Embed Size (px)

Citation preview

A Review of developments in

The Global & Indian Steel Industry

Monthly Special edition

Issue No. 37

April 2019 (Covering March 2019)

Compiled on behalf of Indian Steel Association,

By Mr. Anup Kashyap,

Senior Executive-Technical

Strictly for Internal circulation

About the Report

❑ The Indian Steel Association introduced a monthly report titled ‘A REVIEW

OF DEVELOPMENTS IN GLOBAL & INDIAN STEEL INDUSTRY’, from August

2016.

❑ The report provides general background information reviewing the status

of the developments in the global and Indian steel industry, pertaining to

raw material, production & consumption, trade, shipping, pricing &

forecasts, country reportage, policy developments, economic parameters

etc.

❑ The consistent format of the report provides an insight into the relevant

aspects of steel scenario globally and domestically .

❑ The information has been sourced from independent third party databases,

knowledge sources and news reports, and the authenticity of the same has

not been independently verified by ISA.

❑ The report is issued in the last week of each month to the members of

Indian Steel Association , various ministries / departments / institutions.

Contents of the Report

SI.

No

Title Page

Number

1. Global Economic Development 4-7

2. Global Steel Development 8-14

3. Domestic Steel Development 15-21

4. Indian Economic Development 22-24

5. About ISA 25-31

GLOBAL ECONOMIC DEVELOPMENTS

4

Source: Global Forecasting Service

Country-wise Growth Forecasts

2019 - 2023

As of April 17th 2019.

The assumptions for forecasts are available on the website of the Economist Intelligence Unit

In % 2019 2020 2021 2022 2023

India

Real GDP Growth 7.4 7.2 7.5 7.4 7.1

Inflation 3.3 3.2 3.9 4.4 4.1

China

Real GDP Growth 6.3 6.1 5.6 5.3 5.0

Inflation 2.6 2.5 2.6 2.8 2.7

U.S.A

Real GDP Growth 2.2 1.7 1.7 2.0 1.8

Inflation 2.2 1.4 2.2 2.1 2.1

Japan

Real GDP Growth 1.0 0.4 1.1 1.1 1.0

Inflation 1.5 1.7 1.0 1.2 1.4

EU 28

Real GDP Growth 1.4 1.5 1.8 1.9 1.8

Inflation 1.6 1.6 1.9 2.0 1.9

5

Source: BNP Paribas Wealth Management Report Issued in April 2019 6

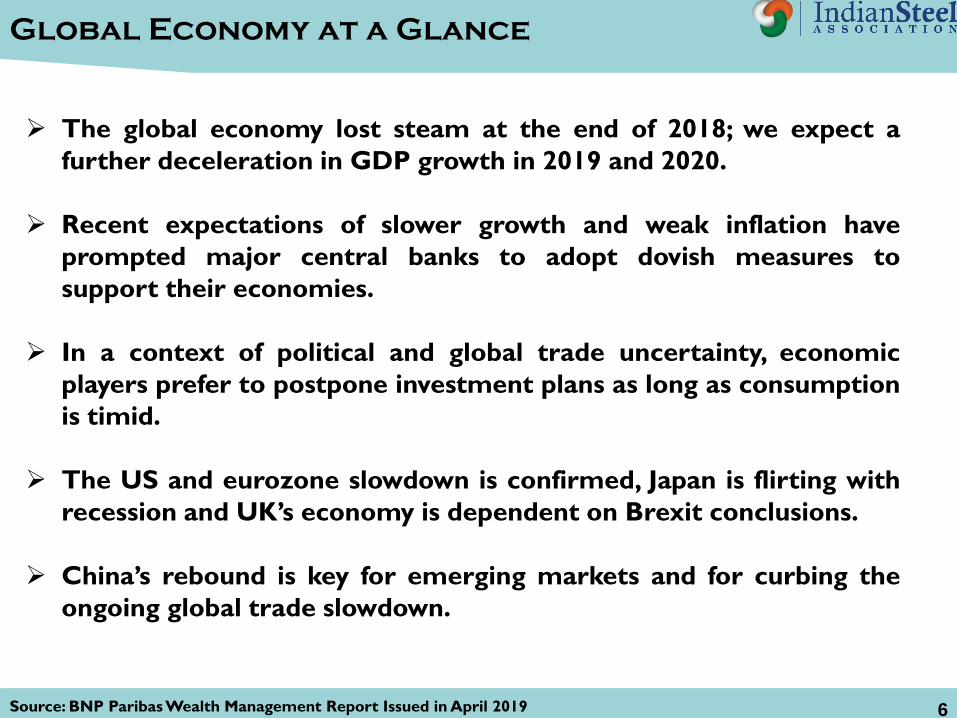

➢ The global economy lost steam at the end of 2018; we expect a

further deceleration in GDP growth in 2019 and 2020.

