Embed Size (px)

Citation preview

Journal of Policy Modeling 29 (2007) 535–540

A note on capital mobility in Greece

Dimitris K. Christopoulos ∗Department of Economics and Regional Development, Panteion University,

Leof. Syngrou 136, 17671 Athens, Greece

Received 1 October 2005; received in revised form 1 March 2006; accepted 1 December 2006Available online 21 March 2007

Abstract

Pelagidis and Mastroyiannis [Pelagidis, T., & Mastroyiannis, T. (2003). The saving–investment correlationin Greece, 1960–1997: Implications for capital mobility. Journal of Policy Modeling] using the cointegra-tion methodology proposed by Jansen and Schulze [Jansen, W.J., & Schulze, G.G. (1993). Theory-basedmeasurement for the saving–investment correlation with an application to Norway. Discussion paper 205.Universitat Kostanz] conclude that the hypothesis of perfect capital mobility cannot be confirmed in thecase of Greece. This note argue that this result is not consistent with the methodology of Johansen whichsuggests that the Feldestein-Horioka hypothesis should be accepted contrary to what the paper of Pelagidisand Mastroyiannis claims.© 2007 Society for Policy Modeling. Published by Elsevier Inc. All rights reserved.

JEL classification: F30; F32

Keywords: International capital mobility; Domestic savings

1. Introduction

In a recent article of this journal Pelagidis and Mastroyiannis (2003) (henceforth PM) investi-gated the Feldstein and Horioka (1980) (henceforth FH) hypothesis of perfect capital mobility inGreece based on the cointegration methodology of Jansen and Schulze (1993). They concludedthat domestic investments and national savings are tied together by a long run relationship prompt-ing the authors to argue that capital mobility was not high in Greece. In this note, I argue that thePM result is related to the methodology used to test for cointegration. To this end, I use Johansen’s

∗ Tel.: +30 210 9224948; fax: +30 210 9229312.E-mail address: [email protected].

0161-8938/$ – see front matter © 2007 Society for Policy Modeling. Published by Elsevier Inc. All rights reserved.doi:10.1016/j.jpolmod.2006.12.009

536 D.K. Christopoulos / Journal of Policy Modeling 29 (2007) 535–540

maximum likelihood approach (Johansen, 1988, 1991) that is superior to old fashioned cointegra-tion tests like Engle and Granger (1988), Jansen and Schulze (1993) and others in the case of I(1)regressors. It is well known that these tests do not take into account the fact that residuals are notexact but generated leading frequently the researcher to misguided conclusions. Going beyondthe paper of PM, to examine the stationarity properties of the series involved, I use the augmentedDickey Fuller test (ADF), the ADF-GLS unit root test of Elliot, Rothenberg, and Stock (1996) aswell as the KPSS test. The ADF-GLS unit root test has the best overall performance in terms ofsmall size-sample size and power with respect the ADF test. The KPSS stationarity test proposedby Kwiatkowski, Phillips, Schmidt, and Shin (1992) is a powerful test which tests the null ofstationarity against the alternative of a unit root. Finally, I use the Perron (1997) unit root test,which allows for the presence of a structural break in our time series. The presence of a structuralbreak biases the results in favour of finding a unit root.

2. The model, the method and the empirical results

To test the FH hypothesis we need to estimate the following equation

IRt = α + βSRt + et t = 1, 2, . . . , T. (1)

where IRt denotes the ratio of domestic investment to gross domestic product (GDP), SRt the ratioof national savings to GDP and et is the usual statistical noise. α and β are parameters to estimate.A value of β close to one is an indication that the FH of perfect capital mobility should be rejected,while a value of β close to zero gives support to the contention that free capital mobility shouldbe accepted.

Argimon and Roldan (1994) and Ho (2002) argue that if both IRt and SRt are integrated oforder one, then the proper way to test for the empirical validity of FH hypothesis is to test if Eq.(1) is a cointegrating relation. Evidence in favour of cointegration or weak evidence in favour ofcointegration suggests that the hypothesis of perfect capital mobility does not hold.

