Embed Size (px)

Citation preview

2009

Sunayna Ali

Gabriel A. Huppé

Yat Hong Sin

For: Professor Robert Forbes

BUSI 4709B

Strategic Management in International

Business

A Strategic Analysis

2 | P a g e

Table of Contents Executive Summary ....................................................................................................................................... 5

Firm Overview – British American Tobacco (BAT) .................................................................................... 5

External Environment Overview ............................................................................................................... 5

Industry Analysis ....................................................................................................................................... 5

Corporate and Business Level Strategy .................................................................................................... 6

Introductory Summary .................................................................................................................................. 7

Macro Environmental Analysis ..................................................................................................................... 9

Foreword .................................................................................................................................................. 9

Technological Trends ................................................................................................................................ 9

Trends Centering around Operative Efficiency. .................................................................................... 9

Trends Centering around New Product Innovation ............................................................................ 12

Economic Environment Trend ................................................................................................................ 15

North America (US as a Proxy) ............................................................................................................ 15

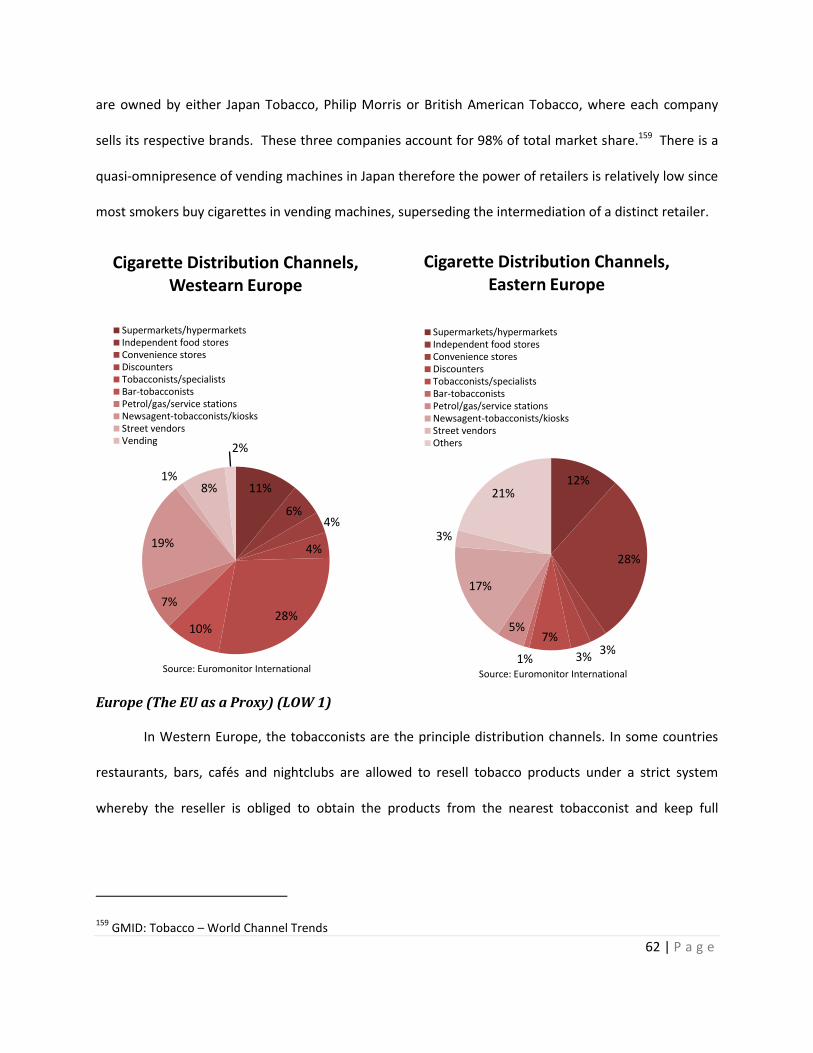

Europe (The European Union as a Proxy) ........................................................................................... 18

Asia (Japan as a Proxy) ........................................................................................................................ 20

Socio-Cultural Environment Trend ......................................................................................................... 22

North America (US as a Proxy) ............................................................................................................ 22

Europe (The European Union as a Proxy) ........................................................................................... 25

Asia (Japan as a Proxy) ........................................................................................................................ 27

Political-Legal Environment Trend.......................................................................................................... 30

North America (US as a Proxy) ............................................................................................................ 30

Europe (The European Union as a Proxy) ........................................................................................... 34

Asia (Japan as a Proxy) ........................................................................................................................ 39

Macro Environmental Summary ............................................................................................................. 41

Industry Analysis ......................................................................................................................................... 43

Strategic Group Map .............................................................................................................................. 45

Porter’s Five Forces ................................................................................................................................ 47

Direct Competitors (LOW 3) ................................................................................................................ 47

Threat of Entry .................................................................................................................................... 52

Threat of Substitutes (VERY LOW 2) ................................................................................................... 55

3 | P a g e

Power of Suppliers (LOW 2) ................................................................................................................ 59

Power of Buyers .................................................................................................................................. 60

Five Forces Summary .............................................................................................................................. 63

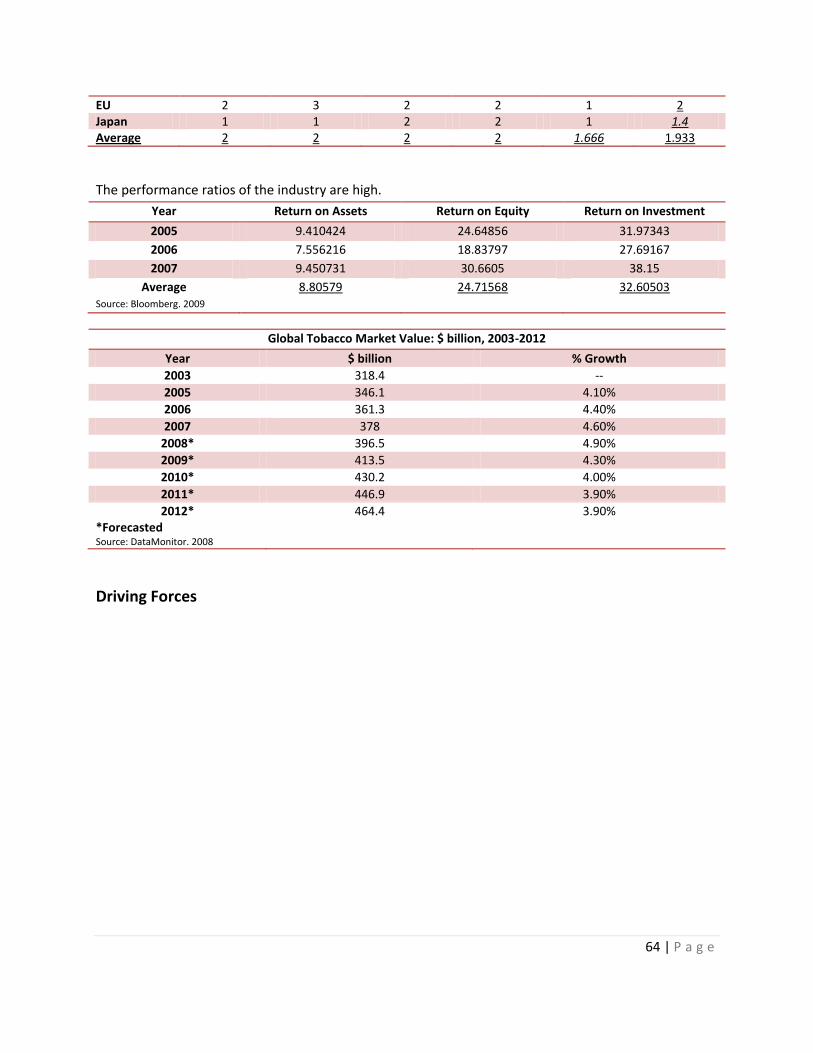

Driving Forces ......................................................................................................................................... 64

Socio-Cultural Impacts ........................................................................................................................ 65

Shift to Emerging Markets .................................................................................................................. 66

Mergers and Acquisitions ................................................................................................................... 66

Effect on Direct Competition .............................................................................................................. 66

Effect on Buyer-Power ........................................................................................................................ 66

Summary of Industry Analysis ................................................................................................................ 67

Business Unit Analysis ................................................................................................................................. 69

Introduction to Value Chain Analysis ..................................................................................................... 69

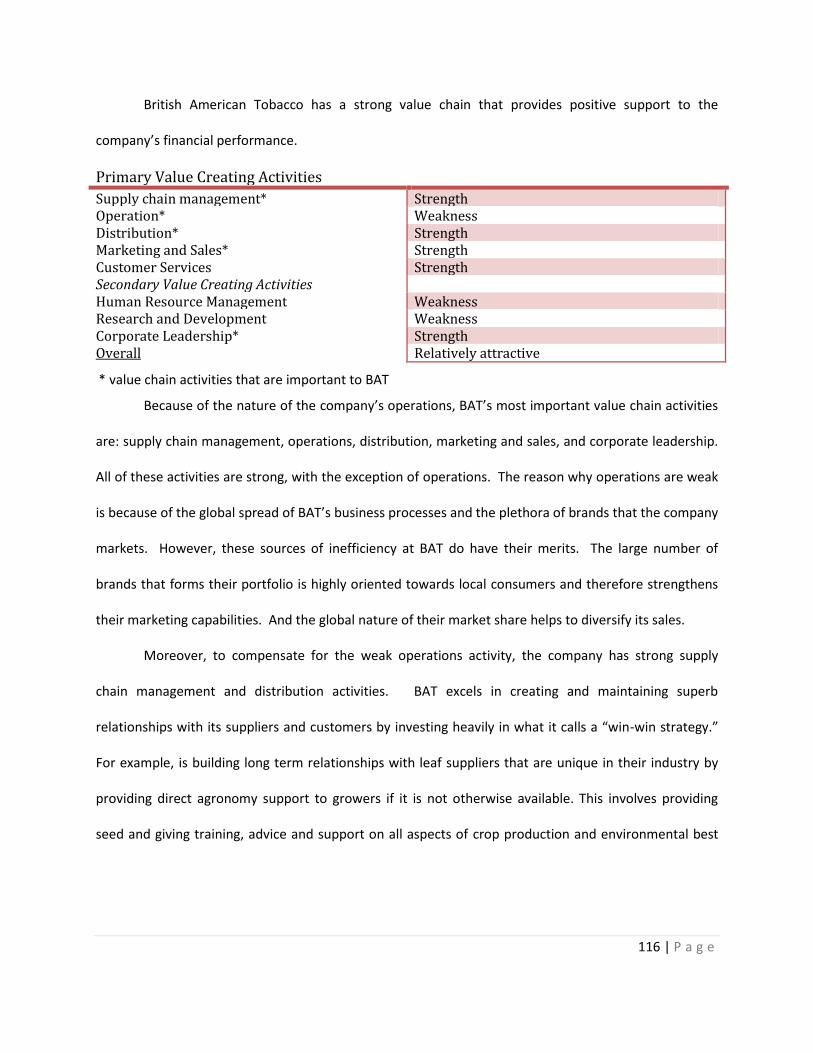

Supply Chain Management (Strength) ................................................................................................... 71

Procurement ....................................................................................................................................... 72

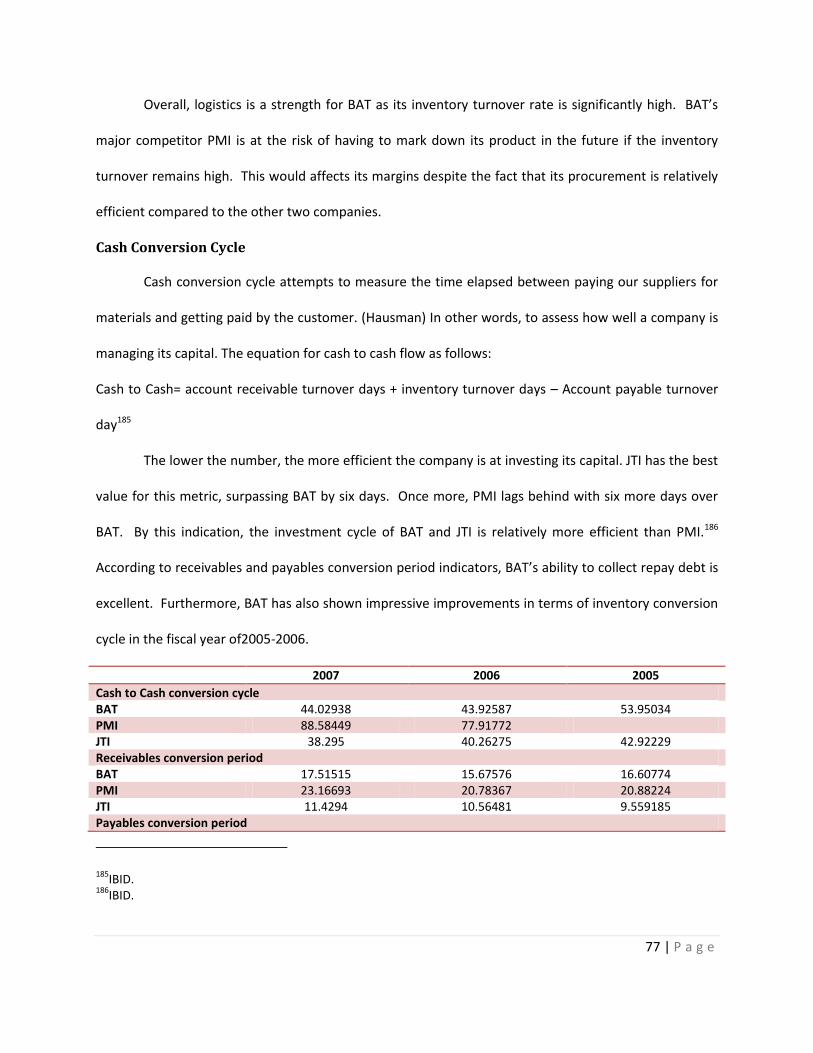

Logistics ............................................................................................................................................... 75

Cash Conversion Cycle ........................................................................................................................ 77

Operations (Weakness) .......................................................................................................................... 78

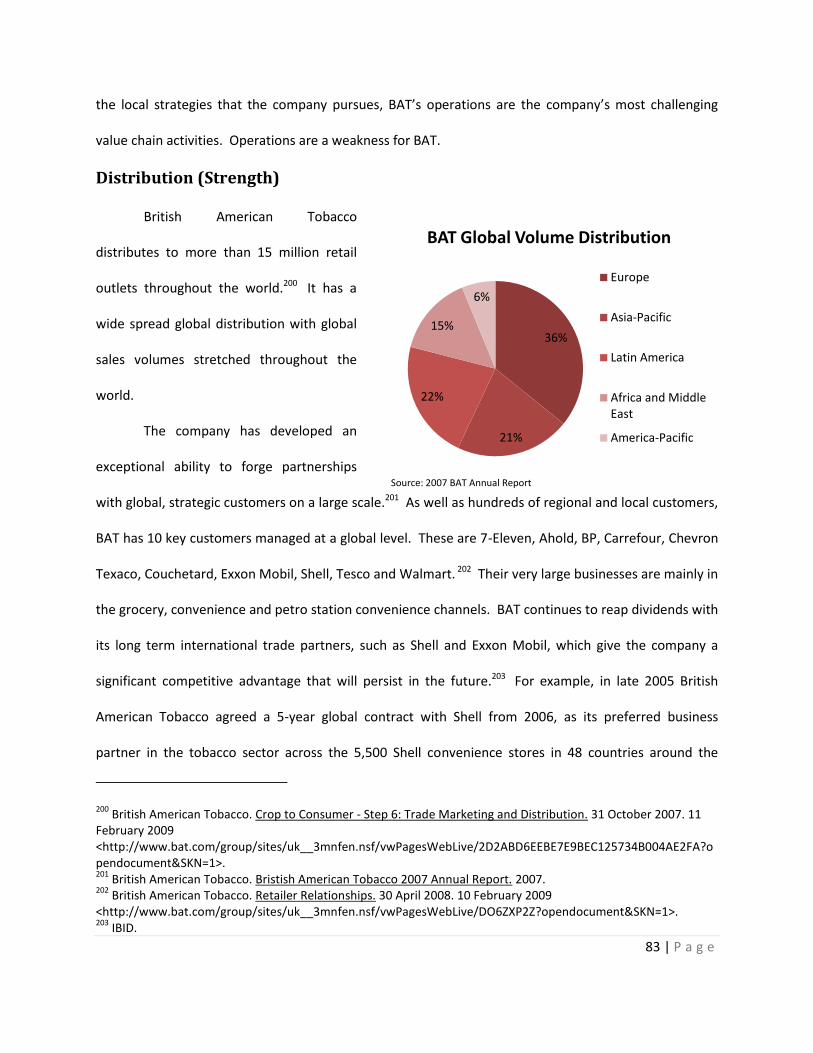

Distribution (Strength) ............................................................................................................................ 83

