Embed Size (px)

Citation preview

1

Advanced Accounting“Path towards IFRS”

2

Introduction

• What is IFRS?– International financial reporting standards are

a set of accounting standards developed by the international accounting standard board that is becoming the global standard for the presentation of public company financial statements

3

Introduction

• Why IFRS?– Demand for one set of common global

reporting Standards– International Companies desire to use one set

of financial standards throughout the world– Growth in capital markets ( IFRS enhances

the ability of filers to raise capital outside their borders)

– Reducing Capital Cost and Reporting Costs

4

How India is Converging?

• Specified approach

• Thirty Five IND AS

• Date of Implementation

• Comparatives

5

Road Map by ICAI

• Two separate sets of accounting standards

• The first set would comprise of IFRS converged accounting standards (IND AS)

• The second set would comprise of existing Indian Accounting Standards

6

Specified Approach

• Specified class of companies• Listed Companies• Un listed companies having networth of 500

Cr INR or more• Holding & Subsidiaries of companies covered

above

7

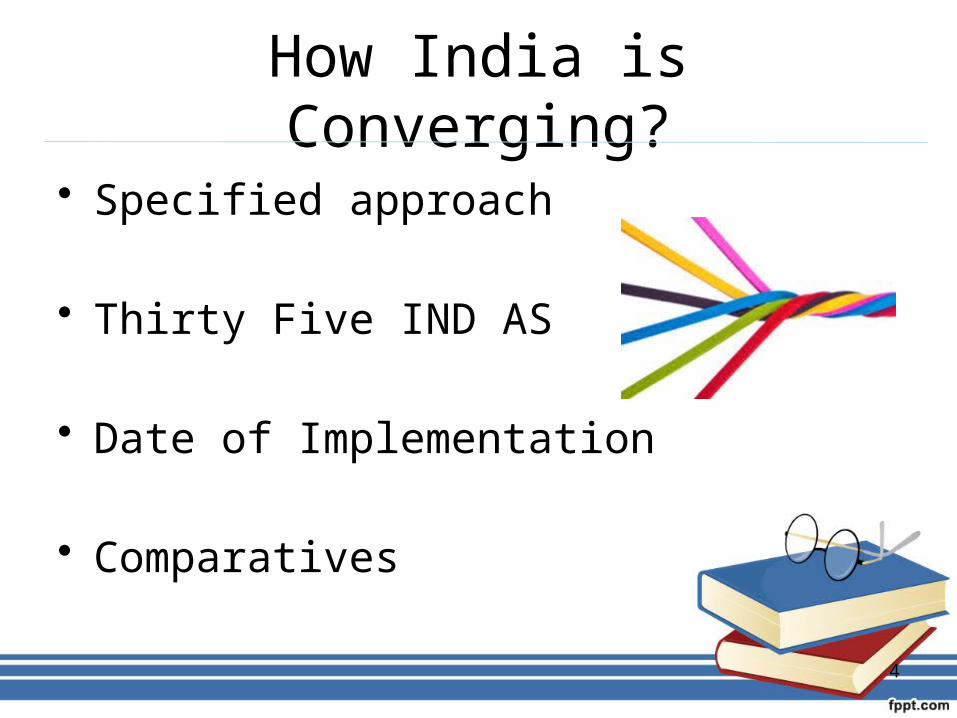

ComparativesFor this purpose an entity should in its op IND AS B/sA)All assets and liabilities whose recognition is required by IND ASB)Not recognize items as assets or liabilities if IND AS do not permit

such recognitionC) Reclassify the items that it recognized in accordance with IND ASD) Apply IND AS in measuring all recognizing assets and liabilites

• It may also be noted that the op. balance Sheet is to be prepared on the date of transition ie., the beginning of the earliest comparative period presented eg: If an entity adopted IND AS from 2016-17 its date of transition will be 1st April 2015 and thus it required to prepare its opening IND AS balance sheet on 1st April, 2015

8

Other Clarifications …….

• Voluntary Adoption– Option for Other than specified companies

• Net worth– Share Capital + Reserve less revaluation

reserve

9

Impact of IFRS

• IFRS is heavy on Transparency and impact accounting

• All the events that have impact on company’s finances have to be accounted

• It also stringent income recognition rules• Global Benchmarking

10

Benefits of Global Compatibility– The Economy– Corporate world– Investors– Accounting Professionals– Bank/Financial Institutions– Regulators