➢ Recent expectations of slower growth and weak inflation have

prompted major central banks to adopt dovish measures to

support their economies.

➢ In a context of political and global trade uncertainty, economic

players prefer to postpone investment plans as long as consumption

is timid.

➢ The US and eurozone slowdown is confirmed, Japan is flirting with

recession and UK’s economy is dependent on Brexit conclusions.

➢ China’s rebound is key for emerging markets and for curbing the

ongoing global trade slowdown.

Global Economy at a Glance

Source: World Fact on Industrial Production 7

❑ The United States is still the world’s largest economy with a nominal GDP of $18

trillion.

❑ The European Union ranks second with $16.8 trillion while China ranks third

with $11.2 trillion.

❑ Japan and Germany rank third and fourth respectively with $4.4 and $3.5 trillion

respectively.

❑ The UK, France, India, Italy, and Brazil complete the top ten in the order

4566

3602

13681050

672 572 505 478 442

0

1000

2000

3000

4000

5000

China USA Japan Germany India South

Korea

United

Kingdom

France Italy

Industrial Output in (USD Billion DOLLARS)

Countries With The Highest

Industrial Outputs In The World

❖ China leads the world in industrial output.

GLOBAL STEEL DEVELOPMENTS

8

Source: World Steel Association Short Range Outlook April 2019 9

Global Steel Demand

▪ The World Steel Association (worldsteel) forecasts global steel demand will

reach 1,735 Mt in 2019, an increase of 1.3% over 2018. In 2020, demand is

projected to grow by 1.0% to reach 1,752 Mt.

▪ In 2018, global steel demand increased by 2.1%, growing slightly slower than in

2017. In 2019 and 2020 growth is still expected, but in a less favourable economic

environment. China’s deceleration, a slowing global economy, and uncertainty

surrounding trade policies and the political situation in many regions suggest a

possible moderation in business confidence and investment.

▪ Chinese steel demand continues to decelerate as the combined effect of

economic rebalancing and trade tension is leading to slowing investment and

sluggish manufacturing performance. Mild government stimulus cushioned the

economic slowdown in 2018. In 2019, the government is likely to heighten the

level of stimulus, which is expected to boost steel demand.

▪ In 2020, a minor contraction in Chinese steel demand is forecasted as the

stimulus effects are expected to subside.

▪ Steel demand in the emerging economies excluding China is expected to grow by

2.9% and 4.6% in 2019 and 2020 respectively.

Source: World Steel Association,f-Forecast 10

0 500 1000 1500 2000

European Union (EU28)

Other European Countries

CIS

NAFTA

Central and South America

Africa

Middle East

Asia and Oceania

World

Region Wise Steel Demand in Million ton(MT)

2020(f) 2019(f) 2018

▪ Steel demand in the developed economies grew by 1.8% in 2018 following a resilient 3.1% growth in

2017. WSA expect demand to further decelerate to 0.3% in 2019 and 0.7% in 2020, reflecting a

deteriorating trade environment.

▪ The EU economies also face the deteriorating trade environment and uncertainty over Brexit.

▪ Steel demand in developing Asia excluding China is expected to grow by 6.5% and 6.4% in 2019 and

2020 respectively, making it the fastest growing region in the global steel industry. In the ASEAN

region, infrastructure development supports demand for steel.

