Embed Size (px)

Citation preview

ANNEXURE 'A'

TIME SCHEDULE FOR SUBMISSION OF VARIOUS RETURNS/STATEMENTS FOR MARCH, 2016 ACCOUNTS

Sr. No.

Particulars of Accounts and Returns Due date by which Accounts & Returns must reach Railway Board

Advance copy to Railway Board

Advance copy to

Local PDA

Audited copy to Railway Board

1 (i) Statement No. 4 Statement of Guarantees given by Central Government. (only Zonal Railways)

(ii) Statement showing capital raised with the approval of the Govt. by the Railway Companies for expenditure on Railways owned by them in respect on share capital have been given (only zonal railways).

13/04/2016

13/04/2016

13/04/2016

13/04/2016

13/05.2016

13/05/2016

2 Exchange and Transfer Certificate for Rolling Stock programme. (iii) The Transfer Certificate should be sent by Railways

to Railway Board. (The date will not be extended in any case)

(iv) The Transfer Certificate should be sent by Railway Board to Railways.

10/04/2016

22/04/2016

--

--

--

--

3 Statement showing important transaction of magnitude which could not be adjusted in the year's accounts through the Reserve Bank of India in time and are proposed to be adjusted with non-Railway Accounts Officer "On Proforma Basis", through Controller General of Account. These proforma adjustments should invariably be supported by acceptance of other parties.

16/04/2016 16/04/2016 16/05/2016

4 Issue of Transfer Certificates by the Railways / Units on account of proforma adjustment of items of magnitude which could not be adjusted in year's account through Reserve Bank of India in time & are proposed to be adjusted with Non-Railway Accounts Officers on proforma basis.

22/04/2016 -- --

5 Statement of “Transfers Without Financial Adjustment” separately for Capital, CF, DRF, DF, and other transactions (except COFMOW).

03/05/2016 03/05/2016 30/06/2016

6 Statements showing calculation of interest on Depreciation Reserve Fund and Pension Fund balances (Proforma XI) (except COFMOW).

11/05/2016 11/05/2016 11/06/2016

7 Account Current with complete schedules. 11/05/2016 11/05/2016 30/06/2015 8 Statement showing calculation of Dividend on Capital-

at-charge & subsidy due from General Revenue, along with following subsidiary statements (except COFMOW) (Proforma I & II attached). a. Statement showing particulars of New Lines on

11/05/2016 11/05/2016 07/07/2016

Sr. No.

Particulars of Accounts and Returns Due date by which Accounts & Returns must reach Railway Board

Advance copy to Railway Board

Advance copy to

Local PDA

Audited copy to Railway Board

which Dividend has been deferred. (proforma III attached)

b. Statement showing Capital outlay (pre-1964) for calculating tax on Railway Passenger Fares.

c. Statement showing particulars of Unremunerative Branch Lines.

d. Statement showing particulars of New Lines taken up on or after 01-4-55 on other than financial considerations.

9 Material for Central Government Finance Accounts Statement No.3 Details of Loans & Advances granted to Co-operative Societies under Head 6425-Loans for Co-operative.

11/05/2016 11/05/2016 11/06/2016

10 (i) Statement No.11 showing investments of Central Government (Railways) in shares of Statutory Corporations, Govt. Companies, other joint stock Companies, Co-operative Banks, Societies and Public Sector Undertaking etc. (only Zonal Railways).

(ii) Statement No. 11 showing investment of Central Government (Railways) in shares of Railway men's Consumer Co-operative Societies, etc. (Only Zonal Railways)

11/05/2016 11/05/2016 11/06/2016

11 Statement of Income Tax credited to major Head 0021 during the year 2014-15 as per prescribed (proforma VI attached).

11/05/2016 11/05/2016 03/07/2016

12 Statement of Service Tax credited to major Head 0044 during the year 2014-15 as per prescribed (proforma VI attached).

11/05/2016 11/05/2016 03/07/2016

13 Statement of Interest Receipts credited to major Head 0049 as per prescribed proforma.

11/05/2016 11/05/2016 11/06/2016

14 Statement of expenditure of Railway Audit Offices Grant No. 33 (Audit) should be reconciled with account (Major Head 2016).

11/05/2016 11/05/2016 11/06/2016

15 Minor head wise Revenue Receipts figures (Abstract X, Abstract Y & Abstract Z). (Only Zonal Railways)

11/05/2016 11/05/2016 10/07/2016

16 Statement showing Major head-wise detail of Pay and Allowances (proforma VIII attached)

11/05/2016 11/05/2016 05/07/2016

17 Statement showing Source wise and Plan head wise Works Expenditure under Grant No.16 incurred on National Projects (For & To end) Proforma X attached)

11/05/2016 11/05/2016 11/06/2016

18 Detail of Working expenses minor head wise. (Credits & Voted/Charged for Commercial and Strategic lines amount shown separately) Please ensure same figures will be adopted in statement submitted for Appropriation Account (Proforma IV attached)

17/05/2016 17/05/2016 10/07/2016

Sr. No.

Particulars of Accounts and Returns Due date by which Accounts & Returns must reach Railway Board

Advance copy to Railway Board

Advance copy to

Local PDA

Audited copy to Railway Board

19 Consolidated correction slip to Account Current for & to end of March, 2016 after thorough review of Accounts/ statements (proforma IX attached).

06/06/2016

06/06/2016

06/07/2016

20 Final Account Current with opening & closing balances for the year.

06/06/2016

06/06/2016

06/07/2016

21 Debt Head Report as per Proforma XII 06/06/2016

06/06/2016

10/07/2016

22 Statement No. 2(a) of Capital-at-charge of Indian Railways as on 31st March, 2016 (except COFMOW) (Proforma V attached).