Marketing and Sales (Strength) .............................................................................................................. 86

Market Share....................................................................................................................................... 87

Sales Trends ........................................................................................................................................ 88

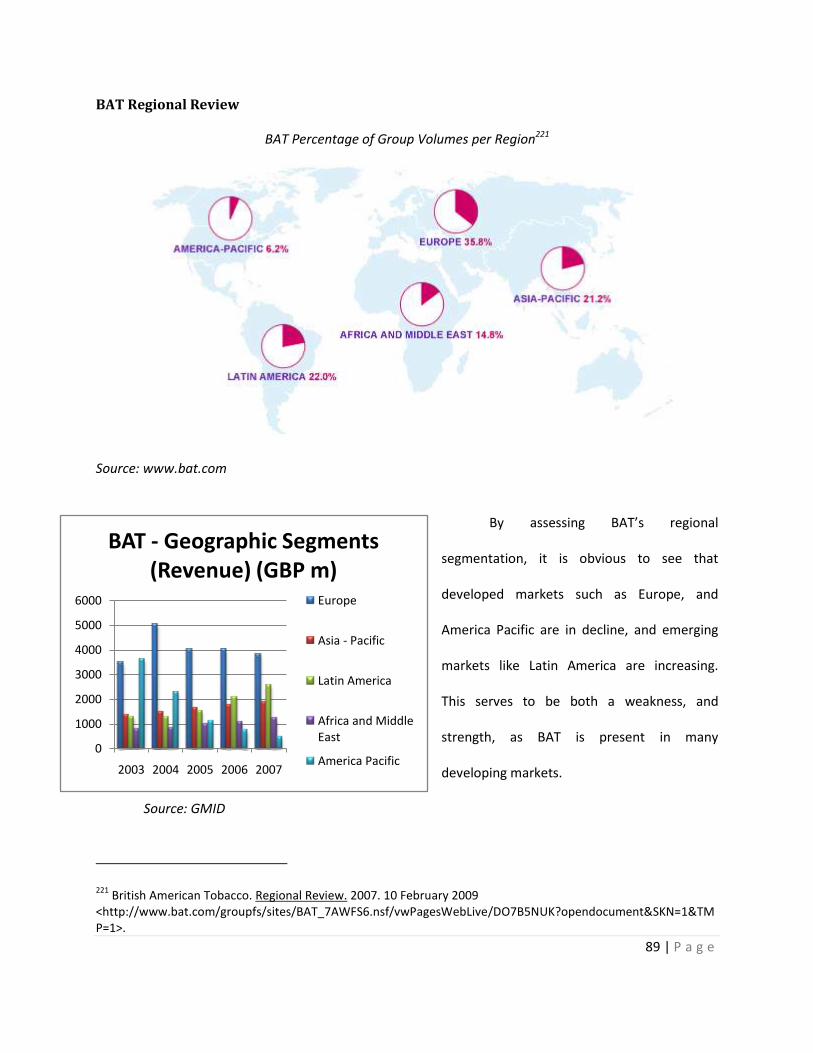

BAT Regional Review ........................................................................................................................... 89

BAT Marketing Mix ............................................................................................................................. 90

Customer Service (Strength) ................................................................................................................... 99

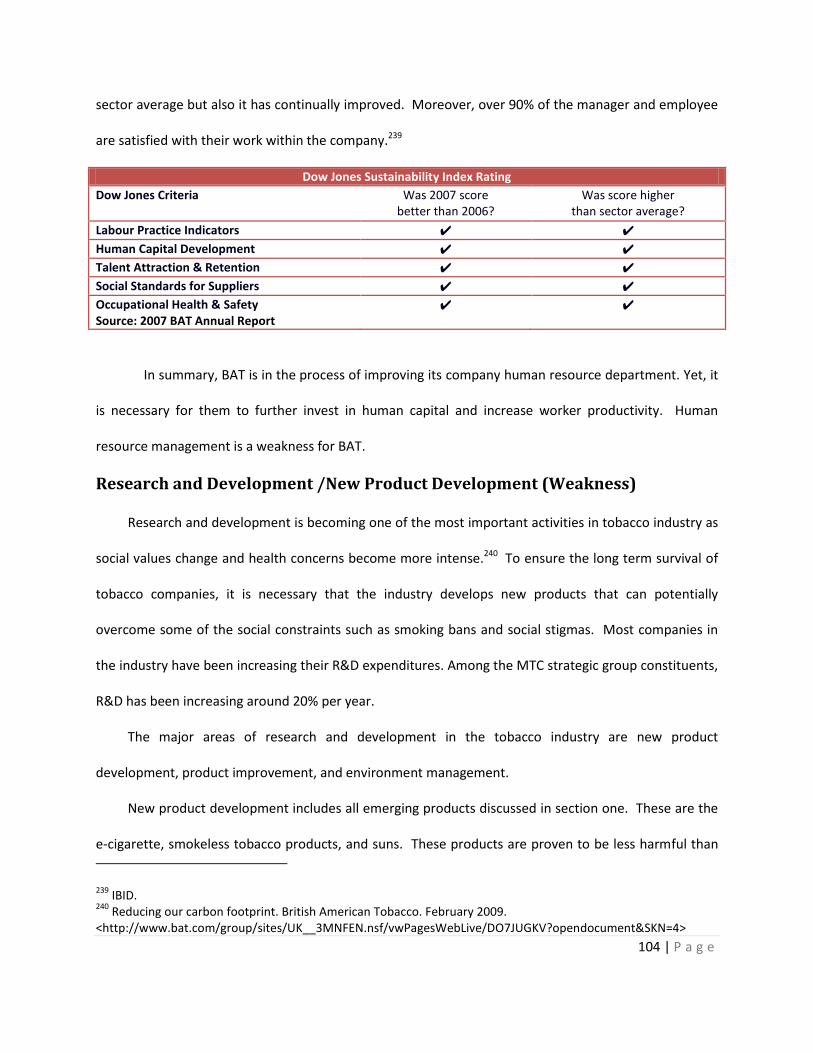

Human Resource Management (Weakness) ........................................................................................ 102

Research and Development /New Product Development (Weakness) ............................................... 104

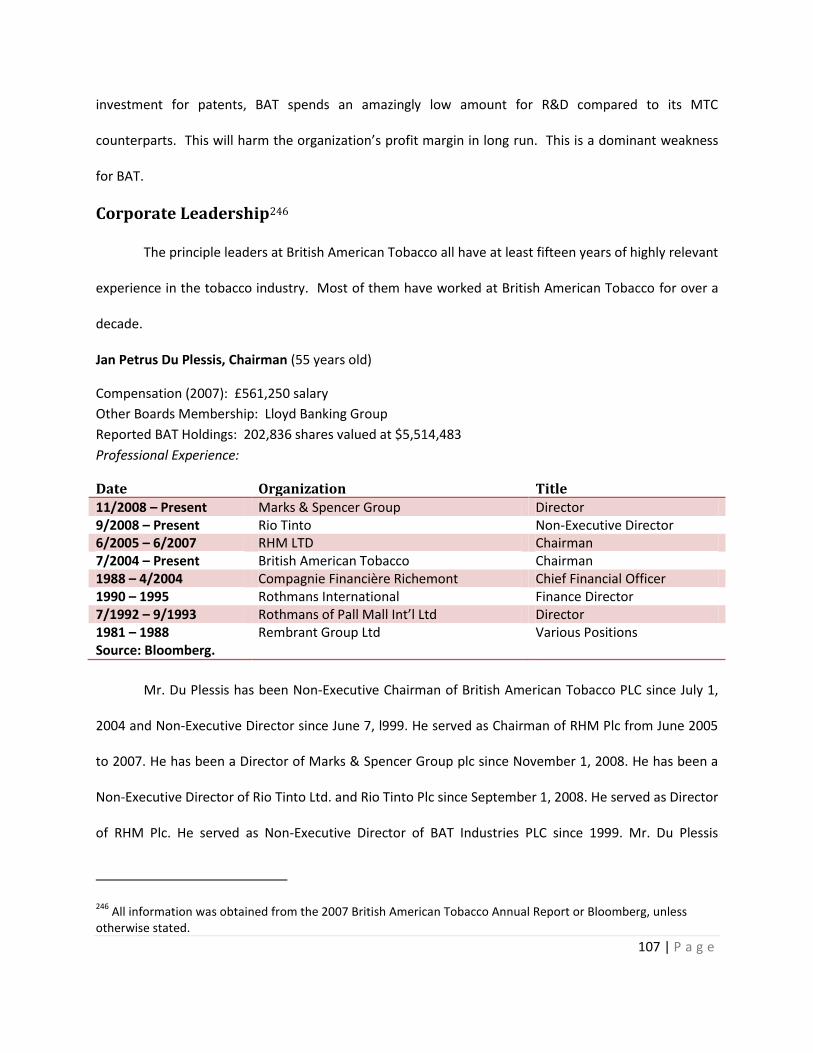

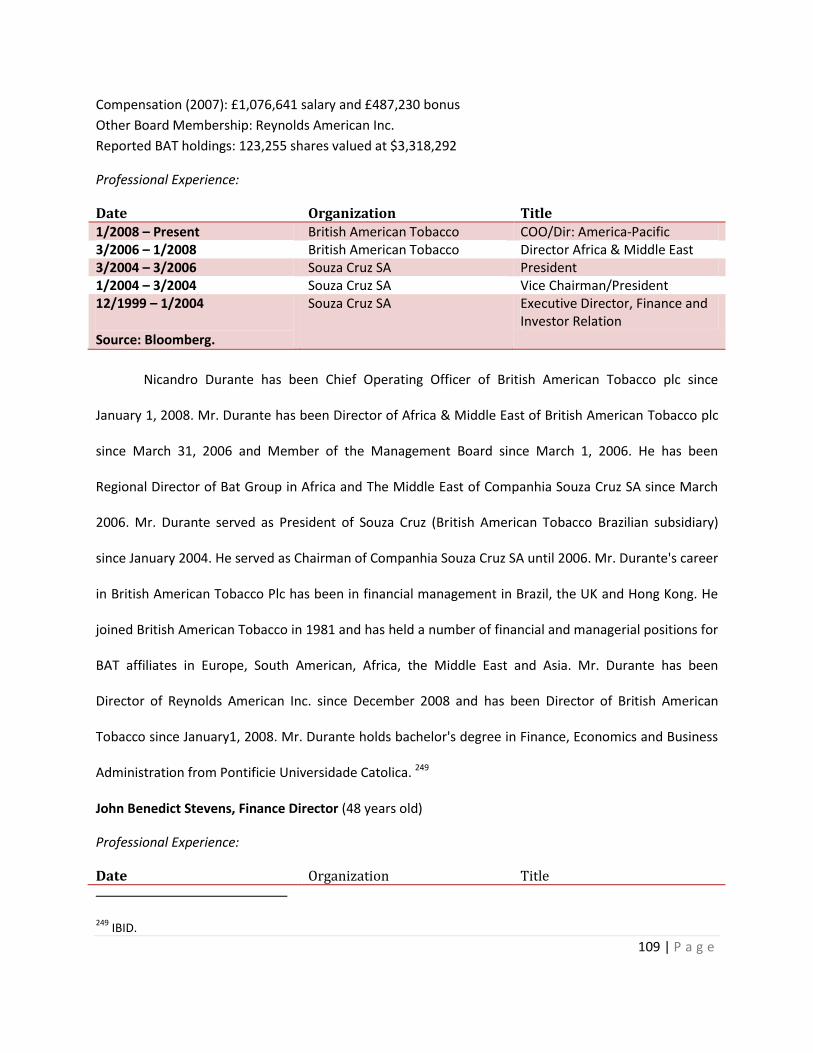

Corporate Leadership ........................................................................................................................... 107

Performance Incentives: ................................................................................................................... 110

Corporate Governance Accountability: ............................................................................................ 110

Measuring Corporate Performance: ................................................................................................. 111

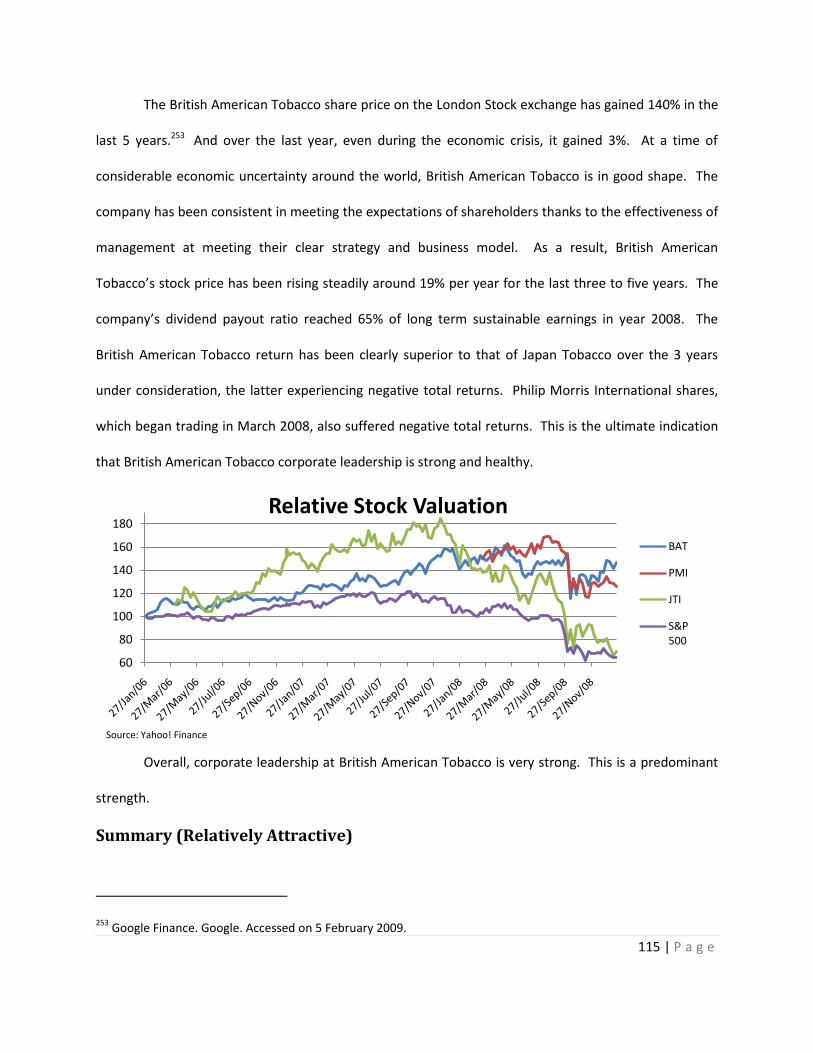

Summary (Relatively Attractive) ........................................................................................................... 115

4 | P a g e

Corporate Level Strategy .......................................................................................................................... 119

Introduction: ......................................................................................................................................... 119

Corporate Strategy Analysis ................................................................................................................. 122

Vertical Integration ........................................................................................................................... 122

Horizontal integration ....................................................................................................................... 123

Geographic Diversification ................................................................................................................ 127

Issues/Problems.................................................................................................................................... 130

Strategy Recommendations ................................................................................................................. 132