Region Wise Steel Demand

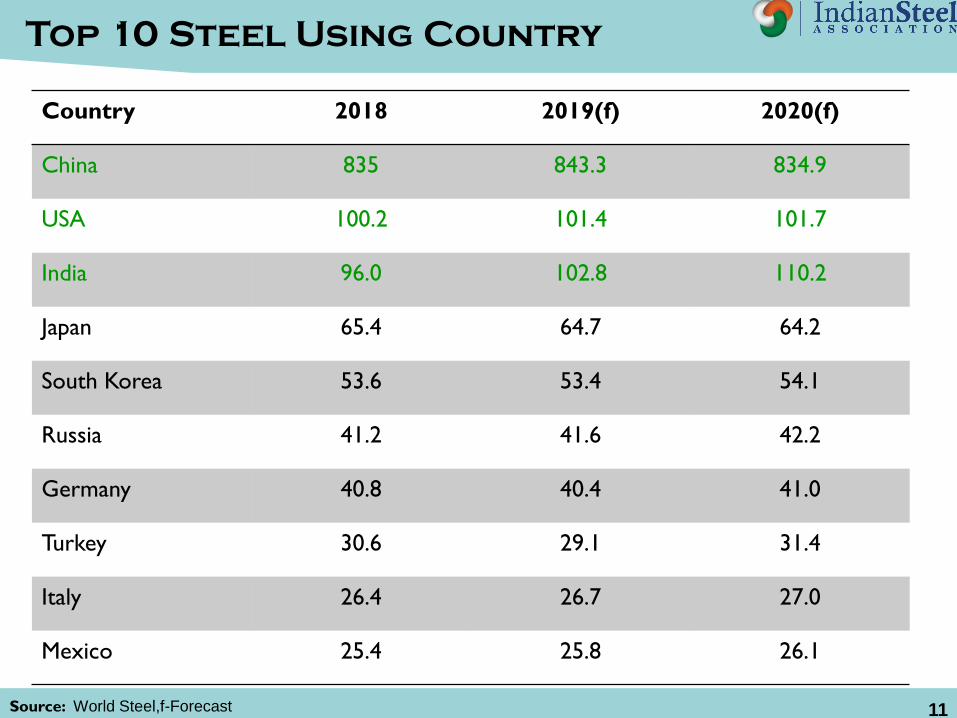

Source: World Steel,f-Forecast 11

Country 2018 2019(f) 2020(f)

China 835 843.3 834.9

USA 100.2 101.4 101.7

India 96.0 102.8 110.2

Japan 65.4 64.7 64.2

South Korea 53.6 53.4 54.1

Russia 41.2 41.6 42.2

Germany 40.8 40.4 41.0

Turkey 30.6 29.1 31.4

Italy 26.4 26.7 27.0

Mexico 25.4 25.8 26.1

Top 10 Steel Using Country

Source: World Steel 12

Trend in Global Sectorial

Growth in Steel

▪ As pent-up demand and government stimulus measures subsided, the automotive

industry saw a sharp slowdown in growth in 2018 in many countries, in particular in

the EU, Turkey and China. The largest decline was observed in Turkey (-9.0%) and in

the UK (-5.5%). As a result, global auto production growth decelerated to 2.2% in

2018 from 4.9% in 2017.

▪ In 2019, global auto production will continue to decelerate to 1% growth with

stabilisation expected in 2020. However, in Latin America, especially in Brazil, auto

production will buck the trend and continue to show a steady rebound.

▪ The momentum of construction activities is also expected to moderate a bit in the

developed economies, but thanks to the rebound in the developing economies, global

growth will be maintained at a 3% level in 2019-20. However, in China, Turkey, South

Korea and Argentina, construction activities are expected to continue to contract in

2019.

▪ With weakening investment and a worsening trade environment, the global machinery

sector is expected to show a steady deceleration that will last till 2020, which will be

more pronounced in major production hubs such as Germany, Japan and China.

Source: US Custom data 13

Trend in USA Steel Export

▪ USA world’s largest ferrous scrap exporter and one of the leading steel exporter observed

rebound in ferrous scrap export in Feb 2019,whereas export of coal ,Iron Ore and finish

steel products dropped on monthly premises against volume registered in Jan 2019.

▪ Largest Importer Turkey with 25% share in total USA Scrap export observed rise of 90

%.Other scrap importer were South Korea with 18% share and Taiwan with 11% Share.

▪ Nation’s flat steel export move down by 7% in Feb 19 to 0.42 MT which was 0.45 Mt in Jan

2019.During the first two months nation’s flat steel exports registered fall by 14% to 0.87

MT as compared to 1.01 Mt in the same time period of previous year.

Particulars Quantity in tons M-o-M % Y-o-Y %

Coal 9,759,163 -18.8 -17

Finish Flat 419,407 -6.6 -15.3

Iron Ore 191,767 -65.5 -11.7

Finish Long 65,361 -7.2 -46.8

Graphite Electrode 1,112 -16 20.3

US Steel Export in Feb 2019

Source: Coal Mint Research 14

▪ Seaborne premium hard metallurgical coal prices have inched slightly lower this week on

muted trading activity in FOB market amidst thin buying interest for spot cargoes from

Northeast Asia Steel makers.

▪ Latest Offers fro Premium HCC grades was around $ 203.75 per ton FOB Australia, For

Indian Buyers the offer was amount $ 216.25 per ton on CNF India basis.

