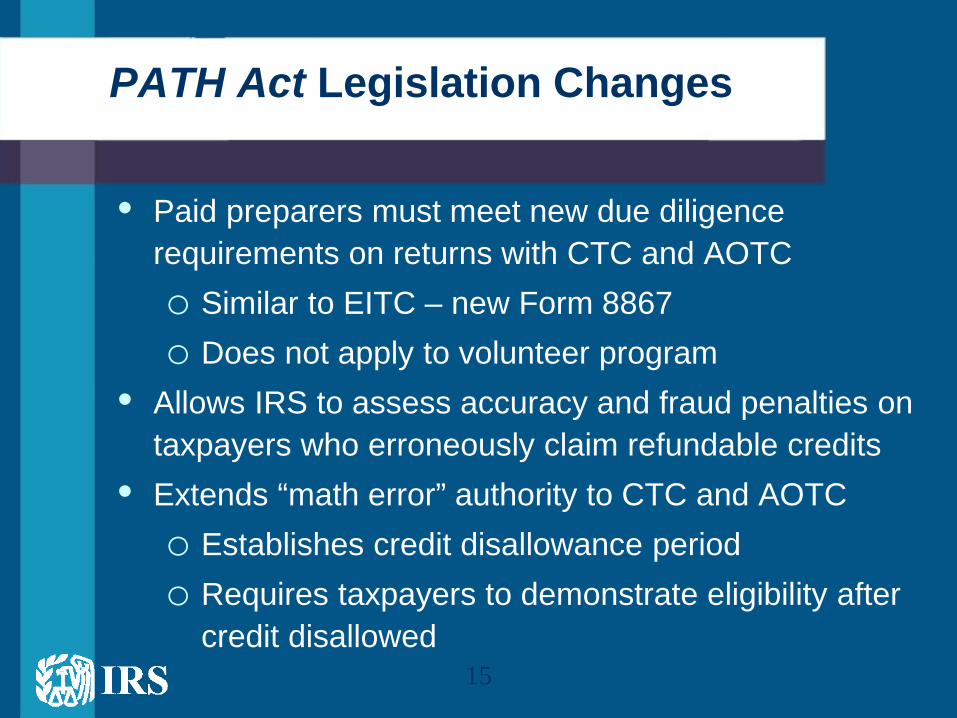

PATH Act Legislation Changes

• Paid preparers must meet new due diligence requirements on returns with CTC and AOTC o Similar to EITC – new Form 8867 o Does not apply to volunteer program

• Allows IRS to assess accuracy and fraud penalties on taxpayers who erroneously claim refundable credits

• Extends “math error” authority to CTC and AOTC o Establishes credit disallowance period o Requires taxpayers to demonstrate eligibility after