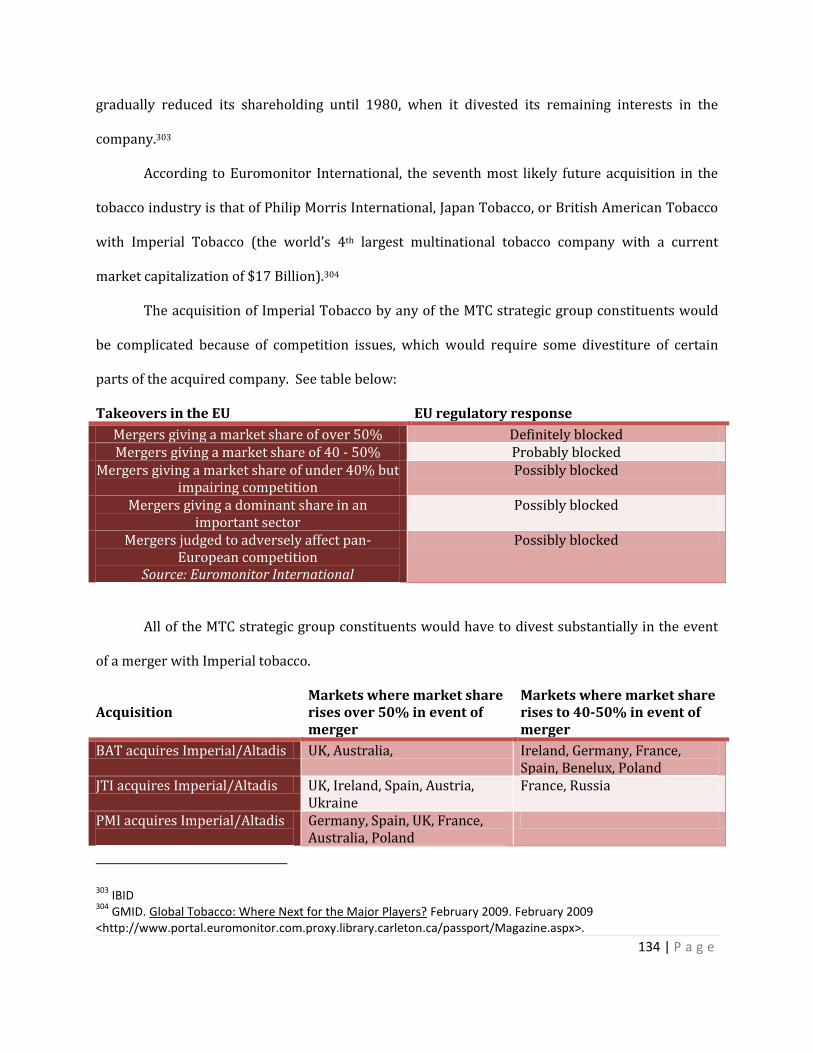

Acquiring Imperial Tobacco .............................................................................................................. 132

Benefits and synergies from the merger: ......................................................................................... 139

Potential Whiteknight: ...................................................................................................................... 141

Business-Functional Strategy Analysis ...................................................................................................... 144

Issues/Problems.................................................................................................................................... 147

Business Level Strategy Recommendations ......................................................................................... 150

Implementing Flexible Manufacturing Systems (FMS) ..................................................................... 151

Better Supply Chain Management Systems ...................................................................................... 151

Roll Out Strategy for the E-cigarette and Snus ................................................................................. 155

Business Level Strategy Summary ........................................................................................................ 158

Strategic Analysis Summary ...................................................................................................................... 158

Bibliography .............................................................................................................................................. 161

Appendices ................................................................................................................................................ 172

5 | P a g e

Executive Summary

Firm Overview – British American Tobacco (BAT)

BAT, founded in 1902, is the world’s second largest tobacco company (excluding the Chinese

Monopoly CNTC) with a market capitalization of $66.7 billion. It produces and markets a diverse range

of brands to suit consumers’ preferences, with a particular focus on its four Global Drive Brands (GDBs),

which are Dunhill, Kent, Lucky Strike and Pall Mall. The Company has over 300 brands in its portfolio

and its brands are sold in over 180 markets.

External Environment Overview

The tobacco industry enjoys a resilient

market for its product. Contrary to most modern

goods, the cigarette as we know it today will not

be easily replaced by advances in technology.

Furthermore, smokers are not tempted to smoke

less in times of economic difficulty or in times of

stress. Therefore, the economic crisis should have little nominal impact on the market for tobacco

products. The social perception of smoking, on the other hand, has changed dramatically since the

Surgeon General’s report in the early 1960’s and a swarm of anti-smoking regulations, bans, and taxes

has ensued in developed countries. The prevalence of smoking has consequently decreased at a

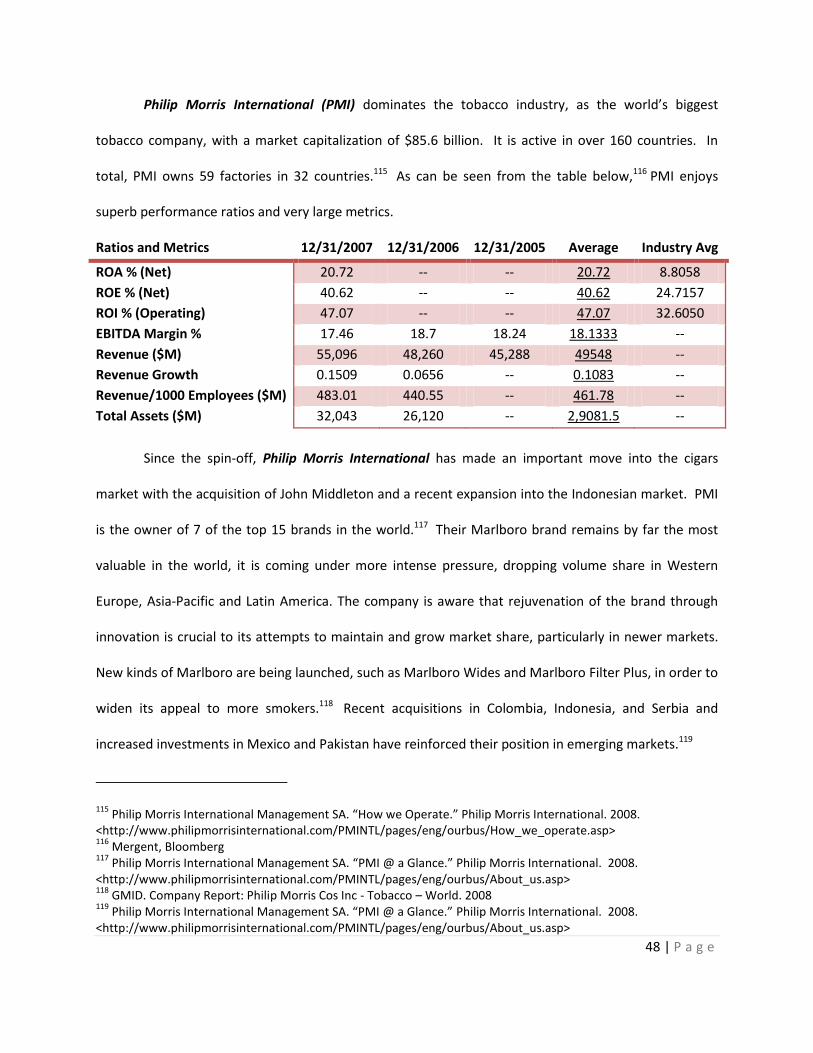

constant rate in these affected countries while this prevalence has increased in developing countries.

This global trend has led to a wave of acquisitions from large Multinational Tobacco Companies,

targeting local companies in developing countries (see adjacent figure).

Industry Analysis

6 | P a g e

The tobacco industry is highly consolidated, the top five international firms accounting for 68.5%

of total sales in year 2007, barriers to entry are therefore relatively high as one should expect heavy

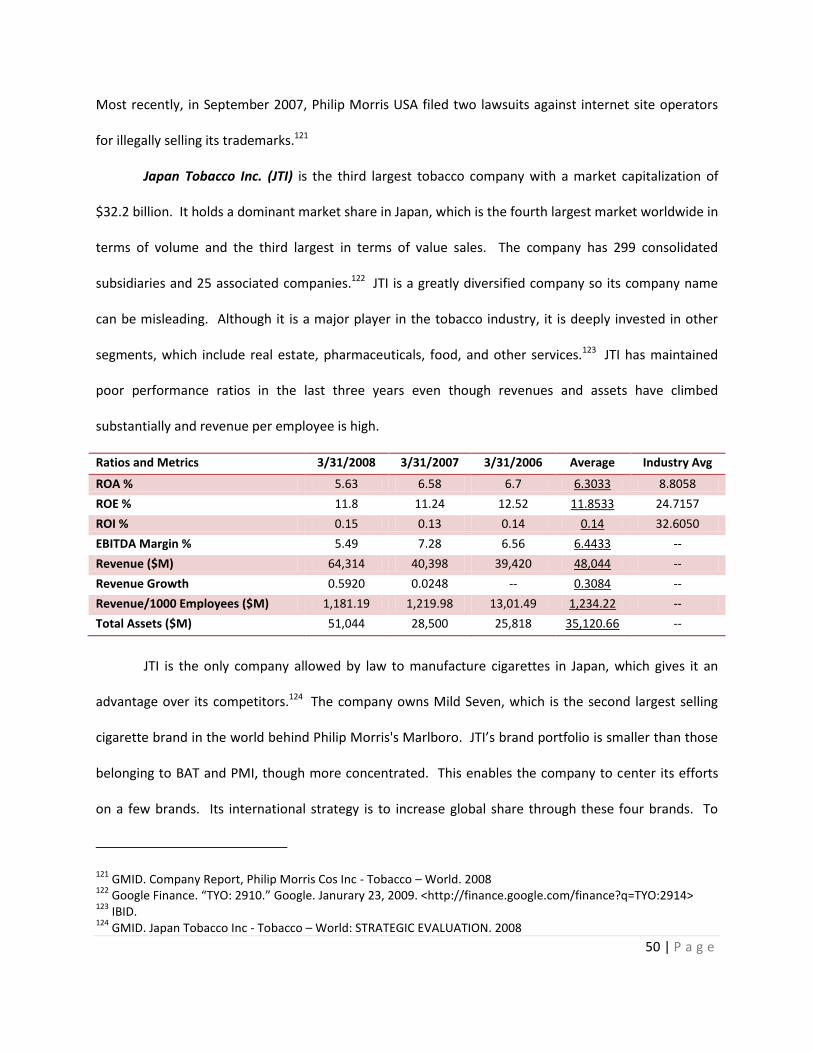

retaliatory behaviour. Cigarette brands enjoy the highest brand loyalty of all consumer products, with

less than 10% of users changing brands annually. Moreover, smokers are addicted to tobacco because it

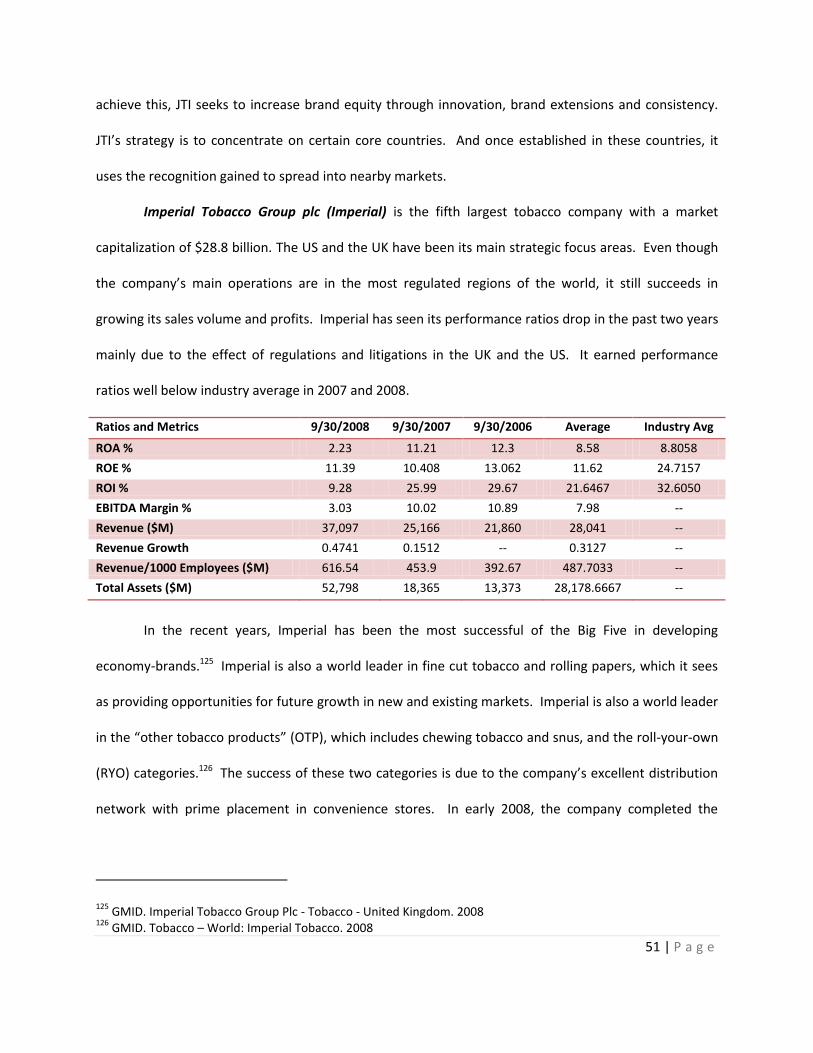

contains nicotine and the only substitute products available are sold at a significantly higher cost (ie.

nicotine gum, nicotine inhalers, etc.). The tobacco industry functions as a sort of oligopoly with millions

of tobacco leaf suppliers and only few large buyers.

Corporate and Business Level Strategy

Since the market for cigarettes in developed (historically most profitable) countries is shrinking,

BAT’s strategy is to increase margins while maintaining sales volume. The company achieves this by

increasing the price of its products while improving cost efficiency. In line with this, we propose that

BAT acquire Imperial Tobacco, the fourth largest competitor in the market thereby allowing BAT to

overtake Philip Morris International and gain leadership of the industry along with valuable market and

pricing power. BAT should also accelerate its number of acquisitions in emerging economies, thus

gaining an advantage as the markets are shifting towards the global south. BAT’s major weakness in its

current business strategy resides in weak brand positioning, which is critical as today’s cigarette sales

are driven by brands. None of BAT’s brands were able to capture over 1% of the market share whereas

both PMI and JTI have at least 2 brands that have a market share over 1%. BAT must also enhance its

R&D department to counter emerging socio-political trends by focusing on healthier alternatives, such

as snus and the e-cigarette to capture greater market share. BAT should also target R&D efforts towards

operative efficiency by striving to emulate the JTI system of flexible manufacturing to ensure that its

operations are as productive and efficient as possible.

7 | P a g e

Introductory Summary

Firm: British American Tobacco plc. (Public, LON:BATS)

Market Capitalization: $50.5 billion

Description: The Company is an international tobacco company engaged in the sale of cigarettes, cigars,

leaf and other tobacco products. It produces and markets a diverse range of brands to suit consumers’

preferences, with a particular focus on its four Global Drive Brands (GDBs), which are Dunhill, Kent,

Lucky Strike and Pall Mall. Its cigar portfolio includes the handmade Dunhill Signed Range. The Company

has over 300 brands in its portfolio and its brands are sold in over 180 markets.

NAICS: 312221 (Cigarette Manufacturing)

We chose the tobacco industry because of the simplicity of the nature of its product and its

global reach. We are interested to see how the competitive context of this industry is changing as social

perceptions towards smoking shift and anti-smoking regulation gets heavier. British American Tobacco is

the second largest player in this industry, behind Philip Morris International. We chose British American

Tobacco because we all had previous knowledge of many of its brand.

In terms of sources of information that we will use to complete the research, we have found

that Euromonitor International (GMID) provides the most comprehensive data on the tobacco industry.

We intend to use it as our primary database. It contains region specific information on everything from

demographic trends to the regulatory environment and company specific reports. Mergent Online and

Bloomberg are valuable tools when it comes to financial analysis. We intend to use them extensively.

Business Source Online and Factiva provide a wide array of industry specific news and reports that are

useful for understanding the industry’s macro environment.

Our group is comprised of three fourth year Bachelor of International Business students.

