Embed Size (px)

Citation preview

> > > > > > >> > > > > > >> > > > > > >> > > > > > >> > > > > > >> > > > > > >> > > > > > >

>

A Toolkit for Developing a Social Purpose Business Plan

SeedcoInnovations in Community Development

Funding provided by Mizuho USA Foundation

Copyright © 2004Structured Employment Economic Development Corporation (Seedco)

All rights reserved.

CONTENTS

Introduction� Acknowledgements� How to Use this Toolkit� Seedco and the Nonprofit

Venture Network

Part I: Getting Started� Key Elements of a Social

Purpose Business� Testing for Mission-fit� Taking Inventory of the

Organization� External Context� Tying it all Together� Building a Business:

Recycle-A-Bicycle� A Framework for Planning:

Introduction to PM&MSM

� Addressing Organizational Change

Part II: The Business Plan� The Executive Summary� Market Opportunity� Business Model� Operations� Management and

Stakeholders� Social Outcomes� Financials

Part III: Resource Guide� Pitching Your Business� Working with Consultants� Understanding Financial

Statements� Glossary

Part IV: Worksheets, Templates and Examples

Part V: Sample Business Plan

SeedcoInnovations in Community Development

ideveloping a social purpose business plan

i n t r o d u c t i o n

A Toolkit for Developing a Social Purpose Business Plan grows out ofSeedco's recognition that many nonprofits are eager to launch businessventures but lack targeted resources to help them through the planningprocess. Over the past three years, the Nonprofit Venture Network (NVN)has provided intensive technical assistance to 21 nonprofit organizationsin New York City and Tampa Bay and has conducted introductoryworkshops with more than 250 nonprofits interested in developing socialpurpose businesses. Based on our experience and expertise, we designedthis step-by-step business planning guide especially for nonprofitorganizations. It is our hope that it becomes a valuable resource toorganizations exploring the possibility of social enterprise and to moreseasoned entrepreneurs.

The Toolkit was created under the supervision of Jaycee Pribulsky, SeniorProgram Manager. Content was developed by a Seedco team includingSarah Eisinger and Rosanna Perry-Stephens, and led by Dawn Techow. Ateam of Seedco staff including Tracey Allard, Khary Cuffe, RachelBluestein and Nikhil Gadkari reviewed the document and providedinsightful feedback. Asif Karmally, an intern from the New YorkUniversity, Stern School of Management also assisted in writing andediting this document. Mimi Grinker and Betty Rauch kindly edited andproduced the document. Giona Maiarelli of Maiarelli Rathkopf Designdesigned the Toolkit with assistance from Josh Reisner at Seedco.

Special thanks to Karen Overton, Executive Director of Recycle-A-Bicycle, for graciously allowing us to pick apart her business plan and useit as an example. She has been a strong supporter of the NonprofitVenture Network and we value her enthusiasm and dedication to socialenterprise.

The development of the Toolkit would not have been possible withoutsupport from the Mizuho USA Foundation. We are especially thankful tothe foundation's Executive Director, Lesley Harris Palmer, for hersupport of the Nonprofit Venture Network since its inception.

NVN has also been supported by the MetLife Foundation, the United Wayof New York City, the Eckerd Family Foundation and the World TradeCenter Small Business Fund.

DIANE BAILLARGEONPresidentSeedco and the Non-Profit Assistance CorporationJanuary 2004

Foreword and Acknowledgements

iiideveloping a social purpose business plan

i n t r o d u c t i o n

Social Purpose Business Development:How to Use this Toolkit

Why a Social Purpose Business Planning Toolkit?

A social purpose business is a business activity started by a nonprofitorganization that applies market-based solutions for the purposes offurthering the mission of the organization, generating income, andaddressing social needs. Over the past five years, the social enterprise fieldhas grown significantly. Nonprofits are seeking innovative methods ofdiversifying their revenues and building more sustainable organizations.As a result, nonprofits are seeking assistance in developing and launchingthese ventures.

While starting a social purpose business shares many characteristics withdeveloping a traditional small business venture, there are markeddifferences. Most importantly, you are not an individual entrepreneur.You have stakeholders and clients, funders and staff who follow a missionto provide a needed service to the community. All of these constituentshave opinions and ideas about how the organization should best use itsresources. In addition, decision-making may happen at multiple levels,the organizational culture may be resistant to becoming more business-like and staff may fear mission creep. On the flip side, as an organizationrather than an individual, you may have access to more resources, be ableto build a planning team consisting of diverse backgrounds and expertise,and have a proven reputation in the community.

This Social Purpose Business Planning Toolkit takes the organization intoconsideration throughout the planning process. In addition, the BusinessPlan you develop with this toolkit will highlight the social components andsocial outcomes of the business. As a communications tool, these sectionsare important to your staff, Board and clients as they show the way that theorganization and clients will benefit. In addition, these sections areimportant to socially conscious funders who are seeking a social return ontheir investments.

Who Should Use this Toolkit?

The Social Purpose Business Planning Toolkit is designed for nonprofitorganizations that are considering starting a revenue-generating activity ora business venture. The toolkit begins with the assessment of an idea in thecontext of your organization, so to begin, you will need to have a few ideaspercolating. In addition, organizations that are currently operating abusiness might use the Toolkit as a guide for developing a plan forexpansion or for revising their business model.

iv developing a social purpose business plan

i n t r o d u c t i o n

Developing a Business Plan

Developing a business plan is an exciting, but challenging process.Developing your business and then writing the business plan can takeanywhere from several months to over a year. Staff time, organizationalresources, outside consultants or experts in the field are required for theprocess. In the end, the business plan serves as both a communicationstool and a management tool to evaluate your performance and revise yourassumptions. It will justify the risks and explain the rewards associated withthe business. A good business plan will:

• Illustrate demand for your product• Demonstrate stakeholders' interests and needs• Confirm that the business concept is viable• Post healthy and realistic financial projections• Demonstrate staff and management expertise• Explain your ability to meet the proposed social outcomes

The Case Study

Throughout the Toolkit, we use an organization that Seedco has workedclosely with for the past four years. This organization, Recycle-A-Bicycle,is an established social enterprise that has completed a business plan forexpansion of the business and programmatic activities. We will refer to theRecycle-A-Bicycle business plan and pull examples to illustrate key points.The full text of the plan is available in Section V.

Using the Toolkit

Throughout the Toolkit, you will find a number of icons, illustrated onthe following page, indicating special sections. In addition, a disk isprovided that contains the Financial Projections Workbook. This is anexcel file that is meant to help you build your financial projections. If youhave difficulty using the disk (PC-format), please go to www.seedco.org/nvnto download the files. You will need the user id and password below.

User id: toolkitPassword: business

If you have comments, would like to purchase additional copies of theToolkit or are interested in learning more about Seedco or the NonprofitVenture Network, please email us at [email protected].

vdeveloping a social purpose business plan

Helpful hints are provided to give you specific informationon a topic.

Actions refer to templates, worksheets and examples whichoffer hands-on opportunities to put the concepts intopractice. We encourage you to stop each time you see theAction symbol and pull out the corresponding worksheetfrom Part IV.

These are actual or “modified” examples of socialpurpose business.

These are questions to help you develop the MarketOpportunity and Business Model Sections of your plan.

This section will assist you in developing your Logic Modelor Action Plan with regard to different sections of thebusiness plan.

i n t r o d u c t i o n

viideveloping a social purpose business plan

i n t r o d u c t i o n

About Seedco

Founded in 1986, Seedco provides financial and technical assistance, andmanagement support, for the community-building efforts of nonprofitorganizations and small businesses in targeted disadvantaged communitiesthroughout the United States. Working in partnership with localcommunity organizations, universities, and other local and nationalgroups, Seedco develops wide-ranging initiatives that support workingfamilies, promote community economic development, and strengthencommunity-based nonprofits. Seedco's approach focuses on increasing itscommunity partners' capacity to implement high-impact projects thatbuild community and individual assets.

Seedco's programs focus on workforce development, affordablehomeownership, and entrepreneurship to achieve our communityrevitalization goals, including:

• Supporting working families;• Promoting economic development;• Strengthening community organizations; and• Providing creative financing to support program activities.

HOW WE WORK

Seedco is committed to innovative, high-impact program developmentand delivery. We provide intensive financial and technical assistance to ournetworks of neighborhood-based partners, enabling them to launchmodel projects and realize their community-building goals.

We Build Community Networks

Central to Seedco's work is the belief that neighborhood organizations areinvaluable partners in planning and implementing community andeconomic development projects. Community-based organizations havethe cultural competency and understanding of local needs that areessential in creating meaningful community-building initiatives. As partof our programs, Seedco brings our network of partner organizationstogether to foster peer learning and collaboration.