06/06/2016

06/06/2016

07/07/2016

23 Statement showing payment into and withdrawal from Treasuries by Branch Line Companies (only Zonal Railways).

06/06/2016

06/06/2016

06/07/2016

24 Statement showing balances under Contingencies Fund (except COFMOW).

06/06/2016

06/06/2016

06/07/2016

25 Statement showing share capital debentures & loans to Branch lines companies (only Zonal Railways).

06/06/2016

06/06/2016

06/07/2016

26 Statement No.1 Regarding Financial Results of Govt. Railways as on 31-3-2016. (Only Zonal Railways)

16/06/2016 -- --

27 Statement showing expenditure (separately) on i. Passenger Amenities.

ii. Other Railway users Amenities. iii. Amenities for staff (except COFMOW)

13/06/2016 -- --

28 Statement of total value of Railway Assets (except COFMOW) (proforma VII attached).

13/06/2016 -- --

29 Statement of Plan Head-wise & Source-wise work expenditure showing voted & charged and Gross, Credit and Net expenditure under Grant No. 16 in thousand of `. A separate statement showing category-wise Bulk order & other than Bulk order figures under PH-2100 (Rolling stock) should be sent. The figures of category-wise & B.O. must tally with the debits accepted in January and March Account. (except COFMOW).

13/06/2016 -- --

Note: Before submitting the above statements, it should be ensured that the figures

shown therein are reconciled with Accounts and that there are no differences.

ANNEXURE 'B'

Guidelines for compilation of accounts for and to end of March, 2016 and related financial / accounts statements. 1. Reconciliation of Intra-Railway & Inter-railway Transfer Transactions Before closing of March, 2016 accounts, it is essential to reconcile completely the transactions both intra & inter - Railways with NIL difference. While reconciliation of the transactions under the head 8782 - "Cash Remittances & adjustments between officers rendering account to the same Accounts Officer - Transfers within the same Railways" has to be arranged within the Railway, the difference, if any, under 8797 - Exchange Account - Accounts between Railways has to be reconciled with other Railway / Unit concerned and eliminated before the close of the Accounts for March, 2016. Adjustments such as for diversion of traffic, compensation claims should be proposed by the Railways, only in accordance with Codal provisions & the latest instructions from the Railway Board. It will be the responsibility of the proposing Unit/Railway to prove the correctness of the proposed adjustments with supporting details. The figures (debits & credits) as finally reconciled with other Railways shall only be shown in the March Accounts under "Transfer between Railways". It should be further ensured that on no account, the amount of transfer certificates is adjusted against the suspense heads such as Miscellaneous Advances/Deposits Miscellaneous. Further 8782 and 8797 should tally as per monthly list of e-recon software. 2. Reconciliation of Deposit with Reserve Bank The net result of 'Receipts & Payments' against the head 8675 - Deposits with Reserve Bank should be completely reconciled with the statement of closing balance for March, 2016 sent by Reserve Bank of India (CAS), Nagpur. 3. Transfer without Financial adjustment The advance/audited copies of the statement showing 'Transfer without Financial Adjustment' for the year 2015-16 should reach Board's office positively by the dates specified in Annexure 'A'. Items involving adjustments of the Capital cost of Rolling Stock and contribution under DRF transferred from one railway to another in terms of para 780 FI, should be included in this statement after obtaining confirmation that contra adjustment has been taken into account by the other Railway concerned so that the net result on the over all balance in the books of Railway Board is NIL. Adjustments of balances under CSRPF & "Govt. contribution to CSRPF" to NCSRPF & Pension Fund respectively in the case of pension optees, if any, should also be included in this statement as per extant orders. Further, for rectification of mistake in the balances affecting two or more heads of accounts, the instructions contained in para 922 F-I should be strictly followed, unless other wise ordered by the Railway Board. In the latter case, reference to the Board's order must be quoted against the relevant item.

Note: TWFA statement should include accepted items only of both the Railways to avoid

dispute at later stage.

4. F. Loans & Advances The debit balances under the various minor heads of F. Loans & Advances, transferred from one accounting unit to another of the same Railway or from one Railway to another should be adjusted as plus and minus credits under the relevant heads in the books of the 'transferring & receiving' accounts officer respectively to avoid second debit under the heads for which funds are allotted so that debits for the year on the outgoing side of accounts should represent only payments of advances made during the year. As the figures of outgoing side are taken as actual expenditure in the Appropriation Account of Civil Grants- Loans to Govt. servants etc. requiring submission to Ministry of Finance, it should be ensured that accountal is done as aforesaid & errors in accounting, if any, are rectified before closing of the accounts for March, 2015. 5. Cash Balance 5.1 The closing cash balance as on 31.3.2016 to be adopted in the Actual Account Current for March, 2016 should be based on ‘ACTUALS’ cash balance which will be available on the railways/units by the time the Approximate Account current and Actual Revenue/Capital Account Current for March, 2016 are compiled. Zonal Railways/Production Units should close their Cash Book by 5th April 2016 (NF Railway by 8th of April 2016). Railways may ensure ‘Zero’ Cash in Transit (CIT) before the closure of Cash Book. Necessary Codal Correction in this regard shall follow. It should be ensured that the closing cash balance appearing in Approximate Account Current and Actual Revenue/Capital Account Current for March, 2016 agree with each other as also with the opening cash balance on 1.4.2016 which will be reflected in April, 2016 Accounts. The above exercise must be completed before submission of the Actual Account Current for March, 2016 to avoid corrections later in the March, 2016 and April, 2016 Accounts. 5.2 Incidentally, cheques & credit note-cum cheques awaiting clearance should not appear as part of closing Cash Balance but only as balance under Remittance into Banks. 6. Interest on Fund Balances Interest on the balances under DRF, Pension Fund should be calculated at the dividend rate of 4%. Care should be taken to ensure that the figures of Receipts & Payments adopted while calculating interest accord with those shown in the account for March, 2015. In the calculation sheet relating to Pension Fund, besides the total contribution to the Fund, the break-up thereof under (i) Railway (ii) Audit (iii) other Misc. Establishments & Transfers from SRPF (Contributory) should also be given. No Transfer Certificate for interest on Depreciation Reserve Fund and Pension Fund is required to be submitted to Railway Board. The amount of interest on these two funds may be credited to fund by debited major head 8675-00-105 “Deposit with Reserve Bank”. 7. Interest on Provident Fund and Staff Benefit Fund