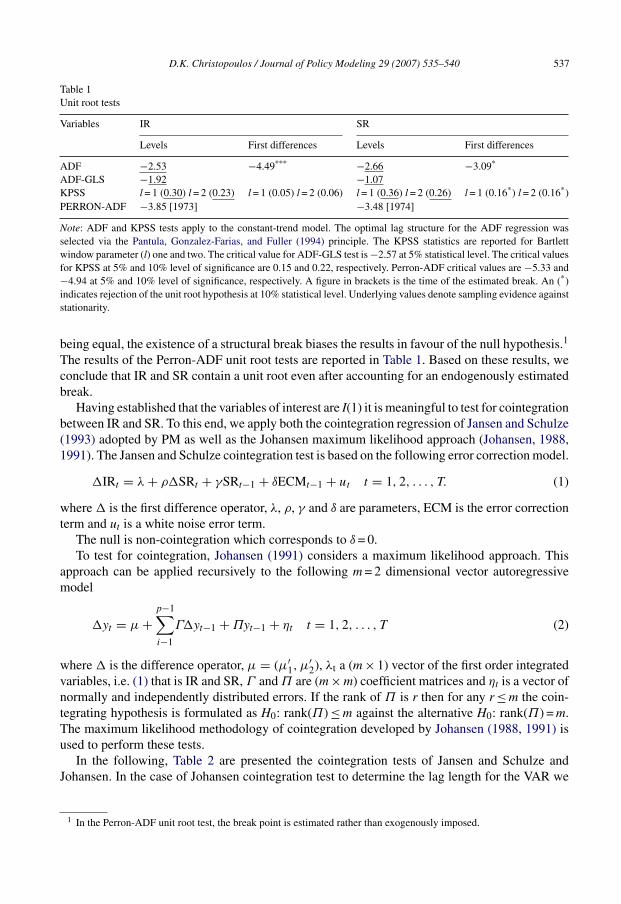

Before we test for cointegration, we need to explore the stationarity properties of the series ofinterest. To this end, we use the ADF unit root test of Dickey and Fuller (1981), the ADF-GLStest of Elliot et al. (1996) as well as the KPSS stationarity test of Kwiatkowski et al. (1992). TheADF-GLS unit root test resembles closely the ADF test as it applies GLS detrending before the(detrended) series is tested via the Dickey–Fuller regression. Compared with the ADF test, theADF-GLS test has best performance in terms of small-sample size and power. Furthermore, sincethe ADF has lower power in rejecting the null of a unit root, we implement a powerful test (theKPSS test) in which the null of stationarity is tested against the alternative of a unit root. Our dataset covers the period 1960–2000 and is taken from European Union’s AMECO data base (AnnualMacro Economic Data Base DG2). Table 1 presents the results of ADF, ADF-GLS and KPSStests. All tests indicate that IR and SR contain a unit root in their levels form. ADF and KPSS infirst differences reveal that for IR the null hypothesis is rejected at the 1% significance level whilefor SR at the 10% statistical level. Since, both ADF and KPSS tests yield similar results we canconclude to a certain degree of safety that both series are integrated of order one.

Next, to ensure that both series are realizations of non-stationary process, we employ the Perron(1997) ADF unit root test. The Perron-ADF unit root test allows for the presence of a structuralbreak. It is well know that the presence of a structural break affects the stationarity properties of aseries leading to the wrong conclusion that the investigated series contains a unit root. Other things

D.K. Christopoulos / Journal of Policy Modeling 29 (2007) 535–540 537

Table 1Unit root tests

Variables IR SR

Levels First differences Levels First differences

ADF −2.53 −4.49*** −2.66 −3.09*

ADF-GLS −1.92 −1.07KPSS l = 1 (0.30) l = 2 (0.23) l = 1 (0.05) l = 2 (0.06) l = 1 (0.36) l = 2 (0.26) l = 1 (0.16*) l = 2 (0.16*)PERRON-ADF −3.85 [1973] −3.48 [1974]

