Embed Size (px)

Citation preview

A Project Report on

A study on Analysis of mutual fund performance at Ascent

Consultancy Service Pvt. Ltd

BY

GUNASHEKHARA I S

1NH15MBA54

Submitted to

DEPARTMENT OF MANAGEMENT STUDIES

NEW HORIZON COLLEGE OF ENGINEERING,

OUTER RING ROAD, MARATHALLI,

BANGALORE

In partial fulfillment of the requirements for the award of the degree of

MASTER OF BUSINESS ADMINISTRATION

Under the guidance of

INTERNAL GUIDE ETERNAL GUIDE

Dr. A. R. Sainath Rajeeth Das

NHCE Ascent Consultancy Service Pvt. Ltd

2015-2017

CERTIFICATE

This is to certify that Gunashekhara I s bearing 1NH15MBA54 is a confide student of Master

of Business Administration course of the Institute 2016-17, autonomous program, affiliated to

Visvesvaraya Technological University, Belgaum. Project report on ‘ANALISIS OF

MUTUAL FUND PERFORMANCE AT ASCENT CONSULTANCY SERVICE

PVT.LTD’ is prepared by him under the guidance of Dr. Sainath, Professor, in partial

fulfillment of requirements for the award of the degree of Master of Business Administration of

Visvesvaraya Technological University, Belgaum Karnataka.

Signature of Internal Guide Signature of HOD Signature of principal

DECLARATION

I, Gunashekhara , hereby declare that the Internship report entitled ‘Analysis of Mutual

fund performance at ascent consultancy service Pvt. Ltd’ prepared by me under

the guidance of Dr. Sainath, Professor, of M.B.A Department, New Horizon College of

Engineering.

I also declare that this mini project work is towards the partial fulfillment of the university

regulations for the award of the degree of Master of Business Administration by Visvesvaraya

Technological University, Belgaum.

I have undergone a project for a period of sixteen weeks. I further declare that this project is

based on the original study undertaken by me and has not been submitted for the award of a

degree/diploma from any other University / Institution.

Signature of Student

Place:

Date:

ACKNOWLEDGEMENT

I express my deep sense of gratitude to chairman DR. MOHAN MANGHNANI and

Principal DR. MANJUNATHA, New Horizon College Of Engineering, for giving the

opportunity of being the part of this institution and for generous help to complete the

project.

I am extremely thankful and pay my gratitude to head of the department DR. SHEELAN

MISRA for her valuable guidance and support on completion of this project in its presently.

I express my special thanks to my internal guide Dr A R SAINATH, professor for him

valuable guidance, support, motivation and inspirations at every stage throughout the

period of my project work.

I would like to thank Mr. RANJEETH DAS. and the Management staff of the ASCENT

CONSULTENCY SERVICE PVT LTD, Bangalore for giving me opportunity to conduct

to study and to be associated with the company.

Finally, I wish to thank my Parents, Friends and to all who helped me in the

successful completion of this project.

GUNASHEKHARA I S

USN NO: 1NH15MBA54

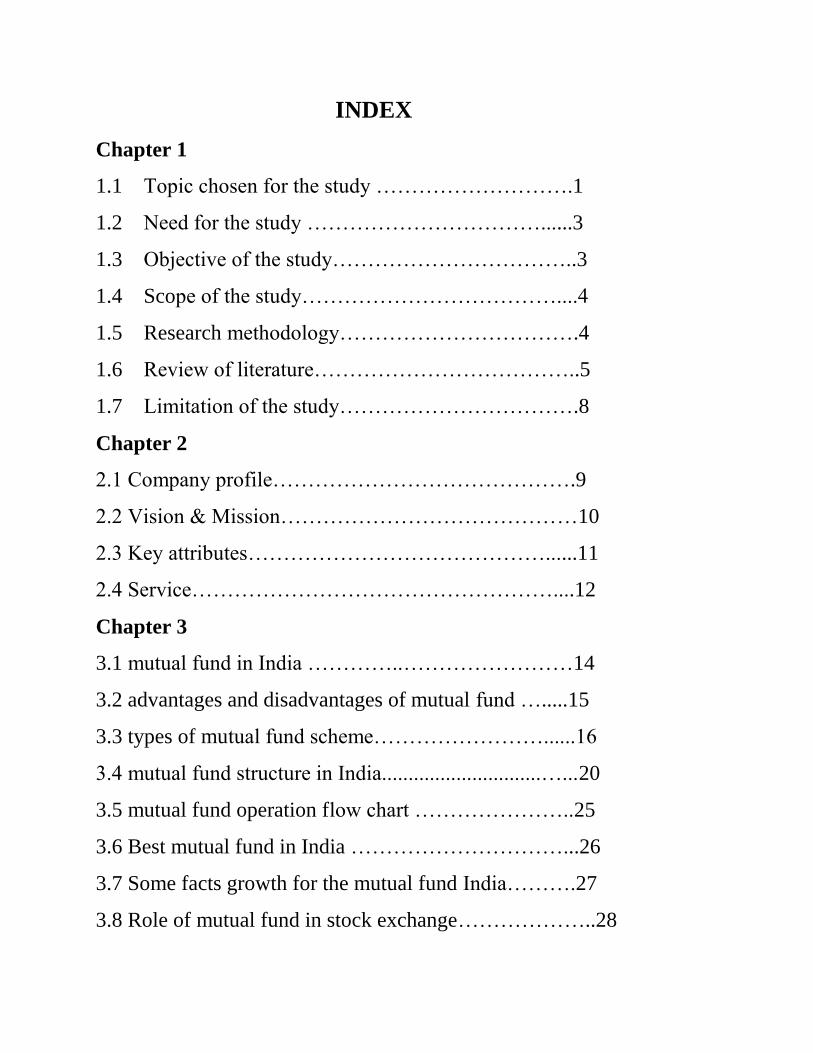

INDEX

Chapter 1

1.1 Topic chosen for the study ……………………….1

1.2 Need for the study ……………………………......3

1.3 Objective of the study……………………………..3

1.4 Scope of the study………………………………....4

1.5 Research methodology…………………………….4

1.6 Review of literature………………………………..5

1.7 Limitation of the study…………………………….8

Chapter 2

2.1 Company profile…………………………………….9

2.2 Vision & Mission……………………………………10

2.3 Key attributes……………………………………......11

2.4 Service……………………………………………....12

Chapter 3

3.1 mutual fund in India …………..……………………14

3.2 advantages and disadvantages of mutual fund ….....15

3.3 types of mutual fund scheme……………………......16

3.4 mutual fund structure in India..............................…...20

3.5 mutual fund operation flow chart …………………..25

3.6 Best mutual fund in India …………………………...26

3.7 Some facts growth for the mutual fund India……….27

3.8 Role of mutual fund in stock exchange………………..28

Chapter 4

Analysis and interpretation of data………………………...42

Chapter 5

5.1 Findings……………………………………………..60

5.2 Suggestions……………………………………….....61

5.3 Conclusion…………………………………………..62

Bibliography

Annexure

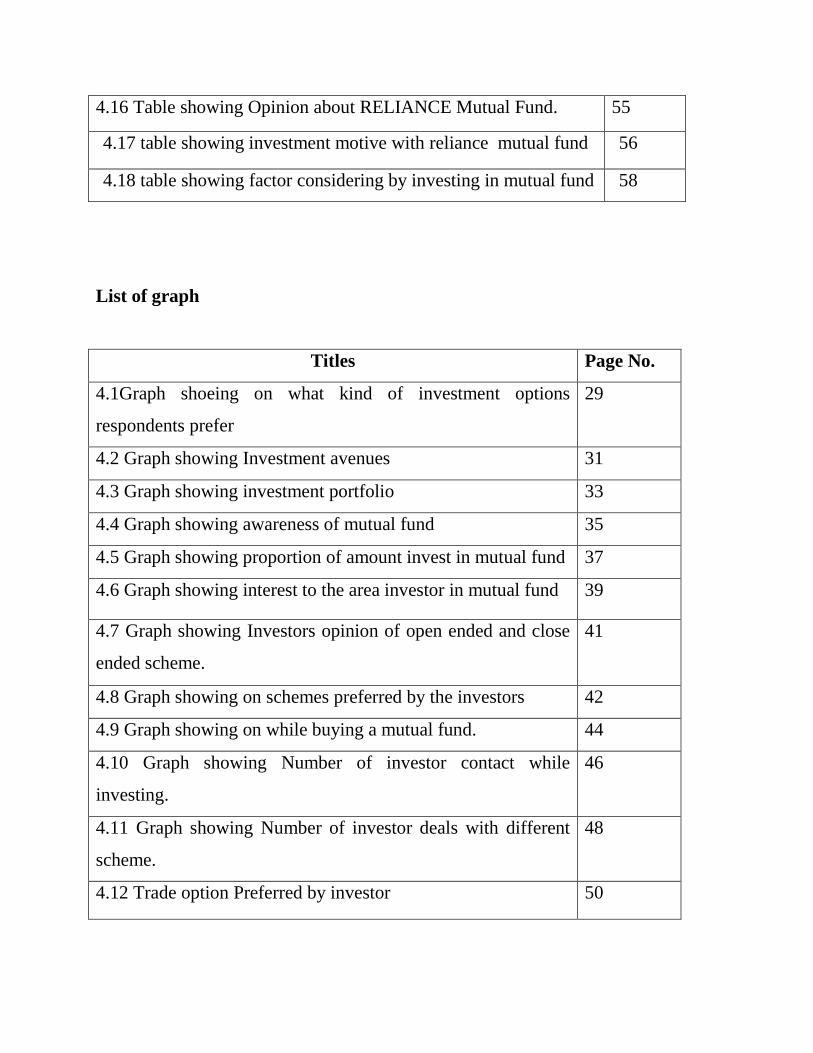

List of Tables

Titles Page

No.

4.1 Table showing on what kind of investment options respondents

prefer

28

4.2 Table showing Investment avenues 30

4.3 Table showing investment portfolio 32

4.4 Table showing awareness of mutual fund 34

4.5 Table showing proportion of amount invest in mutual fund 36

4.6 Table showing interest to the area investor in mutual fund 38

4.7 Table showing Investors opinion of open ended and close

ended scheme.

40

4.8 Table showing on schemes preferred by the investors 42

4.9 Table showing Table showing on while buying a mutual fund. 44

4.10 Table showing Number of investor contact while investing. 46

4.11 Table showing Number of investor deals with different

scheme.

48

4.12 Table showing Trade option Preferred by investor 50

4.13 Table showing Objective behind trading in Mutual Fund. 52

4.14 Table showing percentage of return expect in Mutual Fund. 53

4.15 Table showing Investor willing to take Risk. 54

4.16 Table showing Opinion about RELIANCE Mutual Fund. 55

4.17 table showing investment motive with reliance mutual fund 56

4.18 table showing factor considering by investing in mutual fund 58

List of graph

Titles Page No.

4.1Graph shoeing on what kind of investment options

respondents prefer

29

4.2 Graph showing Investment avenues 31

4.3 Graph showing investment portfolio 33

4.4 Graph showing awareness of mutual fund 35

4.5 Graph showing proportion of amount invest in mutual fund 37

4.6 Graph showing interest to the area investor in mutual fund 39

4.7 Graph showing Investors opinion of open ended and close

ended scheme.

41

4.8 Graph showing on schemes preferred by the investors 42

4.9 Graph showing on while buying a mutual fund. 44

4.10 Graph showing Number of investor contact while

investing.

46

4.11 Graph showing Number of investor deals with different

scheme.

48

4.12 Trade option Preferred by investor 50

4.13 Graph showing behind trading in Mutual Fund. 51

4.14 Graph showing percentage of return expect in Mutual

Fund.

53

4.15 Graph showing Investor willing to take Risk. 54

4.16 Graph showing Opinion about RELIANCE Mutual Fund. 55

4.17 Graph showing investment motive with reliance mutual

fund

57

4.18 Graph showing factor considering by investing in mutual

fund

59

EXECUTIVE SUMMARY

Financial market’s main function is to facilitate transfer of funds from surplus sectors to

deficit sectors. A financial market consists of investor or buyers, sellers, dealers and does not

refer to physical location. Indian financial system consists of two markets, viz. money and

capital market. The core of money market is the inter-bank call money market. It has two

components - organised and unorganised.

Capital market provides the framework in which savings and investments take place. On

one hand it enables companies to raise resources from the investing community and on the other,

it facilitate households to invest their savings in industrial or commercial activities. The capital

market consists of primary and secondary segments. In primary market it deals with the issue of

new instruments by the corporate sector such as equity shares, preference shares, and debentures.