No Transfer Certificate for interest on Provident Fund Account and Staff Benefit Fund is required to be submitted to Railway Board. The amount of interest on Provident Fund

Account and Staff Benefit Fund may be credited to fund by debited major head 8675-00-105 “Deposit with Reserve Bank”. 8. Transactions under 8660-Suspense (Railways) 8.1 Reserve Bank Suspense The balance under Reserve Bank Suspense, if any, remaining unadjusted at the close of March, 2015 Accounts should be cleared by Transfer to Miscellaneous Advance Revenue/ Capital/ Deposit Miscellaneous as laid down in the foot note under para 436AI (1990 Edition). 8.2 CGEG Insurance Scheme, 1980-Accounting of Payments Payments for and to end of the month under Civil Major/Minor Head 8011-Insurance Fund 103-CGEG Insurance Scheme should be shown classified (i.e. by giving break-up) under the subhead "Insurance Funds" & 'Savings Fund'. This should be ensured without fail, as gross figures are not acceptable to CGA/MOF. In this connection, further, amount shown under "Insurance Fund" should be in multiples of five thousand (as payment of insurance made in case of death of the employee is in multiples of five thousand such as `5000/-, `10000/-, `15000/- and `20000/- etc. 8.3 Addl. DA/Wages Deposits Suspense Accounts & Repayment of Addl. Wages Suspense Account

No balances to end of March, 2016 should appear under these heads. 9. Deposits by Indian Railway Finance Corporation (For Northern Railway only) In respect of deposits made by IRFC, out of their surplus fund, under Public Account, necessary accounting adjustments should be ensured so that the transactions under these deposits are distinctly shown in the Account Current under the Major or Minor Head"8342- the Other Deposits-103-Deposits of Govt. Cos., Corporations etc. Deposits by IRFC should not be confused with transactions under head 8445-Indian Railway Deposits in respect of amounts made available by IRFC for Rolling Stock for EBR-IF also. 10. Loans to Co- operatives The transactions under Loans to co-operatives are required to be adjusted and shown under the revised Major Head 6425 and appropriate minor head. It should be ensured that the same are reflected in the Account Current and the Debt Head Report strictly in accordance with Board's instructions. 11. Receipts on account of Recruitment fee by RRBs These receipts are required to be accounted for distinctly under a separate minor head under 1001 Indian Railway Misc. Receipts in the Account Current as well as in the schedule of miscellaneous Receipts.

12. Transactions under Contingency Fund

Withdrawals from the Contingency Fund of India, recoupment to the fund during the year 2015-16 itself, should be brought out in a foot note to the Account Current so that the same are so reflected in the statement of Central Transactions to be sent by the Railway Board to the Controller General of Accounts, Ministry of Finance and the C&AG. 13. Charged & Voted Expenditure The figures of charged & voted expenditure should be shown separately at all stages (in details as well as totals) in the following schedules accompanying the Account Current, by each Revenue Grant/Plan Head (Works Grant) as also under (i) Total Final Heads (ii) Total Final & Suspense Heads etc.

I. 3002/3003 Indian Railway Working Expenses

II. 3001 Policy Formulation, Direction, Research & other Miscellaneous & Organisations;

III. 5002/5003 Capital outlay by each subhead of Account (Plan Head) further split-up

under each source of financing viz. Capital, Capital Fund, DRF, DF, and RSF. In addition, a separate statement showing charged expenditure by various grants should be sent alongwith the Account Current to enable verification of correct reflection of the figures in the various schedules. This should be done without fail.

14 Bifurcation of the Expenditure / Receipts between Commercial and Strategic Lines It should be ensured that the Receipts/Expenditure are shown duly bifurcated under Commercial Lines/Strategic Lines in the Account Current for March, 2016 even through manual correction in case the existing FMIS programme on any Railway does not provide for this. 15 Minus Transactions in the Account Current Normally, there should not be any minus transaction to end of March, 2016 on the 'Receipts' or 'charges' side in the Account Current. In case, any minus figures appear in the Revenue/ Capital Account Current to end of March, 2016, the reason should be explained without fail in the Annexure to the Account Current indicating (i) the Head of Account (ii) the Amount (iii) the reasons for "minus' entry and (iv) years to which the minus transaction pertains. Since it is obligatory upon the Ministry of Railways to explain such reasons in the consolidated Account rendered to the CGA/MOF and the C&AG, any omission on this account on the part of any Units/Railway is likely to delay submission of the consolidated Account by the Railway Board and should, therefore, be avoided. 16 Schedule of expenditure under Major Head 5002/5003-Capital outlay on Indian

Railway-Commercial/Strategic The schedule of expenditure accompanying the Capital Account Current for March 2016 should be prepared in the proforma as usual and should show the expenditure for the

month and to end of the month, cumulative expenditure to end of the year since 1.4.79 and cumulative expenditure from commencement of the operation.