We Create, Develop, and Implement Model Projects

Seedco develops model projects designed to enable community partners todevote their critical resources to program implementation. Model projectsmay include fully developed business plans and financing strategies,program protocols, and web-based information systems that can beadapted to local needs.

viii developing a social purpose business plan

i n t r o d u c t i o n

We Provide Technical Assistance and Capacity Building

To help our community partners achieve their goals, Seedco providesintensive technical assistance and capacity-building services, focusing onprogram implementation that leads to measurable outcomes. One toolthat Seedco uses to assist organizations is its Performance Measurement &ManagementSM (PM&MSM) process, a technical assistance process that helpsorganizations plan, measure, improve, and be accountable for programs.PM&M helps managers articulate outcomes, collect data about theseoutcomes, and use that data to make and implement informed decisions.

We Offer Financial Assistance

Seedco's Community Development Loan Fund provides low-costfinancing for community-based organizations undertaking developmentactivities. We also help community groups gain access to pre-operationaland recoverable grants to enable them to absorb some of the early costsassociated with developing business plans and other activities that buildtheir organizations' assets. Seedco creates targeted loan products aroundthree program areas: Affordable Homeownership, WorkforceDevelopment and Community Economic Development. In response tochanging needs in the market, Seedco has launched our WTC SmallBusiness Fund, which includes loan funding for small businesses affectedby the September 11th attacks.

ixdeveloping a social purpose business plan

i n t r o d u c t i o n

About Seedco’s Nonprofit Venture Network

The Nonprofit Venture Network (NVN) was established in 2001 withsupport from the MetLife Foundation, United Way of New York andMizuho USA Foundation. NVN offers community-based nonprofitorganizations a comprehensive package of technical assistance andfinancing designed to enhance their capacity to launch social purposebusinesses. While there are several definitions of a social purpose business,we define it as a business activity started by a nonprofit organization thatapplies market-based solutions for the purposes of furthering the missionof the organization, generating income, and addressing social needs. In this context, social purpose businesses serve to:

• Promote innovative programs; • Create job and training opportunities; • Encourage entrepreneurial endeavors; and, • Contribute to the financial viability of the parent nonprofit

organization.

The Challenge

In a demanding operating and funding environment, nonprofitorganizations must look to new models of generating revenue streamswhile also fulfilling their expanding missions. Launching a social purposebusiness is an innovative economic development strategy that has emergedin recent years as a way for community-based nonprofits to do both.Through these ventures, nonprofits can increase their ability to fulfill theorganization's mission while serving their constituents in new ways anddiversify revenue sources.

Starting a social purpose business venture can pose risks for thesponsoring nonprofit. When a nonprofit launches a new business venture,it strives to earn income and achieve tangible social outcomes. Thisundertaking can quickly test an organization's culture and managementpractices. The organization must constantly strive to balance its internalgoals of supporting a social mission and generating revenue. NVN helpsorganizations find that balance through a comprehensive package oftechnical assistance services and low-cost financing.

x developing a social purpose business plan

i n t r o d u c t i o n

The NVN Model

NVN technical assistance and services are delivered in three phases.

Phase I: Learning. This phase provides organizations with assessment andcapacity building tools through the MetLife Introductory Workshop Serieson Social Purpose Businesses.

Phase II: Planning. Organizations that have completed the introductoryworkshop series are eligible to apply for pre-development grants generallyin the range of $5,000 to $10,000 through Seedco's EntrepreneurialAssistance Fund, which begins Phase II of the program. Over the course ofthe year-long grant period, Seedco will work with organizations in groupsettings and one-on-one to develop a business plan.

Phase III: Implementation. Phase III offers grantees access to severalforms of financial assistance to support their efforts in pursuing a socialpurpose business, ranging from grants to below-market loans and near-equity instruments. In order for organizations to move from Phase II toPhase III, eligible organizations must have a business plan and meetSeedco's due diligence requirements.

NVN held its Introductory Workshops Series in New York City and TampaBay in Fall 2003 and will bring on new cohorts in 2004. In addition,NVN plans to expand nationally and is exploring opportunities in severalnew cities.

NVN Grantees

To date, Seedco has provided funding through the EntrepreneurialAssistance Fund and technical assistance to the following organizations:

NVN: New York City

Bedford Stuyvesant Restoration Corporation (BSRC) is developing amulti-purpose technology store, an outgrowth of BSRC's computer accessand training program, to offer employment and training opportunitiesfor local youth.

Brooklyn Children's Museum is creating a museum store to provideemployment and training opportunities for local youth.

Brooklyn Woods, Inc. is creating a woodworking business to provideemployment and training to low-income and unemployed individuals.

Center for Alternative Sentencing and Employment (C.A.S.E.S)explored the creation of a greeting card business targeting the youthmarket that would develop the artistic and business skills of youthoffenders participating in its community alternative sentencing program.

xideveloping a social purpose business plan

i n t r o d u c t i o n

The Children's Village is developing an automotive repair and gasolinebusiness to provide employment and training to youth in its residentialtreatment center.

The CityKids Foundation will launch MUSE Productions (MakingUrban Solutions for Education), a youth development and educationalproduct company specializing in issue-based video curricula and music, aswell as youth outcome-measurement solutions.

The Fifth Avenue Committee is creating Brooklyn Moves, atransportation and trucking business to provide employment toparticipants with multiple barriers to employment, including a history ofincarceration.

Gay Men's Health Crisis is developing a food service business that willserve staff, offer catering to groups using GMHC's office for events andmeetings, and provide training and employment to clients who haveexperienced unemployment due to HIV/AIDS.

Groundwork, Inc., a new Brooklyn-based youth leadership developmentprogram, is developing youth-run ventures that will provide communityservices to youth and families in East New York.

Harlem Textile Works, a design and printing business that providesemployment training to youth in the textile and fashion field, is planningto expand its operations through new urban designs and additionalproduct lines.

Managed Work Services of New York, a joint venture between VIPCommunity Services and the National Association on Drug AbuseProblems, Inc., provides employment to individuals with histories ofalcohol/substance abuse through a temporary employment agency.

Neighborhood Coalition for Shelter (NCS), a Manhattan-based housingprovider, is developing an online business to sell donated new and usedgoods including CDs, DVDs, video games and books. NCS will employ andtrain homeless and formerly homeless individuals to operate the business.

New Horizon Courier Service, an outgrowth of Lenox HillNeighborhood House's vocational training program, recently closed itscourier business that provided employment for formerly homelessindividuals.

Pratt Area Community Council is developing a property managementbusiness to provide employment and training to residents of low- andmoderate-income neighborhoods in Brooklyn.

Project Reach Youth in Brooklyn is creating a catering business toprovide training in the culinary arts and employment to local youth.

Recycle-A-Bicycle is expanding its business which teaches low-incomeyouth affiliated with the Henry Street Settlement House to refurbish usedbicycles, which are then sold at two retail outlets in Manhattan andBrooklyn.

TADA!, a youth theater company in Manhattan, is developing a businessto market and provide short-term theater opportunities for New YorkCity youth during holidays and other school breaks.

NVN: Tampa Bay

The Corporation to Develop Communities of Tampa will develop aplan and marketing strategy to increase traffic to an existing cluster ofsocial purpose businesses on 29th Street: a coin laundry, an ice creamshop and an open air market.

Eckerd Youth Alternatives (EYA) plans to develop a copy and computerservices shop to provide training and job opportunities for rural youth inthe Tampa Bay area.

Tampa Bay Academy of Hope publishes the African American Listing, anannual reference manual with information on local minority-ownedbusinesses and services that generates revenue to off-set the Academy'syouth programs. The Academy plans to publish the listing on-line andemploy and train youth in aspects of creating and publishing the Listing.

The YWCA of Tampa Bay runs a successful youth development programfor low-income girls, ages 10-16, which it plans to adapt into a for-profitventure called Y Girls, targeted to more affluent communities in PinellasCounty with an aim to subsidize the Y's other programs.

i n t r o d u c t i o n

developing a social purpose business planxii

I.1developing a social purpose business plan

pa r t i : g e t t i n g s ta r t e d

Part I of theToolkit willprovide you withframeworks tothink aboutbusiness planningin general andyour idea andorganization in particular.

Part IGetting Started

I.1developing a social purpose business plan

pa r t i : g e t t i n g s ta r t e d

� O V E R V I E WYou probably come to the business planning process with an idea born outof your organization’s need to generate new sources of revenue or addressa new need among the population that it serves. But how do you know ifthe idea is sound? This section helps you evaluate the idea and posesquestions to answer as you look at the organization’s capacity to take on amajor new endeavor. It will cover the following topics:

• Five Key Elements of a Social Purpose Business

• Testing for Mission-fit

• Taking Inventory of the Organization

• Looking at the External Context

• Tying it all Together

• Building a Business: The Example of Recycle-A-Bicycle

• A Framework for Planning: Introduction to Performance Measurement and ManagementSM

• Special Section: Addressing Organizational Change

I Have an Idea!!

Pa r t I Getting Started

I.3developing a social purpose business plan

pa r t i : Five Key Elements of a Social Purpose Business

Starting a social purpose business is challenging and will require a projectchampion, staff resources, a significant amount of time and financing. Asyou create your business, you will take into account five key elements:mission, the business idea, your organization, relationships and the environment.