8 | P a g e

Gabriel Huppé is an International Investment, Finance, and Banking major who has strong

quantitative skills. He has experience serving both the private and public sector in Canada and abroad

including a recent internship at the Canadian Chamber of Commerce in Japan, work term at Osaka City

Revitalization board, and summer employment in the constituency office of the Hon. Lawrence Cannon

(MP, Minister of Foreign Affairs). Gabriel will be in charge of the North-American region because of his

understanding of the multiple environmental aspects that affect the tobacco industry.

Ricky Sin is a Strategic Management and International Human Resources major who has strong

analytical skill. He is native of Hong Kong and has worked in various Asian countries including Singapore,

Hong Kong and China and has studied in Japan. He has a deep knowledge of Asian culture, business

environment, and trends and will therefore be in charge of the Asian region.

Sunayna Ali is an International Marketing and Trade major who has strong critical thinking and

presentation skills. She has studied in Europe (Madrid, Spain), where she has travelled and studied

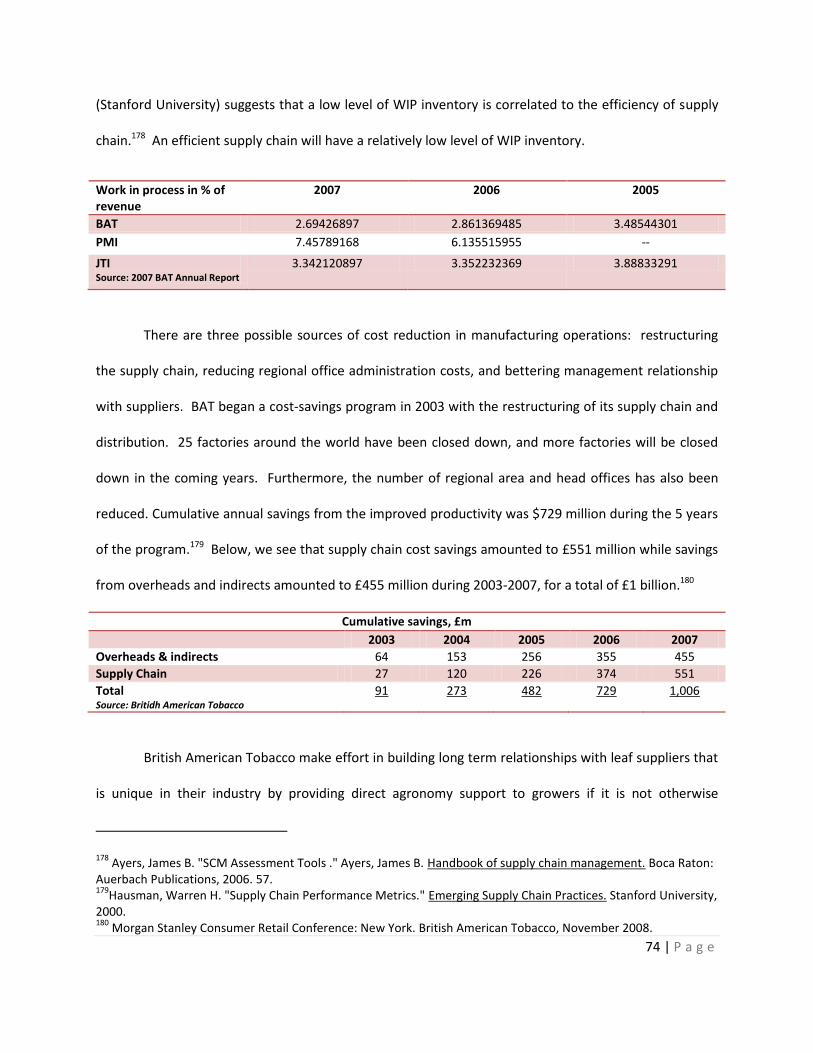

extensively. Therefore she will be in charge of the European region, as she has had the opportunity to

adapt to the European lifestyle as well as been exposed to the business environment there.

9 | P a g e

Only 10.8% of total cigarette revenue comes from Africa, the Middle East, and South America.1

Therefore we have chosen to focus our environmental analysis on the most important regions: North-

America, Europe, and Asia.

Macro Environmental Analysis

Foreword

The tobacco industry enjoys a resilient market for its product. Contrary to most modern goods,

the cigarette as we know it today will not be easily replaced by advances in technology due to the

addictive nature of the product. The technological trends that center on new product innovations are

therefore of minor importance compared to those trends which centre around operative efficiency.

Furthermore, smokers are not tempted to smoke less in times of economic difficulty or in times of

stress. So the fact that we are in a global economic crisis should have little nominal impact on the

market for tobacco products, especially because of the fact that as smokers earn less money they do not

smoke less. This point is easily demonstrated through the big five tobacco companies’ performance in

the last six month. As a case in point, British American Tobacco’s stock on the London Stock Exchange

has seen a modest increase in price in the last six months, compared with a 30% decrease for the S&P

500 index for the same period.2 The most important macro trends affecting the tobacco industry are

therefore socio-cultural and political-legal in nature. As will be investigated throughout this paper, these

latter trends pose a significant challenge – a challenge that is expected to endure in the future.

Technological Trends

Trends Centering around Operative Efficiency.

1 GMID. Tobacco: World. 5 June 2008. 4 February 2009

<http://www.portal.euromonitor.com.proxy.library.carleton.ca/passport/ResultsList.aspx>. 2 Google . Google Finance. 23 January 2009. January 2009 <http://www.google.com/finance>.

10 | P a g e

Global Positioning Systems (GPS) and Geographic Information Systems (GIS) Enabled Radio

Frequency Identification Distribution (RFID)

Efficient Cigarette Distribution Systems (CDS) are critical to the success of tobacco companies. It

is essential that CDS strategies continuously adapt to the trends that affect manufacturing and

distribution operations. Cigarette production chains are currently expanding, as tobacco companies are

expanding in ever more remote areas in the midst of specialization in the social division of labor. Hence

it is increasingly difficult to implement efficient CDS.

RFID was first used in the military to complete the input and processing of information by means

of optical visualization without the need for direct contact or manual intervention.3,4 Typical RFID

systems consist of radio frequency labels, readers, and application systems.

Presently, RFID could have two applications in the tobacco industry: logistics and inventory.

RFID automates processes and optimizes supply-chain processes thereby improving efficiency, reducing

mistakes in transport routes, and reducing packaging errors. RFID also enables the optimization of

inventory levels which may reduce costs and enable more flexibility in the production process.5

Using RFID technology integrated with GPS, GIS, and routing technology, tobacco companies

could keep track of cigarette merchandise handling with real-time visual tracking by linking businesses,

distributors, and retailers to their central information systems.6 This could provide significant assistance

in inventory planning. It could also help ensure a safer distribution of cigarettes, and improve the return

on fixed assets, such as transportation equipment. By integrating such a system, tobacco companies

could achieve vast improvements in the operational efficiency of their entire supply chain and enhance

3 Qiang, Qiao. "The Application of RFID ." Modern Information (2005): 150-151.

4 Fallon, M. "Traceability of poultry and poultry products." Revscitech Offint Epiz (2001): 538-546.

5 Hu, Hongchun, et al. "Research on the Application of Radio Frequency Identification in Cigarette-Distribution

Systems." International Conference on Automation and Logistics (2007): 2586-2591. 6 Zhang Danyu, Liaoli. "Logistics System Course." Shandong University Press (2004).

11 | P a g e

their industry competitiveness. It could also facilitate the fight against cigarette contraband (a

threatening trend that will be discussed in the socio-cultural section) since customers could authenticate

their products with the use of encrypted product information contained on RFID labels.

Logistics Information Systems (LIS)

Logistic Information Systems are based on the creation of logistic data warehouses concerning

delivery documents and stock control. It concerns the implementation of a global system. The big five

tobacco companies each operate in over 100 countries, with various local subsidiaries. Many of these

subsidiaries operate on dissimilar systems, and staff at head office need to collect data manually from

the company’s existing management solution. This makes it difficult to efficiently trace or collect

information for purposes such as data entry, balance sheets, sales orders, and the reporting and

analyzing of accounting data. It also creates lengthy administrative processes and obstructs

collaboration between staff on day-to-day projects. All of this affects staff productivity and the quality

and reliability of important data. Presently, most of the big five tobacco companies are integrating

customizable solutions that automatically consolidate data and simplify reporting and analysis

processes. By implementing a collaborative workflow, they can integrate all of their offices and simplify

data entry, consolidation, and information management. They opt for a solution that offers flexibility,

fast deployment but does not require a lot of employee training. Such systems could be based on

AS/400, JD Edwards, Formula Group, or UNIX, among others. And an integrated environment creates a

collaborative workflow for the rest of the subsidiaries. New systems can automatically retrieve and

consolidate business data. Such technological strategies require a massive amount of investment. The

scale of big tobacco companies can make it very difficult to implement LIS. Once implemented,

however, a tobacco company can achieve a significant competitive advantage by reacting to information

rapidly and effectively. This is both a threat and an opportunity.

Manufacturing and Packaging

12 | P a g e

Tobacco companies must optimize the utilization of resources in the manufacturing and

packaging processes. Specifically, by using cutting-edge machinery, they can free manpower from the

process of sampling, better preventative maintenance, and better product hygiene. All of which benefit

the business in tangibly measurable ways. Because of their economies of scale and their ability to spend

more on R&D, the big five tobacco companies have an advantage over their smaller counterparts in this

technical area. This is an opportunity.

Trends Centering around New Product Innovation

The E-cigarette

The e-cigarette is an alternative to the traditional tobacco product. As its name suggests, it is a

battery-powered device that provides inhaled doses of nicotine in the form of vapor. In addition to

nicotine, this vapor also provides a flavor and physical sensation similar to that of inhaled tobacco

smoke. However, no tobacco, smoke, or combustion is involved. Liquid nicotine solutions for electronic

cigarettes are available in different flavors and nicotine concentrations. Some varieties attempt to

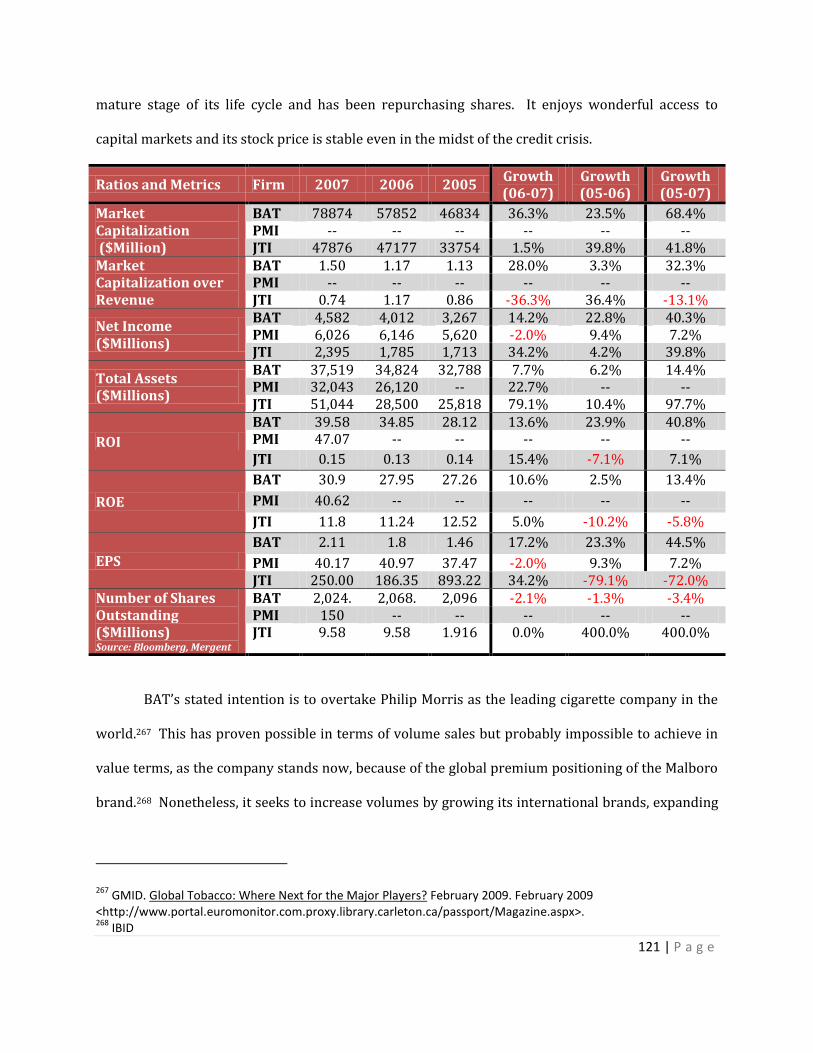

resemble traditional cigarette types, such as regular tobacco and menthol, and some even attempt to

mimic specific cigarette brands, such as Marlboro or Camel. Solutions are also available with candy-type

flavoring, such as strawberry, orange, mint, vanilla, caramel, coffee, etc. Toxicological studies of the

electronic cigarettes have been conducted, with some reporting that electronic cigarettes are less

harmful than traditional tobacco cigarettes.7,8 This technology allows users to attain some of the

benefits of smoking wherever they want, since smoking bans are making it more difficult to fulfill their

nicotine craving in public places. A notable example: Crown7 sells their reusable HYDRO e-cigarette at

7 Health New Zealand Ltd Information. The Ruyan E-cigarette. New Zealand, 31 March 2008.

8 Chemical & Engineering News. "Newscripts." Chemical & Engineering News (2008): 56.

13 | P a g e

$79.95 per unit with replacement cartridges, claimed to be the nicotine equivalent of two packs of 20,

that at $10 each.9 This is a threat to the tobacco industry.

The “Healthier” Cigarette

For decades the fast-moving consumer goods and food industries have seen the enhancement

of products through vitamins and other value-added substances. In June 2007, the German Tobacco

Group AG partnered with a US firm that produced vitamin enhanced water to market the world’s first

vitamin-E enhanced cigarette.10 According to the U.S. patent owner and research firm, the vitamin-E

enhanced cigarette features an improved and soothing flavor and also minimizes the irritation that

usually occurs when using conventional cigarettes.11 The new product addresses the international trend

of consumers becoming increasingly aware and more responsible when using tobacco products (as will

be discussed in the socio-cultural section). This is both a threat and an opportunity.

A number of companies are in search of ways to manufacture a safer cigarette by attempting to

lessen the health risks associated with long-term tobacco use. For example, British American Tobacco

markets a cigarette that uses tobacco that is treated to produce lower levels of cancer-causing

chemicals (carcinogens). It also incorporates a new type of filter said to remove more of the remaining

toxins.12 There is talk that BAT is on the verge of developing a “risk free” or low-risk cigarettes, which

some suggest might cut the chance of disease by as much as 90%.13

The Odorless Cigarette

9 Crown7 . Crown7 Announces New HYDRO Electronic Cigarette Product Line . 12 March 2008. January 2009

<http://www.tobacco.org/news/275473.html>. 10

World Tobacco. Vitamin E cigarette by German Tobacco Group . 9 October 2007. January 2009 <http://www.worldtobacco.co.uk/shownews.asp?secid=&pubid=27&nav=1&newstype=0&key=distribution&page=0&newsid=12988>. 11

Lugmayr, Luigi. World's First Vitamin E Cigarette. 21 September 2007. January 2009 <http://www.i4u.com/article11644.html>. 12

Leake, Jonathan. 'Safe cigarette' claimed to cut cancer by 90%. 6 November 2005. January 2009 <http://www.timesonline.co.uk/tol/news/uk/article587130.ece>. 13

Jha, Alok. Tobacco Firm Plays Down Reports of Safer Cigarette. 7 November 2006. January 2009 <http://www.guardian.co.uk/society/2005/nov/07/health.smoking>.

14 | P a g e

Japan Tobacco International is now marketing a cigarette called Mirage which uses LSS (Less

Smoke Smell), an odor-reducing technology developed in response to consumer demands for the

reduction of the unpleasant smell of smoke.14 Their patent states “a method of fixing flavourant, which

improves sidestream smoke smell of tobacco and cigarette.”15 A "smell-improving agent" comprising of

an ethanol or propylene glycol solution would be applied to the cigarette paper. The final cigarette

product uses two-layer cigarette paper that encloses special citrus capsules which considerably reduce

tobacco smell in the air. This is a threat since the patent is owned by another company.