17 Dividend & Subsidy - Calculation Statement 17.1 The Dividend & Subsidy calculation statements for the year 2015-16 showing the dividend payable to General Revenues & subsidy due from General Revenues should be compiled as per proforma I & II enclosed and sent along with the Account Current for March, 2016. 17.2 While compiling the statement showing dividend on capital-at -charge for 2015-16, the last year’s recommendation contained in the 1st Report of the Railway Convention Committee 2014-19 regarding rate of Dividend and other ancillary matters should be kept in view. The relief in dividend and subsidy are brought out in Annexure ‘C’ for ready reference. 17.3 The dividend calculation statement should be accompanied by the following subsidiary statement.

I. Statement showing New Lines, which have been taken up on or after 1/4/1955 on other financial consideration. The capital cost of such lines should tally with the amount taken for working out subsidy.

II. Statement of Unremunerative Branch Lines with capital cost against each line. The amount

shown in the statement should tally with the amount taken for working out subsidy. It may be mentioned that the financial results of such lines to determine the remunerativeness of the same and consequent admissibility of subsidy are to be worked on marginal cost principle. It should be ensured that no subsidy is claimed on any of the said lines if it becomes remunerative on Marginal Cost Principle. The capital cost of such lines is included in the statement for working out the Dividend.

III. Statement showing capital expenditure incurred on the construction of New lines

commenced on or after 1/4/1955 other than financial considerations and the amount of deferred dividend payable from 6th year of their opening for traffic, the total capital expenditure incurred to the end of 2015-16 should be shown in the statement in three parts viz. relating upto 2014-15 and during 2015-16 & to end of 2015-16 and the same should tally with the outlay shown in such details in the Dividend and subsidy calculation statements. Further it had been noticed in the past that in some of the cases, the column - date of commencement, date of opening for traffic of the lines and capital outlay to end of the year had not been properly filled in. It should be ensured that all the columns including column of ‘date of commencement’ and ‘date of opening’ etc. are invariably shown in the calculation statement.

IV. Statement showing pre-1964 Capital-at-charge for purpose of calculating Passenger Tax

etc.

The information should be furnished in three parts viz. total pre-1964 capital-at-charge, pre-1964 capital eligible for subsidy and net pre-1964 capital-at-charge.

16.4 If any adjustment of arrears of dividend and subsidy is made, it should be distinctly shown as such with reasons & Board's reference, if any.

18. Debt. Head Report 18.1 The balances under the various funds-Depreciation Reserve Funds, Pension Fund as on 31/3/2015 and 31/3/2016 should be reflected separately for "Commercial" and "Strategic" (For Northern, Northeast Frontier, North Western and Western Railways). 18.2 The balances shown against the various heads of accounts in the Debt Head Report should reconcile with those appearing in the Final Account Current with opening & closing balance for the year 2015-16 and the balance under one Head of Account should not be clubbed with the other Head of Accounts either in the Debt Head Report or in the Final Account Current. 18.3 The Heads operated in the Final Account Current for 2014-15 and the Debt Head Report should accord with those which have been operated in March, 2016 Accounts. 18.4 The balances in the Debt Head Report and Final Account Current should not be worked out under F. Loans & Advances for the total but the same should be worked out and reflected separately under various categories of advances i.e., House Building Advance, Motor Car Advance, Advance for purchase of other Motor Conveyance, other Conveyances and other Advances. 18.5 The figures of "Transfers without Financial Adjustment" should be adopted in the Debt Head Report and Final Account Current on the basis of statement of T.W.F.A. sent to Railway Board separately. Instances have come to notice that in the past some of the Railways arbitrarily changed the figures of such transfers concerning S.R.P.F. (Contributory); S.R.P.F. (Non-contributory) and transfers from contributory PF without advising correction to their statement of T.W.F.A. in time. This should be avoided. 19. Works Expenditure 19.1 The statement of Works Expenditure Grant No.16-Annexure 'A' showing expenditure by each source of financing (Capital, Capital Fund, DRF, DF, & RSF) under Gross, Credit and Net should be sent alongwith March, 2016 Accounts as usual to enable certain financial statements being compiled for Board's information. In respect of expenditure under capital-at-charge an additional statement should be attached with Annexure 'A' incorporating the figures in units of Rupees by Gross, Credits, Recoveries and Net separately under final head and Stores Suspense, Manufacturing Suspense and Miscellaneous Advances as these figures are required for utilisation in the check of Grand Summary of Appropriation Accounts. 19.2 A statement showing "Bulk Order Expenditure" booked under Deposit Miscellaneous "IRFC" by categories of Rolling Stock viz. Locos, Carriages and Wagons should accompany the March, 2016 Account Current. The statement shows the figures of expenditure "during 2015-16 and to end of 31.3.2016".

20. Major Head 8342-NPS Fund 20.1 Huge amount of New Pension Fund are lying under Major Head 8342 which is yet to be transferred to the Trustee Bank by most of the Railways/PUs. The serious implications of this balance needs to be appreciated as it is causing permanent pecuniary loss to the subscribers and may eventually lead to major administrative problems. Therefore, balances lying outstanding with the Railways/PUs should be identified and transferred to the Trustee Bank during the closing of March 2016 Accounts positively. General The Account Current alongwith the allied returns for the year 2015-16 and any correspondence on the subject of closing of March, 2016 accounts should be addressed to Shri N.K. Rajgrihar, Senior Accounts Officer, Room No. 564, Ministry of Railways (Railway Board), Raisina Road, New Delhi-110001 to facilitate quick action thereon.

*****

ANNEXURE-C DIVIDEND AND SUBSIDY CALCULATION STATEMENTS

The Dividend and subsidy calculation statements for the year 2015-16 showing the dividend payable to General Revenue and subsidy due from General Revenues should be compiled as per proforma-I and proforma-II enclosed and should be sent along with the Actual Account Current without fail.