Mission. Your mission is central to all the activities that you will pursue informing the business. Seedco defines a social purpose business as a venturethat applies market-based solutions for the purposes of furthering themission of the organization, generating income and addressing socialneeds.

Business Idea. Your idea will evolve into a full-fledged business thatincludes what you are selling, the customers to whom you are selling andyour “market advantage” (i.e. why customers will buy your product/service).

The Organization. Your organization consists of an overlying culture andthe individuals and groups that have a direct stake in the success of thebusiness. These stakeholders include the management, staff, volunteers,target population or clients, board members and funders.

Relationships. Relationships describe the way your business interacts withpeople or other businesses who are not direct stakeholders, but who havean influence on the success of the business. Relationships may includevendors, suppliers and strategic partners.

Environment. The environment consists of the external forces that affectthe business. These are circumstances outside of your control that willinfluence the planning or operations of the business.

A successful business builds strength in all five areas but also understandsthe relationship between these areas. For example, you need the rightpeople to run your business, negotiate effective relationships and maintainfocus on the mission and social outcomes. In addition, your business ideamust provide an opportunity to further the mission of the organizationand also must make sense within the environmental context. Though thisseems very straightforward, continually assessing your business aroundthese five areas will help during both planning and operating stages. Theinter-relationship of the elements is illustrated on the next page.

1.

2.

3.

4.

5.

Five Key Elements of Your Social Purpose Business

I.4 developing a social purpose business plan

pa r t i : g e t t i n g s ta r t e d

As you plan, launch and operate your business, revisit these five elementsand evaluate each one in relation to the others. The elements are dynamicand may change over time. These changes may be deliberate or mayhappen outside your control. When one element changes, you may have toadjust other elements to compensate.

Mission

ORGANIZATION RELATIONSHIP

S

BUSINESS ID

EA ENVIRONMENT

I.5developing a social purpose business plan

pa r t i : Testing for Mission-fit

A key step in the development of a social purpose business is determininghow it aligns with your organization’s mission and program activities. It isalso important to think about the needs and interests of the clients youexpect to serve through your social purpose business.1 The mission of yourorganization and your clients are key factors in developing and assessingyour business idea.

One way to ensure that your business idea makes sense to yourstakeholders and clients is to include them in the development process.Ask them for input before starting the social purpose business. Thefollowing Strategic Questions provide a way for you to articulate yourinitial social and financial goals.

What is the mission of your organization?

What is your social purpose business idea? What product or service do youplan to offer and who are your target customers?

What are the demographics and the needs of the clients that you expect tobenefit from this idea?

How will the venture benefit your clients? What needs, interests and skillssets do they bring to the venture?

- What programs do you have that currently serve the needs ofyour clients?

- Have your clients expressed a special interest for new services? What kinds of new services/programs are they interested in?

- What are your client's key skill sets in terms of what is neededfor the business venture? How would you rate their skill level (low, medium, or high)?

What assets will you use to create the business venture, e.g. building,property, equipment, intellectual property, proprietary processes?

What other ways might you use these assets, e.g. sell the building orequipment, use the equipment for a new program?

What are the anticipated benefits or outcomes for your clients and theorganization that will result from starting a social purpose business?

What are the financial goals of the business (break-even, generate profits tobe used for additional training or spin off revenues for other programs)?“Organization” refers to the nonprofit that is developing the business and “client” refers to the target population that isserved by the nonprofit.

1

Is there a Fit Between Your Business Idea and Your Organization’s Mission?

1.

2.

3.

4.

5.

6.

7.

8.

I.6 developing a social purpose business plan

Distribute the Strategic Questions Worksheet, located inPart IV of the Toolkit, to a group of staff, managers andBoard members in order to evaluate the idea frommultiple perspectives within the organization.

Action

After completing the Strategic Questions and reviewing the responsesreceived from other stakeholders, you, your staff and Board membersshould be better able to assess whether the business idea truly does"extend" the mission of the organization.

� Is the business venture consistent with the overall mission of the organization or is it a major shift from the work you do?

� Are the goals and outcomes of the business venture in line with theorganization's mission? Do they make sense?

� Does the business serve the needs, interests and abilities of your clients?

� Will the business meet the needs of other stakeholders in meaningful ways?

An organization working with ex-offenders opened a thriftstore to provide job training and employment to its clients.Despite writing a business plan and successfully capitalizingthe store, the business manager found that the shop had avery low job retention rate. After talking with severalemployees, the manager learned that most employees werenot interested in selling clothing at a thrift shop. For anadult population, and particularly a male population, thework opportunity did not fit their interests and long termgoals. The organization did not close the thrift shop, but ithas modified the training program to meet the needs of thispopulation: now, the men work in the thrift shop for 4-5months. At that time, if they meet performance targets thatfocus on attendance, punctuality and customer service, themen are eligible to move to other job opportunitiesincluding a new landscaping service and a print shop.

Lessons fromthe Field

pa r t i : g e t t i n g s ta r t e d

I.7developing a social purpose business plan

Now that you have examined the relationship between your business ideaand mission, you are ready to assess the business idea in the context ofyour organization. Social purpose businesses succeed when there is asound opportunity (the right "Business Idea") and an entrepreneurialmanagement team (the right "People") to carry out the task of launching abusiness. Using the Organizational Assessment Survey, you will evaluatewhat your organization already possesses to help you develop the "BusinessIdea", and what "People" are in place to lead the effort. By examining yourorganization's core competencies and the expertise you bring to theprocess you will be able to better determine if this business makes sense foryour organization. The Organizational Assessment includes:

Articulation of the organization's values and strengths.

Assessment of the financial, staff, and physical (equipment, property, etc.)resources that are needed and available for the business planning processand launch.

Identification of advocates, stakeholders and partners that will provideassistance for the planning and launch of the business.

Recognition of the potential challenges and difficulties with planning andlaunching the business.

Definition of roles and responsibilities among current and potential stafffor the business.

Taking Inventory of Your Organization

Use the Organizational Assessment Survey, located in PartIV of the Toolkit, to take stock of the organization, mapyour resources, and evaluate the missing pieces.

Action

pa r t i : Taking Inventory of the Organization

1.

2.

3.

4.

5.

I.8 developing a social purpose business plan

pa r t i : g e t t i n g s ta r t e d

Organizational Commitment ChecklistReview your Organizational Assessment Survey to evaluate whether yourorganization is able and willing to make a commitment to developing abusiness. It is okay if there are missing pieces and unanswered questionsduring the initial planning phase. However, the organization shouldrecognize that the following are needed:

� Dedicated resources to support the business planning process.

� A strategic plan that includes the development of a social purpose business as a near-term strategy and/or a board resolution that supports the development of a social purpose business.

� A clear vision of the goals of the business.

� A set of core values that can drive the development of the social purpose business.

� A general understanding of the risk factors involved in starting a social purpose business.

� Mitigation strategies to address resistance to change among staff, clients and stakeholders.

Entrepreneurship Team ("People") ChecklistReview your Organizational Assessment Survey to evaluate whether yourorganization has the people in place to support the business planningprocess:

� Project champion to lead the business planning process.

� Management team that understands the risks and is realistic about possible results of the social purpose business.

� Board of Directors that supports the development of the social purpose business.

� Board of Directors and staff who understand that the desired outcome for a social purpose business is a mix of social and financial returns.

The Organizational Assessment Survey is meant to help you understand whatyou have and what you might need. Making the decision to launch a socialpurpose business is a significant one and requires a sound business idea andorganizational readiness. Based on what you've learned thus far, are youready to begin the business planning process?

I.9developing a social purpose business plan

pa r t i : Looking at the External Context

Beginning the Business Planning Process: An Initial Look at the External Context

Now that you have evaluated your business idea in the context of yourorganization, it is time to take a look at the market opportunity (i.e. thepotential to sell your product or service) and the external environment.When you write your business plan, you will conduct the research intoyour potential market. However, at this time, it is important to take apreliminary look at what's happening outside of your organization thatcan potentially affect business development. The External EnvironmentAssessment will ask you to look at the following:

Who are your potential customers? Describe them demographically.

What similar products do these customers currently buy? What do theylook for when buying similar products/services?

Do you know who else is operating in the same market and targeting thesame customers? Who are your competitors?

How will you compete? How will your business be different?

What is happening with the economy and your industry in particular?

Are there major changes in what customers need and want, how they accessthe product or the price? How might this affect your business?

Complete the External Environment Assessment located inPart IV of the Toolkit. You may not be able to answer all ofthe questions at length, but you should have a general senseof what kind of opportunity exists.

Action

Through the External Environment Assessment you should haveconsidered your potential to sell your product or service in the context ofyour prospective customers and existing competition. Overall, how willthe external environment affect the development of your business? Howcan you mitigate the associated challenges? One solution may be to reviseyour business idea. Perhaps you need to scale back the idea or even changeit if these conditions prove to be too much of a challenge. You can go backto the Strategic Questions Worksheet to think through a new idea. Keep inmind that sharpening your business idea can be, and oftentimes is, aniterative process.