Note: ADF and KPSS tests apply to the constant-trend model. The optimal lag structure for the ADF regression wasselected via the Pantula, Gonzalez-Farias, and Fuller (1994) principle. The KPSS statistics are reported for Bartlettwindow parameter (l) one and two. The critical value for ADF-GLS test is −2.57 at 5% statistical level. The critical valuesfor KPSS at 5% and 10% level of significance are 0.15 and 0.22, respectively. Perron-ADF critical values are −5.33 and−4.94 at 5% and 10% level of significance, respectively. A figure in brackets is the time of the estimated break. An (*)indicates rejection of the unit root hypothesis at 10% statistical level. Underlying values denote sampling evidence againststationarity.

being equal, the existence of a structural break biases the results in favour of the null hypothesis.1

The results of the Perron-ADF unit root tests are reported in Table 1. Based on these results, weconclude that IR and SR contain a unit root even after accounting for an endogenously estimatedbreak.

Having established that the variables of interest are I(1) it is meaningful to test for cointegrationbetween IR and SR. To this end, we apply both the cointegration regression of Jansen and Schulze(1993) adopted by PM as well as the Johansen maximum likelihood approach (Johansen, 1988,1991). The Jansen and Schulze cointegration test is based on the following error correction model.

�IRt = λ + ρ�SRt + γSRt−1 + δECMt−1 + ut t = 1, 2, . . . , T. (1)

where � is the first difference operator, λ, ρ, γ and δ are parameters, ECM is the error correctionterm and ut is a white noise error term.

The null is non-cointegration which corresponds to δ = 0.To test for cointegration, Johansen (1991) considers a maximum likelihood approach. This

approach can be applied recursively to the following m = 2 dimensional vector autoregressivemodel

�yt = μ +p−1∑

i−1

Γ�yt−1 + Πyt−1 + ηt t = 1, 2, . . . , T (2)

where � is the difference operator, μ = (μ′1, μ

′2), λt a (m × 1) vector of the first order integrated

variables, i.e. (1) that is IR and SR, Γ and Π are (m × m) coefficient matrices and ηt is a vector ofnormally and independently distributed errors. If the rank of Π is r then for any r ≤ m the coin-tegrating hypothesis is formulated as H0: rank(Π) ≤ m against the alternative H0: rank(Π) = m.The maximum likelihood methodology of cointegration developed by Johansen (1988, 1991) isused to perform these tests.

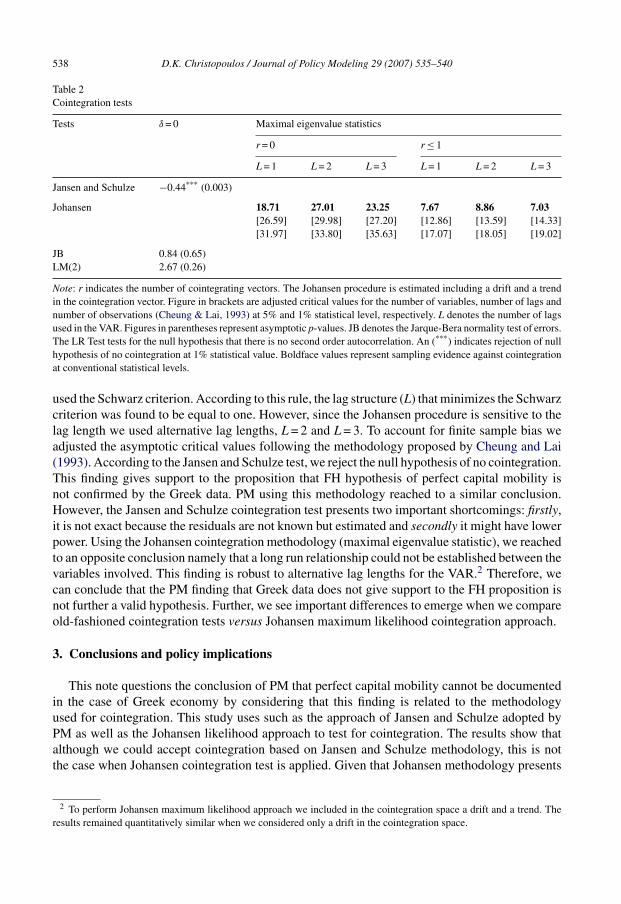

In the following, Table 2 are presented the cointegration tests of Jansen and Schulze andJohansen. In the case of Johansen cointegration test to determine the lag length for the VAR we