The secondary market or stock exchanges where existing Securities are traded. Capital market

plays a major role in Indian financial system.

So, Equities & mutual fund is the part of capital market. Mutual fund industry in India

began with setting up of Unit Trust of India (UTI) in 1964 by the government of India. Now a

day mutual fund is playing very important role in the industry. Investors will get the benefit of

return, capital appreciation, tax benefits and safety to their investment and companies will get

the capital for their growth. Recently they have also started Systematic Investment Plan(SIP)

with the help of this even small investors (minimum of Rs. 100)can start investing, by this even

students can also invest in this fund. So, we came to know how this mutual fund works. .

The saving of an individual are spread through different means of investment one of them

is mutual fund which is a growing investment now a days because of diversified risk and lack of

time to look after their money.

1

Chapter 1

INTRODUCTION

1.1 About the topic

FINANCE

Finance is regarded as „life blood of enterprise‟. This is because in the Modern Money-Oriented

Economy, Finance is one of the basic foundations for all kinds of economic activities; it is the

master key which provides access to all the sources for being employed in Manufacturing and

Merchandising activities.” Finance is also called the “wheel, marrow of bones and spirit of trade,

commerce and industry.”

The word finance comes from the Latin word “finis”, under Roman law contracts was not

completed until there was a binding contract for monetary/ credit agreements

FINANCIAL MANAGEMENT

Financial management Emerged as a distinct field of study at the time of 20th

century. When one

goes through history of financial management it is clear that in the past the scope of financial

management has limited to certain activities , with a focus mainly on certain episodic events like

formation instance of capital , major expansion , merger, recognition and liquidation in the life

cycle of firm. Financial management is descriptive and institutional in nature. In the past, greater

emphasis was given on day – to-day problems faced by financial managers were responsible only

for maintaining financial records, preparing reports on the company‟s status, performance and

arranging funds needed by the company. Their special services were utilized only when required

via, problem with dearth of funds and to procurement of additional funds.

Driven by growing trend of globalization, the revolutionary developments in information

technology and emergence of the digital era, one can witness phenomenal changes in the world

of finance. Today modern corporate finance is changing from domestic funding to multi currency

funding. Financial control is changing from simple accounting to integrated control systems

based on enterprise resource planning.

2

Investment management is shifting from simple equity and debt products to complex derivatives

products like options, futures, and swaps. Financial services like banking &insurance are getting

geared up for virtual delivery in a seamless digital world. These far reaching developments in the

world of finance have redefined the role of financial manager. The fiancé manager‟s, therefore

concerned with all financial activities of planning of fund raising, allocation and controlling but

not with just any one of them besides, he has handle such financial problems that are

encountered by a firm at the time of incorporation, liquidation , consolidation ,recognition and

the like situations that occur frequently. The finance managers of today are called upon to evolve

financial strategies that dovetail with the firms competitive business strategies. In a competitive

environment, access to the cheapest funds is a key element of competitiveness. A finance

manager needs to evaluate his firms cash needs and decide, for example whether to use debt or

equity funding, whether to have fixed or floating debt, whether to borrow in rupees or in foreign

currency, whether to do currency and / or interest swaps to reduce its funding cost, whether to

issue GDR‟S (Global Depository Receipts) ADR‟s (American Depository Receipts) or to go for

a local secondary issue and so on. For each alternative or combination of alternatives, he needs to

evaluate his net costs, the risk involved, the timing issue and so on. For this finance manger

should have analytical bent of mind and intellectuality in various financial concepts.

SPECIFIC AREA OF THE TOPIC CHOSEN

MUTUAL FUND

A Mutual Fund is a trust that pools the savings of a number of investors who share a common

financial goal. The money thus collected is then invested in capital market instruments such as

shares, debentures and other securities. The income earned through these investments and the

capital appreciations realized are shared by its unit holders in proportion to the number of units

owned by them. Thus a Mutual Fund is the most suitable investment for the common man as it

offers an opportunity to invest in a diversified, professionally managed basket of securities at a

relatively low cost.

3

Definition of Mutual Fund-

The SEBI (MF) Regulations, 1993 defines mutual fund as “A fund established in the form

of a trust by a sponsor to raise monies by the trustees through the sale of units to the public under

one or more schemes for investing in securities in accordance with these regulations

1.2 NEED FOR THE STUDY

The project has been undertaken with the aim of Analysing the Mutual funds of the. And

also to analyse how the operation has been undertaken to communicate with the client & how the

services is offered by the company. These operations may involve the following problems

The operations involved in India Info line Ltd.

Differences between Equities & Mutual funds operations and

Mutual understanding between company & its clients.

1.3 OBJECTIVES OF THE STUDY

The research is undertaken with an objective to know the following aspects:

To study the investment pattern by the respondents in Mutual Funds

To know the perception of investors for investing in a Mutual Fund Scheme

To identify the most demandable scheme of mutual fund

To find whether investment in Equities is better or mutual fund is better

To identify the risk & return involved in Equities and Mutual funds

1.4 SCOPE OF THE STUDY

The study conducted on “Analysis of Mutual fund performance in India” swith reference to

ascent consultancy in the real world has wider scope. The economic activity concerned with

great fluctuations in the economic system. Nowadays the business people are interested to invest

in the mutual funds and equities. They are giving a much importance to this particular field,

which leads to study more about this area. By conducting study in this specified field can

understand how the risk and return involved in the future time with the past experience. The

study brings light in various segment, they are,

To gain new and valid ideas.

4

To know the current issues as regards to the research area.

To gain more knowledge, by direct and personal experience.

To broaden the perspective and set the work in context.

To know the actual importance of this research.

To spot the areas which have not been researched

1.5 RESEARCH METHODOLOGY:

A Research design is a method and procedure for acquiring information needed to solve

the problem. A research design is the basic plan that helps in the data collection or analysis. It

specifies the type of information to be collected the sources and data collection procedure.

The present study is descriptive and it is a fact finding investigation with adequate

interpretation. It is undertaken in many circumstances. When the researcher is interested in

knowing, the characteristics of certain groups such as age, educational level, occupation or

income, interested in knowing the proportion of in a given population who have behaved in

particular manner, making the projections of certain things, or determining the relationships

between two or more variables, descriptive study may be necessary. Descriptive data are

commonly used as directed bases of marketing decisions, these studies are well structured.

DATA COLLECTION

In order to information from the respondent survey method has been adopted. A neatly

constructed questionnaire was prepared to collect information from the respondents regarding

information about the mutual fund. It contains both open-ended and close-ended questionnaire.

Primary Data.

Primary data is the first hand data collected by the researcher directly it‟s the fresh data.

The sources of primary data from this study purpose are as follows :

Observation

Interviews

Questionnaires

5

Secondary Data:

Secondary data is the already available information collected someone hence For their own

study purpose and it is the published sources of information. The secondary data sources

for this study purpose are:

Text books

Company broachers , documents & other related materials

Websites

1.6 REVIEW OF LITERATURE

Any scholars‟ Researchers and writers have done the study on “Analysis of mutual fund

performance in India”. Where the objectives were completely different on the basis of the

needs they had as on when it got a raised. The researchers hear as viewed all such work on the

same, for the purpose of these study but the objectives of the researcher on this area on

completely different than that of those and the need two is also having variation is it. As to

increase the knowledge on the same by getting some sort of the practiced exposure

Literature on mutual fund performance evaluation is enormous. A few research studies

that have influenced the preparation of this paper substantially are being followed. Sharpe,

William F. (1966) suggested a measure for the evaluation of Mutual fund

performance. Drawing on results obtained in the field of portfolio analysis,

economist Jack L. Treynor‟s has suggested a new predictor of mutual fund performance,

one that differs from virtually all those used previously by incorporating the volatility of

a fund's return in a simple yet meaning fulmanner. Michael C. Jensen (1967)

derived a risk-adjusted measure of portfolio performance (Jensen‟s alpha) that

estimates how much a manager‟s forecasting ability contributes to fund‟s returns. As indicated

by Stat man (2000), the e SDAR of a fund portfolio is the excess return of the portfolio over the

return of the benchmark index, where the portfolio is leveraged to have the benchmark index‟s

standard deviation.S.Narayan Rao, et. al., evaluated performance of Indian mutual funds in a

bear market through r e l a t i v e p e r f o r m a n c e i n d ex , r i s k - r e t u r n a n a l ys i s ,

T r e yn o r ‟ s r a t i o , S h a r p e ‟ s r a t i o , S h a r p e ‟ s measure , Jensen‟s measure, and Fame‟s

measure. The study used 269 open-ended schemes (out of total schemes of 433) for computing

6

relative performance index. Then after excluding funds whose returns are less than risk-free

returns, 58 schemes are finally used for further analysis. The results of performance measures

suggest that most of mutual fund schemes in the sample of 58were able to satisfy investor‟s

expectations by giving excess returns over expected returns based on both premium for

systematic risk and total risk. Bijan Roy, etc. all cond ucted an empirical study on

conditional performance of Indian mutual funds. This paper measures the performance

of various mutual funds with both unconditional and conditional f o r m o f T r e y n o r ‟ s -

M a g u e y m o d e l a n d H e n d r i c k s o n - M e r t o n m o d e l . T h e e f f e c t

o f i n c o r p o r a t i n g l a g g e d i n f o r m a t i o n v a r i a b l e s i n t o t h e e v a l u a t i o n o f

m u t u a l f u n d m a n ag e r s ‟ performance is examined in the Indian context. The results

suggest that the use of conditioning lagged information variables improves the performance of

mutual fund schemes, causing alphas to shift towards right and reducing the number of

negative timing coefficients. Mishrl, etal., (2002) measured mutual fund performance

using lower partial moment.

Jack Treynor (1965) developed a methodology for performance evaluation of a mutual fund

that is referred to as reward to volatility measure, which is defined as average excess return on

the portfolio. This is followed by Sharpe (1966) reward to variability measure, which is average

excess return on the portfolio divided by the standard deviation of the portfolio.

Sharpe (1966) developed a composite measure of performance evaluation and imported superior

performance of 11 funds out of 34 during the period 1944-63.

Michael C. Jensen (1967) conducted an empirical study of mutual funds in the period of 1954-

64 for 115 mutual funds. The results indicate that these funds are not able to predict security

prices well enough to outperform a buy the market and hold policy. The study ignored the gross

management expenses to be free. There was very little evidence that any individual fund was

able to do significantly better than which investors expected from mere random chance.

Jensen (1968) developed a classic study; an absolute measure of performance based upon the

Capital Asset Pricing Model and reported that mutual funds did not appear to achieve abnormal

performance when transaction costs were taken into account.

Carlsen (1970) evaluated the risk-adjusted performance and emphasized that the conclusions

drawn from calculations of return depend on the time period, type of fund and the choice of

benchmark. Carlsen essentially recalculated the Jensen and Shape results using annual data for

7

common stock funds over the 1948-67 periods. The results contradicted both Sharpe and Jensen

measures.

Fama (1972) developed a methodology for evaluating investment performance of managed

portfolios and suggested that the overall performance could be broken down into several

components.

John McDonald (1974) examined the relationship between the stated fund objectives and their

risks and return attributes. The study concludes that, on an average the fund managers appeared

to keep their portfolios within the stated risk. Some funds in the lower risk group possessed

higher risk than funds in the most risky group.

James R.F. Guy (1978) evaluated the risk-adjusted performance of

UK investment trusts through the application of Sharpe and Jensen measures. The study

concludes that no trust had exhibited superior performance compared to the London Stock

Exchange Index.

Henriksson (1984) reported that mutual fund managers were not able to follow an investment

strategy that successfully times the return on the market portfolio. Again Henriksson (1984)

conclude there is strong evidence that the funds market risk exposures change in response to the

market indicated. But the fund managers were not successful in timing the market.

Grinblatt and Titman (1989) concludes that some mutual funds consistently realize abnormal

returns by systematically picking stocks that realize positive excess returns.

Richard A. Ippolito (1989) concluded that mutual funds on an aggregate offer superior returns.

But expenses and load charges offset them.

This characterizes the efficient market hypothesis.

Ariff and Johnson (1990) made an important study in Singapore and found that the performance

of Singapore unit trusts spread around the market performance with approximately half of the

funds performing below the market and another half performing above the market on a risk-

adjusted basis.

Cole and IP (1993) investigated the performance of Australian equity trusts. The study found

evidence that portfolio managers were unable to earn overall positive excess risk-adjusted

returns.