Internet Retailing

The internet sales of tobacco products are gaining popularity. As an example, the American

Lung Association estimates that there are more than 500 websites that sell tobacco products to U.S.

customers.16 Currently, such sales are largely unregulated. Many companies that sell cigarettes online

do not ensure that only adults can enter and purchase from their websites. They don’t check that their

customers pay all customs duties, excise and other taxes. Some of them even sell counterfeit products.

The U.S. Government Accountability Office has reported that three-quarters of all Internet tobacco

sellers explicitly state that they will not report cigarette sales to tax collection officials, thus violating

federal law.17 This is a major threat to the tobacco industry.

Nicotine Replacement Products

There are a number of recently emerging technologies that can temporarily satisfy a smoker’s

urge for nicotine. These include patches, gums, lozenges, inhalers, nasal sprays, and nicotine water,

14 Japan Tobacco. JT to Release New Camel Product Nationwide. 15 February 2007. January 2009

<http://www.jti.co.jp/JTI_E/Release/2007/02/20070213_01.html>. 15

CanWest News Service. Critics raise stink about cigarettes with less tobacco smell. 7 December 2007. January 2009 <http://www.canada.com/topics/news/national/story.html?id=d522153b-fa74-4f2e-a458-bca6df756cb7&k=74191>. 16

American Lung Association . Curbing Internet Sales of Tobacco Products. 2009. January 2009 <http://www.lungusa.org/site/c.dvLUK9O0E/b.3914925/>. 17

IBID.

15 | P a g e

among others. Such have gained popularity in the last decade as a way to help smokers deal with the

withdrawal symptoms of not obtaining nicotine from cigarettes. These products deliver nicotine to the

smoker's brain in a much slower way than cigarettes do. This helps to damp down the urges to smoke

that most smokers have in the early days and weeks after quitting, rather than remove them totally. It

may provide a more comfortable exit from the smoking habit, thus posing a threat.

Economic Environment Trend

North America (US as a Proxy)

In January, forecasting US macro environmental trends, especially those of economic and

political-legal nature, was exceptionally challenging because of the uncertainty surrounding the impacts

of the still developing economic crisis and the inauguration of a new, celebrated, President. Today, it is

still difficult to accurately forecast these trends but there are signs that the economy might rebound,

although remaining relatively bleak, in the near future: consumer spending is growing again, while

inventories are being wound down.18

To recapitulate: In December 2008, the NBER declared that the United States had been in

recession since December 2007, and would continue to plummet further with no end in sight, in what

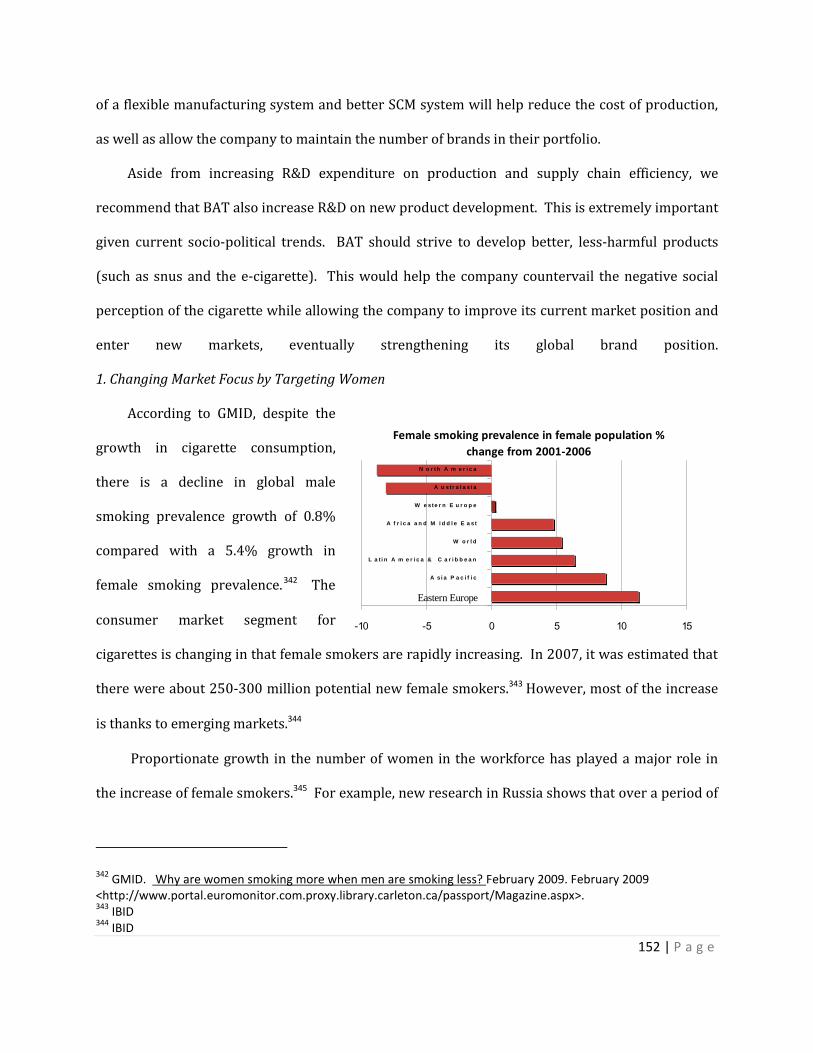

was being called the worst recession since the Great Depression.19 As of mid-November 2008, it was

estimated that the new loans, purchases, and liabilities of the Federal Reserve, the US Treasury, and

FDIC, brought on by the financial crisis, totaled over $5 trillion.20 To make matters even worse, as of the

same time, the total U.S. federal debt was $10.6 trillion and the current account deficit was $731.2

billion. This dangerous combination of mounting debt and economic turmoil has led many economists to

18 US Economy Could Recover Much Sooner Than Expected. CNBC. 9 April 2009.

<http://www.cnbc.com/id/30111906> 19

Isidore, Chris. “It's official: Recession since Dec. '07.” CNNMoney.com. December 1, 2008 <http://money.cnn.com/2008/12/01/news/economy/recession/?postversion=2008120115> 20

Moyer, Elizabeth. “Washington's $5 Trillion Tab.” Forbes.com. December 11, 2008. <http://www.forbes.com/2008/11/12/paulson-bernanke-fed-biz-wall-cx_lm_1112bailout.html>

16 | P a g e

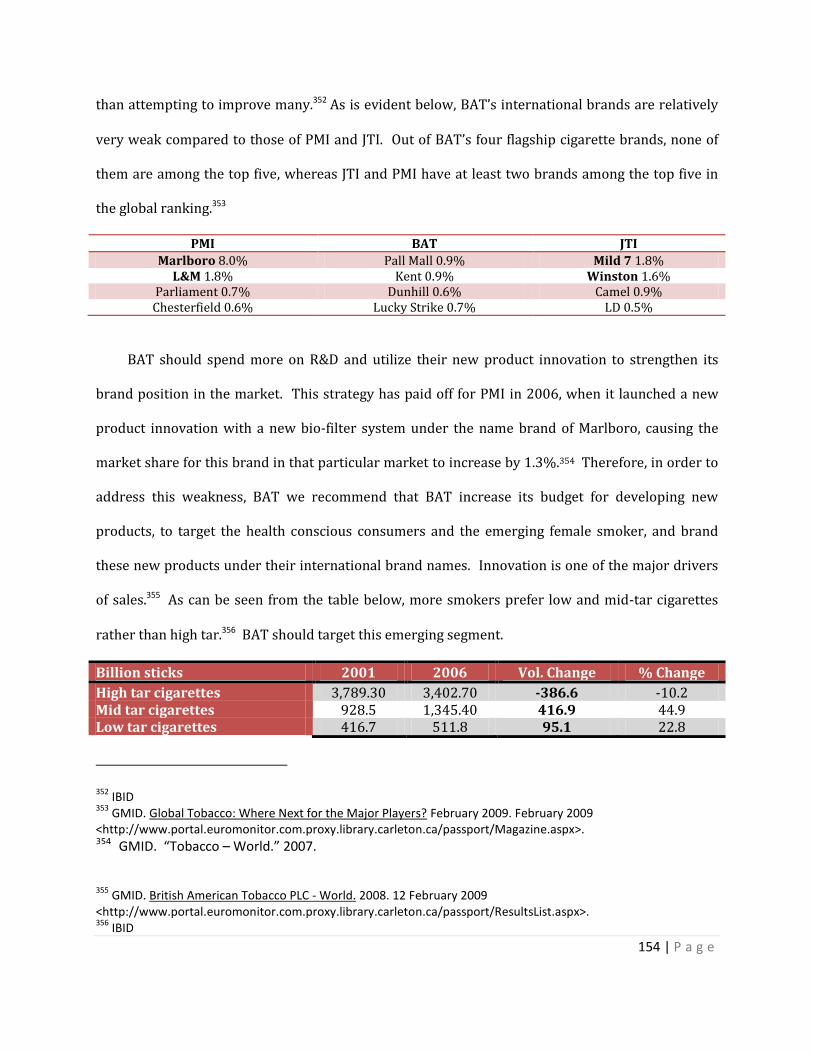

believe that a dollar crisis is looming. Speculation aside, there is a wide ranging consensus that the next

five years will be marked by declining US global affluence.

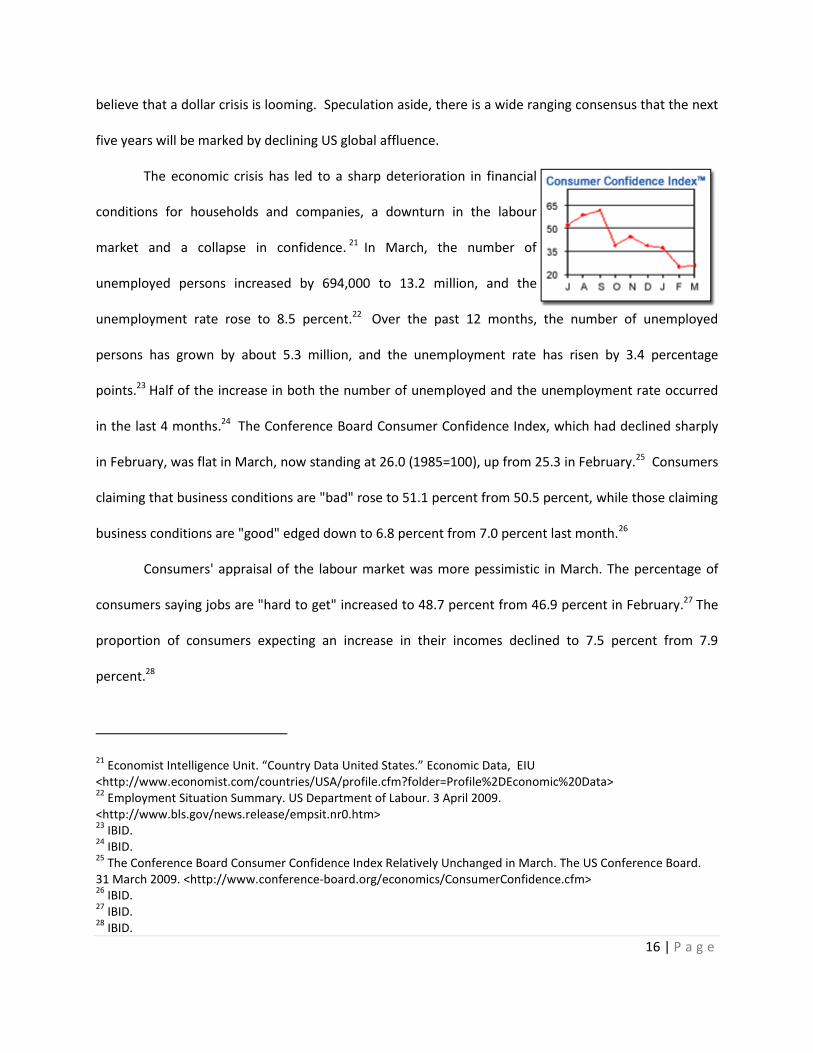

The economic crisis has led to a sharp deterioration in financial

conditions for households and companies, a downturn in the labour

market and a collapse in confidence. 21 In March, the number of

unemployed persons increased by 694,000 to 13.2 million, and the

unemployment rate rose to 8.5 percent.22 Over the past 12 months, the number of unemployed

persons has grown by about 5.3 million, and the unemployment rate has risen by 3.4 percentage

points.23 Half of the increase in both the number of unemployed and the unemployment rate occurred

in the last 4 months.24 The Conference Board Consumer Confidence Index, which had declined sharply

in February, was flat in March, now standing at 26.0 (1985=100), up from 25.3 in February.25 Consumers

claiming that business conditions are "bad" rose to 51.1 percent from 50.5 percent, while those claiming

business conditions are "good" edged down to 6.8 percent from 7.0 percent last month.26

Consumers' appraisal of the labour market was more pessimistic in March. The percentage of

consumers saying jobs are "hard to get" increased to 48.7 percent from 46.9 percent in February.27 The

proportion of consumers expecting an increase in their incomes declined to 7.5 percent from 7.9

percent.28

21 Economist Intelligence Unit. “Country Data United States.” Economic Data, EIU

<http://www.economist.com/countries/USA/profile.cfm?folder=Profile%2DEconomic%20Data> 22

Employment Situation Summary. US Department of Labour. 3 April 2009. <http://www.bls.gov/news.release/empsit.nr0.htm> 23

IBID. 24

IBID. 25

The Conference Board Consumer Confidence Index Relatively Unchanged in March. The US Conference Board. 31 March 2009. <http://www.conference-board.org/economics/ConsumerConfidence.cfm> 26

IBID. 27

IBID. 28

IBID.

17 | P a g e

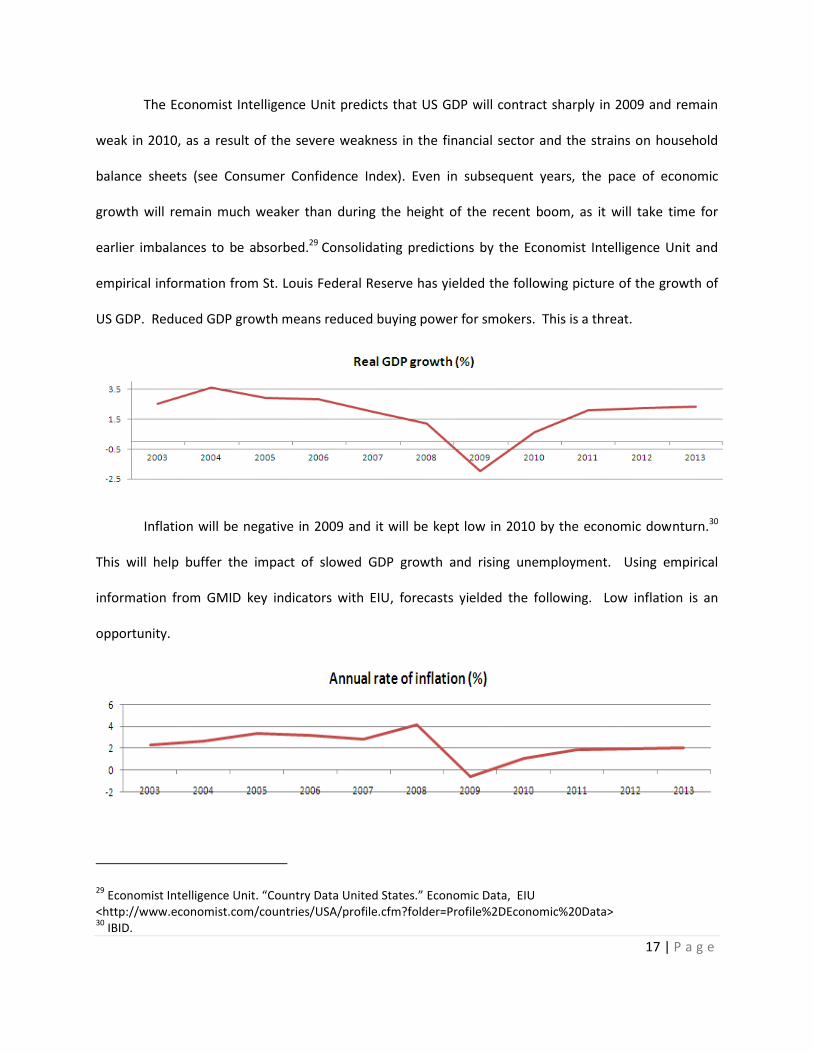

The Economist Intelligence Unit predicts that US GDP will contract sharply in 2009 and remain

weak in 2010, as a result of the severe weakness in the financial sector and the strains on household

balance sheets (see Consumer Confidence Index). Even in subsequent years, the pace of economic

growth will remain much weaker than during the height of the recent boom, as it will take time for

earlier imbalances to be absorbed.29 Consolidating predictions by the Economist Intelligence Unit and

empirical information from St. Louis Federal Reserve has yielded the following picture of the growth of

US GDP. Reduced GDP growth means reduced buying power for smokers. This is a threat.