The rate of dividend on the Capital-at-charge of the Railways and relief in dividend and by way of subsidy, based on the recommendations 1st Report of the Railway Convention Committee (2014-19) applicable for 2015-16 are as under:

1. Dividend a. The rate of dividend during the current financial year 2015-16 is 4% on the entire Capital

invested on the Railways (excluding dividend free capital) irrespective of the year of investment.

b. A concessional dividend i.e. 3.5 percent is payable on the capital cost of residential buildings.

c. In respect of the capital invested on New Lines, excluding the 28 new lines taken up on or after 1.4.1955 on other than financial considerations, the dividend payable is to be calculated at the least of the rate of dividend or average borrowing rate for each year and deferred during the period of construction and the first five years after opening of the lines for traffic. The deferred liability is to be paid out of the future surpluses of the lines after payment of current dividend. The account of unliquidated deferred dividend liability on new lines is to be closed after a period of 20 years from the date of their opening, extinguishing any liability not liquidated within that period.

d. Losses in the working of strategic lines are borne by the General Revenues. Surplus, if any, of such lines, after meeting working expenses, depreciation and other charges are paid to General Revenues upto the level of normal dividend.

e. Shortfall, if any, in the payment of dividend on account of inadequacy of net revenue is treated as a deferred liability on which interest is charged.

2. Subsidy from General Revenue

Capital invested in the following cases qualifies for subsidy from the General Revenues to the extent of the dividend calculated at the rates specified above:-

a. Strategic Lines. b. Gauge conversion works taken up on strategic consideration. c. 28 new lines taken up on or after 1.4.1955 on other than financial considerations,

dividend becomes payable if any line becomes remunerative on the marginal cost principle. The arrangement is to be applied also to the two National Investments viz. Jammu-Kathua and Tirunelveli-Kanyakumari-Trivandrum line.

d. N.F. Railway (Non-Strategic portion). e. Unremunerative Branch Lines subject to their unremunerativeness being established on

the marginal cost principle in each of the case through an annual review of their financial results.

f. The Ore Lines between Bimalgarh-Kiriburu and Sambalpur-Titlagar. g. Ferries and Welfare buildings h. 50 percent of the capital invested on all works in the current year and in the two

previous years, excluding capital invested in strategic lines, Northeast Frontier Railway (commercial) Ore Lines, Jammu-Kathua and Tirunelveli-Kanyakumari-Trivandrum Lines, Ferries and Welfare building and unremunerative branch lines which qualify in full for subsidy, capital invested on new lines on which the dividend payable is deferred during the period of construction and the first five years after opening of the lines for traffic and the capital cost of line wires taken over from the P&T Department.

3. Interest on Railway Funds

a. The balances in the various Railway Reserve Funds (except Development Fund) during

the current financial year 2015-16 carry the same rate of interest at which dividend is actually paid. In the case of Development Fund, the rate of interest on the balance in the Fund is the same as the rate of interest payable on the loans to the Fund provided from General Revenues, as long as such loans are outstanding.

b. Necessary arrears adjustments, if any, for the year 2014-15 may also be made in the current financial year in respect of Depreciation Reserve Fund and Pension Fund.

***

PROFORMA-I Statement showing Calculation of Dividend payable to General Revenue during the year 2015-16 1. Capital-at-charge on 31.3.2015 2. T.W.F.A. 3. Capital-at-charge on 1.4.2015 4. Deduct-Capital contributed by companies. 5. Net capital-at-charge on 1.4.2015 (a) Capital-at-charge relating to Residential Buildings. (b) Capital-at-charge relating to New Lines (moratorium category). (c) Capital-at-charge relating to New Lines (other than moratorium category).

(d) Capital-at-charge relating to P&T. (e) Capital-at-charge other than 5(a) to 5(d). 6. Outlay during 2015-16

(a) Outlay relating to Residential Buildings. (b) Outlay relating to New Lines (moratorium category). (c) Outlay relating to P&T. (d) Outlay other than 6(a) to 6(c). 7. Half of outlay 6(d). 8 Dividend @ of a) Normal 4%

b) Concessional 3.5% c) Average borrowing rate or least 4% 9. Total (8a+8b+8c) 10. Arrear adjustment, if any. 11. Deferred Dividend of new lines, if paid. 12. Total Dividend.

***

PRO

FORM

A II

Stat

emen

t sho

win

g de

tails

of s

ubsid

y un

der s

peci

fic H

eads

rece

ived

from

Gen

eral

Rev

enue

s ag

ains

t equ

itabl

e co

nces

sion

in p

aym

ent o

f Div

iden

d du

ring

the

year

20

15-1

6.

Part

icul

ars

Capi

tal O

utla

y up

to

31.3

.201

5 Ca

pita

l Out

lay

durin

g 20

15-1

6 (h

alf)

Subs

idy

at th

e ra

te o

f

Oth

er th

an

Resi -

dent

ial

Build

ing

Resi-

de

ntia

l Bu

ildin

g

Oth

er th

an

Resid

entia

l Bu

ildin

g

Resi-

de

ntia

l Bu

ildin

g

Nor

mal

4%

Co

nces

siona

l on

Res

. bu

ildin

g 3.

5%

ABR

or L

east

on

new

line

s (4

%)

1 2

3 4

5 6

7 8

Unr

emun

erat

ive

bran

ch li

nes

Fe

rrie

s

Wel

fare

Bui

ldin

gs

O

re li

nes

28

New

line

s ta

ken

up o

n 1.