1 In the Perron-ADF unit root test, the break point is estimated rather than exogenously imposed.

538 D.K. Christopoulos / Journal of Policy Modeling 29 (2007) 535–540

Table 2Cointegration tests

Tests δ = 0 Maximal eigenvalue statistics

r = 0 r ≤ 1

L = 1 L = 2 L = 3 L = 1 L = 2 L = 3

Jansen and Schulze −0.44*** (0.003)

Johansen 18.71 27.01 23.25 7.67 8.86 7.03[26.59] [29.98] [27.20] [12.86] [13.59] [14.33][31.97] [33.80] [35.63] [17.07] [18.05] [19.02]

JB 0.84 (0.65)LM(2) 2.67 (0.26)

Note: r indicates the number of cointegrating vectors. The Johansen procedure is estimated including a drift and a trendin the cointegration vector. Figure in brackets are adjusted critical values for the number of variables, number of lags andnumber of observations (Cheung & Lai, 1993) at 5% and 1% statistical level, respectively. L denotes the number of lagsused in the VAR. Figures in parentheses represent asymptotic p-values. JB denotes the Jarque-Bera normality test of errors.The LR Test tests for the null hypothesis that there is no second order autocorrelation. An (***) indicates rejection of nullhypothesis of no cointegration at 1% statistical value. Boldface values represent sampling evidence against cointegrationat conventional statistical levels.

used the Schwarz criterion. According to this rule, the lag structure (L) that minimizes the Schwarzcriterion was found to be equal to one. However, since the Johansen procedure is sensitive to thelag length we used alternative lag lengths, L = 2 and L = 3. To account for finite sample bias weadjusted the asymptotic critical values following the methodology proposed by Cheung and Lai(1993). According to the Jansen and Schulze test, we reject the null hypothesis of no cointegration.This finding gives support to the proposition that FH hypothesis of perfect capital mobility isnot confirmed by the Greek data. PM using this methodology reached to a similar conclusion.However, the Jansen and Schulze cointegration test presents two important shortcomings: firstly,it is not exact because the residuals are not known but estimated and secondly it might have lowerpower. Using the Johansen cointegration methodology (maximal eigenvalue statistic), we reachedto an opposite conclusion namely that a long run relationship could not be established between thevariables involved. This finding is robust to alternative lag lengths for the VAR.2 Therefore, wecan conclude that the PM finding that Greek data does not give support to the FH proposition isnot further a valid hypothesis. Further, we see important differences to emerge when we compareold-fashioned cointegration tests versus Johansen maximum likelihood cointegration approach.

3. Conclusions and policy implications

This note questions the conclusion of PM that perfect capital mobility cannot be documentedin the case of Greek economy by considering that this finding is related to the methodologyused for cointegration. This study uses such as the approach of Jansen and Schulze adopted byPM as well as the Johansen likelihood approach to test for cointegration. The results show thatalthough we could accept cointegration based on Jansen and Schulze methodology, this is notthe case when Johansen cointegration test is applied. Given that Johansen methodology presents

2 To perform Johansen maximum likelihood approach we included in the cointegration space a drift and a trend. Theresults remained quantitatively similar when we considered only a drift in the cointegration space.

D.K. Christopoulos / Journal of Policy Modeling 29 (2007) 535–540 539

several advantages with respect to old fashioned cointegration tests like that of Jansen and Schulzewe conclude that the FH hypothesis of perfect capital mobility is confirmed in the case Greekeconomy.