Inflation will be negative in 2009 and it will be kept low in 2010 by the economic downturn.30

This will help buffer the impact of slowed GDP growth and rising unemployment. Using empirical

information from GMID key indicators with EIU, forecasts yielded the following. Low inflation is an

opportunity.

29 Economist Intelligence Unit. “Country Data United States.” Economic Data, EIU

<http://www.economist.com/countries/USA/profile.cfm?folder=Profile%2DEconomic%20Data> 30

IBID.

18 | P a g e

The US dollar is expected to remain at around US$1.30-1.40:€1 in coming years, which is a

significant recovery from its estimated average of US$1.47:€1 in 2008.31 Using data from EIU and

OANDA, FXHistory has yielded the following. An expensive US dollar translates into higher profits for

non-US tobacco firms, since US smokers pay more in terms of foreign currency for their product. This is

an opportunity because it increases BAT’s revenue.

Europe (The European Union as a Proxy)

The European Union (EU), which has currently integrated 27 countries, aspires to bring its

citizens peace, prosperity and freedom.32 Since the amalgamation, it has indeed been prosperous and

successful. This is evident when assessing its single market, adoption of the Euro, incorporation of an

economic and monetary union and enlargement into eastern European countries.

The European Union’s Gross Domestic Product (GDP) (purchasing power parity) as of 2008 was

$14.82 trillion.33 However, the economic growth rate has been decelerating in the EU since early 2007.

This slow down seems to have been caused by rising oil prices and the aggravation of financial

circumstances.34 The European GDP growth rate, which has been generally rising, has been forecasted

31 IBID.

32 Europa. Panorama of the European Union. 2009. January 2009

<http://europa.eu/abc/panorama/index_en.htm>. 33

Central Intelligence Agency. European Union. 2 April 2009. 1 April 2009 <https://www.cia.gov/library/publications/the-world-factbook/geos/ee.html>. 34

International Monetary Fund. "Country and Regional Perspectives." 2008. International Monetary Fund. 31 March 2009 <http://www.imf.org/external/pubs/ft/weo/2008/02/pdf/c2.pdf>.

19 | P a g e

to drop dramatically from 2.8% in 2007 to 0.9% in 2008.35 The GDP per capita in 2008 was $33,400;

however, the EU is currently having trouble concocting and implementing policies amongst its states,

due to the fact that they greatly differ in per capita income ($7,000 to $69,000).36 These are both seen

to be threats.

Source: Economic Intelligence Unit

Inflation

An area of specific interest is inflation. As international commodity prices increased, inflation

climaxed to 4% in mid-2008. However, with the economy slowing down, the rate dropped to 2.1% in

November. It is also estimated that it will keep dropping in 2009.37 This is a definite opportunity in the

market, as in the US, lower inflation will help buffer the impact of slower GDP growth and rising

unemployment.

35 Economist Intelligence Unit. Country Report - European Union . March 2009. 9 April 2009

<http://www.eiu.com.proxy.library.carleton.ca/index.asp?layout=displayIssueArticle&issue_id=1814375966&opt=full>. 36

Central Intelligence Agency. European Union. 2 April 2009. 1 April 2009 <https://www.cia.gov/library/publications/the-world-factbook/geos/ee.html>. 37

Economist Intelligence Unit. Country Report - European Union . March 2009. 9 April 2009 <http://www.eiu.com.proxy.library.carleton.ca/index.asp?layout=displayIssueArticle&issue_id=1814375966&opt=full>.

-5

0

5

2003 2004 2005 2006 2007 2008* 2009* 2010* 2011e

Real GDP Growth Rate (%)

20 | P a g e

Asia (Japan as a Proxy)

Japan’s GDP as of 2008 was 4.348 trillion.38 It is the third largest economy in the world, just after

China and US. When the global financial crisis hit Japan; this led the import sector’s sales to decline due

to the rise of the yen’s value and slow down of the world economy.39 Export and investment, the main

engines of economic growth in 2002-07, have now become the weakest components of the GDP. The

economy of Japan currently continues to decline, such that the GDP forecast for Japan in 2009 is said to

contract by 6.4%.40 The current economic conditions in Japan have created a threat to local businesses

in that many of them have had to stop their plans for capital investment, especially when credit is

tightening.41 At the same time, private consumption has and will continue to be constricted by falling

wages and an increase in unemployment. In 2009, the private consumption is predicated to shrink by

1.6%.42 This also creates a threat to the industry.

38 Central Intelligence Agency. Japan. 2 April 2009. 1 April 2009 < https://www.cia.gov/library/publications/the-

world-factbook/geos/ja.html l>. 39

The Japan Times. "Financial crisis hits home." 12 November 2008. The Japan Time Online. 22 01 2009 <http://search.japantimes.co.jp/cig-bin/ed20081112a1.html>. 40

Economist Intelligence Unit. “Country Data Japan.” Economic Data, EIU 41

IBID. 42

IBID.

0

1

2

3

4

2003 2004 2005 2006 2007 2008 2009* 2010* 2011e

Consumer Price Inflation

21 | P a g e

Unlike other countries, the financial crisis has heavily impacted Japan’s exchange rate. The

global financial meltdown, since September, has led to a strengthening of the yen against all other major

currencies. The key reason for this is that investors across the globe are deleveraging and reducing their

risk exposure (by opting for the safest liquid assets that they can find) in huge volumes.43 As the

Japanese Yen is one of the safest currencies, vast amounts of loans have been lent, in Yen, over the past

few years to foreign markets. As a result, the demand for the yen is surging. 44

The strengthening of the Yen has created a major threat for domestic manufacturers, while

creating an opportunity to foreign manufacturers. As the Yen strengthens against all major currencies,

such as the USD and the Euro, the cost to import tobacco products will decrease relatively, in

comparison to the past. In other words, the product margin for importing cigarettes into Japan will

increase compared to the domestic product that has remained stable. Therefore, it creates an

opportunity for foreign firms to increase their revenue.

43 Economist Intelligence Unit(EIU). Japan--country report. Country Report. United Kingdom: EIU, 2009.

44 IBID.

-4

-2

0

2

4

2003 2004 2005 2006 2007 2008 2009 2010 2011

Real GDP Growth

Source: EIU. 2008

100

120

140

160

180

2003 2004 2005 2006 2007 2008 2009 2010

Exchange rate Yen:Euro

22 | P a g e

Socio-Cultural Environment Trend

North America (US as a Proxy)

Social Attitudes towards Tobacco Consumption

Customers are increasingly drawn to

businesses and products that are green, organic,

natural, clean and sustainable. According to the

2007 ImagePower Green Brands Survey, “nearly all

Americans display green attitudes and behaviours

versus a year ago; when asked what their

perceptions were of green brands, respondents said

they are often seen as better quality, though at a higher cost.” Current research suggests that 72% of

the US population believes that smoking one or more packs of cigarettes a day is a great health risk.45 In

line with this popular mindset there have been many court filings, state laws, and public health

awareness campaigns around smoking that have resulted in negative social attitudes to smoking in the

US. This has led to a resilient decline in cigarette consumption. As a result, over the past 40 years, the

prevalence of smokers in the United States has declined

sharply, from 42% in 1965 to 20% today.46,47 This is a threat.

Youth Demographics

45 StateMaster. “Perception of Cigarette Smoking Risk (most recent) by state” Office of Applied Studies. January 10,

2008. <http://www.statemaster.com/graph/hea_per_of_cig_smo_ris-health-perception-cigarette-smoking-risk> 46

Government Printing Office. “Cigarette smoking and health characteristics: United States” . Vital and health statistics. Series 10. No. 34. Center for Disease Control and Prevention. July 1964–June 1965. <http://www.cdc.gov/nchs/data/series/sr_10/sr10_034acc.pdf> 47

Heyman KM, Schiller JS, Barnes P. “Early release of selected estimates based on data from the 2007 National Health Interview Survey.” National Center for Health Statistics, June 2008. <http://www.cdc.gov/nchs/about/major/nhis/released200806.htm.>

23 | P a g e

According to a survey from the Florida Department of Health among middle-and high-school

students (see adjacent graph), the percentage of students who definitely do not think that smoking

cigarettes makes young people “look cool” or “fit in” increased significantly from 1998 to 2000, and then

remained at approximately the same level during 2000-2007.48 As the 1994 report, by the Surgeon

General, "Preventing Tobacco Use among Young People", asserted, “When young people no longer want

to smoke the epidemic itself will die.” The social trend of cigarette being majorly unpopular among the

young generation is the most alarming threat that the tobacco industry will have to countervail. In

addition, the number of teenagers in the US is forecasted to fall by 3.5% to 28.7 million in 2015, which

will represent a fall in their proportion of the total population to 8.9%.49 As two thirds of tobacco

consumers begin smoking before the age of 19,50 the shrinking of the teenage population is a principle

concern. This is a threat.

Anti-smoking Campaigns

There are various non-profit groups in the US who lobby against smoking. The Great American

Smokeout is an annual event held by the American Cancer Society in the United States to encourage

Americans to quit smoking. The event challenges people not to smoke cigarettes for 24 hours, hoping

their decision to quit will last forever. It is held annually on the third Thursday in November.

Government education programs and non-profit advocacy groups have also found an ally in

pharmaceutical companies, which market smoking cessation aids as over the counter products in the

US. The American Legacy Foundation supports many programs directed at teenagers and adults. In one

of their commercials, teens stacked body bags outside a Philip Morris office building, representing the

annual number of deaths caused by smoking. This is a threat to the industry.

48 http://www.dchd.net/files/Ysocialattitudes.pdf

49 Consumer Lifestyles in the United States, GMID

50 Jones, Jeffrey. “Latest Gallup Update Shows Cigarette Smoking Near Historical Lows” GALLUP. June 25, 2007.

<http://www.gallup.com/poll/28213/Latest-Gallup-Update-Shows-Cigarette-Smoking-Near-Historical-Lows.aspx>

24 | P a g e

Contraband and Counterfeit Cigarettes

The trade in counterfeit cigarettes is a rapidly growing problem. And it costs tobacco

manufacturers hundreds of millions of dollars each year.51 It is impossible to know exactly how many

illicit cigarettes are bought each year since it is an illegal market, but the numbers are significant. As an

indication, the U.S. Bureau of Customs and Border Protection at the Port of Los Angeles recently seized a

shipment of 47,378 counterfeit Marlboro cartons.52 Philip Morris USA has under covered 30 such US

cases in the past four years!53 Since 2002, PM USA has identified the existence of contraband cigarettes

at retail outlets in 44 states and the District of Columbia.54 This is a significant threat to the industry.

Smokeless Snus

The smokeless snus is increasing in popularity in developed countries, while cigarettes are

declining in popularity.55 A snus is a form of tobacco that isn’t smoked. It consists of finely ground

tobacco that is packaged in tiny sachets. These tobacco filled sachets are placed under the upper lip. A

snus contains nicotine in similar quantities to cigarettes. Each sachet contains from 0.4 to 1.5 grams of

tobacco and is held in the mouth, without chewing or sucking.56 It is acknowledged by several

independent health experts to be at least 90 per cent less harmful than smoking cigarettes.57 A

particular review suggests that snus is notably less harmful to health than cigarettes, and that, in

Sweden, snus has served as a pathway away from smoking, rather than a gateway to smoking among

51 Philip Morris International Management SA. “The trade in fake cigarettes” Philip Morris International. Accessed

on January 20, 2008. <http://www.philipmorrisinternational.com/PMINTL/pages/eng/busenv/Counterfeiting.asp> 52

Philip Morris USA Media Relations. “Philip Morris USA Files Additional Lawsuits to Stop Importation of Counterfeit Cigarettes” Philip Morris USA. April 9, 2008. <http://www.philipmorrisusa.com/en/cms/Media/Company_Announcements/2008/Philip_Morris_USA_Files_Additional_Lawsuits_to_Stop_Importation_of_Counterfeit_Cigarettes.aspx?src=search> 53

IBID. 54

IBID. 55

GMID. “Tobacco – World.” 2007. 56

http://www.bat.com/group/sites/uk__3mnfen.nsf/vwPagesWebLive/DO6CKJNP?opendocument&SKN=1 57

http://www.bat.com/group/sites/uk__3mnfen.nsf/vwPagesWebLive/DO6CKJNP?opendocument&SKN=1

25 | P a g e

Swedish men.58 In Sweden particularly, snus gained popularity from the 1970s and overtook cigarettes

by the mid 1990s. There is a ban on snus in certain areas of the EU, claiming that it could appeal to

youth. Snus is an appealing alternative to cigarettes because it offers the same benefits of tobacco

without the harm of second-hand smoke. There is a widening market for this product among smokers

who concentrate in public areas where smoking is banned. Snus is more appealing than chewing

tobacco because of the ease of disposability that it offers. Snus maintains its composure, eliminating the

need to spit and facilitating its disposition.

Europe (The European Union as a Proxy)

According to the World Health Organization, there are about 606 billion cigarettes consumed by

Western Europeans every year59. It is also estimated that second-hand smoke killed 79,000 EU citizens

in 2006.60 However, trends in smoking related deaths are decreasing. In 2005, 30% of deaths were

attributable to smoking. This range varies from country to country as well as between genders. In 2006,

32% of Europeans were smokers, and 21% used to smoke; the majority of the smokers smoked

packaged cigarettes, these numbers are not taking much change. This is an opportunity as it often

means that the market is stable and consistent. It is said that 85% of Europeans who smoke, smoke

regularly, whereas only a mere 14% smoke occasionally.61 This is an opportunity to the industry, for as

most smokers smoke regularly, they are purchasing more cigarettes.

Socio-Economic Inequalities

58 Effect of smokeless tobacco (snus) on smoking and public health in Sweden: J. Foulds, L. Ramstrom, M. Burke, K.

Fagerstrom. Review, Tobacco Control, 2003. 59

World Health Organization. Cigarette Consumption. 2007. 2 April 2009 <http://www.who.int/tobacco/en/atlas8.pdf>. 60

Diethelm, Pascal and Martin Mckeen. Lifting the Smokescreen. France, February 2006. 61

European Comission. Attitudes of Europeans towards Tobacco. May 2007.

26 | P a g e

In general, women smoke less than men in the EU, but the number of women smokers are on

the rise, which is a definite opportunity. Smoking is also more popular amongst younger generations

than older ones; European youth have the highest smoking rates in the world. This may pose itself as a

threat because the European population is aging.62 Trends also show that smoking is more prevalent in

those who are less educated and that those with lower education levels are less likely to quit than those

with higher education levels63; this may also be seen as a threat, as more and more Europeans are now

heading towards higher education.64 There is also a higher rate of smokers amongst lower socio-

economic classes.65 The unemployed are 91% more likely to smoke regularly, which is a threat as

unemployment has decreased over the past few years.66

62 European Commission. EuroStat. 2009. January 2009

<http://epp.eurostat.ec.europa.eu/portal/page?_pageid=1996,45323734&_dad=portal&_schema=PORTAL&screen=welcomeref&open=/t_popula/t_pop/t_demo_pop&language=en&product=REF_TB_population&root=REF_TB_population&scrollto=160>. 63

European Union Public Health Information System. Smoking policies. 14 April 2008. January 2009 <http://www.euphix.org/object_document/o4899n27110.html>. 64

European Commission. EuroStat. 2009. January 2009 <http://epp.eurostat.ec.europa.eu/portal/page?_pageid=1996,45323734&_dad=portal&_schema=PORTAL&screen=welcomeref&open=/t_popula/t_pop/t_demo_pop&language=en&product=REF_TB_population&root=REF_TB_population&scrollto=160>. 65

European Union Public Health Information System. Smoking policies. 14 April 2008. January 2009 <http://www.euphix.org/object_document/o4899n27110.html>. 66

Scott, Andrew G. Economic Survey of Western Europe and the European Union. April 2009. April 2009 <http://www.europaworld.com.proxy.library.carleton.ca/entry/we.essay.4>.