8

Vincent A. Warther(1995) in the article entitled “aggregate mutual fund flows and security

returns” concluded that aggregate security returns are highly correlated with concurrent

unexpected cash flows into MFs but unrelated to concurrent expected flows. The study resulted

in an unexpected flow equal to 1 percent of total stock fund assets corresponds to a 5.7 percent

increase in stock price index. Fund flows are correlated with the returns of the securities held by

the funds, but not the returns of other types of securities. The study found an evidence of positive

relation between flows and subsequent returns and evidence of a negative relation between

returns & subsequent flows.

Bansal’s book (1996) “mutual fund management & working” included a descriptive study of

concept of mutual funds, Management of mutual funds, accounting & disclosure standards,

Mutual fund schemes etc.

This study is mainly based on to know perception towards different schemes of mutual

fund to invest.

1.7 Limitations of the Study:

The limitations of the study are as follows:

Sample size is only 100 out of the entire population.

The study concentrated only on the Mutual Funds .

Time constraint.

Study area is Bangalore city only.

9

CHAPTER 2

PROFILE OF THE INDUSTRY AND COMPANY

2.1 Company Profile

Ascent Consulting Pvt Ltd established in the year of 2003.

People Management is a key business function that has a direct impact on competitiveness,

efficiency of operations, and long-term profitability of an organization. Which is why,

organizations have been investing enormous time and resources in the HR function, which

diverts focus from the organization‟s core business.

Ascent Consulting precisely addresses this anomaly through its 360 degree HR Management

Solutions that transform the HR service delivery. While these solutions accomplish cost

reduction, greater efficiencies and improved quality, our larger effort is aimed at improving

organizational efficiency and not just creating incremental change.

Ascent has achieved this by building the right mix of skills and knowledge required for an

effective Outsourced HR Management function. Our solutions employ a matrix of technology,

domain expertise, streamlined business workflow, and highly skilled people to create tangible,

measurable, performance improvements throughout the client‟s organization.

Ascent is recognized as one of the most trusted partners in this business by clients around the

world. We work as an extension of our client‟s business. Our management and delivery teams

are passionate about building efficiencies in our clients‟ business.

Our bespoke technology solutions for HR needs are unique in the industry and are backed by the

best of industry practices in Data management, Information Security, Data Privacy, anywhere

access and very user friendly processes.

10

2.2 Vision and Mission

Vision

To be recognized as a Result Oriented, Innovative and Dedicated partner to clients, constantly

delivering effective HR Solutions that meet client expectations.

11

Mission

To partner our clients to create a competitive edge by providing the best talent and HR Solutions,

thereby enabling them to focus on their core business.

Key Attributes

Extensive and proven track record in Executive Search, Recruitment and Selection Assignments.

Strong database and domain Knowledge.

Quick turnaround time, planning and execution.

Ability to provide recruitment solutions at any operating level in the client organization.

12

Around 25 Senior Recruitment specialists on board.

Commitment to quality and perfection in every assignment undertaken.

Highest level of confidentiality maintained at all levels.

2.4 Services

1. HR Outsourcing:

As an emerging global leader in the HR Outsourcing space, Ascent provides intuitive and

customized solutions to any enterprise irrespective of its size / scale. Our solutions address the

needs from integrated HR outsourcing solutions or complicated multi country Payroll services to

handling benefits and Compliance services across the world.

Payroll & Compliance

Payroll processing is a mundane, repetitive and data-intense activity which can be a drain on the

productivity, resource utilization and costs, in the HR function of any organization.

Benefits Consulting

Our decade-long experience has helped us develop and deliver tax-efficient Flexible Benefit

structures that meet both the employee‟s needs as well as organizational needs.

Labour Compliances

13

While designing these solutions, we are cognizant of the fact that every enterprise must be

treated differently when it comes to labour relations.

HR Consulting

Ascent has the knowledge and ability to provide HR consulting solutions across the value chain,

right from acquisition planning to cost optimization to separation management design.

Training Support

Extensive training plans for clients to ensure better management of HR services, compensation

planning, benefits planning, and compliance.

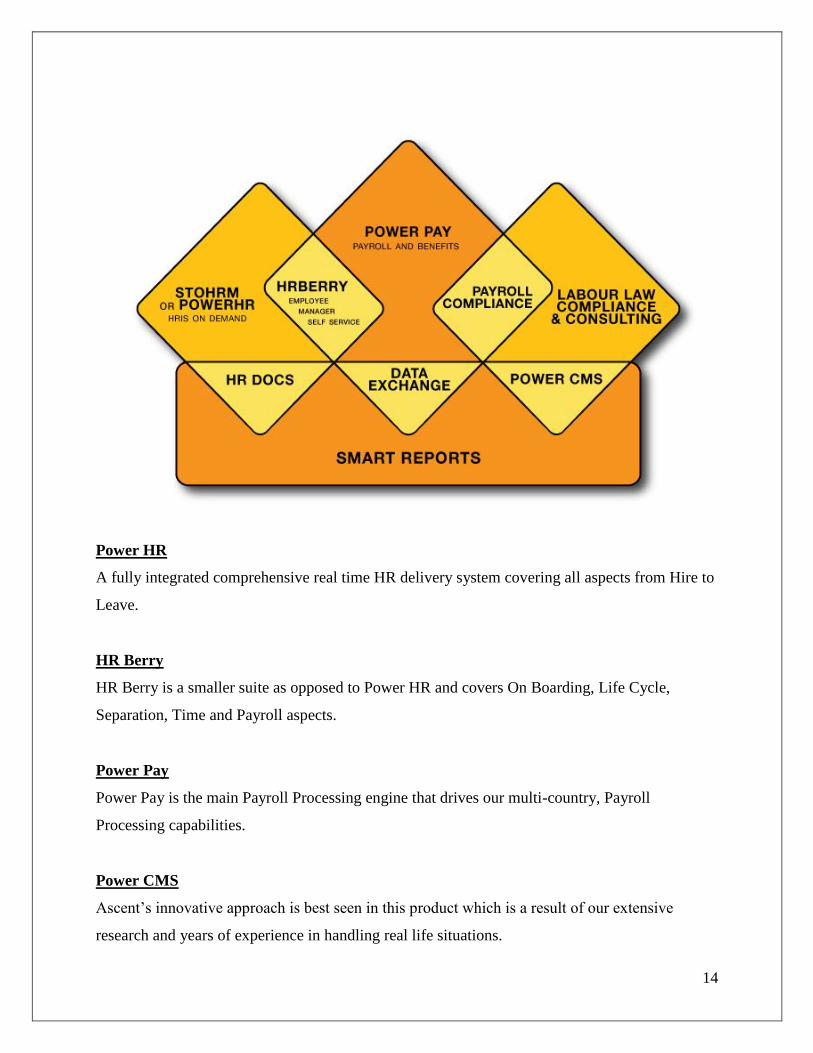

2. HR AUTOMATION

Ascent‟s HR Automation suite comprises five different applications, built over a knowledge base

of vast experience and real life scenarios.

14

Power HR

A fully integrated comprehensive real time HR delivery system covering all aspects from Hire to

Leave.

HR Berry

HR Berry is a smaller suite as opposed to Power HR and covers On Boarding, Life Cycle,

Separation, Time and Payroll aspects.

Power Pay

Power Pay is the main Payroll Processing engine that drives our multi-country, Payroll

Processing capabilities.

Power CMS

Ascent‟s innovative approach is best seen in this product which is a result of our extensive

research and years of experience in handling real life situations.

15

Chapter 3

Theoretical background

3.1 MUTUAL FUND IN INDIA

Concept of mutual fund entered Indian financial scene way back in 1964 that was famous unit 64

later earned famed under name of US 64 had a near monopoly status for more that 2 decades.

This fund was a public sector closed ended fund that list of fund holdings are allocation of total

assets amongst various assets statements was never known to the investing public. It was only at

economic liberalization process that began after 1991 that Indian financial sector began opening

up. This it was in year 1993 the first privet sector open-ended mutual fund was launched by the

Kothari pioneer asset management company. This blue chip fund and prima fund (both equity

funds) provided first hand of competition to Unit Trust of India. Suddenly, Indian investor had

wide range of invest opportunity, were not available in pre-reforms era between 1997 to 2001

tremendous growth of Indian Mutual Fund Industry with number of players increasing and

balanced funds. Between years 1998-2001 boom in Indian stock market was led by InfoTech

companies. Huge project margins saw an unprecedented rise share prices. This was time when

some AMC launched IT sector mutual fund.

SEBI Regulations On Mutual Funds

The Government brought Mutual Funds in the Securities market under the regulatory

framework of the Securities and Exchange board of India (SEBI) in the year 1993. SEBI issued

guidelines in the year 1991 and comprehensive set of regulations relating to the organization and

management of Mutual Funds in 1993.

16

3.2 ADVANTAGES AND DISADVENTAGE OF MUTUAL FUND

ADVANTAGES OF MUTUAL FUND:

1. Portfolio Diversification: Mutual Funds invest in a well-diversified portfolio of

securities which enables investor to hold a diversified investment portfolio (whether the

amount of investment is big or small).

2. Professional Management: Fund manager undergoes through various research works

and has better investment management skills, which ensure higher returns to the investor

than what he can manage on his own.

3. Less Risk: Investors acquire a diversified portfolio of securities even with a small

investment in a Mutual Fund. The risk in a diversified portfolio is lesser than investing in

merely 2 or 3 securities.

4. Low Transaction Costs: Due to the economies of scale (benefits of larger volumes),

mutual funds pay lesser transaction costs. These benefits are passed on to the investors.

5. Flexibility: Investors also benefit from the convenience and flexibility offered by

Mutual Funds. Investors can switch their holdings from a debt scheme to an equity

scheme and vice-versa. Option of systematic (at regular intervals) investment and

withdrawal is also offered to the investors in most open-end schemes.

6. Safety: Mutual Fund industry is part of a well-regulated investment environment where

the interests of the investors are protected by the regulator. All funds are registered with

SEBI and complete transparency is force

DISADVANTAGES OF MUTUAL FUND

1. Cost control not in the Hands of an Investor: Investor has to pay investment

management fees and fund distribution costs as a percentage of the value of his

investments (as long as he holds the units), irrespective of the performance of the fund.

2. No Customized Portfolios: The portfolio of securities in which a fund invests is a

decision taken by the fund manager. Investors have no right to interfere in the decision

making process of a fund manager, which some investors find as a constraint in achieving

their financial objectives.

17

3. Difficulty in Selecting a Suitable Fund Scheme: Many investors find it difficult to

select one option from the plethora of funds/schemes/plans available

3.3 Types of Mutual Fund schemes-

A. Schemes according to Maturity Period:

A mutual fund scheme can be classified into open-ended scheme or close-ended scheme

depending on its maturity period.

Open-ended Fund/ Scheme

An open-ended fund or scheme is one that is available for subscription and repurchase on

a continuous basis. These schemes do not have a fixed maturity period. Investors can

conveniently buy and sell units at Net Asset Value (NAV) related prices which are declared on a

daily basis. The key feature of open-end schemes is liquidity.

Close-ended Fund/ Scheme

A close-ended fund or scheme has a stipulated maturity period e.g. 5-7 years. The fund is

open for subscription only during a specified period at the time of launch of the scheme.

Investors can invest in the scheme at the time of the initial public issue and thereafter they can

buy or sell the units of the scheme on the stock exchanges where the units are listed. In order to

provide an exit route to the investors, some close-ended funds give an option of selling back the

units to the mutual funds NAV related prices. SEBI Regulations stipulate that at least one of the

two exit routes is provided to the investor i.e. either repurchase facility or through listing on

stock exchanges. These mutual funds schemes disclose NAV generally on weekly basis.

B. Schemes according to Investment Objective:

A scheme can also be classified as growth scheme, income scheme, or balanced scheme

considering its investment objective. Such schemes may be open-ended or close-ended schemes

as described earlier. Such schemes may be classified mainly as follows.

18

1 Equity Funds-

Equity funds are considered to be the more risky funds as compared to other fund types,

but they also provide higher returns than other funds. It is advisable that an investor looking to

invest in an equity fund should invest for long term i.e. for 3 years or more. There are different

types of equity funds each falling into different risk bracket. In the order of decreasing risk level,

there are following types of equity funds:

Growth Funds - Growth Funds also invest for capital appreciation (with time horizon of 3

to 5 years) but they are different from Aggressive Growth Funds in the sense that they

invest in companies that are expected to outperform the market in the future. Without

entirely adopting speculative strategies, Growth Funds invest in those companies that are

expected to post above average earnings in the future.

Sector Funds: Equity funds that invest in a particular sector/industry of the market are

known as Sector Funds. The exposure of these funds is limited to a particular sector (say

Information Technology, Auto, Banking, Pharmaceuticals or Fast Moving Consumer

Goods) which is why they are more risky than equity funds that invest in multiple sectors.