credit disallowed

PATH Act Changes ITIN Program

17

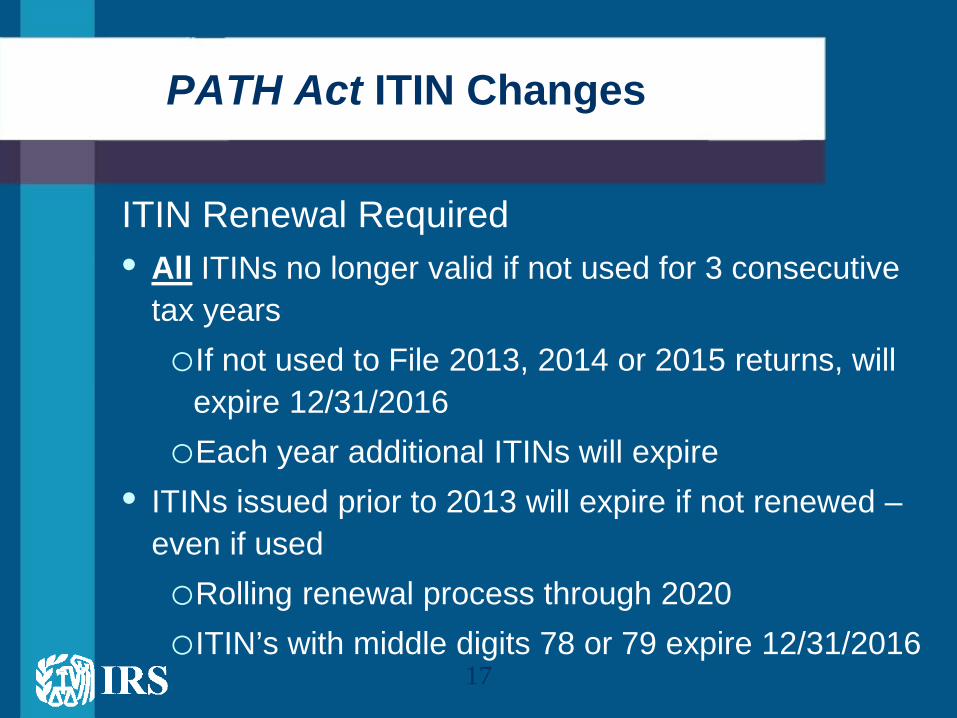

PATH Act ITIN Changes

ITIN Renewal Required • All ITINs no longer valid if not used for 3 consecutive

tax years oIf not used to File 2013, 2014 or 2015 returns, will

expire 12/31/2016 oEach year additional ITINs will expire

• ITINs issued prior to 2013 will expire if not renewed – even if used oRolling renewal process through 2020 oITIN’s with middle digits 78 or 79 expire 12/31/2016

18

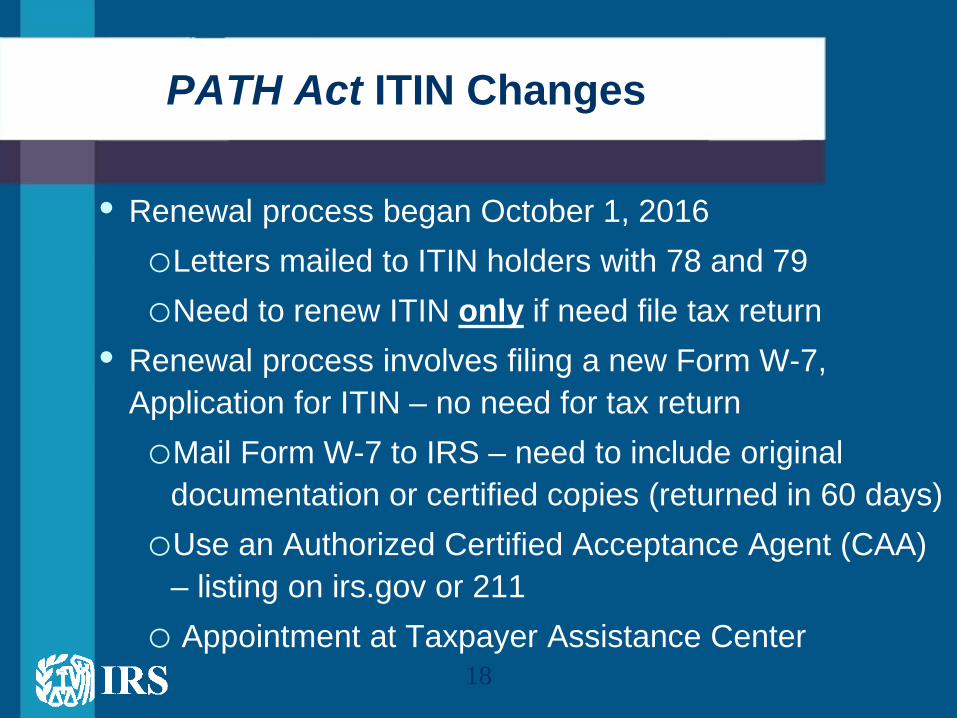

PATH Act ITIN Changes

• Renewal process began October 1, 2016 oLetters mailed to ITIN holders with 78 and 79 oNeed to renew ITIN only if need file tax return

• Renewal process involves filing a new Form W-7, Application for ITIN – no need for tax return oMail Form W-7 to IRS – need to include original

documentation or certified copies (returned in 60 days) oUse an Authorized Certified Acceptance Agent (CAA)