4.55

or

afte

rwar

ds o

n ot

her

than

fin

anci

al c

onsid

erat

ions

New

lin

es t

aken

up

on 1

.4.5

5 or

afte

rwar

ds o

n fin

anci

al

cons

ider

atio

ns (M

orat

oriu

m c

ateg

ory)

Stra

tegi

c lin

es

N

on-s

trat

egic

por

tion

of N

FR

Ga

uge

conv

ersio

n w

orks

take

n up

on

stra

tegi

c co

nsid

erat

ion

W

ork-

in-p

rogr

ess (

Oth

er th

an R

esid

entia

l Bui

ldin

gs)

20

13-1

4

2014

-15

20

15-1

6

Wor

k-in

-pro

gres

s (Re

siden

tial B

uild

ings

)

2013

-14

20

14-1

5

2015

-16

TO

TAL

Su

bsid

y @

of

N

orm

al (4

%)

Co

nces

sion

(3.5

%)

AB

R or

leas

t on

new

line

s (4%

)

Tota

l Sub

sidy

Ar

rear

adj

ustm

ent,

if an

y

Gr

and

Tota

l

***

Proforma-III

Statement of New Lines on which Dividend has been deferred during 2015-16 S.

No.

Nam

e of

Lin

es

Date

of c

omm

ence

men

t

Date

of o

peni

ng fo

r Tra

ffic

Date

of c

ompl

etio

n of

mor

otar

ium

pe

riod

Date

of c

ompl

etin

g 20

yea

rs fr

om

open

ing

of li

ne

Out

lay

to e

nd o

f 201

4-15

Out

lay

durin

g 20

15-1

6

Out

lay

to e

nd o

f 201

5-16

Defe

rred

div

iden

d to

end

of 2

014-

15

Defe

rred

div

iden

d du

e in

201

5-16

Defe

rred

div

iden

d pa

id in

201

5-16

Liab

ility

ext

ingu

ished

aft

er 2

0 ye

ars

Defe

rred

div

iden

d to

end

of 2

015-

16

Defe

rred

div

iden

d af

ter m

orot

oriu

m

Defe

rred

div

iden

d un

der m

orot

oriu

m

1

2

3

4

5

6

7

8

9

10

***

Proforma-IV Statement showing Working Expenses Minor Head wise for the year 2015-16 (Commercial and Strategic lines separately)

Particulars

100

200

300

400

500

600

700

800

900

Total Gross

Credit Total Net

Demand-3 Gross/Voted Gross/Charged Credit/Voted Credit/Charged

Demand-4 Voted Charged

Demand-5 Voted Charged

Demand-6 Voted Charged

Demand-7 Voted Charged

Demand-8 Voted Charged

Demand-9 Voted Charged

Demand-10 Voted Charged

Demand-11 Voted Charged

Demand-12 Voted Charged

Demand-13 Voted Charged

Deduct amount met from Pension fund

Voted Charged

Total excluding suspense Gross Credit Net Demands Payable

Voted Charged

Misc. Advance

Voted Charged

Total including suspense Appropriation to DRF Appropriation to Pension Fund Total Working Expenses (as per A/c)

Note: Please ensure that figures are reconciled with Appropriation Account.

***

Proforma-V

Satatement No. 2(a) (FOR THE YEAR)

Statement of Capital-at-charge of Government Railways as on 31st March 20165

Particulars Works including preliminary

expenditure land etc.

Rolling Stock

General Misc. charges

Floating Assets

Other Assets

Total Capital-at-charge

Commercial Strategic Total

Satatement No. 2(a) (CUMULATIVE)

Statement of Capital-at-charge of Government Railways as on 31st March 2016

Particulars Works including preliminary

expenditure land etc.

Rolling Stock

General Misc. charges

Floating Assets

Other Assets

Total Capital-at-charge

Commercial Strategic Total

***

Proforma-VI

Schedule of Income Tax recovered and credited to Major Head 0021-Tax on income other than corporation tax 101-income tax on union emoluments and 102-income tax on other than union emoluments for and to end of month March 2016. Head of Account For the month To end of the month 101- Income Tax on Union Emoluments including

Pension

102- Income Tax on other than Union Emoluments including Pension

103- Surcharge

504- Primary Education Cess (2%)

505- Higher Education Cess (1%) TOTAL

101- Income Tax on Union Emoluments including Pension

102- Income Tax on other than Union Emoluments including Pension

103- Surcharge

504- Primary Education Cess (2%)

505- Higher Education Cess (1%) TOTAL

GRAND TOTAL

Note: Kindly certified that figures shown in this statement is reconciled with Account Current figures

shown under Major Head 0021. ***

Proforma-VII Statement of Total Value of Railway Assets for and to end of 31st March 2016.

Particulars C A P

DF

C F

D R F

R S F

O L

W R

S R S F

M I S C

T O T A L

Amount as per Block A/c

Vari-ation

A. Non-wasting assets 1 Land 2 Structural Engineering Works a) Formation b) Miscellaneous 3 Floating Assets (Suspense) a) Store Suspense b) Manufacturing Suspense c) Miscellaneous Advance Investment in shares of Govt and other

commercial undertaking

Investment in shares of Govt commercial and public

TOTAL (A) B. Wasting assets 1 Structural Engineering Works a) Stations and offices b) Workshop & Stores buildings c) Residential buildings d) Staff amenities e) Other service building f) Computer hardware 2 Track & Structure a) Formation b) Permanent Way Materials c) Bridges 3 Rolling Stock a) Locos & spare boilers b) Carriage including Rail cars& EMU

stock

c) Wagons d) Ferries e) Rail-cum-Road services f) Road motor cars & carriers g) General charges 4 Equipment (Machinery & Plant etc.)

other than Rolling Stock

TOTAL (B) TOTAL (A+B) Figures as per Block Account Variation

***

Proforma-VIII

Statement of Major Head wise expenditure on pay and allowances for the year 2015-16.