Mid-Cap or Small-Cap Funds: Funds that invest in companies having lower market

capitalization than large capitalization companies are called Mid-Cap or Small-Cap Funds.

Market capitalization of Mid-Cap companies is less than that of big, blue chip companies

(less than Rs. 2500 crores but more than Rs. 500 crores) and Small-Cap companies have

market capitalization of less than Rs. 500 crores. Market Capitalization of a company can

be calculated by multiplying the market Price of the company's share by the total number

of its outstanding shares in the market. The shares of Mid-Cap or Small-Cap Companies

are not as liquid as of Large-Cap Companies which gives rise to volatility in share prices of

these companies and consequently, investment gets risky.

Equity Linked Saving Scheme- These funds are well diversified and reduce sector-specific

or company-specific risk. However, like all other funds diversified equity funds too are

exposed to equity market risk. One prominent type of diversified equity fund in India is

Equity Linked Savings Schemes (ELSS). As per the mandate, a minimum of 90% of

investments by ELSS should be in equities at all times. ELSS investors are eligible to claim

deduction from taxable income (up to Rs 1 lakh) in the past.

19

Dividend Yield Funds -The objective of Equity Income or Dividend Yield Equity Funds is

to generate high recurring income and steady capital appreciation for investors by investing

in those companies, which issue high dividends. Equity Income or Dividend Yield Equity

Funds are generally exposed to the lowest risk level as compared to other equity funds.

Gold Fund- The objective of this fund is accumulating the money at the gold rate according

to the units held by the investors. This is one of the new funds introduced. Here all the

investors will invest for the pool account of mutual fund and that amount is invested in the

gold. And according to the fluctuation of the rates of gold in the market, fund manager

invest when rates are in good rates like this profit earned from this gold fund is distributed

according to the units held by the investors

2. Debt funds-

Funds that invest in medium to long-term debt instruments issued by private

companies, banks, financial institutions, governments and other entities belonging to various

sectors (like infrastructure companies etc.) are known as Debt / Income Funds. Debt funds are

low risk profile funds that seek to generate fixed current income (and not capital appreciation) to

investors. In order to ensure regular income to investors, debt (or income) funds distribute

large fraction of their surplus to investors. Although debt securities are generally less risky than

equities, they are subject to credit risk (risk of default) by the issuer at the time of interest or

principal payment. To minimize the risk of

Default, debt funds usually invest in securities from issuers who are rated by credit rating

agencies and are considered to be of "Investment Grade". Debt funds that target high returns are

more risky. Based on different investment objectives, there can be following types of debt funds:

Diversified Debt Funds - Debt funds that invest in all securities issued by entities belonging

to all sectors of the market are known as diversified debt funds. The best feature of

diversified debt funds is that investments are properly diversified into all sectors which

results in risk reduction. Any loss incurred, on account of default by a debt issuer, is shared

by all investors which further reduces risk for an individual investor.

20

High Yield Debt funds - Understand the risk of default is present in all debt funds, and

therefore, debt funds generally try to minimize the risk of default by investing in securities

issued by only those borrowers who are considered to be of "investment grade". But, High

Yield Debt Funds adopt a different strategy and prefer securities issued by those issuers who

are considered to be of "below investment grade". The motive behind adopting this sort of

risky strategy is to earn higher interest returns from these issuers. These funds are more

volatile and bear higher default risk, although they may earn at times higher returns for

investors.

Assured Return Funds - Although it is not necessary that a fund will meet its objectives or

provide assured returns to investors, but there can be funds that come with a lock-in period

and offer assurance of annual returns to investors during the lock-in period. Any shortfall in

returns is suffered by the sponsors or the Asset Management Companies (AMCs). These

funds are generally debt funds and provide investors with a low-risk investment opportunity.

Fixed Term Plan Series - Fixed Term Plan Series usually are closed-end schemes having

short-term maturity period (of less than one year) that offer a series of plans and issue units

to investors at regular intervals. Unlike closed-end funds, fixed term plans are not listed on

the exchanges. Fixed term plan series usually invest in debt / income schemes and target

short-term investors. The objective of fixed term plan schemes is to gratify investors by

generating some expected returns in a short period.

3. Balanced Fund-

A balanced fund is one that has a portfolio comprising debt instruments, convertible

securities, and Preference equity shares. Their assets are generally held in more or less equal

proportions between debt/money market securities and equities. By investing in a mix of this

nature, balanced funds seek to attain the objectives of income, moderate capital appreciation

and preservation of capital, and are ideal for investors with a conservative and long-term

orientation.

.

21

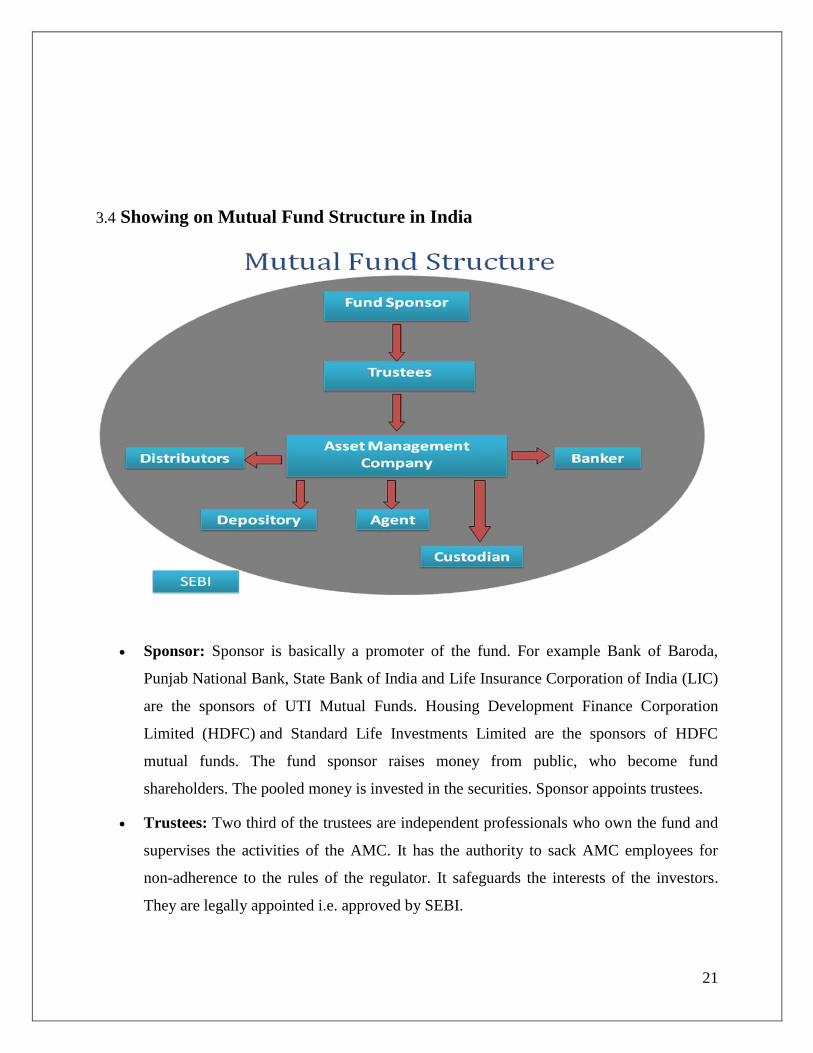

3.4 Showing on Mutual Fund Structure in India

Sponsor: Sponsor is basically a promoter of the fund. For example Bank of Baroda,

Punjab National Bank, State Bank of India and Life Insurance Corporation of India (LIC)

are the sponsors of UTI Mutual Funds. Housing Development Finance Corporation

Limited (HDFC) and Standard Life Investments Limited are the sponsors of HDFC

mutual funds. The fund sponsor raises money from public, who become fund

shareholders. The pooled money is invested in the securities. Sponsor appoints trustees.

Trustees: Two third of the trustees are independent professionals who own the fund and

supervises the activities of the AMC. It has the authority to sack AMC employees for

non-adherence to the rules of the regulator. It safeguards the interests of the investors.

They are legally appointed i.e. approved by SEBI.

22

AMC: Asset Management Company (AMC) is a set of financial professionals who

manage the fund. It takes decisions on when and where to invest the money. It doesn‟t

own the money. AMC is only a fee-for-service provider.

The above 3 tier structure of Indian mutual funds is very strong and virtually no chance

for fraud.

Custodian: A Custodian keeps safe custody of the investments (related documents of

securities invested). A custodian should be a registered entity with SEBI. If the promoter

holds 50% voting rights in the custodian company it can‟t be appointed as custodian for

the fund. This is to avoid influence of the promoter on the custodian. It may also provide

fund accounting services and transfer agent services. JP Morgan Chase is one of the

leading custodians.

Transfer Agents: Transfer Agent Company interfaces with the customers, issue a fund‟s

units, help investors while redeeming units. Provides balance statements and fund

performance fact sheets to the investors.

Flow of operation:

A Mutual Fund is a trust that pools the savings of a number of investors who share a

common financial goal. The money thus collected is then invested in capital market instruments

such as shares, debentures and other securities. The income earned through these investments

and the capital appreciation realised are shared by its unit holders in proportion to the number of

units owned by them. Thus a Mutual Fund is the most suitable investment for the common man

as it offers an opportunity to invest in a diversified, professionally managed basket of securities

at a relatively low cost. The flow chart below describes broadly the working of a mutual fund

23

3.5 Showing on Mutual Fund operation flow chart

Mutual fund schemes may be classified on the basis of:

By its maturity and

By its investment objective

By Maturity:

Open-ended Funds:

An open-end fund is one that is available for subscription all through the year. These do

not have a fixed maturity. Investors can conveniently buy and sell units at Net Asset

Value ("NAV") related prices. The key feature of open-end schemes is liquidity.

24

Closed-ended Funds:

A closed-end fund has a stipulated maturity period which generally ranging from 3 to 15

years. The fund is open for subscription only during a specified period. Investors can

invest in the scheme at the time of the initial public issue and thereafter they can buy or

sell the units of the scheme on the stock exchanges where they are listed.

In order to provide an exit route to the investors, some close-ended funds give an option

of selling back the units to the Mutual Fund through periodic repurchase at NAV related

prices. SEBI Regulations stipulate that at least one of the two exit routes is provided to

the investor.

Interval Funds

Interval funds combine the features of open-ended and close-ended schemes. They are

open for sale or redemption during pre-determined intervals at NAV related prices.

By Investment Objective:

Growth Funds:

The aim of growth funds is to provide capital appreciation over the medium to long-

term. Such schemes normally invest a majority of their corpus in equities. It has been

proven that returns from stocks, have outperformed most other kind of investments held

over the long term. Growth schemes are ideal for investors having a long-term outlook

seeking growth over a period of time.

Income Funds:

The aim of income funds is to provide regular and steady income to investors. Such

schemes generally invest in fixed income securities such as bonds, corporate debentures

and Government securities. Income Funds are ideal for capital stability and regular

income.

Balanced Funds:

The aim of balanced funds is to provide both growth and regular income. Such schemes

periodically distribute a part of their earning and invest both in equities and fixed income

securities in the proportion indicated in their offer documents. In a rising stock market,

the NAV of these schemes may not normally keep pace, or fall equally when the market

25

falls. These are ideal for investors looking for a combination of income and moderate

growth.

Money Market Funds:

The aim of money market funds is to provide easy liquidity, preservation of capital and

moderate income. These schemes generally invest in safer short-term instruments such as

treasury bills, certificates of deposit, commercial paper and inter-bank call money.

Returns on these schemes may fluctuate depending upon the interest rates prevailing in

the market. These are ideal for corporate and individual investors as a means to park their

surplus funds for short periods.

Tax Saving Schemes:

These schemes offer tax rebates to the investors under specific provisions of the Indian

Income Tax laws as the Government offers tax incentives for investment in specified

avenues. Investments made in Equity Linked Savings Schemes (ELSS) and Pension

Schemes are allowed as deduction u/s 88 of the Income Tax Act, 1961. The Act also

provides opportunities to investors to save capital gains u/s 54EA and 54EB by investing

in Mutual Funds.

Index funds: :

Index Funds invest their corpus on the specified index such as BSE Sensex, NSE index,

etc. as mentioned in the offer document. They try to mimic the composition of the index

in their portfolio. Not only are the shares, even their weight age replicated. Index funds

are a passive investment strategy and the fund manager has a limited role to play here.

The NAVs of these funds move along with the index they are trying to mimic save for a

few points here and there. This difference is called tracking error.