– listing on irs.gov or 211 o Appointment at Taxpayer Assistance Center

Filing Returns with Expired ITINs

• IRS encourages taxpayers to submit tax

returns after ITINs have been renewed • Waiting for confirmation will prevent delays

in processing the tax return • Return will be processed, but exemptions

and/or credits claimed applicable to the expired ITIN will not be allowed until the ITIN is renewed

• Options should be discussed with taxpayer

Filing Options with Expired ITINs

Taxpayer or spouse’s ITIN expired • E-file return oAdvise taxpayers they will get letter oTaxpayer will need completed Form W-7 and

submit documentation oCan mail or use CAA or TAC

• Submit paper return oSubmit with completed Form W-7 and

documentation oCan mail or use CAA or TAC

Filing Options with Expired ITINs

Dependent’s ITIN expired • E-file return – advise taxpayer of procedures • Submit paper return – advise taxpayer of

procedures • File return without dependent oSubmit amended return with Form W-7 later oIs dependent beneficial? oIs this person still your dependent?

Who to call for help?

• Check if ITIN expired - 800-908-9982

• Check on the status of an ITIN application

after 7 weeks - 800-829-1040

• Taxpayer must pass disclosure check

Affordable Care Act (ACA)

24

ACA Updates

• Individual Shared Responsibility Payment

Increases to greater of:

o$695 for TY 16 and beyond (was $325)

o2.5% for TY 16 and beyond (was 2%)

• Open enrollment for 2017/2018 benefit years

oNovember 1st – January 31st

oNov 1st to Dec 15th for future years

25

ACA Updates – IRS Letters

• Failure to reconcile Advance Premium Tax Credit oReceived APTC from Marketplace oNo Form 8962 on tax return

• Shared policy allocation needed oReceived 1095-A for person not claimed on return oAnother tax family received 1095-A for person you

claimed on return oDid not complete Part IV of Form 8962 oOut of scope – stress during training

• Respond to letter – not Amended Return

26

ACA Intake/Interview Questions

• If 3a is “yes”, 8962 must be completed

• If 3b is “no”, return is out of scope

Medicaid Waiver Payments

28

Medicaid Waiver

Will In-Home Supportive Services (IHSS) issue W-2s for employees with qualified Medicaid waiver payments? •Notice 2014-7 instructs agencies with independent knowledge of excludable payments to not include those payments in Box 1 of Form W-2 •California Department of Social Services (CDSS) will begin self-certification program for live-in care providers in January 2017. •After self-certification, wages will be excluded from Box 1 of Form W-2 •CDSS will not issue corrected W-2s for TY 2016

29

Medicaid Waiver

How will CDSS’s policy affect our volunteers and clients who provide Medicaid Waiver services? • IHSS/Medicaid Waiver care providers may have 2016

Form W-2 income that needs to be excluded from wages. • Qualified care providers may have Form W-2 income in

Box 1 that is not taxable and needs to be backed out. • Volunteers will need to continue to interview taxpayers to

determine if the wages in Box 1 of Form W-2 are taxable. • Volunteers will need to be trained to recognize

nontaxable payments and how to back them out on TaxSlayer.

Form W-2 from IHSS

• Payments may still be subject to Social Security and Medicare (Boxes 3-6 of W-2), even if not taxable

• Payments not subject to Social Security/Medicare: • Spouse employed by the other spouse not in a

trade or business, such as domestic service in a private home

• Parent employed by son or daughter not in a trade or business

• Child under 21 employed by parent not in a trade or business, such as domestic work in the parent’s private home

30

31

Did You Know?

• Taxpayers who miss 60-day deadline to roll over IRA or retirement plan can qualify for waiver of tax and penalty o Must meet one or more of 11 circumstances o New self-certification procedure described in

Revenue Procedure 2016-47, including model letter to financial institution

• Due date for filing 2016 return is Tuesday, April 18, 2017

• Taxpayers can pay IRS bills in cash at participating 7-11’s

Questions?

![Volunteer Income Tax Assistance “VITA” Earned Income Tax ... · Volunteer Income Tax Assistance “VITA” Earned Income Tax Credit “EITC” Revised 1/28/19 [DOCUMENT TITLE]](https://img.dokumen.tips/doc/110x75/5fa5a5c85aa0bb13122ce462/volunteer-income-tax-assistance-aoevitaa-earned-income-tax-volunteer-income.jpg)