Trend in Coking Coal Price

DOMESTIC STEEL DEVELOPMENTS

15

Source: Joint Plant Committee, Ministry of Steel 16

April – March

2018-19

April-March

2017-18

% Change over April

– Mar. ,2017-18%

Quantity in Million tons

Crude Steel 106.56 103.13 3.3

Finished Steel

Production for Sale 131.57 126.86 3.7

Import 7.83 7.48 4.7

Export 6.36 9.62 -33.9

Real Consumption 97.54 90.71 7.5

Status of Indian Steel Industry

➢ Production of crude steel was at 106.56 million tonnes (mt), a growth of 3.3%.

➢ At 138 mt, crude steel capacity indicated an utilisation of 77% compared to 75% of last year.

➢ Total finished steel gross production was 131.57mt, an increase of 3.7%.

➢ Export of total finished steel reached 6.36mt, a decrease of 33.9%.

➢ Import of total finished steel was 7.83mt, an increase of 4.7%.

➢ India was a net importer of total finished steel.

➢ Consumption of total finished steel was 97.54mt, an increase of 7.5%.

Source: Ministry of Steel Report March 2019. 17

Trend in Indian Steel Export and Import(MT)

0

5

10

15

2014-15 2015-16 2016-17 2017-18 2018-19

TREND IN STEEL EXPORT AND IMPORT IN MILLION

TONS

Import (MT) Export (MT)

➢ Total finished steel exports stood at 6.36 mt in 2018-19 and declined by 33.9% over 2017-

18 while imports stood at 7.83mt and increased by 4.7% in 2018-19 over 2017-18.

➢ Such trends implied that India emerged as a net importer of total finished steel in 2018-19

in contrast to its net exporter status of 2017-18.

➢ Korean imports (2.94 mt) had the largest share (37%) in major flat items, making it the

largest import market for India during this period. China (imports down by 19%) was the

2nd largest import market, with its share in overall total falling from 26% in 2017-18 to 20%

in 2018-19.

➢ Import of total finished steel valued at Rs.

49317 crore in 2018-19.

➢ Nepal (13% share) was the largest export

market for India during this period.

➢ Exports of total finished steel valued at Rs.

33153 crore in 2018-19.

Source: Joint Plant Committee March 2019 18

47%

26%

27%

Route Wise Steel Production in %-2018-19

% Share of

Oxygen Furnace

% Share of EAF

Route

%Share of

Induction Furnace

Route

Crude

Steel-

106 MT

Route Wise Steel Production in India

➢ Total Steel Production in India in

2018-19 was 106 Million ton.

➢ Oxygen Furnace contributed 47 %

in Production in 2018-19 which was

46 % in 2017-18.

➢ Share of Electric Arc Furnace (EAF)

route was 26 % in 2018-19 which

was similar in 2017-18.

➢ Share of Induction Furnace was

27% in 2018-19 which was 28 % in

2017-18.

➢ Public Sector unit (SAIL and RINL)

produced around 21 MT in 2018-19

and shared around 20 % in total

Steel production of India.

Source: Steel Mint Research 19

Trend of Domestic Steel Price of India

➢ Current trade reference prices in trades for HRC (IS2062) 2.5-8 mm is around Rs 42000

per ton (ex- Mumbai).The Prices mentioned above are basic price excluding GST @18 %

on cash payment basis.

➢ Currently trade reference prices for CRC (IS513 ) 0.9 mm is in the range of INR 47000 per

ton (ex-Mumbai). The Prices mentioned above are basic price excluding GST @18 % on

cash payment basis.