Special schemes:

These schemes invest only in the industries specified in the offer document. Examples

are InfoTech funds, FMCG funds, pharmacy funds, etc These scheme are mean for

aggressive and well-informed investors.

RISK V/S REWARD

Volatility in the market activity can be referred to as the risk in the mutual fund

26

investment. The sudden upward and downward sentiments of the markets and individual issues

can be attributed to several key factors. These factors comprise:

Inflation

Interest rate changes

General economic scenario

The aforementioned factors are the main cause of worry amongst the investors. Most of the

investors fear that the value of the stock they have invested will fall considerably. However, it is

here one can notice its reward angle. It is this element of volatility that can also bring them

substantial long-term return in comparison to a savings account.

3.6 BEST MUTUAL FUNDS IN INDIA

Before knowing about the best mutual fund in India. It is important to know the

factors that actually decide their fate in the market. In order to get an actual ideal of the best

performing mutual funds in the market, one need to track its current Net Asset Value or NAV.

NAV stands for the latest market value of the holdings of a fund that brings down the fund's

liabilities, which are generally indicated in terms of per share amount. On a daily basis, most of

the funds' NAV is decided. This is determined after the trade closes on certain financial

exchanges. The net asset value of the mutual funds is ascertained at the end of the trading day.

An increase in NAV signifies rise in the holdings of the shareholder. The Fund Firm will then do

the transaction on the shares along with the sales fees. While open-ended net asset value of the

mutual funds is issued daily, the close-ended NAV of the mutual fund is released on a weekly

basis. You can calculate net asset value of the mutual fund easily. Track the latest market value

of the net assets of the fund and then subtract that by the number of outstanding shares.

Top mutual funds in India

Here are some of the top mutual funds in India that are listed below:

Reliance Mutual Fund.

The DSP ML Tiger Fund.

SBI Magnum Contra Fund.

HDFC Equity Fund.

27

Prudential ICICI mutual Fund.

SBI Mutual Fund.

3.7 Some facts for the growth of mutual fund industry in India:

a) 100% growth in the last 6 years.

b) Numbers of foreign AMC‟s are in the queue to enter the Indian markets like Fidelity

Investments, US based, with over US$1trillion assets under management worldwide.

c) Our saving rate is over 23%, highest in the world. Only channelizing these savings in

mutual funds sector is required.

d) We have approximately 37 mutual funds which are much less than US having more than

800. There is a big scope for expansion.

e) 'B' and 'C' class cities are growing rapidly. Today most of the mutual funds are

concentrating on the 'A' class cities. Soon they will find scope in the growing cities.

f) Mutual fund can penetrate rural like the Indian insurance industry with simple and

limited products

g) SEBI allowing the MF's to launch commodity mutual funds.

h) Emphasis on better corporate governance.

i) Trying to curb the late trading practices.

j) Introduction of Financial Planners who can provide need based advice.

The Indian mutual funds business is expected to grow significantly in the coming years

due to a high degree of transparency and disclosure standards comparable to anywhere in the

world, though there are many challenges that need to be addressed to increase net mobilization of

funds in this sector, as said by Mr. A.P. Kurian, Chairman of the Association of Mutual Funds of

India.

28

Indian Mutual fund industry exhibited 200% growth in the last 10 yrs from Rs.470 billion to

Rs1400 billion in terms of assets under management. The Mutual Funds industry is expected to

jump sharply from its present share of 6% of GDP to 40% in the next 10yrs provided the

country‟s growth rate is consistently above 6%. The growing investor preference for mutual

funds has resulted in the assets under management of mutual funds growing 8-folds in last 5 yrs.

Number of foreign AMC's are in the queue to enter the Indian markets like US based Fidelity

Investments, with over US$1trillion assets under management worldwide. Our saving rate is over

23%, highest in the world. Only channelling these savings in mutual funds sector is required.

There is a big scope for expansion as we have 37 mutual funds which is much less than US

having more than 800.

3.8 Role of mutual fund in stock exchange:

Mutual funds are an ideal vehicle for investment by retail investors in the stock market for

several reasons.

a) It pools investments of small investors together increasingly thereby the participation in the

stock market.

b) Mutual funds being institutional investors, can invest in market analysis generally not

available or accessible to individual investors, providing therefore informed decisions to

small investors.

c) Mutual fund can diversify the portfolio in better way as compared with individual investors

due to the expertise and availability of funds.

29

Chapter 4

ANALYSIS AND INTERPRETATION OF DATA

The analysis and interpretation of data covers an overview of the Mutual fund segment, other

related data with percentage and narrative data, supported by charts and tables form the

information collected during the project study.

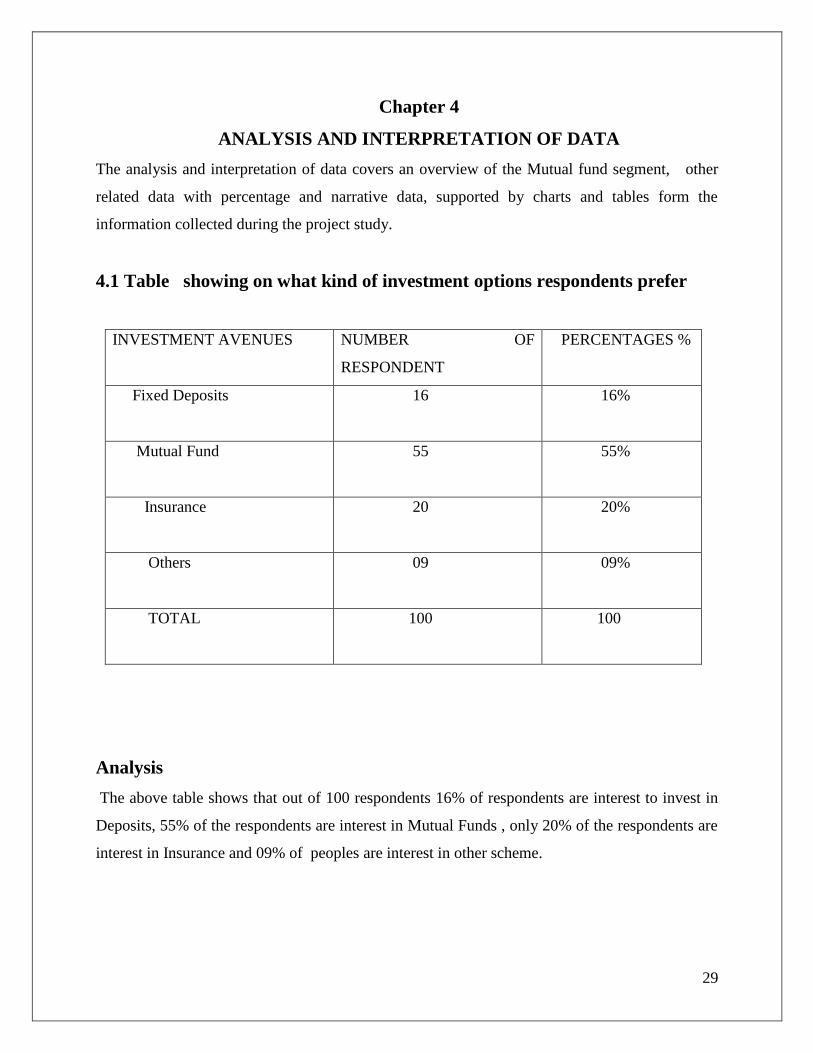

4.1 Table showing on what kind of investment options respondents prefer

INVESTMENT AVENUES

NUMBER OF

RESPONDENT

PERCENTAGES %

Fixed Deposits

16 16%

Mutual Fund

55 55%

Insurance

20 20%

Others

09 09%

TOTAL

100 100

Analysis

The above table shows that out of 100 respondents 16% of respondents are interest to invest in

Deposits, 55% of the respondents are interest in Mutual Funds , only 20% of the respondents are

interest in Insurance and 09% of peoples are interest in other scheme.

30

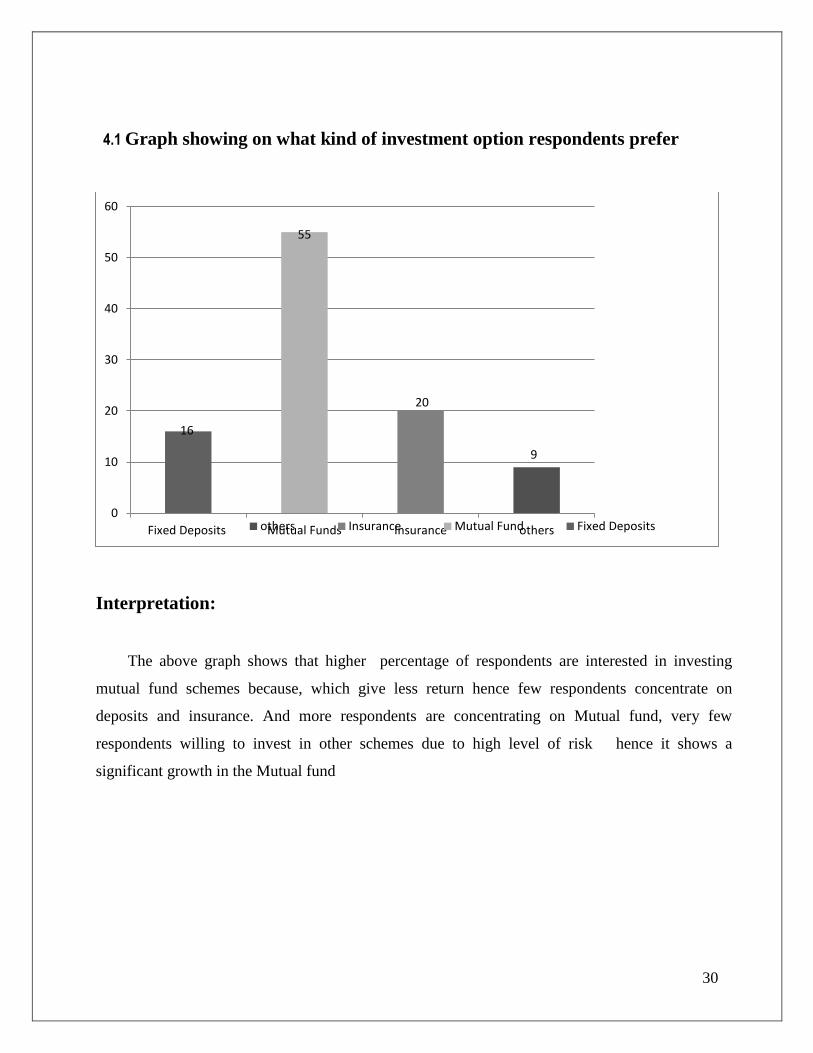

4.1 Graph showing on what kind of investment option respondents prefer

Interpretation:

The above graph shows that higher percentage of respondents are interested in investing

mutual fund schemes because, which give less return hence few respondents concentrate on

deposits and insurance. And more respondents are concentrating on Mutual fund, very few

respondents willing to invest in other schemes due to high level of risk hence it shows a

significant growth in the Mutual fund

16

55

20

9

0

10

20

30

40

50

60

Fixed Deposits Mutual Funds Insurance othersothers Insurance Mutual Fund Fixed Deposits