1.

2.

3.

4.

5.

6.

I.11developing a social purpose business plan

pa r t i : Tying it all Together

Conclusion: Tying It all Together

Understanding where your strengths lie and where you need assistance willenable you to make smart decisions about the business planning process.In the next section you will begin to develop your social purpose businessplan and learn techniques to communicate your ideas to others.

The worksheets and questions in this section will allow you to examineyour idea and organization. After doing this work, you should be able toanswer the following questions:

• Does the business venture further the mission of your organization?

• Is the business venture an undertaking your organization wants to pursue?

• Does your organization have the capacity to develop a social purpose business?

• Do the organization and Board of Directors understand the risks involved and are they willing to take such risks?

• Is the organization being realistic about possible results?

• Is the timing right to develop a social purpose business?

• Does the organization have the right people with the right skills and is it willing to give them the freedom, responsibility and authority necessary for entrepreneurial success?

• Does the organization have enough staying power in terms of time, energy and money?

• Is the organization willing to make mistakes?

I.12 developing a social purpose business plan

pa r t i : g e t t i n g s ta r t e d

Seedco’s Nonprofit Venture Network (NVN) socialentrepreneurs offer this advice on the planning process:

• Business planning takes a lot of TIME.• A business "champion" or point person is vital to

maintain focus and motivation during the planning process.

• Define the decision-making process early on to avoidgetting mired in the details.

• If your nonprofit clients are going to become employees, start the transition early through training and communications.

• Acknowledge and manage organizational culture changes as they occur.

• Secure executive staff and board buy-in during the pre-development phase.

• A business advisory board may increase the time required for the planning process, but can provide invaluable thoughts and perspective.

• Acknowledge the risks and determine realistic mitigation strategies.

• Make sure you understand the numbers.• Don't be afraid to sell your products and services!

NVN social entrepreneurs identified the following commonstumbling blocks:

• Failure to recognize that the business needs a manager with the experience and skills to operate a business.

• Resistance to change within the organization and to new staff roles and responsibilities.

• Securing the financial resources to move from planning to launch.

• Understanding the targeted business customers and market opportunity.

Lessons fromthe Field

I.13developing a social purpose business plan

pa r t i : Building a Business: The Example of Recycle-A-Bicycle

Building a Business: The Example of Recycle-A-Bicycle

Recycle-A-Bicycle (RAB) is a successful social enterprise in New York Citythat demonstrates strength in the five key elements and has recognized theimportance of how the elements fit together.

• Mission: Recycle-A-Bicycle provides youth development to at-risk populations through the operation of two successful full-service used bicycle shops that employ youth trained in bike repair and mechanics. Through these shops, RAB also furthers its second mission to promote environmental stewardship by offering affordable and sustainable transportation options.

• Organization: Recycle-A-Bicycle is led by an energetic Executive Director (ED) who is skilled in bicycle repair and maintenance and who is an avid cyclist. Through her networks within the cycling and community development arenas, she has maintained a strong supply of donated bikes and has built a solid customer base at the retail stores. The ED has learned business management skills on the job. In addition, to further strengthen Recycle-A-Bicycle, she actively recruits volunteers, Board members and others to fill additional

Mission

ORGANIZATION RELATIONSHIP

S

BUSINESS ID

EA ENVIRONMENT

I.14 developing a social purpose business plan

pa r t i : g e t t i n g s ta r t e d

needs. Shop managers oversee the youth interns and ensure highquality repair services for customers. Finally, the youth involved with the program are vital to the success of Recycle-A-Bicycle as they bring both enthusiasm for the program and a source of labor.

• Business idea: Recycle-A-Bicycle's founder responded to a proposal to create an employment and training program for youth. The program provided valuable hard and soft skills for the youth. At the same time, Recycle-A-Bicycle began to think about its customer base. Residents of New York’s East Village neighborhood,where the program was located, were either young, low- to moderate-income individuals or residents of low-income housing. Most customers could not afford a new bicycle or did not want to pay a high price given the high rate of theft in New York City. Recycle-A-Bicycle established its competitive advantage through its location, pricing and the quality of the refurbished bikes and repairservices.

• Environment: Recycle-A-Bicycle makes sense in New York City. The terrain is relatively flat and the city is extremely dense. In general, it is faster to bike to a destination that is within 5 miles than to walk, drive or take public transportation. Recently, the NewYork City Council began talking about finding better options for those who bike to work to store their bikes during the work day. In addition, subway fare hikes in spring 2003 and the relatively mild New York City weather makes biking an attractive option.

Despite the economic downturn that has plagued other small businesses during the past three years, Recycle-A-Bicycle has thrived because it (1) serves a niche market of delivery and messenger personnel, who rely on bicycles to perform their jobs and (2) provides an inexpensive alternative to a new bike for cash-strapped young New York City cyclists.

• Relationships: Recycle-A-Bicycle partners with the Henry Street Settlement House and Children's Aid Society. These partnerships allow Recycle-A-Bicycle to focus on job training, knowing that its partners will provide other youth development activities such as academic tutoring or personal counseling.

Recycle-A-Bicycle also has relationships with building superintendents and community leaders who donate abandoned bikes. Funders and technical assistance providers offer neededservices and support. Recycle-A-Bicycle also has relationships with several cycling organizations including the Montauk Century and Bike New York who provide opportunities to market the business as well as offer youth additional part-time work.

I.15developing a social purpose business plan

pa r t i : Building a Business: The Example of Recycle-A-Bicycle

Recycle-A-Bicycle SuccessRecycle-A-Bicycle did not start out with all of these elements in place, butthey have built strength in each area of the business. The key to Recycle-A-Bicycle's success has been the way that the elements fit together.

Several examples of this include:

• Recycle-A-Bicycle's relationships with youth service providers helps them focus on their employment and training mission and their environmental stewardship mission because they do not offer other youth development services. In addition, these service providers aresuccessful in obtaining youth summer employment stipends from the city government, allowing Recycle-A-Bicycle to maintain low labor costs.

• By collecting abandoned and discarded bikes, Recycle-A-Bicycle provides a valuable service for superintendents and others who would have to pay to dispose of these items.

• The business idea of refurbishing and selling used bikes promotes sustainable transportation alternatives for New York City residents.

• The environmental factors such as the subway and bus fare hike in spring 2003 and the economic downturn actually create new opportunities for business with Recycle-A-Bicycle.

• The founder and shop managers are dedicated to the mission and also have the skills to provide quality products and services.

I.17developing a social purpose business plan

pa r t i : A Framework for Planning: Introduction to PM&MSM

Now that you are ready to begin business plan development, it is essentialthat you begin to think about what needs to take place during the planningprocess, how these activities will be accomplished, who will be responsiblefor completing the work, how results will be measured and the timelinefor completion.

In this section, we introduce Performance Measurement & ManagementSM

(PM&MSM), a process to help you plan, measure, improve and beaccountable for your organization's activities. PM&M is a process thatidentifies how your organization's activities lead to desired outcomes. Inthis Toolkit, you will learn how PM&M can help you to articulate socialoutcomes, collect and measure data about these outcomes, and use thedata to make and implement informed decisions.

Social purpose businesses focus on the double bottom line - the social andfinancial outcomes that are expected from the venture. PM&M is a toolthat will help you to define each of these outcomes and developmechanisms for tracking your results. There are four elements in thePM&M process:

The Logic Model. The Logic Model is a graphic representation of howthe various resources and activities will lead to the benefits created for theorganization, its clients and stakeholders. It can be used to communicatehow the business will work and what outcomes will be achieved to peoplewithin the organization, potential investors and other stakeholders.Examples are provided in Part IV.

The Action Plan. Action Plans guide the business planning process byclarifying and coordinating tasks, assigning responsibilities and specifyingtimeframes and due dates. Action plans are management tools used tohelp in project management, and are most useful during the businessplanning process. Action Plans stem from the Logic Model and the twoelements are used together.

Gathering Evidence and Data Collection. This is the "measurement"component of PM&M. This process involves setting targets and developingindicators that measure your performance, and then establishing systemsfor gathering evidence to track the indicators and determine if you metyour targets.

Management. PM&M provides techniques and tools that can be used forday-to-day and long-term assessment and management of theorganization's activities.

A Framework for Planning: Introduction toPerformance Measurement & ManagementSM

1.

2.

3.

4.

I.18 developing a social purpose business plan

pa r t i : g e t t i n g s ta r t e d

Elements One and Two will be explained in the following pages. ElementsThree and Four will be discussed in Part II of the Toolkit as they relate totracking and measuring the social outcomes of the business and writingthis into your plan.

Laying the Groundwork: Developing the Logic Model

A Logic Model is a way to articulate the theory of change behind yoursocial purpose business. This theory of change is based on the notion thatan activity creates an output that generates an outcome or change. Here isa simple example:

Had the work opportunity not been available, these youth might not havedeveloped the self-esteem and soft skills necessary to go on to highereducation.