64

66

68

70

2000 2001 2002 2003 2004 2005 2006 2007

% Population aged 25 to 64 with at least upper secondary education, EU

Source: EUROSTAT. 2008

27 | P a g e

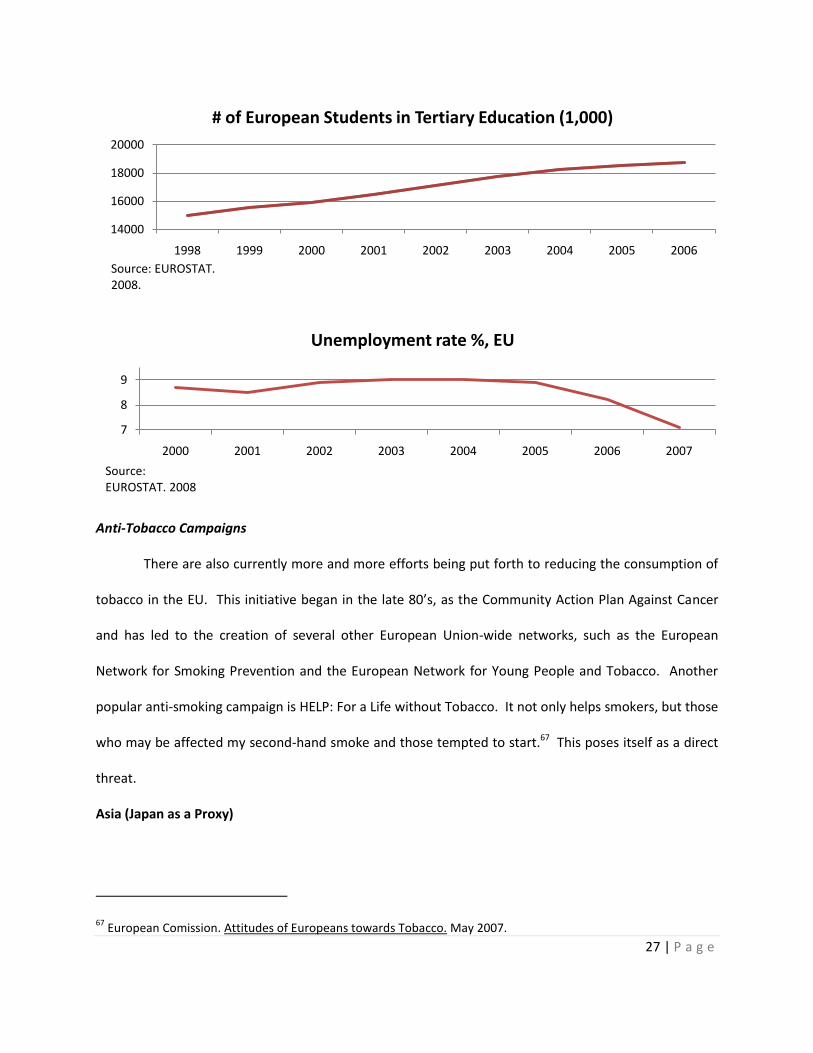

Anti-Tobacco Campaigns

There are also currently more and more efforts being put forth to reducing the consumption of

tobacco in the EU. This initiative began in the late 80’s, as the Community Action Plan Against Cancer

and has led to the creation of several other European Union-wide networks, such as the European

Network for Smoking Prevention and the European Network for Young People and Tobacco. Another

popular anti-smoking campaign is HELP: For a Life without Tobacco. It not only helps smokers, but those

who may be affected my second-hand smoke and those tempted to start.67 This poses itself as a direct

threat.

Asia (Japan as a Proxy)

67 European Comission. Attitudes of Europeans towards Tobacco. May 2007.

14000

16000

18000

20000

1998 1999 2000 2001 2002 2003 2004 2005 2006

# of European Students in Tertiary Education (1,000)

Source: EUROSTAT. 2008.

7

8

9

2000 2001 2002 2003 2004 2005 2006 2007

Unemployment rate %, EU

Source: EUROSTAT. 2008

28 | P a g e

In Japan, there are three major social trends that are affecting the cigarette industry: the aging

population, changing tastes and changes in the consumer segments.

Aging population

The aging population is one of the

most serious problems in Japan. This is

caused by lower birth rates and longer life

expectancies. In the year 2050, about 40%,

of the Japanese population will be 65 or older

compared to 2008, where around 25% of the

population was 65 or older. 68 The aging

population has two major affects on society.

The first is that with the increase in retired

workers, the current government will

experience trouble supporting the current

pension plans in place. The current debt of

the government already sits at $849 trillion;

to accommodate this, the government will

have to find new sources of revenue.69 One possible way to generate this income is to increase cigarette

sales taxes. In order words, this will create a threat to the industry, for an increase in taxes of cigarettes,

will decrease the sales margins. Secondly, the aging population has increased health awareness in the

68 Yamaguchi, Mari. One Fifth of Japanese population age 65 or Older in Rapidly aging Japan. 20 May 2008. 22 01

2009 <http://www.globalaging.org/elderrights/world/2008/japan.htm>. 69

Tabuchi, Hiroko. "Japan eyes new cigarette tax." The Wall Street Journal (2008).

29 | P a g e

society and has put smokers under greater pressure to quit smoking.70 This also presents itself as a

threat to the industry, as an increase in health awareness will inevitably lead to a decrease in demand

for cigarettes.

Changing taste and shift in consumer segments

Health awareness is not only a popular topic amongst the aging population, but also in the

younger generation as well. There is a trend of a shifting in preference towards tar levels. Smoking

cigarettes with high levels of tar is considered to be out of fashion and chauvinistic for the new

generation.71 In 2008, ultra low-tar cigarette sales overtook mid-tar cigarettes to become the biggest

category in sales, in Japan. It is forecasted that in 2012, the ultra low tar cigarettes are expected to

account for 31% share of retail volume sales. Moreover, there is also a trend stating that more smokers

prefer using premium products. This presents an opportunity to the industry which would allow

companies to develop new products to capture this part of the market share.

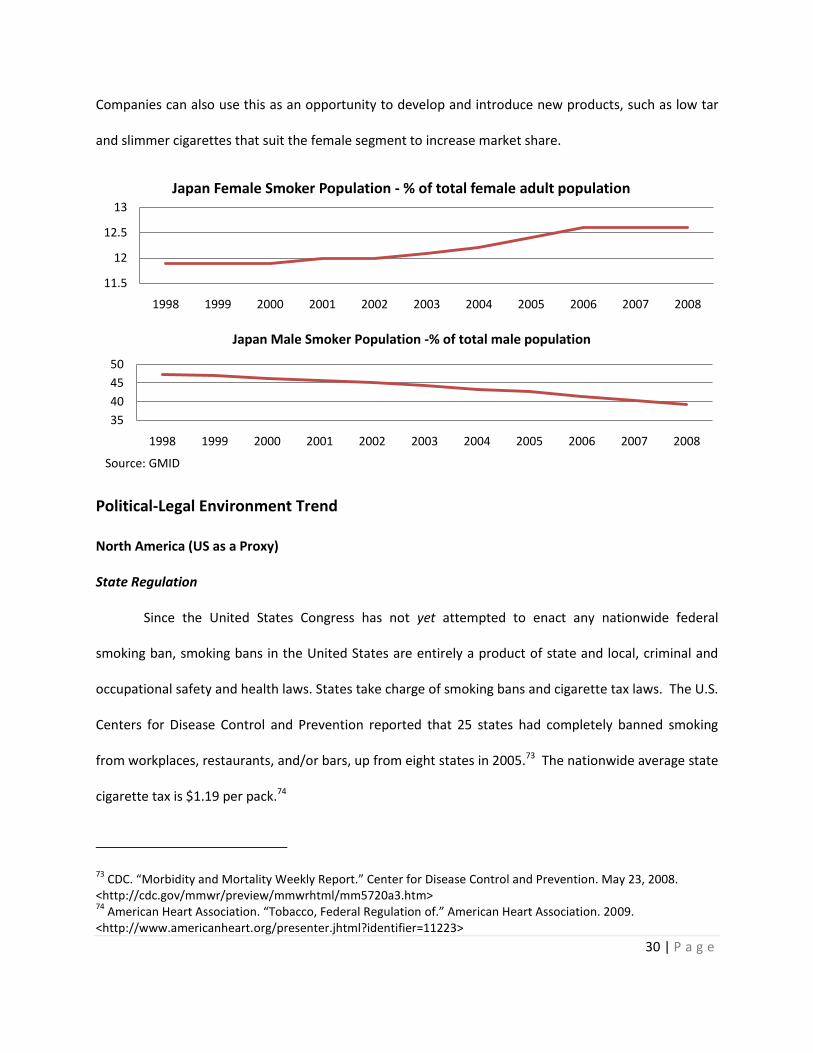

Furthermore, there is a trend in the market showing that the number of female smokers is

increasing, while the number of male smokers is decreasing.72 In other words, this is both an

opportunity and a threat for the industry, as the needs of female and male smokers are different.

70 GMID. "Consumer lifestyles--Japan." Country Report. 2006.

71 GMID. "Tobacco-Japan." Country Report. 2008.

72 IBID.

242526272829

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Japan Total Smoker Population -% of total adult population

Source: GMID

30 | P a g e

Companies can also use this as an opportunity to develop and introduce new products, such as low tar

and slimmer cigarettes that suit the female segment to increase market share.

Political-Legal Environment Trend

North America (US as a Proxy)

State Regulation

Since the United States Congress has not yet attempted to enact any nationwide federal

smoking ban, smoking bans in the United States are entirely a product of state and local, criminal and

occupational safety and health laws. States take charge of smoking bans and cigarette tax laws. The U.S.

Centers for Disease Control and Prevention reported that 25 states had completely banned smoking

from workplaces, restaurants, and/or bars, up from eight states in 2005.73 The nationwide average state

cigarette tax is $1.19 per pack.74

73 CDC. “Morbidity and Mortality Weekly Report.” Center for Disease Control and Prevention. May 23, 2008.

<http://cdc.gov/mmwr/preview/mmwrhtml/mm5720a3.htm> 74

American Heart Association. “Tobacco, Federal Regulation of.” American Heart Association. 2009. <http://www.americanheart.org/presenter.jhtml?identifier=11223>

11.5

12

12.5

13

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Japan Female Smoker Population - % of total female adult population

35

40

45

50

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008

Japan Male Smoker Population -% of total male population

Source: GMID

31 | P a g e

Tobacco Advertising

Tobacco advertising is regulated by the federal Cigarette Labelling and Advertising Act of 1965

and advertisements for cigarettes, like any other ads, are scrutinized under Section 5 of the FTC Act.

There are severe restrictions on advertising and packaging for cigarette manufacturers. The Tobacco

Master Settlement Agreement (MSA) places restrictions on tobacco product marketing, including a ban

on all outdoor advertising; transit advertising; the promotion of tobacco products in films and TV shows;

brand name sponsorship of team sports or other events with a significant youth audience; and the use

of cartoons in the advertising, promotion, packaging, or labelling of tobacco products (as youth are

particularly vulnerable to these).75 This is a threat.

Tobacco Packaging

The Comprehensive Smoking Education Act of 1984 requires that Surgeon General's Warnings

be printed on cigarette packages76. An example of these is "cigarette smoke contains carbon monoxide".

In July 2004, the Senate passed a bill that would make the health warnings larger, with more details

concerning the health risks of smoking. The House of Representatives is expected to approve the bill

before these changes become effective. This is a threat.

Cigarette Chemical Content

The Federal Trade Commission (FTC) also ensures a strict cap on cigarette chemical contents by

regularly testing for tar and nicotine through its outdated 1966 Cambridge Filter Method. As seen in the

current developments below, this regulation is being revised to ensure tighter control of cigarette

content. This is a threat.

Current Legal Developments

75 National Association of Attorneys General. "Master Settlement Agreement." National Association of Attorneys

General. 2008-07-30. < http://www.naag.org/backpages/naag/tobacco/msa/msa pdf/1109185724_1032468605_cigmsa.pdf> 76

Gochman. “Handbook of Health Behavior Research IV” Kluwer Academic Publishers. 2001

32 | P a g e

The FTC has long advocated for the development of a new test for tar and nicotine and has

sought assistance from the scientific community to determine what changes should be made to the

testing method.77 As a result, many have urged the reintroduction of S. 625, the Family Smoking

Prevention and Tobacco Control Act.78 The bill would allow the FDA, which has lacked any authority in

this area for decades, to regulate tobacco products. The bill would authorize FDA scientists to track,

analyze, and regulate the components of tobacco products. If such a bill is passed, the FDA would be

allowed to issue certain regulations concerning tar and nicotine yields, including requirements governing

the methodology for determining tar and nicotine yields and the public disclosure of information about

such yields or other constituents of tobacco smoke. The bill would also coordinate the FTC and the FDA

in enforcing labelling and marketing requirements. It is expected that such legislation will be supported

by the Obama administration. This is a threat.

The Obama Presidency

Barack Obama was inaugurated on January 20th 2008, as the first black president. The event

marks not only the installation of a widely acclaimed Democratic President, but also the leave of an

unpopular Georges W. Bush, as Republican President. This transition in US presidency is a momentous

event. According to experts, “the election of President Obama changes everything *…+ the year 2009 has

the potential to be the most historic year in making progress on tobacco at the federal level since the

first surgeon general’s report in 1964.”79 Quick action is expected on Food and Drug Administration

(FDA) regulation along with a 60% federal tax increase on tobacco and ratification of the above

77 Federal Trade Commission. “Prepared Statement of the Federal Trade Commission Before the Committee on

Commerce, Science, and Transportation, United States Senate” Federal Trade Commission. November 13, 2007, <http://www.ftc.gov/os/testimony/P064508tobacco.pdf> 78

Pamela Jones Harbour. “CONCURRING STATEMENT OF COMMISSIONER PAMELA JONES HARBOUR” Federal Trade Commission. November 26, 2008. < http://www.ftc.gov/os/2008/11/P944509cambridgefiltermethodharbourstmnt.pdf> 79

Wilson, Duff. “Democrats Plan an Early Push Against Tobacco.” New York Times. January 6, 2009. < http://www.nytimes.com/2009/01/06/business/06smoke.html>

33 | P a g e

Framework Convention.80 The proposed H.R. 1108 FDA legislation would set up a new office to deal

especially with tobacco, financed entirely by new industry fees. It also would allow further restraints on

sales and marketing to young people and provide for stronger warning labels, similar to ones in Canada

with graphic depictions of smoking-related illnesses.81 This is a threat.

Besides Obama’s direct impact on cigarette manufacturers, there are various political trends

that can be expected to have indirect effects on the tobacco industry. Contrasted with defunct President

Bush, President Obama seems to be more socially conscious. The Sierra Club has described Obama as

having a "strong record of support for clean air, wetlands protection, and clean energy." Obama believes

that the burning of fossil fuels has contributed significantly to global warming.82 Such a liberal view on

social issues will have a strengthening effect on the US collective social consciousness, of which cigarette

smoking is unfavorably perceived. This is a threat.

President Obama has been quoted saying “I think we need to rethink and decriminalize our

marijuana laws.”83 His campaign says that "he does not believe in legalization of marijuana, but agrees

with President Bush that long minimum sentences for first-time drug users may not be the best way to

occupy jail space or heal people from their disease."84 A temporary decrease in cigarette consumption is

to be expected as marijuana laws become more lenient.85 This is a threat.

Obama's health care plan includes implementing guaranteed eligibility for affordable health care

for all Americans, paid for by insurance reform, reducing costs, removing patent protection for

80 IBID.

81 IBID.

82 Willet, David. “Sierra Club Endorses Obama for President Joins United Steelworkers in Call for Clean Energy

Future” Sierra Club. June 19, 2008. <http://www.sierraclub.org/pressroom/releases/pr2008-06-19.asp> 83

WashingtonTimes.com “Obama: Decriminalize pot” The Washington Times. January 31, 2008. < http://www.washingtontimes.com/news/2008/jan/31/obama-decriminalize-pot/> 84

IBID. 85

Study relates marijuana and tobacco use. Yale Daily News. 19 January 2005. <http://www.yaledailynews.com/articles/view/12772?badlink=1>

34 | P a g e

pharmaceuticals, and required employer contributions.86 Such a policy will reduce healthcare costs for

cigarette smokers. However, it is also expected that the federal government will be more interested in

halting smoking prevalence in order to cut down health costs. This is both an opportunity and a threat.