Source: Steel Mint Research 20

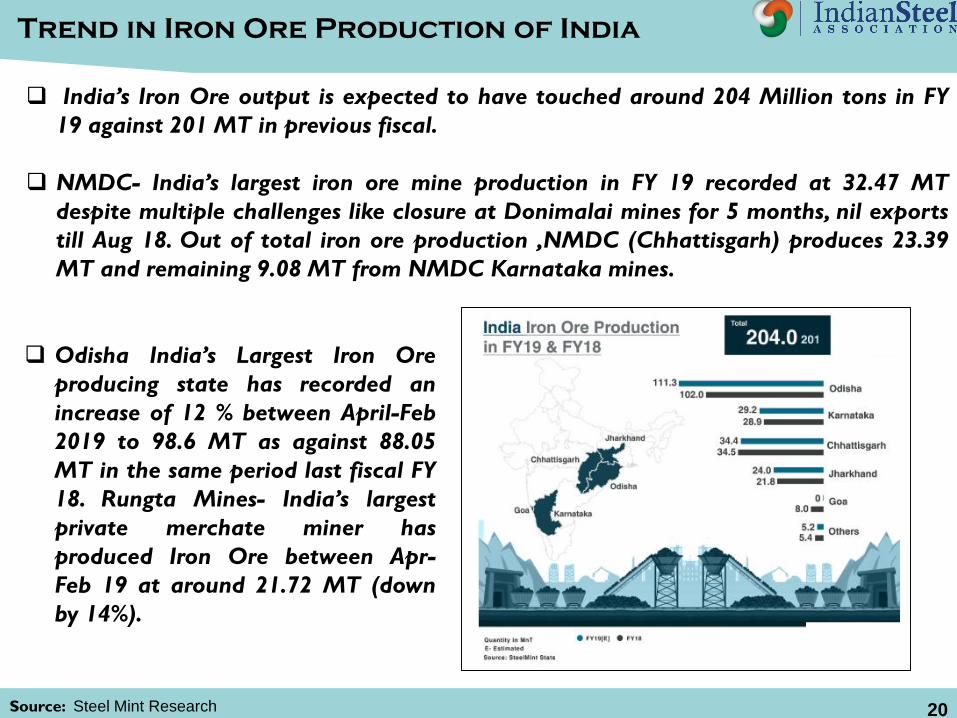

Trend in Iron Ore Production of India

❑ India’s Iron Ore output is expected to have touched around 204 Million tons in FY

19 against 201 MT in previous fiscal.

❑ NMDC- India’s largest iron ore mine production in FY 19 recorded at 32.47 MT

despite multiple challenges like closure at Donimalai mines for 5 months, nil exports

till Aug 18. Out of total iron ore production ,NMDC (Chhattisgarh) produces 23.39

MT and remaining 9.08 MT from NMDC Karnataka mines.

❑ Odisha India’s Largest Iron Ore

producing state has recorded an

increase of 12 % between April-Feb

2019 to 98.6 MT as against 88.05

MT in the same period last fiscal FY

18. Rungta Mines- India’s largest

private merchate miner has

produced Iron Ore between Apr-

Feb 19 at around 21.72 MT (down

by 14%).

Source: Steel mint Research 21

Trend in Coal Import in Million Tons

INDIAN ECONOMIC DEVELOPMENT

22

Source: Central Statistical Organisation 23

➢ The growth rate of the Index of Industrial

Production (IIP) was up by 4 % during April -

February 2018-19 (prov.), encouraged by stable

growth in Electricity (5.5 %), Manufacturing (3.8

%) and Mining (3 %).

➢ The Use-Based scenario of the Index of Industrial

Production (IIP) during April –February 2018-19

(prov.) show that excepting a minor decline in

Intermediate Goods, all the other sectors

recorded a growth with Infrastructure /

Construction Goods (7.7 %)reporting the highest

and Primary Goods, the lowest (3.6 %).

➢ The growth rate of the Eight Core Infrastructure

Industries was up by 4.3 % during April – February

2018-19 (prov.), encouraged by growth in most

sectors, specially Coal (7.1 %) and Cement (13 %),

Electricity (5.4 %) but pulled down by decline in

growth rates in case of Crude Oil (4 %) and

Fertilizers (0.02 %).

Indian Economic Highlights

Source: Reserve Bank of India

CurrencyDate

26th April 2019

I USD 70.14

1 EUR 78.12

1 GBP 90.53

100 YEN 62.80

Base Rate : 8.95-9.40 %

Savings Deposit Rate : 3.50-4.00 %

MCLR (Overnight) : 8.05-8.50 %

Term Deposit Rate > 1 year : 6.25-7.50%

Policy Repo Rate : 6.00 %

Reverse Repo Rate : 5.75 %

Marginal Standing Facility Rate : 6.25 %

Bank Rate : 6.25 %

CRR : 4 %

SLR : 19.00%

Reference Rates

Lending/ Deposit Rates

Reserve RatiosPolicy Rates

Rates at Reserve Bank of India

2019

24

ABOUT ISA

25

About ISA

➢ The Indian Steel Association (ISA) is the voice of the Indian Steel Industry,

in both domestic and global forums. It is at the forefront of all

deliberations pertaining to matters of public & regulatory policy, raw

materials, international trade, logistics, environmental concerns,

technology and other aspects of steel-making. The Indian Steel Industry

looks at ISA to further its critical agenda of sustained growth, both in

steel production and in generating domestic demand.