11

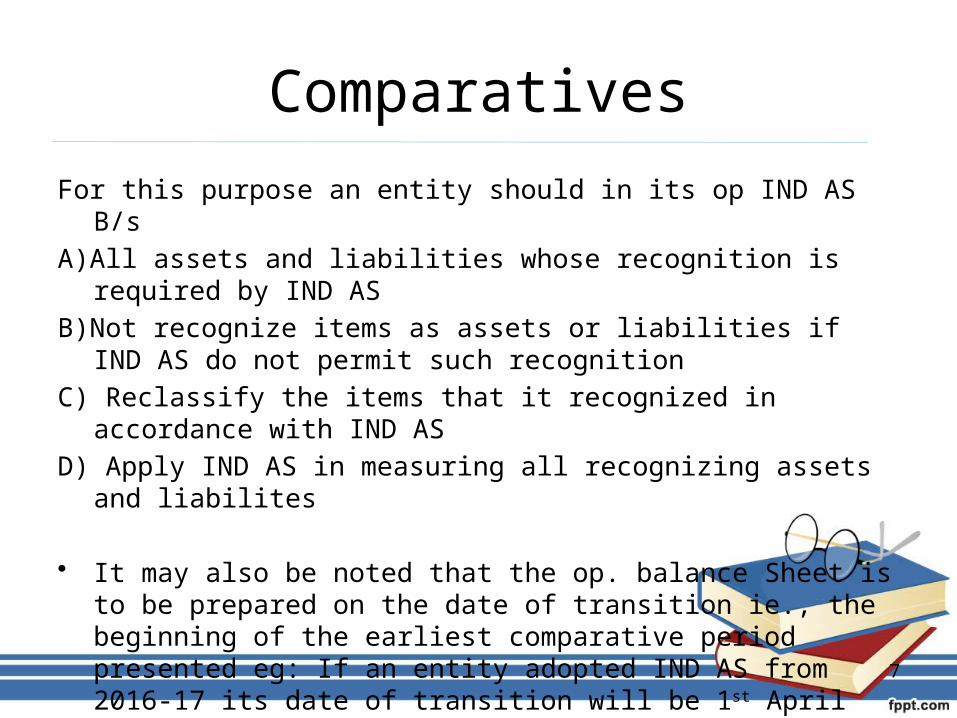

Major Changes of AS/IFRS • Principal Based Vs Rule Based Standards• Standards Vs Local Laws• Presentation of Financial Statements• Depreciation on Fixed assets• Cash Flow Statements• Valuations• Changing in Accounting policy• Adoption Methodology

12

Key Challenges….!!

• Economic Environment

• SME’s problems

• Training to preparers

• Interpretation

13

IND AS & Carve Outs

What is Carve Out??Difference between IND

AS and equivalent requirement under IFRS

14

Categorization….

• Mandatory Deviations from IFRS

• Optional Deviations from IFRS

• Removal of Choices

• Others

15

Mandatory Deviations…..

• Recognition – Revenues from sales of real estate on a

percentage basis– embedded foreign currency conversion option

as equity– Bargain purchase gains as capital reserves– Mandatory use of Govt. securities yields– Fair value of financial liabilities

16

Optional deviations….

• Choice to– Defer exchange differences

– Deemed Cost for fixed assets

– De recognition provisions prospectively

– Exemption for financial instruments

17

Removal of Choices…

• Single Statement presentation• Classification of

– Expenses – Interest and Dividend

• Carry investment property at fair value• Govt. grants should be classified as

deferred income• Recognition of actuarial gains in reserves

18

Others ….

• No Separate guidance on accounting for biological assets

• Deferral of accounting for embedded leases

• Deferral of accounting for service concession arrangements

• Goodwill may be recognized

19

Statutory’s Initiatives

• Providing education and training– Certification courses offered– IFRS e-learning course has been launched– Large scale IFRS awareness drive with MCA

collaboration – Conceptual differences with IASB– Organizing of Workshops

20

Conclusion

• Irrespective of challenges adoption of IFRS in INDIA will significantly change the contents of corporate financial statements as a result of :

More refined measurementsEnhanced disclosures

21

Truthful remarks….

A small truth to make our Life 100% successful ..........

If A B C D E F G H I J K L M N O P Q R S

T U V W X Y Z Is equal to 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

17 18 19 20 21 22 23 24 25 26

22

Continued……

Then • H+A+R+D+W+O+R+K

=8+1+18+4+23+15+18+11 = 98%

K+N+O+W+L+E+D+G+E = 11+14+15+23+12+5+4+7+5 =96%

L+O+V+E = 12+15+22+5= 54%

L+U+C+K = 12+21+3+11 = 47% • (None of them makes 100%) ..............................Then what

makes 100% Is it Money? ..... No!!!!! Leadership? ...... NO!!!!

23

Continued…..

Every problem has a solution, only if we perhaps change our "ATTITUDE". It is OUR ATTITUDE towards Life and Work that makes OUR Life 100% Successful..

A+T+T+I+T+U+D+E = 1+20+20+9+20+21+4+5 =

24

PRESENTATION

By ADITYA AMAR (9700156414)