Several important outcomes can be derived from this situation: (a) The high degree of interna-tional capital mobility in Greece permits the domestic investment-saving gap to be financed alsovia foreign saving releasing thus the intertemporal solvency constraint. Since the early 1970s,Greece has imported foreign capital by the amount of 5–10% of its GDP. After 1981 when thecountry joined the EU, the annual gross capital inflows continued to increase although measuredin relation to GDP they slightly declined, see Buch, 1999. It should be noted that entry into the ECdid not imply a full abolition of capital controls. Greece retained controls on capital flows up to1994. (b) In the presence of perfect capital mobility, the factors giving rise to the current accountimbalance preserve their importance for policy making. Policies aiming at reducing the currentaccount deficit, only by the promotion of domestic savings, ignore the important role the invest-ments play in economic growth. Within this framework, Greek governments should favor policiesthat further encourage long term capital movements to finance domestic investment rather thandiscouraging domestic consumption per se. (c) The absence of a systematic relationship betweensavings and investment should give rise to policies aiming at removing distortions on invest-ment decisions, including financial constraints, capital market imperfections and deficiencies ineducation and R&D spending and (d) for integrated capital markets, like the common currencyEU, measures aiming at increasing domestic savings through tax on profits may induce capitalmovements across borders, so the incidence of the tax falls on the nations’ labor force.

Acknowledgment

The author wish to thank M. Lambrinidis for useful comments on an earlier version.

References

Argimon, I., & Roldan, J.-M. (1994). Saving investment and international capital mobility in EC countries. EuropeanEconomic Review, 38, 59–67.

Buch, C. M. (1999). Capital mobility and EU enlargement. Weltwirtscatliched Arciv, 135, 629–656.Cheung, W.-Y, & Lai, S. K. (1993). Finite-sample sizes of Johansen’s likelihood ratio tests for cointegration. Oxford

Bulletin of Economics and Statistics, 55, 313–328.Dickey, D. A., & Fuller, W. A. (1981). Likelihood ratio statistics for autoregressive time series with a unit root. Econo-

metrica, 49, 1057–1072.Elliot, G., Rothenberg, T. G., & Stock, J. H. (1996). Efficient tests for an autoregressive unit root. Econometrica, 64,

813–836.Engle, R. F., & Granger, C. W. G. (1988). Co-integration and error correction representation, estimation and testing.

Econometrica, 55, 251–276.Feldstein, M., & Horioka, C. (1980). Domestic saving and international capital flows. Economic Journal, 90, 314–329.Ho, T. W. (2002). A panel cointegration approach to the investment-saving correlation. Empirical Economics, 27, 91–100.Jansen, W.J., & Schulze, G.G. (1993). Theory-based measurement for the saving–investment correlation with an appli-

cation to Norway. Discussion paper 205. Universitat Kostanz.Johansen, S. (1988). Statistical analysis of cointegration vectors. Journal of Economics Dynamic and Controls, 8, 231–254.Johansen, S. (1991). Estimation and hypothesis testing of cointegrating vectors in Gaussian vector autoregressive models.

Econometrica, 59, 1551–1580.Kwiatkowski, D., Phillips, P. C. B., Schmidt, P., & Shin, Y. (1992). Testing the null hypothesis of stationarity against the

alternative of a unit root: How sure are we that the economic time series have unit root? Journal of Econometrics, 54,159–178.

540 D.K. Christopoulos / Journal of Policy Modeling 29 (2007) 535–540

Pantula, S. G., Gonzalez-Farias, G., & Fuller, W. A. (1994). A comparison of unit root test criteria. Journal of Businessof Economics and Statistics, 12, 449–459.

Pelagidis, T., & Mastroyiannis, T. (2003). The saving–investment correlation in Greece, 1960-1997: Implications forcapital mobility. Journal of Policy Modeling, 25, 609–616.

Perron, P. (1997). Further evidence on breaking trend functions in macroeconomic variables. Journal of Econometrics,80, 335–345.