➢ ISA was formed in 2014 and has 15 members – eight full members and

seven affiliates. The list of full members includes –Steel Authority of India

(SAIL) and Rashtriya Ispat Nigam Ltd (RINL) – while heavyweights from

the private sector include JSW Steel Ltd, Tata Steel Ltd, Jindal Steel and

Power Ltd, Essar Steel India Ltd, Bhushan Power and Steel Ltd and Tata

Steel BSL Ltd. ISA, an affiliate member of World Steel Association (WSA),

regularly collaborates with WSA on the organisation of events, as well as

taking part in other key meetings with global partners.

26

Our eight Full Members are:

• Tata Steel Ltd

• Steel Authority of India Ltd.

• JSW Steel Ltd.

• Rashtriya Ispat Nigam Ltd.

• Essar Steel Ltd.

• Jindal Steel & Power Ltd.

• Tata Steel BSL Ltd.

• Bhushan Power & Steel Ltd.

Our Seven Affiliate Members are Monnet

Ispat & Energy Ltd., INSDAG (Institute

for Steel Development and Growth),

KISMA (Karnataka Iron and Steel

Manufacturer’s Association), Arjas Steel,

Visa Steel, Electrosteel Steels and Orissa

Metalliks Pvt. Ltd

Members of Indian Steel Association

27

Vision and Objectives of ISA

➢Vision of ISA-

To work towards transforming the Indian Steel Industry as a

global leader acclaimed for its Quality, Productivity and

Competitiveness, with a focus on health, safety and

environment, along with a growing thrust on innovation through

R&D, adopting an inclusive and collective approach.

➢ Objectives of ISA-

▪ Promoting steel by raising awareness about the numerous

advantages of good quality steel

▪ Collaborating with international steel organizations to

tackle issues of mutual interest.

▪Working with the government on matters affecting the

steel industry.

28

Important Ministries/Department/Organization

Ministry of Steel

Name of the person Designation Contact Details

Shri Binoy Kumar Secretary [email protected]

Shri Saraswati Prasad Special Secretary & Financial Adviser [email protected]

Smt. Rasika Chaube Additional Secretary [email protected]

Smt. Ruchika Chaudhry Govil Joint Secretary [email protected]

Shri Puneet kansal Joint Secretary [email protected]

Ministry of Mines

Name of the person Designation Contact Details

Shri Anil Gopishankar Mukim Secretary [email protected]

Dr. K. Rajeswara Rao Additional secretary [email protected]

Ministry of Commerce

Name of the person Designation Contact Details

Shri Anup Wadhawan Secretary [email protected]

Shri Shudhanshu Pandey Additional Secretary [email protected]

Shri Alok Vardhan Chaturvedi DGFT [email protected]

Dr. K.C.Rout Additional Secretary-DGFT [email protected]

Ministry of Environment, Forest and Climate Change

Name of the person Designation Contact Details

Shri C K Mishra Secretary [email protected]

Control Pollution Central Board

Name of the person Designation Contact Details

Shri S.P. Singh Parihar Chairman [email protected]

Dr. Prashant Gargava Member Secretary [email protected]

Ministry of FinanceName of the person Designation Contact Details

Shri Rajiv Kumar Joint Secretary [email protected]

29

Contact Us for data related issues

Address:207-208, 2nd Floor

Kailash Building

New Delhi -110-001

India

Tel: +011 4266 8811

Fax: +011 4266 8805

E-mail: [email protected]

Website: http://indsteel.org/30

THANK YOU

DISCLAIMER

The material in this presentation has been prepared by Indian Steel Association (ISA) and is a general background information reviewing the

status of the developments in the global and Indian steel industry as at the date of this presentation. This presentation is strictly for internal use

of all the member companies of ISA, whose names have been stated in the presentation.

Information is given in summary form and does not purport to be complete or all inclusive. The information has been sourced from independent

third party databases, knowledge sources and news reports, and the authenticity of the same has not been independently verified by ISA.

Additionally, any third party forecasts on financial or economic parameters, projections or estimates should not be construed as an investment

advice or a recommendation to any ISA member. Recipients of this presentation from member companies of the ISA should each make their own

evaluation of the contents and adequacy of the information contained in the presentation.

ISA does not undertake any obligation to publicly release any changes to any revisions, modifications or forward looking statements in the

subsequent editions of this bi-monthly presentation. Unless otherwise specified, all information is for the period April 2019 or prior.

31