The graphic representation of this theory of change is the PM&M LogicModel. The Logic Model demonstrates links between the resources,activities and benefits of the social purpose business, both in terms ofchanges or benefits to your clients and for the organization.

The Logic Model consists of five elements described below. Two examplesand a template for building your own Logic Model are included in Part IVof the Toolkit.

• Inputs. What are the assets that the business possesses today? These are the resources dedicated or consumed by the business. For example: funding, staff, facilities, partners, franchise, consultants, participants/clients, knowledge/expertise.

• Activities. What are the tangible actions that need to take place using the inputs to fulfill business objectives? Think of the activities related to both the business and program side of the venture. Some business activities could include: develop/finalize business plan, pilot the business, make sales calls or conduct advertising. Program activities may include develop/modify thetraining curriculum, and screen and recruit the participants. The best way to express the activities is as action verbs.

Output: Youthgain tangiblework experienceand knowledgeof customerrelations.

Short-termOutcome:Youth gain self-esteem and softskills.

Long-termOutcome:Youth completehigh school and continue to highereducation.

Activity: Youthclients work at acopy shop fillingcustomer orders and performingcustomerservice.

I.19developing a social purpose business plan

pa r t i : A Framework for Planning: Introduction to PM&MSM

• Outputs. What is produced as a direct result of business activities? Outputs generally depict the completion of an activity or are quantified as the number or percent of units produced as a result of the activity. For example: business plan developed, customer survey completed or 15 participants complete job training program.

• Outcomes. What are the benefits or changes for your clients or participants and for the parent organization as a result of the social purpose business? Think of outcomes as the goals that your business seeks to achieve. Outcomes are expressed as initial (within 0-2 years), intermediate (within 2-3 years) and long-term (within 3-5 years). Examples include: business generates net operating income, participants obtain work experience and organization becomes more entrepreneurial. The Logic Model should capture financial, programmatic and organizational outcomes.

• Arrows. The arrows on the Logic Model are used to show the cause and effect relationships between each of the elements. For example, because you have a set of assets, you can operate an activity. In general, arrows move linearly from input to activity to output to outcomes. However, other cause and effect relationships are possible. For example, an output may become an input such as when the activity involves creating a training curriculum or marketing plan. Arrows which represent causal relationships are the key to showing how your social purpose business will work.

If you refer back to the Strategic Questions, you will notice that you havealready thought through many of these Logic Model elements -particularly the assets, activities and outcomes.

Use the Logic Model Template and examples located in PartIV of the Toolkit to craft a Logic Model for your social purpose business.

Action

I.20 developing a social purpose business plan

pa r t i : g e t t i n g s ta r t e d

Helpful Hints on Building your Logic Model

• Add arrows to show the causal linkages between inputs, activities, outputs and outcomes. Generally, inputs will lead to activities, activities to outputs, and outputs to outcomes.

• Some inputs may lead to more than one activity, some activities may lead to more than one output, and some outputs may have more than one outcome.

• Are the inputs sufficient to support all listed activities? Are outcomes plausibly related to the business and programmatic activities? Do the outcomes genuinely represent a change or benefit for the clients/participants/customers?

• Use if/then statements to check if the Logic Model is "logical". Example: If we have dedicated staff, then we can pilot the business plan. Or, if participants attend training, then they will be placed in a job.

• Add or eliminate boxes on the template - you do not need to fill in every single box!

• In filling in the boxes, if it is easier, you may want to start with the outcomes and work backwards.

• The Logic Model can be used as a planning device, tomanage the development of your business and later when your business is up and running.

ActionHelpful Hints

Putting it Together: Building the Logic ModelDeveloping your Logic Model often takes one of two directions. Yourthought process might be direct - you know what activities you willundertake and these will lead to certain outcomes. On the other hand,you might know what outcomes you want and work backwards to determinethe activities that will lead to such outcomes.

Uses of the Logic ModelThere are many uses of the Logic Model. Most commonly, it is used as aplanning, communications and operations tool. For the purposes of thesocial purpose business, the Logic Model is best used to convey the entirescope of the business and its outcomes to staff, prospective funders andclients/participants.

I.21developing a social purpose business plan

pa r t i : A Framework for Planning: Introduction to PM&MSM

The Logic Model can be used in communications to staff, potentialfunders and clients/participants to:

• Reach a shared understanding of the business within the organization

• Help staff understand how their work fits into the business and organization

• Explain the business to new staff and the Board of Directors• Clearly describe the business to funders, potential funders and

other stakeholders

The Logic Model can also be used in business planning to: • Structure the business planning process• Guide business implementation• Identify gaps in service production• Show the relationship between social, financial and organizational

outcomes

Finally, the Logic Model helps with operations management to:• Guide measurement efforts and provide a framework for data

analysis• Understand how activities are linked to business and programmatic

outcomes related to clients• Identify hiring and staff training needs• Encourage staff collaboration by illustrating shared purposes and

common outcomes

I.22 developing a social purpose business plan

pa r t i : g e t t i n g s ta r t e d

Status/Notes

Research in progress

Financial statements developed

Organizational chartdeveloped

Questionnaire sent out to current trainees

Training curriculumdeveloped

Task

Business-related Activities

Conduct Market Research

Develop financial plan

Identify staffing needs

Program-related Activities

Recruit participants fortraining program

Adapt current trainingand curriculum

Person Responsible

Marketing Assistant

Business Manager

Business Manager

Program Manager

Program Manager

Due Date

July 2004

September2004

December2004

December2004

October 2003

Making Things Happen: Action Plans

An Action Plan is a planning tool that can organize the key activities forthe business planning process. Overall, the Action Plan delineates:

• What activities/tasks will be done• Who is responsible for doing these activities and tasks• When each activity/task will be completed

The action plan can be used to communicate expectations and accountability.

To create your Action Plan, refer to your Logic Model which shouldorganize the tasks of the business. Also, review your OrganizationalAssessment Survey and identify the tasks that need to be completed as partof the business planning process. Next, examine the resources andexpertise you have in place to outline how the work will be accomplished.In the Action Plan, you need to include the activities, the deadlines andthe responsible individuals.

You will want to return to your Action Plan on a regular basis to assesswhether tasks have been completed.

I.23developing a social purpose business plan

pa r t i : A Framework for Planning: Introduction to PM&MSM

Use the Action Planning Template located in Part IV of theToolkit to plan the primary activities associated withdeveloping a business plan for your idea.

Action

Reviewing the Action PlanTo complete the action planning process, answer the following questions:

• Are any key activities (or staff) missing from the plan?• Are there potential bottlenecks or delays in any part of the plan that

might cause problems moving forward during implementation?• Which activities have flexible deadlines? Which do not?

Conclusion

Developing a social purpose business is intensive and requires a soundbusiness idea, organizational readiness and a strategy that guides businessdevelopment. The work you have completed in this section has providedyou with an important opportunity to think strategically about yourorganization and the way in which a business venture can strengthen itswork and further its mission. In developing the specific components ofthe business plan, revisit this section and use it as a guide for shaping thestory you want to tell about your social purpose business.

In this section, you have assessed your business idea and how it relates toyour organizational mission. You have also explored the ways in which theexternal environment can impact your business idea.

As a result, you should be able to:

• Articulate the outcomes for your social purpose business• Describe your business idea and its relationship to your mission

and programmatic activities• Describe the potential impact of the external environment on

your business idea• Lay out the business on a Logic Model• Establish an Action Plan for moving forward on the business

planning process

Now it is time to get to the real meat of the business planning process-drafting your business plan. The second part of this Toolkit details thecomponents of the Business Plan and provides a how-to manual toformulate a strong and compelling document.

I.25developing a social purpose business plan

pa r t i : Special Section: Addressing Organizational Change

Special Section - Addressing OrganizationalChange

Whether this is your first or fifth social purpose business, planning andlaunching a new venture will cause organizational changes. These changesmay lead to tensions and uncertainty among staff, clients and otherstakeholders. The cultural change that accompanies the opening of thenew business can be one of the major challenges you will face.

The best way to address organizational change is through transparency andcommunication. People often resist change when they are unsure how itwill affect them. Your staff and stakeholders may resist change because theydo not understand the goals of the new business venture or because theydo not feel that their ideas or concerns are being heard.

To help staff and stakeholders understand the changes that occur whendeveloping a social purpose business, it is important to clearlycommunicate what is happening through formal mechanisms such asmeetings, reports and memos.

Communicating Organizational Change

Address strategic questions:• Why are we doing this?• Why a business venture? • What does this mean for staff and clients? • What does this mean for the organization?• What are we trying to accomplish?

Address practical questions:• Explain what will happen and when. Show where

change will occur and provide structure with an anticipated timeframe for roll-out.

• Outline the differences between how the program functions now and how the business will operate in the future.

• Explain how staff roles will change and how the role of clients will change.

• Establish who the staff/stakeholders should talk to with questions or concerns.