31

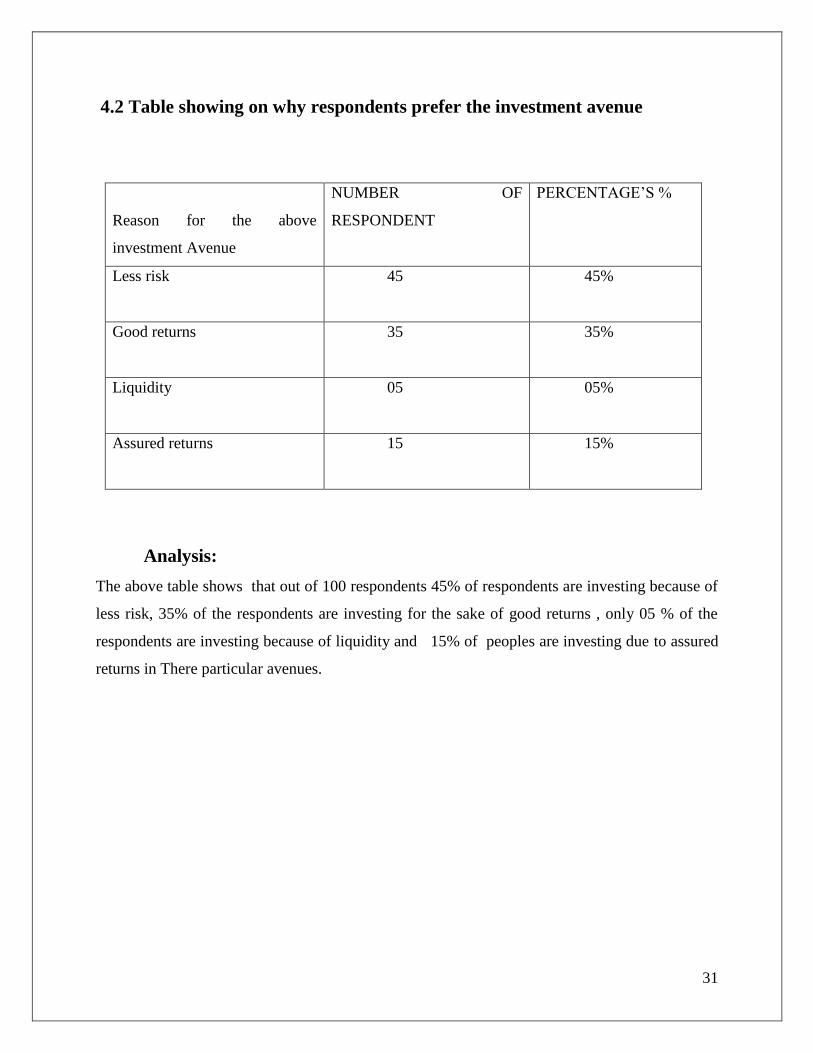

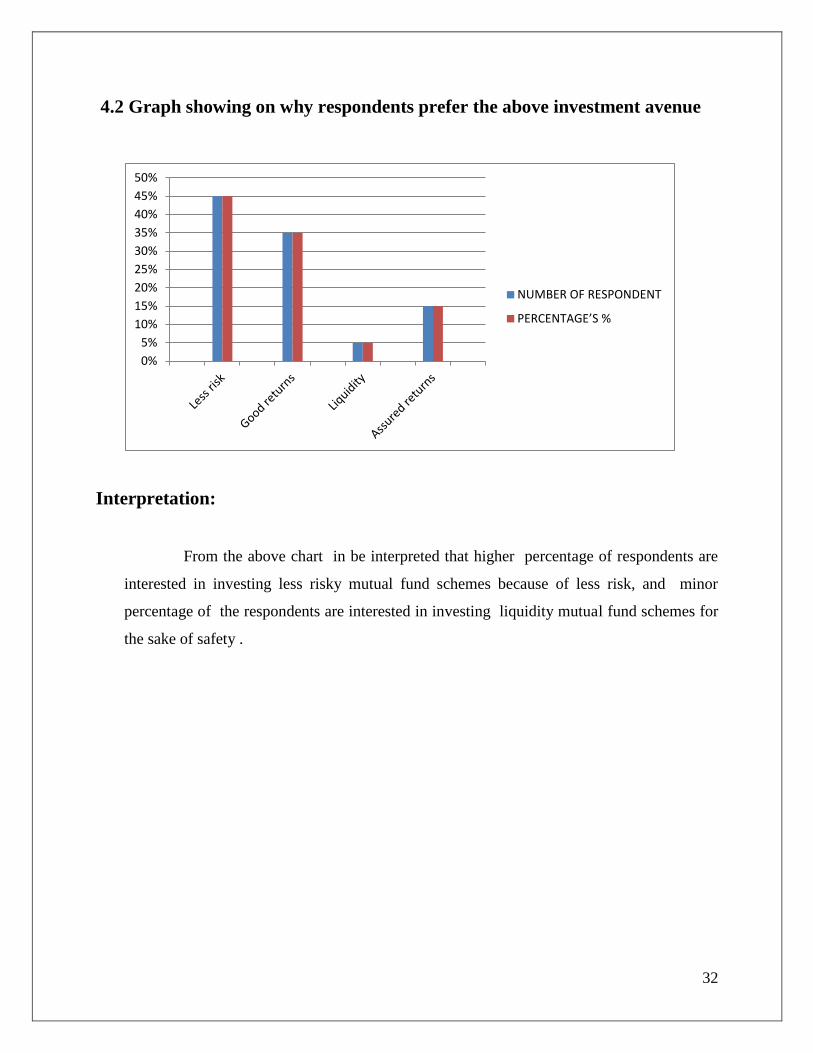

4.2 Table showing on why respondents prefer the investment avenue

Reason for the above

investment Avenue

NUMBER OF

RESPONDENT

PERCENTAGE‟S %

Less risk

45 45%

Good returns

35 35%

Liquidity

05 05%

Assured returns

15 15%

Analysis:

The above table shows that out of 100 respondents 45% of respondents are investing because of

less risk, 35% of the respondents are investing for the sake of good returns , only 05 % of the

respondents are investing because of liquidity and 15% of peoples are investing due to assured

returns in There particular avenues.

32

4.2 Graph showing on why respondents prefer the above investment avenue

Interpretation:

From the above chart in be interpreted that higher percentage of respondents are

interested in investing less risky mutual fund schemes because of less risk, and minor

percentage of the respondents are interested in investing liquidity mutual fund schemes for

the sake of safety .

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

NUMBER OF RESPONDENT

PERCENTAGE’S %

33

4.3 Table showing current investment portfolio:

Current portfolio

NUMBER OF

RESPONDENTS

PERCENTAGE‟S %

Govt. securities and Bonds

30 30%

Mutual funds & fixed deposits 52 52%

Equity

13 13%

Other options

05 05%

Analysis :

The above table shows that 52% of mutual fund & fixed deposits respondents received

good return in equity and 30% of govt securities and bonds respondents are not received good

return in equity 13%. So the opinion of the customers relating to the company is good. The

company as to give more importance to satisfaction of the customers.

34

4.3 Graph showing on current investment portfolio:

Interpretation:

From the above chart shows that higher percentage of respondents are interested in investing

in less risky mutual fund schemes because of mutual fund fixed deposits, and minor percentage

of the respondents are interested in investing other options mutual fund schemes for the sake of

safety

35

4.4 Table showing on the awareness of mutual funds.

AWARENES OF MUTUAL

FUND

NUMBER OF

RESPONDENT

PERCENTAGES %

Yes

85 85%

No

15 15%

Total

100 100

Analysis:

From the above table showing mutual fund awareness of the respondents out of 100%. Most

of them are known about the mutual Fund, 85% of the respondents are having knowledge about

mutual fund only few people are not aware of mutual Fund i.e. only 15%

36

4.4 Graph showing on the awareness of mutual funds.

Interpretation

From the above chart showing Mutual Fund awareness of the respondents while conducting

survey was choose most of the post graduate and graduate since all those people having good

knowledge of mutual fund. Hence chart shows majority of the respondents are having aware of

mutual fund and remaining respondents are not aware of mutual funds.

0

10

20

30

40

50

60

70

80

90

YesNo

85

15 Yes

No

37

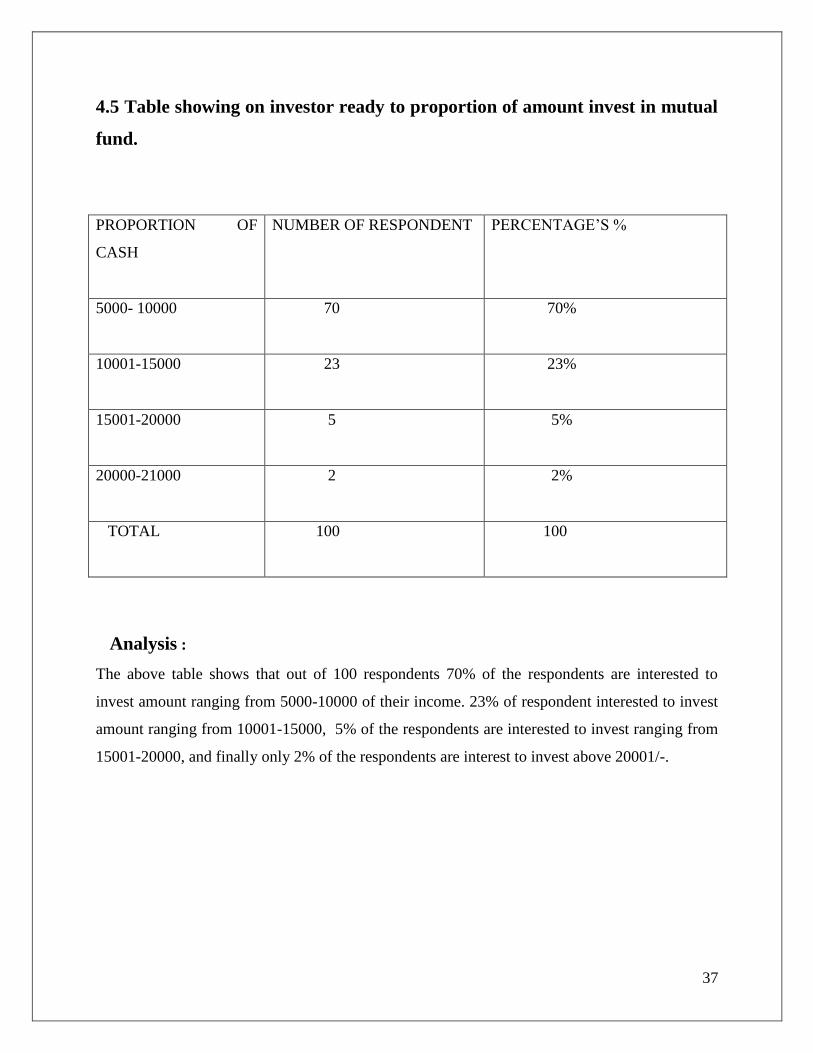

4.5 Table showing on investor ready to proportion of amount invest in mutual

fund.

PROPORTION OF

CASH

NUMBER OF RESPONDENT PERCENTAGE‟S %

5000- 10000

70 70%

10001-15000

23 23%

15001-20000

5 5%

20000-21000

2 2%

TOTAL

100 100

Analysis :

The above table shows that out of 100 respondents 70% of the respondents are interested to

invest amount ranging from 5000-10000 of their income. 23% of respondent interested to invest

amount ranging from 10001-15000, 5% of the respondents are interested to invest ranging from

15001-20000, and finally only 2% of the respondents are interest to invest above 20001/-.

38

4.5 Graph showing on Investor ready to proportion of amount invests in

Mutual fund.

Interpretation:

From the above chart showing a graph shows maximum that is 70

respondents are interested to invest the amount ranging from 5000-10000, And some

others are interested ranging from 10001-15000, and very few i.e. 5 the respondents are

interest to invest ranging from 15001-20000, and finally 2 the respondents are interest to

invest above 20001/-.

70

23

5 2

0

10

20

30

40

50

60

70

80

5000-10000 10001-15000 15001-20000 20001-Above

20001-Above

15001-20000

10001-15000

5000-10000

39

4.6 Table showing respondent’s interest to the area investor in mutual fund.

INVESTMENT

NUMBER OF RESPONDENT PERCENTAGES %

Yes

68 68%

No

32 32%

Total

100 100

Analysis:

The above table shows that out of 100 respondents 68% of the respondents are invested in

various mutual fund schemes, only 32% of the respondents have not made their investment in

mutual funds.

40

4.6 Graph showing respondent’s interest to the area investor in mutual fund.

Interpretation:

From the above graph shows maximum that is majority of respondents are interested to invest

the amount interest to the area investor in mutual fund And some others are interested in mutual

fund, and very higher of the respondents are interest to invest. Very few of the respondents are

interest to invest in mutual fund.

41

4.7 Table Showing on Investors opinion of open ended and close ended

scheme.

SCHEME

NUMBER OF

RESPONDENT

PERCENTAGES %

Open ended

48 48%

Close ended

4 4%

Both

48 48%

TOTAL

100 100

Analysis:

The above table shows that out of 100 respondents 48% of the respondents prefer open- ended

type of Mutual Fund scheme, 4% of the respondents are prefer close-ended Mutual Fund scheme

and 48% of respondents are prefer both open-ended and close-ended scheme.