Europe (The European Union as a Proxy)

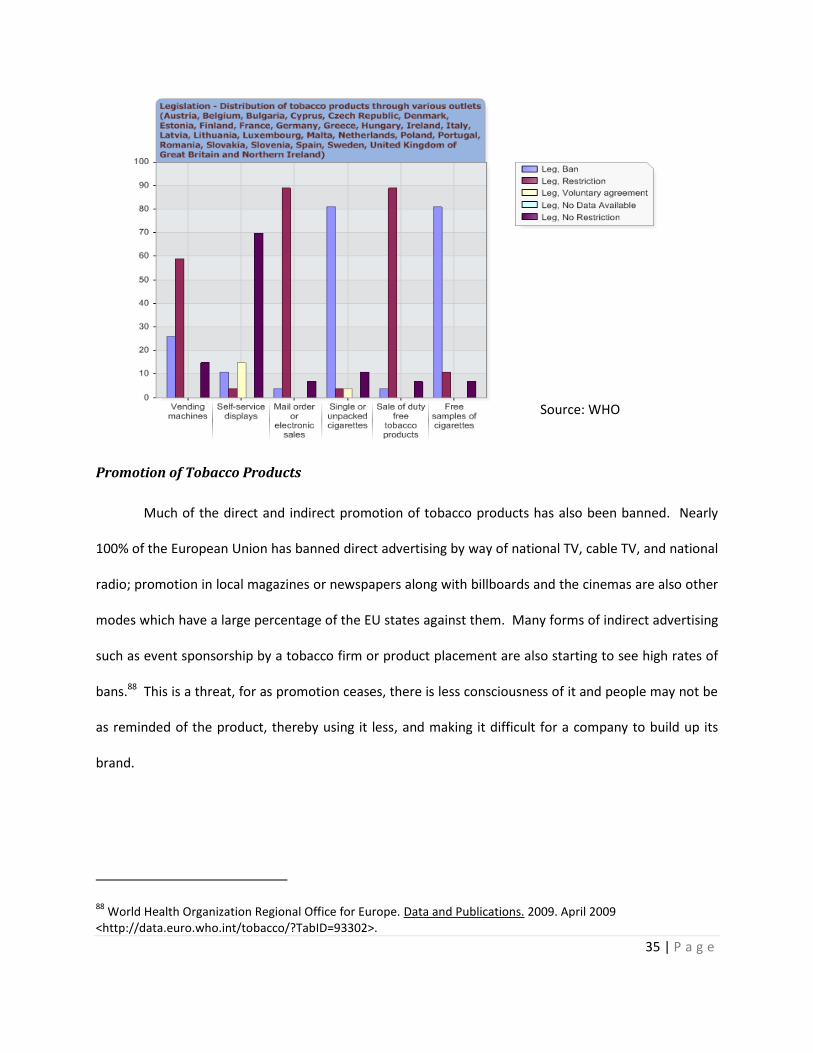

Cigarette Distribution Restrictions

The EU has come a long way in trying to prevent smoking within its boundaries. There have

been many laws, regulations as well as bans passed to ensure that citizens are leading a healthier and

longer life; and that nonsmokers are not impacted by the habits of those who do smoke. The EU has

banned the distribution of tobacco products, for the most part (80%), by way of single or unpacked

cigarettes and free samples. About 25% of the EU has banned the sale of cigarettes through vending

machines, but almost 60% have restricted it. Mail order or Electronic sales, along with the sale of duty

free tobacco, have also been restricted by nearly 90% of the EU. The majority have absolutely no

restriction on self-service displays.87 Restrictions on the sale of cigarettes definitely are a threat because

it limits their availability to the public.

86 Barack Obama. “Health Care.” Barrack Obama and Joe Biden. Januray 27, 2008.

<http://www.barackobama.com/issues/healthcare/> 87

World Health Organization Regional Office for Europe. Data and Publications. 2009. April 2009 <http://data.euro.who.int/tobacco/?TabID=93302>.

35 | P a g e

Promotion of Tobacco Products

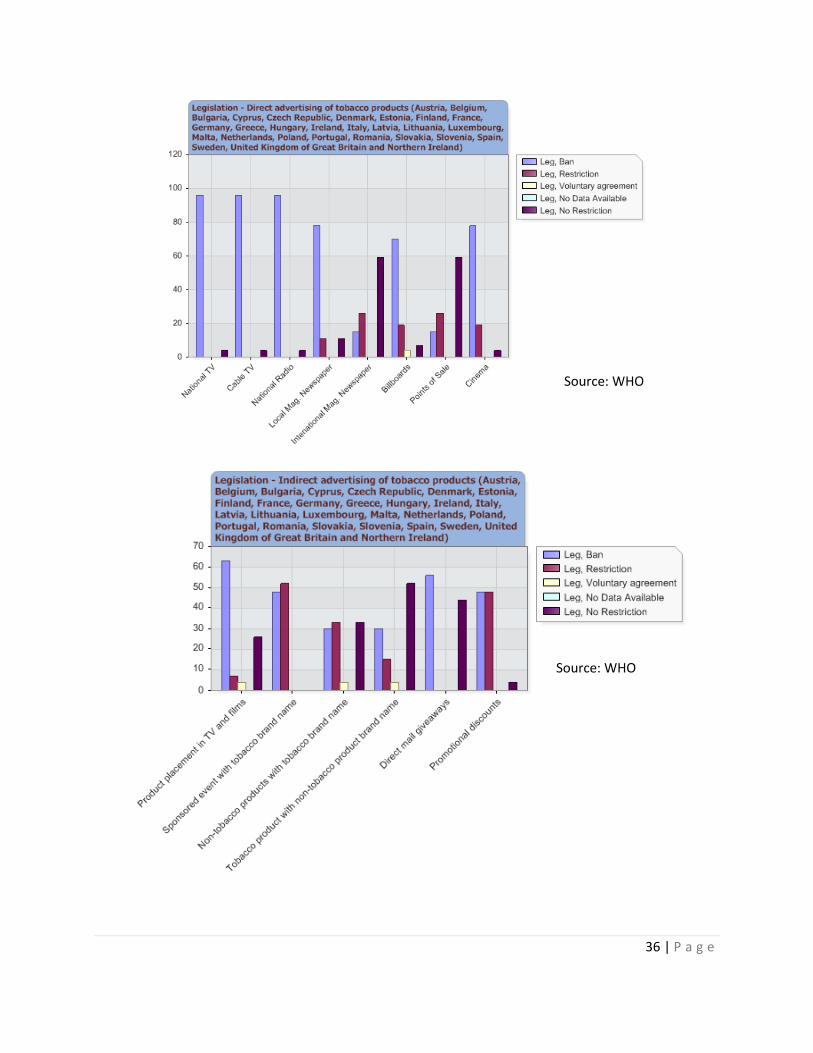

Much of the direct and indirect promotion of tobacco products has also been banned. Nearly

100% of the European Union has banned direct advertising by way of national TV, cable TV, and national

radio; promotion in local magazines or newspapers along with billboards and the cinemas are also other

modes which have a large percentage of the EU states against them. Many forms of indirect advertising

such as event sponsorship by a tobacco firm or product placement are also starting to see high rates of

bans.88 This is a threat, for as promotion ceases, there is less consciousness of it and people may not be

as reminded of the product, thereby using it less, and making it difficult for a company to build up its

brand.

88 World Health Organization Regional Office for Europe. Data and Publications. 2009. April 2009

<http://data.euro.who.int/tobacco/?TabID=93302>.

Source: WHO

36 | P a g e

Source: WHO

Source: WHO

37 | P a g e

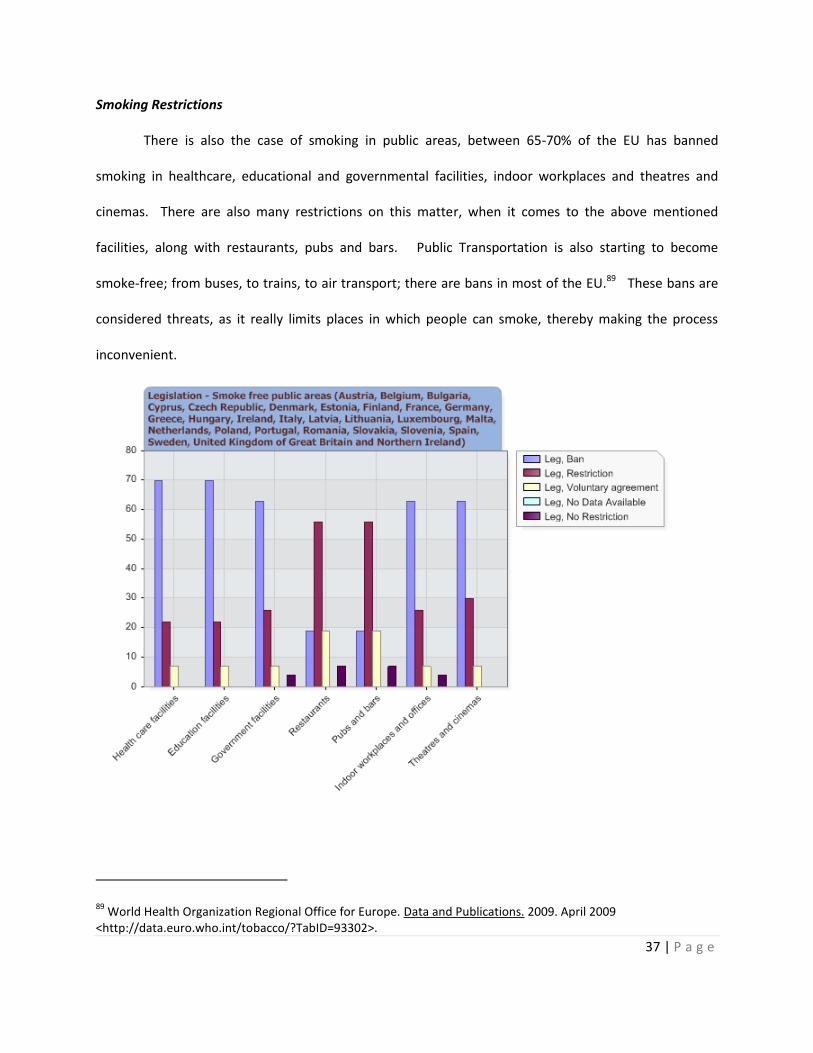

Smoking Restrictions

There is also the case of smoking in public areas, between 65-70% of the EU has banned

smoking in healthcare, educational and governmental facilities, indoor workplaces and theatres and

cinemas. There are also many restrictions on this matter, when it comes to the above mentioned

facilities, along with restaurants, pubs and bars. Public Transportation is also starting to become

smoke-free; from buses, to trains, to air transport; there are bans in most of the EU.89 These bans are

considered threats, as it really limits places in which people can smoke, thereby making the process

inconvenient.

89 World Health Organization Regional Office for Europe. Data and Publications. 2009. April 2009

<http://data.euro.who.int/tobacco/?TabID=93302>.

38 | P a g e

Packaging Restrictions

In May of 2001, it was law that tobacco products must have tobacco warnings covering 30% of

the front of the package and 40% of the back. The use of the words light or mild to describe tobacco

was also stopped, as it demoted the dangers of the product.90 These also pose as a threat as consumers

may be hesitant to purchase such a product.

Tobacco Taxation

The EU has also brought about taxation policies on tobacco products. All member states must

place at least a 57% tax on the retail price of the product. This has increased retail prices by a lot. This

has also led to the promotion of cigarette smuggling and counterfeit.91 Heavy taxation is a threat to the

industry.

Cigarette Smuggling and Counterfeit

Cigarette Smuggling and Counterfeit are becoming more and more popular in recent times.

They are leading to the loss in tobacco sales and taxes worldwide. In 2007, five of the EU member states

reported to having over 12% incidences of illicit trade.92 More and more are beginning to report the

same in Europe and this is also leading to nations losing out on income tax collection as many sellers do

not declare their earnings. These crimes are bringing about more problems as well. Consumers are not

getting the product they paid for and due to the lower cost; they are not seeing it as a crime but rather a

way to save money. There is also the question of civil rights for their workers; this type of business

often promotes child labour and poor working conditions.93

90 Corporate Social Responsibility (and the FMCG Market Response) GMID

91 Corporate Social Responsibility (and the FMCG Market Response) GMID

92 British American Tobacco. Africa and Middle East illicit trade map. 9 April 2009. 2 April 2009

<http://www.bat.com/group/sites/uk__3mnfen.nsf/vwPagesWebLive/DO6TNLJ9?opendocument&SKN=1&TMP=1>. 93

Phillip Morris International . Counterfeiting. 2009. 2 April 2009 <http://www.philipmorrisinternational.com/PMINTL/pages/eng/busenv/Counterfeiting.asp>.

39 | P a g e

Asia (Japan as a Proxy)

Japan has one of the biggest economies in the world; their regulations on smoking however, are

lagging behind. On the other hand, because of the increase in health awareness, international pressures

have influenced their policies significantly. This can further be demonstrated by the fact that Japan

joined the FCTC (The Framework Convention for Tobacco Control) in 2003.94 In order to comply with

FCTC, Japanese governments have continued to revise and implement law relating to the sale and

consumption of cigarettes. 95,96

Packaging

In 2003, the Japanese government imposed a Health Protection Law to implement larger health

warning signs on the packaging of cigarettes.97 The warning labels need to cover 30% of the main

surface area of the package.98 There are eight types of warning labels that will be used by the firms. This

is one of the major threats to the tobacco industry, as the demand of the product may decline, when

consumers see warnings about the health-related problems associated with smoking.

This new regulation has affected the sales of cigarette products; the company's cigarette sales

decreased by 5% in 2006 and by 4% in 2007 in retail volume terms.99

Advertisements

For a long time, Japan had no formal rules for or against advertisement on tobacco products.

There were only voluntary codes that were written by Tobacco Institute of Japan (TIOJ).100 In April of

94 Kazunari Satomura, Suketaka Iwanaga and Megumi Noami. “The Framework Convention on Tobacco Control

(FCTC) and Japnese anti-tobacco measures.” Report. 2008. 95

GMID. "Tobacco-Japan." Country Report. 2008. 96

Kazunari Satomura, Suketaka Iwanaga and Megumi Noami. “The Framework Convention on Tobacco Control (FCTC) and Japnese anti-tobacco measures.” Report. 2008 97

GMID. "Cigaratte--Japan." Country Report. 2008. 98

IBID. 99

GMID. "Tobacco-Japan." Country Report. 2008. 100

Kazunari Satomura, Suketaka Iwanaga and Megumi Noami. “The Framework Convention on Tobacco Control (FCTC) and Japnese anti-tobacco measures.” Report. 2008.

40 | P a g e

2005, because of the FCTC, the Japanese government imposed a law prohibiting selling tobacco

products to minors; the sponsorship of sporting and culturing events by tobacco firms and outdoor

billboards were also all banned. This creates a major threat to the industry for new companies, for it will

be harder for them to establish their brands in Japan.101

Distribution Network

In order to sell cigarettes in Japan, one needs to have been approved by the Ministry of Finance

to obtain a license. From July 2008, the Japanese government has further tightened regulations on

distribution channels, stating that now all vending machines require an electronic ID for purchasing

cigarette.102 Vending machines are one of the major distribution channels in Japan, they account for

more than 60.4% of total sales in the year of 2007.103 This increase in restriction is to support its strategy

for reducing the numbers of minors smoking in order to comply with the FCTC agreement, but this has

created a major threat, in that cigarettes sales will decline. At the same time, there is a trend in the

increase in sales in convenience stores by 6.7%, this is due to the fact that most individuals think it is

inconvenient to apply for the electronic ID. This has created an opportunity for the industry, in that the

company can capture market share by using this new trend as a tool. 104,105

Smoking Bans