ActionHelpful Hints

ii.1developing a social purpose business plan

pa r t i i : Th e B u s i n e s s P l a n

Part II of theToolkit willprovide you withstep-by-stepinstructions fordeveloping yourbusiness andcreating a writtenplan.

Part iiThe Business Plan

ii.1developing a social purpose business plan

pa r t i i : Th e B u s i n e s s P l a n

Pa r t I IThe Business

PlanThe first Part of the Toolkit walked through the process of assessing anidea in the context of the parent organization and introducedPerformance Measurement and ManagementSM (PM&M) a method ofsystematic thinking that will be helpful throughout the planning process.

Part II: The Business Plan introduces the seven sections of a socialpurpose business plan and provides tools and techniques for planning andwriting each section. Portions of the Recycle-A-Bicycle business plan areincluded as an example throughout this section. The full text of thebusiness plan is available in Part V of the Toolkit. Each section alsoincludes information on integrating the tools of PM&M.

The sections of the plan are laid out in the order in which they shouldappear in the final business plan. However, the Executive Summary will bewritten last, incorporating language from other parts of the business plan.In addition, during the planning and writing process, it may be necessaryto jump around between the sections as business development is not alinear process.

The Social Purpose Business Plan includes the following sections:

• The Executive Summary

• Market Opportunity

• Business Model

• Operations

• Management and Stakeholders

• Social Outcomes

• Financials

• Exhibits

Ready, Set, Go.

ii.3developing a social purpose business plan

pa r t i i : The Executive Summary

You never get a second chance to make a first impression.

The Executive Summary of the business plan is often the first and sometimes the only part of the planthat an investor or potential partner will read. You have only a few pages to make a compelling andconcise case for your idea, the funding needs, time frame and your ability to execute the plan.

� O V E R V I E W

The Executive Summary is usually the last section to be written. Return tothe Executive Summary once the other sections of your plan are nearcompletion. After reading the Executive Summary, the reader should havean understanding of the core business and be interested in learning more.

The Executive Summary should be 3-5 pages in length and will summarizekey parts of the business plan.

Overview: The business idea. Explain what are you selling and to whomand include a brief description of the mission and objectives of both thenonprofit and the business. (Business Model Section)

Relationship of the business to the sponsoring nonprofit organization.Describe how the business venture is supported by the parent organizationand the legal structure under which the business will operate. (OperationsSection)

Opportunity: Market summary. Convince the reader that you understandthe marketplace for your product or service by providing highlights of thesize of the market, your target customer base and the competition.(Market Opportunity Section)

1.

2.

3.

The Executive Summary

The Executive Summary

Because it is written last, the Executive Summary can sometimesget short changed in terms of refinement and revision.However, this section should receive significant attention.

• Try to convey your passion for starting this venture.

• Have someone who knows nothing about your business read it to be sure that you are clearly explaining the idea and to give you fresh perspective.

• Use formatting such as bullets, charts and numbered lists to reinforce key points.

Helpful Hints

ii.4 developing a social purpose business plan

pa r t i i : Th e B u s i n e s s P l a n

Competitive advantages and key partnerships. Explain why your venturewill succeed. What do you bring to this market that others do not? Whatstrategic relationships are already in place to help your business succeed?(Business Model and Operations Sections)

Management team highlights. Who will operate this business and why arethey qualified to do this? (Management and Stakeholders Section)

Expected social impact. Outline your social outcomes and the indicatorsand targets for these outcomes. (Social Outcomes Section)

Goals, timeline and benchmarks. Explain how the business will proceedand the key milestones for success. (Operations Section)

Financial overview. Describe the financial outlook of the businessincluding expected year of break-even, upfront costs and the financialstrengths. How much do you need and when do you need it? What willthese funds support? (Financials Section)

Contact information. Who should the reader contact if they want toknow more about the business? Provide the name, title, address, phone,fax and email information for the key contact at the organization.Including this information is extremely important because the ExecutiveSummary might be separated from the body of the business plan andcirculated.

The following example from the Recycle-A-Bicycle business plan providesa comprehensive view of the business. Projections of social outcomes andfinancial performance are clearly delineated in charts.

Every business opportunity is unique, therefore sections of the Recycle-A-Bicycle Business Plan may not be relevant to your business. For example,because Recycle-A-Bicycle is a social enterprise that is not a subsidiary of alarger, parent organization, the legal structure and information about theparent organization are not included. Instead, Recycle-A-Bicycle focuseson its partnerships with other organizations. If your business is asubsidiary of another nonprofit, a brief description of the parentnonprofit should be included.

4.

5.

6.

7.

8.

9.

ii.5developing a social purpose business plan

pa r t i i : The Executive Summary

Overview

Recycle-A-Bicycle, a thriving 501(c)3 nonprofit, has a dual mission: to provide youth developmentopportunities to at-risk populations in New York City and to promote environmental stewardship. Thenonprofit operates two successful full-service used bicycle shops that employ young people trained in bikerepair and mechanics. Through these bicycle shops, Recycle-A-Bicycle offers affordable and environmentallysustainable transportation options for commuters, recreational bikers and messenger/delivery persons. As asocial enterprise, Recycle-A-Bicycle has a triple bottom line in which the social and environmental missionsare balanced with financial returns. Since 1997, Recycle-A-Bicycle has salvaged bikes from the wastestream and refurbished them to sell to the public. Recycle-A-Bicycle also trains young people to fix bikesand assists them in acquiring the soft skills required in today’s competitive job market.

Working closely with the Henry Street Settlement and Children’s Aid Society, Recycle-A-Bicycle integratesfinancial, social and environmental concerns into a successful business model. Recycle-A-Bicycle currentlyoperates two retail stores, one in the East Village of Manhattan, the other in DUMBO, Brooklyn, New York.

Recycle-A-BicycleE X E C U T I V E S U M M A R Y

ii.6 developing a social purpose business plan

pa r t i i : Th e B u s i n e s s P l a n

Year

1995

1998

2001

Bicycles consumed (Millions)

16.2

15.8

16.7

U.S. ridership (Millions)

56.3

43.5

39.0

Bicycles consumed per rider

0.28

0.36

0.42

Toward these goals, Recycle-A-Bicycle:

1 Collects donated bicycles destined for dumping.2 Trains at-risk youth for positions as bike mechanics and sales people, builds skills in basic business

concepts and computer training, and provides a safe alternative that is a positive influence on their development.

3 Refurbishes used bicycles through a training program.4 Sells the bicycles to the community as an affordable, quality transportation option. 5 Employs graduates of the training program.6 Operates retail stores that also sell accessories and repair services that diversify the revenue stream and

create additional profit.7 Offers classes to adults on bicycle repair.

Recycle-a-Bicycle is at a critical juncture in its growth. While the business is currently profitable, thepotential for further growth is significant. To better serve its mission and to address the demand for usedbikes, Recycle-A-Bicycle plans to create a new production facility, fill key staff positions and enhance itsinfrastructure. By pursuing these strategies, Recycle-A-Bicycle can increase its youth outreach by more than100%1 in the next two years as well as create an organization that is sustained on its operating cash flow,thus reducing dependency on corporate grant funds.

MARKET OPPORTUNITY

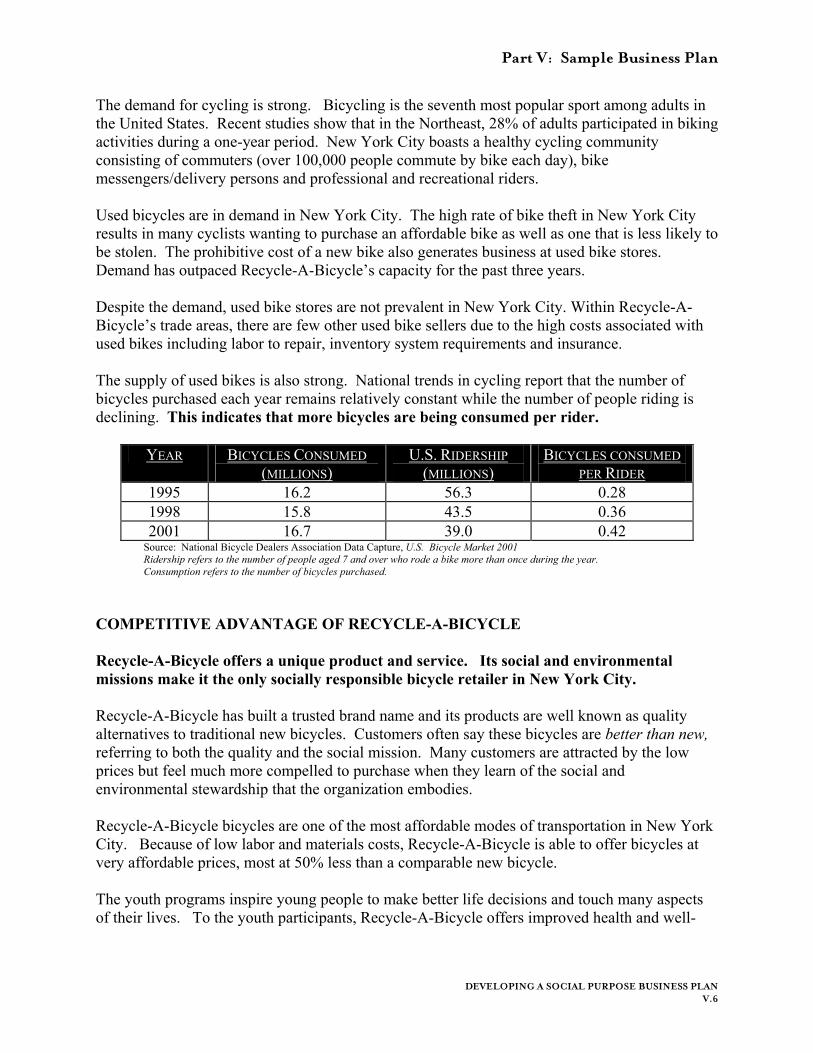

The demand for cycling is strong. Bicycling is the seventh most popular sport among adults in the UnitedStates. Recent studies show that in the Northeast, 28% of adults participated in biking activities during a one-year period. New York City boasts a healthy cycling community consisting of commuters (over 100,000 peoplecommute by bike each day), bike messengers/delivery persons and professional and recreational riders.