42

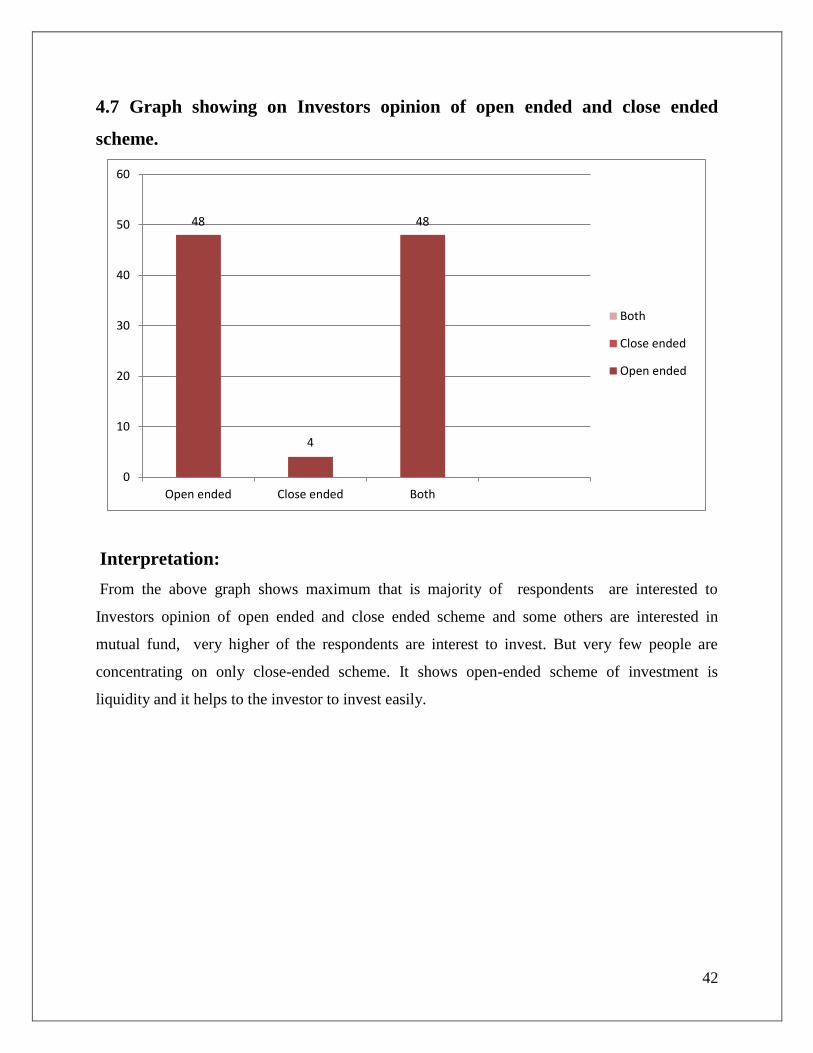

4.7 Graph showing on Investors opinion of open ended and close ended

scheme.

Interpretation:

From the above graph shows maximum that is majority of respondents are interested to

Investors opinion of open ended and close ended scheme and some others are interested in

mutual fund, very higher of the respondents are interest to invest. But very few people are

concentrating on only close-ended scheme. It shows open-ended scheme of investment is

liquidity and it helps to the investor to invest easily.

48

4

48

0

10

20

30

40

50

60

Open ended Close ended Both

Both

Close ended

Open ended

43

4.8 Table showing on schemes preferred by the investors:

SCHEME

NUMBER OF

RESPONDENT

PERCENTAGES %

Equity

36 36%

Debt

24 24%

Balanced

40 40%

TOTAL

100 100

Analysis:

The above table shows that out of 100 respondents 36% of the respondents prefer Equity type of

scheme, 24% of the respondents are prefer Debt scheme and 40% of respondents are prefer

Balanced scheme.

44

4.8 Graph showing this graph showing on schemes preferred by the investors:

Interpretation:

From the above chart showing It is clear from the out of 100 respondents 36 the respondents

prefer Equity type of scheme, 24 the respondents are prefer Debt scheme and 40 of respondents

are prefer Balanced scheme.

4.9 Table showing on while buying a mutual fund.

SCHEME

NUMBER OF

RESPONDENT

PERCENTAGES %

YES

90 90%

NO

10 10%

TOTAL 100 100

Series1

Series2

0

5

10

15

20

25

30

35

40

1 2 3 4 5 6

36

24

40

Series1

Series2

45

Analysis:

The above table shows that out of 100 respondents for making an investment 90% of the

respondents prefer the brand name to invest, only 10% of the respondents do not prefer brand

name for making an investment.

4.9 Graph showing on while buying a Mutual Fund.

Interpretation:

From the above chart showing high 90 by respondents prefer brand name by denoted buying

decision mutual fund and equity share prefer more and more brand it is level 10 of the

respondent‟s mutual funds I have to discuss about mutual currier growth. Brand which is

acquired good brand investor.

46

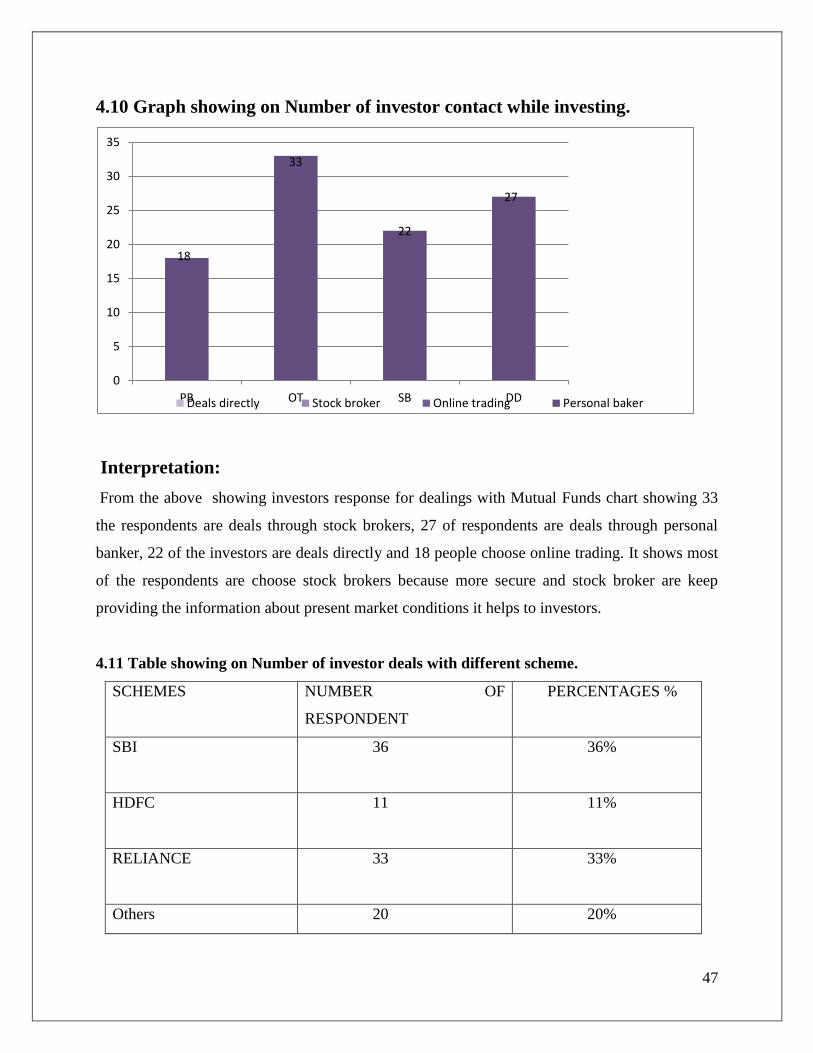

4.10 Table showing on Number of investor contact while investing.

PARTICULAR

NUMBER OF

RESPONDENT

PERCENTAGES %

Personal Banker

18 18%

Online Trader

33 33%

Stock Broker

22 22%

Deals directly

27 27%

TOTAL

100 100

Analysis :

From the above table showing investors response for while deals with Mutual Fund out of 100

people 18% of the respondent are deals through personal banker, 33% of the respondents are

deals through online trading, 22% are deals through stock brokers and 27% people are deals

directly.

47

4.10 Graph showing on Number of investor contact while investing.

Interpretation:

From the above showing investors response for dealings with Mutual Funds chart showing 33

the respondents are deals through stock brokers, 27 of respondents are deals through personal

banker, 22 of the investors are deals directly and 18 people choose online trading. It shows most

of the respondents are choose stock brokers because more secure and stock broker are keep

providing the information about present market conditions it helps to investors.

4.11 Table showing on Number of investor deals with different scheme.

SCHEMES

NUMBER OF

RESPONDENT

PERCENTAGES %

SBI

36 36%

HDFC

11 11%

RELIANCE

33 33%

Others 20 20%

18

33

22

27

0

5

10

15

20

25

30

35

PB OT SB DDDeals directly Stock broker Online trading Personal baker

48

TOTAL

100 100

Analysis :

From the above table showing the different scheme of Mutual Fund out 100 respondents 36%

of the investor choose SBI Mutual Fund, and 33% are choose Reliance mutual funds, 20% of the

respondents are choose Others MF, and 11% of the investors are choose HDFC.

49

4.11 Graph showing on Number of investor deals with different scheme

Interpretation:

From the above chart clearly showing most of the investors are preferred to invested in SBI

Mutual Fund i.e. 36, And 33 of the investor are prefer to invest in RELIANCE Mutual Fund.

20 of the respondents prefer other Mutual Fund. And finally 11 of the respondents are

concentrate on HDFC Mutual Funds when we analyze these data it shows more number of

investor are prefer to invest SBI and RELIANCE because it shows Brand Name as well as good

returns and liquidity.

0

5

10

15

20

25

30

35

40

SBIHDFC

RELIANCE Others

36

11

33

20

Others

RELIANCE

HDFC

SBI

50

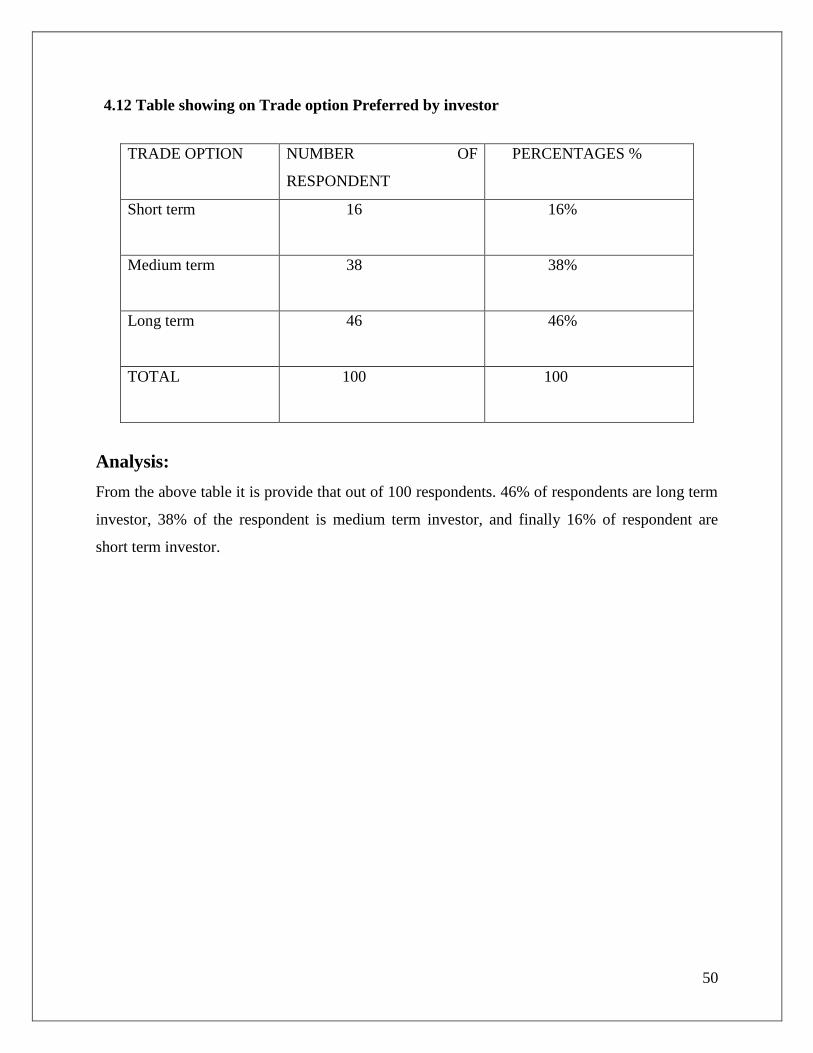

4.12 Table showing on Trade option Preferred by investor

Analysis:

From the above table it is provide that out of 100 respondents. 46% of respondents are long term

investor, 38% of the respondent is medium term investor, and finally 16% of respondent are

short term investor.