Head of Account (Major Head) Plan Expenditure Total Charged Voted

1 2 3 4

5002 5003

Total Non-Plan Expenditure

3001 3002 3003

Total

***

Proforma-IX

Correction slip to the Account Current for the month of March 2016

Correction slip No……….

Dated :

Seq. No. Major Head (with description)

For the month To end of the month

As shown

As should

be

Variation As shown

As should

be

Variation

Receipt side

TOTAL

Outgoing side

TOTAL

***

Proforma-X

Statement showing Source wise and Plan Head wise Works Expenditure under Grant No.16 incurred on National Project during the year 2015-16. Name of Project Plan Head Source For the month To end of the month

Voted Charged Voted Charged

*****

Proforma-XI

Interest Calculation sheet for DRF & Pension fund for the Month of 2015-16

S.N. PARTICULARS AMOUNT ( `̀ in Units)

1 Balance as on 31.3.2015

2 TWFA

3 Balance as on 1.4.2015 (item 1+2)

4 Appropriation/contribution to Funds during 2015-16

5 Payment/Withdrawals from funds during 2015-16

6 Net accretion during 2015-16 (item 4-5)

7 Half of net accretion during 2015-16 (half of item 6)

8 Total amount on which interest is worked out for 2015-16 (item 3+7)

9 Interest @ 4%, on item no. 8

10 Arrear adjustment, if any

11 Net Balance as on 31.3.2016 (item 3+6+9+10)

Annexure-XII

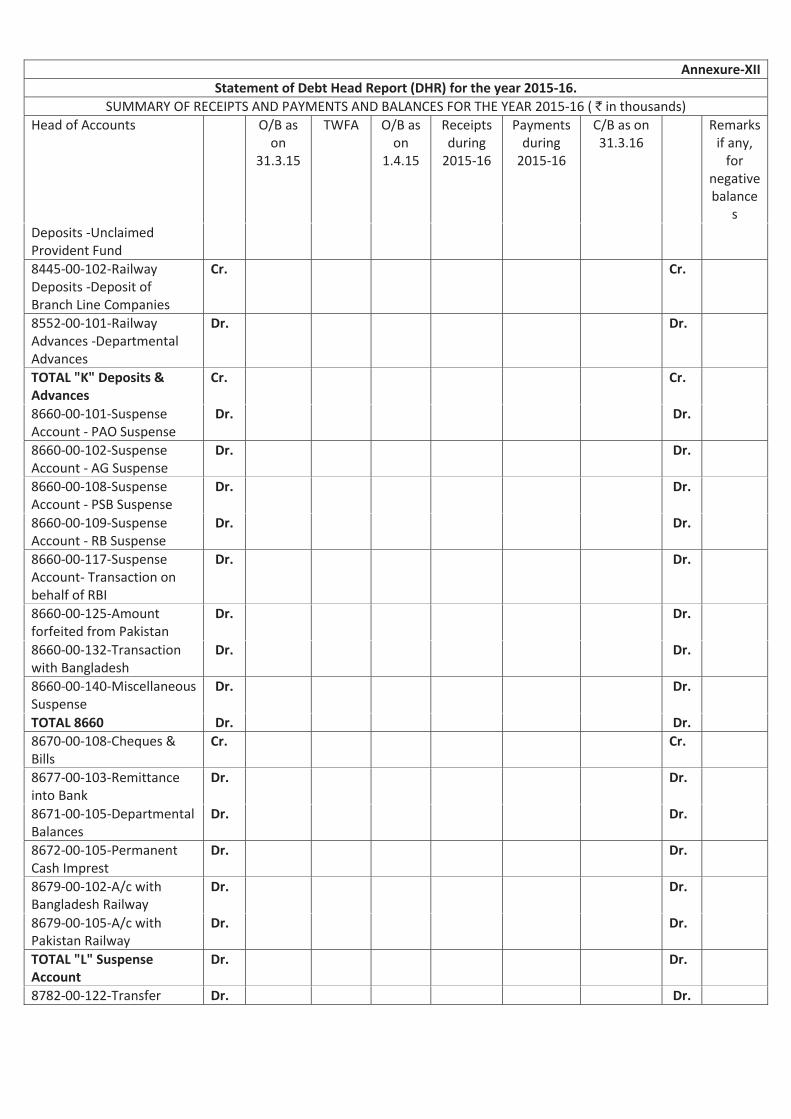

Statement of Debt Head Report (DHR) for the year 2015-16. SUMMARY OF RECEIPTS AND PAYMENTS AND BALANCES FOR THE YEAR 2015-16 ( ` in thousands)

Head of Accounts O/B as on

31.3.15

TWFA O/B as on

1.4.15

Receipts during

2015-16

Payments during

2015-16

C/B as on 31.3.16

Remarks if any,

for negative balance

s 6425-00-108-Loans & Advances to Cunsumer Co-oerative Societies

Dr. Dr.

7610-00-201-Loans & Advances to Govt Servants -HBA

Dr. Dr.

7610-00-202-Loans & Advances to Govt Servants -Motor Conveyance

Dr. Dr.

7610-00-202-Loans & Advances to Govt Servants -Other Motor Conveyance

Dr. Dr.

7610-00-203-Loans & Advances to Govt Servants Other Conveyance

Dr. Dr.

7610-00-204-Personal Computer

Dr. Dr.

7610-00-800-Other Advance

Dr. Dr.

TOTAL 7610 Dr. Dr. TOTAL 7610 and 6425 Dr. Dr. 8009-01-101-General Provident Fund

Cr. Cr.

8009-03-101-State Railway Provident Fund

Cr. Cr.