Used bicycles are in demand in New York City. The high rate of bike theft in New York City results in manycyclists wanting to purchase an affordable bike as well as one that is less likely to be stolen. The prohibitivecost of a new bike also generates business at used bike stores. Demand has outpaced Recycle-A-Bicycle’scapacity to deliver for the past three years. Despite the demand, used bike stores are not prevalent in NewYork City. Within Recycle-A-Bicycle’s trade areas, there are few other used bike sellers due to the high costsassociated with used bikes including labor to repair, inventory system requirements and insurance.

Source: National Bicycle Dealers Association Data Capture, U.S. Bicycle Market 2001Ridership refers to the number of people aged 7 and over who rode a bike more than once during the year. Consumption refers to the number of bicycles purchased.

Outreach refers to the number of youth involved in any RAB activity, including both youth training andorganized youth bike rides.

1

ii.7developing a social purpose business plan

The supply of used bikes is also strong. National trends in cycling report that the number of bicyclespurchased each year remains relatively constant while the number of people riding is declining. Thisindicates that more bicycles are being consumed per rider.

COMPETITIVE ADVANTAGE OF RECYCLE-A-BICYCLE

Recycle-A-Bicycle offers a unique product and service. Its social and environmental missions make it theonly socially responsible bicycle retailer in New York City.

Recycle-A-Bicycle has built a trusted brand name and its products are well known as quality alternatives totraditional new bicycles. Customers often say these bicycles are better than new, referring to both thequality and the social mission. Many customers are attracted by the low prices but feel even morecompelled to purchase when they learn of the social and environmental stewardship that the organizationembodies.

Recycle-A-Bicycle bicycles are one of the most affordable modes of transportation in New York City.Because of low labor and materials costs, Recycle-A-Bicycle is able to offer bicycles at very affordableprices, most at 50% less than a comparable new bicycle.

The youth programs inspire young people to make better life decisions and touch many aspects of theirlives. To the youth participants, Recycle-A-Bicycle offers improved health and well-being, provides a goal-oriented social structure (earning their own bike by helping fix others), and helps improve self-esteem. An“I can do it” attitude pervades Recycle-A-Bicycle.

MANAGEMENT TEAM

The management team consists of three highly skilled and dedicated staff with over 10 years of experiencein bicycling retailing, 13 years in transportation advocacy, and over 7 years experience in youth education.The team has proven its ability over the years and is continuing to develop new strengths. The three keystaff members are:

• Karen Overton - Executive DirectorMs. Overton is the founder and leader of Recycle-A-Bicycle. Ms. Overton worked as the Bikes forAfrica Project Director at the Institute for Transportation and Development Policy; a consultant forthe World Bank, in the International Development Bank, African American Institute; and Pedals for Progress.

• Jared Bunde - Manager, DUMBO ShopMr. Bunde is an expert mechanic and amateur bicycle racer. His cycling career began in 1997 as amessenger. Before joining Recycle-A-Bicycle in 2002, he was employed for over three years as abike mechanic at Bike Works, a high traffic shop in Lower Manhattan that sells used bicycles. Hehas also excelled in his racing career, winning a silver medal for the NY State Track CyclingChampionship in 2000 and 2002.

• Yoandy Ramirez - Manager, East Village StoreMr. Ramirez started his career with Recycle-A-Bicycle as a Summer Youth Employment student in1999. Based on his hard work, Mr. Ramirez was promoted to Assistant Manager in June 2002 andmost recently became the East Village Store Manager. He will graduate from high school this summerand aspires to pursue a degree in computer science.

pa r t i i : The Executive Summary

ii.8 developing a social purpose business plan

pa r t i i : Th e B u s i n e s s P l a n

Members of the Board of Directors complement the skills presented by the management team. The Boardconsists of dedicated individuals from the following professions: education, finance, social work andtransportation advocacy. Each Board member brings enthusiasm, a unique skill perspective and a broadnetwork of contacts to the organization.

SOCIAL AND ENVIRONMENTAL IMPACT

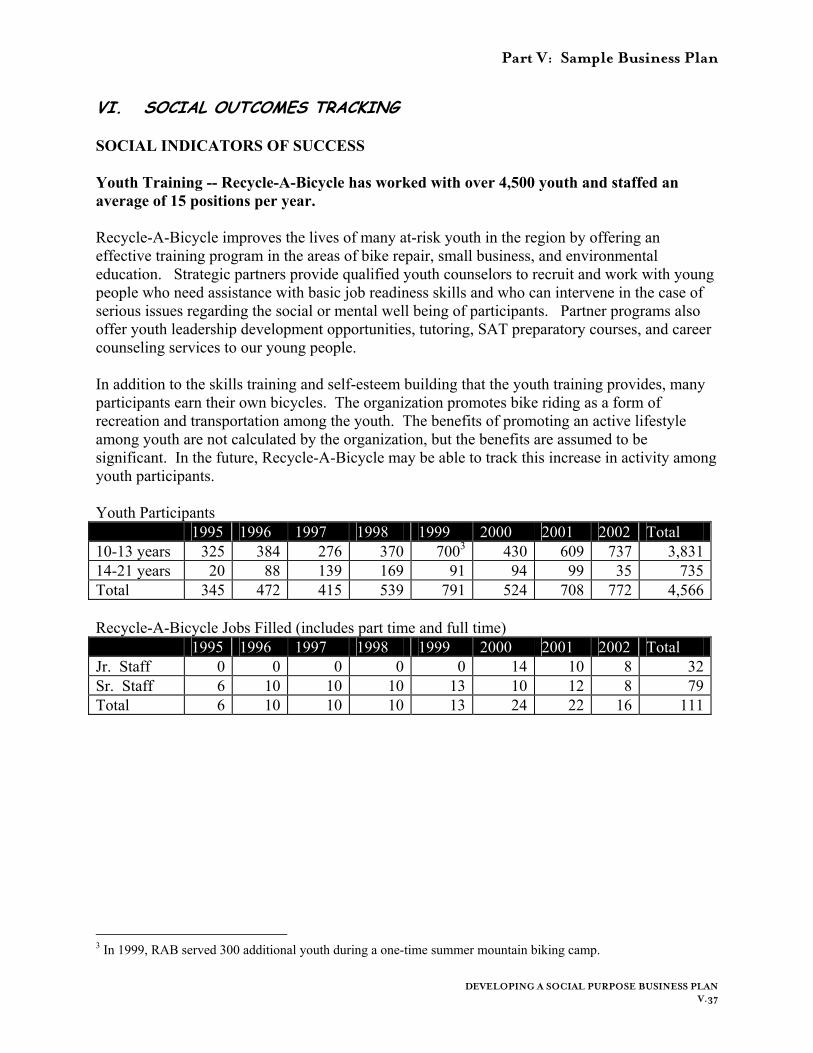

To date, Recycle-A-Bicycle has worked with over 4,500 youth and staffed an average of 15 positions per year.

Recycle-A-Bicycle improves the lives of at-risk youth in the New York City metro area through a hands-on,formal training program in bike repair, small business and environmental education. After completing thetraining program, many youth fill the part- and full-time positions available at the Recycle-A-Bicycle retailstores. In addition, some secure positions in other bike shops across New York City. The organization’sstrategic partners provide qualified youth counselors that recruit and work with young people who needassistance with basic job readiness skills and who can intervene in the case of serious issues regarding thesocial or mental well-being of participants.

In 2002, Recycle-A-Bicycle worked with 772 youth through its training program. Over the next five years,the organization will increase its youth impact by 54%.