TRADE OPTION

NUMBER OF

RESPONDENT

PERCENTAGES %

Short term

16 16%

Medium term

38 38%

Long term

46 46%

TOTAL

100 100

51

4.12 Graph showing on Trade option Preferred by investor.

Interpretation:

From the above chart shows that most of the respondents are long term investor i.e. 46, and 38

the respondents are medium term investors And only few i.e. 16 are short term investor.

4.13 Table showing on Objective behind trading in Mutual Fund.

OBJECTIVE

NUMBER OF

RESPONDENT

PERCENTAGE %

For diversified the portfolio

28 28%

For Higher return

36 36%

Monthly Income

16 16%

Tax Benefit

20 20%

16

38

46

TRADE OPTION

Short term

Mediumterm

52

TOTAL

100 100

Analysis :

From the above table shows why investors are trade or choose mutual fund as a best scheme of

investment out of 101 respondents. 36% respondents are prefer to mutual fund for high return,

28% of the respondents are prefer mutual fund for diversified the income, and 20% of the

respondents are prefer for tax benefit and finally 16% of the respondents are prefer for monthly

Income.

4.13 Graph showing on Objective behind trading in Mutual Fund.

28

36

16

20

0

5

10

15

20

25

30

35

40

DP HR MI TB

Tax benefit

Monthly income

High return

Diversifide portfolio

53

Interpretation:

Form the above chart showing why investor is choosing mutual fund as a good option of

investment. It is clearly showing more number of investor is interested to invest in Mutual Fund

because of high return i.e.36. and 28 of investor are prefer to invest in Mutual Fund for

diversified the portfolio of their income, 20 of the respondents prefer for tax benefit. And finally

16 of the respondents are choosing Mutual fund because of monthly income.

4.14 Table showing on percentage of return expect in Mutual Fund.

INCOME EXPECT NUMBER OF RESPONDENT PERCENTAGES %

10% -15%

56 56%

16%-20%

21 21%

21%-25%

15 15%

26 & Above

8 8%

TOTAL

100 100

Analysis:

The above table showing investor expectation or return of the mutual fund. 56% of respondents

are expect 10% - 15% return, , and 21% of the respondents are expect 16%-20% return, and 15%

of the respondents are expect 21%-25% of return. And finally only 8% of respondents are expect

above 26% of return.

4.14 Graph showing on percentage of return expect in Mutual Fund.

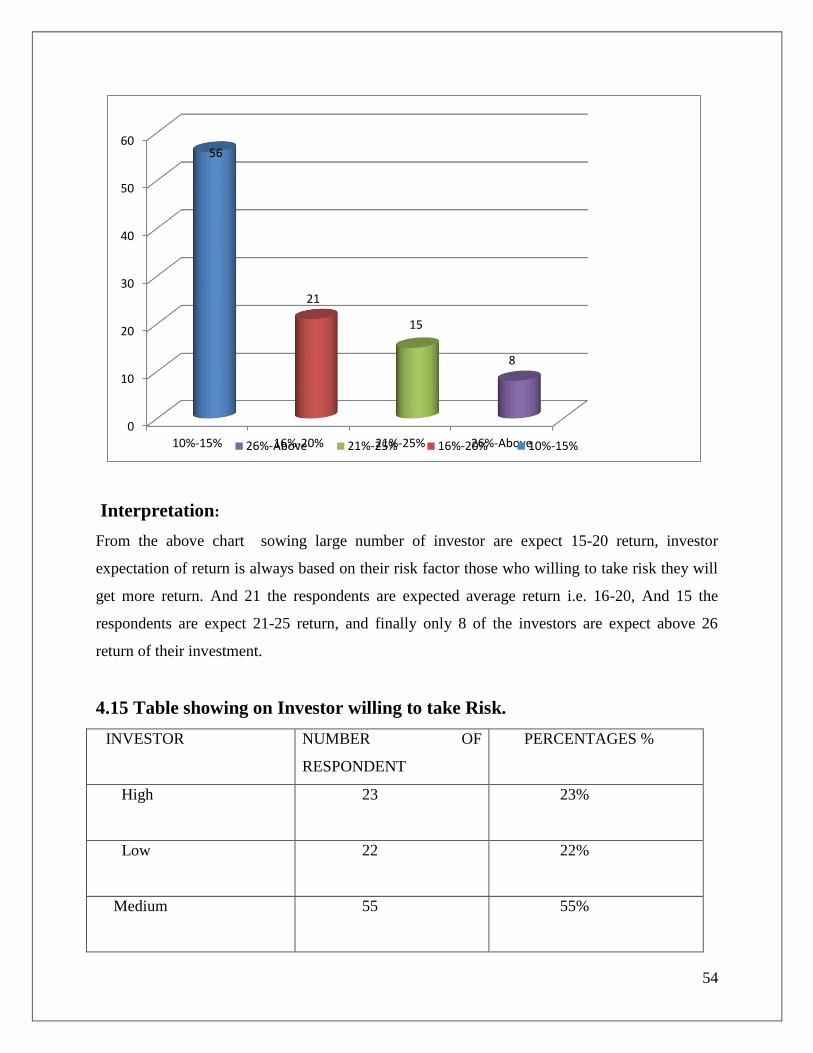

54

Interpretation:

From the above chart sowing large number of investor are expect 15-20 return, investor

expectation of return is always based on their risk factor those who willing to take risk they will

get more return. And 21 the respondents are expected average return i.e. 16-20, And 15 the

respondents are expect 21-25 return, and finally only 8 of the investors are expect above 26

return of their investment.

4.15 Table showing on Investor willing to take Risk.

INVESTOR

NUMBER OF

RESPONDENT

PERCENTAGES %

High

23 23%

Low

22 22%

Medium

55 55%

0

10

20

30

40

50

60

10%-15% 16%-20% 21%-25% 26%-Above

56

21

15

8

26%-Above 21%-25% 16%-20% 10%-15%

55

TOTAL

100 100

Analysis:

The above table shows risk factor of the investor, out 100 respondents 23% of the respondents

are high risk‟s taker , 55% of the medium risk‟s taker, and 22% of respondents are low risk‟

4.15 Graph showing on Investor willing to take Risk.

Interpretation:

From the above chart showing large number of investors are take medium risk i.e. 55, And 23 of

investor are willingly ready to take risk these persons will get more return. And 22 of the

respondents are takes low risk

23

22

55

RISK FACTOR

High Risk

Low Risk

Medium Risk

56

4.16 Table showing on Opinion about RELIANCE Mutual Fund.

OPINION

NUMBER OF

RESPONDENT

PERCENTAGE %

Excellent

3 3%

Good

53 53%

Moderate

27 27%

Not aware

17 17%

TOTAL

100 100

Analysis :

From the above table showing investors opinion of the RELIANCE MUTUAL FUND. 3% of

investor are saying excellent, 53% of the respondents are say‟s good, 27% of the respondents are

say‟s moderate, And 17% of the respondents are not aware of mutual fund

57

4.16 Graph showing on Opinion about RELIANCE Mutual Fund.

Interpretation

From the above chart showing investor opinion with RELIANCE Mutual fund. While investor

investing with reliance MF they rates the Securities. 3 respondents are rates excellent. Most of

the respondents are rates good, and 55 the respondents are rates fair, And 18 of the respondents

thought poor securities.

4.17 Table showing on Investment motive with Reliance Mutual fund.

INVESTMENT MOTIVE

NUMBER OF

RESPONDENT

PERCENTAGES %

Excellent

3 3%

Good

55 55%

Fair

40 40%

0

0.2

0.4

0.6

0.8

1

1.2

1 2 3 4 5 6 7 8 9

3%

53%

27%

17%

PERCENTAGE %

NUMBER OFRESPONDENT

OPINION

58

Poor

2 2%

TOTAL

100 100

Analysis :

From the above table showing investment motive with RELIANCE MF. 3% of the respondents

are rates excellent securities, 55% of the respondents are rates good, 40% of the respondents

rates fair, and finally 2% of the respondents are rates poor.

4.17 Graph showing on Investment motive with Reliance mutual fund.

Interpretation:

From the above chart showing investor motive with RELIANCE Mutual fund. While investor

investing with reliance MF they rates the Securities. 3 respondents are rates excellent. most of

the respondents are rates good, and 40 the respondents are rates fair, And 2 the respondents

thought poor security

0

10

20

30

40

50

60

Excellent Good Fair Poor

3

55

40

2

Poor Fair Good Excellent

59

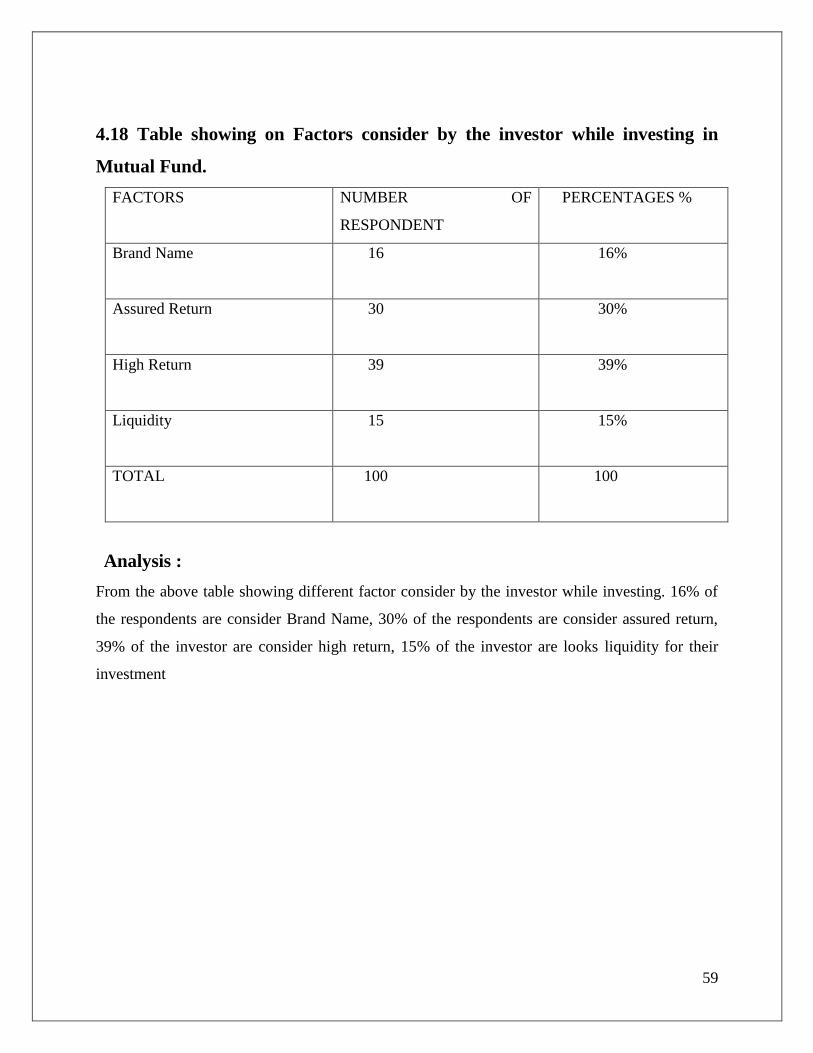

4.18 Table showing on Factors consider by the investor while investing in

Mutual Fund.

FACTORS

NUMBER OF

RESPONDENT

PERCENTAGES %

Brand Name

16 16%

Assured Return

30 30%

High Return

39 39%

Liquidity

15 15%

TOTAL

100 100

Analysis :

From the above table showing different factor consider by the investor while investing. 16% of

the respondents are consider Brand Name, 30% of the respondents are consider assured return,

39% of the investor are consider high return, 15% of the investor are looks liquidity for their

investment

60

4.18 Graph showing on Factors consider by the investor while investing in

Mutual Fund

Interpretation:

From the above chart showing most number of the investor are consider high return while they

are investing i.e. 39 the respondents. And 30 the respondents are considered assured return, and

16 the respondents are considered brand name, and few respondents are considered liquidity. 15

the investor are looks liquidity for their investment

While investing in Mutual Fund most of the respondents are looks High Return its common but

high returns is always depend on risk factor. Some others are considered Assured Return, Brand

Name, and Liquidity.

16

30

39

15

0

5

10

15

20

25

30

35

40

45

BN AR HR LTLiquidity Hihg Return Assured Return Brand Name

61

Chapter 5

FINDINGS CONCLUSION & SUGGESTIONS:

5.1 FINDINGS:

16% of respondents are interested to invest in fixed Deposits, 55% of the respondents are

interested in Mutual Funds, only 20% of the respondents are interested in Insurance and

09% of peoples are interested in other scheme.

45% of respondents are investing because of less risk, 35% of the respondents are

investing for the sake of good returns , only 05 % of the respondents are investing