8009-03-102-Transferred Railway Personnel Provident Fund

Cr. Cr.

8009-60-103-Other Misc. Provident Fund

Cr. Cr.

TOTAL 8009 Cr. Cr. 8011-00-103-Insurance & Pension Fund -Central Govt Employyes Insurance Scheme

Cr. Cr.

TOTAL "I" Small Saving, Provident Fund etc.

Cr. Cr.

8115-00-101 DRF (Commercial)

Cr. Cr.

8115-00-102 DRF (Strategic)

Cr. Cr.

8117-00-101 Railway Cr. Cr.

Annexure-XII Statement of Debt Head Report (DHR) for the year 2015-16.

SUMMARY OF RECEIPTS AND PAYMENTS AND BALANCES FOR THE YEAR 2015-16 ( ` in thousands) Head of Accounts O/B as

on 31.3.15

TWFA O/B as on

1.4.15

Receipts during

2015-16

Payments during

2015-16

C/B as on 31.3.16

Remarks if any,

for negative balance

s Development Fund (Commercial) 8117-00-102 Railway Development Fund (Strategic)

Cr. Cr.

8117- Investment Account Dr. Dr. 8117-Loans to branch line companies

Dr. Dr.

8118-00-106- Railway Capital Fund

Cr. Cr.

8121-00-103- Railway Pension Fund (Commercial)

Cr. Cr.

8121-00-104-Railway Pension Fund (Strategic)

Cr. Cr.

8121-00-107- Staff Benefit Fund (Commercial)

Cr. Cr.

8121-00-108- Staff Benefit Fund (Strategic)

Cr. Cr.

8121-Staff Benefit Fund Investment Account

Dr. Dr.

8231-00-101- Railway Safety Fund (Commercial)

Cr. Cr.

8231-00-102- Railway Safety Fund (Strategic)

Cr. Cr.

TOTAL "J" Reserve Fund Cr. Cr. 8337-00-102-IRCA Emp. PF (Contributory & Non-contributory)

Cr. Cr.

8337-00-103-IRCA Emp. PF(Investment A/c)

Dr. Dr.

8337-00-104-IRCA Emp PF(Investment A/c)

Dr. Dr.

8342-00-103-Other Deposits of Govt Co./Corpn.

Cr. Cr.

8342-00-117-NPS Cr. Cr. 8445-00-101-Indain Railway Deposits

Cr. Cr.

8445-00-104-Railway Deposits -Trust Account

Cr. Cr.

8445-00-800-Railway Deposits -Other Deposits

Cr. Cr.

8445-00-103-Railway Cr. Cr.

Annexure-XII Statement of Debt Head Report (DHR) for the year 2015-16.

SUMMARY OF RECEIPTS AND PAYMENTS AND BALANCES FOR THE YEAR 2015-16 ( ` in thousands) Head of Accounts O/B as

on 31.3.15

TWFA O/B as on

1.4.15

Receipts during

2015-16

Payments during

2015-16

C/B as on 31.3.16

Remarks if any,

for negative balance

s Deposits -Unclaimed Provident Fund 8445-00-102-Railway Deposits -Deposit of Branch Line Companies

Cr. Cr.

8552-00-101-Railway Advances -Departmental Advances

Dr. Dr.

TOTAL "K" Deposits & Advances

Cr. Cr.

8660-00-101-Suspense Account - PAO Suspense

Dr. Dr.

8660-00-102-Suspense Account - AG Suspense

Dr. Dr.

8660-00-108-Suspense Account - PSB Suspense

Dr. Dr.

8660-00-109-Suspense Account - RB Suspense

Dr. Dr.

8660-00-117-Suspense Account- Transaction on behalf of RBI

Dr. Dr.

8660-00-125-Amount forfeited from Pakistan

Dr. Dr.

8660-00-132-Transaction with Bangladesh

Dr. Dr.

8660-00-140-Miscellaneous Suspense

Dr. Dr.

TOTAL 8660 Dr. Dr. 8670-00-108-Cheques & Bills

Cr. Cr.

8677-00-103-Remittance into Bank

Dr. Dr.

8671-00-105-Departmental Balances

Dr. Dr.

8672-00-105-Permanent Cash Imprest

Dr. Dr.

8679-00-102-A/c with Bangladesh Railway

Dr. Dr.

8679-00-105-A/c with Pakistan Railway

Dr. Dr.

TOTAL "L" Suspense Account

Dr. Dr.

8782-00-122-Transfer Dr. Dr.

Annexure-XII Statement of Debt Head Report (DHR) for the year 2015-16.

SUMMARY OF RECEIPTS AND PAYMENTS AND BALANCES FOR THE YEAR 2015-16 ( ` in thousands) Head of Accounts O/B as

on 31.3.15

TWFA O/B as on

1.4.15

Receipts during

2015-16

Payments during

2015-16

C/B as on 31.3.16

Remarks if any,

for negative balance

s within the same Railways 8788-00-101-Adjustment Account with P&T

Dr. Dr.

8789-00-101-Adjustment Account with Defence

Dr. Dr.

8790-00-101-Account with States and Central Civil Railways

Dr. Dr.

8797-03-100-Account Between Railways

Dr. Dr.

TOTAL "M" Remittance Dr. Dr. Note:- Kindly arrange to send in soft copy also through e-mail at [email protected] and

![cmcntm report vol[1].1 - Indian Railwayindianrailways.gov.in/railwayboard/uploads/directorate/civil_engg/pdf... · Committee on Manpower and Cost Norms for Track Maintenance (MCNTM)](https://img.dokumen.tips/doc/110x75/5e94fc080276fd396c67c452/cmcntm-report-vol11-indian-r-committee-on-manpower-and-cost-norms-for-track.jpg)