In addition, Recycle-A-Bicycle has a strong impact on the environmental conditions of New York City. In2002, Recycle-A-Bicycle recycled over 14 tons of material destined for New York City’s landfills. Recycle-A-Bicycle expects to increase the amount of materials recycled to over 27 tons in 2007.

2003

780

22

17

2004

850

28

22

2005

950

31

24

2006

1050

34

26

2007

1200

37

27

Youth participants to be trained

Number of positions to be filled

Tonnage of material to be removed from the waste stream

ii.9developing a social purpose business plan

pa r t i i : The Executive Summary

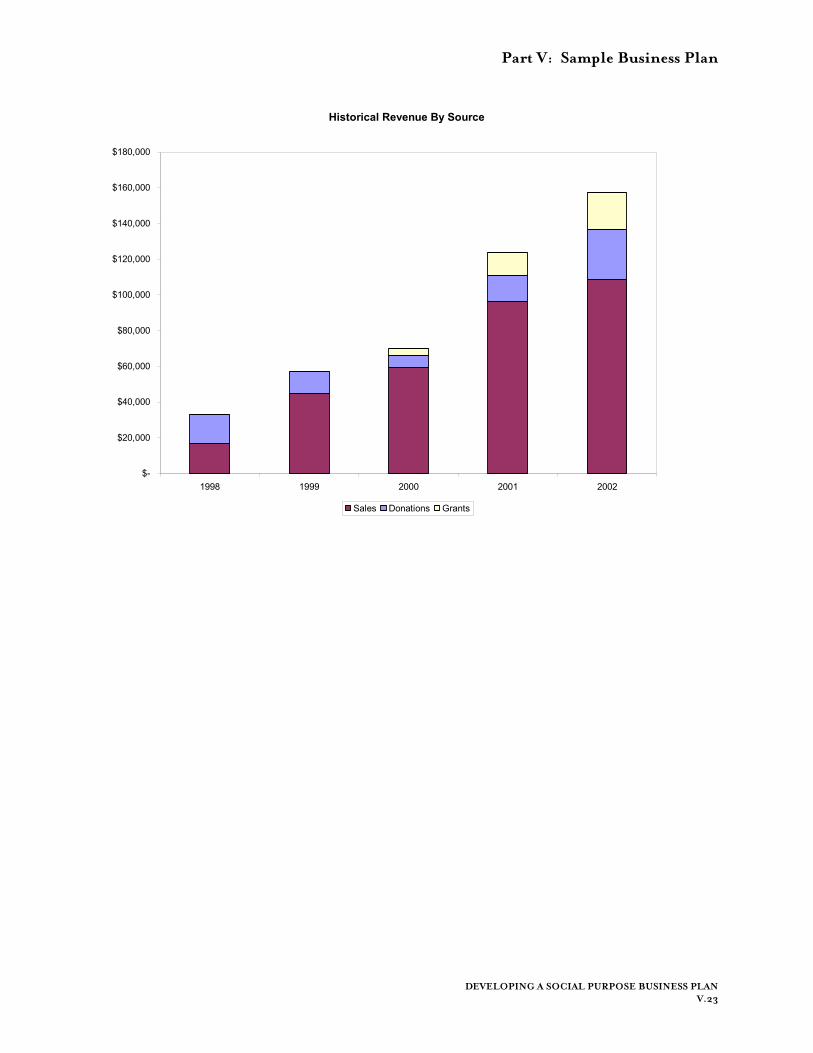

Sales Revenues

Grant Revenues

Net Income

Net Retail Margin

FINANCIAL OVERVIEW

Recycle-A-Bicycle plans to make three key investments over the next three to five years to expand itsprograms and create opportunity for revenue growth:

• Acquire a production and training facility that will provide an expanded and dedicated space fortraining youth as well as refurbishing bikes, therefore meeting more of the demand for used bikes in New York City;

• Acquire a van and hire transportation staff to allow for more strategic and coordinated pick-up ofdonated bikes as well as transfer of inventory between production facility and retail stores; and

• Hire additional staff to enable the organization to raise capital from institutional grantors for businessexpansion as well as for increased training and youth program services.

Recycle-A-Bicycle projects net operating losses in 2003 while development and fundraising efforts areinvigorated, and the marketing, internet sales capacity, retail signage/merchandising, and other criticalcorporate infrastructure projects are further developed. The results of this investment will be greater salesrevenue and significant improvement in net margin.

2003

$167,657

$ 71,091

$ (11,472)2n/a

2004

$232,932

$176,396

$ 47,868

21%

2005

$290,281

$172,049

$ 80,105200628%

2006

$318,775

$188,875

$111,275200735%

2007

$334,446

$198,129

$126,475

38%

SUMMARY OF REVENUE PROJECTIONS AND NET INCOME

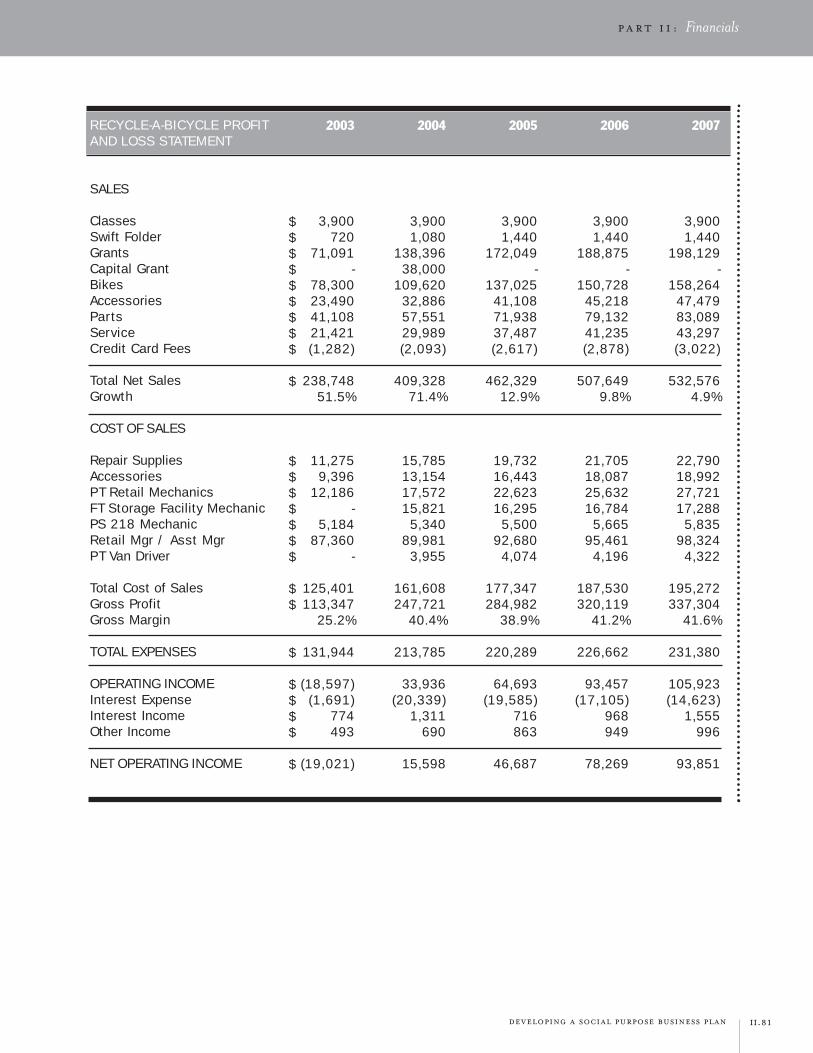

Recycle-A-Bicycle seeks grant funding to finance the growth objectives laid out in its Five-Year StrategicPlan. These grants will be pursued through institutional funders with an interest in environmentalstewardship and/or youth development.

2003Recycle-A-Bicycle seeks $171,000 in funding in 2003. Approximately $71,000 in grant funding will serve asworking capital to support current operations as well as implement new marketing efforts. The additional$100,000 will support hiring a Development Officer, support costs associated with sourcing and obtainingthe new production and training center and provide for other infrastructure improvements.

2004Recycle-A-Bicycle expects to raise $176,000 in grant funding during 2004. These funds will be used in partfor working capital and in part to support more of the Five-Year Strategic Plan. This includes hiring aProduction Assistant to staff the production and training center, hiring a van driver to facilitate the pick-upof supply and transfer of bikes between facilities and funding to pursue e-business strategies. In addition,part of these funds ($38,000) will be used for a down payment on the production and training center.

ii.10 developing a social purpose business plan

pa r t i i : Th e B u s i n e s s P l a n

Recycle-A-Bicycle will raise the additional $106,000 through fundraising efforts spearheaded by the newDevelopment Officer.

2005Recycle-A-Bicycle expects to raise $172,000 in grant funding in order to offset additional costs related toexpansion including research into new retail opportunities. In 2005, Recycle-A-Bicycle will also launch theTours by Teens program.

Recycle-A-Bicycle is facing growing supply and demand for its products. It has a solid track record ofgrowth and is now looking for capital in order to expand the social and environmental outcomes anddevelop more sustainable systems within the business.